Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1115.70 down $7.50 (comex closing time)

Silver $15.39 down 8 cents.

In the access market 5:15 pm

Gold $1115.00

Silver: $15.43

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a poor delivery day, registering 1 notice for 100 ounces Silver saw 0 notices for nil oz

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 230.85 tonnes for a loss of 72 tonnes over that period.

In silver, the open interest fell by 3037 contracts despite the fact that silver was up in price 18 cents yesterday. The total silver OI continues to remain extremely high, with today’s reading at 174,865 contracts In ounces, the OI is represented by .874 billion oz or 124% of annual global silver production (ex Russia ex China). This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end as they continue to raid as basically they have no other alternative.

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rests tonight at 435,603. We had 1 notice filed for 100 oz today.

We had no changes at the GLD today / thus the inventory rests tonight at 671.87 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. I thought that 700 tonnes is the rock bottom inventory in GLD gold, but I guess I was wrong. However we must be coming pretty close to a level of only paper gold and the GLD being totally void of physical gold. In silver, we had a big withdrawal in silver inventory at the SLV to the tune of 1.241 million oz, / Inventory rests at 324.968 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fell by 3,037 contracts down to 174,865 even though silver was up 18 cents in price with respect to yesterday’s trading. Again, we must have had some short covering. The OI for gold only rose by 114 contracts to 435,603 contracts despite the fact that gold was up by $15.60 yesterday. We still have close to 20 tonnes of gold standing with only 15.206 tonnes of registered gold in the dealer vaults ready to satisfy that which stands.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. One story on Greece

(zero hedge)

4. Five stories on China devaluing their yuan and how this will lead to a huge deflation throughout the globe. The USA dollar will skyrocket and there is nothing they can do about it.

(Zero hedge/Reuters)

5 Trading of equities/ New York

(zero hedge)

6. Three oil related story

(zero hedge)

7. Michael Snyder describes 12 clues as to the upcoming market crash

(Michael Snyder)

8. USA stories:

i) Atlanta Fed lowers estimation on 3rd quarter GDP to only.7%

ii) Business inventories rising faster than sales: sure sign of a recession.

Physical stories:

i) Bill Holter delivers a dandy tonight:

titled:

“Did the FINAL WAR just start?”

ii) Alasdair Macleod delivers a great paper:

titled: “Welcome to the world of ZIRP zombies”

Let us head over and see the comex results for today.

August contract month:

initial standing

August 13.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1 contract (100 oz) |

| No of oz to be served (notices) | 2509 contracts (250,900 oz) |

| Total monthly oz gold served (contracts) so far this month | 3824 contracts(382,400 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 448,877.6 oz |

Total customer deposit: nil oz

JPMorgan has 7.1966 tonnes left in its registered or dealer inventory. (231,469.56 oz) and only 844,938.531 oz in its customer (eligible) account or 26.28 tonnes

We gained 50 contracts or an additional 5,000 ounces will stand for delivery. Thus we have 19.698 tonnes of gold standing and only 15.206 tonnes of registered or dealer gold to service it.

August silver initial standings

August 13 2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | nil |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 16 contracts (80,000 oz) |

| Total monthly oz silver served (contracts) | 59 contracts (295,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 85,818.47 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,512,645.1 oz |

Today, we had 0 deposits into the dealer account:

total customer deposits: nil oz

total withdrawals from customer: nil oz

we neither lost nor gained any silver ounces standing in this non delivery month of August.

August 12./ a huge deposit of 4.18 tonnes of gold into the GLD/Inventory rests at 671.87 tonnes

August 7./no change in gold inventory at the GLD/Inventory rests at 667.93 tonnes August 6/no change in gold inventory at the GLD/Inventory rests at 667.93 tonnes August 5.we had a huge withdrawal of 4.77 tonnes from the GLD tonight/Inventory rests at 667.93 tonnes

August 4.2015: no change in inventory/rests tonight at 672.70 tonnes

And now SLV:

August 13.2013: a huge withdrawal of 1.241 million oz/Inventory rests tonight at 324.968 million oz

August 12.2015: no change in SLV inventory/rests tonight at 326.209 million oz.

August 11./ no changes in SLV inventory/rests tonight at 326.209 million oz.

August 7.no changes in SLV/Inventory rests this weekend at 326.209 million oz

August 6/no changes in SLV/inventory rests at 326.209 million oz

August 5/ a small withdrawal of 142,000 oz of inventory leaves the SLV/Inventory rests tonight at 326.209 million oz

August 4.2015: a small withdrawal of 476,000 oz of inventory at the SLV/Inventory rests at 326.351 million oz August 3.2015; no change in inventory at the SLV/inventory remains at 326.829 million oz

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

(courtesy/Mark O’Byrne/Goldcore)

Gold, The Fed, Exter’s Pyramid – When John Exter Met Paul Volcker

DAILY PRICES

Today’s Gold prices were USD 1,117.35, EUR 1005.54 and GBP 715.56 per ounce.

Yesterday’s Gold prices were USD 1,116.80, EUR 1003.23 and GBP 717.18 per ounce.

[LBMA AM prices]

Gold in USD – 10 Years

Gold and silver rose on the COMEX again yesterday – up 1% to $1,123.80 and silver was up 1.3% to $15.52 per ounce. This morning, gold is 0.7% lower to $1,118 per ounce.

Silver is 1% lower to $15.47 per ounce. Platinum and palladium are 0.8% and 1.4% higher to $997 and $622 per ounce respectively.

Gold, The Fed, Exter’s Pyramid – When John Exter Met Paul Volcker

GoldCore are blessed to have many well connected, informed and enlightened subscribers and clients throughout the world. On a daily basis, we receive interesting tidbits and insights from all corners of the world. A common thread in the dialogue with our growing 31,824 email subscribers and wider online and social media following is a genuine concern about the economic, financial and indeed monetary outlook for the world.

Some are what Paul Krugman and other currency debasement advocates would deride as ‘goldbugs.’ Most are ordinary people – of both modest means and wealthy – who are worried about their friends, family and fellow man’s financial and indeed general well being. Some are left wing, some are right wing, most are libertarian. Very few are the greedy, irrational ‘goldbugs’ that is a prevailing narrative in sections of the media today.

We have a fascinating dialogue with many readers. One of our readers living in the U.S. has first hand experience of people involved at the highest levels of the Federal Reserve. He is very concerned about the astronomical levels of debt in the U.S. and internationally and the fact that this debt continues to balloon in a completely unsustainable way.

With his permission, we are publishing his recent email to me (mark.obyrne at goldcore.com) in its entirety. It is about a private meeting between ex-New York Fed Vice President John Exter and ex Fed Chairman Paul Volcker.

We have added a few images in order to help understand the gravity of the building financial and monetary risks of today.

Hi Mark,

While reading your piece last week on the US Federal debt having reached $18 trillion, it brought back my memory of a visit John Exter and I had with Fed Chairman Paul Volcker, back in 1981. It was a instance I’ll never forget!

John and I had a mutual billionaire widow client whose husband had been a Washington DC real estate magnet. He had died suddenly and she decided she wanted to have a part of her assets in physical gold and mining stocks. I recall she set the allocation at $50 million.

John Exter and Paul Volcker – Prudent Central Bankers

The widow had us travel to DC for a morning consultation followed by a luncheon. It was early April 1981 and 91 day US Treasury Bill rates were near 18%.

Our luncheon ended around 1:30 PM and we had a few hours to kill before our flight back to New York.

John Exter and Paul Volcker knew each other having been at the New York Fed as Vice Presidents and John decided he’d phone Volcker to see if he could see us before our return flight. Volcker took the call, said he would cancel his afternoon engagements and to come right over to the Fed. We got to the Fed and there were 36″ high lumber piles of one foot long 2″X4″ pieces all around Volcker’s office and the offices of his staff. Sky high interest rates had turned the construction industry down and the masses of unemployed construction workers were mailing Volcker the 2X4 pieces with nasty messages written on them in protest of the high rates.

John and I were at the Fed in a private conversation with Volcker for nearly three hours and in fact we nearly missed our flight because we stayed so long.

National Debt of $18.2 Trillion – Unfunded Liabilities of $100 Trillion to $200 Trillion

US Federal debt, in 1981 was rising through the $1 trillion level and I remember Volcker lamenting over the situation and asking John what he would recommend to get a handle on Federal spending. John gave Volcker a stern lecture on the Fed’s expansionary policies and told him the Fed would eventually end up destroying the whole American economy and the dollar because the Fed had become a prisoner of it’s own expansionism and it was something it couldn’t stop. John and Volcker discussed all the pitfalls of Keynesian and monetarism and Volcker didn’t rule out an eventual collapse of the dollar and second deflationary depression. I remember Volcker asking John when he would begin dropping short term rates and John commented that rates would have to drop soon or else the economy would fall off a cliff. It’s interesting that it wasn’t long after our session that rates started to come down.

The meeting was an experience of a lifetime for me to be sitting there in Volcker’s office listening to one gold standard economist central banker conversing with a Keynesian economist central banker. John Exter spelled out his scenario for Volcker and warned him of how badly the Keynesian experiment would end if it went on for an extended period of time. Volcker just sat there and listened and showed his concern.

Here we are 33 years later with US Federal Debt of $18 trillion with the country’s GDP at $17 trillion. A pretty disturbing situation, to say the least!

Exter’s Pyramid via Zerohedge.com – h/t ‘Adam’

Volcker has joined my old club The Pilgrims of the United States which is based out of New York. I’ve been a member for nearly 40 years but don’t get back for meetings and events because of the travel distance. I hear Volcker goes to all the events and a fellow Pilgrim friend has approached him at meetings and when the late John Exter’s name is mentioned Volcker stops and has nothing but kind things to say about him.

Thought you’d be interested in learning of my anecdotal experience.

Best regards,

—————-

When reading this, some will say that this was in the past and these are different times and may not understand this warning from our recent history. However, it offers a lesson from the past that has significant relevance for today. The debasement of currency has ended in economic debacles in every single country, in every single instance throughout history.

Today, we see currency debasement internationally on a global scale – this has never happened before and has never been seen throughout history. The uber Keynesians attack those who warn about monetary risks and proclaim that none of the ‘goldbugs’ warnings have come to pass. Except of course, possibly the worst financial crisis that the world has ever seen and meager, unsustainable recovery.

We would caution that ‘yet’ may be the appropriate word here and we should all be vigilant and focus on the long terms risks – not the short term panaceas, tentative recoveries and massive asset bubbles of today.

end

(courtesy Bron Suchecki/Perth Mint/GATA)

Bron Suchecki: Telling a metal shortage from a production capacity shortage

Submitted by cpowell on Thu, 2015-08-13 15:29. Section: Daily Dispatches

11:29a ET Thursday, August 13, 2015

Dear Friend of GATA and Gold:

Perth Mint research director Bron Suchecki writes this week about distinguishing a shortage of monetary metal from bottlenecks in coin and bar production capacity. Suchecki’s commentary is headlined “Coin Shortage FAQs: Telling a Real Shortage from a Capacity Shortage” and it’s posted at the Perth Mint’s Internet site here:

http://research.perthmint.com.au/2015/08/12/coin-shortage-faqs-telling-a…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Alasdair Macleod attacks the global zero interest rate policies:

(courtesy Alasdair Macleod/GATA)

Alasdair Macleod: Welcome to the world of ZIRP zombies

Submitted by cpowell on Thu, 2015-08-13 16:06. Section: Daily Dispatches

12:05p ET Thursday, August 13, 2015

Dear Friend of GATA and Gold:

GoldMoney research chief Alaadair Macleod writes today that central banks are about to discover that zero interest rates don’t revive the real economy but only put it in grave danger as the policy is reversed.

Macleod writes: “Normalising interest rates could generate a stock market collapse, risk setting off an avalanche of bankruptcies from overleveraged businesses, and make government finances wholly untenable. Higher interest rates risk triggering a second financial crisis that could also undermine currencies, pushing up price inflation. While macroeconomic theories can be faulted on the basis of outcomes, there is little doubt the systemic threat from a trend of rising interest rates is very real.”

His commentary is headlined “Welcome to the World of ZIRP Zombies” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/analysis/welcome-to-the-world-of-zirp…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The UK Telegraph talks about the press conference last night where China continues to devalue

p.s. the futures in china looks like another 1% devaulation in the yuan for tomorrow’s trading!!

(courtesy London’s Telegraph/GATA)

‘Trust the market,’ Chinese central banker says after rigging it

Submitted by cpowell on Thu, 2015-08-13 17:20. Section: Daily Dispatches

China’s Central Bank Vows to Control Market “Herding” as Yuan Falls for Third Day

By Szu Ping Chan and Tara Cunningham

The Telegaph, London

Thursday, August 13, 2015

China’s central bank has dismissed claims that it is trying to engineer a 10-percent fall in the yuan as “groundless,” just days after it devalued its currency for the first time in over 20 years.

As the renminbi weakened for another day, the People’s Bank of China said strong economic fundamentals and the country’s deep foreign exchange reserves provided “strong support” to the exchange rate.

Yi Gang, deputy governor of the central bank, said it stood ready to step in if volatility became “excessive” and the market started “behaving like a herd of sheep.”

“Trust the market, respect the market, fear the market, and follow the market,” he told a press conference.

China pushed down its official guidance rate by 2 percent on Tuesday, which rocked markets and triggered fears of a “currency war.” …

… For the remainder of the report:

http://www.telegraph.co.uk/finance/economics/11800155/China-says-no-more..

end

Dave Kranzler goes one on one with John Embry:

SoT #52 John Embry: The Public Has Been Set Up For Slaugher – It Doesn’t Have A Chance

One of the things that has bothered me a lot is the cognitive dissonance amongst – not the public, the public doesn’t have a chance, they’re being lied to constantly by the media – but what I find distressing is the cognitive dissonance amongst financial professionals. – John Embry on Shadow of Truth

The precious metals sector has been under violent manipulative attack since gold and silver peaked in price in 2011. The western Governments and Central Banks had no choice but to attack real money because it would be the only way that they could continue implementing their ultimately catastrophic monetary policies in order to prevent systemic collapse.

But as Ayn Rand asserted a long time ago, you can ignore reality but you can’t ignore the consequences of ignoring reality. It is likely that the move by the Chinese to begin devaluing their currency is an acknowledgement of this reality and it represents China’s attempt to get a head start on the rest of the world in order to minimize the consequences it will suffer relative everyone else.

The surprise move by the Chinese to devalue the yuan is a “signal event” because basically it’s going to lead to currency debasement everywhere – it’s going to expose everyone else. What could be a better advertisement for gold and silver?…When this finally explodes [gold] it’s not going to go up $50 or $100 bucks it’s going go up massively because the whole paper Ponzi scheme will be exposed. – John Embry

We have never in history witnessed extreme systemic imbalances in the world financial economic system to the extent that they are now occurring. As an example, Mr. Embry referenced the fact that, “The U.S., Japan and Canada have 52% of the Federal funded debt in world and they have only 7% of the population base.”

One of the things that has bothered me a lot is the cognitive dissonance amongst – not the public, the public doesn’t have a chance, they’re being lied to constantly by the media – but what I find distressing is the cognitive dissonance amongst financial professionals. – John Embry

Finally, there’s a massive trade to be had in the gold and silver stocks, assuming our worse scenario does not play out. That is to say that the mining stocks have never been cheaper relative the price of gold and silver than they are now. In fact, I would venture to say that it might be the most undervalued market sector in history right now.

Of course, the “worst scenario” is the scenario that hits our system in which you wished you were watching the collapse from another planet…

end

And now Bill Holter, with a sensational commentary.

(courtesy Bill Holter/Sinclair-Holter collaberation)

Did the FINAL WAR just start?

As our backdrop, we are “told” the world is in recovery from the very bad experience of 2008. Since then, various central banks have monetized debt on a massive scale, led by the Federal Reserve of the U.S.. Undoubtedly, the greatest “export” from the U.S. has been dollars themselves and financial products known as derivatives. For the most part, the world spun merrily until last fall when Saudi Arabia decided to increase production and lower prices. This was presumably done at the request of the U.S. and meant as a tool to injure Russia’s energy sector, economy and financial system. Can the petrodollar which became accustomed to $100 oil be supported with sub $50 oil? There are two sides to this coin, yes the consumer of oil saves but doesn’t lower oil price mean less liquidity in the system? Doesn’t it mean lower velocity and less demand for dollars?

Moving along, did anyone really wonder “why” or what (or better yet, WHO) was behind China being put off for acceptance as a component of the SDR? Then just two trading days later, China devalued their currency in a surprise move…followed by two more devaluations! Remember, the U.S. has been prodding China to strengthen their currency and has gone so far as to call them a “currency manipulator”! Now we see China doing the exact opposite of U.S. requests (demands?). World markets have been shaken, and at a time when liquidity is quite tight.

A stronger dollar since last fall has acted as a constant and nagging “margin call” to the world which has contributed to the lack of liquidity. Have the Chinese finally said “fine, you want to issue a margin call to the world, we will help you issue it. Let’s see what happens to your financial system when the margin call fails to be met?”. Do you see what I am getting at here? The Chinese are now forcing the dollar higher by devaluing their own currency. They understand the dollar is nothing more than a debt instrument, are they attacking and intending to destroy the dollar with its own strength?

Follow this through, a stronger dollar will decrease our exports and slow our already slow or negative economy. A too strong dollar can actually undermine itself and even kick off a derivatives chain explosion. Our banks and brokers are very thinly capitalized, can they withstand losses in derivatives caused by a currency crisis? Can they withstand the losses from failed counterparties unable to pay? Do you see? A currency crisis “caused” by China could be a calamity. China has already accused Citadel (Ben Bernanke’s new employer) of creating the crash in their equity markets, is a currency crisis retaliation for their equity crash and public shaming by the IMF? If you understand how the Chinese think and also understand the works of Sun Tzu, Jim and I ask if China’s strategy is … “In order to destroy the dollar permanently make it stronger temporarily.”?

Another area to look at is gold and silver. Supplies have recently gotten very tight, not just for retail in the U.S. but all over the world. Has production slowed or have buyers stepped up their hoarding? Or, have Western central banks reduced their “dis hoarding”? Whatever it is, something in the supply/demand dynamics has definitely changed …and it has not taken much money to do it! Are these separate events or are they tied together somehow?

This is where it gets weird or some might say “coincidental”. Did anyone see the explosion at the Chinese port city of Tianjin yesterday?https://www.youtube.com/watch?v=_92WaPxeqCs “Yesterday” being one day after China devalued their currency? I am no rocket scientist and cannot say for sure, but does this not look like a nuclear explosion? Can someone out there explain to me in simple terms how a chemical explosion could look like this? As for the word “coincidence”, the CIA says there is no such thing as a coincidence!Speaking of coincidences and I have permission to pass this along to you. Jim Sinclair wrote just a few days ago for the first time in many a moon, he said “gold has very limited downside from here and could move to $2,000 as an initial stop”. Do you believe it was a coincidence that he speaks now? No, he was called and was “told” by the same people who guided him in 1980 at the market top. Do you believe it was a coincidence following Jim’s writing, the IMF shunned China followed by the shot heard ’round the world of a yuan devaluation …three times?!!! …not to mention an explosion that could be seen from space! My mind is made up, no it is not any coincidence at all.

For months I have been suggesting Mr. Putin would drop a “truth bomb” revealing all sorts of false flag events and fraud perpetrated by the U.S.. I still believe this is to come and now even more likely. Why more likely? Because the financial sparring between East and West may have taken a very serious turn yesterday and I seriously believe a tactical nuke was set off. If this is the case, China will provide proof and they will retaliate. I believe the smoldering stages of what was a financial/technological/trade war have now become hot and the first shot was fired. I truly do ask for comments regarding what happened in Tianjin. Please do not send me opinions, I would like to hear exactly why or why not the explosion was nuclear. I will believe a tactical nuke until someone proves to me it was not. May God help us all with what comes!Standing Watch,Bill Holter

Holter-Sinclair collaboration

Comments welcome!

bholter@Hotmail.com

end

1 Chinese yuan vs USA dollar/yuan drops big time to 6.398/Shanghai bourse: green and Hang Sang: green

2 Nikkei up 202.78 or 0.99%

3. Europe stocks all in the green /USA dollar index up to 96.52/Euro down to 1.1120

3b Japan 10 year bond yield: rises to 38% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 124.49

3c Nikkei still just above 20,000

3d USA/Yen rate now just above the 124 barrier this morning

3e WTI 43.27 and Brent: 49.96

3f Gold down /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund slightly rises to .63 per cent. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate rises to 14.77%/Greek stocks this morning down by 0.11%: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield rises to : 10.27%

3k Gold at $1117.50 /silver $15.34

3l USA vs Russian rouble; (Russian rouble up 6/10 in roubles/dollar) 64.28,

3m oil into the 43 dollar handle for WTI and 49 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9789 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0844 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving further away from negativity to +.63%

3s The ELA rose another 900 million euros to 90.4 billion euros. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.17% early this morning. Thirty year rate below 3% at 2.85% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Risk On Despite Third Chinese Devaluation In A Row As PBOC Jawbones, Intervenes In FX Market

With everyone now focused on what China’s daily Yuan fixing will be every night, there was some confusion why last night the PBOC decided to devalue the CNY by another 1.1% to 6.4010, despite its promise that the devaluation would be a “one-off” event, taking the 3 day devaluation to just about 4.5%. However, subsequently in a press conference in which the central banks which now have to handle a metaphorical grenade going off not only in its burst stock market bubble but in its FX market as well, vice-governor Yi Gang said that the PBoC will continue to step in when the market is ‘distorted’, that there is no economic basis for the Yuan to fall continuously and that it will look to keep the exchange rate ‘basically stable’. The Vice-Governor also said that the PBoC will closely monitor cross-border capital flows and that reports suggesting the Central Banks wants to see the currency depreciate 10% are ‘groundless’.

Which is ironic considering after just 3 days, the PBOC is already half the way there!

In any event, in an attempt to calm nerves and smooth the volatility, there was another bout of PBOC FX intervention, and as can be seen in the chart below, the onshore Yuan actually closed stronger than the fixing after a bout of buying in the last minute sent it under 6.40: this was the first time the onshore currency has traded stronger than the PBOC fix since November!

End result: the market and China’s trading partners are still trying to assess the motive for this week’s move and how far they’re likely to allow the currency to fall. As DB summarizes, the PBOC’s soothing if contradictory comments may give some comfort “but it does feel there’s a lot more to come on this story over the weeks ahead.”

For now, however, the risk on mood has returned and futures appear set for a 0.3% rise at the open, with the 200DMA firmly in the S&P’s rearview mirror after yesterday’s epic stock buyback spree (noted previously), and with the VIX almost certain to trade under 13 shortly after the market open as the Fed does everything in its power to add to the PBOC’s artificial calm.

Asian equity markets staged a mild recovery after US equities rebounded on bargain hunting. Shanghai Comp (+1.8%) and Hang Seng (+0.5%) traded between gains and losses throughout the session, with the latter led by index heavyweight Tencent (+4.5%) after the Co. reported strong earnings. ASX 200 (+0.1%) rose as a bounce back in the commodity complex benefitted large miners and energy names. Elsewhere, the Nikkei 225 (+1.0%) was led higher by gains in IT names offsetting the weakness in telecoms where Softbank declined after Alibaba sales saw its slowest growth in 3-years. JGBs rose on the back of a strong 5-year bond auction following a better than prior b/c and average yield.

Elsewhere, much of today’s price action has been a reversal of the recent trend, with European equities (Euro Stoxx: +1.4%) firmly in the green after the DAX fell around 6% in the last two days of trade, with equities benefitting from positive sentiment seen in the latter half of the US session, where equities reversed early losses to finish in the green.

In fixed income markets, Bunds reside in negative territory this morning as dealers suggest leveraged and real money selling of both Bunds and periphery bonds. Volumes have been relatively light so far today however analysts at I FR note that the German curve has steepened particularly with 2/10s and 10s/30s. T-Notes also trade lower heading into the pit open, after USTs gained over 1.5 points over the last two days, ahead of today’s USD 16bIn 30yr auction. This, of course, is quite ironic because when the PBOC intervenes to offset its devaluation, it sells less TSYs or even outright buys them. But the math there is too confusing for algos so all those who took profits on their 10Y positions after the Gartman fade yesterday, great timing as usual.

The USD has seen a bout of strength this morning (USD-Index: +0.3%) after falling over 1% yesterday ; in terms of the reaction in PBoC, USD/CNH initially moved higher after the PBoC weakened their currency before paring the move as the central bank refuted claims of a 10% devaluation in the currency and said there is no basis for continued devaluation of CNY and signalled that CNY will appreciate in the future.

The metals complex has weakened on the back of USD strength overnight, with gold coming off its 3 week highs seen yesterday, while copper prices also mildly retreated from best levels . Elsewhere the energy complex has seen a widening of the WTI/Brent spread, with positioning seen in Brent ahead of tomorrow’s futures contract expiry has seen a widening.

All that said, China may quickly be forgotten if only for a few hours when looking ahead at today’s key economic data which is in the form of US retail sales. Should the retail sales print be far stronger than expected, then the shaky September rate hike case will be right back on the table, and as has been the case recently, will be another instance of “good economic news is bad news for stocks.” Which may explain why equities are far less exuberant this morning than usual following massive central bank intervention.

In Summary: European shares rise after 2 days of declines, as China’s central bank signaled support for its currency, the tech and financial services sectors outperform, basic resources, insurance underperform. PBOC says there’s no basis for yuan depreciation to persist, will step in to control large fluctuations. Companies including Nestle, ThyssenKrupp, RWE and Maersk released earnings. The Swiss and French markets are the best-performing larger bourses, U.K. the worst. The euro is weaker against the dollar. Japanese 10yr bond yields rise; German yields increase. Commodities gain, with silver, natural gas underperforming and Brent crude outperforming. U.S. jobless claims, continuing claims, Bloomberg consumer comfort, retail sales, import price index, business inventories due later.

Market Wrap

- S&P 500 futures up 0.2% to 2088.2

- Stoxx 600 up 1.3% to 387.9

- US 10Yr yield up 1bps to 2.16%

- German 10Yr yield up 2bps to 0.63%

- MSCI Asia Pacific up 0.1% to 138.4

- Gold spot down 0.5% to $1119.3/oz

- Eurostoxx 50 +1.2%, FTSE 100 +0.5%, CAC 40 +1.5%, DAX +1%, IBEX +0.9%, FTSEMIB +1.4%, SMI +1.5%

- Asian stocks rise with the Shanghai Composite outperforming and the ASX underperforming; MSCI Asia Pacific up 0.1% to 138.4

- Nikkei 225 up 1%, Hang Seng up 0.4%, Kospi up 0.4%, Shanghai Composite up 1.8%, ASX up 0.1%, Sensex up 0.7%

- Euro down 0.34% to $1.1121

- Dollar Index up 0.27% to 96.52

- Italian 10Yr yield down 1bps to 1.81%

- Spanish 10Yr yield up 0bps to 1.98%

- French 10Yr yield up 2bps to 0.95%

- S&P GSCI Index up 0.7% to 370.4

- Brent Futures up 1.2% to $50.3/bbl, WTI Futures up 0.6% to $43.6/bbl

- LME 3m Copper up 0.7% to $5225/MT

- LME 3m Nickel up 0.5% to $10650/MT

- Wheat futures up 1% to 502.3 USd/bu

Bulletin Headline Summary from Bloomberg and RanSquawk

- Despite the PBoC weakening the CNY for a third consecutive day, the less dramatic move failed to see a sustained reaction in most asset classes

- As such much of today’s price action has been a reversal of the recent trend, with European equities and the USD both firmly in the green

- Looking ahead, today’s highlight comes in the form of US retail sales, while participants will also be looking out for US import prices and weekly jobs numbers

- Treasuries decline amid gains in stocks and before week’s auctions conclude with $16b 30Y, WI 2.855%, lowest since April, vs. 3.084% in July.

- Onshore yuan spot rate pared declines in late trading to close 0.19% lower in Shanghai, following the steepest two- day drop since 1994

- It was the second day in a row that at least one major Chinese bank sold dollars to influence the closing level, according to traders

- Japan “need not worry” about China’s devaluation of the yuan because it can always offset the effects by easing monetary policy, said an adviser to Prime Minister Shinzo Abe

- Explosions rocked a hazardous-chemicals storage site in the northern Chinese city of Tianjin, killing at least 44 people and disrupting operations at one of the world’s busiest ports

- Germany’s government withheld approval of the draft bailout plan for Greece, saying a bridge loan remains an option if a full aid program isn’t agreed in time for a payment to the European Central Bank due next week

- Greece’s statistical agency said GDP rose 0.8% in 2Q as it revised up 1Q to show stagnation. Nominal GDP, which excludes adjustments for price changes, fell 0.7% in 2Q

- Former U.K. Prime Minister Tony Blair warned that his Labour Party faces “annihilation” if it elects anti-austerity, pro- renationalization lawmaker Jeremy Corbyn as its new leader

- $1.5b IG and $1.7b HY priced yesterday. BofAML Corporate Master Index OAS +2 to new YTD wide +164; YTD low 129. High Yield Master II OAS +12 to 567, new YTD wide; YTD low 438

- Sovereign 10Y bond yields higher. Asian, European stocks gain, U.S. equity-index futures rise. Crude oil and copper steady, gold falls

DB’s Jim Reid completes the overnight recap

It’s straight to China this morning where the PBoC has, for the third consecutive day, moved to devalue the Yuan further after setting the fix 1.1% weaker than Wednesday at a reference rate of 6.401. That’s a touch higher than yesterday’s closing price (6.386) after the currency actually bounced in the last 15 minutes of trading after authorities stepped in. The move in the fix this morning was modest-ish relative to the previous two days (after a 1.6% and 1.9% cut), but still significant enough to see the onshore Yuan depreciate a further 0.34% this morning to 6.408, although that’s well off yesterday’s 6.449 high print before the late rally. The offshore Yuan is 0.19% weaker meanwhile.

Meanwhile, we’ve also heard from the PBoC this morning after the Central Bank held a press conference to address the recent events. Vice-Governor Yi Gang said that the PBoC will continue to step in when the market is ‘distorted’, that there is no economic basis for the Yuan to fall continuously and that it will look to keep the exchange rate ‘basically stable’. The Vice-Governor also said that the PBoC will closely monitor cross-border capital flows and that reports suggesting the Central Banks wants to see the currency depreciate 10% are ‘groundless’. The market and trading partners are still trying to assess the motive for this week’s move and how far they’re likely to allow the currency to fall. These comments may give some comfort but it does feel there’s a lot more to come on this story over the weeks ahead.

As we point out below there was a decent rebound in risk assets through the US session yesterday which has overnight helped lift some of the more China sensitive currencies too. This morning however we’ve seen the better sentiment continue with the likes of the Aussie Dollar (+0.10%), Korean Won (+1.16%), Malaysian Ringgit (+0.67%) and Indonesian Rupiah (+0.44%) some of the notable movers. 10y Treasuries are 2.6bps higher in yield meanwhile at 2.171% while across the equity space it’s been a better start to trading for the most part with the Nikkei (+0.65%), Hang Seng (+0.30%), Kospi (+0.62%) and ASX (+0.74%) in particular all up. China bourses have pared earlier gains however with the Shanghai Comp and Shenzhen -0.62% and -0.56% respectively.

Looking back at yesterday’s events, it appeared that markets were on course to mirror much of what we saw on Tuesday post the first PBoC devaluation of the Yuan, only for risk assets in the US to stage a large turnaround and buck the sell-off trend that had dominated the European session and the early part of the US one. On the back some steep losses out of equity markets in Asia, European bourses opened up softer and proceeded to weaken over the course of the session. The Stoxx 600 eventually finished down 2.70% for its biggest one-day loss since October 15th last year, while the DAX (-3.27%), CAC (-3.40%), IBEX (-2.44%) and FTSE MIB (-2.96%) also suffered heavy falls. Losses were again led by the auto and consumer names with notable falls for BMW and Daimler pushing the Stoxx 600 auto gauge down nearly 8% over the last two days, the largest fall since 2011. Credit markets also suffered through the European session with Crossover in particular nudging 9bps wider.

That weakness carried over into the US open where the S&P 500 promptly fell 1.5% and in turn seeing the index turn negative YTD. Sentiment swiftly changed however and the index did something it hasn’t done since May 2012 in reversing a 1.5% intraday decline to close just about in positive territory at +0.10%. There were similar rebounds too for the Dow and NASDAQ which closed flat and +0.15% respectively. In the credit space meanwhile, having traded as much as 2.5bps wider CDX IG also benefited from the turnaround, recovering to close about half a basis point wider. With the S&P 500 advancing 1.32% so far this year, US equities have seemingly failed to break with conviction one way or the other and the index has now traded in its tightest range since 1927. It wasn’t entirely obvious what triggered yesterday’s change of sentiment in the US session with some of the reasoning being placed on technical triggers driven by the S&P 500 declining below its 200-day moving average (a level its only closed below twice this year). A bounce back in the Oil space however which saw WTI (+0.51%) and Brent (+0.98%) recover off the recent lows helped support a decent recovery for energy stocks (+1.86%) which ended the day the best performing sector.

That turnaround in sentiment also saw some material moves in the Treasury market yesterday. Having plummeted as much as 10bps lower in yield intraday and touching 2.043%, the 10y benchmark weakened throughout much of the US session and eventually finished more or less unchanged (+0.7bps) at 2.149%. Yesterday’s 10y bond auction caught our eye too and helped nudge yields slightly higher after the auction came at the lowest yield (2.115%) since April 30th and the weakest bid-to-cover ratio (2.40) since March 2009. It’ll be interesting to see how today’s 30y auction goes as a result. Fed Funds Dec15 (+0.5bps) and Dec16 (-2.5bps) were slightly mixed, while the probability of a September move by the Fed rose 4% to 44%.

Data wise we got more employment data with the June JOLTS job openings print which pointed to some encouraging signs in the details. Although job openings declined by 108k to 5.25m (vs. 5.35m expected), the hiring rate improved a tenth to 3.7% and in the process matching its post-recession high. The quits rate remained unchanged at 1.9% and our US colleagues note that both the hiring and quits rates are now just a tenth of a percent below their respective readings when the Fed began hiking in June 2004. Meanwhile, the July monthly budget statement showed a slightly higher than expected deficit ($149bn vs. $140bn expected).

There was also more Fedspeak for us to digest yesterday and this time from the NY Fed President Dudley. The Fed official offered very little however in terms of trying to nail down his bias for hike timing, saying that ‘hopefully we’re going to make progress in terms of our goals’ and so ‘hopefully in the near future, we’ll be able to actually begin to raise interest rates’ but that ‘when that is precisely, depends on the data’. In the first comments that we’ve seen from any Fed officials on China, Dudley also added that it’s not inappropriate for the currency to adjust in consequence to the weakness in the economy. Dudley did however also go on to say that it’s still too soon to draw firm conclusions about what all this means.

European data flow yesterday was highlighted by a softer than expected June industrial production reading (-0.4% mom vs. -0.1%), dragging the annualized reading down to +1.2% yoy from 1.6% previously and raising questions ahead of Friday’s Q2 GDP report. Over in the UK meanwhile we got a host of employment indicators yesterday. The ILO unemployment rate held steady in June at 5.6% as expected and about half a percent above the BoE’s view of the long-term equilibrium rate. Jobless claims resumed their monthly decline in July (-4.9k) with June’s reading largely revised away. Headline wage growth of 2.4% yoy in Q2 was lower than the 2.8% expected and well below the 3.2% rate for the previous overlapping quarter. DB’s George Buckley noted that we should treat this with caution however with a number of explanations for this fall including base effects, falling bonuses and weak public sector pay. In fact, stripping out the bonus effect saw earnings in line at 2.8% yoy for the quarter. George thinks that yesterday’s data suggests that we are moving ever closer to the need for a rise in rates. Sterling had a stronger session yesterday with the Pound closing up +0.26% versus the Dollar.

Before we move on, yesterday we heard of some slight setback for Greece in gaining parliamentary approval for its new deal with further pushback from Germany in particular. German Chancellor Merkel’s spokesman, Steffen Seibert, said that the deal ‘goes in the right direction’ but that it was ‘not possibly to say’ whether or not it’s ready for a vote through the Bundestag as per a report from Ekathimerini. Another Finance Ministry spokesman said that ‘bridge financing is not off the table’ and that ‘we’re still taking bridge financing into consideration if it’s not possible to pay out a first tranche in August to meet the outstanding obligations’.

Taking a look at today’s calendar now, it’s a busy morning of inflation data in Europe where we get the July CPI prints for Germany, France and Spain. As well as this, we’ll also get the ECB minutes from the last Council meeting. The highlight in the US this afternoon meanwhile will no doubt be on the July retail sales reading with the market looking for a +0.6% mom reading at the headline and +0.4% mom print at the ex auto and gas level. The retail control group reading (which goes into the national accounts) will also be closely monitored while away from this we get the import price index print, business inventories and initial jobless claims.

end

Last night in China: authorities devalue again for the third day as the yuan hits its 4 year low. Japan states that it will lower rates to compete with China as the race to the bottom escalates:

(courtesy zero hedge)

Chinese Devaluation Extends To 3rd Day – Yuan Hits 4 Year Low, Japan Escalates Currency Race-To-The-Bottom Rhetoric

The “one-off” adjustment has now reached its 3rd day asThe PBOC has now devalued the Yuan fix by 4.65% back to July 2011 lows.

The PBOC seeks to reassure…

- *CHINA PBOC SAYS YUAN REMAINS STRONG CURRENCY IN LONG-TERM

- *PBOC SAYS THERE IS DEMAND FOR DEVALUATION OF YUAN VS USD

- *PBOC CHANGE OF YUAN MECHANISM RELATED TO JULY CREDIT: ZHANG

- *PBOC SAYS YUAN CHANGE IS BENEFICIAL TO LONG TERM STABILITY

- *PBOC SAYS YUAN EXCHANGE RATE ADJUSTMENT ALMOST COMPLETED

- *YUAN RATE ADJUSTMENT POSITIVE TO CONFIDENCE IN YUAN: PBOC’S YI

- *NEW YUAN MECHANISM `POSITIVE’ TO INTERNATIONALIZATION: PBOC YI

- *PBOC SAYS NO BASIS FOR YUAN’S CONSTANT DEVALUATION: ZHANG

Even before this evening’s date with debasement history, Japan felt the need to step up the currency war rhetoric. Following disappointing Machine Orders data, Abe advisors Hamada warned that “Japan can offset Yuan devaluation by monetary easing,” and so the race to the bottom escalates. China has its own problems as BofAML’s leading economic indicator showed “the foundation for a growth recovery is not solid, facing more downward pressure,” and while confusion reigns over why The PBOC would intervene at the close to strengthen the Yuan last night, the reality is the commitment isn’t to a devaluation for China’s exports, butundoubtedly its actions are directed toward trying to keep the wholesale finance interfaces somewhat orderly. Finally, China’s devaluation couldn’t come at a worse time for Argentina – about a quarter of the country’s $33.7 billion of foreign reserves are now denominated in yuan, which suffered its biggest loss since 1994 on Tuesday.

Having devalued the (onshore) Yuan fix by 3.5% in the last 2 days, China did it again… shifting Yuan to 4 year lows

- *CHINA SETS YUAN REFERENCE RATE AT 6.4010 AGAINST U.S. DOLLAR

Offshore Yuan dropped back to 6.50…

And China Stocks have opened lower…

- *CHINA’S CSI 300 STOCK-INDEX FUTURES FALL 1% TO 3,975.2

S&P Futures are fading…

Some more liquidity needed…

- *PBOC TO INJECT 40B YUAN WITH 7-DAY REVERSE REPOS: TRADER

And sure enough, not be outdone, Japan threatens to re-escalate the currency war…

- *ABE ADVISER HAMADA SAYS CHINA’S FX MOVE WILL TEND TO BOOST YEN

- *HAMADA: JAPAN CAN OFFSET YUAN DEVALUATION BY MONETARY EASING

- *HAMADA:BOJ MAY EASE IF CHINA MOVE HITS EXTERNAL DEMAND TOO MUCH

But China has it’s own problems, as BofAML notes, China LEAP (leading economic activity pulse) fell to-3.9% YoY in July from -2.6% in June, as five of the seven LEAP components weakened.

Similarly, other macro activity data released in July worsened from a surprisingly strong June and disappointed the market. It suggests the foundation for a growth recovery is not solid, and economic growth faces more downward pressure as financial sector activity has slowed after the recent stock market slump.

On the demand side, housing starts further declined to 16.4% yoy in July after dropping 14.3% in June. We think destocking could still be ongoing in tier 3-4 cities and the housing market recovery has yet to drive acceleration in housing starts. Auto sales growth slumped to -7.1% YoY from -2.3%, likely due to weakening consumer demand for some big-ticket items amid stock market turmoil while staple good sales remained resilient.

Production-side components were mixed,with weaker power and steel output growth but slightly better cement output growth. Power and steel output growth was particularly poor in July, likely due to plummet in commodity and raw material prices on a bearish growth outlook amid stock market turmoil.

Medium- to long-term loan growth edged down by 0.8pp, but if taking into account local government debt swap, the decline would be 0.3pp instead.

* * *

The fallout from China’s decision is going global…

China’s devaluation couldn’t come at a worse time for Argentina.

About a quarter of the country’s $33.7 billion of foreign reserves are now denominated in yuan, which suffered its biggest loss since 1994 on Tuesday.

* * *

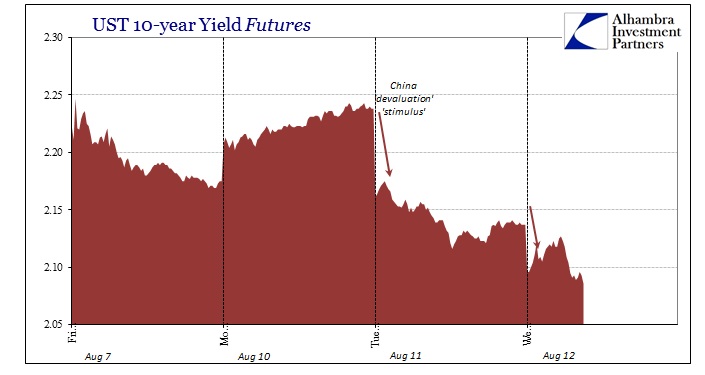

And finally, here is Jeffrey Snider of Alhambra Investment Partners discussing the other reality of what is occurring in China – as opposed to the paint-by-numbers version spun on TV – explaining why the PBOC would seemingly “allow” devaluation one day and then act against it the very next. They are just trying to hold on for dear life, managing imbalances that are beyond their grasp.

While everyone remains sure that the PBOC is actively trying to “allow” the yuan to depreciate as some kind of export catalyst, the “dollar” continues to show (not suggest) otherwise. Liquidity and “dollar” markets are still roiled rather than soothed,especially the US treasury market where the bid right at the open (what look very much like continued collateral calls) pushes more like a combination of October 15 and January 15.

As if to underscore the runaway nature, the PBOC apparently intervened against this “devaluation” just last night. From the Wall Street Journal:

Tuesday, the People’s Bank of China surprised global markets with what looked like a win-win currency depreciation for the country—appearing to cede more control of its exchange rate to market forces, which the International Monetary Fund and others have long urged it to do, while also helping Chinese exporters.

Its intervention only one day later raised questions about its commitment to an exchange rate driven more by supply and demand and less by government direction.

The Journal’s confusion here is demonstrated by what is a mistaken assumption in the first paragraph leading to the mystery of the second. The PBOC’s commitment isn’t to a devaluation for China’s exports, but undoubtedly its actions are directed toward trying to keep the wholesale finance interfaces somewhat orderly.When the yuan was trading exactly sideways for nearly five months, that was the same setup; the PBOC was keeping the yuan stable so that it wouldn’t devalue and thus signal the depth of the “dollar” financing strain.

That is the problem orthodox commentary and theory has with wholesale finance, they just don’t get it.Devaluation of currency doesn’t mean that in this context just as a “strong dollar” isn’t anything like the term. Both are forms of internal disruption, the direction of that is just an expression of what manner of wholesale finance is becoming most unruly. Credit-based “money” systems do not operate like the currency systems from before 1971. Floating currencies aren’t really that, so much as they are just another form of traded liabilities in global banking.

The Chinese have a “dollar” problem just the same as the Swiss, Brazilians and the rest (including the dollar). There is a global retreat in eurodollar funding that is wreaking havoc, expectedly, globally. And in China that is particularly true as the Chinese banks through external corporates joined the “dollar short” several years back. Joined now under PBOC “reform”, there has been an almost hostility if not at least disfavor over the “dollar” intrusion as it has been taken as one primary element of the bubbles (what mainstream mistakes for “hot money”). As a result, the PBOC has been almost chasing “dollars” out of the system in an attemptedorderly purge.

That led to what looked like historic “outflows” in 2015 as “dollar” conditions for the Chinese “short”, so it is absolutely no surprise to see this occurring now. The only mystery has been, as I have been writing for some time, what the PBOC was doing to counteract it during those five months. That would tell us both how serious the turmoil was and how ineffective whatever intervention would ultimately be.

From July 22:

The yuan has suddenly, right at the March FOMC meeting, gone limp. Trading has been confined, except for very brief, intraday outbursts, to an increasingly narrow range. Given its behavior particularly as a full part of the reform agenda to that point, this amounts to what can only be hidden and inorganic factors. Whether that means PBOC intervention is unclear, though suggested by even TIC, but this is the most important and unexplained dynamic in the “dollar” world at present.

Perhaps the June TIC updates will help shed some light on what has been going on with China’s “dollar short”, but I doubt it. The nature and especially the scale of what might be happening in the money markets has global implications, and may (conjecture on my part) start to explain the reversal in the Chinese stock bubble and ultimately even relate to the “dollar’s” renewed disruption in July so far.

Earlier July 8:

It’s not enough to notice how this [zero yuan volatility] is odd, as it appears, given wider circumstances, to be almost odd with a purpose. Whenever uncertainties grew about China’s reform, especially “allowing” defaults, “dollar” supplies tightened significantly and the yuan devalued. Given the fragility of the current situation, you can understand why, possibly, the PBOC might not want too much to get so far out of hand and so they may be supplying “dollars” to maintain orderly money markets both onshore and off. Given the plunge in import activity they may not really need to supply all that much, particularly in combination with prior and intended outflows as they effectively tried to chase speculators out of the country. Perhaps they did too much?

Whatever the case may ultimately be, it bears close scrutiny for several reasons. First, if this is correct (a very big “if”) then the financial system in China is worse, far worse, than it appears. Second, central bank attempts such as this are extremely finite as they are, over time, hugely inefficient. The PBOC might just be throwing everything in its arsenal at the financial system short of open “flood” declarations (which are themselves destabilizing; declaring an open emergency is as much confirmation of how bad everything is) trying to calm everything down in order to reassess. [emphasis added]

That is why the PBOC would seemingly “allow” devaluation one day and then act against it the very next. They are just trying to hold on for dear life, managing imbalances that are beyond their grasp.That is what occurred last night, as the Wall Street Journal confirms that Chinese banks were “selling” dollars on the PBOC’s behalf; which is, in the wholesale context, supplying“dollars.” The currency translation is just the recognition of that imbalance, which is in many forms like this kind of convertibility almost a “run.”

The PBOC then instructed state-owned Chinese banks to sell dollars on its behalf in the last 15 minutes of Wednesday’s trading, according to people close to the state banks.

The central bank took it as far as it could and then the “dollar” dam just burst on really bad economic data that was expected instead to confirm the bottom.At this point, it looks like they are left only to try to mitigate the damage they had been for five months hoping would never occur as the global economy was supposed to have healed on its own long before then (which was nothing more than FOMC and orthodox pipe dreams).

Another central bank has fallen prey to thedecomposing “dollar”, as the global tremors of such central bank upsets ripple further and further.

end

Both ECB And BOJ Warn More QE May Be Response To Chinese Currency War

Minutes from the ECB’s most recent policy meeting reveal that Mario Draghi and company have a number of concerns about the pace of economic growth in the euroarea and about the outlook for inflation which, much to the governing council’s surprise, “remains unusually low.”

Board members also took note of increasingly volatile EGB markets and made special mention of the second bund VaR shock which took place at the first of June, something the central bank attributes to “overvaluation [and] one?way market positioning related to the public sector purchase programme.” In other words: “our bad.”

The bank gave itself the now customary pat on the back for the “success” of PSPP noting that the “moderate frontloading of purchases” (a reference to the effective expansion of QE that was leaked to a room full of hedge funds at an event in May) was going smoothly, other than the above-mentioned nasty bout of extreme volatility.

As for the economy and inflation, well, that’s not going so hot. “Overall, the recovery in the euro area was expected to remain moderate and gradual, which was considered disappointing from both a longer-term and an international perspective [while] consumer price inflation had remained unusually low.”

Between that rather grim assessment and the comments cited above regarding volatility, one is certainly left to wonder what it is exactly about PSPP that’s going so “smoothly.”

But as interesting as all of that is (or isn’t), the most compelling comments were related to China. Here’s the excerpt:

In particular, financial developments in China could have a larger than expected adverse impact, given this country’s prominent role in global trade.

Consider that, and consider the following statement sent to Bloomberg by an adviser to Japanese PM Shinzo Abe:

If [the Chinese move to devalue to yuan] suppresses external demand in Japan too much, the BOJ may further relax monetary policy.

Clearly, the ECB meeting took place ahead of China’s FX shocker, so the governing council’s reference to “financial developments in China” likely referred to the stock market collapse that was unfolding at the time, but the takeaway is the same: if developments in China’s financial markets serve to further undercut Japan and Europe’s quest to boost growth and stoke inflation (i.e. if China succeeds in exporting its deflation to trading partners), more QE and more easing will be just around the corner.

The yuan devaluation will cause emerging market currencies to crash anywhere from 30 to 50% so says economist Jen. This is the fellow that accurately predicted the mess in 1997.

(courtesy zero hedge)

Emerging Market Currencies To Crash 30-50%, Jen Says

Less than 24 hours ago, we argued that although it might have seemed as though Brazil hit rock bottom in Q2 when it suffered through the worst inflation-growth mix in over a decade, things were likely to get worse still.

The country, which is also coping with twin deficits and a terribly fractious political environment, is at the center of what Morgan Stanley recently called “a triple unwind of EM credit, China’s leverage, and US monetary easing” and now that its most critical trading partner has officially entered the global currency war, all roads lead to further devaluation of the faltering BRL.

And it’s not just the BRL. As Bloomberg reports, former IMF economist Stephen Jen (who called the 1997 Asian crisis while at Morgan Stanley) thinks EM currencies could fall by an average of 30% going forward on the back of the PBoC’s move to devalue the yuan. Here’s more:

[The] devaluation of the yuan risks a new round of competitive easing that may send currencies from Brazil’s real to Indonesia’s rupiah tumbling by an average 30 percent to 50 percent in the next nine months, according to investor and former International Monetary Fund economist Stephen Jen.

Volatility measures were already signaling rising distress in emerging markets even before China’s shock move. An index of anticipated price swings climbed above a rich-world gauge at the end of July, reversing the trend seen for most of the past six months.

“If this is the beginning of a new phase in Beijing’s currency policy, it would be the biggest development in the currency world this year,” said Jen, founder of London-based hedge fund SLJ Macro Partners LLP. “The emerging-market currency weakening trend is now going global.”

Latin America is a particular concern because of the region’s high levels of corporate debt, said Jen

Jen recommends selling the real, rupiah and South African rand — all currencies of commodity exporters, which rely on China for a large chunk of their foreign earnings.

As well as the drop in raw-materials prices, the prospect of higher interest rates in the U.S. has also drawn away investment, pushing a Bloomberg index of emerging-market exchange rates down 20 percent in the past year. A Latin American measure headed for its 13th monthly loss out of 14, while an Asian gauge plunged Tuesday to its lowest in six years.

And a bit more color from WSJ:

If China’s devaluation deepens, pressure to weaken currencies could become particularly intense in other Asian nations that export large amounts to China or compete with Beijing in other markets. Asian currencies tumbled on Tuesday, notably the South Korean won, Australian dollar and Thai baht, as investors bet China’s move could lead to further monetary easing in those nations. Many Asian nations have cut rates this year and could be forced to take further action in coming months.

“A new theme has emerged—one of Asian currency weakness,” said Wai Ho Leong, an economist in Asia at Barclays.

To be sure, it’s all down hill from here, and on that note, we’ll reprise our conclusion from last week’s “Emerging Market Mayhem” piece: Between an inevitable (if now delayed) Fed hike, stubbornly low commodities prices, the entry of the world’s most important economy into the global currency wars, and, perhaps most importantly from a big picture, long-term perspective, a seismic shift in the pace of global demand and trade, we could begin to see a wholesale shift in which the markets formerly known as “emerging” quickly descend into “frontier” status and after that, well, cue the “humanitarian aid” packages.

* * *

Here’s a look at the damage since Monday, right before the devaluation:

PBoC Falls On Yuan Grenade With “Forceful” Overnight Presser

“These comments may give some comfort but it does feel there’s a lot more to come on this story over the weeks ahead.”

That’s from Deutsche Bank’s Jim Reid and the reference is to a “forceful” PBoC press conference held overnight at which China’s central bank attempted to manage expectations after sparking a panic earlier this week with a “surprise” move to devalue the yuan.

Since then, it’s been carnage in the EM FX markets and every strategist from New York to Beijing has scrambled to figure out the read-through for the Fed in September.What’s fairly obvious to everyone now (and what’s been very clear to us all year), is that China had no choice but to devalue. A string of policy rate cuts hadn’t succeeded in boosting the export-driven economy and keeping the yuan pegged to the strong dollar had led to REER appreciation on the order of 15% in the space of a year.

Between the pace of the three-day plunge and rampant accusations that Beijing entered the global currency wars solely to export China’s deflation and prop up the economy, the PBoC had apparently seen enough. Cue an ad hoc presser.

Here’s Goldman with the summary:

The PBOC press conference held this morning followed the recent sharp sell-off of the RMB as well as heightened market uncertainty about the implications of the reform to the CNY fixing mechanism introduced on August 11. It was attended by Deputy Governor Yi Gang and Assistant Governor Zhang Xiaohui.

The PBOC officials said that the main reasons for the reform are the need to correct the pent-up misalignment of the exchange rate (including from depreciation pressure created by a period of loose liquidity conditions) and the structural goal of transitioning the previous de-facto USD peg to a managed floating rate system. Notably, they did not mention the need to boost growth as a main reason, and also particularly ruled out the need to stimulate exports through a large (10%) depreciation.

Importantly, while the officials said that they would not comment on what the equilibrium exchange rate level is, they said that the misalignment had been about 3%, citing “market survey and analysts’ general estimate” (although it is not known who was covered in the sample), and the roughly 3% depreciation since August 11th has already largely removed this misalignment (it is unclear what the 3% depreciation referred to, but possibly the closing spot rate yesterday vs. the closing spot rate on the 10th). They emphasized that solid fundamentals (e.g., strong trade surplus, abundant FX reserves) would continue to support the currency, and they expected the exchange rate would remain on a broad appreciation path in the future. They reiterated their long-term objective of increasing the market-orientation of the CNY regime.

We think the clearest signal from the statements is that further sharp CNY weakening has become much less likely. While we think they will continue to follow closely the new fixing mechanism (i.e., setting CNY fixing close to the closing spot price of the previous day), the PBOC will now likely start relying more on open FX operations as needed to manage market expectations and curb large depreciation in the near term. The strong policy guidance from today’s press conference, though, may in any case help reduce the need for FX operations for expectation management going forward. Coincidentally, it is interesting to note that the spot exchange rate appreciated suddenly by about 0.5% and converged to the fixing around the beginning of the press conference, although it is not known whether it was a result of PBOC operations or market’s reaction to the PBOC’s statements. We think it is likely that from this point on, the principle of maintaining a broadly stable CNY NEER will be a main (but not the only) factor guiding the USDCNY movement.

Regarding domestic monetary conditions, the officials emphasized that liquidity is ample and interest rates are stable. We think that signals against a major reduction in interbank interest rates. We think, however, broad RRR cuts are still likely, especially as they would be an effective way to replace the liquidity drain related to possible PBOC’s FX operations in recent days (and potentially days ahead).

So in other words, the PBoC will continue to intervene as they did on Wednesday and Thursday in the event the effort to devalue causes the market to become “distorted”, and because intervention comes at a cost to liquidity, Beijing will in all likelihood cut RRR for a fourth (and then fifth) time this year.

Below, find a bit of further color on the presser and some commentary on broader implications from Bloomberg and UBS.

From Bloomberg:

The main economic benefit of a weaker yuan is restored competitiveness for exports, a sector that continues to add up to more than 20 percent of GDP. Even so, a large-scale export rebound will happen only with a lag and only if depreciation is more significant than seen in the last few days. Our calculations suggest 10 percent depreciation in China’s real effective exchange rate could add 10 percentage points to export growth, with a lag of three months. At its press conference yesterday, the PBOC was dismissive of the idea that this is what it is targeting.

There are also costs to depreciation. Most obvious is the risk of capital flight. Our estimates suggest that 10 percent depreciation against the dollar would risk capital flight of some $400 billion. China’s leaders likely calculate that set against their $3.65 trillion foreign exchange stash, that’s a risk they can handle. A weaker yuan will also reduce the appeal of domestic assets, potentially dealing a further blow to equities and to the nascent recovery in the real estate sector.

From a UBS Q&A:

Question: Will the weakening of the RMB lead to greater capital outflows from China? Could you give me your view on capital outflows?

Answer: One of the reasons that the authorities don’t want the currency to move too fast is that it might generate its own momentum, encouraging capital outflows. I don’t think that’s something the authorities would want to encourage. So, in other words, the process will be managed so that it doesn’t generate significant capital outflows.

I think capital outflows would really depend on the trajectory of currency depreciation. The local A-share market has lost its charm to many domestic investors. It means capital outflows are, I think, kind of inevitable. But massive capital flight could only happen when currency depreciation is very sharp. In such a case, not only will domestic investors convert RMB to foreign currencies, but many global companies will also repatriate their cumulative profits back home. They have operated in China for years but, due to capital account restrictions, usually select to harbor most profits in China. So if – only if RMB depreciates suddenly by 10% or more, would I expect these multinational companies to start repatriating capital.

My guess is that very sharp depreciation, like 10% within one or two quarters, will trigger serious capital flight.

Question: I have a number for capital flow: for every one percentage point of RMB depreciation, the impact on capital outflow would be about $40 billion so I just want to know whether this number is roughly correct. And also, for every 100 basis points RRR cut, what would be the liquidity injection to the domestic market?

Answer: Capital outflow has definitely increased since mid last year, partly driven by expectations of RMB depreciation and one important mechanism of that was the unwinding of foreign exchange liabilities that was built up in the previous episode of strengthening RMB expectations. When everybody was expecting RMB to appreciate, people borrowed from offshore or basically gained FX exposure offshore to bring the liquidity home. A lot of that was short term, trade credit and so on. Now, with expectations changing, this is reversing. But, as of second quarter, this outflow had actually started to stabilize; outflows are no longer that big. So as for your question – how much will this trigger? I don’t think you can have a one on one relationship of 1% depreciation leading to $40 billion; that’s probably some correlation based on short term data rather than causality.

Directional wise, depreciation could become entrenched if people expect further depreciation, now that could actually facilitate further outflows, even if that took place in just companies paying down their foreign debt more quickly. So that could happen and that’s why we say, directional wise, it could tighten domestic liquidity. The Central Bank, of course, can use various liquidity facilities, including RRR cuts, to offset it. A 100 basis point cut in RRR would release liquidity of 1.2–1.3 trillion RMB.

Question: In terms of the export sensitivity, for every 1% of RMB depreciation, what would be the positive uplift for exports?

Answer: On the price elasticity of China’s exports – many people have done estimates on that and generally they take it as one on one, meaning that a 10% depreciation leads to a 10% change in export price, that leads to a 10% change in exports. However, it’s very much up to the exporters in how much they transmit that exchange rate movement to their pricing. For example, in the past, we have noticed that they don’t pass all exchange rate appreciation through into more expensive prices. They pass on only part of it, which means that they actually squeeze their own margins. So in this respect, when China’s currency depreciates, they could do something similar to widen their own margins, rather than completely passing on cheaper Chinese export prices to consumers.

On the benchmark – as I said, if Chinese exporters pass on all depreciation effects it could translate into a 1% uplift for exports, but in reality it will probably be more like 0.5%. So a 1% depreciation, could help 0.05% of exports.

Question: Could you actually shed some light on the impact of the weaker Chinese yuan on the prices of commodities, such as coal, natural gas and oil, maybe?

Answer: So on the linkage to commodity prices, I think the biggest driver of commodity prices, of course, are China’s demand and their supply situation. That said, I think if the Chinese currency weakens to the extent that demand from other countries for commodities will also weaken, this will be considered as somewhat of a negative.

Question: What will be the impact of the weaker Chinese yuan on domestic interest rates?

Answer: As I mentioned, we don’t think it would inhibit another rate cut. Traditionally people would say that because the Fed is about to raise rates and because its currency is weakening, the Chinese government may not have much room left to cut rates. But in our view, actually, given that: the domestic economy needs help and that the real interest rate level is still very high domestically; the government still retains some control on capital flows; and inflation is still very low — I think they still have room to cut.

Greeks Ditch Euro For Alternative Currencies As Parliament Votes On Bailout

Greece released a bit of amusing econ data on Thursday, as the country’s statistical authority claimed GDP grew by 0.8% in Q2, well ahead of estimates of a 0.5% contraction. While we suppose it’s feasible that things weren’t as bad in Q2 as they have been since (capital controls weren’t in place during the quarter), we think you’d be hard pressed to find anyone in Greece who thought things were looking up for the economy heading into the referendum. In any event it doesn’t matter, because as WSJ notes, the fiscal retrenchment enshrined in the country’s third bailout program combined with the generally poor outlook means Greece faces a two-year recession – at least:

Greece faces two years of recession amid sharp budget cuts and overhauls mandated by its €86 billion ($95 billion) bailout agreement, European Union officials said, as Greek Prime MinisterAlexis Tsipras expressed confidence that the deal would be completed.

The country’s economy is expected to shrink 2.3% this year because of the recent months of turmoil and the cuts required by the bailout, the officials said, citing the latest estimates from the institutions that have been negotiating Greece’s new aid program. Next year, it is projected to contract 1.3%.