Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1219.30 up $15.40 (comex closing time)

Silver: $16.60 up 42 cents (comex closing time)

In the access market 5:15 pm

Gold $1218.50

silver $16.53

Today we had a lot of developments. First WTI breaks into the 47 dollar column creating havoc for our sovereign countries loaded with oil e.g Canada, Russia, USA, England (North sea), Venezuela etc. The dollar keeps rising due to the breaking up of the dollar carry trade. As we have mentioned to you on many occasions, this in turn blows up the derivatives in oil and the major banks who have underwritten much of these contracts when oil was north of 100 dollars per barrel. It certainly looks like the bankers are having a tough time trying to contain gold.

Generally the bankers do not like to see gold/silver rise on two consecutive days, but that is what we got today.

Over in Greece, the Oxford Economic group have done a lot of research into the upcoming election and they have come to the conclusion that Syriza will have a majority and as such Syriza can ask for a Greek haircut or pullout of the Euro monetary zone. Markets reacted negatively to this news.

In other developments we are witnessing the Euro/Swiss Franc trade at 1.20088 as I publish this report. The Swiss National bank is the only guys bidding for Euros. If this all important 1.20 peg is broken you can be assured this will create a lot of havoc for the Swiss government and its citizens.

The gold comex today had a poor delivery day, registering 0 notices served for nil oz. Silver comex registered 0 notices for nil oz.

Three months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 246.72 tonnes for a loss of 56 tonnes over that period.

In silver, the open interest rose by 17 contracts as yesterday’s silver price rose by 45 cents. It is obvious that somebody is taking on the banks. The total silver OI still remains relatively high with today’s reading at 151,282 contracts. The January silver OI contract reads 91 contracts.

In gold we had an increase in OI with the rise in price of gold on yesterday to the tune of $12.90. The total comex gold OI rests tonight at 378,485 for a gain of 3,391 contracts. The January gold contract reads 150 contracts

TRADING OF GOLD AND SILVER TODAY

you have more important things to read instead of how gold/silver traded today.

Today, we lost 2.99 tonnes of gold/Inventory 707.82 tonnes

In silver, we lost 149,000 oz of silver inventory/

SLV’s inventory rests tonight at 329.415 million oz

.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today

.

First: GOFO rates:

Today, the rates hardly moved. The one month GOFO stayed stationary and in backwardation. The two month GOFO moved more negative.

The Three MOnth GOFO went to zero and thus still in backwardation. The 6 month and 12 month are positive and out of backwardation and it moved more to the positive needle.

Sometime in January the LBMA will officially stop providing the GOFO rates.

Jan 6 2015

-.05% -0300% -.00% +.0167 .145%

Jan 5 2014:

-.05% -.025% -.01330 % +.015% +.1375%

end

Let us now head over to the comex and assess trading over there today.

Here are today’s comex results:

The total gold comex open interest rose today by 3,301 contracts from 375,184 all the way up to 378,485 with gold up by $12.90 yesterday (at the comex close). We are now onto the January contract month. The non active January contract month saw it’s OI fall by 209 contracts down to 150. We had 0 contracts served yesterday. Thus we lost a massive 209 contracts or 20,900 oz will not stand. Obviously this was cash settled with a fiat bonus. The next big delivery month is February and here the OI rose by 1819 contracts to 218,396 contracts. The estimated volume today was poor at 76,287. The confirmed volume yesterday was fair at 159,496 contracts, even although they had some help from our high frequency traders. The comex now has no credibility and many investors have vanished from this crooked casino. Today we had 0 notices filed for nil oz .

And now for the wild silver comex results. Silver OI rose by 17 contracts from 151,265 up to 151,282 as silver was up by 45 cents yesterday. The front January contract month saw its OI fall by 12 contracts down to 91. We had 12 notices filed yesterday, so we neither gained nor lost any silver contracts standing for silver in the January contract month. The next big contract month is March and here the OI fell by 346 contracts down to 102,606. The estimated volume today was simply awful at 17,598. The confirmed volume yesterday was excellent at 50,058. We had 0 notices filed for nil oz today.

January initial standings

Jan 6.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | nil oz |

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 36,972.500 (Scotia) 1150 kilobars oz |

| No of oz served (contracts) today | 0 contracts(nil oz) |

| No of oz to be served (notices) | 150 contracts (15,000 oz) |

| Total monthly oz gold served (contracts) so far this month | 2 contracts(200 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

192.9 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

we had 0 dealer deposit:

total dealer deposit: nil oz

we had 0 customer withdrawals

total customer withdrawal: nil oz

we had 1 customer deposits: the farce continues

i) Into Scotia; 36,972.500 oz (1150 kilobars)

total customer deposits; 36,972.500 oz oz

We had 0 adjustments

Today, 0 notice was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the December contract month, we take the total number of notices filed for the month (2) x 100 oz or 200 oz to which we add the difference between the January OI (150) minus the number of notices served upon today (0) x 100 oz =15,200 the amount of gold oz standing for the January contract month. (.4727 tonnes of gold)

we lost a whopping 20,900 oz to cash settlements.

Thus the initial standings:

2 (notices filed for the month x 100 oz) +OI for January (150) – 0(no. of notices served upon today) =15,200 oz (.4727 tonnes)

we lost a whopping 20900 oz to cash settlements.

Total dealer inventory: 770,987.09 oz or 23.98 tonnes

Total gold inventory (dealer and customer) = 7.932 million oz. (246.72) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 56 tonnes have been net transferred out. We will be watching this closely!

This initializes the month of January for gold.

end

And now for silver

Jan 6 2015:

January silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | 1,178,381.35 (Delaware, HSBC,Scotia) oz |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil oz |

| No of oz served (contracts) | 0 contracts (60,000 oz) |

| No of oz to be served (notices) | 91 contracts (455,000 oz) |

| Total monthly oz silver served (contracts) | 28 contracts (140,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,714,405.5 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 0 customer deposits:

total customer deposit nil oz

We had 3 customer withdrawals:

i) Out of Delaware: 5,926.75 oz

ii) Out of HSBC: 914,827.26 oz

iii) Out of Scotia; 257,627.34 oz

total customer withdrawal: 1,178,381.35 oz

we had 1 adjustments

i)Out of Delaware/an accounting error and 1058.78 oz was subtracted out of inventory.

Total dealer inventory: 64.662 million oz

Total of all silver inventory (dealer and customer) 174.359 million oz.

The total number of notices filed today is represented by 0 contracts for nil oz. To calculate the number of silver ounces that will stand for delivery in December, we take the total number of notices filed for the month (28) x 5,000 oz to which we add the difference between the OI for the front month of January (91) – the Number of notices served upon today (0) x 5,000 oz = 595,000 oz the number of ounces standing so far for the January delivery month.

Initial standings for silver for the January contract month:

28 contracts x 5000 oz= 140,000 oz +OI standing so far in January (91)- no. of notices served upon today(0) x 5,000 oz = 595,000 oz

we neither gained nor lost silver ounces standing for the January contract month.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.com or http://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

Jan 6.2015: we lost 2.99 tonnes of gold from the GLD./Inventory 709.82

Jan 5/2015 we added 1.79 tonnes of gold inventory into the GLD/Inventory tonight: 710.81 tonnes

Jan 2 2015: inventory remained constant/inventory 709.02 tonnes

Dec 31.2014: we lost another 1.79 tonnes of gold at the GLD today/Inventory 709.02 tonnes

Dec 30.2014/ we lost 1.49 tonnes of gold at the GLD today/inventory 710.81 tonnes

Dec 29.2014 no change in gold inventory at the GLD/inventory 712.30 tonnes

Dec 26.2013/ a small loss of .6 tonnes of gold. Inventory tonight at 712.30 tonnes

Dec 24.2014: wow!! somebody robbed the cookie jar/ we had a huge withdrawal of 11.65 tonnes from the GLD inventory/inventory at 712.90 tonnes. England must be bleeding badly!

Dec 23.2014; no change in gold inventory at GLD/724.55 tonnes

Dec 22.2014: no change in gold inventory at the GLD/724.55 tonnes

Dec 19.2014: a huge addition of 2.99 tonnes at the GLD/724.55 tonnes

Dec 18.2014: no change in inventory at the GLD/721.56 tonnes

Dec 17.2014: no change in inventory at the GLD/721.56 tones

Dec 16.2015 we lost 1.80 tonnes in tonnage at the GLD/721.56 tonnes

Dec 15.2014: we lost 2.39 tonnes of gold inventory at the GLD/Inventory at 723.36 tonnes

dec 12.2014: we had no change in gold inventory/GLD inventory 725.75 tonnes

Dec 11.2014: we had another addition of .95 tonnes of gold inventory at the GLD/Inventory 725.75 tonnes

Today, Jan 6/2015 / we lost 2.99 tonnes in gold inventory at the GLD /Inventory rests tonight at 707.82 tonnes

inventory: 707.82 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 707.82 tonnes.

end

And now for silver (SLV):

jAN 6.2015: we had a small loss of 149,000 oz/inventory 329.415 million oz

Jan 5 no change in silver inventory/Inventory at 329.564 million oz

jan 2.2015: no change in silver inventory/ Inventory 329.564 million oz

Dec 31.2014: we had no change in silver inventory at the SLV./Inventory

at 329.564 million oz

Dec 30.2014: we lost another 574,000 oz of silver from the SLV/Inventory at 329.564 million oz/

Dec 29.2014 we had a small loss of 431,000 oz at the SLV to probably pay for fees/inventory 330.138 million oz.

Dec 26/ no change in silver inventory at the SLV/inventory 330.569

million oz.

Dec 24.2014: we had a huge loss of 7.566 million oz/inventory 330.569 million oz

Dec 23.2014: no change in silver inventory/338.135 million oz

Dec 22.2014: today we lost 862,000 oz of silver inventory from the SLV. this left late Friday night./Inventory 338.135 million oz

Dec 19.2014; No change in silver inventory at the SLV/Inventory 338.997 million oz.

Dec 18.2014: we lost 2.012 million oz of silver from the SLV vaults/inventory 338.997 million oz

Dec 17.2014: no change in silver inventory/SLV 341.009 million oz

Dec 16.2014/ no change in silver inventory/SLV 341.009 million oz

Jan 6/2015 /we had a small loss of in silver inventory at the SLV to the tune of 149,000 oz

registers: 329.415 million oz

end

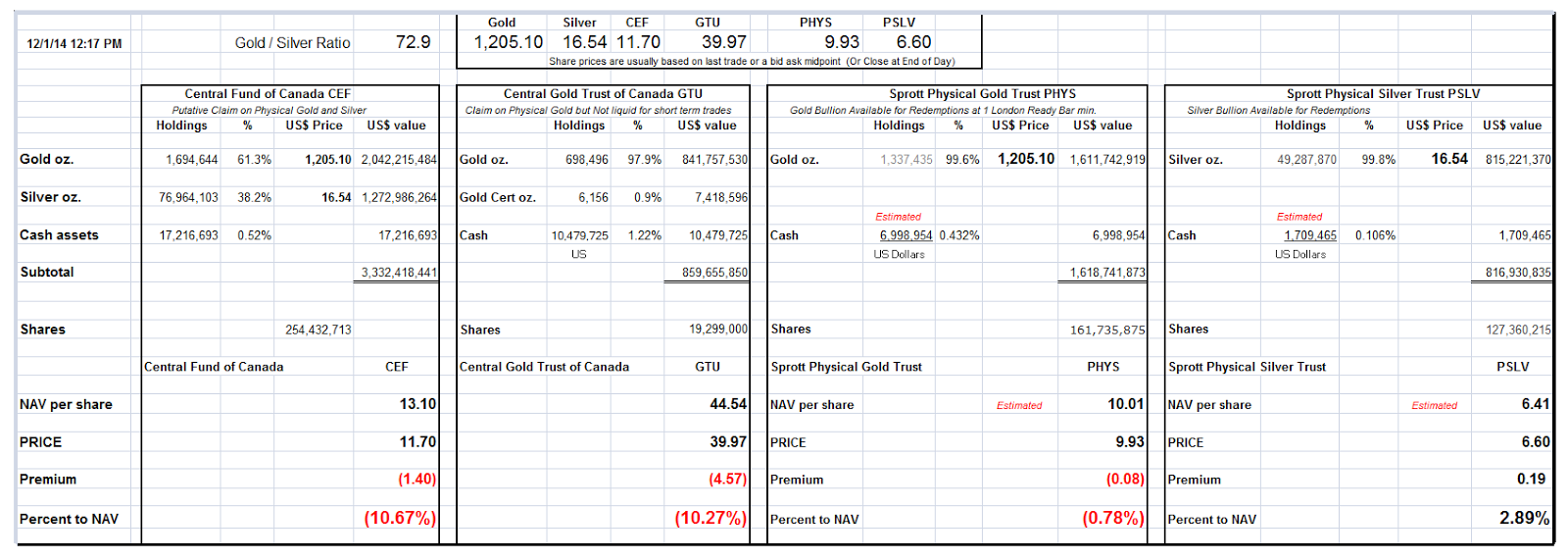

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now for the first time into the negative to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 8.2% percent to NAV in usa funds and Negative 8.0 % to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.8%

Percentage of fund in silver:37.8.%

cash .4%

( Jan 6/2015)

2. Sprott silver fund (PSLV): Premium to NAV rises to + 1.08%!!!!! NAV (Jan 6/2015)

3. Sprott gold fund (PHYS): premium to NAV rises to negative -0.48% to NAV(Jan 6/2015)

Note: Sprott silver trust back into positive territory at +1.08%.

Sprott physical gold trust is back in negative territory at -0.48%

Central fund of Canada’s is still in jail.

end

And now for your most important physical stories on gold and silver today:

Early gold trading from Europe early Tuesday morning:

(courtesy Mark O’Byrne)

‘Grexit’ Risk and Lehman Collapse Concerns See Euro Gold at 1,020 Per Ounce

With Greeks going to the polls to elect a new government in just over two weeks, concerns over a potential Greek exit or ‘Grexit’ from the euro is growing and this has led to the euro falling against the dollar and particularly gold.

Speculation as to the consequences of a Syriza victory has caused the euro to fall to it’s lowest level against the dollar since 2010. Gold has surged to close to EUR 1,020 per ounce this morning – building upon the 11% gains seen in 2014.

Gold in Euros – 10 Years (Thomson Reuters)

Over the weekend Germany’s Der Spiegel reported Angela Merkel’s view that Germany would be “comfortable” with a Greek exit and that “any fallout would be manageable.”

That the Chancellor felt the need to make such comments is been seen by some as an attempt to scare the Greek people away from voting for anti-austerity group Syriza.

Syriza’s leader, Alexis Tsipras has already indicated that it is not his intention to pull Greece out of the Euro-zone but to renegotiate certain aspects of the bailout agreements with the Troika, particularly those seen as an unjust debt burden placed on average Greek citizens.

However, it may be that Germany fears the precedent of reopening negotiations between the Troika and Greece lest other countries upon whom onerous conditions were placed – such as Ireland – follow their example.

The assertion that the EU could “comfortably” manage the exit of Greece is a silly one – particularly at this very delicate and uncertain time.

European sanctions on Russia appear to be taking a significant toll on the already fragile European economy. Italy’s former Prime Minister, and former head of the European Commission, Romano Prodi, highlights the problem thus:

“The lowering of the oil and gas prices in combination with the sanctions, pushed by the Ukrainian crisis, will drop the Russian GDP by five percent per annum, and thus it will cause cutting of the Italian exports by about 50%.”

Similar dynamics are playing out in Poland and France.

Continued antagonisation of Russia may have dire consequences for Europe, if Russia chooses to respond more aggressively. France’s Societe General, alone, is exposed to Russia to the tune of €26 billion.

Were Russia to renege on this and other obligations to European banks it would likely trigger a Lehman’s style crisis.

Or Russia could cut its supplies of natural gas to Europe upon which German industry, in particular, relies. Thankfully, for now, Russia has reacted with cool heads, even inviting Europe to become a partner in the newly formed Eurasian Economic Union.

Germany is now dangerously close to deflation as the major states reported from 0% to 0.3% inflation in December, with Saxony at 0.5%, – down from November rates of between 0.5% and 0.8%.

With these and countless other considerations weighing upon the EU, it is not accurate to suggest that a Greek exit and return to the drachma could be comfortably managed.

For one, there is no framework in place for an orderly secession of a member state from the Union. An antagonistic break up would likely cause contagion to many large banks exposed to Greece.

The ensuing turmoil might also prompt other member states to break away in chaotic fashion – Spain, Portugal and Italy being prime contenders.

Many periphery nations are slowly becoming jaded by the not so single currency – which for almost half it’s existence has been in crisis.

It is likely that the EU will do everything in it’s power to accommodate Syriza should they gain power in Greece. Whether it will be enough to keep Greece on board and the drachma off the printing presses remains to be seen.

Gold will protect from currency devaluations – whether that be in the form of the euro itself being devalued or in the form of reversions to drachmas, escudos, pesetas and punts and subsequent devaluations.

Review of 2014 – Gold Second Best Currency, +13% in EUR, +6% GBP

MARKET UPDATE

Today’s AM fix was USD 1,211.00, EUR 1,017.31 and GBP 797.08 per ounce.

Yesterday’s AM fix was USD 1,192.00, EUR 998.91 and GBP 779.90 per ounce.

Spot gold rose $18.00 or 1.52% to $1,205.50 per ounce yesterday and silver soared $0.41 or 2.6% to $16.20 per ounce.

Gold in Euros – 5 Years (Thomson Reuters)

In Singapore, gold continued to eke out gains prior to a small drop off in prices in London trading from $1,214 per ounce to $1,209 per ounce.

Gold’s safe haven status is being appreciated anew due to the concern that Greece may exit the monetary union. This made the euro plummet against the dollar to it’s lowest point since 2006 and euro gold surged to touch €1,020 per ounce.

A close above €1,000 per ounce today will be important technically and could see gold challenge the next level of resistance at €1,072 and then €1,140 per ounce. Gold in euros rose 11% in 2014 – possibly in anticipation of the coming problems in the Eurozone – and appears to consolidating on those gains.

Gold is up over 7.2% since reaching a four-year low in early November 2014.

Traders and hedge funds are becoming jittery over the uncertain snap elections to occur in Greece in 3 weeks which could lead to their exit from the EU. U.S. Commodities and Futures Trading (CFTC) figures show short wagers slid 8.2% and net-long positions rose 5.7% to 98,391 futures and options in the week ended Dec. 30th, after dropping 11% in the previous two week

Bullish bets on gold bullion have doubled since November and have risen for the first time in three weeks.

Shanghai Gold Exchange (SGE) premiums were $5-$6 an ounce over the global benchmark. Chinese buying has increased ahead of their Lunar New Year holiday, where gold is purchased for gifts, and demand will most likely remain strong until the holiday in February.

The Perth Mint‘s sales of gold coins and minted bars fell to a four-month low in the traditionally slow month of December.

CME Group announced today that it will launch its kilobar contract in Hong Kong on January 26.

This new contract will be listed on COMEX and will have contract listings similar to the familiar structure of the benchmark 100 troy ounce Gold Futures contract listed on COMEX. It will be tied directly to 9999 gold prices in Hong Kong and can be physically delivered in Hong Kong.

“The introduction of our Gold Kilo Futures contract will provide price discovery in this key Asia bullion trading hub to market participants around the world, virtually 24 hours a day,” the CME said in a statement.

Chinese demand remains robust but has fallen from higher levels seen in recent days and is down from $7 yesterday to $4 or$5 today.

Silver was up another 1% at $16.40 an ounce. Platinum was up 0.9% at $1,215.50 an ounce, and spot palladium was up 1.1% at $798.45 an ounce.

Get Breaking Gold News and Updates Here

end

Sprott funds saw another 30,000 oz of gold bullion redeemed.

From Dec 1.2014 until now, a total of 66,680 oz or 2 tonnes have been redeemed. It looks like the bankers are desperate to find any physical gold around:

(courtesy Jessie/American cafe)

NAV Premiums of Certain Precious Metal Trusts and Funds – Another 30,000 Gold Ounces Redeemed

Sprott Physical Gold Trust saw about 30,000 ounces of gold bullion redeeming, with a commensurate elimination of unit shares in the exchange. That makes it about 66,680 ounces, or 2 tonnes, redeemed at these prices since December 1, 2014.

The withdrawal from Sprott Gold Trust is an indication of the mispricing of gold bullion and the tightness and leverage behind the scenes in the physical gold market.

The Sprott Physical Silver Trust’s cash levels have fallen below one million. There is going to be a secondary offering to bulk up those cash levels some time this year.

While the spike in gold and silver prices today were enjoyable for those who are bullish on the metals, these sharps rises and drops are symptomatic of the highly leveraged paper pricing that is called the Comex.

And one’s mind goes back to the last high, which was ruthlessly driven down by equally baseless, paper selling.

There is a Non-Farm Payrolls Report on Friday. Let’s see what happens with this.

***

end

A must read commentary from bill Holter who dots the i’s and puts everything into perspective

(courtesy Bill Holter/Miles Franklin)

They See It Coming …Ready or Not?

And now for the important paper stories for today:

Early Tuesday morning trading from Europe/Asia

1. Stocks mixed on major Asian bourses / the yen a tiny rise to 119.09

1b Chinese yuan vs USA dollar/ yuan strengthens to 6.2135

2 Nikkei down 526 points or 3.02%

3. Europe stocks in the green /Euro crashes/ USA dollar index up to 91.55/

3b WOW!!! Japan 10 year yield at .29% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.17/poor Japanese numbers on financial matters/

3c Nikkei now below 17,000

3e The USA/Yen rate well below the 120 barrier this morning/

3fOil: WTI 48.93 Brent: 51.87 /all eyes are focusing on oil prices. This should cause major defaults.

3g/ Gold up/yen up;

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt (see Von Greyerz)

3j Oil falls this morning for both WTI and Brent

3k China to stimulate its economy by 1 trillion dollars worth of infrastructure

3l Germany’s Merkel states that she is OK with a GREXIT/immediately the euro crashes./Disappointing European PMI numbers/Greek 3 yr bond yield over 13.5%

3m Gold at $1212. dollars/ Silver: $16.27

3n USA vs Russian rouble: ( Russian rouble down 2 roubles per dollar in value) 62.42!!!!!!

3 0 oil crashes into the 48 dollar handle for WTI and 51 handle for Brent

3p volatility high/commodity de-risking!/Europe heading into outright deflation including Germany

4. USA 10 yr treasury bond at 1.99% early this morning. Thirty year rate well below 3% (2.54%!!!!)/yield curve flattens/foreshadowing recession

5. Details: Ransquawk, Bloomberg/Deutsche bank Jim Reid

(courtesy zero hedge)/your early morning trading from Asia and Europe)

The Crunch Continues: WTI Tumbles Under $49, 10Y Dips Below 2%

Same slide, different day, as the crude crash continues, with both WTI and Brent tumbling to multi-year highs, below $49 and $52 respectively. This happened despite the news overnight that China is accelerating 300 infrastructure projects valued at 7 trillion yuan ($1.1 trillion) this year, suggesting that China will focus more on fiscal policy than monetary easing, which in turn led to much confusion in the SHCOMP, which fluctuated up and down for the day several times before finally closing unchanged. There was no confusion about the stops slamming USDJPY, and its Nikkei225 derivative which tumbled 3%, sending Japanese Treasury yields to fresh record lows. Record low yields were also seen in Germany, Austria, Belgium, Netherlands, Finland, France (and many other places), which in turn forced the US 10 Year to finally dip back under 2.00%. In fact, taken together, the average 10Y bond yield of the U.S., Japan and Germany has dropped below 1% for the first time ever, according to Citi.

The impetus for today’s panic bond buying was a report in Dutch Het Financieele Dagblad which says the ECB is considering three possible options for QE, all of which would naturally lead to lower yields, and further pricing in of well over 100% of any easing program the QE may launch (recall that Goldman and MS both said ECB’s QE had been fully priced in as long ago as October).

The Euro weakened again overnight, and is now flirting with the 1.19 level after another month of disappointing Eurozone PMI, as the final Composite PMI missed expectations. From Goldman: The December Euro area final composite PMI came in at 51.4, 0.3 pt below the Flash (and Consensus) estimate. Relative to November, the composite PMI rose by 0.3pt. The weaker Final composite PMI was driven partly by flash/final downward revisions to the French manufacturing PMI. The most notable country developments in December were that the Italian Composite PMI weakened substantially by 1.9 (the other ‘big 4’ countries, most notably France, all recorded gains in December).

But while the deflation story is well known, the bigger problem for the mainstream media is that even NBC is starting to hint that stocks are sliding for all the “wrong reason”, namely sliding oil. This crushes the narrative that lower oil is good for the economy, as it makes one wonder just why is the market dumping when it should be discounting a stronger US economy. As such everyone will again be following every tick of crude, and certainly Russia whose 5 year CDS jumped over 50 bps to about 610 bps. the widest since March 2009 as increasingly more are worried about Russia’s default risk.

Meanwhile, jittery global stocks, lacking any visibility on the multiple expansion front (because EPS are now guaranteed to decline with the energy rout assured to crush the EPS of at least 15% of the S&P), continue to trade as a derivative of either the USDJPY or the EURJPY carry pair: whichever one is higher and/or igniting upward momentum at any given moment.

Some more detail on the overnight action from RanSquawk:

WTI and Brent crude future prices continue to decline which in turn, has weighed once again on global equities with the DJIA and S&P 500 posting its worst losses in 3 months as well as the Nikkei (-3.02%) printing its largest decline in 10 months. As such, this has filtered through to European bourses coupled with the negative sentiment in Europe with energy being the worst performing sector. The dampened risk appetite in the market provided support to USTs as the US 10 yield broke back below 2% for the first time since October 2014, prompting the German 10yr yields to also fall back below 0.5%. Analysts at IFR have noted that the correlation between oil and US breakevens shows that much of a rally is about expectations of lower inflation with the EUR 5y5y forward swap rate now down to a new record low.

In Eurozone related news, reports suggested that the SYRIZA party are not looking to trigger an exit should they win the Greek snap-election after the sources say that the ECB plan to discuss the implications of a possible Grexit tomorrow in their non-monetary policy meeting, although the news has had little impact on the market.

In the FX market the USD-index (+0.15%) continues to trade near multiyear highs, however the greenback has been unable to lift USD/JPY to a sustained break of 119.00 as safe haven flows and sharp selling in JPY crosses persist from yesterday. Separately, UK Services PMI 55.8 vs Exp. 58.5 missed expectations causing GBP/USD to break 1.5200 alongside the relatively stronger USD. Oil related currencies continue to remain weak (CAD, NOK, RUB) amid the persistent pressure in crude prices as WTI has fallen below USD 49.00 this morning. Overnight, antipodean currencies outperformed amid better than expected Aus Nov. Trade Balance (-925mln vs. Exp. -1600mln (Prev. -1323mln, Rev. -877mln). AUD/USD consequently broke above 0.8100, dragging NZD/USD higher in sympathy to send the pair back above 0.7700.

In the energy complex, WTI and Brent crude futures continue to print fresh 5 and a half year lows as the USD remains near multi year highs. The move has seen WTI consolidate below USD 50.00 with Russian production reaching record highs adding to the oversupply in the market. In addition, early estimates for this week’s DoE oil inventories show an expectation for a build of 750K compared to a draw last week of 1.754mln. Meanwhile, precious metals, Gold (+0.90%) is a major beneficiary of the Greek political instability and slump in energy prices as safe haven flows into the have helped the metal trade firmly above the USD 1,200/oz level.

In summary:

European shares remain lower with the tech and oil & gas sectors underperforming and autos, chemicals outperforming. Euro-zone composite PMI below expectations, as was U.K. services PMI. China said to accelerate $1 trillion of projects to boost economic growth. WTI crude falls below $50 a barrel. Global bond yields fall to record low. The U.K. and Spanish markets are the worst-performing larger bourses, the Italian the best. The euro is weaker against the dollar. Japanese 10yr bond yields fall; German yields decline. Commodities decline, with Brent crude, WTI crude underperforming and wheat outperforming. U.S. ISM non-manufacturing, factory orders, RBC consumer outlook, Markit U.S. composite PMI, Markit U.S. services PMI due later.

Market Wrap

- S&P 500 futures up 0.1% to 2012.7

- Stoxx 600 down 0.6% to 331.9

- US 10Yr yield down 3bps to 2%

- German 10Yr yield down 3bps to 0.48%

- MSCI Asia Pacific down 1.8% to 134.9

- Gold spot up 0.6% to $1211.5/oz

- Asian stocks fall with the Shanghai Composite outperforming and the Sensex underperforming.

- MSCI Asia Pacific down 1.8% to 134.9

- Nikkei 225 down 3%, Hang Seng down 1%, Kospi down 1.7%, Shanghai Composite up 0%, ASX down 1.6%, Sensex down 3.1%

- Euro down 0.27% to $1.1901

- Dollar Index up 0.2% to 91.56

- Italian 10Yr yield down 3bps to 1.81%

- Spanish 10Yr yield down 3bps to 1.58%

- French 10Yr yield down 4bps to 0.77%

- S&P GSCI Index down 1.2% to 399.6

- Brent Futures down 2.6% to $51.7/bbl, WTI Futures down 2.5% to $48.8/bbl

- LME 3m Copper down 0.2% to $6131/MT

- LME 3m Nickel up 0.5% to $15269/MT

- Wheat futures up 1.1% to 595.5 USd/bu

Bulletin Headline Summary from Bloomberg and RanSquawk:

- The slide in energy prices continues to weigh on global sentiment as WTI trades through USD 49.00 to the downside

- Weakness in energy names allied to expectations of lower inflation has sent US 10yr yields back below 2% for the first time since October 2014

- Treasuries extend yesterday’s rally as global stocks decline, WTI crude extends its losses below $50/bbl; 10Y yield falls below 2.00% for first time since October.

- Taken together, the average 10Y bond yield of the U.S., Japan and Germany has dropped below 1% for the first time ever, according to Steven Englander, Citi global head of G-10 forex strategy

- China is accelerating 300 infrastructure projects valued at $1.1t this year as policy makers seek to shore up growth that’s in danger of slipping below 7%

- Markit’s euro-area composite PMI rose to 51.4 in Dec., less than expected, from 51.1; weakness will “add to calls for more aggressive central-bank stimulus,” according to Markit’s chief economist

- ECB is working on discussion paper on different ways to execute govt bond buying, Dutch newspaper Het Financieele Dagblad reports, citing people familiar with ECB discussions

- Growth at U.K. service companies slowed more than economists forecast in December, adding to signs the economy lost momentum at the end of 2014

- About 18,000 people marched through Dresden yesterday night in the latest weekly rally backed by organizers who call themselves Patriotic Europeans Against the Islamization of the West, or Pegida. The group says it’s for stricter immigration and asylum laws, protecting “western culture” and avoiding “parallel societies” of Muslims in Germany

- Two New York Police officers were shot while responding to a call about a robbery in the Bronx, leading to a manhunt for the suspects as the city’s officers remain on edge after a pair were gunned down last month

- Sovereign yields fall. Asian and European stocks slide, Nikkei -3%, FTSE -1.3%. U.S. equity-index futures decline. Brent crude, WTI fall; gold gains, copper little changed

- Looking ahead, heading into the US session highlights include US Factory

Orders and ISM Non-Manufacturing Composite both due at 1500GMT/0900CST

DB’s Jim Reid concludes the overnight event summary

It’s been a tough start to the year for risk assets as further steep declines in oil markets caused equity markets to take a sharp leg lower yesterday. A softer German inflation print and further falls in Greek assets, which we will touch on later, did little to help sentiment but taking a quick look firstly at market moves the S&P 500 closed 1.83% lower yesterday – its biggest one-day slump since October 9th and the first four-day drop since December 2013. With regards to oil both WTI (-5.03%) and Brent (-5.87%) tumbled to finish the day at $50.04/bbl and $53.11/bbl, respectively. Unsurprisingly, energy stocks (-3.99%) were the main underperformer, dragged down further by declines for large cap names including Exxon Mobil (-2.74%) and Chevron (-4.00%), although in reality all sectors finished the day in the red.

Just touching on the moves in oil, WTI briefly fell below $50/bbl intraday for the first time since April 2009 whilst the close in Brent below $55/bbl takes it to the lowest level since May 2009. Yesterday’s moves appear to be fueled by a report from the Russian Energy Ministry on the weekend showing production out of Russia rising to a post-Soviet era high and news that Iraq exported the highest amount of crude in December since the 1980s. As well as this, an article on Reuters noted that Saudi Arabia made significant discounts to its monthly oil prices for European buyers yesterday, offering the lowest discount since 2009. The article also noted that the region made its fifth consecutive monthly price cut to US refiners. We’ve previously highlighted the effects of the slump at the micro-level and yesterday we saw further evidence with Canadian producer Syncrude reporting a 12% decline in production in December relative to November. The latest data out of Baker Hughes also paints a fairly bleak picture, reporting that oil rigs were cut by 17 this week, the sixth weekly decline in seven and follows data which showed that the Q4 rig count dropped by the largest quarterly amount since Q1 2009. After taking something of a pause for breath over the holiday period, US HY energy names widened 25bps yesterday to a spread of 789bps – the widest level since mid-December.

Turning over to fixed income markets, the risk-off tone gave a firm bid to US Treasuries with the benchmark 10y yield closing 7.7bps tighter at 2.0337%. That level is now the lowest since May 2013 with the 10y yield now 27bps off the December highs. At the longer end of the curve 30y yields closed 8.9bps tighter to 2.5994, now the lowest since August 2012. The recent bull flattening has now compressed the spread difference between 2y and 30y yields to 194bps – the tightest level since January 2009. The US Dollar also benefited with the DXY finishing +0.33%, helped by further gains versus the Euro (more later). Meanwhile, credit markets ended the day weaker with CDX IG closing 2.8bps wider and CDX HY closing nearly three-quarters of a point lower. Elsewhere, it was a fairly light day data-wise with December total vehicle sales coming in a tad under consensus at 16.8m (vs. 16.9m expected). In terms of Fedspeak, the San Francisco Fed President Williams was reported in the WSJ saying that he sees no rush to raise interest rates, although reiterated a mid-2015 lift off would be a ‘reasonable guess’. Although Williams highlighted an improving US economy, he noted that he ‘sees no reason whatsoever to rush tightening’ and that ‘these financial stability concerns that people do raise are real things we want to take into account, but doesn’t argue for moving today or in next the next few months relative to, say, later in the year’.

Before we look at the remainder of market moves yesterday, refreshing our screens this morning bourses in Asia are following the US lead and trading lower as we type. The Nikkei (-2.74%), Hang Seng (-1.59%), Shanghai Comp (-0.34%) and Kospi (-1.85%) are all weaker whilst credit markets have tumbled with Asian IG 9bps wider as we go to print. WTI is largely unchanged. The falls come despite modestly robust data out of China and Japan. Services PMI’s in both China (53.4 vs. 50.0 previously) and Japan (51.7 vs. 50.6 previously) have climbed relative to November’s readings. Staying on China, Bloomberg reported this morning that Premier Li Keqiang’s government has approved for the acceleration of ¥7tn ($1.1tn) of infrastructure projects for 2015. The projects are part of the ¥10tn plan which due to run until 2016.

Coming back to yesterday, European equity markets didn’t fare much better with the Stoxx 600 (-2.15%) and DAX (-2.99%) both declining sharply. There were similar losses for energy stocks (-5.02%) whilst the Euro tumbled after a softer than expected German inflation print and further worries over Greece. Indeed, the single currency weakened a further 0.57% versus the Dollar yesterday to $1.1933, although touched an intraday low of $1.1864 which marked the lowest level for nine years. With regards to data, German headline inflation was significantly weaker relative to November (+0.2% yoy vs. +0.6% previously) and below consensus of +0.3%. Our European colleagues noted that the decline in energy prices was unsurprisingly a factor (-6.6% vs. -2.5% previously) although the substantial drop in food prices (-1.2% vs. 0.0% previously) was a surprise. Our colleagues also reported that annual inflation was +0.9% in 2014 (versus +1.5% in 2013) which marked the lowest rate of the last 15 years excluding 2009, although they expect that the core rate averaged +1.4% compared to +1.2% in 2013 highlighting the disinflationary effects of energy markets. Bunds closed weaker, the yield on the 10y benchmark bouncing off Friday’s record lows to close 2bps wider at 0.517%.

Wrapping up Europe, with the market weighing up the potential implications of a ‘Grexit’ there were further sharp moves in Greek assets yesterday with 3y yields widening 131bps to 13.5% and the ASE closing 5.63% lower – its lowest close since November 2012. With various conflicting reports out over the weekend comments from the German Social Democratic Party’s Poss yesterday saying that ‘Europe can’t afford a Greek exit’ were perhaps on the more supportive side. French President Hollande took a slightly different view however, saying that ‘The Greeks are free to choose their own destiny. But, having said that, there are certain engagements that have been made and all those must be of course respected’.

Looking at the day ahead, the calendar steps up a notch today with the final December composite and services PMI prints due for the Euro-area as well as regionally in Germany and France. We’ll also get the December consumer confidence reading in the latter as well as the preliminary services and composite PMI prints for the UK. Across the pond this afternoon, we also get the final PMI composite and services reading in the US, as well November factory orders and the ISM non-manufacturing print.

end

As I have stated to you in past commentaries, the speed from which these energy prices fall causes a massive derivative loss. The unwinding of the 9 trillion USA dollar trade, “carrying” the big oil asset ( oil derivatives at around 1.5 trillion USA dollars) has no doubt caused losses somewhere around 2 trillion uSA (dollar loss = 1.55 trillion/oil 0.75 trillion). Most of these derivatives were underwritten by our major 5 USA banks (JPMorgan, Citibank, Bank of America, Goldman Sachs, Morgan Stanley) along with Europe’s Deutsche bank. Altogether these guys have underwritten 95% of all derivatives. Also remember that the second carry trade: the USA/yen is also unwinding. This is the reason the dollar is rising as the entire global asset purchases are unwinding and these resulting trades causes the short dollar to be repurchased.

(courtesy zero hedge)

Crude Crash Crushes Credit Risk: WTI Hits $47 Handle, Energy Spreads Top 1000bps

As energy stocks continue to catch down to oil-price’s incessant weakness, US energy company credit risk has surged back above 1000bps for the first time in 3 weeks. WTI Crude oil prices just traded to a $47 handle – the lowest since April 2009.

Another day, another fresh low…

And energy stocks are catching down fast to oil’s weakness…

Fool me once (or twice or three times)…

Charts: Bloomberg

end

Dave Kranzler writes that the derivative mess will blow up and we now have Citibank at the largest holder of this powder keg. Now wonder they passed legislation that taxpayers will be on the hook for this crap:

(courtesy IRD/Dave Kranzler)

Is The Brown Stuff About To Hit The Fan?

Set aside for a moment the fact that the S&P 500 just closed down 4 days in a row – something which never happened in 2014. Zerhohedge had an interesting post today in which it wondered if Citibank was the next AIG (LINK) after it discovered that Citi is now the largest single holder of derivatives in the U.S., with $70.3 trillion innotional exposure holdings.

Not pointed out by Zerohedge was an interesting relationship between Citi and Goldman Sachs. Recall, that Goldman Sachs was AIG’s biggest counter-party. And the fact of the matter is that Goldman would have blown up along with AIG had the Government and the Fed – with close to a trillion dollars in taxpayer money – not bailed out AIG and the big banks. Let’s wipe the lipstick off that pig and call it what it was: An AIG/Goldman Sachs de facto collapse.

Recall that Henry Paulson was Treasury Secretary when Goldman de facto collapsed. Paulson was the former CEO of Goldman and had been appointed Treasury Secretary in July 2006. As it turns out, Goldman had been impaled on AIG’s nuclear mortgage -derived credit default swaps, to which GS was the main counter-party. I have always suspected that Paulson was inserted into the Treasury post because “they” knew that eventually the big banks – led by Goldman – were going to hit the derivatives wall and a Wall Street bank representative inside the Treasury would be needed to fix the problem.

Fast-forward to today. Who is the Treasury Secretary? Jack Lew. Jack Lew worked at Citibank up until late 2010, when he was moved into Government “service” as Director of the OMB. After that he was appointed Obama’s Chief of Staff. In 2013 Obama appointed him to be Treasury Secretary. Lew is clearly a political beast but I find it interesting that a former Citi employee is now Treasury Secretary at a time when Citi is now the largest derivatives owner in the U.S. and the 2nd largest in the world (Deutsche Bank is #1).

And, Zerohedge points out, Citibank was the primary force behind the recent legislation passed by Congress – legislation that was buried into the controversial budget Bill – which allows banks to move their derivatives into their FDIC insured subsidiary. This legislation, by the way, is a de facto bailout-in-advance for the Too Big To Fail Banks. Remember, Obama promised no more bank bailouts. Once again he lied.

At any rate, it may of course be just a mere coincidence that Paulson was appointed to Treasury Secretary about 2 years before Goldman blew up on derivatives and Lew was appointed Treasury Secretary, well, about 2 years before Citi might blow up on derivatives. I mean, why else would Citi aggressively push for FDIC coverage of its derivatives exposure if it were not worried about fomenting risks? By the way, Citi has now moved all of its derivatives into its FDIC-covered subsidiary and it’s the only bank to have done so.

Mere coincidence? Maybe. But when blood money is at stake, nothing happens by coincidence.

end

The low price of oil is certainly having a great effect on Canada as rig counts hit record lows for January. The oil price (heavy oil) in Canada falls below 35.00 dollars USA

(courtesy zero hedge)

Canada Heavy Oil Drops Below $35 As Rig Count Hits Record Low For January

Think Texas and Pennsylvania have a problem with plunging oil prices, don’t look North. West Canada Select (Heavy) crude oil prices have collapsed to below $35 per barrel (the lowest since Feb 2009). This is a 60% plunge in the last 6 months and has left the industry stunned.

While US rig counts have fallen for the last few weeks as the lagged response to falling prices finally catches up to reality, the Canadian oil rig count has never been lower for the first week of January.

Will the Canadian housing bubble be next?

Charts: Bloomberg

end

Shale related?

(courtesy zero hedge)

3.5 Magnitude Earthquake Shakes Dallas

Submitted by Tyler Durden on 01/06/2015 16:30 -0500

Just a few short hours after a series of deep, if not very strong, eartquakes shook north-central Oklahoma, moments ago the ground zero of the US energy industry, the city of Dallas, TX, felt the ground shaking. According to the USGS, this was due to a 3.5 magnitude quake, which stuck at a depth of some 3.2 miles below the Texas city.

From NBC DFW:

The United States Geological Survey reports a 3.5 magnitude earthquake struck in Irving near the former site of Texas Stadium Tuesday afternoon.

The newsroom at NBC 5 at CentrePort near Dallas-Fort Worth International Airport felt significant vibration at about 3:10 p.m. as desks and chairs shook inside the building. Our media partners at The Dallas Morning News in Downtown Dallas also reported feeling the tremblor.

The tremor was also reportedly felt in Oak Cliff, Arlington, Carrollton, Addison and elsewhere.

A number of quakes have been reported in the Irving-area since October.

A researcher from Southern Methodist University and his team are studying the source of several recent earthquakes in North Texas.

Was it shale related? The experts will opine, however if the answer is yes, Saudi Arabia, in all its humanitarian generosity, will make sure that the Lone Star state doesn’t host many more such tremors.

We wish the ECB all the luck in the world. They have just released 3 possible scenarios as to how they can QE:

1. buy all bonds pari pars u with member states shareholdering in the ECB

2. Buy only triple A bonds driving these rates to below zero and then have investors buy the junk

3. Let central banks buy bonds and then swap (exactly what they are doing right now)

in a nutshell/they are not ready yet. They fear a Grexit and of course Germany. The market reaction was not good as spreads widened!

(courtesy zero hedge)

The ECB “Leaks” Its 3 QE Choices

In its usual ‘leak the plans and judge market reactions’ methodology, unnamed sources have released to Dutch newspaper Het Financieele Dagblad, three potential options that the ECB is considering for buying government bonds. As the Jan 22nd ECB meeting looms, Reuters reports that while the ECB declined to comment, this ‘strawman’ appears very similar to comments made by ECB chief economists Peter Praet last week.

As fears grow that cheaper oil will tip the euro zone into deflation, speculation is rife that the ECB will unveil plans for mass purchases of euro zone government bonds with new money, a policy known as quantitative easing, as soon as this month.

According to the paper, one option officials are considering is to pump liquidity into the financial system by having the ECB itself buy government bonds in a quantity proportionate to the given member state’s shareholding in the central bank.

A second option is for the ECB to buy only triple-A rated government bonds, driving their yields down to zero or into negative territory. The hope is that this would push investors into buying riskier sovereign and corporate debt.

The third option is similar to the first, but national central banks would do the buying, meaning that the risk would “in principle” remain with the country in question, the paper said.

* * *

With German 5Y yields negative, and the entire curve at record lows, we can’t help but wonder just how much ‘bang’ for the European taxpayers’ buck any of these plans will have now that speculative capital has more than priced in Draghi’s decision.

For now, the reaction is not positive…

As this is definitely a problem as if Draghi announces plans in principal on Jan 22nd, the market will not be happy. It is clear the ECB is not close to a decision…

end

A huge story today. Greek bonds tumble as an independent research group, Oxford Economics state that the Syriza party can achieve a decisive victory in the big January elections. Syriza stands for two major platforms:

1. renegotiate the terms of the loans outstanding and of course demanding major haircuts on those loans.

2. if the ECB is to purchase bonds, they must also purchase Greek bonds.

It looks like a GREXIT is more promising today…

(courtesy zero hedge)

Greek Bonds Tumble As Report Sees “Decisive Victory” For Syriza

The Greek 3Y-10Y yield curve is back over 400bps inverted this morning as bond (and stock) prices re-tumble following a new reports. As The FT reports,forecasting group Oxford Economics says it has carried out an “in-depth” analysis of opinion polls ahead of Greece’s snap general election on January 25, which shows that the radical Syriza party is on course to win a “clear mandate” to push through anti-austerity policies. Will German worry now?

The Greek yield curve has moved even more inverted…

[Oxford Economics] analysis shows that Syriza’s support is sufficient to secure a workable majority in Greece.The report says:

36% of the final vote is the approximate threshold beyond which a strong anti-austerity government is plausible. Syriza’s performance has been consistent with this in each of the last 20 opinion polls, and over 40% of the vote on average in the last five.

The report, written by Oxford Economics’ Gabriel Sterne, points out that the ruling New Democracy party could close the gap, if a tactic pays off to portray the election as effectively a referendum on an exit from the euro.

But Mr Sterne adds:

But the binary (in or out) nature of the vote decision may also help Syriza to achieve a decisive victory by squeezing out smaller parties (eg. Independent Greeks), as voters herd to the big two.

And as Reuters adds, Syriza’s leader Tsipras has warned Draghi that is QE is undertaken, it must include buying Greek bonds…

Greek leftwing opposition leader Alexis Tsipras said the European Central Bank (ECB) could not exclude Greece if it decides to move to a full “quantitative easing” program to stimulate the euro zone’s faltering economy.

…

Tsipras said he hoped ECB President Mario Draghi would decide to go ahead with the program and said Greece could not be shut out, as some economists and politicians from countries including Germany have suggested.

“Quantitative easing by the ECB with direct purchases of government bonds must include Greece,” Tsipras said.

…

In a speech laced with barbs against German Chancellor Angela Merkel and finance minister Wolfgang Schaeuble, Tsipras said his party would roll back many of the austerity policies imposed by the bailout “troika”.

“Austerity is both irrational and destructive. To pay back debt, a bold restructuring is needed,” he said.

* * *

For now, bonds don’t seem to care. As bond prices slide to new lows..

Russian Default Risk Surges To New 6-Year Highs As Ruble Rubble Returns

Just when you thought it was all over… Having bounced post-CBR intervention and somewhat stabilized, the re-collapse in crude oil prices and continued weakness in Russian macro data provided just the impetus for a re-plunge in the Ruble (back above 63.5/USD) and surge in Russian bond yields (back to 14%). While Russian stocks are also retesting towards recent lows, it is Russian CDS that is the most telling as it closed to day at 595bps – the widest since March 2009. While these violent gyrations are new for recent history, they are not a new phenomenon, but are quite characteristic of the country’s financial history.

The Ruble and stocks are not quite back to recent lows…

But Russian credit risk has hit new highs…

However, as RT explains, this is nothing new for Russia…

The dramatic fall of the Russian ruble made headlines in December. The violent gyrations in the ruble are not a new phenomenon, but are quite characteristic of the country’s financial history.

On December 15 and 16, the ruble took a 22 percent dive, which prompted a run on the Russian national currency.

The ruble’s spectacular 22 percent plunge on December 15 and December 16 has prompted investors to liken the crisis to 1998, when the ruble lost 27 percent on August 17. Reaching a 16-year low, the ruble fell to 80 against the USD. By the time of publication, it had recovered to 62.7, compared to 32.9 at the beginning of 2014.

800 years of history

One of Europe’s oldest currencies, the ruble has been in use since the 13th century. First made of silver, the currency derives its namesake from the Russian word ‘rubit’ which means to chop or hack, and originally was made from fragmented pieces of the Ukrainian hryvnia.

The ruble has been chopped, hacked, collapsed, and re-denominated several times throughout its nearly 800-year history. The most volatile years came along with regime change and revolution.

After the 1917 Bolshevik revolution, the ruble lost one third of its value, and in the following years while the country was gripped by civil war, the ruble dropped from 31 against the dollar to nearly 1,400. The ruble hit its historic low of 2.4 million per USD after the civil war and the year the revolution’s leader Vladimir Lenin died. It was re-denominated to 2.22.

Throughout the Soviet Union, the ruble was little used outside state borders, so the government kept the official rate close to the dollar, a massive overvaluation.

In the last years of the Soviet Union, the economic crisis caused panic among the population who were ‘stuck’ with their increasingly worthless rubles. A black market naturally developed, and while the official rate for the ruble was 0.56 per dollar, a single greenback actually sold for 30-33 rubles on the street.

From Soviet to Shock Therapy

The ruble collapsed along with the Soviet state, and different currencies were set up in the 15 different republics. The Central Bank of Russia replaced the State Bank of the USSR (Gosbank) on January 1, 1992 and the Russian ruble replaced the Soviet ruble.

The new Russian Central Bank set the official exchange rate at the Moscow Interbank Currency Exchange (MICEX) at 125 rubles to the US dollar. By December 1992, the ruble had already lost about two third’s of its value.

Russia’s post-Soviet economy was dominated by ‘shock therapy’, and as President Boris Yeltsin’s reforms spurred rapid inflation, millions of Russians lost their savings.

Boris Yelstin’s political infighting with the Communists in 1993 caused the ruble to slide more, down to 1,247 per 1 USD. Yeltsin won the political coup, and a constitution was signed on December 12, 1993.

Shortly after the political victory, in January 1994, the authorities banned the use of the US dollar and other foreign currencies in circulation in an attempt to stymie the ruble’s decline.

Black Tuesday and Black Thursday

On October 11, 1994, an event known as ‘Black Tuesday’ hit the Russian financial market, and the ruble collapsed 27 percent in one day, which on top of a decline in GDP and massive inflation, catapulted Russia into an economic recession.

By the end of 1995, chronic inflation had reached 200 percent.

In 1996 the currency closed at 5,560 rubles per US dollar. 1997 was the first year of relative stability, but the ruble still fell to 5960 rubles per dollar. An era of stability prompted the government to devalue the currency and slash 3 decimal places, and on January 1, 1998, the ruble was set to 5.96 against the US dollar.

The bottom was ready to fall out of the economy. On August 17, 1998, Russia announced a technical default on its $40 billion in domestic debt and ceased to support the ruble on the same day. At the time, the bank only had $24 billion in reserves. The stock market and ruble both lost more than 70 percent, and nearly a third of the country’s population fell below the poverty line.

Along with the default came another mass devaluation of the ruble. In six months the value of the ruble fell from 6 to the dollar to 21 to the dollar.

“There was a desire to escape from the ruble from any direction,” Sergey Aleksashenko, deputy finance minister under Boris Yeltsin, has observed. Aleksashenko says today’s ruble crisis reminds him of 1998.

On May 27, 1998, the Central Bank increased the main lending rate to 150 percent, which brought loans to a near halt. By the end of 1998, inflation was 84 percent and the Russia GDP lost 4.9 percent.

Both currency crises in the 90s forced the governors of the Central Bank to resign.

The 1998 ruble crisis, like today, was driven by falling oil prices, which went as low as $18 in August 1998. However, today’s crisis is much less of a risk, as Russia has more than 10x the amount of currency reserves as it did in 1998.

The ruble met the new millennium with a rate of 28 to the dollar, and after hitting a low of 31 in 2003, started to slowly strengthen.

Recession: in, out, and in again?

In 2008, Russia along with the much of the rest of the world fell into recession, losing 7.8 percent of GDP in 2009. The Russian economy fared the crisis rather well, and the economy was back on track with 4.5 percent growth in 2010.

Russia is facing its biggest currency crisis since 1998. The ruble has mostly been tumbling in tandem with weak oil prices, which have nearly halved since June, when Brent crude went for $115 a barrel. In January, pricesplummeted below $50 a barrel. The ruble has lost more than half its value since the beginning of the year. Investors worry that the devaluation, along with falling oil and political tensions, will send Russia into recession this year.

The Central Bank forecast a 4.7 percent decline in GDP if oil prices stay at $60 per barrel.

On December 15 the ruble plunged 11 percent, and to counter the plummet, the Central Bank increased the key lending interest rate to 17 percent, in the middle of the night. The next morning after slight gains in the early morning hours, panic against ensued, and the ruble shot up 22 percent, the biggest single day loss since 1998.

Russians called it ‘Black Tuesday’ in reference to the 1998 currency devaluation when the ruble jumped from 6 to the US dollar to 21 in less than 24 hours.

During his annual end of the year press conference, Russian President Putin didn’t place blame on any particular government department, but said the Central Bank’s response had been appropriate, but possibly too late. So far, Putin continues to describe the Central Bank’s policy as “adequate.”

The government has already made many swift moves to salvage the ruble since mid-December. It hiked the key interest rate to 17 percent to control ruble flows, has lent money to the company’s biggest oil producer, Rosneft, and bailed out the country’s 29th largest lender, Trust Bank.

Russia’s biggest oil producers, including Gazprom and Rosneft, have been ordered to sell a fraction of their foreign exchange revenues over the next couple of months in order to support the ruble, adding an estimated $1 billion to the daily market.

Seven Reasons To Be Fearful

Bloomberg’s Rich Yamarone explains 7 reasons to be fearful today:

Please pay special attention to them:

(courtesy Yamarone/Bloomberg/ zero hedge)

Hope springs eternal that 2015 is the year that the US economy stretches its escape velocity growth as consensus growth expectations at 2.9% are still at their highest since 2005 (although world GDP expectations are falling rapidly). However, as Bloomberg’s Rich Yamarone explains, with 5 of the Top 10 economies in the world in or near recession, the wall of worry can be constructed as follows…

1) Strong Dollar

A strong dollar is in the best interests of the U.S. Until it isn’t. Dollar strength can carry some costs, particularly for investors. Corporate profits usually get crimped by a rising currency. Recently U.S. companies have started commenting on the dollar’s earnings impact. Lower profits traditionally mean diminished capital spending and hiring. Import prices fall and this may be an invitation to deflation, which is something the Fed wants to avoid at all costs. Further dollar appreciation can be viewed as a tax on exports, since they appear higher-priced compared to products fabricated overseas.

2) Emerging Markets

For the developing world, persistent dollar strengthening invites a great deal of instability. In the past, this has led to revaluations, pegging and de-coupling from the dollar. The Thai baht crisis in 1997 had long tentacles that hit Russia, causing a default on sovereign bonds, and a Fed-arranged rescue of the hedge fund Long Term Capital Management.

3) Cheap Oil

The dollar rally has also resulted in lower-priced commodities. This is welcomed by businesses in general, but hurts a good number of oil-producing companies and nations that depend on those revenues. Savings at the pump are positive for most households. Economic costs of cheap oil are more unevenly distributed. North American oil corporations’ capital expenditure plans are getting slashed for 2015 and job cuts are probably not too far away if the price slide is sustained. Regionally, low oil prices could prove costly to some outperformers among the United States in recent years, including Texas, North and South Dakota, Minnesota and Oklahoma. This alsocarries negative consequences for state and local tax revenues.

4) The Federal Reserve

The least likely risk is that the Fed adopts a severely restrictive policy stance that precipitates a recession. Historically, it’s always been the Fed that trips up the economy. That’s probably not the case with Fed Chair Janet Yellen at the helm. Her feelings are well-known about keeping the foot on the accommodation accelerator for as long as necessary. She also has total support of the Fed governors. Rates will rise when the data support a full employment and stable price environment. That appears close, if not already achieved. Yet the rate increase won’t happen if the situation regarding key world economies, the stronger dollar or oil unfolds in an unpleasant manner.

5) China

In the Chinese Zodiac, 2014 was the Year of the Horse, and the second largest economy in the world pulled up lame. Estimates by economists polled by Bloomberg expect 7.0 percent growth in 2015, and some respected forecasting outfits now anticipate growth as low as 5.6 percent for China in 2016. China’s current pace of aggregate demand is the same as during the global crisis and market meltdown in 2008. In order to combat that, the Chinese government implemented a four trillion yuan ($586 billion) stimulus plan, ultimately sending economic activity toward 12 percent growth. Today, Chinese policy makers have no such plans. Rumors are running through the market of a Chinese devaluation.Don’t look for China to be the hero. We’re entering the Year of the Goat.

6) Japan

When a country is stuck in a liquidity trap, monetary policy prescriptions of lower interest rates are ineffective. If it adopts a fiscally restrictive policy such as a consumption tax increase when things are just barely improving, it tends to send the economy into a tailspin. That’s exactly what occurred for Japan, as its economy slipped into its third recession since 2008 and entered its third lost decade. Japan cannot even benefit from the plunge in oil prices since the massive devaluation of the yen has negated much of the price decline in purchase terms.

7) Europe

Multinational companies complain about Europe, where too many economies are on very thin ice. A collapse in Greece or Russia could precipitate a global crisis. If Russia implodes, the likelihood of a severe European recession increases sharply. Essentially all companies in the Bloomberg Orange Book of CEO Comments that have dealings in Russia have already made mention of the drag on their performance because of the sanctions imposed internationally.

Source: Bloomberg Briefs

end

Your more important currency crosses early Tuesday morning:

Eur/USA 1.1909 down .0029

USA/JAPAN YEN 119.06 down .274

GBP/USA 1.5188 down .0069

USA/CAN 1.1767 up .0022

This morning in Europe, the euro continues its spiraled downward movement , trading now just above the 1.19 level at 1.1909 as Europe reacts to deflation, announcements of massive stimulation. In Japan Abe went all in with Abenomics with another round of QE purchasing 80 trillion yen from 70 trillion on Oct 31. He now wishes to give gift cards to poor people in order to spend. The yen continues to trade in yoyo fashion. This morning it settled up in Japan by 27 basis points and settling well below the 120 barrier to 119.06 yen to the dollar. The pound also spiraled massively southbound this morning as it now trades well below the 1.52 level at 1.5188.(very worried about the health of Barclays Bank and the FX/precious metals criminal investigation/Dec 12 a new separate criminal investigation on gold,silver oil manipulation). The Canadian dollar is well down today trading at 1.1767 to the dollar. It seems that the global dollar trade is being unwound. The total dollar global short is 9 trillion Usa, and as such we now witness a sea of red blood on the streets as derivatives blow up.We also have the second big yen carry trade unwind as the yen refuses to blow past the 120 level. These massive carry trades are causing deflation as the world reacts to a lack of demand.

Early Tuesday morning USA 10 year bond yield: 1.96% !!! down 7 in basis points from Monday night/

USA dollar index early Tuesday morning: 91.56 up 19 cents from Monday’s close

The NIKKEI: Tuesday morning : down 526 points or 3.02%

Trading from Europe and Asia:

1. Europe stocks mostly in the green.

2/ Asian bourses mostly in the red … Chinese bourses: Hang Sang in the red ,Shanghai in the green, Australia in the red: /Nikkei (Japan) red/India’s Sensex in the red/

Gold early morning trading: $1212

silver:$16.29

Closing Portuguese 10 year bond yield: 2.58% up 5 in basis points from Monday

Closing Japanese 10 year bond yield: .29% !!! down 4 in basis points from Monday

Your closing Spanish 10 year government bond, Tuesday up 4 in basis points in yield from Monday night.

Spanish 10 year bond yield: 1.64% !!!!!!

Your Tuesday closing Italian 10 year bond yield: 1.86% up 2 in basis points from Monday:

trading 22 basis points higher than Spain:

IMPORTANT CLOSES FOR TODAY

Closing currency crosses for Tuesday night/USA dollar index/USA 10 yr bond:

Euro/USA: 1.1898 down .0040

USA/Japan: 118.62 down .800

Great Britain/USA: 1.5150 down .0106

USA/Canada: 1.1826 up .0069

The euro fell again in value during the afternoon after being battered overnight. It was down by closing time , finishing just below the 1.19 level to 1.1898. The yen was up in the afternoon, and it was well up by closing to the tune of 80 basis points and closing well below the 120 cross at 118.62 causing much grief again to our yen carry traders. The British pound lost huge ground during the afternoon session and it was down badly on the day closing at 1.5150. The Canadian dollar was down in the afternoon and was down on the day at 1.1826 to the dollar.

As explained above, the short dollar carry trade is being unwound and this is causing massive derivative losses. This is being coupled with those unwinding their yen carry trades. As such massive derivative losses have occurred, blowing up this powder keg!!

Your closing USA dollar index: 91.38 up 30 cents from Monday.

your 10 year USA bond yield , down 8 in basis points on the day: 2.o4%!!!!

European and Dow Jones stock index closes:

England FTSE down 50.65 points or 0.79%

Paris CAC down 27.86 or 0.68%

German Dax down 3.5 or 0.04%

Spain’s Ibex down 122.20 or 1.22%

Italian FTSE-MIB down 45.18 or 0.25%

The Dow: down 130.01 or 0.74%

Nasdaq; down 59.84 or 1.29%

OIL: WTI 47.81 !!!!!!!

Brent: 50.87!!!!

Closing USA/Russian rouble cross: 62.73 down 2 roubles per dollar during the day.

end

And now for your more important USA economic stories for today:

Your trading today from the New York:

How many are feeling after the worst 3-day start to a year EVER…

Market internals triggered a 2nd Hindenburg Omen…

The S&P 500 is down 5 days in a row – the first time since Sept 2013… with the biggest 5-day decline since Jim Bullard saved the world…(finding support at its 100DMA for now)

And broad equity indices bounced intraday off that 100DMA support (in Dow and S&P) – with JPY ramping stocks back to VWAP…

From the Russell 2000’s peak, stocks are still down notably…

But today had a similar feel to yesterday with some afternoon dip-buyers vanquished… (but the S&P 500 just held 2,000)

As Energy stocks tumbled back towards oil’s weakness…

as Energy credit risk topped 1000bps again and broad spreads widened…

As WTI traded with a $47 handle!! After Saudi “demand” comments…

The biggest news of the day – apart from the worst start to the year in stocks ever… and oil trading with a $47 handle!! – was the total collapse in bond yields…

The USD rose modestly in the day (rallying during the US afternoon unlike yesterday)…

but overall JPYwas still in charge of stocks…

Once again – despite USD gains, Gold and silver rose with the yellow metal testing $1220… (and silver surging)

Charts: Bloomberg

Bonus Chart: For The White House onlookers – NOT Europe…

end

I guess we can rule out a 5% GDP for the 4th quarter.December jubs significantly below 200,000 warns Markit:

(courtesy Markit/zero hedge)

December Jobs “Significantly Below 200,000”, Q4 GDP Tumbles To 2%, Markit Warns

Markit’s US Services PMI missed expectations of 53.7, priting at 53.3, its lowest since Feb 2014 (mid Polar Vortex). From record highs in June, PMI has plunged non-stop for six months leaving Markit noting Q4 growth is looking more like 2.0% than the 5.0% exuberance in Q3.

US Services PMI plunges…

and along with the tumble in manufacturing leaves the US Composite PMI at 14 month lows…

It gets worse. From the report, via Chris Williamson, Chief Economist at Markit said:

“The US economy lost significant growth momentum at the close of the year. Excluding the drop in activity caused by the October 2013 government shutdown, the manufacturing and service sector PMIs collectively signalled the weakest expansion since the end of 2012. This is also not just a one-month wobble: the pace of growth has now slowed for six consecutive months.

“The PMI surveys act as good leading indicators of GDP data, and suggest that the pace of US economic growth will have slowed in the fourth quarter. According to the PMIs, fourth quarter growth is looking more like 2.0% rather than the 5.0% annualised rate of expansion enjoyed in the third quarter.

“Job creation has waned alongside the slowdown, with the survey indicating that monthly payroll growth has slipped significantly below the 200,000 mark. Companies have become increasingly reluctant to take on staff due to the cloudier economic outlook, in turn linked to various factors ranging from global geopolitical concerns, worries about higher interest rates and uncertainty about rising staff healthcare costs.

“However, it’s important to note that growth is merely slowing from an unusually powerful rate rather than stalling. Lower oil and fuel prices should also help foster stronger economic growth as we move into 2015, by reducing the fuel bills of households and companies. Measured across both sectors, input costs showed the smallest rise since April 2013 in December. Lower prices will also of course provide added leeway for interest rates to remain on hold for longer.”

end

And here is the lousy service PMI USA numbers mentioned above as it tumbles to its lowest levels since 2013/ the price component crashes to 2009 level:

(courtesy Service PMI/zero hedge)

Service ISM Tumbles To Lowest Since June, Biggest Miss Since 2013, Prices Crash To 2009 Level

Submitted by Tyler Durden on 01/06/2015 10:18 -0500

Following a disastrous Manufacturing ISM report last week, today it was the turn for its Service cousin to report. And while it wasn’t quite the abysmal faceplant that some had expected the seasonally adjusted number to be, printing at 56.2, down from 59.3 and far below the 58.0 expected (but just above the lowest estimate of 56.0), it still was the biggest miss to expectations since September 2013, and the lowest print since June.

And while the details were just as atrocious, with every single ISM component declining in December – something that has not happened since the Great Financial Crisis – a report which literallyh said “Obamacare and wages are still the biggest enemies to profitability“, all eyes are focused not so much on the tumble in Business Activity and New Orders, but on Prices, which at 49.5, posted their first contraction since September 2009.

For those asking, here is how New Orders looked like Seasonally adusted and unadjusted:

Finally, and always amusing, were the ISM’s goalseeked, and “seasonally-adjusted” responses. These, too, were not compiled using Nielsen:

- “Delays at West Coast ports are requiring re-routing to east coast facilities.” (Management of Companies & Support Services)

- “Still struggling with supply of solutions for patient care.” (Health Care & Social Assistance)

- “Low oil prices are easing tensions on wholesale prices. Energy exports should be able to boost the economy upward. Obamacare and wages are still the biggest enemies to profitability.” (Accommodation & Food Services)

- “Outlook for 1Q 2015 is strong. Up from a relatively strong 4th quarter 2014.” (Professional, Scientific & Technical Services)

- “Reduced fuel prices will improve the cash position of the company.” (Transportation & Warehousing)

- “We are finishing the year strong.” (Wholesale Trade)

- “Another terrific month in the auto industry. Sales are near historic highs.” (Retail Trade)

Yup: everything is so great that the other, non-goalseeked and seasonally adjusted Service ISM report just warned that December payrolls will be well below 200,000 and Q4 GDP will tumble by more than half to 2.0%. Golfclap, dear ministry of BS and “truth.”

end

USA factory orders drop the most in almost 2 years:

(courtesy zero hedge)

US Factory Orders Drop Most YoY In 19 Months