Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1090.20 up $4.50 (comex closing time)

Silver $14.67 up 12 cents.

In the access market 5:15 pm

Gold $1090.00

Silver: $14.67

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a poor delivery day, registering 8 notices for 800 ounces Silver saw 27 notices for 135,000 oz

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 235.44 tonnes for a loss of 67 tonnes over that period.

In silver, the open interest fell by 1637 contracts despite the fact that silver was unchanged yesterday. The total silver OI continues to remain extremely high, with today’s reading at 184,211 contracts In ounces, the OI is represented by .9210 billion oz or 131% of annual global silver production (ex Russia ex China). This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end as they continue to raid as basically they have no other alternative.

In silver we had 27 notices served upon for 135,000 oz.

In gold, the total comex gold OI rests tonight at 432,301. We had 8 notices filed for 800 oz today.

We had no change in gold leaving the GLD today / thus the inventory rests tonight at 667.93 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. I thought that 700 tonnes is the rock bottom inventory in GLD gold, but I guess I was wrong. However we must be coming pretty close to a level of only paper gold and the GLD being totally void of physical gold. In silver, we had no changes in silver inventory at the SLV, / Inventory rests at 326.209 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fell by 1637 contracts down to 184,211 even though silver was unchanged in price yesterday. Again, we must have had some short covering. The OI for gold fell by 1972 contracts to 432,301 contracts as gold was down by $5.00 yesterday. We still have close to 22 tonnes of gold standing with only 19.66 tonnes of registered gold in the dealer vaults ready to satisfy that which stands.

(report Harvey)

2. One story on Greece whereby the IMF will delay making a decision to join in the bailout until the fall

(courtesy Reuters)

3.Gold trading overnight, Goldcore

(/Mark OByrne)

4. Two stories on the plummeting stock market and economy inside China

(zero hedge)

5 Trading of equities/ New York

(zero hedge)

6. USA stories:

i) Data for today:

a) huge layoffs reported in the Challenger/Christmas/Gray report

b) the Thursday jobless report

c) Atlanta Fed reports that they believe 3rd quarter GDP will be only 1%

d) Personal finance confidence falters badly

ii) Looks like the FBI are undergoing a criminal probe on Hillary

(zero hedge)

6. Two oil related stories:

(zero hedge/Wolf Richter)

7. James Turk discusses gold backwardation with greg Hunter

(Greg Hunter usa watchdog/James Turk/Dave Kranzler)

8. The next “Argentina” is Brazil: (i.e. to default)

(two stories/zero hedge)

9. Iran refuses to let inspectors in:

(zero hedge)

10. The Bank of England reports that they are now moving to the dovish side as the global economy is sinking:

(zero hedge/Bloomberg)

11.Silver production from the mines fell off the cliff these past few months;

(Steve St Angelo/SRSRocco report)

12.

Here are today’s comex results:

The total gold comex open interest fell from 434,273 down to 432,301 for a loss of 1972 contracts as gold was down $5.00 yesterday. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month, and today the latter stopped its decline and actually rose. What is interesting is that the LBMA gold is witnessing a 7.40 premium spot/next nearby month as gold is now in backwardation over there. We are now in the contract month of August and here the OI fell by 2718 contracts falling to 3875 contracts. We had 2828 notices filed upon on yesterday and thus we gained 110 contracts or 11,000 additional ounces will stand for delivery. The next delivery month is September and here the OI rose by 245 contracts up to 2523. The next active delivery month if October and here the OI rose by 300 contracts up to 26,713. The estimated volume on today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was poor at 82,238. The confirmed volume on yesterday (which includes the volume during regular business hours + access market sales the previous day was poor at 127,924 contracts. Today we had 8 notices filed for 800 oz.

And now for the wild silver comex results. Silver OI fell by 1637 contracts from 185,848 contracts down to 184,211 despite the fact that silver was unchanged in price yesterday . We continue to have some short covering as our bankers pulling their hair out with respect to the continued high silver OI as the world senses something is brewing in the silver arena. We are in the delivery month of August and here the OI fell by 0 contracts remaining at 60. We had 0 delivery notices filed yesterday and thus we gained 0 contracts or an additional zero ounces will stand for delivery in this non active August contract month. The next major active delivery month is September and here the OI fell by 3023 contracts to 113,664. The estimated volume today was poor at 21,236 contracts (just comex sales during regular business hours). The confirmed volume yesterday (regular plus access market) came in at 43,932 contracts which is excellent in volume. We had 27 notices filed for 135,000 oz.

August contract month: initial standing

August 6.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 16,916.156 oz (JPMorgan,Scotia) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 18,043.443 (Delaware,Scotia) |

| No of oz served (contracts) today | 8 contracts (800 oz) |

| No of oz to be served (notices) | 3867 contracts (386,700 oz) |

| Total monthly oz gold served (contracts) so far this month | 3178 contracts(317,800 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 292,138.1 oz |

Today, we had 0 dealer transactions

total Dealer withdrawals: nil oz

we had 0 dealer deposits

total dealer deposit: zero

total customer withdrawal: 16,916.156 oz

We had 2 customer deposits:

i) Into Delaware: 1770.37 oz

ii) Into Scotia: 16,273.406 oz

Total customer deposit: 18,043.443 oz

We had 1 adjustment

ii) out of Scotia: 10,754.504 oz was adjusted out of the dealer and this landed into the customer account of Scotia.

JPMorgan has 11.66 tonnes left in its registered or dealer inventory.

(375,019.978 oz)

.

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 8 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 2 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the August contract month, we take the total number of notices filed so far for the month (3178) x 100 oz or 317,800 oz , to which we add the difference between the open interest for the front month of August (3875) and the number of notices served upon today (8) x 100 oz equals the number of ounces standing

Thus the initial standings for gold for the August contract month:

No of notices served so far (3178) x 100 oz or ounces + {OI for the front month (3875) – the number of notices served upon today (8) x 100 oz which equals 704,600 oz standing so far in this month of August (21.916 tonnes of gold).

Thus we have 21.916 tonnes of gold standing and only 19.66 tonnes of registered or dealer gold to service it.

We gained 110 contracts or an additional 11,000 oz will stand for delivery in this active month of August.

Total dealer inventory 632,041.588 or 19.66 tonnes

Total gold inventory (dealer and customer) = 7,569,584.573 oz or 235.44 tonnes

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 235.41 tonnes for a loss of 67 tonnes over that period.

end

And now for silver

August silver initial standings

August 6 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,028,623.39 oz (CNT,Brinks, Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 27 contracts (135,000 oz) |

| No of oz to be served (notices) | 33 contracts (165,000 oz) |

| Total monthly oz silver served (contracts) | 45 contracts (225,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 85,818.47 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,039,673.1 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 0 customer deposits:

total customer deposits: nil oz

We had 3 customer withdrawals:

i)Out of Brinks: 1000.000 oz ????

ii) Out of CNT: 967,619.46 oz

iii) Out of Scotia: 1,028,623.38 oz

total withdrawals from customer: 1,028,623.38 oz

we had 2 adjustments

Total dealer inventory: 55.829 million oz

Total of all silver inventory (dealer and customer) 172.381 million oz

The comex has been bleeding silver lately.

The total number of notices filed today for the August contract month is represented by 27 contracts for 135,000 oz. To calculate the number of silver ounces that will stand for delivery in August, we take the total number of notices filed for the month so far at (45) x 5,000 oz = 225,000 oz to which we add the difference between the open interest for the front month of August (60) and the number of notices served upon today (27) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the August contract month:

45 (notices served so far)x 5000 oz + { OI for front month of August (60) -number of notices served upon today (27} x 5000 oz ,= 390,000 oz of silver standing for the August contract month.

we neither gained nor lost any silver ounces in this delivery month of August.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.comorhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

August 6/no change in gold inventory at the GLD/Inventory rests at 667.93 tonnes

August 5.we had a huge withdrawal of 4.77 tonnes from the GLD tonight/Inventory rests at 667.93 tonnes

August 4.2015: no change in inventory/rests tonight at 672.70 tonnes

August 3.2015: no change in inventory at the GLD./Inventory remains at 672.70 tonnes

July 31/we had a huge withdrawal of 7.45 tonnes/Inventory rests this weekend at 672.70 tonnes

July 29/no change in inventory/rests tonight at 680.13 tonnes

July 28/no change in inventory/rests tonight at 680.13 tonnes

July 27/no change in inventory/rests tonight at 680.13 tonnes

July 24.2015/we had another massive withdrawal of 4.48 tonnes of gold form the GLD/Inventory rests at 680.13 tonnes.

July 23.2015: we had another withdrawal of 2.68 tonnes of gold from the GLD/Inventory rests at 684.63 tonnes

july 22/another withdrawal of 2.38 tonnes of gold from the GLD/Inventory rests at 687.31

July 21.2015: a massive withdrawal of 6.56 tonnes of gold from the GLD.

Inventory rests at 689.69 tonnes. China and Russia need their physical gold badly and they are drawing their physical from this facility.

July 2o.2015: no change in inventory

July 17./a massive withdrawal of 11.63 tonnes in gold tonnage tonight from the GLD/Inventory rests at 696.25 tonnes

July 16./we lost 1.19 tonnes of gold tonight/Inventory rests at 707.88 tonnes

August 6 GLD : 667.93 tonnes

end

And now SLV:

August 6/no changes in SLV/inventory rests at 326.209 million oz

August 5/ a small withdrawal of 142,000 oz of inventory leaves the SLV/Inventory rests tonight at 326.209 million oz

August 4.2015: a small withdrawal of 476,000 oz of inventory at the SLV/Inventory rests at 326.351 million oz

August 3.2015; no change in inventory at the SLV/inventory remains at 326.829 million oz

And now for silver (SLV) July 31/no change in inventory/rests tonight at 326.829 million oz

July 29/no change in silver inventory/326.829 million oz

July 28/we had a huge withdrawal of 2.005 million oz from the SLV/Inventory rests at 326.829 oz

July 27/no change in silver inventory/inventory rests tonight at 328.834 million oz

July 24/no change in silver inventory/inventory rests tonight at 328.834 million oz

July 23.2015; no change in silver inventory/rests tonight at 328.834 million oz

july 22/no change in silver inventory/inventory rests at 328.834 million oz.

July 21.we had a massive addition of 1.241 million oz into the SLV/Inventory rests tonight at 328.834 million oz.

Please note the difference between gold and silver (GLD and SLV). In GLD gold is being depleted and sent to the east. In silver: no depletions, as I guess this vehicle cannot supply physical metal.

July 20/no change

july 17.2015/no change in silver inventory tonight/inventory at 327.593 million oz

July 16./no change in silver inventory/rests tonight at 327.593 million oz

August 6/2015: tonight inventory rests at 326.209 million oz

end

And now for our premiums to NAV for the funds I follow:

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 11.4 percent to NAV usa funds and Negative 11.7% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 62.0%

Percentage of fund in silver:37.7%

cash .3%

( August 6/2015)

2. Sprott silver fund (PSLV): Premium to NAV falls to -1.04%!!!! NAV (August 5/2015) not out today

3. Sprott gold fund (PHYS): premium to NAV rises to – .76% to NAV(July August5/2015) not out today

Note: Sprott silver trust back into negative territory at- 1.04%

Sprott physical gold trust is back into negative territory at -.76%

Central fund of Canada’s is still in jail.

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64)

Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis.

Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer.

Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer.

* * * * *

>end

And now for your overnight trading in gold and silver plus stories

on gold and silver issues:

(courtesy/Mark O’Byrne/Goldcore)

a must read….

Gold Bullion Demand In ‘Chindia’ Heading Over 2,000 Tons Again

- Shanghai Gold Exchange deliveries at 73.289 tonnes last week

- 3rd largest week of gold withdrawals ever on SGE

- Both China and India heading for over 1,000 metric tonnes in 2015 … again

- India imports 96.1 tonnes in May alone

- ‘Chindia’ imports 296.55 tonnes in May – 14% greater than global production

- South Korean gold demand surges in wake of Chinese crash

- Asian and global gold demand robust contrary to anti-gold narrative

The recent lower prices in gold have not deterred investors internationally from buying gold coins and bars in large volumes again. Indeed the Perth Mint and the US Mint are struggling to fulfill demand for gold coins and bars.

This is particularly the case in the eastern hemisphere – especially in India and China – where demand has again increased significantly on price weakness.

Between them, these two countries are on-track to import 2,000 tonnes of gold this year – that is more than two thirds of the total annual global gold mine production, which is set to be about 2,800 tonnes this year. (Harvey: 2,200 ex China ex Russia)

The Shanghai Gold Exchange, which deals exclusively in physical bullion, saw buyers take delivery of over 73 tonnes of gold last week, the third largest withdrawal on record. This follows two weeks of steadily increasing demand as investors pull or attempt to pull money out of the Chinese stock market.

Demand out of China is on track to surpass last year’s official figure of 974 tonnes and may reach 1,000 tonnes this year. Chinese demand has been steadily growing, with the encouragement of the government. The ban on gold ownership imposed by Chairman Mao in 1949 was lifted in 2003.

As such, demand from the nation of 1.3 billion people who have a strong cultural affinity to gold – and experience of monetary mismanagement and hyperinflation – has been rising from a base of nearly zero and has recently surpassed that of India to become the world’s top gold buying nation. Nonetheless, Chinese gold ownership remains very low when compared to that of India.

Prudent Indian households hold 11% of the world’s gold. That is more gold than the gold reserves that the U.S. Federal Reserve, the German Bundesbank and the Swiss central bank are believed to own put together.

Indian demand remains robust. In April and May alone the country imported over 155 tonnes of the precious metal.

Demand so far this year has greatly exceeded that of the same period last year – up 61% – as Indians take advantage of the low prices despite the fact that we are some months away from the typical gold buying season. Indian demand is also expected to hit 1,000 tonnes this year.

Together, “Chindia” imported 296.55 tonnes of gold in May. This surpasses current monthly mine supply globally by 14%. Clearly there is an imbalance in the gold market when demand from two countries alone exceeds total mine supply, which must then be supplemented by existing stocks. (Harvey: world produces 183 tonnes per month)

Yet prices remain in a downward trend as speculative short selling continues to depress prices. Indeed it not just the huge Asian nations of China and India where demand remains high. There are reports of strong demand – including by thePerth Mint – in Thailand, Vietnam and Malaysia. Demand for gold in South Korea has surged in recent weeks, according to Reuters.

Koreans, nervous about the fallout from the crash in China’s stock market, are choosing to diversify into gold and take advantage of lower dollar prices.

This trend is likely to be repeated across east and south-east Asia in countries who are reliant on the increasingly important Chinese economy.

While it is unlikely to have significant impact on global demand – last year’s demand from South Korea amounted to only 17 tonnes – it demonstrates the psychological appeal that gold still has in times of economic crisis among people across the world – and especially in Asia.

The triumphalism with which some Wall Street commentators have covered the temporary set-back in gold prices looks misplaced and misguided. This is especially the case when the bigger picture is taken into account – including the significant macreconomic, systemic, geopolitical and monetary risks of today.

These are being ignored for now – as they were in 2007 and early 2008.

Gold will continue to retain value well into the future – a claim we would not be too confident about making with regards to paper currencies and bonds issued by the most indebted nations in the world.

Own allocated, segregated gold coins and bars of which you can take delivery.

MARKET UPDATE

Today’s AM LBMA Gold Prices were USD 1,085.00, EUR 996.05 and GBP 694.56 per ounce.

Yesterday’s AM LBMA Gold Prices were USD 1,086.50, EUR 1,000.18 and GBP 697.82 per ounce.

Gold and silver on the COMEX were nearly unchanged yesterday – down $3.20 and up 1 cent respectively – to $1,085.00/oz and $14.60/oz.

Silver futures for September delivery fell less than 0.1 percent to $14.66 on the Comex.

Palladium for September delivery rose 0.8 percent to $602 an ounce on the New York Mercantile Exchange. Platinum for October delivery rose 0.3 percent to $955.90 an ounce.

Breaking News and Research Here

Follow GoldCore on Twitter, GoldCore on Facebook, GoldCore on LinkedIn

end

(courtesy Moneymetals.com/GATA)

Surging demand for the real stuff even as paper gold prices fall

10:07a ET Wednesday, August 5, 2015

Dear Friend of GATA and Gold:

Another monetary metals dealer, Money Metals Exchange in Idaho, reports surging demand for the real stuff even as prices for “paper gold” fall, “more buying interest than at any time since the 2008 financial crisis.” The firm reports its recent sales data here:

https://www.moneymetals.com/news/2015/08/05/gold-silver-demand-000746

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CXPowell@yahoo.com

end

I brought this to your attention yesterday, but it is worth repeating due to its importance:

(courtesy James Turk/Greg Hunter/GATA)

Unprecedented backwardation in gold, Turk tells USAWatchdog

4:40p ET Wednesday, August 5, 2015

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk today tells USAWatchdog’s Greg Hunter that he has never seen such a long period of backwardation in the gold market. Turk says that “the money bubble” is getting ready to pop. His interview is 26 minutes long and can be watched at USAWatchdog here:

http://usawatchdog.com/prolonged-gold-backwardation-has-never-happened-i…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

the following commentary from Dave Kranzler is extremely important.

The number of shorts in the GLD has now risen from 9 million shares to over 14 million shares. This is how the criminals are obtaining some gold by borrowing shares and then redeeming them for metal. Gold is in severe backwardation in the physical gold market in London. Although we do not get the GOFO rates, Kitco publishes the gold lease rates. The higher the rate, the more gold is in tight supplies. The lease rates today are extremely high!!

(courtesy Dave Kranzler/IRD)

Massive Shortages In Gold And Silver Developing – GLD Looting Continues

Renowned gold expert James Turk says prolonged gold backwardation like we are seeing now, where the spot price is higher than the future price, has never happened before. Turk contends, “No, never, and I am a student of monetary history as well, and I have never seen it happen like this in monetary history. – James Turk on Greg Hunter’s USAWatchdog

The signs are everywhere. We are seeing extreme “backwardation” in gold on the LBMA. Backwardation occurs when the spot price is higher than the future price for LBMA forward contracts. It means that buyers of gold are willing to pay more for gold for immediate delivery than pay a lower price to receive delivery in the future (30-day, 60-day, etc). It means that physical gold buyers do not trust the ability of the market to delivery physical gold in the future.

It is an unmistakable sign of physical gold shortages.

Not surprisingly, the LBMA suspended reporting the gold forward rate which was the best indicator of physical gold shortages in London, but we can still get reports onphysical market conditions from London gold market participants, like James Turk.

To reinforce this information, Bill Murphy reported his latest conversation with his LBMA trader source in London (www.lemetropolecafe.com):

The essence of it is more confirmation that the BIG MONEY is buying down here at these price levels.More confirmation that silver is extremely difficult to buy in size. It takes two to four weeks for delivery. What is new is that buying gold in size is now becoming a thing … for our source says it now takes two weeks to buy in size.

Perhaps the most visible sign is the removal of gold from the GLD ETF. The only way gold is removed from the Trust is when an Approved Participant bank redeems 100k share block in exchange for delivery of bars from the Trust. – (source: John Titus of the “Best Evidence” Youtube channel, edits are mine) – click to enlarge:

Make no mistake about it, the bullion banks often can borrow GLD shares to scrape together 100k share lots in order to redeem gold. Or they can smash the gold price with paper and force weak holders of GLD to sell shares in the hands of the bullion banks. In the last two weeks the short interest in GLD has soared 49% from 9.4 million shares to 14 million. That represents roughly 46 tonnes.

The ongoing raid of GLD gold is perhaps the most direct evidence that the Central Banks and their bullion bank agents are struggling to find gold in which to deliver into Asia. But speaking of which, something interesting is occurring on the Shanghai gold exchange. In the last three days, 298 tonnes of gold have been delivered into the SGE. While everyone monitors the amount of gold withdrawn from the SGE, the amount of gold flowing in to the SGE is just as important. This is by far the most amount of gold that has been delivered into the SGE that I can recall.

I get my data from John Brimelow’s “Gold Jottings” report, which is invaluable for tracking the physical gold market outside of London. He had this to say about the stunning flow of gold into China over the last three days:

Delivery Volume was 90.444 tonnes (Wednesday 112.454 tonnes) and open interest surged 48.374 tonnes (11.26%) to 477.920 tonnes. Since last Friday Shanghai open interest has risen 18.68%. Something is happening in gold in China. What is not immediately apparent.

Finally, to further reinforce the evidence of physical market shortages, we can monitor the gold lease rates, published by Kitco everyday. I sourced this graph from Jesse’s Cafe Americain, who sourced it from Sharelynx – click to enlarge:

Gold lease rates spike up like this when there is heavy demand from bullion banks to borrow physical gold from Central Banks in order to sell the gold into the market or deliver gold that can’t be readily procured in adequate quantities in the spot market. It is one of the most visible signs that there is a shortage of physical gold on the market.

Gold lease rates spike up like this when there is heavy demand from bullion banks to borrow physical gold from Central Banks in order to sell the gold into the market or deliver gold that can’t be readily procured in adequate quantities in the spot market. It is one of the most visible signs that there is a shortage of physical gold on the market.

To be sure, the unprecedented degree manipulation of the gold price in the paper gold market reflects a serious desperation by the Central Banks and western Governments to cover up an enormous disaster fomenting beneath the heavily applied of veneer of “things are so good we need to raise interest rates in September” mantra. In fact, the specific reason to keep a lid on the price of is to enable the Central Banks to maintain a zero interest rate policy.

The truth is, the Fed can’t afford to raise interest rates and anyone with two brain cells to rub together and a willingness to look at the truth knows that the Fed is trapped – unless it wants to crash the system for some reason.

We note that physical off-take of gold is spiking higher, with Reuters reporting yesterday that the South Koreans are buying gold in record sums while the US Mint reports that sales of gold coins in July were nearly 5 times what they were a year ago. – John Brimelow, “Gold Jottings” report

end

Not only is demand for silver skyrocketing but the supply side of the equation is well down with all the 3 major countries reporting lower production of silver:

1, Mexico

2. Peru

3. Australia

it will not be long before silver is in backwardation in London.

a must read…

(courtesy Steve St Angelo/SRSRocco report)

In a stunning development, the world’s largest silver producing countries reported big declines in recent months. This was surprising because the top two producers, Mexico and Peru, stated positive growth in the first two months of the year. However, silver production from these two countries reversed this trend by declining in April and May.

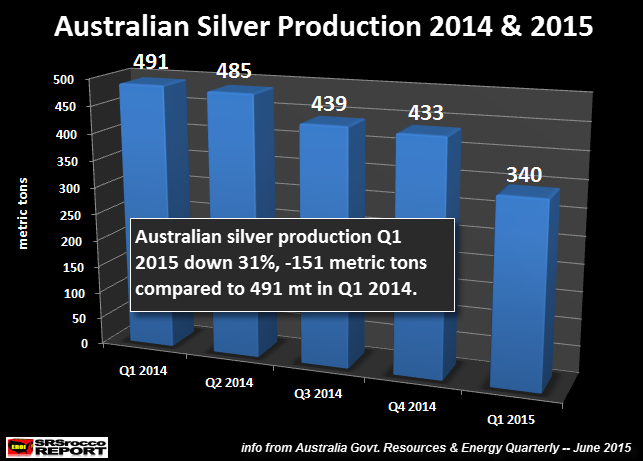

While this was a significant drop in silver mine supply from the leading producers, what took place in Australia (world’s fourth largest silver producer), was quite a shocker. Not only did Australian silver production fall precipitously, it was down a stunning 31% during the first quarter of 2015 compared to the same period last year:

As we can see, Australian silver production declined from 491 metric tons (mt) in Q1 2014, to 340 mt Q1 2015. This was a 151 mt decline (31%) year-over-year (y.o.y.). I tried to contact the Australian Government Department that provides the Resources & Energy Quarterly Reports on this figure, but did not receive a reply.

Often, the figures are revised. However, I have never seen silver production figures revised more than 5-8%. Furthermore, I went back to the site several times to see if there was a revision, or if the figure was a misprint… no change. Here is the table from their June 2015 Quarterly Report:

You will notice silver production started to decline in Q3 2014, but fell off a cliff in the first quarter of 2015. Queensland, Australia suffered the largest declines, falling from 381 mt in Q2 2014, to 246 mt in Q1 2014.

Again, I am reporting the data put out by the Australian Government. I will put out an update when their Q2 figures come out. If they still show the 340 mt (or figure close to it), this will not be good news.

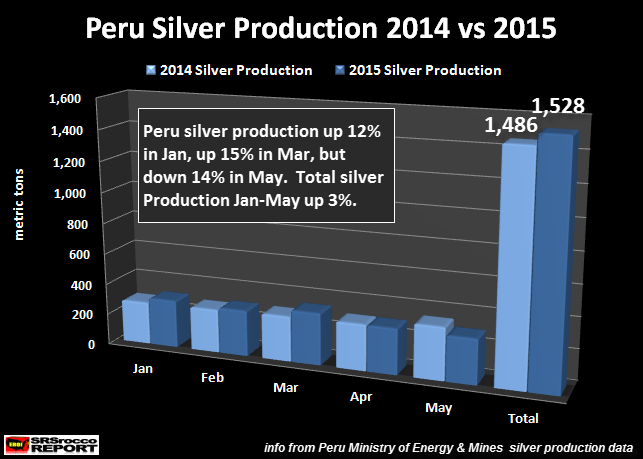

Okay, let’s look at Peru silver production. Peru is the second largest silver producer in the world. In the first three months of the year, Peru’s silver production was up a whopping 11%. However, production was flat y.o.y. in April, and really declined in May. Here is Peru’s silver production in the first five months of 2015:

Even though production was up 11% in the first quarter, when we factor in the large 14% decline in May, total production for the first five months was only up 42 mt or 3%. This same trend (to a lessor extent), was also experienced in Mexico… the world’s largest silver producer.

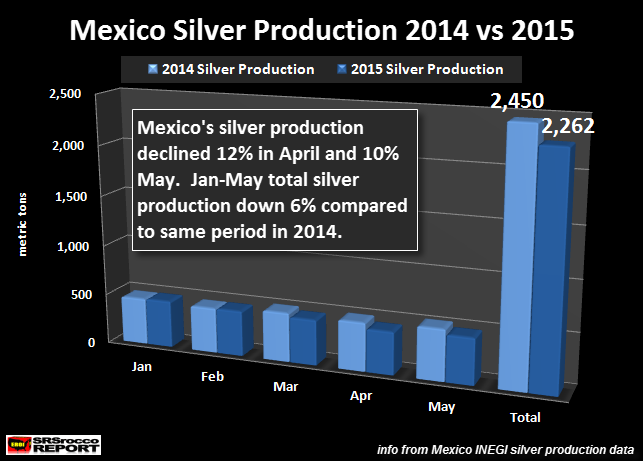

Mexico’s silver production was up slightly during the first two months of 2015, but this all changed starting in March. Silver mine supply from Mexico dropped 7% in March compared to the same month last year, a stunning 12% in April, and another 10% in May:

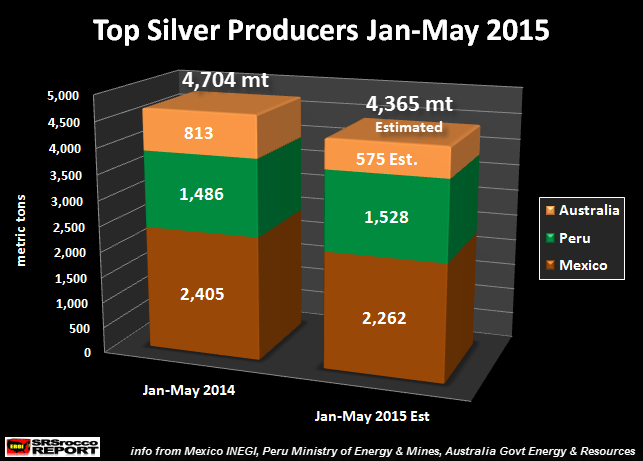

Which means, Mexico’s silver production is down 188 mt (6%) in the first five months of 2015, compared to the same period last year. If we combine the figures for Mexico, Peru and Australia, this is the total decline of silver production in the first five months of the year:

Total estimated silver production from these top producers in the world would be down from 4,704 mt (Jan-May) 2014, to 4,365 mt in 2015. Again, I say estimated because I don’t have Q2 data for Australia. I assumed a small build in production in the second quarter and estimated Australia’s silver production for the first five months of 2015.

If my assumption for Australia’s Q2 silver production is correct (or close), then total silver mine supply from these top producers will be down 339 mt (7%) compared to the same period last year. This is a lot of silver…. nearly 11 million oz.

Falling silver mine supply from the world’s leader producers (China is ranked 3rd, no public data released) comes at a time when silver investment demand has gone into HIGH GEAR. How high? Well, we know the U.S. Mint sold more Silver Eagles than ever in the first half of the year. Furthermore, July’s Silver Eagle sales which reached 5,529,000 were even higher than June (4,840,000).

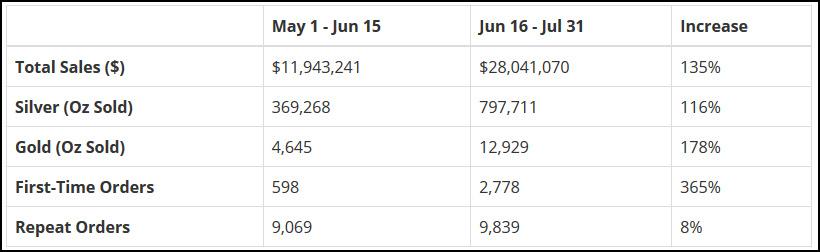

Then we had this news release by the folks at Money Metals Exchange on the huge increase in precious metal purchases, especially from first-time buyers, Retail Gold & Silver Demand Surged 135% since June, 365% More First-Timers:

From June 16 to July 31, Money Metals Exchange experienced a 135% surge in gold and silver sales over the prior 45-day period (which was representative of the early months of 2015). Since June 16, the number of first-time customers rose even more dramatically, with 365% more new purchasers than the prior period.

Not only did their total precious metals sales double from June 16-July 31, First-Time orders increased 365%. I would imagine this was similar through-out the precious metals retail industry.

Precious metals investors need to realize there are very few real STORES OF WEALTH to own in the future. These stores of wealth are based on stores of ECONOMIC ENERGY. The world is about to witness a huge collapse in the Great U.S. Shale Oil Industry. Watch for fireworks to start in Q3 and pick up speed in Q4 when the shale oil companies will have to revalue their reserves due to much lower oil prices.

This should start to speed up the peak and decline of lousy global unconventional oil production. Falling oil production will be DEATH on most PHYSICAL & PAPER ASSETS. This is the most important reason to own gold and silver. More on this in future articles and reports.

end

(courtesy Avery Goodman/seeking Alpha/GATA)

Avery Goodman: U.S. guarantees Comex gold, hastening offtake there

Demand for Physical Gold Deliveries Doubles in August

By Avery Goodman

Tuesday, August 4, 2015

Last month I wrote about an usual situation at the COMEX futures exchange:

http://seekingalpha.com/article/3227026-gold-market-tightness-puts-comex…

At that time, only 376,000 ounces of gold were available to back up a delivery requirement of about 550,000 ounces. A day later, JPMorgan Chase bailed out the clearing firms that handle short-side speculators, adding enough registered gold to meet deliveries.

In the article, I reached several conclusions. First, given that commercial for-profit institutions don’t normally put themselves at financial risk to bail out their competitors, it was likely that JPMorgan was an agent of the U.S. government. I also concluded that the Comex is an excellent place for large physical gold buyers to source gold. …

… For the full commentary:

http://seekingalpha.com/article/3396845-demand-for-comex-physical-gold-d…

end

And now your overnight Thursday morning trading in bourses, currencies, and interest rates from Europe and Asia:

1 Chinese yuan vs USA dollar/yuan remains constant at 6.2096/Shanghai bourse: red and Hang Sang: red

2 Nikkei up 50.38 or 0.24%

3. Europe stocks mixed /USA dollar index up to 97.98/Euro down to 1.0900

3b Japan 10 year bond yield: rises to 42% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 124.84

3c Nikkei still just above 20,000

3d USA/Yen rate now just above the 124 barrier this morning

3e WTI 44.73 and Brent: 49.45

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund slightly rises to .75 per cent. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate rises to 20.65%/Greek stocks this morning up by 3.34%: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield rises to : 11.98%

3k Gold at $1086.45 /silver $14.60

3l USA vs Russian rouble; (Russian rouble down 1.05 in roubles/dollar) 64.03,

3m oil into the 44 dollar handle for WTI and 49 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9829 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0713 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving further from negativity to +.75%

3s The ELA rose another 900 million euros to 90.4 billion euros. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.25% early this morning. Thirty year rate below 3% at 2.94% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Flat, China Slides Again, Oil Tumbles Near 2015 Lows

It has been more of the same in the latest quiet overnight session where many await tomorrow’s NFP data for much needed guidance, and where Chinese markets opened weaker, rose during the day, then went through a mini rollercoaster, then sold off in the afternoon. The Shanghai Composite and HS China Enterprises indices finished down .9% and .3%, respectively. Trading volume continued to be very subdued, running at half the thirty day average assome 20 million “investors” have pulled out of the market to be replaced with HFTs such as Virtu.

Despite what some have estimate is as much as a trillion in Chinese “plunge protection” allocation, the Shanghai Composite is now near the lows hit on July 8 when China openly threatened sellers and shorters with arrest. If that low is taken out, China will have a big headache on its hands.

Other Asian equities traded mixed following the positive close on Wall Street where sentiment was supported by strong US data and comments by Fed’s Powell which contradicted recent hawkish remarks from Fed’s Lockhart. Nikkei 225 (+0.2%) was bolstered by a slew of strong earnings, while gains where further underpinned by JPY weakening to a 2-month low against the greenback. The ASX 200 (-1.1%) was led lower by broad losses in large banks. Finally, JGBs fell following the EU and US counterpart, with losses exacerbated by a weak enhanced liquidity auction drawing the lowest b/c on record.

European shares are lower, for the moment halting a rally that has been on-going since July 28. The Stoxx 600 index is up about 18% YTD. There has been no discernable difference between core and peripheral performance. Despite the looming risk events, including the release of the latest NFP report on Friday and the eagerly awaited “Super Thursday” in the UK today, stocks traded mixed (Euro Stoxx: -0.1 %), with Greece’s stock market rebounding after three days of heavy losses. The FTSE-100 index underperformed (-0.3%), weighed on by BP (-3%) and Anglo American (-3%), with both trading ex-dividend. Overall, energy names underperformed, as WTI prices remained under-pressure, while the upside support was provided by industrials and financials sectors.

The release of the much better than expected German Factory Orders data, together with somewhat mixed retail PMIs did little to drive the price action across asset classes , with Bunds and Gilts trading little changed. At the same time, the expected volatility in GBP/USD later on in the session failed to weigh on the pair, which traded with little changed after giving back some of it overnight gains following mixed UK data (Industrial Production M/M -0.4% vs. Exp. 0.10%, Manufacturing Production M/M 0.20% vs. Exp. 0.10%). While the USD (USD-index: +0.1%) heading into the North American crossover flat on the day.

Elsewhere, AUD was in focus overnight following a mixed Australian jobs reports, where AUD initially surged higher amid a significant beat in employment change (M/M 38.5K vs. Exp. 10.0K Prey. 7.3K, Rev. 7.0K ). However, AUD/USD fell below preannouncement levels as the unemployment rate rose to a 7-month high (M/M 6.3% vs. Exp. 6.1% Prey. 6.0%, Rev. 6.1%).

But while stock action has been muted, the story of the night so far is oil and the energy complex broke out of a tight overnight range early in the European session to continue yesterday’s downward trend, seeing WTI Sep’15 futures fall below the USD 45.00 handle after yesterday’s DoE crude oil inventories saw US crude output rise by 0.552%.

As of this moment oil was trading at $44.72, just pennies above the low print of 2015.

Perhaps the catalyst for the latest weakness was another report out of Goldman’s Jeff Currie in which he says the “lost decade reinforces lower for longer.” Some more details:

Although spot oil prices have only retraced to the lows of this winter, forward oil prices, commodity currencies and energy equities/credit (relative to the broad indices) have now all retraced to levels not seen since 2005, erasing a decade of gains. This creates a very different economic environment as the search for a new equilibrium resumes: financial stress is higher, operational stress as defined below is more extreme and costs have declined further due to more productivity gains, a substantially stronger dollar and sharp declines in other commodity prices. These differences reflect not only a further deterioration in fundamentals, but also the financial markets’ decreasing confidence in a quick rebound in prices and a recognition that the rebalancing of supply and demand will likely prove to be far more difficult than what was previously priced into the market. This is all in line with our lower-for-longer view. While we maintain our near-term WTI target of $45/bbl, we want to emphasize that the risks remain substantially skewed to the downside, particularly as we enter the shoulder months this autumn.

Elsewhere, metals have traded relatively range bound overnight with gold flat, remaining near yesterday lows after strong US data pressured prices, while investors are looking ahead to the key risk event in the form of US jobs data on Friday to give more clues as to the timing of a Fed rate hike.

Moving onto today’s calendar now. This morning all eyes turn to the UK and the BoE where we’ll have a lot of information to get through with the BoE rate decision, meeting minutes and the Inflation Report, while the BoE Carney is also scheduled to speak in what’s being billed as ‘Super Thursday’. June readings for industrial and manufacturing production are also expected for the UK. We also get more employment data in the US with initial jobless claims and Challenger job cuts data. This will be the last chance for economists to fine tune their payroll forecasts for tomorrow’s important number.

In Summary: European shares fall with the oil & gas and basic resources sectors underperforming and retail, insurance outperforming. oil little changed. German factory orders above expectations, U.K. industrial output below. U.K., Denmark, Norwegian bourses underperform in Europe; Greece, Finland outperform. Yields fall on eurozone 10-yr bonds with Spanish, Portuguese yields down most. U.S. jobless claims, continuing claims, Bloomberg consumer comfort, Challenger job cuts due later.

Market Wrap

- S&P 500 futures little changed at 2094.5

- Stoxx 600 down 0.4% to 402.4

- US 10Yr yield down 1bps to 2.26%

- German 10Yr yield down 2bps to 0.73%

- MSCI Asia Pacific down 0.3% to 140.7

- Gold spot up 0% to $1085.4/oz

- Eurostoxx 50 -0.2%, FTSE 100 -0.3%, CAC 40 -0.2%, DAX +0%, IBEX +0.1%, FTSEMIB -0.3%, SMI -0.2%

- CF Industries, OCI Said Near Agreement for Fertilizer Merger

- Bill Ackman Amasses $5.6b Stake in Oreo Maker Mondelez

- Jeff Bezos Sells More Than $500m in Amazon Shares

- Euro down 0.17% to $1.0887

- Dollar Index up 0.04% to 98

- Italian 10Yr yield down 4bps to 1.87%

- Spanish 10Yr yield down 5bps to 2.02%

- French 10Yr yield down 2bps to 1.04%

- S&P GSCI Index down 0.2% to 368.4

- Brent Futures down 0% to $49.6/bbl, WTI Futures down 0.5% to $44.9/bbl

- LME 3m Copper up 0.5% to $5201.5/MT

- LME 3m Nickel up 0.4% to $10905/MT

- Wheat futures flat at 502 USd/bu

Bulletin Headline Summary from RanSquawk and Bloomberg

- The release of the much better than expected German Factory Orders data, together with somewhat mixed retail PMIs did little to drive the price action across asset classes as market participants await the BoE’s ‘Super Thursday release

- See a preview of today’s ‘Super Thursday’ release here (http://portal.ransquawk.com/headlines/501389)

- Going forward, apart from focusing on the releases from the BoE, other data releases include US Challenger Job Cuts, US weekly jobs reports, EIA natural gas storage change data, as well as earnings by Duke Energy and Allergan

- Treasury yields little changed ahead of today’s job cuts/jobless claims data; 2Y yield touched three-year high yday after July ISM Non-Manufacturing Composite reached highest level in nearly a decade.

- Along with its August interest-rate decision, BOE will also release officials’ votes and new forecasts, the realization of Carney’s push to revamp communications by releasing all elements of the Monetary Policy Committee’s decisions at once

- The pound strengthened for a fourth day versus the euro as investors braced for an unprecedented slew of data from the BoE that may lend clarity on the timing of its first interest-rate increase in eight years

- Unconventional monetary policy is now conventional as asset purchases introduced during the financial crisis and beefed up in the subsequent fight against recession now represent a permanent part of officials’ toolkit

- ECB officials must be patient for quantitative easing to work its way through the economy and drive a pickup in inflation, Governing Council member Bostjan Jazbec said

- China Securities Finance Corp., the government agency mandated to buy stocks to stem a market rout, is seeking access to an additional 2 trillion yuan ($322 billion), said people with knowledge of the matter

- While Greece’s Alexis Tsipras finds himself running a country in a state of economic emergency, his popularity remains unchallenged as polls show Syriza has as much as twice the support of its nearest rival

- Almost a month after Saudi Arabia sold $4 billion of bonds to domestic banks the world still knows next to nothing about the securities as details of the issuance, including the price, the maturity and even the date of the sale remain elusive

- $4.4b IG deals priced yesterday, $2.01b high yield. BofAMLCorporate Master Index OAS holds at new YTD wide 158; YTD low 129. High Yield Master II OAS -12 to 529; reached YTD wide 549 last week; YTD low 438

- Sovereign 10Y bond yields mixed. Asian, European stocks mostly lower, U.S. equity-index futures mixed. Crude oil lower; copper and gold rise

DB’s Jim Reid concludes the overnight recap

Bond market appetite has also shrunk over the last 36 hours after Lockhart’s interview on Tuesday night concerning a possible September hike, and after yesterday’s highest US non-manufacturing ISM since August 2005 (60.3 vs. 56.2 expected). This overshadowed what was a softish ADP report (185k vs. 215k expected). Had it not been for the ISM we wonder whether there would have been intense debate as to whether the ADP represented ‘some’ improvements in the jobs data or not. We won’t have to wait too long for the main event though as US payrolls comes tomorrow.

The data sparked a fairly choppy session for the Treasury market yesterday. The benchmark 10y eventually closed up 4.9bps higher in yield at the close to 2.271% although that was after yields dipped as low as 2.212% in the moments shortly following the ADP print, only to then march higher post ISM. 2y Treasury yields actually touched an intraday high in yield of 0.756%, the highest since 2011 before closing more or less unchanged at 0.726%. Looking across the Fed Funds contracts, the Dec15 contract was unmoved at 0.330% while the Dec16 (+1.5bps) and Dec17 (+4.0bps) contracts rose slightly to 1.045% and 1.675%. The probability of a September move meanwhile, based on market pricing, has remained steady at 50%. In the FX space the closing level for the Dollar index (+0.05%) masked what was a fairly volatile day as the Greenback ebbed and flowed with the various data, trading in a 60bps range.

Meanwhile in the equity space the S&P 500 (+0.31%), although weakening as the day went on, managed to halt three consecutive days of losses with the tech sector in particular leading the way (supported by a first rise in six days for Apple). That saw the NASDAQ (+0.67%) outperform although the Dow (-0.06%) failed to hold earlier gains, led lower by a disappointing earnings report from Walt Disney. In the commodity space Oil again took another leg lower with WTI (-1.29%) and Brent (-0.80%) both down with the latter at one stage creeping closer to $49 as the market digested the latest US inventory data. Other commodity markets followed suit with Gold (-0.25%), Aluminum (-1.36%) and Copper (-1.09%) all closing down.

Looking at how markets have followed up this morning, with the exception of the Nikkei (+0.78%) it’s been a fairly soft start across most of Asia this morning. In China the Shanghai Comp (-0.33%) and Shenzhen (-0.29%) are lower as we go to print, although both have bounced back from an initial 2% drop at the open. Elsewhere the ASX (-0.98%), Hang Seng (-0.52%) and Kospi (-0.60%) have also declined, the former coming after a weaker than expected unemployment rate print out of Australia (6.3% vs. 6.1% expected). Treasury yields have pared back some of yesterdays move higher, with 10y yields -1.1bps at 2.259%. Bond markets in the rest of Asia are largely mixed. Credit markets in Asia and Australia are largely unchanged.

Digging deeper into yesterday’s data in the US, there were some notable improvements in the components of yesterdays non-manufacturing ISM print. Of particular interest was the new orders measure which rose to 63.8 (from 58.3) and also at a decade high, business activity which moved to 64.9 (from 61.5) and the highest since 2004 while the employment component, in stark contrast to the softish ADP print, moved 6.9pts higher to 59.6 – the biggest one-month increase in the 18-year history of the report. Elsewhere, the separate final services PMI reading was revised up 0.5pts to 55.7, helping to push the composite print up (+0.5pts to 55.7) for the month. Meanwhile the trade deficit for June widened $2.9bn to $43.8bn during the month and slightly above market ($43bn expected). Following on from Lockhart’s comments on Tuesday, Fed Governor Powell said that the ‘time is coming’ to raise rates but that he has not yet decided on a timeframe and instead is ‘going to be very, very focused on the data’.

It wasn’t just the Treasury market where we saw yields move higher yesterday. Over in Europe, supported by both the US data and European PMI numbers as well as a delayed reaction to Lockhart’s comments the previous evening, yields surged higher with 10y Bund yields closing up 11.5bps at 0.752%. Similar maturity yields in France (+10.4bps) and Netherlands (+11.3bps) also rose while in the periphery we saw Italy, Spain and Portugal yields move +14.3bps, +13.0bps and +11.5bps higher respectively. Equity markets were well supported meanwhile with the Stoxx 600 closing +1.30% and the DAX (+1.57%) and CAC (+1.65%) also having stronger sessions.

Looking at the data-flow in the region, DB’s Peter Sidorov suggested that the final July PMIs confirmed the broadly stable data tone that we have seen recently for the Euro area. The composite Euro area PMI was revised up 0.2pts at the final revision to 53.9 (down slightly from the 54.2 in June) on the back of a 0.2pt upward revision to the services reading to 54.0. Spain was the main surprise in the services reading (+3.5pts to 59.7) while Germany and France saw little change on their initial flash reading. Italy’s services print (-1pt to 52.0) was the notable downward revision. Peter notes that the message for inflation is improving with the latest PMI numbers, with the output price index reaching its highest level since March 2012. In the UK meanwhile we saw the services print revised down 0.6pts to 57.4, a drop of nearly a point from June. Elsewhere we saw a softer than expected Euro area retail sales reading for June (-0.6% mom vs. -0.2% expected).

Staying in Europe, yesterday we got the latest polls data out of Spain which showed a boost for Spanish PM Rajoy’s ruling People’s Party and declining support for the radical Podemos party. The poll, run by CIS, showed support for the People’s Party at 28.2%, up nearly 3% from the last poll in April and ahead of the opposition Socialists on 24.9%. On the other side, Podemos support fell to 15.7%, a fall of nearly a point from April and nearly 8 points from the January peak. The political situation in Spain is clearly still far from certain with still a reasonable degree of fragmentation, but the latest polls will likely be seen as encouraging in the sense of declining support for the more radical Podemos party in light of recent events in Greece.

Before we take a look at the day ahead, refreshing our earnings beats/miss monitor again and with 426 S&P 500 companies now having reported, there was no change yesterday to our earnings (74%) and sales (49%) beats numbers. In Europe there was no change either at 64% and 66% respectively.

Moving onto today’s calendar now. German factory orders data for June will kick proceedings off this morning before all eyes turn to the UK and the BoE where we’ll have a lot of information to get through with the BoE rate decision, meeting minutes and the Inflation Report, while the BoE Carney is also scheduled to speak in what’s being billed as ‘Super Thursday’. June readings for industrial and manufacturing production are also expected for the UK. We also get more employment data in the US this afternoon with initial jobless claims and Challenger job cuts data. This will be the last chance for economists to fine tune their payroll forecasts for tomorrow’s important number.

Chinese Stocks Tumble Despite Margin Debt Rises As Virtu Is Unleashed To Provide “Liquidity” After Citadel Ban

No lesser liquidity-providing high-frequency-trading never-a-losing-trade shop than Virtu financial has been ‘allowed’ to trade Chinese capital markets. Coming just days after Citadel’s ban, one can only assume that Chinese regulators made a deal with the devil CEO Doug Cifu to levitate markets at any and every cost in order to pick up pennies in front of de-leveraging, over-margined army of farmers and grandmas now seeking exits. Sure enough for the second day in a row margin debt is on the rise again. The retail-dominated Chinese stock market will be ripe picking for the HFTs, as long as not to many are allowed and a tail-chasing flash-crash ensues… but for now its appears yesterday afternoon’s selling pressure continues with CSI-300 down almost 2% at the open.

Each bounce yesterday saw immediate selling pressure..

All that matters for now is keeping Shanghai Composite above the 200-day moving average…

So today’s key level will be what happens when SHCOMP hits 3574?

And it appears the 200DMA will be tested again…

- *CHINA’S CSI 300 INDEX SET TO OPEN DOWN 1.7% TO 3,802.93

- *CHINA SHANGHAI COMPOSITE SET TO OPEN DOWN 1.9% TO 3,625.50

As Bloomberg reports, Virtu Financial Inc., one of the world’s biggest high-speed trading firms, has started trading in its 35th country: China.

The company reached an agreement during the second quarter with a Chinese brokerage house to provide liquidity on “a very limited basis,” according to Virtu Chief Executive Officer Doug Cifu. Virtu is using automated market-making strategies to buy and sell commodities listed in mainland China. In other markets, it trades other assets including stocks and currencies.

“This agreement is the first step in what we view as a very long process,” Cifu said in a conference call on Wednesday. He did not identify the firm’s Chinese partner.

…

Mainland exchanges have frozen 38 accounts, including one owned by Citadel Securities, as the local authorities investigate algorithmic traders.

“We are certainly cognizant of the recent market volatility in China, and the regulatory scrutiny being placed on electronic trading by the local regulator,”Cifu said. “Long term, we view China as an established capital market with volumes comparable to the largest markets in which we operate.”

Virtu will confine its presence to Chinese data centers. It won’t be opening offices or “putting boots on the ground,” he said.

What does it take for famers to learn?

- *SHANGHAI EXCHANGE MARGIN DEBT RISES FOR SECOND DAY

Another crash it would appear...

* * *

Having tried (and failed) with everything so far, it seems China is willing to unleash HFT hell on their retail citizens… we suspect Virtu’s agreement will be torn up if stocks drop any more..

end

This is not good. Bad debt soars almost 35% in China. How on earth will China continue to hide this?

(courtesy zero hedge)

Bad Debt Soars 35% In China As Government Set To Fabricate Dismal Loan Data

Back in March, we noted that decelerating economic growth and bad debt are taking a toll on profitability at China’s largest banks, leading them to slash payouts to shareholders.

“Particularly hard hit is ABC, which saw its non-performing loans jump 25bps Q/Q,” we observed, adding that “NPLs for loans made to manufacturers more than doubled that number, rising 54bps sequentially.” That figure underscores the degree to which China’s transition from an investment-led, smokestack economy to a model driven by consumption and services is weighing heavily on industry and in turn, on banks that lend to the manufacturing sector.

Although NPLs have been rising for some time in China, determining the true extent of the problem is largely impossible due to Beijing’s “management” of bad loans. As we outlined in “How China’s Banks Hide Trillions In Credit Risk,” there’s no way to know how pervasive Beijing’s practice of forcing banks to roll-over problem loans truly is, meaning that even if we ignore the fact that quite a bit of credit risk is obscured by the practice of shifting it around, moving it off balance sheet, and reclassifying it, (i.e. if we just look at traditional loans) it’s still difficult to know what percentage of loans are actually impaired because it’s entirely possible that a non-trivial percentage of sour debt is forcibly restructured and thus never makes it into the official NPL figures.

Indeed, the fact that NPLs are remarkably similar across banks suggests the numbers are, much like China’s GDP data, “smoothed out.” That said, a look at “special mention” loans and overdue loans can help to paint a more accurate picture although the figures still look grossly understated.

Source: Fitch

On Thursday, we got still more evidence that the NPL situation is deteriorating rapidly in China when Reuters reported that according to a transcript of an internal meeting of the China Banking Regulatory Commission,bad loans jumped CNY322.2 billion in H1 to CNY1.8 trillion, a 36% increase. The NPL ratio was 1.82 as of June 30, up 22 bps on the year. Here’s more:

Shang Fulin, chairman of China Banking Regulatory Commission (CBRC), told an internal meeting last week that non-performing loans (NPLs) at banks rose 322.2 billion yuan in the first six months of the year to 1.8 trillion yuan ($289.9 billion), according to a transcript of the meeting seen by Reuters.

He also said the banks’ profit growth in the first-half slowed by 13.03 percentage points from a year ago, with total net profits amounting to 1.1 trillion yuan in the first six months.

“In the bigger context of (China’s) economic slowdown, the whole truth of the banking sector’s credit risks is beginning to emerge,” Shang said, according to the transcript.

Lower profit growth will “reduce shareholder return, weaken banks’ capability to supplement capital and prevent risks,” he added, saying it was now the “new normal.”

Of course this “new normal” isn’t going to please the Politburo which is why we suspect efforts to manage the data will now kick into high gear and indeed, it looks as though the PBoC has already figured out a way to mask anemic demand for credit.

According to MNI, the central bank will begin including interbank loans to non-banking institutions in its calculations, a practice which could mean the headline figure will be “three times” what it would have been were it calculated using the old methodology.

The PBoC, MNI continues, will include loans made to CSF, China’s plunge protection vehicle, in the figures, meaning Beijing will pretend that the state-directed effort to artificially shore up the country’s stock market represents real, organic demand for credit.

As for the real situation, one loan officer at a Big Four bank told MNI that “our bank’s loans in July in the Beijing area were even weaker than in June. We can’t find the demand.”

But that’s ok because in the absence of government intervention, Chinese stocks “can’t find” a bid, which is why, as Bloomberg reported earlier today, CSF “seeks access to as much as CNY5 trillion to support the stock market if needed.”

The government has already lined up nearly CNY3 trillion for the vehicle, so where will the other CNY5 trillion come from you ask? Why, from the banks of course. Here’s Bloomberg again: “CSF is currently seeking funding from banks for periods ranging between 3 and 12 mos at rate of as much as 4.4%.”

So there you have it, another CNY2 trillion in loan “demand” created out of thin air.

The only question now is what happens when the PBoC loses complete control of the market again and the loans to CSF themselves go bad.

There will be no IMF decision on a Greek bailout until the fall. Remember that the IMF wants a haircut on Greek debt, something that Germany does not want to give.

end

It seems that the IMF will wait until the fall to give its decision if it wishes to help with the Greek bailout:

(courtesy Reuters)

No IMF decision on Greek bailout until autumn, Swedish representative tells paper

There is strong support at the IMF for joining a new bailout package for Greece but the fund will not decide whether to participate until autumn, Sweden’s representative to its executive board told a newspaper.

The International Monetary Fund has been part of Greece’s first two financial rescues, but doubts have been raised about its commitment to a third package.

The European Commission said on Friday the Fund was participating fully in bailout talks between Greece and its international lenders that started in the last week of July.

A day earlier the Financial Times, citing a summary of an IMF board meeting, said the Fund could not officially join the talks until after Greece agreed comprehensive reforms.

Thomas Ostros, who is an alternate – or replacement – director on the fund’s 24-member board, said there was “strong (IMF) support for being part of a new loan program, but it will take time,” according to an interview in Thursday’s edition of Swedish daily Dagens Nyheter.

“There is going to be a discussion during the summer and autumn and then the board will make a decision during the autumn,” he said.

Athens is seeking up to 86 billion euros ($94.5 billion) in aid in what would be its third bailout since 2010.

Ostros, a former government minister, said there was a risk a new package would simply delay the day of reckoning unless Greece adopted painful reforms.

“It can not be something that is forced on them. Greece must own the problem. The Greek government is not there yet,” he said.

“…They have an inefficient public sector, corruption is a relatively big problem and the pension system is more expensive than other countries.”

(Reporting by Simon Johnson, editing by John Stonestreet)

end

I guess this was to expected!!!

(courtesy zero hedge)

Iran Refuses UN Inspector Access To Scientists, Caught Trying To “Clean Up” Suspected Nuclear Site

Surprise! In what must be the most predictable geopolitical event in recent days, WSJ reports that Iran has refused to let United Nations inspectors interview key scientists and military officers to investigate allegations Tehran maintained a covert nuclear-weapons program. This comes hours after CNN reported that the intelligence community believes Iran has been attempting to clean up the suspected nuclear site at Parchin prior to the arrival of international inspectors based on new satellite imagery. While the administration attempts to ‘clear up’ any misunderstandings, Senate Foreign Relations Committee Chairman Bob Corker told reporters. “It was not a reassuring meeting…I would say most members left with greater concerns about the inspection regime than we came in with.”

For now, the landmark nuclear agreement forged between world powers and Iran on July 14 in Vienna is on hold. AsThe Wall Street Journal reports,Iran’s stance complicates the International Atomic Energy Agency’s investigation into Tehran’s suspected nuclear-military program—a study that is scheduled to be finished by mid-October, as required by the treaty.

The IAEA and its director-general, Yukiya Amano, have been trying for more than five years to debrief Mohsen Fakhrizadeh-Mahabadi, an Iranian military officer the U.S., Israel and IAEA suspect oversaw weaponization work in Tehran until at least 2003.

Mr. Amano said Tehran still hasn’t agreed to let Mr. Fakhrizadeh or other Iranian military officers and nuclear scientists help the IAEA complete its investigation. The Japanese diplomat indicated that he believed his agency could complete its probe even without access to top-level Iranian personnel.

Tehran has repeatedly denied it ever had a secret nuclear weapons program.

But Mr. Amano said in a 25-minute interview in Washington that Iran still hasn’t agreed to provide access to Mr. Fakhrizadeh or other top Iranian military officers and nuclear scientists to assist the IAEA in completing its probe.

“We don’t know yet,” Mr. Amano said about the agency’s interview requests. “If someone who has a different name to Fakhrizadeh can clarify our issues, that is fine with us.

But, as CNN reports, the intelligence community believes Iran has been attempting to clean up the suspected nuclear site at Parchin prior to the arrival of international inspectors based on new satellite imagery, a senior intelligence official told CNN on Wednesday.

The commercial imagery shows that Iran has moved heavy construction equipment to the area. But the senior intelligence official, who is familiar with the imagery in question, said the U.S. is confident that such sanitization efforts cannot succeed because radioactive materials, if present, are extremely difficult to conceal.

“The (International Atomic Energy Agency) isfamiliar with sanitization efforts and the international community has confidence in the IAEA’s technical expertise,” the official said.

Sen. Chris Coons, D-Delaware, told reporters on Tuesday that he has “concerns about the vigorous efforts by Iran to sanitize Parchin.”

A furious lobbying effort by both supporters and foes of the Iran nuclear deal continues in the Senate ahead of a mid-September vote on the agreement.On Wednesday, Senate Majority Leader Mitch McConnell said the Iran debate will begin on the Senate floor on Sept. 8 after the August recess is over.

Mr. Amano visited Capitol Hill on Wednesday in a bid to assure skeptical U.S. lawmakers the IAEA is capable of implementing a vast inspections regime of Iran’s nuclear facilities and clarifying the weaponization issue.

Senate Republicans and skeptical Democrats, however, left the 90-minute closed-door meeting frustrated that Mr. Amano refused to share the agency’s classified agreements on access to Iranian military sites, scientists and documents.

“I would say most members left with greater concerns about the inspection regime than we came in with,” Senate Foreign Relations Committee Chairman Bob Corker (R., Tenn.) told reporters. “It was not a reassuring meeting.”

* * *

Somewhere Benjamin Netanyahu is doing “the told you so” dance… as Kerry’s deal and Obama’s legacy hang by a thread.

3 Charts To Watch During Today’s More Dovish Than Expected BoE “Super Thursday”

Update: the release and Minutes are out, and it would appear that the BOE finally pulled up an oil chart, and as a result the report was far more dovish than consensus had expected”

From the announcement:

The Bank of England’s Monetary Policy Committee (MPC) sets monetary policy in order to meet the 2% inflation target and in a way that helps to sustain growth and employment. At its meeting ending on 5 August 2015, the MPC voted by a majority of 8-1 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of purchased assets financed by the issuance of central bank reserves at £375 billion, and so to reinvest the £16.9 billion of cash flows associated with the redemption of the September 2015 gilt held in the Asset Purchase Facility.

CPI inflation fell back to zero in June. As set out in the Governor’s open letter to the Chancellor, around three quarters of the deviation of inflation from the 2% target, or 1½ percentage points, reflects unusually low contributions from energy, food, and other imported goods prices. The remaining quarter of the deviation of inflation from target, or ½ a percentage point, reflects the past weakness of domestic cost growth, and unit labour costs in particular. The combined weakness in domestic costs and imported goods prices is evident in subdued core inflation, which on most measures is currently around 1%.

With some underutilised resources remaining in the economy and with inflation below the target, the Committee intends to set monetary policy in order to ensure that growth is sufficient to absorb the remaining economic slack so as to return inflation to the target within two years. Conditional upon Bank Rate following the gently rising path implied by market yields, the Committee judges that this is likely to be achieved.

In its latest economic projections, the Committee projects UK-weighted world demand to expand at a moderate pace. Growth in advanced economies is expected to be a touch faster, and growth in emerging economies a little slower, than in the past few years. The support to UK exports from steady global demand growth is expected to be counterbalanced, however, by the effect of the past appreciation of sterling. Risks to global growth are judged to be skewed moderately to the downside reflecting, for example, risks to activity in the euro area and China.

More importantly, the inflation report which was also released, and it was here where the dovish revisions were most acute:

The GBP is not happy, and promptly tumbled over 100 pips:

* * *

A preview of today’s BOE “Super Thursday” from RanSquawk and Forex.com

Today the Bank of England releases its rate decision, minutes and quarterly inflation report (QIR) all at 1200BST with the QIR press conference to be held by Governor Carney at 1245BST. Given the volume of information on offer, the release is likely to be met with volatility.

Background

The rate decision is expected to see the BoE keep policy on hold , however the minutes could prove to be more interesting.

Consensus suggest this month’s minutes could see a 7-2 vote (currently 9-0) with some analysts even suggesting a 6-3 vote after July’s meeting saw ‘a few’ members suggest a ‘fine balance’ between voting for a rate hike or not. The two most touted members to vote for a rate hike are McCafferty and Weale. Other names include Miles, who is leaving the committee after this month and has recently forecast inflation rising to the 2% target towards the end of this year, and Forbes who has previously been considered the most likely member to join McCafferty and Weale. It should be noted however that if BoE’s Miles were to vote for a rate hike, it would be less consequential than other members as he is being replaced in September by Gertjan Vlieghe, who analysts at Barclays and Citi both forecast will have a more dovish leaning.

The BoE’s QIR could also prove of interest to many participants, with the report potentially shedding more light on the bank’s outlook for inflation and growth. The previous report said CPI is on track to return to the 2% target in 2 years despite cutting the 2016 CPI forecast to 1.6% citing downside risk to near term inflation. More specifically, the BoE said inflation is likely to be below as above 2.0% in Q2 2017, therefore any shift in the distribution of inflation expectations around 2% will be key.

Since this report, inflation has failed to show any marked pick-up (currently stands at 0.0% Y/Y). However, the central bank themselves have been more upbeat for the inflation outlook (as per above comments from Miles). That said, analysts suggest that although it is hard to pinpoint an exact forecast, there is downside risk to near-term inflation outlook given the appreciation of GBP and continued decline in oil prices. Nonetheless, analysts at Goldman Sachs suggest that the 2yr outlook for inflation could be lifted and if so then participants could be presented with a steeper curve.

From a growth perspective, the latest GDP reading saw Q2 print at 0.7% Q/Q which has subsequently led to a more optimistic outlook for UK growth (also allied with a dissipation of fears surrounding Greece) and as such there could be a potential shift in expectations on this metric despite having been cut in the previous report for 2015 and 2016. Some commentators add that the latest figures could lead policy-makers to shrug off the disappointing Q1 reading of 0.4% and thus could provide one of the more hawkish elements of the release.

In terms of other metrics, hawkish tones could also be provided by any further mentions on slack which was seen as shrinking in the previous minutes release . With regards to wage growth, this may take somewhat of a back-seat this time round given that economists’ view that little has changed on this front since the previous report in May.

Market Reaction

With so much to digest from the BOE later today, we need to find easy ways to try and break if down to see what impact the combined release of the BoE interest rate decision, minutes and Inflation Report could have on the markets.

Rather than try to track everything, we will be looking at 3 assets to determine the impact of Super Tuesday.

1, The Sonia rate

The Sonia rate is useful to look at today to get a sense of the market’s expectations of UK interest rates in 3 months’ time. If this is considered hawkish then Sonia rates should rise and the market may start to price in a potential rate hike before the end of this year, helping the UK to play catch up with US rate expectations.

Chart 1:

Source: City Index and Bloomberg

2, GBPUSD

Can a hawkish Carney take us out of this range? We hope so, since GBPUSD has been as dull as dishwater recently. If the BoE talks tough on wage pressures and the need to get started on normalising interest rates then we think this could push GBPUSD outside of its range and back towards 1.60.

Chart 2:

Source: City Index and Bloomberg

3, The performance of highly indebted, UK-listed companies such as Aggreko