Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1200.90 down $7.20 (comex closing time)

Silver: $16.69 down 39 cents (comex closing time)

In the access market 5:15 pm

Gold $1202.00

Silver: $16.70

Gold/silver trading: see kitco charts on the right side of the commentary.

Following is a brief outline on gold and silver comex figures for today:

The gold comex today, we surprisingly had a good delivery day, registering 667 notices served for 66,700 oz. Silver comex registered 1 notice for 5,000 oz .

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 244.16 tonnes for a loss of 59 tonnes over that period. Lately the removals have been rising!

In silver, the open interest rose by 1,616 contracts, as Wednesday’s silver price was up by 46 cents. The total silver OI continues to remain extremely high with today’s reading at 171,721 contracts. The front April month has an OI of 180 contracts for a gain of 50 contracts. The gain of silver OI in the front month for two days in a row is quite telling as the bankers seem to be in need of silver. We are still close to multi year high in the total OI complex despite a record low price. This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end.

We had 1 notice served upon for 5,000 oz.

In gold the collapse of OI has stopped. The total comex gold OI rests tonight at 387,264 for another loss of 321 contracts despite the rise in gold price yesterday to the tune of $25.55. We had 667 notices served upon for 66,700 oz.

Today, we had no changes in gold inventory at the GLD/ Gold Inventory rests at 737.24 tonnes

In silver, / the SLV/Inventory remains constant, at 321.975 million oz

We have a few important stories to bring to your attention today…

1, Today we had the open interest in silver rise quite appreciably with the 46 cent rise yesterday. The OI for gold surprisingly fell by 321 contracts despite the huge rise in price of gold yesterday (25.50)

(report Harvey/)

2. Greece will likely miss some payments in April. However they do have a 30 day grace period. The action may begin on April 9 with a missed payment to the IMF:

(Bank of America)

3. Iran and the P 5 plus 1 countries “agree” to a settlement on their nuclear capabilities. The problem is that it is not an agreement but only a document that outlines the parameters for a deal.

(zero hedge)

4. Yemeni rebels are in the centre of Aden and they may obtain a stranglehold on the Bab al Mandeb strait. Also a division of the central bank of Yemen is in Aden. Saudi Arabia is reading to invade as they suffered their first casualty.

(zero hedge)

5. India’s imports of gold in March seem to total in excess of 100 tonnes

(Dave Kranzler/IRD/John Brimelow)

6. Israel joins the AIIB as almost all of the USA’s friends are departing.

This could be a huge game changer

(GATA/Reuters)

7. With respect to USA economic data:

The trade deficit plummets. The real scary situation is the fact that imports have fallen faster than USA exports. We can understand the USA exports falling with the high dollar but imports falling through the roof? And the higher dollar encourages imports!!

(zero hedge)

8. USA factory orders fall. On a non seasonal report new factory orders have fallen quite badly in the latest 12 months and this geneally signals a recession

(zero hedge)

we have these and other stories for you tonight

Let us now head over to the comex and assess trading over there today.

Here are today’s comex results:

The total gold comex open interest fell by another 321 contracts from 387,585 down to 387,264 despite the fact that gold was up by $25.55 yesterday (at the comex close). We are now in the active delivery month of April and here the OI fell by 627 contracts down to 4795. We had 1 contract filed upon yesterday so we lost another 626 contracts or 62600 oz will not stand for delivery in April. The next non active delivery month is May and here the OI rose by 115 contracts up to 657. The next big active delivery contract month is June and here the OI fell by 222 contracts down to 262,398. June is the second biggest delivery month on the comex gold calender. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was poor at 62,275 (Where on earth are the high frequency boys?). The confirmed volume yesterday ( which includes the volume during regular business hours + access market sales the previous day) was poor at 160,912 contracts. Today we had 667 notices filed for 66,700 oz.

And now for the wild silver comex results. Silver OI rose by 1616 contracts from 170,105 up to 171,721 as silver was up by 46 cents, with respect to Wednesday’s trading . It certainly seems that we have some resolute longs who refuse to part with their silver contracts. We are now in the non active delivery month of April and here the OI rose to 180 for a gain of 50 contracts.(most unusual). we had 0 notices filed yesterday so we gained 50 contracts or an additional 250,000 oz of silver will stand for delivery in April. The next big active delivery month is May and here the OI dropped by 361 contracts down to 98,756 The estimated volume today was poor at 17,352 contracts (just comex sales during regular business hours. The confirmed volume yesterday (regular plus access market) came in at 49,009 contracts which is good in volume. We had 1 notice filed for 5,000 oz today.

April initial standings

April 2.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 161,135.800oz (Manfra,Scotia) 5012 kilobars |

| Deposits to the Dealer Inventory in oz | 300.000 oz ??? |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 667 contracts (66,700 oz) |

| No of oz to be served (notices) | 4128 contracts(412,800) oz |

| Total monthly oz gold served (contracts) so far this month | 674 contracts(67,400 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

163,579.2 oz |

Today, we had 1 dealer transaction

total Dealer withdrawals: nil oz

we had 1 dealer deposit

i) Into Brinks: 300.000 oz (can someone explain this??? exact oz deposit)

total dealer deposit: 300.000 oz

And the farce on kilobars continues!!

we had 2 customer withdrawals

i) Out of Manfra: 321.50 oz (10 kilobars)

ii) Out of Scotia: 160,814.300 oz (5002 kilobars

total customer withdrawal: 161,135.800 oz (5012 kilobars)

we had 0 customer deposit:

total customer deposit: nil oz

We had 1 adjustment

Out of Scotia: 12,060.695 oz was adjusted out of the dealer and this landed into the customer account of Scotia.

Today, 0 notices was issued from JPMorgan dealer account and 600 notices were issued from their client or customer account. The total of all issuance by all participants equates to 667 contract of which 0 notices were stopped (received) by JPMorgan dealer and 209 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the March contract month, we take the total number of notices filed so far for the month (671) x 100 oz or 67,100 oz , to which we add the difference between the open interest for the front month of April (4795) and the number of notices served upon today (667) x 100 oz equals the number of ounces standing.

Thus the initial standings for gold for the April contract month:

No of notices served so far (671) x 100 oz or ounces + {OI for the front month (4795) – the number of notices served upon today (667) x 100 oz which equals 479,500 oz or 14.91 tonnes of gold.

we lost 626 contracts or 62,600 oz of gold that will not stand for delivery in April

Total dealer inventory: 647,270.900 or 20.13 tonnes

Total gold inventory (dealer and customer) = 7,849,806.094 oz. (244.16) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 59.0 tonnes have been net transferred out. However I believe that the gold that enters the gold comex is not real. I cannot see continual additions of strictly kilobars.

end

And now for silver

April silver initial standings

April 2 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory | nil oz |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 157,052.770 oz (Brinks,Scotia) |

| No of oz served (contracts) | 1 contracts (5,000 oz) |

| No of oz to be served (notices) | 179 contracts(895,000 oz) |

| Total monthly oz silver served (contracts) | 1 contracts (5,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | |

| Total accumulative withdrawal of silver from the Customer inventory this month | 586,230.1 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 0 customer deposits:

total customer deposits: nil oz

We had 2 customer withdrawals:

i) Out of Brinks: 15,729.12 oz

ii) Out of Scotia: 141,323.659

total withdrawals; 157,052.77 oz

we had 1 adjustments:

Out of Delaware:

4,923.545 oz was adjusted out of the customer at Delaware into the dealer account of Delaware

Total dealer inventory: 70.297 million oz

Total of all silver inventory (dealer and customer) 176.493 million oz

.

The total number of notices filed today is represented by 1 contract for 5,000 oz. To calculate the number of silver ounces that will stand for delivery in April, we take the total number of notices filed for the month so far at (1) x 5,000 oz = 5,000 oz to which we add the difference between the open interest for the front month of April (180) and the number of notices served upon today (1) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the April contract month:

1 (notices served so far) + { OI for front month of April(180) -number of notices served upon today (1} x 5000 oz = 900,000 oz standing for the April contract month.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.com orhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

April 2/no changes in gold inventory at the GLD/Inventory at 737.24 tonnes

April 1/2015/ no changes in gold inventory at the GLD/Inventory at 737.24 tonnes

march 31.2015/ no changes in gold inventory at the GLD/Inventory at 737.24 tonnes

March 30/no changes in gold inventory at the GLD/Inventory at 737.24 tonnes.

March 27/no changes in gold inventory at the GLD/Inventory at 737.24 tonnes

March 26 we had another huge withdrawal of 5.97 tonnes of gold. This gold is heading straight to the vaults of Shanghai, China/GLD inventory 737.24 tonnes

March 25.2015 we had a withdrawal of 1.19 tonnes of gold from the GLD/Inventory at 743.21 tonnes

March 24/ no changes in gold inventory at the GLD/Inventory 744.40 tonnes

March 23/we had a huge withdrawal of 5.37 tonnes of gold from the GLD vaults/Inventory 744.40 tonnes

march 20/we had no changes in inventory at the GLD/Inventory at 749.77 tonnes

March 19/we had no changes in inventory at the GLD/Inventory 749.77 tonnes

April 2/2015 / we had no changes in gold/Inventory at 737.24 tonnes

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD : 737.24 tonnes.

end

And now for silver (SLV):

April 2/2015: no changes in inventory/SLV inventory rests this weekend at 321.975 million oz

April 1.2015: we had a huge withdrawal of 1.913 million oz of silver from the SLV vaults/Inventory 321.975 million oz

March 31.2015: no changes in inventory at the SLV/Inventory at 323.88 million oz

March 30.2015: no changes in inventory at the SLV/inventory at 323.888 million oz.

March 27. we had a huge withdrawal of 1.439 million oz leave the SLV/Inventory rests this weekend at 323.888 million oz

March 26.2015; no change in silver inventory/SLV inventory 325.323 million oz

March 25.2015:no change in silver inventory/SLV inventory 325.323 million oz

March 24.2015/ we had another withdrawal of 835,000 oz of silver from the SLV/Inventory rests tonight at 325.323 million oz

March 23./we had a huge withdrawal of 1.174 million oz of silver from the SLV vaults/Inventory 326.158 million oz

March 20/ no changes in silver inventory/327.332 million oz

April 2/2015 we had no changes in inventory at the SLV/This weekend inventory rests at 321.975 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now for the first time into the negative to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 8.2% percent to NAV in usa funds and Negative 8.6% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.8%

Percentage of fund in silver:38.8%

cash .4%

( April 2/2015)

Sprott gold fund finally rising in NAV

2. Sprott silver fund (PSLV): Premium to NAV falls to + 0.25%!!!!! NAV (April 2/2015)

3. Sprott gold fund (PHYS): premium to NAV rises -.41% to NAV(April 2/2015

Note: Sprott silver trust back into positive territory at +0.25%.

Sprott physical gold trust is back into negative territory at -.41%

Central fund of Canada’s is still in jail.

end

And now for your more important physical gold/silver stories:

Gold and silver trading early this morning

(courtesy Goldcore/Mark O’Byrne)

“Faith Many People Have In Gold Is Rising As Instability Increases”

- Inflation fears have caused a surge in Russian demand for gold jewellery

- Currency depreciation and falling wages weighing on average Russians

- Classified ad websites booming as Russians try to raise cash

- Ruble has fallen more than 35% against gold in recent months

- Ruble today … other fiat currencies tomorrow

Gold in Russian Ruble – 1 Year

Currency depreciation, inflation fears and falling wages are weighing on average Russians and leading them to buy gold and silver bullion and some are making “unusually large purchases” of gold jewellery.

A large Russian chain of jewellery stores, Adamas, with 250 outlets across the country saw “same-store sales climb 40 percent in December,” according to a report from Bloomberg.

The role of gold as a store of value in times of high inflation is well known to Russians. “Many are still scarred by the memories of the ruble devaluation of 1998, which sent the annual inflation rate over 100 percent several months later” according to Bloomberg.

Inflation rose 17% in February against 6% for the same period in 2014. Since the economic crisis in Russia took root gold price in roubles has risen substantially.

Gold in Russian Ruble – 5 Years

Between October and early January gold surged from around 50,000 roubles an ounce to over 87,000 roubles an ounce.

However, with the price of Russia’s main exports – oil and gas – stabilising at lower levels, the rouble has also stabilised following a collapse of 46% last year. Gold has since retraced some of its gains and now trades at 70,000 roubles – up from below 45,000 in June 2014.

However, the crisis does not look like ending any time soon. People in Russia continue to struggle. Real wages have declined 9.9% in February when compared to the same time last year. The Russian government is projecting a 3% contraction in the economy this year.

Bloomberg report on how for Avito – Russia’s largest classified ad website – business is booming as Russians buy and sell used goods to raise cash and make ends meet. It has seen a 43% increase in goods for sale since the crisis began.

Gold in Russian Ruble – 20 Year

Canned food businesses are also thriving – sales are up 10% – suggesting that Russians fear sustained crisis and potential supply chain disruptions. War frequently leases to supply chain disruptions and shortages of food, energy and staples.

Russian people suffered many economic crises over the course of the past century and the protective function that gold can play is understood by many.

“The faith many people have in gold is rising as instability increases,” Adamas executive director Maksim Vainberg said in an e-mail. “Unlike home electronics, gold jewelry can be always resold.”

The depreciation seen in the ruble is likely to be seen by other fiat currencies in the coming months and years as competitive currency devaluations and currency wars intensify.

Click here in order to read GoldCore Insight –

Currency Wars: Bye Bye Petrodollar – Buy, Buy Gold

MARKET UPDATE

Today’s AM LBMA Gold Price was USD 1,201.50, EUR 1,110.91 and GBP 811.11 per ounce.

Yesterday’s AM LBMA Gold Price was USD 1,181.25, EUR 1,099.50 and GBP 800.36 per ounce.

Gold in USD – 1 Month

Gold rose 1.69 percent or $20 and closed at $1,204.20 an ounce yesterday, while silver gained 1.86 percent or $0.31, closing at $16.96 an ounce. Overnight in Singapore, gold prices went sideways prior to very slight gains in London this morning.

Gold is hovering above $1,200 an ounce after the nearly 2 per cent gain yesterday, its biggest single-day rally since January 30.

Gold priced in euros is down 0.4% this morning, underperforming spot after posting it biggest quarterly rise since Q3 2011 in the first quarter, rising 12.7%. This was largely due to a particularly strong performance in January, when it rose 16.2% prior to weakness in February in particular.

Gold ETFs posted their first net inflows in Q1 since Q4 2012 due to heavy inflows in January. Although March saw net outflows of 55.7 tons on dollar price weakness.

Breaking News and Award Winning Research

end

USA Mint sales for silver flying off the shelves:

(courtesy seeking alpha)

Pay Attention GLD, PHYS, PSLV, and SLV investors – the U.S. Mint’s full March sales numbers show the strongest March in terms of silver eagles sold. We will go inside the numbers to show this to investors, but the dichotomy between the silver price and silver sold seems to continue, with strong physical investment demand being opposed by relentless paper sales.

Analyzing the U.S. Mint Sales Numbers

When analyzing sales numbers it is important that investors go past the headlines and dig deep into the true nature of the sales. For brevity we are only showing the last few years of sales, but for doing comparisons we have used data from the beginning of the current bull market in 2001.

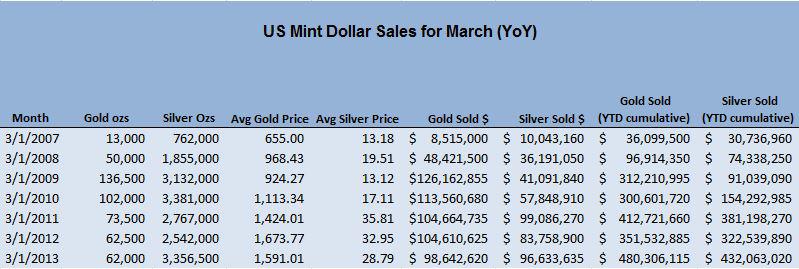

To start, let’s take a look at the U.S. Mint sales numbers for silver and gold for March and compare them to the same month in previous years. We are doing a year-over-year comparison because coin sales are very seasonal in nature; to get a fair read we have to compare March to March.

(Click to enlarge)

The first thing that stands out about the numbers is that silver eagle sales continue to be very strong with 3,356,500 ounces sold in March. This was the second largest amount ever sold in March, and the only March that surpassed this number was in 2010 – when silver prices were 40% lower. The year-to-date numbers continue to impress with 14 million silver ounces sold through March – which is 15% higher than the second highest month (March 2011). As a reminder, 2011 was the strongest year for silver eagle sales (and for the silver price) with 39 million silver eagles selling in 2011, and if we continue matching this sales pace, 2013 will be 15% higher than 2011 and reach 45 million silver eagles sold.

To put these numbers in perspective, according to the U.S. Geological Society, the U.S. mined 1050 tons of silver in 2012 (or 33.6 million ounces). If sales maintain their pace of 45 million ounces of silver, the U.S. will use ALL of its mined silver to mint silver eagles and then have to import and additional 350 tons of silver (11.4 million ounces) simply to meet silver eagle demand – leaving no domestically mined silver for anything else. This is a very extraordinary situation!

Gold eagle sales were relatively subdued with 62,000 ounces of gold eagles sold. Not particularly impressive but on the low side of average. Cumulative gold sales of 292,500 ounces were much better, with the third highest amount of year-to-date sales in the current bull market.

On a dollar-basis these sales numbers are shown in the following table.

(Click to enlarge)

In the table above we have used the average monthly London price fix to calculate the dollar value of the month’s bullion sales. Investors can see that monthly silver sales (in terms of the total dollar amount) have almost tied their record-high amount of $99 million dollars worth of sold silver in 2011 and were only $3 million (3% short) of the record-high dollar sold amount. But in terms of the year-to-date numbers, the $432 million dollars worth of sold silver are 15% higher than the previous high set in 2011 (the best year in silver since the 1980 high), and are continuing to impress.

Not only are silver sales impressive, but gold sales year-to-date are also very impressive. With $480 million dollars worth of gold sold year-to-date, it is more than 15% higher than the previous high and that includes a lackluster March.

Conclusion

Based on the U.S. Mint sales numbers, physical gold and silver are being bought at an unprecedented level which, if the pace keeps up, will break both the gold and silver annual totals. Additionally, silver demand should use up all of mine supply, if it keeps up at this current rate, and should force the U.S. Mint to eat up additional silver supply to make up the difference.

Investors have had a rough year investing in gold and silver and the strange divergence between the physical market and the paper market continues. This is an epic tug-of-war between investors, but we believe that the physical end will win as the physical and paper markets continue to duke it out for two reasons. First, physical silver investors are much “stickier” than paper investors because the investor buying $50,000 worth of silver eagles is less likely to sell if the price drops 2, 3, or 4 dollars – while the paper investors can buy and sell on a whim. This is essentially moving silver from weak hands to strong hands and when the paper investors come back into silver the market can reverse rather quickly.

The second reason we believe that the physical investors will win the battle is that the physical market is ultimately what determines price when sales numbers get high enough. As we mentioned, if sales numbers continue then ALL of U.S. mined silver will be used to mint silver eagles and large amounts of silver will have to emerge from secondary sources simply to meet silver eagle demand. Paper markets can set the price short-term but as other users of silver find it harder to source the metal, you may see some interesting things happen in the paper market (and large jumps in price) as paper contracts are used as a way to deliver physical silver. SLV and PSLV investors be patient and make sure you buy some physical silver as a way to hedge your paper position.

end

Gold figures from the USA Mint:

Sales of the gold bullion coins during 2014 totaled 524,500 ounces.

end

(courtesy Chris Powell/GATA)

Former BIS official criticizes central bank ‘guidance’ on interest rates

9:27p ET Wednesday, April 1, 2015

Dear Friend of GATA and Gold:

In the second part of his interview with the Cobden Center’s Sean Corrigan and Max Rangeley, former Bank for International Settlements official William R. White criticizes what has come to pass for transparency in Western central banking — “guidance” about likely changes in interest rates, which, White says, promotes financial speculation. If only transparency in central banking constituted full disclosure of the interventions central banks already are undertaking in the markets. Part 2 of the interview is posted at Hinde Capital’s Internet site here:

https://hindesightletters.com/blog/william-white-interview-part-ii/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

The following is no surprise as Obama and Netanyahu friendship is frosty:

(courtesy UKTelegraph/GATA)

Israel applies to become founding member of Asian development bank

By Mehreen Khan

The Telegraph, London

Wednesday, April 1, 2015

The Israeli government has submitted its application to become a founding member of a controversial Chinese-led development bank, in a move that is likely to cause consternation in Washington.

Newly re-elected Prime Minister Benjamin Netanyahu signed a letter to join the Asian Infrastructure Investment Bank by the March 31 deadline, according to the country’s foreign ministry.

Israel would become the latest country to join the 40-nation bank, which already includes the UK, Germany, France, Italy, and Australia.

“Israel’s membership in the bank will open opportunities for integration of Israeli companies in various infrastructure projects, which will be financed by the bank,” said an Israeli government statement.

The creation of the bank, under the vision of Chinese premier Xi Jinping, has attracted criticism from the United States, which has warned its closest allies against courting better relations with Beijing. …

… For the remainder of the report:

http://www.telegraph.co.uk/finance/economics/11509242/Israel-applies-to-…

end

Looks good on Barrick. These guys were the original hedgers and became the best friends with our criminal bankers. Now they are in deep trouble…

(courtesy Reuters/GATA)

Barrick Gold must face U.S. lawsuit over mothballed mine

By Jonathan Stempel

Reuters

Wednesday, April 1, 2015

NEW YORK — Barrick Gold Corp. has lost its bid to dismiss a U.S. lawsuit that accuses the world’s largest gold producer of concealing problems at a troubled South American mine and of fraudulently inflating the company’s market value by billions of dollars.

U.S. District Judge Shira Scheindlin in Manhattan ruled on Wednesday that shareholders can pursue class-action claims that Barrick intended to deceive them about environmental problems afflicting its Pascua-Lama project on the border of Argentina and Chile.

“Though plaintiffs have not alleged a motive, they have sufficiently alleged strong circumstantial evidence of conscious misbehavior or recklessness,” the judge wrote in a 55-page decision. …

… For the remainder of the report:

http://www.reuters.com/article/2015/04/01/barrick-gold-lawsuit-idUSL2N0W…

end

Kraft manipulating wheat??? and the CFTC files civil charges against them? These CFTC guys have to be the biggest bozos on the planet.

Kranzler through John Brimelow who follows the Indian market better than anybody notes that India may have imported 100 tonnes of gold in the month of March. Gold is on fire in both India and China.

(courtesy Dave Kranzler/IRD)

Paper Gold Manipulation And India’s Physical Demand

I had to laugh yesterday when a colleague sent me a news report that the CFTC filed a civil enforecement Complaint against Kraft Foods for manipulating wheat futures. Thank GOD the Government has decided to crack down on wheat futures manipulation. Of course, I would bet that no one in the world other than wheat traders knew that the manipulation was occurring.

Contrast this to the incessant and escalating manipulation of the gold futures market by the U.S. Treasury’s Exchange Stabilization Fund in conjunction with the NY Fed and the big bullion banks like JP Morgan, HSBC, Scotia Mocatta and Citigroup. Everyone in the precious metals market knows about this manipulation. GATA has exhaustively produced evidence, including FOIA inquiries which produced information from the Fed verifying that gold is manipulated. For some reason the CFTC just can’t see it.

After spiking higher yesterday on the release of very bearish economic and geopolitical reports which signify the continued collapse of the U.S. economy and sphere of global influence (see my earlier post on the AIIB), the gold manipulation cartel took advantage of the fact that India is closed Thursday and Friday and hit the price of gold on non-event news:

The factory orders report for February was released at 10:00 a.m. It came it slighly higher than the consensus expectations BUT the previous month’s report was revised substantially lower from -.2% to -.7%. Net-net the report reflected a significantly weakening U.S. economy, which should be bullish for gold.

As you can see from the graph above, the paper gold market was smashed at 10:00 a.m. EST. 3,326 contracts were unloaded onto the Comex (both the floor and electronically. This was 15x greater than the minute by minute average volume during the previous hour of trading.

The mechanism that enabled the paper manipulators to throw this much paper onto the market was India’s absence from the physical gold market last night and tonight (India’s markets are closed today and tomorrow).

However, on balance, it appears as if India’s demand for gold significantly increased this year, including the expectation that India may have imported 100 tonnes in March. John Brimelow tracks India’s gold market in his “Gold Jottings” subscription report. The major gold dealing city of Ahemedabad is reporting that 20.73 tonnes of gold were imported into that city in March. This was vs. 5 tonnes over the previous three months. As JB says:

There was talk recently that Indian March gold imports as a whole might have doubled over the preceding month to 100 tonnes. A quadrupling of imports by this key Province is something the Bears ought to think about.

It appears to me that something fundamental has changed in the gold market. I believe it’s based on an enormous uptick in demand from China (after its Lunar New Year) and from India. At some point the physical gold market will overwhelm and “break” the ability of the United States to control the price of gold with paper. I believe that this control is beginning to fade now.

end

Bill Holter discusses the insanity with respect to the huge QE orchestrated by the Japanese government through the Bank of Japan:

(courtesy Bill Holter/Miles Franklin)

Insanity.

Full Definition of INSANITY

And now for the important paper stories for today:

end

Early Thursday morning trading from Europe/Asia

1. Stocks all higher on major Chinese bourses /Japan and Australia higher as well/yen rises to 11957

1b Chinese yuan vs USA dollar/yuan slightly strengthens to 6.1970

2 Nikkei up by 277.95 or 1.46%

3. Europe stocks mixed/USA dollar index down to 97.86/Euro rises to 1.0828

3b Japan 10 year bond yield .34% (Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 119.57/

3c Nikkei still barely above 19,000

3d USA/Yen rate now just below the 120 barrier this morning

3e WTI 48.87 Brent 55.59

3f Gold up/Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning despite the fact a proxy civil war continues in Yemen

3i European bond buying continues to push yields lower on all fronts in the EMU

Except Greece which sees its 2 year rate rises to 24.00%/Greek stocks down by .01% today/ still expect continual bank runs on Greek banks.

3j Greek 10 year bond yield: 11.79% (up by 40 basis point in yield)

3k Gold at 1205.50 dollars/silver $16.84

3l USA vs Russian rouble; (Russian rouble down 1/4 rouble/dollar in value) 57.98 , rising even with the lower brent oil price

3m oil into the 48 dollar handle for WTI and 55 handle for Brent

3n Higher foreign deposits out of China sees hugh risk of outflows and a currency depreciation. This scan spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF

3p Britain’s serious fraud squad investigating the Bank of England/ the British pound is suffering

3r the 7 year German bund still is in negative territory/no doubt the ECB will have trouble meeting its quota of purchases and thus European QE will be a total failure.

3s Eurogroup reject Greece’s bid for more euros of bailout funds as proposal is to vague. The ECB increases ELA by .7 billion euros up to 72.0 billion euros. This money is used to replace fleeing depositors.

3t USA non farm payrolls to be released tomorrow at 8:30

4. USA 10 year treasury bond at 1.84% early this morning. Thirty year rate well below 3% at 2.44%/yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy zero hedge/Jim Reid Deutsche bank)

Futures, Dollar Drift Lower, Oil Slides Ahead Of “Whisper Miss” Payrolls

Unlike yesterday’s vertigo-inducing overnight session, today has been a smooth sea by comparison even if one which has flowed from the top left to the bottom right for now, with futures erasing all of the last minute surge which was HFT programmed to sticksave the S&P just green for the year and then some. It is difficult to pinpoint the catalyst that will be today’s market narrative although with NFP in just over 24 hours, falling on a holiday which will allow S&P futures just 45 minutes of trading after the BLS report hits before closing for the day, and with the weak ADP not to mention the 0.0% Atlanta Fed Q1 GDP forecast, the “whisper” expectation is for a NFP print that will be well below consensus, somewhere in the mid-100,000s if not worse now that the bartender hiring spree is over. The fact that March payrolls have missed on 6 of the last 7 reports probably adds to the dollar weakness, even if a huge miss tomorrow may just be the catalyst Yellen needs to launch the QE4 trial balloon.

A quick look at oil, and the energy complex, shows Brent and WTI crude futures were initially seen lower amid profit taking: at last check WTI was approaching $49 to the downside, around yesterday’s low and accelerating on hope an Iran deal, which almost certainly is not coming, will be announced at some point today. Earlier today we learned that Iran Foreign Minister Zarif said a joint statement expected today, says no agreement yet.

Progress in Greece continues to remain slow and despite the government submitting an updated ‘list’ yesterday, it’s looking increasingly likely that the government won’t receive any sort of early fund disbursement or mini tranche approval ahead of next week’s T-Bill auction and IMF payment. According to Reuters, eurozone officials noted that they received the list from Greece too late for it be discussed at yesterday’s teleconference for deputy finance ministers. It’s looking more likely that talks will resume next week which means in the meantime Greece will need to scrape together the funds to pay next week’s financial maturities as well as pension’s and public sector salaries.

Slower progress is also being felt in the Iran nuclear talks where negotiations have already passed the end-March deadline and appear set to move onto this morning. According to Bloomberg, US Secretary of State John Kerry will stay until at least Thursday morning while yesterday the French foreign minister Fabius returned to talks having previously left. German finance minister Steinmeier acknowledged that a collapse in negotiations is still a possibility but maintained that progress is being made. With a hard deadline for a final agreement set for the end of June, and with few key points appearing to be remaining it could well be that talks are left somewhat unresolved or postponed until a later date, giving both sides longer to firm up on an agreement.

Asian stocks rose after shrugging off yesterday’s negative Wall Street close, led by the Nikkei 225 (+1.46%) after tracking back all of yesterday’s declines. Furthermore, sentiment was lifted by prospects of further easing from the BoJ, after the second-part of the central bank’s Tankan survey showed that large companies see inflation at 1.6% in 5yrs, well off the BoJ’s around end-FY15 2% target. Elsewhere, both the Hang Seng (+0.77%) and Shanghai Comp (+0.41%) trade in the green, the latter in close proximity to its 7yr highs, in an extension of the yesterday’s post Chinese HSBC/Official Mfg. PMIs.

European equities trade relatively mixed to unchanged in what has been a subdued start to the session ahead of tomorrow’s NFP report and Easter weekend. In terms of index-specific moves, the DAX underperforms albeit modestly so after being dragged lower by Deutsche Lufthansa who were subject to a negative broker move and Daimler who are trading ex-div. Elsewhere, the FTSE 100 has been buoyed by Marks & Spencer following their pre-market update which saw a beat on expectations. In terms of the latest developments for Greece, markets still await any notable progress in negotiations, although according to banking sources, the ELA for Greek Banks has been increased by EUR 700mln by the ECB, while the Greek Labour Minister has stated the country will repay the IMF next week and has enough cash to last until the end of the month.

For fixed income markets, Bunds were dragged lower in early trade ahead of this morning’s auction from the French Tresor with analysts at IFR noting extra concession being built in for longer-dated taps. In terms of the auction, it was relatively well-received with French paper being dragged modestly lower after the auction as a result of minor-profit-taking, while Bunds returned to relatively unchanged territory with the supply out of the way.

In FX markets, the USD-index has taken a breather from recent gains ahead of the aforementioned US jobs report, subsequently providing a modest boost to some of its major counterparts, with nothing else in terms of fundamental news driving the index. Elsewhere, GBP saw a minor bout of weakness in the wake of the latest UK construction PMI data which fell short of expectations (57.8 vs. Exp. 59.8), while political uncertainty continues to weigh on the UK currency. Finally, the AUD continues to remain softer against its peers ahead of the looming April 7th RBA rate decision, with markets pricing in a 78% probability of a 25bps rate cut.

Iranian foreign minister Zarif stated today that there has been significant inroads in nuclear negotiations however no agreements have been made as yet. This comes as they continue to work towards a technical compromise ahead of a final deal expected in late June this year. (RTRS)

Iraq (2nd largest OPEC producing nation by production) has reported that exports were at 92.401mln/bbl in March, an increase of 15%. (BBG) In other notable news, Flint Hills Corpus Christi west plant in Texas, US, has sent notifications of an unscheduled shutdown affecting several units. (RTRS)

In precious metals markets, both spot gold and silver trade relatively unchanged with gold holding above the USD 1,200/oz level. Elsewhere, Nickel has trimmed its losses for the week amid technical and physical buying stoked by Asian demand after the industrial metal fell to 6-year lows earlier during the week.

In Summary: European shares decline and U.S. equity index futures fall, signaling S&P 500 Index decline for third day, with dollar weakening before U.S. jobs report. Asian equities rise, led by Nikkei 400. European underperforming sectors incl. autos, basic resources; retail, oil & gas stocks outperform ahead of Good Friday holiday. Yields rise on most eurozone 10-yr sovereign notes, while Portuguese yields fall slightly. Brent, gold, copper fall while wheat gains among food commodities. U.S. jobless claims, Bloomberg consumer comfort, ISM New York, factory orders, trade balance, Challenger job cuts due later.

Market Wrap

- S&P 500 futures down 0.4% to 2045.5

- Stoxx 600 down 0.1% to 398.1

- US 10Yr yield down 0bps to 1.86%

- German 10Yr yield up 1bps to 0.17%

- MSCI Asia Pacific up 1.2% to 147.7

- Gold spot down 0.1% to $1202.7/oz

- Eurostoxx 50 -0.1%, FTSE 100 +0.2%, CAC 40 +0.1%, DAX -0.2%, IBEX -0%, FTSEMIB -0.1%, SMI +0.1%

- Asian stocks rise with the Nikkei outperforming and FTSE Straights Times STI, Jakarta Composite underperforming

- MSCI Asia Pacific up 1.2% to 147.7

- Nikkei 225 up 1.5%, Hang Seng up 0.8%, Kospi little changed, Shanghai Composite up 0.4%, ASX up 0.6%, Sensex up 1.1%

- 10 out of 10 sectors rise with telecom, industrials outperforming and helath care, materials lagging

- Euro up 0.58% to $1.0825

- Dollar Index down 0.38% to 97.81

- Italian 10Yr yield up 1bps to 1.28%

- Spanish 10Yr yield up 3bps to 1.24%

- French 10Yr yield up 1bps to 0.47%

- S&P GSCI Index down 0.1% to 406.2

- Brent Futures down 0.2% to $57/bbl, WTI Futures down 0.2% to $50/bbl

- LME 3m Copper down 0.5% to $6017.5/MT

- LME 3m Nickel up 1.3% to $12870/MT

- Wheat futures up 0% to 528.8 USd/bu

Bulletin Headline Summary

- European equities trade relatively unchanged, while the USD-index takes a pause from recent gains ahead of tomorrow’s US jobs report

- USD-index trades lower ahead of tomorrow’s widely anticipated NFP report, subsequently helping to lift some of the greenback’s major counterparts

- Looking ahead, today sees the release of the weekly US jobs data, trade balance, factory orders and potential comments from Fed’s Yellen

- Treasury yields lower overnight as negotiations with Iran over its nuclear program still ongoing; tomorrow’s holiday-shortened trade session offers nonfarm payroll release.

- Iran said diplomats failed to bridge differences over its nuclear program in a marathon round of overnight negotiations, and may only release a statement that falls short of the blueprint they had sought to end a 12-year standoff

- Greek opposition leader Antonis Samaras, who was ousted by Tsipras in January elections, signaled his willingness to join a unity government if the concessions required to win emergency loans drive a wedge through the ruling anti- austerity coalition

- Bank of Japan policy makers remain confident that inflation is on track to meet their target, even after the latest monthly reading showed price gains stalling, said people familiar with discussions inside the bank

- China now has an outpost in America’s backyard to challenge the U.S. dollar’s dominance in global finance, enlisting Canada in its campaign to help put the yuan among the ranks of the world’s reserve currencies

- U.S. Senator Bob Menendez promised to fight federal corruption charges that he took almost $1 million in gifts and campaign donations to help a longtime friend, vowing to stay in office as he temporarily leaves a key committee post

- Sovereign 10Y yields mixed, Portugal 10Y 11bps higher at 1.67%. Asian stocks rise. European stocks mostly higher, U.S. equity-index futures decrease. Crude and copper fall, gold rises

DB’s Jim Reid concludes the overnight event summary

As we move on from a busy quarter for global markets, trends that we had seen for the majority of Q1 continued into the first day of Q2 as equity markets in the US retreated, European bourses firmed and bond yields tightened. The one caveat was the Dollar which closed out a fairly choppy session a touch lower. Starting in the US, ahead of tomorrow’s all important payrolls data, focus was on yesterday’s ADP employment change reading as a prelude into Friday with the +189k print (vs. +225k expected) surprising to the downside and falling 25k from the February print. Having opened some 1% weaker, the S&P 500 pared back some of the initial losses but traded softly for most of the session before closing down 0.40%. The Dollar, as measured by the DXY eventually closed -0.17% having initially traded between gains and losses. The weaker sentiment generally helped support a bid for Treasuries however. Indeed, 2y (-2.0bps), 10y (-6.6bps) and 30y (-7.1bps) yields all closed tighter, with 10y yields in particular now nearly 40bps off the highs in yield of early March. The commodity complex had a stronger day also as Gold (+1.72%) was well supported while the latest IEA data showing a fall in US crude output helped push WTI (+5.23%) and Brent (+3.61%) higher.

Back to the data, as well as the softer than expected employment reading, yesterday’s ISM manufacturing print for March also weighed on sentiment with the 51.5 print down versus both expectations (52.5) and last month’s print (52.9). The reading was in fact the lowest since May 2013 and the export orders component in particular contracted a point further to 47.5, reflective of the effects of the stronger Dollar but also important given it’s read through into the Q1 GDP print. Elsewhere, the ISM prices paid, despite still at historically low levels, rose 4 points to 39.0 (vs. 38.0 expected) while the final March reading for the manufacturing PMI was revised up slightly to 55.7, from 55.3 previously. Construction spending (-0.1% mom) was as expected and total vehicle sales rose to 17.1m SAAR in March, ahead of expectations of 16.9m.

Yesterday’s softer data saw another cut in the forecast for the Atlanta Fed GDPNow forecast of Q1 GDP to 0.0% SAAR, a 0.2% cut from the previous revision. The model is interesting to us given its divergence from the current market forecasts, which sit in the range of 1-2.5% for Q1. Our colleagues in the US, who currently have a +1.7% Q1 GDP forecast, note that today’s trade data in particular will be an important reading – a wider gap than forecast by the market could see growth estimates revised lower. Elsewhere, the Atlanta Fed’s Lockhart, somewhat unsurprisingly reiterated his June-September timeframe for rate liftoff, but noted that ‘certainly, the weakness of the first quarter gets my attention’.

There was a better tone in Europe yesterday and despite a slight pullback post the US data, equity markets closed higher with the Stoxx 600 (+0.31%), DAX (+0.29%) and CAC (+0.57%) all firmer. Core and peripheral sovereign bonds extended their gains meanwhile. Bunds in particular struck fresh record lows as a strong 5-year auction, in which the government managed to issue 5y debt at a record low of -0.10%, helped support a bid. Indeed, 2y (-0.5bps), 10y (-1.4bps) and 30y (-0.4bps) yields all struck fresh lows at -0.257%, 0.167% and 0.601% respectively. With the curve trading in negative territory up until the 7y maturity (-0.04%), it’s perhaps only a matter of time before 8y (0.02%), 9y (0.09%) and possibly even 10y yields dip below zero.

Data yesterday in Europe was highlighted by better than expected PMI indicators in particular. The final March Euro-area manufacturing reading was revised up slightly to 52.2 from 51.9 previously. Regionally we also saw upward revisions in Germany to 52.8 (+0.4pts) and France to 48.8 (+0.6pts). Elsewhere, in Italy the manufacturing PMI rose 1.4pts to 53.3 and in Spain the reading was more or less in line at 54.3. It was a similar story in the UK also with the indicator rising 0.4pts to 54.4 and in line with consensus.

Progress in Greece continues to remain slow and despite the government submitting an updated ‘list’ yesterday, it’s looking increasingly likely that the government won’t receive any sort of early fund disbursement or mini tranche approval ahead of next week’s T-Bill auction and IMF payment. According to Reuters, eurozone officials noted that they received the list from Greece too late for it be discussed at yesterday’s teleconference for deputy finance ministers. It’s looking more likely that talks will resume next week which means in the meantime Greece will need to scrape together the funds to pay next week’s financial maturities as well as pension’s and public sector salaries.

Slower progress is also being felt in the Iran nuclear talks where negotiations have already passed the end-March deadline and appear set to move onto this morning. According to Bloomberg, US Secretary of State John Kerry will stay until at least Thursday morning while yesterday the French foreign minister Fabius returned to talks having previously left. German finance minister Steinmeier acknowledged that a collapse in negotiations is still a possibility but maintained that progress is being made. With a hard deadline for a final agreement set for the end of June, and with few key points appearing to be remaining it could well be that talks are left somewhat unresolved or postponed until a later date, giving both sides longer to firm up on an agreement.

Geopolitics appears to be more of a theme in markets at present as the conflict in Yemen is showing little sign of abating. According to the BBC, Houthi rebels have reportedly advanced deeper into Aden in a bid to seize control of the city despite the airstrikes from the Saudi-led coalition. With concerns of the number of casualties rising, fears are also mounting over the potential for rebels to consolidate their position on the key parts of the city.

Before we take a look at today’s calendar, quickly refreshing our screens this morning Asian equity markets are mostly ignoring the weakness in the US yesterday and trading firmer. The Shanghai Comp (+0.19%), Nikkei (+1.82%), Hang Seng (+0.44%) and Kospi (+0.11%) are all higher as we go to print. Credit markets in Asia too are around a basis point tighter. Meanwhile, oil markets have given up around a percent of yesterday’s gains.

Turning to the day ahead now, it’s quiet in Europe this morning ahead of the Easter break with just the construction PMI in the UK due. In the US this afternoon, we get more employment data with Challenger job cuts and initial jobless claims while the February trade balance will be an important indicator into Q1 GDP. The ISM NY and factory orders round off the data releases while Fedspeak wise Yellen speaking in Washington this afternoon will be worth keeping an eye on. With most major markets closed tomorrow ahead of the Easter holidays, payrolls reaction will be felt next week when the US market reopens on Monday and European markets open again on Tuesday. Of course, next week also see’s the start of the Q1 reporting season with Alcoa unofficially kicking things off on Wednesday so plenty for us and the market to digest next week.

end

It looks like Greece faces its D Day on April 9 th and then they have a grace period of 30 days.

(courtesy Bank of America/zero hedge)

Greece Faces D-Day On April 9, Will Default Within 30 Days Of Missed Payment, BofAML Says

As “difficult” negotiations between Greece and its creditors drag on, Athens is perilously close to running completely out of cash, and with the banking sector becoming ever more reliant on incremental increases in the ELA ceiling, it may be time to start considering what happens if the cash-strapped Syriza government can’t “borrow” enough public sector funds or otherwise find the money to meet its obligations over the next several months. As a reminder, here’s what the country is up against in the near-term:

If you believe the government (and why wouldn’t you?), Greece will make a scheduled payment to the IMF on April 9 and should have enough cash to carry it through the month. That said, BofAML thinks it’s time to consider the “negative scenarios” that would play out in the event Athens finally comes up short.

Via BofAML:

If Greece misses the payment to the IMF on 9-Apr, this would not necessarily trigger an immediate default. Greece may have an implicit grace period of one month. 1 The sequence of events would be as follows: 1) IMF Staff immediately sends a cable urging the member to make the payment promptly; this communication is followed up through the office of the concerned Executive Director. The member is not permitted any use of the Fund’s resources, nor is any request for the use of Fund resources placed before the Executive Board until the arrears are cleared; 2) After 2 weeks, management sends a communication to the Governor for the member, stressing the seriousness of the failure to meet obligations and urging full and prompt settlement, and 3) After 1 month, the Managing Director notifies the Executive Board that an obligation is overdue.

It is once the Executive Board has been notified of the missed payment that a critical sequence of events could unfold. According to the master financial assistance facility agreement between the EFSF and Greece, the notification of an overdue payment to the IMF would constitute an event of default for the EFSF loans. Such a scenario would risk the EFSF cancelling all or part of its facility, or even declaring the principal amount of the loan to be due immediately. In turn, the acceleration of EFSF loans linked to the PSI exchange would trigger a default event for the PSI GGBs. Even if Greece repays the IMF loan of €458mln on April 9, note that they also have to repay €200mln on May 1 and €763mln on May 12.

Same applies to ECB interest due. Greece also has to pay €274mln of interest on GGBs in April. Assuming it pays €194mln interest to private bondholders on 17-Apr, it will be left with the €80mln interest payment due to the ECB on 20-Apr. The prospectus of the bond held by the ECB indicates a 30-day grace period on interest payments, before a default is declared. Note that this is also the case for the privately held PSI GGBs.

So a missed payment this month triggers a default next month, and at that juncture the following creditors can refer to the ECB’s own projections to determine the likely value of their holdings: “the value of Greek government debt – currently around € 320 billion – in the event of a sudden, ‘accident-like’ Farewell to the Greeks from the Euro-zone (“Graccident”) shrink to around 5 percent of the principal amount.”

Meanwhile, Greece will need to roll over some €1.4 billion in t-bills in two weeks, something which Commerzbank suggests the market should “not ignore” because without access to bailout funds, bill auctions represent a substantial “event risk” for Athens. Furthermore, whatever foreign demand there might have been is likely to dissipate in lockstep with any deterioration in the prospects for a deal with creditors.

Via Bloomberg:

Greece may announce tomorrow that its next t-bill auction will take place on April 8, before the IMF payment scheduled for April 9 (April 10 and April 13 are holidays in Greece).

Primary mkt activity is an event risk for Greece because it’s unlikely that any bailout money will flow over coming days.

Greece will have to roll over EU1.4b of 26-week GTB maturing on April 14 and also EU1b 13-week GTB maturing on April 17.

April 14 GTB rollover may well be more difficult than April 17 one as foreigners probably have more exposure in that line as it was sold in early Oct., before meltdown in GGBs triggered by prospect of snap elections.

This time, it’s unlikely foreigners will roll over their complete exposure, leaving net supply to be taken down by Greek domestic institutions.

Together with fears that any net GTB supply to been absorbed by domestics will be a big challenge, this should trigger more pressure on Greece.

* * *

And speaking of April 9, that is the day that the country has told Eurozone officials it will officially run out of cash according to Reuters.

Coincidentally, it’s also the day Tsipras will be in Moscow to discuss “international developments” with President Putin.

end

China becomes the lender of last resort to Brazil’s Petrobras.

(courtesy zero hedge)

China Becomes Global Lender Of Last Resort With Bailout Of World’s Most Indebted Oil Company

Over the course of last month we variously described the Asian Infrastructure Investment Bank as an attempt by Beijing to deal a decisive blow to the post-World War II global economic order by undermining US-dominated multinational institutions, as an attempt to usher in a new era characterized by yuan hegemony, and as an effort to cement China’s regional influence via the implicit establishment of a sino-Monroe Doctrine.

With that in mind, we find it somewhat ironic that the China Development Bank (which isn’t the same as the AIIB but which we think might offer some clues as the how the new venture will be run under Beijing’s control), is set to provide $3.5 billion in financing to Brazil’s deeply indebted Petrobras. The new funding comes 6 years after a $10 billion oil export deal between the company and China and just days after Brazil signed up as a founding member of the AIIB.

More, via WSJ:

Brazil’s state-run Petroleo Brasileiro SA said on Wednesday it signed a $3.5 billion financing deal with the China Development Bank, highlighting the oil giant’s deteriorating financial condition in the wake of a vast corruption scandal as well as China’s growing ties to Latin America.

Petrobras didn’t provide any details of the deal, which is part of a cooperation agreement to be implemented this year and in 2016. But the transaction deepens the Brazilian government’s relationship with its largest trading partner and fellow BRIC country.

The Asian giant has provided similar assistance to countries like Ecuador, Venezuela and Argentina, helping those countries deal with falling global oil prices and their own debt problems.

“China again is…lending to state-owned companies that cannot access the market,” said Adriano Pires, an energy expert with the Brazilian Center of Infrastructure in Rio de Janeiro.

China has extended more than $100 billion in credit to Latin America since 2005, according to figures from Boston University’s Global Economic Governance Initiative. In January, Chinese President Xi Jinping said China’s foreign investment in Latin America would hit $250 billion over the next decade.

At the risk of extrapolating too much, it appears as though Beijing isn’t opposed to throwing billions behind serving as a lender of last resort and we can’t help but wonder if the new round of Petrobras financing is indicative of where China will steer initial AIIB funding — that is, into oil and Latin America. What’s interesting (and very ironic given how we’ve characterized the AIIB), is that it appears Beijing may look to channel the bank’s lending straight into Washington’s backyard, effectively slighting the original Monroe Doctrine even as China tacitly implements its own take on an official policy of regional influence and control.

Meanwhile, US allies continue to fall in line with France, Italy, and Israel set to jump on the bandwagon. Here’s more via Reuters:

Prime Minister Benjamin Netanyahu has signed a letter of application for Israelto join the China-led Asian Infrastructure Investment Bank (AIIB), the Israeli Foreign Ministry said on Wednesday.

More than 40 countries, including Australia, South Korea, Britain, France, Germany andItaly, have said they would sign up to the AIIB, with Japan and the United States the two notable absentees.

In a statement on its website, the Foreign Ministry said Israel’s AIIB membership would open up opportunities to integrate Israeli companies into infrastructure projects it financed.

Israeli companies are increasingly turning to Asia to capture a boom in demand for their technology, as the government urges them to diversify export markets in response to Europe’s rising anti-Semitism and potential trade sanctions.

And just like the ADB, the IMF isn’t intent on undermining the new institution. Via Bloomberg:

The Asian Infrastructure Investment Bank is welcomed as long as it commits to cooperation and efficient operations, China Business News cites IMF Managing Director Christine Lagarde in an interview.

AIIB is a wake-up call for countries that don’t agree with IMF’s quota system: Lagarde

China’s IMF quota should match the size of its economy, Lagarde says

Yuan becoming SDR currency is a matter of time: Lagarde says

* * *

We’ll close with the following quote from US Under Secretary Of State for Economic Growth, Energy, and the Environment:

“We hope that the governance of that institution and the environmental impacts are going to be done in way that’s consistent with what other multilateral development banks aredoing. We don’t have any concern, in theory, about the development of an Asian infrastructure bank.”

end

Michael Snyder illustrates 5 charts to show that we are facing an economic crash!!

(courtesy Michael Snyder/EconomicCollapse blog)

5 Charts Which Show That The Next Economic Crash Is Dead Ahead

Submitted by Michael Snyder via The Economic Collapse blog,

When an economic crisis is coming, there are usually certain indicators that appear in advance. For example, commodity prices usually start to plunge before a recession begins. And as you can see from the Bloomberg Commodity Index which you can find right here, this has already been happening. In addition, I have previously written about how the U.S. dollar went on a great run just before the financial collapse of 2008. This is something that has also been happening over the past few months. Some people would have you believe that nobody can anticipate the next great economic downturn and that to try to do so is just an exercise in “guesswork”. But that is not the case at all. We can look back over history and see patterns that keep repeating. And a lot of the exact same patterns that happened just before previous stock market crashes are happening again right now.

For example, let’s talk about the price of oil. There are only two times in history when the price of oil has fallen by more than 50 dollars in a six month time period. One was just before the financial crisis in 2008, and the other has just happened…

As a result of crashing oil prices, we are witnessing oil rigs shut down in the United States at a blistering pace. In fact, almost half of all oil rigs in the U.S. have already shut down. The following commentary and chart come from Wolf Richter…

In the latest week, drillers idled another 41 oil rigs, according to Baker Hughes. Only 825 rigs were still active, down 48.7% from October. In the 23 weeks since, drillers have idled 784 oil rigs, the steepest, deepest cliff-dive in the history of the data:

We are looking at a full-blown fracking bust, and this bust is already having a dramatic impact on the economies of states that are heavily dependent on the energy industry.

For example, just check out the disturbing number that just came out of Texas…

The crash in oil prices is hammering the Texas economy.

The latest manufacturing outlook index from the Dallas Fed plunged again in March, to -17.4 from -11.2 in February, indicating deteriorating business conditions in the state.

Ouch.

But this pain is going to be felt far beyond Texas. In recent years, Wall Street banks have made a massive amount of money packaging up energy industry loans, bonds, etc. and selling them off to investors.

If that sounds similar to the kind of behavior that preceded the subprime mortgage meltdown, that is because it is.

Now those loans, bonds, etc. are going bad as the fracking bust intensifies, and whoever is left holding all of this worthless paper at the end of the day is going to lose an extraordinary amount of money. Here is more from Wolf Richter…

It suited Wall Street just fine: according to Dealogic, banks extracted $31 billion in fees from the US oil and gas industry and its investors over the past five years by handling IPOs, spin-offs, “leveraged-loan” transactions, the sale of bonds and junk bonds, and M&A.

That’s $6 billion in fees per year! Over the last four years, these banks made over $4 billion in fees on just “leveraged loans.” These loans to over-indebted, junk-rated companies soared from about $40 billion in 2009 to $210 billion in 2014 before it came to a screeching halt.

For Wall Street it doesn’t matter what happens to these junk bonds and leveraged loans after they’ve been moved on to mutual funds where they can decompose sight-unseen. And it doesn’t matter to Wall Street what happens to leverage loans after they’ve been repackaged into highly rated Collateralized Loan Obligations that are then sold to others.

At the same time, we are also witnessing a slowdown in global trade. This usually happens when economic conditions are about to turn sour, and that is why it is so alarming that the total volume of global trade in January was down 1.4 percent from December. According to Tyler Durden of Zero Hedge, that was the largest drop since 2011…

Presenting the latest data from the CPB Netherlands Bureau for Economic Policy Analysis, according to which in January world trade by volume dropped by a whopping 1.4% from December: the biggest drop since 2011!

We are seeing some troubling signs in the U.S. as well.

I shared the following chart in a previous article, but it bears repeating. It comes from Charles Hugh Smith, and it shows that new orders for consumer goods are falling at a rate not seen since the last recession…

Well, what about the stock market? It was up more than 200 points on Monday. Isn’t that good news?

Yes, but the euphoria on Wall Street will not last for long.

When corporate earnings per share either start flattening out or start to decline, that is a huge red flag. We saw this just prior to the stock market crash of 2008, and it is happening again right now. The following commentary and chart come from Phoenix Capital Research…

Take a look at the below chart showing current stock levels and changes in forward Earnings Per Share (EPS). Note, in particular how divergences between EPS and stocks tend to play out (hint look at 2007-2008).

We all know what came next.

And guess what?

According to CNBC, a lot of the “smart money” is pulling their money out of the stock market right now while the getting is good…

Recent market volatility has sent stock market investors rushing for the exits and into cash.

Outflows from equity-based funds in 2015 have reached their highest level since 2009, thanks to a seesaw market that has come under pressure from weak economic data, a stronger dollar and the the prospect of monetary tightening.

Funds that invest in stocks have seen $44 billion in outflows, or redemptions, year to date, according to Bank of America Merrill Lynch. Equity funds have seen outflows in five of the last six weeks, including $6.1 billion in just the last week.

It doesn’t matter if you are a millionaire “on paper” today.

What matters is if the money is going to be there when you really need it.

At the moment, a whole lot of people have been lulled into a false sense of complacency by the soaring stock market and by the bubble of false economic stability that we have been enjoying.

But under the surface, there is a whole lot of turmoil going on.

Those that are looking for the signs are going to see the next crisis approaching well in advance.

Those that are not are going to get absolutely blindsided by what is coming.

Don’t let that happen to you.

end

And now the Iran “deal”.

First reported both sides walk away with no real substance to an agreement:

(courtesy zero hedge)

Another Iran “Deal” Failure Spun As Success – Live Webcast

In the same style as we have grown used to around the world, a major negotiation has ended with all sides claiming victory and no sides offering any actual solutions. Iran proclaims the talks have made “significant progress,” yet Western diplomats are saying progress is “limited,” only to be confused even more by Iran’s Foreign Minister stating that “but still we have not agreed on the reviewed solutions.” So in summing it all up, a press conference will be held shortly to explain that ‘they agree on the outline of a plan which will pave the way for an agreement but aren’t sure how much of the plan or hypothetical agreement they want to share’. New normal geopolitics… no deal is the new deal.

Nuclear talks between the Iranian delegation and foreign ministers of the P5+1 group might bear fruit on Thursday, RT reports, if the sides manage to agree certain solutions.

Western negotiators are saying progress is ‘limited.’

However, Reuters cited Iranian Foreign Minister Mohammad Javad Zarif as saying: “We have made significant progress in the talks, but still we have not agreed on the reviewed solutions.”

…

The meeting has been going on through the night between US Secretary of State John Kerry and his Iranian counterpart.

The German and French foreign ministers are also present, as well as the UK foreign secretary and European Union negotiator Helga Schmid.

The foreign ministers of China, Russia and France left the country on Tuesday after the initial deadline passed, saying they would return when necessary.

“We are a few meters from the finishing line, but it’s always the last meters that are the most difficult. We will try and cross them,” French Foreign Minister Laurent Fabius said in Switzerland on Wednesday night when he returned to negotiations.

Iran and and six world powers have agreed on the outlines of an understanding that would open the path to a final phase of nuclear negotiations but are in a dispute over how much to make public, officials told AP.

Got it?

So both sides are cornered by their domestic needs to save face and international reputations…

Pressured by congressional critics in the U.S. who threaten to impose new sanctions on Iran over what they say is a bad emerging deal, the Obama administration is demanding significant public disclosure of agreements and understandings reached at the current round. But the officials say Iran wants a minimum made public.

Iranian leaders are opposed to two agreements, saying previous two-stage negotiations were detrimental to their interests. They results reached in the Swiss city of Lausanne as less than a deal and more of an informal understanding.

The officials demanded anonymity because they are not authorized to discuss the negotiations publicly.

They spoke after senior diplomats from the six countries negotiating with Iran huddled overnight in strategy sessions meant to advance the pace of agonizingly slow nuclear talks. Iran’s foreign minister said the sides were close to a preliminary agreement, but not yet there.

* * *

And then there’s the Neocons…

“It is clear, the negotiations are not going well,” Sens. John McCain of Arizona and Lindsey Graham of South Carolina said in a statement.

“At every step, the Iranians appear intent on retaining the capacity to achieve a nuclear weapon.”

* * *

Summing it all up… a process that started in February 2013 has now been extended yet again from another self-imposed deadline to June 30… Guess what happens next?

* * *

end

Then crude tumbles on an “announced deal” which turns out to be nothing but parameters for a deal to be concluded later:

Crude Tumbles On Iran “Deal” Headlines

Despite the “deal” having absolutely no content whatsoever… the headlines:

- IRAN OIL, BANK SANCTIONS WILL BE LIFTED ONCE DEAL IMPLEMENTED

…are enough to send the algos scrambling and spark weakness across the crude complex (even though this ‘news’ is stating what will/may/could/won’t happen after June 30th).

WTI Tanking…

Brent unwinds it all…

Charts: Bloomberg

end

More Oil related stories:

Revolving credit from the banks to shale companies is being unwound.

This will cause huge problems for our shale companies. Samson Resources purchased by KKR in 2013 will no doubt have to file for bankruptcy protection. Also Sabine Oil announced that it may miss a debt payment and thus at risk of defaulting:

(courtesy zero hedge)

The “Revolver Raid” Arrives: A Wave Of Shale Bankruptcies Has Just Been Unleashed

Back in early 2007, just as the first cracks of the bursting housing and credit bubble were becoming visible, one of the primary harbingers of impending doom was banks slowly but surely yanking availability (aka dry powder) under secured revolving credit facilities to companies across America. This, in effect, was the first snowflake in what would ultimately become the lack of liquidity avalanche that swept away AIG and unleashed the biggest bailout of capitalism in history. Back then, analysts had a pet name for banks calling CFOs and telling them “so sorry, but your secured credit availability has been cut by 50%, 75% or worse” – revolver raids.

We bring it up because the infamous revolver raids are back, only unlike 7 years ago when they initially focused on retail companies, it should come as no surprise this time the sector hit first and foremost is energy.

As Bloomberg reports, “lenders are preparing to cut the credit lines to a group of junk-rated shale oil companies by as much as 30 percent in the coming days, dealing another blow as they struggle with a slump in crude prices, according to people familiar with the matter.

Sabine Oil & Gas Corp. became one of the first companies to warn investors that it faces a cash shortage from a reduced credit line, saying Tuesday that it raises “substantial doubt” about the company’s ability to continue as a going concern.

It’s going to get worse: “About 10 firms are having trouble finding backup financing, said the people familiar with the matter, who asked not to be named because the information hasn’t been announced.”

Why now? Bloomberg explains that “April is a crucial month for the industry because it’s when lenders are due to recalculate the value of properties that energy companies staked as loan collateral. With those assets in decline along with oil prices, banks are preparing to cut the amount they’re willing to lend. And that will only squeeze companies’ ability to produce more oil.

Those loans are typically reset in April and October based on the average price of oil over the previous 12 months. That measure has dropped to about $80, down from $99 when credit lines were last reset.

That represents billions of dollars in reduced funding for dozens of companies that relied on debt to fund drilling operations in U.S. shale basins, according to data compiled by Bloomberg.

“If they can’t drill, they can’t make money,” said Kristen Campana, a New York-based partner in Bracewell & Giuliani LLP’s finance and financial restructuring groups. “It’s a downward spiral.”

And it is all as we warned here months ago, because with shale companies having exhausted their ZIRP reserves which are mostly unsecured funding, it means that once the secured funding crunch arrives, it is truly game over, and it is just a matter of months if not weeks before the current stakeholders give the keys over to either the secured lender of their bondholders.

The good news is that unlike almost a decade ago, this time the news of impending corporate doom will come nearly in real time: “Publicly traded firms are required to disclose such news to investors within four business days, under U.S. Securities and Exchange Commission rules. Some of the companies facing liquidity shortfalls will also disclose that they have fully drawn down their revolving credit lines like Sabine, according to one of the people.”

Speaking of Sabine, its day of reckoning has arrived

Sabine, the Houston-based exploration and production company that merged with Forest Oil Corp. last year, told investors Tuesday that it’s at risk of defaulting on $2 billion of loans and other debt if its banks don’t grant a waiver.

Another company is Samson Resource, which said in a filing on Tuesday that it might have to file for a Chapter 11 bankruptcy protection if the company is unable to refinance its debt obligations. And unless oil soars in the coming days, it won’t.

Its borrowing base may be reduced due to weak oil and gas prices, requiring the company to repay a portion of its credit line, according to a regulatory filing on Tuesday. That could “result in an event of default,” Tulsa, Oklahoma-based Samson said in the filing.

Indicatively, Samson Resources, which was acquired in a $7.2-billion deal in 2011 by a team of investors led by KKR & Co, had a total debt of $3.9 billion as of Dec. 31. It is unlikely that its sponsors will agree to throw in more good money after bad in hopes of delaying the inevitable.

The revolver raids explian the surge in equity and bond issuance seen in recent weeks: