Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1264.70 up $30.30 (comex closing time)

Silver: $17.07 up 11 cents (comex closing time)

In the access market 5:15 pm

Gold $1262.50

silver $16.93

Last night, I thought that the boys were going to keep gold and silver under wraps. During the early evening, it sure looked that way with gold trading around 1227 when the Swiss announced the unpegging of its currency to the USA dollar. Immediately gold shot up into the 1265 dollar level with silver trailing noticeably behind. Actually if you want to get a glimpse as to what gold will do just notice what happened to the Swiss Franc which rose 30% today, from 1.20 to the dollar to, at one point, .75 francs to the dollar and settled at .86 to the dollar( and the Euro/Swiss Franc at parity at 1.00.) Even as the world perceives the Swiss Franc as a safe haven you can just imagine what gold would do and rise even greater than 30% in one day as our ancient metal of kings is the ultimate safe haven ( and ultimate money)

The second big story of the day was the Russians stopping the shipment of gas through the Ukraine to six European countries stating that gas was being recycled back.

The Russians are now flexing their muscles knowing full well that China is behind them.

We will spend a lot of time on both of these big stories.

Gold/silver trading: see kitco charts on right side of the commentary.

The gold comex today had a poor delivery day, registering 0 notices served for nil oz. Silver comex registered 0 notices for nil oz.

Three months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 247.23 tonnes for a loss of 56 tonnes over that period.

In silver, the open interest fell by 346 contracts with yesterday’s silver price being down by 17 cents. The total silver OI continues to remains relatively high with today’s reading at 156,936 contracts. However the bankers are still loathe to supply much of the non backed silver paper. The January silver OI contract fell by 126 contracts down to 126.

In gold we had a small increase in OI with the small rise in price of gold yesterday to the tune of $.10. The total comex gold OI rests tonight at 403,082 for a gain of 974 contracts. The January gold contract remains constant at 87 contracts.

Today, we had no change in gold inventory at the GLD/ /Inventory 707.59 tonnes

In silver, we had a huge reduction in silver inventory at the SLV of 1.628 million oz

SLV’s inventory rests tonight at 326.351 million oz

.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today

.

First: GOFO rates:

Most rates moved mostly in the negative direction/ All months are in contango and thus positive in rates.

Sometime in January the LBMA will officially stop providing the GOFO rates.

Jan 15 2015

+.105% +1075% +.1075% +.1175 .1475%

Jan 14 2014:

+.1075% +.1025% +.1075 % +.12% +.15%

end

Let us now head over to the comex and assess trading over there today.

Here are today’s comex results:

The total gold comex open interest rose today by 974 contracts from 402,108 all the way up to 403,082 with gold up by $0.10 yesterday (at the comex close). We are now onto the January contract month. The non active January contract month saw it’s OI contracts remain constant at 87 for a loss of 0 contracts. We had 0 contracts served yesterday. Thus we neither lost nor gained any gold contracts standing for delivery in this January contract month. The next big delivery month is February and here the OI fell by 5,549 contracts to 178,496 contracts with many moving to April. The estimated volume today was fair at 171,454. The confirmed volume yesterday was good at 229,831 contracts, even though the high frequency traders gave some help with respect to volume. Today we had 0 notices filed for nil oz .

And now for the wild silver comex results. Silver OI fell by 346 contracts from 157,282 down to 156,936 with silver down by 17 cents yesterday. The front January contract month saw its OI fall to 126 contracts for a loss of 126 contracts. We had 130 notices filed yesterday, so we gained 4 silver contracts or an additional 20,000 oz will stand for silver in the January contract month. As I mentioned yesterday, somebody was in great need of physical silver and they robbed the cookie jar if very valuable silver. The next big contract month is March and here the OI fell by 1321 contracts down to 102,894. The estimated volume today was fair at 30,771. The confirmed volume yesterday was excellent at 53,543. We had 0 notices filed for nil oz today. The rise in silver is certainly scaring our bankers into supplying more non backed paper. The OI in silver has seen a slow and steady rise for the past few weeks.

January initial standings

Jan 15.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | nil |

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 contracts(nil oz) |

| No of oz to be served (notices) | 87 contracts (8700 oz) |

| Total monthly oz gold served (contracts) so far this month | 8 contracts(800 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

2507.7 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

we had 0 dealer deposit:

total dealer deposit: nil oz

we had 0 customer withdrawal

total customer withdrawal: nil oz

we had 0 customer deposits:

total customer deposits; nil oz

We had 0 adjustments

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the December contract month, we take the total number of notices filed for the month (8) x 100 oz or 800 oz to which we add the difference between the January OI (87) minus the number of notices served upon today (0) x 100 oz = 9500 oz , the amount of gold oz standing for the January contract month. (.2954 tonnes of gold)

Thus the initial standings:

8 (notices filed for the month x 100 oz) +OI for January (87) – 0(no. of notices served upon today) 9500 oz (.2954 tonnes).

We neither lost nor gained any gold ounces standing for delivery today.

Total dealer inventory: 770,487.09 oz or 23.96 tonnes

Total gold inventory (dealer and customer) = 7.948 million oz. (247.23) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 56 tonnes have been net transferred out. We will be watching this closely!

This initializes the month of January for gold.

end

And now for silver

Jan 15 2015:

January silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | 512,555.21 oz (CNT,SCOTIA,) oz |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 498,115.800 oz (Scotia) |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 122 contracts (610,,000 oz) |

| Total monthly oz silver served (contracts) | 234 contracts (1,170,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,124,500.1 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 1 customer deposit:

i) Into Scotia: 498,115.800 oz (one decimal)

total customer deposit 498,115.800 oz

We had 2 customer withdrawals:

i) Out of CNT: 387,154.56 oz

ii) Out of Scotia: 125,400.65 oz

total customer withdrawal: 512,555.21 oz

we had 0 adjustments

Total dealer inventory: 65.694 million oz

Total of all silver inventory (dealer and customer) 173.914 million oz.

The total number of notices filed today is represented by 0 contracts for nil oz. To calculate the number of silver ounces that will stand for delivery in December, we take the total number of notices filed for the month (234) x 5,000 oz to which we add the difference between the OI for the front month of January (126) – the Number of notices served upon today (0) x 5,000 oz = 1,780,000 oz the number of ounces standing so far for the January delivery month.

Initial standings for silver for the January contract month:

234 contracts x 5000 oz= 1,170,000 oz +OI standing so far in January (126)- no. of notices served upon today(0) x 5,000 oz = 1,800,000 oz

we gained 4 contracts or an additional 20,000 oz will stand for the January contract month.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.com or http://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

Jan 15/ no change in inventory at the GLD today/inventory 707.59 tonnes

Jan 14.2015 we had a small withdrawal of .23 tonnes of gold from the GLD/inventory 707.59 tonnes

Jan 13.2015 no change in gold inventory/GLD inventory tonight at 707.82 tonnes

Jan 12 no change in gold inventory/GLD inventory tonight at 707.82 tonnes

January 9.2015: an addition of 2.99 tonnes of gold/Inventory 707.82 tonnes

Jan 8.2015: no change/inventory 704.83 tonnes

Jan 7.2015: we lost another exact 2.99 tonnes of gold inventory at the GLD/Inventory at 704.83 tonnes

Jan 6.2015: we lost 2.99 tonnes of gold inventory at the GLD//inventory 707.82 tonnes

Today, Jan 15/2015 /no change in gold inventory at the GLD ) /Inventory rests tonight at 707.59 tonnes

inventory: 707.59 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 707.59 tonnes.

end

And now for silver (SLV):

Jan 15.2015 we had a huge withdrawal of 1.628 million oz/Inventory 327.351 million oz

Jan 15.2015: no change in silver inventory/327.979 million oz

Jan 13.2015 no change in silver inventory/327.979 million oz/

Jan 12.2015 we had a huge withdrawal of 1.915 million at the SLV/inventory at 327.979 million oz.

Jan 9.2015: we had a huge addition of 1.437 million oz at the SLV/Inventory 329.894 million oz

Jan 8.2015: no change in silver inventory/inventory at 328.457 million oz.

Jan 7.2015: we had another loss of 958,000 oz of silver from the SLV/Inventory 328.457 million oz

jAN 6.2015: we had a small loss of 149,000 oz/inventory 329.415 million oz

Jan 15/2015 / a huge withdrawal of 1.628 million oz of silver from the SLV/ inventory at the SLV

registers: 326.351 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now for the first time into the negative to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 9.5% percent to NAV in usa funds and Negative 9.2 % to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.5%

Percentage of fund in silver:38.0%

cash .5%

( Jan 15/2015)

2. Sprott silver fund (PSLV): Premium to NAV falls to + 1.35%!!!!! NAV (Jan 15/2015)

3. Sprott gold fund (PHYS): premium to NAV falls to negative -0.60% to NAV(Jan 15/2015)

Note: Sprott silver trust back into positive territory at +1.35%.

Sprott physical gold trust is back in negative territory at -0.60%

Central fund of Canada’s is still in jail.

end

And now for your most important physical stories on gold and silver today:

Early gold trading from Europe early Thursday morning:

(courtesy Mark O’Byrne)

Market Chaos as Swiss Franc Surges 30% In 13 Minutes, Gold Rises Sharply

Chaos was seen in financial markets today as participants were thrown a curveball when Switzerland surprised the world by removing its three-year cap on the Swiss franc, unpegging it from the euro. This sent the undervalued currency soaring and Europe’s shares and bond yields tumbling.

In just 13 minutes, from 0930 to 0952 BST, the franc collapsed by 30%. Swiss shares fell more than 12% – their largest crash since 1987. Stock markets around Europe fell with investors buying “safe haven” assets such as German bunds and gold bullion.

Gold rose in all major currencies and approached a three-month high following Switzerland’s unexpected decision to decouple its currency from the euro.

In a chaotic few minutes on markets after the SNB’s announcement, the Swiss franc jumped to a record high against the euro, rocketed nearly 30 percent in a few minutes. The franc broke past parity against the euro to trade at 0.8052 francs per euro before trimming those gains to stand at 88.00 francs – it removed the 1.20 per euro cap it has had in place since late 2011. It also gained 25 percent against the dollar to trade at 74 francs per dollar.

The SNB ended a three-year-old policy designed to shield the economy from the euro area’s sovereign debt crisis, prevent the Swiss franc appreciating and pricing Swiss exports out of markets. The central bank lowered the interest rate on sight deposit account balances that exceed a given exemption threshold to minus 0.75 percent from minus 0.25 percent, it said in a statement today.

This is likely a coordinated move by the SNB in conjunction with the ECB in anticipation of a move against the flood of money that will likely materialise with the ECB in Frankfurt looking likely to start quantitative easing.

Gold climbed on the news and bullion for immediate delivery increased 2.3 percent to $1,257.01 near a 12 week high, as the dollar weakened. Gold is higher for a fifth day, the longest streak since June.

The move by the SNB is a dramatic one and smells of an emergency measure. Ultra loose monetary policies are here to stay and the SNB actions suggest loose money policies will intensify in the coming months.

The revaluation of the Swiss franc versus the dollar, pound and euro is a harbinger of what will happen to those same fiat currencies versus gold in the coming months and years. The Swiss franc is one of the safest fiat currencies in the world but gold remains the ultimate safe haven asset and form of money as has been seen throughout history and in recent years.

REVIEW of 2014 – Gold Second Best Currency, +13% in EUR, +6% GBP

OUTLOOK 2015 – Uncertainty, Volatility, Possible Reset – DIVERSIFY

Today’s AM fix was USD 1,235.25, EUR 1,055.41 and GBP 811.76 per ounce.

Yesterday’s AM fix was USD 1,228.75, EUR 1,044.99 and GBP 808.76 per ounce.

Spot gold in Singapore was flat and yesterday spot gold fell $2.40 or 0.2% to $1,228.00 per ounce yesterday and silver slipped $0.18 or 1.06% to $16.83 per ounce.

GET BREAKING NEWS and UPDATES HERE

end

My goodness: a huge 61 tonnes of gold demanded by Chinese citizens.

Also please remember that this is not sovereign China, who purchases gold separately from the Shanghai Gold Exchange with their unwanted USA dollars. The SGE purchases gold/scrap etc with yuan.

(courtesy Koos Jansen)

Posted on 15 Jan 2015 by Koos Jansen

Chinese Lunar Year Gold Buying At Full Steam: 61t Withdrawn From SGE Vaults In 1 Week

As I mentioned last week, January is the time of the year for the Chinese to buy golden gifts for their love ones. And that is exactly what they are currently doing en masse, according to the latest data from the Shanghai Gold Exchange (SGE).

An astonishing 61 tonnes have been withdrawn from the vaults in SGE trading week 1 (January 5 -9), the strongest week since early October 2014. SGEI volume was very little at 3.5 tonnes; meaning withdrawals from vaults in the mainland must have been at least 58 tonnes. (Read this post for a comprehensive explanation of the relationship between SGEI trading volume and withdrawals.)

As most of Chinese gold demand needs to be sourced from abroad (import), this is draining global gold inventory. One of the largest suppliers to this market is the UK, home of the London Bullion Market. It remains to be seen how long the UK can export to China – the question is will all gold from London be shipped to the Orient, or will it stop before they’re empty. From the LBMA website, January 2015:

There are seven custodians offering vaulting services in the London bullion market, three of whom are also clearing members of the LBMA (Barclays, HSBC and JP Morgan). There are also four other security carriers, who are also LBMA members (Brinks, G4S Cash Solutions (UK), Malca Amit and ViaMat). The Bank of England also offers a custodian service (gold only). In total it is estimated that there are approximately 7,500 tonnes of gold held in London vaults, of which about three quarters is stored in the Bank of England.

In July 2014, the LBMA mentioned:

In total there is approximately 9,000 tonnes of gold held in London vaults, of which about two thirds is stored in the Bank of England.

This is not an exact scientific way of measuring changes in London’s gold stock over a given period, but it is significant. According the Eurostat the UK has net exported 1,871 tonnes from January 1, 2013, until November 31, 2014. Let’s see how this will play out this year.

(h/t @ronanmanly for LBMA data)

Koos Jansen

end

Quite a story: many of gold companies are witnessing the complete collapse of their retained earnings

(courtesy Koven /National Post/Toronto/GATA)

Gold sector’s bad bets wiping out lifetime earnings — and investor confidence

By Peter Koven

National Post, Toronto

Wednesday, January 14, 2015

TORONTO — Goldcorp Inc. could soon join an inglorious group: large gold miners that have a net loss to show for their entire history as corporate entities.

The Vancouver-based company warned this week that it expects to record an impairment charge of US$2.3 billion to US$2.7 billion on its Cerro Negro mine in Argentina. Given that Goldcorp’s retained earnings were US$2.2 billion as of Sept. 30, they may be completely wiped out in the company’s next quarterly report.

That would not be unusual in the gold industry, where writedowns have destroyed historic profits in recent years. Barrick Gold Corp. has retained earnings of negative US$7.8 billion, while Kinross Gold Corp. is at minus US$8.5 billion. AngloGold Ashanti Ltd. has a US$4 billion historic loss, while Agnico Eagle Mines Ltd. has a slimmer loss of US$740 million.

These companies have highly profitable operations that continue to perform well in a tough gold market. But they paid the price for taking risky bets that backfired and crushed shareholder value when gold prices dropped. …

… For the remainder of the report:

http://business.financialpost.com/2015/01/14/inglorious-writedowns-gold-…

end

We are now witnessing novel ways to finance new gold mines

(courtesy Antonioli/Denina/Reuters/GATA)

Banks’ withdrawal opens doors for niche financiers in gold sector

By Silvia Antonioli and Clara Denina

Reuters

Wednesday, January 14, 2015

LONDON — Struggling gold miners are turning increasingly to alternative sources of finance for funds as banks and equity investors shy away.

Stream financing and royalty deals and investments by private individuals are throwing a lifeline to some bullion miners but critics say it comes at the expense of future returns, damaging the industry’s longer-term appeal for more conventional investors.

They may also be keeping alive production that would not be viable at current spot prices, delaying a rebalancing of supply and demand. Gold shed around a quarter of its value in the last two years after a more than decade-long bull run.

“We have never been busier,” said David Harquail, chief executive of royalty and streaming company Franco-Nevada. “Our office is now full and we spend all our time trying to juggle which projects we can devote resources too.” …

… For the remainder of the report:

http://www.reuters.com/article/2015/01/14/gold-mining-financing-idUSL6N0…

end

Bill Kaye on the cutting off of Russian gas and on gold

(courtesy Bill Kaye/kingworldnews/GATA)

Kaye notes Russian gas cutoff, sees sovereign bids for gold at $1,205

11:55p ET Wednesday, January 14, 2015

Dear Friend of GATA and Gold:

In an interview today with King World News, Hong Kong fund manager William Kaye notes that Russia has begun terminating natural gas delivery to Europe, which likely will raise geopolitical tensions. Kaye pegs the government bids in the gold market at about the $1,205 level. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/west-troubled-latest-russian-move-sovereigns-bi…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

A dandy commentary from Bill Holter

a must read….

(courtesy Bill Holter/Miles Franklin)

Oil, Copper and Credit

There are two separate subjects to talk about today, one is oil and the other copper. Oil has been cut by more than half in just six months. As I speculated last week, I believe someone, somewhere “is already dead”. For all intents and purposes, the shale businesses across the globe have been rendered upside down. Along with the business models of course is all of the debt taken on to create the businesses. The debt is estimated in North America alone to be greater than $500 billion and has provided much of what little growth GDP has recorded the past few years.

And now for the important paper stories for today:

Early Thursday morning trading from Europe/Asia

1. Stocks up on major Asian bourses / the yen rises to 116.53

1b Chinese yuan vs USA dollar/ yuan strengthens to 6.1955

2 Nikkei up 313 points or 1.86%

3. Europe stocks all in the green /Euro collapses/ SWISS FRANC EXPLODES HIGHER as they remove the peg/ USA dollar index down to 91.71/

3b WOW!!! Japan 10 year yield at .25% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 116.53/

3c Nikkei now slightly above 17,000

3e The USA/Yen rate well below the 120 barrier this morning/

3fOil: WTI 45.69 Brent: 46.54 /all eyes are focusing on oil prices. This should cause major defaults.

3g/ Gold way up/yen up;

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt (see Von Greyerz)

3j Oil rises this morning for both WTI and Brent

3k China to stimulate its economy by 1 trillion dollars worth of infrastructure/poor Chinese PPI numbers as their economy softens.

3l

3m Gold at $1252. dollars/ Silver: $17.10

3n USA vs Russian rouble: ( Russian rouble up 1 4/5 roubles per dollar in value) 64.21!!!!!!

3 0 oil rises into the 49 dollar handle for WTI and 49 handle for Brent

3p volatility high/commodity de-risking!/Europe heading into outright deflation including Germany/Germany has low unemployment/Italy very high unemployment (high jobless rate)/Germany bad factory order numbers/

3Q ECB still unsure of QE format weighs down European bourses/OMT opinion gives green light to outright QE on conditions/sends the Euro southbound

4. USA 10 yr treasury bond at 1.82% early this morning. Thirty year rate well below 3% (2.44%!!!!)/yield curve flattens/foreshadowing recession

5. Details: Ransquawk, Bloomberg/Deutsche bank Jim Reid

(courtesy zero hedge)/your early morning trading from Asia and Europe)

Market Wrap: “It’s Turmoil” – Overnight Gains Wiped Out, Futures Trade Below 2000 On SNB “Shock And Awe”

To paraphrase a trader who walked into the biggest FX clusterfuck in years, “it’s total, unprecedented market turmoil.” So while the world gets a grip on what today’s historic move by the SNB means, which judging by the record 13% collapse in the Swiss Stock Market shows clearly that the SNB market put is dead and the SNB may be the first central-banking hedge fund which just folded (we can’t wait to see what the SNB P&L losses on its EURCHF holdings will be), here is what has happened so far for anyone unlucky enough to be walking into the carnage some 2 hours late.

Session highlights courtesy of RanSquawk

- SNB surprise the market by calling an end to their minimum exchange rate and lower their interest rate to -0.75%

- Initial reaction EUR/CHF briefly fell ~35 points (30%) while USD/CHF dropped its most since 1971. In sympathy EUR/USD printed an 11yr low at 1.1580 and the SMI remains down ~9% for the session

- Looking forward SNB’s Jordan is due to hold a press conference to explain today’s decision at 1215GMT/0615CST. Major data from the States come in the form of Empire manufacturing, PPI, Philly Fed, EIA nat gas storage change as well as earnings from the likes of Citigroup, Bank of America and Intel.

**SNB DROPS CHF FLOOR AND CUT RATES**

The trading day was off to a quiet start ahead of US data and earnings later today when the SNB decided to drop the bombshell. In a surprise and unscheduled announcement the SNB called an end to their minimum exchange rate and lowered their interest rate to -0.75%, concluding that the CHF cap was no longer justified. In an initial reaction EUR/CHF dropped like a stone with USD/CHF marking its biggest fall since 1971, while EUR/USD printed an 11yr low at 1.1580. From a stock perspective the SMI fell 8% as the strength in the local currency is likely to impact negatively corporate profits as well as the Swiss economy itself which has already been battling a currency that was too strong even when the floor was in place. The move has also resulted in weakness in the HUF and PLN as both have relatively large loan exposure to Switzerland. Once the dust settled European stock futures bounced off the lows as EUR/CHF pared approximately half of the initial 30% move lower in the cross now trading around 1.05. This also came amid unconfirmed market talk that the SNB were back into the market helping prop up the currency from its lowest level.

Looking ahead we will see how the US interpret the news especially given the timing as we head closer towards the scheduled ECB rate decision due on the 22nd of January where it is broadly expected that the ECB will announce QE. Snap analysis from some banks suggests that the SNB may well have taken pre-emptive action ahead of anticipated ECB action by scrapping the floor as the cost would have been amplified by the drop in the EUR allied to cutting rates in order to deter market participants from parking their cash at the Swiss central bank.

FIXED INCOME/EQUITIES

The European curve is seen flatter this morning as a result of the surprise announcement from the SNB which is likely to further fuel the flames of ECB QE at the looming meeting next Thursday (22nd). Bund futures spiked higher on the release of the Swiss news tripping stops on the rise to further exacerbate the gains with the German 10yr yield now at 0.472%. In equity market the SMI is the standout trading down in excess of 9% as fears that strength in the local currency is likely to impact negatively corporate profits, particularly when there are large export names such as Nestle, Roche and Swatch based in the country.

OTHER FX NEWS

Overnight AUD outperformed bolstered by a stellar December jobs report (Employment Change +37.4k vs. Exp. +5.0k (Prev. +42.7k, Rev. +45.0k) and a fall in the unemployment rate to 6.1% from 6.3%, supported by a surge in full-time employment 41.6k (Prev. 1.8k).

In other news of note, the RBI unexpectedly cut its Repo Rate by 25bps to 7.75% from 8.00% in a surprise move in an attempt to curb falling inflation. The central bank also cut its Reverse Repo Rate by 25bps to 6.75% but kept the cash reserve ratio unchanged at 4.00%. (BBG)

COMMODITIES

Overnight, the commodities complex staged a recovery as Brent crude broke back above the USD 50 handle and WTI rallied to trade near USD 50/bbl it’s the biggest surge in two-and-a-half years. Although, WTI and Brent has since come off best levels in the European session. Furthermore, COMEX copper prices have traded slightly rebounded from yesterday’s sharp decline to 5 and-a-half year lows providing the material sector with some reprieve. As we head toward the North American session, gold is testing its 200DMA at USD 1253.47 and has not traded above there since August 2014.

Other notable headlines via Bloomberg:

- Treasuries gain, led by 3Y and 5Y; 10Y yields at lowest since May 2013, 30Y near record low as Swiss National Bank unexpectedly drops franc cap, Reserve Bank of India cuts benchmark rate.

- OPEC cuts demand for its crude in 2015, already at 12-yr low, by 100k b/d to to 28.8m b/d; forecast U.S. output is slowing as prices tumble, group says in its monthly oil market report

- BP said to expects $50-$60 oil for next three years, BBC’s eco editor Robert Peston says in Twitter post, without saying where he got info

- CHF soars as SNB abandons 1.20 cap vs EUR, says enforcing cap no longer justified, brings forward planned rate cut -0.75% initially set for Jan. 22

- Move comes just one week before ECB policy makers meet to discuss the purchase of government bonds, a move that may add to pressure on the franc against the euro

- Indian stocks, bonds and INR surged after Rajan lowered repo rate to 7.75% from 8%, first reduction in 20 months; move sets India apart from BRIC counterparts Russia and Brazil, which boosted rates after currency declines that spurred inflation

- Yellen has signaled she wants to look past short-term market fluctuations and place economic outlook at center of policy making; to succeed, she must wean investors from the notion that the Fed will bail them out if their bets go bad

- Germany’s economy grew 1.5% in 2014, fastest pace in three years, matching median estimate in a Bloomberg survey

- China’s shadow banking industry staged a comeback in December as equity investors and local governments contributed to a surge in credit

- Bank of China Ltd. is suing a unit of Kaisa Group Holdings Ltd. after the developer skipped a payment on its USD bonds and as local creditors seek to recoup funds

- Sovereign yields mixed. Asian stocks rise; European stocks, U.S. equity-index futures decline. Crude lower; copper and gold higher

end

As I warned you last month to expect problems facing the Swiss National bank as they were technically the only bidder for Euros.

The SNB had purchased a sum of euros already the equivalent of 80% of their GDP. No doubt Jordan, manager of the SNB probably got wind of Draghi’s next huge QE and Switzerland just could not adsorb any more euros. He removed the peg and also raised the negative interest rate on the Swiss Franc. He was desperately trying to stop the rise in the Swiss franc vs the Euro. This caused gold to rise as well as oil. Gold stayed high throughout the day but oil retreated by days end.

First story: the unpegging of the 1.20 Swiss Franc/Euro peg:

(courtesy zero hedge)

“It’s Carnage” – Swiss Franc Soars Most Ever After SNB Abandons EURCHF Floor; Macro Hedge Funds Crushed

“As if millions of macro hedge funds suddenly cried out in terror and were suddenly silenced”

Over two decades ago, George Soros took on the Bank of England, and won. Just before lunch local time, the Swiss National Bank took on virtually every single macro hedge fund, the vast majority of which were short the Swiss Franc and crushed them, when it announced, first, that it would go further into NIRP, pushing its interest rate on deposit balances even more negative from -0.25% to -0.75%, a move which in itself would have been unprecedented and, second,announcing that the 1.20 EURCHF floor it had instituted in September 2011, the day gold hit its all time nominal high, was no more.

What happened next was truly shock and awe as algo after algo saw their EURCHF 1.1999 stops hit, and moments thereafter the EURCHF pair crashed to less then 0.75, margining out virtually every single long EURCHF position, before finally rebounding to a level just above 1.00, which is where it was trading just before the SNB instituted the currency floor over three years ago.

Visually:

The SNB press release:

Swiss National Bank discontinues minimum exchange rate and lowers interest rate to –0.75%

Target range moved further into negative territory

The Swiss National Bank (SNB) is discontinuing the minimum exchange rate of CHF 1.20 per euro. At the same time, it is lowering the interest rate on sight deposit account balances that exceed a given exemption threshold by 0.5 percentage points, to ?0.75%. It is moving the target range for the three-month Libor further into negative territory, to between –1.25% and -0.25%, from the current range of between -0.75% and 0.25%.

The minimum exchange rate was introduced during a period of exceptional overvaluation of the Swiss franc and an extremely high level of uncertainty on the financial markets. This exceptional and temporary measure protected the Swiss economy from serious harm. While the Swiss franc is still high, the overvaluation has decreased as a whole since the introduction of the minimum exchange rate. The economy was able to take advantage of this phase to adjust to the new situation.

Recently, divergences between the monetary policies of the major currency areas have increased significantly – a trend that is likely to become even more pronounced. The euro has depreciated considerably against the US dollar and this, in turn, has caused the Swiss franc to weaken against the US dollar. In these circumstances, the SNB concluded that enforcing and maintaining the minimum exchange rate for the Swiss franc against the euro is no longer justified.

The SNB is lowering interest rates significantly to ensure that the discontinuation of the minimum exchange rate does not lead to an inappropriate tightening of monetary conditions. The SNB will continue to take account of the exchange rate situation in formulating its monetary policy in future. If necessary, it will therefore remain active in the foreign exchange market to influence monetary conditions.

The resultant move across all currency pairs has seen the EUR and USD sliding, the USDJPY crashing, and US futures tumbling even as European stocks plunged only to kneejerk higher as markets are in clear turmoil and nobody knows just what is going on right now.

In other asset classes, Treasury yields, understandably plunged across the entire world, and the entire Swiss bond curve lest of the 10 Year is now negative, with the On The Run itself threatening to go negative soon as can be seen on the table below:

Crude and other commodities, except gold, are also tumbling, as are most risk assets over concerns what today’s epic margin call will mean when the closing bell arrives.

An immediate, and amusing, soundbite came from the CEO of Swatch Nick Hayek who said that “words fail me” at the SNB action: “Today’s SNB action is a tsunami for the export industry and for tourism, and finally for the entire country.” More from Reuters:

Swatch Group UHR.VX Chief Executive Nick Hayek called the Swiss National Bank’s decision to discontinue the minimum exchange rate on the Swiss franc a “tsunami” for the Alpine country and its economy.

“Words fail me! Jordan is not only the name of the SNB president, but also of a river… and today’s SNB action is a tsunami; for the export industry and for tourism, and finally for the entire country,” Hayek said in an emailed statement on Thursday.

Swiss watchmakers, which are also grappling with weak demand in Asia, are very exposed to moves in the Swiss franc exchange rate because their production costs are largely in Swiss francs, but most of their sales are done abroad.

Shares in Swatch Group fell 15 percent at 1056 GMT, while Richemont CFR.VX was down 14 percent, underperforming a 9 percent drop in the Swiss market index .SSMI following the SNB’s announcement.

“Absolutely shocking … For companies with international operations – translated earnings are going to be lower and if companies make products in Switzerland it is going to hurt margin. It is a terrible day for corporate Switzerland,” Kepler Cheuvreux analyst Jon Cox said

Indeed, in retrospect, it does seem foolhardy that the SNB, whose balance sheet ballooned to record proportions just to defends it currency for over three years would give up so easily. The one silver lining, so to say, is that gold prices in CHF just crashed by some 13%.

Some more soundbites from strategists, none of whom foresaw this stunning move:

ALEXANDRE BARADEZ, CHIEF MARKET ANALYST AT IG FRANCE

“This is extremely violent and totally unexpected, the central bank didn’t prepare the market for it. It’s sparking panic across all asset classes. It suddenly revives the risk of central bank policy mistakes, right when central bank action is what’s keeping equity markets going.”

LEX VAN DAM, HAMPSTEAD CAPITAL LLP HEDGE FUND MANAGER:

“Major losses in euro-franc trades are causing panic selling and deleveraging across the board.”

CHRIS BEAUCHAMP, MARKET ANALYST AT IG

“My initial reaction was that it is a sign the ECB is about to do something, which makes it odd that the reaction has been so negative across European stocks. However, it’s not every day that a central bank pulls the rug out from underneath something in such a massive way, and clearly people are worried that there’s something bigger afoot.This kind of event is the kind of thing that will trigger volatility. This is not a one day thing now.”

DARREN COURTNEY-COOK, HEAD OF TRADING AT CENTRAL MARKETS INVESTMENT MANAGEMENT

“They’ve stopped defending the 1.20 floor.It’s carnage.”

PATRICK JACQ, RATE STRATEGIST, BNP PARIBAS, PARIS

“The decision of the SNB means it no longer needs to buy euro-denominated paper in order to defend the 1.20 position. This should normally weigh on European debt but the SNB also said they will continue to monitor in order to prevent the exchange rate from rising substantially.

“This means that at the end of the day even if they don’t defend the 1.20 level, if they want to prevent a collapse of the euro versus the Swiss franc they will probably have to keep on buying, maybe at a lesser extent, euro denominated paper.”

JONATHAN WEBB, HEAD OF FX STRATEGY AT JEFFERIES, LONDON

“It has taken the market by complete surprise. The SNB probably expects the ECB to launch QE next week and along with the Greek elections coming up, it would make it pretty tough on the Swiss to keep bidding the euro.

So they have abandoned the cap and cut rates deeper into negative territory. We expect euro/Swiss to trade around 0.90-1.00 francs after all the stop loss orders have been cleared”

GEOFFREY YU, CURRENCY STRATEGIST AT UBS IN LONDON:

“They think too much money is going to come in, especially with QE coming, and so they think they need a ‘Plan B’.”

“Let it run, let it settle, and we’ll see what happens next.”

However, the best soundbites today will surely come from US hedge funds which are just waking up to the biggest FX shocked in years, and of course, any retail investors who may have been long the EURCHF, and who are not only facing epic margin calls, but are unable to cover their positions, and one after another retail FX brokerage has commenced “Rubling” the Swissy and as CHF pair as suddenly not available for trading.

To say that today will be interesting, is an understatement.

end

CME Just Doubled (And Tripled) Swiss Franc Margins

We suspect there will be a few more “taps on the shoulder” tonight (and tomorrow)…

As per the normal review of market volatility to ensure adequate collateral coverage, the Chicago Mercantile

Exchange Inc., Clearing House Risk Management staff approved the performance bond requirements for the

following products listed below.

The rates will be effective after the close of business on Thursday, January 15, 2015.

DOUBLED!

The rates will be effective after the close of business on Friday, January 16, 2015.

TRIPLED!

end

And panic did set in: expect massive margin calls:

(courtesy zero hedge)

Margin Calls? EURCHF Breaks Back Below Parity

12 hours after it first broke back above parity, EURCHF is back below 1.00 as post-NY-close FX trading is seeing a notable drop in the cross…

And close up…

and it’s accelerating…

Panic Begins…

Charts: Bloomberg

end

UBS states that the Swiss are in for a huge deflationary shock.

Many firms cannot compete as the Swiss Franc is just too high and exporters have priced themselves out of business. Tourism which is a big part of Switzerland’s economy will also be hurt with the high Swiss Franc.

The other big problem with the unpegging of the Swiss franc is the huge derivative blow up from many hedge funds. They took the word of the central bank of Switzerland that they will never unpeg the SF. They were the huge short in the Swiss Franc and believe it or not, the big long position was the dollar. The boys were doing OK for quite a while as the dollar rose in value and the Swiss franc hardly budged from the peg. However today, that well apart along with other carry trades.

(courtesy UBS/zero hedge)

UBS’ Take On The Swiss Shocker: “The SNB’s Standing Is Undermined… There Could Be A Significant Deflationary Shock”

From UBS’ Beat Siegenthaler:

No more floor

The SNB today dropped the 1.20 EURCHF floor while at the same time lowering the negative interest rate on sight deposits to -0.75% from -0.25% previously, as well as moving the 3m Libor target to between -0.25% and -0.75%. The SNB argues that the floor was an exceptional and temporary measure that ‘protected the Swiss economy from serious harm’ but that the economy had had time to adjust to the new situation. It continues to argue that the franc had recently depreciated ‘considerably’ against the dollar. ‘In these circumstances, the SNB concluded that enforcing the minimum exchange rate for the Swiss franc against the euro is no longer justified’.

Dramatic market impact

The announcement has had a dramatic impact on markets with EURCHF initially dropping 40% to almost 0.85. It quickly reversed seemingly with the help of SNB interventions at levels just above parity to the euro.The statement noted that ‘if necessary’ the central bank will ‘remain active in the foreign exchange market to influence monetary conditions’. The SMI equity index dropped by more than 8% on the news and has recovered little since. On the rates side cross currency basis moved around another 20bp lower.

Economic repercussions

It would seem likely that today’s decision will have significant ramifications in Switzerland as very few observers expected the floor to be dropped with some arguing that it looked set to remain in place for years. Unless EURCHF was to recover back to levels much closer to the old 1.20 floor, the economy could be significantly impacted, as seems well reflected in the reaction of equity prices. At levels close to parity many businesses and investment decisions might not be seen as viable anymore and over time a significant volume of economic production could move outside the country. If so, there could be a significant deflationary shock possibly not too dissimilar to the one Switzerland might have suffered had the floor not been introduced in 2011.

Hope of a limited drop

Where will EURCHF settle after today? The big question is whether investors will want to buy Swiss francs despite substantially negative interest rates and at clearly expensive levels. Nevertheless, safe haven flows have so far demonstrated a remarkable stickiness which can be expected to continue as long as global risk aversion reigns. The SNB might be hoping to be able to stabilise EURCHF at around 1.10 which may be deemed a level that the economy can cope with. However, defending such a level might still be quite costly assuming that global risk aversion continues to linger.

Credibility cost

The other question is about the cost of today’s decision for the SNB, both in monetary and credibility terms. The SNB is holding roughly half of their CHF500bn in euros, which implies a loss of possibly not dissimilar to the CHF38bn that the SNB made in profit last year.The monetary impact might thus be manageable. The credibility impact might be harder to gauge though. Domestically, many economic actors relied on what was seen as a ‘promise’ to hold the 1.20 floor.Internationally, following the negative rates confusion back in December today’s decision might be further undermined the standing of the SNB among investors.

end

Our resident expert on Swiss Franc vs the Euro comments on the unpegging:

(courtesy Bruce Krasting)

End of CB Power – SNB Folds

I wrote about the Swiss National Bank being forced to abandon its currency peg to the Euro on 12/3/14, 12/8/14 and 1/11/15. That said, I’m blown away that this has happened today.

Thomas Jordan, the head of the SNB has repeated said that the Franc peg would last forever, and that he would be willing to intervene in “Unlimited Amounts” in support of the peg. Jordan has folded on his promise like a cheap suit in the rain. When push came to shove, Jordan failed to deliver.

The Swiss economy will rapidly fall into recession as a result of the SNB move. The Swiss stock market has been blasted, the currency is now nearly 20% higher than it was a day before. Someone will have to fall on the sword, the arrows are pointing at Jordan.

The dust has not settled on this development as of this morning. I will stick my neck out and say that the failure to hold the minimum rate will result in a one time loss for the SNB of close to $100B. That’s a huge amount of money. It comes to 20% of the Swiss GDP! If this type of loss were incurred by the US Fed it would result in a loss in excess of $2 Trillion!

In the coming days and weeks there will be more fallout from the SNB disaster. There will be reports of big losses and gains from today’s events. But that is a side show to the real story. We have just witnesses the collapse of a promise by a major central bank.

The Fed, Bank of Japan, ECB, SNB and other Central Banks have repeatedly made the same promises over the past half decade:

Don’t worry! We are here. We will do anything it takes to achieve the stability we desire. We are stronger than the markets. We can overwhelm all forces. We will never let go – just trust us!

I never believed in these promises, but the vast majority of those who are active in financial markets did. The entire world has signed onto the notion that Central Banks are all powerful. We now have evidence that they are not.

Anyone who continues to believes in the All Powerful CB after today is a fool. Those who believed in Jordan’s promises now have red ink on their hands – lots of it!

The next central bank that will come into the market’s cross hairs is the ECB. Mario Draghi has made promises that he would “Do anything – in any amount”. Like I said, you would be a fool to continue to believe in that promise as of this morning.

We’ve just taken a huge leap into chaos. The linchpin of the capital markets has been the trust in the CBs. The market’s anchors have now been tossed overboard.

end

The 10 yr Swiss Franc bond yield is only 3 basis points above zero.Swiss stocks collapse the most in 25 years with today’s unpegging. The Swiss yield curve inverted indicating recession as totally inevitable over there:

(courtesy zero hedge)

Swiss Stocks Collapse Most In 25 Years: Surveying The European Close Carnage

Swiss 10Y rates crashed over 10bps by the close (having plunged as low as 3.3bps at one point) but the entire Swiss curve is negative at any maturity less than that. EURUSD crashed over 200pips back below 1.16 – the lowest since November 2003. Swiss stocks crashed around 15% before bouncing back to a 8-9% loss – the biggest drop since 1989. Away from Switzerland (and Greece) European stocks and sovereign bonds saw initial dips bought on ECB QE implications but EU Sovereigns did bleed back wider. European VIX spiked from sub-29 to over 32 and all the way back down to close lower on the day.

The big story is EURCHF – which collapsed 35 handles at its worst…

EURUSD breaks 1.16 – lowest in over 11 years…

Swiss Stocks crashed… the biggest daily drop since 1989…

And The Swiss Yield Curve crashed to negative rates to 9 years…

Away from Switzerland, markets were bulled up by this news implying moar QE coming down the pike…

Sovereign bond spreads collapsed at the open but bled back wider as the day went on…

And ex-Swiss and Greek stocks, European stock markets rallied…

With The DAX dumped and then pumped back over 10,000 near record highs…

European VIX roundtripped…

Charts: Bloomberg

end

Last night, this was surely the biggest story of the year only to be trumped by the Swiss announcement: Russia cuts off Ukraine Gas Supply to 6 European countries. It is payback time for Russia to inflict damage to the west for their sanctions on Russia:

(courtesy zero hedge)

Russia Cuts Off Ukraine Gas Supply To 6 European Countries

Vladimir Putin ordered the Russian state energy giant Gazprom to cut supplies to and through Ukraine amid accusations, according to The Daily Mail,that its neighbor has been siphoning off and stealing Russian gas. Due to these “transit risks for European consumers in the territory of Ukraine,” Gazprom cut gas exports to Europe by 60%, plunging the continent into an energy crisis “within hours.” Perhaps explaining the explosion higher in NatGas prices (and oil) today, gas companies in Ukraine confirmed that Russia had cut off supply; and six countries reported a complete shut-off of Russian gas. The EU raged that the sudden cut-off to some of its member countries was “completely unacceptable,” but Gazprom CEO Alexey Miller later added that Russia plans to shift all its natural gas flows crossing Ukraine to a route via Turkey; and Russian Energy Minister Alexander Novak stated unequivocally,“the decision has been made.”

Russia plans to shift all its natural gas flows crossing Ukraine to a route via Turkey, a surprise move that the European Union’s energy chief said would hurt its reputation as a supplier.

The decision makes no economic sense,Maros Sefcovic, the European Commission’s vice president for energy union, told reporters today after talks with Russian government officials and the head of gas exporter, OAO Gazprom, in Moscow.

Gazprom, the world’s biggest natural gas supplier, plans to send 63 billion cubic meters through a proposed link under the Black Sea to Turkey, fully replacing shipments via Ukraine, Chief Executive Officer Alexey Miller said during the discussions. About 40 percent of Russia’s gas exports to Europe and Turkey travel through Ukraine’s Soviet-era network.

…

Sefcovic said he was “very surprised” by Miller’s comment, adding that relying on a Turkish route, without Ukraine, won’t fit with the EU’s gas system.

Gazprom plans to deliver the fuel to Turkey’s border with Greece and “it’s up to the EU to decide what to do” with it further,according to Sefcovic.

Which, as The Daily Mail reports, has led to a major (and imminent) problem for Europe…

Russia cut gas exports to Europe by 60 per cent today, plunging the continent into an energy crisis ‘within hours’ as a dispute with Ukraine escalated.

This morning, gas companies in Ukraine said that Russia had completely cut off their supply.

Six countries reported a complete shut-off of Russian gas shipped via Ukraine today, in a sharp escalation of a struggle over energy that threatens Europe as winter sets in.

Bulgaria, Greece, Macedonia, Romania, Croatia and Turkey all reported a halt in gas shipments from Russia through Ukraine.

* * *

As Bloomberg goes on to note, Gazprom has reduced deliveries via Ukraine after price and debt disputeswith the neighboring country that twice in the past decade disrupted supplies to the EU during freezing weather.

“Transit risks for European consumers on the territory of Ukraine remain,” Miller said in an e-mailed statement. “There are no other options” except for the planned Turkish Stream link, he said.

“We have informed our European partners, and now it is up to them to put in place the necessary infrastructure starting from the Turkish-Greek border,”Miller said.

Russia won’t hurt its image with a shift to Turkey because it has always been a reliable gas supplier and never violated its obligations, Russian Energy Minister Alexander Novak told reporters today in Moscow after meeting Sefcovic.

“The decision has been made,” Novak said. “We are diversifying and eliminating the risks of unreliable countries that caused problems in past years, including for European consumers.”

* * *

That helps to explain today’s epic meltup in NatGas futures…

* * *

“They [the Russians] have reduced deliveries to 92million cubic metres per 24 hours compared to the promised 221million cubic metres without explanation,” said Valentin Zemlyansky of the Ukrainian gas company Naftogaz.

“We do not understand how we will deliver gas to Europe. This means that in a few hours problems with supplies to Europe will begin.”

* * *

Check to you Europe (i.e. Washington)… Because it’s getting might cold in Europe…

Canada Crude Contagion: Calgary Home Prices Drop Most In 2 Years

For the 2nd month in a row, home prices in Calgary – corporate hub of Canada’s oil industry – have fallen. This is the biggest 2-month-drop in almost 2 years (and comes on the heels of yesterday’s news that Suncor is slashing jobs and capex). As Bloomberg reports, Bank of Canada Deputy Governor Tim Lane said yesterday development of the more expensive deposits are threatened by lower crude oil prices. “The dive in energy prices will put pressure on house prices in the Western provinces in the coming months,” warns one economist and as the following chart shows, more pain is likely...

It appears the price of homes in Canada’s most important energy region are extremely correlated with a lagged oil price… which suggests a lot more pain is to come…

* * *

As we explained previously, this won’t end well…

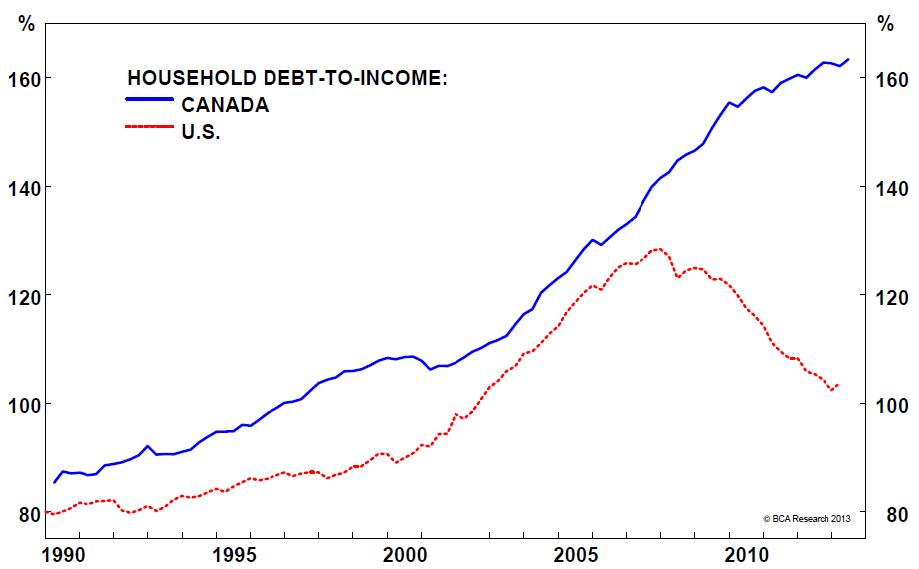

In Canadian debt we trust

There was an inflexion point for US markets when household debt surpassed household income. People kept saying it was a liquidity crisis initially but it was truly a solvency crisis. People took on too much debt and were walking on a financial tightrope. In the US, this peaked above 120 percent. Canada is well on its way above 160 percent:

Basically Canadians are deeper in debt relative to their income. And a large part of this debt is housing related. A large part of the economy is also tied to oil and as you may know, oil just took a massive cut.

…

Canada has enjoyed many years of the global commodities boom and now finds itself contending with a market full of debt and inflated housing values. Short of oil rising back up to $80 a barrel and higher Canada is likely going to face some short-term pain. The housing market is due for a correction. Those of us in California realize that booms and busts can occur all of a sudden but the events leading up to this are largely foreseeable.

I’m sure many in Canada assume that home values will simply continue to go up and just because banks check incomes doesn’t mean squat. As the above data shows, households are already deep in the quicksand of massive debt. It is all dandy when everything is going up including oil. When oil gets smashed as it did, it came on quickly. Canada has their versions of $700,000 crap shacks usually in the form of condos. Hey, at least with a crap shack you don’t have to share a common wall. When you look at the Canadian housing market it makes the US look like a frugal uncle.

end

After initially rising, oil falls almost 10% from yesterday’s highs and erases totally yesterday’s gains:

(courtesy zero hedge)

Crude Collapses Almost 10% From Post-SNB Highs, Erases Yesterday’s OPEX Ramp

Well that escalated quickly. It appears those hoping for ‘stability’ are once again seeing any strength immediately sold into… Having smashed higher yesterday into the OPEX/close and then again this morning (breaking above $51 post-SNB), WTI Crude has collapsed back to $46.50… the scene of the crime for yesterday’s “spoof”-ramp manipulation.

The Greek Bank Runs Have Begun: Two Greek Banks Request Emergency Liquidity Assistance

The first time the phrase Emergency Liquidity Assistance, or ELA, was used in the context of Greecewas in August 2011, when Greece was imploding, when its banking sector was on (and past) the verge of collapse, and just before the ECB had to unleash a global coordinated bailout with other central banks including global central bank liquidity swap and unleash the LTRO to preserve the Eurozone.

As a reminder, this is what happened back then: “In a move described as the “last stand for Greek banks”, the embattled country’s central bank activated Emergency Liquidity Assistance (ELA) for the first time on Wednesday night.”

“Although it was done discreetly, news that Athens had opened the fund filtered out and was one of the factors that rattled markets across Europe. At one point Germany’s Dax was down 4pc before it recovered. The ELA was designed under European rules to allow national central banks to provide liquidity for their own lenders when they run out of collateral of a quality that can be used to trade with the ECB. It is an obscure tool that is supposed to be temporary and one of the last resorts for indebted banks.”

Raoul Ruparel of Open Europe told The Telegraph: “The activation of the so-called ELA looks to be the last stand for Greek banks and suggests they are running alarmingly short of quality collateral usually used to obtain funding.”

He added: “This kicks off another huge round of nearly worthless assets being shifted from the books of private banks onto books backed by taxpayers. Combined with the purchases of Spanish and Italian bonds, the already questionable balance sheet of the euro system is looking increasingly risky.”

As a further reminder, this is how cryptically little the ECB has to say about its “last-ditch” liquidity bailout program:

Euro area credit institutions can receive central bank credit not only through monetary policy operations but exceptionally also through emergency liquidity assistance (ELA). ELA means the provision by a Eurosystem national central bank (NCB) of

- central bank money and/or

- any other assistance that may lead to an increase in central bank money

to a solvent financial institution, or group of solvent financial institutions, that is facing temporary liquidity problems, without such operation being part of the single monetary policy.

We bring this up because things in Greece just went bump in the night. Again.

Recall that as we reported three days ago, while Greece refused to admit that it was suffering a bank run ahead of a potentially game-changing election, it did report that “most taxpayers have chosen to delay their [tax] payments, given that the positions of the two main parties leading the election polls are diametrically opposite: Poll leader SYRIZA promises to cancel the ENFIA and even write off bad loans, while ruling New Democracy acknowledges the difficulties but is avoiding raising issues that would generate problems and fiscal consequences.”

Well, yesterday we got some more details on the collapse in tax payments when Kathimerini reported that indeed as feared, Greek tax remittances have plunged by up to 80% compared to last year, in the process making a mockery of any Greek reforms.

Finance Ministry officials believe there will be no problem meeting the targets of the bailout program as far as the general government primary surplus, which amounts to 1.5 percent of gross domestic product for 2014, is concerned. There are, however, worries regarding the 2015 budget, as the year has got off to a terrible start in terms of revenue collections.

The target for January is 4.5 billion euros, but tax officials report that they saw no activity that would support that goal in the first 10 days of the month. Sources say that the decline compared to the first 10 days of 2014 ranges between 70 and 80 percent.

That’s not the bad news. The bad news is that as we also speculated, and as Greek officials tried to cover up as usual, the Greeks have resumed doing what they do best any time their country is facing a grand crisis: walking to the bank and withdrawing what little deposits they have left. Or rather running to the bank.

Which brings us back to the topic of the Emergency Liquidity Assistnace, which as Kathimerini reported moments ago, at least two Greek systemic banks have reportedly resorted to, indicating that the liquidity situation in Greece is once again as dire as it was in the depth of the European collapse.

To wit:

Two Greek systemic banks reportedly submitted the first requests to the Bank of Greece for cash via the emergency liquidity assistance (ELA) system on Thursday, in response to the pressing liquidity conditions resulting from the growing outflow of deposits as well as the acquisition of treasury bills forced onto them by the state.

Banks usually resort to ELA when they face a cash crunch and do not have adequate collateral to draw liquidity from the European Central Bank, their main funding tool. ELA is particularly costly as it carries an interest rate of 1.55 percent, against just 0.05 percent for ECB funding.

The requests by the two lenders will be discussed by the ECB next Wednesday.

Bank officials commented that lenders are resorting to ELA earlier than expected, which reflects the deteriorating liquidity conditions in the credit sector.

Besides the decline in deposits, banks were dealt another blow on Thursday with the scrapping of the euro cap on the Swiss franc. Bank estimates put the impact of the euro’s drop on the local system’s cash flow at between 1.5 and 2 billion euros.

Deposits recorded a decline of 3 billion euros in December – a month when they traditionally expand – while in the first couple of weeks of January the outflow continued, although banks say it is under control.

A major blow to the system’s liquidity has come from the repeated issue of T-bills: In November the state drew 2.75 billion euros in this way, in December it secured 3.25 billion euros, and it has already tapped another 2.7 billion in January. Of the above amounts, a significant share – amounting to 3 billion euros according to bank estimates – was in the hands of foreign investors who will not renew them, so they have to be bought by the Greek banks.

Local lenders had also resorted to ELA in 2011 to cope with the outflow of deposits and consecutive credit rating downgrades of the state (and the banks) that made Greek paper insufficient for the supply of liquidity by the Eurosystem. In May 2012, due to the uncertainty of the twin elections at the time, local banks drew 124 billion euros in ELA to handle the unprecedented outflow of deposits.

And just like that, it’s deja vu all over again, and the worst days of the summer of 2011 are ahead of us once more, only this time Draghi’s “Whatever it takes”unconditional OMT bazooka has conditions, and anyway after today’s SNB fiasco, what a central bank threatens, warns, begs or even does, may no longer even matter.

2 Dead, 1 Arrested After Massive Anti-Terrorism Raids In Belgium

Belgium has raised its terror alert level from 3 to 4 for police forces (maintaining alert level 2 for everyone else) as it unleashes 10 raids in Verviers (near the capital) on returning Syrian fighters:

- *BELGIAN SUSPECTED TERRORISTS OPENED FIRE AT POLICE DURING RAID

- *BELGIAN POLICE KILLS TWO TERRORISTS, NO WOUNDED AMONG POLICE

Anti-terrorist operations continue (despite reassurances that this not linked to the Paris attacks) as prosecutors say the suspected terrorists planned large, imminent attacks.

Bloomberg headlines…

- *BELGIAN CONDUCTED 1O SEARCHES IN VERVIERS, NEAR CAPITAL

- *BELGIAN POLICE FOILS TERRORISM PLOT BY RETURNED SYRIA FIGHTERS

- *BELGIUM RAISES THREAT LEVEL TO 3 OUT OF 4 FOR POLICE FORCES

- *BELGIAN ANTI-TERRORISM OPERATIONS STILL CONTINUING

- *BELGIAN POLICE KILLS TWO SUSPECTED TERRORISTS IN VERVIERS

- *BELGIAN POLICE DETAINS THIRD SUSPECTED TERRORIST IN VERVIERS

- *BELGIAN SUSPECTED TERRORISTS PLANNED LARGE, IMMINENT ATTACKS

- *BELGIAN SUSPECTED TERRORISTS OPENED FIRE AT POLICE DURING RAID

- *BELGIAN PROSECUTORS SEE NO LINK FOR NOW WITH PARIS ATTACKS

- *BELGIAN PROSECUTORS SAY PROBE STARTED COUPLE OF WEEKS AGO

Raids caught on tape…

* * *

Your more important currency crosses early Thursday morning:

Eur/USA 1.1714 down .0070

USA/JAPAN YEN 116.53 down .926

GBP/USA 1.5246 up .0013

USA/CAN 1.1844 down .0103

This morning in Europe, the euro continues on its downward spiral, trading down and now well below the 1.18 level at 1.1714 as Europe reacts to deflation, and announcements of massive stimulation. In Japan Abe went all in with Abenomics with another round of QE purchasing 80 trillion yen from 70 trillion on Oct 31. He now wishes to give gift cards to poor people in order to spend. The yen continues to trade in yoyo fashion. This morning it settled up again in Japan by 93 basis points and settling still well below the 117 barrier to 116.53 yen to the dollar. The pound was up this morning as it now trades just above the 1.52 level at 1.5246.(very worried about the health of Barclays Bank and the FX/precious metals criminal investigation/Dec 12 a new separate criminal investigation on gold,silver oil manipulation). The Canadian dollar is well up today trading at 1.1845 to the dollar. It seems that the three major global carry trades are being unwound. (1) The total dollar global short is 9 trillion USA, and as such we now witness a sea of red blood on the streets as derivatives blow up with the massive rise in the dollar against all paper currencies.We also have the second big yen carry trade unwind as the yen refuses to blow past the 120 level.(3) the Nikkei vs gold carry trade as the Nikkei now collapses causing those short gold to purchase our scarce physical yellow metal. These massive carry trades are causing deflation as the world reacts to a lack of demand. Bourses around the globe are reacting in kind to these events.

Early Thursday morning USA 10 year bond yield: 1.82% !!! down 3 in basis points from Wednesday night/

USA dollar index early Thursday morning: 91.71 down 46 in cents from Wednesday’s close

The NIKKEI: Thursday morning : up 313 points or 1.86%

Trading from Europe and Asia:

1. Europe stocks all in the green.

2/ Asian bourses mostly in the green … Chinese bourses: Hang Sang in the green ,Shanghai in the green, Australia in the red: /Nikkei (Japan) green/India’s Sensex in the green/

Gold early morning trading: $1252

silver:$17.10

Closing Portuguese 10 year bond yield: 2.66% par in basis points from Wednesday

Closing Japanese 10 year bond yield: .26% !!! down 1 in basis points from Wednesday

Your closing Spanish 10 year government bond, Thursday down 11 in basis points in yield from Wednesday night.

Spanish 10 year bond yield: 1.55% !!!!!!

Your Thursday closing Italian 10 year bond yield: 1.73% down 9 in basis points from Wednesday:

trading 18 basis points higher than Spain:

IMPORTANT CLOSES FOR TODAY

Closing currency crosses for Thursday night/USA dollar index/USA 10 yr bond:

Euro/USA: 1.1622 down .0162

USA/Japan: 116.37 down 1.065

Great Britain/USA: 1.5186 down .0048

USA/Canada: 1.1962 up .0016

The euro collapsed today and by closing time finished down by a whopping .0162 and well below the 1.18 level to 1.1622. The yen was up in the afternoon, but it was well up by closing to the tune of 107 basis points and closing well below the 118 cross at 116.37 still causing much grief again to our yen carry traders who need a much lower yen. The British pound lost some ground during the afternoon session and it was down on the day closing at 1.5186. The Canadian dollar was down again in the afternoon and it was down on the day at 1.1962 to the dollar.

As explained above, the short dollar carry trade is being unwound, the yen carry trade and now the Nikkei/gold carry trade and these unwinding are causing massive derivative losses. And as such. these massive derivative losses is the powder keg that will destroy the entire financial system.

Your closing USA dollar index: 92.32 down 15 cents from Wednesday.

your 10 year USA bond yield , down 9 in basis points on the day: 1.76%!!!!

European and Dow Jones stock index closes:

England FTSE up 110.32 points or 1.73%

Paris CAC up 99.96 or 2.37%

German Dax up 215.53 or 2.20%

Spain’s Ibex up 135.50 or 1.39%

Italian FTSE-MIB up 433.84 or 2.36%

The Dow: down 106.38 or 0.61%

Nasdaq; down 68.50 or 1.48%

OIL: WTI 46.22 !!!!!!!

Brent: 46.79!!!!

Closing USA/Russian rouble cross: 65.16 down 1/4 rouble per dollar on the day.

And now for your more important USA economic stories for today:

(Your trading today from the New York):

Swissnado Stuns Stocks, Bonds & Bullion Bid

Lagarde seemed to admit there is a problem… Overheard at The SNB building earlier…

And as a bonus, we thought this was appropriate…

Stocks initially jerked higher on the SNB news (as didbond yields and crude oil) as the removal of the EURCHF ceiling prompted belief in ECB QE being imminent… but that quickly reverted – not helped by Christine Lagarde’s clear discontent with the SNB decision and investors realized that for the first time in years, a central bank surprised traders…

Stocks are down 5 days in a row (Dow hasn’t seen that since Jim Bullard saved the world in Mid-October)

And the S&P 500 hasn’t fallen 5 days in a row since Dec 2013… and closed below its 100DMA

S&P could not get back above 2,000…

Quite a ride the last few days… Year-to-date – Trannies and Small Caps losing

Futures show today’s swing better… “NOT OFF THE LOWS”

as stocks slump back to pre-FOMC levels…

Homebuilders were hammered today again as hope from Monday has been crushed…

Financials continue to get whacked – playing catch down to credit… US Majors Credit risk surges to 10 months highs

Treasury yields collapsed 8-12bps today with 10Y below 1.75% and 30Y at 2.38%!!! Not closing off the lows!!

For fun – here is the Swissy move in context this week…

Note the USD strengthened significantly on the day as EUR collapsed (despite the CHF strength)

Despite the USD strength, gold surged…

And WTI Crude totally roundtripped both the OPEX ramp and the SNB ramp for a massive +/-10% swing…

Charts: Bloomberg

end

Bank of America delivers an awful financial report as trading revenue falters by over 2 billion dollars.

Bank Of America Misses Revenue By $2 Billion As Trading Revenue Collapses; Fires Thousands

Following disappointing results from JPM and Wells Fargo yesterday, it was Bank of America’s turn to “surprise” investors with its disclosure just how bad its quarter was. And with the bank reporting a 50% collapse in its sales and trading from Q3, down $600 million from a year ago to just $1.7 billion in Q4, it should come as no surprise that the bank just reported Net Income, before the usual spate of amusing addbacks, of $0.25 well below the $0.31 expected. And while one may argue whether ot not BofA’s EPS deserve non-GAAP adbacks, it was the Revenue of $18.96 billion, which missed expectations of $21.03 billion by over $2 billion (!) and down $2.7 billion from a year ago, that was truly a showstropper and shows that without the Fed’s visible hand manipulating markets every day, banks are a ticking time bomb just waiting to blow.

In BofA’s own words: “Bank of America Corporation today reported net income of $3.1 billion, or $0.25 per diluted share, for the fourth quarter of 2014, compared to $3.4 billion, or $0.29 per diluted share in the year-ago period. Revenue, net of interest expense, on an FTE basis(B) was $19.0 billion, compared to $21.7 billion in the fourth quarter of 2013.”

And keep in mind that the $4.5 billion in pretax earnings included the usual piggybank accounting gimmick of adding back of $0.7 billion in loan loss reserve releases.

Here is the collapse in Sales and Trading, regardless of whether one observes it with or without DVA/FVA:

But here is the best indicator of what BofA’s earnings truly were: its headcount. And after firing over 4K FTEs, or down 2.5% from the prior quarter, dropping the total FTE count to 207.9, one can see which way management is positioned.

The good news is that the criminal enterprise that is BofA only had to pay $393 million in litigation expenses, far below the $2.3 billion a year ago. Then again, putting in context, BofA paid up $16.4 billion and $6.1 billion in 2014 and 2013, respectively, in “cost of doing business as a criminal enterprise.”

Finally, while JPM “forgot” to report its Net Interest Margin data, BofA was kind enough to provide it. One look at the chart below, which impact all banks, shows why JPM decided it could just do without this data in Q4.

And there you have it: lowest. NIM. Ever.

Q4 earnings presentation below (see zero hedge)

end

The Philly Manufacturing index crashes from a 21 year high to a 12 month low as employment tumbles:

(courtesy BLS/zero hedg)

Philly Fed Crashes From 21 Year Highs To 12 Month Lows, Employment Tumbles

With the biggest miss since August 2011, The Philly Fed Factory Index crashed from 21 year highs in November to the lowest since Feb 2014. The headline 6.3 print, missing expectations of 18.7, follows last month’s drop for the biggest 2-month drop since Lehman. Under the surface things are even worse with the employment sub-index plunging to its worsdt since June 2013 and the outlook for CapEx slashed in half from 24.8 to 13.2. But but but fundamentals…

From best in 21 years to total carnage and biggest 2-month slump since Lehman…

And under the covers its ugly…

Charts: Bloomberg

end

The initial jobless claims surge above the 300,000 mark:

(courtesy zero hedge)

Initial Jobless Claims Surge Above 300k, Highest Since June 2014

Tumbling retail sales and now surging jobless claims… perhaps the “low oil is awesome” narrative is not true after all. Initial Jobless claims surged to 316k (smashing expectations of 290k) and has not been higher since June 2014. The BLS reports no unusual activity – so economists can’t hust shrug this one off. Details on state-by-state job losses are lagged a week so we will not know if this is Shale Oil region-related but yesterday’s Beige Book and day after day of announced job cuts by the energy sector suggest it is.

Caesars Files For Bankruptcy

Et tu, Caesars?

In what has been the most anticipated bankruptcy case in the past several years, hours ago Caesars Entertainment put its main operating unit under Chapter 11 bankruptcy protection in Northern Illinois bankruptcy court (case 15-01153) even as a splinter group of dissident creditors including Appaloosa and Oaktree, holders of about $41 million of Caesars debt and which allege the company has siphoned off billions in value from creditors, put the company into involuntary bankruptcy in Delaware bankruptcy court on January 12. As a reminder, Caesars was one of the sterling LBOs of the last credit bubble, when in 2008 Apollo and TPG decided to take the company private. The problem, as is always the case: too much debt, especially when combined with a broken business model, as Caesars has lost money every year since 2009.

While the Voluntary Bankruptcy Petition, see below, lists some three pages of operating units and affiliate debtors, it preserves the equity interests of the financial sponsors by keeping the parent Caesars Entertainment, out of bankruptcy.