Gold $1272.50 UP $4.30

Silver 17.68 UP 8 cents

In the access market 5:15 pm

Gold: 1276.00

Silver: 17.77

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix OCT 28 (10:15 pm est last night): $ 1275.87

NY ACCESS PRICE: $1270.90 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1273.38

NY ACCESS PRICE: 1267.95 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!! 5 dollars

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: OCT 28: 5:30 am est: $1265.90 (NY: same time: $1266.00: 5:30AM)

London Second fix OCT 27: 10 am est: $1273.00 (NY same time: $1272.20 , 10 AM)

Shanghai premium in silver over NY: 80 cents.

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

.

For comex gold:

1 NOTICE(S) FILED FOR 100 OZ

For silver:

for the Oct contract month: 13 notices for 65,000 oz.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 1772 contracts DOWN to 193,605. The open interest FELL despite the fact that the silver price was UP 1 cent in yesterday’s trading .In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .968 BILLION TO BE EXACT or 138% of annual global silver production (ex Russia &ex China).

In silver for October we had 13 notices served upon for 65,000 oz

In gold, the total comex gold ROSE by 417 contracts WITH THE RISE in price of gold ($3.10 YESTERDAY) . The total gold OI stands at 506,392 contracts.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

TODAY WE HAD NO CHANGES AT THE GLD OUT OF THE GLD

Total gold inventory rests tonight at: 942.59 tonnes of gold

SLV

we had NO CHANGES at the SLV/

THE SLV Inventory rests at: 360.673 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL by 1,772 contracts DOWN to 193,605 DESPITE the price of silver RISING by 1 cent with yesterday’s trading.The gold open interest ROSE by 417 contracts UP to 506,809 as the price of gold ROSE $3.10 IN YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3c COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 8.08 POINTS OR 0.26%/ /Hang Sang closed DOWN 177.54 OR 0.77%. The Nikkei closed UP 109.99 POINTS OR 0.63% Australia’s all ordinaires CLOSED DOWN 0.14% /Chinese yuan (ONSHORE) closed UP at 6.7802/Oil FELL to 49.34 dollars per barrel for WTI and 50.15 for Brent. Stocks in Europe: ALL IN THE MIXED Offshore yuan trades 6.7937 yuan to the dollar vs 6.7802 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS A BIT AS MORE USA DOLLARS LEAVE CHINA’S SHORES / CHINA SENDS A MESSAGE TO THE USA TO NOT RAISE RATES IN DECEMBER.

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

NONE TODAY

4 EUROPEAN AFFAIRS

i)ENGLAND

The pound tumbles after a Northern Irish judge rejected a pair of challenges to the PREXIT process. This removes at least one obstacle to Prime Minister May’s plan as it begins to sever ties with the European Union by the end of March 2017:

( zero hedge)

ii)The crashing pound causes Apple and other companies to raise their electronic prices:

( zero hedge)

iii)London real estate is crashing

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Sooner or later an accident is going to happen: Russia and USA jets in a “near miss” situation over Syria:

( zero hedge)

6.GLOBAL ISSUES

7.OIL ISSUES

i)The oil producers have engaged in heavy hedging. If the oil price drops, they will survive but not necessarily the likes of Saudi Arabia and other producing nations:

( zerohedge)

ii)WHAT A JOKE!! Iraq and Iran refuse to freeze output and thus WTI plummets into the 48 dollar handle.

8.EMERGING MARKETS

The extremely clever Horseman Capital calls it quits on an emerging fund. These guys are 100% short and now they cannot make money

(courtesy zero hedge)

9.PHYSICAL STORIES

i)A huge commentary from Alasdair tonight as he explains how China is manipulating the dollar through its exchange rate and how China is selling its dollar reserves to accumulate commodities like oil and gold. Alasdair is the one who 2 yrs ago claims that China may have over 20,000 tonnes of gold to its credit.

a must read..

( Alasdair Macleod)

ii)Egon Von Greyerz explains correctly that gold denominated in any other currency than the USA dollar is at close to record levels or near their 2011 highs:

( Egon Von Greyerz)

iii)Barrick desperate to sell some of its prized assets. These clowns went to bed with the crooked banks and look at the trouble they are in

(courtesy Danielle Bochove/Bloomberg)

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)At first blush, the estimate for Q3 GDP climbs to 2.9% due to inventory and export gains. This will be adjusted southbound in the next two readings.

( zero hedge)

ii)We have pointed this out to you on several occasions: slumping used car prices will be catastrophic for the auto industry due to the heavy subprime auto securitization. Auto loan balances continue to rise. This will be a huge bubble when it burst:

( zero hedge)

iii)This kind of shows you the trouble the retail is having in the USA: American Apparel is now preparing a second bankruptcy filing in a year:

( zero hedge)

iv)The all important Michigan national consumer confidence crashes to a 2 yr low:The democrats are getting a little nervous.

( zero hedge/Michigan Consumer Confidence)

v)Another sign that there is trouble on the economic scene : Healthcare stocks tumble on terrible McKesson earnings;

( zero hedge)

vi) Finally we get the Wall Street Journal lashing out at the Clintons for their crimes:

( Wall Street Journal/.zero hedge)

vii) a.The big news of the day: the FBI reopens probe into Hillary’s emails

(courtesy FBI/zero hedge)

vii.b To complicate matters, Ryan issues a statement on the FBI re-opening of Hillary’s email scandal:

and the election is 11 days from today:

( Paul Ryan/zero hedge)

vii c. Hillary refuses to comment on the FBI renewal of investigation on her email scandal

( zero hedge)

vii dThe new investigation by the FBI commences due to a “device” which contained new emails and these were discovered as part of an unrelated investigation

( zero hedge)

vii. e The odds for a Trump victory just shot up!

( zero hedge)

vii f) What a riot: the device is from Huma Abedin and the target is former congressman Weiner who texted sexual messages to an under aged 15 yr old. Obviously there was some good stuff on Hillary on that device

(courtesy zero hedge)

viii g Our good friend John Podesta is mighty angry with the re opening of the FBI probe:

( zero hedge)

vii h)Here is another strange one!! The White House had no prior knowledge of the new attack on Hillary by the FBI

Let us head over to the comex:

The total gold comex open interest ROSE BY 417 CONTRACTS to an OI level of 506,809 as the price of gold ROSE $3.10 with YESTERDAY’S trading.

We are in the delivery month is October and here the OI GAINED 33 contracts UP to 342. We had 20 notices filed YESTERDAY so we GAINED 53 contracts or 5300 additional oz will stand for delivery.

The next delivery month is November and here the OI FELL by 79 contract(s) DOWN to 1,804 contracts. This level is extremely elevated as generally November is a very poor delivery month.To give you an idea of size, on Oct 26 2015, we had an OI of only 421 contracts standing. Eventually by the end of Nov 2015, a total of 214 notices stood for delivery for 21,400 oz (.6656 tonnes).The next contract month and the biggest of the year is December and here this month showed an decrease of 5156 contracts down to 362,790.

And now for the wild silver comex results. Total silver OI FELL by 1772 contracts from 196,374 DOWN TO 193,605 even though the price of silver ROSE to the tune of 1 cent yesterday. We are moving further from the all time record high for silver open interest set on Wednesday August 3: (224,540). The next non active delivery month is October and here the OI rose by 11 contracts up to 52. We had 3 notices filed yesterday so we gained 14 contracts or an additional 70,000 oz will stand for delivery. The November contract month saw its OI LOSE 6 contracts down to 334. The next major delivery month is December and here it fell BY 3,821 contracts down to 142,965.

we had 13 notices filed for 65,000 oz

VOLUMES: for the gold comex

Today the estimated volume was 96.439 contracts which is EXTREMELY POOR.

Yesterday’s confirmed volume was 147,680 which is ALSO POOR.

The CME has shot themselves in the foot as many do not want to play in a crooked cascino which will explain the terrible volumes.

today we had 20 notices filed for 2000 oz of gold:

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | NIL |

| Withdrawals from Customer Inventory in oz nil |

128.60 oz

4 kilobars

Manfra

|

| Deposits to the Dealer Inventory in oz | nil oz

|

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

1 notice

100 oz

|

| No of oz to be served (notices) |

341 contracts

34,100

oz

|

| Total monthly oz gold served (contracts) so far this month |

9435 contracts

943,500 oz

29.346 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 388,912.1 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract of which 0 notices were stopped (received) by jPMorgan dealer and 1 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

349,998.58 oz

Brinks

CNT

|

| Deposits to the Dealer Inventory |

NIL OZ

|

| Deposits to the Customer Inventory |

600,726.75 oz

CNT

|

| No of oz served today (contracts) |

13 CONTRACT(S)

(65,000 OZ)

|

| No of oz to be served (notices) |

39 contracts

(195,000 oz)

|

| Total monthly oz silver served (contracts) | 516 contracts (2,580,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 8,082,802.5 oz |

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 285,376 | 88,396 | 57,916 | 114,700 | 332,299 | 457,992 | 478,611 |

| Change from Prior Reporting Period | ||||||

| 11,031 | -6,331 | 1,661 | -741 | 14,187 | 11,951 | 9,517 |

| Traders | ||||||

| 188 | 103 | 83 | 51 | 55 | 284 | 200 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 49,625 | 29,006 | 507,617 | ||||

| -1,395 | 1,039 | 10,556 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, October 25, 2016 | |||||

SILVER COT

Our large specs

those large specs who have been long in silver pitched a large 2017 contracts from their long side.

those large specs who have been short in silver added a tiny 196 contracts to their short side.

Our commercials;

those commercials who have been long in silver added 3349 contracts to their long side

those commercials who have been short in silver added 1834 contracts to their short side

Our small specs;

those small specs who have been long in silver pitched 2023 contracts to their long side

those small specs who have been short in silver added 101 contracts to their short side.

Conclusions; the commercials are still having trouble vacating their short position in silver: they go net long again by 1515 contracts

end

NPV for Sprott and Central Fund of Canada

end

And now your overnight trading in gold,FRIDAY MORNING and also physical stories that may interest you:

Trump “Will Probably Win” and Gold “May Rise $100” Overnight – Rickards

Jim Rickards: Trump “Will Probably Win” and Gold “May Rise $100” Overnight

The US election is just two weeks away on November 8th, and one of Hillary Clinton’s most vocal critics on the business side is finance commentator and monetary expert Jim Rickards. Jim is in Sydney this week, armed with his latest book, hot off the press entitled ‘The Road to Ruin – The Global Elites’ Secret Plan for the Next Financial Crisis’ and gave an interesting television interview to ‘The Business’ on ABC Australia.

Rickards says that Trump “will probably win” and, if he does, stock markets will crash 10% and gold will rise $100 over night.

The markets and polls believe Clinton will win and that is priced into markets in the same way that a ‘Bremain’ was priced into markets prior to the ‘Brexit’ vote.

Kilkenomics 2016 – Where Comedy Meets Economics

“If Hillary wins nothing happens, if Trump wins you will have an earthquake.”

Should Trump win, which looking at the polls is not an impossibility, gold would likely surge $100 per ounce overnight, says Rickards.

What Hillary did was appalling Rickards says in relation to the Clinton email scandal. There will be ‘another reckoning on November 8th’ which the market has failed to price in, creating a good scenario for gold. He says you don’t have to agree that Trump will win, but agree that that in reality he could win.

For Rickards, this is an excellent opportunity for investors, particularly those who have an allocation to physical gold which he believes is set to rise in the coming months and years.

Jim is editor of Strategic Intelligence for Agora Financial as well as the founder of the James Rickards Project: an inquiry into complex dynamics of geopolitics and capital. He is also the author of New York Times bestsellers The New Case for Gold, Currency Wars: The Making of the Next Global Crisis and The Death of Money: The Coming Collapse of the International Financial System.

Jim’s newest book, The Road to Ruin will be published in November and he is appearing at Kilkenomics 2016 where he will speak at a number of events.

Watch extended interview with Rickards on ABC Australia here

Kilkenomics was Europe’s first economics festival and is taking place November 10th (Thurs) to November 13th (Sunday) in beautiful Kilkenny, Ireland.

Often referred to as ‘Davos with jokes’, Kilkenomics brings together leading economists, financial analysts and media commentators with some of the funniest stand-up comedians around.

This year GoldCore are one of the sponsors and are speaking on a panel with Jim Rickards and David McWilliams, the founder of Kilkenomics, on the Saturday, November 12th at 3pm. Click here for more info:

A Guide to Investing in 2017

Excellent contributors this year include:

- Nicolas Taleb

- Paul McCulley

- Steve Keen

- Dan Ariely

- Dara Ó Briain

- Linda Yueh

- Wolfgang Münchau

- Bill Black

- Matthew Bishop

- Liam Halligan

Tickets are on sale now and will sell out fast. More information about the event and bookings can be made here

Buy tickets for Kilkenomics 2016

Gold and Silver Bullion – News and Commentary

Gold ends higher as economic data raise uncertainty for interest-rate hike (MarketWatch.com)

Gold prices show small gains in Asia as U.S. durable goods data noted (Investing.com)

Gold steady on subdued stocks, set for second weekly gain (Reuters.com)

Gold’s Not Budging From 200-Day Average as India Buys: Chart (Bloomberg.com)

Gold Imports by China Increase for First Time in Four Months (Bloomberg.com)

Clinton win doesn’t mean market stability, says gold firm (IrishExaminer.com)

Do you own long-term bonds? You might want to think about selling (MoneyWeek.com)

This Is What Gold Does In A Currency Crisis, Brexit Edition (DollarCollapse.com)

These Are the Charts That Scare Wall Street (Bloomberg.com)

Gold Prices (LBMA AM)

28 Oct: USD 1,265.90, GBP 1,042.47 & EUR 1,160.96 per ounce

27 Oct: USD 1,269.30, GBP 1,038.29 & EUR 1,162.93 per ounce

26 Oct: USD 1,273.90, GBP 1,043.45 & EUR 1,166.13 per ounce

25 Oct: USD 1,269.30, GBP 1,037.53 & EUR 1,165.85 per ounce

24 Oct: USD 1,267.00, GBP 1,034.89 & EUR 1,163.61 per ounce

21 Oct: USD 1,263.95, GBP 1,033.79 & EUR 1,160.69 per ounce

20 Oct: USD 1,269.20, GBP 1,034.65 & EUR 1,156.75 per ounce

Silver Prices (LBMA)

28 Oct: USD 17.61, GBP 14.51 & EUR 16.13 per ounce

27 Oct: USD 17.66, GBP 14.41 & EUR 16.16 per ounce

26 Oct: USD 17.66, GBP 14.46 & EUR 16.17 per ounce

25 Oct: USD 17.73, GBP 14.49 & EUR 16.30 per ounce

24 Oct: USD 17.64, GBP 14.41 & EUR 16.19 per ounce

21 Oct: USD 17.51, GBP 14.34 & EUR 16.08 per ounce

20 Oct: USD 17.60, GBP 14.35 & EUR 16.03 per ounce

Recent Market Updates

– World Is Out of Weapons

– Gold Is The “Kardashian of Commodities” – Herbert & Keiser Interview Skoyles

– Value of Gold – Unlike Paper Currency Gold Maintained Value Throughout Ages

– Fed Risks Lehman Crisis As US Recession Storm Gathers

– Silver Eagle Demand ‘Returned with a Vengeance’

– Cashless Society – War On Cash to Benefit Gold?

– “Higher Gold Prices” On Global Trade Slowdown – HSBC

– Euro “Will Collapse” As Is “House of Cards” Warns Architect of Euro

– Property Bubble In Ireland Developing Again

– “Gold Is A Great Hedge Against Politicians” – Goldman

– Sell Gold Now – Time To Liquidate Gold ETF, Pooled and Digital Gold

– Gold In GBP Up 43% YTD – “Massive Twin Deficits” To Impact UK Assets

– Ron Paul Says “Gold Going Up” Whether Trump Or Clinton Elected

END

A huge commentary from Alasdair tonight as he explains how China is manipulating the dollar through its exchange rate and how China is selling its dollar reserves to accumulate commodities like oil and gold. Alasdair is the one who 2 yrs ago claims that China may have over 20,000 tonnes of gold to its credit.

a must read..

(courtesy Alasdair Macleod)

Alasdair Macleod: The vexed question of the dollar

Submitted by cpowell on Thu, 2016-10-27 17:13. Section: Daily Dispatches

12:15p CT Thursday, October 27, 2016

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod writes today that China is controlling both interest rates and gold prices and likely already has enough gold to hedge its dollar exposure in its huge foreign exchange reserves. Macleod’s analysis is headlined “The Vexed Question of the Dollar” and it’s posted at GoldMoney here:

https://wealth.goldmoney.com/research/goldmoney-insights/the-vexed-quest…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Egon Von Greyerz explains correctly that gold denominated in any other currency than the USA dollar is at close to record levels or near their 2011 highs:

(courtesy Egon Von Greyerz)

Egon von Greyerz: Except in dollars, gold is near the 2011 highs

Submitted by cpowell on Thu, 2016-10-27 17:43. Section: Daily Dispatches

12:45p CT Thursday, October 27, 2016

Dear Friend of GATA and Gold:

Swiss gold fund manager Egon von Greyerz writes that while gold lately has not been doing well in U.S. dollar terms, in terms of other currencies it has being doing very well indeed, even spectacularly. Von Greyerz’s analysis is headlined “Gold Is Near the 2011 Highs” and it’s posted at the Gold Switzerland internet site here:

https://goldswitzerland.com/gold-is-near-the-2011-highs/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

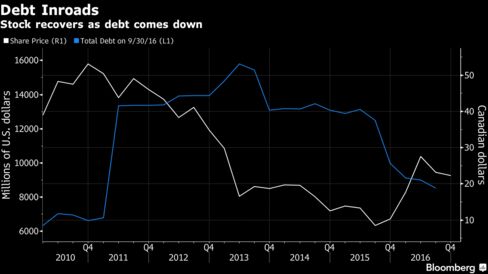

Barrick desperate to sell some of its prized assets. These clowns went to bed with the crooked banks and look at the trouble they are in

(courtesy Danielle Bochove/Bloomberg)

Barrick Gold Keeps Door Open to Selling Most Prized Assets

-

Selling stakes in Veladero and Pascua-Lama ‘could make sense’

-

Dushnisky reiterates will only sell Kalgoorlie for full value

Barrick Gold Corp. is keeping the door open to selling pieces of its most-prized assets, with South American partnerships among the more likely opportunities.

The company would consider forming partnerships with investors at its Veladero mine and its Pascua-Lama project, Kelvin Dushnisky said. But while “you never say never,” selling stakes in Barrick’s two key Nevada mines is unlikely.

“A core mine doesn’t stay a core mine forever,” he said Thursday in a phone interview. “But if you consider a Goldstrike or a Cortez, those are examples where these are engines of growth for company. They’ll be core mines for a very, very long period of time.”

Over the past three years, the world’s biggest gold producer has been divesting non-core assets to reduce debt. In an interview earlier this year, Executive Chairman John Thornton raised the possibility that sales could extend to some core assets. On Thursday, Dushnisky expanded on that view.

Barrick would consider selling assets it owns in the 140-kilometer (87-mile) stretch between Argentina and Chile that includes Veladero and the Pascua-Lama project, he said, but would only do so if there was a “strategic rationale.” Asked if this could include selling a stake in Veladero in exchange for help in developing Pascua-Lama, Dushnisky said such an arrangement “could make sense.” He declined to comment on whether potential buyers have approached the company about this.

Andes Project

Pascua-Lama, a $8.5 billion project high in the Andes, has been mostly shuttered since 2013 when a Chilean court accepted an injunction filed by indigenous groups over water-contamination concerns.

Toronto-based Barrick considers five mines as core assets: Cortez and Goldstrike, its 60 percent stake in Pueblo Viejo in the Dominican Republic, Lagunas Norte in Peru, and Veladero. The company has viewed its Turquoise Ridge mine in Nevada as an “emerging core” asset.

Barrick expanded through the commodities super cycle, purchasing Equinox Minerals Ltd. in 2011 and swelling its debt to a peak of $15.8 billion in 2013. Hit by a lengthy gold rout, it has been working ever since to cut costs and sell assets. Those include the sale of a 50 percent stake in the Porgera mine in Papua New Guinea and half its stake in the Zaldivar copper mine in Chile.

The company isn’t concerned that selling core mines, or stakes in those mines, would reduce production, Dushnisky said. “The notion of producing less gold isn’t something that would necessarily be troubling to us,” he said, noting that the company remains focused on improving margins. Thornton recently unveiled ambitious plans to use technology to increase efficiency across operations, starting with Cortez.

‘Medium Term’

Proceeds from asset sales would be more likely used for debt repayment than to replenish production, Dushnisky said. Barrick’s debt stood at about $8.5 billion at the end of the third quarter, and should be down to $8 billion by year end, he said. Although the cost to buy back debt is rising, the company remains committed to cutting debt to $5 billion in the “near to medium term,” he said.

Barrick rose 1.8 percent to C$22.96 at 10:01 a.m. in Toronto. The shares have more than doubled this year.

On Wednesday, Barrick reported better-than-expected earnings as it produced more ounces at lower costs than analysts estimated at a time of recovering prices.

Third-quarter profit excluding one-time items rose to 24 cents a share, the company said in a statement. That compares with a 21-cent average estimate among analysts tracked by Bloomberg. Sales were also slightly ahead of projections.

Super Pit

In an interview in July, Dushnisky said the company will continue divesting non-core assets assuming it can get full value. These include its 50 percent stake in Zaldivar; its Zambian Lumwana copper mine; and its 64 percent interest in the publicly traded African operation, Acacia Mining Plc.

In July, Barrick announced a formal process was under way to sell its 50 percent stake in the Kalgoorlie Super Pit in Australia, which it co-owns with operator Newmont Mining Corp. The company has put no timeline on closing the Kalgoorlie deal, Dushnisky said.

“What we’re hopeful is to extract the best possible value,” he said Thursday of Kalgoorlie. “If we feel that at the end of the process we’re not where we think we should be, then we’re happy to continue to own the asset. We’re not going to lose that discipline.”

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.7802( REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN WIDENS TO 6.7938 / Shanghai bourse CLOSED DOWN 8.08 POINTS OR 0.26% / HANG SANG CLOSED DOWN 177.54 OR 0.77%

2 Nikkei closed UP 109.99 OR 0.63% /USA: YEN RISES TO 105.34

3. Europe stocks opened ALL MIXED ( /USA dollar index DOWN to 98.84/Euro UP to 1.0917

3b Japan 10 year bond yield: RISES TO -.042%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 104.00/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 49.34 and Brent:50.15

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES A BIT to +.170%

3j Greek 10 year bond yield RISES to : 8.39%

3k Gold at $1266.50/silver $17.64(7:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble DOWN 22/100 in roubles/dollar) 62.95-

3m oil into the 49 dollar handle for WTI and 50 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a REVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.34 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9942 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0855 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.170%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.856% early this morning. Thirty year rate at 2.610% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Drop On Poor Earnings, Bond “Bloodbath” Ahead Of US Q3 GDP

S&P futures and Asian stocks were little changed while European shares fell as the global bonds sell-off deepened on speculation major central banks are moving closer to reining in stimulus, while stocks retreated after disappointing results from companies including Amazon.com and AB InBev. The dollar hit a three-month high against the yen as investors grew more confident that the Federal Reserve will raise U.S. interest rates by the end of the year.

Benchmark 10-year U.S. and euro zone yields rose to their highest since May and 10-year British yields were firmly on track for their biggest monthly rise since January 2009, the second biggest in over 20 years. “Bond markets are facing a recurring nightmare at the moment as we continue to see yields rise sharply,” said DB’s Jim Reid. Key overnight data included Japanese CPI, which printed -0.5% as expected; the first print of US Q3 GDP will be revealed at 8:30am ET.

Among the stories, UBS reported a drop in wealth earnings as CEO focuses on cost cuts, Amazon missed on EPS and forecast holiday sales that were below analysts’ estimates sending it shares sharply lower, while AB InBev – one of Europe’s biggest companies – plunged on a profit miss; Novo Nordisk, the world’s biggest maker of insulin, cut its long-term growth target; the WSJ reported that GE was discussing an acquisition of Baker Hughes although the company later denied the rumors saying partnership negotiations don’t include an “outright purchase.”

“The guidance has been a bit disappointing,” said Daniel Murray, head of research at EFG Asset Management in London. “Sentiment has been damaged by the fact that we are in the U.S. election period and the fact that expectations with respect to the ECB are coalescing around the fact that it’s going to be less expansive than it has been this year.”

As a result, a rally in global equities is pulling back in October and bonds worldwide are on course for their worst month since the taper tantrum of 2013 as global central bank tapering fears return while the Fed moves closer to raising interest rates as the economy improves. Quoted by Bloomberg, James Woods, a strategist at Rivkin Securities in Sydney said “there are so many risk events coming up, people just sort of want to get those out of the way before they commit. There’s quite a bit of cash sitting on the sidelines, waiting to be deployed.” He did not explain where the cash those who sell to the “buyers on the sidelines” will end up; one assumes on the sidelines too…

Looking at today’s main event, the advance Q3 GDP release in the US this afternoon, the range of expectations for the data is huge. Indeed the consensus (Bloomberg) is currently sitting at 2.6% for the annualized QoQ print while the range among economists spans 1.3% to 3.6%. DB’s Joe Lavorgna is at the low end of that range with his forecast. A couple of factors lead to that conclusion. Firstly, Joe highlights that inflation-adjusted retail control is pointing towards sub-1% annualized growth of overall real personal consumption expenditures in Q3. This expected slowdown would follow a relatively large 4.3% increase in the previous quarter. The biggest risk in his view however remains inventories. The level of stockpiles is still elevated relative to the pace of sales throughout most of this year and Joe expects another drawdown in inventories for Q3. It’s worth noting that the two GDP tracker models from the Atlanta Fed and NY Fed are at 2.1% and 2.2% respectively.

Back to markets, Asian stocks headed for a weekly drop as Chinese shares retreated and investors weighed mixed earnings reports before central bank meetings and the U.S. election. Japanese equities rallied after the yen fell. European stocks fell for a fifth day as companies reported disappointing results while a bond rout abated and metals rallied.

The Stoxx Europe 600 Index headed for its longest losing streak in six weeks after Anheuser-Busch InBev NV posted a surprise drop in profit and Novo Nordisk A/S, the world’s biggest maker of insulin, cut its long-term growth target. 71% of Stoxx 600 members decline, 27% gain. The index fell 0.5%, taking its weekly loss to 1.2 percent – the biggest slump since mid-September. While most industry groups retreated in the past five days, banks climbed and lost their spot as the year’s biggest losers, thanks to better-than-forecast reports at Spanish firms such as Banco Santander SA and Banco Bilbao Vizcaya Argentaria SA.

The S&P 500 fell for the past three days, its longest losing streak since early September. Futures on the S&P 500 Index were little changed, with the gauge heading for its third weekly decline in four. Contracts on the Nasdaq 100 Index dropped less than 0.1 percent on Friday.

Among companies moving on earnings, courtesy of Bloomberg:

- AB InBev lost 4.6 percent after cutting its revenue projection.

- Total SA fell 1.7 percent after posting an earnings decline.

- Novo Nordisk sank 14 percent after slashing its long-term target for earnings growth by half.

- Software company Gemalto NV tumbled 12 percent as its revenue missed estimates.

- Amazon.com Inc. lost 5.4 percent in early New York trading after forecasting holiday sales that may miss projections.

- Alphabet Inc. added 1.1 percent after reporting revenue and profit that topped projections.

- Sanofi rallied 7 percent after the drugmaker raised its profit forecast.

- British Airways owner IAG SA, which reported a decline in quarterly earnings amid a weaker pound, climbed 3.4 percent as its annual profit forecast was in line with analysts’ estimates.

A gauge of dollar strength was near a seven-month high before the U.S. reports gross domestic product. Aluminum rose to a 15-month high after a rally in iron ore prices in China.

German 10-year Bunds were little changed, with yields near the highest in almost six months. The annual consumer-price inflation rate in four German regions, including Saxony and Brandenburg, rose in October, according to reports released before data for the nation is made available later Friday. “The premise of the selloff so far was higher inflation and uncertainty on what the ECB is going to do next and particularly about how the next leg of quantitative easing would look,” said Peter Chatwell, head of rates strategy at Mizuho International Plc in London. “These conditions remain in place, so it’s difficult to envisage markets finding strong support until there is much stronger conviction as to the ECB.” German 10-year bund yields were at 0.16 on Friday, after reaching 0.22 percent, the highest since May 5. The yield has climbed 28 basis points this month.

The yield on 10-year U.S. Treasuries was little changed at 1.85 percent, leaving it up 25 basis points this month.

Fixed-income assets are retreating as fund managers boost cash holdings before the presidential vote Nov. 8 and as monetary policies show signs of turning less accommodative in the U.S., Europe and Japan. The Bank of Japan shifted to targeting bond levels from its goal to push yields lower, while ECB officials have said the authority will probably gradually wind down its bond purchases.

Bonds have lost 2.9 percent in October, according to the Bloomberg Barclays Global Aggregate Index.

Exxon Mobil Corp., Chevron Corp. and Mastercard Inc. are among companies reporting on Friday. U.S. GDP growth quickened in the third quarter, economists in a Bloomberg survey said before a report on Friday.

* * *

Market Snapshot

- S&P 500 futures down less than 0.1% to 2122

- Stoxx 600 down 0.6% to 340

- FTSE 100 down 0.5% to 6954

- DAX down 0.6% to 10654

- German 10Yr yield down less than 1bp to 0.17%

- Italian 10Yr yield up 3bps to 1.56%

- Spanish 10Yr yield up 3bps to 1.22%

- S&P GSCI Index down 0.1% to 373.2

- MSCI Asia Pacific up less than 0.1% to 139

- Nikkei 225 up 0.6% to 17446

- Hang Seng down 0.8% to 22955

- Shanghai Composite down 0.3% to 3104

- S&P/ASX 200 down 0.2% to 5284

- US 10-yr yield up less than 1bp to 1.86%

- Dollar Index down 0.08% to 98.81

- WTI Crude futures down 0.2% to $49.60

- Brent Futures down less than 0.1% to $50.44

- Gold spot down less than 0.1% to $1,268

- Silver spot down 0.1% to $17.61

Global Headline News

- German bonds headed for their worst month since 2013 as a global selloff deepened

- UBS Reports Drop in Wealth Earnings as CEO Focuses on Cost Cuts: Wealth management profit declines 21% in third quarter

- Amazon Forecasts Holiday Sales That May Miss Analysts’ Estimates: Shares declined as much as 9 percent in extended trading

- AB InBev Needing Megabrew Tonic as Shares Plunge on Profit Miss: Budweiser maker cuts full-year revenue forecast on slowdown

- GE Discussing Baker Hughes Partnership as Oil Slump Endures: Negotiations don’t include an ‘outright purchase,’ GE says

- Chipotle said to hire Goldman, Wachtell to help defend against activist investor Bill Ackman, Reuters reports

- Marvell is close to hiring Goldman as an adviser after the company replaced its CEO and rejected a series of Chinese bids

- Samsung Biologics priced its $2b initial public offering at the high end of a marketed range

- U.S. said to probe Tullett, BGC, TFS-ICAP over currency options

- Companies in Europe cutting their record amounts of cash they possess, buying short-term securities instead of expanding

- Bond investors are worried that things are about to get worse for Brazilian banks already battered by delinquencies

- Brookfield agreed to buy a 70% stake in Brazilian water and sewage company Odebrecht Ambiental for as much as $1b

- Apple Increases Prices of Macs in U.K. by 20 Percent: Amount charged in the U.S. hasn’t changed over the same period

- In European primary, higher-yielding borrowers are dominating a busy end to the third-busiest week of the year, with at least EU2.5b expected to price across 7 deals

* * *

Looking at regional markets, we start in Asia where stocks headed for a weekly drop as Chinese shares retreated and investors weighed mixed earnings reports before central bank meetings and the U.S. election. Japanese equities rallied after the yen fell. Relief for the BoJ ahead of their meeting next week with the latest inflation figures not deteriorating further, while the Tokyo CPI (often regarded as a leading indicator for the national reading) which would have taken into account the BoJ’s new yield curve policy, printed firmer than expected. However, as is typically the case, a muted reaction was observed in the JPY, which had been notably weaker following the USD strength throughout EU and US hours. As such, the Nikkei 225 (+0.5%) outperformed to hover around 6-month highs with exporters benefitting from the

weaker currency, coupled with financials gaining from the pick-up in yields. Elsewhere, the ASX 200 (-0.3%) was dragged lower by AMP shares after the company booked a AUD 668m1n impairment charge for their wealth protection unit, while Chinese markets were indecisive with Shanghai Comp (unch) initially underpinned from a larger net weekly liquidity injection and encouraging earnings, before gains were then pared alongside weakness in the Hang Seng (-0.3%) on a disappointing trading debut for China Resources Pharmaceuticals which was one of HK’s largest IPOs this year. In credit markets, JGB yields were higher across the curve taking the impetus from the rally in yields from its global counterparts throughout yesterday’s session. Yields also continued to climb higher post Japanese CPI release, although outperformance had been observed in the belly of the curve after the BoJ offered to purchase 5-10yrs. PBoC injected CNY 95b1n 7-day reverse repos, CNY 65b1n in 14-day reverse repos, CNY 35b1n in 28-day reverse repos for a weekly net injection of CNY 595b1n vs. Prey CNY 95.5bIn injection.

Asia Top News

- Japan Consumer Prices Keep Falling, Household Spending Slips: Downbeat inflation and spending data came despite an increasingly tight labor market

- Hong Kong Regulator Said to Call in Brokerages to Settle Probes: SFC plans public consultation on manager responsibility regime

- Singapore’s Mall Vacancies Jump to Highest Level in a Decade: Office vacancies also climb in quarter to a four- year high

- Daiwa Profit Climbs 25% on Trading Income; Announces Buyback: 2Q net income 30.4b yen vs 24.4b yen year ago

- UOB Net Income Beats Estimate as Credit-Card, Fund Income Rises: 3Q net S$791m vs est. $771m

- Macquarie Group Profit Beats Estimates on Asset Sales: Full- year profit to be in line with last year’s record result

- Tata Said to Tap Sovereign Funds on Buying Out Ousted Chairman: Indian industrialist prepares for possible Mistry family sale

European equities opened in the red this morning as one of Europe’s biggest companies AB InBev (ABI BB) fell as much as 5.5%. This general negative sentiment led the DAX future to break Wednesdays low of around 10625 and remains lower by around 1 %. In terms of other large caps, RBS (RBS LN) posted a loss but with a higher than Prey. CETI ratio; the Co. opened +4.9% before retracing these gains in line with the downside across the rest of the market. In Germany, Linde (LIN GY) are currently up +2.7% off the back of a stellar earnings report and are the out performer in the DAX.

Top European News

- RBS Shares Rise as Trading Unit Boosts Third-Quarter Revenue: RBS says it won’t meet deadline for shedding Williams & Glyn

- Sanofi Overcomes Diabetes Crunch, Surges After Boosting Forecast: Drugmaker to divest EU generics business within 12-24 months

- BNP Profit Rises, Beating Estimates, Buoyed by Debt Trading: French firm joins other banks benefiting from debt operations

- Spain’s Economic Growth Slows as Rajoy Gets Closer to Power: Rajoy may take office this week as Socialists drop veto

- Facebook Told to Stop Exploiting WhatsApp Data During EU Probe: EU privacy chiefs say use isn’t in line with terms of service

- Eni Posts Wider-Than-Expected Loss as Low Oil Prices Bite: Oil major cites declining profitability in refining, chemicals

- Novo Plunges After Slashing Long-Term Growth Profit Target: Cut its long-term target for profit growth by half due to pressure on prices in the U.S., its largest market

In FX, the Bloomberg Dollar Spot Index was little changed, heading for a 2.5 percent gain this move, the most since May. The probability of a Fed rate hike this year climbed 5 percentage points this week to 73 percent in the futures market. Sweden’s krona rebounded from the lowest level since 2010 against the euro on Thursday, having slumped after the central bank signaled it’s prepared to extend bond purchases into next year. The yuan held near a six-year low amid speculation that China’s policy makers are becoming more tolerant of declines as exports slump and the dollar advances. It’s dropped 1.5 percent in October, set for its biggest monthly loss since an August 2015 devaluation. Bitcoin surged 8.4 percent this week to about $684, the biggest increase since June, as yuan declines spurred demand for the cryptocurrency. China accounts for about 90 percent of trading in bitcoins as the digital tender offers its citizens a means to hedge against yuan depreciation amid capital controls.

In commodities, oil was set for the first weekly drop since September as an OPEC committee meets in Vienna on Friday to discuss output quotas for members participating in an agreement to cut production. Saudi Arabia and its Gulf allies are willing to cut 4 percent from their peak production, Reuters reported, citing people familiar with the matter. Iron ore is rallying as coal prices surge, with futures in China heading for the longest run of daily gains since 2013 and contracts in Singapore poised for a third weekly climb. The stronger prices helped to lift shares of producers in Australia, the world’s largest shipper. Aluminum climbed as much as 0.6 percent in London and has gained more than 10 percent since last Friday’s close in Shanghai, its biggest weekly advance. Zinc reached a fresh five-year high and iron ore climbed a seventh day.

Looking at the day ahead, the focus will be on that Q3 GDP report while the final October University of Michigan consumer sentiment reading will also be released. Away from the data, the ECB’s Coeure is scheduled to speak this morning followed by Governing Council member Lane shortly after. Earnings wise today we’ve got just 16 S&P 500 companies due today with the highlights being Exxon Mobil and Chevron. UBS reports in Europe.

US Event Calendar

- 8:30am: Employment Cost Index, 3Q, est. 0.6% (prior 0.6%)

- 8:30am: GDP Annualized q/q, 3Q A, est. 2.6% (prior 1.4%)

- 10:00am: U. of Mich. Sentiment, Oct. F, est. 88.2 (prior 87.9)

- 1pm: Baker Hughes rig count

DB’s Jim Reid concludes the overnight wrap

The problems with writing the EMR so early in the morning is that invariably I start writing within seconds of my alarm waking me up out of a deep sleep and often from a strange dream that stays firmly in my mind while I’m writing about crucial multi trillion dollar financial markets. This morning I’m particularly impacted as I just woke from a dream where BBC local radio randomly asked me to commentate on the football World Cup final between Republic of Ireland and Croatia. I wasn’t very good but fortunately my alarm woke me up after the final whistle so at least I know the result. The Irish won 6-4 with man of the match being ex-England and Liverpool player John Barnes who as I informed the listeners had just completed a 15 year residency qualification to play for Ireland at the age of 52. If there’s anyone that can interpret this dream then I’d be very pleased to hear from you. I did have cheesecake late at night at a work dinner in Oslo where I’m writing this from. So maybe that’s it.

Bond markets are facing a recurring nightmare of their own at the moment as we continue to see yields rise sharply. Yesterday’s move seemed to be sparked by the move for Gilts after UK Q3 GDP surprised to the upside (+0.5% qoq vs. +0.3% expected) despite the details suggesting a continuation of an increasingly unbalanced growth profile with services accelerating but production and construction struggling. In any case 10y Gilt yields surged a little over +10bps to close at 1.251% and in the process have narrowed the gap to the pre-Brexit level on June 23rd to just 12bps. That gap has been as big as 86bps.

Other European bond markets followed suit. 10y Bund yields were up +8.5bps to 0.168% and the highest yield since May while yields in the periphery were 7-8bps higher too. In fact, 5y Bund yields finished up 4bps at -0.397% and so taking the yield above the ECB’s -0.40% floor in the depo rate for the first time since June and therefore making them eligible for QE purchases again. Meanwhile Treasuries weren’t exempt from the moves. The benchmark 10y yield ended +6bps higher at 1.855% and so finally snapped out of the 1.70-1.80% range that they’d been stuck in for much of the month. That move actually came despite a relatively unimpressive durable and capital goods orders report. More on that later. This morning in Asia most major bond markets have followed the lead. Yields in the antipodeans in particular are up +5bps and generally at the highest levels since May.

Interestingly the bond selloff comes despite Fed rate hike expectations remaining relatively stable. The December probability of 73% was actually unchanged yesterday and means that since the end of last week the probability has only increased 5%. The various headlines and noise around ECB tapering hasn’t really shifted market re-pricing either. Where we are seeing significant shifts however are in inflation expectations. 10y US inflation breakevens are up over 30bps from the lows in June. It’s a similar story in Europe where Eurozone breakeven rates have marched higher this month and are now over 20bps up from the July lows. Stability in commodity markets is certainly helping. Despite all the back and forth of OPEC production cut speculation, Oil has still only traded $2/bbl either side of the $50/bbl mark this month while base metals have also been fairly stable.

It might be another active day in bond markets given the important advance Q3 GDP release in the US this afternoon where the range of expectations for the data is huge. Indeed the consensus (Bloomberg) is currently sitting at 2.6% for the annualized QoQ print while the range among economists spans 1.3% to 3.6%. DB’s Joe Lavorgna is at the low end of that range with his forecast. A couple of factors lead to that conclusion. Firstly, Joe highlights that inflation-adjusted retail control is pointing towards sub-1% annualized growth of overall real personal consumption expenditures in Q3. This expected slowdown would follow a relatively large 4.3% increase in the previous quarter. The biggest risk in his view however remains inventories. The level of stockpiles is still elevated relative to the pace of sales throughout most of this year and Joe expects another drawdown in inventories for Q3. It’s worth noting that the two GDP tracker models from the Atlanta Fed and NY Fed are at 2.1% and 2.2% respectively.

Another potentially important event today is the decision from Northern Ireland’s High Court on the UK’s Brexit process where claimants are arguing that triggering Article 50 without the consent of the devolved authorities is unlawful. It had been thought that the Northern Ireland decision would come after the decision from the parallel review at the London High Court, so there will probably be a lot of eyes on this outcome ahead of a possible decision in London next week.

Switching to the latest in Asia where it’s a bit of a mixed end to the week for markets. Yesterday’s weaker session for the Yen (-0.78%) is helping the Nikkei (+0.53%) to climb while the Shanghai Comp (+0.27%) is also a touch higher. The Hang Seng is little changed while the Kospi (-0.15%) and ASX (-0.36%) have edged lower. Earnings in the region are dictating much of the moves this morning across bourses however. Elsewhere US equity index futures are up following better than expected quarterly earnings from Alphabet after the close which sent shares up 4% in extended trading. Amazon did however disappoint after the close.

There’s also been some important data released in Japan this morning. In terms of consumer prices, headline CPI has remained unchanged in September at -0.5% yoy as expected, while the core was also unchanged at -0.5% yoy and in line with the market. The core-core reading (0.0% yoy vs. +0.1% expected) was softer than expected however after declining two-tenths from August. Meanwhile household spending (-2.1% yoy vs. -2.7% expected) wasn’t as weak as expected and the jobless rate was reported as declining one-tenth to +3.0% (vs. +3.1% expected). That matches the joint lowest reading in 21 years. It’s worth noting that the BoJ meet next week with some suggestion that they may look to revise their inflation outlook.

The moves this morning come after the S&P 500 finished -0.30% last night and in doing so closed lower for the third time in a row for the first time since early September. REITS felt it again given the moves in rates with the sector alone down -2.45%. Telecoms had a better day as did financials. Earnings also played their part with better than expected results for Dow Chemical and Bristol-Myers Squibb offset by declines for UPS and Simon Property following their latest quartiles. In Europe the Stoxx 600 (-0.01%) finished virtually unchanged following a choppy day. Amazingly in the last 5 sessions the index has closed either flat or -0.01% on 3 of them. Directionless. Much like the US however, European Banks (+1.18%) had another good day and have now finished higher in 7 out of the last 8 sessions. The Stoxx 600 Banks index is now at the highest since May 30th. Interestingly, the last time we were there US 10y yields were 1.851%. So the positive correlation between the sector and yields continues.

In terms of the US durable and capital goods orders data yesterday that we highlighted at the top, headline durable goods orders declined slightly in September (-0.1% mom vs. 0.0% expected) although ex-transportation did rise +0.2% mom as expected. The weakness was in core capex orders however which tumbled -1.2% mom last month (vs. -0.1% expected). Core shipments (+0.3% mom) met expectations. In fairness the core capex order decline was offset by the upwardly revised +1.2% mom print for August. Elsewhere, initial jobless claims declined 3k last week to 258k. Pending home sales (+1.5% mom vs. +1.0% expected) rose a little bit more than expected in September while there was no change in the Kansas City Fed’s manufacturing survey index at +6.

There wasn’t really any other data to highlight in Europe aside from the UK GDP print although we did get the latest BoE CBSP holdings data. Total purchases now stand at £1.994bn as of October 26th. This implies net purchases settled in the latest weekly period of £435m which works out at an average of £145m per auction in that week. That is a touch below the £166m since the program started. While it is a little below the run rate it’s still an overall strong start to the programme for the BoE.

Elsewhere yesterday, the ECB’s Nowotny highlighted what most in the market already think in that the ECB will make a decision on whether or not to extend QE in December. He also said that the ECB will examine ‘looking at volumes and then deciding on assets’. The ECB’s Mersch also said that the ECB should ‘largely achieve’ its inflation goal in 2019.

Wrapping up markets yesterday. It was a fairly volatile day for currencies although the standout was the tumble for the Swedish Krona (-1.92%) which plunged to the weakest level since 2010. That came after the Riksbank kept its benchmark repo rate at -0.5% yesterday but dovishly signalled that it’s prepared to extend bond purchases into 2017 and also keep rates negative for longer. The Swedish Krona has now fallen over 7% this year so far with only Sterling weakening more in the G10.

Looking at the day ahead now, this morning and shortly after this goes to print we’ll be kicking off with Q3 GDP data in France before we then get the PPI and CPI reports shortly after for the economy. Germany will also release its October inflation data today while Euro area confidence indicators are also due out this morning. Across the pond this afternoon, as noted earlier the focus will be on that Q3 GDP report while the final October University of Michigan consumer sentiment reading will also be released. Away from the data, the ECB’s Coeure is scheduled to speak this morning followed by Governing Council member Lane shortly after. Earnings wise today we’ve got just 16 S&P 500 companies due today with the highlights being Exxon Mobil and Chevron. UBS reports in Europe.

Before we wrap up there’s a few potentially interesting things to highlight this weekend. Spain’s Parliament is due to hold a second investiture vote in which Mariano Rajoy is expected to be confirmed for a second term. He should also announce his cabinet over the coming days. In Italy PM Renzi is scheduled to address a rally of his Democratic Party as part of his December 4th referendum campaign. Finally Iceland is due to hold a snap election this weekend. The latest polls have suggested that it will be a close call with the Guardian newspaper suggesting that the activist Pirate Party looks on course to either win or finish a close second. Results should be out on Sunday morning.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 8.08 POINTS OR 0.26%/ /Hang Sang closed DOWN 177.54 OR 0.77%. The Nikkei closed UP 109.99 POINTS OR 0.63% Australia’s all ordinaires CLOSED DOWN 0.14% /Chinese yuan (ONSHORE) closed UP at 6.7802/Oil FELL to 49.34 dollars per barrel for WTI and 50.15 for Brent. Stocks in Europe: ALL IN THE MIXED Offshore yuan trades 6.7937 yuan to the dollar vs 6.7802 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS A BIT AS MORE USA DOLLARS LEAVE CHINA’S SHORES / CHINA SENDS A MESSAGE TO THE USA TO NOT RAISE RATES IN DECEMBER.

3a)THAILAND/SOUTH KOREA/SOUTHEAST ASIA:

none today

b) REPORT ON JAPAN

none today

c) Report on CHINA

4 EUROPEAN AFFAIRS

The pound tumbles after a Northern Irish judge rejected a pair of challenges to the PREXIT process. This removes at least one obstacle to Prime Minister May’s plan as it begins to sever ties with the European Union by the end of March 2017:

(courtesy zero hedge)

Pound Tumbles After UK Government Wins Brexit Suit In Northern Ireland Court

Moments ago sterling did what it has been doing so well these past few months, it tumbled by as much as 50 pips after the UK government won a Brexit suit in a Northern Ireland court: a Northern Irish judge rejected a pair of challenges to the Brexit process, removing at least one obstacle to Prime Minister Theresa May’s plan to begin severing ties with the European Union by the end of March.

The Northern Irish High Court ruled that lawmakers don’t need to hold a vote to start the two-year countdown to Brexit. The judge also rejected a challenge based on Good Friday Peace Agreement.

But the court also said that it would defer to English courts on the wider issue of whether Prime Minister Theresa May and her ministers have the authority to invoke Article 50 of the EU Lisbon Treaty, the mechanism by which a nation can leave the bloc, without the explicit backing of the British parliament.

Reuters adds that Northern Ireland rights activist McCord will appeal the high court ruling to the UK Supreme Court, however according to ING analyst Petr Krpata, the decision reduced the probability that article 50 won’t get triggered, Bloomberg reported.

In the immediate aftermath, GBP/USD dropped 0.32% to day low of 1.2125 while EUR climbs to 0.89941 against the pound in sharp moves. GBP/USD next support at 1.2118; EUR/GBP resistance at 0.9027. Cable now trading -0.21% at 1.2140; EUR/GBP +0.33% at 0.89874.

END

The crashing pound causes Apple and other companies to raise their electronic prices:

(courtesy zero hedge)

Brexit Blowback Begins: UK Home Electronics Prices Spike As Currency Crashes

The Brexit blowback on British consumers tightened today as Apple and Electrolux responded to the collapsing pound by charging dramatically more for their products in the UK. As Bloomberg reports, Apple quietly raised the cost of some of its machines including the “Mac Pro” by 20% overnight, while Sweden’s Electrolux said it’s boosting the prices of its home appliances by 10%.

With inflation already accelerating at the fastest in two years, Bloomberg notes that price pressures are likely to mount as the weakest pound in three decades forces up the cost of imports just weeks before Christmas.

The price hikes came days after “Marmitegate” saw supermarket Tesco Plc battle with supplier Unilever over the cost of goods and Microsoft Corp. began charging Britons more for some of its software.

“We will see more price increases, possibly more at the higher end of the market, and we’ll see a significant squeeze on real incomes and then we’ll see how it plays out,” said Kit Juckes, a London-based strategist at Societe Generale SA.

Apple began charging 2,999 pounds ($3,650) for its “Mac Pro” desktop machine, up from 2,499 pounds earlier in the week. The “Mac Mini” now retails at 479 pounds compared to 399 pounds.The U.S. prices for the Mac Mini and Mac Pro haven’t been changed.

“Apple suggests product prices internationally on the basis of several factors, including currency exchange rates, local import laws, business practices, taxes, and the cost of doing business,” an Apple spokesman said in a statement. “These factors vary from region to region and over time, such that international prices are not always comparable to U.S. suggested retail prices.”

Electrolux CEO Jonas Samuelson says main effect of Brexit is that GBP has devalued sharply against EUR, adding that “we need to compensate by raising prices,” in the U.K. Samuelson raised prices in U.K. by up to 10% and notes “we’ve seen clear cautiousness from retail and construction, which has put slight pressure on demand, but we haven’t seen any larger effects on consumer demand”

One government official this week told British consumers to brace for higher prices.

“We have had Marmageddon,” Mark Garnier, the U.K.’s trade minister, said in an interview.

“Consumers are going to start to see rising prices and there’s nothing we can do about that. That was a well-predicted effect of Brexit. The point was very clearly made by everybody: Brexit could easily result in a slump in the value of sterling. That has transpired.”

With the pound continuing to collapse this morning following the Brexit suit outcome, and Goldman’s estimates of considerably more pain to come, inflationary pressures may just be too much for Carney to overlook as transitory this time.

end

London real estate is crashing

(courtesy zero hedge)

London Real Estate Prices Are Crashing

And the easiest way to confirm it, is to look at recent (and not so recent) home listings in Kensington and Chelsea, where we find something stunning: out of 130 pages of adverts, with 15 ads per page, nearly half of all properties, or 53 of the pages show price reductions.

… through Page 53

And it will only get much worse: there are 23 pages worth of property that has been on the market for more than a year.

The liquidation sales are coming.

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Sooner or later an accident is going to happen: Russia and USA jets in a “near miss” situation over Syria:

(courtesy zero hedge)

Russian, US Jets In “Near Miss” Over Syria

The potentially bellicose close encounters above Syria are starting to get awfully close for comfort.

Moments ago AFP reported, from the deck of an aircraft carrier, that a Russian fighter flew dangerously close to a US warplane over eastern Syria, US defense officials said Friday, highlighting the risks of a serious mishap in the increasingly crowded airspace.

#BREAKING Russian, US jets had near miss over Syria: US officials

The near miss occurred late on October 17, when a Russian jet that was escorting a larger spy plane manoeuvred in the vicinity of an American warplane, Air Force Lieutenant General Jeff Harrigan said. The Russian jet came to “inside of half a mile”, he added. Another US military official, speaking on condition of anonymity , said the American pilot could feel the turbulence produced by the Russian jet’s engines.

“It was close enough you could feel the jet wash of the plane passing by,” the official said.

The incident appears did not take place out to malice, as the Russian pilot had simply not seen the US jet, as it was dark and the planes were flying without lights according to AGP. This incident was deemed unsafe, but not necessarily unprofessional, officials said. “I would attribute it to not having the necessary situational awareness given all those platforms operating together,” Harrigan said.

The incident raises serious questions about the extent to which pilots are able to track the complex airspace they operate in.

The US-led coalition has set up a hotline with Russian counterparts so the different militaries can discuss the approximate locations and missions of planes, and avoid operating in the same space at the same time. In this case, the American pilot tried unsuccessfully to reach the Russian jet via an emergency radio channel.

The next day, US officers used the hotline to ask Russia what had happened and they said “the pilot didn’t see” the American plane, the official said.

Harrigan said there had been an increase in close calls over the past six weeks, with intentional near misses — when a Russian jet deliberately follows a coalition plane too closely — “happening one every 10 days-ish”. Russia is flying constant air patrols over Syria, the vast majority of them over the devastated city of Aleppo, and routinely transits parts of the country the US-coalition operates in, officials said.

The Pentagon has periodically chided Russia for “unsafe and unprofessional behaviour” in air operations, with many Russian “fly-bys” having made the news in recent months, many of which Russia claims are in retaliation for close approaches by NATO jets to its own borders.

6. GLOBAL ISSUES

7. OIL ISSUES

The oil producers have engaged in heavy hedging. If the oil price drops, they will survive but not necessarily the likes of Saudi Arabia and other producing nations:

(courtesy zerohedge)

Let Crude Crash: US Oil Producers Are Hedging At Levels Not Seen Since 2007

As warned here one month ago after the farcical OPEC meeting in Algiers, the cartel’s latest jawboning ploy to keep prices artificially higher – if only for one more month – is fast falling apart. Just a few hours ago, Bloomberg reporter Daniel Kruger penned the following assessment of the situation:

Production-Cut Talk Is as Good as It Gets for Oil. Some OPEC members are talking about cutting production again, and so prices are rising. Saudi Arabia and other producers both in and out of the cartel have done a good job fostering the storyline that there are terms under which parties can agree to pump less crude. Continuing signs of concord among producer nations have boosted oil prices to an average of $50 a barrel this month in New York. Yet several obstacles make it difficult for countries to commit to signing on to a deal. One obstacle is that sacrifices are needed for the agreements to succeed. Another is that those sacrifices aren’t shared equally.

Having successfully raised $18 billion in the bond market, Saudi Arabia is better positioned to withstand the loss of some revenue. Iraq, OPEC’s second-biggest producer, was the latest to plead for an exemption from a cut, citing its fight against Islamic State as a cause of hardship. Ultimately, no one wants to pump less because the upside is so limited. Saudi Arabia’s 2014 decision to double down on production in a drive for market share succeeded in making it more difficult for higher-cost producers to thrive as they once had. But having committed to that goal, they also locked themselves into a fight to keep what they’d won.

And while ConocoPhillips’ announcement this week that it plans to cut spending on major projects demonstrates the partial success of the Saudi plan to drive out rivals, it also shows producers see diminishing chances for crude to climb much above $60, said Wells Fargo Fund Management’s James Kochan. The big reason, of course, is latent U.S. supply. Baker Hughes data shows the most rigs at work in the Permian Basin since January. Sanford C. Bernstein analyst Bob Brackett suggests the per-acre price of drilling lease land will rise to $100,000 from about $60,000 now.

The one agreement players seem to have reached is that oil isn’t able to go much higher.

That oil’s upside is capped at this point is clear; in fact as both Goldman and Citi have warned, unless OPEC can come to a definitive and auditable agreement – no just another verbal can kicking – in which the member states, by which we mean almost entirely Saudi Arabia as most of the marginal producers are exempt or want to be, immediately curtail production, oil will promptly crash to $40 or below.

But an even more amusing twist is that a plunge in oil prices may be just what US shale producers are waiting for. The reason for that is that while OPEC has been busy desperately jawboning oil higher, US producers have been thinking of the inevitable next step, oil’s upcoming reacquaintance with gravity. As a result, as the EIA reports, the amount of WTI short positions held be producers and merchants is just shy of a decade high.

According to a recent EIA report, short positions in West Texas Intermediate (WTI) crude oil futures contracts held by producers or merchants totaled more than 540,000 contracts as of October 11, 2016, the most since 2007, according to data from the U.S. Commodity Futures Trading Commission (CFTC). Banks have tightened lending standards for some energy companies as crude oil prices declined throughout 2014 and 2015, and some banks require producers to hedge against future price risk as a condition for lending.

Short positions of WTI futures increased at a faster pace than futures contracts of Brent (an international crude oil benchmark) since summer 2016, suggesting U.S. producers are able to drill for oil profitably in the $50 per barrel range. In the Crude Oil Markets Review section of the October Short-Term Energy Outlook (STEO), the U.S. Energy Information Administration (EIA) discusses an increase in U.S. onshore producers’ capital expenditures that is contributing to rising drilling activity, which EIA projects will lead to an increase in U.S. onshore production by the second quarter of 2017.

* * *

Which closes the circle of irony: almost exactly two years ago, Saudi Arabia set off a sequence of events with which it hoped to crush US shale producers and its high cost OPEC competitors. It succeeded partially and briefly, however now the remaining US shale companies are more efficient, restructured, have less debt, a far lower all-in cost of production; and – best of all – they will all make a killing the next time oil plunges, as it will once OPEC’s hollow gambit is exposed.

Meanwhile, the last shred of OPEC credibility will be crushed, the truly high cost oil exporters within OPEC will suffer sovereign defaults and social unrest, as will Saudi Arabia. The good news for Riyadh is that at least it got a $17.5 billion in fresh cash from a bunch of idiots who will never get repaid. We are curious just how long that cash will last the country which burned through $98 billion just last year, before the threat of social unrest and financial system collapse returns? Two months? Three?

WTI Tumbles To $48 Handle After Iraq, Iran Refuse To Freeze Output; OPEC Admits “It’s Getting Complicated”

“It is getting complicated…every day there is a new issue coming up,” one OPEC delegate said this morning as it is clearly becoming harder to keep the smoke and mirrors jawboning of a possible cut/freeze alive in the face of a reality that is very clearly enunciated by Russia’s energy minister, “any output freeze could be offset by a quick recovery in US shale oil output.” In other words, why bother with a freeze at all.. which is exactly what Iran and Iraq just said…

- IRAQ AND IRAN REFUSE TO FREEZE OUTPUT – SOURCES

- *IRAQ, IRAN SAY OPEC UNDERESTIMATES THEIR PRODUCTION: DJ

- *OPEC MTG SAID DEADLOCKED AS IRAQ, IRAN DISPUTE DATA: DJ

The reaction is clear, disappointment.

Pushing WTI to near one-month lows.

And now that the machines have run $50 stops twice in 2 days, we suspect there is little ammo left to keep the dream alive.

end

8. EMERGING MARKETS

The extremely clever Horseman Capital calls it quits on an emerging fund. These guys are 100% short and now they cannot make money

(courtesy zero hedge)

“World’s Most Bearish Hedge Fund” Shuts Emerging Markets Unit After 17% Loss

We had previously dubbed Horseman Capital the world’s most bearish hedge fund for one reason: as recently as a few months ago the firm’s Global Fund had taken its net equity short position to an unprecedented -100%. Horseman is now in the news once again as it is liquidating an emerging markets focused hedge fund following losses totaling 17% this year and difficulties raising capital, according to a letter sent to investors.

“In light of fund returns and lack of investor interest, the directors of the fund have sadly decided to close the Horseman Emerging Market Fund Ltd.,” according to the letter seen by Bloomberg News. A spokesman for the London-based firm confirmed the contents of the letter.

“The resulting performance squeeze since February has made holding short positions a near impossibility for many funds and is typical of a true bear market,” Burke said in the letter.

“Returns are customarily destroyed in both long and short funds as the market cycle plays out.”

As Bloomberg reports, the fund, which managed $28 million and is led by John-Paul Burke, lagged a 13.8 percent advance in the MSCI Emerging Markets Index through September this year.

Horseman Capital manages $2.4 billion across a number of hedge funds and the firm is joining a growing number of money managers closing down funds in Europe where poor returns, the mounting cost of regulatory compliance and investors’ reluctance to allocate capital has led to more funds shutting than starting since 2015.

About 557 hedge funds have closed in the region since the start of 2015 through September this year, while only 476 have started, according to Eurekahedge data. Investors redeemed about $5.5 billion from hedge funds focused on Europe in the third quarter of the year, the most since they pulled $9.3 billion in the third quarter of 2012, according to a report from data provider eVestment.

However, as CIO Russell Clark noted,

My other observations about fund management has been that investors are pulling out of active strategies and buying passive strategies. There are good reasons for this, as the unpredictable shifts in momentum in the markets have caused active fund management to underperform significantly. However, it feels to me that passive strategies have grown too fast too quickly. I think active fund management is about to have its day in the sun.

Given that the Horseman Global fund is short equities and long bonds, that is about as active as you can get. Or in other words, I am getting bullish on bearishness!

end

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:00 am

Euro/USA 1.0917 UP .0020/REACTING TO NO DECISION IN JAPAN AND USA + huge Deutsche bank problems

USA/JAPAN YEN 105.34 UP .121(Abe’s new negative interest rate (NIRP), a total DISASTER/SIGNALS U TURN WITH INCREASED NEGATIVITY IN NIRP/JAPAN OUT OF WEAPONS TO FIGHT ECONOMIC DISASTER/KURODA: HELICOPTER MONEY ON THE TABLE AND DECISION ON SEPT 21 DISAPPOINTS WITH STIMULUS/OPERATION REVERSE TWIST

GBP/USA 1.2124 DOWN.0044 (Brexit by March 201/pound clobbered)

USA/CAN 1.3387 UP .0002

Early THIS FRIDAY morning in Europe, the Euro ROSE by 20 basis points, trading now JUST above the important 1.08 level RISING to 1.0917; Europe is still reacting to Gr Britain BREXIT,deflation, announcements of massive stimulation (QE), a proxy middle east war, and the ramifications of a default at the Austrian Hypo bank, an imminent default of Greece, Glencore, Nysmark and the Ukraine, along with rising peripheral bond yield further stimulation as the EU is moving more into NIRP, THE USA’S NON tightening by FAILING TO RAISE THEIR INTEREST RATE AND NOW THE HUGE PROBLEMS FACING TOO BIG TO FAIL DEUTSCHE BANK / Last night the Shanghai composite CLOSED DOWN 8.08 OR 0.26% / Hang Sang CLOSED D0WN 177.54 OR 0.77% /AUSTRALIA IS LOWER BY 0.14% / EUROPEAN BOURSES ALL MIXED

We are seeing that the 3 major global carry trades are being unwound. The BIGGY is the first one;

1. the total dollar global short is 9 trillion USA and as such we are now witnessing a sea of red blood on the streets as derivatives blow up with the massive rise in the rise in the dollar against all paper currencies and especially with the fall of the yuan carry trade. The emerging market which house close to 50% of the 9 trillion dollar short is feeling the massive pain as their debt is quite unmanageable.

2, the Nikkei average vs gold carry trade ( NIKKEI blowing up and the yen carry trade HAS BLOWN up/and now NIRP)

3. Short Swiss franc/long assets blew up ( Eastern European housing/Nikkei etc.