My website is now ready but we still have to add a little stuff to it. You can find my site at the following url:

harveyorganblog.com or harveyorgan.wordpress.com

I will continue to send the comex data down to my good friends at the Doctorsilvers website on a continual basis.

They provide the comex data. I also provide other pertinent data that may interest you. So if you wish you can view that part on my website.

Gold: $1190.90 down $3.00

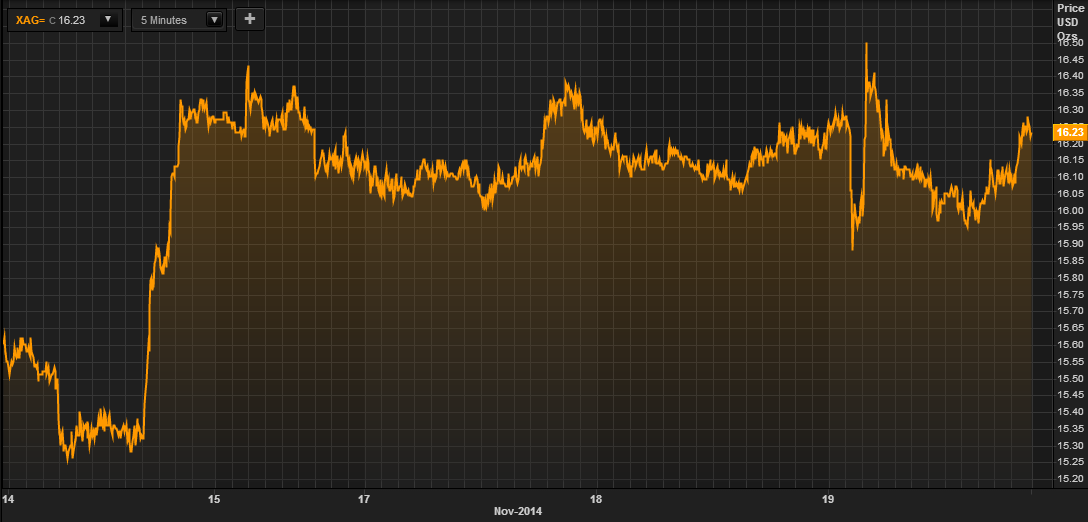

Silver: $16.13 down 16 cents

In the access market 5:15 pm

Gold $1194.30

silver $16.27

Gold and silver had a very strong day despite the antics of our bankers..

(described below)

The gold comex today had a poor delivery day, registering 0 notices served for nil oz.Silver comex registered 0 notices for nil oz.

A few months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 252.709 tonnes for a loss of 51 tonnes over that period. .

In silver, the open interest rose again despite yesterday’s loss in price ( 12 cents). It looks like we have a few nervous shorts in silver racing against the clock to cover some of their shortfall!! The total silver OI remains extremely high with today’s reading at 174,655 contracts. The big December silver OI contract lowered to 65,627 contracts. We have 5 more trading days before first day notice and our banker friends are not sleeping well these past couple of days.

In gold we had a tiny loss in OI as yesterday we saw a loss in price of gold to the tune of $3.10. The total comex gold OI rests tonight quite elevated at 459,559 for a loss of 98 contracts. The December gold OI rests tonight at 176,347 contracts which had a fairly sizable contraction of 19,736 contracts. We lost most of these paper longs rolling into February .

In trading of gold and silver today, our two precious metals were hit pretty hard in last night’s access market. I thought that we were going to have another test of 1180 dollar gold.

Right after London’s first fixing of gold (2 am est) registering $1183.00, gold swooned to $1181 upon which it said, it had enough of the bankers games and it marched northbound hitting peaks of $1195.00 at 5 am and again right now as I am writing my commentary 5 pm est tonight.

Tomorrow should be interesting:

Will we see our 3rd Friday positive outside day reversal

as the bankers defend their 1200 dollar gold turf and $16.30 for silver?

Also remember that options expiry is on Monday for comex and on next Friday for the OTC gold and silver markets.

Silver trading:

Silver fared a little better than gold. It briefly fell below $16.00 last evening and then it began its slow advance.

At 2 am (first London fix) silver was at $16.18. Attempts to knock it down failed and it hit it’s zenith at $16.33 at 5 am and right now at 5 pm it is $16.29

Today, we had no changes in tonnage of gold Inventory at the GLD / inventory rests tonight at 720.91 tonnes.

In silver, no changes:

SLV’s inventory rests tonight at 349.296 million oz.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today.

First: Most GOFO rates: move slightly towards the positive (except the one year) but remain deep in backwardation!!

Most months basically remain deep into backwardation

Now, all the months of GOFO rates( one, two, three six month GOFO and one year) moved toward the positive with the mostly used 1 to 6 month rates still negative and in backwardation. On the 22nd of September the LBMA stated that they will not publish GOFO rates. However today we still received today’s GOFO rates.

It looks to me like these rates even though negative are still fully manipulated.

London good delivery bars are still quite scarce.

The backwardation in gold is incompatible with the raid on gold . It does not make any economic sense.

Nov 20 2014

1 Month Rate: 2 Month Rate 3 Month Rate 6 month rate 1 yr rate

-.22250% -0.1525% -0.0925% – .007500% + .110%

Nov 19 .2014:

1 Month Rate 2 Month Rate 3 Month Rate 6 month Rate 1 yr rate

-.24% -.1675% -1175% -0100% +1050%

end

Let us now head over to the comex and assess trading over there today,

Here are today’s comex results:

The total gold comex open interest fell by a tiny margin of 98 contracts from 459,657 down to 459,559 with gold down by $3.10 yesterday (at the comex close). As I have stated on numerous occasions, the bankers will continue to sell non backed paper on a continual basis whereupon major entities are taking on those bankers like today. It seems to me that we now have a major entity going after gold as well as silver. The front delivery month is November and here the OI rose by 8 contracts. We had 1 delivery notices filed yesterday so we gained 9 contract or 900 additional gold ounces will stand for the November contact delivery month. The big December contract month saw it’s Oi fall by a normal 19,736 contracts down to 176,347 with the November contract moving off the board next week. Most of the selling December longs rolled into February. The estimated volume today was fair at 142,657 . The confirmed volume yesterday was huge at 315,971 with a huge assist to Bart’s HFT team.. Strangely on this 18th day of notices, we had 0 notices filed for nil oz.

And now for the wild silver comex results. The total OI surprisingly rose by a huge 1,380 contracts from 173,075 up to 174,655 despite the fact that silver was down 12 cents yesterday. It seems that judging from silver’s OI, our banker friends are now getting paranoid as they try to cover their massive shortfall in silver but to no avail as raids no longer work. In ounces, the total OI represents a total of 873 million oz or 124.7% of annual global supply. We are now in the non active silver contract month of November and here the OI remained constant at 88. We had 0 notices filed yesterday so we neither gained nor lost any silver contracts oz that will stand for the November contract month. The big December active contract month saw it’s OI fall by only 6,011 contracts down to 65,627. A normal contraction now is around 7,000 contracts per day on a roll. The December contract month remains highly elevated for this time in the delivery cycle. In ounces the December contract is represented by 328 million oz or 46.8% of annual global production (production = 700 million oz – China). The estimated volume today was poor at 31,525. The confirmed volume yesterday was atmospheric at 114,203. (and OI rises with a sizable drop in price?) We also had 0 notices filed today for nil oz.

I have been corrected on the first day notice. It will be on Friday, Nov 28.2014 the day after Thanksgiving. That will be exciting as nobody will be around.We thus have 5 more comex sessions.

Data for the November delivery month.

November initial standings

Nov 20.2014

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 48,225.000 oz (,Scotia)includes 1500 kilobars |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1 contracts(100 oz) |

| No of oz to be served (notices) | 28 contracts (2800 oz) |

| Total monthly oz gold served (contracts) so far this month | 1393 contracts (139,300 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 80,623.1 oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

613,813.6 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

total dealer deposit: nil oz

we had 1 customer withdrawal: and it was a dandy!!

i) Out of Scotia: 48,225.000 oz (exactly 1500 kilobars)

how can this be possible?

we had 0 customer deposits:

total customer deposits : nil oz

We had 0 adjustments:

Total Dealer inventory: 868,910.561 oz or 27.02 tonnes

Total gold inventory (dealer and customer) = 8.172 million oz. (252.709) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 51 tonnes have been net transferred out. We will be watching this closely!

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the November contract month, we take the total number of notices filed for the month (1393) x 100 oz to which we add the difference between the OI for the front month of November (28) – the number of gold notices filed today (0) x 100 oz = the amount of gold oz standing for the November contract month.

Thus the initial standings:

139,300 (notices filed today x 100 oz + ( 28) OI for November – 0 (no of notices filed today)= 142,100 oz or 4.419 tonnes.

We gained 900 oz of gold standing for the November contract month.

And now for silver

Nov 20/2014:

November silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | 630,404.490 oz (,Scotia, CNT,) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 88 contracts (440,000 oz) |

| Total monthly oz silver served (contracts) | 156 contracts 780,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 1,383,689.0 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 8,136,354.9 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 2 customer withdrawals:

i) Out of CNT: 600,020.68 oz

ii) Out of Scotia: 30,383.810 oz

total customer withdrawal 630,404.49 oz

We had 0 customer deposits:

total customer deposits: nil oz

we had 0 adjustments

Total dealer inventory: 64.820 million oz

Total of all silver inventory (dealer and customer) 177.699 million oz.

The total number of notices filed today is represented by 0 contract or nil oz. To calculate the number of silver ounces that will stand for delivery in November, we take the total number of notices filed for the month (156 ) x 5,000 oz to which we add the difference between the total OI for the front month of November (88) minus (the number of notices filed today (0) x 5,000 oz = the total number of silver oz standing so far in November.

Thus: 156 contracts x 5000 oz + (88) OI for the November contract month – 0 (the number of notices filed today) = amount standing or 1,220,000 oz of silver standing.

we neither gained nor lost any silver ounces standing today.

It looks like China is still in a holding pattern ready to pounce when needed.

For those wishing to see data on the currencies and bourse closings you can see it on my site at harveyorgan.wordpress.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

Nov 20.2014; no changes in tonnage of gold at the GLD/tonnage 720.91 tonnes

Nov 19.2014: we lost 2.1 tonnes of gold/Inventory back to 720.91 tonnes. No doubt physical gold is heading to China.

Nov 18.2014: no change in inventory/ Inventory level 723.01 tonnes

Nov 17.2014; we had a huge addition of 2.39 tonnes of gold added to the GLF inventory/inventory rests tonight at 723.01 tonnes. They may be running out of metal to give China!!!

Nov 14. we had no change in gold inventory at the GLD/inventory 720.62 tonnes

nov 13. we lost another 2.05 tonnes of gold at the GLD/Inventory at 720.62 tonnes

Nov 12.2014; we lost another 1.79 tonnes of gold at the GLD/Inventory at 722.67 tonnes

This gold left the shores of England and landed in Shanghai.

Nov 11.2014: we lost another 0.900 tonnes of gold at the GLD/Inventory 724.46 tonnes

Nov 10. we lost another 1.79 tonnes of gold at the GLD/Inventory 725.36 tonnes

Nov 7 wow!! we lost another huge 5.68 tonnes of gold at the GLD/inventory 727.15 tonnes

Nov 6.2014: we had another huge withdrawal of 2.99 tonnes of gold. Inventory 732.83 tonnes

This gold is also heading to Shanghai. If I was a shareholder of GLD I would be quite concerned as there will be no real gold inventory left per outstanding shares.

Nov 5 we had another huge withdrawal of 3.000 tonnes of gold. This gold will be heading to Shanghai/GLD inventory 735.82 tonnes

Today, Nov 20 no changes in tonnes of gold inventory

inventory: 720.91 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 720.91 tonnes.

It has been pointed out that John Paulson owns 13.4 million oz or 323 tonnes. He thus owns almost 45% of the entire GLD.

He is a solid supporter of gold and has so far refused to liquidate any of his gold. I am sure that this will be a problem for our bankers if they continue to sell physical gold to China as at some point the shorts will have to supply the real metal as the GLD will be void of gold along with the Bank of England.

end

And now for silver:

Nov 20.2014: no change in silver inventory at the SLV

Inventory: 349.296 million oz

Nov 19.2014: a huge addition of silver inventory to the tune of 2.396 million oz/inventory 349.296 million oz

Nov 18.2014; no change in silver inventory 346.90 million oz

Nov 17.2014 .SLV inventories remain constant tonight at 346.90 million oz

Nov 14.2014; wow!! we had an addition of 2.012 million oz into the SLV/inventory at 346.900 million oz

Nov 13. no change in silver inventory at the SLV/344.888 million oz.

Nov 12.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz. And please note that gold leaves GLD/silver does not. Why? there is no physical silver at the SLV..just paper obligations.

Nov 11.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz.

Nov 10/ we had an addition of 1.438 million oz of silver into inventory at the SLV/Inventory 344.888 million oz (again note the difference between gold and silver)

Nov 7/ 2014/no change in silver inventory/inventory rests at 343.45 million oz. (please note the difference between silver (SLV) and gold (GLD)

Nov 6.2014: no change in silver inventory/(as of 6 pm est) inventory rests at 343.45 million oz.

Nov 5 today, the total silver inventory drops of 2.074 million oz/SLV inventory: 343.45 million oz

Nov 4.2014: wow!! we had another addition of 1.151 million oz of silver inventory/SLV inventory rises to 345.524

Please note the difference between GLD and SLV. The GLD has physical gold to send on its way to Shanghai/SLV has no silver to offer to the participants to give to various players..

Nov 20.2014 no change in inventory at the SLV /349.296 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now deeply into the positive to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 9.7% percent to NAV in usa funds and Negative 9.7% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.5%

Percentage of fund in silver:38.00%

cash .5%

( Nov 20/2014)

2. Sprott silver fund (PSLV): Premium to NAV falls to positive 3.36% NAV (Nov 19/2014)

3. Sprott gold fund (PHYS): premium to NAV falls to negative -0.42% to NAV(Nov 20/2014)

Note: Sprott silver trust back hugely into positive territory at 3.36%.

Sprott physical gold trust is back in negative territory at -0.42%

Central fund of Canada’s is still in jail.

end

And now for your most important physical stories on gold and silver today:

Early gold trading from Europe early Thursday morning:

(courtesy Goldcore/Mark O’Byrne)

Ebola Remains a Risk – Deaths in Nebraska and New York

The Ebola crisis has faded from headlines but remains a risk after the death of another Ebola patient in Nebraska and the death of a suspected victim in New York yesterday. This brings the number of confirmed deaths to two in the U.S. and possibly three if the New York victim is confirmed as having had Ebola.

The toll in the Ebola epidemic has risen to 5,420 deaths out of 15,145 cases in eight countries, the World Health Organization (WHO) said today. Transmission of the deadly virus still “intense and widespread” in Sierra Leone.

The figures, through November 16, represent a jump of 243 deaths and 732 cases since those issued last Friday. Cases continue to be under-reported, the WHO said in its latest update.

Tragic scenes unfolded in Brooklyn yesterday afternoon when a woman collapsed, dead, in a salon with reports of bleeding from her mouth and nose. This is frequently how Ebola victims die as Ebola disables the body’s coagulation system, leading to uncontrolled bleeding. By the time the body can rally its second line of defense, the adaptive immune system, is frequently too late.

The unfortunate woman, who had travelled from Guinea three weeks ago and was on a watch list of the New York Health Department, showed no prior symptoms of having Ebola and was apparently being checked daily.

Her remains were collected by an emergency medical team wearing hazmat suits and the salon was later sterilized. While she is believed to have died of a suspected heart attack it seems protective measures to prevent the spread of the virus, if tests determine that Ebola was indeed the cause of death, were rather lax.

The salon remained open for business and none of the staff were decontaminated.

A death also occurred yesterday of Martin Salia, a doctor who was flown into the U.S. on Saturday for treatment. Initial tests for the virus came back negative but as his condition deteriorated he was found to have contracted Ebola.

Salia is the second person to die of Ebola in the United States. Thomas Eric Duncan, a Liberian man living in Texas, contracted the disease in his native country but was not diagnosed until after his return to Dallas.

“We are reminded today that even though this was the best possible place for a patient with this virus to be, that in the very advanced stages, even the most modern techniques that we have at our disposal are not enough to help these patients once they reach the critical threshold,” said Jeffrey Gold, chancellor of the University of Nebraska Medical Center, lamenting Salia’s death.

The latest Ebola death shows danger remains and the fact that U.S. trained doctors working in west Africa have been contracting Ebola demonstrates the virulent nature of the virus. It also contradicts the suggestion that it is the incompetence on the part of African healthcare professionals that has allowed Ebola to get out of hand.

It also suggests that the means by which Ebola spreads are not fully understood. The government of Liberia have achieved some success in bringing the epidemic under control. Public transport is rigorously monitored. Bus passengers are scanned with laser thermometers. Those with high or low temperatures are not admitted and are reported. Passengers must wash their hands upon boarding.

The statistics relating to the epidemic are difficult to interpret. In the three countries where Ebola has been most prevalent there is quite a discrepancy between the death rates of those that contract the virus.

In Guinea the death rate has been about 60%, in Sierra Leone it has been around 21% and in Liberia it has been 40%. One would expect Guinea to have the least proportion of fatalities given the dire poverty suffered by the other two nations who are emerging from civil wars.

In war-ravaged Congo the fatality rate is very high although the number of incidents has been quite low at 66.

Ebola has spread from Africa to the U.S, UK, France, Germany, Italy and Spain.

All the focus has rightly been on the medical implications and the tragic human consequences in Africa. Understandably, there has been little attention on the financial and economic consequences of a pandemic. Unless it is contained in the U.S. and Europe, it will likely soon impact consumer confidence and already fragile economic growth.

The outbreak and spread of Ebola is a worrying development and should remind people and companies, the world over, to be aware of the risks and become prepared.

A primary focus of ours is on financial and economic risk which we believe is underestimated by people, companies and governments. Our modern financial and economic systems are more complex and this more fragile than is realised.

We warned of this prior to the Irish and global financial crisis and believe there are many unappreciated financial and economic risks again today – one of which is a global pandemic.

Global economic growth remains weak and vulnerable and the global financial system remains fragile. Confidence and psychology is key.

Concerns about the Ebola virus and the likelihood of a pandemic are likely overblown. However, more cases in the western world will likely badly impact on already fragile economic confidence. This has the potential to be the straw that breaks the proverbial camel’s back with ramifications for financial markets and the global economy.

Get Breaking News and Updates On Gold Markets Here

MARKET UPDATE

Today’s AM fix was USD 1,194.00, EUR 953.60 and GBP 762.65 per ounce.

Yesterday’s AM fix was USD 1,200.75, EUR 957.61 and GBP 766.08 per ounce.

Gold prices fell $13.80 or 1.15% to $1,183.00/oz yesterday. Silver slipped $0.08 or 0.49% to $16.14/oz.

Gold in USD – 5 Days (Thomson Reuters)

Gold declined for a second day in volatile trade. The market rose following the Russian central bank gold announcement but priced were then capped in mid morning trading in London.

Some attributed the weakness to the negative gold poll in Switzerland. However, gold had fallen prior to the release of the Swiss poll and was trading below $1,180/oz and near the lows of the day at 1600 BST when the poll results were released.

The poll yesterday showed Swiss voters will likely reject an initiative that would require the nation’s central bank to boost bullion holdings. 47% percent of voters are seen as voting “no” on the Nov. 30 Swiss gold proposal and 15 percent were undecided, according to a gfs.bern poll for Swiss public broadcaster SRF. It was conducted Nov. 7 to Nov. 15 and had a margin of error of 2.7 percentage points.

Although many such polls favouring the establishment position have been very wrong in recent years.

Silver in USD – 5 Days (Thomson Reuters)

One way or another, gold and silver quickly bounced higher again. Gold retested $1,200/oz prior to further weakness set in once again in less liquid markets after the close in New York.

Besides ongoing manipulation, gold’s weakness may also be related to traders selling as the dollar remains firm and oil prices weak. For now they are ignoring the continuing ultra loose monetary policies globally and focussing on the Fed’s ‘jawboning’ and signalling that they will increase interest rates. We will believe it when we see it.

Monetary policies globally have actually become looser in recent days due to Japan’s monetary ‘bazooka’ and the threat of ‘Super Mario’s’ bazooka.

Futures trading volume on the Comex was more than double the 100-day average for this time of day, data compiled by Bloomberg show. Holdings in gold ETFs fell 1.9 metric tons to 1,616.7 tons yesterday, the lowest since May 2009 as traders and weak hands sell and gold flows to stronger hands in allocated storage and in Asia.

Senate report criticizes Goldman and JPMorgan over their roles in commodities market

By Nathaniel Popper and Peter Eavis

The New York Times

Wednesday, November 19, 2014

http://dealbook.nytimes.com//2014/11/19/senate-report-criticizes-goldman…

A two-year Senate-led investigation is throwing back the curtain on the outsize and sometimes hidden sway that Wall Street banks have gained over the markets for essential commodities like oil, aluminum, and coal.

The Senate’s Permanent Subcommittee on Investigations found that Goldman Sachs and JPMorgan Chase assumed a role of such significance in the commodities markets that it became possible for the banks to influence the prices that consumers pay while also securing inside information about the markets that could be used by the banks’ own traders.

Bankers from both firms, along with other industry executives and regulators, will testify about the allegations at hearings on Thursday and Friday.

“Regular audits, including by Goldman Sachs’ Compliance Department and third-party auditors, have identified no instances in which Metro’s confidential information has been disseminated improperly to Goldman Sachs’ sales or trading personnel,” the report said.

Until about 20 years ago, regulated banks faced tight constraints that barred them from owning physical commodities and limited them to trading in financial contracts that were linked to the prices of commodities. But a substantial relaxation of the rules allowed the banks to own actual commodities themselves — known as “physical assets” on Wall Street.

The banks’ hunger for commodities profits even led them to acquire the plants that produce and transport commodities, like coal mines and power stations. The banks still face some restrictions, though, and the report argues that Wall Street firms have moved to exploit those gray areas.

Federal Reserve rules mandate that bank holding companies cannot hold physical commodity assets that exceed 5 percent of their capital.

But the report says that JPMorgan Chase held physical commodities assets in 2012 that were equivalent to 12 percent of a measure of the bank’s capital. The bank justified this by assigning those commodities to its bank, rather than the larger bank holding company.

JPMorgan said on Wednesday that it had never gone beyond the Fed’s 5 percent limit.

One notable flashpoint occurred in 2011 when JPMorgan carried out a huge trade in aluminum that caused it to surpass a regulatory limit established by the Office of the Comptroller of the Currency.

The bank responded by shifting some of the position to an affiliate. The report asserts that the incident caused the Federal Reserve to realize for the first time that JPMorgan was not counting assets at its bank as part of the assets with the bank holding company, the entity the Fed regulates.

The Fed has been reconsidering its rules on how commodities are reported, but it so far has not objected to JPMorgan’s approach.

The Senate committee recommended some changes in its report. In particular, it said that regulators should reconsider the banking rules that relate to holding physical commodities.

The committee called on the regulators to clarify the limits on the amount of physical commodities that banks can hold. It also said action was needed to close loopholes and prevent firms from using information gained from physical commodities activities to benefit their trading in financial products.

Goldman, Glencore Found in ‘Merry-Go-Round’ Aluminum Trades

November 19, 2014 5:00 PM EST

1 Comments

1 Comments. Where did this gold go to? It is speculated the gold was “flown out” (to the U.S.?). There are also questions as to what happened to Libya’s gold after we bombed them back to the stone ages and dethroned Qadaffi. Same questions regarding Iraq and their gold. Do you see a pattern here? In the case of Sadam Hussein and Qadaffi, they both made rumblings of going to gold or silver backed currencies and presto …they are gone and so is their gold? Now, ISIS is talking about going to a gold backed dinar, who do we dethrone and where is their gold? There is one more “recent” event regarding gold. Germany asked to repatriate her gold in 2013 and doesn’t seem to be getting much of it. Only 5 tons last year of a scheduled 37. As a funny side note, if Ukraine lost 40+tons of gold …and Mr. Putin bought 55 tons over the last quarter …might some (all?) of this gold have simply come to rest a little bit further to the northeast. What is even funnier in my mind is that Mr. Putin may have bought exactly what once was Ukrainian gold and paid for it in dollars, did he not give the West something they can create freely for stolen goods of value. So in essence, Mr. Putin may have sent the US some of their dollars back for what may have been Soviet gold in the first place? Sorry, I had to put that in here because it strikes me as so ironic!

And now for the important paper stories for today:

Early Thursday morning trading from Europe/Asia

1. Stocks mixed on major Asian bourses (Hang Sang and Australia down with the rest up with a lower yen value falling to 11823

2 Nikkei up 12 points or 0.07%

3. Europe stocks all down /Euro falls/ USA dollar index up at 87.74.

3b Japan 10 year yield at .47% (Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 118.23

3c Nikkei now above 17,000

3fOil: WTI 74.46 Brent: 78.06 /all eyes are focusing on oil prices. A drop to the mid 60′s would cause major defaults.

3g/ Gold up/yen down; yen well above 118 to the dollar/at fresh 7 year lows.

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt (see Von Greyerz)

3j Japanese GDP plummets/sales tax hike will no doubt be delayed and

Snap election called. Stimulus of 26 billion usa to be initiated.

3k Chinese home sales suffer/iron ore plummets as does copper

3l: Global miss on all PMI’s

3m Gold at $1193.00 dollars/ Silver: $16.20

4. USA 10 yr treasury bond at 2.34% early this morning.

5. Details: Ransquawk, Bloomberg/Deutsceh bank Jim Reid

(courtesy zero hedge/your early morning trading from Asia and Europe)

Global Slowdown Confirmed By PMIs Missing From Japan To China To Europe; USDJPY Nears 119 Then Slides

The continuation of the two major themes witnessed over the past month continued overnight: i) the USDJPY rout accelerated, with the Yen running to within 2 pips of 119 against the dollar as Albert Edwards’ revised USDJPY target of 145 now appears just a matter of weeks not months (even though subsequent newsflow halted today’s currency decimation and the Yen has since risen 100 pips , and ii) the global economic slowdown was once again validated by global PMIs missing expectations from Japan to China (as noted earlier) and as of this morning, to Europe, where the Manufacturing, Services and Composite PMI all missed across the board, driven by a particular weakness in France (Mfg PMI down from 48.5 to 47.6, below the 48.8 expected), but mostly Germany, after Europe’s growth dynamo, which disappointed everyone after yesterday’s rebound in the Zew sentiment print, printed a PMI of only 50.0, down from 51.4 a month ago, down from 52.7 a year ago, and below the 51.5 expected.

This was driven by a tumble in New Orders from 49.8 to 47.8, which is the lowest reading since December 2012 and is the 3rd consecutive month of contraction. In other words, that Chinese import demand is just not coming back, and once again Draghi’s attempts to restart Europe’s economy by doing more of what has already failed, have failed.

This is how Goldman spun the data:

The Euro area composite PMI fell from 52.1 to 51.4 in November, against consensus expectations of a 0.3pt increase and our forecast of a flat reading (Cons: 52.3, GS: 52.1). The decline in the composite PMI was driven by a 1.0pt fall in the services component to 51.3, while the manufacturing PMI edged down 0.2pt to 50.4. The German composite PMI showed a notable large decline. The level of PMIs continues to point to small positive growth rates in Q4.

- The manufacturing PMI fell marginally from 50.6 to 50.4 in November, offsetting most of the small gain observed in October. The manufacturing PMI is down 3.6pt relative to its recent peak in January 2014. The services PMI recorded a sharper decline, falling from 52.3 to 51.3, extending its downward move to a fourth consecutive month (Exhibit 1). The consensus expectation was for small increase in both the manufacturing and services PMI.

- The breakdown showed a mixed picture. New orders fell 0.4pt but the forward-looking orders-to-stock difference rose by 0.8pt on the back of lower stocks (Exhibit 2). Other subcomponents of the manufacturing PMI sent mixed signals, with output rising 0.2pt, but employment falling 0.3pt. For services, the forward-looking subcomponents (which are not part of the headline services PMI figure) were mixed: ‘incoming new business’ fell 1.0pt, while ‘business expectations’ ticked up by 0.6pt.

- In addition to the Euro area aggregate, Flash PMIs were released for Germany and France. The German composite PMI contracted by 1.8pt to 52.1, against consensus expectations of a small increase (Cons: 54.0). This was driven by a sharp decline in both the manufacturing PMI (-1.4pt to 50.0) and services PMI (-2.4pt to 52.1). The German composite PMI has been volatile since the start of the year, but today’s weak reading drives the index back to its May 2013’s level. In contrast, the French composite PMI printed at 48.4 in November, 0.2pt above its October level. The decline in the manufacturing component (-0.9pt to 47.6) was more than offset by a 0.5pt increase in the service component (to 48.8) (Exhibit 3).

- Based on historical correlations, a reading of 51.4 is associated with +0.1%qoq GDP growth. In the same vein, our CAI points to similar growth in November (+0.2%), in line with the October reading (Exhibit 4).

As a result European equities initially opened in relatively unchanged territory following on from the neutral FOMC minutes release which failed to see participants adjust their expectations for a Fed rate hike. Thereafter, attention turned towards the slew of Eurozone PMI releases, which confirmed the global weakness previously revealed in Japan anad China. The main market-mover this morning was from Germany which saw an across the board miss for the Eurozone-heavyweight with manufacturing slipping to 50.0 and thus only narrowingly missing a contractionary reading. This subsequently saw European equities firmly slip into the red with participants beginning to question the efficacy of the ECB’s stimulus package, while fixed income products firmed alongside the softness seen in stocks. On an index specific basis for Europe, the IBEX is the notable underperformer after being weighed on by BBVA following the completion of their stock offering.

Bulletin Headline Summary from RanSquawk and Bloomberg

- Eurozone PMI figures send European equities lower after painting a particularly dreary picture of the area’s manufacturing and service sector.

- USD/JPY continued its move higher overnight as JPY remains out of favour, although failed to make a break above 119.00, while GBP found reprieve following a strong retail sales release.

- Looking ahead, attention turns towards US CPI, weekly jobs figures, manufacturing PMI, Philadelphia Fed outlook, existing home sales and any comments from Fed’s Tarullo, ECB’s Mersch and Lautenschlaeger.

- Treasuries gain as PMI reports show risk of renewed slowdown in euro area and a decline in Chinese manufacturing; U.S. CPI due today before auction of 10Y TIPS.

- HSBC/Markit’s China PMI fell to 50.0 in November, a six-month low, below the 50.2 median in a Bloomberg survey and lower than last month’s 50.4

- PBOC is considering changing the way it calculates banks’ loan-to-deposit ratios, a government official briefed on the matter said, signaling efforts to boost credit as the economy falters

- Euro-area PMI for factories and services fell to 51.4 in November, lowest in 16 months; a composite measure for Germany also declined

- U.K. retail sales rose at the fastest pace in six months in October, as prices fell 1.5% last month from a year earlier, their biggest decline since 2002

- German Foreign Minister Frank-Walter Steinmeier said mounting tensions in eastern Ukraine raised the risk of a “major military confrontation”

- Obama’s deputy national security adviser said the administration would welcome congressional authorization for U.S. military action against Islamic State with limits on duration and ground combat

- Obama will use a prime-time television speech tonight to present the biggest reprieve for undocumented immigrants in a generation, even as his order falls short of goals embraced by legislation the U.S. Senate passed last year

- If the U.K. Independence Party wins a second elected seat in Parliament today, it will be a rebuke to Conservatives and Labour, suggesting that Cameron’s promises of a referendum on EU membership and tighter rules on immigration have done nothing to win voters and that Labour isn’t the beneficiary

- Sovereign yields mostly lower. Asian stocks flat to lower. European stocks slide, U.S. equity-index futures lower. Brent crude falls, gold and copper gain

Central Banks

- 7:45am: Fed’s Tarullo speaks in New York

- 1:30pm: Fed’s Mester speaks in London

- 8:30pm: Fed’s Williams speaks in Seoul

FX

In FX markets, EUR/USD was initially provided a bid following a bout of USD weakness after USD/JPY failed to break above 119.00 which also then provided some reprieve for antipodean currencies, with AUD and NZD weighed on by declining iron ore prices and weak PPI data respectively. However, this upside for EUR was short-lived following the Eurozone PMI report which subsequently saw the USD-index pare earlier losses. Another key mover in FX markets has been GBP following the UK’s across the board stronger than expected retail sales report which saw GBP extend on yesterday’s BoE inspired gains.

COMMODITIES

Elsewhere, energy markets trade in modest negative territory while largely tracking movements in the USD-index. However, overnight saw some interesting rhetoric from the Venezuelan President Maduro, who said Venezuela is defending the oil price and fair price for oil is USD 100/bbl while the Iranian Oil Minister said ‘under no circumstance, will we reduce our global market share, even by one barrel’. In terms of price action in metals markets precious metals declined overnight as Chinese factory output appeared to stall in November, while sentiment for gold was further weakened following a poll that showed a drop in support for the Swiss referendum, nonetheless the yellow metal has seen somewhat of a rebound heading into the North American open.

* * *

DB’s Jim Reid concludes the overnight event summary in a way only he can

Before we get to the FOMC minutes and the first slightly weaker (Japan and China) PMI releases of the day there are a few interesting and potentially head scratching themes bubbling under the surface at the moment. One such theme is the continued slow but meaningful divergence in the direction of IG credit spreads in Europe and the US. US cash IG is at YTD spread wides whereas Euro cash IG at close to YTD tights. As an example European non-financial Single-As and BBBs are both about 15bps tighter in 2014 to Govt bonds. On the other hand the equivalent two US indices are 15-20bp wider with BBBs actually being about 40bps wider than the tights for the year back around the end of June (Single-As 20bp wider). We’ve put these charts in the pdf today alongside the sterling equivalent which are closer to the US in performance than the European market. So what’s going on?

Well as we’ve highlighted over the last couple of weeks the lower Oil price is seriously depressing the Energy credit sentiment in the US in both HY and IG. However Energy makes up ‘only’ 10.6% of the US IG credit index and although its the second largest sector, nearly 90% clearly isn’t in that sector. We’d also say that after discussions with our US credit strategist Oleg Melentyev, the fall in oil for now is more of a profitability issue than a credit quality issue for IG. At the moment he doesn’t even expect much in the way of IG rating actions as a result of the oil move assuming we don’t fall much further. Clearly there are risks though and the market is pricing these.

So oil is an issue in the US but it can’t explain the whole story. So is it the fear of an increasingly hawkish Fed in 2015? Well perhaps so but since the spread tights in June, 10 year USTs are around 25-30bps lower in yield and equity markets close to their all-time high so these markets aren’t that fearful. In fact after the wobble in September/October markets largely priced out a Fed hike in 2015 even if the Fed certainly haven’t (see the FOMC minutes below).

Added to this, supply has been picking up but not to unusual levels for the time of year and increasing leverage is still not a big feature of the US IG credit market. So it is likely a combination of the factors above and a perhaps simple reaction to the end of QE which may be slowly reducing liquidity and confidence from the system. However this argument would be more compelling if US equities weren’t around their all time highs. Looking at it from the opposite side of the divergence, European IG credit is close to YTD tights because of low yields, fixed income inflows, and expectations that the ECB might buy corporate and government bonds soon thus helping demand for credit and ensuring the yield environment remains lows. So perhaps QE trends are having a bigger impact on the divergence even if the conundrum continues given that European equities are little better than flat for the year. So an interesting theme and one to carry on watching. It seems unlikely that US credit can sustain itself at YTD wides while US equities are around time highs. Something will likely give.

Coming back to the FOMC yesterday, the details did little to get the market excited with the minutes indicating that most committee members support keeping rates low even after the Fed has reached its goal. Interestingly they also highlighted that the members considered removing the ‘considerable time’ language from the statement, possibly highlighting a generally more hawkish consensus stance here. However they also debated inflation and there doesn’t seem to be much certainty for the outlook here with the risks on the downside so we’ll likely to continue to be data dependant. DB’s Alan Ruskin made an interesting point yesterday. He suggested that if Oil stays where it is and other components remain in-line, the CPI could be zero in a year at the same time as the unemployment rate falls to 5%. Even if this is part right it throws up some fascinating dilemmas for policy makers.

As we mentioned, market reaction was fairly muted on the whole yesterday. The S&P 500 closed -0.15% as the small post FOMC rally was quickly repelled into the close. Treasuries were notably weaker across the curve, the 10y +3.7bps higher to 2.36% whilst the Dollar traded modestly firmer.

Looking at the day ahead, we’ve got a host of flash PMIs to look forward to. Before we preview these, we’ve already had the November manufacturing and HSBC flash prints for Japan and China respectively. The readings are fairly subdued, both China (50.0 vs. 50.2 expected) and Japan (52.1 vs. 52.7) coming in under consensus. The former has now fallen to a six month low after hitting 50.4 in October whilst on the production side the output print hit a seven month low at 49.5. However there was some positive news out of Japan, the trade data print this morning shows that exports have risen by the most in eight months in October, although no doubt helped by a weaker JPY. Just on this, as we type the Dollar has extended a seven year highs versus the JPY, trading now at 118.16 (+0.2%). In terms of market reaction in Asia, the Nikkei (+0.11%) and CSI 300 (+0.19%) are trading relatively unchanged following the PMI’s and elsewhere bourses are mostly mixed with the Hang Seng and Kospi +0.26% and -0.45% respectively.

Following this up today we’ve got the preliminary November services and manufacturing readings for the eurozone as well as regional flash prints for Germany and France. With regards to the eurozone, the market is expecting a 52.3 reading, a touch up on October’s 51.2. Meanwhile in Germany the market will likely be disappointed with anything less than 54 for the composite. It’ll be interesting to see if the numbers back up the slightly better sentiment in the market following Draghi’s comments the other day and the modestly better-than-expected Q3 GDP.

Later in the day, we will be focusing our attention back on the US with the much anticipated CPI reading. Our US colleagues are expecting a fall in the headline to -0.1% given declining energy prices which should offset further gains to food prices. They do however expect the core to round up to +0.2% on the back of rising pressure on rental costs due to a shortage of housing supply. Interestingly on this, our colleagues note that the nationwide rental vacancy rate fell to 7.4% from last quarter (from 7.5%), marking the lowest reading since Q1 1995. As a result they expect that the rising rents should keep service inflation above 2% and offset some of the weakness elsewhere in the sector – we note the importance of this factor given that shelter costs account for around 41% of overall core CPI inflation.

Just before we look at the rest of the day ahead, the FT has reported that recent polls in Switzerland show the Swiss National Bank succeeding in beating back the initiative that would force the central bank to hold at least 20% of its assets in gold ahead of the vote at the end of the month. The latest figure from Gfs Bern agency found that support for the initiative had dropped to 38% from 44% last month, with the opposition figure rising to 47%. Gold declined 1.2% yesterday following the news and is 0.3% lower this morning.

In terms of the rest of the day ahead, we’ve got a busy calendar to get through. As well as the anticipated CPI reading this afternoon in the US, we’ve also got initial claims, the Philadelphia Fed index as well October readings for existing home sales and the leading indicator in the region. Just on the latter, we’re not expecting much in the way of a market-moving event given that nearly all of subcomponents are already known. Our US colleagues point out that the current year-to-date annualized gain in the index is 6.6%, marking the fastest rate since 2004 (if we exclude the 2009 print which came off a record low base).

Before all this in Europe, away from the PMI prints we also have industrial sales and orders in Italy as well as the eurozone consumer confidence survey. In terms of data here in the UK, we’ve got the October retail sales reading and CBI trends orders. Not wanting to leave out the usual central bank speak, the ECB’s Mersch will be worth listening out for whilst Fed speakers include Tarullo and Mester speaking on liquidity and forward guidance respectively.

While hopes of the J-Curve recovery in the deficit are long forgotten in the annals of Goldman Sachs history, silver-lining-seekers will proclaim the very modest beat in tonight’s Japanese trade deficit a moral victory for a nation whose economic data has been nothing but abysmal for months. However, the near $1 trillion Yen deficit is the 44th month in a row as exports to US and Europe rose modestly in Yen terms but dropped to China and US in volume terms. USDJPY continues its march higher (now 118.25) but, unfoirtunately for Abe’s approval ratings,Japanese stocks continue to languish an implied 1000 points behind – unable to break back above pre-GDP levels... as faith in Kuroda’s omnipotence falters.

44th month in a row…

And the currency and stocks are rapidly diverging…

Charts: bloomberg

end

Chinese Manufacturing PMI hits the skids and slides to 6 month lows. China is slowing rapidly

(courtesy zero hedge)

China Manufacturing PMI Misses, Slides To 6 Month Lows

For the 13th month in a row, according to Bloomberg data, China Manufacturing PMI missed expectations. Printing at a 6-month low of 50.0 (against expectations of 50.2), the most notable individual component was theslump in output to a contractionary 49.5 reading for the first time since May. New export orders (umm US decoupling?) also dropped. It seems after last month’s idiocy (take a look at these charts for a good laugh), that Japan’s Manufacturing PMI is also catching down to reality having missed expectations and dropped to 52.1. Chinese and Japanese stocks are tumbling after this data (with Nikkei 225 200 points off US day session closing levels).

13th miss in a row, 6 month lows…

As Output and New Export Orders eased…

Not pretty…

Time to demand some moar stimulus…

“New export order growth continued to ease and led to a below-50 reading for the output sub-index for the first time since May.

Disinflationary pressures remain strong and the labour market showed further signs of weakening. Weak price pressures and low capacity utilization point to insufficient demand in the economy. Furthermore, we still see uncertainties in the months ahead from the property market and on the export front. We think growth still faces significant downward pressures, and more monetary and fiscal easing measures should be deployed.”

The reaction…

Charts: bloomberg

end

Japan again with another trade deficit to this once upon a time, huge exporter of goods:

(courtesy zero hedge)

Japanese Trade Deficit Streak Hits Record 44 Months, Yen & Stocks Decoupling

Submitted by Tyler Durden on 11/19/2014 19:08 -050

While hopes of the J-Curve recovery in the deficit are long forgotten in the annals of Goldman Sachs history, silver-lining-seekers will proclaim the very modest beat in tonight’s Japanese trade deficit a moral victory for a nation whose economic data has been nothing but abysmal for months. However, the near $1 trillion Yen deficit is the 44th month in a row as exports to US and Europe rose modestly in Yen terms but dropped to China and US in volume terms. USDJPY continues its march higher (now 118.25) but, unfoirtunately for Abe’s approval ratings,Japanese stocks continue to languish an implied 1000 points behind – unable to break back above pre-GDP levels... as faith in Kuroda’s omnipotence falters.

44th month in a row…

And the currency and stocks are rapidly diverging…

Charts: bloomberg

This Is Not Good: The Yen Is Melting Down

The yen is down 1% today vs. the $. This is a huge move in one day for any currency. The yen has lost well more than half of its value vs. the dollar since the beginning of 2012. In other words, the yen is now collapsing.

If the yen goes “super-nova” – i.e. collapses – it could bring down the U.S. The U.S. QE/Keynesian Ponzi scheme relies on Japan to help keep the scheme together. The yen is beginning to hyperinflate and it is now entering “parabolic” mode. First, this will cause the Japanese banks to implode because they’re loaded up with Japanese stocks and bonds, the way our banks are loaded with Treasuries. The banking system would not survive a yen collapse.

If the Japanese banking system collapses, it will translate into massive derivative losses and short term funding losses in the U.S. banking and hedge funds. In other words, U.S. banks have massive credit exposure risk to Japanese banks.

We’re watching the unfolding of suicidal fiat/Ponzi policy schemes for the purpose of supporting the U.S. dollar. It’s what’s going in with the latest manipulation of the yen and it’s what’s going on in the fiat paper gold and silver markets.

Perhaps the plan is to force Japan to use the dollar. But at this point the wheels are coming off the system and we are witnessing acts of desperation from the desperate criminals running our banking and political system.

What’s not being openly discussed is that Japanese citizens are buying a lot of physical gold now. I know this from a daily bullion market report we get. Soon we will start to see even more Americans move their monopoly dollars into physical. This is why the U.S. mint is now rationing silver eagles.

European Consumer Confidence Tumbles To 9 Month Lows

Despite record low bond yields and all the promises one can bear from politicians and central bankers, the people of Europe are the least confident since February. At -11.6, missing expectations of a slight improvement from -11.1 to -10.7, this is the biggest miss since August 2011. It’s perhaps not surprising given the near-record highs in unemployment but oddly, confidence seems highly correlated to EUR strength (or weakness)… the opposite of what the market hopes for.

EU Confidence at 9 month lows…

As Confidence correlates rather too strongly with a weaker EUR…

Charts: Bloomberg

Retail Rapture: UK Grocery Sales Drop 1st Time In 20 Years, Dollar General To Shut 4000 Stores

For the first time since it began collecting data in 1994,Kantar Worldpanel, the market researcher, reported a decline in UK grocery sales by value, as The FT reports the biggest UK grocers were “losing market share hand over fist,” as analysts warn “there are phoney price wars, and there are real price wars. This is a real price war.” This comes on the heels of Goldman report claiming 20% of British grocers are surplus to requirements. But it’s not just Britain… in the the cleanest dirty shirt world-economic-growth supporting decoupled economy of the USA, Reuters reports Dollar General may need to divest more than 4,000 stores to win approval from the U.S. Federal Trade Commission for its acquisition of Family Dollar.

As The FT reports, Britain’s supermarkets have suffered their first fall in sales in at least 20 years as lower food prices and a vicious price war cut the amount customers spend on groceries.

For the first time since it began collecting data in 1994, Kantar Worldpanel, the market researcher, reported a decline in UK grocery sales by value.

“There are phoney price wars, and there are real price wars. This is a real price war,” said Fraser McKevitt, head of retail and consumer insight at Kantar Worldpanel.

…

Britain’s big chains have pledged to spend billions of pounds cutting prices in an effort tostem the growth of German discounters Aldi and Lidl.

…

On Monday, research from Goldman Sachs said 20 per cent of UK supermarket space was surplus to requirements following the rise of discounters including Aldi and Lidl, the demise of the weekly shop and the increase in online grocery shopping.

But it’s not just Britain that faces retail pressure… (as Reuters reports)

Dollar General may need to divest more than 4,000 stores to win approval from the U.S. Federal Trade Commission for its acquisition of Family Dollar Stores, theNew York Post reported, citing two sources close to the situation.

Dollar General has agreed to sell up to 1,500 stores as part of its $9.1 billion offer. It approached Family Dollar shareholders with its offer directly in September after twice being spurned by its smaller rival.

The New York Post reported on Wednesday that Dollar General could be forced either to raise its bid again or to divest more than double the number of stores previously pledged.

Synergies?

* * *

But apart from that…escape velocity here we come.

end

from Greece today:

Greece:

Greece will table budget without approval from the troika: Ekathimerini reported that Greek Finance Minister Hardouvelis is set to table the final draft of the 2015 budget in Parliament on Friday without having secured the approval of the country’s creditors. It said the numbers will be based on the midterm fiscal plan agreed by Athens and the troika. It noted that the representatives of the country’s three creditors – the European Commission, the ECB and the IMF – are for now sticking with their estimate for a fiscal gap next year that could reach up to €3.6B, which the government has rejected. It added that the troika is unlikely to budge on its estimates and the most likely outcome is it would let a few months pass to see which side was right. It said If there is a shortfall then a supplementary budget could be tabled.

end

Eur/USA 1.2533 down .0021

USA/JAPAN YEN 118.23 up .260

GBP/USA 1.5679 down .0003

USA/CAN 1.1330 down .0011

This morning in Europe, the euro is down, trading now just above 1.25 level at 1.2533 as Europe reacts to deflation and announcements of massive stimulation and crumbling bourses. Abe went all in with Abenomics with another round of QE purchasing 80 trillion yen from 70 trillion on Oct 31. And now he wishes to give gift cards to poor people in order to spend. The yen reversed like a yoyo last night as the world reacts to its crumbling GDP. It finally settled in Japan down 70 basis points and settling above the 118 barrier to 118.23 yen to the dollar (heading towards 120). The pound is slightly down this morning as it now trades well below the 1.57 level at 1.5679.(very worried about the health of Barclays Bank and the FX/precious metals criminal investigation). The Canadian dollar is up again today trading at 1.1330 to the dollar.

Early Thursday morning USA 10 year bond yield: 2.32% !!! down 4 in basis points from Wednesday night/

USA dollar index early Thursday morning: 87.74 up 10 cents from Wednesday’s close

end

The NIKKEI: Thursday morning up 12 points or 0.07% (Abe’s helicopter route to provide free cash)

Trading from Europe and Asia:

1. Europe all in the red

2/ Asian bourses all in the green except Hang Sang and Australia / Chinese bourses: Hang Sang in the red, Shanghai in the green, Australia in the red: /Nikkei (Japan) green/India’s Sensex in the green/

Gold early morning trading: $1193.00

silver:$ 16.20

Closing Portuguese 10 year bond yield: 3.13% par in basis points on the day

Closing Japanese 10 year bond yield: .47% down 4 basis point from Wednesday

Your closing Spanish 10 year government bond Thursday/ down 3 in basis points in yield from Wednesday night.

Spanish 10 year bond yield: 2.10% !!!!!!

Your Wednesday closing Italian 10 year bond yield: 2.31% down 2 in basis points:

trading 21 basis points higher than Spain:

IMPORTANT CLOSES FOR TODAY

Closing currency crosses for Thursday night/USA dollar index/USA 10 yr bond:

Euro/USA: 1.2548 up .0008

USA/Japan: 118.00 down .1300 !!!!

Great Britain/USA: 1.5695 up .0013

USA/Canada: 1.1303 up .0009

The euro rose nicely in value during this afternoon’s session, and it was up by closing time , closing well above the 1.25 level to 1.2548. The yen was up badly during the afternoon session, and it gained 13 basis points on the day closing at the 118 cross at 118.00. The British pound gained back more ground during the afternoon session and it was up on the day closing at 1.5695. The Canadian dollar was up in the afternoon but was up on the day at 1.1303 to the dollar.

Currency wars at their finest today.

Your closing USA dollar index: 87. 58 down 7 cents from Wednesday.

your 10 year USA bond yield , up 1 in basis points on the day: 2.33%

European and Dow Jones stock index closes:

England FTSE down 17.70 or 0.26%

Paris CAC down 31.98 or 0.75%

German Dax up 11.17 or 0.12%

Spain’s Ibex down 167.60 or 1.62%

Italian FTSE-MIB down 170.60.07 or 0.88%

The Dow: up 33.27 or .19%

Nasdaq; up 26.16 or 0.56%

OIL: WTI 75.58 !!!!!!!

Brent: 79.20!!!!

end

And now for your big USA stories

Today’s NY trading:

(courtesy zero hedge)

Stocks Up, Bonds Up, Gold Up, Oil Up, USD Up… Give Up?

For the 25th day in a row (one short of an all-time record), the S&P closed above its 5-day moving-average. Despite dismal Asian, European, and US PMIs, US equity markets sreaked higher at the US Open, tagging yesterday’s highs, then stalling when Europe closed. Small Caps led the day as shorts were squeezed once again butTrannies and Russell 2000 remain negative on the week. US Treasury yields dropped notably after European and ended the day 2-3bps lower (with 30Y unch on the week). The USD rose very modestly close-to-cvlose but traded lower thru the EU and US sessions (AUDJPY was in charge of stocks today). Copper dropped on China growth fears but oil, silver, and gold rose on the day (leaving gold +0.5% on the week). HY credit slammed tighter with stocks early then decoupled after EU closed.Dow & S&P close at record highs.

It’s OPEX tomorrow…

25 in a row.. and counting…

Small Caps led the day…

As shorts got squeezed ouit of the gate

Trannies and Russell remain red on the week despite today’s big surge in small caps…

USDJPY gave up at the US open and AUDJPY took over

Treasury yields and HY credit once again decoupled…

VIX’s opening hour was insanely spotted with fat finger mnanipulations… ramped then rose into the close

FX markets saw the USD flat but USDJPY roundtriup back to 118.00

Treasury yields saw volatility today but closed lower with 30Y practically unch on the week

Copper dropped (China weakness) but oil, gold, and silver rose on the day pulling gold green on the week

Gold rallied all the way back up to the pre-Swiss Gold Poll results yesterday…

Charts: Bloomberg

end

The huge USA manufacturing PMI misses the most on record and it is the lowest since January.

Good reason for the Dow to continue to advance:

(courtesy zero hedge)

US Manufacturing PMI Misses By Most On Record, Lowest Since January

Recovery, we have a problem… November’s Flash US Manufacturing PMI printed a 10-month lows 54.7, missing expectation sof 56.3 by the most on record and tumbling for the third month in a row. The last 2 mnths have seen the biggest drop since June 2013 ands as Markit notes, suggests a further drop in GDP growth expectations of only 2.5% in Q4. Output is down for the 3rd straight month and Surprise!! Export market weakness is being blamed… as it seems the US cannot decouple from the rest of the world’s slump after all and is – as we have explained numerous times – merely on a lagged cycle.

10-month lows…

“The manufacturing sector is undergoing a marked slowdown in the fall after enjoying a buoyant summer.

Output growth has now fallen for three straight months, taking the pace of expansion down to its lowest since the start of the year. Unlike January, however, this time the weaker rate of growth can’t be blamed on the weather.

Export market weakness holds the key to the recent slowdown, with manufacturers reporting the largest drop in export orders for nearly one and a half years.

“There’s some reassurance from manufacturers continuing to boost their payroll numbers at a robust pace, but with backlogs of work showing almost no growth, the rate of job creation looks likely to moderate in coming months unless new order inflows pick up again.

“The manufacturing and service sector PMI data available so far point to GDP growth slowing to around 2.5% in the fourth quarter.”

* * *

So – in summary – China PMI is at 6-month low, Europe at 16-month low, Japan dropped and is in a quadruple-dip recession, and now US manufacturing is at 10-month low… seems like QE really worked eh!?

* * *

We’re gonna need more Fed-fueled subprime-auto-loan malarkey to keep this dream alive.

end

Another huge story today:

The Latest Scandal: Goldman, Fed Employees Busted For Illegally Sharing Confidential Information

On the morning of Friday, September 26, in addition to the shocking news of Bill Gross’ departure from Pimco, the world was just as shocked, or not as the case was for many, that a former NY Fed staffer, Carmen Segarra, who had been previously fired for suggesting that Goldman Sachs has an undue influence on the NY Fed and gets a preferential treatment (certainly as a result of NY Fed’s president Bill Dudley being working previously at Goldman Sachs), had released nearly 50 hours of tapes confirming her allegations: that the NY Fed was nothing but a branch of the bank that controls every central bank. The full details were presented in “How Goldman Controls The New York Fed: 47.5 Hours Of “The Secret Goldman Sachs Tapes” Explain.”

Ironically it was on that very day that another recent Goldman hire from the NY Fed – a classic case of, as the NY Times puts it, the “revolving door, the symbolic portal that connects financial regulators to Wall Street” – a 29-year-old former New York Fed regulator named Rohit Bansal, got into hot water after something “shocking” was revealed: he had an inside source at the NY Fed who was providing him with illegal, confidential information on a regular basis.

Here is William Dudley, formerly of Goldman Sachs and president

of the New York Fed, saying “I don’t think anyone should question

our motives.” It may have been an order.

As Bloomberg notes, following the re-escalation of the Segarra scandal, Bansal was promptly fired. Of course, had Carmen not revealed to the world just how extensive Goldman’s domination of the NY Fed is, as Bansal’s action demonstrated, he would still be fed confidential information from the New York Fed itself.

The banker, who had joined the company in July from the New York Fed, was dismissed a week after the discovery in late September along with another employee who failed to escalate the issue, according to an internal memo obtained by Bloomberg News that didn’t identify the pair. Jake Siewert, a bank spokesman, confirmed the contents of the memo, which was prompted by a report in the New York Times yesterday.

“We have zero tolerance for improper handling of confidential information,” New York-based Goldman Sachs said in the memo. “We are reviewing our policies regarding any hiring from governmental institutions to ensure that they are appropriately effective and robust.”

Wrong: what Goldman has zero tolerance for is having its bankers getting caught, or its manipulative action exposed to the general public, as took place on September 26. Once that happens, one or two bankers are shown the door, while the law-breaking culture continues unabated.

According to the NY Times, which broke the story, this is what happened:

From his desk in Lower Manhattan, a banker at Goldman Sachs thumbed through confidential documents — courtesy of a source inside the United States government.

The banker came to Goldman through the so-called revolving door, the symbolic portal that connects financial regulators to Wall Street. He joined in July after spending seven years as a regulator at the Federal Reserve Bank of New York, the government’s front line in overseeing the financial industry. He received the confidential information, lawyers briefed on the matter suspect, from a former colleague who was still working at the New York Fed.

As a reminder, the NY Fed is also the world’s biggest hegde fund, as it is the place where, at Liberty 33, the Fed’s market moving operations are executed. It is also where the legendary PPT is located. Continuing:

The previously unreported leak, recounted in interviews with the lawyers briefed on the matter who spoke anonymously because the episode is not public, illustrates the blurred lines between Wall Street and the government — and the potential conflicts of interest that can result. When Goldman hired the former New York Fed regulator, who is 29, it assigned him to advise the same type of banks that he once policed. And the banker obtained confidential information, along with several publicly available facts, in the course of assignments from his bosses at Goldman, the lawyers said.

What exactly data was one current NY Fed staffer leaking to a former NY Fed staffer, currently working at Goldman?

The information provided Goldman a window into the New York Fed’s private insights, the lawyers said, including details about at least one of Goldman’s clients, a midsize bank regulated by the Fed. Although it is unclear how Goldman bankers used the information, if at all, the confidential details could have helped them advise the client.

Because if you are not a part of the club, Goldman will chew you up and spit you out, courtesy of confidential NY Fed information.

Naturally, “the emergence of the leak comes as questions mount about a perceived coziness between the New York Fed and Wall Street banks — Goldman in particular. Revelations from a former New York Fed employee, Carmen Segarra, recently stoked that debate. Ms. Segarra released taped conversations suggesting that her supervisors went soft on Goldman, specifically over a deal that one regulator called “legal, but shady.””

What questions? Goldman controls the NY Fed, period, the end. For the NYT the conclusion is a little more roundabout: “The leak strikes at the heart of questions about the ability of the New York Fed — the public’s eyes and ears on Wall Street — to maintain its independence from the banks it regulates. It also comes as a popular image of Goldman as a bank that puts profit above all has begun to fade.”

Which is precisely what Goldman wanted: keeping a low profile while changing absolutely nothing about its corrupt culture, a culture which is enabled by its very regulators who are captured courtesy of former Goldman employees being placed at strategic top posts. It really isn’t rocket science.

And the biggest irony is that Bansal’s illegal abuse of confidential NY Fed data only was noticed for the first time… when Carmen Segarra’s allegations hit the public for the second time on September 26 as noted above:

At the request of his bosses, Mr. Bansal gathered information about how regulators might view various issues facing Goldman’s banking clients, the lawyers briefed on the matter said. Much of what Mr. Bansal learned, the lawyers said, was fair game.

But in an email to his supervisor, Joseph Jiampietro, Mr. Bansal shared some potentially confidential supervisory information about a Goldman banking client. Mr. Jiampietro — a managing director at Goldman who was once a senior adviser to Sheila Bair, the former F.D.I.C. head — has since told colleagues he had no idea the information was subject to regulatory restrictions.

“Mr. Jiampietro never knowingly or improperly reviewed or misused” confidential supervisory information, his lawyer, Adam Ford, said in a statement. “He should not have been terminated. Any compliance failings regarding Mr. Bansal had nothing to do with Mr. Jiampietro.”

It was not until the morning of Sept. 26 that Goldman executives objected to some of Mr. Bansal’s information, the lawyers briefed on the matter said. During a conference call with Mr. Jiampietro and two higher-ranking Goldman executives, Mr. Bansal circulated an email with a spreadsheet attached. The email apparently set off alarms within Goldman. Within hours, the bank opened an internal investigation and alerted the New York Fed.

Goldman determined that the spreadsheet contained confidential bank supervisory information. Federal and state rules classify certain records, including those generated during bank exams, as confidential. Unless the Federal Reserve provides special approval, it can be a federal crime to share them outside the Fed.

Of course, had the Segarra story not resurfaced, Bansal would still be at Goldman.

As for the leaker at the NY Fed, we know this: “Some of Mr. Bansal’s information, the lawyers said, may have come from Jason Gross, who worked at the New York Fed at the time.”

This guy: a bank examiner, and formerly a controller at Deutsche Bank, a person interested in “pro-bono consulting.” We already know Bansal is one of Gross’ connections. Who are the other 10, and how soon until all his connections “unfriend” him?

It appears Gross is no longer at the NY Fed either: “Andrea Priest, a spokeswoman for the New York Fed, didn’t immediately respond to an e-mail seeking comment on the dismissed Goldman Sachs workers after normal business hours. The regulator also fired an employee it suspected of sharing information with the banker, the New York Times reported. In a statement to the paper, the New York Fed said it has “zero tolerance” for personnel who don’t safeguard confidential information.”

What happens next? Tomorrow, Senator Sherrod Brown, an Ohio Democrat, has scheduled a hearing before his banking subcommittee on “regulatory capture” following Segarra’s claims.

There will be much posturing, and lots of angry words, because clearly Mr. Brown did not get enough financial support from the “Business Services” industry. After all he too would prefer millions more in bribes, pardon, lobby spending from Goldman et al.

Will anything change? Of course not. After all it is Goldman that runs the United States of America. Expect this latest scandal to be swept under the rug within days.

The NY Fed’s Attempt To Explain That It Is Not A Subsidiary Of Goldman Sachs

Submitted by Tyler Durden on 11/20/2014 15:18 -0500

The most shocking, if already completely buried, news of the day was that – in yet another confirmation that Goldman Sachs is in charge of the New York Fed – a NY Fed staffer was colluding and leaking confidential, material information to a 29-year-old Goldman vice president, himself a former Federal Reserve employee. This only happened because on the day Carmen Segarra disclosed her 47 hours of “secret Goldman tapes” on This American Life, Goldman executives asked the former Fed staffer where he had gotten what appeared to be confidential information from. To nobody’s surprise the answer was: The New York Fed.

So as the latter, also known as the biggest hedge fund of the western world with $2.7 trillion in AUM, is scrambling to once again prove it is shocked, shocked, that it has become merely the latest subsidiary of Goldman Sachs, Inc., it released the following statement explaining what “really” happened.

From the NY Fed:

As soon as we learned that Goldman Sachs suspected one of its employees may have inappropriately obtained confidential supervisory information, we alerted law enforcement authorities. We have been working with law enforcement authorities since then. Because any public statement about the investigation could be prejudicial to a potential future criminal case, we are unable to comment on the specific facts that are under investigation.

As a general matter, we have detailed rules and controls protecting confidential information. All employees with access to confidential supervisory information need to agree to safeguard that information appropriately, and not to disclose it without the necessary approval. Employees receive training relating to the handling and protection of confidential supervisory information and other information security matters. Employees are informed that a violation of these restrictions could lead to criminal prosecution.

Employees also receive ongoing ethics training and are required to do an annual certification that they understand and will adhere to the Bank’s Code of Conduct. In addition, we use off-boarding procedures to confirm with departing employees that no confidential information may be taken. With respect to all New York Fed staff, departing Officers may have no official contact with the Federal Reserve System for a period of one year. In addition, all departing New York Fed employees may not have substantive business contacts with the New York Fed relating to any particular matter that he or she had worked on when employed by the New York Fed. Further, with respect to employees departing from the financial institution supervision group, if the departing employee had served as a senior supervisory officer or central point of contact at a large and complex banking organization, that employee may not receive compensation from the supervised organization as an employee, officer, director or consultant for a period of one year. Finally, the New York Fed has in place technology to help identify and prevent the forwarding of confidential information in violation of our rules.

So did this technology fail? Or is Goldman simply one of the exempted parties?