Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1183.20 down $5.90 (comex closing time)

Silver $16.30 down 14 cents (comex closing time)

In the access market 5:15 pm

Gold $1184.10

Silver: $16.32

Gold/Silver trading: see kitco charts on the right side of the commentary

Following is a brief outline on gold and silver comex figures for today:

At the gold comex today, we had a poor delivery day, registering 0 notices serviced for nil oz. Silver comex filed with 8 notices for 40,000 oz

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 240.06 tonnes for a loss of 63 tonnes over that period. Looks to me like the comex is bleeding profusely!!

In silver, the open interest fell slightly by 492 contracts despite the fact that Friday’s silver price was up by 17 cents The total silver OI continues to remain extremely high with today’s reading at 176,026 contracts maintaining itself near multi-year highs despite a record low price. This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end.

In silver we had 8 notices served upon for 40,000 oz.

In gold, the total comex gold OI rests tonight at 408,43 for a gain of 8444 contracts as gold was up by $6.70 on Friday. We had 0 notices served upon for nil oz.

Today, we had no changes in gold Inventory, at the GLD. It rests tonight at 728.32 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold.

In silver, / no changes with respect to silver inventory at the SLV/ and thus the inventory tonight remains at 322.662 million oz

We have a few important stories to bring to your attention today…

1. Today we had the open interest in silver fall by 492 contracts as silver was up in price on Friday by 17 cents. The OI for gold rose by 8444 contracts up to 408,432 contracts as the price of gold was up by $6.70 on Friday. GLD had no change and SLV, no changes with respect to the inventory levels.

(report Harvey)

2,Today we had 7 major commentaries on Greece today:

(zero hedge/ UKTelegraph)

3.China cuts it’s interest rate again

(zero hedge)

4 Saudi Arabia on the doorstep of Yemen, ready to raid.

(zero hedge)

5. Goldcore and Mark Faber discuss Greece.

Mark Faber/Goldcore)

6. Bill Holter discusses the mammoth rise in European 10 year bonds on Wednesday and the resultant derivative mess>

we have these and other stories for you tonight

Let us now head over to the comex and assess trading over there today.

Here are today’s comex results:

The total gold comex open interest rose by 8444 contracts from 399,988 up to 408,432 as gold was up by $6.970 on Friday (at the comex close). We are in our next non active delivery month of May and here the OI fell by 37 contracts falling to 156. We had 0 notices filed upon yesterday. Thus we lost 37 gold contracts or an additional 3700 ounces will not stand for gold in May. The next big active delivery contract month is June and here the OI fell by 5,527 contracts down to 221,660. June is the second biggest delivery month on the comex gold calendar. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was poor at 7062. The confirmed volume yesterday ( which includes the volume during regular business hours + access market sales the previous day) was fair at 176,90 contracts. Today we had 0 notices filed for nil oz.

And now for the wild silver comex results. Silver OI fell by 492 contracts from 176,518 down to 176,026 despite the fact that the price of silver was up in price by 17 cents, with respect to Friday’s trading. We are into the active delivery month of May. In our May delivery month the OI fell by 31 contracts down to 715. We had 70 contracts filed upon with respect Friday’s trading. So we gained 39 contracts or an additional 195,000 oz will stand for delivery in this May delivery month. The estimated volume today was extremely poor at 9,327 contracts (just comex sales during regular business hours. The confirmed volume on Friday (regular plus access market) came in at 35,054 contracts which is fair in volume. We had 70 notices filed for 350,000 oz today.

May initial standings

May 11.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 602.97 oz Manfra |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 33,128.842 oz (Scotia) |

| No of oz served (contracts) today | 0 contracts (nil oz) |

| No of oz to be served (notices) | 156 contracts(15,600) oz |

| Total monthly oz gold served (contracts) so far this month | 1 contracts(100 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 164,151.8 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 36,176.6 oz |

Today, we had 0 dealer transactions

total Dealer withdrawals: nil oz

we had 0 dealer deposit

total dealer deposit: nil oz

we had 1 customer withdrawal

i) Out of Manfra; 602.97

total customer withdrawal: 602.97 oz

We had 2 customer deposits:

i) Into Delaware:602.541 oz

ii) Into Scotia: 32,526.301 oz

total customer deposit: 33,526.301 oz

We had 1 major adjustment:

i) out of Scotia:

35,167.632 oz was adjusted out of the dealer and back into the customer account at Scotia

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the May contract month, we take the total number of notices filed so far for the month (1) x 100 oz or 100 oz , to which we add the difference between the open interest for the front month of May (156) and the number of notices served upon today (0) x 100 oz equals the number of ounces standing.

Thus the initial standings for gold for the May contract month:

No of notices served so far (1) x 100 oz or ounces + {OI for the front month (156) – the number of notices served upon today (0) x 100 oz which equals 15,700 oz standing so far in this month of May. (833 tonnes of gold)

we lost 3700 oz that will not stand for delivery

Total dealer inventory: 372,234.632 or 11.58 tonnes

Total gold inventory (dealer and customer) = 7,718,386.684. (240.06) tonnes)

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 240.06 tonnes for a loss of 63 tonnes over that period. Lately the removals have been rising!

It looks like somebody major is draining the gold from the dealer comex. Something is seriously happening behind the scenes.

end

And now for silver

May silver initial standings

May 11 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 231,458.110 oz (CNT, Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1,631,216.600 (CNT, Scotia) |

| No of oz served (contracts) | 70 contracts (350,000 oz) |

| No of oz to be served (notices) | 707 contracts (3,535,000 oz) |

| Total monthly oz silver served (contracts) | 2330 contracts (11,650,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 126,359.680 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 2,776,890.6 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 2 customer deposits:

i) Out of CNT 1,193,956.521 oz

ii) Out of Scotia: 477,259.580 oz

total customer deposits:1,631,216.101 oz

We had 2 customer withdrawals:

i) Out of Scotia: 30,179.01 oz

ii) Out of CNT: 201,279.100 oz

total withdrawals; 231,458.110 oz

we had 1 adjustment

i) Out of CNT: 37,244.600 oz was adjusted out of the customer and this landed into the dealer account at CNT

Total dealer inventory: 59.683 million oz

Total of all silver inventory (dealer and customer) 176.310 million oz

So we have both gold and silver being drained from the dealer (registered) side at the comex.

.

The total number of notices filed today is represented by 70 contracts for 350,000 oz. To calculate the number of silver ounces that will stand for delivery in April, we take the total number of notices filed for the month so far at (2330) x 5,000 oz = 11,650,000 oz to which we add the difference between the open interest for the front month of April (71) and the number of notices served upon today (8) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the May contract month:

2330 (notices served so far) + { OI for front month of April (715) -number of notices served upon today (8} x 5000 oz = 15,185,000 oz of silver standing for the May contract month.

we gained 39 contracts or an additional 195,000 oz will stand for delivery.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.com orhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

May 11/ no changes at the GLD/Inventory rests at 728.32 tonnes

May 8/ they should call in the Serious Fraud squad as the owners of the GLD just saw 13.43 tonnes of gold leave its vaults heading for China:

Inventory tonight: 728.32 tonnes

May 7. no change in gold inventory at the GLD/741.75 tonnes

May 6/no change in gold inventory at the GLD/741.75 tonnes

may 5/no change in gold inventory at the GLD/741.75 tonnes

may 4/no change in gold inventory at the GLD./741.75 tonnes

May 1/ we had a huge addition of 2.69 tonnes of gold into the GLD/Inventory rests tonight at 741.75 tonnes

April 30/ no change in gold inventory/739.06 tonnes of gold at the GLD

April 29/no change in gold inventory/739.06 tonnes of gold at the GLD

April 28/ no change in inventory/739.06 tonnes of gold at the GLD

April 27. we lost 3.29 tonnes of gold inventory at the GLD/Inventory rests tonight at 739.06 tonnes

April 24. no changes in gold inventory at the GLD/Inventory at 742.35 tonnes

April 23. no changes in gold inventory at the GLD/inventory at 742.35 tonnes

April 22. no changes in gold inventory at the GLD/inventory at 742.35 tonnes

April 21.2015: a huge addition of 3.26 tonnes of gold inventory at the GLD/Inventory rests at 742.35 tonnes

April 20.2015: no change in gold inventory at the GLD/Inventory rests at 739.06 tonnes

April 17.2015/ we had a huge addition of 3.01 tonnes of gold inventory at the GLD. It looks like the raids at the GLD have stopped.

April 16.2015: no change in inventory at the GLD/total inventory at 736.08 tonnes

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

May 11 GLD : 728.32 tonnes.

end

And now for silver (SLV)

May 11/no changes at the SLV/Inventory rest at 322.662 million oz

May 8/ today we lost a huge 2.87 million oz of silver from the SLV/Inventory 322.662

May 7/no change in silver inventory/325.53 million oz

May 6/we had a huge withdrawal of 2.143 million oz of silver from the SLV/325.53 million oz

May 5/no change in silver inventory at the SLV/327.673 million oz

May 4/ no change in silver inventory at the SLV/327.673 million oz

May 1/no change in silver inventory at the SLV/327.673 million oz

April 30/no change in silver inventory at the SLV/327.673 million oz

April 29/ we lost 2.963 million oz of silver inventory from the SLV/inventory tonight 327.673 million oz

April 28/another huge addition of 1.434 million oz to the SLV/Inventory stands tonight at 330.636 million oz

April 27.we had a huge addition of 2.976 million oz to the SLV/Inventory stands tonight at 329.202 million oz

April 24/ we had a small withdrawal of 88,000 oz of silver at the SLV/326.226 million oz

April 23.no changes in silver inventory at the SLV/326.334 million oz of inventory

April 22/no changes in silver inventory at the SLV/326.334 million oz of inventory

April 21.2015/we had another huge addition of 1.434 million oz of silver into the SLV

April 20/ no change in silver inventory tonight/SLV 324.900 million oz.

May 11/2015 no changes at the SLV / inventory rests at 322.662 million oz

end

And now for our premiums to NAV for the funds I follow:

Central fund of Canada data not available today/

Note: Sprott silver fund now for the first time into the negative to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 7.6% percent to NAV in usa funds and Negative 7.7% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 61.3%

Percentage of fund in silver:38.3%

cash .4%

( May 11/2015)

2. Sprott silver fund (PSLV): Premium to NAV falls to-0.57%!!!!! NAV (May 11/2015)

3. Sprott gold fund (PHYS): premium to NAV rises to -.27% to NAV(May 11/2015

Note: Sprott silver trust back into negative territory at -0.57%.

Sprott physical gold trust is back into negative territory at -.27%

Central fund of Canada’s is still in jail.

end

Early morning trading from Asia and Europe last night:

Gold and silver trading from Europe overnight/and important physical stories(courtesy Mark O’Byrne/Goldcore)

“This Is A New World Order” – Greece Not Allowed Leave EU – Faber

– Greece will not be ejected from the EU – Faber on CNBC

– Greek default will trigger massive losses for ECB and European banks

– Highlights geo-political impetus to keep Greece within EU, NATO fold

– Shows strategic geo-political importance of Greece in NATO’s Cold war with Russia

– China and Russia’s ever-closer relationship more important than declining UK

– “This Is A New World Order” – Dr Faber

In another fascinating interview, this time on CNBC, Dr. Marc Faber discussed the factors involved in the ongoing Greek crisis and made some interesting points.

Dr. Faber – who edits the Gloom, Boom and Doom report – is in no doubt that Greece will not be allowed to default because of both economic and geo-political considerations.

“It’s about the ECB and European banks that have lent money to Greece and if Greece defaults would have to take a huge loss and write-off. So they will lend more money and kick the can down the road.”

Of even greater significance is Greece’s strategically vital location as a gateway between the Black Sea and the Mediterranean.

It is this geo-political factor which Faber believes will ensure that Greece is kept within the EU fold at any cost. For this reason he insists that Russia will never cede Crimea to the western powers.

“From the Black Sea, the Russian fleet can move into the Mediterranean. and without that, they can’t – they have no access to the Mediterranean, without the Black Sea and Crimea.”

Between the Black Sea and the Mediterranean, he adds, lie Turkey, Moldavia and then Greece making Greece “a very strategically important part of Europe”.

The implication is that were the EU to cut Greece loose Russia would be only too happy to step in and potentially project military power directly into Europe.

Faber was then asked to clarify whether he was suggesting that the EU would never let Greece go so that “Putin … cannot recapture the glory of the Soviet Union.”

He subtly points out that imperialism is by no means confined to Russia and that Russia’s recent actions may have been in response to U.S. imperialism.

“Basically, America has had the Wolfowitz doctrine to contain countries like China and Russia.”

He goes on to highlight the new emerging geo-political order where emerging powers China and Russia grow ever closer. There was plenty of Asian media attention on Premier Xi’s visit to Russia.

In contrast, Britain’s election was regarded by western and some international media as being important. Faber believes there is evidence that the global influence of the UK and the U.S. is in decline.

He cites China and Russia’s ever-closer relationship as being more important than the the relative insignificance of Britain’s election and suggests China and Russia’s increasing power is a “new world order.”

He says that it may be that the EU will, until the eleventh hour, make threats and jawbone Greece in order to extract the best terms. Ultimately, however, they are left with little choice but to bail Greece out and postpone the inevitable for a little while longer.

Dr. Faber’s lucid analysis indicates that from both an economic and geopolitical point of view the world and particularly Europe, is in a vulnerable position.

He has previously advised readers and clients to act as their own central bank and buy physical precious metals (gold, silver, platinum and palladium) as a hedge against currency depreciation and geopolitical crises. Faber believes that storing gold in Singapore is the safest way to own gold today.

Interview Transcript

Dr Marc Faber:

I don’t think it’s about Greece economically. It’s about the ECB and European banks that have lent money to Greece and if Greece defaults would have to take a huge loss and write-off. So they will lend more money and kick the can down the road.

Number 2; and this is overlooked by many people, it’s a political issue. If Greece leaves; or if Portugal leaves; or if Spain leaves; or if anyone leaves; the NATO countries led by America, basically, are very afraid that either the Russians establish closer relationship…. you have to look at the geography of Eastern Europe. You have the northern part of the Mediterranean – The Black Sea. And there you have Crimea Island and to the east of Crimea Island you have Eastern Ukraine.

The Russians will never give up Eastern Ukraine. It’s like the Chinese will not give up Hainan Island, you understand? It’s not going to happen under any condition. The West can bitch and talk and whatever they want – they’re not going to give it up.

CNBC:

I’m trying to figure this out – what has this to do with Greece not leaving the EU?

Dr Marc Faber:

Well this is what i am trying to explain to you because you have little knowledge of the Eastern European geography. from The Black Sea the Russian fleet can move into the Mediterranean and without that, they can’t – they have no access to the Mediterranean, without The Black Sea and Crimea.

And in the Mediterranean you have first Turkey, Moldavia and then Greece…and Greece is a very strategically important part of Europe.

CNBC

So you’re saying that at any cost the EU will make sure Greece stays in so Putin can’t get his hands….cannot recapture the glory of the Soviet Union…?

Dr Marc Faber:

Basically, America has had the Wolfowitz doctrine to contain countries like China and Russia. And why do you think is? Xi in Russia and is prominently featured with Putin? This is the new world order. And Americans and the western countries – You just had the news on Cameron. You look at Cameron. What interest is he to the people of the world? Britain is no longer an empire – it’s a degenerated country….Britain is a great country but economically it’s completely meaningless.

CNBC Interview here

Must View Investment Webinar with Dr Faber here

MARKET UPDATE

Today’s AM LBMA Gold Price was USD 1,184.75, EUR 1,062.20 and GBP 768.37 per ounce.

Friday’s AM LBMA Gold Price was USD 1,185.25, EUR 1,054.26 and GBP 767.46 per ounce.

Gold climbed $5.60 or 0.47 percent on Friday to $1,188.50 an ounce, and silver rose $0.17 or 1.04 percent to $16.48 an ounce.

Gold rose 1.2% on the week and silver was 2.1% higher on the week. Gold finished higher on Friday and had a weekly gain in dollars after a volatile week which saw sharp losses in government bond markets.

Yemen’s militias and the Saudi army traded heavy artillery and rocket fire in border areas today, a day before a five day humanitarian truce was due to take effect. The Houthis said they fired Katyusha rockets and mortars on the Saudi cities of Jizan and Najran on Monday, after the Saudis hit Saada and Hajjah provinces with some 150 rockets.

Warnings of an accidental default loom over debt swamped Greece as Prime Minister Tsipras’ anti-austerity government heads for another confrontation with an increasingly testy German-led bloc of creditors.

German Finance Minister Schaeuble and his Greek counterpart Varoufakis meet in Brussels this lunch time ahead of a Eurogroup meeting of Eurozone finance ministers, a spokesman for the German finance ministry said. A time was not confirmed the spokesman said it would be before the gathering starts at 1300 GMT.

Breaking News and Research Here

(courtesy Chris Powell/GATA)

Nazis invented currency market rigging, U.S. perfected it, GATA secretary tells KWN

Submitted by cpowell on Sat, 2015-05-09 00:29. Section: Daily Dispatches

8:30p ET Friday, May 8, 2015

Dear Friend of GATA and Gold:

Interviewed today by King World News, your secretary/treasurer said that currency market rigging is the primary mechanism of imperialism, invented by Nazi Germany for its exploitation of occupied Europe during World War II and perfected by the United States afterward. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/is-this-the-most-shocking-interview-of-2015/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Alasdair Macleod writes that the bad debt on the books of the Greek banks are equal to 22%-165% of bank equity. What is worse is that the majority of assets on the books of the Greek banks is the sovereign Greek bonds held up them. If the Greek government defaults then the banks are a nanosecond behind them:

(courtesy Alasdair Macleod)

Bond Yields Rise And Greece Failing

The gold price and silver price initially rallied this week from the lows of $1170 and $15.93 respectively last Friday to challenge the $1200 level for gold and $16.70 for silver on Wednesday, before losing about half these gains yesterday.

On the year gold, is now hardly changed while silver is up 5% and is one of the best performing assets in financial markets over this timescale.

Precious metals appear to be locked into the same torpor as other markets, but there are two developing stories. At the beginning of this week government bond yields were low with negative rates commonplace, despite record government borrowing. Rational investors are barely involved in bond markets, remaining for the most part side-lined in the knowledge these distortions cannot last forever.

However, as the week progressed, a reaction in US Treasuries set in with the yield on the US 10-year Treasury rising sharply to 2.29%, shown in the chart below (though a reaction to 2.19% set in this morning). The dotted line is the neckline of a head-and-shoulder reversal chart pattern now completed, suggesting Treasury yields might be at risk of rising significantly higher, taking other bond markets and lower-grade bonds with them.

Since early February 10-year Treasury yields have risen 37%, implying large portfolio losses for the banks loaded up with sovereign debt. This week has seen similar rises in other key sovereign bond yields, and the losses in investment-grade and junk bonds have been correspondingly greater. The importance of this development for precious metals is that deteriorating bond markets increase the likelihood of new rounds of quantitative easing.

It could be that at last bond markets are beginning to discount the growing likelihood that Greece will default on its debt and that the Greek banks will fail. This is the second developing story, also likely to affect gold and silver.

Professor Steve Hanke of John Hopkins University recently pointed outthat at the end of last year the book value of bad debts on the Greek banks’ balance sheets exceeded the sum of tangible bank equity and reserves by between 22% in the case of the National Bank of Greece, to as much as 165% in the case of Piraeus Bank, with other banks falling in between these extremes. Furthermore in the last five months deposit withdrawals have accelerated, making the position worse. This being the case, not only are Greece’s banks insolvent, but Greece has the potential to be Europe’s “Lehman moment”, with all the unintended consequences implied.

Greece’s default and the failure of its banking system now seem inevitable. The remaining question is what monetary support the ECB will offer to prevent other Eurozone bond yields from rising further, and what assistance it will extend to highly-geared Eurozone banks whose own viability may be threatened.

Lastly, the UK’s unexpected election result this morning initially boosted sterling. Whether or not it holds this rise only time will tell.

end

Announcement from Bill Holter:

1 Chinese yuan vs USA dollar/yuan strengthens to 6.2084/Shanghai bourse and Hang Sang up

2 Nikkei closed up by 241.72 points or 1.25%

3. Europe stocks mostly down/USA dollar index up to 95.06/Euro falls to 1.1159/

3b Japan 10 year bond yield: huge fall to .40% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 119.12/

3c Nikkei still just above 20,000

3d USA/Yen rate now just below the 120 barrier this morning

3e WTI 58.99 Brent 64.63

3f Gold down/Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt. Last night Japan refused to increase it’s QE

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to 53.0 basis points. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate falls slightly to 20.57%/Greek stocks down 3.46%/ still expect continual bank runs on Greek banks.

3j Greek 10 year bond yield rises to: 10.73%

3k Gold at 1187.00 dollars/silver $16.45

3l USA vs Russian rouble; (Russian rouble down 6/10 rouble/dollar in value) 51.40 , the rouble is still the best acting currency this year!!

3m oil into the 58 dollar handle for WTI and 64 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 93.27 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0420 well below the floor set by the Swiss Finance Minister.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving further away from negativity at +.53/the ECB losing control over the bond market.

3s This week the ECB increased the ELA to Greece by another large 2.0 billion euros. The new maximum is 78.9 billion euros. The ELA is used to replace depositors fleeing the Greek banking system. The bank runs are increasing exponentially. The ECB is contemplating cutting off the ELA which would be a death sentence to Greece and they are as well considering a 50% haircut to all Greek sovereign collateral which will totally wipe out the entire Gr. banking and financial sector.

3t Greece paid the 200 million euros owed to the IMF as interest payment on Wednesday. They need another 700 million plus payment to the ECB on Tuesday.

3 u. If the ECB cuts off Greece’s ELA they would have very little money left to function.

4. USA 10 year treasury bond at 2.17% early this morning. Thirty year rate well below 3% at 2.92%/yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy zero hedge/Jim Reid Deutsche bank)

Futures Jittery As Attention Returns To Greece; China Stocks Rebound On Latest Central Bank Intervention

With the big macro data out of the way, attention today and for the rest of the week will focus on the aftermath of the latest Chinese rate cut – its third in the past 6 months – which managed to boost the Shanghai Composite up by 3% overnight but not nearly enough to make up for losses in the past week; any resumption of the 6+ sigma volatility in the German Bund, which already has been jittery with the yield sliding to 0.52% only to spike to 0.62% shortly thereafter before retracing some of the losses; and finally Greece, which in a normal world would have concluded its negotiations during today’s Eurogroup meeting and unlocked up to €7 billion in funds for the coming months. Instead, Greece may not only not make its €770 million IMF payment tomorrow but according to ever louder rumors, is contemplating a parallel currency on its way out of the Eurozone.

This is how DB’s summarized the latest news out of Greece:

Greece will no doubt be front and centre at today’s Eurogroup meeting, however the likelihood of any material outcome looks fairly slim with more ‘progress’ likely to be a popular term used by officials in both camps. One topic which we await news on is the potential for increased haircuts on Greek collateral, which may or may not come to fruition depending on just how much ‘progress’ is made at today’s meeting. There was little in the way of new news over the weekend on the subject. Instead, German finance minister Schaeuble was quoted as warning that ‘experience in other parts of the world has shown that a country can suddenly slide into bankruptcy’ in German press FAS, while Eurogroup President Dijsselbloem reiterated that today’s meeting ‘won’t be decisive’. Perhaps of more interest, pressure appears to be growing internally from German Chancellor Merkel’s Christian Democratic Party to give up on Greece for the sake of the single currency with arguments suggesting that the Euro will be stronger should Greece leave (Bloomberg). As well as digesting European official commentary on just how much progress is being made post today’s meeting, one eye will also be on tomorrow’s €750m IMF repayment with Greek press Ekathimerini commenting that some Greek officials are in favour of not repaying should today’s meeting be deemed ‘not satisfactory’.

Back to Asia, where stocks rose in reaction to Friday’s NFP-miss and its implications on rate expectations, with the surprise PBoC rate cut further bolstering the Shanghai Comp (+3%) and Hang Seng (+0.5%). Nikkei 225 (+1.3%) rose with broad gains. However large tech names such as Sharp (-23%) and Toshiba (-16%) have witnessed its largest decline since 1974 and 2011 respectively, with Sharp reaching limit down amid reports that the Co. is mulling cutting capital by 99%, while Toshiba withdrew its FY 2015 forecast amid an ongoing accounting probe. JGB’s rose following Friday’s spill over buying in UST’s as yields fell with prospects that the Fed will keep rates lower for longer.

Focus turns to Greece with the market expecting today’s Eurogroup meeting to be downbeat after comments from Eurogroup President Dijsselbloem stating that the meeting will not see any accord reached on Greece. Greek banks have been pressured with the tomorrow’s pending EUR 750mln IMF debt repayment dragging the Athens Stock Exchange (-3.5%) lower while Greek bonds remain sideways and Bunds under selling pressure after a bout of technical selling. Meanwhile, source comments suggested that a senior Greek official called Treasury Secretary Jack Lew and said that Greece may not pay EUR 750mln back to the IMF, however Washington believes this is a bluff, according to sources. Furthermore, a senior Greek official stated that they do not have a ‘plan b’ and reiterated that the debt-stricken nation will reach its debt obligations. This uncertainty has caused European equities (Eurostoxx50 -0.9%) to reside in negative territory with the exception of the FTSE 100 (+0.3%), as basic materials are supported by the PBOC conducting further stimulus after cutting their 1 year lending rate and raising their deposit rate by 25bps to 5.1% and 2.25% respectively in an attempt to combat lacklustre inflation and growth in the world’s second largest economy. Furthermore, BMW (-0.6%) and Daimler (-0.3%) are seen lower after Chinese car sales are at its lowest level since Feb 2013 as Chinese consumers opt for domestic auto names.

The USD-index has gained ground on the major pairs across the board with the EUR exhibiting broad-based weakness amid uncertainty regarding Greek finances with source comments suggesting that Greece may not have enough funds after tomorrow’s IMF payment. GBP/USD has shrugged off the post-election euphoria and is seen lower with focus switching to today’s BoE rate decision which is not scheduled at its usual day of Thursday given the UK election disruption. NZD is the session’s laggard as participants continued to bring forward rate cut expectations, with OIS markets now pricing in an 46% chance of a 25bps rate cut at the June meeting. NZD/USD broke below 0.7400 and is on course for its largest decline since March 6th, with tech cross-related selling spurred by NZD/JPY breaking below its 200 DMA (0.8923) and AUD/NZD testing 1.0700 to the upside to trade at 2-month highs. Elsewhere, there are some large FX options today in AUD/USD at 0.7800 (3.8bln), NZD/USD at 0.7525-30 (1bln) and USD/JPY at 120.00 (2.3bln), 121.00 (1.7bln) due to roll of at the 1500BST NY cut.

WTI (-0.3%) and Brent crude (-0.3%) futures trade marginally lower alongside the stronger USD-index (+0.2%), where spot gold is also weighed upon in what has been an uninspiring session in the commodity complex due to a lack of fundamental news. Copper declined overnight as participants booked profits following the bull market rally seen last week, while Dalian iron ore futures rose by over 1% in tandem with Chinese steel prices after the PBoC surprise rate cut over the weekend.

In summary: European shares little changed with the autos and health care sectors underperforming and basic resources, retail outperforming. Euro-area finance ministers meet today to discuss aid to Greece. German 10-year bond yields resume rise. China cuts interest rates for 3rd time in six months. The French and German markets are the worst-performing larger bourses, the U.K. the best. The euro is weaker against the dollar. German 10yr bond yields rise; Japanese yields decline. Commodities little changed, with Brent crude, WTI crude underperforming and nickel outperforming.

Market Wrap

- S&P 500 futures down 0.1% to 2105.8

- Stoxx 600 down 0.1% to 399.8

- US 10Yr yield up 2bps to 2.17%

- German 10Yr yield up 3bps to 0.58%

- MSCI Asia Pacific up 0.3% to 151.7

- Gold spot down 0.1% to $1187.3/oz

- 37.7% of Stoxx 600 members gain, 60.5% decline

- Eurostoxx 50 -1%, FTSE 100 +0.2%, CAC 40 -1.5%, DAX -0.6%, IBEX -0.2%, FTSEMIB -0.6%, SMI -0.2%

- Asian stocks rise with the Shanghai Composite outperforming and the ASX underperforming.

- MSCI Asia Pacific up 0.3% to 151.7; Nikkei 225 up 1.2%, Hang Seng up 0.5%, Kospi up 0.6%, Shanghai Composite up 3%, ASX down 0.2%, Sensex up 1.5%

- Bonderman’s TPG Purchases Cushman & Wakefield for $2 Billion

- Euro down 0.35% to $1.116

- Dollar Index up 0.3% to 95.08

- Italian 10Yr yield up 6bps to 1.74%

- Spanish 10Yr yield up 6bps to 1.72%

- French 10Yr yield up 4bps to 0.87%

- S&P GSCI Index up 0.1% to 444.6

- Brent Futures down 0.3% to $65.2/bbl, WTI Futures down 0.3% to $59.2/bbl

- LME 3m Copper up 0.1% to $6396/MT

- LME 3m Nickel up 1% to $14450/MT

- Wheat futures up 0.2% to 482.5 USd/bu

Bulletin Headlin Summary from RanSquawk And Bloomberg

- The PBoC have once again cut rates, with a 25bps cut to the 1-year lending and deposit rates in an attempt to revive inflation and export/import growth

- Downbeat expectations of today’s Greek Eurogroup meeting and ongoing uncertainty regarding Greek funds are weighing on European equities

- In terms of today’s Eurogroup meeting, arrivals are scheduled for 1500BST/0900CDT, roundtable at 1530BST/0930CDT and no time given for the press conference but historically begins at 1900BST/1300CDT

- Looking ahead today’s calendar is particularly light with the sole highlights being the BoE rate decision and Eurogroup meeting

- Treasuries decline with bunds and gilts as euro-area finance ministers meet to discuss Greece; $64b quarterly refunding this week, starting with $24b 3Y notes tomorrow.

- China’s central bank cut interest rates for the third time in six months as it ratchets up support for an economy grappling with a debt overhang and property slump; China’s stocks rallied the most in two weeks

- PBOC dismissed idea of introducing QE, MNI reports

- Greek PM Tsipras’s anti-austerity government heads for another confrontation with an increasingly testy German-led bloc of creditors as warnings of an accidental default loom over his debt-swamped nation

- Troika doesn’t expect positive outcome from talks; its plans on Greece include one positive, three negative scenarios, Welt newspaper reports, citing an unidentified negotiator

- Merkel is coming under growing pressure from within the ranks of her own party bloc to give up on Greece for the sake of the euro

- Greece needs at least a symbolic show of progress today to persuade ECB to keep emergency funding flowing to nation’s banks; EU750m due to IMF tomorrow. Click here for Greece debt distribution

- Greece’s ballooning debt load is casting doubt over the IMF’s role in future bailouts; IMF typically needs debt to be sustainable and, with the economy faltering, Greece is heading in the wrong direction

- Saudi Arabia said its new king won’t attend this week’s long-planned summit for Persian Gulf countries at the U.S. presidential retreat; comes as Obama tries to restore flagging confidence of Gulf Arab leaders in U.S. leadership

- Sovereign bond yields rise. Asian stocks higher, European stocks, U.S. equity-index futures lower. Crude oil, gold lower, copper higher

DB’s Jim Reid concludes the overnight recap

The great thing about the UK opinion poll companies is that they are now making us strategist and economists look very good at our jobs. As a final word on the UK election, on Thursday I discussed how the polls argued that it would be the first election since 1918 that neither of the main two parties would receive 35% of the vote. Well the Conservatives polled 36.9% shocking the pollsters. However behind the scenes it was a still an election of extremes. In Scotland the Labour party has had a minimum of 40 seats for the last 51 years. On Friday morning they were left with 1 and the Scottish Nationalist Party with 56 out of 59. UKIP ended up with 3.88 million votes (12.6%) and came second in 120 seats. Interestingly the SNP achieved 55 more seats than UKIP with 2.43 million less votes. In the end perhaps the winning Conservatives weren’t loved but the alternative of a Labour Party keen to move pretty left wing (e.g. price/rent controls, a suspicion of big business and notably higher taxes for the wealthy) wasn’t appealing to voters in an economy with quite a low unemployment rate, a growing economy but with a fragility caused by high debts. The point on the economy is key as this still remains the best way for politicians to get elected. Europe, with its still structurally high unemployment rate and limited domestic policy tools is certainly not out of the woods in terms of more non-mainstream political shocks over the years ahead. The cyclical recovery of 2015 will probably save Spain from such an outcome at the end of the year but the wider threat hasn’t gone away.

Before the election, the ‘Brexit’ EU referendum risk was a key question from clients. The UK will now hold one by 2017 which could eventually create much more nerves than the Scottish independence referendum last year. It’s worth pointing out though that an opinion poll (Survation for the Mail on Sunday) over the weekend suggested that 45% want to remain and 38% want to leave (with the remaining 18% unsure). However at the peak of the Euro crisis in 2012 the polls consistently suggested 50% wanted to leave the EU and only around 30% to stay (YouGov). It’s only the recovery in the UK economy and the gradual return to stability in Europe that has turned the tide. So a lot can happen by 2017 but it shows again that the economy on both sides of the channel at the time will likely decide the vote. So if you want to know the outcome ask an economist to predict the economy in 2017 and as we know they are now far above pollsters in the forecasting pecking order!!

Onto markets now and firstly to China where over the weekend the People’s Bank of China has cut the benchmark deposit and lending rates by 25bps and also lifted the ceiling of deposit rates to 1.5x of the benchmark rate (from 1.3x previously) – which in turn is another significant step forward in interest rate liberalization. The moves come on the back of slightly softer than expected inflation data out on Saturday (+1.5% yoy vs. +1.6% expected) and continued downward pressure on the PPI (-4.6% yoy vs. -4.5% expected). Our China Economist Zhiwei Zhang believes that there is now a stronger sense of urgency in policy circles and has revised his interest rate call for two more cuts in 2015 (one in June and another in Q3) as well as one more RRR cut in Q3. Zhiwei also highlights that he does not expect China to replicate exactly the QE policies in developed countries, but that the PBOC will highly likely get involved in financing the fiscal gap in order to stop issuance driving up market interest rates and slowing growth. On the growth side, Zhiwei maintains his view that growth may slow to 6.8% in Q2 and rebound to 7.0% in Q3 and 7.2% in Q4, before then decelerating to 6.7% in 2016.

In terms of the early reaction in the Asia timezone, the Shanghai Comp and CSI 300 are +1.18% and +1.09% respectively on the back of the news while China 5y CDS is around 2bps tighter. The stronger US session on Friday along with the PBOC moves appear to be fueling a better sentiment generally across most markets in Asia this morning. The Nikkei (+1.17%), Hang Seng (+0.50%) and Kospi (+0.77%) are all up as we go to print and Asia credit markets are around 2bps tighter.

Greece will no doubt be front and centre at today’s Eurogroup meeting, however the likelihood of any material outcome looks fairly slim with more ‘progress’ likely to be a popular term used by officials in both camps. One topic which we await news on is the potential for increased haircuts on Greek collateral, which may or may not come to fruition depending on just how much ‘progress’ is made at today’s meeting. There was little in the way of new news over the weekend on the subject. Instead, German finance minister Schaeuble was quoted as warning that ‘experience in other parts of the world has shown that a country can suddenly slide into bankruptcy’ in German press FAS, while Eurogroup President Dijsselbloem reiterated that today’s meeting ‘won’t be decisive’. Perhaps of more interest, pressure appears to be growing internally from German Chancellor Merkel’s Christian Democratic Party to give up on Greece for the sake of the single currency with arguments suggesting that the Euro will be stronger should Greece leave (Bloomberg). As well as digesting European official commentary on just how much progress is being made post today’s meeting, one eye will also be on tomorrow’s €750m IMF repayment with Greek press Ekathimerini commenting that some Greek officials are in favour of not repaying should today’s meeting be deemed ‘not satisfactory’.

After another hugely volatile week for global bond markets last week in which we saw 10y Bunds hit a 5-month high in yield at 0.775% intraday on Wednesday having started the week at 0.373%, yields actually closed lower for the first time since April 24th as 10y Bunds closed -4.3bps tighter at 0.547%. Other core European bond markets were firmer as 10y yields in Netherlands, Sweden, Switzerland and France closed -4.5bps, -4.2bps, -8.0bps and -5.9bps respectively. Peripherals were also some 8-12bps tighter at the close. There were similar moves in Treasuries meanwhile as the benchmark 10y closed 3.2bps tighter at 2.148% as Friday’s payrolls largely dictated price action.

With equity markets also having a better day as the S&P 500 (+1.35%), Dow (+1.49%), Stoxx 600 (+2.87%) and DAX (+2.65%) all climbed and credit markets firmed (CDX IG +3bps), it’s probably fair to say that the +223k reading (vs. +228k expected) offered a little something for both the hawks and the doves with the better tone generally across most markets. The improved April number also came on the back of a downward revision to the already low March print (revised down 39k to +85k) which made it the lowest reading since June 2012. The hawks will no doubt point to the April reading being suggestive of a more supportive growth profile for Q2 and therefore keeping the September timeframe firmly in play, however the lack of improvement in wage growth, as evidenced by the lower than expected growth in average hourly earnings (+0.1% mom vs. +0.2% expected) will mean the doves will continue to point towards the 2016 timeframe. In terms of the reaction in Fed Funds contracts, the Dec15 contract closed 3bps tighter at 0.320% while the Dec16 (-8.5bps) and Dec17 (-9.5bps) contracts fell to 1.080% and 1.705% respectively.

Elsewhere, the unemployment rate dropped as expected by one-tenth of a per cent to 5.4%, while later in the day wholesale inventories (+0.1% mom vs. +0.3% expected) and trade sales (-0.2% mom vs. +0.5% expected) both disappointed. Our US colleagues noted in fact that the weaker wholesale inventories report could lead to Q1 real GDP being revised down to -0.8% compared to their prior estimate of -0.5% on the back of the weaker trade data.

It was fairly light data-wise in Europe on Friday. The notable releases came out of Germany where industrial production (-0.5% mom vs. +0.4% expected) came in well below expectations and the German trade balance surplus (€23bn vs. €20bn expected) printed higher than expected in March following a better than expected exports reading (+1.2% mom vs. +0.4% expected) in particular. Back to the industrial production print, following the weak number our European colleagues have now lowered their Q1 GDP forecast to +0.6% qoq after a previous call of +0.8%, although still a tad ahead of the current market consensus (+0.5% qoq) with the reading due on Wednesday. The view reflects the fact that construction did not benefit as much from the mild winter and pull-forward effects as expected. However, on the flip side, this means that Q2 growth will not be affected by a strong counter movement to Q1 construction and they now see Q2 growth at +0.4% qoq instead of +0.2% about in line with PMI and IFO data.

Running through this week’s calendar now, it’s a quiet start data wise in Europe this morning with no releases expected, but today’s Eurogroup meeting will be key in determining where Greece and its creditors negotiations currently stand. Over in the US this afternoon, it’s the usual post payrolls lull with just the labor market conditions data expected. We kick off in Japan tomorrow with leading and coincident index prints, before we move onto the European timezone where we see French business sentiment and UK industrial and manufacturing production. Focus in the US on Tuesday will be on the JOLTS report as well as the monthly budget statement. The NFIB small business optimism survey is also due. It’s a busy start in Asia on Wednesday as we get trade data out of Japan as well as retail sales, industrial production and fixed assets investment readings in China. It’s no less busy in Europe where we see Euro area Q1 GDP (advanced reading) and industrial production as well as German Q1 (provisional) GDP and the final April CPI print. Over in France, we also get CPI data along with employment indicators. In the UK we get the BoE inflation report as well as the usual monthly employment data dump including unemployment and average weekly earnings. In the US on Wednesday, April retail sales will be the main highlight while the import price index is also due. Its quiet data wise on Thursday with no notable releases in Asia or Europe while in the US PPI and jobless claims prints are expected. It’s a similarly quiet end to the week on Friday with just Japan PPI and consumer confidence due in the early session, followed by US industrial and manufacturing production, capacity utilization and the University of Michigan consumer sentiment print. Fedspeak wise we’ve got Williams expected to talk on Tuesday while earnings seasons creeps to an end with 15 S&P 500 companies due to report and 56 Stoxx 600 companies expected.

end

China cuts its rates again as the global economy is in big trouble.

As you will see below, the Chinese Shipping rate index falls to 17 year lows:

(courtesy zero hedge)

China Cuts Rates (Again) In Desperate Bid To Buoy Stocks, Rescue Economy

For the third time since November, China has cut its benchmark lending rate.

Hours ago, the PBoC slashed the 1-year lending rate by 25bps to 5.1% and the 1-year deposit rate to 2.25%. The move comes just three weeks after Beijing cut the reserve requirement ratio for the second time this year and marks a continuation of a heretofore unseen trend in China: easing into a stock market rally.

From the PBoC announcement:

The further decline in deposit and lending rates, the focus is to continue to play a leading role in a good benchmark interest rate, the cost of financing to further promote the social downside, support sustained and healthy development of the real economy. According to the unified deployment of the State Council, November 2014 and March 2015, the People’s Bank has twice lowered the financial institutions lending and deposit benchmark interest rate. With the gradual implementation of the policy measures, financial institutions, lending rates continued to decline, the market interest rates dropped significantly, the overall social financing costs decreased. At present, the domestic economy accelerated restructuring, fluctuations in external demand, China’s economy is still facing greater downward pressure. Meanwhile, the overall level of domestic prices remain low, real interest rates are still higher than the historical average for the continued appropriate use of interest rate instruments to provide space. In view of this, the People’s Bank of China decided as from May 11, 2015, loans and deposits of financial institutions lowered the benchmark interest rate by 0.25 percentage point, to create a neutral appropriate monetary and financial environment for economic structural adjustment and restructuring and upgrading.

As we noted when the RRR cut hit last month, the country’s latest easing measures come as Beijing faces an increasingly perilous economic situation characterized by shifting demographics, a tough transition from investment to consumption, and slumping exports. To the latter point, the country has found itself stuck between the proverbial rock and a hard place as $300 billion in capital outflows over the last four quarters (and an IMF SDR bid) make yuan devaluation an unpalatable tool for countering slowing export growth. As such, lowering policy rates is seen as the preferable option for supporting the stalling economy.

Against this backdrop, and with the latest data on PPI inflation (or, more appropriately, deflation) adding fuel to the fire, further easing was a foregone conclusion. Here’s Barclays:

PPI deflation and soft CPI inflation point to persistent deflation risks. On the back of weakening economic growth and rising deflation risks, we note a shift in the PBoC’s monetary policy bias towards more easing since March, along with the government’s stepped-up policy easing in other areas including fiscal policy and the property sector. It is worth noting that the PBoC has guided the reverse repo rate lower five times by a total of 50bp since March, which has resulted in a sharp drop in the 7d repo rate to 3.0% from 4.8%. The still elevated cost of funding, down only 10-20bp in Q1 despite the 65bp of cuts in the benchmark lending rate since November, point to the need of further monetary easing. We maintain our call for one additional 25bp benchmark rate cut in Q2 and look for two more 50bp RRR cuts in 2015, with the risk of more if growth continues to disappoint.

And a bit more color from Reuters:

Economists had said it was not a matter of if, but when China eased policy again after economic growth in the first quarter cooled to 7 percent, the slowest pace since 2009.

Some market watchers had even said the central bank was risking falling behind the curve in responding to rapidly deteriorating conditions.

Initial indicators and industry surveys for April released over the last few weeks had pointed to a further loss of momentum heading into the second quarter.

“Currently, the pace of domestic economic restructuring is quickening and the fluctuation of external demand is relatively big. China’s economy is still facing relatively big downward pressure,” the central bank said.

“This is not a surprise. The consumer inflation reading for April was lower than expected and employment faces downward pressures,” said Lin Hu, an economist at Guosen Securities in Beijing.

“But the effectiveness of the rate cut won’t be very big, it may (only) help stabilize expectations. Fiscal policy should be stepped up and there will be further monetary policy easing if economic data continues to underwhelm. We expect the worst could be over after the second quarter and growth may stabilize in the third or fourth quarters as the property sector recovers.”

Although there’s no question that China’s economy is sputtering and that growth is probably running well short of the official 7% headline figure, we would ask the same question we asked on the heels of last month’s RRR cut.Namely, is it really about the economy? At the time, we said the following:

Recall that on Friday Chinese equity futures crashed after the close following news that the China Securities and Regulatory Commission (CSRC) put out an announcement which tightened up rules governing certain trading on margin while simultaneously liberalized rules on short selling.

Coincidentally, it was just last Tuesday that brokerages such as CITIC Securities Co Ltd, Haitong Securities Co Ltd and Huatai Securities Co Ltd tightened requirements for margin financing in an effort to “control risks.” The result: Chinese stocks promptly suffered their biggest drop since January, falling more than 4.1%.

We wonder then, if Beijing is taking its cues from stocks or from the economy and because this looks like deja vu all over again, we’ll close with exactly what we said three Sundays ago:

Expect last week’s selloff to be more then BTFDed as soon as China opens for trading in a few hours, and the SHCOMP to surge even higher and to even more unsustainable, and centrally-planned levels, merely pushing back the day of reckoning by a few weeks or months, as yet one more bank scrambles to preserve the “wealth effect” by artificially pushing its stock market higher.

China’s Container Shipping Index Hits 17-Year Low, Import/Export Volumes Plummet

by Wolf Richter • May 9, 2015

When the Reserve Bank of Australia cut its cash rate target to a record low of 2.0% this week, it specifically blamed the slowdown in China. It is the key market for Australia’s most important exports, such as iron ore, whose price has plunged due to slowing demand in China, dragged down by a number of factors, including weak exports of manufactured goods to slowing economies around the globe.

Trade moves in wobbly circles.

So today, China’s General Administration of Customs announced that imports had plunged 16.2% in April from a year ago, after they’d already plunged 12.7% in March (hence the fretting by the Reserve Bank of Australia). And exports dropped 6.4% from a year ago, after they’d plummeted 14.6% in March.

Analysts, who apparently never look at the collapsing shipping rates from China to certain parts of the world, had inexplicably expected exports to rise 2.4%. So the drop was “unexpected.”

The morose economic climate was unexpected apparently even at the very top in China: Reuters was told by “policy insiders” that China’s leaders were “caught off guard by the sharpness of the downturn.”

That hasn’t kept the Chinese stock market from soaring 75% over the past six months, despite the 5% swoon this week, the worst weekly loss in five years.

And so rumors of more stimulus of one kind or another have been circulating. Stimulating demand by creating more credit and building more high-speed rail lines and subway systems and allowing local governments to borrow more to build even more overcapacity is one thing. But stimulating demand in other countries is quite another. And that’s one of the sources of the China slowdown.

Exports to the US inched up 3.1% in April from a year ago, not exactly a dizzying pace. But exports to the EU plunged 10.4%.

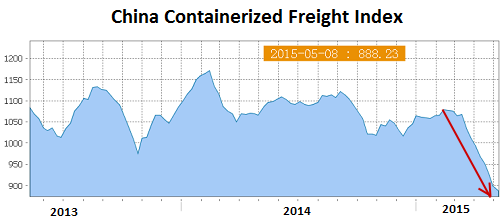

The collapse of containerized freight rates from China to Europe have reflected that kind of drop in exports for two months, and I have been hammering on it [most recently a week ago]. And freight data released today are even worse.

The China Containerized Freight Index (CCFI), operated by Shanghai Shipping Exchange and sponsored by the Chinese Ministry of Communications, tracks spot and contractual freight rates from Chinese container ports for 11 shipping routes across the globe, based on data from 16 global carriers. According to the SSE, it’s considered “the second world freight index” after the Baltic Dry Index.

And it skidded again. The index for the week just ended dropped another 11 points, or 1.2%, from the prior week to a new multi-year low of 888. It’s down 17% since mid-February. This is what the 2-month plunge looks like:

How ugly is this? The index was set at 1,000 on January 1, 1998. Today, the index is 11% below where it was 17 years ago, a journey it accomplished in two months!

Trade is a circular machine. Manufacturing and export economies, like China, import commodities and export manufactured goods. The plunge in imports is an all-around terrible reflection of demand in China, despite the still relatively glorious and most likely illusory 7% GDP growth bandied about by the government.

But the slowdown in exports is a sign of slowing demand in other parts of the world, particularly in Europe, where the purposeful devaluation of the euro is sinking in. Tough times ahead, not only for China.

As if a toggle switch had been flipped late last year, Americans suddenly gained confidence in the economy, to levels not seen since before the Financial Crisis. But now, it’s all unraveling. And the culprits are being lined up. Read… Confidence in the US Economy Plunges

end

Sunday:

It looks inevitable that Greece will default. The the fun begins;

(courtesy zero hedge)

Merkel Under Pressure To Let Greece Go As Default Risk Rises

In case you forgot, Greece is on the brink of insolvency and without an agreement with creditors in the very near future, will default on its obligations to either the IMF, the ECB, its own citizens, or all of the above. The most pressing concern is a €750 million payment due to the IMF on Tuesday, a payment Greek FinMin Yanis Varoufakis says Athens will make, although it doesn’t seem as though anyone has a clear idea about exactly where the money will come from.

The important headlines from last week included anapparent split between the IMF and the rest of the Troika on what constitutes an acceptable list of reforms, a report that Greek banks were being cut off from interbank trading, and news that Varoufakis had distributed a Greek recovery “blueprint” containing estimates and assumptions that bore little resemblance to figures presented by PM Tsipras and his reshuffled negotiating team.

Now, with less than 48 hours to go until three quarters of a billion euros comes due to the IMF, Greece faces marathon negotiations on Monday with eurozone FinMins including the incorrigible, hot-tempered Wolfgang Schaeuble who made a splash on Saturday when he suggested that Athens may default “by accident” if the government continues to vacillate.

Via FAZ (Google translated):

Federal Finance Minister Wolfgang Schäuble has warned of the possibility of surprising Greek default. “Experiences elsewhere in the world have shown that a country can suddenly slip into insolvency,” Schaeuble told the Frankfurter Allgemeine Sonntagszeitung (FAS). He wanted a date in his first newspaper interview since detailed months but not speculate.

When asked whether the government had made preparations for such an eventuality, he said: “There are issues that can not answer a sensible politician. Otherwise there will be misunderstandings. Jean Claude Juncker once said, one must not take it then sometimes the truth always as accurate. I see these things more complicated. Therefore I say to prefer nothing at all. “

And while Schaeuble indicated that if Greece left the euro it would not be “because of” Germany, Bloomberg isreporting that Chancellor Merkel’s own party bloc now supports a Greek exit. Here’s more:

Members of Merkel’s Christian Democratic bloc are openly challenging her stance of keeping Europe’s most-indebted country in the 19-nation currency region. Even some officials in the Finance Ministry are leaning toward the conclusion that the euro area would be better off without Greece, two people familiar with the matter said.

“The euro would be strengthened if Greece left,” Alexander Radwan, a Merkel-affiliated lawmaker who voted for granting Greece a temporary extension of its bailout in February, said in an interview. “The other countries could then move closer together and apply the rules more strictly.”

With European finance ministers due to resume talks on Greece on Monday, hardening sentiment in Germany risks sending mixed signals to investors as Prime Minister Alexis Tsipras’s government attempts to reach a deal with creditors.

Merkel has repeatedly voiced public support for keeping the country in the euro, partly for geopolitical reasons. Other officials in her government view Greece as a rule-breaker and a drag on the region’s economy, said the people, who asked not to be named discussing the deliberations.

Finance Minister Wolfgang Schaeuble, a prominent German advocate of European unity for decades, has given plenty of signs of exasperation with Greece since Tsipras and Finance Minister Yanis Varoufakis took office in January on an anti-austerity platform.

Clearly, any statement from the Eurogroup on Monday has the potential to move markets, but we would also note that the ECB last week reserved judgement on hiking haircuts on collateral pledged by Greek banks for ELA until after tomorrow’s meeting. So although there’s probably room to extend and pretend from a political perspective, any move by the ECB to tighten the screws on the Greek banking sector could cause the situation to deteriorate rapidly and indeed, if an ECB ELA decision that’s ostensibly designed to push negotiations forward inadvertently causes a bank run with negotiations still stalled, Schaeuble’s “accidental” insolvency may well become reality.

end

Sunday:

Schauble warns of a sudden Greek default

a must read…

(courtesy Wolf Richter/WolfStreet)

Schäuble Warns of “Sudden” Greek Default

Wolf Richter www.wolfstreet.comwww.amazon.com/author/wolfrichter

The governments of Greece – new and old – screwed up. Other debt-sinner countries are able to borrow at near-zero or negative interest rates, simply taking money from investors with a promise to return it on a given day in the future if investors give it new money to do so. These investors, it must be said, had their brains washed by the ECB and other central banks in order to allow this to happen. But the governments of Greece somehow missed that gravy train.

Now, no one wants to lend Greece money at negative interest rates, least of all the Greeks themselves, who know their governments better than anyone else on the planet and have less trust in it than anyone else on the planet: they’re yanking their euros out of their banks even as the ECB is propping them up with fresh euros that ultimately belong to taxpayers elsewhere.

This weekend, representatives of the “institutions” – the unmentionable “Troika” – are trying the hash out a reform package with the new team from Greece that does not include Finance Minister Yanis Varoufakis, who’d been shoved aside. On Monday, the finance ministers of the Eurogroup will meet in Brussels.

Without an agreement on the implementation of the reforms, Greece won’t get the outstanding relief funds of €7.2 billion. And then what? The government has practically no funds left. Time is running out. Monday is it. The Big Day. Again.

“I don’t see that everything will be solved by then,” German Finance Minister Wolfgang Schäuble said in an interview in the Sunday edition of the Frankfurter Allgemeine Zeitung, one of Germany’s largest papers, throwing cold water on any hopes. He doubted that the Greek government even knew what exactly was going on in its finances.

“Such processes also have irrational elements,” Schäuble warned. “Experiences elsewhere in the world have shown that a country can suddenly slide into insolvency.”

On the principle that a country is slowly zigzagging down that path paved with lots of good intentions, false hopes, and lofty promises and, BAM, suddenly, it’s over. So maybe Monday? Or next month? He refused to nail down a specific point in time.

When asked if the German government has made preparations for such an eventuality, he said:

“There are issues that a prudent politician must not answer. Otherwise there will be misunderstandings. Jean Claude Juncker [President of the European Commission and former President of the Eurogroup] once said that sometimes you must play fast and loose with the truth. For me, these things are more complicated. Therefore, I rather say nothing at all.”

That’s a resounding “yes.” Germany is prepared. The financial markets have no doubts and refuse to get panicky. The German government is going to handle this just fine, they’re saying.

But in August 2013, during the run-up to the general elections in the fall, when the cost of the Greek bailouts to German taxpayers was one of the themes, Schäuble had this to say, thus playing fast and loose with the truth:

“One thing is certain: there won’t be a second debt cut for Athens.”

The first one having been the 70% haircut imposed “voluntarily” on private-sector bondholders in 2012. The second one would hit public institutions, such as the ECB and the bailout funds, and ultimately taxpayers in Germany and other countries.

The “one thing” that was certain in 2013 before the election is now out the window. A Greek default would almost certainly entail some kind of debt relief for Greece, hence a haircut for taxpayers in other countries. They just haven’t been told yet.

But Germany would “do everything to keep Greece under responsible conditions in the Eurozone,” he said. “It must not fall apart because of us.” On this issue, he and Chancellor Angela Merkel are in complete agreement, he said.

There have long been voices that confirmed that if Greece defaults, there could be a haircut for public bondholders in some form (swapping existing debt for zero-interest debt with a 1,000-year maturity?) while Greece remains in the Eurozone. That appears to be the direction the German government is heading.

And Schäuble defended his best buddy Varoufakis. Few people have managed to rise to such media adulation and then plunge from it as quickly as Varoufakis. Whatever he was trying to do, it didn’t work. Forget game theory. “We both are finance ministers and bear responsibility, so we work well together,” Schäuble said. “First, the media make Varoufakis into a superstar, now they’re writing him off. The one is as wrong as the other.”

With this immaculately-timed interview, the German government acknowledged that it’s ready for Greece’s insolvency and default, whenever it may come, including Monday, after having denied it for years, and that it would continue working with Greece to keep the Eurozone together. What’s sacred for the Merkel government is the Eurozone, not its taxpayers. They already got shafted.

But here is the thing: the Greeks could solve the crisis on their own, if they wanted to. Or do they know something that others don’t? Read… If Greeks Did This, the Terrible Crisis Would Be Over

end

Sunday:

It looks hopeless for an agreement as now the IMF are preparing for a Greek default. (and also contingency plans)

IMF Preparing Greek Default Contingency Plan

The biggest slow motion trainwreck in history, one thateveryone knows how it ends just not when (especially since the “when” is about 5 years overdue), that of the Greek sovereign default may just got a bit more exciting earlier today when the WSJ reported that the IMF can no longer lie – like Mario Draghi did to Zero Hedge in 2013 – that there are preparation for a Plan B. To wit: “the International Monetary Fund is working with national authorities in southeastern Europe on contingency plans for a Greek default, a senior fund official said—a rare public admission that regulators are preparing for the potential failure to agree on continued aid for Athens.”

According to the WSJ, the IMF is focusing on nations neighboring Greece, asking their national banking supervisors to “ensure that subsidiaries of Greek banks have enough assets that they can exchange for emergency financing at their own central banks—in case financing from their parent institutions is suddenly cut off—and that deposit-insurance funds are at sufficient levels, Mr. Decressin said.”

In other words, have a Greek default Plan B ready, preferably right now.

“We are in a dialogue with all of these countries,” said Jörg Decressin, deputy director of the IMF’s Europe department. “We are talking with them about the contingency plans they have, what measures they can take.”

Greek banks are big players in some of its neighbors’ financial systems. In Bulgaria, subsidiaries of National Bank of Greece SA, Alpha Bank SA, Piraeus Bank SA and Eurobank Ergasias SA own around 22% of banking assets, roughly the same as Greek banks own in Macedonia. Greek banks are also active in Romania, Albania and Serbia.

Should anyone be worried that a day before the critical Eurozone meeting which was supposed to conclude the Greek bailout negotiations, not only is there not a deal but Greece is once again on the edge of collapse?

“It would be foolish for anyone in the policy world not to be worried at this stage,” Mr. Decressin said.

Thanks for the warning.

And while we have covered the background story in detail, here it is again: “European officials expect no breakthroughs at a meeting of the currency union’s finance ministers on Monday. That means Greek lenders will remain under pressure, dependent on relatively expensive liquidity from the Greek central bank and at risk of bank runs in case doubts emerge over their ability to pay out deposits.”

As noted above it is not if, but when. Here’s why.

Going back to the WSJ story, while there is nothing that has actually changed in the narrative, it is almost as if the IMF, having failed to spur a wholesale bank run in Greece, one that would have toppled the government, is now trying to spur bank runs in Greek bank subsidiaries in neighboring nations.

One scenario that the IMF is concerned about is what could happen if panic over Greece’s finances pushes savers in the region to pull their money out of Greek-owned banks. “These banks…may be totally fine, but there could still be in the population a perception, these are Greek banks and they are not fine, and people would turn up and try to withdraw their deposits. That is something you cannot model,” Mr. Decressin said.

National safety nets have in the past been vulnerable to rumor-fueled bank runs. In June last year, the Bulgarian government had to take over Corporate Commercial Bank, after depositors pulled out their savings amid negative news reports about the lender’s main shareholder. It took the government six months to compensate the bank’s depositors, far longer than the 25 days mandated under European Union law.

Of course, if there is a Greek default and suddenly it becomes clear to everyone that the unbreakable monetary union is quite, well, breakable, the IMF will have to worry not about bank runs in Bulgaria et al, but the countries in Europe’s periphery, such as the one with the second largest amount of sovereign debt outstanding: Italy, as well as Spain, Portugal and so on. Because if the common people have learned one thing, it is that if a political party is elected that the ECB does not approve of, that country’s days of financial mirth are over, and insolvent reality is just around the corner.

And just to make sure that the IMF’s concerns are unwarraned, the NYT reports that “discussions in the Greek government have included assessing the pros and cons of not paying the central bank and the monetary fund, said two people who were briefed on the discussions but who spoke on the condition of anonymity. In such a case, which was described as a last-ditch option and not a plan for action, Greece would keep paying debts owed to private sector bondholders and other European governments.”

What is most shocking is that it has taken the Greeks five years to realize there are no more pros to perpetuating the massive con that is it failed zombie nation status, one that has resulted in the biggest national depression in history.

end

Monday:

The Greek War cabinet after a Sunday meeting has decided to play hardball. Officials state that there is nothing more to be gained by Greece to continue reforms when there is no benefit to the state.

(courtesy Ambrose Pritchard Evans/UKTelegraph)

Greece’s ‘war cabinet’ prepares to battle EU creditors as anger mounts

The country’s radical-Left leaders have concluded that there is little to be gained from any further concessions to EMU creditors

Greece’s “war cabinet” has resolved to defy the European creditor powers after a nine-hour meeting on Sunday, ensuring a crescendo of brinkmanship as the increasingly bitter fight comes to a head this month.

Premier Alexis Tsipras and the leading figures of his Syriza movement agreed to defend their “red lines” on pensions and collective bargaining and prepare for battle whatever the consequences, deeming the olive-branch policy of recent weeks to have reached a dead end.

“We have agreed on a tougher strategy to stop making compromises. We were unified and we have a spring our step once again,” said one participant.

The Syriza government knows that this an extremely high-risk strategy. The Greek treasury is already empty and emergency funds seized from local authoritiesand state entities will soon run out.

Greece’s mayors warned over the weekend that they would not release any more funds to the central government. The Greek finance ministry must pay the International Monetary Fund €750m (£544m) on Tuesday, the first of an escalating set of deadlines running into August.

http://cloud.highcharts.com/embed/uxiqiq

“We have enough money to pay the IMF this week but not enough to get through to the end of the month. We all know that,” said one minister, speaking to The Telegraph immediately after the emotional conclave.

The war council came a day before Greece’s three-headed team – deputy premier Giannis Dragasakis, finance minister Yanis Varoufakis and deputy foreign minister Euclid Tsakalotos – are due to go to Brussels for a crucial meeting with Eurogroup ministers.