Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1118.60 up $5.70 (comex closing time)

Silver $15.30 up 9 cents.

In the access market 5:15 pm

Gold $1117.30

Silver: $15.34

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a poor delivery day, registering 0 notice for nil ounces Silver saw 0 notices for nil oz

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 227.62 tonnes for a loss of 75 tonnes over that period.

In silver, the open interest fell by 364 contracts as silver was down in price by 18 cents on Friday. The total silver OI continues to remain extremely high, with today’s reading at 174,507 contracts In ounces, the OI is represented by .872 billion oz or 124% of annual global silver production (ex Russia ex China). This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end as they continue to raid as basically they have no other alternative.

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rests tonight at 431,081. We had 0 notices filed for nil oz today.

We had no changes at the GLD today / thus the inventory rests tonight at 671.87 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. I thought that 700 tonnes is the rock bottom inventory in GLD gold, but I guess I was wrong. However we must be coming pretty close to a level of only paper gold and the GLD being totally void of physical gold. In silver, we had no changes in silver inventory at the SLV tune of / Inventory rests at 324.968 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by 364 contracts down to 174,507 as silver was down 18 cents in price with respect to Friday’s trading. Again, we must have had some short covering. The OI for gold fell by 932 contracts to 431,081 contracts as gold was down by $2.80 on Friday. We still have close to 19 tonnes of gold standing with only 15.206 tonnes of registered gold in the dealer vaults ready to satisfy that which stands.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. Seven stories on China devaluing their yuan and how this will lead to a huge deflation throughout the globe and also discussing the ramifications of the toxic explosion in Tianjin.

(zerohedge,David Stockman,Raul Meijer/UKtelegraph/John Ficenec/)

5 Trading of equities/ New York

(zero hedge)

6. Two oil related stories

(zero hedge)

7. Stories on Brazil and Turkey

(zero hedge)

8. Explosion in Central Bangkok,Thailand

9. USA stories:

i Huge collapse in the Empire Manufacturing index

ii American Malls in total meltdown

(Jim Quinn)

Physical stories:

i) 56 tonnes of gold demand into China

(Lawrence Williams/mineweb)

ii) Gold imports and exports out of the USA

(Steve St Angelo/SRSRocco report)

iii) Silver Report chart

showing deficit of 930 million oz of silver

(Steve St Angelo/SRSRocco report)

iv)

Let us head over and see the comex results for today.

August contract month:

initial standing

August 14.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 32.15 oz (Manfra/1 kilobar) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 contract (nil oz) |

| No of oz to be served (notices) | 2123 contracts (212,300 oz) |

| Total monthly oz gold served (contracts) so far this month | 3824 contracts(382,400 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 552,940.1 oz |

Total customer deposit: nil oz

JPMorgan has 7.1966 tonnes left in its registered or dealer inventory. (231,469.56 oz) and only 741,358.273 oz in its customer (eligible) account or 23.05 tonnes

We lost 379 contracts or an additional 37,900 ounces will not stand for delivery. Thus we have 18.497 tonnes of gold standing and only 15.206 tonnes of registered or dealer gold to service it. today we must have had considerable cash settlements.

August silver initial standings

August 14 2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 882,484.03 oz (Brinks,CNT,HSBC) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 16 contracts (80,000 oz) |

| Total monthly oz silver served (contracts) | 59 contracts (295,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 85,818.47 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 7,424,066.4 oz |

Today, we had 0 deposits into the dealer account:

total customer deposits: nil oz

total withdrawals from customer: 882,484.02 oz

we neither lost nor gained any silver ounces standing in this non delivery month of August.

August 12./ a huge deposit of 4.18 tonnes of gold into the GLD/Inventory rests at 671.87 tonnes

August 7./no change in gold inventory at the GLD/Inventory rests at 667.93 tonnes August 6/no change in gold inventory at the GLD/Inventory rests at 667.93 tonnes August 5.we had a huge withdrawal of 4.77 tonnes from the GLD tonight/Inventory rests at 667.93 tonnes

August 4.2015: no change in inventory/rests tonight at 672.70 tonnes

And now SLV:

August 17.2015: no changes in inventory at the SLV/Inventory rests tonight at 324.968 million oz.

August 14/no changes in inventory at the SLV/Inventory rests at 324.968 million oz.

August 13.2013: a huge withdrawal of 1.241 million oz/Inventory rests tonight at 324.968 million oz

August 12.2015: no change in SLV inventory/rests tonight at 326.209 million oz.

August 11./ no changes in SLV inventory/rests tonight at 326.209 million oz.

August 7.no changes in SLV/Inventory rests this weekend at 326.209 million oz

August 6/no changes in SLV/inventory rests at 326.209 million oz

August 5/ a small withdrawal of 142,000 oz of inventory leaves the SLV/Inventory rests tonight at 326.209 million oz

August 4.2015: a small withdrawal of 476,000 oz of inventory at the SLV/Inventory rests at 326.351 million oz August 3.2015; no change in inventory at the SLV/inventory remains at 326.829 million oz

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

(courtesy/Mark O’Byrne/Goldcore)

Doomsday Clock Strikes One Minute To Midnight For Global Market Crash

It is only a matter of time before stock markets collapse under the weight of their lofty expectations and record valuations.

China currency devaluation signals endgame leaving equity markets free to collapse under the weight of impossible expectations.

Photo: Reuters

The Telegraph’s John Ficenec has written an excellent piece warning of a possible market crash in the coming weeks.

He identifies eight key “signs things could get a whole lot worse.”

1 – China slowdown

2 – Commodity collapse

3 – Resource sector credit crisis

4 – Dominoes begin to fall

5 – Credit markets roll over

6 – Interest rate shock

7 – Bull market third longest on record

8 – Overvalued US market

John Ficenec is a market and finance expert and is Editor of the Questor column at Telegraph Media Group working across the Daily and Sunday titles and online. He is a qualified accountant who trained at KPMG before moving into asset management and the private equity industry. He has worked in financial journalism since 2011 and joined the Telegraph in 2013. He won ‘Article of the Year’ in the 2013 CFA Society of UK awards.

As we know, a picture paints a thousand words and the article is replete with a number of excellent charts which should give even the most complacent investor pause for thought.

The convincing thesis can be read in GoldCore Commentaryhere

DAILY PRICES

Today’s Gold Prices: USD 1,117.30, EUR 1006.17 and GBP 714.34 per ounce.

Friday’s Gold Prices: USD 1,116.75, EUR 1002.11 and GBP 715.29 per ounce

(LBMA AM)

Gold in USD – 1 Year

Gold and silver gained over 2% and 3% last week. After those gains, both precious metal took a breather on the COMEX on Friday. Gold and silver were mixed – gold was flat and silver fell 1%.

This morning, gold is 0.4% higher to $1,118.60 per ounce. Silver is 0.2% higher to $15.37 per ounce.

Platinum and palladium are 0.5% and 0.2% higher to $1,001 and $623 per ounce respectively.

Download Essential Guide To Storing Gold Offshore

BREAKING NEWS

China Surprises for a Second Time This Week With More Gold Data – Bloomberg

Gold Holds Gain After Posting First Weekly Advance Since June – Bloomberg

Gold steady as focus returns to U.S. rate hike view – Reuters

Bears Miss Gold’s Best Rally Since June as Analysts See Declines – Bloomberg

China Says Gold Hoard Climbs 1.1% in Data Transparency Push – Bloomberg

IMPORTANT COMMENTARY

Doomsday Clock Strikes One Minute To Midnight For Global Market Crash – The Telegraph

Beware a China crisis that could crash down on us all – The Telegraph

How The Wall Street Ponzi Works——The Stock Pumping Swindle Behind Four Retail Zombies – David Stockman’s Contra Corner

The ‘Big Long’ Gets Bigger As Goldman And HSBC Gobble Up Tons More Gold – Seeking Alpha

Germany Continues To Lead The West In Physical Gold Demand – GoldSeek

Billionaire Stanley Drucknemiller Loads Up On Gold, Makes It His Largest Position For First Time Ever – Zero Hedge

Click on News and Commentary

end

Many follow the following gentleman: Stanley Druckenmiller:

for the first time he is buying gold:

(courtesy zero hedge)

Billionaire Stanley Drucknemiller Loads Up On Gold, Makes It His Largest Position For First Time Ever

Over the past several years, one of the biggest critics of the Fed’s ruinous monetary policy has been billionaire investor Stanley Druckenmiller, who in 2010 announcedhe would be shutting down his legendary Duquesne Capital Management, and convert it to a family office. Yet, despite his constant drumbeat of warnings that the period of ZIRP/QE/NIPR will end in tears, he had yet to put money where his mouth was (aside for a brief period in mid-2012 when we bought a lot of GLD calls, only to unwind the almost instantly).

This ended on June 30, when following Friday’s filing by the Duquesne Family Office, we learned that as of the end of Q2, the largest position for Stanley Druckenmiller was none other than gold, following the purchase of 2.9 million shares of the GLD ETF shares. In other words, as of this moment, gold amount to over 20% of Druckenmiller’s total holdings.

In a world in which starved for ideas alpha-chasers do anything and everything that billionaires report they did a month and a half ago, we wonder if this marks the end of the relentless liquidation in the GLD, which recently hit a multi-year low, as a result driving the price of paper gold to multi-year lows even as physical demand has approached record levels.

So with Druckenmiller now back and strapped in for the ride, we wonder which other prominent investor will promptly follow?

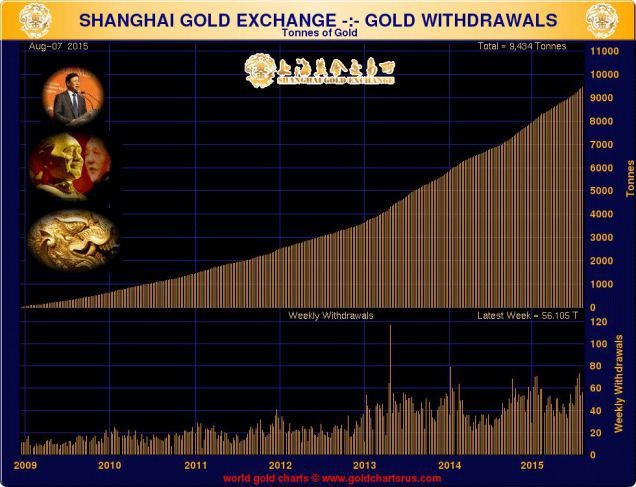

Chinese Gold Demand Still Running Extremely High For Summer Months

Contrary to some of the expressed media-disseminated information, Chinese physical gold demand, as indicated by gold withdrawals from the Shanghai Gold Exchange (SGE), remains at a very high level indeed for this time of year. The latest figure for withdrawals for the week ended August 7th was 56 tonnes, bringing the total for the year to date to a massive 1,520 tonnes. This is a full 135 tonnes higher than the previous record for Chinese gold demand at the same time of year – back in 2013.

A particular feature of this year’s SGE withdrawal figures has been the continuing strength of demand so expressed through the summer months when demand normally falls away. This year weekly demand over the period has been mostly above the 50 tonne mark – indeed it was well over 70 tonnes just three weeks ago – and this is at a time of year when 30 tonnes plus normally represents a strong demand week on the SGE! See chart below from sharelynx.com.

If one checks out the weekly withdrawals bar chart (the lower section), one can see just how strong recent movement through the exchange has been in comparison with previous years.

Interestingly, the Chinese Central Bank – the Peoples Bank of China (PBoC) – has also now started to report monthly updates in its gold reserves (see China gold reserves up 19 tonnes in July. Really?!) which could be seen as adding to overall Chinese demand, although many Western analysts are unconvinced about the accuracy of PBoC statements regarding the size of the nation’s real gold reserves.

The big question may well be has the recent devaluation of the yuan against the dollar, coupled with the admittedly fairly small gold price recovery to date, started to redress sentiment in the gold market in the West where prices are set. There is news now of some of the big bullion banks taking deliveries of physical gold on their own account, and also of shortages of registered gold available for delivery in COMEX warehouses having to be ‘rescued’ from dangerously low levels by a major reclassification of a big hunk of gold from the Eligible to the Registered category by JPMorgan. Is the tide turning at last? This could presage a very interesting second half of the year in the gold markets of the world.

********

end

THE U.S. EMPIRE INVESTMENT STRATEGY: Export All Of It’s Gold… The Barbarous Relic

by SRSrocco on August 17, 2015

As the world races towards another financial calamity, the U.S. Empire’s strategy to shield itself from this impending disaster, is to export all of its gold supply. That’s correct. The U.S. Gold Market can be explained in three simple words… ZERO SUM GAME.

This is quite a different strategy from the once great super power which held over 20,000 metric tons (mt) of official gold reserves in 1950. While the official figures now show the U.S. presently holds 8,133 mt of gold in reserve, anyone with an IQ greater than a “10”, realizes this is just an accounting gimmick. Unfortunately, most of that gold was probably dumped on the market (or leased) to help cap and rig the paper price lower.

According to the recently released USGS data, the U.S. exported every single ounce of its gold supply in April. Let’s take a look at the chart below:

U.S. gold production declined in April to 15 mt compared to 16.5 mt last year. Total U.S. gold production year to date is down a whopping 8%. When we add U.S. mine supply to imports for April, total U.S. gold supply for the month was 42 mt. Now, if we look at the total export figure, we can see the United States exported its entire gold supply. Thus, the net result was a BIG PHAT ZERO.

Again, a ZERO SUM GAME.

And, if you have been reading my articles in the past, it’s even worse than that. If we look at the total U.S. Gold Market supply and demand equation for the first four months of the year, this is the result:

Here we can see the U.S. domestic gold mine supply of 63 mt and total imports of 88 mt equaling 151 mt was less than total exports of 165 mt. Which means, the U.S. Gold Market had to cough up an addition 14 mt to satisfy demand (Jan-Apr). I did not include gold scrap supply or domestic consumption figures as these basically cancel each other out (actually Americans consume more gold than gold recycle scrap supply).

Now, why would the U.S. continue to export all of its gold supply? Well, we can certainly thank the folks on the financial networks, such as CNBC, for brainwashing Americans into believing gold is a “Barbarous Relic.”

As I stated before, you’ll never hear financial network hosts claiming that “Bread” or “Brooms” are barbarous relics. I imagine if you go to any large supermarket or home-improvement outlet you are going to find an entire shelf of bread and brooms. The Romans consumed a lot of bread and used lots of brooms, but these aren’t considered barbarous relics today.

To tell you the truth, I can’t stomach watching CNBC anymore. Some say it’s now just for entertainment. However, I think its worse than that. CNBC has been instrumental in totally destroying the ability for (most) Americans to understand the present economic and financial situation. So, when the next financial crisis finally arrives (worse than 2008), CNBC viewers will be more shocked and unprepared than ever.

Now, where did the U.S. export all of its barbarous relic (Jan-Apr)? According to the data, Switzerland received the most at 62.6 mt, followed by Hong Kong (39.6 mt), the U.K. (24.7 mt), India (19.2 mt), U.A.E. (8.7 mt), Thailand (3.9 mt) and Singapore (2.4 mt). The top four countries accounted for 88% of the total.

If we consider that most of the U.S. gold being shipped to Switzerland and the United Kingdom is being refined and exported to the East, then India and Asia are ultimately the largest importers of the U.S. gold supply. Which means, it’s nice to know that Americans are giving up their gold so Asians and Indians are better protected when the (next, even worse) financial crisis arrives. Who says Americans aren’t giving??

I will be putting out an article about the present Wholesale Silver Shortage situation in the next few days. There seems to be a great deal of misunderstanding of what this really means for the market. Please look out for this article which should be posted Wednesday or Thursday.

Lastly, if you haven’t checked out THE SILVER CHART REPORT, there’s a great deal of information on the Silver Industry & Market not found in any single publication on the internet. There is one chart in this report (Chart #19) that I can guarantee that 99.9% of precious metal investors haven’t seen before.

-END-

The following is one of Steve’s hard work in the silver arena.

He reports a deficit of 930 million oz of silver. Since there is no supply of above ground silver this silver had to come from somewhere!!

I wonder who would have supplied this much silver?

I know of no other nation other than China that could have had this much silver stored away

(courtesy Steve St Angelo/SRSRocco report/the Silver Chart Report)

The charts in these five sections give the investor a broad background of the silver industry and market. Silver will likely be one of the most sought-after physical assets in the future. Why? There are several factors that will impact its price (value) in the future, and they are explained thoroughly in The Silver Chart Report.

One factor is the huge cumulative global silver deficit developed over the past decade. Basically, the world invested and consumed a lot more silver than total global output. How large was the silver deficit? This answer can be found on one of the charts in The Silver Market section of the report, and here’s a sample:

The global silver market suffered annual deficits nine out of 10 years reaching a staggering 930 million ounces over the past decade. To fill this large deficit, silver was supplemented by government and private stocks. The report shows how government silver sales have plummeted since 2005 and why China refuses to sell anymore of its official silver stocks.

The global silver market suffered annual deficits nine out of 10 years reaching a staggering 930 million ounces over the past decade. To fill this large deficit, silver was supplemented by government and private stocks. The report shows how government silver sales have plummeted since 2005 and why China refuses to sell anymore of its official silver stocks.

(courtesy Bill Holter/SGT report)

1 Chinese yuan vs USA dollar/yuan falls slightly this time to 6.3946/Shanghai bourse: green and Hang Sang: red

Surprisingly, last week, officially, China added another 19 tonnes of gold to its official reserves now totaling 1677.

2 Nikkei up 10081. or 0.49%

3. Europe stocks mostly in the green /USA dollar index up to 96.79/Euro up to 1.1085

3b Japan 10 year bond yield: remains at 39% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 124.56

3c Nikkei still just above 20,000

3d USA/Yen rate now just above the 124 barrier this morning

3e WTI 41.99 and Brent: 49.20

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund slightly rises to .65 per cent. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate falls to 10.26%/Greek stocks this morning up by 0.84%: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield falls to : 9.41%

3k Gold at $1116.40 /silver $15.25

3l USA vs Russian rouble; (Russian rouble down 6/10 in roubles/dollar) 65.52,

3m oil into the 41 dollar handle for WTI and 49 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9779 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0838 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving further from negativity to +.65%

3s The ELA remains at 90.4 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.17% early this morning. Thirty year rate below 3% at 2.82% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Flat As Oil Drops To Fresh 6 Year Low; EM Currencies Crumble Under Continuing FX War

It was a relatively quiet weekend out of China, where FX warfare has taken a back seat to evaluating the full damage from the Tianjin explosion which as we reported on Saturday has prompted the evacuation of a 3 km radius around the blast zone, and instead it was Japan that featured prominently in Sunday’s headlines after its Q2 GDP tumbled by 1.6% (a number which would have been far worse had Japan used a correct deflator), and is now halfway to its fifth recession in the past 6 year,underscoring Abenomics complete success in destroying Japan’s economy just to get a few rich people richer. Of course, economic disintegration is great news for stocks, and courtesy of the latest Yen collapse driven by the bad GDP data which has raised the likelihood of even more Japanese QE, the Nikkei closed 100 points, or 0.5% higher.

Chinese stocks also rose by 0.7% to just shy of 4000 as a result of margin debt soaring once more, rising by $13 billion, and the longest streak in 2 months. What else can one say about Chinese investors except that they sure learned their lesson.

And while markets are levitating around the globe, if not so much in the US for now where futures are just fractionally in the red, which we expect will change in the now patented volumeless levitation into the market open and then close, economies are grinding to a halt, as expressed by the price of WTI, which earlier today dropped to a fresh 6 year low below $42 after Iran said OPEC production may rise to a record after sanctions on the

country are lifted and as U.S. drilling activity increased, although the black gold has since recouped some of its losses following unconfirmed reports of an explosion in Kuwait’s Shuaiba refinery.

Also confirming yet again just how clueless economists really are, is the following chart from the WSJ showing that at no point in the last 12 months did economists expect oil to drop as low as it is today.

A closer look at Asian equities reveals a mixed picture despite a positive Wall Street close on Friday amid light news flow. ASX 200 (+0.16 %) traded in positive territory following a bout of strong earnings, the Nikkei 225 (+0.49%) rose as participants shrugged off disappointing Q2 GDP figures as this increases calls for further measures by Japanese authorities. Chinese bourses began the week on the back foot after posting its strongest week of gains in 2-months, as the region was dragged lower by energy names. JGBs fell amid strength in equities coupled with the BoJ refraining from conducting its massive JGB purchase program. IMF forecasts China economic growth to slow to 6.8% in 2015 and 6.3% in 2016 but see more sustainable growth. There were also comments from PBoC’s Jun that China is likely to hit its target of 7% growth.

Stocks in Europe failed to hold onto the opening best levels and heading into the North American session are seen mixed, with the FTSE-100 index under performing, as the ongoing commodity market rout continues to take its toll on energy and materials sectors. The consequent retreat in stocks, in part driven by the uncertainty over the future growth prospects in China, as evidenced by the latest IMF growth forecasts.

In terms of Greek related news flow, ECB’s Coeure said rules that prohibit the buying of Greek bonds could be scrapped, while German Chancellor Merkel said there cannot be a Greek debt haircut but added there’s room for an extension of Greek debt maturities.

EUR/GBP held onto the 50% retracement level of Aug 5th low to Aug 12th high in early European trade, before the upside traction by EUR/USD towards the sizeable 1.1100 option strike saw the cross stage a recovery back into minor positive territory. At the same time, GBP failed to benefit from somewhat hawkish comments by BoE’s Forbes who said that a rate hike is needed ‘well before’ inflation reaches 2%, while departing BoE member Miles said that the case was building for a rise in Bank rate despite current low inflation.

More importantly, the EM currency war continues apace, as confirmed by headlines such as these:

- TAIWAN DOLLAR FALLS TO WEAKEST SINCE NOV. 2009

- INDIA’S RUPEE DROPS TO LOWEST LEVEL SINCE SEPT. 6, 2013.

- TURKISH LIRA DROPS TO RECORD 2.85 PER DOLLAR, DOWN 0.6% TODAY

Expect many more fireworks as everyone joins in the race to debase. Yes, here’s looking at you Janet Yellen…

Commodity prices remained under pressure, with copper prices falling amid subdued sentiment towards growth prospects in China, while Japan also posted weak data. Elsewhere, Dalian iron ore prices fell nearly 1% as demand from Chinese steel mills are said to weaken. While analysts at Goldman Sachs expect iron ore to lose 30% over the forthcoming 18-months. Despite the bearish sentiment towards commodity complex, analysts at Morgan Stanley believe that the slump in commodities following China’s devaluation may be overstated. Brent crude futures outperformed WTI following reports that an explosion has been witnessed at Kuwait’s Shuaiba refinery, damage to the site is unclear.

In summary: European stocks rise with euro falling vs dollar. U.S. equity index futures fall, with Asian stocks also declining. Gold, silver gain with corn and wheat while copper, cotton decline. WTI crude dropped as much as 2%. Yields on European 10-year notes fall, with those on Greek, Spanish, Italian bonds falling most. French, Italian bourses outperform in Europe, with FTSE 100 underperforming. U.S. Empire manufacturing, net TIC flows, NAHB housing market index due later.

Market Wrap

- S&P 500 futures down 0.1% to 2087

- Stoxx 600 up 0.4% to 387.7

- US 10Yr yield down 3bps to 2.17%

- German 10Yr yield down 3bps to 0.63%

- MSCI Asia Pacific down 0.4% to 137.8

- Gold spot up 0.2% to $1117.4/oz

- Eurostoxx 50 +0.5%, FTSE 100 -0.3%, CAC 40 +0.5%, DAX +0.4%, IBEX +0.3%, FTSEMIB +0.4%, SMI +0.3%

Asian stocks fall with the Shenzhen Composite outperforming and the Taiex underperforming; MSCI Asia Pacific down 0.4% to 137.8 - Nikkei 225 up 0.5%, Hang Seng down 0.6%, Kospi down 0.8%, Shanghai Composite up 0.7%, ASX up 0.2%, Sensex down 0.5%

- Cargill to Buy Ewos for EU1.35b, Enter Salmon Market

- Goldman Said to Buy $150m Minority Stake in Piramal Realty: WSJ

- Euro down 0.29% to $1.1077

- Dollar Index up 0.32% to 96.83

- Italian 10Yr yield down 5bps to 1.77%

- Spanish 10Yr yield down 4bps to 1.97%

- French 10Yr yield down 4bps to 0.94%

- S&P GSCI Index down 0.8% to 362

- Brent Futures down 1.5% to $48.5/bbl, WTI Futures down 1.9% to $41.7/bbl

- LME 3m Copper down 0.7% to $5131/MT

- LME 3m Nickel up 0.3% to $10630/MT

- Wheat futures up 0.2% to 512.8 USd/bu

Bulletin headline summary from Bloomberg

- Treasuries gain overnight, volumes light amid summer holidays; data this week include consumer prices and FOMC minutes, both on Wednesday.

- Oil resumed its decline, with futures sliding as much as 2%, as Iran said OPEC production may rise to a record after sanctions on the country are lifted and as U.S. drilling activity increased.

- Senior Greek bank bonds tumbled after Eurogroup President Dijsselbloem said on Friday depositors will be shielded from any losses resulting from the restructuring of the nation’s financial system

- Merkel said she’s confident the IMF will join Greece’s third bailout and signaled willingness to consider debt relief to help make it happen

- China’s economy is growing more slowly than official data suggests and below potential, a Bloomberg survey indicates, helping explain why policy makers have stepped up stimulus and the move to boost exports with a weaker yuan

- China is planning to unveil a plan as early as this week to overhaul the way state-run companies operate and are regulated, according to people familiar with the matter

- Sovereign 10Y bond yields mostly lower. Asian, Europeanstocks mixed, U.S. equity-index futures decline.Crude oil and copper lower, gold gains

DB’s Jim Reid concludes the overnight wrap

In 18 years time we’ll reach our ‘china anniversary’ which is the only way I could think to link this into the most important story running at the moment. It’s been a quiet overnight session but it feels to us that the full ramifications of last week’s China move will take time to reverberate and might actually be out of China’s hand. For all their talk on Thursday last week about keeping the Yuan ‘basically stable’ and it being ‘groundless’ to talk of a 10% devaluation they have set off a chain of events around the world. They are continuing to try to ease fears with the PBoC’s chief economist and ex-DB economist Jun Ma yesterday suggesting that China has “no intention or need to participate in a currency war”. Well that might depend on how Europe, Japan, the rest of Asia and even the Fed respond to the move. If they ease policy further or in the Fed’s case keep policy looser than it would have been then China’s exchange rate may naturally appreciate again which may encourage further depreciations periodically at their daily fix. So maybe they’ve now lit the touchpaper and we’ll see how others react.

Overnight the PBoC made little change (+0.01%) to the Yuan fix, resulting in a modest fall for the onshore Yuan (-0.06%) but a slight strengthening for the more freely traded offshore Yuan (+0.18%). In a note on Friday, DB’s Zhiwei Zhang believes that this round of rapid RMB depreciation has come to an end. On the back of the moves however, Zhiwei has updated his USD/CNY forecasts and now expects the exchange rate to be around 6.5 by the end of 2015 (from 6.3) and 6.9 by the end of 2016 (from 6.5) but with high volatilities expected in both direction. Despite the expectation of depreciation in the currency however, Zhiwei does not think this alone will generate a visible impact on exports or overall growth and continues to forecast one more interest rate cut this year, as well as an RRR cut this year and next.

Even with the steady overnight fix, there’s been further weakness across the Asia FX space again with the Malaysian Ringgit (-0.62%) and Indonesian Rupiah (-0.65%) in particular suffering a sell off, the former in particular extending a slump which saw it plummet nearly 4% last week. There was plenty of concern in the weekend press about the Ringgit and the country’s dwindling reserves. Parallels to 1997/8 are being drawn. Capital controls were introduced in 1998 after a 30% FX decline. We are at 24% declines over the last year.

Looking at the rest of market moves this morning, Chinese equity markets have started the week on the back foot with the Shanghai Comp (-0.12%) and CSI 300 (-0.46%) both down at the midday break (although paring earlier heavy losses), while the Hang Seng (-0.99%) and Kospi (-0.38%) have also declined this morning. The ASX is +0.38% while the Nikkei has risen 0.20% after Japan, although soft, reported a slightly better than expected preliminary Q2 GDP report (-0.4% qoq vs. -0.5% expected), resulting in an annualized 1.6% yoy contraction (vs. -1.8% expected). Elsewhere, in the commodity space WTI (-1.41%) and Brent (-1.32%) have tumbled in early trading not helped by the latest Baker Hughes data showing an increase in the number of operating rigs in the US last week for the fourth straight week.

After the choppiness in markets for most of last week, Friday’s trading saw a much calmer session for the most part after the PBoC’s much more muted move in the fix, resulting in a 0.11% gain for the Yuan and halting the three-day selloff. European equities finished a tad lower after some softer than expected GDP reports while US equity markets firmed slightly, supported in some part by Greece headlines confirming Eurogroup approval of a third bailout programme which filtered through in the late afternoon. The S&P 500 closed up 0.39% along with gains for the Dow (+0.40%) and NASDAQ (+0.29%), while in Europe we saw the Stoxx 600 (-0.12%) and DAX (-0.27%) finish a touch weaker. Despite some weakness in energy stocks, it was actually a relatively more benign day of price action in the commodity complex with Brent (-0.89%) and WTI (+0.64%) mixed, Gold (0.00%) ending unchanged, Copper (-0.39%) slightly lower and Aluminum (+0.41%) a tad higher.

US rates markets saw yields tick up slightly in the afternoon session as the US data flow rolled in, although again the price action was reasonably muted. The benchmark 10y yield finished 1.2bps higher at 2.199%, while 2y yields closed up 1.4bps to 0.724%. The Dollar had a much more choppy session however, with the Dollar index firming +0.08% at the close. On the inflation front, July PPI rose +0.2% mom in July (and ahead of market expectations of +0.1%) but saw the annualized rate tick lower to -0.8% yoy (from -0.7%). The core firmed greater than expected (+0.3% mom vs. +0.1% expected), but again the annualized rate nudged down, declining two-tenths to +0.6% yoy. Industrial production (+0.6% mom vs. +0.3% expected) and manufacturing production (+0.8% mom vs. +0.4% expected) were both stronger than expected in July, however both saw downward revisions to prior month reports while capacity utilization was in-line with expectations at 78%. Finally, the first reading of the University of Michigan consumer sentiment reading declined a fairly modest 0.2pts from July to 92.9 (vs. 93.5 expected) with the expectations reading in particular dropping 0.3pts to 83.8 after forecasts for a rise to 85.0. Despite the slight nudge up in yields, the probability of a Fed rate move edged down slightly at Friday’s close to 48% from 50%, a range it’s hovered in since last Wednesday. That’s in stark contrast to the latest WSJ survey which shows 82% of economists surveyed expect the Fed to liftoff in September, unchanged on last month and up from 72% in June.

European data flow on Friday was centered on the various Q2 GDP reports. There was some modest disappointment in the Euro area reading which came in slightly below expectations for the quarter (+0.3% qoq vs. +0.4% expected), although it was enough to see the annualized rate nudge up to 1.2% yoy and the highest since Q3 2011. Regionally we saw quarterly misses out of Germany (+0.4% qoq vs. +0.5% expected), France (0.0% qoq vs. +0.2% expected) and Italy (+0.2% qoq vs. +0.3% expected) although annual rates nudged up slightly for each country. Meanwhile, there was no change to the final July CPI report at +0.2% yoy for the headline and +1.0% yoy for the core.

With the Eurogroup approval of Greece’s €86bn bailout deal, focus will likely turn to the Bundestag vote this week where it’s expected that, although legislative approval is highly certain, German Chancellor Merkel is likely to run into dissent from fellow lawmakers.

Ahead of this and over the weekend, Merkel has expressed that she is confident that the IMF will join Greece’s third bailout program, signaling in the process that she is ready to discuss debt relief and specifically ‘leeway on the extension of maturities on interest rates’.

end

Sunday afternoon:

The huge toxic blast in Tianjin may well be a huge black swan event as the authorities have now ordered a evacuation surrounding 3 km from the contaminated site. Authorities have found sodium cyanide which if it comes in contact with water or fire can release the deadly gas Hydrogen cyanide.

What is critical is the fact that Tianjin is the major export/importing port especially iron ore. With no areas to receive imports or to export, this would have a huge dampening effect on its economy and thus expect further devaluations in the yuan.

(courtesy zero hedge)

China Sends In Chemical Warfare Troops, Orders Tianjin Blast Site Evacuation After Toxic Sodium Cyanide Found

our years ago, following the Sendai tsunami and resulting explosion at the Fukushima nuclear power plant, the Japanese government had just one goal: to minimize panic among the population, even if it meant blatantly lying about the resulting deadly radioactive fallout the public was exposed to. After all the top prerogative among government bureaucrats has always been to minimize social disturbance even if it means sacrificing countless individuals to a death that could have been avoided if only the government had told the truth from the beginning.

This was also the playbook followed by the Chinese government three days ago after the massive chemical plant explosion in China’s port of Tianjin where the casualty count is increasing with every passing day (85 dead at last check and rising fast), but where the real danger is that toxic gases and chemical fallout, just as dangerous and lethal as Fukushima’s beta and gamma waves, have spread in the air and water, and are jeopardizing the local population.

Initially the government did everything in its power to cover up the spread of deadly contaminants. As we reported yesterday, People’s Daily openly lied to the local population: “Authorities tasked with marine monitoring announced there were no hazardous chemicals detected in waters off the blast site in north China’s port city Tianjin on Friday.

A statement from the State Oceanic Administration (SOA) said major measurement of seawater composition did not show any anomaly compared with historical records.

Hazardous materials such as cyanide and volatile phenol were not detected, while the variety of zooplankton was not affected either, it added.

The problem is that the Chinese government long ago lost all credibility and as we reported yesterday, local residents “wondered if even the air was safe because of the smoke, still billowing hours later from vestiges of the inferno, which destroyed an industrial zone near the port. Many people wore masks.”

“Right now, we don’t know anything,” said Sun Meirong, 52, an office cleaner who descended 13 flights of stairs with her 1-year-old grandson after the explosions blew in her apartment windows and front door.

… According to the Tianjin Tanggu Environmental Monitoring Station, calcium carbide was one of several toxic industrial chemicals stored by the company. The others included sodium cyanide, which can produce hydrogen cyanide, a volatile and flammable liquid; and toluene diisocyanate, which can also react violently in the presence of water.

We were quite skeptical the Chinese government can maintain the charade for long: unlike radiation whose effects take years to materialize, and thus afforded the Japanese government free reign to lie to the people with impunity for years, the effect of the Chinese toxic gases manifest themselves quickly, and usually with a combustible or deadly outcome.

Which is why we were not surprised to learn that Chinese authorities ordered the evacuation of residents within a 3km radius of the Tianjin blast site “over fears of chemical contamination” according to BBC.

Replace fears with reality: the evacuation came as police confirmed the highly toxic chemical sodium cyanide was found near the site.

People sheltering at a school used as a safe haven since the disaster have been asked to leave wearing masks and long trousers, reports say.

According to a tweet by The People’s Daily, anti-chemical warfare troops have entered the site to handle highly toxic sodium cyanide which had been found there.

The discovery was confirmed by police “roughly east of the blast site” in an industrial zone, state-run Beijing News said.

What is Sodium Cyanide?

The chemical sodium cyanide is white crystalline or granular powder which can be rapidly fatal if inhaled or ingested, as it interferes with the body’s ability to use oxygen.

It is mostly used in chemical manufacturing, for fumigation and in the mining industry to extract gold and silver.

It is soluble in water, and absorbs water from air, and its dust is also easy to inhale. When dissolved or burned, it releases the highly poisonous gas hydrogen cyanide.

* * *

Which means that the lies can now end: officials have so far insisted that air and water quality levels are safe.

BBC adds that officials have also confirmed the presence of calcium carbide, potassium nitrate and sodium nitrate. Calcium carbide reacts with water to create the highly explosive acetylene.

Ironically, just like in the case of Fukushima where the government is desperately hiding the fact that there has been a core meltdown, so in Tianjin the deadly chemicals have made such a toxic mix that some fires have continued to smoulder and at least one reignited on Saturday.

Xinhua said several cars at the site had “exploded again”.

* * *

Since the port of Tianjin a critical infrastructure hub in the inbound commodity pathway, handling a substantial portion of China’s iron ore and steel supply chain, today’s evacuation and the admission that the chemical fallout from the explosion was far worse than officially admitted, means that a non-trivial component of China’s trade is about to be mothballed indefinitely.

It also means that with both imports and exports set to suffer even more following last month’s shocking prolapse, which was the sole reason for China’s currency devaluation (the justification used by some pundits that China is simply eager to gain SDR acceptance is utter nonsense: China would not reveal it is adding to its gold holdings if it intended to appease the IMF, and certainly would not intervene daily to prop up its stock market, something the “free market” IMF finds abhorrent if only publicly), and with critical logistical networks now certain to be blocked indefinitely, resulting in GDP-crushing supply chain bottlenecks, Beijing – which was eager to slowdown its Yuan devaluation on Friday in order to avoid cross-asset contagion and further selling of stocks and an acceleration of the capital outflow – will have no choice but to devalue the currency even more in the coming week as the only offset to what may have well been a true black (or rather mushroom cloud shaped) swan event, one for which neither China nor the world, had absolutely any contingency plan.

end

Sunday evening; trading in Chinese/Asian markets:

Chinese markets hold but Malaysian ringgit plummets. Japan reports a fall in GDP and thus is still in recession mode for the past 5 years:

(courtesy zero hedge)

Asian Currency Crisis Continues As China Holds, Malaysia Folds, & Japan Heads For Quintuple Dip Recession

Asia got off to an inauspicious start this evening withJapan printing a disappointing 1.6% drop in GDP – heading for its fifth recession in 6 years… so much for Abenomics, but, of course, Amari spewed forth some standard propaganda that he expects Japan to recover moderately (and Japanese stocks popped modestly assuming moar QQE). Then Malaysia continued its collapse with the Ringgit down another 1% hitting fresh 17-year lows and stocks dropping further, as the Asian Currency crisis continues. Heading into the China open, offshore Yuan signaled further devaluation but the CNY Fix printed very modestly stronger at 6.3969; and following last week’s best gains in 2 months, Chinese stocks are plunging at the open after Chinese farmers extend their streak of margin debt increases. Finally, WTI Crude drifted back to a $41 handle in early futures trading.

Asian Contagion…

Japan heads for Quintuple Dip recession…

The Asian currency crisis continues (led by Malaysia)

- *MALAYSIAN RINGGIT DROPS 0.9% TO 4.1155 PER DOLLAR

- *MALAYSIA’S KEY STOCK INDEX OPENS DOWN 0.4% AT 1,590.81

But broad-based USD strength against Asian FX continues…

Then China opened..

Great news – Chinese farmers and grandmas are releveraging!!

- *SHANGHAI MARGIN DEBT HAS LONGEST STREAK OF RISE IN TWO MONTHS

Seriously!

And Chinese futures appeared to mini-flash-crash…

As China revalues modestly..

- *CHINA SETS YUAN REFERENCE RATE AT 6.3969 AGAINST U.S. DOLLAR (against 6.3975 fix Friday)

- *PBOC’S YUAN REFERENCE RATE SET WITHIN 0.1% OF FRIDAY’S CLOSE

Offshore Yuan leaking weaker…

And finally WTI Crude continues to drift lower… once again trading with a $41 handle…

So while China may have succeeded in jawboning/intervening the yuan back to some semblance of (temporary) stability, the global reverberations look to have just begun.

Charts: Bloomberg

end

Zero hedge weighs in on what will happen in the coming months as China continues to devalue the yuan:

(courtesy zero hedge)

Why Everyone Is So Nervous About What China Does Next, In One Chart

Whether the motive behind China’s stunning August 11 devaluation announcement was to get one step closer to the SDR basket by promoting a market-based FX regime demanded by the IMF, to further ease financial conditions in China, to boost exports, or merely to telegraph to the Fed that with the US preparing to hike rates China will no longer be pegged to the USD, is unclear, but one thing that is certain is just how much everyone (if not this website) was shocked by the PBOC announcement. Goldman summarizes it best: “The sharp 3% devaluation in the CNY fix last week was a surprise to us.”

What happens next? Clearly more devaluation, or else China would not have pursued this step, especially since the paltry 4% devaluing in one week will hardly move the needle on Chinese exports, which is the real reason why China did this move (weeks after it boosted its official gold holdings by 57%). Goldman also admits as much: “It is hard to have a high degree of conviction in anticipating the increasingly fitful reactions of the Chinese policymakers, and by extension the near-term direction of the CNY. But on a longer horizon, the risks are tilted towards further CNY weakness.”

The weakness is further guaranteed when one considers that China has all but tapped out its credit capacity (where even the IMF admits China’s debt/GDP is headed to 250%), forcing the country to seek growth not from within (via credit creation), but without, in the form of beggaring its neighbors and promoting its competitiveness using external devaluation (a similar internal devaluation to what Greece has undergone in the past 5 years would result in a very violent civil war), i.e. currency war, as much as the serious people want to avoid calling it for fear headlines such as these (from overnight) will become a daily event…

- TAIWAN DOLLAR FALLS TO WEAKEST SINCE NOV. 2009

- INDIA’S RUPEE DROPS TO LOWEST LEVEL SINCE SEPT. 6, 2013.

- TURKISH LIRA DROPS TO RECORD 2.85 PER DOLLAR, DOWN 0.6% TODAY

… and the FX war will spiral out of control.And yet that is precisely what will happen.

This is how Goldman pivots to the unpleasant reality of not only China now aggressively engaging fellow exporters, but those same fellow expoerters devaluing preemptively before China gets them:

It is hard to have a high degree of conviction in anticipating the increasingly fitful reactions of the Chinese policymakers, and by extension the near-term direction of the CNY. But on a longer horizon, the risks are tilted towards further CNY weakness. The core of this argument rests on our view that China’s bumpy downshift in growth is likely to extend, making for greater macro and market volatility along the way. China has experienced a substantial credit build-up, which will need to be unwound in coming years. As Andrew Tilton and team have discussed, unwinding such a large credit imbalance is typically associated with a period of below-trend domestic demand growth, and this is coinciding with slowing potential growth as the impulses from labour and capital deepening slow. China’s current account surplus is also not what it used to be, with a growing services deficit offsetting a still large trade surplus. Given this macro backdrop, where a greater contribution to growth from net exports would be very welcome, a 25% appreciation in trade-weighted terms – as the CNY has experienced over the past three years on account of its tight link to the USD – looks increasingly untenable.

And while nobody wants to admit it, the writing on the wall is clear: the age of all out FX warfare is upon us, and only the Fed believes it is immune… if only for the time being.

The clearest implication of China joining the currency depreciation train is that it further increases depreciation pressures on the rest of the EM FX complex. There are two important channels of transmission here: First, because China as a producer competes with several EMs in global markets, those EM exporters just became a touch less competitive relative to Chinese exporters; and second because China as a consumer is also a large destination for exports from the rest of EM, although in this case there is at least the possibility of a partial offset from any improvement in demand if an easing in financial conditions is delivered. So for EMs that have been trying to address their external balance, and have seen depreciating currencies since 2013, some of that relative price shift has just been undone. And if the recent CNY moves are the start of a journey, even undoing half of the accumulated trade-weighted appreciation of the last three years, this may provoke a meaningful additional bout of currency depreciation across the EM complex.

Translation: once begun, the currency war, which for the time being is being fought with conventional means, has no choice but to become nuclear.

Here, in one chart, is the reason why anyone following China’s devaluation is very nervous. And if they aren’t yet, they should be. Because if China is indeed intent on catching up with the rest of the EM complex – whose FX is trading about 30% lower – then the resulting devaluation will lead to nothing short of a global FX neutron bomb.

global FX neutron bomb.

Monday morning EST in China (evening China)

(courtesy zero hedge)

Toxic Rain Feared In Tianjin As Death Toll Rumored At 1,400

The fallout from last week’s massive explosion in the Chinese port of Tianjin continues to worsen, despite Beijing’s best efforts to play down the danger to the public.

The official death toll from the apocalyptic blast – which was described by witnesses as akin to a nuclear explosion – has risen to 114. Some reports suggest the number of people confirmed killed may ultimately rise to 1,400. Some 6,000 have been displaced and more than 700 are reported injured. “The whole sky was lit up, and the blast wave sent me into the air,” a first responder told local media, describing the scene that unfolded last Wednesday. “My helmet was gone. It was like a different world, with flames falling like raindrops on my head.”

(Harvey: the following is extremely important)

Speaking of raindrops, authorities now fear that storms in the area could transform sodium cyanide (which is water soluble) present on the scene into hydrogen cyanide. Here’s the CDC’s definition of hydrogen cyanide:

Hydrogen cyanide (AC) is a systemic chemical asphyxiant. It interferes with the normal use of oxygen by nearly every organ of the body. Exposure to hydrogen cyanide (AC) can be rapidly fatal. It has whole-body (systemic) effects, particularly affecting those organ systems most sensitive to low oxygen levels: the central nervous system (brain), the cardiovascular system (heart and blood vessels), and the pulmonary system (lungs). Hydrogen cyanide (AC) is a chemical warfare agent (military designation, AC). It is used commercially for fumigation, electroplating, mining, chemical synthesis, and the production of synthetic fibers, plastics, dyes, and pesticides. Hydrogen cyanide (AC) gas has a distinctive bitter almond odor (others describe a musty “old sneakers smell”), but a large proportion of people cannot detect it; the odor does not provide adequate warning of hazardous concentrations. It also has a bitter burning taste and is often used as a solution in water.

Tianjin’s vice mayor said “around 700 tonnes” of sodium cyanide was being stored at the facility. That’s a problem because as it turns out, the warehouse was only authorized to store around 24 tonnes.

As we noted over the weekend, China has tried its best to go by the Fukushima playbook. In short, the overarching goal is to minimize panic among the population, even if it means blatantly lying about exactly what it is that the public is exposed to. After all, the priority among government bureaucrats has always been to minimize social disturbance even if it means sacrificing countless individuals that could have been saved if only the government had told the truth from the beginning.

This mentality led China to claim last week that no hazardous chemicals had leaked into the water. That contention has come under increased scrutiny. “The closest water test point to the blast site revealed cyanide 27.4 times standards on Sunday”,AFP says. The State Oceanic Association admitted that “minute traces of cyanide have been detected in waters near the Tianjin port.” Here’s more from The Guardian:

With the official death toll raised to 112 and the number of missing people at 95, rescue workers wearing gas masks and hazard suits were racing to clear the area before the weather changes because of concerns that wind could spread the toxins and rain could cause a dangerous reaction with chemicals at the site.

Eric Liu, a campaigner at Greenpeace East Asia, said that without precise data on how much calcium carbide was involved in the blast, it was impossible to predict how serious these reactions could be.

“The other danger rain poses is that chemicals stored in warehouse could be washed into water supplies, with a potentially large impact on local ecosystems,” Liu said. “However, again, without more specific information it is difficult to say what impacts exactly.”

Meanwhile, the public is getting restless as some suspect the government of obscuring the facts and masking possible corruption. Here’s NBC again:

State media Monday carried large photographs of Premier Li Keqiang with local officials in identical whites shirt and trousers visiting the scene of massive toxic Tianjin explosions.

Li has promised a thorough investigation and punishment for those responsible — even while the authorities were busy closing down dozens of “rumor-mongering” websites for demanding pretty much the same thing.

Tianjin is tricky for the Communist Party because, according to numerous local reports, there appear to have been big regulatory and legal failures — from the type and quantity of highly toxic chemicals stored at the site to the apparent lack of an inventory and the location of such a dangerous stockpile so close to residential areas.

While the name of the company that owned the warehouse complex has been made public — Ruihai International Logistics, a four-year-old firm that employed about 70 workers — the company’s website has been taken down, as has the corporate registry database of the city of Tianjin. That has fueled online speculation that local officials were involved with the company. No evidence to that effect has been presented, but such involvement would not be unusual in China.

http://player.theplatform.com/p/2E2eJC/nbcNewsOffsite?guid=x_lon_chinaprotests_150817

And here’s The Globe and Mail:

Online, meanwhile, authorities struggled to cleanse a raging conversation that attacked the official response and the system that had allowed such a disaster to happen. Social-media users shared photos of families rallying behind a giant handwritten banner demanding an details about the missing: “Either we see them alive or see their bodies,” read one.

Anger emerged in hashtags calling the situation “A real life Pinocchio” and demanding “Tanggu explosion truth,” a reference to the Tianjin neighbourhood where the blasts left a gaping crater.

“We demand the truth, and strict punishment to comfort the victims!” wrote one person on China’s Facebook-like Weibo site.

And while citizens can “demand the truth” until they are blue in the face, they will apparently have to do so very quietly and not in a public forum, because as The Guardian goes on to note, “fifty websites have been punished for ‘spreading Tianjin blast rumours’ and close to 400 Weibo and WeChat accounts have been shut down.” So while the public will always be at an informational disadvantage in the wake of a disaster thanks to government efforts to maintain order, that goes double in China, where we imagine the suppression of online discussion will continue until the death toll and the fallout becomes so difficult to downplay that Beijing will be forced to either acknowledge the true extent of the catastrophe or face widespread social upheaval.

end

Two extremely important papers and both dealing with the devaluation of the yuan. In the first paper Meijer states that we are now at the end of the line and the game changes.

This is your most important paper this year:

(courtesy Raul Meijer)

“We’ve Reached The End Of The Line; Now, The Game Changes”

Submitted by Raul Ilargi Meijer via The Automatic Earth blog,

Eventful days in the middle of summer. Just as the Greek Pandora’s box appears to be closing for the holidays (but we know what happens once it’s open), and Europe’s ultra-slim remnants of democracy erode into the sunset, China moves in with a one-off but then super-cubed renminbi devaluation. And 100,000 divergent opinions get published, by experts, pundits and just about everyone else under the illusion they still know what is going on.

We’ve been watching from the sidelines for a few days, letting the first storm subside. But here’s what we think is happening. It helps to understand, and repeat, a few things:

• There have been no functioning financial markets in the richer parts of the world for 7 years (at the very least).Various stimulus measures, in particular QE, have made sure of that.

A market cannot be said to function if and when central banks buy up stocks and bonds with impunity. One main reason is that this makes price discovery impossible, and without price discovery there is, per definition, no market. There may be something that looks like it, but that’s not the same. If you want to go full-frontal philosophical, you may even ponder whether a country like the US still has a functioning economy, for that matter.

• There are therefore no investors anymore either (they would need functioning markets). There are people who insist on calling themselves investors, but that’s not the same either. Definitions matter, lest we confuse them.

Today’s so-called ‘investors’ put to shame both the definition and the profession; I’ve called them grifters before, and we could go with gamblers, but that’s not really it: they’re sucking central bank’s udders. WHatever we would settle on, investors they’re not.

• The stimulus measures, QE, were never designed to induce economic recovery.They were meant to transfer private losses to public purses. In that, they have been wildly successful.

• China is the end of the line. It was the only economy left that until recently could boast actual growth on a scale that mattered to the global economy. Growth stopped when China, too, introduced stimulus measures. To the tune of some $25 trillion or more, no less.

The perhaps most pivotal importance of China is that it was the world’s latest financial hope. The yuan devaluation shatters that hope once and for all. The global economy looks a lot more bleak for it, even if many people already didn’t believe official growth numbers anymore.

Because we’ve reached the end of the line, the game changes. Of course there will be additional attempts at stimulus, but China’s central bank has de facto conceded that its measures have failed. The yuan devaluations, three days in a row now, mean the central People’s Bank of China has, openly though reluctantly, acknowledged its QE has failed, and quite dramatically at that. They just hope you won’t notice, and try to bring it on with a positive spin.

Central banks are not “beginning” to lose control, they lost control a long time ago. The age of central bank omnipotence has “left and gone away” like Joltin’ Joe. Omnipotence has been replaced by impotence.

This admission will reverberate across the globe.China is simply that big. It may take a while longer for other central bankers to admit to their own failures (though ‘failures’, in view of the wealth transfer, is a relative term here), but it won’t really matter much. One is enough.

What will happen from here on in will be decided by how, where and in what amounts deleveraging will take place. This will of necessity be a chaotic process.

Debt deleveraging leads to, or can even be seen as equal to, debt deflation. This is a process that has already started in various places and parts of economies (real estate), but was kept at bay by QE programs. It will now accelerate to wash over our societies like a biblical plague.

The Automatic Earth started warning about this upcoming deflation wave many years ago. I am wondering if I should rerun some of the articles we posted over the past 8 years or so. I might just do that soon.

It is fine for people to say that since it hasn’t happened yet, we were wrong about this, but for us it was never, and is not now, about timing. If you think like an investor -or at least you think you do- timing may seem to be the most important thing in the world. But that’s just another narrow point of view.

When deflation takes its inevitable place center stage, it will wipe away so much wealth, be it real or virtual or plain zombie, that the timing issue will be irrelevant even retroactively. Whether the total sum of global QE measures is $22 trillion or $42 trillion, its deflation-driven demise will wipe out individuals, companies and nations alike at such a pace, people will wonder why they ever bothered with trying to get the timing right.

This may be hard to understand in today’s world where so many eyes are still focused on central banks and asset- and equity markets, on commodities and precious metals, on housing markets. In that regard, again, it is important to note that there have been no functioning markets for many years. Those eyes are focused on something that merely poses as a market.

For us this was clear years ago. It was never about the timing, it was always about the inevitability. Back in the day there were still lots of voices clamoring for – near-term or imminent – hyperinflation. Not so much now. We always left open the hyperinflation option, but far into the future, only after deflation was done wreaking its havoc. A havoc that will be so devastating you’ll feel silly for ever even thinking about hyperinflation.

Deflation will obliterate our economies as we know them. Imagine an economy for instance where next to no-one sells cars, or houses, or college educations, simply because next to no-one can afford any of it.

Where everything that today is bought on credit will no longer be bought, because the credit will be gone. Where homes are not worth more than the cardboard they’re made of, and still don’t sell.

Where ships won’t sail because letters of credit won’t be issued, where stores won’t open in the morning because they can’t afford their inventory even if it arrives in a nearby port.

As for today’s reality, the Chinese leadership has been eclipsed by its own ignorance about economic systems, the limits of their control over them, and the overall hubris they live in on a daily basis. These people were educated in the 1960s and 70s China of Mao and Deng Xiaoping. In the same air of omnipotence that today betrays all central bankers. Why try to understand the world if you’re the one who shapes it?!

It was obvious this moment would arrive in Beijing as soon as the one millionth empty apartment was counted. There are some 60 million ’empties’ now, a number equal to half the total US housing contingent.

Beijing then heavily promoted the stock market for its citizens, as a way to hide the real estate slump. All the while, it kept the dollar peg going. And now all this is gone. And all that’s left is devaluation. As Bill Pesek put it: “China Adds a Chainsaw to Its Juggling Act”.

Ostensibly to improve the country’s trade position, for lack of a better word. Whether that will work is a huge question. For one thing, the potential increase in capital flight may turn out to be a bigger problem than the devaluation is a solution.

Moreover, one of the main reasons to devalue one’s currency is the idea that then people will start buying your stuff again. But in today’s deflationary predicament, one of the main failures of mainstream economics pops up its ugly head: the refusal to see that many people have little or nothing left to spend.

This as opposed to economists’ theories that people must be sitting on huge savings whenever they don’t spend “what they should”. Ignoring the importance of personal debt levels plays a major part in this. Any which way you define it, the result is a drag on the velocity of money in either a particular economy, or, as we are increasingly witnessing, a major spending slowdown in the entire global economy.

Seen in that light, what good could a 1.9% devaluation (or even a, what is it, super-cubed 5% one, now?!) possibly do when China producer prices fell for the 40th straight month, exports were down 8.3% in July, and cars sell at 30% discounts? Those numbers indicate a fast and furious reduction in spending.

Which in turn lowers the velocity of money in an economy. If money doesn’t move, an economy can’t keep going. If money velocity slows down considerably, so does the entire economy, its GDP, job creation, everything.

This of course is the moment to, once again, point out that we at the Automatic Earth define deflation differently from most. Inflation/deflation is not rising/falling prices, but money and credit supply relative to available good and services, and that, multiplied by the velocity of money.

When this whole debate took off, even before Lehman, there were only a few people I can remember who emphasized the role of deflation the way we did: Steve Keen, Mike Mish Shedlock and Bob Prechter.

And Mish doesn’t even seem think the velocity of money is a big factor, if only because it is hard to quantify. We do though. Steve is a good friend, he’s the very future of economics, and a much smarter man than I am, but still, last time I looked, stumbling over the inflation equals rising prices issue (note to self: bring that up next time we meet). Prechter gets it, but believes in abiotic oil, as Nicole just pointed out from across the other room.

So yeah, we’re sticking out our necks on this one, but after 8+ years of thinking about it, we’re more sure than ever that we must insist. Rising prices are not the same as inflation, and falling prices are but a lagging effect of deflation.

Spending stops when people are maxed out and dead broke. And then prices drop, because no-one can afford anything anymore.

We’ve had a great deal of inflation in the past decade or two, like in US housing. We still have some, for instance in global stock markets and Canada and Australia housing. But these things are nothing but small pockets, where spending persists for a while longer.

Problem is, those pockets pale in comparison to diving -consumer- spending in the US, China, Europe, Japan. Spending that wouldn’t even exist anymore if not for QE, ZIRP and cheap credit.

The yuan devaluation tells us the era of cheap credit is now over. The first major central bank in the world has conceded defeat and acknowledged the limits to its alleged omnipotence.

It always only took one. And then nothing would stand in the way of the biblical plague. It was never a question. Only the timing was. And the timing was always irrelevant.

end

The second paper by Stockman basically states the same as Meijer that we will now have a complete economic and financial trainwreck due to the devaluation of the yuan. The huge deflation that will travel around the globe will devastate the world’s finances:

(courtesy David Stockman)

The Great China Ponzi – An Economic And Financial Trainwreck Which Will Rattle The World

Submitted by David Stockman via Contra Corner blog,

There is an economic and financial trainwreck rumbling through the world economy. Namely, the Great China Ponzi. In all of economic history there has never been anything like it. It is only a matter of time before it ends in a spectacular collapse, leaving the global financial bubble of the last two decades in shambles.

But here’s the Wall Street meme that is stupendously wrong and that engenders blind complacency with respect to the impending upheaval.To wit, the same folks who brought you the myth of the BRICs miracle would now have you believe that China is undergoing a difficult but doable transition –from an economy driven by booming exports and monumental fixed asset investment to one based on steady as she goes US-style consumption and services.

There may well be some bumps and grinds along the way, we are cautioned, such as the recent stock market and currency turmoil. But do not be troubled—–the great locomotive of the world economy will come out the other side better and stronger. That’s because the wise, pragmatic and powerful leaders and economic managers who deftly guide China’s version of capitalism have the capacity to make it all happen.

No they don’t!

China is not a clone-in-the-making of America’s $18 trillion consume till you drop economy—-even if that model were stable and sustainable, which it is not. China is actually sui generis—–a historical freak accident that has no destination other than a crash landing.

It’s leaders are neither wise nor deft economic managers. In fact, they are a bunch of communist party political hacks who have an iron grip on state power because China is a crude dictatorship. But their grasp of the fundamentals of economic law and sound finance can not even be described as negligible; it’s non-existent.

Indeed, their reputation for savvy and successful economic management is an unadulterated Wall Street myth. The truth is, the 25 year growth boom in China is just a giant, credit-driven Ponzi. Any fool can run a central bank printing press until it glows white hot.

At the end of the day, that’s all the Beijing suzerains of red capitalism have actually done. They have not created any of the rudiments of viable capitalism. There are no honest financial markets, no genuinely solvent banks, no market driven allocation of capital and no financial discipline which comes from the right to fail as well as succeed.

There are, for instance, 287 million equity trading accounts in China, most of them opened within the last year and overwhelmingly held by retail punters with sub-high school educations. In less than 12 months they took down upwards of $1 trillion of margin debt through official brokerage channels and a massive network of shadow banking sources including dodgy peer-to-peer lending arrangements.

So fortified, they clambered after a stock market bubble that expanded by $3 trillion in just 60 trading days ending on June 14, and then broke into a panicked selling stampede that liquidated that very same $3 trillion of bottled air in hardly 20 trading days thereafter.

Then the state sent out the paddy wagons to arrest and intimidate the panicked sellers and threw-open the central bank’s credit lines to fund hundreds of billions of unwanted stocks. That is not capitalism, red or otherwise; it’s desperate, mindless madness.

Likewise, there are no credible institutions of contract law and bankruptcy. There is not even minimally honest corporate financial reporting and no restraints at all on the propensity of China’s newly affluent masses to gamble in real estate, stocks, commodity financing schemes, dodgy private lending clubs, chain letters and endless similar get rich quick schemes.

Most importantly, there are no lines of demarcation between the property of the state and the license of officialdom and their cronies to expropriate it. In a word, China wallows in the greatest cesspool of corruption known to history because that’s what happens when you erect a $10 trillion command economy virtually over night.

And the swaying edifice of red capitalism has indeed been stood up overnight. At the time that Mr. Deng radically changed the party line——proclaiming that it is glorious to be rich and the PBOC slashed the RMB exchange rate by 60% in 1994 in order to jump start an export boom——there was less than one half trillion dollars of credit market debt outstanding. Alas, that figure today is $28 trillion according the cautious reckoning of McKenzie, and most likely far more.

Here’s the thing. You can not safely, sanely or efficiently grow by 56X in hardly two decades something as combustible as cheap, come-and-get it state supplied credit in an environment where the rudiments of market capitalism do not even exist. If you pursue that kind of financial Frankenstein, that’s exactly what you will get, and that’s what the comrades in Beijing actually got.

Now, however, the iron law of financial bubbles has caught up with them. That is, when you stop supplying increasingly massive amounts of new credit to what eventually becomes an elephantine bubble, it begins to fall inward.

This happens slowly at first, then with accelerating momentum, and finally culminates in a panic-riven meltdown. That sequence encapsulates the entirety of the 2006-2008 securitized mortgage meltdown on Wall Street, the late 1980s and early 1990s Tokyo real estate boom and bust, the 1979-1980 silver and gold bubbles and countless others stretching back centuries in time.

So the passive-aggressive posture of China’s officialdom about what even they recognize as the out-of-control credit bubbles in their realm has no rhyme or reason. Beijing’s recent hoping from one foot to the other, first stimulating and then braking, is rooted in pure desperation and seat of the pants adhockery.