Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1205.10 up $7.80 (comex closing time)

Silver: $17.12 up 14 cents (comex closing time)

In the access market 5:15 pm

Gold $1203.55

Silver: $17.08

Gold/silver trading: see kitco charts on the right side of the commentary.

Following is a brief outline on gold and silver comex figures for today:

The gold comex today had a poor delivery day, registering 1 notice served for 100 oz. Silver comex registered 129 notices for 645,000 oz .

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 248.27 tonnes for a loss of 55 tonnes over that period. Lately the removals have been rising!

In silver, the open interest fell by 589 contracts, due to short covering, as Wednesday’s silver price was up by 1 cent. The total silver OI continues to remain extremely high with today’s reading at 172,070 contracts. The front month of March fell by 171 contracts to 312 contracts. We are still close to multi year high in the total OI complex despite a record low price. This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end.

We had 129 notices served upon for 645,000 oz.

In gold we again have a total collapse of OI as we enter the next active delivery month of April . The total comex gold OI rests tonight at 416,312 for a whopping loss 17,455 contracts. With June gold almost equal to April gold in price, it just does not make sense why so many would liquidate their positions.Today is options expiry. Surprisingly we had 1 notice served upon for 100 oz.

Today, we had a huge withdrawal of 5.97 tonnes at the GLD/ Gold Inventory rests at 737.24 tonnes

In silver, /SLV we had no changes in silver inventory at the SLV/Inventory, at 325.323 million oz

We have a few important stories to bring to your attention today…

1, Today we again had some short covering in the silver comex with the silver OI falling by 589 contracts. Gold OI fell by a whopping 17,455 contracts. Both gold and silver rose nicely again today. 1,028.80 oz of . (report Harvey)

2. Yemen rebels heading straight for the strategic city of Aden, on the southern tip of the Red Sea. Saudi Arabia and 10 nations join force to oust these rebels in what is becoming another proxy war with Sunnis on one side (Saudi Arabia, Egypt, Kuwait etc and Iran on the other side. The big question of course is where does China and Russia sit with this.

(zero hedge/IRD/Dave Kranzler)

3.The ECB is quietly asking its banks how much exposure they have to the big Austrian Hypo bank failure. Bail ins will commence in about one month . (zero hedge)

4. Russia refuses to take a haircut on the 3 billion usa dollar loan given to the Ukraine. The IMF is requesting everybody take a haircut on its debt for the new loan from the iMF to commence. Russia can call this note early setting off a disorderly default. (zero hedge)

5. Has the USA blundered with respect to the latest Chinese initiative infrastructure bank

(Ambrose Evans Pritchard/UKTelegraph/Bill Holter/Miles Franklin)

we have these and other stories for you tonight

Let us now head over to the comex and assess trading over there today.

Here are today’s comex results:

The total gold comex open interest fell by a whopping 17,455 contracts from 433,767 down to 416,312 as gold was up by $5.60 yesterday (at the comex close). As I mentioned above, the complete collapse of OI as we enter an active delivery month makes no sense.The fact that we have a middle eastern war, troubles in Ukraine and in Greece and then to have a complete collapse in OI is beyond comprehension. We are now in the contract month of March which saw it’s OI fall to 92 for a loss of 389 contracts. We had 0 notices filed upon on Tuesday so we lost 389 gold contracts or an additional 38,900 ounces will not stand for delivery in this delivery month of March. The next big active delivery month is April and here the OI fell by 43,312 contracts down to 111,698. We have 5 days before first day notice for the April gold contract month, on Tuesday, March 31.2015. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was poor at 203,523. (Where on earth are the high frequency boys?). The confirmed volume on yesterday ( which includes the volume during regular business hours + access market sales the previous day) was fair at 290,533 contracts. Today we had 1 notice filed for 100 oz.

And now for the wild silver comex results. Silver OI fell by 589 contracts from 172,659 down to 172,070 despite the fact that silver was up 1 cent, with respect to Wednesday’s trading . We therefore again had some more short covering by our bankers. We are now in the active contract month of March and here the OI fell by 134 contracts falling to 212. We had 154 contracts served upon yesterday. Thus we gained 20 contracts or an additional 100,000 oz will stand in this March delivery month. The estimated volume today was fair at 27,073 contracts (just comex sales during regular business hours. The confirmed volume on Wednesday (regular plus access market) came in at 33,300 contracts which is also fair in volume. We had 129 notices filed for 645,000 oz today.

March initial standings

March 26.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3552.160 oz (Manfra,Brinks, Delaware, Scotia, HSBC) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 97,738.120 oz (Delaware, HSBC, Scotia) |

| No of oz served (contracts) today | 1 contracts (100 oz) |

| No of oz to be served (notices) | 108 contracts (10,800 oz) |

| Total monthly oz gold served (contracts) so far this month | 9 contracts(900 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 114,790.651 oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

656,689.9 oz |

Today, we had 0 dealer transaction

total Dealer withdrawals: nil oz

we had 0 dealer deposit

total dealer deposit: nil

we had 5 customer withdrawals

i) Out of Manfra: 64.3 oz (2 kilobars)

ii) Out of Scotia: 2989.95oz (93 kilobars)

iii)Out of Delaware: 204.64 oz (real bars)

iv) Out of Brinks: 96.45 (3 kilobars)

v)Out of HSBC 196.82 oz (real bars)

total customer withdrawal: 3,552.16

we had 3 customer deposits:

i) Into Delaware: 888.415 oz

ii) Into HSBC: 202.886 oz

iii) Into Scotia: 96,450.000 oz

total customer deposit: 97,738.12 oz

We had 2 adjustments

Out of Brinks; 96.45 oz was adjusted out of the customer and this landed into the dealer account at Brinks

Out of Delaware; 199.74 oz was adjusted out of the customer and this landed into the dealer account at Delaware.

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the March contract month, we take the total number of notices filed so far for the month (9) x 100 oz or 900 oz , to which we add the difference between the open interest for the front month of March (92) and the number of notices served upon today (1) x 100 oz equals the number of ounces standing.

Thus the initial standings for gold for the March contract month:

No of notices served so far (9) x 100 oz or ounces + {OI for the front month (92) – the number of notices served upon today (1) x 100 oz} = 10,000 oz or .3110 tonnes

we lost a huge 389 contracts or 38,900 oz will not stand for delivery.

Total dealer inventory: 658,833.604 oz or 20.49 tonnes

Total gold inventory (dealer and customer) = 7,981,965.774 oz. (248.27) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 55.0 tonnes have been net transferred out. However I believe that the gold that enters the gold comex is not real. I cannot see continual additions of strictly kilobars.

end

And now for silver

March silver initial standings

March 26 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | 401,239.24 oz (Delaware, HSBC) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 234,806.700 oz (Scotia) |

| No of oz served (contracts) | 129 contracts (645,000 oz) |

| No of oz to be served (notices) | 83 contracts (415,000) |

| Total monthly oz silver served (contracts) | 2432 contracts (12,160,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | |

| Total accumulative withdrawal of silver from the Customer inventory this month | 7,416,837.6 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 1 customer deposits:

i) Into Scotia: 234.806.700 oz

total customer deposit: 234,806.700 oz

We had 2 customer withdrawals:

i) Out of HSBC: 400,248.09 oz

ii) Out of Delaware; 991.15 oz

total withdrawals; 401,239.24 oz

we had 0 adjustments:

Total dealer inventory: 70.569 million oz

Total of all silver inventory (dealer and customer) 175.180 million oz

.

The total number of notices filed today is represented by 129 contracts for 645,000 oz. To calculate the number of silver ounces that will stand for delivery in March, we take the total number of notices filed for the month so far at (2432) x 5,000 oz = 12,160,000 oz to which we add the difference between the open interest for the front month of March (212) and the number of notices served upon today (129) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the March contract month:

2432 (notices served so far) + { OI for front month of March(212) -number of notices served upon today (129} x 5000 oz = 12,575,000 oz standing for the March contract month.

we gained 100,000 oz of additional silver standing in this March delivery month.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.com orhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

March 26 we had another huge withdrawal of 5.97 tonnes of gold. This gold is heading straight to the vaults of Shanghai, China/GLD inventory 737.24 tonnes

March 25.2015 we had a withdrawal of 1.19 tonnes of gold from the GLD/Inventory at 743.21 tonnes

March 24/ no changes in gold inventory at the GLD/Inventory 744.40 tonnes

March 23/we had a huge withdrawal of 5.37 tonnes of gold from the GLD vaults/Inventory 744.40 tonnes

march 20/we had no changes in inventory at the GLD/Inventory at 749.77 tonnes

March 19/we had no changes in inventory at the GLD/Inventory 749.77 tonnes

March 18/ we had a withdrawal of .9 tonnes of gold from the GLD/Inventory at 749.77 tonnes

March 17.2015: no change in gold inventory at the GLD/Inventory 750.67 tonnes

March 16/no change in gold inventory at the GLD/Inventory 750.67 tonnes

March 26/2015 / we had a withdrawal of 5.97 tonnes of gold/Inventory at 737.24 tonnes

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 737.24 tonnes.

end

And now for silver (SLV):

March 26.2015; no change in silver inventory/SLV inventory 325.323 million oz

March 25.2015:no change in silver inventory/SLV inventory 325.323 million oz

March 24.2015/ we had another withdrawal of 835,000 oz of silver from the SLV/Inventory rests tonight at 325.323 million oz

March 23./we had a huge withdrawal of 1.174 million oz of silver from the SLV vaults/Inventory 326.158 million oz

March 20/ no changes in silver inventory/327.332 million oz

March 19/ no change in silver inventory/327.332 million oz

March 18/ no change in silver inventory/327.332 million oz

March 17/ no change in silver inventory/327.332 million oz

March 16/no change in silver inventory/327.332 million oz

March 26/2015 we had no changes in inventory/SLV inventory at 325.323 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now for the first time into the negative to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 8.8% percent to NAV in usa funds and Negative 8.6% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.5%

Percentage of fund in silver:39.1%

cash .4%

( March 26/2015)

Sprott gold fund finally rising in NAV

2. Sprott silver fund (PSLV): Premium to NAV falls to + 1.22%!!!!! NAV (March 26/2015)

3. Sprott gold fund (PHYS): premium to NAV falls -.45% to NAV(March 26 /2015)

Note: Sprott silver trust back into positive territory at +1.22%.

Sprott physical gold trust is back into negative territory at -.45%

Central fund of Canada’s is still in jail.

end

And now for your more important physical gold/silver stories:

Gold and silver trading early this morning

(courtesy Goldcore/Mark O’Byrne)

Oil Surges, Gold and Silver Spike as Saudi Arabia Bombs Yemen

– Geopolitical tensions in Middle East escalate dramatically as Saudi Arabia bombs Yemen

– Yemen’s government seized power in coup – Regarded as hostile to Saudi and ally of Iran

– Saudi attack is an escalation of Middle Eastern proxy war between Gulf States and Iran

– Action has broader geopolitical implications in deepening cold war between the West and East

– Oil surged 6% and gold 2% on the the news

– Should oil prices return to new record highs will impact struggling global economy

Geopolitical tensions escalated dramatically over night as Saudi Arabia launched military operations including air strikes in Yemen. The Saudis claim the action is to counter Iran-allied forces besieging the southern city of Aden where the U.S. backed Yemeni president had taken refuge.

Oil surged and gold rose nearly 2% following a sharp drop in stocks on Wall Street globally in response to the bombing in Yemen.

Gulf broadcaster al-Arabiya TV reported that the kingdom was contributing as many as 150,000 troops and 100 war planes to the operations. Egypt, Jordan, Sudan and Pakistan were ready to take part in a ground offensive in Yemen, the broadcaster said.

The Saudi’s seem determined to pull geopolitically strategic Yemen back into its orbit following the coup d’etat in February.

The Syrian state news agency said the Saudi-led military operation is an act of “blatant aggression”.

“Gulf war planes led by the regime of the Saudi family launch a blatant aggression on Yemen,” read their headline. The Syrian government led by President Bashar al Assad is an ally of Iran, which is in turn allied with the Yemeni Houthi rebels who are fighting to oust the country’s U.S. backed president.

Saudi Arabia and other Gulf states have been important sponsors of the insurgency against Assad.

Traditionally Saudi Arabia has kept Yemen under its control through patronage of various tribal factions. This system was disrupted in 2011 when internal social pressures forced the incumbent President Saleh to step down.

In September, the Houthis – a Shia group seen as allied to Iran – seized control of Yemen’s capital Sana’a. Shia’s make up up to 45% of Yemen’s population. In February, the Houthis declared themselves the new government of Yemen filling the vacuum caused by the resignation of the previous government amid a political impasse.

Saudi’s actions in Yemen is a dramatic escalation in the proxy war between the Gulf states and Iran now raging in Iraq and Syria. The tensions arise out of competition over who has access to the lucrative, oil-hungry, European markets.

That a country would choose to directly intervene militarily in the affairs of another country is a dangerous precedent and could lead to a wider conflagration in the region – especially if Syria or Iran decide to retaliate against Saudi Arabia.

Iran now may claim to have justification to involve itself directly into the affairs of neighbouring countries and the potential for direct conflict and a full scale regional war has just increased.

It may also lead to heightened tensions in the simmering Cold War between the West and the East. Russian diplomacy disrupted moves by the West and western-backed Gulf states to remove yet another secular leader, one of the few remaining secular leaders, in the Islamic world – Assad in Syria.

Iran and Syria have close diplomatic and business ties with Russia. The White House has already made its support for Saudi actions clear and it is likely that Russia will support Iran in any response it may deliver.

Given the strategically vital nature of the whole region it is unlikely that either the U.S. or Russia will allow events to be determined by local players and this has serious implications in the new Cold War.

Oil surged over 6% on the news. A full-on conflict between Iran and the Gulf states would likely shut off the Straits of Hormuz, dramatically reducing the supply of oil coming out of the Gulf and a spike in oil prices.

This would benefit both Russia’s struggling economy and the U.S. energy sector but impact struggling consumers in the U.S. and internationally. Indeed, Europeans are particularly vulnerable to a sharp rise in oil prices now after the significant fall in the euro in recent months.

Gold’s rise is indicative of its function as a hedge against economic and geopolitical uncertainty. A supply crunch in oil in the middle of a slump driven by lack of demand would put even more pressure on industries struggling to sell product to heavily indebted western consumers.

While oil prices remain very depressed, surging oil prices could again be the ‘straw that breaks the global economies back’.

“A must read for family offices seeking wealth preservation”

Essential Family Office Guide to Investing In Gold

MARKET UPDATE

Today’s AM fix was USD 1,209.40, EUR 1,097.26 and GBP 809.23 per ounce.

Yesterday’s AM fix was USD 1,192.55, EUR 1,088.89 and GBP 801.18 per ounce.

Gold rose 0.16 percent or $1.90 and closed at $1,195.60 an ounce yesterday, while silver slipped 0.18 percent or $0.03 at $16.97 an ounce.

Gold has been bid higher due to the escalation of geopolitical risk in the Middle East and technical buying after gold rose above the $1,200/oz level.

Gold climbed more than 1.4% to a three and a half week high and silver soared almost 3 percent as air strikes in Yemen had a ripple effect on markets.

Saudi Arabia and its Arab allies launched air strikes in Yemen against allies of Iran in the southern city of Aden. The return of ‘risk off’ sentiment for the first time in many weeks, boosted gold, silver and German bunds while equities and the U.S. dollar fell.

The question is whether this is a flash in the pan for gold or the start of a more meaningful rally in prices. Gold appears overbought in the very short term. The last winning streak for 7 days in a row for the yellow metal was in August 2012.

In the end of day trading in Singapore, gold prices rose 0.8 percent to $1,204.20 an ounce, but earlier reached $1,204.60, its highest since March 5th. In London, Spot gold hit a peak of $1,219.40 an ounce and climbed 1.2 percent at $1,210.30 in morning trading. Comex U.S. gold futures for April delivery were up $12.70 an ounce at $1,209.70.

On the Shanghai Gold Exchange (SGE), premiums pulled back to about $2-$3 an ounce, compared with $6-$7 last week.

Silver prices jumped to a three month high at $17.38 per ounce. Platinum was $1,153.25 per ounce up 0.6 percent, while palladium was $770.39 an ounce or up 1 percent.

end

Gold market manipulation is ‘too inflammatory’ to be debated at Hong Kong conference

6:51p HKT Thursday, March 26, 2015

Dear Friend of GATA and Gold:

Yesterday’s concentration on gold at the spectacular Mines and Money Hong Kong conference may have inadvertently proved GATA’s longstanding contention that gold market manipulation simply can’t be discussed in polite company almost anywhere in the world.

For at the outset of a panel discussion described as a debate about the direction of the gold price, its moderator, Rod Whyte, a longtime gold advocate and member of the Board of Directors of Australia-based business information provider Aspermont Ltd., announced that the panelists had agreed that gold market manipulation would not be discussed because the topic is “too inflammatory.”

Since Whyte has expressed support for GATA at other venues, the calculated avoidance of the manipulation issue would seem to have been someone else’s idea. In any case the panel included two members who could not have been expected to want to discuss the issue: Philip Klapwijk, formerly an analyst for Gold Fields Mineral Services, now managing director of Precious Metals Insights Ltd. in Hong Kong, and Albert Cheng, Far East managing director for the World Gold Council.

While Klapwijk predicted that the price of gold will fall substantially, predictions for the gold price are of no particular concern to GATA. We recognize that as long as the futures markets are operating, central banks can drive the price down to zero or up to infinity.But your secretary/treasurer was in the audience and would have liked to ask Klapwijk and Cheng a few questions.

For example:

— Was the Banque de France’s director of market operations, Alexandre Gautier, telling the truth when he told the London Bullion Market Association meeting in Rome in September 2013, that the bank is secretly trading gold for its own account and the accounts of other central banks “nearly on a daily basis”? (See:http://www.gata.org/node/13373.)

— Is the Bank for International Settlements telling the truth when it maintains in its annual report that it does the same sort of secret trading on behalf of its member central banks, trading not only gold itself but also gold futures, options, and other derivatives? (See: http://www.gata.org/node/12717.)

— Is the BIS sincere when it advertises that it undertakes secret interventions in the gold market for its members? (See http://www.gata.org/node/11012.)

— If these central banks are indeed doing so much secret trading in the gold market, what are their objectives and might this secret trading manipulate the market and thereby deceive and cheat investors?

— And for the World Gold Council’s Cheng in particular: In its various analyses of the gold market, does the World Gold Council ever consider this secret trading by central banks, and does the council have any opinion about it?

Unfortunately the program did not permit questions.

An hour later your secretary/treasurer began his own presentation by noting the gold debate panel’s determination that discussion of market manipulation is “too inflammatory” to be discussed and reminding the audience that they had been warned and might want to leave so as to avoid the ensuing unpleasantness. It was gratifying that no one walked out, though of course Klapwijk and Cheng had not stuck around.

Your secretary/treasurer said that GATA has spent 15 years collecting the documentation of largely surreptitious manipulation of the gold market by central banks and clamoring and litigating against it —

http://www.gata.org/taxonomy/term/21

— and that the presentation of this documentation had served mainly to get GATA disparaged as “conspiracy theorists.”

But your secretary/treasurer added that there is such a thing as conspiracy fact — as when the European Central Bank gathers its members secretly every few years to determine their policy in the gold market and then announces that this policy indeed has been determined in secret and that it will continue to be determined in secret and executed in secret as well:

http://www.ecb.europa.eu/press/pr/date/2014/html/pr140519.en.html

It is also conspiracy fact when the G-10 Gold and Foreign Exchange Committee, representing the treasury departments and central banks of the industrial world, undertakes the same sort of secret meetings for policy formation and execution —

— just as it is conspiracy fact when the U.S. Federal Reserve secretly undertakes and executes gold swap arrangements with foreign banks —

— and when members of the International Monetary Fund swap and lease gold in secret to facilitate their secret interventions in the gold and currency markets:

http://www.gata.org/node/12016

Indeed, insofar as it operates largely in secret much of the time, government itself is by definition one big conspiracy.

Any serious analysis of the gold market, your secretary/treasurer said, must begin with these questions:

— Are central banks in the gold market largely surreptitiously or not?

— If central banks are in the gold market largely surreptitiously, is it just for fun — for example, to see which central bank’s trading desk can make the most money by cheating the most investors — or is it for policy purposes?

— If central banks are in the gold market for policy purposes, are these the traditional purposes of defeating a potentially competitive world reserve currency (see http://www.gata.org/node/13310) or might there be other purposes as well (see http://www.gata.org/node/14994)?

Then your secretary/treasurer presented as many documents as the remainder of his 20 minutes allowed. Fortunately this allowed citation of the U.S. Commodity Futures Trading Commission and U.S. Securities and Exchange Commission documents indicating that central banks are secretly trading all major U.S. futures markets and contracts:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

http://www.gata.org/node/14818

Grateful as he was to be allowed to participate again at the Hong Kong conference, your secretary/treasurer would be even more grateful to participate in any forum at which anyone of any standing in the gold market who dismisses complaints of gold market manipulation as “conspiracy theory” would be prepared to address the questions and documents cited here.

Of course it would be ideal if anyone in authority in government anywhere would attend a forum for addressing these questions and documents.

Yes, these questions and documents may be considered inflammatory, but only insofar as the world’s financial system has become a cosmic fraud that deserves to go up in flames.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

(courtesy Koos Jansen)

Posted on 26 Mar 2015 by Koos Jansen

Euronews: If China Joins The New Gold Fix, There’ll Be Less Manipulation

On March 24, 2015, Euronews broadcasted Business Middle East, in which Nour Al Hammoury from ADS securities, stated that if Chinese banks would join the new gold fix it would be less sensitive for manipulation. Having Chinese banks participate in the fix, would indeed be very welcome.

If you like to read more about if Chinese banks will participate in the new fix read Chinese Banks as direct participants in the new LBMA Gold and Silver Price auctions? Not so fast!

Global gold price setting arrives in the 21st century

…Better late than never, the gold market has entered the digital era, joining other precious metals in the 21st century. Criticism of an archaic global price fixing system intensified with some claiming it lacked credibility. Following numerous fines on international banks due to scandals of price manipulation, gold traders may now have more peace of mind with a new electronic system to manage price setting.

…Since 1919, the gold price setting process was limited to four international banks “Barclays, HSBC, Société Générale and Scotiabank”. In the original process, inter-bank representatives would set up a secure conference call each day in order to determine the price. UBS Swiss and Goldman Sachs have now joined this list of bank representatives. The new digital system follows the same process:

Each round is 45 seconds long. Bids and offers are displayed and updated in real-time. The difference is automatically calculated and if it stays within 20,000 troy ounces, the price is fixed. In this new system, orders are separated between clients and the banks’ trading desks.

Daleen Hassan

“Is the new electronic system able to make the daily price benchmark less vulnerable to manipulation?”

Nour Al Hammoury

“We hope. Major global banks have faced many scandals related to commodities and not only gold. The banks who were predicting the price of gold to reach above 2,000 USD/oz are the same banks who are predicting now that the price will fall below 1,000 USD/oz. Despite that, the major banks remain the biggest gold buyers, according to the latest report from the world gold council. In the meantime, the new pricing might give the market some confidence, especially if its transparent and this is what we will be watching out for the coming period.”

Daleen Hassan

“According to projections, China could play a key role in the new pricing system. How so?”

Nour Al Hammoury

“From the start of the financial crisis until today, China has been buying a huge amount of gold, making it one of the biggest consumer and buyers of gold in the past few months. Indeed, if China joins the new pricing plan, there’ll be less manipulation; the more they increase the participants the less chance of manipulation as we’ve seen before, when price setting was done by a few banks.”

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

end

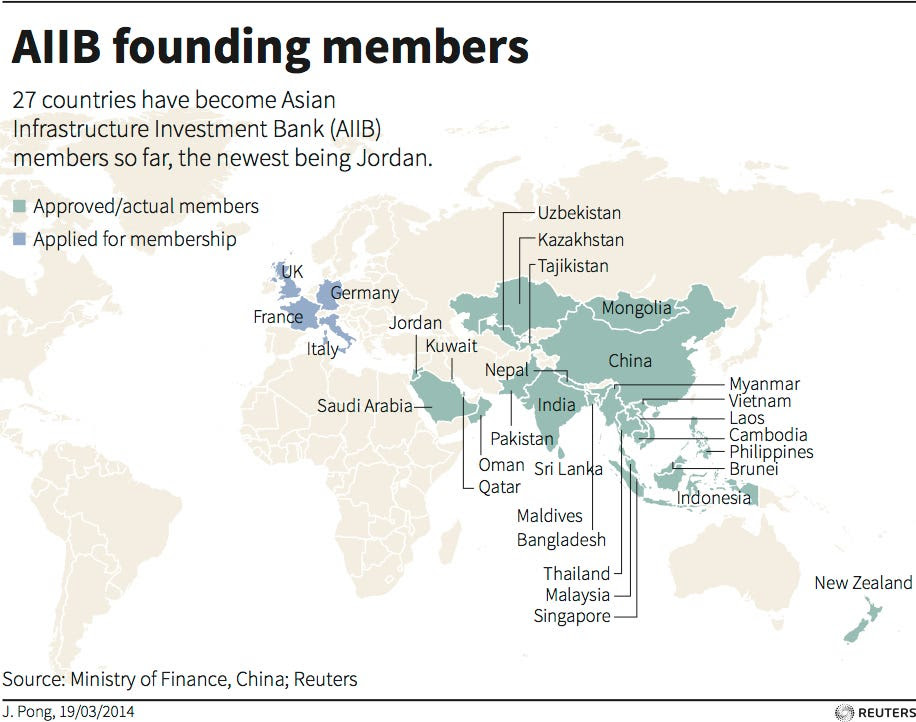

Bill Holter pounds the table on what the AIIB initiate will mean.

Bill’s commentary is also reinforced by Ambrose Evans Pritchard

(below)

(courtesy Bill Holter/Miles Franklin)

Dropping an F-bomb at a Sunday afternoon social?

Many people believe the Chinese are on the cusp of replacing the U.S. in many fashions, I believe this myself. There are others out there who believe the Chinese economy and financial markets will crash and burn with all the rest when the derivatives chain finally breaks, I don’t disagree with this either. Let’s look at what the Chinese have done, what they are doing and where they may end up. The spoiler is this, I believe you can equate the Chinese to where the United States stood in the late 1920’s and early 1930’s.

Do you notice anything strange about this map? All of the names from Asia you would expect to see are on the list, but there are others that are (were) shockers. Two weeks ago we heard Britain had applied for charter member status. This was followed by president Obama’s very harsh words the next day …which was then followed by Germany, France and Italy making their application. This is all old news, I know. Let me ask you again, is there something else quite strange about this map?

And now for the important paper stories for today:

Early Thursday morning trading from Europe/Asia

1. Stocks generally lower on major Chinese bourses (only Shanghai higher)/yen rises to 118.70

1b Chinese yuan vs USA dollar/yuan slightly weakens to 6.2124

2 Nikkei down by 275.08 or 1.39%

3. Europe stocks all in the red/USA dollar index down to 96.51/Euro rises to 1.1003

3b Japan 10 year bond yield .33% (Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 118.70/

3c Nikkei still above 19,000

3d USA/Yen rate now below the 119 barrier this morning

3e WTI 51.23 Brent 58.73

3f Gold up/Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning as a proxy civil war breaks out in Yemen (see below zero hedge commentary)

3i European bond buying continues to push yields lower on all fronts in the EMU

Except Greece which sees its 2 year rate slightly rises to 19.89%/Greek stocks down by a huge 2.54%today/ still expect continual bank runs on Greek banks.

3j Greek 10 year bond yield: 10.94% (up by 15 basis point in yield)

3k Gold at 1208.00 dollars/silver $17.16

3l USA vs Russian rouble; (Russian rouble up 1/2 rouble/dollar in value) 56.45 rising with the higher brent oil price

3m oil into the 51 dollar handle for WTI and 58 handle for Brent

3n Higher foreign deposits out of China sees hugh risk of outflows and a currency depreciation. This scan spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF

3p Britain’s serious fraud squad investigating the Bank of England/ the British pound is suffering

3r the 7 year German bund still is in negative territory/no doubt the ECB will have trouble meeting its quota of purchases and thus European QE will be a total failure.

3s Eurogroup reject Greece’s bid for the return of previous 1.2 billion euros of bailout funds. The ECB increases ELA by 1.5 billion euros up to 71.3 billion euros. This money is used to replace fleeing depositors.

3t Bloomberg calculates Greece’s shortfall in March at 3.5 billion euros.

4. USA 10 year treasury bond at 1.91% early this morning. Thirty year rate well below 3% at 2.50%/yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy zero hedge/Jim Reid Deutsche bank)

Futures Tumble As Yemen War Starts; Oil, Gold Surges

In a somewhat surprising turn of events, this morning’s futures reaction to last night’s shocking start of a completely unexpected Yemen proxy war, which has seen an alliance of Gulf State launch an air, and soon land, war against Yemen’s Houthi rebels, is what one would expect: down, and down big.

This is surprising, because on previous occasions one would expect the NY Fed, or its pet hedge fund, Citadel, or the BOJ or ECB (via the CME’s “Central Bank Incentive Program“) to aggressively buy ES to prevent a slide, something has changed, and for the BTFDers, that something may be very fatal with the e-Mini rapidly approaching a 1-handle yet again.

The offset to tumbling stocks, as previously observed, is oil, with WTI soaring over 6% in a delayed algo response to the Qatar headlines.

WTI rose as high as mid-$52 before retreating modestly:

“Rising prices could become a self-fulfilling prophecy if market participants see this as the beginning of a rally and start buying,” says Global Risk Management oil risk manager Michael Poulsen. “We are already seeing some reaction, as buyers start looking for protection from more costly oil.”

It wasn’t just oil: gold also soared briefly after European traders arrived in the office, but since then the BIS gold trading desk headed by Benoit Gilson has managed to get things mostly back in order.

Why is tiny Yemen, which produced just about 133,000 barrels a day of oil in 2013, making it the 39th biggest producer, according to the U.S. Energy Information Administration, roiling the market? Bloomberg has a quick explainer:

While Yemen contributes less than 0.2 percent of global oil output, its location puts it near the center of world energy trade. The nation shares a border with Saudi Arabia, the world’s biggest crude exporter, and sits on one side of a shipping chokepoint used by crude tankers heading West from the Persian Gulf. Global oil prices jumped more than 5 percent on Thursday after regional powers began bombing rebel targets in the country that produced less than Denmark in 2013.

“While thousands of barrels of oil from Yemen will not be noticed, millions from Saudi Arabia will matter,” said John Vautrain, who has more than 30 years’ experience in the energy industry and is the head of Vautrain & Co., a consultant in Singapore. “Saudi Arabia has been concerned about unrest spreading from Yemen.”

Shipping Chokepoint

Brent, the benchmark grade for more than half the world’s crude, gained as much as $3.30, or 5.8 percent, to $59.78 a barrel in electronic trading on the London-based ICE Futures Europe exchange on Thursday. West Texas Intermediate futures, the U.S. marker, jumped as much as 6.6 percent to $52.48 on the New York Mercantile Exchange.

“Yemen is not an oil producer of great significance but it is located geographically and politically in a very important part of the Middle East,” said Ric Spooner, a chief strategist at CMC Markets in Sydney.

The Bab el-Mandeb strait is the fourth-biggest shipping chokepoint in the world by volume, and is 18 miles wide at its narrowest point, according to the EIA. It’s located between Yemen, Djibouti, and Eritrea, and connects the Red Sea with the Gulf of Aden and the Arabian Sea.

Transport Threat

In 2013, 3.8 million barrels a day of oil and petroleum products flowed through Bab el-Mandeb, EIA data shows. More than half of the shipments moved to the Suez Canal and SUMED Pipeline, which serve as the link between Egypt’s ports of Ain Sukhna on the Red Sea and Sidi Kerir on the Mediterranean.

Closure of the waterway may keep tankers from the Persian Gulf from reaching the Suez Canal and the SUMED Pipeline, diverting them around the southern tip of Africa, adding to transit time and cost, according to the EIA. Ships carrying oil from Europe and North Africa won’t be able to take the most direct route to Asian markets if Bab el-Mandeb is shut, the EIA said on its website.

“As the situation in Yemen has dramatically escalated, it’s seen primarily as a threat to international shipping and oil transport,” Theodore Karasik, an independent geopolitical analyst, said from Dubai. “There’s concern that the more ungovernable Yemen becomes, the more it could become a base for piracy in the Red Sea area.”

Saudi Arabia, the United Arab Emirates, Bahrain, Qatar and Kuwait responded to a request from Yemen’s President Abdurabuh Mansur Hadi, according to a statement carried by the official Saudi Press Agency.

Proxy War

Saudi Arabia led OPEC’s decision in November to resist calls to reduce its output target of 30 million barrels a day, a resolution that Iranian Oil Minister Bijan Namdar Zanganeh said was “not in line with what we wanted.”

OPEC’s decision and an expanding U.S. supply glut have driven global benchmark oil prices to a six-year low.

“In the longer term, Iran will be happy to disrupt oil supplies,” Vautrain said. “They literally want to control Saudi Arabia and Iraq. They would love that. They’re fighting a proxy war and they will continue to fight a proxy war.” The Houthis, who follow the Zaydi branch of Shiite Islam, say they operate independently of Iran and represent only their group’s interests.

* * *

For now surging oil appears to be dragging the tightly correlated EURUSD by the bootstraps, and as a result the US Dollar despite it traditionally being a flight to safety during global proxy wars such as this one.

Looking at equities, overnight developments in Yemen have also been the key focus in early European trade after Saudi Arabia and a coalition of regional allies launched a military operation in Yemen against the Iranian-backed Houthi rebels, who deposed the US-backed Yemeni president last month. WTI crude futures rallied overnight, heading for its biggest 5 day gain since 2011 after Saudi Arabia and its allies confirmed that they had started military operations. Although Yemen is not a large oil-exporter, markets have become concerned by the situation in Yemen, largely because of the involvement OPEC nations in a Middle-Eastern conflict and because in a worst case scenario this conflict between Sunni and Shia Muslims could be used as a proxy for a larger conflict between Saudi and Iran. Alongside geopolitical concerns, European stocks are also being weighed upon by heavy selling in Asia, particularly in tech names, and with window dressing ahead of quarter-end.

Another slide in the USD led to moves across the FX space and a break above post-FOMC highs in EUR/USD and trades sources note large size (~EUR 1bln) bought on a break of 1.1000 in the pair. GBP sees some outperformance in early trade, gilts are underperforming and the short sterling strip lower following overnight comments from BoE’s Miles (soft dove) who said he believes the next move by the BoE will be a hike. This followed comments made yesterday by BoE Deputy Governor Shafik (Soft Dove) who said that the next move in rates is likely to be higher and BoE’s Forbes who said that low inflation would be temporary.

Asian stocks mostly fell overnight in a continuation of similar moves seen yesterday in European and US equity markets, which saw the S&P 500 erase all of its gains for the year to close below its 50 DMA. Consequently, both the Nikkei 225 (-1.6%) and ASX 200 (-1.6%) finished in the red, the latter recording its steepest drop in more than 2-weeks. Elsewhere, the Hang Seng (+0.2%) and Shanghai Comp (+1%) bucked the negative trend, led by financials and energy names ahead of earnings from PetroChina and ICBC.

Bund have been supported this morning with flows seen out of equities and into core fixed income, alongside little supply this week and prelim month-end extensions fairly average. Concerns over the situation in Greece also continue to linger and have supported this morning’s bid in bund futures.

Barclays Prelim Pan Euro Agg month-end extensions +0.07yrs (Prev. +0.07yrs, Avg. Of last 12 months +0.08yrs) Barclays Prelim month-end extensions for US Treasury +0.09yrs (Prev. +0.13yrs, Average of last 12 months +0.10yrs).

WTI crude futures rallied overnight, heading for its biggest 5 day gain since 2011 after Saudi Arabia and its allies confirmed that they had started military operations. In early trade WTI broke above its 50DMA and both WTI and Brent are trading with gains of over USD 2.00 ahead of the US open. Concerns have not only led to a bit in crude and equity markets in Europe falling over 1%, but has also led to a bid in gold which earlier broke above USD 1,200/oz and its 100DMA.

In summary: European shares fall with the tech and financial services sectors underperforming and oil & gas, basic resources outperforming. Stoxx 600 trades near session low; European energy stocks outperform as Saudi Arabia directs bombing sorties at Shiite Houthi rebels in Yemen. Brent, WTI crude futures both gain. U.K. retail sales rise more than forecast. The German and Swedish markets are the worst-performing larger bourses, the U.K. the best. The euro is stronger against the dollar. German 10yr bond yields fall; U.S. yields decline. Commodities gain, with soybeans, corn underperforming and WTI crude outperforming. U.S. jobless claims, continuing claims, Bloomberg consumer comfort, Kansas City Fed index, Markit U.S. composite PMI, Markit U.S. services PMI due later.

Market Wrap

- S&P 500 futures down 0.9% to 2034.7

- Stoxx 600 down 1.7% to 391.1

- US 10Yr yield down 3bps to 1.89%

- German 10Yr yield down 2bps to 0.21%

- MSCI Asia Pacific down 0.8% to 148

- Gold spot up 1.4% to $1212/oz

- Eurostoxx 50 -1.8%, FTSE 100 -1.4%, CAC 40 -1.6%, DAX -2%, IBEX -1.4%, FTSEMIB -1.9%, SMI -1.8%

- Asian stocks fall with the Shanghai Composite outperforming and the Sensex underperforming.

- MSCI Asia Pacific down 0.8% to 148; Nikkei 225 down 1.4%, Hang Seng down 0.1%, Kospi down 1%, Shanghai Composite up 0.6%, ASX down 1.6%, Sensex down 1.7%

- Euro up 0.55% to $1.103

- Dollar Index down 0.7% to 96.3

- Italian 10Yr yield up 1bps to 1.35%

- Spanish 10Yr yield little changed at 1.29%

- French 10Yr yield down 1bps to 0.49%

- S&P GSCI Index up 2.4% to 414.6

- Brent Futures up 4% to $58.7/bbl, WTI Futures up 4.3% to $51.4/bbl

- LME 3m Copper up 1.8% to $6237.5/MT

- LME 3m Nickel up 0.9% to $13805/MT

- Wheat futures up 1.2% to 525.3 USd/bu

Bulletin Headline Summary from Bloomberg and RanSquawk

- Developments in Yemen overnight unsettle markets as Saudi intervene, leading to significant gains in oil overnight and European equities falling over 1%

- WTI crude futures trade higher by over USD 2.00 after rallying overnight and this morning, and heads for its biggest 5 day gain since 2011

- Treasuries rally overnight as Saudi Arabia launches air strikes in Yemen while U.S. aids Iraqi forces attacking Tikrit; week’s auctions conclude with $29b 7Y, yield 1.71% in WI trading vs. 1.83% award in February.

- Saudia Arabia considering ground troops in Yemen, according to Saudi state TV, citing a person it didn’t identify

- Oil headed for its biggest five-day gain since 2009, while gold rallied with the yen; global stocks retreated with U.S. equity-index futures

- Negotiators aim to conclude a political framework on Iran’s nuclear work by March 29, according to three diplomats with direct knowledge of the talks taking place in Switzerland this week

- China plans to push for the yuan to take prominence in projects under the Asian Infrastructure Investment Bank and the Silk Road Fund as it seeks broader global use of its currency, said people familiar with the matter

- U.K. retail sales rose 0.7% in February, more than economists forecast, amid declining inflation

- Sovereign 10Y yields mixed, Greek 10Y steady. Asian stocks drop, European stocks decline, U.S. equity-index futures fall. Crude, gold and copper rise

DB’s Jim Reid completes the overnight event recap

the US equity market is stalling like my unloved car at the moment. The S&P 500 (-1.46%), Dow (-1.62%) and NASDAQ (-2.37%) all fell – the latter having its largest single daily decline since April last year as weakness in tech stocks in particular dragged bourses down. Our base case remains that the post-QE environment will be a challenge for US equities and although the S&P 500 is still +0.10% YTD, its being left behind by most other developed markets. It’s now back to levels first crossed back on November 21st – only a few weeks after QE finally ended. Bloomberg also extended the analysis we included yesterday that states that the S&P 500 hasn’t been this long without back to back gains (26 days now) since 1994. Quite a stat.

Soft US data helped support the generally weaker sentiment. The February reading for durable goods orders was a notable miss at -1.4% mom (vs. +0.2% expected) and was down significantly from the +2.0% print last month. The ex-transport reading fared little better with the -0.4% mom reading below expectations of +0.2%. Data for core capex orders meanwhile was also weak with the non-defense ex-aircraft (-1.4% mom vs. +0.3% expected) reading below market. The reading has now declined for six consecutive months. With US economic data surprises continuing to come in below consensus and extending the recent 6-year lows, the Atlanta Fed GDPNow tracking forecast was yesterday downgraded to +0.2% SAAR for Q1 of this year, having previously been running at +0.3%. With a raft of weak data prints of late, the forecast has in fact been lowered from an initial +1.9% back in early February. The Q4 reading is due this Friday, but it’ll be interesting to see where the market places Q1 growth forecasts following the data we’ve seen thus far.

There was plenty of chatter out of the Fed yesterday as well. Comments from the Chicago Fed’s Evans in particular were interesting, who noted that there is ‘no compelling reason’ to raise rates until the Fed is confident that inflation is moving back towards its 2% target. Specifically, Evans noted that lift-off in 2016 would be more appropriate, citing in particular the disinflationary effects of the Dollar putting pressure on US import prices. The Fed’s Lockhart, on the other hand, said that whilst he’s not ‘100% confident’ that the Fed will raise rates in June, July or September, ‘it’s quite likely’ (NY Times) it’ll be one of those months. Lockhart did however highlight that any reason for a move to come post-September would be due to a disappointment in the data. Elsewhere, Treasury yields were higher with the benchmark 10y yield finishing +5.2bps at 1.925% while Dollar weakness was a theme again, with the broader DXY closing -0.22%. Interestingly, Energy (+1.22%) was the one sector that had a better day yesterday as WTI (+3.58%) and Brent (+2.49%) rose. Overnight Oil is dominating the headlines with both WTI (+3.45%) and Brent (+2.80%) firmer again – both markets at one point trading over 5% higher intraday. Bloomberg is reporting that Oil has seen the biggest 5-day rally since 2011. Saudi Arabia’s (and its allies) bombing of Shiite rebels in Yemen is seemingly to blame as tensions with Iran build.

Refreshing our screens elsewhere this morning, it’s a fairly mixed reaction in equity markets on the back of moves in Oil and weakness in the US overnight. The Nikkei (-1.40%) and Kospi (-0.95%) have both declined while the Hang Seng (+0.11%) and Shanghai Comp (+0.66%) are both trading higher. Credit markets are a touch softer while the Dollar has extended declines with the DXY -0.27%.

It was a similar story to the US in Europe yesterday, as a weaker day for tech stocks dragged equity markets lower. Indeed, the Stoxx 600 (-1.13%) had its largest one-day decline since January 14th, while the DAX (-1.17%) and CAC (-1.32%) both closed lower. Bond markets were more mixed however. 10y Bunds closed 1.6bps lower at 0.218% while 10y yields in Spain (-0.5bps), Italy (+0.8bps) and Portugal (+2.3bps) traded more mixed. Despite the generally weaker sentiment, data was in fact supportive on the whole yesterday. Specifically, the March IFO reading for Germany provided further evidence of positive momentum for the economy. The index rose 1.1pts to 107.9 and ahead of expectations of 107.3. The reading was in fact the highest since July last year. Both the current assessment (112.0 vs. 111.3 previously) and expectations (103.9 vs. 102.5 previously) readings bounced. Our colleagues in Europe noted that the breakdown by sector pointed to fairly broad based growth and believe that the reading, along with generally solid prints thus far for the economy, support upside risks for their +0.5% qoq GDP forecast for Q1.

In Greece the pressure on the government to push through its reform proposals by Monday will only have heightened yesterday after we learned that the Eurogroup rejected Greece’s claim for the return of €1.2bn in funds the government believes it is owed at the EFSF. The hopes that reform proposals will soon be provided to the Eurogroup have led to some more conciliatory comments of late, backed up again by the EC President Juncker who said that he believes that a successful conclusion for both Greece and the EU will soon be realized. The fragile situation persists in the near term however. Yesterday we also learned that the ECB increased the ceiling on the ELA to €71.3bn, from €69.8bn previously – highlighting further stress in deposit outflows at Greek banks. Equity markets in Greece were closed yesterday for a public holiday.

Elsewhere yesterday, following comments from the Bank of England’s Haldane last week that a rate cut might be needed, a fellow MPC member, David Miles, yesterday said that he expected the next move in rates to likely be up, specifically saying that ‘I can certainly imagine a situation where inflation is under the target level perhaps by a significant amount and the right strategy would be gradually to start a process of normalization and edging (rates) up’ (FT). Miles highlighted that so far he hasn’t seen any persistent underlying deflationary pressures in the economy and believes that prices should rise towards the end of the year.

Turning to today’s calendar, we kick off this morning in Europe with German consumer confidence data, followed closely by French GDP data and money supply readings for the Euro-area. Retail sales and CBI data out of the UK are also due this morning. This afternoon in the US employment indicators are highlighted by the initial jobless claims print while the composite and services PMI’s and Kansas City Fed manufacturing activity reading are also due.

end

The proxy war in the middle east commenced last night

(courtesy zero hedge)

Another Middle East War Breaks Out: Saudis Begin Bombing Yemen, US Military Taking Action

Update: *OBAMA AUTHORIZED LOGISTICAL AND INTELLIGENCE SUPPORT TO GULF, U.S. MILITARY TAKING MILITARY ACTION TO DEFEND SAUDI BORDER, TO DEFEND AGAINST HOUTHI VIOLENCE

John McCain & Lindsay Graham explain Obama’s move…

U.S. Senators John McCain (R-AZ) and Lindsey Graham (R-SC) today released the following statement on Saudi Arabia leading an international coalition conducting air strikes against Iranian-backed separatists in Yemen:

“Saudi Arabia and our Arab partners deserve our support as they seek to restore order in Yemen, which has collapsed into civil war.

“We understand why our Saudi and other Arab partners felt compelled to take action. The prospect of radical groups like Al-Qaeda, as well as Iranian-backed militants, finding safe haven on the border of Saudi Arabia was more than our Arab partners could withstand. Their action also stems from their perception of America’s disengagement from the region and absence of U.S. leadership.

“A country that President Obama recently praised as a model for U.S. counterterrorism has now become a sectarian conflict and a regional proxy war that threatens to engulf the Middle East. What’s worse, while our Arab partners conduct air strikes to halt the offensive of Iranian proxies in Yemen, the United States is conducting air strikes to support the offensive of Iranian proxies in Tikrit. This is as bizarre as it is misguided – another tragic case of leading from behind.”

* * *

Earlier today we reported that, on very short notice, Saudi Arabia had moved heavy military equipment including artillery to areas near its border with Yemen, “raising the risk that the Middle East’s top oil power will be drawn into the worsening Yemeni conflict.” In other words, Saudi Arabia was preparing for war.

Shortly thereafter, but before Yemen’s presidentbravely fled the country over fears of the Houthi rebel advance, Yemen’s foreign minister called for Arab military intervention against advancing Shiite rebels.

As we explicitly warned, “the conflict risked spiraling into a proxy war with Shi’ite Iran backing the Houthis, whose leaders adhere Shi’ite Islam, and Saudi Arabia and the other regional Sunni Muslim monarchies backing Hadi.”

Moments ago all these warnings were borne out when Al-Arabiya reported that the latest middle-east war is now official after Saudi Arabia and Arab Gulf States had launched a bombing campaign against Yemen.

More details:

This is just the beginning:

and now the US is involved:

And tanks are crossing the border:

From Al-Arabiya:

Saudi Arabia’s Royal Air Force bombed the positions of Yemen’s Houthi militia, Al Arabiya News Channel reported early on Thursday.

Arab Gulf states had announced that they have decided to “repel Houthi aggression” in neighboring Yemen, following a request from the country’s President Abedrabbo Mansour Hadi.

In their joint statement Saudi Arabia, UAE, Bahrain, Qatar and Kuwait said they “decided to repel Houthi militias, al-Qaeda and ISIS [Islamic State of Iraq and Syria] in the country.”

The Gulf states warned that the Houthi coup in Yemen represented a “major threat” to the region’s stability.

It also accused the Iranian-backed militia of conducting military drills on the border of Saudi Arabia, a leading member of the GCC, with “heavy weapons.”

In an apparent reference to Iran, the statement said the “Houthi militia is backed by regional powers in order for it be their base of influence.”

The Gulf states said they had monitored the situation and the Houthi coup in Yemen with “great pain” and accused the Shiite militia of failing to respond to warnings from the United Nations Security Council as well as the GCC.

The statement stressed that the Arab states had sought over the previous period to restore stability in Yemen, noting the last initiative to host peace talks under the auspices of the Gulf Cooperation Council.

As reported this morning, in a letter sent the U.N. Security Council and seen by Al Arabiya News, Hadi requested “immediate support for the legitimate authority with all means and necessary measures to protect Yemen and repel the aggression of the Houthi militia that is expected at any time on the city of Aden and the province of Taiz, Marib, al-Jouf [and] an-Baidah.”

In his letter Hadi said such support was also needed to control “the missile capability that was looted” by the Houthi militias.

Hadi also told the Council that he had requested from the Arab Gulf states and the Arab League “immediate support with all means and necessary measures, including the military intervention to protect Yemen and its people from the ongoing Houthi aggression.”

To summarize: Saudi Arabia is now bombing a rebel force that has been armed by the US and is backed by Iran, even as the US is bombing an enemy of Iran in Iraq with the blessing of Saudi Arabia.

All in a day’s work in the Middle East.

As for oil’s reaction: after the algos initially appeared not to get the memo, they woke up…

As The Crude Curve flattens dramatically

* * *

The action has begun…

* * *

Saudi Arabia Imposes Naval Blockade On Red Sea Strait, Deploys 150,000 Troops As Iran Condemns Military Action

As noted earlier, the biggest significance of any Yemen conflict has little to do with its own domestic oil production, which at 133,000 bpd is negligible, but due to its location, which not only shares a border with Saudi Arabia, but more importantly due to the Bab el-Mandeb strait which connects the Red Sea with the Gulf of Aden: it is the fourth-biggest shipping chokepoint in the world by volume (3.8 million barrels a day of oil and petroleum products flowed through it in 2013) and is just 18 miles wide at its narrowest point. It’s located between Yemen, Djibouti, and Eritrea, and connects the Red Sea with the Gulf of Aden and the Arabian Sea.

And since to Saudi Arabia preserving the logistics of oil supply is critical, it is hardly surprising that as Egypt’s Ahram Gate reported earlier, the Saudi-led Firmness Storm coalition imposed a naval blockade on Bab El-Mandab strait earlier today. The Saudi navy’s western fleet has also secured Yemen’s main ports including Aden and Midi.

It is not just Saudi Arabia: moments ago Reuters reportedthat four Egyptian naval vessels have crossed the Suez Canal en route to Yemen to secure the Gulf of Aden, maritime sources at the Suez Canal said on Thursday. The sources said they expected the vessels to reach the Red Sea by Thursday evening.

The naval blockade is just part of what so far has been mostly an air-based proxy war. As Al Arabia reported previously, as part of the “Decisive Storm” coalition against the Yemen rebels, Saudi Arabia has deployed at least 150,000 soldiers in preparation for what appears to be a land assault next, an assault that already has the preemptive blessing of the US. As a reminder, Saudi Arabia will be fighting US-armed rebels, but that’s a different story.

Just as importantly, and since as we reported first yesterday the Yemen conflict is merely a proxy war between the Saudis and Iran, we also now have reports that Iran has condemned Saudi Arabia’s intervention, is demanding an immediate halt to the military action, and has warned that a war on Yemen won’t be contained in one area.

From Reuters:

Iran demanded an immediate halt to Saudi-led military operations in Yemen on Thursday and said it would make all necessary efforts to control the crisis there, Iranian news agencies reported.

“The Saudi-led air strikes should stop immediately and it is against Yemen’s sovereignty,” the Students News Agency quoted Iranian Foreign Minister Mohammad Javad Zarif as saying. “We will make all efforts to control the crisis in Yemen,” Zarif said, according to the agency’s report from the Swiss city of Lausanne where he is negotiating with six world powers to resolve a years-old dispute over Tehran’s nuclear ambitions.

Earlier on Thursday, the Foreign Ministry in Tehran called for an end to the military operation.

“Iran wants an immediate halt to all military aggressions and air strikes against Yemen and its people,” Fars quoted Foreign Ministry spokeswoman Marzieh Afkham as saying.

“Military actions in Yemen, which faces a domestic crisis, … will further complicate the situation … and will hinder efforts to resolve the crisis through peaceful ways.”

Prior to that, Bloomberg cited the head of the Iranian parliament’s national security and foreign policy committee, who told Iran’s Fars News Agency that Saudi Arabia’s strikes on Yemen will haunt the kingdom as war won’t be contained,

So as the proxy war snags more and more countries, threatens to become less proxy, more war and much more global, keep an eye on Russia which is caught in that “other” proxy war from 2014 and which is also going nowhere fast. Because if and when Russia and China pick sides and get involved, that’s when it may be a good time to take a vacation far away from any major metropolitan areas.

end

This afternoon, an expected ground invasion by Saudi and Egyptians troops is imminent:

(courtesy zero hedge)

Yemen Ground Invasion By Saudi, Egyptian Troops Imminent

As reported first thing today, while the initial phase of the military campaign against Yemen has been taking place for the past 18 hours and been exclusively one of airborne assaults by forces of the “Decisive Storm” coalition, Saudi hinted at what is coming next following reports that it had built up a massive 150,000 troop deployment on the border with Yemen.

And as expected, moments ago AP reported that Egyptian military and security officials told The Associated Press that the military intervention will go further, with a ground assault into Yemen by Egyptian, Saudi and other forces, planned once airstrikes have weakened the capabilities of the rebels.

Will this invasion mean that Yemen as we know it will no longer exist and become annexed by Saudi Arabia? According to coalition military sources, the answer is no, but that remains to be seen:

Three Egyptian military and security officials told The Associated Press that a coalition of countries led by Egypt and Saudi Arabia will conduct a ground invasion into Yemen once the airstrikes have sufficiently diminished the Houthis and Saleh’s forces. They said the assault will be by ground from Saudi Arabia and by landings on Yemen’s Red and Arabian Sea coasts.

The aim is not to occupy Yemen but to weaken the Houthis and their allies until they enter negotiations for power-sharing, the officials said.

They said three to five Egyptian troop carriers are stationed off Yemen’s coasts. They would not specify the numbers of troops or when the operation would begin. They spoke on condition of anonymity because they were not authorized to talk about the plans with the press.

Egypt’s leadership role in the next stage of the campaign has come as somewhat of a surprise to observers. Egypt’s presidency said in a statement Thursday that its naval and air forces were participating in the coalition campaign already. Egypt is “prepared for participation with naval, air and ground forces if necessary,” Foreign Minister Sameh Shukri said at a gathering of Arab foreign ministers preparing for a weekend Arab summit in the Egyptian resort of Sharm el-Sheikh.

This may be just the beginning:

The Arab Summit starting Saturday is expected to approve the creation of a new joint Arab military force to intervene in regional crises. The Egyptian security and military officials said the force is planned to include some 40,000 men backed by jet fighters, warships and light armor. Hadi is expected to attend the summit.

The locals do not sound much enthused about the prospect of allowing foreign troops to enter their country uncontested, and as AP notes, support for the Houthis is far from universal in Yemen – but foreign intervention risks bringing a backlash.

On Thursday, thousands gathered outside Sanaa’s old city in the Houthi-organized protest, chanting against Saudi Arabia and the United States.

Khaled al-Madani, a Houthi activist, told the crowd that “God was on the side of Yemen.” He blasted Saudi Arabia saying it is “buying mercenaries with money to attack Yemen. But Yemen will, God willing, will be their tomb.”

Anger against the strikes was already brewing – particularly after airstrikes targeting an air base near Sanaa’s airport flattening half a dozen homes in an impoverished neighborhood and killing at least 18 civilians, according to the health ministry.

For now Yemeni anger is focused on Saudi Arabia:

TV stations affiliated with the rebels and Saleh showed the aftermath of the strikes Thursday. Yemen Today, a TV station affiliated with Saleh, showed hundreds of residents congregating around the rubbles, some chanting “Death to Al-Saud”, in reference to the kingdom’s royal family. The civilians were sifting through the rubble, pulling out mattresses, bricks and shrapnel.

Ahmed al-Sumaini said an entire alley close to the airport was wiped out in the strikes overnight. He said people ran out from their homes in the middle of the night, many jolted out of bed to run into the streets.“These people have nothing to do with the Houthis or with Hadi. This is destructive. These random acts will push people toward Houthis,” he said, as he waved shrapnel from the strikes.

Strikes also hit in the southern province Lahj and the stronghold of Houthis in the northern Saada province. In Sanaa, they also hit the camp of U.S.-trained Yemeni special forces, which is controlled by generals loyal to Saleh, and a missile base held by the Houthis.

But that will soon change, as it is a virtual certainty that the US will intervene at a point in the near future, with its own military assets. So while we await to see just where US troops make landfall, here is the most updated map showing the locations of US naval assets around the globe in general, and in proximity to Yemen in particular. Keep a very close eye on the LHD-7 Iwo Jima amphibious assault ship (which carries some 2,000 marines of the 24th Marine Expeditionary Unit), currently located just off the coast of Yemen.

Most Americans Will Miss The Start Of World War Three

The start of what could be a major military conflict in the Middle East began yesterday when Saudi Arabia began bombing Yemen last night. But if you get your news from Bloomberg.com or CNN or Fox, the only big news to which you would be exposed is the German commercial airliner crash, which occurred nearly three days ago.

Just for grins – in order to see what kind of pig vomit the major cable news networks are feeding to the masses who even make an attempt to stay current on news that doesn’t relate to the Kardashians or The Voice, I like to surf between Fox News and CNN in the morning. I can say with conviction that had I not known about the Saudi/Yemen war escalation through the althernative internet-based media, I might think that the only real world event this weeks has been the 3-day old plane crash. The front page of Bloomberg.com this morning does not have one reference to the Saudi bombing.

However, aside from the ongoing global economic collapse, the developing military conflict in the Middle East has the potential to profoundly affect life in this country as we know it. The plane crash? Bad for the people who died and their families – a non-event for the cable news tv junkies.

But the Mid-East situation, at the root, is the escalation of an ongoing political and economic conflict between the Saudis and Iran. The Saudis are the driving force behind the U.S. insistence that Iran give up its nuclear program (and yet, there’s Israel sitting in the middle of it with enough nuclear firepower to incinerate the globe). I’m sure less than 1% of the U.S. population realizes this, but Yemen is now to a agree controlled by Iran (link).

We know that the U.S. and Saudi Arabia in bed together. But guess who is implicitly allied with Iran? Russia and China both have strong economic ties with Iran and it is my belief that is why the U.S. has been backing down from it’s original stance regarding Iran’s nuclear program.

But if Iran and Saudi engage in a war by proxy with Yemen as the battle ground, it could well draw in a military engagement between Russia/China and the U.S. In fact, the Nobel Peace Prize-toting Obama has already authorized military support for Saudi Arabia – LINK. I would not be surprised, just as happened in Syria, if Putin flexes his muscles at some point if this situation escalates further in support of Iran.

The U.S. is inciting chaos and military activity all over the globe now. It is highly reminiscent of the period of time leading up to the collapse of Rome…but hey, someone has to profit from war. The American defense companies are smiling all the way to the bank. And the big multi-national oil companies are jumping with joy as oil is now $8 above it’s recent lows, having gapped up about $5 in the last 2 days in response to the Saudi/Yemen developments…(Q: “how can you shoot women and children?” A: Easy, ya just don’t lead ‘em so much…AIN’T WAR HELL? )

end

As promised to you last month, where I warned you to expect many dead bodies to surface with the failure of Austria’s Hypo bank. The ECB is quietly asking all the banks to detail their exposure:

(courtesy zero hedge)

One Month After Austria’s Black Swan Shocker, The ECB Quietly Asks Banks to “Detail Their Exposure”

Nearly a month after the Hype Alpe Adria bad bank Heta Asset Resolution “unexpectedly” imploded under a house of non-GAAP and misreported cards, and which led to only the second European creditor bail-in after Cyprus in what until then was considered the safest European nation, unleashing a herd of black swans which will result in not only the insolvency of one of Austria’s provinces, Carinthia, but a week ago led to its first foreign casualty, German Duesseldorfer Hypothekenbank AG which had to be bailed out by the German FDIC-equivalent, the ECB has finally realized it may have a major problem at hand.

So, doing what it does best, a month after the fact and long after the black swans have left the stable so to speak, Mario Draghi’s ECB has asked Eurozone banks “to detail their exposure to Austria and provisions they plan to make after the country halted debt repayments by a “bad bank” winding down defunct lender Hypo Alpe Adria,” financial sources told Reuters.

From Reuters:

The questionnaire sent to banks and a video conference to discuss the potential fallout underscore the sensitivity of Austria’s path-breaking move to invoke new European rules on ensuring creditors, not just taxpayers, fund bailouts.

“They are taking this seriously,” one senior executive said of the ECB on the condition he not be identified. The ECB declined to comment.

Bankers say Austria’s credibility is on the line after the second move in two years to impose losses on creditors of Hypo, many of whom assumed they had iron-clad backing from the state.

Odd how these things happen: first EURCHF longs “assumed” iron-clad backing from the SNB… until it was yanked from under their feet. Then, creditors in what many saw as the safest European nation “assumed” they would never suffer losses and would be bailed out for ever… until they saw 50% losses in a matter of minutes.

And if you can’t trust an Aaa/AA+ rated country, just who can you trust? One can see why the confidence in a system in which risk until recently was illegal, is starting to crack.

For now, however, one can still keep kicking the can, as the creditor losses haven’t been fully digested yet.

The debt moratorium gives the FMA time to work out a plan that ensures equal treatment of creditors. It has given no details on what size “haircut” bondholders might expect and has not ruled out sending Heta into insolvency.

The moratorium on more than 11 billion euros in Heta debt has sent shock waves beyond Austria.

Germany’s Bundesbank central bank said German banks have around 5.5 billion euros in Heta exposure. Germany’s deposit protection fund had to take over property lender Duesseldorfer Hypothekenbank AG after it ran aground over Heta exposure.

The Heta move comes after Austria entered uncharted waters for debt markets last year by wiping out via a special law holders of nearly 900 million euros worth of Hypo subordinated debt despite guarantees from its home province of Carinthia. That triggered lawsuits that the country’s Constitutional Court is set to rule on by October.

Some creditors have said they are looking into taking legal steps over the Heta decision, and the FMA is preparing itself for legal action against its decisions.

And hell hath no fury like a bondholder who assumed par recovery is 100% assured, scorned.

Our only question now is that as the flock of Austrian black swans gets tired and prepares to land, just which “assumed” safe financial institution is about to lead to even more creditor scorn.

end

This will be fun. I have pointed out to you on several occasions that Putin loaned the Ukraine 3 billion USA. The note is due this December. However, it has a stipulation: if the Ukraine’s debt to GDP exceeds 60% then Russia can call on that note. Right now the Debt to GDP has already exceeded 60%.

Russia is in no mood to take a haircut on its debt in order to give the west an orderly default. Europe still needs Russia for its oil. Will Putin just ask for the 3 billion usa now and put the Ukraine into a disorderly bankruptcy and throw billions of dollars in credit default swaps into the wind????

Popcorn anyone???

(courtesy zero hedge)

Putin Is Becoming A “Vulture” Bond Investor

With Washington throwing its full faith and credit behind a new Ukrainian bond issue, it appears it’s time for Moscow to play spoiler to current debt restructuring talks between Kiev and its creditors. Russia is the country’s second-largest creditor after buying $3 billion in bonds back in the days of Viktor Yanukovych (who was once the victim of an attempted assassination by egg and who famously fled the country amid widespread protests last year) and now the Kremlin wants its money and isn’t likely to be amenable to any haircuts imposed on private creditors. Here’s more from Bloomberg:

Ukraine, after gaining a lifeline from the International Monetary Fund, included Russia’s bond among the 29 securities and enterprise loans it seeks to renegotiate with creditors before June. Finance Minister Natalie Jaresko has promised not to give any creditor special treatment. The revamp will include a reduction in the coupon, an extension in maturities as well as a cut in the face value, she said.

Russian Deputy Finance Minister Sergey Storchak said March 17 that the nation isn’t taking part in the debt negotiations because it’s an “official” creditor, not a private bondholder.

Should Russia decide to stick with a hardline stance on the negotiations (and it’s likely they will) it could not only embolden other prospective holdouts, but may indeed force Ukraine into a default:

Holding out can lead to two outcomes: Russia gets paid back in full after the notes mature in December, or Ukraine defaults. The former option is politically unacceptable in Kiev, according to Tim Ash, chief emerging-market economist at Standard Bank Group Plc, while the latter would likely start litigation and delay the borrower’s return to foreign capital markets, which Jaresko expects in 2017.

“Russia will be holdouts, to try and force a messy restructuring,” Ash said by e-mail on March 19.

If Russia holds out and litigates, there is a “real threat” that Ukraine will deem the Eurobond an odious debt, Lutz Roehmeyer, a money manager at Landesbank Berlin Investment GmbH, said by e-mail on March 23. This refers to a legal theory that a nation shouldn’t be forced to repay international obligations if they don’t serve the best interests of the country and its citizens.