Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1106.80 (comex closing time)

Silver $14.67

In the access market 5:15 pm

Gold $1096.70

Silver: $14.67

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a poor delivery day, registering 0 notices for nil ounces . Silver saw 27 notices filed for 135,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 243.49 tonnes for a loss of 60 tonnes over that period.

In silver, the open interest rose by 1,113 contracts despite the fact that Friday’s price was down by 14 cents. The total silver OI continues to remain extremely high, with today’s reading at 188,772 contracts now at decade highs despite a record low price. In ounces, the OI is represented by .944 billion oz or 135% of annual global silver production (ex Russia ex China). This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end as they continue to raid as basically they have no other alternative. Today again, we must have had banker shortcovering.

In silver we had 27 notices served upon for 135,000 oz.

In gold, the total comex gold OI rests tonight at 474,057 for a gain of 3,337 contracts despite the fact that gold was down $12.00 on Friday. We had 0 notices filed for nil oz today.

We had a massive withdrawal in gold tonnage at the GLD to the tune of 11.63 tonnes/ thus the inventory rests tonight at 696.25 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. I thought that 700 tonnes is the rock bottom inventory in gold, but I guess I was wrong. However we must be coming pretty close to a level of only paper gold and the GLD being totally void of physical gold. In silver, we had no change in inventory at the SLV / Inventory now rests at 327.593 million oz.

Here are today’s comex results:

The total gold comex open interest rose by 274 contracts from 474,057 up to 474,331 despite the fact that gold was down $12.00 in price yesterday (at the comex close). We are now in the next contract month of July and here the OI rose by 60 contracts to 218 contracts. We had 0 notices filed yesterday and thus we gained 60 contracts or an additional 6,000 ounces will stand in this non active delivery month of July. The next big delivery month is August and here the OI decreased by 1560 contracts down to 226,979. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was excellent at 329,371.However today’s volume was aided by HFT traders. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was poor at 195,751 contracts. Today we had 0 notices filed for nil oz.

And now for the wild silver comex results. Silver OI rose by 1113 contracts from 187,659 up to 188,772 despite the fact that the price of silver was down by 14 cents with respect to Friday’s trading and now the OI is rising in total sympathy with gold. We continue to have our bankers pulling their hair out with respect to the continued high silver OI as the world senses something is brewing in the silver (and gold ) arena. The next delivery month is July and here the OI rose by 22 contracts down to 137. We had 0 notices served upon yesterday and thus we gained 22 contracts or an additional 110,000 ounces of silver will stand for delivery in this active month of July. This is the first time in quite some time that we have not lost any silver ounces standing immediately after first day notice. The August contract month saw it’s OI rise by 57 contracts down to 174. The next major active delivery month is September and here the OI rose by 710 contracts to 128,557. The estimated volume today was excellent at 67,208 contracts (just comex sales during regular business hours). The confirmed volume yesterday (regular plus access market) came in at 30,878contracts which is fair in volume. We had 27 notices filed for 135,000 oz.

July initial standing

July 20.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 64,196.711 (Scotia, Manfra) and includes 5 kilobars |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 16,075.000 (Scotia)(500 kilobars) |

| No of oz served (contracts) today | 0 contracts (nil oz) |

| No of oz to be served (notices) | 218 contracts 21,800 oz |

| Total monthly oz gold served (contracts) so far this month | 412 contracts(41,200 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 203.60 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 288,163.4 oz |

Today, we had 0 dealer transactions

total Dealer withdrawals: nil oz

we had 0 dealer deposits

total dealer deposit: zero

we had 2 customer withdrawal

i) out of Scotia: 64,196.711 oz

ii) Out of Manfra: 160.75 oz (5 kilobars)

total customer withdrawal: 64,357.461 oz

We had 1 customer deposit:

i) Into Scotia: 16,075.000 oz or 500 kilobars

Total customer deposit: 16,075.000 ounces

We had 0 adjustments.

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the July contract month, we take the total number of notices filed so far for the month (412) x 100 oz or 41,200 oz , to which we add the difference between the open interest for the front month of July (218) and the number of notices served upon today (0) x 100 oz equals the number of ounces standing.

Thus the initial standings for gold for the July contract month:

No of notices served so far (412) x 100 oz or ounces + {OI for the front month (218) – the number of notices served upon today (0) x 100 oz which equals 63,000 oz standing so far in this month of July (1.9595 tonnes of gold).

we gained 60 contracts or an additional 6000 oz will stand in this non active delivery month of JULY.

Total dealer inventory 482,778.738 or 15.016 tonnes

Total gold inventory (dealer and customer) = 7,828,512.94 oz or 243.49 tonnes

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 243.49 tonnes for a loss of 60 tonnes over that period.

end

And now for silver

July silver initial standings

July 20 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 116,978.120 oz (CNT, Delaware,Brinks,Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 587,971.400 oz (JPM) |

| No of oz served (contracts) | 27 contracts (135,000 oz) |

| No of oz to be served (notices) | 110 contracts (550000 oz) |

| Total monthly oz silver served (contracts) | 3304 contracts (16,520,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,383,162.0 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 1 customer deposits:

i) Into JPMorgan: 587,971.400 oz

total customer deposit: 587,971.400 oz

We had 4 customer withdrawals:

i)Out of CNT: 10,472.84 oz

ii) Out of Delaware: 980.700 oz

iii) Out of Brinks: 29,351.48 oz

iv) Scotia; 76,173.100 oz

total withdrawals from customer: 116,978.120 oz

we had 0 adjustments

Total dealer inventory: 58.96 million oz

Total of all silver inventory (dealer and customer) 178.879 million oz

The total number of notices filed today for the July contract month is represented by 27 contracts for 135,000 oz. To calculate the number of silver ounces that will stand for delivery in July, we take the total number of notices filed for the month so far at (3304) x 5,000 oz = 16,520,000 oz to which we add the difference between the open interest for the front month of July (137) and the number of notices served upon today (27) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the July contract month:

3304 (notices served so far) + { OI for front month of July (137) -number of notices served upon today (27} x 5000 oz ,= 17,070,000 oz of silver standing for the July contract month.

We gained 22 contracts or an additional 110,000 ounces will stand in this active delivery month of July.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.comorhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

July 20

July 17./a massive withdrawal of 11.63 tonnes in gold tonnage tonight from the GLD/Inventory rests at 696.25 tonnes

July 16./we lost 1.19 tonnes of gold tonight/Inventory rests at 707.88 tonnes

July 15/no change in inventory/gold inventory rests tonight at 709.07 tonnes.

July 14.2015:no change in inventory/gold inventory rests at 709.07 tonnes

July 13.2015: a big inventory gain of 1.49 tonnes/Inventory rests tonight at 709.07 tonnes

July 10/ we had a big withdrawal of 2.07 tonnes of gold from the GLD/Inventory rests this weekend at 707.58 tonnes

July 9/ no change in gold inventory at the GLD/Inventory at 709.65 tonnes

July 8/no change in gold inventory at the GLD/Inventory at 709.65 tonnes

July 7/ no change in gold inventory at the GLD/Inventory at 709.65 tonnes

July 6/no change in gold inventory at the GLD/Inventory at 709.65 tonnes

July 2/we had a huge withdrawal of inventory to the tune of 1.79 tonnes/rests tonight at 709.65 tonnes

July 20 GLD : 696.25 tonnes

end

And now for silver (SLV)

July 20

july 17.2015/no change in silver inventory tonight/inventory at 327.593 million oz

July 16./no change in silver inventory/rests tonight at 327.593 million oz

July 15./no change in silver inventory/rests tonight at 327.593 million oz/

July 14.2015: no change in silver inventory/rests tonight at 327.593 million oz.

July 13./an inventory gain of 1.051 million oz/Inventory rests at 327.593 million oz

july 10/no change in silver inventory at the SLV tonight/inventory 326.542 million oz/

July 9/ a huge increase in inventory at the SLV of 1.337 million oz. Inventory rests tonight at 326.542 million oz

July 8/no change in inventory at the SLV/rests at 325.205

July 7/no change in inventory at the SLV/rests at 325.205 tonnes

July 6/we have a slight inventory withdrawal which no doubt paid fees. we lost 137,000 oz/Inventory rests tonight at 325.205 million oz

July 2/ no change in inventory at the SLV/rests tonight at 325.342 million oz

July 20/2015: tonight inventory rests at 327.593 million oz

end

And now for our premiums to NAV for the funds I follow:

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 10.3 percent to NAV usa funds and Negative 10.40% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 62.2%

Percentage of fund in silver:37.4%

cash .4%

( July 20/2015)

2. Sprott silver fund (PSLV): Premium to NAV falls to 1.58%!!!! NAV (July 20/2015) (silver must be in short supply)

3. Sprott gold fund (PHYS): premium to NAV falls to – .73% toNAV(July 20/2015

Note: Sprott silver trust back into positive territory at 2.21%

Sprott physical gold trust is back into negative territory at -.73%

Central fund of Canada’s is still in jail.

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64)

Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis.

Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer.

Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer.

* * * * *

>

And now for your overnight trading in gold and silver plus stories

on gold and silver issues:

(courtesy/Mark O’Byrne/Goldcore)

China’s Total Gold Holdings Much Higher – Owns Gold In SAFE and CIC

– China revises up its stated gold reserves in bid for IMF membership and reserve currency status

– China announces a 604 tonne increase in gold reserves

– First public disclosure re reserves in since 2009

– China officially owns around 1,660 tonnes of gold reserves – true total figure is likely much larger

– Playing long game – protecting USD reserves and positioning RMB as global reserve currency

– China true gold holdings much higher as also owns gold in SAFE and CIC

China officially revised its gold reserves upward for the first time since 2009 on Friday. The People’s Bank of China (PBOC) stated on Friday that it had added 604 tonnes of gold to its official reserves last month.

Gold is no longer used to back paper and digital money of today, however it remains an important part of monetary reserves internationally. This can be seen in the People’s Bank of China’s (PBOC) announcement of an increase in their gold reserves.

China’s official reserves are now almost 1660 tonnes of gold. Analysts, including Bloomberg and ourselves, had been expecting a sharp jump to at least 2,000 tonnes and possibly as high as 3,000 or 4,000 tonnes.

It is clear by the secrecy surrounding China’s reserves that they view gold as a vital strategic asset. Chinese gold reserves increased by 57 percent and China’s holdings have now surpassed those of Russia to become the fifth-largest. The U.S. is believed to have the biggest reserves at 8,133.5 tons. The current official holdings rank them as the fifth largest holder of gold in the world (see chart).

Many analysts believe this figure to be an understatement given the enormous volumes of gold that have been passing through Hong Kong – and through Shanghai in more recent years – and the large amounts that have been produced and bought domestically.

It is important to remember that as we have long pointed out two other entities, besides the PBOC, have also been buying gold – the State Administration of Foreign Exchange (SAFE) and theChina Investment Corporation (CIC).

Although if the combined holdings of the PBOC, SAFE and CIC were added together, China may well be the second largest holder of gold bullion – after the U.S. – assuming that U.S. gold reserve figures, which have not been publicly audited in over 60 years, are accurate.

It is likely, that in total and between the three China’s financial institutions, China may in fact be holding between 3,000 tonnes and 6,000 tonnes of gold.

China is playing the long game and they could be low balling their total gold holdings – official central bank reserves and non official holdings – in order to maintain confidence in their substantial US dollar holdings and to aid their bid to join the IMF.

China became the world’s second-largest economy in 2010 and has stepped up efforts to internationalize its currency – the yuan. The Chinese are pushing for full convertibility of the RMB and increasing their gold holdings will create confidence in the fledgling reserve currency and aid them in this regard.

China, regardless of its ambitions, is not currently in a position to challenge the the dollar’s reserve currency supremacy. The absence of a deep and liquid bond market is one impediment that they need to overcome on this regard.

On the other hand, it certainly is strong enough to take its place at the IMF and have the yuan included in the currency basket that makes up Special Drawing Rights (SDRs).

Whoever has the gold makes the rules. While gold is denigrated at every opportunity by some commentators – frequently Keynesians anti gold ideologues – it is clear that the true power-brokers in the world – leading international banks and central banks – still adhere to that adage.

To demonstrate its fitness to join the IMF, China must demonstrate its financial and monetary strength by declaring sufficient gold reserves which it has now done.

The bloated, debt-based international monetary system faces huge challenges and the scale of debts globally could indeed lead to collapse. In time China may disclose its true gold holdings and partially back its currency with gold to discourage capital flight.

Gold is no longer used to back the trillions and trillions of paper and digital money of today, however it clearly remains money contrary to assertions to the contrary. Gold bullion remains a substantial part of central bank reserves in the U.S. and Europe.

The PBOC gold announcement is the continuation of the trend of China positioning the yuan as global reserve currency. China’s gold reserves remain miniscule as a percent of their massive $3.7 trillion foreign exchange reserves – less than 2%. In marked contrast to the U.S., Germany and even France and Italy when gold’s share of national forex reserves is over 70%.

We would not be surprised if the PBOC begins to accumulate a minimum of 100 metric tonnes in gold reserves a month going forward as the Russians have done in recent years. Alternatively, they may elect to continue accumulating gold bullion quietly through SAFE and the CIC – indeed they have been buying hundreds of gold mines in South America, Africa and internationally in recent years – likely securing another important source of supply.

Central banks internationally still hold physical gold as financial insurance. Investors and savers should do the same and have an allocation to gold bullion outside of the banking system, in the safest vaults in the world.

Must-read guides to international bullion storage:

Essential Guide to Gold Storage in Switzerland

Essential Guide to Gold Storage in Singapore

MARKET UPDATE

Today’s AM LBMA Gold Price was USD 1,115.00, EUR 1,029.17 and GBP 717.41 per ounce.

Friday’s AM LBMA Gold Price was USD 1,143.00, EUR 1,049.25 and GBP 730.68 per ounce.

For the week, gold was lower in dollars and pounds but eked out slight gains in euros. Gold fell 2.5% to $1133.90 per ounce and silver fell 4.4% to $14.89 per ounce.

This morning, massive concentrated selling in the futures market again led to sharp price falls and at one stage gold fell nearly 5% to below $1,100 per ounce. Gold in Singapore for immediate delivery fell sharply while gold in Switzerland bounced higher from the intra day lows.

In what looked like another successful bid to manipulate the gold market lower, there was massive selling of gold futures contracts – some 700,000 ounces worth of gold futures in mere seconds. The equivalent of one-fifth of a whole day’s trade in a normal session, was sold in a concentrated manner in less than two minutes – pushing prices lower again.

ANZ Bank analyst Victor Thianpiriya said in a note that the“nature, size and timing of the heavy selling” suggests someone “was taking advantage of low liquidity or some sort of forced selling had taken place.“

The sell off in the gold market spooked other commodities and most commodities are seeing sharp selling today, while stocks have continued to eke out further gains.

This is somewhat counter intuitive as the sharp falls in commodities in recent days suggest the global economy is weakening and threatened by deflation. Thus, stocks should be falling too. However, it appears that stocks are being supported by ultra loose monetary policies and currency debasement for now.

Gold looks horrible technically after having a fourth weekly loss last week. This is the longest series of price falls since February.The price falls are despite strong coin and bar demand internationally. U.S. Mint gold bullion coin sales remain very robust and dealers, mints and refineries report robust demand – particularly in Germany and wider Europe and indeed in the U.S.

This suggests that we are close to capitulation and a bottom and gold looks very oversold. Gold mining stocks absolutely collapsed last week with the XAU index down 8.1% and the HUI index down 9.3% – another indication that we may be close to a bottom.

Although as ever we caution to never ‘catch a falling knife’ and $1,000 per ounce remains possible on the down side. Dollar cost averaging into a physical position remains prudent.

Silver for immediate delivery fell 0.6% to $14.84 an ounce. Spot platinum fell 1.1 percent to $984.51 an ounce, while palladium fell 1 percent to $611 an ounce.

Breaking News and Research Here

end

Gata responds to China’s official gold holdings:

(courtesy GATA)

China’s official gold reserves total is still phony — and so is most everybody else’s

Submitted by cpowell on Fri, 2015-07-17 22:58. Section: Daily Dispatches

7:41p ET Friday, July 17, 2015

Dear Friend of GATA and Gold:

Most people in the gold business seems disappointed with China’s announcement today of its gold reserve total, which, as Sharps Pixley CEO Ross Norman told The Wall Street Journal, was only about half of what the market expected, since it was the first updating of gold reserves by the People’s Bank of China in six years:

http://www.wsj.com/articles/china-discloses-its-gold-holdings-1437144149

But this expectation was probably always unrealistic, for as Zero Hedge writes —

http://www.zerohedge.com/news/2015-07-17/china-increases-gold-holdings-5…

— China’s announcement today was also an admission that its gold reserve figures have been misleading. Indeed, the announcement was almost certainly hugely misleading, China’s true gold reserves likely being far larger.

That is, for six years, right through yesterday, China asserted that its official gold reserves were 1.054 tonnes, but today China reported its official reserves as 1,658 tonnes, an increase of 604 tonnes or 57 percent —

http://www.reuters.com/article/2015/07/17/china-gold-reserves-idUSL4N0ZX…

— and of course that much additional metal was not obtained in the last 24 hours.

Zero Hedge writes: “China has finally admitted that its official gold numbers were fabricated (alongside all other official data released from the communist country), as it is impossible that the People’s Bank of China could have bought 600 tons of gold in the open market in June when the price of the yellow metal actually dropped by 2 percent.”

But China has not “finally” admitted anything, as these are the same circumstances that prevailed when China updated its reserve report in 2009. For from 2003 to 2009 China maintained that its gold reserves were just 454 tonnes. Then one day in April 2009 the reserves report jumped 146 tonnes to 600 tonnes:

end

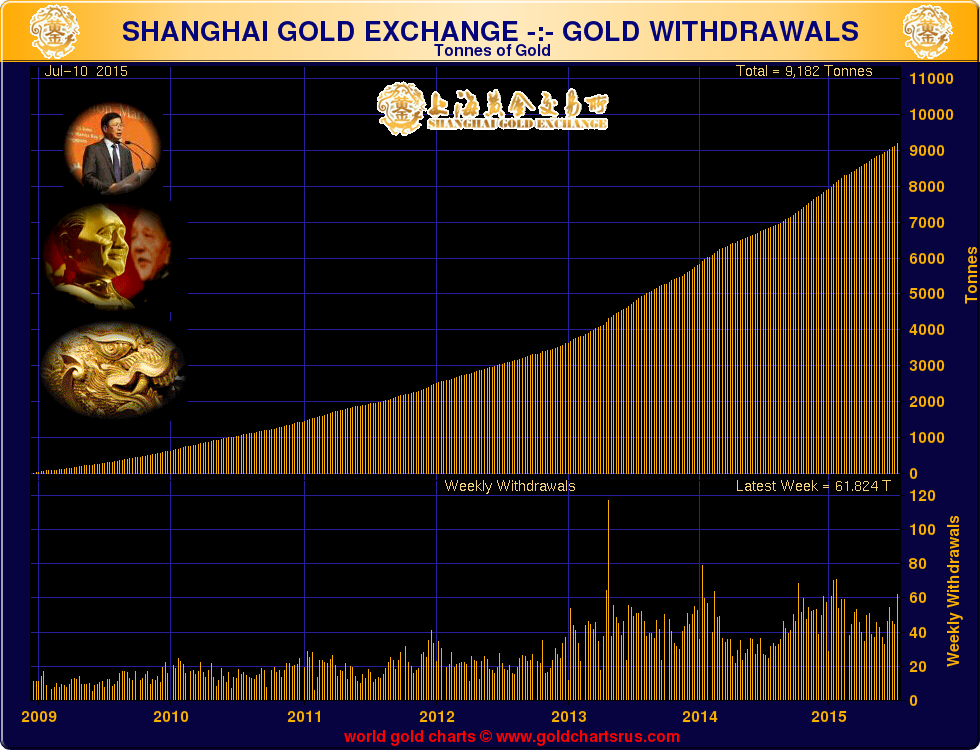

China adds a whopping 62 tonnes in the latest week. This is a big increase from the week before.

(courtesy Jessie/American Cafe/GATA)

Shanghai Gold Exchange Sees 61.8 Tonnes Withdrawn In

Eighth Largest Week Ever – Talk To the Hand

Asia continues to add significant amounts of gold bullion to their wealth reserves.

Wall Street and its sycophants would like us to consider gold to be just ‘a pet rock’ or ‘like trading sardines.’ And yet central banks have turned to be net buyers, and Asia and the Mideast continue to buy bullion in record amounts. Talk to the Chan.

One of the few coherent things Alan Greenspan said was that statists of all persuasions, both right and left, have ‘an almost hysterical antagonism towards gold.’ This is because gold resists their will to power over others.

So why isn’t gold ‘working’ at this moment in history?

“We hypothesize that, having learned from the misadventures of the 1960s, the policy elites, well-versed in the practice of financial engineering and market manipulation, would have seen no need to dump stocks of government gold reserves onto the market, 1960s style, to keep the price in check.

Instead, synthetic gold, sourced in pyramids of credit extended to bullion bankers by central banks with little or no claim on physical substance, have provided a more efficient, better-camouflaged form of intervention. COMEX synthetic gold and related over-the-counter derivatives are traded in macro strategies implemented by hedge funds, high-frequency trades, and commodity funds in pair trades with interest-rate, currencies, equity futures, or even more exotic offsets. The volumes traded are huge, and bear little resemblance to actual flows of physical metal.

We suspect that shorting gold has come to seem like a riskless proposition as long as there is confidence in the Fed. Synthetic gold is the perfect substance for a carry trade: an easy borrow with very low carrying cost and little upside basis risk. Such a hypothesis, in our opinion, does much to explain the incongruity of a declining gold price while fundamentals for paper currency, and the U.S. dollar in particular, obviously deteriorate; while demand for physical gold has exceeded new mine supply for several years running; and while above-ground 400-ounce .995-gold bars located in London, New York, and other financial capitals (in cohabitation with speculative trading activity in paper markets) have steadily dwindled and disappeared into Asian financial centers reformulated as .9999 kilo bars.”

The dumping at market of very large amounts of paper assets into quiet market hours has been well documented in many places. It is a well worn market manipulating strategy abused by some very large trading desks, often playing with other people’s money. Citi privately called it their ‘Dr. Evil Strategy.’

It is funny how the systematic rigging of so many financially related markets has been revealed, but the blatant manipulation of the precious metals market, which is certainly knowable by anyone with a basic knowledge of the markets and a computer terminal, is so willfully ignored. A love of money, lust for power, and a lack of integrity will alloy to make people hypocrites.

When we see such trash articles being written, and passed along mindlessly by those who yearn to warm themselves by the fires of the oligarchs, we know that gold has cast a cold fear into the hearts of those who would be kings, or their privileged servants.

And considering the long, cynical rally in paper assets that culminated in the financial crisis of 2008, when people start believing in the power of fraud and willful distortion of markets, we can only say as we did then, this will end badly.

A man cannot serve two masters. He will love the one and come to hate the other. You love what you serve.

end

(courtesy Bix Weir)

Good Sign for Silver in the Short Term

A few weeks back the US Mint announced that US Treasury Secretary, Jack Lew, had ordered them to stop selling the #1 retail silver coin in the world…the 1oz Silver Eagle. He ordered it because too many were being sold at the low, manipulated silver price below $15/oz and he knew that there was more pain to come in the silver price suppression so he cut off supply to slow the physical dishoarding of the remaining stockpiles of silver.

That’s the truth and there is no other way to describe it.

Yesterday, the US Mint announced that the sales of US Silver Eagles will resume on July 27th on an allocated basis as mandated by US Treasury Secretary, Jack Lew.

US Mint to Resume Silver Eagle Sales July 27

http://www.kitco.com/news/2015-07-17/U-S-Mint-To-Restart-Silver-Sales-July-27-Gold-Demand-Remains-Strong.html

Silver bullion investors will have to wait one more week to buy more 2015 U.S. American Eagle Silver coins from the U.S. Mint.

Friday, the U.S. Mint said announced that it would resume sales of their popular silver coin, on an allocated basis, July 27.

The mint sold out of its American eagle coins July 7 after silver prices dropped below $15 an ounce, creating “significant demand” for the bullion coins. According to sales data compiled by the mint, more than 2.7 million silver coins have been sold in July, completely surpassing sales of 1.98 million coins in 2014. For the year, the mint has sold more than 24.5 million silver coins.

The mint’s sales data also shows strong demand for gold bullion coins. The mint has seen its busy month since April 2013 in only the first few weeks of July. The data shows that so far the mint has sold a total of 101,000 ounces of gold so far this month. Last year the mint sold 30,000 ounces of gold for the entire July 2014.

END

So let me get this straight, the price of silver is plummeting and the demand for silver is going through the roof so much so that the US Treasury Secretary, Jack Lew, found it necessary to halt the production (ie demand) for the #1 use of retail physical silver. His other choice, and the one that is mandated by the Bullion Coin Act of 1985, was to continue purchasing silver blanks to fill demand even though it may drive the price of silver much higher.

BY DEFINITION: US Treasury Secretary, Jack Lew, is artificially manipulating the silver market as his actions are meant to STOP the upward pressure on the price of silver and support the manipulation actions.

US Treasury Secretary, Jack Lew, should be charged for the illegal act of willfully manipulating the silver market!

The bright side of all this: Jack Lew is telegraphing just how long we should expect to see the silver price held down until the next leg up begins – July 27th!

Tick, tick, Tick.

May the Road you choose be the Right Road.

Bix Weir

www.RoadtoRoota.com

end

(courtesy Stephen Leeb/Egon Von Greyerz/Kingowrld news)

At KWN, China’s gold reserves announcement ridiculed by Leeb, von Greyerz, Maguire

11:34a ET Saturday, July 18, 2015

Dear Friend of GATA and Gold:

In interviews with King World News, fund managers Stephen Leeb and Egon von Greyerz and London metals trader Andrew Maguire ridicule Friday’s announcement by China about its gold reserves, which, they maintain, are much greater than announced. The interviews are posted here:

http://kingworldnews.com/andrew-maguire-egon-von-greyerz-and-stephen-lee…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

(courtesy John Hathaway/Tocqueville Asset Management/GATA)

Tocqueville’s Hathaway summarizes and updates the gold suppression scheme

10:55a ET Saturday, July 18, 2015

Dear Friend of GATA and Gold:

In his new gold strategy letter, Tocqueville Asset Management’s senior portfolio manager, John Hathaway, updates and summarizes the central bank gold price suppression scheme, which is getting more obvious every day with the counterintuitive behavior of the markets.

Hathaway writes:

“We and others have commented at length about the contradictions between the markets for paper (synthetic) and physical gold. The declining price of paper gold quotes in NY and London doesn’t square with worldwide physical flows that reflect demand far in excess of mine production. It appears to us that gold positions traded in London and New York among bullion banks, high-frequency traders, hedge funds, and commodity traders constitute highly levered derivatives with only distant and notional relationships to the physical substance. The power of synthetic gold markets (COMEX in New York and over-the-counter in London, in conjunction with the London Bullion Market Association fix) to determine gold prices could start to ebb as physical gold migrates to Asian financial centers.

“China has built an institutional infrastructure in the form of the Shanghai Gold Exchange, shortly to be merged with the Hong Kong Gold Exchange, which will facilitate settlement of international transactions in physical, not synthetic, gold, as described by Yao Yudong in his recent LBMA presentation. We expect an increasing percentage of gold transactions to be denominated in renminbi.

“The well-documented disappearance of bullion from Western vaults may mean that credit required for transactions in synthetic gold — that is, some sort of claim on underlying physical gold — will become increasingly difficult to obtain. …

“Evidence of possible stress on this system of credit links between physical gold and derivatives may have been revealed by the first-quarter Office of the Comptroller of the Currency (OCC) report, which showed that JPMorgan’s commodities derivative contracts (less than one year) exploded from $131 million to $3.8 trillion in just one quarter — a staggering and unprecedented change.

“The mystery deepens because the OCC for the first time inexplicably obfuscated the reporting categories by eliminating the separate, long-standing category (at least 10 years) for gold by including it together with foreign exchange. This curious retreat from transparency by the OCC suggests to us attempted deception. By whom and for what reasons we can only speculate.

“For our part, it makes us wonder whether we are witnessing the final moments of a second, more sophisticated version of the 1960s London Gold Pool (the ‘Gold Pool’), a scheme organized by the U.S. and European governments to suppress the free-market gold price to camouflage the growing adverse fundamentals for the U.S. dollar. …

“A bit of history is instructive here: The collapse of the 1960s Gold Pool, the aforementioned secret and collusive effort by seven central banks to keep a lid on the gold price, preceded a most difficult decade for financial assets. A lesson to be learned from the 1960s is the unpredictability of government actions, their inherently anti-free-market nature, and the unintended consequences that can arise from them.

“The Gold Pool was, in retrospect, a clumsy attempt by Western democracies to disguise the deteriorating fundamentals of the U.S. dollar stemming from the Vietnam War, rising inflation, and the weakening balance of payments. The dollar had been pegged to gold at $35/ounce since the end of World War II, a number that proved too low in light of the changing fiscal realities for U.S. sovereign credit caused by the escalation of the Vietnam War and the introduction of large scale welfare policies under the umbrella of the Johnson administration’s ‘Great Society’ initiative.

“In retrospect, the scheme was clumsy because the manipulation of the gold price was accomplished by the exchange of physical gold for dollars held by foreign creditors who saw the writing on the wall. The objective of the Gold Pool was to disguise reality. In the long run, that price-suppression scheme did not work. The failure of the Gold Pool of course was resolved by the suspension of dollar/gold convertibility in 1971. When free-market gold trading resumed in 1974, the gold price rose by nearly 20 fold over the next eight years.

“The present-day magnitude of fiscal and monetary irresponsibility in our view exceeds the precedent of the 1960s by multiples. It is only fitting that the elaboration and complexity of disguise required to beautify the underlying realities would be proportional. Government intervention via price suppression (interest rates, currencies) or price inflation (financial assets) seems to pervade all financial markets. Why should gold be exempt?

“At some basic level, all investors are aware of the gold price. Unruly behavior by the metal could render the ‘Truman Show’ dysfunctional. Allowing free-market expression of gold prices may have been seen as a serious risk at the highest policy levels. The strong rise of the gold price amidst liberal doses of QE post-2008 through 2011 would have been a note discordant with an otherwise happy fable. Gold strength might confirm what many investors suspect: QE and ZIRP have failed to produce economic growth and may well have jeopardized future prospects for a return to solid economic footing.

“We hypothesize that, having learned from the misadventures of the 1960s, the policy elites, well-versed in the practice of financial engineering and market manipulation, would have seen no need to dump stocks of government gold reserves onto the market, 1960s style, to keep the price in check. Instead, synthetic gold, sourced in pyramids of credit extended to bullion bankers by central banks with little or no claim on physical substance, have provided a more efficient, better-camouflaged form of intervention. COMEX synthetic gold and related over-the-counter derivatives are traded in macro strategies implemented by hedge funds, high-frequency trades, and commodity funds in pair trades with interest-rate, currencies, equity futures, or even more exotic offsets. The volumes traded are huge, and bear little resemblance to actual flows of physical metal.

“We suspect that shorting gold has come to seem like a riskless proposition as long as there is confidence in the Fed. Synthetic gold is the perfect substance for a carry trade: an easy borrow with very low carrying cost and little upside basis risk. Such a hypothesis, in our opinion, does much to explain the incongruity of a declining gold price while fundamentals for paper currency, and the U.S. dollar in particular, obviously deteriorate; while demand for physical gold has exceeded new mine supply for several years running; and while above-ground 400-ounce .995-gold bars located in London, New York, and other financial capitals (in cohabitation with speculative trading activity in paper markets) have steadily dwindled and disappeared into Asian financial centers reformulated as .9999 kilo bars.”

Hathaway’s letter is posted at the Tocqueville Internet site here:

http://tocqueville.com/insights/tocqueville-gold-strategy-2Q15-partII

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Sunday night: Flash crash on gold

Gold, Precious Metals Flash Crash Following $2.7 Billion Notional Dump

The last time gold plummeted by just over $30 per ounce (dragging down silver and bitcoin with it) and resulted in a crash so furious it led to a “Velocity Logic” market halt for 10 seconds, was in February 2014. Many said this was just perfectly normal selling, although we explicitly said (and showed) that it was a clear case of an HFT algo gone wild (following an order to do just that and slam all sell stops) when someone manipulated the market and repriced gold substantially lower.

Precisely one month ago, some 18 months after the incident, the Comex admitted as much, when it blamed the collapse on “unusually large and atypical trading activity by several of the Firm’s customers and caused the mass entry of order messages by Zenfire, which resulted in a disruptive and rapid price movement in the February 2014 Gold Futures market and prompted a Velocity Logic event.” Curiously despite the “errant” order, gold did not rebound because the entire purpose of the selling slam was to reset the prevailing price far lower. This is what the Comex said in Disciplinary action 14-9807-BC:

Pursuant to an offer of settlement Mirus Futures LLC (“Mirus” or the “Firm”) presented at a hearing on June 16, 2015, in which Mirus neither admitted nor denied the rule violations upon which the penalty is based, a Panel of the COMEX Business Conduct Committee (“BCC”) found that it had jurisdiction over Mirus pursuant to Exchange Rule 418 and that on January 6, 2014, Mirus failed to adequately monitor the operation of its trading platform (Zenfire), and connectivity of its trading system (Zenfire) with Globex. This failure resulted in unusually large and atypical trading activity by several of the Firm’s customers and caused the mass entry of order messages by Zenfire, which resulted in a disruptive and rapid price movement in the February 2014 Gold Futures market and prompted a Velocity Logic event.

The Panel found that as a result, Mirus violated Rules 432.Q. (Conduct Detrimental to the Exchange) and 432.W.

We bring this up because moments ago, just before 9:30pm Eastern time or right as China opened for trading, gold (as well as platinum, silver, and virtually all precious metals) flashed crashed when “someone” sold $2.7 billion notional in gold, resulting in a 4.2% crash in gold, which tumbled to the lowest level since March 2010.

Gold:

Silver:

Platinum:

Once again, as in February 2014 and on various prior cases, the fact that someone meant to take out the entire bid stack reveals that this was not a normal order and price discovery was the last thing on the seller’s mind, but an intentional HFT-induced slam with one purpose: force the sell stops.

So what caused it?

The answer is probably irrelevant: it could be another HFT-orchestrated smash a la February 2014, or it could be the BIS’ gold and FX trading desk under Benoit Gilson, or it could be just a massive commodity fund unwind, or it could be simply Citigroup, which as we showed earlier this month has now captured the precious metals market via derivatives.

Whatever the reason, gold just had its biggest flash crash in nearly two years, as a targeted stop hunt launched by the dumping of $2.7 billion notional in product, accelerates the capitulation of the momentum buyers (and in this case sellers) pushing gold to a level not seen almost since 2009.

The price appears to have rebounded after the initial shock, up about $20 from the intraday low of $1,086 but we expect that to be retested shortly, and for gold to plunge further into triple digits, at which point gold miners will simply cease to produce the metal show all-in production costs are in the $1200 and higher range, at which point it will be clear that only derivatives and “paper” are in play.

But perhaps the biggest irony of the night is that moments before the flash crash, the PBOC revised its shocking Friday announcement revealing its gold holdings had increased by 57%. As Bloomberg said:

- CHINA PBOC REVISES GOLD RESERVES TO 53.32M FINE TROY OUNCES

Previously, this was said to be 53.31 million ounces or 10,000 ounces lower, confirming China is just making up gold inventory “numbers” as it goes along, and clearly buying ever more physical while the price of paper precious metals conveniently plunge ever lower. One thing is certain: the PBOC will be quite grateful to whoever (or whatever) was the catalyst for the latest and greatest gold flash crash as well.

end

And now your overnight trading in bourses, currencies, and interest rates from Europe and Asia:

1 Chinese yuan vs USA dollar/yuan weakens to 6.2097/Shanghai bourse green and Hang Sang: red

2 Nikkei closed

3. Europe stocks in the green /USA dollar index up to 97.97/Euro down to 1.0837

3b Japan 10 year bond yield: remains at 43% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 124.22

3c Nikkei still just above 20,000

3d USA/Yen rate now just above the 124 barrier this morning

3e WTI 50.80 and Brent: 56.99

3f Gold well down /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .80 per cent. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate falls to 21.02%/Greek stocks this morning: stock exchange closed again/ still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield falls to: 11.34%

3k Gold at 1114.65 dollars/silver $14.82

3l USA vs Russian rouble; (Russian rouble down 1/5 in roubles/dollar in value) 57.01,

3m oil into the 50 dollar handle for WTI and 56 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9619 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0431 well below the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving closer to negativity at +.80%

3s The ELA is still frozen today at 88.6 billion euros. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.34% early this morning. Thirty year rate above 3% at 3.07% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

end

Futures Levitate After Greek Creditors Repay Themselves; Commodities Tumble To 13 Year Low

As we said in our Friday morning wrap, a low volume levitation coupled with a stronger dollar managed to lift stocks to yet another green close, while the Nasdaq soared to a new all time high on terrible breadth with decliners far outpacing advancers however it was all about Google which added in value more than the market cap of about 80% of S&P companies.

The dollar’s resumed strength means corporate revenues are about to slide again, confirming the revenue recession that the S&P has found itself will last a long time. However, judging by recent non-GAAP revenue numbers, the algos will gladly ignore the 2-3% recurring decline in top-line number because USD strength is expected to be “one-time” non-recurring which is somewhat of a paradox in a world in which, according to economists, the Fed is poised to hike rates as soon as September.

Today’s action is so far an exact replica of Friday’s zero-volume ES overnight levitation higher (even if Europe’s derivatives market, the EUREX exchange, did break at the open for good measure leading to a delayed market open just to make sure nobody sells) with the “catalyst” today being the official Greek repayment to both the ECB and the IMF which will use up €6.8 billion of the €7.2 billion bridge loan the EU just handed over Athens so it can immediately repay its creditors. In other words, Greek creditors including the ECB, just repaid themselves once again.

One thing which is not “one-time” or “non-recurring” is the total collapse in commodities, which after last night’s precious metals flash crash has sent the Bloomberg commodity complex to a 13 year low.

Finally, of the notable overnight items, when Chinese stocks swooned following comments in Caijing that China’s plunge protection vehicle, the CSF, is studying an exit plan for the stock stabilization plan, China’s Securities Regulatory Commission had no choice but to immediately come out and deny this, which it did: shortly before the Chinese close, the CSRC said it would “continue to focus on stabilizing market and preventing systemic risks.” As a result, the early weakness was BTFDed, and Chinese stocks closed just off intraday highs, up 0.88% to 3,992.

The re-opening of Greek banks after being shut for 3 weeks amid the fall-out between Greece and its creditors failed to spur volatility, with stocks opening up the week in a very muted and contained price action (Euro Stoxx: +1.1%) . More so, the delayed open by EUREX exchange did little to anguish market participants, as the absence of any new pertinent macroeconomic news-flow did little to provide an incentive for sharp moves. As a result, stocks are seen broadly higher, with information tech and energy sectors leading the gains.

At the same time Bunds edged lower, with peripheral bond yield spreads also tighter, albeit marginally as market participants reacted to the re-opening of Greek banks , as well as source comments suggesting that Greece have given the order to make the EUR 6.8bIn repayment to its creditors.

Asian equities shrugged off the positive lead from Wall Street , which saw the NASDAQ-100 hit fresh record highs following a slew of strong earnings from large tech names including Intel and Google . ASX 200 (+0.3%) initially fell amid weakness in miners after the slump in commodity prices, before paring the move late in the session. Shanghai Comp (+0.9%) fluctuated between gains and losses with the index having briefly broke above 4,000, with Chinese property prices over the weekend showing a 2nd consecutive monthly increase, while Y/Y figures continued to decline albeit at a slower pace . Finally markets in Japan remained closed due to Marine day holiday.

In FX, EUR/USD edged higher, with the 1-month implied volatility falling to its lowest level since March , supporting other EUR related crosses such as EUR/JPY and EUR/GBP, which in turn saw GBP/USD move through the 50DMA to the downside. The apparent risk on sentiment meant that EUR/CHF remained bid since the open, while USD/JPY grinded to its higher level since 24th June.

In commodities, the most notable move was the previously noted Gold flash crash which trades lower, albeit off the overnight lows where prices fell by as much as USD 43/oz in a minute to hit the lowest level since March’10. Some analysts noted that the move was exacerbated by stops being tripped on the break of last week’s lows and through USD 1100 which was also the lowest in 5 years . For a summary of the selling seen in Gold please click here. Elsewhere in the metals complex Platinum fell below USD 1000/oz for the first time since February 2009 while analysts at Goldman Sachs have said that they are still extremely bearish on copper and consider the current nickel price as an opportunity to buy or hedge. The energy markets trades relatively range bound amid light news flow, with Brent underperforming WTI amid concerns over increasing Iranian crude supplies.

Going forward, the ongoing earnings reporting season will regain the focus, with the attention centred on IBM and Morgan Stanley.

In summary: European shares rise with the tech and health care sectors outperforming and basic resources, media underperforming. Greece gave order to repay EU6.8b to creditors after last week’s tentative bailout deal as Greek banks reopened. Gold drops, dollar trades near a 3-month high versus euro. The Italian and Swedish markets are the best-performing larger bourses, U.K. the worst. The euro is little changed against the dollar. Irish 10yr bond yields fall; French yields decline. Commodities decline, with gold, natural gas underperforming and WTI crude outperforming.

Market Wrap

- S&P 500 futures up 0.1% to 2121.5

- Stoxx 600 up 0.6% to 408.1

- US 10Yr yield little changed at 2.35%

- German 10Yr yield down 3bps to 0.76%

- MSCI Asia Pacific down 0.3% to 144.2

- Gold spot down 1.9% to $1112.5/oz

- 18 out of 19 Stoxx 600 sectors rise; tech, health care outperform, basic resources, media underperform

- Asian stocks fall with the Shanghai Composite outperforming and the Kospi underperforming; MSCI Asia Pacific down 0.3% to 144.2

- Nikkei closed, Hang Seng down 0%, Kospi down 0.2%, Shanghai Composite up 0.9%, ASX up 0.3%, Sensex down 0.2%

- Euro up 0.07% to $1.0838

- Dollar Index up 0.13% to 97.99

- Italian 10Yr yield down 6bps to 1.86%

- Spanish 10Yr yield down 6bps to 1.88%

- French 10Yr yield down 4bps to 1.03%

- S&P GSCI Index down 0.7% to 401.8

- Brent Futures down 0.8% to $56.6/bbl, WTI Futures down 0.3% to $50.7/bbl

- LME 3m Copper down 0.5% to $5455/MT

- LME 3m Nickel down 0.4% to $11450/MT

- Wheat futures down 1.4% to 546 USd/bu

Bulletin headline summary from Bloomberg and RanSquawk

- Gold trades lower, albeit off the overnight lows where prices fell by as much as USD 43/oz in a minute to hit the lowest level since March’10.

- The re-opening of Greek banks after being shut for 3 weeks amid the fall-out between Greece and its creditors failed to spur volatility, with stocks opening up the week in a very muted and contained price action.

- Going forward, the ongoing earnings reporting season will regain the focus, with the attention centred on IBM and Morgan Stanley.

- Treasury curve little changed in overnight trading, today offers no economic data nor Fed speakers ahead of next week’s FOMC meeting; 3M and 6M bill auctions today; Japan closed for Marine Day.

- Greece gave the order to repay €6.8b ($7.4b) to creditors after last week’s tentative bailout deal, the Finance Ministry said, as Greek banks reopened

- BlackRock, which oversees about $4.7t, bought Greek debt last week, benefiting from prices that were overly depressed by investor concern that the nation would struggle to implement requirements of its latest bailout deal

- Barclays is considering deeper job cuts that could see its workforce shrink by about a quarter over the coming years, said a person with knowledge of the matter

- Job vacancies in London’s financial services industry jumped 56% in June, reversing a drop in the previous month, led by compliance hiring, a survey showed

- The business of financing China’s trade is shrinking, curbing what had been a fast-growing revenue stream for banks in Hong Kong and Singapore over the past decade

- A fifth of China’s stock market remains frozen as 576 companies were suspended on mainland exchanges as of the midday break on Monday, equivalent to 20% of total listings, and down from 635 at the close on Friday

- Gold fell to the lowest level in more than five years on the outlook for higher U.S. interest rates and as China said it held less of the metal in reserves than some analysts forecast

- Gold pared losses amid speculation the sudden slump in prices in morning trade in Asia was driven by larger- than-usual volumes being sold in China and New York

- Sovereign 10Y bond yields mostly lower. European stocks rise, China drops and Japan closed for Marine Day, U.S. equity- index futures rises. Crude oil, copper and gold fall

US Event Calendar

- No major reports

DB’s Jim Reid completes the overnight summary

After three successive Sundays spent ruminating about Greece, it felt like there was a big void in my life yesterday. A very heavy England loss in the cricket deepened it. Given that the last three Sunday evenings had been spent working, I offered my wife her choice of how we spent last night. She suggested I cook dinner and we watch “Fifty Shades of Grey”. All I can say is that it was a terrible movie and that I longed for a Greece conference call to distract me. I nearly tried to invent a fake one!

Talking of Greece, the banks re-open today for the first time in three weeks. Greece is unlikely to be a huge macro influence now for a couple of months but events like this are certainly worth keeping an eye on to assess the likelihood of future progress or lack of it. Aside from the banks we also heard from German Chancellor Merkel who suggested that it would be possible to discuss Greek debt relief through extending maturities once the ESM deal has been negotiated, but she once again reiterated the ruling out of any haircuts. Merkel also dismissed any suggestions of a dispute with German Finance Minister Schaeuble who had said in a Der Spiegel interview over the weekend that the two had differences, although he downplayed any talks of a potential resignation. Meanwhile, late on Friday we also saw Greek PM Tsipras announce a cabinet reshuffle as largely expected, replacing various members of the Syriza party who had previously opposed the proposals at the parliamentary vote last week, including the more outspoken Left Platform faction leader Lafazanis.

Looking at how markets have kicked off the week in Asia this morning, as well as most equity bourses starting on a soft-ish note Gold (-2.26%) has taken a steep leg lower to a five-year low of $1109/oz after a report out of the PBoC on Friday shedding light on the amount of reserves China was holding. Despite a 60% rise relative to the last report in 2009, the amount of reserves have seemingly disappointed the market relative to expectations with bullion at once stage falling nearly 5% this morning. The tumble follows a 1% fall on Friday. Elsewhere the Dollar index is +0.2% in early trading while equity bourses are mostly trading down. In China the Shanghai Comp (-0.43%) and CSI 300 (-0.93%) have reversed earlier gains, while the Shenzhen (+0.12%) is fluctuating between gains and losses with 633 companies (around 22% of listings) still suspended from trading on the mainland exchanges. The Hang Seng (-0.24%) and Kospi (-0.25%) are also down while bourses in Japan are closed for a public holiday. Asia credit is unchanged this morning.

Back to Friday, it was a reasonably quiet day on the whole in markets with investors seemingly taking something of a breather following the Greece and China driven moves of the last few weeks. In the US the S&P 500 closed +0.11%, although this hid what was largely broad based declines with all sectors closing in negative territory aside from tech stocks which benefited from a 16% rally for Google following Thursday’s post market close earnings report. This helped support the NASDAQ (+0.91%) which extended its recent record high while the Dow (-0.19%) finished a touch lower. The Dollar benefited from a post-CPI print boost with the Dollar index finishing +0.20% having initially traded lower on Friday to close out a solid week (+1.91%). Just on the data, the June headline (+0.3% mom) and core (+0.2% mom) both came in as expected, helping to lift the annualized rates to +0.1% yoy and 1.8% yoy respectively, a 0.1% increase for both relative to May. A decent lift in shelter costs during the month was cited as contributing significantly to the month’s print, while the 6-month annualized core print of 2.3% is now the highest since January 2012.

Elsewhere on the data front, housing starts (+9.8% mom vs. +6.7% expected) and building permits (+7.4% vs. -8.0% expected) for June both came in well ahead of expectations with the latter in particular rising to a 8-year high on an annualized basis although the expiring tax abatement program in the Northeast has been a large reason for the recent surge in permits. The preliminary University of Michigan reading for July was slightly disappointing however, falling 2.8pts to 93.3 (vs. 96.0 expected). Declines were fairly evenly split across the current conditions (-2.9pts to 106.0) and expectations (-2.6pts to 85.2) surveys although we did see +0.1% increases for the 1yr (+2.8%) and 5-10yr (+2.7%) inflation expectations surveys. 10yr Treasuries closed virtually unchanged on the day at 2.348% having traded in a tight range.

There was an equally subdued feeling to trading in European markets on Friday. The Stoxx 600 saw a modest +0.06% gain to help cap a 4.3% return for the week, while regionally it was reasonably mixed with the CAC (+0.06%) up but with declines for the DAX (-0.37%), IBEX (-0.26%) and FTSE MIB (-0.07%). Despite no data in the region, bond yields declined with 10y Bunds closing 4.4bps lower at 0.786% while Italy (-7.0bps), Spain (-4.8bps) and Portugal (-4.1bps) were all led lower with also a decline in yields across the Greek curve.

Elsewhere, with Greek headlines abating, some of that focus is now turning to Ukraine where the FT is reporting that the nation has extended talks with creditors amid precautions that the country could default as soon as Friday if no agreement is reached. A joint statement issued last week suggested that progress has been made, however a deal to restructure Ukraine’s $70bn debt load has still yet to have been reached. The FT is reporting that Ukraine is looking for a 40% haircut on bonds in order to make the debt load sustainable, however the group of four creditors, much like the Greek situation, continue to insist that a haircut is not needed and instead have proposed maturity extensions and coupon reductions. One to keep an eye on for now.

Taking a look at this week’s calendar. With no data due in the US it’s a reasonably quiet start to proceedings today with just German PPI for June the only notable release. Tuesday starts in Japan where we get the Conference Board leading index before we turn over to the UK where we get public sector net borrowing data. It’s quiet once again in the US tomorrow with no data due. We kick off the Asia session on Wednesday with the June Conference Board leading indicator out of China. French business and manufacturing confidence and Italian industrial orders follow before we get the Bank of England minutes. In the US on Wednesday we’ve got existing home sales for June along with the FHFA house price index due. Turning to Thursday, Japan trade data will be closely watched in the morning while we get UK retail sales and Euro area consumer confidence closer to home. Initial jobless claims, Chicago Fed National activity index, Conference Board leading indicator and the Kansas City Fed manufacturing activity print are all due in the US. We end the week on Friday with the flash July PMI indicators for the Euro area as well as regionally in Germany and France. Meanwhile in the US we conclude the week with new home sales for June as well the flash manufacturing PMI for July. With a fairly quiet calendar for data, there will be much focus on earnings where we see 131 S&P 500 companies reporting this week including Apple, Microsoft, Amazon, Verizon, AT&T and Coca-Cola.

The huge losses in the stock market is having a devastating effect on the Chinese property market as we are witnessing massive cancellations on property deals:

China Stock Rout “Rocks” Property Market: “Massive” Cancellations Expected

To be sure, we’ve had our fair share of laughs at the expense of China’s newly-minted day traders.

Back in March, Bloomberg highlighted a study which suggested that some 31% of new investors in China’s equity markets had an elementary school education or less. Shortly thereafter, we began to look at data from the China Securities Depository and Clearing Co which showed that millions of new stock trading accounts were being created in China every single month. Once reports began to come in from the front lines of China’s inexorable equity rally, it became clear that (to say the least) not everyone pouring money into the SHCOMP and The Shenzhen was what you might call a “seasoned” investor.

From there, all it took was the suggestion from Bloombergthat in some cases, Chinese housewives had traded in the crochet kit for technical analysis and the race was on to see who could come up with the most entertaining characterization of China’s day trading hordes. Although the mainstream media has been careful not to be terribly explicit in their ridicule, the increasingly hilarious pictures of bemused Chinese grandmas staring at ticker tapes that have appeared atop WSJ and Reuters articles betray the fact that everyone, everywhere sees the humor in a multi-trillion dollar stock bubble driven by margin-trading hairdressers.

Admittedly, all of the above was even more amusing on days when Chinese stocks closed red, as it became quickly apparent that many Chinese investors might not have fully appreciated the fact that stocks can go down as well as up.

In the good old days of the China stock rally (so, around two months ago), down days were few and far between and the outright confusion that reigned in the wake of a rare close lower served as a much needed comic interlude for the slow motion train wreck unfolding in the Aegean and, on the weekends, at various Euro summits.

However, once the unwind began in China’s CNY1 trillion backdoor margin lending channels, we couldn’t help but feel slightly sorry for the millions of Chinese who quickly went from bewildered to dejected after watching their life savings evaporate over the course of a brutal three week sell-off that totaled more than 30% on some exchanges.

Due to significant retail participation and due to the fact that the equity mania had served as a distraction for a nation coping with decelerating economic growth and a bursting property bubble, some (and we were among the first) began to suggest that the broader economy, and indeed, social stability, may be at risk in China if stocks continued to fall.

The extent to which this suggestion represented a real concern (as opposed to the ravings of a tin foil hat fringe blog) was underscored by the extraordinary measuresChina adopted in a desperate attempt to stop the bleeding and later by several sellside strategists who began to warn about possible spillovers into the real economy.

Now, with Beijing still struggling to restore the stock bubble, the first signs of knock-on effects are beginning to emerge. Here’s Nikkei with more:

Turbulence on China’s equity market is starting to rock the country’s property market. Investors are quickly pulling their cash out of housing they purchased to cover losses incurred by stock investments. Some have begun offering discounts on property due to difficulties with finding buyers. Continued turmoil on the stock market looks as though it will have a heavy impact on the country’s real estate market.

China’s stock market rally also helped drive up sales of domestic homes. The Shanghai Composite Index surged 60% from its low of around 3,200 in early March, rising to 5,166 logged on June 12. China Securities Depository and Clearing said that the number of accounts opened to trade yuan-denominated A-shares reached 980,000 in May in Shenzhen, where property prices are climbing faster than other areas. The figure accounted for roughly 80% of the total 1170,000 accounts in Guangdong Province, where large numbers of such account holders reside.

Many newbie investors, who have just jumped into the stock market, likely gave a fresh impetus to the property market.China’s share price upswing prompted investors to reach out for new investments, including houses and other properties. A property analyst at major Chinese brokerage Guotai Junan Securities said that sales of luxury properties worth over 10 million yuan ($1.61 million) each for the first half of the year topped annual sales last year in Shanghai and Beijing.

After this, Chinese stocks began to crumble. In early July, the Shanghai Composite Index dropped more than 30%, after hitting a seven-year high in mid-June. Investors who suffered big losses on the stock market were forced to sell property and cancel real estate purchase agreements. The Hong Kong Economic Times said that consumers are increasingly asking real estate firms for grace periods on down payments for mortgage loans, as they run out of cash because of weak stocks.

Some canceled home purchase contracts, while others canceled mortgage loans,according to China’s largest property developer China Vanke, which has a strong foothold in Shenzhen. Local media reported that an official at China Vanke is concerned about massive numbers of cancellations in the future.

So no, the damage isn’t “contained” and indeed it’s somewhat ironic that the first place the contagion is showing up is in China’s property market. What’s particularly interesting here is that one argument for why the collapse of China’s equity bubble would not spill over into the real economy revolved around the fact that the majority of Chinese household wealth is concentrated in real estate. “Ultimately, we think the impact of the sell-off in Chinese equities on the real economy will be relatively limited. This is because equities are only 10% of household wealth (at peak; just over 5% at the turn of the year),” Credit Suisse noted last week.

If, however, what Nikkei says about the knock-on effect in property is true, it could put further pressure on an already fragile housing market. On that note, we’ll close with the following excerpt which is, ironically, from the same Credit Suisse note cited above.

House prices are now falling at a record annual rate – the first time they have fallen without it being policy induced. With housing accounting for just over half of total household assets, the negative wealth impact could be significant.

end

Greek banks are now set to open as Tsipras’s new cabinet takes over. However capital controls will still be in place. The only difference is that if a depositor misses a day they can make it up the following day. Greeks are allowed to withdraw only 60 euros per day or 420 euros per week. The citizens are not happy campers.

(courtesy Bloomberg/Chrepa)

Greek Banks to Reopen as Tsipras’s New Cabinet Takes Over

Greek banks will reopen on Monday as Prime Minister Alexis Tsipras rebuilds his government to shore up support for a bailout agreed upon with the country’s creditors.

The banks, which have remained closed since June 29, will open July 20, the government said on Saturday. Most capital controls concerning withdrawals and money transfers will remain, and while the daily limit was held at 60 euros ($65), a cumulative limit of 420 euros a week was set, it said.

Lenders will reopen a week after Tsipras and creditors agreed to a bailout program and Greek lawmakers approved legislation needed to release funding for the country. Hours after the vote, the European Central Bank approved emergency financing for the country’s lenders and the European Union finalized a bridge loan on Friday to provide a stop-gap until a full three-year rescue program, worth as much as 86 billion euros, is settled.

“This will improve the image of the economy for Greeks inside the country,” said Aristides Hatzis, an associate professor of law and economics at the University of Athens. “It’s just the beginning and a more ambitious option wasn’t possible.”

The prime minister’s office said Panagiotis Skourletis will replace Panagiotis Lafazanis, who heads the Left Platform fraction of Tsipras’s Syriza party, as energy minister. George Katrougalos will succeed Skourletis as labor minister. Nadia Valavani, Dimitris Stratoulis, Kostas Isichos and Nikos Chountis, who also, as Lafazanis, voted against the legislation, were removed from the government.

Held Hostage

Following Thursday’s vote, Tsipras told his associates that he would be forced to lead a minority government until a final deal with creditors is concluded. In all, 64 of the parliament’s 300 lawmakers voted against the bill. Half of the “no” votes came from Syriza, including former Finance Minister Yanis Varoufakis.

Tsipras is “being held hostage by both his lawmakers, who refuse to vote for the measures, and by the opposition, whose support he needs to pass the measures through parliament,” Hatzis said. “The only way out is elections.” His new government will probably last “a maximum of two months,” he said.

The German parliament also cleared the way for talks on a third bailout after Chancellor Angela Merkel warned that failing to try would be reckless and sow chaos. Finland’s parliament gave its approval Thursday, while Austrian lawmakers also backed negotiations.

“What we are witnessing is European solidarity in action,” Valdis Dombrovskis, EU Commission vice president for euro policy, said Friday. “This agreement backed by 28 European Union member states prevents Greece from an immediate default.”

end

Greeks Get First Look At Their Future: Long Bank Lines And Punishing Taxes

Although the details of Greece’s third bailout program have yet to be finalized, Monday marked the beginning of a new dawn for Greeks. Last week, PM Alexis Tsipras forced a set of draconian “reforms” through parliament and sacked political rivals, effectively legislating away the country’s sovereignty while condemning the Greek people to a fate of even tougher austerity and ensuring that despite rhetoric out of Athens, “normality” will not return to Greece for a very long time.

Greek banks reopened and as expected there were long lines. On the bright side, the queues were described as “orderly.” From AP:

In downtown Athens, people lined up in an orderly fashion as the banks unlocked their doors at 8 a.m., taking a number and reading the paper as they waited for their turn at the till.

Many restrictions on transactions, including cash withdrawals, remained, however.

The Greek government kept the daily cash withdrawal limit at 60 euros ($65) but added a weekly limit of 420 euros ($455) that will be available beginning Sunday. This means depositors who don’t make it to the bank on Monday to withdraw cash could pull out 120 euros ($130) on Tuesday instead, and so on, so Greeks don’t have to feel they need to visit an ATM every day.

Bank customers will still not be able to cash checks, only deposit them into their accounts, and they will not be able to get cash abroad with their credit or cash cards, only make purchases. There are also restrictions on opening new accounts or activating dormant ones.

Meanwhile, the VAT hike – one of the most contentious “red lines” from Greece’s negotiations with creditors – kicked in. The tax rose to 23% from 13% on everything from salt to firewood. Restaurants and taxi fares are also affected. Just call it an EMU member fee.

Additionally, Greece gave the go ahead for Europe to pay itself back for previous loans to Athens. Over the weekend, the country received an EFSM bridge loan for €7 billion – €6.8 billion was used on Monday to repay creditors, including the ECB. As noted on Sunday, “now that a new circular funding scheme has been devised that will allow Greece to make a €3.5 billion (€4.2 billion with interest) payment to Mario Draghi on Monday, the ELA liquidity drip can continue.”

As for the possibility that Greece could see its debt written down as part of a push by Brussels to appease the IMF (and by extension, the US Treasury), Angela Merkel looks to have driven the final nail in that coffin on Sunday. Here’s Bloomberg:

“A classic haircut — writing down 30 or 40 percent of the debt — this cannot happen in a currency union,” Merkel says in interview with German broadcaster ARD. “You can have it outside a currency union, but you can’t have it in a currency union.“

“Part of the wish for Greece to remain in the euro area is that such a haircut is not possible,” Merkel says

Merkel says euro leaders will discuss extension of Greek debt maturities and easing interest rates “when the first successful assessment of the program being negotiated now is completed.”

“Exactly this question will be discussed then,” Merkel says on debt relief. “Not now, but then.”

In other words, there can be “re-profiling” (as suggested by the EU Commission), but there will be no writedown, and indeed Christine Lagarde seemed resigned to the impossibility of a haircut last week.

So that’s it – a rather depressing and anticlimactic end to the Syriza “revolution” and, by extension, to “hope” in Greece. More austerity is now the law and Athens is once again completely beholden to the German purse string.

But hey, at least there are no tanks in the streets.

end

Greece today in 9 charts:

(courtesy zero hedge)

Greece Is Now A Full-Blown Humanitarian Crisis – In 9 Charts

The people of Greece are facing further years of economic hardship following a Eurozone agreement over the terms of a third bailout. The deal included more tax rises and spending cuts, despite the Syriza government coming to power promising to end what it described as the “humiliation and pain” of austerity. With the country having already endured years of economic contraction since the global downturn, The BBC asks, justhow does Greece’s ordeal compare with other recessions and how have the lives of the country’s people been affected?

The long recession

It is now generally agreed that Greece has experienced an economic crisis on the scale of the US Great Depression of the 1930s.

According to the Greek government’s own figures, the economy first contracted in the final quarter of 2008 and – apart from some weak growth in 2014 – has been shrinking ever since. The recession has cut the size of the Greek economy by around a quarter, the largest contraction of an advanced economy since the 1950s.