My website is now ready but we still have to add a little stuff to it. You can find my site at the following url:

harveyorganblog.com or harveyorgan.wordpress.com

I will continue to send the comex data down to my good friends at the Doctorsilvers website on a continual basis.

They provide the comex data. I also provide other pertinent data that may interest you. So if you wish you can view that part on my website.

I would like to thank you for your patience and I would like to thank my son, Stephen for his invaluable assistance in setting my website up. We are confident that it will not be shut down.

Gold: $1197.10 up $13.60

Silver: $16.17 up 12 cents

In the access market 5:15 pm

Gold $1197.50

silver $16.20

Gold and silver had a great day price wise.

The gold comex today had a poor delivery day, registering 0 notices served for nil oz.

Silver comex registered 0 notices for nil oz.

A few months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 255.02 tonnes for a loss of 48 tonnes over that period. .

In silver, the open interest rose considerably despite yesterday’s loss in price ( 26 cents). It looks like we have a few nervous shorts in silver racing against the clock to cover some of their shortfall!! The total silver OI remains extremely high with today’s reading at 173,617 contracts. The big December silver OI contract marginally lowered to 78,239 contracts. The high December OI is huge news as those longs remain firmly planted ready to take on the bankers.

In gold we had a huge gain in OI despite yesterday’s loss in price of gold to the tune of $2.00 . The total comex gold OI rests tonight quite elevated at 457,086 for a gain of a 3,032 contracts. The December gold OI rests tonight at 204,689 contracts which had a smallish contraction of 8451 contracts. We lost some of the paper longs into February .

Today, we had no change in tonnage of gold Inventory at the GLD / inventory rests tonight at 723.01 tonnes.

In silver, the SLV inventory remained constant tonight:

SLV’s inventory rests tonight at 346.900 million oz.

In trading of the gold and silver today, gold started to rocket northbound during the early hours reaching its zenith at 5 am this morning at $1204.65. The 1200 dollar mark is important to the bankers and they will defend that number until physical strength overpowers the non backed paper suppliers. Gold will no doubt try to pierce the 1200 level tomorrow.

Silver reached its pinnacle at exactly the same time 5 am reaching $16.42 upon which the bankers were not impressed and they whacked the metal all the way back to $16.20 level where it hovered slightly above and below that level.

.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today.

First: Most GOFO rates: move again deeper in backwardation!!

OH!!! OH!!

Most months basically moved deeper into backwardation

Now, the first 4 months of GOFO rates( one, two, three and six month GOFO) moved deeply into the negative with the 6th month GOFO now negative again and in backwardation. The front one month GOFO moved every so slightly towards the positive but still very deep into backwardation. On the 22nd of September the LBMA stated that they will not publish GOFO rates. However today we still received today’s GOFO rates.

It looks to me like these rates even though negative are still fully manipulated.

London good delivery bars are still quite scarce.

The backwardation in gold is incompatible with the raid on gold . It does not make any economic sense.

Nov 18 2014

1 Month Rate: 2 Month Rate 3 Month Rate 6 month rate 1 yr rate

-.2175% -0.17% -0.1175% – .0100% + .10750%

Nov 17 .2014:

1 Month Rate 2 Month Rate 3 Month Rate 6 month Rate 1 yr rate

-.22% -.16% -1075% -0075% +1150%

end

Let us now head over to the comex and assess trading over there today,

Here are today’s comex results:

The total gold comex open interest rose by a wide margin of 3032 contracts from 453,974 up to 457,006 with gold down $2.00 on yesterday. I guess the bankers continue to sell non backed paper whereupon major entities are taking on those bankers. The front delivery month is November and here the OI fell by 457 contracts. We had 462 delivery notices filed on yesterday so we gained 5 contracts or 500 additional gold ounces will stand for the November contact delivery month. The big December contract month saw it’s Oi fall by a normal 58451 contracts down to 204,689. Most of the selling December longs rolled into February. The estimated volume today was weak at 118,390 . Today the boys seemed a little timid providing the paper. The confirmed volume yesterday was very good at 240,140. Strangely on this 15th day of notices, we had 0 notices filed for nil oz.

And now for the silver comex results. The total OI rose sharply by 892 contracts from 172,725 up to 173,617 as silver was down 26 cents yesterday. It seems that judging from silver’s OI, our banker friends are still very nervous as they try to cover their massive shortfall in silver. In ounces, this represents a total of 868 million oz or 124.0% of annual global supply. We are now in the non active silver contract month of November and here the OI fell by one contract from 89 down to 88. We had 1 notice filed yesterday so we neither gained nor lost any silver contracts oz that will stand for the November contract month. The big December active contract month saw it’s OI fall by only 1,758 contracts down to 78,239 which sent shock waves throughout Wall Street and comex officials. A normal contraction is around 5,000 contracts per day on a roll. The December contract month remains highly elevated for this time in the delivery cycle. In ounces the December contract is represented by 391 million oz or 55.8% of annual global production (production = 700 million oz – China). The estimated volume today was fair at 33,304. The confirmed volume yesterday was huge at 71,760. We also had 0 notices filed today for nil oz.

I have been corrected on the first day notice. It will be on Friday, Nov 28.2014 the day after Thanksgiving. That will be exciting as nobody will be around.We thus have 6 more comex sessions.

Data for the November delivery month.

November initial standings

Nov 18.2014

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 64.30 oz (Manfra) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 482.25 oz (15 Kilobars???) |

| No of oz served (contracts) today | 0 contracts(nil oz) |

| No of oz to be served (notices) | 19 contracts (1900 oz) |

| Total monthly oz gold served (contracts) so far this month | 1392 contracts (139,200 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 80,623.1 oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

532,652.7 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

total dealer deposit: nil oz

we had 1 customer withdrawal:

i) Out of Manfra 64.30 oz (2 kilobars

total customer withdrawals : 64.30 oz

we had 1 customer deposits:

Into Manfra 482.25 oz or 15 kilobars.

total customer deposits : 482.25 oz

We had 0 adjustments:

Total Dealer inventory: 868,910.561 oz or 27.02 tonnes

Total gold inventory (dealer and customer) = 8.205 million oz. (255.22) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 48 tonnes have been net transferred out. We will be watching this closely!

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the November contract month, we take the total number of notices filed for the month (1392) x 100 oz to which we add the difference between the OI for the front month of November (19) – the number of gold notices filed today (0) x 100 oz = the amount of gold oz standing for the November contract month.

Thus the initial standings:

139,200 (notices filed today x 100 oz + ( 19) OI for November – 0 (no of notices filed today)= 141,100 oz or 4.388 tonnes.

We gained 500 oz of gold standing for the November contract month.

And now for silver

Nov 18/2014:

November silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | 1,018,220.210 oz (,Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 728,248.76 oz (CNT,HSBC,Scotia) |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 88 contracts (440,000 oz) |

| Total monthly oz silver served (contracts) | 156 contracts 780,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 781,023.9 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,924,775.4 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 3 customer withdrawals:

i) Out of CNT: 150,480.07 oz

ii) Out of HSBC: 517,142.79 oz

iii) Out of Scotia: 60,625.900 oz

total customer withdrawal 728,248.76 oz

We had 1 customer deposits:

i) Into Scotia: 1,018,220.210 oz

total customer deposits: 1,018,220.210 oz

we had 0 adjustment

Total dealer inventory: 65.350 million oz

Total of all silver inventory (dealer and customer) 178.005 million oz.

The total number of notices filed today is represented by 0 contract or nil oz. To calculate the number of silver ounces that will stand for delivery in November, we take the total number of notices filed for the month (156 ) x 5,000 oz to which we add the difference between the total OI for the front month of November(88) minus (the number of notices filed today (0) x 5,000 oz = the total number of silver oz standing so far in November.

Thus: 156 contracts x 5000 oz + (88) OI for the November contract month – 0 (the number of notices filed today) = amount standing or 1,220,000 oz of silver standing.

we neither gained nor lost any silver ounces standing today.

It looks like China is still in a holding pattern ready to pounce when needed.

For those wishing to see data on the currencies and bourse closings you can see it on my site at harveyorgan.wordpress.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

Nov 18.2014: no change in inventory/ Inventory level 723.01 tonnes

Nov 17.2014; we had a huge addition of 2.39 tonnes of gold added to the GLF inventory/inventory rests tonight at 723.01 tonnes. They may be running out of metal to give China!!!

Nov 14. we had no change in gold inventory at the GLD/inventory 720.62 tonnes

nov 13. we lost another 2.05 tonnes of gold at the GLD/Inventory at 720.62 tonnes

Nov 12.2014; we lost another 1.79 tonnes of gold at the GLD/Inventory at 722.67 tonnes

This gold left the shores of England and landed in Shanghai.

Nov 11.2014: we lost another 0.900 tonnes of gold at the GLD/Inventory 724.46 tonnes

Nov 10. we lost another 1.79 tonnes of gold at the GLD/Inventory 725.36 tonnes

Nov 7 wow!! we lost another huge 5.68 tonnes of gold at the GLD/inventory 727.15 tonnes

Nov 6.2014: we had another huge withdrawal of 2.99 tonnes of gold. Inventory 732.83 tonnes

This gold is also heading to Shanghai. If I was a shareholder of GLD I would be quite concerned as there will be no real gold inventory left per outstanding shares.

Nov 5 we had another huge withdrawal of 3.000 tonnes of gold. This gold will be heading to Shanghai/GLD inventory 735.82 tonnes

Nov 4.2014: a huge withdrawal of 2.39 tonnes of gold/GLD inventory/738.82 tonnes

Nov 3.2014: no change in gold inventory at the GLD/741.21 tonnes

Oct 31.2014: no change in gold inventory at the GLD despite the raid/inventory at 741.21 tonnes

October 30.2014: we had another 1.2 tonnes of gold leave the GLD and heading to Shanghai/Inventory 741.21 tonnes

October 29.2014: we had another .99 tonnes of gold removed from the GLD/inventory 742.40 tonnes

Today, Nov 18. no change in gold inventory

inventory: 723.01 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 723.01 tonnes.

end

And now for silver:

Nov 18.2014; no change in silver inventory 346.90 million oz

Nov 17.2014 .SLV inventories remain constant tonight at 346.90 million oz

Nov 14.2014; wow!! we had an addition of 2.012 million oz into the SLV/inventory at 346.900 million oz

Nov 13. no change in silver inventory at the SLV/344.888 million oz.

Nov 12.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz. And please note that gold leaves GLD/silver does not. Why? there is no physical silver at the SLV..just paper obligations.

Nov 11.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz.

Nov 10/ we had an addition of 1.438 million oz of silver into inventory at the SLV/Inventory 344.888 million oz (again note the difference between gold and silver)

Nov 7/ 2014/no change in silver inventory/inventory rests at 343.45 million oz. (please note the difference between silver (SLV) and gold (GLD)

Nov 6.2014: no change in silver inventory/(as of 6 pm est) inventory rests at 343.45 million oz.

Nov 5 today, the total silver inventory drops of 2.074 million oz/SLV inventory: 343.45 million oz

Nov 4.2014: wow!! we had another addition of 1.151 million oz of silver inventory/SLV inventory rises to 345.524

Please note the difference between GLD and SLV. The GLD has physical gold to send on its way to Shanghai/SLV has no silver to offer to the participants to give to various players..

Nov 18.2014 no change in silver inventory at the SLV/346.900 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now deeply into the positive to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 9.3% percent to NAV in usa funds and Negative 9.6% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.4%

Percentage of fund in silver:38.00%

cash .6%

( Nov 18/2014)

2. Sprott silver fund (PSLV): Premium to NAV rises to positive 4.18% NAV (Nov 18/2014)

3. Sprott gold fund (PHYS): premium to NAV falls to negative -0.38% to NAV(Nov 18/2014)

Note: Sprott silver trust back hugely into positive territory at 4.18%.

Sprott physical gold trust is back in negative territory at -0.38%

Central fund of Canada’s is still in jail.

end

And now for your most important physical stories on gold and silver today:

Early gold trading form Europe early Tuesday morning:

(courtesy Goldcore/Mark O’Byrne)

Despite gold’s rebound, backwardation has gotten worse, Turk tells KWN

Submitted by cpowell on Tue, 2014-11-18 04:12. Section: Daily Dispatches

11:13p ET Monday, November 17, 2014

Dear Friend of GATA and Gold:

Despite the big increase in the gold price over the last week, backwardation in the monetary metal has gotten worse, GoldMoney founder and GATA consultant James Turk tells King World News tonight. Turk adds that gold shorts seem to be operating on a hair trigger. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/11/17_G…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Another article on gold backwardation by Larkin/Bloomberg)

Lending gold pays record high as 400-oz bars are lost to insatiable Asian demand

Submitted by cpowell on Tue, 2014-11-18 04:04. Section: Daily Dispatches

Gold Lending Rate Most Negative Since 2001 on Longer Refining

By Nicholas Larkin and Laura Clarke

Bloomberg News

Monday, November 17, 2014

LONDON — The rate at which gold is lent for dollars is the most negative in 13 years as refineries spend longer recasting bars from vaults to meet demand from Asia, where consumers prefer smaller ingots and jewelry.

The one-month gold forward offered rate was at minus 0.22 percent today, the most negative since March 2001, signaling that dealers are paid to lend metal against cash, rather than paying for the privilege. It’s also a form of backwardation, when earlier prices are more expensive than for later dates.

Holdings in gold-backed funds have slid to the lowest since 2009 and prices are near a four-year low as a stronger dollar and improving U.S. economy curbed haven demand. The gold lending rate has turned negative because refiners such as those in Switzerland are turning more bars typically weighing 400 ounces into smaller items such as 1-kilogram products. Indian third-quarter bullion imports more than doubled from a year earlier.

“There’s a lot of demand going into Swiss refineries, which are basically transforming those big bars into smaller bars,” Bernard Dahdah, an analyst at Natixis SA in London, said today by phone. “The leasable stuff is only for big bars. Once those bars become small bars and they go into households, they become much harder to go back into the market into a leasable form.” …

… For the remainder of the report:

http://www.bloomberg.com/news/2014-11-17/gold-lending-rate-most-negative…

end

Your big story of the day. Back in March we brought you the story that during one night, right after Yanukovich was ousted, it was reported that during the night, Ukraine’s gold was taken during the night and flown to the FRBNY. There was no official word.

Details on the event are provided by zero hedge. Now the Ukrainian central bank admits it’s gold is gone or approximately 20.8 tonnes of gold. They do not venture a guess as to what happened to it!!

Two commentaries on this;

first zero hedge

(courtesy zero hedge)

Ukraine Admits Its Gold Is Gone: “There Is Almost No Gold Left In The Central Bank Vault”

Back in March, at a time when the IMF reported that Ukraine’s official gold holdings as of the end of February, so just as the State Department-facilitated coup against former president Victor Yanukovich was concluding, amounted to 42.3 tonnes or 8% of reserves…

… and notably under the previous “hated” president, Ukraine gold’s reserves had constantly increased hitting a record high just before the presidential coup…

… we reported of a strange incident that took place just after the Ukraine presidential coup, namely that according to at least one source, “in a mysterious operation under the cover of night, Ukraine’s gold reserves were promptly loaded onboard an unmarked plane, which subsequently took the gold to the US.” To wit:

Tonight, around at 2:00 am, an unregistered transport plane took off took off from Boryspil airport. According to Boryspil staff, prior to the plane’s appearance, four trucks and two cargo minibuses arrived at the airport all with their license plates missing. Fifteen people in black uniforms, masks and body armor stepped out, some armed with machine guns. These people loaded the plane with more than forty heavy boxes.

After this, several mysterious men arrived and also entered the plane. The loading was carried out in a hurry. After unloading, the plateless cars immediately left the runway, and the plane took off on an emergency basis.

Airport officials who saw this mysterious “special operation” immediately notified the administration of the airport, which however strongly advised them “not to meddle in other people’s business.”

Later, the editors were called by one of the senior officials of the former Ministry of Income and Fees, who reported that, according to him, tonight on the orders of one of the “new leaders” of Ukraine, all the gold reserves of the Ukraine were taken to the United States.

Needless to say there was no official confirmation of any of this taking place, and in fact our report, in which we mused if the “price of Ukraine’s liberation” was the handover of its gold to the Fed at a time when Germany was actively seeking to repatriate its own physical gold located at the bedrock of the NY Fed, led to the usual mainstream media mockery.

Until now.

In an interview on Ukraine TV, none other than the head of the Ukraine Central Bank made the stunning admission that “in the vaults of the central bank there is almost no gold left. There is a small amount of gold bullion left, but it’s just 1% of reserves.”

As Ukraina further reports, this stunning revelation means that not only has Ukraine been quietly depleting its gold throughout the year, but that the latest official number, according to which Ukraine gold was 8 times greater than the reported 1%, was fabricated, and that the real number is about 90% lower.

According to official statistics the NBU, the amount of gold in the vaults should be eight times more than is actually in stock. At the beginning of this month, the volume of gold was about $ 1 billion, or 8% of the total gold reserves. Now this is just one percent.

Of course, considering the official reserve data at the Central Bank has been clearly fabricated, one wonders just how long ago the actual gold “dmsplacement” took place.

We get some additional information from Rusila:

According to recent data, the value of Ukraine gold should be $988.7 million. That is the value of gold proportion of gold in gold reserves is 8%. If you believe Gontareva, it turns out there is a mere $123.6 million in gold remaining.

The figure is fantastic, considering that the amount of gold at the end of February (when the new authorities have already taken key positions) was $1.8 billion or 12% of the reserves.

In other words, since the beginning of the year gold reserves dropped almost 16 times. Gold stock in February were approximately 21 tons of gold, the presence of which was once proudly reported by Sergei Arbuzov, who led the NBU in 2010-2012. So what happened to 20.8 tons of gold?

Explaining the dramatic reduction in the context of the hryvnia devaluation through gold sales is impossible. After all, 92% of the reserves of the National Bank is in the form of a foreign currency that is much easier to use to maintain hryvnia levels and cover current liabilities. Besides since March the international price of gold has plummeted. Selling ??gold under such circumstances is a crime. In fact it would be more expedient to increase gold reserves through currency conversion in precious metals.

But apparently the result is not due to someone’s negligence or carelessness. The gold reserve has been actively carted out of the country, as a result of the very vague economic and political prospects of Ukraine. Something similar happened to the gold reserves of the USSR – when the Gorbachev elite realized that perestroika is leading the country to the abyss, gold simply disappeared in an unknown direction.

The article’s conclusion:

As history shows, the reduction of the gold reserves in the context of an acute political crisis is usually preceded by the collapse of the state.

Oddly enough there was no official gold reduction just prior to the time when Victoria “Fuck the EU” Nulandwas planning Yanukovich’s ouster, and as shown above, quite the contrary. It is a little more odd that it was during the period when Ukraine was “supported” by its western allies that several billion dollars worth of physical gold – the people’s gold – just “vaporized.”

In any event, now that the disappearance of Ukraine’s gold has been confirmed, perhaps it is time to refresh the “unconfirmed” story that a little after the current Ukraine regime took power the bulk of Ukraine’s gold was taken to the United States.

As of this writing, The NY Fed has still not answered our March request for a comment whether Ukraine’s gold has been redomiciled at the gold vault located some 80 feet below Liberty 33.

end

And now Chris Powell of GATA comments on the above story:

(courtesy Chris Powell/GATA)

One way or another, Ukraine’s gold reserves have gone away

Submitted by cpowell on Tue, 2014-11-18 18:23. Section: Daily Dispatches

1:23p ET Tuesday, November 18, 2014

Dear Friend of GATA and Gold:

Zero Hedge reports today that one way or another, Ukraine’s gold reserves have disappeared:

http://www.zerohedge.com/news/2014-11-18/ukraine-admits-its-gold-gone

A report about their supposed removal from Kiev in the dead of night last March is posted at GATA’s Internet site here:

http://www.gata.org/node/13754

The refusal of the gold-vaulting Federal Reserve Bank of New York to disclose to GATA in March whether it had taken custody of the Ukrainian reserves is here:

http://www.gata.org/node/13761

The U.S. State Department never responded to GATA’s inquiry.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Today’s action on gold

(courtesy Mineweb/Lawrence Williams)

Gold bounces back above $1 200 – will it jump higher?

Gold moved back above the psychological $1,200 level this morning. Can it retain this upwards move and perhaps extend it?

Author: Lawrence Williams

Posted: Tuesday , 18 Nov 2014

LONDON (MINEWEB) –

Gold bounced back above $1 200 this morning in London, but before one can be sure that this is the start of the long-expected recovery there could yet be teeth in the bear. The big money playing the futures markets with paper gold can still exert ultimate control over where the price is headed short term and if it suits them there could yet be another sharp price drop to try and drive out any remaining weak gold holders.

But medium term it may be that options are becoming more and more limited for keeping the market depressed. Gold continues to flow from West to East with the big recovery in Indian demand coupled with continuing high levels of withdrawals from the Shanghai Gold Exchange as the key elements in this. Although whether Indian demand has recovered to overtake China’s over the past two quarters as World Gold Council figures might suggest, and which has been reported as fact by much of the media, given SGE withdrawal figures have been running at such high levels of late we think is not a true picture of the real situation, but in combination India and China are taking in gold at back to peak levels.

Demand is also seen as high in a number of other countries in Europe, the Middle East and elsewhere in Asia, while Russia and some of the old FSU countries are adding to their gold reserves thus taking even more metal off the markets. It is hard to see where all this volume of gold is coming from as it certainly substantially exceeds new global gold output.

Gold in backwardation too also suggests that supplies of physical metal in the West are becoming more and more limited and the logic of shorting gold may be about to disappear. There has been the suggestion that the recent fall in the gold price down to $1 140 has been a bear trap to catch the short traders out.

Indeed with the bank analysts virtually all feverishly cutting their price forecasts the temptation for the short position holders to hold firm, or increase their positions, has been strong, but if the big money is buying physical metal at these levels, perhaps quietly, then they may be positioning themselves to drive prices up, and once the momentum starts flowing the upside potential could be large.

But it is too early to call the gold price bottom yet. As we pointed out in our article yesterday on WaveTrack International’s Elliott Wave interpretation of what has been happening there could be yet another price drop before the true recovery – which the analysis sees as both inevitable and immense – really gets under way.

See: Elliott Wave analyst sees big gold and silver price surge ahead

If gold holds above the psychological $1200 level this week, then the momentum could well stay with the bulls and it could move sharply higher still. If investor sentiment towards gold should become more positive – particularly if the major stock indices start to stutter with the realisation that economic recovery is not what many politicians and bankers are telling us, but remains fragile, then this could be the dawn of a new gold bull market.

And if this is so silver, which has been underperforming, should do even better than its sibling. But picking bottoms is not easy and there are still pressures out there which could presage yet another fall. However all the time the fundamentals for gold are improving given the physical metal flows into ever stronger hands and at some stage, quite probably within the next year (it could even be within the next few months), gold is indeed going to start to move significantly higher.

We may not be there yet, but as Peter Goodburn of WaveTrack International is convinced, the mega upturn in precious metals – and perhaps even more so in precious metals mining stocks – has moved from probability to inevitability. It’s just the actual timing that is uncertain.

end

my goodness

(courtesy zero hedge)

Goldman FX Trader Fired For Participating In Currency-Rigging Cartel Even As Goldman Avoids Any Charges

As we noted previously, one of the glaring omissions from the list of banks that were charged with rigging FX markets, and subsequently promptly settled with nobody going to prison as usual, which consisted of:

- Barclays PLC

- HSBC Holdings PLC

- Royal Bank of Scotland Group PLC

- UBS AG

- Citigroup

- J.P. Morgan Chase

- Bank of America Corp. Bank of America

Was none other than the bank which according to recent revelations, has undue control over the NY Fed, Goldman Sachs. And yet, moments ago the WSJ reported that Goldman Sachs just fired a currencies trader who “allegedly was involved with the misconduct before he joined the firm.”

So how is it possible that Goldman, which housed one of “The Cartel’s” (or was it Bandits?) riggers, was never busted in the first place? Because apparently Goldman had no clue of his impeccable FX-rigging chat room credentials when it hired him from HSBC back in 2012.

Incidentally, when Cahill was hired by HSBC from Barclays, the bank said the following:

“Frank is a talented trader and we look forward to welcoming him to the team, where he will run our GBP/USD book. His hire is part of our continued build-out of our overall product and distribution capability.”

Talented indeed. As for Frank’s FX-rigging credentials, we find it very believable that he never again used these while employed by Goldman because the moment he walked through the door at 200 West, he was a changed man, doing merely god’s work and nobody else’s.

Frank Cahill, who joined Goldman Sachs in 2012 as a currencies trader after working at HSBC Holdings PLC, was asked to leave Goldman’s London offices on Tuesday as a result of his alleged involvement in the currencies-rigging affair, according to a person familiar with the matter.

“This relates to a period before he joined Goldman Sachs and he has now left the firm,” a Goldman Sachs spokeswoman said.

And then when he joined Goldman, he dropped everything, never entered another chat room ever again, and everyone lived happily ever after. Until now that is, because someone had to take the fall: that someone was Mr. Cahill was also happens to be a “cable rigger“, no pun intended.

Mr. Cahill, a sterling trader, worked at Barclays PLC before joining HSBC in 2010, according to U.K. regulatory records. He was one of a number of unidentified HSBC traders whose conversations in electronic chat sessions were quoted by the U.K.’s Financial Conduct Authority and the U.S. Commodity Futures Trading Commission as part of their settlements with the British bank last week, according to people familiar with the chat transcripts.

Which is ironic, because the FCA complaint involving HSBC revolves precisely around a manipulator of sterling. Let’s recall just how that one particular chat session, which generated $162K in profit for HCBS and Mr. Frank Cahill who ran HSBC’s Cable book and almost certainly is the participant in the chat session – went:

An example of HSBC’s involvement in this behaviour occurred on one day within the Relevant Period when HSBC attempted to manipulate the WMR fix in the GBP/USD currency pair. On this day, HSBC had net client sell orders at the fix which meant that it would benefit if it was able to move the WMR fix rate lower.10 The chances of successfully manipulating the fix rate in this manner would be improved if HSBC and other firms adopted trading strategies based upon the information they shared with each other about their net orders.

In the period between 2:50pm and 3:44pm on this day, traders at four different firms (including HSBC) inappropriately disclosed to each other via chat rooms details of their net orders in respect of the forthcoming 4pm WMR fix in order to determine their trading strategies. The other three firms are referred to in this Final Notice as Firms A, B and C, as well as two other firms as Firms D and E. HSBC participated in a series of actions described below in an attempt to manipulate the fix rate lower.

- At 2:50pm, Firm A disclosed in a chat room (including to HSBC) that it had net sell orders for more than GBP100 million at the fix. At 3:25pm, Firm A indicated that the orders were for approximately GBP130 million.

- At 3:25pm, HSBC disclosed to Firm A in a one-to-one chat that it had net client sell orders for GBP400 million at the fix. Since HSBC and Firm A each needed to sell GBP at the fix each would profit to the extent that the fix rate at which it bought GBP was lower than the average rate at which it sold GBP in the market.

- Firm A informed HSBC that it now had net sell orders of GBP150 million at the fix. HSBC responded by saying “lets go”,11 to which Firm A replied “yeah baby”. The Authority considers these statements to refer to the possibility of HSBC and Firm A co-ordinating their actions in an attempt to manipulate the fix rate downwards.

- At 3:28pm in a chat room which included HSBC, Firm A expressed the hope that other traders would also have sell orders at the fix (“hopefulyl a fe wmore get same way and we can team whack it”). At 3:36pm, Firm B, which was a participant in the chat room, confirmed to the other traders that he now also had net sell orders for GBP40 million at the fix.

- At 3:28pm, HSBC informed Firm C via a one-to-one chat room that he had net client sell orders of around GBP300 million at the fix and asked the trader to do some “digging” to see if anyone else had orders in the same direction at the fix. Firm C replied at 3:34pm and disclosed to HSBC that it now also had net sell orders of GBP83 million at the fix.

- At 3:36pm, Firm D asked Firm A in a chat room (which included HSBC), for an update on its net sell orders. Firm A disclosed that it had now increased to GBP170 million. Firm D noted that it did not have any fix orders at that time, but commented that he expected Firm A to “bash the fck out of it”.

- At 3:38pm, HSBC commented simultaneously into chat rooms in which Firms A, C and D participated that it had net client sell orders at the fix for GBP in a “good amount”.

- At 3:42pm, in a one-to-one chat Firm A warned HSBC that another firm which was not a participant in the chat room (Firm E) was “buidling” in the opposite direction to them and would be buying at the fix.

- At 3:43pm, Firm A updated HSBC by indicating that it had netted some of its sell order off with Firm E and “taken him out… so shud have giot rid of main buyer for u…im stilla seller of 90… gives us a chance”. The Authority considers that this refers to Firm A’s belief that Firm E would no longer be transacting its orders in the opposite direction at the fix. It also confirmed that Firm A still held net sell orders for GBP90 million to trade at the fix and could still participate in the co-ordinated behaviour. This is an example of Firm A “clearing the decks”.

In the period from 3:32pm to 4:01pm, HSBC sold GBP381 million on Reuters and other trading platforms. Approximately GBP70 million (or 18%) of this volume was sold by HSBC in advance of the 60 second fix window around 4pm. During the period from 3:32pm to the start of the fix window, the GBP/USD rate fell from 1.6044 to 1.6009. These early trades were designed to take advantage of the expected downwards movement in the fix rate following the discussions within the chat rooms described above.

In the first five seconds of the fix window, HSBC entered a further nine offers to sell GBP101 million. During the first five seconds, the bid rate fell from 1.6009 to 1.6000. HSBC continued to enter offers throughout the remainder of the fix window and the bid rate fluctuated between 1.6000 and 1.6005.

HSBC sold GBP311 million during the fix window on Reuters and other trading platforms. The amount it sold on Reuters accounted for 51% of the volume sold in the GBP/USD currency pair on the Reuters platform during the fix window. Cumulatively HSBC and Firms A to C accounted for 63% of selling during the fix window. Subsequently, WM Reuters published the 4pm fix rate for GBP/USD at 1.6003.

The information disclosed between HSBC and Firms A, B and C, regarding their order flows was used to determine their trading strategies. The consequent trading by HSBC during the fix window was designed to decrease the WMR fix rate to HSBC’s benefit. HSBC’s trading in GBP/USD in this example generated a profit of approximately USD162,000.

Subsequent to the fix, traders in the chat rooms congratulated one another by saying: “nice work gents…I don my hat”, “Hooray nice team work”, “bravo…cudnt been better” and “have that my son…v nice mate” and “dont mess with our ccy [currency]”. One of the traders commented “there you go … go early, move it, hold it, push it”. HSBC stated “loved that mate… worked lovely… pity we couldn’t get it below the 00” and “we need a few more of those for me to get back on track this month”.

There you go indeed Mr. Cahill: “go early, move it, hold it, push it”, and don’t le the door hit you on your wait out when your new employer realizes that you were just guilty of the biggest crime possible in finance: getting caught.

As for Goldman, we expect the firm to never be charged with any rigging crimes: after all none of said riggers actually every abused their privilege while working at 200 West. They merely were hired for such manipulative skills.

end

And now Bill Holter:

Pay close attention to Bill’s latest piece…

(courtesy Bill Holter/Miles Franklin)

Gold and Silver supply is VERY tight!

Folks, this is really big news and a huge “tell” as to the state of supply in the gold market. Just add these two pieces together, negative GOFO rates and notices instantly being served in a very small delivery month… you get a picture of severe supply tightness. This in no way is compatible with weak pricing! Something has to give and since “delivery” in the gold market is a major part of the equation, the sale of derivatives will not cut it much longer. Just as machinery will not run on COMEX diesel futures, Eastern vaults will not be filled with derivative contracts! Regards, Bill Holter

And now for the important paper stories for today:

Early Tuesday morning trading from Europe/Asia

1. Stocks down with major Asian bourses with a slightly lower yen value to 116.68

2 Nikkei up 370 points or 2.18%

3. Europe stocks all up /Euro rises/ USA dollar index up at 87.61.

3b Japan 10 year yield at .52%/Japanese yen vs usa cross now at 116.68

3c Nikkei now above 17,000

3fOil: WTI 75.60 Brent: 79.08 /all eyes are focusing on oil prices. A drop to the mid 60′s would cause major defaults.

3g/ Gold up/yen up; yen well above 116 to the dollar/

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt (see Von Greyerz)

3j German confidence surprises to the upside

3k Japanese GDP plummets/sales tax hike will no doubt be delayed and

Snap election called. Stimulus of 26 billion usa to be initiated.

3l Chinese home sales suffer

3m Gold at $1200 dollars/ Silver: $16.26

4. USA 10 yr treasury bond at 2.34% early this morning.

5. Details

Ransquawk/Bloomberg/Deutche bank/Jim Reid

(courtesy zero hedge/your early morning trading

from Asia and Europe)

Algos Sell The News, Then BTFD Following Much Anticipated Abe Snap Election Announcement

Submitted by Tyler Durden on 11/18/2014 07:54 -0500

After weeks of relentless flashing red headline barrage whose only purpose was to force snap algo buying of the USDJPY pair time after time after time, Japan is once again out of FX algo danging carrots after moments ago Abe confirmed what everyone had known already: he called a snap election to seek a mandate for his decision to delay by 18 months a further sales-tax increase that had been planned for next year; he also said he would dissolve the lower house of parliament on Nov. 21 in preparation for an election in December, without specifying a date. Cited by the WSJ, Abe said “To ensure the success of Abenomics, I’ve concluded that it shouldn’t be carried out next October and instead be postponed by 18 months,” the prime minister told a nationally televised news conference, stressing that the additional tax burden would risk putting the economy back into deflation. “I will seek the people’s judgment over our economic policy.”

What was left unsaid is that at the very same time the ruling party effectively bribed the population to vote for it after Japan’s FinMin Aso said the government would prioritise passing through parliament a supplementary budget for the current fiscal year to fund a stimulus package, which media reports have said could be worth 2-3 trillion yen (which actually is just a rather tiny $17-$26 billion).

So while Abe is running on hopes that the people will vote for less taxes and more fiscal spending – because the last thing the country with the 230% debt/GDP and which is monetizing all of its debt issuance is, gasp, more austerity – the people may just decide to get rid of him altogether not for his endless barage of promises about the future but for his constant failures in the real world, such as goosing the market by $1 trillion and only getting only lousy recession to show for it.

Bottom line, as Bloomberg noted:

- ABE: LOSS OF MAJORITY WOULD BE REJECTION OF ABENOMICS

And if indeed people vote with their wallets and the electric, food and gas bills on December 14, when Goldman believes the vote will take place, Abe is voted out, watch as the global asset reflation spectacle comes crashing down to earth.

That said, the market reaction was hilarious: one USDJPY regained all the losses from yesterday’s shocking quaruple-dip announcement, and touched 117, then that old “sell the news” kneejerk reaction kicked in just as Abe was holding his press conference. And then, to remind everyone that we live in the new normal after all, the USDJPY was quickly BTFD. End result: a 100 pip move in seconds.

Perfectly normal.

The best news is that no more will the USDJPY jump by 20-100 pips when the very same headline is regurgitated at strategic market inflection points. At least not until Japan comes up with yet another dangling carrot to goose the ever-trigger happy algos.

Elsewhere in Europe, European equities trade in the green with gains of 0.75-1.0% with sentiment largely buoyed by the ongoing events in Japan. More specifically, PM Abe is to delay the sale-tax hike and dissolve Parliament. However, Abe is yet to confirm as to whether or not he will prepare a stimulus package in lieu of the recent GDP numbers. In index specific moves, the IBEX outperforms after being led by Abengoa (+12%) in a pull-back of recent heavy losses with little other major stocks news on offer as European earnings season draws to a close. Elsewhere, fixed income products traded relatively unchanged for a large part of the session until the German ZEW survey which saw the headline expectations figure exceed forecasts by coming in at 11.5 vs. Exp. 0.5 and thus extended the move higher for European equities while dragging fixed income products lower into negative territory.

In summary, European shares rise, close to intraday highs, with the oil & gas and chemicals sectors outperforming and travel & leisure, personal & household underperforming. Japan’s Abe says he’ll dissolve parliament, delay tax hike. German ZEW November investor expectations above estimates. European car sales rise for 14th straight month. Greece’s bailout review said to stall. The German and Spanish markets are the best-performing larger bourses, Swedish the worst. The euro is stronger against the dollar. Japanese 10yr bond yields rise; Greek yields increase. Commodities gain, with natural gas, copper underperforming and gold outperforming.

In Asia, Chinese equities are generally trading weaker following somewhat disappointing home price data whilst bourses are mostly mixed elsewhere. The print has done little to boost sentiment following news that home prices have dropped in 69 out of 70 cities in October relative to September and the average is now 2.6% lower versus last year. The CSI 300 is 1.1% lower as we type whilst the Hang Seng, Kospi and ASX 200 -1.0%, +1.1% and -0.2% respectively. Also in China, Bloomberg yesterday reported that the PBOC has issued rules allowing local financial institutions to invest in yuan assets abroad and in the meantime has refrained setting any limits on the amount that can be invested.

The US docket brings both the PPI and the NAHB housing market index reading. On the former, the market is expecting a -0.1% mom headline number. Away from the data prints, the Fed’s Kocherlakota will be speaking on monetary policy outlook this afternoon, whilst in Europe we will hear from the ECB’s Lautenschlaeger and Knot.

Bulletin headline summary

- European equities trade firmly in the green following on from the latest policy announcements in Japan, while the German ZEW survey surprises to the upside.

- USD/JPY edged higher throughout the session upon anticipation of the announcements from Japan before pulling away from 117.00 in a buy the rumour, sell the fact fashion as the policy decisions were largely priced in by the time they were announced.

- Looking ahead, attention turns towards US PPI data, API inventories and any comments from ECB’s Knot, Fed’s Kocherlaktoa and BoE’s Forbes.

Japan’s Abe called for an early election and delayed for 18 months a second planned sales-tax increase as he sought to extend his term and salvage his Abenomics policies after the country slipped into recession

German investor confidence rose for the first time in 11 months as the ZEW index increased to 11.5 in November (est. 0.5) from -3.6 in October

U.K. inflation unexpectedly accelerated last month as transport prices fell less than a year earlier and the cost of toys rose in the run-up to Christmas

Greece’s government and its international creditors are deadlocked over a final round of measures required to release the last tranche of the country’s bailout, two people familiar with the negotiations said

Chinese new-home prices dropped in October in 67 of 70 cities tracked by the government from a year earlier, according to the National Bureau of Statistics; prices in Beijing declined 1.3%, the first annual decrease since November 2012

Reserve Bank of Australia governor Stevens sees accommodative policy continuing for some time, cites spare capacity, controlled inflation

Even if Mary Landrieu (D-LA) is able to win passage of her Senate bill tonight to approve the Keystone XL oil pipeline, analysts said it may not be enough to affect the outcome of her re-election bid

Goldman says it’s adding staff to its European ABS business as the bank prepares for a resurgence in the $305b market that shrank more than 40% over the past four years

Sovereign yields mixed. Asian stocks mixed, Nikkei +2.1%, Shanghai -0.7%. European stocks gain, U.S. equity-index futures decline. Brent crude gains, copper little changed, gold +1.4%

Market Wrap

- S&P 500 futures down 0.1% to 2037.4

- Stoxx 600 up 0.6% to 339.2

- US 10Yr yield down 1bps to 2.33%

- German 10Yr yield down 1bps to 0.8%

- MSCI Asia Pacific up 0.6% to 140.6

- Gold spot up 1.3% to $1201.5/oz

FX

Following the expectations of announcements from Japan, USD/JPY ebbed higher throughout the session and in close proximity to the 117.00 handle, however, the pair proceeded to pull away from these levels as by the time they were announced the news was already priced into the market. Nonetheless, this move to the downside was halted by talk of leveraged names on the bid in the pair. GBP/USD traded higher following the last UK inflation report which saw the Y/Y CPI figure come in at 1.3% vs. Exp. 1.2% and thus avoided the dovish surprise that some had been expecting in the backdrop of last week’s QIR which warned that inflation could drop below 1.0% in the next 6 months. Elsewhere, broad-based USD strength has led EUR/USD to consolidate its move above 1.2500. Furthermore, the EUR strength has seen EUR/AUD trade higher by over 100 pips with the move to the upside exacerbated by comments from RBA governor Stevens who said a further AUD fall is likely to happen.

COMMODITIES

WTI and Brent crude prices enter the North American crossover in the green in a modest recovery of recent losses ahead of the upcoming OPEC meeting. In terms of notable commentary the Russian and Venezuelan oil ministers are said to be planning a meeting whereby they will discuss the need to coordinate actions in defence of prices. Furthermore, one thing for energy traders to keep an eye on today is the US Senate vote on the future of the Keystone XL pipeline, whereby those in favour of the bill need to secure 60 votes to prevent a filibuster by opponents. Elsewhere, spot gold broke above USD 1,200 to print its highest price this month alongside the weaker USD and fresh geopolitical concerns from the Israeli/Palestine situation. More specifically, Israel’s Netanyahu says Israel will react with an `iron fist` to an attack where 4 Israelis were killed and several others wounded in a terror attack in a synagogue in the western Jerusalem neighbourhood of Har Nof.

* * *

Deutsche Bank’s Jim Reid completes the overnight recap

Did Government QE in Europe get closer yesterday? It probably did slightly after Draghi comments to lawmakers at the European Parliament but to be honest markets are probably going to need more to be convinced that it will eventually happen. We still think Q1 2015 is the likely announcement time as taboos are being slowly broken down. To recap what Draghi said in his quarterly testimony, he said “Other unconventional measures might entail the purchase of a variety of assets, one of which is sovereign bonds”. He did say monetary policy alone can’t bring the economy back on track but it’s clear to us that the ECB are edging closer to action. Markets in Europe certainly appreciated the comments. The Stoxx 600 closed the day +0.48%, although traded as low as -0.8% pre-statement whilst peripheral assets finished stronger with 10yr yields in Spain, Italy and Portugal rallying 1bp, 4bps and 4bps respectively. The ECB’s Mersch was also dovish earlier, suggesting that the central bank could theoretically purchase a range of assets including sovereign debt, gold and ETFs. However his comments were a little more caveated than Draghi’s noting that such a decision must be subject to a cost-benefit analysis.

In Japan this morning the market has turned its focus away from yesterdays GDP print and onto a report from the Japanese Yomiuri newspaper suggesting that Abe could hold a press conference as soon as today with regards to delaying the sales tax increase. Following this we’ve also had a news report out of the Nikkei Review suggesting that the Prime Minister is expected to tell his ministers today to assemble a stimulus package focusing on consumer spending. The package is expected to total ¥2tn to ¥3tn with the aim of stimulating what has been fairly subdued consumer spending over recent times. Bloomberg and other wires are also suggesting that he will call an early election today with December 14th mooted as a possible date. The market appears to be expecting some sort of confirmation of the above packages with the Nikkei +2.2% and Topix +2.1% as we type.

With the news from yesterday that Japan is back in recession again it got us thinking about our shorter business cycle theory that we established back in 2010. The theory has worked spectacularly well across pretty much most of the DM world apart from the most important country namely the US. However outside the US, parts of Europe have been in and out of recession since and yesterday it re-claimed another victim with Japan in recession again for the third time post-GFC. The theory was based on the ‘great moderation’ (1980-2008) super cycles being driven by total flexibility of monetary and fiscal policy and that post crisis both would be far less able to be stretched at will. Most governments were looking to be or being forced to be more disciplined fiscally with a liquidity trap at the zero bound preventing monetary policy being used anywhere near as effectively as it had been during the prior decades. Policy has indeed been compromised but what we’ve also learned from this period is that fiscal is perhaps more important for growth and monetary policy for asset prices. The US maxed out on both beyond what most would have thought possible which helped avoid our shorter cycle theory and pump up asset prices whereas Europe implemented austerity around 2011/2 and Japan raised taxes earlier this year. Both sparked recessions. So we think the theory is still a valid one unless you’re able to max out on stimulus beyond what anyone would have thought possible a few years back. The US has been virtually the only country to so far pull this off and maybe the only country that might manage to do so.

Anyway back to looking at the rest of Asia this morning. Chinese equities are generally trading weaker following somewhat disappointing home price data whilst bourses are mostly mixed elsewhere. The print has done little to boost sentiment following news that home prices have dropped in 69 out of 70 cities in October relative to September and the average is now 2.6% lower versus last year. The CSI 300 is 1.1% lower as we type whilst the Hang Seng, Kospi and ASX 200 -1.0%, +1.1% and -0.2% respectively. Also in China, Bloomberg yesterday reported that the PBOC has issued rules allowing local financial institutions to invest in yuan assets abroad and in the meantime has refrained setting any limits on the amount that can be invested.

In terms of the rest of markets yesterday, with headlines dominated by Draghi it was easy to overlook what was a relatively solid expansion in the Eurozone September trade balance surplus to €17.7bn from €15.4bn in August. Over in the US the S&P 500 continued its trend of modest gains, closing +0.07% on the day. After a recent flurry of strong data, readings yesterday were fairly disappointing with misses in empire manufacturing (10.16 vs. 12 expected), industrial production (-0.1% vs. +0.2%) and capacity utilization (78.9% vs. 79.3% exp.). Elsewhere a research paper from the San Francisco Fed mentioned that inflation will remain low in the near future with the ‘probability of low inflation by the end of 2016 being twice as high as the probability of high inflation’. Just wrapping up market moves, the Dollar closed stronger on the day versus most major currencies, with the DXY +0.47% whilst both WTI and Brent extended declines, down -0.42% and -0.47% respectively.

Looking at the highlights today we will kick off with the CPI/RPI/PPI prints out of the UK. Our UK colleagues argued that the market reaction to the latest BoE November inflation report in which markets priced out the chances of an early tightening was not an appropriate response to what was said in the report. Instead they suggest that the Bank remains optimistic about economic growth despite Eurozone concerns and continues to see inflation rising back to target over the horizon forecast, supported by better wage inflation numbers. So it’ll be interesting to see how the market reacts to today’s figure. We will also be keeping an eye on the ever-important ZEW survey reading out of Germany and the Eurozone. In the afternoon our focus will cross to the other side of the pond where we will get both PPI and the NAHB housing market index reading. On the former, the market is expecting a -0.1% mom headline number. DB’s Joe Lavorgna shares the same forecast and as mentioned in yesterday’s report, notes that investors should keep a keen eye on the price data for ‘selected healthcare industries’ which is used to estimate the healthcare component of the PCE deflator. Away from the data prints, the Fed’s Kocherlakota will be speaking on monetary policy outlook this afternoon, whilst in Europe we will hear from the ECB’s Lautenschlaeger and Knot..

Japan Goes Full Helicopter-Ben: Prints “Free Gift-Cards” To Spark Consumption

Submitted by Tyler Durden on 11/17/2014 20:55 -0500

Since Ben Bernanke reminded the world of the existence of government printing-presses, echoed Milton Friedman’s “helicopter drop” solution to fighting deflation, and decried Japan for not being as insane as it could be… it has only been a matter of time before some global central bank decided that the dropping of cash onto the populace was the key to economic recovery. Having blown their wad on QQE (and been left with a triple-dip recession), it appears Japan has reached that limit. As Japan’s News47 reports, Prime Minister Shinzo Abe has instructed his cabinet to develop economic measures such as handing out ‘gift certificates’ to the poor to “support personal consumption directly.”

As Japan’s News47 reports (Via Google Translate),

Following the negative growth of the gross domestic product of the July-September period (GDP), Prime Minister Shinzo Abe is to instruct the relevant ministries to develop new economic measures whereby income is handed out, such as gift certificates to the poor and to people building energy-saving housing, thought to support the personal consumption directly.

Abe also said mitigation measures for the energy price rise due to depreciation of the yen should be included.

Prime Minister in the express policy to dissolve the House of Representatives on the 18th, economic measures is expected to become the backbone of the ruling party commitment in the House of Representatives election.

The activation of consumption stimulus and regional economy and pillars, and founded the grants that local governments can use freely.Local governments to distribute the vouchers to people with low income.

Policy to revive the “housing eco-point” to grant the point in new construction and renovation of energy-saving housing.

* * *

And so while some might liken it to EBT cards in the US… it appears this is simply a hidden way to directly hand out free money to those that spend and thus… increase inflation… So no need for firms to raise wages after all!??! Well played Abe.

end

The following is trouble as Greece cannot find 3 billion USA to plug it’s financial hole.

The risk here if we get a Greek default then all of those credit default swaps underwritten by our bankers will have to be paid and that may cause them to default themselves.

(courtesy zero hedge)

Greek Bonds Tumble As Bailout Talks Stall On $3bn Troika ‘Savings’ Demands

Can beggars be choosers again? Judging by the drop in Greek bond prices, the answer is no. As Bloomberg reports, Greek PM Samaras is pushing back againstTroika demands for up to $3 billion more savings (i.e. cuts to spending) in 2015. The impasse risks leaving Greece without a backstop on Jan. 1 after the program ends, they said. With Greece full of bravado over managing to issue debt publicly, perhaps they feel they can ignore warnings from the uberlords in Brussels. “It’s crucial that Greek authorities work with the troika to complete the current review,” but with the government in Athens refusing to concede there is a funding hole, the standoff means Greece may miss a Dec. 8 deadline for agreement on the steps required to unlock the ‘aid’ tranche.

Of course in this idiotic world, while GGBs are down over 1 pt – hovering near 9-month low prices (high yields), Greek stocks are up 3.3% today…

Greece’s government and its international creditors are deadlocked over a final round of measures required to release the last tranche of the country’s bailout, two people familiar with the negotiations said.

Prime Minister Antonis Samaras’s government is resisting pressure from the so-called troika of creditors for additional budget savings in 2015 of as much as 2.5 billion euros ($3.1 billion),said the people, who asked not to be named because the negotiations are private. The impasse risks leaving Greece without a backstop on Jan. 1 after the program ends, they said.

Troika representatives are furious because the Greek government has failed to come up with any concrete measures to plug the fiscal gap since euro-area finance ministers warned earlier this month about a lack of progress in Greece meeting its commitments, one person said. With the government in Athens refusing to concede there is a funding hole, the standoff means Greece may miss a Dec. 8 deadline for agreement on the steps required to unlock the aid and what comes after it, both said.

…

While reviews by the troika of the International Monetary Fund, the European Commission and the European Central Bank have been characterized by unforeseen twists and deadlock, the difference now is that Greece’s 144.6 billion-euro bailout program is due to expire in a matter of weeks.

…

A compromise needs to be found within hours, one of the people involved in the talks said yesterday. Failure to resume the review this week would make it impossible to complete it by Dec. 8, the person said.

* * *

Greece! again? But they are the cleanestr dirty short in Europe right? all that yummy GDP growth?

end

Eur/USA 1.2514 up .0064

USA/JAPAN YEN 116.68 up .040

GBP/USA 1.5653 up .0017

USA/CAN 1.1287 down .0009

Eur/USA 1.2514 up .0064

This morning in Europe, the euro is down, trading now well above 1.25 level at 1.2514 as Europe reacts to deflation and announcements of massive stimulation. Abe went all in with Abenomics with another round of QE purchasing 80 trillion yen from 70 trillion on Oct 31. And now he wishes to give gift cards to poor people in order to spend. The yen reversed like a yoyo last night as the world reacts to its crumbling GDP. It finally settled in Japan down 4 basis points and settling above the 116 barrier to 116.68 yen to the dollar. The pound is well up this morning as it now trades well below the 1.57 level at 1.5653.(very worried about the health of Barclays Bank and the FX/precious metals criminal investigation). The Canadian dollar is up again today trading at 1.1287 to the dollar.

Early Tuesday morning USA 10 year bond yield: 2.34% !!! up 4 in basis points from Monday night/

USA dollar index early Tuesday morning: 87.61 down 31 cents from Monday’s close

end

The NIKKEI: Tuesday morning up 370 points or 2.18% (Abe’s helicopter route to provide free cash)

Trading from Europe and Asia:

1. Europe all in the green

2/ Asian bourses all in the red except Japan / Chinese bourses: Hang Sang in the red, Shanghai in the red, Australia in the red: /Nikkei (Japan) green/India’s Sensex in the red/

Gold early morning trading: $1200.00

silver:$ 16.26

Closing Portuguese 10 year bond yield: 3.13% down 2 in basis points on the day

Closing Japanese 10 year bond yield: .51% up 3 basis point from Monday.(scary!!)

Your closing Spanish 10 year government bond Tuesday/ up 1 in basis points in yield from Monday night.

Spanish 10 year bond yield: 2.12% !!!!!!

Your Tuesday closing Italian 10 year bond yield: 2.33% / down 2 in basis points:

trading 21 basis points higher than Spain:

IMPORTANT CLOSES FOR TODAY

Closing currency crosses for Tuesday night/USA dollar index/USA 10 yr bond:

Euro/USA: 1.2530 up .0084!!!!!!

USA/Japan: 116.86 up .230

Great Britain/USA: 1.5633 down .0003 (Barclay’s in big trouble)

USA/Canada: 1.1299 up .0003

The euro rose dramatically in value during this afternoon’s session, and it was up by closing time , closing well above the 1.25 level to 1.2530. The yen was down during the afternoon session, and it lost 23 basis points on the day closing well above the 116 cross at 116.86. The British pound lost more ground during the afternoon session and it was down on the day closing at 1.5633. The Canadian dollar was down in the afternoon and was down on the day at 1.1299 to the dollar.

Currency wars at their finest today.

Your closing USA dollar index: 87. 59 down 33 cents from Monday.

your 10 year USA bond yield , up 1 in basis points on the day: 2.33%

European and Dow Jones stock index closes:

England FTSE up 37.16 or 0.56%

Paris CAC up 36.28 or 0.86%

German Dax up 150.18 or 1.61%

Spain’s Ibex up 123.90 or 1.20%

Italian FTSE-MIB up 136.21 or 0.71%

The Dow: up 40.07 or .23%

Nasdaq; down 31.44 or 0.67%

OIL: WTI 74.20 !!!!!!!

Brent: 78.37!!!!

end

And now for your big USA stories

Today’s NY trading:

Dollar Drop Sparks BTFEverything-Except-Oil Algo

From its lowest 5-day range in history and near-longest streak of closes above its short-term average, the S&P 500 broke to new record highs today (as did the Dow) above 2,050, leaving every other asset class in the dust (besides USDJPY of course). The incessant push for the stops above 117.00 dragged the S&P higher on no catalyst whatsoever. Treasury yields traded 2-3bps lower on the day (and HY credit spreads widened) in the face of equity exuberance. The USD faded on the day back to unchanged on the week on the back of EUR strength (post-Germany). Gold rallied to $1195 (+0.5% on the week) and silver rose modestly but the USD weakness did nothing for the rest of the commodity complex. Copper was whacked (after China housing data) but the big story is WTI Crude plunged again (-2% on the week) closing just shy of 4-year lows. Russell 2000 and Trannies close in the red for the week.

In summary: Stocks Up, Gold Up, Bonds Up… USD Down, Oil Down, Copper Down ahead of Fed Minutes tomorrow (credit and stocks protected).

Off the Bullard lows, the Nasdaq is now up over 14%, Dow, S&P, & Russell up around 12% and Trannies up near 18%…

Despite gains today, Trannies and Small Caps remain red on the week….

USDJPY was in charge from the US Open…

And while VIX did drop, the decoupling remains clear…

Here’s the day in VIX and S&P 500 – note the fat finger algofests…

Treasury yields and HY credit decoupled remarkedly from stocks at the US open…

And don’t forget this…

The USD fell today as EUR rallied on the back of better than expected German data

USDJPY tested up to 117.00 and reversed (twice) but Nikkei is unable to recover the post-GDP losses (yet)

Gold & Silver gained on the day (gold up for the week) but oil and copper were slammed…

As oil roundtrips once again from Friday’s gains

Charts: Bloomberg

Bonus Chart: This is the 23rd day in a row that the S&P has closed above its 5-day moving-average – nearly an all-time high in terms of sustained rallies in all of market history… (h/t MKM’s Mike Kransky)

Bonus Bonus Chart: Prior to today’s push, the 5-day closing range of the S&P is the lowest ever (at 7.7bps) – since 1928 when Bloomberg data began… (h/t @JackDamn)

end

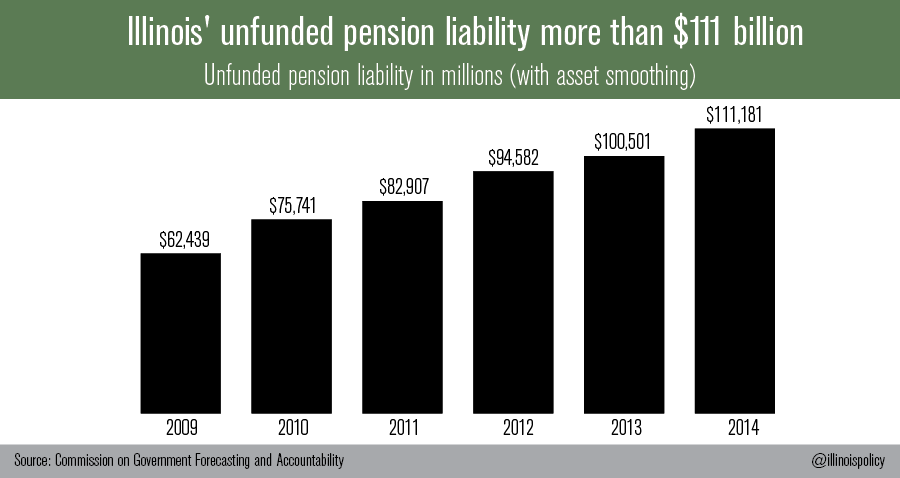

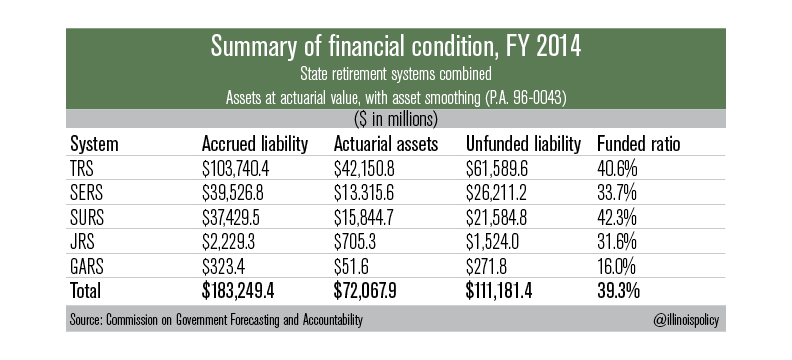

Illinois’ public pension debt soars to 111 billion from just 62 billion in 2009.

It is basically bust:

(courtesy zero hedge)

Illinois Pension Debt Soars To $111 Billion

Submitted by Tyler Durden on 11/17/2014 19:32 -0500

Authored by Benjamin VanMetre via IllinoisPolicy.org,

Pension debt in the Land of Lincoln is a big problem. So big, in fact, that it would take three years of a complete government shutdown, during which the entire general fund went toward pensions, just to break even. No funding for schools, no money for public safety and nothing for health care and human services.

Illinois’ unfunded pension liability grew to more than $111 billion this year, according to official estimates. That’s a $48 billion increase just since 2009.

That $111 billion pension shortfall means the state now has only 39 cents of every dollar it should have in the bank today to pay for future benefits. In the private sector, these funds would be deemed bankrupt.

Gov. Pat Quinn signed into law Senate Bill 1 last December, which is projected to reduce the state’s annual pension payment by more than $1 billion. But SB 1 is still bad news for Illinois. The bill may provide temporary relief, but it does nothing to fix the current defined-benefit system. And it keeps Illinois politicians in control of public-employee pension funds. Illinois’ history with politician-run pensions shows that’s a recipe for disaster.

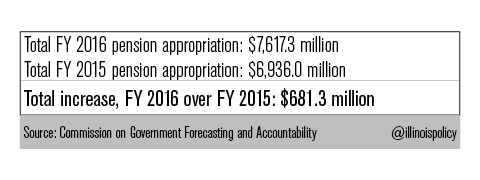

SB 1 is currently tangled up in the courts. But as we wait for a decision, Illinois’ pension debt continues to grow. The state’s pension payment for the current budget year totals $6.9 billion, and without reform, that pension payment will balloon to $7.6 billion for the 2016 budget year; an increase of $681 million.

Illinois politicians have looted and mismanaged public-employee pension funds for decades. The system is no longer sustainable or affordable. With or without SB 1, the same politicians who got the state into this mess will continue to control and abuse the retirement security of public employees.

It’s time to take politicians out of the retirement businesses.

end

The following is very worrisome!

(courtesy zero hedge)

Wholesale Inflation Heats Up Due To Jump In Car, Food Costs, New Calculation Method

Janet Yellen will be pleased, or maybe not. Producer Price Inflation printed hotter than expected across all its various incarnations (good news, no deflation; bad news, no deflation excuse for The Fed). Ex Food-and-Energy prices rose 1.8% YoY (4-month highs), considerably more than the 1.5% expectations and surged 0.4% MoM – the most in 16 months. PPI Final Demand rose 1.5% YoY (1.3% exp).

The rise in PPI appears driven by Food prices which are up 1.0% (the most since April), car prices (up 1.0%) and pharmaceuticals, but mostly thanks to a new calculation change because as the BLS reports, “In October, a 26.1-percent jump in margins for fuels and lubricants retailing accounted for nearly 40 percent of the increase in the index for final demand services.” In other words, of the 0.5% jump in PPI services, 40% was due to a new calculation for in margins for fuels and lubricants retailing.

Away from calculation-fudged services, the story was much different: prices for final demand goods moved down 0.4 percent, the worst monthly tumble in over a year.

So on one hand running hot.

Except for actual goods, which were dragged down by a whopping 3.0% plunge in energy prices, mostly thanks to gasoline.

The breakdown:

Some more details on what caused the move:

- Final demand services: The index for final demand services moved up 0.5 percent in October, the largest increase since a 0.5-percent rise in July 2013. The October advance can be traced to a 1.5-percent increase in margins for final demand trade services. (Trade indexes measure changes in margins received by wholesalers and retailers.) Prices for final demand services less trade, transportation, and warehousing inched up 0.1 percent. Conversely, the index for final demand transportation and warehousing services edged down 0.1 percent.

- Product detail: In October, a 26.1-percent jump in margins for fuels and lubricants retailing accounted for nearly 40 percent of the increase in the index for final demand services. The indexes for machinery, equipment, parts, and supplies wholesaling; food and alcohol retailing; food and alcohol wholesaling; inpatient care; and traveler accommodation services also moved higher. In contrast, prices for airline passenger services declined 0.7 percent. The indexes for loan services (partial) and for chemicals and allied products wholesaling also decreased

- Final demand goods: The index for final demand goods moved down 0.4 percent in October, the fourth consecutive decrease. The October decline was led by prices for final demand energy, which fell 3.0 percent. The index for final demand goods less foods and energy edged down 0.1 percent. Conversely, prices for final demand foods moved up 1.0 percent.

- Product detail: Over 80 percent of the October decline in prices for final demand goods can be attributed to the index for gasoline, which dropped 5.8 percent. Prices for liquefied petroleum gas, prepared animal feeds, home heating oil, diesel fuel, and ethanol also moved lower. In contrast, the index for meats increased 5.3 percent. Prices for electric power, pharmaceutical preparations, and passenger cars also advanced.

- The index for finished consumer foods rose 1.4 percent, and prices for finished goods less foods and energy edged up 0.1 percent.

And then there was the good old hedonic adjusment. As SMRA explains:

Each November the BLS includes a report on the average dollar value of quality changes for the new model year for passenger cars and light trucks. The estimate is calculated primarily from information supplied for the October PPI data.

Quality changes can include a variety of improvements such as safety features (for example, brakes, airbags or tire pressure monitors), audio systems, warranty changes, and changes in the level of standard of optional equipment.

These changes can be voluntary or mandated by law, but in either case add something to the average cost of a motor vehicle that is reflected in the PPI components.

There is no predictable pattern to how much quality changes will add to the value of motor vehicles in a model year, nor do passenger cars and light trucks have the same amount or types quality improvements each year. Due to their increased popularity and use as a passenger vehicle, light trucks, minivans, crossovers, and SUVs have generally seen more quality improvements. Upgrades tend to be related to safety, emissions, and comfort as what were once perceived as utility vehicles now serve as family cars. Since 1996, the average amount of quality improvement for passenger cars is about $120, with light trucks at about $201.

Producer prices for passenger cars have been rising more slowly than those for the light trucks category. This is an artefact of the move to motor vehicles other than passenger cars as household transportation. The popularity of SUVs, crossovers, and more traditional light trucks and minivans is reflected in firmer prices and, as noted above, enhancements to make them more like passenger cars.

However, the quality adjustment is only one factor affecting the prices for cars and trucks. Even a substantial increase in the quality adjustment may be more than offset by heavy discounting and big incentives imposed to help sales.

The best news: prices of alcoholic beverages dropped both from September (-0.4%), and a year ago (-0.3%).

end

That is all for today

I will see you Wednesday night

bye for now

Harvey,

Do you see a substantial uptick in physical silver prices before the year end?

LikeLike