My website is now ready but we still have to add a little stuff to it. You can find my site at the following url:

http://www.harveyorganblog.com or www .harveyorgan.wordpress.com

I will continue to send the comex data down to my good friends at the Doctorsilvers website on a continual basis.

They provide the comex data. I also provide other pertinent data that may interest you. So if you wish you can view that part on my website.

Gold: $1195.50 down $2.00

Silver: $16.38 down 2 cents

In the access market 5:15 pm

Gold $1198.00

silver $16.50

Gold and silver had a good day despite the antics of our bankers due to options expiry

(described below)

The gold comex today had a fair delivery day, registering 4 notices served for 400 oz. Silver comex registered 0 notices for nil oz.

A few months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 247.44 tonnes for a loss of 56 tonnes over that period. .

In silver, the open interest fell slightly despite Friday’s rise in price ( 26 cents). It looks like we have a few nervous shorts in silver racing against the clock to cover some of their shortfall!! The total silver OI remains extremely high with today’s reading at 174,893 contracts. The big December silver OI contract lowered by only 7,634 contracts down to 54,129 contracts. We have 3 more trading days before first day notice and our banker friends are not sleeping well these past couple of days.

In gold we had a good gain in OI as Friday saw a gain in price of gold to the tune of $6.80. The total comex gold OI rests tonight quite elevated at 468,748 for a gain of 697 contracts. The December gold OI rests tonight at 149,255 contracts. We witnessed a subnormal contraction of 13,254 contracts. We lost most of these paper longs into February as these fellows wished to keep the paper game alive .

TRADING OF GOLD AND SILVER TODAY

GOLD

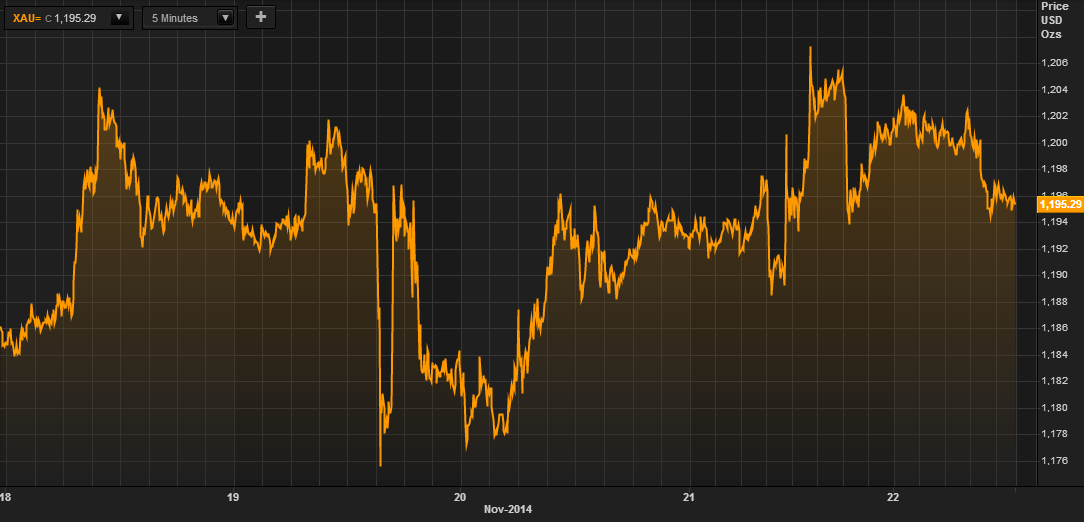

In trading of gold and silver today, our two precious metals were doing nicely in the Asian trading zone last night. It hit its high spot right at London’s first fixing of gold (2 am est), with our ancient metal of kings registering a fix of $1202.75. Gold then swooned to $1194, its nadir for the day at 8 am just prior to comex opening. It is obvious that this being options expiry day had a lot to do with trading today. Gold again advanced and hit $1200.00 as we hit the second London gold fix.

From that point until comex closing gold just meandered around and finally finishing at the above closing price.

Silver:

Silver performed much better than gold during last night’s trading. By London’s first fix the price of silver had already reached $16.45.(same fix as yesterday) The bankers would have no part of silver’s advance so they whacked it all the way down to $16.29, its nadir by 4 am. From there it was one steady climb whereupon silver hit its zenith at $16.50 close to 10 am (the second London fix). In sympathy to gold, silver was hit again by the criminal bankers once London was put to bed. However this time, silver behaved much better and finished at $16.47

Remember that options expiry for comex is over today but we still have options expiry for the OTC gold this Friday.

Today, we had no changes in tonnage of gold Inventory at the GLD / inventory rests tonight at 720.91 tonnes.

In silver, no changes:

SLV’s inventory rests tonight at 349.296 million oz.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today.

OH OH!!!

First: GOFO rates:

all rates move again deeper into the negative and thus deeper into backwardation!!

Now, all the months of GOFO rates( one, two, three six month GOFO and one year) moved toward the negative with the mostly used 1 to 6 month rates deeper into the negative and thus in backwardation Even the one year rate is closing in on backwardation. On the 22nd of September the LBMA stated that they will not publish GOFO rates. However today we still received today’s GOFO rates.

It looks to me like these rates even though negative are still fully manipulated.

London good delivery bars are still quite scarce.

The backwardation in gold is incompatible with the raid on gold . It does not make any economic sense.

Nov 24 2014

1 Month Rate: 2 Month Rate 3 Month Rate 6 month rate 1 yr rate

-.25250% -0.1975% -0.1275% – .037500% + .0900%

Nov 21 .2014:

1 Month Rate 2 Month Rate 3 Month Rate 6 month Rate 1 yr rate

-.2450% -.1725% -.1125% -02500% +10250%

end

Let us now head over to the comex and assess trading over there today,

Here are today’s comex results:

The total gold comex open interest rose by a small margin of 697 contracts from 468,051 all the way to 468,748 with gold up by $6.80 on Friday (at the comex close). As I have stated on numerous occasions, the bankers will continue to sell non backed paper on a continual basis whereupon major entities are taking on those bankers like today. It seems to me that we now have a major entity going after gold as well as silver. The front delivery month is November and here the OI lowered from 28 contracts down to 20 for a loss of 8. We had 0 delivery notices filed on Friday so we lost 8 gold contacts or 800 additional ounces will not stand for the November delivery month. The big December contract month saw it’s Oi fall by a subnormal 13,254 contracts down to 149,255 with the November contract moving off the board today. All of the selling December longs rolled into February. The estimated volume today was poor at 129,609 when you consider many had to roll . Something serious is happening inside the comex vaults. The confirmed volume on Friday was excellent at 244,522 with a huge assist to Bart’s HFT team and the many rollovers. On this 20th day of notices, we had 4 notices filed for 400 oz.

And now for the wild silver comex results. The total OI fell by a slight 1,630 contracts from 176,523 falling to 174,893 despite the fact that silver was up 26 cents on Friday. It seems that judging from silver’s OI, our banker friends are now getting paranoid as they try to cover their massive shortfall in silver but to no avail as raids no longer work. In ounces, the total OI represents a total of 874 million oz or 124.9% of annual global supply. We are now in the non active silver contract month of November and here the OI remained constant at 88. We had 0 notices filed yesterday so we neither gained nor lost any silver contracts oz that will stand for the November contract month. The big December active contract month saw it’s OI fall by a subnormal 7,634 contracts down to 54,129. A normal contraction now is around 9000-10,000 contracts per day on a roll. The December contract month remains highly elevated for this time in the delivery cycle. In ounces the December contract is represented by 270 million oz or 38.6% of annual global production (production = 700 million oz – China). The estimated volume today was fair at 41,345. The confirmed volume on Friday was humongous at 100,689.(and yet no massive rolls into March?) We also had 0 notices filed today for nil oz.

The first day notice for both metals will be on Friday, Nov 28.2014 the day after Thanksgiving. Options expiry as mentioned above is today. We thus have 3 more comex sessions.

Data for the November delivery month.

November initial standings

Nov 24.2014

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 6,028.800 oz (,Scotia,Manfra)includes 2 kilobars |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 4 contracts(400 oz) |

| No of oz to be served (notices) | 16 contracts (1600 oz) |

| Total monthly oz gold served (contracts) so far this month | 1413 contracts (141,300 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 80,623.1 oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

783,166.9 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

total dealer deposit: nil oz

we had 2 customer withdrawal:

i) Out of Scotia: 5,964.500 oz (we have been witnessing this lately..suppose to be to 3 decimals)

ii) Out of Manfra: 64.30 oz (2 kilobars)

total withdrawal: 6028.800 oz

we had 0 customer deposits:

total customer deposits : nil oz

We had 0 adjustments:

Total Dealer inventory: 868,910.561 oz or 27.02 tonnes

Total gold inventory (dealer and customer) = 7.955 million oz. (247.44) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 56 tonnes have been net transferred out. We will be watching this closely!

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 4 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the November contract month, we take the total number of notices filed for the month (1413) x 100 oz to which we add the difference between the OI for the front month of November (20) – the number of gold notices filed today (4) x 100 oz = the amount of gold oz standing for the November contract month.

Thus the initial standings:

141,300 (notices filed today x 100 oz + ( 20) OI for November – 4 (no of notices filed today)= 141,300 oz standing for the November contract month.(4.395 tonnes)

we lost 800 oz of gold standing for the November contract month.

And now for silver

Nov 24/2014:

November silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | 387,118.414 oz (CNT,Delaware,Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 96,672.600 oz (CNT) |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 88 contracts (440,000 oz) |

| Total monthly oz silver served (contracts) | 156 contracts 780,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 1,383,689.0 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 8,812,053.8 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 3 customer withdrawals:

i) Out of CNT: 60,094.900 oz (lately we have been having figures to one decimal place)

ii) Out of Delaware: 15,426.794 oz

iii) Out of Scotia: 311,596.720 oz

total customer withdrawal 387,118.414 oz

We had 1 customer deposits:

i) Into CNT; 96,672.600 oz

total customer deposits: 96,672.600 oz

we had 0 adjustment

Total dealer inventory: 64.899 million oz

Total of all silver inventory (dealer and customer) 177.346 million oz.

The total number of notices filed today is represented by 0 contract or nil oz. To calculate the number of silver ounces that will stand for delivery in November, we take the total number of notices filed for the month (156 ) x 5,000 oz to which we add the difference between the total OI for the front month of November (88) minus (the number of notices filed today (0) x 5,000 oz = the total number of silver oz standing so far in November.

Thus: 156 contracts x 5000 oz + (88) OI for the November contract month – 0 (the number of notices filed today) = amount standing or 1,220,000 oz of silver standing.

we neither gained nor lost any silver ounces standing today.

It looks like China is still in a holding pattern ready to pounce when needed.

For those wishing to see data on the currencies and bourse closings you can see it on my site at http://www.harveyorgan.wordpress.com or http://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

Nov 24.2015: no change in tonnage of gold inventory at the GLD/inventory at 720.91 tonnes

Nov 21.2014: no change in tonnage of gold inventory at the GLD/inventory 720.91 tonnes

Nov 20.2014; no changes in tonnage of gold at the GLD/tonnage 720.91 tonnes

Nov 19.2014: we lost 2.1 tonnes of gold/Inventory back to 720.91 tonnes. No doubt physical gold is heading to China.

Nov 18.2014: no change in inventory/ Inventory level 723.01 tonnes

Nov 17.2014; we had a huge addition of 2.39 tonnes of gold added to the GLF inventory/inventory rests tonight at 723.01 tonnes. They may be running out of metal to give China!!!

Nov 14. we had no change in gold inventory at the GLD/inventory 720.62 tonnes

nov 13. we lost another 2.05 tonnes of gold at the GLD/Inventory at 720.62 tonnes

Nov 12.2014; we lost another 1.79 tonnes of gold at the GLD/Inventory at 722.67 tonnes

This gold left the shores of England and landed in Shanghai.

Today, Nov 24 no changes in tonnes of gold inventory

inventory: 720.91 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 720.91 tonnes.

end

And now for silver:

Nov 24.2014: no change in silver inventory at the SLV/Inventory 349.296 million oz

Nov 21.2014: no change in silver inventory at the SLV

Inventory: 349.296 million oz

Nov 20.2014; no change/inventory 349.296 million oz

Nov 19.2014: a huge addition of silver inventory to the tune of 2.396 million oz/inventory 349.296 million oz

Nov 18.2014; no change in silver inventory 346.90 million oz

Nov 17.2014 .SLV inventories remain constant tonight at 346.90 million oz

Nov 14.2014; wow!! we had an addition of 2.012 million oz into the SLV/inventory at 346.900 million oz

Nov 13. no change in silver inventory at the SLV/344.888 million oz.

Nov 12.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz. And please note that gold leaves GLD/silver does not. Why? there is no physical silver at the SLV..just paper obligations.

Nov 11.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz.

Nov 24.2014 no change in inventory at the SLV /349.296 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now deeply into the positive to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 10.3% percent to NAV in usa funds and Negative 10.4% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.4%

Percentage of fund in silver:38.00%

cash .6%

( Nov 24/2014)

2. Sprott silver fund (PSLV): Premium to NAV falls to positive 2.42% NAV (Nov 24/2014)

3. Sprott gold fund (PHYS): premium to NAV rises to negative -0.48% to NAV(Nov 24/2014)

Note: Sprott silver trust back hugely into positive territory at 2.42%.

Sprott physical gold trust is back in negative territory at -0.48%

Central fund of Canada’s is still in jail.

end

And now for your most important physical stories on gold and silver today:

Early gold trading from Europe early Friday morning:

O’Byrne comments on the 122 tonnes of repatriation.

Also Bill Holter gives an astounding commentary on the repatriation plus other important details that you must read..

(courtesy Goldcore/Mark O’Byrne)

122 Tonnes of Gold Secretly Repatriated to Netherlands

The Dutch central bank said Friday it is repatriating some of its gold reserves from the U.S., making it the latest central bank in Europe to address public concerns about the safety of its gold in the wake of the eurozone debt crisis.

As the debate regarding whether or not Switzerland should keep the bulk of its gold reserves at home on Swiss soil reaches it’s climax – the referendum takes place on Sunday – it is telling that the Dutch announced on Friday that they have just secretly repatriated 122 tonnes of their sovereign gold reserves from New York back to Amsterdam.

The gold, worth $5 billion at today’s prices, represents 20% of the Netherlands total reserves. It now keeps 31% of its reserves in Amsterdam. Another 31% is believed to be in New York, with the remainder spread between Ottawa and London – the same locations where the bulk of Swiss gold is purported to be stored.

The trend towards gold repatriation began with Hugo Chavez bringing Venezuelan gold back to Caracas in 2011. It has been followed by similar moves by other large gold owning nations and central banks, most notably, Germany.

The repatriation movement has been driven by suspicion that the Federal Reserve and other central banks may have leased or sold gold it was holding on behalf of other countries to bullion banks and that this gold may have been used in order to suppress the price of gold in recent years.

Bizarrely, the Federal Reserve’s gold holdings have not been audited in over 50 years.

The last audit, and the last public visit, was in 1953, just after U.S. President Dwight Eisenhower took office. No outside experts were allowed during that audit, and the audit team tested only about 5% of gold there. So, there hasn’t been a comprehensive audit of Fort Knox in over 60 years.

Demands for gold repatriation also accelerated after the Lehman collapse and during the global financial crisis due to concerns that if the U.S. and world suffered a systemic collapse or a dollar crisis , nations may find it hard to secure their gold reserves.

The concern was that a desperate Fed could nationalise international gold reserves in order to prevent a dollar collapse or to rebuild confidence in the dollar after a currency crisis.

It is interesting to note that while some western economists, such as Paul Krugman, continue to denigrate gold, western central banks, do not appear to view gold as a “barbarous relic.” Nor do their eastern counterparts and their Chinese counterparts many of whom have been quietly reducing their dollar, euro and pound foreign exchange reserves and adding to their gold reserves in recent years.

The Dutch Central Bank went so far as to state that the action was designed to install public confidence in the ability of the central bank to manage crises. The prospect of further shipments from the U.S. remains open as they are keeping the logistical details secret.

Questions are already being asked about how the Dutch were able to repatriate such a sizeable volume of gold when Germany’s request was brushed aside. It may be that by taking a discreet approach the Dutch allowed the Federal Reserve room to manoeuvre – allowing them to harvest the metal from the open market. Skeptical analysts have suggested that the fall in the ETF gold holdings may have come in handy for the New York Federal Reserve.

Questions are also being asked about the faith of the Ukrainian gold reserves after the gold disappeared from the Ukraine’s central bank soon after the U.S. sponsored coup brought the new government to power.

The Dutch clearly view gold favourably as an important monetary asset and they also have demonstrated their belief that owning gold in a secure manner is of utmost importance.

Although the German Central Bank has stated that it trusts the Americans as custodians of it’s gold reserves – despite being denied access to vaults in New York to view their own gold – the campaign for repatriation of Germany’s gold remains strong.

Whether the Swiss gold initiative passes or fails this weekend it is still worth noting that a very large minority of Swiss are very conscious of the role that gold plays particularly in times of crisis.

During the reformation in Europe it was in these three countries – Germany, Switzerland and the Netherlands – that independent thought flourished. Populations globally have been “dumbed down” in recent years but these nations still have a high level of public discourse and debate and the importance of prudence, saving, thrift and gold remains understood by many.

We believe that other central banks may have already quietly sought or indeed will seek repatriation of their gold from New York, Ottawa and London. This has the potential to create a short squeeze as central banks may be forced to enter the market to acquire the physical bullion that they thought they already owned.

If these custodians are not in possession of the gold they claim to hold they, too, will be forced to buy gold on the open market where supply is now extremely tight as seen in gold remaining in backwardation.

We believe, like the Dutch, that only gold bullion in your possession or allocated gold stored in secure locations such as Singapore, Hong Kong and Zurich can be viewed as a safe-haven asset.

Get Breaking News and Updates On Gold Markets Here

MARKET UPDATE

Today’s AM fix was USD 1,196.00, EUR 964.67 and GBP 764.51 per ounce.

Friday’s AM fix was USD 1,193.25, EUR 958.59 and GBP 761.54 per ounce.

Gold prices were 1% higher last week. Gold and silver rose to three week highs Friday after China cut benchmark interest rates to support economic growth, leading to demand for precious metals as a store of value.

Gold in USD – 5 Days (Thomson Reuters)

China’s rate cut on Friday aligns them with the European Central Bank and Bank of Japan in deploying fresh stimulus and QE as ultra loose monetary policies continue globally.

Russia added to gold reserves in October, bringing holdings to the highest in at least two decades, IMF data showed last week and as announced by the Russian central bank governor (see here).

Gold has climbed 6% after touching a four-year low on November 7 amid increased demand for coins and jewelry, combined with signs that nations are boosting reserves. Central banks may raise purchases by as much as 22 percent in 2014, the World Gold Council estimates.

Gold in USD – 2 Years (Thomson Reuters)

The net-long position in gold rose by 21,634 contracts to 60,307 futures and options in the week ended November 18, according to U.S. Commodity Futures Trading Commission (CFTC) data published three days later. Short wagers fell to 65,405 contracts, the least since September 9.

Gold rose 70% from December 2008 to June 2011 as central banks increased quantitative easing on a massive scale and currencies internationally were debased. The precious metal fell 28% in 2013, the most in three decades, after sharp and severe selling in the futures market, often during less liquid markets overnight in Asia, led to price falls.

Switzerland holds its referendum on the Swiss Gold Initiative this Sunday (Nov. 30). If passed it would to require the Swiss National Bank to hold at least 20% of its assets in gold, up from about 8%.

Opinion polls suggest the no side will win but many opinion polls have been badly wrong in recent years. Voter discontent with the political establishment is likely to make the referendum tighter than is expected. A yes vote would surprise the market and lead to fireworks in the gold market Sunday night, Monday and next week.

end

Chinese demand last week: 52 tonnes. That works out to 7.42 tonnes per day on a 7 day week. The world produces 6.02 tonnes per day on a 7 day week (ex China ex Russia). I would also like to point out that this demand does not include any sovereign gold purchases as China uses its unwanted USA dollars to do the purchasing. It is not included in the SGE withdrawals:

Total Chinese Gold Reserves Approaching 16,000t

Chinese gold demand remains very strong throughout week 46 (November 10 – 14), withdrawals from the vaults of the Shanghai Gold Exchange (SGE) accounted for 52 tonnes. The year to date counter has reached 1,761 tonnes.

Below you can see a screen shot of the Chinese weekly SGE report disclosing total withdrawals.

Since we have confirmation from the SGE about the exact rules for Chinese domestic banks on importing gold through the Shanghai International Gold Exchange (SGEI), we know for sure trading volume on the SGEI can distort Chinese wholesale gold demand measured by SGE withdrawals (which also include SGEI withdrawals).

Given the fact total SGE withdrawals are very strong tells us the Chinese are buying massive amounts of gold, of which most is imported. In contrast SGEI trading volumes are quite low, which suggests domestic banks do not import through the SGEI (I read from one domestic bank having imported 500 Kg through the SGEI).

Consequently I think SGEI trading is primarily done by foreigners in the Shanghai Free Trade Zone. All this volume is concentrated in the iAu9999 physical gold contract. Because this is a physical contract (100 % margin), and because of the low volumes, SGEI trading is not likely to be speculation, but simple physical buying. If these foreigners that buy physical also withdrawal the gold to ship it home or leave it in the SGEI vaults we don’t know.

By not knowing what happens on the SGEI, I think the best way of approaching Chinese wholesale gold demand is this: If we look at week 46, SGE total withdrawals were 52,260.2 Kg, SGEI volume was 1,478 Kg, meaning Chinese wholesale gold demand was in between 52,260.2 Kg and 50,782.2 Kg. This way year to date demand is in between 1,761 tonnes and 1,746 tonnes. Let’s stay conservative and use the bottom limit, which would have required 1,143 tonnes to be imported year to date, annualized 1,293 tonnes.

Using 1,143 tonnes as net imports year to date and 399 tonnes of mine supply, we can make the following estimate of total (public and private) Chinese gold reserves; 15,496 Tonnes. (click here for a detailed explanation of how I conceived this estimate.)

More proof on PBOC purchases was disclosed by Deutsche Bank (DB) recently. In a report about the Swiss gold referendum they stated:

Of course, the passing of the referendum could act as a signal for speculators to ‘front-run’ SNB purchases. This additional demand could drive up prices. But there have been a number of examples of publically flagged large-scale official gold transactions that have had a limited market impact. In the IMF example above, gold prices rose steadily despite the IMF being a reliable seller of almost 20 tonnes each month. In another example, the Chinese government’s open market purchases of roughly 500 tonnes per year have not prevented the gold price from plummeting in recent years.

Let’s not discuss the price of gold for a second, but focus on what DB states on PBOC demand, which has been 500 tonnes for the last couple of years. This is not exact or official data, but it is more confirmation the PBOC is buying such amounts every year. We know the PBOC does not purchase gold through the SGE, so these purchases are in addition of Chinese wholesale gold demand and strengthen the composition of the previous chart.

Silver

Silver on the Shanghai Futures Exchange (SHFE) is trading in backwardation since August 6.

The discount on silver in China mainland relative to London is near 7 %.

That’s it for this week’s China update. (I found some interesting things ‘on the ground’ here in Amsterdam regarding the repatriation of Dutch gold from New York by DNB, I think it’s in everybody’s interets I continue writing on that story.)

Koos Jansen

end

xxx

Central banks are thinking about repatriating their gold from New York and London as they fear that their gold is gone.

(courtesy James Turk/Kingworldnews/Eric King)

Central banks getting nervous about gold vaulted elsewhere, Turk tells KWN

10:42p ET Friday, November 21, 2014

Dear Friend of GATA and Gold:

Concerns about the fractional-reserve gold banking system will increase because of the Netherlands central bank’s repatriation of gold from the U.S. Federal Reserve, GoldMoney founder and GATA consultant James Turk tells King World News tonight. “People are getting nervous” about gold vaulted with others, Turk says, and central banks making contingency plans for their currencies need to ensure that they control their gold. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/11/21_E…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

What an absolute joke: “Optimization of Reserve Structure” ???

in English: their gold was stolen by the uSA who then sent them a check for their gold!!

(courtesy zero hedge)

Ukraine Central Bank Admits Gold Outflow, Calls It “Optimization Of Reserve Structure”

A week after we reported that the head of the Ukraine central bank admitted in an unofficial, informal interview that Ukraine’s gold is gone, all gone, moments ago the Central Bank revealed that, sure enough, the gold holdings in the civil war-torn country have tumbled, as a result of a decision in September to “increase the share of US dollars in a reserve basket”, or in other words, to sell the gold. Just don’t call it that: in fact, as of today we have a brand new buzzword for gold liquidations: “optimization of international reserves.”

From the central bank:

National Bank of Ukraine has optimized the structure of international reserves. This is due to timing structure of international reserves and the external position of the country. National Bank of Ukraine decided in September 2014 to increase the share of US dollar in a reserve basket, because the structure of the trade balance of the country is 70.3% in US dollars, 15% in euros. 77.7% of gross foreign debt denominated in Ukraine USD in EUR – 11.2% in SDR – 5.8%.

Recently, there was a significant volatility in global currency markets associated with the strengthening of the US dollar against other world currencies. Therefore, the National Bank of Ukraine decided to reduce the share of gold in foreign exchange reserves to 8%. To this end, the international markets has sold 0.46 million. Troy ounces of gold in US dollars, respectively proportion of gold in international reserves declined to 7.9%.

According to the IMF, the proportion of gold in global reserves at an average of 11.7%, while international reserves of developing countries, the proportion of gold in an average of 4.4%.

So Ukraine’s central bank decided to conver its gold into dollars just as the USD has been surging to levels not seen in years? Just who says central bankers are bad traders. Furthermore, while one assumes this is the asset update as of the end of October, we can’t wait to learn just what happened in the first days of November when the Valeria Gontareva interview took place.

And while the fate of the Swiss gold referendum may lie in the hands of the Zurich subsidiary of Diebold, perhaps it is time for Ukraine’s population to ask its “elected” rulers just where Ukraine’s gold has gone, pardon, been “optimized” to.

end

(courtesy New York Sun/GATA)

New York Sun: Fair and balanced Fed?

From the New York Sun

Sunday, November 23, 2014

So just where is Janet Yellen going by inviting left-wing groups into the boardroom of the Federal Reserve to give her their views on monetary policy? Is the Fed chairman prepared to extend the same courtesy to conservative groups?

Those questions are being raised after Mrs. Yellen and several other members of the central bank’s board of governors met at Washington with a group of left-wing critics of the central bank. They are being raised by American Principles in Action, a right-of-center group that is mounting a campaign for sound money. …

… For the remainder of the commentary:

http://www.nysun.com/editorials/fair-and-balanced-fed/88939/

end

(courtesy GATA/ChrisPowell)

Senate report shows how easily banks can rig gold, copper, and other markets

10:30a ET Sunday, November 23, 2014

Dear Friend of GATA and Gold:

The heavy involvement of investment banks in commodity trading creates the potential for market manipulation and conflicts of interest in the gold market, and exchange-traded gold funds may be mechanisms of market manipulation contrary to the basics of supply and demand, according to the 396-page report published last week by the Permanent Subcommittee on Investigations of the U.S. Senate’s Committee on Homeland Security and Governmental Affairs.

GATA’s friend J.H. points out these findings on Page 38 of the report:

“Possible conflicts of interest permeate virtually every type of commodity activity. If the bank’s affiliate leases an electrical power plant, the bank may attempt to use regional pricing conventions to boost its profits, even at the expense of clients that pay the higher electricity costs. If the bank’s affiliate mines coal while the bank trades coal swaps, the bank may ask its affiliate to store the coal rather than sell it to help restrict supplies, and benefit from long swap positions, while causing its counterparties to incur losses. If the bank’s affiliate operates a commodity-based exchange-traded fund backed by gold, the bank may ask the affiliate to release some of the gold into the marketplace and lower gold prices, so that the bank can profit from a short position in gold futures or swaps, even if some clients hold long positions.

“A fourth problem with mixing banking and commerce is that, in the context of physical commodities, it invites market manipulation and excessive speculation in commodity prices. If a bank’s affiliate owns or controls a metals warehouse, oil pipeline, a coal-shipping operation, refinery, grain elevator, or exchange-traded fund backed by physical

commodities, the bank has the means to affect the marginal supply of a commodity and can use those means to benefit the bank’s physical or financial commodities trading positions. If a bank’s affiliate controls a power plant, the bank can ‘manipulate the availability of energy for advantage’ or to obtain higher profits.”

And on Page 368: “At the same time, a commodity-backed ETF can have a significant impact on the price and volatility of the underlying commodity, even when a precious metal is involved. For example, gold-related ETFs first surfaced in 2004, with dozens of similar ETFs springing up over time. Today, it has become clear that significant movements in the gold-related ETFs have had direct impacts on the price of physical gold.

“As one analyst in the field noted: ‘You watch the flow of money. … No matter what the supply-and-demand fundamentals [for physical gold] may suggest, if that money’s flowing, those prices are going to move.’

“The Wall Street Journal cited as a possible explanation for the impact of gold ETFs on physical gold prices the relatively small size of the gold market, estimated at $236 billion in annual sales in 2012, and the ETFs’ significant share of those sales.”

Starting on Page 353, the report describes JPMorganChase’s acquisition of the copper market, thanks in large part to an exemption from position limits granted by the Federal Reserve and Office of the Comptroller of the Currency to banks trading copper, an exemption previously granted only to banks trading gold and silver. The implication of the copper exemption is that the U.S. government decided that manipulating gold and silver prices was not enough if the major industrial metal was still able to trade freely and broadcast inflation signals as gold and silver also would do if they were traded freely.

Interesting as it is, the Senate report really has done little more than reiterate the old principle, the first premise of anti-trust law, that if a market participant is big enough, it can push any market around. Unfortunately that premise has been pretty much overlooked in the United States since Wall Street took over both major political parties.

Also unfortunately, if predictably, the Senate report does not touch on direct but surreptitious government intervention in the commodity markets, though sensational documentation of such recently became available, documentation that central banks and governments are receiviing volume discounts for surreptitiously trading all major commodity futures contracts in the United States:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

Apparently the work of exposing that surreptitious intervention will continue to be left to outsiders like GATA.

The Senate report is posted at GATA’s Internet site here:

http://www.gata.org/files/SenateReportOnBanks&Commodities-11-20-2014.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

No wonder the Dutch got their 122 tonnes. In exchange for keeping the black box secret, the Dutch gets to repatriate her gold

(courtesy RT news)

Dutch government refuses to reveal ‘secret deal’ into MH17 crash probe — RT News

Would you want to bet that NOT releasing the details has something to do with them actually getting the gold?

http://rt.com/news/207243-netherlands-mh17-investigation-documents/

end

The Real Reason Why The Netherlands Repatriated Its Gold

Submitted by Sprout Money on 11/23/2014 10:03 -0500

In what could definitely be called a stunning move, the Netherlands has announced it has repatriated in excess of 120 tonnes of gold from the vaults of the Federal Reserve in New York to the Dutch Central Bank in Amsterdam. Officially a move made to rebalance the locations where the gold is being stored, one cannot ignore the fact that the Netherlands only repatriated a large part of the gold which was stored in New York and it did not touch the gold stored in Canada and London.

Additionally, it’s not just ‘some’ gold being brought back home, no, the total amount is 122.47 tonnes or almost 4 million ounces with a market value of $5B. This will reduce the exposure of the Dutch Central Bank to the US financial system as now just 31% of its gold is being stored in the vault of the Fed, coming down from 51%. We have the impression this won’t be the last repatriation as the Dutch Central Bank is keeping its shipping route secret ‘in case more gold needs to be repatriated’.

So what was the main reason why the Netherlands brought the shiny precious metal back home? The central bank wants you to believe it’s just an ordinary decision, but believe it or not, the only reason for this move was torestore the confidence of the public in the Central Bank. By publishing this statement, the Dutch Central Bank basically admits that holding gold increases the public trust in the central bank as an institution, and that’s an statement which should not and cannot be underestimated as it basically means that only physical gold can be trusted and that the gold should be stored inside the country. ‘He who owns the gold makes the rules’ once again seems to be up-and-coming again.

The best place to store your gold is obviously in your own back yard, and it looks like the Netherlands aren’t agreeing with the Germans which also wanted to repatriate most of its gold which was stored in the vaults of the Federal Reserve. However, after bringing just a fraction of its gold back to Berlin, Germany publicly stated it would not repatriate any more gold as it ‘fully trusts the Federal Reserve as an institution’ and ‘the Americans are taking good care of their gold’. That’s obviously a bogus reason as the Fed obviously wasn’t suddenly taking better care of the gold than a year before. It’s also interesting to notice that the Netherlands and Germany used a different approach. Whilst Germany was boasting about its attempt to repatriate the gold, the Netherlands chose the ‘stealth’ way and repatriated it first before announcing it.

President Knot of the Dutch Central Bank with ‘his’ gold.

This strategy isn’t surprising as the Dutch always have been quite savvy. Keep in mind it was one of the most powerful nations right after the middle ages when the VOC really ruled the world shipping five times more goods to and from Asia than its main competitor in Great Britain. This savvy business mind is still in place and we wouldn’t be surprised if the Netherlands would be the frontrunner in a worldwide move to repatriate gold.

Keeping the German repatriation story in mind, the Netherlands are basically giving the Federal Reserve the finger. Unlike Germany, it does not trust the Federal Reserve more than its own central bank and it prefers to ‘sit’ on the gold in Amsterdam rather than store it in a foreign nation. This is a huge policy shift which cannot be underestimated, especially not if you look at all pieces of the puzzle.

As you know, China is still buying gold like crazy and was recently joined by Russia which has bought more gold every month since the beginning of this year. People were fast to dismiss this increased interest in gold as those were ‘special’ countries. Well, that argument is no longer valid. Germany wanted to repatriate its gold last year (but came under pressure to drop its plan), the Netherlands have now successfully repatriated almost 4 million ounces of gold, and there’s a Swiss referendum which asks the opinion of its citizens to increase the gold holdings once again. It’s unlikely the Swiss will approve this proposal as the latest polls show 38% in favor and 47% against the proposal with approximately 15% undecided voters.

The main takeaway here is not that 47% of the people are against increasing the gold reserves, but that 38% is strongly in favor of backing the Swiss Franc with Gold and an additional 15% might consider it. We are sure that a better explanation of the proposal would reduce the amount of opponents. Additionally, a lot of nay-sayers are voting against the party which proposed the idea and aren’t necessarily against the renewed gold standard.

This gold repatriation isn’t an isolated case. All signs are pointing in the direction that several central banks are now getting increasingly interested to increase their gold holdings and to have the gold inside the country instead of somewhere else. The Dutch repatriation is the first step, but we expect more pieces of the puzzle to fall into place soon. Very soon.

>>> Check Out Our Latest Gold Report!

Sprout Money offers a fresh look at investing. We analyze long lasting cycles, coupled with a collection of strategic investments and concrete tips for different types of assets. The methods and strategies from Sprout Money are transformed into the Gold & Silver Report and theTechnology Report.

Follow us on Twitter @SproutMoney

end

Grant Williams talks with Lars Schall on gold:

(courtesy Grant Williams/Lars Schall)

xxx

Gold market is manipulated, Grant Williams tells Lars Schall

3:53p ET Sunday, November 23, 2014

Dear Friend of GATA and Gold:

Interviewed by the German financial journalist Lars Schall for Matterhorn Asset Management’s Gold Switzerland, Singapore fund manager and “Things That Make You Go Hmmm. …” letter editor Grant Williams says there’s no doubt that the gold market is manipulated, that the only question is how much, and that because of central bank intervention there’s not much left to free markets. Schall and Williams cover other subjects, including the nature of money, the abuse of money creation and credit, the likelihood of returning to a gold standard, and the Swiss Gold Initiative. The interview is an hour long and can be heard at Gold Switzerland here:

http://goldswitzerland.com/gold-is-a-belief-grant-williams/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Ben Davies talks with Eric King on gold issues

(courtesy Ben Davies/Eric King/Kingworldnews)

xxx

Hinde Capital’s Davies calls turn in markets, favors gold and even mining shares

9:07p ET Sunday, November 23, 2014

Dear Friend of GATA and Gold:

Hinde Capital CEO Ben Davies, in commentary posted at King World News, predicts the “Weimarization of equity” and a turn in the markets, making it a time to buy not just gold but gold mining shares. Davies’ commentary is posted at the KWN blog here:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/11/24_T…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Dr Craig Roberts on the Swiss referendum:

Swiss Gold Referendum: What It Really Means

(courtesy Paul Craig Roberts)

In a few days the Swiss people will go to the polls to decide whether the Swiss central bank is to be required to hold 20% of its reserves in the form of gold. Polls show that the gold requirement is favored by the less well off and opposed by wealthy Swiss invested in stocks.http://snbchf.com/gold/swiss-gold-referendum-latest-news/ These poll results provide new insight into the real reason for Quantitative Easing by the Federal Reserve and European Central Bank.

First, let’s examine the reasons for these class-based poll results. The view in Switzerland is that a gold backed Swiss franc would be more valuable, and a more valuable franc would increase the purchasing power of wage earners, thus reducing their living costs. For the wealthy stock owners, a stronger franc would reduce Swiss exports, and less exports would reduce stock prices and the wealth of the wealthy.

The vote is clearly a vote about income shares between the rich and the poor. The Swiss establishment opposes the gold-backed franc, as does Washington.

A few years ago the Swiss government, after experiencing a strong rise in the exchange value of the Swiss franc as a result of dollar and euro inflows seeking safety in the Swiss franc, decided to expand the Swiss money supply in line with the foreign currency inflows in order to stop the rise of the franc. The liquidity supplied by the central bank creating new francs has stopped the rise of the franc and supports exports and stock prices. As a vote in favor of a gold backed franc is not in the interest of the elite, it is unclear that the vote will be honest.

What does this tell us about the Federal Reserve’s policy of Quantitative Easing, which is an euphemism for printing an enormous amount of new dollars?

The official reason for QE is the Keynesian Phillips Curve claim that economic growth requires mild inflation of 2-3%. This false theory was put to death by the supply-side policy of the Reagan administration, but the misrepresentation of the Reagan administration’s policy by the Establishment has kept the bogus Phillips curve theory alive. http://www.paulcraigroberts.org/2014/11/14/global-house-cards-paul-craig-roberts/

The claim based in disproven Phillips Curve theory that the Fed’s policy is directed at helping the overall economy is another example of the deception practiced by US authorities. The real purpose of QE is to drive up the wealth and income of the one percent by providing the liquidity that flows into financial asset prices such as stocks and bonds.

Since the 2008 US recession, skeptics of the Fed’s explanation of QE as support for the US economy have stressed instead that the purpose of US economic policy has been to support the federal deficit at low interest rate costs and to support the balance sheets of the troubled banks by pushing up the prices of debt-related derivatives on the banks balance sheets.

These have been important purposes, but it now appears that the main purpose has been to make the rich richer. This is why we have a stock market whose high values are not based in fundamentals but, instead, are based on the outpouring of liquidity by the Federal Reserve. As the economic policy of the US is entirely in the hands of the rich, it is not surprising that the rich use it to enrich themselves at the expense of everyone else. The Fed’s monetary policy that enriches the rich by driving up the prices of stocks and bonds also has robbed retirees of hundreds of billions of dollars, perhaps trillions, in lost interest income on their savings. http://www.lewrockwell.com/2014/11/bill-sardi/how-10000-in-a-bank-in-2008/

As Nomi Prins and Pam Martens have made clear, QE is not over. The Fed is rolling over its interest and principal payments on its $4.5 trillion bond inventory into new bond purchases, and the banks now infused with $2.6 trillion in cash from the Fed are purchasing the bonds in place of the Fed’s QE purchases.

According to the latest news reports, Mario Draghi, the head of the European Central Bank will print all the money necessary to support financial asset prices. http://www.marketwatch.com/story/draghi-says-ecb-will-do-what-it-must-on-asset-buying-to-lift-inflation-2014-11-21?dist=beforebell Draghi, like the Federal Reserve, masks his policy of enriching the rich in Phillips curve terms of driving up inflation in order to support economic growth. Of course, the real purpose is to drive up stock prices.

Like the Fed, the ECB pretends that the money it prints flows into the economy. But given the poor condition of the banks and potential borrowers, loan volume is low. Instead the money created by central banks flows into paper financial asset prices. Thus, the monetary policy of the Western world is directed toward supporting the wealth of the rich and worsening the inequality in the distribution of income and wealth.

The rich are far from finished with their pillage. In exchange for campaign donations, state governors are turning over state pension funds to the management of high-fee, high-risk private pension fund managers who do a better job of maximizing their fee income than protecting the nest eggs of retirees. http://www.informationclearinghouse.info/article40287.htm

Throughout the Western world economic policy is run for the sole benefit of the one percent and at the cost of everyone else. The greed and stupidity of the rich are creating ideal conditions for violent revolution. Karl Marx might yet triumph.

end

In my opinion, the following is the most important piece written by Bill Holter

(courtesy Bill Holter/Miles Franklin)

xxx

Is COMEX Cornered?

It is with a deep sense of gratitude that I have had all of you as friends and associates during what has been a long war, not a good war, but a very long “financial war”. As you know from these writings; this has been a war conducted by the Federal Reserve against the entire world, aided and abetted by major international banks via the manipulation of most every market on the planet. The ethics and morals our country was originally built on …be damned!

end

xxxx

And now for the important paper stories for today:

Early Thursday morning trading from Europe/Asia

1. Stocks up on major Asian bourses with a lower yen value falling to 118.27

2 Nikkei up 57 points or 0.33%

3. Europe stocks all up (except London /Euro rises/ USA dollar index down at 88.26.

3b Japan 10 year yield at .46% (Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 118.27

3c Nikkei now above 17,000

3fOil: WTI 76.13 Brent: 79.89 /all eyes are focusing on oil prices. A drop to the mid 60′s would cause major defaults.

3g/ Gold up/yen up; yen just below 118 to the dollar/at fresh 7 year lows.

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt (see Von Greyerz)

3j Two European central bankers state that deflation is upon Europe and is dangerous

3k China set to do another rate cut

3l: Yields on peripheral Europe drops drop precipitously.

3m Gold at $1194.00 dollars/ Silver: $16.31

4. USA 10 yr treasury bond at 2.33% early this morning.

5. Details: Ransquawk, Bloomberg/Deutsceh bank Jim Reid

(courtesy zero hedge/your early morning trading from Asia and Europe)

Futures Poised For New Record Highs On Weekend Central Bank Double Whammy

Another day, another case of central banks, not one but two this time, dictating “price” action.

On Saturday, traders woke up to the following headlines from the ECB’s Constancio, which the market promptly digested and spun as bullish from more ECB QE, leading to one after another bank pulling forward their estimates of first bond monetization by Mario Draghi (CSFB now believes it will take place in December from Q1 of 2015):

- ECB’S CONSTANCIO SAYS CURRENT SITUATION DIFFERENT FROM 2012

- CONSTANCIO SAYS INFLATION SHOULD BE IN HANDS OF MONETARY POLICY

- CONSTANCIO SAYS INFLATION VERY CLOSE TO ZERO IS `DANGEROUS’

- CONSTANCIO SAYS DEFLATION `VERY NASTY’

- CONSTANCIO SAYS ECB SHOWING WILLINGESS TO DO MORE IF NEED BE

So the “deflation monster” is “very nasty”, got it.

Colorful rhetoric aimed at 5-year-olds aside, the Portuguese central banker said no decision has been made yet on buying sovereign bonds but if banks finding existing measures insufficient then the ECB will have to consider buying other assets including sovereign bonds. This follows last week’s comments from Draghi when he said he would “do what we must to raise inflation and inflation expectations as fast as possible”. As a result there has been a fresh round of calls for an ECB programme and as such has benefited peripheral fixed income products. This has led to the Spanish 10yr yield breaking below 2.0% and Italian 5yr below 1.0% for the first time.

And then to further make the BTFATH case, Reuters reported citing an “unnamed official” that China’s Friday rate cut is just the first of many, and as a result the entire fixed income curve across Chinese product has repriced substantially, even as the Chinese Yuan is starting to crack on what we hinted weeks ago will be a devaluation of the currency as China is now, in the words of BNP, “losing the currency war.” This happens when in a delayed session (the Friday PBOC announcement took place after China close), Asia risk assets rallied higher across the board, led by a relative outperformance in Chinese assets. The CSI 300 Shanghai Composite and the Hang Seng are currently +3.24% and +2.04% respectively. China 5y CDS is also 2bp tighter. CNH has opened some 0.1% weaker versus the Dollar. Markets in Japan are closed but major bourses in Korea and Australia are also +0.72% and +1.08% stronger respectively.

US equity futures are also poised for another session at record highs thanks to a German IFO business climate print which followed last week’s ZEW rebound, and rose for the first time in 7 months, printing at 104.7, above the 103.0 expected, up from 103.2 in October. Expect more multiple expansion just that much more on their way to a 20x GAAP P/E on the S&P 500.

Finally, with volumes exceedingly thin headed into Thanksgiving, this week’s eco calendar relatively light, and Japan away from market overnight the mandated wealth effect levitation is set to continue: even crude has managed to bounce modestly from extremely oversold conditions, on hopes this week’s OPEV meeting will result in a production cut. Perhaps the only place where central banks are so far failing to buoy prices is iron ore futures which fell below $70/tonne for the first time since 2009.

Overnight Bulletin Headlines

- Peripheral banks lead the way higher for European equities as ECB’s Constancio provides yet more dovish rhetoric from the central bank regarding a potential sovereign QE programme.

- Sentiment for Europe has also been further bolstered by a strong German IFO release, in what has been a relatively quiet session.

- Looking ahead, the main data release will be the US services PMI figure in what is set to be a relatively quiet session.

- Treasuries fall before week’s $105b note auctions begin with $28b 2Y notes; WI yield 0.565% vs 0.425% in October.

- German business confidence unexpectedly rose for the first time in seven months, with the Ifo institute’s business climate index increasing to 104.7 in Nov. (est. 103) from 103.2 in Oct.

- Italy, France and Germany will face off over how to rebuild euro-area growth when the European Commission passes judgment this week on their draft budgets

- Greek government officials will meet in Paris tomorrow with troika representatives in a bid to break a deadlock over freeing up the last tranche of the country’s bailout

- China is poised to deliver deeper interest rate cuts after last week’s unexpected decision to reduce borrowing costs for the first time since 2012

- With the deadline for their nuclear talks just hours away, the U.S. and Iran took up the fall-back option of putting more time on the clock

- Iran may propose that OPEC cut its output target by as much as 1m barrels a day to halt the slide in crude prices when the country’s oil minister consults with his Saudi counterpart before the group gathers this week

- Nearly $41b IG priced last week, $10b high yield. BofAML Corporate Master Index OAS narrows 1bp to 134 from YTD wide 135; YTD low 106. High Yield Master II OAS narrows 7bps to 454. YTD range 508-335bps. CDX High Yield closed at 106.96 from 106.48; YTD range 104.52-109.15

- Sovereign yields mixed. Tokyo closed for holiday; Asian and European stocks, U.S. equity-index futures higher. Brent crude, copper gain; gold falls

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, Oct., est. 0.40 (prior 0.47)

- 9:45am: Markit US Services PMI, Nov. preliminary, est. 57.3 (prior 57.1); Markit US Composite PMI, Nov. preliminary, (prior 57.2)

- 10:30am: Dallas Fed Manufacturing Activity, Nov., est. 9 (prior 10.5)

DB’s Jim Reid concludes the overnight recap

With China cutting rates unexpectedly and with Draghi earlier expressing urgency about the need to return inflation back towards target (“without delay”) it does feel that most countries still want to ease and with the BoJs recent move, it seems that if you stand still you might actually be at risk of effectively tightening policy. If anyone should doubt Draghi’s dovishness he also said they would “do what we must to raise inflation and inflation expectations as fast as possible”. For us government QE in Q1 continues to be a near inevitability but we may still have enough conflict within the ECB that may mean December is still too early. Whatever the timing it was clear that the market was surprised by the explicitness of the speech. The Stoxx 600 closing 2.06% higher, Xover rallying 16bps and the euro selling off 1.2% versus the dollar. Yields in the periphery were also significantly lower with the 10 year benchmark yield in Italy, Portugal and Spain down 9bps, 13bps and 9bps to 2.21%, 2.98% and 2.01%, respectively.

Turning our attention over to China, the PBOC certainly surprised the market with a 25bps cut in the benchmark deposit rate to 2.75% and 40bps cut in the lending rate to 5.60%. The Central Bank also lifted the ceiling on deposit rates to 1.2x of the benchmark deposit. DB’s Chief Chinese Economist, Zhiwei Zhang, wrote on Friday that he believes this marks the beginning of a policy easing cycle, given that the policy stance has clearly changed from marginally loose towards broad based easing. He also expects this easing cycle to last for the full year of 2015 and continues to expect two rate cuts in 2015 (first cut of 25bp in Q2 and second 25bp cut in Q3). So why act now given that China is still on track to meet the ‘around 7.5% growth target this year? Zhiwei believes that a plausible answer could be as a result of the cumulative fiscal pressure at the local government level that has built up this year. He points out that local governments revenues have suffered from the sharp slowdown in land sales in 2014 as well as a rising LGFV debt burden – given this, he argues that a rate cut is the most effective way for a central government to help lower their finance costs. With regards to the impact on FX, given that the government is now willing to use traditional monetary tools, our FX strategist believes that the use of RMB as a form of monetary policy will likely wane and as a result China will likely start to gradual weaken the currency given that on a REER basis, the RMB is already very expensive.

Asia risk assets are rallying higher across the board this morning, led by a relative outperformance in Chinese assets. The CSI 300 Shanghai Composite and the Hang Seng are currently +3.24% and +2.04% respectively. China 5y CDS is also 2bp tighter. CNH has opened some 0.1% weaker versus the Dollar. Markets in Japan are closed but major bourses in Korea and Australia are also +0.72% and +1.08% stronger respectively.

Some of these overnight moves could have been also been a continuation of what was a fairly positive US risk session last Friday. The S&P 500 closed +0.52% to mark the fifth consecutive week of gains and further extend record highs. Most sectors were higher on the day but materials (+1.26%) and energy (+1.22%) were the main outperformers. The recent respite in crude was probably a driver for that as we’ve now seen Brent and WTI bounce around 4% off their recent lows to trade at around $81/bbl and $77/bbl as we type. Interestingly despite a stronger day for equities, Treasuries were mostly stronger across the curve last Friday. The 10y was 2bps lower to 2.325% with the only data release for the day being the Kansas City Fed’s manufacturing which came in a tad firmer than expected (7 vs. 6 expected).

Staying on the theme of oil, Thursday’s OPEC meeting at Vienna will be a closely watched affair. There has been no shortage of news-flow around the event recently with prices declining sharply over the last couple months in anticipation that OPEC will not cut production. In recent weeks it appears that the camp has become split with the likes of Saudi Arabia and other low-cost producers with large FX reserves happy to run down the price to gain market share. On the other hand the likes of Venezuela and more recently Iran are reported (Bloomberg) as saying that they may propose a 1m a day cut in barrels produced. They are campaigning for higher prices to balance their budget and improve fiscal positions. We will no doubt hear further statements this week from producers in the run up to the meeting so it’s something to keep an eye on.

Coming back to Europe quickly, over the weekend Bloomberg have reported that the EU is planning a new leveraged fund as part of EC president Juncker’s investment plan. The article suggests that the €21bn fund is designed to have a proposed leverage rate of 15x, with the idea that private investors will be able to share the risks of new projects and kick-start those currently under-resourced.

Just staying in the region, there was news ( Financial Times) in Greece on Friday that the government has failed to come to an agreement with the Troika over bailout monitors around the reported fiscal gap. This is important given that the program legally expires at the end of this year and places greater importance of striking a deal ahead of the December 8th meeting of eurozone ministers that would set the terms of a bailout exit. It appears that the disagreement stems from Athens’ argument that accelerating economic growth next year, along with various fiscal measures, will close the perceived fiscal gap set at €2bn of the 2015 budget by the Troika. With no date set for the arrival of the Troika in Athens however, and further implications to consider down the road with regards to ECB support of Greek banks, it’ll be worth keeping an eye on how events progress as we run into the end of the year.

In terms of the day ahead, this morning will likely be highlighted by the IFO print out of Germany with the market expecting the readings to be unchanged versus last month. Later on today and across the pond we get the Chicago Fed and November flash services and composite PMI’s with again the market expecting little change versus last month.

Finally, with regards to the week ahead, it looks like that there will be no sign of a breather for markets with a packed macro calendar to look forward to. Starting in the US, things kick into gear tomorrow when we have the preliminary release of Q3 real GDP. DB’s Joe Lavorgna notes that information released since the advance GDP release indicated modestly more consumption and inventories last quarter than what the bureau of economic analysis had assumed in its initial snapshot- Joe points out that this should offset most of the downward revisions to exports and construction and so he expects minimal revision. Elsewhere in the US tomorrow we get readings for consumer confidence, Case-Shiller and FHFA house price data. Closer to home in Europe tomorrow we start the day with Germany’s Q3 GDP release. The market is looking for a +0.1% qoq print and comes following the weak flash PMI reading last week. As we mentioned then our German economists are expecting GDP to stagnate through the next two quarters and haven’t ruled out the potential for a negative quarter so it’ll be interesting to see what we get. Elsewhere we get a host of further data out of Germany including government spending and private consumption along with Italian retail sales and Spanish PPI. Elsewhere we will get the OECD outlook with Japan’s Kuroda speaking in the morning so it’ll be interesting to see what comes of that. We start Wednesday closer to home with GDP in the UK. Later in the day we’ll see mortgage applications out of the US, closely followed by another raft of prints in the region including durable goods, claims, personal income, new home sales, Michigan confidence and the monthly and year-on-year PCE core and deflator readings are also out. Thursday will bring a break in proceedings with Thanksgiving in the US. However that’s not to say things slow down in Europe with eurozone consumer confidence due along with money supply. The market however will likely be more focused on the CPI, retail sales and unemployment prints for Germany. We round Thursday off with business confidence in Italy and Spanish GDP and CPI. The day after Thanksgiving of course brings the well known ‘Black Friday’ which also coincides with a relatively low data day in the US with just the Chicago PMI. Japan will likely hog the spotlight however with CPI, retail sales, industrial production and housing starts to print. Elsewhere in Asia we get leading indicators out of China. We round the week off in Europe with the all important CPI and unemployment readings for the Eurozone.

end

Two big stories on Iran this morning.

(courtesy zero hedge)

The Iran Nuclear Talks (In 1 Lonely Photo)

Submitted by Tyler Durden on 11/23/2014 16:57 -0500

With President Obama proclaiming this morning “it’s too early to tell” if a nuclear-deal with Iran is still possible; and apparent confirmation this afternoon that differences are “still significant,” the US is said to be discussing extending the nuclear-deal deadline. Yet again no consequences (for a newfound ‘ally’) and yet again John Kerry finds himself purposeless… and now we hear Vladimir Putin will be calling Iran’s Rouhani tomorrow (one can only imagine the topic of conversation).

h/t @Shahr2ad

As Reuters reports, talks between Iran and six powers, which include China and Russia as well as the United States and three big EU countries, are expected to fail to reach a deal to lift U.S. and EU sanctions by a deadline on Monday.

While the deadline, already extended in July, could be extended again, Iranian officials have said they are working on an alternative if the talks collapse altogether, which would see them look east and north for diplomatic and economic support.

“Of course we have a plan B,” a senior Iranian official told Reuters. “I cannot reveal more details but we have always had good relations with Russia and China. Naturally, if the nuclear talks fail, we will increase our cooperation with our friends and will provide them more opportunities in Iran’s high-potential market.”

He added: “We share common views (with Russia and China) on many issues, including Syria and Iraq.”

China is the biggest buyer of Iranian oil and one of the few countries to continue absorbing large volumes of Iranian exports without any big decrease since U.S. and EU sanctions were tightened in the past three years. Russia has sold Iran weapons, built a nuclear power station and could provide technology.

Both countries can provide diplomatic cover at the U.N. Security Council, where they wield vetoes that can help prevent sanctions from be widened.

But…

If the nuclear talks collapse completely – an outcome none of the parties wants – neither China nor Russia can stop the United States and European Union from taking unilateral steps outside the United Nations to expand the painful energy and financial sanctions that hobbled the Iranian economy since 2011.

However, it seems ‘another’ nation may be about to align towards the Russia-China axis… (via Sputnink News)

Russian President Vladimir Putin is planning to have a phone conversation on Monday with his Iranian counterpart Hassan Rouhani, Russian Foreign Minister Sergei Lavrov said on Sunday during his meeting with Iran’s Foreign Minister Javad Zarif.

“Tomorrow, he [Putin] plans to talk to Rouhani, the administrations are in touch,” Lavrov said.

* * *

The more the west pushes, the greater the impetus for ending the unipolar reign of the Petrodollar.

In what is hardly a surprising outcome, the parties involved in the Iran nuclear talks have decided it best for all to extend (and pretend) the discussion for another 7 months:

- *IRAN NUCLEAR TALKS EXTENDED UNTIL JULY 1, OFFICIALS SAY

Diplomatic teams will reconvene in December and the US State Department is proclaiming “good progress” in a brief statement. 7 more months of sanctions, a call with Putin today, and OPEC later in the week… one wonders if any of this will be relevant in 7 months. Additionally, it seems beggars can be choosers as P5+1 says Iran can get $700 million per month in frozen assets back…

One of the primary sticking points in this round of talks has been how to lift sanctions against Iran.

Hardliners in Iran have insisted that significant sanctions be lifted right away as a sign of good faith from the P5+1 countries. Such penalties, including banking and energy sanctions, would affect tens of billions of dollars.

Earlier this month, 200 Iranian members of parliament signed a statement demanding that Iranian negotiators “vigorously defend” the country’s nuclear rights and ensure a “total lifting of sanctions.”

But P5+1 members have said they’d prefer to lift the sanctions incrementally so they can have leverage on Iran and to make sure Tehran makes good on its commitments to whatever deal is reached.

…

Reaching a deal by the deadline “would be impossible” based on the differences that remain between negotiators, the Iranian Students’ News Agency reported Sunday, citing an unidentified Iranian official involved in the talks.

Before Monday’s extension of talks, a U.S. State Department official said negotiators had been “chipping away” at the issues.

“The focus of discussions remains on an agreement, but we are discussing both internally and with our partners a range of options for the best path forward,” the official said.

This isn’t the first time negotiations over Iran’s nuclear program have been extended. The previous deadline had been pushed back four months, to this round of talks.

* * *

It seems, once again, beggars can be choosers and consequences are a thing of the past anyway…

- *IRAN TO GET $700M IN FROZEN ASSETS PER MONTH, U.K. SAYS: AFP

- *IRAN SAYS TO RECEIVE $700 MLN/MONTH UNDER EXTENSION: Lavrov

So deal extended, no benefits for West… but you can have some of your funds back… *as long as you keep pressuring OPEC to keep oil prices low (but not too low)

Gold & EUR Drop After ECB’s Coeure Counters Weidmann’s Warnings

More of the same blather from Europe as following Weidmann’s earlier comments with regard the high-hurdles that the ECB still faces over sovereign QE, Coeure has come out to counter that by noting that the ECB does not have to see deflation to act and that they want to have a discussion of asset-purchases next week. EUR faded the Weidmann gains and Gold and silver are sliding as USD strengthens.

The head of Germany’s Bundesbank cautioned the European Central Bank on Monday about the legal hurdles it would face in embarking on money printing to buy government bonds, underlining its opposition to such a move.

“Instead of focusing on the purchasing programme, we should focus on how you find growth,” Weidmann told an audience in Madrid, when asked about the possibility of the ECB purchasing bonds issued by euro zone states.

He warned that it would be difficult to pursue such steps to lift low price inflation, a key yardstick of economic health.

“Of course there are other measures which are more difficult, because they are untested, because they are less clear … and of course they hit the legal limits of what you can do,” said Weidmann.

“This is why discussions are so intense,” he added, having earlier highlighted “high legal hurdles” to any financing of states.

Then Coeure…

- *COEURE SAYS ECB WANTS TO HAVE ASSET-BUYING DISCUSSION NEXT WEEK

- *COEURE SAYS ECB MUST DISCUSS ALL OPTIONS ON BUYING NEW ASSETS

- *COEURE: LOW INFLATION AS BAD AS DEFLATION REGARDING DEBT IMPACT

- *COEURE SAYS ECB DOESN’T NEED TO SEE DEFLATION TO BE WORRIED

- *COEURE SAYS ECB WILL HAVE SERIOUS, PRINCIPLE-BASED DISCUSSION

And this…

Charts: bloomberg

Brent Plunge To $60 If OPEC Fails To Cut, Junk Bond Rout, Default Cycle To Follow

While OPEC has been mostly irrelevant in the past 5 years as a result of Saudi Arabia’s recurring cartel-busting moves, which have seen the oil exporter frequently align with the US instead of with its OPEC “peers”, and thanks to central banks flooding the market with liquidity helping crude prices remain high regardless of where actual global spot or future demand was, this week everyone will be refreshing their favorite headline news service for updates from Vienna, where a failure by OPEC to implement a significant output cut could send oil prices could plunging to $60 a barrel according to Reuters citing“market players” say.

By way of background, the key reason OPEC is struggling to remain relevant is because, as the FT reported over the weekend, “US imports of crude oil from Opec nations are at their lowest level in almost 30 years, underlining the impact of the shale revolution on global trade flows. The lower dependence on imports from the cartel, which pumps a third of the world’s crude, comes amid advances in hydraulic fracturing that has propelled domestic US production to about 9m barrels a day – the highest level since the mid-1980s.”

The US “shale miracle” is best seen on the following chart showing the total output of the US compared to perennial crude powerhouse, Saudi Arabia:

It is this shale threat that has become the dominant concern for OPEC, far beyond whatever current US national interest are vis-a-vis Ukraine, and Russia’s sovereign oil revenues, and as reported previously, Brent has to drop below to $75 or lower for US shale player to one by one start going offline.

Unfortunately, it may bee too little too late for the splintered cartel. As Bloomberg reports, “the days when OPEC members could all but guarantee consensus when deciding production levels for oil are long gone, according to a veteran of almost two decades of the group’s meetings.”

The global glut of crude, which has contributed to a 30 percent decline in prices since June 19, has left the Organization of Petroleum Exporting Countries disunited and dependent on non-members to shore up the market, said former Qatari Oil Minister Abdullah Bin Hamad Al Attiyah. The 12-member group is set to meet in Vienna on Nov. 27.

“OPEC can’t balance the market alone,” Al Attiyah, who participated in the group’s policy meetings from 1992 to 2011, said in a Nov. 19 phone interview. “This time, Russia, Norway and Mexico must all come to the table. OPEC can make a cut, but what will happen is that non-OPEC supply will continue to grow. Then what will the market do?”

…

“OPEC had been enjoying easy meetings, and decisions were taken without a sweat,” Al Attiyah said. “Now the situation is different.”

Oil markets are oversupplied by about 2 million barrels a day, and global economic growth is below expectations, he said. “The U.S., which was a major market for OPEC, is no longer welcoming imports.It’s now striving to become an oil exporter. It’s already exporting condensates.”

So if OPEC is unable to reach an agreement, what is the worst case? Back to Reuters, which says that “The market would question the credibility of OPEC and its influence on global oil markets if there was no cut,” said Daniel Bathe, of Lupus alpha Commodity Invest Fund.

That could send Brent down to around $60, Bathe said.