My website is now ready You can find my site at the following url:

http://www.harveyorganblog.com or www .harveyorgan.wordpress.com

I will continue to send the comex data down to my good friends at the Doctorsilvers website on a continual basis.

They provide the comex data. I also provide other pertinent data that may interest you. So if you wish you can view that part on my website.

Gold: $1194.70 up $4.70

Silver: $16.22 up $0.02

In the access market 5:15 pm

Gold $1203.75

silver $16.36

The gold comex today had a poor delivery day, registering 2 notices served for 200 oz. Silver comex registered 1 notices for 5,000 oz.

A few months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 245.83 tonnes for a loss of 57 tonnes over that period.

In silver, the open interest rose by a small 445 contracts with Friday’s fall in price of $0.23. Looks like some of the shorts are vacating the arena. For the past year, we have been witnessing massive liquidation of contracts despite the fact that it cost nothing to roll. This makes no sense and it smacks of cash settlements which are totally illegal. Since I have been following comex data, I have never witnessed such a massive liquidation in both gold and silver. The total silver OI still remains relatively high with today’s reading at 147,360 contracts. The big December silver OI contract rose by 43 contracts up to 616 contracts.

In gold we had a rise in OI with the fall in price of gold Friday to the tune of $17.50. The total comex gold OI rests tonight at 370,120 for a gain of 445 contracts. The December gold OI rests tonight at 1963 contracts losing 12 contracts.

TRADING OF GOLD AND SILVER TODAY

GOLD

Gold started out at midnight exactly where we left off in NY at $1192.00. At 2 am (London’s first fix) gold hit $1196. and then gold straddled the $1195 level throughout the early morning and early comex trading. By London’s second fix, it again hit $1196.50 only to be repelled again back down to $1192. That is where it stayed until 2pm in the access market, gold rocketed to $1207.00 only to be knocked down again to settle around the $1204.00 area.

Silver

Silver traded a bit below its NY close (no doubt due to the increase in margin rates orchestrated by the CME Friday night). By London’s first fix silver remained at $16.25. However by 5 am, it rebounded northbound to $16.35 only to be repelled back down to $16.23. The second London fix had silver at $16.31. It jumped in sympathy to gold at 2 pm to $16.41 but settled down to close in the the access market at $16.36

Today, we lost .9 tonnes of gold Inventory at the GLD / inventory rests tonight at 719.12 tonnes.

In silver, we had no change in silver inventory

SLV’s inventory rests tonight at 345.223 million oz

.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today.

First: GOFO rates:

all rates moved closer to the positive and out of backwardation!!

Now, all the months of GOFO rates( one, two, three six and 12 month GOFO moved positive and moved closer to the positive needle. They must have found a few bars to lease. On the 22nd of September the LBMA stated that they will not publish GOFO rates. However today we still received today’s GOFO rates. It looks to me like these rates even though negative are still fully manipulated. London good delivery bars are still quite scarce.

The backwardation in gold is incompatible with the raid on gold. It does not make any economic sense.

Dec 8 2014

1 Month Rate: 2 Month Rate 3 Month Rate 6 month rate 1 yr rate

+.072.% + .07500 -% -+08250 -% +. 095 .% +. 1775%

Dec 5 2014:

+.035% +.0300% +.0450 % +.06% +.11%

end

Let us now head over to the comex and assess trading over there today,

Here are today’s comex results:

The total gold comex open interest rose today by 1207 contracts from 368,913 all the way up to 370,120 with gold down by $17.50 on Friday (at the comex close). We are now into the big December contract month where the number of OI standing for the gold metal registers 1963 contracts for a loss of 12 contracts. We had 0 delivery notices served on Friday so we lost 12 contracts or 1200 oz of gold will not stand for the December contract month. The non active January contract month rose by 60 contracts up to 524. The next big delivery month is February and here the OI fell to 234,103 contracts for a gain of 635 contracts. The estimated volume today was awful at 56,855. The confirmed volume on Friday was fair at 167,283 even with the help of high frequency traders. The comex now has no credibility and many investors have vanished from this crooked casino. Today we had 2 notices filed for 200 oz .

And now for the wild silver comex results. Silver OI rose by 445 contracts from 146,915 up to 147,360 even though silver was down by $0.23 on Friday. I do believe we lost a few more bankers along the way. The big December active contract month saw it’s OI rise by 43 contracts up to 616 contracts. We had 13 notices served upon for Fri. delivery. Thus we gained 56 contracts or an additional 280,000 oz will stand. The estimated volume today was unbelievable registering a tiny 12,882. ??? The confirmed volume on Friday was good at 43,105. We had 1 notices filed for 5,000 oz today

December initial standings

Dec 8.2014

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 10,383.487 oz (Scotia,Brinks) |

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 186,465.538 (HSBC,Manfra,Scotia oz |

| No of oz served (contracts) today | 2 contracts(200 oz) |

| No of oz to be served (notices) | 1963 contracts (196,300 oz) |

| Total monthly oz gold served (contracts) so far this month | 1851 contracts(184900 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 150,109.154 oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

145,803.5 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

we had 0 dealer deposits:

total dealer deposit: nil oz

we had 2 customer withdrawals

i) Out of Brinks: 398.54 oz

ii) Out Scotia: 9984.947 oz

total customer withdrawal: 10,393.487 oz

we had 4 customer deposits:

i) Into Scotia; 74,644.677 oz

ii) Into HSBC: 10,383.487 oz (arriving from our two withdrawals)

iii) Into JPMorgan; 100,633.624 oz

iv) 803.75 oz (Manfra)

total customer deposits :186,465.538 oz

We had 0 adjustments:

Total dealer inventory: 721,123.608 oz or 22.429 tonnes

Total gold inventory (dealer and customer) = 7.903 million oz. (245.83) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 57 tonnes have been net transferred out. We will be watching this closely!

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contracts of which 2 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the December contract month, we take the total number of notices filed for the month (1851) x 100 oz to which we add the difference between the OI for the front month of December (1963) minus the # gold notices filed today (2) x 100 oz = the amount of gold oz standing for the December contract month.

Thus the initial standings:

1851 (notices filed for the month x 100 oz + 1963) the number of OI notices for the front month of December served upon – (2) notices served today equals 381,200 oz or 11.856 tonnes

we lost 12 contracts or 1200 oz that will not stand.

This initiates the month of December for gold.

And now for silver

Dec 8/2014:

December silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,064,019.522 oz (CNT,Brinks, Scotia,HSBC) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 600,325.78 oz (CNT) |

| No of oz served (contracts) | 1 contracts (5,000 oz) |

| No of oz to be served (notices) | 615 contracts (3,075,000 oz) |

| Total monthly oz silver served (contracts) | 2486 contracts (12,425,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 1,163,562.6 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,201,802.6 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 4 customer withdrawal:

i) Out of CNT: 125,949.9 oz (one decimal)

ii) Out of Brinks: 304,844.210 oz

iii) Out of Scotia: 60,920.8 oz (one decimal)

iv) Out of HSBC: 572,304.612 oz

total customer withdrawal 1,064,019.522 oz

We had 1 customer deposits:

i) Into CNT; 600,325.78 oz

total customer deposits: 600,325.78 oz

we had 1 adjustment

from the brink’s vault:

99,998.96 oz was adjusted out of the dealer as an accounting error.

Total dealer inventory: 64.479 million oz

Total of all silver inventory (dealer and customer) 177.169 million oz.

The total number of notices filed today is represented by 1 contracts or 5,000 oz. To calculate the number of silver ounces that will stand for delivery in December, we take the total number of notices filed for the month (2486) x 5,000 oz to which we add the difference between the total OI for the front month of December (616) minus (the number of notices filed today (1) x 5,000 oz = the total number of silver oz standing so far in November.

Thus: 2486 contracts x 5000 oz + (616) OI for the November contract month – 1 (the number of notices filed today) =15,505,000 oz of silver that will stand for delivery in December.

we gained 280,000 oz standing.

for those wishing to see the rest of data today see:

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

Dec 8.2014: we lost .900 tonnes of gold/inventory 719.12 tonnes

Dec 5.2014: no change in tonnage/720.02 tonnes

Dec 4 no change in tonnage/720.02 tonnes

Dec 3 no change in tonnage/720.02 tonnes/

December 2/2014; wow!! we had a huge addition of 2.39 tonnes of gold /Inventory 720.02 tonnes

December 1.2014: no change in gold inventory at GLD

Nov 28.2014: a loss in inventory of 1.19 tonnes/tonnage 717.63 tonnes

Nov 26.2014: we lost 2.09 tonnes of gold heading to India and or China/inventory at 718.82 tonnes

Today, December 8 we lost .900 tonnes of inventory at GLD.

inventory: 719.12 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 719.12 tonnes.

end

And now for silver:

Dec 8.2014: no change in inventory/345.223 million oz

Dec 5/2014: no change in inventory/345.223 million oz

Dec 4/we lost another 2.204 million oz of silver/inventory 345.223 million oz

dec 3. we lost 2.73 million oz of silver/inventory 347.427 million oz and back where we were on Dec 1.2014.

dec 2 wow@!!@ a huge addition of 2.20 million oz of silver/inventory 350.158 million oz.

December 1: no change in inventory/347.954 million oz

Nov 28.2014: no change in inventory/347.954 million oz

Nov 26.2014; no change in inventory/347.954 million oz

December 8/2014/ we had no change in silver/inventory registers: 345.223 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now deeply into the positive to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 10.6% percent to NAV in usa funds and Negative 10.6% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.4%

Percentage of fund in silver:38.10%

cash .5%

( December 5/2014) will update later

2. Sprott silver fund (PSLV): Premium to NAV falls to positive 0.86% NAV (Dec 8/2014)

3. Sprott gold fund (PHYS): premium to NAV rises to negative -0.19% to NAV(Dec 8/2014)

Note: Sprott silver trust back hugely into positive territory at 0.86%.

Sprott physical gold trust is back in negative territory at -0.19%

Central fund of Canada’s is still in jail.

end

And now for your most important physical stories on gold and silver today:

Early gold trading from Europe early Monday morning:

Gold Prices Kept Low But Only For Americans

The SGT Report interviewed GoldCore’s Head of Research Mark O’Byrne over the weekend. The video was released yesterday evening and has already had over 5,300 views.

Click on image or here to watch

Topics covered in the interview included:

- Gold performing well in all currencies in 2014

- A yes vote to Swiss gold referendum would have been “icing on cake” for gold market

- Existing fundamentals sound due to India and China demand and Russian, Chinese and other central bank demand

- Germans can’t get their gold reserves. Do how did the Dutch get their 122 tonnes of gold?

- Is Germany being prevented from holding gold to prevent independent foreign policy action?

- The mind boggling scale of the U.S. $18 trillion national debt and over $100 trillion to $200 trillion in unfunded liabilities

- How humongous is a billion, a trillion and a quadrillion?

- The illusion of digital “wealth” and the coming wealth transfer when system implodes

Here is a transcript of the first 11 minutes of the 26 minute interview.

SGT Report: What I wanted to do gentlemen is start with a headline that we rarely see and it’s this one which I haven’t written yet – “Strong dollar keeps gold prices low for Americans” and the reason I’m saying that is that according to your own blog at Goldcore.com Mark ( GoldCore blog ), gold is up 14.3% in japanese yen this year, 12.3% in euros, 5.8% in British pounds and of course only 0.4% when priced in dollars.

And that’s the real story, isn’t it – gold continues to be real money and act as real money around the globe as fiat currencies are printed and annihilated.

Mark O’Byrne: ABSOLUTELY and I think it speaks to the dollar-centric nature of the world today.

We all look at things in dollars – not just in America, you guys do that naturally enough, but throughout the western world, particularly in the investment and finance sphere, the dollar is still king and everything is looked at in terms of pricing in dollars. That’s created the perception that gold has been weak this year when in reality, it has been anything but.

It’s actually slightly higher in dollar terms ytd in 2014. So it’s performed quite well versus other things, obviously not the stock markets which have roared ahead again but it has performed very well in all the other major fiat currencies.

I think what we are seeing in terms yen and euro and pounds to a certain extent is a precursor to what we will see in terms of the dollar probably next year. We had the fall in 2013, I think this year we are seeing a consolidation, a bottoming-out process. I think it’s also a function of manipulation, and we might talk about that in the course of the interview.

But it’s not just the major fiat currencies. It’s very strong in yen, and they are debasing the yen in a huge way. And the euro – they haven’t even started debasing the euro yet and there is talk that Draghi is going to start that in 2015 but it’s up 12% in euro terms without them even starting QE in the eurozone. But even more importantly if you look to Russia, Ukraine, Syria and countries like that their currencies are being devalued in a very significant way and gold has gone up 30-50% in these currencies.

So it shows again gold is a safe haven asset, it is money. it has been throughout history and it is today. It makes a complete mockery of the idiotic and simplistic anti-gold propaganda in effect. The stuff that has come out recently, Willem Buiter from Citibank and others like Barry Ritholtz, a very prominent blogger who gets picked up and has a very prominent pulpit on Bloomberg. And these guys are coming out and attacking gold in quite a serious way and saying that gold is in a 6000-year old bubble and a whole host of silly, silly things.

I mean even the 6000-year old bubble thing is ridiculous because there were no bubbles 6000 years ago because there were no markets. We’ve only had bubbles, big bubbles particularly, since the Federal Reserve in 1913, and particularly since Nixon went off the gold standard in 1971 – that’s what has created really big bubbles.

So there were no bubbles even 1,000 years ago. So it’s important for people to realize that and to stay focused on that because there is a lot of propaganda that shakes people out positions.

We have had a lot of clients selling in recent months and we tell them – and it’s not in our interest to tell them – not to sell. As a dealer we make money when people buy and sell. But we have always said that if we do the right thing by our clients, we give them good advice, we tell them to hold for the long term, to own gold as financial insurance, we believe that they will appreciate that and we will get good word of mouth and they tell their friends and family and it is just doing the right thing by your client as well.

SGT Report: THAT’s right, and we try to do the right thing by our listeners and you read my mind when you mentioned propaganda because that is exactly what it is and that’s why I wanted to lead with these facts. When priced in other currencies around the world gold is up a lot this year.

Now what we hear from the mainstream mocking-bird corporate media in this country is that gold is a barbarous relic and stock market’s are roaring higher. And the reason for this is that central banks are buying S&P futures to drive markets higher while they are simultaneously working in collaboration to suppress gold and silver prices. That’s a fact. So it’s pretty interesting to stand back at a 30,000 foot view and look at the facts and realise that despite the fact that they are trying to crush the paper prices of gold and silver, gold is still up half a percent when priced in dollars this year and that’s only because the dollar has been surging.

So why do we care about this? Why do we still talk about precious metals at this point? Well, as you noted in an article recently Mark, US DEBT HAS SURPASSED THE $18 TRILLION MARK, surging 70% higher during this “recovery” under Barack Obama. It’s all an illusion of debt. Everything they’re doing to create this recovery, a roaring economy, a roaring stock market is an illusion of bankster debt, period. Do you agree?

Mark O’Byrne: I DO INDEED YES. I was shocked by – when I went into Google News to see how the – because when we hit $18 trillion debt I thought that could be a penny dropping for people and I thought some of the media might say “oh, wow, maybe the recovery isn’t as strong as we thought” and there would be some interesting coverage of this but it was barely covered at all. Things have been quite Orwellian for a while but I actually think it’s becoming more Orwellian and it’s amazing that you could hit the 18 trillion number in terms of national government debt – it does not cover unfunded liabilities which are between $100 trillion and $200 trillion – so it’s just incredible that this number would be hit. It’s increased roughly $1 trillion per year under the Obama presidency, in this so-called ‘recovery’ and it’s pure propaganda that it’s a recovery. You can’t have a recovery when the balance sheet of your nation is deteriorating in a massive way which is what is happening. And there is no reduction in debt, either the nominal national debt or the unfunded liabilities so it makes a complete mockery of the so-called ‘recovery’ meme that goes on.

There are lots of other data points recently that suggests that the recovery is much, much more fragile and obviously a lot of the statistics are ‘hedonically adjusted’ and they are tweaked and manipulated to suggest that there is recovery but I think you have to question that.

People get so jaded and so bombarded with numbers and they are almost blase about a trillion. They don’t realize how big a trillion is.

A trillion is a thousand billion. But they don’t even realize how big a billion is. A billion is a thousand million and they don’t understand how big that is.

If you put it in terms of time that’s a good way for people to understand it. So I actually pulled up the blog we did previously: a billion seconds ago was 1967, nearly fifty years ago. A billion minutes ago Jesus Christ was alive, back in Bethlehem and Jerusalem, 2014 years ago. A billion hours ago our ancestors were back in the Stone Age. So that’s how big a billion is. It’s a huge number and the U.S. debt increased $1 trillion in 1 year.

SGT Report: AND THAT’S A THOUSAND BILLION! You’re right. The numbers are so large. No-one can get their arms around them at this point.

Forget talking to your friends, neighbours and colleagues about the $1 quadrillion dollar derivatives market. I’ve often said, and Rory and I and other guests have talked about the fact that I think, and I believe firmly that what’s going on behind the scenes is far scarier and far more dire than any of us can possibly imagine as these banksters need to reconcile these numbers on a daily basis. Really, in fact, they are unreconcilable, even mentally, when you just consider the magnitude of the numbers. Can you even imagine having to be the DTCC and reconciling these high frequency trades at the end of every day? It’s absolutely impossible and it’s not nutty to say that. I just is true, even with the help of machines and computers. It’s impossible to reconcile all of these trades because at the end of the day, in a fair and honest market, at the end of the 3-day DTCC SETTLEMENT PERIOD the paper certificates need to transfer to the new rightful owner. That’s not happening. How can that possibly happen when you are talking about trillions of trades in a year.

Now Rory, I know you’ve got some great questions to prepare for Mark so I want you to feel free to jump in at any point. Why don’t we talk about the Swiss gold referendum before we pass it over to you because a vote against sovereignty and freedom is what this was and as Peter Schiff has summarized that the Swiss had hitched their wagon to the euro, a thought they once firmly rejected by refusing to join the european union. But they’ve turned their back on their own currency, but as you put it, Mark, and I agree, demand from India, Russia and china is far more important. And as I said before the referendum had even occurred it doesn’t matter what they do, because we know the truth.

And the truth is that central banks and nation states around the world are hoarding gold and acquiring gold as fast as they can. What do you make of the Swiss referendum vote? Do we have this right – it really doesn’t matter?

Mark O’Byrne: YES, ABSOLUTELY. I think the Swiss gold referendum, if they had voted yes – which was unlikely from day one because of the scale of the propaganda war that was going to go on – was going to be so huge that, and indeed it turned out to be, that it was unlikely. But at one stage the polls were showing that there was a chance. But for us that was always going to be the icing on the cake … and that was going to be a victory for sound money …

In order to watch the rest of the interview please click here

MARKET UPDATE

Today’s AM fix was USD 1,195.25, EUR 975.48 and GBP 766.73 per ounce.

Friday’s AM fix was USD 1,204.50, EUR 974.28 and GBP 768.37 per ounce.

Gold and silver were very strong last week and were up at 2.1% and 5.5% respectively.

Gold in USD – 2014 YTD (Thomson Reuters)

Despite the weekly gains, gold fell $14.90 or 1.24% to $1,191.40 per ounce Friday. Silver slid $0.17 or 1% to $16.29 per ounce.

Gold is marginally higher today and testing resistance at $1,200/oz and is being supported by lower European shares following soft economic data from China and Japan and an S&P downgrade of Italy’s credit rating. A much needed reminder that the Eurozone debt crisis may soon make an unwelcome return to jolt markets.

Technically, immediate support is around $1,186, while on the upside $1,210-$1,220 will provide resistance.

Hedge funds and money managers pushed a bullish position in U.S. gold futures to the highest level since August in the week to December 2, data shows. Holdings in SPDR Gold Trust, the world’s largest gold exchange traded fund, rose 0.12% to 720.91 tonnes on Friday, though still close to a six-year low.

Friday’s payroll report pushed the U.S. dollar to a five year high which pressurised gold.

Buying from Japan and particularly China offered good support to gold overnight.

MKS noted this morning that “gold edged lower through $1,190 to the daily low before the Tocom open on moderate volumes,” it said. “Tocom provided some light buying interest which helped the yellow metal approach $1,190 again, but the real jolt came when the Shanghai Gold Exchange (SGE) opened up. Good buying interest was seen through the exchange in early trade when the spot price propelled through $1,190 and up towards $1,195 where some visible offering in Feb gold was apparent.”

Silver in USD – 5 Years (Thomson Reuters)

Silver was up 0.45% at $16.45 an ounce. Platinum rose 1.2% to $1,237.25 an ounce and palladium rose 0.4% to $807 an ounce.

Get Breaking News and Updates On Gold Markets Here

end

Early morning gold prices in its various currencies:

8:10 am

|

Name

|

Bid

|

Ask

|

Change

|

%Change

|

High

|

Low

|

Time

|

Y %Change

|

52W High

|

52W Low

|

|||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Gold (USD)

|

|

alert.") |

1193.38

|

1193.55

|

1.3

|

0.11%

|

1198.07

|

1188.59

|

08-08:10:00

|

-0.92

|

1388.541

|

1130.02

|

|

|

Gold (GBP)

|

|

|

763.99

|

763.99

|

-0.5

|

-0.07%

|

770.31

|

763.32

|

08-08:10:00

|

5.08

|

836.118

|

712.956

|

|

|

Gold (CAD)

|

|

|

1365.44

|

1365.85

|

3.75

|

0.28%

|

1371.80

|

1360.41

|

08-08:09:50

|

6.74

|

1541.009

|

1258.418

|

|

|

Gold (AUD)

|

|

|

1439.94

|

1440.19

|

9.09

|

0.64%

|

1448.81

|

1430.83

|

08-08:09:49

|

6.70

|

1539.327

|

1316.747

|

|

|

Gold (INR)

|

|

|

73866.3

|

73876.30

|

-82.3

|

-0.11%

|

74195.10

|

73585.20

|

08-08:10:00

|

-0.81

|

84912.7

|

69683.5

|

|

|

Gold (CHF)

|

|

|

1170.83

|

1171.10

|

5.65

|

0.48%

|

1174.25

|

1162.77

|

08-08:10:00

|

8.93

|

1212.132

|

1052.824

|

|

|

Gold (EUR)

|

|

|

973.82

|

973.95

|

3.95

|

0.41%

|

976.37

|

966.91

|

08-08:09:59

|

11.14

|

999.673

|

857.599

|

|

|

Gold (JPY)

|

|

|

144529.06

|

144555.61

|

-295.55

|

-0.20%

|

145336.67

|

144415.60

|

08-08:10:01

|

13.95

|

145653.267

|

123737.264

|

|

|

Gold (TRY)

|

|

|

2720.84

|

2721.39

|

31.22

|

1.16%

|

2723.66

|

2684.36

|

08-08:09:53

|

5.29

|

3103.045

|

2460.602

|

|

|

Palladium

|

|

|

801.5

|

806.50

|

4.5

|

0.56%

|

805.90

|

799.25

|

08-08:09:33

|

12.63

|

910.3

|

689.75

|

|

|

Platinum

|

|

|

1229.7

|

1232.80

|

9.2

|

0.75%

|

1232.90

|

1215.75

|

08-08:09:49

|

-10.11

|

1518.7

|

1174.75

|

|

|

Gold/Silver …

|

|

|

73.33

|

73.40

|

0.19

|

0.26%

|

73.64

|

73.04

|

08-08:10:00

|

18.67

|

78.5595

|

59.9678

|

|

|

Silver (USD)

|

|

|

16.26

|

16.27

|

-0.01

|

-0.07%

|

16.38

|

16.18

|

08-08:09:59

|

-16.21

|

22.179

|

14.651

|

|

|

Silver (GBP)

|

|

|

10.41

|

10.41

|

-0.03

|

-0.26%

|

10.53

|

10.39

|

08-08:09:59

|

-11.24

|

13.31137

|

9.38138

|

|

|

Silver (CAD)

|

|

|

18.61

|

18.62

|

0.01

|

0.03%

|

18.75

|

18.52

|

08-08:09:50

|

-9.83

|

24.6444

|

16.7731

|

|

|

Silver (AUD)

|

|

|

19.62

|

19.63

|

0.08

|

0.42%

|

19.81

|

19.49

|

08-08:09:49

|

-9.91

|

24.6792

|

17.3465

|

|

|

Silver (INR)

|

|

|

1004.5

|

1008.53

|

-2.65

|

-0.26%

|

1012.54

|

1000.84

|

08-08:09:00

|

-16.36

|

1372.68

|

811.72

|

|

|

Silver (CHF)

|

|

|

15.95

|

15.97

|

0.03

|

0.22%

|

16.06

|

15.83

|

08-08:10:00

|

-7.97

|

19.6772

|

14.17514

|

|

|

Silver (EUR)

|

|

|

13.27

|

13.28

|

0.03

|

0.19%

|

13.35

|

13.15

|

08-08:10:00

|

-6.05

|

16.122

|

11.77875

|

|

|

Silver (JPY)

|

|

|

1969.35

|

1970.89

|

-8.09

|

-0.41%

|

1985.51

|

1964.55

|

end

Demand for gold in China (ex Sovereign China) this week totals 54 tonnes of gold. The Chinese are not letting up purchasing gold!!

(courtesy Koos Jansen)

China Net Gold Import 1,212t Jan – Nov

Withdrawals from the Shanghai Gold Exchange (SGE) – currently the best indicator of Chinese wholesale demand – keep up a strong pace.

In week 48 (November 24 – 28) SGE withdrawals accounted for 54 tonnes, year to date 1,867 tonnes have been withdrawn.

Corrected by the trading volume of the SGE contracts that are available for foreign traders (to take delivery, withdrawal from the vaults and export from the Shanghai Free Trade Zone), the weekly withdrawals in the mainland were 46 tonnes at minimum in week 48; year to date the bottom limit is at 1,841 tonnes.

Putting 1,841 tonnes in our basic equation (import = SGE withdrawals – scrap – mine), we can estimate mainland China has net imported 1,212 tonnes of gold up until November 28. Seasonally December and January are the strongest months for Chinese demand; I wouldn’t be surprised if total Chinese net gold import reaches 1,350 tonnes in 2014.

If nothing changes in the way the SGE reports on aggregated withdrawals from vaults in the mainland and vaults in the Shanghai Free Trade Zone – where foreign traders can take delivery, withdrawal and export – 2014 will likely be the last year in which we can accurately grasp the size of Chinese wholesale demand and total net import by using SGE withdrawals as a proxy. At this stage it’s impossible to know how much of the contracts traded by foreigners are physically withdrawn from the vaults in the Shanghai Free Trade Zone and thus distort total withdrawal numbers as disclosed by the SGE. The next screen shot is from the latest weekly SGE report. In green the total withdrawals are highlighted.

Some more details

Bloomberg came out with a story on December 3, titled Shanghai Gold Trade Passes Record as China Seeks More Sway. There is some additional information I would like to share regarding this article. The writer notes:

The volume of all contracts on the Shanghai Gold Exchange, including those in the city’s free-trade zone, was 12,077 metric tons in the 10 months to October, compared with 11,614 tons during all of 2013, according to data on the bourse’s website.

- purple = unit, Kg

- red = total gold volume traded in 2013, counted bilaterally

1) The SGE volumes disclosed by Bloomberg are double counted. This is because volume, open interest, turnover and delivery – not withdrawals – are all published bilaterally by the SGE. Later on in the article, the writer compares these SGE volumes to the data from the London Bullion Market, that publishes numbers unilaterally. From Koos Jansen, August 2, 2014:

The numbers disclosed of the SHFE and SGE are double-counted. Volume and Open Interest on both exchanges are published bilaterally, in contrast to the COMEX that publishes these numbers unilaterally. Meaning: if the volume disclosed by the COMEX is 1,000, than 1,000 contracts changed hands – 1,000 contracts were sold and 1,000 were bought. If the volume disclosed by the SHFE is 1,000, than 500 contracts were sold and 500 were bought.

… To compare SGE & SHFE numbers to COMEX one has to divide the Chinese numbers by 2, only then are all the numbers single-sided.

Perhaps this is valuable information for you when comparing Chinese and Western precious metals markets.

2) The writer notes the total traded volume includes the contracts traded in the Shanghai Free Trade Zone, hinting at the fact those contracts might have caused elevated trading volumes on the SGE. However, the volume traded in the Shanghai Free Trade Zone has been very low year to date. The contracts traded in the mainland are the ones that caused the overall volume to surge.

For a thorough analysis on the SGE and its subsidiary, the Shanghai International Gold Exchange (SGEI), click here.

What caused the most recent spike (week 47 and week 48) was trading volume of the Au(T+N1) and Au(T+N2) contracts (that can’t be traded by foreigners). These contracts hadn’t been traded since October 2013. The volumes of Au(T+N1) and Au(T+N2) are not disclosed on the English SGE website, just like SGE withdrawal and OTC data.

- yellow = date (week 48)

- purple = unit, Kg

- green = last week

- blue = this week

- red = Au(T+N1) and Au(T+N2) volume, counted bilaterally

- brown = OTC

3) So what? SGE total trading volume is still very little compared to the Shanghai Futures Exchange (SHFE), let alone the COMEX or the London Bullion Market. However, SGE withdrawal data is extremely significant, but these numbers are almost never disclosed by mainstream media outlets, nor by the World Gold Council, Thomson Reuters GFMS or CPM Group. Bloomberg and Reuters only published SGE withdrawals once (correct me if I’m wrong).

4) From Bloomberg:

Average daily volumes for the SGE’s 99.99 percent purity contract increased to about 20,427 kilograms (656,743 ounces) in October from 11,704 kilograms a year earlier, according to exchange data. By comparison, an average 17.4 million ounces changed hands daily between members of the London Bullion Market Association, according to the group’s data.

The next screen shot shows total trading volume of all SGE contracts in October 2014, we can see the 20,427 Kg number disclosed bilaterally.

On the website of the LBMA the clearing amount is disclosed unilaterally.

Note, 17.4 million ounces (541 tonnes) are cleared daily in the London Bullion Market. But, clearing and volume are two different things. Because the London Bullion Market is an OTC market we no very little of what is taking place in this market, however, the latest estimates of 2011 show the daily volume traded in London is 5,000 tonnes – counted unilaterally.

In short, Bloomberg compared the monthly volume of one SGE contract; 20 tonnes, which is actually 10 tonnes if counted unilaterally, to a daily amount of 541 tonnes, which is actually more likely to be 5,000 tonnes if counted unilaterally.

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

end

And now the huge importation of gold into India:

(courtesy Rastello/Bloomberg)

Indian Current-Account Gap Widens to Largest in a Year on Gold

By Sandrine Rastello Dec 8, 2014 1:30 PM ET India’s current-account deficit widened more than estimated to the largest since the quarter through June 2013 as exports slowed and gold imports surged.

The July-September shortfall in the broadest measure of trade widened to $10.1 billion from $7.8 billion the previous quarter, the Reserve Bank of India said in a statement yesterday. That compared with a $9.4 billion median estimate in a Bloomberg survey of 16 economists. The gap amounts to 2.1 percent of gross domestic product, lower than the 2.5 percent the central bank considers sustainable.

A recession in Japan and deteriorating outlook for the euro-area economy are keeping a lid on demand for Indian products as Prime Minister Narendra Modi seeks to revive manufacturing in Asia’s third-largest economy. Any further increase in gold shipments after authorities again eased import curbs last month will probably be partly offset by a drop in oil prices.

“Gold imports are likely to increase but they are not as attractive as they used to be in early 2013 as an asset class, so that should limit the pick-up in demand,” Anubhuti Sahay, an economist at Standard Chartered Plc in Mumbai, said by phone. “Oil is a much bigger proportion in the total imports and lower prices should benefit.”

The Reserve Bank of India in November scrapped a requirement for trading companies to export 20 percent of imported gold. Known as the 80:20 rule, it was part of a series of curbs imposed over the past two years to contain the current-account deficit, which hit a record $88 billion in the fiscal year through March 2013. In May, the government allowed more companies to ship in the metal.

Outlook

Gold imports rose sharply in the July-September period, the RBI said yesterday.

Foreign-exchange reserves fell by $1.5 billion rupees to $314 billion last quarter from the preceding three months, central bank data show. The rupee weakened 2.5 percent in that time.

The current-account shortfall will keep widening in the next two quarters, according to Madan Sabnavis, an economist at Credit Analysis & Research Ltd.

“Oil will be providing relief but it’s going to be probably countered by slowing exports” as well as other imports including gold, he said by phone in Mumbai.

To contact the reporter on this story: Sandrine Rastello in Mumbai at srastello@bloomberg.net

end

Chris Powell interviewed by Max Keiser. Start at the 10 minute mark:

(courtesy Chris Powell/Max Keiser report)

RT’s ‘Keiser Report’ interviews GATA secretary about gold price suppression

4:26p GMT Sunday, December 7, 2014

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed last week about gold price suppression by Max Keiser on the Russia Today network’s “Keiser Report” program. The interview is about 13 minutes long and begins at the 15:35 mark at YouTube here:

https://www.youtube.com/watch?v=75OyloKQzbo

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

(courtesy Tim Price/the Sovereign Man)

On Precious Metals, Patience, & Paper-Bugs

Submitted by Tim Price via Sovereign Man blog,

You can be for gold, or you can be for paper, but you cannot possibly be for both. It may soon be time to take a stand.

The arguments in favour of gold are well known. Yet they are widely ignored by the paperbugs, who have a curious belief system given that its end product (paper currency) is destined to fail. We just do not know precisely when.

The price of gold is weakly correlated to other prices in financial markets, as the last three years have clearly demonstrated.

Indeed gold may be the only asset whose price is being suppressed by the monetary authorities, as opposed to those sundry instruments whose prices are being just as artificially inflated to offer the illusion of health in the financial system (stocks and bonds being the primary financial victims).

Beware appearances in an unhinged financial system, because they can be dangerously deceptive.

It is quite easy to manipulate the paper price of gold on a financial futures exchange if you never have to make delivery of the physical asset and are content to play games with paper.

At some point that will change.

Contrary to popular belief, gold is supremely liquid, though its supply is not inexhaustible.

It is no-one’s liability – this aspect may be one of the most crucial in the months to come, as and when investors learn to start fearing counterparty risk all over again.

Gold offers a degree of protection against uncertainty. And unlike paper money, there are fundamental and finite limits to its creation and supply.

What protection? There is, of course, one argument against gold that seems to trump all others and blares loudly to skeptical ears.

Its price in US dollars has recently fallen. Not in rubles, and not perhaps in yen, of course, but certainly in US dollars.

Perhaps gold is really a currency, then, as opposed to a tiresome commodity? But the belief system of the paperbug dies hard.

The curious might ask why so many central banks are busily repatriating their gold? Or why so any Asian central banks are busily accumulating it?

It is surely not just, in Ben Bernanke’s weasel words, tradition?

If you plot the assets of central banks against the gold price, you see a more or less perfect fit going back at least to 2002.

It is almost as if gold were linked in some way to money. That correlative trend for some reason broke down in 2012 and has yet to re-emerge.

We think it will return, because 6,000 years of human history weigh heavily in its favour.

Or you can put your faith in paper. History, however, would not recommend it. Fiat money has a 100% failure rate.

Please note that we are not advocating gold to the exclusion of all else within the context of a balanced investment portfolio.

There is a role for objectively creditworthy debt, especially if deflation really does take hold – it’s just that the provision of objectively creditworthy bonds in a global debt bubble is now vanishingly small.

There is a role for listed businesses run by principled, decent management, where the market’s assessment of value for those businesses sits comfortably below those businesses’ intrinsic worth.

But you need to look far and wide for such opportunities, because six years of central and commercial banks playing games with paper have made many stock markets thoroughly unattractive to the discerning value investor.

We suggest looking in Asia.

As investors we are all trapped within a horrifying bubble. We must play the hand we’ve been dealt, however bad it is.

But there are now growing signs of end-of-bubble instability. The system does not appear remotely sound.

Since political vision in Europe, in particular, is clearly absent, the field has been left to central bankers to run amok.

The only question we cannot answer is: precisely when does the centre fail?

The correct response is to recall the words of the famed value investor Peter Cundill, when he confided in his diary:

“The most important attribute for success in value investing is patience, patience, and more patience. THE MAJORITY OF INVESTORS DO NOT POSSESS THIS CHARACTERISTIC.”

But the absence of patience by the majority of investors is fine, because it leaves more money on the table for the rest of us.

The only question remaining is: in what exact form should we hold that money?

“What will futurity make of the Ph.D. standard? Likely, it will be even more baffled than we are. Imagine trying to explain the present-day arrangements to your 20-something grandchild a couple of decades hence – after the Crash of, say, 2016, that wiped out the youngster’s inheritance and provoked a central bank response so heavy-handed as to shatter the confidence even of Wall Street in the Federal Reserve’s methods.

“I expect you’ll wind up saying something like this:

“My generation gave former tenured economics professors discretionary authority to fabricate money and to fix interest rates. We put the cart of asset prices before the horse of enterprise. We entertained the fantasy that high asset prices made for prosperity, rather than the other way around. We actually worked to foster inflation, which we called ‘price stability’ (this was on the eve of the hyperinflation of 2017).

We seem to have miscalculated.”

The latest BIS report and how it relates to gold; and they are very worried about the USA dollar strength

Two stories:

First:

(courtesy Graham/Reuters)

Currency ties key to dollar reserve hegemony, BIS study says

By Patrick Graham

Reuters

Sunday, December 7, 2014

LONDON — Changes in the size of a loosely defined global “dollar zone” could lead to faster than expected shifts in the composition of world currency reserves, potentially eroding the role of the U.S. unit, said a study published on Sunday.

The study, part of a quarterly review by the Bank for International Settlements —

http://www.bis.org/publ/qtrpdf/r_qt1412e.htm

— argues the dollar’s domination of reserves stems chiefly from the extent to which many currencies are tied either formally or through trade links like a dependence on oil or other dollar-priced commodities.

As a result, while the dollar’s overall value has declined by 18 percent since the 1970s against major currencies, and by more than half against the euro and yen, its share of reserves has fallen just 5 percentage points from 66 percent to 61 percent. …

… For the remainder of the report:

http://www.reuters.com/article/2014/12/07/banks-bis-currencies-idUSL6N0T…

end

2nd: (courtesy London’s Financial times)

Bank for International Settlements sounds alarm over dollar

end

The following is a blockbuster from Friday. I am repeating it just it case you missed it.

(courtesy Koos Jansen)

Koos Jansen: Belgium’s central bank considers repatriating gold

12:55a GMT Saturday, December 6, 2014

Dear Friend of GATA and Gold:

Following those in Germany and the Netherlands, Belgium’s central bank is considering repatriating its gold reserves, Bullion Star market analyst and GATA consultant Koos Jansen reports tonight, citing the Flemish commercial broadcaster VTM:

https://www.bullionstar.com/blog/koos-jansen/belgium-investigating-to-re…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Bill Holter puts it all together. The following is a must read…

(courtesy Bill Holter/Miles Franklin)

The Mother of all Bank Runs!

end

Early Monday morning trading from Europe/Asia

1. Stocks up on major Asian bourses with a higher yen value rising to 121.03 ( Moody’s lowering of its investment grade on Friday)

2 Nikkei up 15 points or 0.08%

3. Europe stocks all down /Euro down/ USA dollar index up to 89.42./

3b Japan 10 year yield at .44% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 117.70

3c Nikkei now above 17,000

3fOil: WTI 64.28 Brent: 66.36 /all eyes are focusing on oil prices. A drop to the mid 60′s would cause major defaults.

3g/ Gold up/yen up;

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt (see Von Greyerz)

3j German industrial production misses again sending European bourses into the toilet.

3k Japan loses battle in the defense of 120 yen to the dollar level/Japanese GDP shocks the world falling at 1.9% Q/Q (see zero hedge article below)

3l :BIS is shocked how broken the markets are behaving

3m Gold at $1196 dollars/ Silver: $16.31

3n USA vs russian rouble: 53.53 ( slightly stronger against the dollar)

4. USA 10 yr treasury bond at 2.32% early this morning.

5. Details: Ransquawk, Bloomberg/Deutsche bank Jim Reid

(courtesy zero hedge/your early morning trading from Asia and Europe)

China Surges, Japan Closes Green On Horrible Econ Data; Oil Tumbles To Fresh 5 Year Lows

Without doubt, the most memorable line from the latest quarterly report by the BIS, one which shows how shocked even the central banks’ central bank is with how perverted and broken the “market” has become is the following: “The highly abnormal is becoming uncomfortably normal…. There is something vaguely troubling when the unthinkable becomes routine.”

Overnight, “markets” did all in their (central banks’) power to justify the BIS’ amazement, when first the Nikkei closed green following another shocker of Japanese econ data, when it was revealed that the quadruple-dip recession was even worse than expected, and then the Shanghai composite soaring over 3000 or up 2.8% for the session, following news of the worst trade data – whether completely fabricated or not – out of China in over half a year. Perhaps the biggest surprise out of the broken, rigged market is that the massively overbought Dollar is actually listening to the BIS and as of this moment is at overnight lows, dragging European stocks (despite yet another miss of German industrial production printing at 0.2%, vs Exp. 0.4%, and the prior revised from 1.4% to 1.1%, something which normally would be super bullish) and US futures to session lows too: because it is truly shocking to see rationality in the “market” these days.

And speaking of China, it too is now caught in one of those New Normal infinite loops, with DB saying that the probability of a rate cut and liquidity flood by the PBOC – the primary driver for the recent market surge – has been slashed as a result of the market surge as China would be leery to fan the flames of the euphoric market any further. In other words, courtesy of the reflexive nature of central planning, the market has frontrun PBOC action so much it has effectively made such action impossible.

The Nikkei 225 closed slightly higher (+0.08%) as upside was capped with continued weakness in the JPY against the greenback, despite the final reading of the Japanese GDP Q/Q number -0.5% vs. Exp. -0.1% (Prev. -0.4%) confirming that the Japanese economy contracted. The Hang Seng (+0.5%) and Shanghai Comp (+2.9%) whipsawed in yet another volatile session, the latter breaking above 3,000 for the first since 2011 as Chinese Trade Balance (USD) (Nov) M/M 54.47bln vs. Exp. 43.95bln (Prev. 45.41bln) printed a record surplus aided of by lower oil prices. However, the export and imports component was weak as speculation mounts on further PBoC stimulus.

European equities have started this week under selling pressure, with Bunds ticking higher after being spurred on by dovish comments by ECB’s Nowotny stating that the ECB sees ‘massive weakening’ in the Euro-Area and remained downbeat on inflation. Nowotny was previously known as a hawk but was dovish on Friday and is now making very downbeat comments.

Bunds have now retraced all of the losses seen on Friday following the strong US jobs report and back to levels last seen during the ECB press conference. The continued divergence in the strong US economy and a weak European economy takes the US/GE 10yr spread to the highest levels since the Eurozone was formed at 157.5bps.

Downside seen in European equities is also attributed to the pull-back from Friday’s record highs. The FTSE 100 underperforms the European bourses as the materials sector drags the index lower due to Chinese Trade Balance data which showed a weak import and export component.

On the commodity front the one thing everyone is watching continues to be oil, where futures dropped for 5th Day, in part driven by Morgan Stanley cutting its 2015 Brent estimate by $28/bbl to $70 “With OPEC on the sidelines, oil prices face their greatest threat since 2009 and appear on track for an extremely volatile 2015.” Overnight brent trades down ~$1.50/bbl after hitting new 5-yr low of $67.35. WTI also lower, discount to Brent narrows. WTI speculator net-long positions increased in week through Dec. 2 as prices fell; Brent data due today. Kuwait Petroleum CEO sees oil staying near ~$65 for 6 months. “There is no discernible floor to the mkt right now, we are in for 3 mos., 6 mos, maybe longer of weak prices,” says Jefferies Bache senior broker Christopher Bellew, in London. “Prices may now go below $60 before recovering.” Jan. Brent -$1.43 to $67.64 as of 10:33am London, range $67.35-$68.79; 14-day RSI ~22%, agg volume down 21% on 100-day avg. WTI -$1.13 at $64.71; day low $64.59, earlier high $65.55; RSI ~26%. Brent-WTI narrows to $2.95, settled Friday at $3.23.

Today is the start of the two-day Eurogroup/ECOFIN finance ministers’ meeting which also marks an important date for Greece. Recent talks between Athens and the Troika have ended in something of a standstill and it looks increasingly likely that a technical extension to the programme will be required although the finer details remain unclear – we could however hear some greater clarification around the topic over the next couple of days.

In summary: European shares remain lower with the construction and oil & gas sectors underperforming and tech, basic resources outperforming. The U.K. and French markets are the worst-performing larger bourses, the Spanish the best. China’s Shanghai Composite index rises to 3-year high, trade surplus advances to record. Japan 3Q GDP below estimates. German industrial output also less than estimated. Russian 10-year yields rise to 5-year high, Brent crude drops to 5-year low. The euro is weaker against the dollar. Japanese 10yr bond yields rise; German yields decline. Commodities decline, with oil underperforming and silver outperforming.

Market Wrap:

- S&P 500 futures down 0.3% to 2070

- Stoxx 600 down 0.3% to 349.8

- US 10Yr yield up 2bps to 2.32%

- German 10Yr yield down 4bps to 0.74%

- MSCI Asia Pacific down 0% to 139.9

- Gold spot up 0.2% to $1195.2/oz

Bulletin Headline Summary from RanSquawk and Bloomberg

- European equities in negative territory across the board with earlier ECB’s Nowotny comments denting Eurozone sentiment as bleak Eurozone prospects are highlighted.

- EUR, JPY, CNY, AUD all trade near lows against the greenback as policy divergence is the theme of today’s session.

- Looking ahead, today’s data slate is relatively light with Canadian Housing Starts, Building Permits with possible comments from Fed’s Lockhart, ECB’s Draghi and Coeure.

- Treasuries decline, 2Y yield at highest since April 2011, 3Y approaching YTD high, as Friday’s strong Nov. employment report spurred reassessment of how soon Fed may begin raising interest rates.

- China’s exports rose 4.7% in Nov., less than 8% median estimate in Bloomberg News survey; imports fell 6.7% vs expectations for 3.8% increase, leaving a trade surplus of $54.47b, the customs administration said today

- PBOC adviser Chen Yulu expects 2015 China GDP growth at about 7.1% and inflation at about 2.5%, Takungpao reports, citing an interview

- Japan’s economy contracted an annualized 1.9% in 3Q, weaker than the 1.6% preliminary estimate amid a surprise decline in business investment; result was below every forecast in a Bloomberg News survey that showed a median 0.5%

- German industrial production gained 0.2% in October, less than the median estimate of 0.4% in a Bloomberg News survey

- ECB Governing Council member Ewald Nowotny sees “high probability” that inflation rate will slow further in 1Q, ECB sees “massive” weakening in euro-area economy, with Germany contributing to downturn

- Nowotny also told reporters in Frankfurt that for any potential QE, “the biggest relevant market surely is the market for government bonds”; “there’s a possible debate about corporate bonds, and you could think about other things”

- The U.S. said it was unaware of the possibly imminent release of a South African hostage in Yemen, who was killed during a raid to free one of his American co-captives

- The euro area signaled that Greece will win extra time to qualify for its next installment of international aid as the government in Athens resists calls for more spending cuts

- As Alexis Tsipras, leader of the Coalition of the Radical Left, moves closer to taking control of Greece, most indebted country, he’s trying to convince bond investors they have nothing to fear

- Eleven months after New Jersey Governor Chris Christie apologized for deliberate traffic jams at the George Washington Bridge, no evidence has linked him to the plot

- Sovereign yields mostly higher. Nikkei little changed while Shanghai +2.8%. European stocks fall; U.S. equity-index futures higher. Brent crude declines to a new five-year low, gold higher, copper falls

FX

EUR, JPY, CNY, AUD are all trading near their lows with each respective country erring towards easing. The latest weak currency in focus is now the Yuan which is at its lowest levels since August with the Shanghai comp speculating further easing closing higher by 2.9%.

WSJ sources suggest China’s banks are pressing the PBOC to cut the RRR as banks want to reduce the share of deposits it must set aside.

Over the weekend the BIS warned that the strong USD will hurt EM economies and companies, as borrowers leveraged with cheap debt will now have to repay more because of currency moves. This may cause serious issues and threaten financial stability and has pushed EM currencies to their weakest since 2000. YTD USD is up more than 10% against EUR.

Weakening commodity prices (oil and iron ore) is impacting global corporates and oil producing nations such as Russia, Nigeria and Venezuela who are feeling the pain. The Middle East has larger wealth funds to weather the storm but analysts are already forecasting Saudi’s revenues as a nation will fall by 16%. On the corporate front both BP, Total and Anglo American have warned about falling commodity prices and are already on cost cutting drives.

ZAR is at a six year low, TRY has weakened to lowest levels in a month, IDR and MYR at their lowest since 2008/2009.

Fridays CFTC data shows all currencies are net short against the USD which is a trend that is expected to continue.

From a technical perspective analysts have noted the USD index may well have the momentum to break above the 2009 high of 89.63 as this time instead of a flight to quality boosting the USD the recent move is now a story of fundamental strength in the US economy, as evident in Friday’s jobs report.

With ECB, RBA, PBOC and BOJ having an easing bias and as the USD continues to firm, GBP has benefited as it is the only major central bank likely to follow a Fed rate hike. Weekend BOE reports that the UK could withstand a rate hike also helping.

COMMODITIES

In the energy complex, WTI and Brent futures recover some of the overnight losses following the slight pullback from highs seen in the USD-index but still trade in a particularly tight range with a lack of macro-news giving commodities a lack of direction as the US-index settles around the 88.50 level. Furthermore, Fitch cut Brent oil price to USD 83 per barrel in 2015, USD 90 per barrel in 2016 on the back of Brent Futures falling to its lowest level since October 2012 on the subsequent USD strength with Morgan Stanley also slashing its 2015 base case forecast for Brent to USD 70 from USD 98 and for 2016 to USD 88 from USD 102. In its bear-case scenario, the bank sees Brent falling to a low of USD 43 in the Q2’15.

DB’s Jim Reid concludes the overnight even recap

It’ll be interesting to see the ramifications this week from the largest payroll print since January 2012 on Friday. It certainly spices things up ahead of next week’s FOMC. Indeed, the +321k headline print came in well ahead of market consensus of +225k and there were total cumulative upward revisions of 44k – which in turn has lifted the three-month average growth rate to 278k and the fastest since 2006. Perhaps more encouragingly for the economy was the breadth of job gains which showed impressive broad-based growth. The diffusion index of private employment (a measure of the breadth of job gains) touched 69.7 – now the highest reading since January 1998. With regards to other employment indicators, the unemployment rate remained unchanged at 5.8% along with the labour force participation rate at 62.8% although the broader U-6 measure dropped down to 11.4% which represents the lowest level since September 2008. Finally, average hourly earnings climbed +0.4% mom (vs. +0.2% mom expected) which ticked the annual rate up a notch to +2.1%.

Taking a look at the price action on Friday, the Treasury curve flattened with 2yr yields closing 10bps higher at 0.643% – the highest level since early 2011 whilst 10yr notes (+7bps) and 30yr notes (+3bps) advanced to 2.307% and 2.967% respectively. In terms of Fed Funds expectations, the Dec15 contract jumped 11bps to 0.64%, although this still remains below the highs of earlier in the year, whilst further out the curve the Dec16 contract rose 14bps to 1.59%. Meanwhile the Dollar closed firmer, with the DXY Index advancing +0.63% including a notable gain against the JPY (+1.68%) to close at a seven year high of ¥121.46. Equity indices on the other hand were fairly subdued, perhaps weighed down somewhat following declines to both WTI (-1.45%) and Brent (-0.82%) – which have slid further this morning – dragging down energy stocks. The S&P closed +0.17% and Dow Jones +0.33% – although both finished at record highs. With the final FOMC meeting of 2014 due next week on the 16th, we’ve got limited Fedspeak running up to the event so the market may be forced to wait before getting any official reaction from members.

Turning our attention to the reaction in Asia this morning, markets in China are generally leading the way with the CSI 300 +2.93% and marking its twelfth consecutive day of gains. These gains come on the back of trade data out of China which shows the economy reporting a record trade surplus of $54.47bn, up from $45.4bn in October and boosted by an unexpected fall in imports to -6.7% yoy (vs. expectations of +3.8%). Elsewhere around Asia, bourses are generally mixed as we type. There are modest gains for the Hang Seng (+0.20%, whilst the ASX 200 is +0.70% after results over the weekend showed that Australian banks, as expected, would be required to hold additional capital to cover potential loan losses. Elsewhere in Japan the Topix (-0.08%) is softer after a downward revision to Q3 GDP to -1.9% SAAR.

Returning back to China, our colleagues have noted that the recent equity rally since the surprise rate cut on 21st November (Shanghai +18.1%) has lowered the probability of a cut in the reserve requirement ratio (RRR) to under 20% from 40% initially following the rate cut. Although the rally in equities reflects a strong expectation that policy easing is coming soon, they suggest that cutting the RRR amid a sharp stock market rally may add fuel to the fire and jeopardize financial stability. This is especially true given the sharp rise in financial leverage in the market currently along with tight liquidity conditions. Overall they think the recent market rally may delay major policy easing measures.

Also of note within DB this weekend was our US credit strategy colleagues publishing their 2015 Outlook. We’ve been discussing the recent spread divergence between European (tighter) and US credit (wider) with them a lot of late and we both think it could go further at the start of 2015. As a start, with the ECB likely about to go in the opposite direction of the Fed the technicals are different. Experience though tells us that a large decoupling is unlikely but we expect more widening before US credit starts to out-perform. A lot also depends on where Oil prices go early in 2015. The problem is that few have genuine intelligence here. Oil is down by 37% since June and our commodity strategists see a possibility of further price declines given the likely over supply. In their Outlook our US credit strategists have updated their recent analysis showing that the weakest US shale producers could enter a zone of deep distress at oil prices below $60/bbl. Their updated analysis shows they could actually have an additional $5 room before this happens. If prices were to stay sustainably below these levels for a few months/quarters, chances of a broad sector restructuring increase materially. This scenario would have repercussions for the timing of the overall HY default cycle. With this, they believe HY defaults have seen their lows for this cycle at 1.7% in September, and are now heading towards a 3.5% level next year.

Just wrapping up the moves on Friday, risk assets ended the week on a positive foot in Europe with the Stoxx closing +1.8% and Xover rallying 10bps tighter. Following stronger than expected German factory orders (+2.5% mom) and firmer Spanish industrial output (+1.2% yoy), 10yr benchmark yields in Spain (-5bps), Italy (-6bps) and Portugal (-5bps) hit fresh lows at 1.83%, 1.98% and 2.75% respectively. Rounding off the data releases on Friday, preliminary Q3 GDP for the Euro-area was confirmed at +0.8% yoy.

Before we look at this week’s calendar, today is the start of the two-day Eurogroup/ECOFIN finance ministers’ meeting which also marks an important date for Greece. Recent talks between Athens and the Troika have ended in something of a standstill and it looks increasingly likely that a technical extension to the programme will be required although the finer details remain unclear – we could however hear some greater clarification around the topic over the next couple of days.

Looking at the week ahead, the calendar is reasonably light following the usual post-payrolls lull for data. We kick this morning off in Germany with industrial production followed soon after with the business sentiment reading out of France. As mentioned the two-day Eurogroup meeting starts today whilst over in the US we just have the Fed labour market conditions index due out. On Tuesday we have the continuation of the Eurogroup meeting in Brussels with notable data prints for the morning session being trade data out of Germany and France as well as industrial and manufacturing production in the UK. Across the pond in the afternoon we are expecting consumer optimism, wholesale inventories and perhaps of the more interest the JOLTS October print which DB expect to be strong although they note the one month lag versus other employment indicators. On Wednesday we kick off the morning in Asia with data out of China including CPI, PPI and money supply as well as consumer confidence in Japan. We follow this up in Europe with industrial and manufacturing data out of France followed by trade data in the UK. Attention in the afternoon however will likely be on the US budget print for November. Perhaps of some interest, the OPEC monthly oil report is due out on Wednesday at some point also. We start Thursday with machine orders data due out of Japan, although eyes will likely be on the European session with the final CPI print due for Germany (+0.6% yoy) as well as inflation data due for France and Portugal. In the afternoon in the US, the market will likely be focused on the retail sales reading as well as claims, business inventories and the import price index. We close the week out on Friday with capacity utilisation and industrial production due out of Japan, as well as the industrial production, retail sales and fixed asset investment prints for China. Closer to home in Europe on Friday, we have wholesale inventories due in Germany, as well as inflation prints in Spain and Italy (final) and finally industrial production for the Euro-area. Finally, over in the US we will keep an eye out for the PPI and University of Michigan prints.

end

Japan slides deeper than expected as their recession is getting a pretty good stronghold. Japan is having record number of bankruptcies. In the latest quarter the drop in GDP is 1.9% Q over Q

(courtesy zero hedge)

Nikkei Slides Back Below 18,000 On Deeper-Than-Expected Recession, Record Bankruptcies

Remember when that absolute disaster of a Q3 GDP print hit Japan and the world of talking-heads proclaimed… “yeah, but.. capex revisions and stuff and things will make it all better” or some such nonsense? Well that’s exactly what it was – utter nonsense. Going entirely the opposite direction to expectations of a revision up to -0.5% QoQ, Japanese GDP was revsied even lower to -1.9% QoQ (from -1.6% QoQ initial) confirming the quadrupled-dip-recession. Add to that the fact that Abenomics has ushered in record bankruptcies this year as small- and medium-sized businesses have been crushed by soaring import costsamid the collapsing JPY and you have a recipe for domestic disaster… and having rallied in anticipation of the exuberant revisions in Friday’s US session, Japanese stocks are sliding quickly off the 18,000 level.

Quadruple-dip recession… well played Abe…

Goldman was surprised… and is not very hopeful about the future…

Government revised down real GDP, contrary to expectations: The government’s second estimate for Jul-Sep (3Q) 2014 real GDP came in at -1.9% qoq annualized, a slight downward revision from the first estimate of -1.6% and contrary to the market forecast for an upward revision to -0.5%. In the second set of estimates, the government mainly adjusts its capex and inventory figures to reflect MOF Corporate Statistics announced the week before. In the latest MOF Corporate Statistics, capex turned upward qoq, and the market accordingly expected the capex figure in the second set of GDP estimates to be raised (from -0.9% qoq annualized in the first preliminary data). In a surprise move, however, the government revised down the capex figure to -1.5% qoq annualized. Meanwhile, it slightly raised its estimate for the contribution from inventories to -2.5 pp, from -2.6 pp, and slightly lowered estimates for government spending and public fixed capital formation.

Nominal GDP was revised downward from -3.0% to -3.5% qoq annualized.

We expect a GDP rebound in 4Q, but the momentum of recovery will likely be weak: The pullback from pre-tax-hike rush demand is gradually fading. However, we see potential for declining real disposable incomes and high inventory levels to continue exerting downward pressure on domestic demand that deals a setback to the economy for a comparatively long time. We look for real GDP to rebound from two quarters of contraction in 4Q, but we think the strength of recovery will be weak.

Oh, and don’t forget record bankruptcies…

Japanese stocks are – for once – actually selling off modestly haveing ripped higher on Friday in anticipation of the exuberant upward revision everyone hoped for…

Rather notably decoupling from USDJPY!!

* * *

On a side note, PBOC fixed the Yuan at its strongest against the USDollar since March as the market’s view of USDCNY started to rapidly weaken…

* * *

end

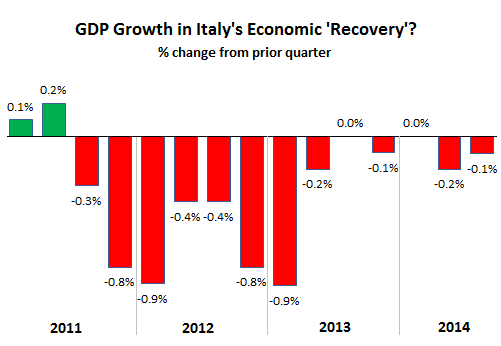

Wolf Richter comments on the cut in Italy’s grade to only one notch above junk as their economy is one big mess”

(courtesy Wolf Richter/Wolfstreet/com)

S&P Wakes Up, Cuts Italy to One Notch Above Junk, Economy Sinks into Terrific Mess

by Wolf Richter • December 5, 2014

Italy has one of the most troubled economies in the EU. Businesses and individuals are buckling under confiscatory taxes that everyone is feverishly trying to dodge. Banks are stuffed with non-performing loans that have jumped 20% from a year ago. The economy is crumbling under an immense burden of government debt that, unlike Japan, Italy cannot slough off the easy way by devaluing its own currency and stirring up a big bout of inflation – because it doesn’t have its own currency.

Devaluation and inflation used to be Italy’s favorite methods of dealing with its economic problems. It went like this: Politicians made promises that they knew couldn’t be kept but that bought a lot of votes. When everything ground down as industries were getting hammered by competition from across the border, the government stirred up inflation, and then over some weekend, the lira would be devalued. It was bitter medicine. It was painful. It didn’t even cure anything. It impoverished the people. But it temporarily made Italy competitive with its neighbors once again.

Most recently, Italy devalued in 1990 and then again 1992 against the European Exchange Rate Mechanism, a predecessor to the euro. Having to take this bitter medicine time and again had made Italians the most eager to adopt the euro. The idea of a currency that would be out of reach of politicians and that would function as a reliable store of value, run by the Germans as if it were the mark, and in turn, keep politicians honest – all that seemed like paradise.

But it just hasn’t kept Italian politicians honest.

Only this time, their favorite tools are gone. The economy is now a mess. Economic “growth” has been negative or zero for the last 13 quarters. It looks like this:

And the country’s debt, no matter of how hard the government tries to fudge the numbers, just keeps ballooning.

So, on Friday, ratings agency Standard & Poor’s woke up and cut Italy’s sovereign credit rating to BBB–, just one notch above junk, which is the dreaded BB. It cited the economy’s perennial shrinkage and lousy competitiveness. The deteriorating economic fundamentals and a political unwillingness to address the deficit were making the mountain of public debt increasingly unsustainable.

The ECB has been busy doing “whatever it takes” to keep the cost of funding this wobbly construct as low as possible. It lowered its own benchmark interest rate to near zero. It instituted negative deposit rates, it’s contemplating a big round of QE, all to keep Italy (and some of its cohorts) afloat a little while longer.

The last time S&P struck out at Italy was in July 2013, when it knocked the credit rating down to BBB from BBB+. This is a slow tango that is falling further behind reality. Without the backdoor bailout from the ECB, which is run by Italian Mario Draghi, Italy would by now be discussing fashionable high-and-tight haircuts with its creditors.

And that would be a good thing for Italy – but no, wait….

These creditors include Italy’s largest banks who’ve been the dominant buyers of this crappy debt, with money they get from the ECB for free. It’s the easiest way to profit. Why even bother lending to struggling Italian companies? Hence the ECB’s guarantee on the Italian debt. It must not be allowed to blow up.

It just hasn’t done anything to solve Italy’s problems.

Yet Italy is a country of entrepreneurs and of vibrant small enterprises. Or was. Now these businesses are dying. “We are crushed by our country’s debt,” one of them told me. Read… Italy’s Crazy New Economy from Hell

end

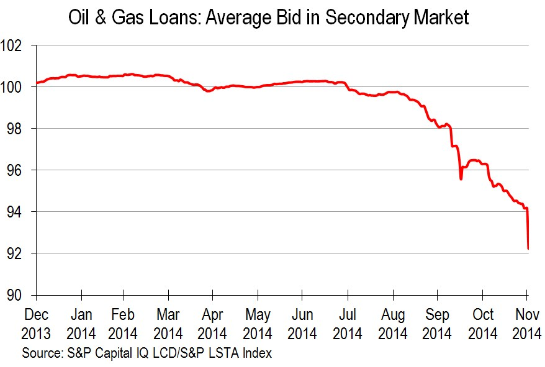

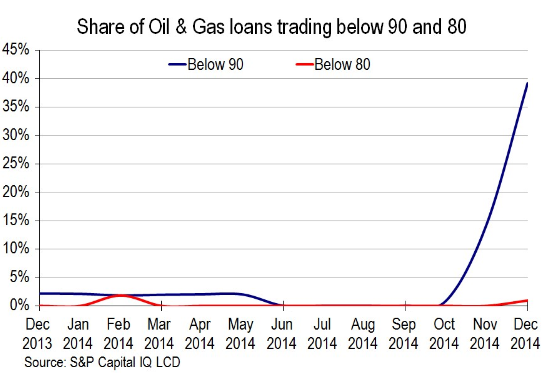

With an encore, Wolf Richter discusses the huge oil and gas bloodbath that await the global economic scene:

(courtesy Wolf Richter/WolfStreet)

Oil and Gas Bloodbath Spreads to Junk Bonds, Leveraged Loans. Defaults Next

by Wolf Richter • December 7, 2014