My website is now ready You can find my site at the following url:

http://www.harveyorganblog.com or www .harveyorgan.wordpress.com

I will continue to send the comex data down to my good friends at the Doctorsilvers website on a continual basis.

They provide the comex data. I also provide other pertinent data that may interest you. So if you wish you can view that part on my website.

Gold: $1199.20. down $18.80

Silver: $16.41 down $0.14

In the access market 5:15 pm

Gold $1199.00

silver $16.48

The gold comex today had another good delivery day, registering 1,150 notices served for 1,150,000 oz. Silver comex registered 174 notices for 870,000 oz.

A few months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 245.45 tonnes for a loss of 58 tonnes over that period.

In silver, the open interest fell by a huge 5390 contracts despite Monday’s huge gain in price of $1.49. Looks like some of the shorts are vacating the arena. For the past year, we have been witnessing massive liquidation of contracts despite the fact that it cost nothing to roll. This makes no sense and it smacks of cash settlements which are totally illegal. Since I have been following comex data, I have never witnessed such a massive liquidation in both gold and silver these past 5 days. The total silver OI still remains relatively high with today’s reading at 150,718 contracts. The big December silver OI contract lowered by 809 contracts down to 926 contracts.

In gold we had a tame loss in OI despite the huge gain in price of gold yesterday to the tune of $42.80. The total comex gold OI rests tonight at 372,025 for a loss of 834 contracts. The December gold OI rests tonight at 3609 contracts. As mentioned above we lost only 834 contracts despite the fact that it costs nothing to roll..

TRADING OF GOLD AND SILVER TODAY

GOLD

Gold was hit immediately in yesterday’s access market due to the fact that the banking cartel never allow gold to rise for two consecutive days. The other goal was to keep gold below $1200.00. It is my belief that above that level it is very toxic to the bankers due to the huge derivatives placed on gold to keep it suppressed.

Gold hit it’s zenith at 2 am (first London fix) with a price of $1209.00 From there it was downhill, where it hit rock bottom at $1193.25. From there it straddled the 1200 dollar level until comex closing and access market closing. ($1199.20 and 1199.00)

Silver

was much more volatile and this is good as it seems the bankers are losing control of their favourite whipping boy.

At midnight silver was $16.31

At first London fixing: $16.43

At it’s nadir at 8 am: $16.10

At 8:20 comex opening: $16.41

At 11 am: its zenith at $16.49

and it generally stayed there until comex closing.

Today, we had a huge increase in tonnage of gold Inventory at the GLD / inventory rests tonight at 720.02 tonnes.

In silver, we had a huge increase in silver inventory of 2.20 million oz:

SLV’s inventory rests tonight at 350.158 million oz.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today.

First: GOFO rates:

all rates moved closer to the positive but still in backwardation!!

Now, all the months of GOFO rates( one, two, three six month GOFO remain negative but moved closer to the positive needle. They must have found a few bars to lease. On the 22nd of September the LBMA stated that they will not publish GOFO rates. However today we still received today’s GOFO rates.

It looks to me like these rates even though negative are still fully manipulated.

London good delivery bars are still quite scarce.

The backwardation in gold is incompatible with the raid on gold . It does not make any economic sense.

Dec 2 2014

1 Month Rate: 2 Month Rate 3 Month Rate 6 month rate 1 yr rate

-3825.% – 2800 -% -2050 -% – 04 .% + 035%

Dec 1 2014:

-..5825% -.46500% -,3150 % -12333% +00667%

end

Let us now head over to the comex and assess trading over there today,

Here are today’s comex results:

The total gold comex open interest fell again by 834 contracts from 372,859 all the way down to 372,025 with gold up by $42.80 yesterday (at the comex close). We are now into the big December contract month where the number of OI standing for the gold metal registers 3609 contracts for a loss of 927 contracts. We had 109 delivery notices yesterday so we lost 818 contracts or 81,800 oz of gold standing for the December contract month. The non active January contract month rose by 485 contracts up to 826. The next big delivery month is February and here the OI fell to 236,278 contracts for a loss of 2637 contracts. The estimated volume today was poor at 110,510 . The confirmed volume yesterday was huge at 370,767 with the help of high frequency traders. We had 1,150 notices filed for 115,000 oz .

And now for the wild silver comex results. Silver OI surprisingly fell by 4,390 contracts from 155,108 down to 150,718 as silver up by $1.49 yesterday. I do believe we lost a few bankers. The big December active contract month saw it’s OI fall by 809 contracts down to 926 contracts. We had 517 notices served upon for Monday’s delivery. Thus we lost 292 contracts or 1,460,000 oz will not stand. The estimated volume today was fair at 36,563. The confirmed volume yesterday was huge at 129,796. We also had 174 notices filed today for 870,000 oz today.

December initial standings

Dec 2.2014

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 32.15 oz (Manfra) 1 kilobar |

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 3215.000 ozScotia (100 kilobars) |

| No of oz served (contracts) today | 1150 contracts(115,000 oz) |

| No of oz to be served (notices) | 2459 contracts ( 245,900 oz) |

| Total monthly oz gold served (contracts) so far this month | 1841 contracts (184,100 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

69,964.360 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

we had 0 dealer deposits:

total dealer deposit: nil oz

we had 1 customer withdrawal

i) Out of Manfra: 32.15 oz (1 kilobar)

we had 1 customer deposit:

i) Into Scotia; 3,215.000 oz (100 kilobars)

total customer deposits : 3,215.000 oz

We had 2 adjustments:

i) Out of Manfra:

We had 1,224.725 oz removed from the dealer Manfra and this landed into the customer account of Manfra.

Manfra has approximately 10,000 or or .31 of a tonne left in its dealer account.

ii) Out of Scotia:

59,683.04 oz was adjusted out of the customer account at scotia and this landed into the dealer at Scotia

Total dealer inventory: 871,329.222 oz or 27.10 tonnes

Total gold inventory (dealer and customer) = 7.891 million oz. (245.45) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 58 tonnes have been net transferred out. We will be watching this closely!

Today, 0 notices was issued from JPMorgan dealer account and 501 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1150 contracts of which 587 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the December contract month, we take the total number of notices filed for the month (1841) x 100 oz to which we add the difference between the OI for the front month of December (3609) – the number of gold notices filed today (1150) x 100 oz = the amount of gold oz standing for the December contract month.

Thus the initial standings:

1150 (notices filed for the month x 100 oz + (3609) OI for November – 1150 (# of notices filed today equals 430,000 oz standing for the December contract month or 13.375 tonnes)

we lost a massive 818 contracts 81,800 oz standing.

This initiates the month of December for gold.

And now for silver

Dec 2/2014:

December silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | 612,489.09 oz CNT |

| Withdrawals from Customer Inventory | 2,981.25 oz(Delaware) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 600,072.55 oz (Brinks) |

| No of oz served (contracts) | 174 contracts (874,000 oz) |

| No of oz to be served (notices) | 752 contracts (3,760,000 oz) |

| Total monthly oz silver served (contracts) | 2305 contracts (11,525,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 612,489.09 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 2981.25 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 1 dealer withdrawal:

i) Out of CNT: 612,489.09 oz

total dealer withdrawal: 612,489.09 oz

We had 1 customer withdrawal:

i) Out of Delaware: 2981.250 oz

total customer withdrawal 2981.25 oz

We had 1 customer deposits:

i) Into CNT: 600,072.55 oz

total customer deposits: 600,072.55 oz

we had 1 adjustment

i) Out of the Delaware vault:

94,490.544 oz was adjusted out of the customer account and into the dealer account at Delaware

Total dealer inventory: 64.679 million oz

Total of all silver inventory (dealer and customer) 177.975 million oz.

The total number of notices filed today is represented by 174 contracts or 870,000 oz. To calculate the number of silver ounces that will stand for delivery in December, we take the total number of notices filed for the month (2305 ) x 5,000 oz to which we add the difference between the total OI for the front month of December (926) minus (the number of notices filed today (174) x 5,000 oz = the total number of silver oz standing so far in November.

Thus: 2305 contracts x 5000 oz + (926) OI for the November contract month – 174 (the number of notices filed today) =15,285,000 oz of silver that will stand for delivery in December.

we lost 1,460,000 oz standing.

For those wishing to see data on the currencies and bourse closings you can see it on my site

athttp://www.harveyorgan.wordpress.com or http://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

December 2/2014; wow!! we had a huge addition of 2.39 tonnes of gold /Inventory 720.02 tonnes

December 1.2014: no change in gold inventory at GLD

Nov 28.2014: a loss in inventory of 1.19 tonnes/tonnage 717.63 tonnes

Nov 26.2014: we lost 2.09 tonnes of gold heading to India and or China/inventory at 718.82 tonnes

Nov 25.2014/no change in tonnage of gold inventory at the GLD/inventory at 720.91 tonnes

Nov 24.2015: no change in tonnage of gold inventory at the GLD/inventory at 720.91 tonnes

Nov 21.2014: no change in tonnage of gold inventory at the GLD/inventory 720.91 tonnes

Nov 20.2014; no changes in tonnage of gold at the GLD/tonnage 720.91 tonnes

Nov 19.2014: we lost 2.1 tonnes of gold/Inventory back to 720.91 tonnes. No doubt physical gold is heading to China.

Nov 18.2014: no change in inventory/ Inventory level 723.01 tonnes

Nov 17.2014; we had a huge addition of 2.39 tonnes of gold added to the GLF inventory/inventory rests tonight at 723.01 tonnes. They may be running out of metal to give China!!!

Nov 14. we had no change in gold inventory at the GLD/inventory 720.62 tonnes

nov 13. we lost another 2.05 tonnes of gold at the GLD/Inventory at 720.62 tonnes

Nov 12.2014; we lost another 1.79 tonnes of gold at the GLD/Inventory at 722.67 tonnes

This gold left the shores of England and landed in Shanghai.

Today, December 2 a huge addition of 2.39 tonnes of gold inventory at the GLD. It looks like the gold inventory at the Bank of England is running dry.

inventory: 720.03 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 720.03 tonnes.

end

And now for silver: wow@!!@ a huge addition of 2.20 million oz of silver/inventory 350.158 million oz.

December 1: no change in inventory/347.954 million oz

Nov 28.2014: no change in inventory/347.954 million oz

Nov 26.2014; no change in inventory/347.954 million oz

Nov 25.14 we had a loss of 1.342 million oz from the SLV/inventory 347.954 million oz

Nov 24.2014: no change in silver inventory at the SLV/Inventory 349.296 million oz

Nov 21.2014: no change in silver inventory at the SLV

Inventory: 349.296 million oz

Nov 20.2014; no change/inventory 349.296 million oz

Nov 19.2014: a huge addition of silver inventory to the tune of 2.396 million oz/inventory 349.296 million oz

Nov 18.2014; no change in silver inventory 346.90 million oz

Nov 17.2014 .SLV inventories remain constant tonight at 346.90 million oz

Nov 14.2014; wow!! we had an addition of 2.012 million oz into the SLV/inventory at 346.900 million oz

Nov 13. no change in silver inventory at the SLV/344.888 million oz.

Nov 12.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz. And please note that gold leaves GLD/silver does not. Why? there is no physical silver at the SLV..just paper obligations.

Nov 11.2014: no change in silver inventory at the SLV/inventory rests tonight at 344.888 million oz.

December 2.2014 a huge addition in inventory of 2.20 million oz/350.158 million oz.

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now deeply into the positive to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 10.5% percent to NAV in usa funds and Negative 10.7% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.6%

Percentage of fund in silver:37.80%

cash .6%

( December 2/2014)

2. Sprott silver fund (PSLV): Premium to NAV falls to positive 2.32% NAV (Dec 2/2014)

3. Sprott gold fund (PHYS): premium to NAV falls to negative -0.37% to NAV(Dec 2/2014)

Note: Sprott silver trust back hugely into positive territory at 2.32%.

Sprott physical gold trust is back in negative territory at -0.37%

Central fund of Canada’s is still in jail.

end

At 3:30 pm we got the COT report.

First gold;

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 167,394 | 91,187 | 31,561 | 156,334 | 224,819 | 355,289 | 347,567 |

| Change from Prior Reporting Period | ||||||

| -20,561 | -15,346 | -13,165 | -37,334 | -39,846 | -71,060 | -68,357 |

| Traders | ||||||

| 110 | 90 | 78 | 51 | 58 | 204 | 193 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 32,856 | 40,578 | 388,145 | ||||

| -452 | -3,155 | -71,512 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, November 25, 2014 | |||||

Our large specs:

Those large specs that have been long in gold pitched a huge 20,561 contracts from their long side

Those large specs that have been short in gold covered 15,346 contracts from their short side.

Our commercials:

Those commercials that have been long in gold pitched a mammoth 37,334 contracts from their long side ???

Those commercials that have been short in gold covered a monstrous 39,846 contracts from their short side.

Our small specs:

Those small specs that have been long in gold pitched a tiny 482 contracts from their long side

Those small specs that have been short in gold covered a rather large 3155 contracts from their short side.

And now for silver:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 52,883 | 37,427 | 16,352 | 65,268 | 87,311 | |

| -3,948 | -7,650 | -2,390 | -8,868 | -5,192 | |

| Traders | |||||

| 71 | 69 | 49 | 41 | 48 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 156,984 | Long | Short | |

| 22,481 | 15,894 | 134,503 | 141,090 | ||

| -885 | -859 | -16,091 | -15,206 | -15,232 | |

| non reportable positions | Positions as of: | 139 | 143 | ||

| Tuesday, November 25, 2014 | © SilverSeek.com | ||||

Our large specs:

Those large specs that have been long in silver pitched a rather large 3948 contracts from their long side

Those large specs that have been short in silver covered a huge 7650 contracts from their short side???

Commercials;

Those commercials that have been long in silver pitched a huge 8668 contracts from their long side??

Those commercials that have been short in silver only covered 5,192 contracts from their short side???

Small specs:

Those small specs that have been long in silver pitched 855 contracts from their long side

Those small specs that have been short in silver covered 859 contracts from their short side.

end

And now for your most important physical stories on gold and silver today:

Early gold trading from Europe early Monday morning:

US Debt Reaches $18 Trillion; Surges 70% In ‘Recovery’ of President Obama

Total U.S. national debt hit a new record high overnight at over $18 trillion as the Obama administration continues to pile debt onto the back of the U.S. taxpayer at a rate that would have made George W. Bush look positively prudent.

A sudden fall in stock markets globally made traders nervous and likely contributed to gold’s safe haven bounce.

With the U.S. national debt or government debt now at over a staggering $18 trillion, it means that each household in the U.S. now carries the burden of $124,000 in national debt alone – or $56,378 per individual. This does not include the massive private debt or household debt burden – people’s mortgages, personal loans, credit card debt, student loans, car loans and other household debt.

When Obama took office in 2009, the national debt had surged to $10.6 trillion up from $3 trillion at the beginning of Bush’s tenure in 2001.

The total U.S. debt has increased by 70% under Obama, from $10.625 trillion on January 21, 2009 to over $18.005 trillion today

In short, the federal government has borrowed, and spent, nearly $7.5 trillion more since President Obama took office than it has collected in taxes.

Obama’s policies have continued to favour Wall Street and corporate interests over Main Street.

As ever, historical context is all important. The U.S National Debt took 43 Presidents from 1789 until 2008 to reach $10 trillion. The National Debt rose $4.899 trillion during the two terms of the Bush presidency. It has now gone up nearly $8 trillion since President Obama took office.

The U.S. national debt is spiralling out of control, seemingly without any plan to ever reign it in and yet the rise above $18 trillion was not reported in mainstream media.

Brillig.com

Compared to this time last year, the national debt has grown by another $1 trillion.

Astoundingly, more than $7 trillion of additional US national debt will have been accumulated over the 8 year duration of Obama’s two presidencies, which is more than the accumulated U.S. national debt of all previous U.S. presidents combined.

This is not to mention the astronomical expenses of more than $200 trillion of U.S. government unfunded liabilities such as medicare, medicaid and social security.

Household debt–including mortgages, credit cards, auto loans and student loans — remains close to $12 trillion.

The U.S. debt position increasingly has all the hallmarks of a Ponzi scheme. The Daily Treasury Statement that was released last Wednesday afternoon as Americans were preparing to eat turkey on Thanksgiving revealed that the

U.S. Treasury has been forced to issue $1,040,965,000,000 in new debt since fiscal 2015 started. This is just eight weeks ago. they had to do this in order to raise the money to pay off Treasurysecurities that were maturing and to cover new deficit spending by the government.

During those eight weeks, Treasury took in $341,591,000,000 ($341 billion) in revenues. That was a record for the period between October 1 and November 25. But that record $341,591,000,000 ($341 billion) in revenues was not enough to finance ongoing government spending let alone pay off old debt that matured.

A conservative measure of the U.S. National Debt to GDP ratio is now around 103%. The talking heads have, for many years, downplayed the out of control spending of successive administrations with the justification that it was below the “psychologically important” debt to GDP ratio of 100%.

Well, here we are now over 100% and all is quiet.

The Total U.S. Debt to GDP ratio is now over 300%. Such debt levels ordinarily give rise to debt crises and currency crises.

So how can we expect this scenario to play out? If it hasn’t mattered thus far why should it matter now? Well for one, U.S. government profligacy has been protected by the extraordinary status that the dollar has enjoyed as a reserve currency since the early 1970s and Nixon going off the Gold Standard.

Heretofore, almost all balance of trade deficits have been settled with dollars. All oil transactions have been settled in dollars. This has allowed the U.S. an “exorbitant privilege” in the words of Valéry Giscard d’Estaing, the former French Minister of Finance. It has allowed the U.S. to live beyond its means because its currency remained in demand regardless of its economic performance.

Over the course of this year, however, the dollar has taken what should be seen as an alarming series of blows to its status as trusted sole global reserve currency ascurrency wars intensify.

Increasingly, the new power bloc that are the BRICS nations are settling their trade deficits with domestic currencies, by-passing the dollar. Russia and Turkey have just signed a gas-line agreement to this effect. As have russia and the emerging superpower China.

There is a perception that the U.S. dollar is still strong and is still the reserve currency of choice.

This is based on the strong performance of the Dollar Index as of late. It is important to note the distinction between the dollar and the Dollar Index. The index rates the dollar relative to a basket of other mainly western currencies, primarily the euro. The recent “strength” of the dollar is merely strength against these other struggling currencies including the euro.

Russia’s foreign minister, Sergei Lavrov, pointed out last week that “the seven developing economies headed by BRICS already have a bigger GDP than the Western G7.” This drives home the message that the economic might of the U.S. is waning. It is doubtful whether it will be able to re-establish or indeed maintain the Bretton Woods paradigm which gave the dollar it’s preeminent status.

Another major cause for concern should be the impending rise in interest rates. The ability of the U.S. to service its debt will be drastically reduced if rates move higher. Already a number of states have defaulted. The luxury of determining interest rates may not be one that the Fed will enjoy for very much longer. When rates do finally rise we may witness the default of the U.S..

If this spectre comes to pass – and possibly independent of it – there will be demand for a new store of wealth. History teaches us, regardless of our own philosophical or economic outlook, that gold will be one such store.

The BRICs countries are major purchasers of gold – both their people and their central banks. If economic influence is moving East it would be prudent to emulate them and acquire gold as a store of value. As always, we advocate allocated and segregated gold coins and bars in secure vaults and in safe jurisdictions around the world.

This continuing surge in the U.S. national debt means that the U.S. is now the largest debtor nation in the world – by a significant margin. This profligacy will be paid back by the American people, and most likely by people every where, in the form of higher taxes, higher interest rates, inflation and almost certainly currency crises.

Get Breaking News and Updates On Gold Markets Here

MARKET UPDATE

Today’s AM fix was USD 1,197.00, EUR 962.68 and GBP 761.60 per ounce.

Yesterday’s AM fix was USD 1,178.75, EUR 945.46 and GBP 750.56 per ounce.

Gold climbed $45.60 or 3.91% to $1,212.60/oz yesterday. Silver soared $1.03 or 6.67% to $16.47/oz and surged nearly 17% from the interday low. Such volatility and intra-day reversals frequently presages a bottom.

Gold’s rally was likely due to technical buy signals and a short squeeze, robust demand from China and India with the potential for increased Indian imports. GOFO backwardation continues suggesting stresses in the physical inter bank market for large London good delivery bars.

A sudden fall in stock markets globally made traders nervous and likely contributed to gold’s safe haven bounce.

Gold has fallen marginally today and is testing the $1,200/oz level today. The greenback rose to the highest since 2009 yesterday amid continual hints and suggestions that the Federal Reserve will raise interest rates next year.

With the U.S. national debt surging another $1 trillion in recent months to over $18 trillion, it is difficult to see how interest rates can be raised in any meaningful way without creating an economic collapse. This is not too mention the huge levels of private debt at every level of American society and indeed the unfunded liabilities of between $100 trillion and $200 trillion.

The precious metals group climbed as crude oil went south and dropped to its lowest price in 5 years prior to a sharp bounce.

Silver for immediate delivery dropped 1.7% to $16.183 an ounce in London. It rebounded yesterday from a five-year low of $14.4235 to settle 6.5% higher, the biggest gain since January 2012.

Platinum slid 1.7% to $1,217.50 an ounce. Prices gained 3.2% yesterday, the most since August 2013. Palladium lost 0.7% to $802 an ounce.

Essential Guide to Storing Gold Bullion In Switzerland

end

The CME is surely out to protect somebody here:

The hedge funds are so deep in trouble. Maybe the extra margin is to help the bankers who loaned these hedge funds the money. Thoughts anyone?

(courtesy CME/zero hedge)

CME Hikes Crude Oil Margins For Second Time In A Week

The last time the CME hiked margins across the entire crude oil space was one short week ago, on Tuesday to be specific, when the most important contract, the CL Crude Oil Future, saw its initial margin rise by a little over 4%, from $4070 to $4235.

However, as last week’s subsequent events clearly showed, the margin hike was nowhere near enough to bring some stability to the market, when the crude plunge accelerated toward the end of the week, leading to a near-record rout in the product.

Which perhaps is why moments ago the CME once again hiked both initial and maintenance margins across the board for some 151 pages worth of futures contracts, only this time the required cash for initial positions or to maintain existing spec bets for the front month contract was increased four times as much, from $4235 to $4895…

… which means the weekly increase in crude margins is now about 20%, which also means that those specs who were in margined, money-losing positions until today, will have to pony up substantially more cash, or else the crude dump will resume and rather quickly. Unless of course, the recently most margined positions happen to be new shorts, who would now rush to cover.

end

A little history lesson for you tonight. For centuries the biggest company in the world was VOC (Dutch East India Company). They controlled the shipping lanes for centuries and provided a dividend on average of 18% per year. As author Simon Black states the Dutch are very savvy people. So when the government reiterates the following:

The Central Bank’s official statement itself said “this may also contribute to a positive confidence effect with the public.”

and according to Simon:

Translation: The US is not to be trusted anymore with the custody of our gold.

his view is a little different from James Turk

(courtesy Simon Black/Sovereign Man)

end

This Was The Most Valuable Company In History (Worth 10 Times More Than Apple)

Submitted by Simon Black via Sovereign Man blog,

Over four centuries ago, the Dutch East India Company made history as the world’s first IPO.

Known as VOC in the Netherlands, the company was one of the most successful ventures in the last several hundred years.

When adjusted for inflation, its highest market capitalization would be worth over $7 TRILLION today (i.e. ten times the size of Apple).

More importantly, it completely dominated the Asian trade in the 17thand 18th centuries.

While the British East India Company is usually more famous nowadays, VOC had almost twice as many ships and moved five times more cargo than its British rivals.

The company was so successful over the long-term that it paid an astonishing 18% annual dividend to its shareholders for almost 200 years.

* * *

Given their long tradition of being financially savvy, when the Dutch do something dramatic in the financial markets, it’s important to take notice.

Which is why when the Dutch Central Bank recently announced they had just moved 122.5 tons of gold, worth $5 billion, from storage in New York back to Amsterdam everyone’s alarm bells should be ringing.

The Central Bank’s official statement itself said “this may also contribute to a positive confidence effect with the public.”

Translation: The US is not to be trusted anymore with the custody of our gold.

It’s becoming so obvious where things are headed.

It’s easy to dismiss gold repatriation when “foes” like Venezuela were doing it.

But when your own allies think you’re not to be trusted as a custodian of their gold—that’s the end of your credibility.

What does this mean to you?

The whole system that’s based on the dominance of the US dollar and the US financial institutions is in clear decline.

Governments and businesses are screaming for alternatives and some are actively pursuing them.

The US has spent the last several years debasing its currency. The Fed’s balance sheet has exploded by 529% since 2008.

The US federal government is now just hours away from hitting $18 trillion in debt.

Yet they continue to run up huge deficits, blowing their tax revenue on more bombs, drones, wars, and body scanners.

They slam foreign businesses with enormous fines (up to $9 billion) for doing business in countries the US doesn’t like.

Meanwhile they brazenly and arrogantly spy on their ‘allies’, let alone their own citizens.

Is it any wonder they have lost credibility?

Bear in mind that the US government’s power – and the dollar’s prominence – are based almost exclusively on US credibility.

Where do you think the trend for the dollar is headed when America’s own allies no longer trust the government?

end

Popcorn anyone?

(courtesy hedge)

With Its Gold “Vaporized”, A Furious Ukraine Turns On Its Central Bankers

As reported two weeks ago, following a stunning announcement by the head of Ukraine’s central bank, Valeriya Gontareva, on primetime TV we learned that (virtually) all of Ukraine’s gold was gone, or – in the parlance of Jon Corzine – had “vaporized.”

And as we also predicted two weeks ago, it was only a matter of time before Ukraine’s people – the vast majority of whom are innocent pawns in a vast game of realpolitik between the west and east – finally got angry and demanded some answers, if not heads. That time came earlier today when as Interfax.ua reported “a Kyiv-based court has instructed Kyiv prosecutors to bring an action against National Bank of Ukraine (NBU) Governor Valeriya Gontareva on charges of abuse of power or misuse of office to obtain illegal profit, the Vesti newspaper reported on Tuesday.”

According to Interfax, “This decision was taken by Kyiv’s Pechersk district court on December 1 after it had examined case No. 757/33660/14. It ordered the Kyiv prosecutor’s office to launch an investigation and include it in the register of pre-trial investigations,” the newspaper reported.

Gontareva is charged with abuse of power or misuse of office under Article 364 of the Criminal Code of Ukraine.

The plaintiff is lawyer Rostyslav Kravets, the newspaper said. He confirmed this information in his post on Facebook, saying that the decision was taken by the court at the third attempt, and in November 2014, the prosecutors declined to bring an action to meet his claim.

The charges against the chief banker involve foreign currency interventions by the Central Bank in August 2014: On August 5 the NBU bought U.S. dollars on the interbank forex market for UAH 11.93 per U.S. dollar and sold them for UAH 12.26 per U.S. dollar. During the same week, on August 8, it traded in foreign currency at a higher rate: UAH 12.45-12.6 per U.S. dollar. First it sold $69 million on the interbank forex market at a lower rate, and some days later it bought $35 million at a more favorable price.

As a result of these transactions, the NBU lost 19 kopecks per U.S. dollar, Kravets said.

Kravets claims that by acting so, Gontareva “has intentionally committed an extremely unfavorable transaction for the gold and forex reserves of Ukraine, despite the fact that under Ukraine’s Constitution it is the Central Bank that is in charge of maintaining the country’s gold reserves.”

* * *

That, and of course, there is also that as a result of central bank “transactions” the Ukraine central bank is now essentially gold-free, which per Gontareva’s recent appearance, has just 1% of total reserves in the form of the yellow metal.

And while it remains to be seen if this will be the spark that lights the counter-revolution (after all it took Egypt not less than a year to turn against the puppet regime dumped upon it by the CIA and the US State Department) others are already sensing which way the wind is blowing. As Bloomberg reported moments ago, another central banker, Olena Shcherbakova who is head of the monetary policy department at the Ukrainian central bank, said she is resigning. When reaced by phone she stated that she “has the right to step down,” without giving reason for decision.

She sure does, although we doubt even a former Goldman Sachs partner would be willing to replace her, as the realization among the Ukraine people finally seeps through that they were thoroughly betrayed by the same people who promised they would fix the country following the February presidential coup.

end

Perth Mint’s silver sales jump to 10-month high in November

Reuters Dec 1, 2014, 02.59PM IST

SINGAPORE: The Perth Mint’s silver sales in November climbed to their highest since January as lower prices attracted retail investors, while gold sales fell to a three-month low.

The Perth Mint runs the only gold refinery in Australia, the world’s second-biggest gold producer after China.

Silver coin sales jumped to 851,836 ounces in November from 655,881 ounces in October, data on the mint’s website showed

-END-

Chris Powell of GATA explains the manipulation of gold/silver. The result is a rigging of their currencies to fool markets:

(courtesy GATA/Reuters/)

How the global central banks are manipulating the gold price to rig their currencies and fool markets

Posted on 02 December 2014

Central banks around the world are suppressing the gold price in order to defend their currencies, explains Chris Powell, secretary of the Gold Antitrust Action Committee. GATA has accumulated overwhelming evidence of this gold price manipulation to support currencies over decades.

Of course, central banks are not always successful at keeping gold prices down. Yesterday gold prices bounced almost $70 higher as the Swiss voted against an increase in gold reserves in a referendum. Should prices not have fallen? Central banks don’t always get this right…

Chris Powell video link

-END-

Ben Davies talks with Eric King of Kingworldnews

(courtesy Ben Davies/Kingworldnews/GATA)

Markets likely reversing, Hinde Capital CEO Davies tell KWN

12:11p GMT Tuesday, December 1, 2014

Dear Friend of GATA and Gold:

Interviewed by King World News, Hinde Capital CEO Ben Davies elaborates on his call on CNBC Europe Monday morning, hours before the explosive rally in the monetary metals began, that despite recent surreptitious activity in the gold market, the monetary metals have bottomed and markets generally are at an inflection point indicating reversals. An excerpt from Davies’ commentary is posted at the KWN blog here:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/12/2_Wi…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

amazing!!

(courtesy Bloomberg/GATA)

Fed leak tipped traders to historic stimulus move, prompted secret inquiry

But no findings were ever made public.

* * *

By Craig Torres

Bloomberg News

Monday, December 1, 2014

Alarms went off inside the Federal Reserve: the Fed’s innermost secrets had leaked to Wall Street.

Confidential deliberations of the Federal Open Market Committee made their way into a research note circulated among traders.

The report — a fly-on-the-wall account of the FOMC’s September 2012 meeting, with hints of Fed action to come that December — prompted a mole hunt that reached the highest levels of the central bank.

The story of the FOMC leak underscores the lengths to which outsiders will go to penetrate the inner workings of the Fed, and how valuable access can be. The Fed has never disclosed the investigation or its findings. …

In their November memo, Alvarez and English asked officials to disclose any communications with Schleiger and Hilsenrath and to hand over e-mail and phone records. Under Fed rules, the general counsel and FOMC secretary investigate if the chain of confidentiality is broken and report their findings to the chairman.

The Fed has never disclosed the findings.

The Fed’s general counsel can also ask the Fed inspector general to investigate breaches. No specific mention was made of an inspector general investigation into the 2012 FOMC leak in that office’s 2013 reports to Congress.

John Manibusan, a spokesman for the inspector general, declined to comment.

… For the remainder of the report:

http://www.bloomberg.com/news/2014-12-01/fed-leak-handed-traders-profita…

end

(courtesy Dave Kranzler/Dr Craig Roberts)

US Resorts to Illegality to Protect Failed Policies — Paul Craig Roberts & Dave Kranzler

US resorts to Illegality To Protect Failed Policies

Paul Craig Roberts & Dave Kranzler

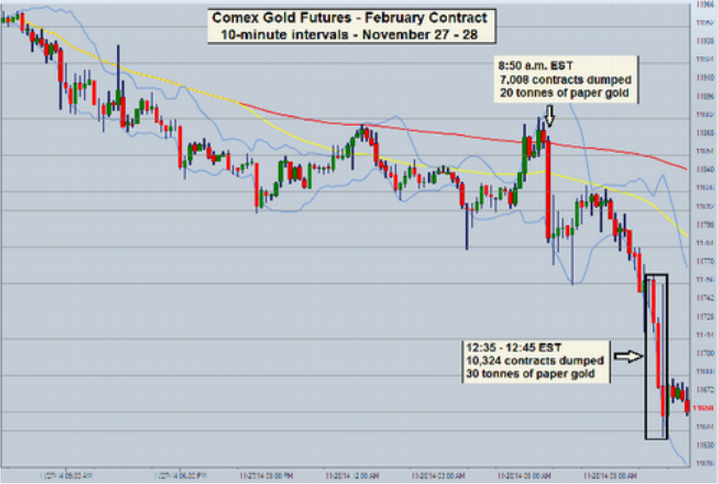

In a blatant and massive market intervention, the price of gold was smashed on Friday. Right after the Comex opened on Friday morning 7,008 paper gold contracts representing 20 tonnes of gold were dumped in the New York Comex futures market at 8:50 a.m. EST. At 12:35 a.m. EST 10,324 contracts representing 30 tonnes of gold were dropped on the Comex futures market:

No relevant news or events occurred that would have triggered this sudden sell-off in gold. Furthermore, none of the other markets experienced any unusual movement (stocks, bonds, currencies).

The intervention in the gold market occurred on the Friday after the U.S. had observed its Thanksgiving Day holiday. It is one of the lowest volume trading days of the year on the Comex.

A rational person who wants to short gold because he believes the price will fall wants to obtain the highest price for the contracts he sells in order to maximize his profits when he settles the contracts. If his sale of contracts drives down the price of gold, he reduces the spread between the amount he receives for his contracts and the price at settlement, thus minimizing his profits, or if the price goes against him maximizing his losses. A bona fide seller speculating on the direction of the gold price would choose a more liquid market period and dribble out his contract sales so as not to cause a significant impact on the price.

As you can see from the price-action on the graph, massive sales concentrated within a few minutes minimize sales proceeds and are at odds with profit maximization. A rational seller would not behave in this way. What we are witnessing in the bullion futures market are short sales designed to drive down the price of bullion. This is price manipulation.

Here is the Security and Exchange Commission’s definition of manipulation:

Manipulation is intentional conduct designed to deceive investors by controlling or artificially affecting the market for a security…[this includes] rigging quotes, prices or trades to create a false or deceptive picture of the demand for a security. Those who engage in manipulation are subject to various civil and criminal sanctions.

Why is manipulation of the price of gold in the futures market not investigated and prosecuted?

The manipulation has been blatant and repetitious since 2011.

The answer to the question is that suppressing the price of gold helps to protect the U.S. dollar’s value from the excessive debt and money creation of the past six years. The attacks on gold also enable the bullion banks to purchase large blocks of shares in the GLD gold trust that can be redeemed in gold with which to supply Asian purchasers. Whether or not the Federal Reserve and the U.S. Treasury are instigators of the price manipulation, government authorities tolerate it as it supports the dollar’s value in the face of an enormous creation of new dollars and new federal debt.

In other words, the illegal rigging of the price of gold in the futures market is deemed by the US government to be essential to the success of its economic policy, just as illegal torture, illegal military invasions and attacks on sovereign countries, unconstitutional violation of habeas corpus, unconstitutional spying on U.S. citizens, and illegal and unconstitutional murder of U.S. citizens by the executive branch are essential to the U.S. government’s “war on terror.”

The U.S. government resorts to massive illegality across the board in order to protect its failed policies. The rule of law and accountable government have been sacrificed to failed policies.

end

A very sad day!!

(courtesy Lipsky/Wall Street Journal/)

Seth Lipsky on Liberty Dollar founder: A monetary gadfly in an age of fiat money

By Seth Lipsky

The Wall Street Journal

Monday, December 1, 2014

Tuesday morning at 9:30, a federal judge in North Carolina will gavel his court into session to pronounce a sentence on Bernard von NotHaus. A monetary gadfly in an age of fiat money, Mr. von NotHaus, 70, could be looking at the rest of his life in prison.

Nearly four years ago, a jury convicted Mr. von NotHaus of “uttering”—putting into circulation—coins of pure silver that he called Liberty Dollars. The government is also seeking the forfeiture of 16,000 pounds of coins and precious metals whose value it reckons at $7 million. …

… Mr. von NotHaus’s Liberty Dollar poses the opposite danger of Copernicus’ famous monetary principle. That principle, also known as Gresham’s law, holds that bad money drives out good. Mr. von NotHaus has instilled in the government the contrary fear — that good money in the form of silver dollars will drive out the bad money issued by the Federal Reserve. …

These matters were considered by Judge Voorhees, who has been presiding in the von NotHaus case. They were raised most pointedly in an amicus brief by the Gold Anti-Trust Action Committee, a charity that fights for a constitutional view of money. …

… For the remainder of the commentary, in the clear:

http://online.wsj.com/articles/seth-lipsky-a-monetary-gadfly-in-an-age-o.

end

Just in case you missed the video of Rob Kirby being interviewed by Greg Hunter, here is the big line:

(courtesy Rob Kirby/Greg Hunter/USAWatchdog/yesterday’s video)

“For large amounts of bullion in the Asian market, the pricing mechanism has completely and utterly divorced itself from the fraudulent paper prices that are being reflected in the exchanges in the Western world.

In the Asian market, if you could find . . . physical bullion . . . as cheap as spot plus 50%, you’d be doing really, really, really well . . . and you’d be hard pressed to find serious tonnage at that price in Asia.”

end

James Turk believes that the 122.5 tonnes of gold that arrived in Amsterdam will not be stored there but leased out by their central bank. I sure hope that this is not so. However the GOFO rates this morning went less negative as it seems that they found some gold to lease. James who is very close to the London market states that many investors of Eastern persuasion are now taking delivery of forwards purchased earlier in the year which is putting huge pressure on the London gold and silver market. Thus the reason for the Dutch recall of their gold to the leased. Of course this presents a massive problem for the uSA who have no doubt hypothecated and rehypothecated many of these bars leaving a huge derivative mess over here.

John Embry is his talk with Eric King highlights the fact that the smash in gold was orchestrated to convince Swiss voters to vote no.

(courtesy James Turk/ John EmbryKingworldnews)

Turk: Dutch gold was returned only for leasing; Embry: Gold was smashed to discourage Swiss

11:21 GMT Monday, December 1, 2014

Dear Friend of GATA and Gold:

The Netherlands central bank, GoldMoney founder and GATA consultant James Turk tells King World News today, probably managed to repatriate its gold from the Federal Reserve Bank of New York because the Netherlands central bank plans to lend it back into the market for price suppression. An excerpt of the interview with Turk is posted at the KWN blog here:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/12/1_Wi…

And Sprott Asset Management’s John Embry tells KWN that last week’s smash of gold in the futures market was probably part of an effort to discourage Swiss voters from supporting the Swiss Gold Initiative proposal at Sunday’s referendum:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/12/1_Sh…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Hugo on his continual fight to create a silver coin in Mexico that constitutes money: the Libertad..

(courtesy Hugo Salinas Price/GATA)

Hugo Salinas Price: A silver coin that is money to calm the national tantrum in Mexico

11:30p GMT Monday, December 1, 2014

Dear Friend of GATA and Gold:

Hugo Salinas Price, president of the Mexican Civic Association for Silver, writes today that his country badly needs some good news and encouragement and he again recommends what could be a mechanism of national pride: monetization of Mexico’s own undenominated silver coin, the Libertad, made from metal drawn from the country’s own soil, money that puts its own people to work. Salinas Price’s commentary is headlined “A Silver Coin That Is Money To Calm the National Tantrum in Mexico” and it’s posted at the association’s Internet site, Plata.com, here:

http://www.plata.com.mx/Mplata/articulos/articlesFilt.asp?fiidarticulo=2…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

The following commentary is a dandy and is a must read….

(courtesy Bill Holter/Miles Franklin)

Oil crashes, who really wins?

I’d like to address the outright crash of the oil market this past week. The hope was the Saudis would cut back on production to stabilize prices somewhere in the $80+ range. This was not to be as Saudi Arabia announced no cutback whatsoever …oil then fell over 10% in one day on Friday and actually traded to a $65 handle. First and most importantly, oil is THE biggest and most widely used commodity on the planet. For a market of this importance to outright crash or rise over 10% in one day, unintended consequences not seen or anticipated can be expected at some point.

end

Early Tuesday morning trading from Europe/Asia

1. Stocks up on major Asian bourses with a lowerer yen value rising to 118.940 ( Moody’s lowering of its investment grade)

2 Nikkei up 73 points or 0.42%

3. Europe stocks all up except Germany /Euro falls/ USA dollar index up to 88.28./

3b Japan 10 year yield at .43% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 117.70

3c Nikkei now above 17,000

3fOil: WTI 67.89 Brent: 71.69 /all eyes are focusing on oil prices. A drop to the mid 60′s would cause major defaults.

3g/ Gold down/yen down;

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt (see Von Greyerz)

3j ruble slides to record lows again (53.24 rubles to the dollar) as brent and WTI fall again

3k Russian 10 yr bond yield: 10.76% up 15 basis points.

3l: Ukraine and rebels may be nearing a truce/thus tensions easing

3m Gold at $1196.00 dollars/ Silver: $16.17

4. USA 10 yr treasury bond at 2.23% early this morning.

5. Details: Ransquawk, Bloomberg/Deutsceh bank Jim Reid

(courtesy zero hedge/your early morning trading from Asia and Europe)

Stocks Rebound, Oil Resumes Slide, Ruble Tumbles As Yen Flirts With 119

Submitted by Tyler Durden on 12/02/2014 07:05 -0500

A few days of near-record crude volatility (which the CME is scrambling to reduce following 2 crude margin hikes in the past week) is giving way to the New Normal default thinking: that central banks will soon take care of everything.

And sure enough, just an hour earlier, US equity futures had jumped 8 points on virtually zero volume, wiping out all of yesterday’s losses, driven higher by that new “old favorite”, the USDJPY, which has once again resumed its climb higher, briefly rising above 119.00 once again and sending the Nikkei and the Topix to fresh 7 year highs, perfectly oblivious to both yesterday’s Moody’s downgrade and now open warnings from both Eisuke Sakakibara andGoldman Sachs that further declines in the Yen will accelerate the collapse of the Japanese economy. And, since there is also zero liquidity in the market, that entire gain was also just as promptly wiped out with futures now practically unchanged from yesterday’s close.

With everyone focused on crude, it is worth noting that both Brent and WTI have resumed their downward trend, down a little over 1% each, following yesterday’s mad short-covering scramble which may have been all the dead cat bounce we will get this time around as Saudi appears perfectly happy to send Brent to $60 or even lower.

The other thing everyone appears to be focused on these days is Russia, which earlier announced its economy would shrink 0.8% next year on oil price drop, sanctions. The immediate result was a sharp reversal in the Ruble, which wiped away all gains and tumbled to another day of record lows against western currencies, sliding 2.3% against the dollar. Comments from VTB Chairman Dubinin who said there was “some panic” in the Russian bank system did not help the mood. The Ruble has now declined 30% since the end of September. Russia’s 5yr CDS widened a further 26bps yesterday to 344bps whilst the 10y government bond yield finished 15bps higher at 10.76%. The moves also come on the back of an announcement by the Finance Minister Siluanov last week that capital flight may reach $130bn in 2014 – the most since 2009.

This morning’s European session initially kicked off on a positive note with the DAX breaking above 10,000 for the first time since June 2014 after tripping stops at the handle, although the index has since come off best levels on concerns over Russian. On a sector specific basis, basic materials and energy names led the way higher for European equities following on from yesterday’s gains in the commodities complex, which subsequently saw some mild outperformance for the FTSE 100. However, gains for oil services names have been limited by news that Russia are to abandon their Southstream pipeline plans. Furthermore, financials are also seen higher in a continuation of the trend seen overnight on the expectation that the PBoC may implement further easing policies. Elsewhere, Bunds have crept higher throughout the European session helped with the decline in equities and thus paring some of yesterday’s fixed income-related losses following positive US ISM manufacturing and rate lock selling due to a large corporate bond issuance.

Switching focus to Asia, the Japan Topix is modestly stronger (+0.49%) and shrugging off Moody’s sovereign rating cut yesterday (to A1/stable from Aa3). For the record, Japan’s foreign currency rating is still AA-/Neg by S&P and A+/Neg by Fitch. The Moody’s action comes just before Prime Minister Abe commences his campaign today ahead of the election later this month. Just on the subject, the Nikkei QUICK monthly bond survey yesterday showed that respondents saw a 79.9% probability that the LDP/Komeito ruling coalition would do better than its stated victory of 270 seats. Away from Japan, with the exception of Korea, major bourses are largely trading in the green. The Hang Seng (+0.74%), Shanghai Composite (+1.80%) and ASX 200 (+1.41%) are all trading firmer. On the latter, the RBA has kept its benchmark rate unchanged at 2.50% (as expected by most) overnight but it is worth noting that our Australian economist now expects a cumulative 50bps cut by the RBA in 2015 citing a forecasts of rising unemployment, nascent signs of moderation in house price growth and ongoing commodity price declines. This is a non-consensus call by DB so we’ll see if the street follows from here.

Looking at today’s calendar, In the US this afternoon we’ve got the ISM NY due with the market expecting a slight uptick to 55.0 (from 54.8). Shortly after, we get the construction spending print which is expected to increase – residential construction in particular is expected to show a decent gain given the improvements in housing permits. We round today off with November vehicle sales data in the US. In terms of Fedspeak, early this afternoon both Fischer and Yellen will be talking in Washington so watch out headlines here.

Bulletin Headline Summary from Bloomberg and Ransquawk

- With the lack of any tier 1 economic data and lingering concerns over Russia, equities have edged lower (Eurostoxx50 -0.1%), Bunds have retraced some of yesterday’s losses and commodities are on the back foot with WTI trading marginally below USD 68 and Gold below USD 1200.

- Treasuries mixed, curve spreads flatten as U.S. investment-grade calendar builds, with AMZN 5- part likely to price today after MDT sold $17b yesterday in year’s largest deal.

- Europe’s latest bank stress test was flawed, and dozens of the region’s lenders, including Deutsche Bank and BNP Paribas, aren’t sufficiently capitalized to improve the economy’s anemic growth or withstand a repeat of the 2008 financial crisis

- The EU faces a rebuke from global regulators for shortcomings in its implementation of bank capital rules, according to two people with knowledge of the matter

- Russia is entering its first recession since 2009 as sanctions over the Ukraine conflict combine with plunging oil prices and the weakening ruble to hammer the economy and force the government to prop up banks

- China is tightening checks on local bond sales in its latest bid to reduce risks as debt loads surge to a record amid slowing economic growth

- Prime Minister Shinzo Abe took his economic message to Japan’s regions today, starting his campaign for re-election with the country in recession

- The 3Q contraction that tipped Japan into recession may not be as sharp as first thought, with economists revising gross domestic product forecasts

- Greece needs a debt haircut and easier servicing costs, Greek opposition Alexis Tsipras said at a conference today; also said Syriza will be at forefront of radical progressive change in Europe

- Sovereign yields rise. Asian stocks gain; European stocks, U.S. equity-index futures rise. Brent crude and gold fall, copper rises

- Looking ahead, attention turns to ISM New York and API Crude Inventories

and any comments from Fed’s Fischer, Yellen and Brainard.

FX

The USD remains broadly stronger alongside the recovery in US yield, which has subsequently seen USD/JPY ebb higher back towards the 119.00 handle amid favourable interest differential flows. Elsewhere, AUD was seen higher overnight following a less-dovish than anticipated RBA despite the recent slump in commodity prices, however, this upside has since been pared following the movements in the USD-index with RANsquawk sources also reporting Middle-Eastern selling in the pair. Elsewhere, heading into the North American crossover, the RUB is once again seen weaker as concerns over the Russia economy remain at the forefront with the Russian Finance Ministry warning of a potential recession in Q1 2015.

COMMODITIES

In terms of precious metals, gold has ebbed lower breaking back below USD 1,200.00 after retracing around 38.25% of the move, furthermore, on a geopolitical front tensions appear to be easing between Ukraine and Russia amid reports that the Ukraine and Russian rebels could reach a truce following the recent fighting around Donetsk airport. In the energy complex oil is trading in negative territory and is trading around the USD 68.00 level in what has been a relatively choppy morning with price movements largely led by USD fluctuations. Nonetheless, expectations for tomorrow’s DoE inventories are looking for yet another build for the headline figure and thus due to further increase the global glut of supply in oil markets

DB’s Jim Reid Completes the overnight Event Summary

The falling oil price continues to dominate the agenda at the moment although we did see some respite yesterday. Both WTI (+4.31%) and Brent (+3.41%) finished the NY session off the morning session lows to close at around $69 and $72 respectively although they are somewhat softer in the overnight Asian session (more below). The rebound in Oil yesterday also coincided with what was generally a firmer day across the commodity complex. After falling to a three week low on the back of the SNB vote over the weekend, Gold was +3.83% stronger yesterday at $1212.10 whilst Silver traded +6.53% to close at $16.46/oz. For equities it was a fairly weak day for the S&P 500 (-0.68%) despite the rebound of Energy stocks (+0.7%) as the market was weighed down by losses in 8 out of the ten major sector groups. Industrials (-1.29%), IT (-1.11%) and Consumer Discretionary (-1.09%) were main decliners at the end of play which to some degree probably reflects the sluggishness of the retail numbers coming out from the Thanksgiving weekend.

Away from the strength in commodities and the weakness in equities, the move in Treasuries was another big theme yesterday. The 10yr benchmark reversed Friday’s gains to close 7bp wider at 2.235%. Some hawkish comments from the Fed’s Dudley probably didn’t help matters after the NY Fed President suggested that a mid-2015 rate hike still seemed reasonable. To be fair though he did highlight the need for patience over rate hikes but the market seemed to zoom in on Dudley’s comments that an increase would be a ‘welcome development’ and signal that the economy has healed enough to warrant ‘somewhat less accommodative’ policy, even if we see a bump or two in financial markets. Highlighting the moves in the oil price, Dudley also noted that the recent drop in prices was a clear positive for the US economy and that it could spur more expansive monetary policy in other countries by pulling down inflation. Elsewhere, the Fed’s Fisher was quoted on Reuters downplaying the dis-inflationary effect of the fall in the oil price – commenting specifically that it would be a ‘temporary’ drag on inflation and ultimately lower energy costs would help growth in the US.

Away from Fed speak and Oil, the ISM reading yesterday was also a notable release for markets. November’s manufacturing ISM survey (58.7 vs. 58.0) came in a touch above consensus. Whilst this is a tad lower than the 59 print in October it was still the third highest reading for the current business cycle. Prices paid fell nine points to 44.5 in November (lowest reading since July 2012) which was largely driven by the sharp decline in energy prices.

Taking a look at developments on the other side of the Atlantic we saw the Stoxx 600 close -0.46% lower and Xover widen 10bps on the day probably not supported by what was seen to be a generally soft set of data. The final November manufacturing PMI for the Euro-area printed at 50.1, down from the 50.4 flash estimate and 50.6 October reading. DB’s Peter Sidorov notes that the details in the report were not particularly encouraging either. With new orders falling by 0.8pts and new export orders unchanged it suggests that the weakness in manufacturing cannot be explained simply by external weakness.

Regionally across Europe, the German manufacturing PMI disappointed 49.5 (revised down 0.5pts from the flash estimate) and is now at its weakest level since June 2013. The French reading was revised up (to 48.4) but declined 0.1pts relative to the October print whilst the Italian reading was unchanged at 49. Spain was a relative standout registering a 2.1pt rise to 54.7 marking a new post-2007 high. Peripheral bonds performed well yesterday as 10y benchmark yields in Spain (-6bps), Italy (-2bps) and Portugal (-2bps) fell to around 1.83%, 2.01% and 2.81% respectively.

Briefly back to the Oil theme, the effect of the recent slump continues to have a negative impact on the Russian Rouble. The currency was down as much as 6.6% yesterday versus the dollar before paring back some of those intra-day losses to close around 4.5% lower on the day (at 51.65). The currency has now declined 30% since the end of September. Russia’s 5yr CDS widened a further 26bps yesterday to 344bps whilst the 10y government bond yield finished 15bps higher at 10.76%. The moves also come on the back of an announcement by the Finance Minister Siluanov last week that capital flight may reach $130bn in 2014 – the most since 2009.

Switching focus to Asia, the Japan Topix is modestly stronger (+0.49%) and shrugging off Moody’s sovereign rating cut yesterday (to A1/stable from Aa3). For the record, Japan’s foreign currency rating is still AA-/Neg by S&P and A+/Neg by Fitch. The Moody’s action comes just before Prime Minister Abe commences his campaign today ahead of the election later this month. Just on the subject, the Nikkei QUICK monthly bond survey yesterday showed that respondents saw a 79.9% probability that the LDP/Komeito ruling coalition would do better than its stated victory of 270 seats. Away from Japan, with the exception of Korea, major bourses are largely trading in the green. The Hang Seng (+0.74%), Shanghai Composite (+1.80%) and ASX 200 (+1.41%) are all trading firmer. On the latter, the RBA has kept its benchmark rate unchanged at 2.50% (as expected by most) overnight but it is worth noting that our Australian economist now expects a cumulative 50bps cut by the RBA in 2015 citing a forecasts of rising unemployment, nascent signs of moderation in house price growth and ongoing commodity price declines. This is a non-consensus call by DB so we’ll see if the street follows from here.

Looking at today’s calendar, we’re fairly light on data prints today with just unemployment data in Spain to look forward to as well as PPI for the Euro-area. In the US this afternoon we’ve got the ISM NY due with the market expecting a slight uptick to 55.0 (from 54.8). Shortly after, we get the construction spending print which is expected to increase – residential construction in particular is expected to show a decent gain given the improvements in housing permits. We round today off with November vehicle sales data in the US. In terms of Fedspeak, early this afternoon both Fischer and Yellen will be talking in Washington so watch out headlines here.

end

The Russian ruble crashes to a record low of 54.00 to the dollar. It looks like the Russian central bank must intervene. Bond yields rise to over 10.5% for the 10 year bond

(courtesy zero hedge)

Russian Ruble Crashes To New Record Lows – Intervention Imminent?

Despite yesterday’s big bounce back in the price of oil, this morning’s weakness across the crude complex has rekindled selling pressure on the Russian Ruble as it crashes back to yesterday’s record lows against the USD.

At around 54 Ruble to the USD, yesterday saw ‘alleged’ intervention by the Russian Central Bank with a dramatic reversal back to around 50 intraday… it appears the market wants to test the Central Bank’s free-float commitment once again.

Yesterday saw notable Treasury selling as the Ruble was rescued/intervened, one wonders if the move higher in yields for 30Y bonds in the last few minutes signal Russian central bank intervention coming soon. [Sell TSY, Rcv USD, sell USD, buy RUB]

end

One of the major reasons for Abenomics was to get Japanese real wages higher.

Thus the massive stimulation. Abenomics is a complete failure:

(courtesy zerohedge)

The Abenomics Devastation: Japanese Real Wages Decline For Record 16 Consecutive Months

Those seeking proof that Abenomics is working are advised to look elsewhere. Overnight Japan released its latest, October, wage data, which showed that total cash wages rose 0.5% yoy, slightly slowing from the 0.7% growth recorded in September. As the chart below shows, Nominal wages have been slowing down from the peak in July when the figure was boosted to +2.4% on summer bonus payments. Overtime pay grew +0.4% yoy (September: +1.9%), slowing from the peak recorded in April (+6.0%) on a slowdown in economic activities. The figure contributed to overall wages by only +0.03 pp.

Some more details from Goldman: “Basic wages rose 0.4% yoy in October, unchanged from September. The effect of the shunto spring wage hike seems to be fully reflected into base wage growth and settling at a stable growth around 0.5%. However, with overtime pay near zero, the 0.4% increase in basic wages virtually determines the overall wage growth during non-bonus months. We also note that preliminary basic wages tend to be revised down at the final stage.”

Looking at nominal wages by type of employment, regular employees saw a 0.6% yoy increase, significantly slowing down from +1.1% in September. Wage for part-timers turned negative at -0.3% (September: +0.5%). Part-timers saw a sharp fall in basic working hours (-1.6% yoy) and overtime hours (-6.9% yoy).

In other words, when Japan turns to wage controls some time in 2015, a move that is now essentially assured as Japan has gone all in on central planning, it will demand that corporations boost pay to part-timers first, and then force all corporations to hike wages across the board.

But as everyone knows, for the past 2 years nominal wages are just half the story. The reason is that courtesy of the crashing Yen, everything has to be converted into real terms to adjust for soaring inflation and exploding import prices. It is here that we find that for the 16th consecutive month, real wages continued to decline heavily.

Real wages (nominal wages less the CPI inflation) continued to register a large decline of 2.8% yoy, after falling 3.0% in September. Despite high one-time bonus payments, the much lower pace of increase in basic wages (around +0.5%, conceptually close to permanent income) relative to inflation rate, and the resulting large decline in real wages at normal times, is restricting consumer behavior.

And with Japan’s snap election in less than two weeks, Abe’s reign may be yet again prematurely interrupted if the local population decides it has had enough of being on the receiving end of the most cruel Keynesian experiment in recent history. As Bloomberg notes, “With the effect of the sales tax hike, I don’t see real wages rising in the financial year through April,” said Toru Suehiro, an economist at Mizuho Securities Co. “People will be asking themselves whether they feel better off, and there probably aren’t that many who think the economy has got better.”

Which is to be expected. After all we now know that the brain trust behind the latest Japanese push into outright lunacy, is none other than Paul Krugman. Is there any doubt that Japan is now an economic basket case, with an unsustainable demographic implosion to boot?

end

Goldman Sachs purchases 4 billion of oil debt (issued by the Dominion Republic) at 41 cents on the dollar. Venezuela needs cash now!! Default is imminent:

(courtesy zero hedge)

How Goldman Sachs Became Broke Venezuela’s Loan Shark

Add the title of “loan shark to Dictatorships” to Goldman Sachs many varied roles around the world. As Venezuela teeters on the brink of tearings its utopian social fabric apart (by which we mean paying its soldiers while impoverishing its people to in order to maintain ‘peace’) crushed by plunging oil revenues, everyone’s favorite American bank ‘generously’ offered to buy (from Venezuela) $4bn worth of oil debt owed by the Dominican Republic for 41% of its value, according to El Nuevo Herald. Doing god’s work indeed. “This is a tremendous bargain for Goldman,” said one source, as Venezuela is “liquidating the few assets they have, trying to find the cash flow, cash, they do not have.”

Venezuelan bonds continues to crash

Cornered by liquidity problems, the regime of Nicholas Maduro sold to US investment bank Goldman Sachs obligations for more than $4,000 million Dominican Republic owed to Venezuela for oil supplied through Petrocaribe, receiving only 41 percent the total value of debt, sources close to the operation.

The transaction would involve a gain of 59 percent for Goldman Sachs, equivalent to $ 2.360 billion, on payment of $ 1.750 million grant to Venezuela for the obligations in August this year totaled about $ 4.090 million.

According to the sources, who spoke on condition of anonymity, Goldman Sachs is currently holding talks with the Venezuelan government to reach a similar agreement on oil debt that Jamaica has with the South American nation.

…

“This is a tremendous bargain for Goldman Sachs,” said one of the sources. “The only negative is that it is a debt to 20 years, but the discount is as bestial, Goldman snatched from the hands in exchange for giving PDVSA a little liquidity.”

But the operation denotes a high degree of desperation of the Venezuelan state whose oil sales generate more than 95 percent of the dollars entering the country.

“They’re liquidating the few assets they have, trying to find the cash flow, cash, they do not have,” said the source.

…

“They’re scraping the pot” from New York said Venezuela’s former ambassador to the UN, Diego Arria, who has close links with the international financial sector.

It is also a clear signal to the international markets on the economic problems facing the regime.

“A discount as significant [59 percent], besides the great monetary loss for the nation, is a great loss of credibility on the Venezuelan financial situation,” said Arria.

“But it could also be a crime,” the diplomat added. “Giving such obligations at a discount from those proportions, is attacking the national heritage”.

…

But the financial crisis facing the regime generated great doubts about the country’s ability to continue to support the costs of subsidizing oil economy with Cuba and its other allies.

* * *

Instabiliteee…..

end

Putin kills the South Stream pipeline which will be a huge blow to Bulgaria. However these guys sided with the west so they must pay the price.

Putin then sidesteps the south stream pipeline, and instead a new project going through Turkey who were more than obliging. And their reward: lower prices!!

(courtesy zero hedge)

Putin Kills “South Stream” Pipeline, Will Build New Massive Pipeline To Turkey Instead

In retrospect, it should have been obvious in August.

Back then we wrote that the EU’s poorest member nation,Bulgaria, had been an enthusiastic supporter of the Russian-backed South Stream gas pipeline project, whose construction has stoked tensions between the West and Moscow as it enabled gas supply to bypass troubled Ukraine (thus squeezing the desparate economy back into Russia’s hands). In early June, Bulgaria’s Prime Minister Plamen Oresharski ordered an initial halt (after Europe offered the nation’s suddenly collapsing banking system a lifeline). Subsequently, Energy Minister Vasil Shtonov has ordered Bulgaria’s Energy Holding to halt any actions in regards of the project as it does not meet the requirements of the European Commission.

And then, just to send Putin a very clear message where the allegiances of this former Soviet satellite nation lie,NATO deployed 12 F-15s and 180 troops to Bulgaria’s Graf Ignatievo Air Base.

A dozen F-15s and approximately 180 personnel from the 493rd, based at RAF Lakenheath, England, have deployed to Graf Ignatievo Air Base to participate in a two-week bilateral training exercise with the Bulgarian air force, Pentagon spokesmen Col. Steve Warren told reporters Monday.

The exercise began Monday and will continue through Sept. 1.

The purpose of the deployment is to “conduct training and focus on maintain joint readiness while building interoperability,” Warren said.

The move comes at a time when America’s Eastern European partners and allies are concerned about Russian military intervention in Ukraine. There are fears that Moscow might try to destabilize other countries in the region.

“This is a reflection of our steadfast commitment to enhancing regional security,” Warren said about the exercise.

We concluded as follows: “How will Putin react one wonders?”

We now have the answer: earlier today, in a stunning announcement, Putin revealed that the South Stream project is now finished. As the WSJ reports, “Putin said Moscow will stop pursuing Gazprom’s South Stream pipeline project that would supply natural gas to Europe with an underwater link to Bulgaria, blaming the European Union for scuttling the project.”

“We couldn’t get necessary permissions from Bulgaria, so we cannot continue with the project. We can’t make all the investment just to be stopped at the Bulgarian border,” Mr. Putin said. “Of course, this is the choice of our friends in Europe.”

“We think that the European Commission’s position was not constructive,” Mr. Putin said. “If Europe does not want to implement it, it will not be implemented.”

Putin is right: Europe – Austria excluded – had seen rising resistance to the South Stream in recent months as the crisis in Ukraine has intensified. The EU is concerned that the project would cement Russia’s position as Europe’s dominant supplier of natural gas. Russia already meets around 30% of Europe’s annual needs.

So what does Putin do? He signs a strategic alliance with NATO member Turkey, the only country in Europe that is anything but European (over the endless veto of Germany preventing its entrance into the EU over fears of cheap, migrant labor) and which lately has been increasingly anti-Western, to build a new mega-pipeline to Turkey instead. As RT reports, Gazprom CEO Aleksey Miller said the energy giant will build a massive gas pipeline that will travel from Russia, transit through Turkey, and stop at the Greek border – giving Russia access to the Southern European market. In effect, Russia will still have access to the Southern Stream endmarkets

The pipeline will have an annual capacity of 63 billion cubic meters. A total of 14 bcm will be delivered to Turkey, which is Gazprom’s second biggest customer in the region after Germany.

Russia’s energy minister Aleksandr Novak said that the new project will include a specially-constructed hub on the Turkish-Greek border for customers in southern Europe.