Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1153.30 up $0.70 (comex closing time)

Silver: $15.60 up 12 cents (comex closing time)

In the access market 5:15 pm

Gold $1154.45

Silver: $15.64

Gold/silver trading: see kitco charts on the right side of the commentary.

Following is a brief outline on gold and silver comex figures for today:

The gold comex today had a poor delivery day, registering 1 notice served for 100 oz. Silver comex registered 113 notices for 565,000 oz .

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 249.88 tonnes for a loss of 53 tonnes over that period. Lately the removals have been rising!

In silver, the open interest rose by another astonishing 2,458 contracts even though Friday’s silver price was down by 1 cent. The total silver OI continues to remain extremely high with today’s reading at 177,160 contracts. The front month of March fell by 39 contracts. We are now at multi year high in the OI despite a record low price. This dichotomy has been happening now for quite a while and defies logic.What is also strange today is the fact that the OI in went up with a very tiny volume on Friday. This must be scaring our bankers to no end.

We had 113 notices served upon for 565,000 oz.

In gold we had a slight fall in OI with gold down by $0.50 on Friday. The total comex gold OI rests tonight at 424,231 for a loss of 204 contracts. Today, surprisingly we again had only 1 notices served upon for 100 oz.

Today, we had a constant inventory at the GLD/Inventory rests at 750.67 tonnes

In silver, /SLV we had no change in inventory at the SLV/Inventory, remaining at 327.332 million oz

We have a few important stories to bring to your attention today…

1, Strange data again at the comex tonight: huge OI increases in silver despite lower prices/silver OI at multi year highs and yet silver is extremely low in price. Again at the gold comex, we are witnessing massive amounts of our ancient metal of kings leaving the vaults. (harvey)

2, The ECB only purchases 9.8 billion euros of bonds on its first week. The program will turn out to be a huge failure.

(zero hedge)

3. China has 45 tonnes of gold as demand (=withdrawals from SGE)

Koos Jansen

4. China sells 5.5 billion USA of Treasuries in January after sellin g 6 billion in December. Japan now equals China in total USA treasuries held ( 1.239 trillion.usa) zero hedge

5. War of words between Germany and Greece. Greece is attempting to seize German assets as war reparations. Varoufakis gives the Germans the royal finger.

Today, 3 yr Greek paper trades over 20% in yield/ no foreigner will touch Greek paper/total confidence is now lost in Greece.

Greece repays 580 million euros by borrowing from its pension fund

(zero hedge)

6. In the Oil sector, WTI closed at $43.77. The globe is producing in excess 2 million barrels per day and this oil has to be stored somewhere. There will be no more storage space by June. (zero hedge)

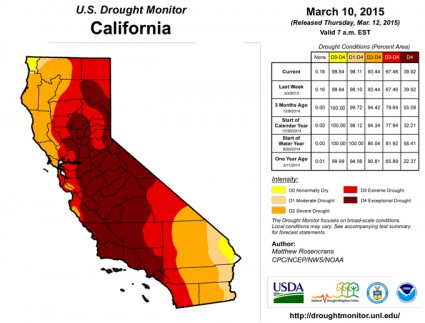

7. Now we have Michael Snyder warn us that California has about 1 year of water left: (Michael Snyder)

8. Italian non performing loans equal to 11.5% of GDP. Italy becoming a basket case.

9. We have our first foreign casualty in the meltdown on Austrian Hypo. The German bank DuesselHyp, with a tiny writedown of 348 million euros goes bell up. Is this foreshadowing a future nightmare when a tiny write off of 1.5% of assets creates a total meltdown of a bank?

we have these and other stories for you tonight.

Let us now head over to the comex and assess trading over there today.

Here are today’s comex results:

The total gold comex open interest fell by a tiny margin of 204 contracts today from 424,435 down to 424,231 as gold was down by $0.50 on Friday (at the comex close). We are now in the contract month of March which saw it’s OI lower to 111 for a loss of 19 contracts. We had 0 notices filed on Friday so we lost 19 contracts or an additional 1900 gold oz will not stand for delivery in this delivery month of March. The next big active delivery month is April and here the OI fell by 3683 contracts down to 213,865. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was poor at 59,201. The confirmed volume on Friday ( which includes the volume during regular business hours + access market sales the previous day) was poor at 141,212 contracts. I wonder what happened to our HFT boys…probably scared off with the lawsuit filed. Today we had 1 notices filed for 100 oz.

And now for the wild silver comex results. Silver OI rose by an extremely high 2,458 contracts from 174,702 up to 177,160 despite the fact that silver was down by 1 cent with respect to Friday’s trading and equally astonishing that the volume on Friday was extremely light. We are now in the active contract month of March and here the OI fell by 39 contracts down to 805. We had 35 contracts served upon on Friday. Thus we lost 4 contracts or an additional 20,000 oz will not stand in this March delivery month. The estimated volume today was simply awful at 12,513 contracts (just comex sales during regular business hours. Something scared our HFT boys today. The confirmed volume on Friday (regular plus access market) came in at 27,478 contracts which is poor in volume. We had 113 notices filed for 565,000 oz today.

March initial standings

March 16.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 45,010.200 oz (Scotia, HSBC) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1 contracts (100 oz) |

| No of oz to be served (notices) | 110 contracts (11,000 oz) |

| Total monthly oz gold served (contracts) so far this month | 6 contracts(600 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 114,790.651 oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

8,511,333.3 oz |

Today, we had 0 dealer transactions

total Dealer withdrawals: nil oz

we had 0 dealer deposit

total dealer deposit: nil oz

we had 2 customer withdrawals (and the farce continues)

i) Out of Scotia: 38,580.000 oz (1200 kilobars)

ii) Out of HSBC: 6,430.200 oz (??? not exactly 200 kilobars)

total customer withdrawal: 45,010.200 oz

we had 0 customer deposits:

total customer deposits; nil oz

We had 0 adjustments

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account.

To calculate the total number of gold ounces standing for the March contract month, we take the total number of notices filed so far for the month (6) x 100 oz or 600 oz , to which we add the difference between the open interest for the front month of March (111) and the number of notices served upon today (1) x 100 oz equals the number of ounces standing.

Thus the initial standings for gold for the March contract month:

No of notices served so far (6) x 100 oz or ounces + {OI for the front month (111) – the number of notices served upon today (1) x 100 oz} = 11,800 oz or.3608 tonnes

we lost 19 contracts or 1900 oz which no doubt were cash settled.

Total dealer inventory: 656,644.474 oz or 20.424 tonnes

Total gold inventory (dealer and customer) = 8.033 million oz. (249.88) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 53.0 tonnes have been net transferred out. However I believe that the gold that enters the gold comex is not real. I cannot see continual additions of strictly kilobars.

end

And now for silver

March silver initial standings

March 16 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | 504,618.650 oz (Brinks,Scotia,Delaware,HSBC,CNT) |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 590,147.200 oz (Scotia) |

| No of oz served (contracts) | 113 contracts (565,000 oz) |

| No of oz to be served (notices) | 692 contracts (3,460,000) |

| Total monthly oz silver served (contracts) | 1883 contracts (9,415,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,176,155.6 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 1 customer deposits:

i) Into Scotia: 590,147.200 oz

total customer deposit: 590,147.200 oz

We had 4 customer withdrawals:

i) Out of Brinks: 7863.15 oz

ii) Out of Scotia: 60,874.400 oz

iii) Out of Delaware: 8,758.300 oz

iv) Out of HSBC: 400142.120 oz

v) Out of CNT: 26,980.68 oz

total withdrawals; 504,618.65 oz

we had 1 adjustment

i) out of CNT: 574,284.88 oz was adjusted out of the customer and this landed into the dealer account of CNT;

Total dealer inventory: 69.433 million oz

Total of all silver inventory (dealer and customer) 176.432 million oz

.

The total number of notices filed today is represented by 113 contracts for 565,000 oz. To calculate the number of silver ounces that will stand for delivery in March, we take the total number of notices filed for the month so far at (1883) x 5,000 oz = 9,415,000 oz to which we add the difference between the open interest for the front month of March (805) and the number of notices served upon today (113) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the March contract month:

1883 (notices served so far) + { OI for front month of March( 805) -number of notices served upon today (113} x 5000 oz = 12,895,000 oz standing for the March contract month.

we lost 4 contracts or an additional 20,000 oz will not stand for delivery in March.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.com orhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

March 16/no change in gold inventory at the GLD/Inventory 750.67 tonnes

March 13/ we had a small change in gold inventory at the GLD (small withdrawal/probably to pay for fees)/Inventory at 750.67 tonnes

March 12.we had a withdrawal of 2.09 tonnes of gold at the GLD/Inventory at 750.95 tonnes

March 11.2015: no changes in gold inventory at the GLD/Inventory at 753.04 tonnes

March 10 no report on the GLD tonight/computer down/inventory remains 753.04 tonnes

March 9/ we had another huge withdrawal of 3.38 tonnes of gold from the GLD, no doubt heading for Shanghai/Inventory 753.04 tonnes

March 6/we had a huge withdrawal of 4.48 tonnes of gold from the GLD/inventory rests tonight at 756.32/Also HSBC is getting out of the gold business in London and is giving up all of its 7 vaults.

March 5 no change in gold inventory at the GLD/760.80 tonnnes

March 4/ no change/inventory 760.80 tonnes

March 3 we had another 2.69 tonnes of gold withdrawn from the GLD. Inventory is now 760.80 tonnes.

March 2 we had 7.76 tonnes of withdrawal from the GLD today and this physical gold landed in Shanghai/Inventory 763.49 tonnes

March 16/2015 / no change from Friday/Inventory at 750.67 tonnes

inventory: 750.67 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 750.67 tonnes.

end

And now for silver (SLV):

March 16/no change in silver inventory/327.332 million oz

March 13.2015: no change in silver inventory/327.332 million oz

March 12: no changes in silver inventory/327.332 million oz

March 11/no changes in silver inventory/327.332 million oz

March 10/ no change in silver inventory/327.332 million oz

March 9/ no change in silver inventory at the SLV/327.332 million oz

March 6: huge addition of 1.34 million oz of silver into the SLV/Inventory 727.332 million oz

March 5 no change in inventory/725.992 million oz

March 4 a slight reduction of 126,000 oz of silver/SLV inventory at 725.992 (probably to pay for fees)

March 3 a small deposit of 328,000 oz of silver into the SLV/Inventory at 726.118 million oz.

March 2/ no change in silver inventory tonight; 725.734 million oz

Feb 27.2015 no change in silver inventory tonight: 725.734 million oz

Feb 26. no change in silver inventory at the SLV/Inventory at 725.734 million oz

Feb 25. no changes in silver inventory/SLV inventory at 725.734 million oz

March 16/2015 no change in silver inventory at the SLV/ SLV inventory rests tonight at 327.332 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now for the first time into the negative to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

Not available tonight

1. Central Fund of Canada: traded at Negative 7.9% percent to NAV in usa funds and Negative 7.9% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.6%

Percentage of fund in silver:37.9%

cash .5%

( March 16/2015)

Sprott gold fund finally rising in NAV

2. Sprott silver fund (PSLV): Premium to NAV rises to + 1.71%!!!!! NAV (March 16/2015)

3. Sprott gold fund (PHYS): premium to NAV rises to +.02% to NAV(March 16 /2015)

Note: Sprott silver trust back into positive territory at +1.26%.

Sprott physical gold trust is back into positive territory at +.02%

Central fund of Canada’s is still in jail.

end

And now for your more important physical gold/silver stories:

Gold and silver trading early this morning

(courtesy Mark O’Byrne)

Irish Finance Minister Dumps Stocks to Buy Gold

– Ireland’s Minister of Finance shifted personal wealth out of stocks and into gold

– Minister invested in SPDR Gold Shares ETF, Portuguese government bonds and other ETFs

– Maintained holdings in bank and agricultural commodities ETFs

– Gold ETF not a safe haven asset – much unappreciated counterparty risk

The Minister for Finance in Ireland, Michael Noonan, sold his shares in funds that track European and US stocks and diversified his portfolio including allocating some of his personal wealth into a gold exchange traded fund (ETF) in 2014.

Noonan sold out of his positions in the Lyxor Eurostoxx 50 ETF and SPDR DJIA ETF in 2014 and opted to invest in the SPDR gold shares ETF and Portuguese government bonds. He maintained his holdings in SPDR KBW Banks ETF, Ishares FTSE 100 ETF, Market Vectors Agri Business ETF, ETFS Agricultural Commodities ETF.

The information was published last week in the Register of Members Interests, in which members of Oireachtas – the Irish Parliament – must declare financial interests valued at over €13,000.

The changes to the Minister’s portfolio were highlighted by Ireland’s Sunday Independent yesterday, who described Noonan as “bearish” and interpreted the move as a “hedge against euro deflation”.

The piece acknowledged that gold is a safe haven – the “traditional hedge against tough times” and that “gold is an asset that has outperformed in times of both inflation and deflation.”

Noonan is believed to be quite a shrewed investor. The Sunday Independent reported that

“Noonan’s personal investments give an insight into his thinking and his views on the risk and opportunities facing the global and European economies and markets. He has a track record stretching back decades of canny private investments.”

The news is of interest given Noonan’s status within the Eurogroup of Finance Ministers, the Council of the European Union and the Ecofin. The Economic and Financial Affairs Council (Ecofin), is composed of the Economics and Finance Ministers of the Member States, generally meets once a month under the chair of the rotating EU Presidency.

Noonan is an EU economic insider and would have access to good information with regards to financial and economic developments in Europe.

Noonan represents Ireland at these meetings and chaired the Council during the first half of 2013. He is committed to the European political project. The political opposition and an angry public have accused him of putting the interests of EU banks and political elites over those of Irish society.

Given Noonan is close to EU elites, it is interesting that he chose to sell his European stocks and his allocation to Eurostoxx. Was the decision made prior to the ECB mooting the possibility of QE? If so it would suggest that Noonan may have been concerned about deflation. And yet the ECB never considered factoring the potential for deflation into its stress tests for banks.

Or was the decision made with knowledge of the ECB’s intention? If this were so it would indicate a lack of faith by a European finance minister in the ability of the ECB to achieve its stated objectives, given that QE should raise European stock markets.

Unfortunately, the Register of Members Interests does not detail the timeline of investments or their relative value so it is difficult to speculate whether the minister dumped his stock market investments prior to buying the gold ETF.

Noonan also bought Portugal 4.35% October 2017 government bonds. This either suggests that he has more confidence in the economic outlook for Portugal than for Ireland or more likely it is a form of diversification.

He continues to hold SPDR KBW US Banks ETF – which tracks US banks, iShares FTSE 100 ETF, Market Vectors Agribusiness ETF and ETFS Agricultural Commodities ETF.

Whatever the motivation of a European finance minister to buy into a gold ETF – which, incidentally, is not the same as owning physical gold as it carries significant counterparty risk – it represents a significant shift in attitude toward gold.

It also demonstrates that the recovery narrative is not one that the Minister appears to have much faith in. Noonan is prudently hedging his bets in this regard.

We advise readers and clients to do as the Minister has done and prudently hedge the many risks of today by diversifying into gold – not paper gold but physical gold. The gold ETF is not a safe haven asset rather it is a derivative that tracks the price of gold and in which one does not have legal title to or own the underlying asset.

Download: Comprehensive Guide To Investing In Gold

MARKET UPDATE

Today’s AM fix was USD 1,157.00, EUR 1,097.67 and GBP 782.13 per ounce.

Friday’s AM fix was USD 1,156.50, EUR 1,091.24 and GBP 779.58 per ounce.

Gold climbed 0.17% percent or $1.90 and closed at $1,155.20 an ounce Friday, while silver remained unchanged at $15.57 an ounce. Gold and silver both traded down for the week at 0.90 percent and 1.89 percent.

In Singapore, bullion for immediate delivery ticked lower and then higher and was up 0.3 percent to $1,162.50 an ounce near the end of day trading.

Gold hovered at its lowest in nearly three months today pressured by the still strong U.S. dollar. The two day U.S. Federal Reserve policy meeting starting Tuesday, may hint at the timing of any hike in U.S. interest rates.

Bearish sentiment continued as holdings in SPDR Gold Trust, the world’s largest gold-backed exchange-traded fund, fell to 750.67 tonnes down 0.28 tonnes on Friday – the lowest since late January.

Asians continue to buy physical bullion on dips in price and premiums on the Shanghai Gold Exchange were about $5-$6 an ounce above the global benchmark, even stronger than Friday’s premiums.

In Ireland, in late morning trading gold is trading at $1,157.03 or off 0.09 percent. Silver is at $15.64 or up 0.15 percent and platinum is $1,115.32 or up 0.03 percent

end

During the first week of March a huge 45 tonnes of gold was demanded in China. This gold leaves the SGE vaults and with the expert analysis of Koos Jansen, equals gold demand in China. We would also like to point out that this gold demanded excludes any sovereign gold purchases from mainland China. We are on tap for demand of 550 tonnes this quarter. By talking mining and scrap away from the figures, China imported 340 tonnes of gold which is huge.

The 45 tonnes of gold demanded by China works out to 6.4 tonnes of gold.The world produces 6.02 tonnes of gold ex China ex Russia. Thus these guys are purchasing over 100% of annual global production.

(I subtract out China and Russia gold production because no gold is allowed to leave their respective countries)

(courtesy Koos Jansen)

SGE Withdrawals 45t Week 9, YTD 456t

Chinese wholesale gold demand, that equals withdrawals from the vaults of the Shanghai Gold Exchange (SGE),accounted for 45 metric tonnes in week 9 of 2015 (March 2 – 6). Year to date 456 tonnes have been withdrawn from the SGE vaults. An estimate suggests 340 tonnes has been net imported into the Chinese domestic gold marketover this period (calculating with a yearly SGE scrap rate of 250 tonnes).

Since the inception of the Shanghai International Gold Exchange (SGEI) there was a possibility the significance of SGE withdrawals, as published in the Chinese weekly reports, became distorted by activity on the SGEI – in the Free Trade Zone. That’s why I corrected SGE withdrawals by trading volume from the SGEI, just to be on the safe side of measuring Chinese wholesale demand.

However, we just learned that what was traded and withdrawn on the SGEI in 2014 was primarily imported into the Chinese domestic gold market. So, for the time being we can assume SGE withdrawals are still an accurate proxy for Chinese wholesale demand – a metric described in this post.

I like to note SGEI trading volume has jumped recently, reaching a record in week 9 at 34 tonnes (counted unilaterally). Perhaps this is exchange is slowly coming to life.

Only the 1kg physical contract iAu99.99 is traded on the International Board (SGEI), there seems to be nil interest in the 100 gram physical contract iAu100 and in the 12.5kg (London Good Delivery bars) contract iAu995.

Overall SGE volume is somewhat dropping as the spot deferred contracts Au(T+N1) and Au(T+N2) are falling back after a resurrection that started late November 2014.

On the Shanghai Futures Exchange (SHFE) we can see the same trend; slightly dropping volumes. Nothing “worth mentioning”.

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

end

Chris Powell comments on the above Koos Jansen story.

Chris uses 2800 tonnes per year of annual production which includes Russia and China.

(courtesy Chris Powell/GATA)

China seems to be claiming 88 percent of world gold mine production

11:31a ICT Sunday, March 15, 2015

Dear Friend of GATA and Gold:

Bullion Star market analyst and GATA consultant Koos Jansen reports today that the international division of the Shanghai Gold Exchange is not moving gold out of China but rather supplementing the country’s gold imports. As a result, Jansen writes, withdrawals from the Shanghai Gold Exchange remain a good proxy for China’s domestic gold demand, and 456 tonnes have been withdrawn this year through March 6.

If annual gold mine production is around 2,800 tonnes and monthly mine production averages 233 tonnes and weekly production averages 54 tonnes, the Shanghai figures suggest that, as Jansen’s chart shows, Chinese demand is running at about 47 tonnes per week, or about 88 percent of world mine production.

Of course gold possession is not static; the metal doesn’t disappear but rather is always available to the market at the right price. People and institutions throughout the world may be selling even as China may be buying. But that a single nation has started to buy so much relative to mine production suggests that inventories elsewhere are getting drawn down.

The obvious place to look for such inventories would be those central banks that purport to be major gold holders and that may be swapping and leasing gold for currency market management purposes:

http://www.gata.org/node/12016

Fortunately for those central banks, the first principle of gold market analysis by mainstream financial news organizations and financial letter writers is never to put a critical question to the biggest participants in the market even though those participants are governments that might owe some accountability to the people they govern.

That is, the mainstream offers no serious gold market analysis at all, just interpretation of the holograms that are disguised as market prices.

Jansen’s report is posted at Bullion Star here:

https://www.bullionstar.com/blogs/koos-jansen/sge-withdrawals-45t-week-9…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Nothing but kickback money to the USA government:

(courtesy GATA/Bloomberg)

U.S. seeks billions from global banks in currency manipulation settlement

That is: Nobody rigs our markets but us.

* * *

By Keri Geiger and Greg Farrell

Bloomberg News

Friday, March 13, 2015

NEW YORK — The U.S. Justice Department is seeking about $1 billion each from global banks being investigated for manipulation of currency markets, according to two people familiar with the talks.

The figure is a starting point in settlement discussions, with some banks being asked for more and some less than $1 billion. One bank that has cooperated from the beginning is expected to pay far less, one of the people said. Penalties of about $4 billion are on the table, according to one of the people, though the number could change markedly.

Banks are pushing back harder than in some previous negotiations, including those for mortgage-backed securities, and the final penalties could be lower, people close to the talks said. …

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2015-03-13/u-s-said-to-start-at-1…

end

unbelievable!!

(courtesy zero hedge)

ICE Futures Broke Law “Thousands” Of Times In 20 Months, CFTC Fines Exchange 0.75% Of 2015 Revenues

From October 2012 to May 2014, the CFTC found that ICE Futures exchange submitted reports and data containing errors and omissions on every reporting day, with cumulative inaccuracies totaling in the thousands. The CFTC stated unequivocally that, those “who fail to meet their reporting obligations will be held accountable,” and required ICE to pay a $3 million civil monetary penalty. With expectations of over $4 billion in revenues for FY 2015, the $3 million fine represents just 0.75% of the exchange’s income… that will teach them!!!

Full CFTC Statement:

CFTC Orders ICE Futures U.S., Inc. to Pay a $3 Million Civil Monetary Penalty for Recurring Data Reporting Violations

The U.S. Commodity Futures Trading Commission (CFTC) today issued an Order filing and simultaneously settling charges against ICE Futures U.S., Inc. (ICE), a designated contract market (DCM), forsubmitting inaccurate and incomplete reports and data to the CFTC over at least a 20-month period, from at least October 2012 through at least May 2014.

According to the CFTC Order, on every reporting day during the period above, ICE submitted reports and data containing errors and omissions, with cumulative inaccuracies totaling in the thousands.The Order further finds that CFTC staff repeatedly notified ICE of the problems with its reports and data and requested that ICE take action to correct the mistakes, but that ICE continued to submit inaccurate reports and data. The Order requires ICE to pay a $3 million civil monetary penalty and to comply with undertakings aimed at improving its regulatory reporting.

CFTC Director of Enforcement Aitan Goelman commented: “The CFTC cannot carry out its vital mission of protecting market participants and ensuring market integrity without correct and complete reporting by registrants, including DCMs. Today’s action makes clear that registrants who fail to meet their reporting obligations will be held accountable and that the CFTC takes a particularly dim view of reporting violations that continue over many months, especially after CFTC staff has repeatedly alerted the registrant in question to the problems in its reporting.”

Pursuant to Part 16 of the CFTC Regulations, a DCM is required to submit certain trading and market-related reports and data to the CFTC. In particular, a DCM is required to submit, for each business day, clearing member reports showing certain information for each future or option contract, including, among other things, the quantity of contracts currently open, the quantity of contracts bought and sold throughout the day, and the quantity of delivery notices. A DCM is also required to provide the CFTC with permanent record data relating to trading volume, open contracts, prices, and certain critical dates, and transaction-level trade data and related order information for each futures or options contract.

The Order specifically finds that, beginning in at least October 2012, CFTC staff notified ICE about its data and reporting errors, which included incorrect clearing member reports, permanent record data, and transaction-level trade data. ICE responded that these errors resulted primarily from technology upgrades and data migration projects, and while they affected data provided to the CFTC, they did not affect data published by ICE on its website. ICE further assured CFTC staff that its data-reporting problems would be fixed with the conversion to a new data-reporting format. CFTC staff informed ICE that continuing to report faulty data in the interim was unacceptable. Nevertheless, ICE continued to submit inaccurate and incomplete reports.

Further, ICE did not respond in a timely and satisfactory manner to inquiries from CFTC staff from multiple divisions about these data-reporting issues, including initial inquiries from the Division of Enforcement. Eventually, ICE did cooperate fully with the investigation and took effective corrective actions to address its reporting deficiencies. The CFTC has taken that cooperation and those actions into account in settling this matter.

In addition to imposing the $3 million civil monetary penalty, the CFTC ordered ICE to comply with undertakings to improve its regulatory reporting. For instance, ICE must create and maintain a new senior position of Chief Data Officer, who will have direct responsibility for systems and procedures relating to regulatory reporting, and ICE must hire and maintain at least three additional quality assurance staff who will be dedicated to regulatory reporting. ICE also must undertake certain data-reconciliation efforts, including reviewing certain prior data submissions to the CFTC to identify further violations of the charged CFTC Regulations and, beginning 120 days from the date of the Order, endeavoring to reconcile data provided to the CFTC with data published on its website, as well as with other data existing within ICE’s systems and its clearing providers’ systems. Additionally, ICE must correct any errors or omissions in data provided to the CFTC pursuant to Part 16 of the CFTC Regulations within one week of discovery or notification of the errors or omissions, or, in the event such corrections will take more than a week’s time, reporting to the CFTC why additional time will be necessary.

The CFTC Division of Enforcement staff members responsible for this matter are Margaret Aisenbrey, Allison Sizemore, Jeff Le Riche, and Charles Marvine, with assistance from the CFTC Division of Market Oversight staff Kelly Beck, Matthew Hunter, Harry Hild, and Anthony Saldukas and the CFTC Office of Data and Technology staff Regina Sanders, Margie Sweet, Rene Garcia, and Ed Wehner.

* * *

And don’t do it again…

China Sells U.S. Treasuries, Yields Collapse…. China Buys Gold, Prices Collapse…. “Markets” At Work??

(By Chris Hamilton)

China, the largest buyer of US Treasury’s ceases buying Treasury’s…and US Treasury yields collapse?!? The Chinese (and others) buy record amounts of gold and create an imbalance of demand over available supply…and prices collapse?!? These are clearly not the actions of a market attempting to find a balance between price, supply, and demand.

July ’11 to December of ’14, China decreased its holdings of US Treasury debt by $71 Billion (according to the most recent TIC data)…while China continued to run record trade surplus’ with the US. China took in excess of a trillion new dollars since August of 2011 through 2014 and simultaneously sold or rolled off $71 Billion in US Treasury holdings…so China had to find a home for nearly $1.1 trillion new dollars. The chart below highlights China’s annual trade surplus with the US, annual Treasury purchases, and total Treasury holdings.

(Source: US Census, Trade, Source, Treasury, TIC report)

From ’00 to ’11, China had (on average) recycled 50% of its trade surplus dollar reserves into Treasury’s. However, as noted above, China has been a net seller since July ’11…why is this date important? It was the month of the US debt ceiling fiasco…and the date when China’s purported gold purchase binge began. It’s also August ’11 that gold hit its peak price and has fallen since. I don’t think these happenings were a coincidence.

Since we know China didn’t buy Treasurys over this period, perhaps we should speculate what those new dollars would do if focused on gold purchases?!? If China rotated the 50% of surplus dollars it had been utilizing to buy Treasurys and instead bought Gold…at an average of say $1500 an ounce since August ’11…that would buy China 10,000 tons of gold by year end 2014. Hmmm…Implications abound.

According to the World Gold Council (WGC), China’s gold demand rose from 300 metric tons up to 1300 metric tons in 2013 and about 1200/mt as of 2014. This is important as WGC reporting nets all newly produced global mine supply, global recycled scrap, and (based on the above WGC data on Chinese demand) denotes that the gold market is in balance between global supply and global demand. However, based on the data from the Shanghai Gold Exchange (SGE), the central clearing house for all Chinese gold purchasing, China’s demand is far greater (the chart below highlights the discrepancy). But if the data from SGE is correct, then where did all the additional gold come from and why did the price collapse on record demand? The answer is almost certainly, the gold was imported from someone else’s inventories willing to sell something of great value at low prices. But according to the SGE data, the Chinese demand was about 2,700 metric tons greater than global available WGC available supply since July 2011 (3.5 years) or about 771 tons annually. In the prior 3.5 years, the WGC and SGE had only diverged by about 600 metric tons or a 171 ton differential annually. So, China had massive dollar reserves not utilized to buy Treasury’s and someone sold a lot of gold to China and in the process drew down their own inventories as the demand was far greater than mining supply!

Who would have this massive amount of gold in inventory (and willingly sell it at significantly lower prices) and why would the price of gold collapse on this clear imbalance in demand over supply? Most sources of potential inventory are audited on a regular basis and this draw-down would be quite noticeable. Of course, the greatest source of gold holdings are collectively held by the Federal Reserve and the US Federal government…and this is not openly audited.

Some questions spring to mind!

From ’08-’09, could China and the US agreed to perform the thousands of years old activity of recycling excess currency, officially purchasing US Treasurys, but quietly and in secret being paid in some sort of gold arrangement? This would certainly serve both parties nicely allowing US deficit spending in an economic downturn without spiking interest rates. China for it’s part would continue its export driven economic miracle.

- China increased its holdings of US Treasury debt from $65 billion in ’00 to $1,315 billion ($1.3 Trillion) in July of ’11…and in particular, from ’08 to July ’11, China increased its Treasury holdings by $588 billion while the US ran massive budget deficits flooding the Treasury market with new supply…and China’s trade surplus with the US ebbed on lower US consumer demand during the ’08 through ’11 economic slowdown (said more plainly, China bought more when they had less with which to make those purchases).

Since July ’11 China has net sold $71 billion in US Treasury debt on record dollar trade surplus in excess of a trillion dollars.

- China as of July ’11 suddenly changed course with their dollar surplus even as their trade surplus with the US reached new records annually over ’12-’14? Did China suddenly decide gold was valuable and begin buying in the open market? My guess is China believed gold was of value all along but once the gold was no longer available (perhaps the US ran out or simply determined, like Nixon in ’71 (who watched almost 60% of US gold depart in the prior decade) that closing the gold arrangement, was essential to save whatever gold reserves the US had left).

Put it all together…China, the largest buyer of US Treasury’s ceases buying Treasury’s…and US Treasury yields collapse?!? The Chinese (and others) buy record amounts of gold and create an imbalance of demand over available supply…and prices collapse?!? These are clearly not the actions of a market attempting to find a balance between price, supply, and demand.

Of course I can’t prove that China did purchase any amount of gold. The Chinese authorities haven’t made any updates since 2009 when they last made public a 600 ton increase (to their then official holdings of 454 tons) to the current official Chinese gold reserve of 1054.1 tons. What I can say is Russia, which likewise has a large dollar trade surplus and likewise to China has been reducing its Treasury exposure since August of 2011…has been busily and openly adding to its gold reserves, now up to 1153.3 tons. Then again, I (nor the US government?) can’t prove the US truly has 8133.5 tons. Or the Germans 3384.2 tons or Italians 2451.8 tons. Still waiting on those open and transparent audits.

All I can say is the above math regarding China’s dollar hoard would nicely support what is visible in the chart below and also support those that claim Chinese gold buying and gold reserves are far larger than advertised.

This article was written by Chris Hamilton at the econimica.blogspot.com.

Please check back for new articles and updates at the SRSrocco Report.

(courtesy Bill Holter/Miles Franklin)

And now for the important paper stories for today:

Early Monday morning trading from Europe/Asia

1. Stocks generally higher on major Chinese bourses (India, Japan and Australia lower)/yen rises to 121.27

1b Chinese yuan vs USA dollar/yuan weakens to 6.2625

2 Nikkei down 8.19 or 0.04%

3. Europe stocks in the green/USA dollar index down to 99.89/Euro rises to 1.0533

3b Japan 10 year bond yield .42% (Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 121.27/

3c Nikkei still above 19,000

3d USA/Yen rate now above 121 barrier this morning

3e WTI 44.34 Brent 54.00

3f Gold up/Yen slightly up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for both WTI and Brent this morning.

3i European bond buying continues to push yields lower on all fronts in the EMU

Except Greece which sees its 2 year rate rise to 19.55%/Greek stocks down again by .35% today/expect continual bank runs on Greek banks.

3j Greek 10 year bond yield: 10.78% (down slightly by 5 basis points in yield)

Greece made another payment of 568 million euros raiding their pension fund.

3k Gold at 1157.00 dollars/silver $15.65

3l USA vs Russian rouble; (Russian rouble down 1 3/4 rouble/dollar in value) 62.29

3m oil into the 44 dollar handle for WTI and 54 handle for Brent

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This scan spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF

3p Britain’s serious fraud squad investigating the Bank of England

3r the 7 year German bund still is in negative territory/no doubt the ECB will have trouble meeting its quota of purchases and thus European QE will be a total failure.

3s Russian troops on full exercise/

3t Riots in Brazil

3u World awaits the USA Fed decision on “patience” to see if wording is removed

4. USA 10 year treasury bond at 2.09% early this morning. Thirty year rate well below 3% at 2.67/yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

Futures Rebound After EUR Finds 1.05 Support; China Stocks Soar; Im-“Patient” Fed On Deck

It started off as the perfect storm for futures: after Sunday night’s latest plunge in WTI, which saw it drop to the lowest price since Lehman, the double whammy that has now forced Deutsche Bank to become the first major institution to forecast no growth for S&P500 EPS in 2015, namely the strong dollar, reared its ugly head and the EURUSD seemed dangerouly close to breaching the all important 1.04-1.05 support level we first noted last week. However, overnight parties tasked with preserving “financial stability” appear to have once again stepped in, and not only has the EURUSD rebounded off 1.05, but crude is now just barely down from the Friday close as all firepower is put to the same use, that sent the Shanghai Composite soaring by 2.3% overnight, and which sent the Dax over 12,000 for the first time ever.

In actual news, the collapse of Austria’s Heta bad bank has claimed its first German casualty, Duesseldorfer Hypothekenbank, which would be bailed out by the German depositor protection agency, while moments ago the question whether Greek pensions would be plundered even more was answered affirmatively, when a Greek finance ministry official announced that Greece made a €584m repayment due to IMF.

But the main event this week will be none other than the FOMC’s announcement on Wednesday when every algo will be programmed to scan the prepared text whether the word “patient” is present. As DB notes, “this week will be all about whether the Fed’s bark is worse than its bite as the conclusion of the 2-day March FOMC takes centre stage on Wednesday. It seems increasingly likely that they’ll remove ‘patient’ in order to give them increased flexibility but they’ll probably want to stress data dependency as to if and when they raise rates. Perhaps the Fed’s updated economic and financial projections will give us clues as to how likely a June rate hike might be. The dots will probably also garnish much attention both for the near-term dots and those that venture into 2016 and 2017. Overall as employment has seemingly met the criteria for lift off, much depends on how they see inflation and perhaps the dollar. These are currently good reasons to stay cautious with regards to hikes but how much will the Fed acknowledge them. We mentioned on Friday that headline CPI could be -0.43% come June and as regular readers will be aware we’re still not convinced they’ll be able to pull the trigger in 2015 even if they clearly expect and want to. Whatever happens, there should be plenty of inflation and dollar related questions in the press conference.”

Should the Fed no longer be patient, expect the relentless strengthening move USD to resume for yet another parabolic thrust higher, assuring that S&P earnings post their first Y/Y decline since 2011.

Back to stocks, European equities have started the week on the front-foot, with the DAX breaking above 12,000 for the first time on record, albeit amid light macro newsflow. Gains for Europe have primarily been led by stock specific news with positive sentiment overnight, particularly in Asia also helping to prop up equities. More specifically, overnight the Shanghai Composite closed higher by 2.26% following comments from Chinese Premier Li who pledged to prop up the economy if growth was at risk of breaching a lower limit. Other than that, with a pretty light calendar for Europe, price action has been relatively muted with Bunds lower alongside the strength in stocks and USTs subsequently coming off their best levels seen overnight. In terms of the latest updates for Greece, A government source has stated that Greece will pay EUR 580mln tranche of its IMF loan due today.

One thing to be aware of is that Russian President Putin has ordered his troops to be on full alert today, according to Interfax. However, reports suggest that this is linked to continued drills in the country similar to what we saw last week.

In FX markets, the USD-index has yet again been the main driving force with participants using today’s subdued session as an opportunity to book profits from last week’s steep gains and ahead of Wednesday’s FOMC meeting. As such, the USD-index has broken below 100.00, much to the benefit of its major counterparts, subsequently lifting EUR/USD back above 1.0500.

In commodity markets, both Brent and WTI crude futures trade lower, albeit off their worst levels after falling by nearly 3% overnight on heavy trading volumes to touch their lowest intra-day level since March 2009. This followed last week’s sharp declines as the IEA indicated that they expect the global glut in oil to worsen, coupled with revival of the USD strength. Elsewhere, precious metal markets remain rangebound, while iron ore futures declined overnight with prices remaining near record lows as sentiment in China’s steel sector remains weak. Goldman Sachs lowers its US oil-production growth forecast to 230k bpd vs. Prev. 290k bpd Y/Y by Q4.

In summary: European shares rise close to intraday highs with the autos and financial services sectors outperforming and construction, utilities underperforming. WTI crude falls to lowest since 2009, euro strengthens from 12-year low vs dollar. German DAX index rises above 12,000 for first time. The Italian and Dutch markets are the best-performing larger bourses, Swiss the worst. The euro is stronger against the dollar. German 10yr bond yields rise; French yields increase. Commodities decline, with Brent crude, WTI crude underperforming and copper outperforming. U.S. Empire manufacturing, NAHB housing market index, industrial production, capacity utilization due later.

Market Wrap

- S&P 500 futures up 0.4% to 2050.4

- Stoxx 600 up 0.6% to 399.1

US 10Yr yield down 1bps to 2.1% - German 10Yr yield up 2bps to 0.28%

- MSCI Asia Pacific down 0.2% to 143.7

- Gold spot little changed at $1158.1/oz

- Eurostoxx 50 +0.8%, FTSE 100 +0.5%, CAC 40 +0.7%, DAX +1%, IBEX +0.6%, FTSEMIB +1.1%, SMI +0.3%

- Asian stocks fall with the Shanghai Composite outperforming and the ASX underperforming.

- MSCI Asia Pacific down 0.2% to 143.7, Nikkei 225 down 0%, Hang Seng up 0.5%, Kospi up 0.1%, Shanghai Composite up 2.3%, ASX down 0.3%, Sensex down 0.2%

- Euro up 0.33% to $1.0531

- Dollar Index down 0.4% to 99.93

- Italian 10Yr yield down 0bps to 1.15%

- Spanish 10Yr yield up 1bps to 1.16%

- French 10Yr yield up 1bps to 0.51%

- S&P GSCI Index down 0.4% to 391.7

- Brent Futures down 1.1% to $54.1/bbl, WTI Futures down 1.1% to $44.4/bbl

- LME 3m Copper up 0.4% to $5882.5/MT

- LME 3m Nickel up 0.4% to $14185/MT

- Wheat futures down 0.3% to 500.3 USd/bu

Bulletin Headline Summary

- Stock specific news and a strong close in China has seen the DAX break above 12,000 for the first time, with newsflow otherwise light

- The USD-index has moved back below 100.00 following profit-taking, subsequently leading EUR/USD back above 1.0500

- Looking ahead, today sees the release of US Empire Manufacturing and Industrial Production, as well as potential comments from ECB’s Draghi, Costa, Praet and Lautenchlaeger.

- Treasuries 7Y and longer gain, extending last week’s rally, as market participants await Fed statement, updated Summary of Economic Projections and Yellen press conference on Wednesday.

- Fed seen dropping “patient” from statement, moving closer to eventual increase in fed funds rate, analysts said

- Chinese policy makers will take action if China’s growth, which the government targeted at about 7% this year, drifts toward the lower limit of its range and cuts into employment or wages, Premier Li Keqiang said

- Greece is due to make its next repayment to the IMF Monday, further depleting cash reserves that risk running out this month unless a deal is reached with European partners

- 52% of Germans no longer want Greece to remain in the euro; 80% of Germans believe Greece “isn’t behaving seriously toward its European partners”: poll by public broadcaster ZDF

- Duesseldorfer Hypothekenbank AG, a covered bond issuer bailed out by Germany’s deposit protection fund in 2008, is set to be rescued a second time as the country’s banks attempt to limit contagion from Austria’s decision to inflict losses on bondholders of Heta Asset Resolution AG

- Putin ordered troops placed on full combat readiness in snap drills in western Russia, as Defense Minister Sergei Shoigu warned the country was facing new threats to its security

- Brazil’s government will present a package of anti- corruption measures after more than 1 million people, some of them calling for President Dilma Rousseff’s impeachment, took to the nation’s streets Sunday

- Sovereign 10Y yields mixed. Asian stocks mixed, European stocks and U.S. equity-index futures gain. Crude lower, gold little changed, copper higher

DB’s Jim Reid concludes the weekend event recap

The weather impact on data also continues to complicate the story and this has helped push negative US data surprises to their worst level in 6 years. The dollar might not be helping the data either and it’s interesting that David Bianco, our US equity strategist, again cut his S&P 500 EPS over the weekend from $120 to $118 due to the Dollar strength. This makes YoY numbers pretty much flat. So if correct this does make it difficult for US equities to get much momentum without a re-rating. This is tough in a world without Fed QE. So given continued ECB QE and help from a lower Euro we still think the Euro equities vs. US equity trade is still very much alive. The biggest concern is that this is becoming more consensus, however while inflows have stepped up in 2015, on a 12-month basis European equities have still seen outflows where US equities have seen sizeable inflows. So if the macro trends remain intact this trade should continue

Aside from the build up to this week’s FOMC, news flow was reasonably light over the weekend. One story that has generated some headlines this morning however is out of China where Premier Li Keqiang has suggested that the country will intervene should economic growth be at risk of breaching a ‘lower limit’. Specifically, Li was quoted on Bloomberg as saying that ‘the good news is that in the past couple of years we did not resort to massive stimulus measures for economic growth’ and ‘that has made it possible for us to have fairly ample room to exercise macro-economic regulation, and we still have a host of policy instruments at our disposal’. In terms of the market reaction, equity markets in China have bounced on the talks with both the Shanghai Composite (+1.92%) and CSI 300 (+2.03%) higher as we type. The former is in fact at its highest level since August 2009. It’s a generally positive tone across the Asia region with the Nikkei (+0.13%), Hang Seng (+0.40%) and Kospi (+0.24%) all firmer.

Recapping the price action on Friday, it continues to be a similar theme in the US as the Dollar extended gains and equity markets weakened and decoupled from Europe. The S&P 500 finished down 0.61% at the close to mark its third consecutive weekly decline – the second such occurrence this year already and which takes it back into negative territory YTD (-0.27%). There appears to be little let up for the Dollar however with the DXY finishing the day +0.90% and at the highest level since April 2003. This included a 1.31% gain versus the Euro to break $1.05 and finish at $1.0496. Treasuries on the other hand were subdued with benchmark 10y yields more or less unchanged at 2.114%.

Macro data on Friday was on the soft side. PPI in particular was a notable miss with the both the energy related headline (-0.6% yoy vs. 0.0% expected) and core (ex. food and energy) print (+1.0% yoy vs. 1.6% expected) surprising to the downside. The preliminary March reading for the University of Michigan consumer sentiment was a significant miss also. The 91.2 reading was down 4.2pts from the previous print to mark the lowest level since November last year, supported by both a fall in the current conditions and expectations indices. The reading did however reveal a slight uptick in inflation expectations at both the 1y and 5-10y ranges.

Oil was once again generating headlines as both WTI (-4.70%) and Brent (-4.22%) declined to $44.84/bbl and $54.67/bbl respectively. Both markets have declined around a percent further in trading this morning with WTI at one point trading at its lowest intraday level since March 2009. The latest leg down appears to be as a result of a report from the IEA that higher US inventories ‘would inevitably lead to renewed price weakness’. The agency also cited that the appearance of any price stability was a ‘façade’ and that the ‘rebalancing triggered by the price collapse has yet to run its course, and it might be overly optimistic to expect it to proceed smoothly’.

Over in Europe meanwhile, the QE momentum train continued with the Stoxx 600 (+0.32%), DAX (+0.87%) and CAC (+0.46%) all finishing firmer whilst Xover closed 2.5bps tighter. It was more of a subdued day for peripheral sovereign bonds with 10y yields in Spain (+0.3bps) and Italy (+2.1bps) a touch weaker although yields in Portugal (-1.7bps) continued their downward trend to mark a fresh record low at 1.56%. Bunds were a touch softer (+1bp) at 0.256%. The first week of ECB QE has certainly made its mark in terms of price action however. The Stoxx 600 (+0.62%), DAX (+3.04%) and CAC (+0.93%) have all strengthened, 10y yields in Germany (-14bps), Spain (-15bps), Portugal (-20bps) and Italy (-17bps) are all lower and the Euro is some 3% weaker versus the Dollar.

Indeed, Italian finance minister Padoan has so far deemed the programme a success with the weaker Euro in particular being in line with the Euro-area’s long term economic outlook. Greek finance minister Varoufakis appears to have taken a slightly different stance thus far however. Specifically, Varoufakis was reported on Reuters as saying that the programme will fuel an unsustainable stock market rally and is unlikely to boost euro zone investments. In terms of the latest on Greece meanwhile, both Varoukais and PM Tsipras were reported in the weekend press saying that the nation is not facing a cash shortage. Specifically, Tsipras was reported on Ekathimerini as saying that ‘there is absolutely no problem with liquidity’. The comments come ahead of the latest funding requirements this week where the government will be required to refinance €1.6bn of T-Bills and repay over €900m in IMF payments.

Taking a look at this week’s calendar, it’s a quiet start in both the Asia and European time zones with no data releases of note although the ECB’s Draghi and Lautenschlaeger are due to speak this morning in Frankfurt and the EU foreign ministers are due to meet in Brussels. Over in the US this afternoon, we’ve got the industrial and manufacturing production prints, March reading for empire manufacturing and also the capacity utilization reading for February. The calendar picks up a bit tomorrow and we start in Japan with the BoJ monetary policy meeting which are becoming interesting given some hints of policy tensions in the council. Focus in Europe will be on the final February CPI readings for the Euro-area as well as the ZEW survey out of both the Euro-area and Germany. Employment data out of the Euro-area is also due on Tuesday morning. The main focus however will of course be the start of the FOMC meeting in the US on Tuesday. Data prints in the US on Tuesday include the February housing starts and building permits. We kick off Wednesday with trade data out of Japan. Closer to home, the (pre-election) Budget, BoE minutes and various employment indicators in the UK will be a big focus, whilst trade data for the Euro-area rounds off the prints in the morning. The conclusion of the FOMC will of course be the key event for markets along with the associated Yellen press-conference shortly after. There is little in the way of releases for Europe and Asia on Thursday with focus instead on the US where we get trade data, jobless claims, the leading index and the Philadelphia Fed business outlook. We finish the week on Friday with PPI due for Germany, and net borrowing data due out of the UK. Its quiet data-wise in the US on Friday with no releases due however we’ll keep an eye on the Fed’s Evans and Lockhart who are both due to separately speak on monetary policy.

end

When you mock ECB’s Draghi, you know the game is up:

(courtesy zero hedge)

When Even Varoufakis Mocks The QE “Wizard”, The Game Is Almost Up

Last Wednesday, Mario Draghi and ECB chief economist Peter Praet had a clear message for critics of PSPP: we’ll keep printing money forever if we have to, but in the end, this is going to work. As skepticism grows regarding not only the soundness of the philosophy that underpins QE, but about whether the structure of the ECB’s asset purchase program is even viable, the central bank remains defiant to the end and indeed Praet doubled down on the rhetoric last week, noting that the ECB would “use all tools available” to ensure that “monetary dominance prevails.”

That kind of language may be good for morale in some circles, but a growing number of critics are suggesting that perhaps the world would be better off in terms of financial stability if the powers behind “monetary dominance” would let the market prevail for once so that some semblance of price discovery could begin to reassert itself. We’re a long way from that though and in fact, the outlook for euro money markets is anything but normal as Barclays made very clear last week. Here is our summaryof their take on the market:

In a nutshell: short-end core paper will trade below -0.20%, extreme supply/demand imbalances will cause general collateral rates to trade through the depo rate, money market fund yields will turn decisively negative testing investor patience, and central banks had better make good on promises to make some of their inventory available for lending or risk impairing the functioning of the repo market (never a good idea)…

What should be clear from the above is that while central banks’ ability to alter inflation expectations and/or stimulate aggregate demand may be limited, their ability to distort markets, inhibit price discovery, and create systemic risk is alive and well.

Meanwhile, the bund curve has a date with outright flatness and the ECB, by driving yields on even half-decent credits negative, is setting itself up to onboard hundreds of billions in negative yielding assets onto its balance sheet, guaranteeing a loss if held to maturity and we won’t even begin to speculate on what the paper losses will look like on a trillion euro portfolio of bonds purchased at 124% of par if either the central bank loses control of the narrative or some tail event (like a Grexit, or a Podemos-inspired Spexit) triggers a repricing of periphery risk.

In sum: the world’s central banks are playing a trillion dollar/euro/yen/soon-to-be-yuan game of poker where every player at the table is pot committed and has no choice but to go all in.

If you want to understand just how precarious the situation is, just ask Greek FinMin Yanis Varoufakis, a man who knows something about how to create and aggravate precarious situations:

“I find it hard to understand how the broadening of the monetary base in our fragmented and fragmenting monetary union will transform itself into a substantial increase in productive investments. The result of this is going to be an equity run boost that will prove unsustainable.”

The irony there is that Greece could definitely use some help in the way of outside demand for its sovereign debt and by criticizing QE, the FinMin is essentially shooting himself in the foot. Varoufakis — apparently not wanting to ruin his newly minted image as a man who is loving life right now — did note that he wasn’t trying play the role of the “party pooper” (he actually said that). We, however, will play that role by pointing out that Varoufakis is exactly right when it comes to runaway QE producing unsustainable equity rallies as evidenced by the following:

Since 2010, The Bank of Japan has ‘openly’ – no conspiracy theory here – been a buyer of Japanese stock ETFs. Their bravado increased as the years passed and Abe pressured them from their independence to ‘show’ that his policies were working to the point that in September 2014, The BoJ bought a record amount of Japanese stock ETFs taking its holdings to over 1.5% of the entire market cap, surpassing Nippon Life as the largest individual holder of Japanese stocks. However, as WSJ reports, The BoJ has now gone full intervention-tard – buying Japanese stocks on 76% of the days when the market opened lower.

It’s so simple and obvious, even a Greek FinMin can figure it out.

And so can the Financial Times, where columnists are beginning to write about ECB asset purchases with a not-imperceptible hint of disdain in their voices:

The advent of negative yields for the best European government or corporate issuers is usually reported in the media as some sort of curiosity, like a bright object in the night sky that seems to be getting bigger. What it really represents is the breakdown of the policy world’s response to the global financial crisis.

A large European bank’s credit strategist told me: “We have searched through the records, and asked the ECB how they think their (asset purchase strategy) will work, and there is no evidence they know the answer.

“From a cycle perspective, the time for the ECB to carry out QE was back when asset prices were too distorted and low. But credit spreads are already low. They are chasing investors into markets that will create a problem when markets normalise. It is just perverse.”

The fiduciaries’ hunger for yield on respectable assets has also run into the requirements for banks and other market participants to put up more high quality collateral for derivatives transactions. Jeremy Stein of Harvard, when he was still a Federal Reserve governor, addressed this issue in February 2013.

Mr Stein referred to how institutions short of high quality collateral required by reform-mandated clearinghouses might get the high quality stuff by swapping, or “transforming” it, with low quality paper. As he said in the paper, these collateral transformations “reproduce some of the same unwind risks that would exist had the clearinghouse lowered its own collateral standards in the first place”, and these transactions “create additional counterparty exposures (among the market participants).”

I asked around how the Fed had followed up on Dr Stein’s curiosity about these unintended risks to the clearing and settling plumbing of the post-reform system and found that while there was some interest there was not enough systematic data gathering or dynamic modelling. For all the Fed knows, the plane is being held together by spit and baling wire.

Speaking of anecdotal, it appears that the ECB is not able to buy the European sovereigns and first class bonds it wants at the rate of purchase it intended. Instead of €50m or €100m bonds at a time, its dealers are being filled at a fraction of those levels in each buying round. Nobody wants to sell an earning asset. What will replace it?

* * *

Someone call the ECB because it looks like the game is well nigh up. Greek FinMins are taking time away from photo shoots and looting pension funds to call out QE for creating equity bubbles and the mainstream financial news media has figured out that there’s an acute collateral shortage and that buying €1.1 trillion in bonds €15 million at a time probably indicates a forced deviation from the original plan.

With lackluster economic growth, disinflation, and exploding central bank balance sheets now a staple across the developed world, we think it’s time someone tells the central banks of the world what Dorothy told Oz:

“If you were really great and powerful you’d keep your promises.”

end

These war of words is not helping:

(courtesy zero hedge)

Nazi Archives Will Support Greece’s Escalating Claims For German War Reparations

As Greeks solemnly remembered the horrific acts of 72 years ago (when the first of 19 trains transported nearly 50,000 local jews to Nazi death camps), the Greek President Pavlopoulos made statements today that he “remains adamant” that “Greece’s demands for German war reparations and the occupation loan are active and can be claimed legally.” German Finance Minister Wolfgang Schaeuble has once again ruled out the possibility of a retreat from what Berlin has already officially said on the matter – that the issue has been settled decades ago. But, today the Greek Defense Minister issued a statement confirming that archives that they possess from Nazi armed forces support the country’s claims for reparations.

As we previously explained, Kathimerini reports,

Greece’s Supreme Court ruled in favor of Distomo survivors in 2000, but the decision has not been enforced. Distomo, a small village in central Greece, lost 218 lives in a Nazi massacre in 1944.

“The law states that in order to implement the ruling of the Supreme Court, the minister of justice has to order it. I believe this permission should be given and I’m ready to give it, notwithstanding any obstacles,”Paraskevopoulos told Antenna TV on Wednesday.

“There must probably be some negotiation with Germany,” said Paraskevopoulos, who first announced his intention Tuesday during a Parliament debate on the creation of a committee to seek war reparations, the repayment of a forced loan and the return of antiquities.

But, as Bloomberg now reports, it apoears the Greek legal standing just improved further…

Greece to use archives it possesses of Wehrmacht, or Nazi armed forces, to support country’s claim for war reparations from Germany for damages inflicted during World War II in period 1941-1944, Greek Defense Ministry says in e-mailed statement.

Archives on Nazi occupation of Greece contain >400,000 pages.

Work to digitize microfilms containing archives to be completed soon.

Archives include Wehrmacht officer diary entries, reports to superiors.

As would be expected, GreekReporter notes, Germany is not happy…

The long standing dispute regarding Germany’s war reparations toward Greece have once again topped news headlines in both countries, amid a “cold” period in their relations. German Finance Minister Wolfgang Schaeuble has once again ruled out the possibility of a retreat from what Berlin has already officially said on the matter. As he explained in an interview to Austrian newspaper Der Standard, in which he also commented on the Greek program, the issue has been settled decades ago.

At the same time, Spiegel became the first German publication to propose that World War II reparations should be paid to Greece in order to close the matter and subtract an argument from Greek Prime Minister Alexis Tsipras’ negotiations quiver. The article noted that such a move would be politically and morally correct, and added that this will also reduce the arguments of the Greek side.

“Alexis Tsipras has threatened with confiscation of German property in Greek territory,” the article reminded, regarding Greek media reports on the matter, which said that this would be the Greek government’s “plan b,” while adding that Defense Minister Panos Kammenos has argued that the war reparations payment would be a good solution for today’s debt crisis.

“Seventy years after the war ended and while there has been a large transfer of funds through the European Union, this is not honest,” Spiegel noted, blaming the German government for helping the Greek criticism when appearing unwilling to discuss the matter and repeated that it has already been settled.

As we concluded previously,

…digging up old wounds will merely accelerate the (less than) amicable parting of ways, especially after a speech earlier by ECB’s Draghi in which he said that ECB bond buying “may be shielding countries in the euro zone from any knock-on effect from events in Greece, ECB President Mario Draghi said on Wednesday.“

* * *

end

The Greeks make their 585 million euro payment to the iMF by raiding their pension funds again.

(courtesy Sputnik news and special thanks to Robert H for sending this to me)

Greece Makes $615Mln IMF Repayment as Scheduled

The Greek government transferred €580 million ($615 million) in loan repayments to the International Monetary Fund (IMF) on time as the country tries to reach a deal with its international lenders to unlock further bailout funds.

The payment was made by the Greek Public Debt Management Agency (PDMA).

Greece needs to make a further payment of €350 million ($370 million) due on Friday. The country will also have to refinance €1.6 billion ($1.7 billion) of three-month treasury bills this week.

The country is rumored to be running out of cash reserves. Greek Prime Minister Alexis Tsipras allayed these fears on Sunday, saying there was “no problem with liquidity.”

Greece has been kept afloat since May 2010 by financial aid from the EU and the IMF. The country has borrowed a total of €240 billion ($254 billion) under two aid packages from the troika of creditors comprising the European Union, the European Central Bank and the IMF.

However, the newly appointed government has to reach a deal with its creditors to unlock further bailout funds. The negotiations with a delegation of technical inspectors on the new set of reforms are still ongoing.

Read more: http://sputniknews.com/business/20150316/1019564530.html#ixzz3UZeUXtw5

end

The Germans are not happy. It seems in a video Varoufakis raised his middle finger against Germany. He claims the video is fake but the people who uploaded the you tube film, claims it is authentic.

(courtesy zero hedge)

Varoufakis’ Latest Fiasco: FinMin Claims “Middle Finger To Germany” Clip Fake; Germany Disagrees

It was a tough weekend (again) for Greece’s embattled FinMin Yanis Varoufakis. After walking out on a CNBC interview when asked if he was a liability (after his photo shoot caused a storm in Greece), a video surfaced showing the outspoken minister giving the middle finger to Germany saying “solve the problem yourself.” He has come out swinging this morning, as The Telegraph reports, Varoufakis exclaims, “That video was doctored. I’ve never given the finger, I’ve never given the middle finger ever.” However, the user who uploaded it to YouTube denied it was a fake and, based on The Telegraph’s poll, 67% believe Varoufakis did it. Furthemore, the German talk-show that aired the clip has confirmed “no evidence of manipulation or falsification,” and, for the first time, a majority of Germans now want Greece out of the union.

The selected image from the video…

Greece “sticking the finger to Germany”

Which he denied as ‘fake’ but… 67% of survey respondents do not believe him…

In a further sign of the deterioration of trust in the ‘union,52% of polled Germans said they no longer wanted Greece to remain part of the currency union, up from 41% last month.

Worst of all, ekathimerini reports that German TV has now stated that the video is not fake, suggesting Varoufakis is in fact a liar.

Varoufakis, who took part in a live discussion with other guests via a link from Athens, insisted on air that the video of him speaking at a 2013 event in the Croatian capital, Zagreb, had been “doctored”.

Jauch, the host of the popular show that draws millions of viewers, announced at the end of the programme that the video would be examined to try to clear the matter up.

“As far as we know at this stage the editorial department of Guenther Jauch can determine no indication whatsoever of manipulation or falsification in the video shown during the live show,” it said in a statement Monday.

It said the video was being further checked by experts.

So will Varoufakis reign as FinMin outlast Greece’s liquidity, pardon, (lack of) cash flow?

end

This is huge news today:

Schauble does not know what to do with Greece after today’s performance.

Big developments:

1 Treasury 3 yr Greek paper now over 20%

2. No foreigner will touch Greek paper/Greece must raise funds internally within the country/good luck to that

3. Greek treasury bill auction today destroyed confidence/expect huge trouble from this day forth!!

(courtesy zero hedge)

Germany Has Had It With Greece: Schauble Says “Doesn’t Know What To Do With Greece Now”

In his fiercest rhetoric yet, Germany’s angry Finance Minister Wolfgang Schaeuble unloaded at a CDU event today:

- SCHAEUBLE SAYS DOESN’T KNOW WHAT TO DO WITH GREECE NOW

- SCHAEUBLE SAYS NEW GREEK GOVERNMENT HAS DESTROYED ALL THE TRUST THAT HAD BEEN REBUILT

He went on to explain that “no one I talk to sees how Greek approach can work,” which perhaps explains why Greek 3Y bond yields spiked back above 20%for the first time since the election today.

Some additional headlines:

- *SCHAEUBLE SAYS GREEK T-BILL AUCTION DESTROYED CONFIDENCE

- *NO FOREIGN INVESTOR WANTED TO BUY GREEK T-BILLS, SCHAEUBLE SAYS

- *SCHAEUBLE: NO ONE I TALK TO SEES HOW GREEK APPROACH CAN WORK

And GGB yields are exploding…

As Bloomberg reports,

“Greece was able to sell those treasury bills only in Greece, with no foreign investor ready to invest,” German Finance Minister Wolfgang Schaeuble says in Berlin.“That means that all of the confidence was destroyed again.”

On Greek govt’s efforts to balance curbing austerity and fulfilling obligations for economic reforms: “None of my colleagues, or anyone in the international institutions, can tell me how this is supposed to work”

Schaeuble comments at Christian Democratic Union event in Berlin today

Charts: Bloomberg

end

As promised: the contagion due to the collapse of Austrian Hypo bank claims its first foreign casualty: Duesselhyp Bank.

This is amazing: a 348 million euro loss brings bankruptcy to a bank with 11 billion euros in assets.

How many more are to going to fail like this?

(courtesy zero hedge)

The Austrian Black Swan Claims Its First Foreign Casualty: German Duesselhyp Collapses, To Be Bailed Out

Precisely one week ago in “A Black Swan Lands In Southern Austria: The Ripple Effects Of “Mini-Greece Going Off In The Heartland Of Europe“, when analyzing the consequences of the collapse of Austria’s bad bank, we noted perhaps the biggest paradox of Europe’s emergency preparedness response to the Greek collapse and imminent expulsion from the Eurozone: namely that the biggest threat to German banks was no longer in some Mediterranean nation, but in its very own back yard. To wit:

Irony #2, and the biggest one of all: while German banks had spent the past 3 years preparing for the inevitable Grexit and offloading all their exposure to the now insolvent Greek state, it was a waterfall chain of events which started in Germany’s own “back yard”, courtesy of auditors who decided it was unnecessary to mark losses to market until it was far too late, and the immediate outcome is that one ninth of until recently Aaa/AAA-rated Austria is now also insolvent.And that is just the beginning.

One can only imagine how many such other “0% risk-weighted” Pandora boxes lie in wait across what are otherwise considered Europe’s safest banks, provinces and nations.