Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1131.60 down $1.50 (comex closing time)

Silver $14.57 up 3 cents.

In the access market 5:15 pm

Gold $1135.00

Silver: $14.63

Here is the schedule for options expiry:

LBMA: options expire Monday, August 31.2015:

OTC contracts: Monday August 31.2015:

First, here is an outline of what will be discussed tonight:

I reported to you late Friday night, that an additional 58 contracts of gold were served upon. There has been no additional filings.

At the gold comex today on first day notice, we had a poor delivery day, registering only 4 notices for 400 ounces Silver saw 167 notices for 835,000 oz.

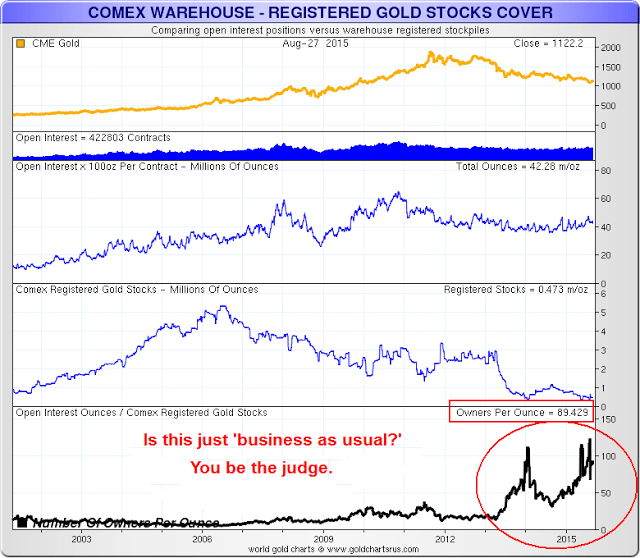

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 224.60 tonnes for a loss of 78 tonnes over that period.

In silver, the open interest fell by 5161 contracts despite the fact that silver was up in price by 12 cents on Friday. Again, our banker friends used the opportunity to cover as many silver shorts as they could. The total silver OI now rests at 158,436 contracts In ounces, the OI is still represented by .819 billion oz or 117% of annual global silver production (ex Russia ex China).

In silver we had 167 notices served upon for 835,000 oz.

In gold, the total comex gold OI collapsed to 413,158 for a loss of 2479 contracts. We had 4 notices filed on first day notice for 400 oz today.

We had no change in tonnage at the GLD today/ thus the inventory rests tonight at 682.59 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had a huge addition of 954,000 in silver inventory at the SLV tune of / Inventory rests at 325.922 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by 5161 contracts down to 158,646 despite the fact that silver was up by 12 cents in price with respect to Friday’s trading. The total OI for gold fell by 2479 contracts to 415,637 contracts, as gold was up by $10.70 on Friday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. Six stories on China tonight. The markets were again rescued by POBC and now arrests are being made. The big news last week was official announcement of China selling its hoard of USA treasuries. China is angry at the USA as they state that the market crash is USA’s fault. Today the yuan was bought in volumes by the POBC and thus wads of USA treasuries were again sold. It also looks like German bunds were also sold. We had another chemical explosion in Shandong province. This is the 3rd major blast in 3 weeks.

(Reuters/zero hedge)

4.A Grenade attack on the Ukrainian Parliament today.

(zero hedge)

5. Over the weekend massive protests in Malaysia.

(3 stories/Bloomberg/zero hedge)

6.Venezuela is running out of food

(zero hedge)

7. Three oil related stories

(zero hedge)

8 Trading of equities/ New York

(zero hedge)

9. USA stories:

a) Chicago PMI and Milwaukee PMI both stall

b) the all important Dallas Fed now in negative territory

both of the above caused the NYSE to have a bad day today.

c. This week’s wrap up with Greg Hunter and Craig Hemke

(Greg Hunter/USAWatchdog,Craig Hemke)

10. Physical stories:

- Premiums for physical gold and silver rising (Jessie’s Americain cafe)

- South Africa to promote platinum (but not gold???) /Reuters

- Smaulgld reports a huge 73 tonnes of gold demand from China in latest reporting week. Also Jessie reports on the same subject.

- Two commentaries on the finding of that Nazi Gold Train/Reuters/Newsmax

- Another ten tonnes of gold leaves FRBNY after a one month hiatus/Harvey,FRBNY,zero hedge

- Isis advertises new gold coin as currency but pay their soldiers in dollars (DailyMail/London/GATA)

- New app to store gold from Bitcoin/CanadianPress/Toronto

- Bill Holter’s important paper tonight is titled: “”Something” just happened!”

- A gold dealer/jeweller from Dubai with 150 stores has defaulted over 135 million owing to several banks. (GATA/Reuters)

- Gold quantities spiking over at the LBMA as massive quantities move from London to China, India and Russia. (jessie/Americain cafe)

Let us head over and see the comex results for today.

September contract month:

Initial standings

August 31.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 268.47 oz Delaware,HSBC,Manfra) oz |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 1060.87 oz (HSBC,Manfra)_ |

| No of oz served (contracts) today | 4 contracts (400 oz) |

| No of oz to be served (notices) | 268 contracts (26,800 oz) |

| Total monthly oz gold served (contracts) so far this month | 4 contracts(400 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 268.47 oz |

Total customer deposit: 1060.87 oz

JPMorgan has 7.1966 tonnes left in its registered or dealer inventory. (231,469.56 oz) and only 741,358.273 oz in its customer (eligible) account or 23.05 tonnes

August silver final standings

August 31 2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,603,393.382 oz (Brinks,Delaware,CNT, Scotia) |

| Deposits to the Dealer Inventory | 99,961.45 oz CNT |

| Deposits to the Customer Inventory | 904,454.05 oz (Brinks, CNT) |

| No of oz served (contracts) | 167 contracts (835,000 oz) |

| No of oz to be served (notices) | 2031 contracts (10,155,000 oz) |

| Total monthly oz silver served (contracts) | 167 contracts (835,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,603,353.382 oz |

Today, we had 1 deposit into the dealer account:

i) Into CNT: 99,691.45 oz

total dealer deposit; 99,691.45 oz

total customer deposits: 904,454.05 oz

total withdrawals from customer: 1,603,353.382 oz

And now SLV:

August 31.a huge addition of 954,000 oz were added to inventory today at the SLV/Inventory rests at 325.922

August 28.2015: no change in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 27.no change in inventory at the SLV/Inventory rests at 324.698 million oz (for the 11th straight trading day)

August 26.2015/no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 25.2015:no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 24./no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 21.2015/ no change in inventory at the SLV/Inventory rests at

324.698 million oz

August 20.2015:/no changes in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 19/no changes in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 18.2015: no changes in inventory at the SLV/Inventory rests tonight at 324.968 million oz

August 17.2015: no changes in inventory at the SLV/Inventory rests tonight at 324.968 million oz.

August 14/no changes in inventory at the SLV/Inventory rests at 324.968 million oz.

August 13.2013: a huge withdrawal of 1.241 million oz/Inventory rests tonight at 324.968 million oz

August 12.2015: no change in SLV inventory/rests tonight at 326.209 million oz.

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

(courtesy/Mark O’Byrne/Goldcore)

Gold Set for Best Month Since January as Stock Market Rout Lifts Safe Haven

DAILY PRICES

Today’s Gold Prices: Bank Holiday in UK today

Friday’s Gold Prices: USD 1,125.50, EUR 998.23 and GBP 730.99 per ounce.

(LBMA AM)

Last week gold and silver prices fell and gave up some of the gains from the previous week. Gold was 2% lower on Friday and indeed 2% lower for the week and closed at $1134.40 per ounce. Silver was 4.5% lower for the week and closed at $14.59 per ounce but is just 1.8% lower for the month of August.

August has been a tumultuous month with stocks seeing sharp losses and gold has again protected investors from sharp losses. Gold has had a 3.36% gain for the month so far (see table below).

Gold is on track for the best monthly advance since January after most market participants were surprised by the devaluation of China’s currency. This has fueled concerns about furthercurrency wars and about the world’s second-largest economy and indeed the global economy may be vulnerable to a recession – potentially a severe one.

Gold exchange-traded fund holdings rose to a one-month high last week on safe haven demand. The MSCI All-Country World Index of equities is headed for the worst monthly performance since May 2012 and a gauge of 22 raw materials was set to decline for a second month.

Monthly Asset Performance – Finviz.com

IMPORTANT NEWS

Gold Set for Best Month Since January as Rout Lifts Haven Assets – Bloomberg

Asian stocks set for worst monthly drop in three years on global rout – Reuters

Stocks Set for Worst Month Since 2012 as Fed, China Woes Collide – Bloomberg

Polish Government Confirms Discovery Of Nazi “Gold Train”, Warns It May Be Booby-Trapped – Zero Hedge

App for that? BitGold looks to take gold savings mainstream – CTV News

South Africa to promote platinum as central bank reserve asset – Reuters

The Fed Spent $23 Billion In 3 Days, But Still Had A Hard Time Pushing Up Stocks – Seeking Alpha

Red Alert For 2nd Crash Downwave… – CliveMaund.com

The Central Bankers’ Malodorous War On Savers – David Stockman’s Contra Corner

Since 2014 Foreign Central Banks Have Withdrawn 246 Tons Of Gold From The NY Fed – Zero Hedge

When David beats Goliath – Davidmcwilliams.ie

end

(courtesy Jessie’s American cafe)

Despite Being A ‘Pet Rock’, The Premium For Physical Bullion Is Exploding

While status quo-huggers are all too happy to point out gold and silver’s lack of utter exuberance amid this week’s carnage, perhaps they need to re-comprehend the difference between a heavily manipulated ‘paper’ market and the surging demand for physical precious metals that is evident in the 20-plus percent premium – and rising – being paid for silver bullion currently…

“One important aspect of the physical market that is often overlooked is the premium it commands over spot price. Right before the Global Financial Crisis in 2008, the spot Silver price fell as low as USD 9 per oz., whereas the price of a 1 oz. Silver Eagle was around USD 17 on the wholesale market and even higher on the retail market! That’s a price premium of 188%!

That means that if you had held 100 oz. of paper Silver, you might have had to liquidate that for USD 900 (assuming the market was not halted for trading then), whereas if you had held 100 pieces of 1 oz. Silver Eagle coins, you would have gotten at least USD 1700 for them if not more.”

BullionStar, The Difference in Paper and Physical Gold and Silver in times of Crisis

end

Gold quantities are spiking off the LBMA:

(courtesy Jessie of Americain cafe)

30 August 2015

Gold Coming Off the LBMA Spiked Last Week

There was a interesting spike in physical gold activity last week on the LBMA.

It could be some seasonal phenomenon connected with the end of August and the approach of the prime season for gold.

But it also seems consistent with the ‘tension on the tape’ that I have been seeing. And a number of little indicators and some interesting things, like the generally ‘well informed’ Goldman taking delivery of gold at the Comex for their house account.

One outcome of this increase in physical gold flows *might* be the realization of the cup and handle bottom formation on the gold chart, and a quick run to target around the 1250 to 1270 area. And depending on what else goes with it, that might just be for openers.

Or it might once again be ignored and come to nothing.

But it does seem that the gold flows from the West to the markets in China and India are intensifying at these prices based on a number of diverse data points.

One cause of this could be a divergence between the paper price of gold with leverage and the actual physical markets because the price of gold as set in London and New York is below the clearing price in dollars as part of a momentum trend in the forex markets.

If a commodity price is set below the natural clearing price, one would expect to see the demand for the real underlying asset increasing.

Those who flatly dismiss the possibility there can be such a divergence between the market price and the natural clearing price have not been paying attention to what has been going on in any number of rigged markets over the past few years.

The excessive speculation fueled by a surfeit of paper money in a few hands and slack regulation that permits the unsustainable reckless pyramiding of positions is a good contender for the theme of the last two decades.

For what it is worth, I am seeing what appear to be increasing signs of ‘fragility’ in the precious metals market. And in a nutshell, I am thinking that we are seeing a bear market bottom. Trends, especially in forex related markets, often tend to overshoot and overstay their time.

But like the proverbial search for the lost keys, we will find the end of this era of financial madness in the last crisis, and perhaps that will be the one that breaks the Banks.

The chart below was provided by Nick Laird at goldchartsrus.com.

***

end

Fascinating!! and not promote gold???

(courtesy Reuters)

Reuters: South Africa to promote platinum as central bank reserve asset

Submitted by cpowell on Sat, 2015-08-29 20:47. Section: Daily Dispatches

So why haven’t they figured this out for gold too? Are there no patriots in South Africa’s government?

* * *

South African Mine Industry Job Plan Targets Platinum as Central Bank Reserve Asset

By Ed Stoddard

Reuters

Wednesday, August 26, 2015

JOHANNESBURG, South African — South Africa’s mining industry, unions, and the government have committed to a broad plan to stem job losses, including boosting platinum by promoting the metal as a central bank reserve asset, according to a draft agreement seen by Reuters on Wednesday.

The parties also said they would strive to delay layoffs, sell distressed mining assets instead of closing them, and look at ways of streamlining the legal process employers must follow to cut jobs.

The mining industry, which contributes around 7 percent to Africa’s most developed economy, is struggling with sinking commodity prices, rising costs, and labor unrest, forcing a number of companies into mine closures and layoffs.

The agreement is expected to be signed on Monday next week after its details were hammered out on Tuesday.

The draft agreement lays out 10 wide interventions including getting the BRICS group of emerging nations to hold “platinum as a reserve asset” — like gold — in their central banks. Brazil, Russia, India, China, and South Africa comprise the BRICS.

South Africa sits on close to 80 percent of the world’s known reserves of platinum, a metal used in emissions-capping catalytic converters and facing depressed demand. …

… For the remainder of the report:

http://www.reuters.com/article/2015/08/26/us-safrica-mining-idUSKCN0QV0W…

end

Two stories…

(courtesy Reuters/GATA)

Polish Government Confirms Discovery Of Nazi “Gold Train”, Warns It May Be Booby-Trapped

Last weekend we reported that in the past month two men, a Pole and German, claimed to have discovered the legendary Nazi “gold train” – a 150 meter long German train alleged to be full of gold, gems and weapons, which disappeared just before the end of World War II – in the proximity of the Polish town of Walbrzych, close to where the Nazi are said to have loaded up the train with valuables for its final voyage in the town of Wroclaw, just as the Soviet forces approached in 1945.

As we detailed, the train is said to have been entombed in the vast tunnel labyrinth located close to Ksiaz castle, which served as Nazi headquarters during World War II…

Ksiaz castle, Nazi headquarters during World War II

… and specifically, was said to be located at the foot of the Sowa mountain, in the woods three miles outside the town of Walbrych.

The “gold train” is said to be located under this hill

While many were skeptical that the mystical Nazi treasure train had been finally discovered after many years of searching, an official update last Friday by the Polish government suggested that that may indeed be the case. As the Mail reported on Friday, a representative of the Polish culture ministry, Poland’s National Heritage and Conservation Officer Piotr Zuchowski, said that the man who helped hide the train had revealed its location shortly before he died, and that proof of the train has been observed on radar.

Zuchowski added that “Information about where this train is and what its contents are were revealed on the deathbed of a person who had knowledge of the secret of this train.’ He added that Polish authorities had now seen evidence of the train’s existence in a picture taken using a ground-penetrating radar. He said the image – albeit blurred – showed the shape of a train platform and cannons.

Piotr Zuchowski, Poland’s National Heritage and Conservation Officer, confirmed the ‘unprecedented’ find

Mr Zuchowski said the find was ‘unprecedented’, adding: ‘We do not know what is inside the train.‘Probably military equipment but also possibly jewellery, works of art and archive documents.

‘Armored trains from this period were used to carry extremely valuable items and this is an armored train, it is a big clue.’ He said authorities were now ’99 percent sure the train exists’ and whatever is on it will be returned to the rightful owners, if they can be found. ‘We will be 100 per cent sure only when we find the train,’ Mr Zuchowski added.

The train found in the mountains is an ‘armored train’ which looks similar to the one pictured

Mr Zuchowski told reporters that the train was about 100 metres long but added: ‘It is not possible to disclose the exact location of where the train can be found. Still, he noted cryptically that “The local government in Walbrzych knows where it is.”

He explained it is hidden along a 4km stretch of track on the Wroclaw-Walbrzych line.

Mr Zuchowski said the person who claimed he helped load the gold train in 1945 said in a ‘deathbed statement’ the train is secured with explosives. The official declined to comment further about the man who said this but speculation is now rife that it was a former SS guard or a local Pole who stumbled upon the train before hiding it.

Deputy Mayor of Walbrzych, Zygmunt Nowaczyk told the press: ‘The city is full of mysterious stories because of its history. ‘Now it is formal information – we have found something.’

Key excerpts from the press conference by the Polish official can be seen on the Euronews clip below:

The confirmation of the discovery unleashed a surge of treasury hunters, and forced the Polish government to warn the population to stop looking because it could be booby-trapped and dangerous. Zuchowski said “foragers” have become active since two people claimed to have discovered the train last week and urged eager fortune-hunters to stop searching, saying they risk injury or death.

Zuchowski adds that “there may be hazardous substances dating from the Second World War in the hidden train, which I’m convinced exists. I am appealing to people to stop any such searches until the end of official procedures leading to the securing of the find. There’s a huge probability that the train is booby-trapped.’

If anything, tthese warnings are sure to unleash an even more aggressive wave of seekers now that the train’s existience has been confirmed, and the government is actually warning seekers to be careful in their search.

But perhaps what is more interesting is just what the discovery, which would be straight out of an Indian Jones sequel, will contain, and whether someone already got to the precious cargo over the past 7 decades. The answer should be made public shortly.

end

(courtesy Newsmax)

Report: Putin Could Seize Nazi Gold Train for Alleged Soviet Reparations

Report: Putin Could Seize Nazi Gold Train for Alleged Soviet Reparations

Sunday, 30 Aug 2015 02:02 PM

Russian strongman Vladimir Putin may be moving to seize the famed Nazi ghost train laden with gold that has ostensibly been discovered in Poland.

How could he do it? A Russian lawyer says Kremlin could lay claim to the valuables as compensation for the country’s losses in the Second World War, according to the Independent.

The so-called ‘Nazi gold train’ has been reportedly been found hear the town of Walbrzych, where rumors have been constant for years that a train filled with gold had been abandoned during the Nazi era and was lying undiscovered nearby. Polish government officials say that they are now “more than 99 per cent certain the train exists.”

The train could reveal the long-sought solution to the mystery of the ‘Amber room’ – an ornate chamber made of amber pearls thought to be worth at least $300 million. It was stolen by German troops from a palace near St. Petersburg during the war.

The Russian lawyer told a Russian news site that “representatives of Russia should undoubtedly be involved in determining the value of the items discovered if the train is located.

“In this case, Poland is obliged to engage international experts to clarify what is in the cargo. If the property has been taken away from territory, including the USSR, then the cargo, in accordance with international law, must be passed to the Russian side,” the lawyer said.

© 2015 Newsmax. All rights reserved.

Read Latest Breaking News from Newsmax.com http://www.newsmax.com/Newsfront/nazi-gold-train-russia/2015/08/30/id/672660/#ixzz3kORNFsaO

Urgent: Rate Obama on His Job Performance. Vote Here Now!

end

Saturday morning August 29, saw the FRBNY report its earmarked gold.

The report showed that :

| 311,319 | 311,852 | 290,949 | 286,779 | 284,197 | 284,884 | 284,538 | 287,685 | 298,627 | 295,692 | ||

| 4 | Earmarked gold4 | 8,417 | 8,410 | 8,170 | 8,143 | 8,130 | 8,116 | 8,103 | 8,089 | 8,089 | 8,076 |

|---|

(courtesy zero hedge)

Since 2014 Foreign Central Banks Have Withdrawn 246 Tons Of Gold From The NY Fed

First it was Germany who redeemed 120 tons of physical gold in 2014; then it was the Netherlands who “secretly” redomiciled 122 tons of gold; then this past May, we learned that Austria would be the third “core” European nation to repatriate most of its offshore gold, held primarily in the Bank of England, redepositing it in Vienna and Switzerland.

In short, beginning in 2014 and continuing through today, the gold “bleeding “from the vault located 90 feet below street level at 33 Liberty Street (and which may or may not be connected by a tunnel to the JPM gold vault locatedjust across the street at 1 Chase Manhattan Plaza) has continued. As the chart below shows, while central banks assure the population that there is nothing to worry about when it comes to paper money, and in fact it is the evil ISIS terrorists who plot and scheme to crush the benevolent Fed with their terroristy “gold dinars” and if not that then their made in Hollywood propaganda movies, they have been quietly pulling gold from the biggest centralized depository of global gold in the world: the New York Federal Reserve.

According to the latest just released monthly update of foreign official assets held in custody at the NY Fed, in July the total holdings of foreign earmarked, i.e., physical, gold declined to just over $8 billion when evaluated at the legacy “price” of $42.22 per ounce. In ton terms, this means that after declining below 6000 tons in January, for the first time since FDR’s infamous gold confiscation spree, the total physical gold held at the NY Fed dropped another 9.6 tons in July, down to 5,950 tons.

This is the lowest amount of gold held by the NY Fed in custody in decades, is the 18th consecutive month of flat or declining gold, and when added to previous outflows, amounts to 192 tons of gold withdrawn in the past 12 months, and a whopping 246 tons pulled since the start of 2014.

Indicatively, during the last crisis period, starting in March 2007 and lasting through November 2008, foreign central banks withdrew gold for a total of 20 out of 21 consecutive months, repatriating a grand total of 409 tons of gold. The last period of peak redemption culminated with the failure of Lehman in September 2008, the near failure of AIG in October and November 2008, coupled with the Fed’s bailout of the western financial system.

If past is prologue, one should ask: what current or future event is driving the ongoing redemption of gold from the NY Fed this time?

end

(courtesy London’s Daily Mail/GATA)

ISIS advertises its new gold coins but still pays its gunmen in U.S. dollars

Submitted by cpowell on Sun, 2015-08-30 18:08. Section: Daily Dispatches

ISIS Release Pictures of Their New Gold Coins They Say Will ‘Break Capitalist Enslavement’ — So Why Are They Still Paying Their Deranged Gunmen in U.S. Dollars?

By Tom Wyke

Daily Mail, London

Sunday, August 30, 2015

ISIS have released a new hour-long video, showing off their latest propaganda tool — their very own coin currency.

The video, which includes a dreary and distorted history of world economics, shows the smelting of gold, silver, and copper coins.

Dramatised by clips from Hollywood war films, the film accuses the United States of “confiscating Americans’ real wealth through an executive decree” with the introduction of the Gold Reserve Act in 1934.

Yet despite their glorification of their new currency, ISIS have no other means to pay their band of jihadis except through the use of U.S. dollars. …

… For the remainder of the report:

http://www.dailymail.co.uk/news/article-3215910/ISIS-release-pictures-ne…

end

(courtesy Canadian Press/Toronto)

App for that? BitGold looks to take gold savings mainstream

Submitted by cpowell on Sun, 2015-08-30 17:59. Section: Daily Dispatches

By Ian Bickis

The Canadian Press

via CTV News, Toronto

August 30, 2015

CALGARY, Alberta, Canada — Want to buy gold as a savings alternative? Well, you guessed it — there’s an app for that.

Josh Crumb, co-founder of BitGold, says he created the software that automatically links buyers to bullion dealers and storage companies because he wanted to make it easier for people to own gold as a hedge against inflation and as a store of value.

“It’s just so much easier, like everything else, to do it from your mobile phone,” Crumb said.

The system charges a 1 percent fee to exchange cash into gold and back but storage is free. It also allows users to transfer their gold value to a prepaid credit card, so they can actually buy a cup of coffee with their gold holdings, Crumb said.

“It gives the ability without having to go to coin shops and shave off some flakes of gold to buy something.” …

… For the remainder of the report:

http://www.ctvnews.ca/business/app-for-that-bitgold-looks-to-take-gold-s.

end

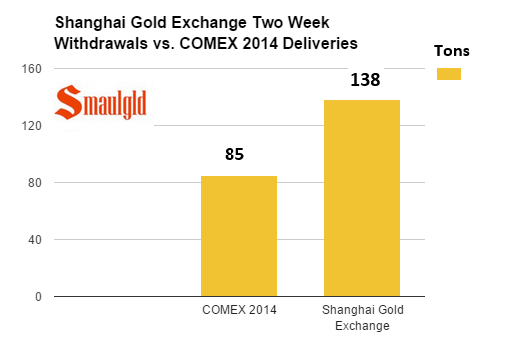

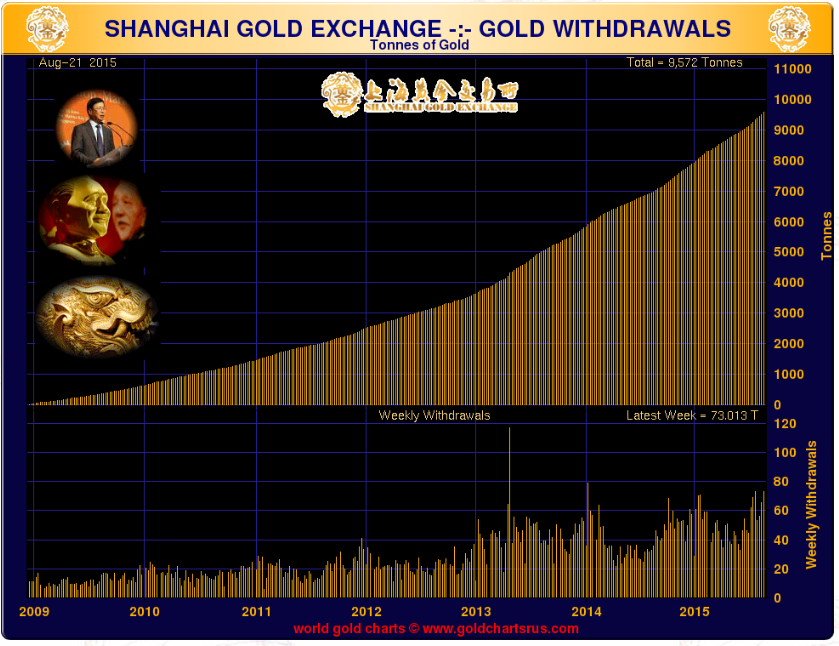

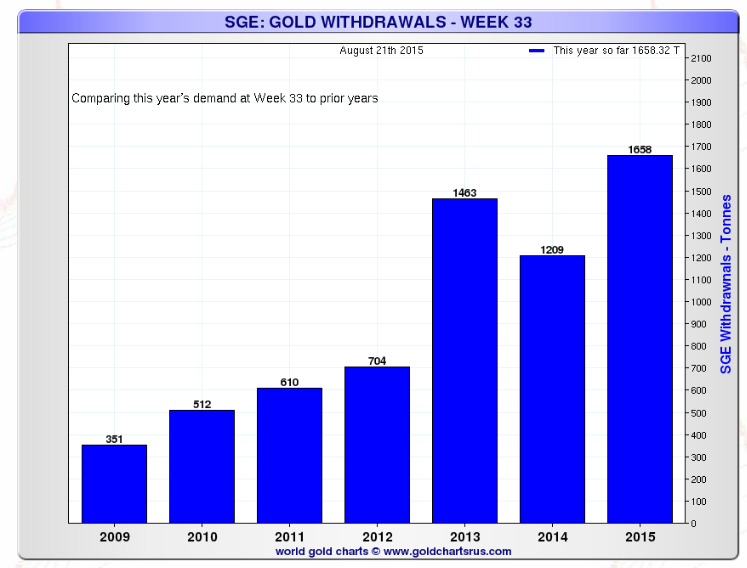

A huge 73 tonnes of gold was withdrawn from vaults last week.

(courtesy Smaulgld)

Shanghai Gold Exchange volume for the week ended August 21, 2015.

The Shanghai Gold Exchange withdrawals were 72.91 tons of gold during the week ended August 21, 2015.

Withdrawals on the Shanghai Gold Exchange were the fourth largest ever.

Total gold withdrawals on the Shanghai Gold Exchange year to date are 1,658.22 tons.

Withdrawals on the Shanghai Gold Exchange are running 37.2% higher than last year.

China’s Insatiable Demand for Gold

The Shanghai Gold Exchange (SGE) delivered 72.91 tons of gold during the week ended August 21, 2015. The prior week the SGE delivered 65.31 tons of gold.

The two week total of withdrawals is over 121 tons of gold and the year to date total is1,585.31 tons, for an annualized run rate of approximately 2,600 tons.

Shanghai Gold Exchange Withdrawals During the Two Week Period Ended 8/21/2015 vs. Comex 2014 Deliveries

Volume of Gold Withdrawals on the Shanghai Gold Exchange

The volume of withdrawals of gold on the Shanghai Gold Exchange as of August 21, 2015, is running 37% higher than 2014 during the same period and 13.3% higher than 2013’s record pace.

China is becoming the center of the Asian gold world. A $16 billion China Gold Fund was announced in May and the Shanghai Gold Exchange continues to establish itself as viable competitor to the gold trading centers in London and Chicago. China’s gold imports, trading and mining production are one of the cornerstones of China’s de-dollarization/Yuan strengthening initiatives that focuses no so much on selling U.S. Treasuries but creating alternative financial systems like the Asian Infrastrucure Investment Bank.

China is widely believed to be making a play for inclusion in the International Monetary Fund’s (IMF) Special Drawing Rights (SDRs) Program later this year. If China fails to gain inclusion in the SDR, its recent initiatives to strengthen its currency and gain greater acceptance of the Yuan may provide a strong alternative to the IMF regime.

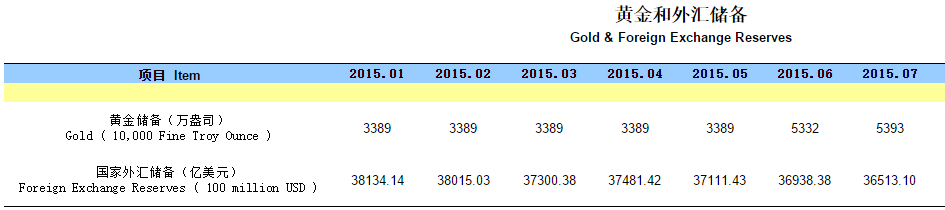

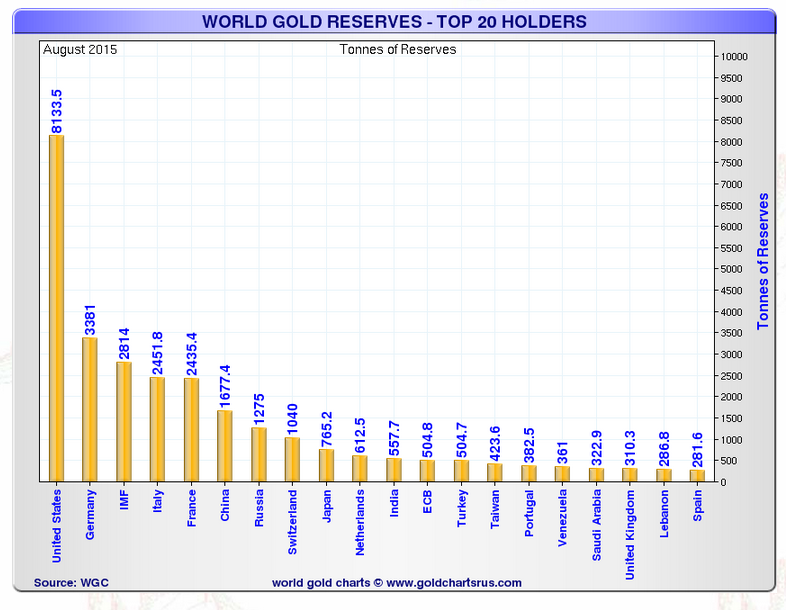

China Updates its Gold Holdings

China recently announced their first update to their official gold holdings since 2009. The People’s Bank of China announced that their gold holdings had climbed from 1054 tons to 1658 tons, making China the fifth largest gold holding nation in the world.

China chose to incude six years worth of gold accumulation (over 600 tons) all in the month of June.

Earlier this month China reported that they added 19.3 tons (610,000 ounces) of gold to their reserves in July bringing their total to 1,677 tons (53.93 million ounces).

end

Jessie, of Americain cafe on the same subject as to the huge 73 tonnes of gold demand coming from the citizenry of China:

28 August 2015

Shanghai Exchange Has 73 Tonnes of Gold Withdrawn In 4th Largest Week In History

There were a little over 73 tonnes of physical gold withdrawn from the Shanghai Gold Exchange in the latest week ending August 21st.

This is the 4th largest withdrawal of bullion in its history.

It is hard to tell what exactly is going on in such a dodgy, highly leveraged market, with its determined attempts to keep the price knocked lower so often during the late London to NY trading hours.

But I am sensing a change in the market, and more things running under the surface than meets the eye.

Goldman is no major player in the gold bullion market, but it did strike me as odd that they are suddenly stopping large amounts of bullion for their own house account this month. It is not that they are a player in gold, because they are not. But that they are wired into many sources of information, are good at spotting trends, and are more like a hedge fund, comfortable running on the edge of the markets.

And the gold chart, for what it is worth in these times of market interventions, seems to be trying to form a rounded bottom in the form of a cup and handle, with a successful retest of the handle this week. This calls out a price around the bottom of the old trend channel at 1270.

It could also be nothing. I will pursue the details of such a chart formation if we see the right kinds of follow through next week.

And I will certainly be watching silver very carefully for any signs of life. It may be pivotal next month.

Let’s see what next week brings. Gold is just one market among many, and it is certainly not the largest one in play.

And while I have your attention, I thought I would include a long term chart of the relation of deliverable gold at current prices to open interest. It might mean nothing. But it doesn’t seem to be anything familiar before 2013.

The charts below courtesy of data wrangler Nick Laird at goldchartsrus.com.

***

end

This is interesting

they do not know why they defaulted!!

(courtesy Reuters/GATA)

Dubai gold retailer defaults on $136 million

Submitted by cpowell on Mon, 2015-08-31 14:11. Section: Daily Dispatches

By Stanley Carvalho and Tom Arnold

Reuters

Monday, August 31, 2015

DUBAI, United Arab Emirates — A Dubai-based gold and jewellery retailer has defaulted on loans worth about 500 million dirhams ($136.2 million), with banks considering options including legal action to retrieve the money, four banking and trade sources told Reuters.

The non-payment by Atlas Jewellery, which has more than 50 branches across the Gulf and in India, affects at least 15 banks, the sources said on condition of anonymity because the information isn’t public.

It was not clear why Atlas Jewellery had failed to honor its debts. Company officials declined to comment and Reuters was unable to contact the company’s owner, M.M. Ramachandran. …

… For the remainder of the report:

http://www.reuters.com/article/2015/08/31/emirates-gold-default-idUSL5N1

end

And now Bill Holter with an important paper tonight…

(courtesy Bill Holter/Holter-Sinclair collaberation)

“Something” just happened! (reprint)

“Something” happened three weeks ago. While we cannot be sure “what” exactly happened, we can speculate. We have many dots and lots of data points to help us but first it needs to be pointed out, even if wrong in conclusion …just the knowledge alone that “something changed” is enough. If you know something has changed, you can take clues and look at various markets for inflection points. Currently, most markets are stretched to various limits. Whether it be zero bound credit markets, equities, real estate, commodities or gold and silver, all values had reached extreme highs or lows.

end

1 Chinese yuan vs USA dollar/yuan rises considerably this time to 6.3761/Shanghai bourse: red and Hang Sang: green

Surprisingly, last week, officially, China added another 19 tonnes of gold to its official reserves now totaling 1677.

2 Nikkei down 245.84 or 1.28.%

3. Europe stocks all deeply in the red /USA dollar index up to 96.00/Euro up to 1.1208

3b Japan 10 year bond yield: falls to .3760% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 121.26

3c Nikkei now below 19,000

3d USA/Yen rate now just above the 121 barrier this morning

3e WTI: 44.35 and Brent: 48.86

3f Gold up /Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .738 per cent. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate rises to 13.03%/Greek stocks this morning down by 1.43%: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield rises to : 9.31%

3k Gold at $1132.60 /silver $14.54 (8 am est)

3l USA vs Russian rouble; (Russian rouble down 1 2/3 in roubles/dollar) 66.88,

3m oil into the 44 dollar handle for WTI and 48 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9645 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0810 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund now enters in negative territory with the 10 year moving further from negativity to +.738%

3s The ELA lowers to 89.7 billion euros, a reduction of .7 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.16% early this morning. Thirty year rate below 3% at 2.88% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

China Dramatically Intervenes To Boost Stocks Despite Reports It Won’t; US Futtures Slump On J-Hole

Yesterday, the FT triumphantly proclaimed: “Beijing abandons large-scale share purchases“, and that instead of manipulating stocks directly as China did last week on Thursday and Friday, China would instead focus on punishing sellers, shorters, and various other entities. We snickered, especially after the Shanghai Composite opened down 2% and dropped as low as 4% overnight:

Less than five hours after this tweet, we found out that our cynical skepticism was again spot on: the moment the afternoon trading session opened, the “National Team’s” favorite plunge protection trade, the SSE 50 index of biggest companies, went super-bid and ramped from a low of 2071 to close 140 points higher, ending trading with a last minute government-facilitated surge, and pushing the Composite just 0.8% lower after trading down as much as -4.0%.

It wasn’t just direct stock market intervention: Bloomberg reported that additionally the PBOC also conducted another Short-term Liquidity Operations with some banks Monday, adding that tenors offered included six-day loans. Recently, the PBOC had conducted 7-day CNY60b SLO at 2.35% on Aug 28 and 140b yuan 6-day SLO at 2.30% on Aug 26.

China’s interventions were to be expected: what the FT got right is that the government is intent on “providing a “positive market environment in preparation for a big military parade this week to celebrate the 70th anniversary of the “victory of the Chinese people’s war of resistance against Japanese aggression.” The question is whether once the September 3 event is over, will China finally allow stocks to truly trade down. We doubt it: just like the Fed has found 7 years later when even the tiniest of rate hikes threatens to collapse the house of cards, so China will hardly dare to step away at least until the Chinese premier Li Keqiang is sacrificed, literally or metaphorically, to appease the millions who have lost everything and then some (thanks to margin).

Elsewhere in Asia, equity markets traded lower following Fed’s Fischer comments over the weekend which implied that a September rate hike has not been completely ruled out. China’s Shanghai Comp, despite the late government intervention, led the region lower, after reports authorities would stop supporting stock markets through large scale buying, while Nikkei 225 (-1.3%) traded in negative territory following the release of Japanese industrial output where both M/M (-0.6%) and WY (+0.2%) figures missed expectations. 10yr JGBs traded higher amid the risk off tone in Asia while the BoJ were also in the market for JPY 1.18trl of JGBs.

Utilities underperformed on the sector breakdown as European equities spend the morning in the red (Euro Stoxx -1.2%) as participants remain concerned over the ongoing volatility in Asian markets, with RWE (-2.5%) trading sharply lower following reports that one of RWE’s municipal shareholders, expects the company to slash its dividend by as much as half. On the other hand, ENI (+3%) shares surged at the open after the company and also ensured that the Italian benchmark FTSE-MIB index outperformed, despite falling into the red during the morning, after the Co. announced that it has made a huge gas field discovery off Egyptian coast Lower stocks and dovish comments by ECB’s Constancio, who said that the fall in oil prices is an issue with regards to inflation despite the efforts of the central banks’ QE programme, kept Bunds bid, albeit marginally. However it is worth noting that trade volumes were below the usual levels given the closure of the UK’s financial district due to the August bank holiday.

In FX, EUR/USD gradually moved off the best levels printed ruing the late Asian trading hours, weighed on by touted selling by macro and corporate accounts, failure to break above 0.7300 level by EUR/GBP and dovish comments by ECB’s Constancio. Elsewhere, the ongoing volatility stemming from China, together with lower copper prices, saw AUD trade lower, with AUD/USD consolidating in 0.7100 area.

Going forward, market participants will get to digest the release of the latest EU CPI, which printed in fractionally hotter than expected, at 0.2%, vs consensus of 0.1%, and the release of the latest Chicago PMI report.

In terms of Central bank speakers and news from over the weekend:

- Fed’s Fischer (Voter, Soft Dove) said the first rate-hike would come when there is “some further improvement in the labour market” while ‘there is good reason to believe inflation will move higher and forces holding down inflation will dissipate further’. (WSJ) This comes after earlier comments that that it was too early to make a decision on a rate-hike in September. (CNBC/RTRS)

- Fed’s Lockhart (voter, neutral) stated that a rate lift-off is near and that it is an “open question” whether

the members of the FOMC decide to lift interest rates now or delay until another meeting. (RTRS) - Fed’s Kocherlakota (Non-voter, Dove) stated that he would prefer a rate hike to occur in the 2H of 2016. (Fox Business)

- Fed Watcher Hilsenrath interpreted these comments as hawkish suggesting that the central banker did not rule out September and the point at which Fischer believes inflation will pick-up is getting closer. (WSJ)

- ECB’s Constancio (Dove) says the fall in oil prices is an issue with regards to inflation despite the efforts of the central banks’ QE programme. (RTRS)

- BoE Governor Carney (Neutral) said that a slowdown in China’s economy could push down further on inflation but at this moment in time does not alter the central bank’s position on when it will hike rates. (Observer)

- SNB’s Jordan stated the CHF is highly overvalued at present levels and interest rates will remain negative for a while. (RTRS)

Energy and base metals markets remained under pressure amid the ongoing supply glut in the market, as well as the slowdown in China. Nonetheless, despite the downside across the metals complex, gold prices traded relatively flat overnight with a mild gain seen amid a pullback in the greenback from Friday’s highs and weakness across equity markets and are on track for their best month since January.

Bulletin Headlin Summary from Bloomberg and RanSquawk

- Stocks in Europe traded lower, as market participants continued to fret over the ongoing volatility in Asian markets

- Appetite for risk was dented by somewhat hawkish comments by Fed’s Fischer, with WSJ’s Hilsenrath subsequently pointing out that comments indicate that the central banker did not rule out September rate hike

- Focus going forward will be on the release of the latest Chicago PMI report for the month of August

- Treasuries diverge as decline in long yields drives curve flattening; global stocks and crude oil lower as markets await August payrolls report on Friday.

- China’s securities regulator held meeting with representatives from 50 brokerages on Aug. 29 and told them to contribute an additional 100b yuan to support the stock market, said people familiar with the matter

- China has decided to abandon attempts to boost the stock market through large-scale share purchases and has shifted its focus to investigating and punishing manipulators, FT reports, citing an account of unidentified senior regulatory officials speaking at a meeting on Thursday

- Options traders have never been so pessimistic on China’s stock market, betting the government’s renewed effort to prop up share prices is doomed to fail

- Fed Vice-Chair Stanley Fischer proclaimed his faith at Jackson Hole this weekend that inflation is poised to move upward, suggesting a September move by Fed has not been ruled out

- The euro area’s inflation rate held steady in August, highlighting the challenge facing ECB policy makers as they seek to revive consumer-price growth

- Democratic Senator Jeff Merkley of Oregon said he will vote to support the Iran nuclear deal, a pledge that puts Obama only three votes short of protecting the pact in Congress

- One IG deal for $700m priced last week, no HY deals. BofAML Corporate Master Index -3 to +169 from +172, widest since Sept 2012; YTD low 129. High Yield Master II OAS -19bp to +572; reached +614 last week, widest since July 2012; YTD low 438

- Sovereign 10Y bond yields mostly lower. Asian and European stocks mostly lower, U.S.equity-index futures decline. Crude oil falls, gold and copper little changed

DB’s Jim Reid completes the overnight recap

So after we put an interesting and exhausting week of huge swings in markets behind us and look forward to the next five days, any hope that we might see some calm return to markets may have to be put on hold temporarily with the last payrolls report before the September 16th/17th FOMC meeting due on Friday afternoon, giving economists, analysts and the market another chance to fine tune their liftoff expectations. Fedspeak between now and then will also take on more significance with each passing day and we can look forward to comments from Rosengren on Tuesday and Lacker on Friday. We’ve got the usual full run down of the week ahead at the end but it’s Fedspeak that we start with this morning after a bumper last few days of comments, including from Fed-Vice Chair Fischer on Saturday at the Jackson Hole symposium.

Without pinning down any specific hints on timing but still leaving the September liftoff door open, Fischer’s tone certainly felt like it weighed on the more hawkish side, saying that the Fed should not wait until it meets its inflation goal while voicing confidence that prices should head higher. Specifically, Fischer said that ‘given the apparent stability of inflation expectations, there is good reason to believe that inflation will move higher as the forces holding down inflation dissipate further’ and that ‘with inflation low, we can probably remove accommodation at a gradual pace’ however ‘because monetary policy influences real activity with a substantial lag, we should not wait until inflation is back to 2% to begin tightening’. The comments came a day after a TV interview with CNBC in which Fischer noted that ‘the change in the circumstance which began with the Chinese devaluation is relatively new and we’re still watching how it unfolds, so I wouldn’t want to go ahead and decide right now what the case is – more compelling, less compelling etc’, before noting that ‘we’ve got a little over two weeks before we make the decision’ and that ‘we’ve got time to wait and see the incoming data, and see what is going on now in the economy’.

It wasn’t just Fischer we heard from at the event. Speaking on Friday, more hawkish commentary came in the form of non-voters Mester and Bullard. Mester in particular said that ‘my view so far in looking at all of the factors is that the economy can sustain an increase in interest rates’, while Bullard signaled that the volatility of the last 10 days would not be enough to change his view that the US economy can sustain a rate rise. The lone voice in the dovish camp on Friday, Kocherlakota, said that ‘I don’t see a near term increase in interest rates as being appropriate, and by near-term I mean really through the course of 2015’. Meanwhile Lockhart, speaking once again, commented that timing for liftoff ‘is close’ but that it’s an ‘open question’ whether the Fed moves now or waits a little, noting that the October FOMC is a ‘live meeting’ and ‘in play’.

So with all the comments, the probability of a September move by the Fed has now jumped to 38% from 30% at Thursday’s close. This morning we’ve seen little change in 2y (+0.6bps) or 5y (0.0bps) Treasury yields, while the benchmark 10y is down 2.1bps to 2.159%. Much of the action is again in equity markets where S&P 500 futures are down over a percent in trading this morning. It’s much the same in bourses across Asia too. Led by China once again with the Shanghai Comp (-2.61%) and Shenzhen (-2.25%) both taking another steep leg lower into the midday break, the Nikkei (-1.94%), Hang Seng (-0.77%), Kospi (-0.32%) and ASX (-1.51%) have all followed suit with material moves lower. The lower tone this morning in markets has also been reflected in the Oil complex which is down 2% as we go to print.

With regards to the moves in Chinese equities in particular, it’s hard to tell how much of this is in response to conflicting reports of state intervention in the market this morning. The FT is running an article suggesting that state-owned investment funds and institutions, which were previously boosting the stock market through large scale purchases, are set to refrain from such actions with the government switching its attention to punishing those involved in ‘destabilizing the market’. Meanwhile, according to a Bloomberg report and in contrast to the FT article, Chinese authorities are set to seek to stabilize markets before an important military parade this week, with the regulatory commission asking 50 brokerages to contribute an additional 100bn yuan to the rescue fund.

Back to the Jackson Hole gathering quickly where along with the Fed, we also got some hints into the current thinking at the BoE and ECB. Along with Fischer, the comments echoed a more hawkish tone largely. The ECB’s Constancio noted that ‘the link between inflation and real activity appears to have strengthened in the euro area recently’ and that ‘provided our policies are able to significantly reduce the output gap, we can rely on a material effect to help bring the inflation rate closer to target’. The BoE’s Carney stated that the ‘prospect of sustained momentum’ in the economy ‘will likely put the decision as to when to start the process of gradual monetary policy normalization into sharper relief around the turn of this year’. On the hot topic of the China turmoil, Carney said that ‘recent events’ there didn’t call for a change in strategy, while Constancio warned that ‘we all know about the big challenges they face, so that is a situation we monitor closely’, but hinted that no immediate shift in policy would be needed for now. Fischer was a bit more moderate in his view, noting that the Fed is monitoring developments there more closely than usual.

Prior to the commentary on the weekend, it felt like markets entered something of a calmer state on Friday relative to the volatility of the prior ten days in particular. The S&P 500 (+0.06%) finished virtually unchanged at the close having traded in a much tighter range, although in turn posted its best three-day gain (+6.5%) since November 2011. Despite trading over 5% down part way through the week, the index managed to finish in positive territory (+0.91%) for the five days, while the VIX, having closed unchanged on Friday actually managed to retreat over 50% from Monday’s intraday highs. With little change in European equity markets too (Stoxx 600 +0.28%, DAX -0.17%, CAC +0.36%), Friday’s notable price mover was again in the oil complex where we saw WTI (+6.25%) cap its biggest two-day gain since January 2009 (+17%) after climbing to $45.22/bbl, seemingly on the back on further momentum from Thursday’s gains. There was a similar rally for Brent (+5.24%) also, while the rest of the commodity space generally had a strong session with the likes of Gold (+0.76%), Aluminum (+2.76%), Zinc (+3.28%) and Lead (+3.22%) all up.

Fischer’s comments on Friday helped support another strong day for the Dollar, with Dollar index closing up 0.52% to cap a rally of nearly 3% since Monday. There was little change in 10y Treasury yields (-0.3bps) at Friday’s close, finishing the week at 2.182% and 28bps off Monday’s intraday lows. Friday’s economic data contributed to the fairly benign price action. Much of the focus was on the July PCE readings where both the deflator (+0.1% mom) and core (+0.1% mom) prints came in line with market expectations. There was some disappointment in the August University of Michigan consumer sentiment print which was revised down 1pt to 91.9, while personal income (+0.4% mom vs. expected) and spending (+0.3% mom vs. +0.4% expected) were slightly mixed.

Over in Europe we got a slightly higher than expected inflation reading out of Germany for August, with the 0.0% mom (vs. -0.1% expected) print keeping the annualized rate at +0.2% yoy after forecasts for a slight drop to 0.1%. Euro area confidence indicators were a lot more mixed for the month, with better than expected economic (104.2 vs. 103.8 expected) and services (10.2 vs. 8.8 expected) readings, but softer industrial (-3.7 vs. -3.2 expected) and business climate (0.21 vs. 0.34 expected) indicators. UK Q2 GDP offered little in the way of surprise, unrevised at +0.7% qoq as expected with the annualized rate at +2.6% yoy.

Staying in Europe, as well as the obvious Fed progress to watch in September, Greece’s election campaign is set to garner further attention as we approach the end of the month. The first set of polls released over the weekend suggest that support for Tsipras’ Syriza party is dwindling somewhat. A poll run for Agora newspaper showed Syriza with 24.6% of total votes, a lead of 1.8% over New Democracy while a poll for Alpha TV showed Syriza with a lead of 2.1% and a Proto Thema poll suggested the lead is as small as 1.5%, opening up the possibility of messy coalition talks and a long way from the 15% lead Syriza held over its main rival back in May.

end

Sunday night 9:30 pm/(Monday morning 9:30 am Shanghai time): Chinese markets open. Stocks open down 2.1% as China arrests 4 major citizens.

courtesy zero hedge)

Chinese Stocks Slump After “Arrest-Fest”, Yuan Strengthens Most In 9 Months, Goldman Cuts Outlook

Update: So much for the “no more intervention” Since the government bailout fund has run dry of money, the brokerages have to step up – CHINA SAID TO ORDER BROKERAGES TO BOOST STOCK MARKET SUPPORT

A busy weekend in Asia was dominated by mayhem in Malaysia, and witch-huntery in China. Chinese authorities began a wide-scale crackdown on rumor-mongerers, arrested journalists, and even detained a regulator for insider trading, as they lifted loan caps on the banking system at the same as withdrawing (verbally) support for the stock market. China strengthen the Yuan fix by 0.15% to 6.3893 – this is the biggest 2-day strengthening of the Yuan fix since Nov 2014. Then just to rub some more salt in the wounds, Goldman cut China growth expectations to 6.4% and 6.1% respectively for the next 2 years. Chinese stocks are opening modestly lower (SHCOMP -01.8%).

- *SHANGHAI COMPOSITE INDEX FALLS 1.8% AT OPEN

- *CHINA’S CSI 300 INDEX SET TO OPEN DOWN 1% TO 3,307.40

Yuan fixed stronger for 2nd day in a row…

- *CHINA SETS YUAN REFERENCE RATE AT 6.3893 AGAINST U.S. DOLLAR

- *CHINA RAISES YUAN REFERENCE RATE BY 0.15% TO 6.3893/USD

Then Goldman slahes China growth…

- *CHINA 2016 GDP GROWTH FORECAST CUT TO 6.4% VS 6.7% AT GOLDMAN

- *CHINA 2017 GDP GROWTH FORECAST CUT TO 6.1% VS 6.5% AT GOLDMAN

- *CHINA 2018 GDP GROWTH FORECAST CUT TO 5.8% VS 6.2% AT GOLDMAN

A “double-dip” in China’s growth in 2015…

China’s economic growth was very weak in early 2015, reflecting a combination of slowing money/credit growth, reform-driven fiscal tightening, and an appreciating CNY, among other factors. Policy easing starting in March seemed to help revive growth in May and especially June. But growth has slowed anew in July and August, prompting market and policymaker concerns and a further spate of easing measures. We retain our 2015 real GDP growth forecast of 6.8%, but note that alternative indicators of activity suggest a sharper slowdown, and mark down our 2016/17/18 forecasts to 6.4%/6.1%/5.8% respectively from 6.7%/6.5%/6.2% previously. We now expect short-term interest rates to fall further, to 1.5% by end-2016 (from 2.25% previously).

…and increased policy uncertainty…

Policy uncertainty has increased. Measures to contain local governments’ off-balance sheet financing have taken a back seat for now to a focus on reviving infrastructure spending. Equity market volatility has been large, diminishing the near-term potential for this channel to reduce reliance on debt financing. The snap 3% depreciation in the CNY is small in a macro context, but represents the sharpest weakening in two decades that were dominated by stability/appreciation vs USD, and has prompted an acceleration in capital outflows, heightening the risk of a larger move down the road.

But before all that, this happened…

First, as The FT reports, China “says” it will abandon buying stocks...

China’s government has decided to abandon attempts to boost the stock market through large-scale share purchases, and will instead intensify efforts to find and punish those suspected of “destabilising the market”, according to senior officials.

For two months, a “national team” of state-owned investment funds and institutions has collectively spent about $200bn trying to prop up a market that is still down 37 per cent since its mid-June peak.

…

Traders and officials said the latest intervention was aimed at providing a “positive market environment” in preparation for a big military parade this week to celebrate the 70th anniversary of the “victory of the Chinese people’s war of resistance against Japanese aggression”.

Senior financial regulatory officials insist that this was an anomaly, and that the government will refrain from further large-scale buying of equities.

Which could be a problem as all that stopped total and utter carnage last week was their buying…

But then they unleashed full scale fractional reserve banking…

- *SCRAPPING OF LOAN CAP TO HELP STABILIZING ECO GROWTH: FIN. NEWS

Though we suspect this is as much use as a chocalate fireguard for the already maximally-indebted Chinese public.

But nothing stops the propaganda from flowing…

- *CHINA ECO FUNDAMENTALS BETTER THAN OTHER MAJOR ECONOMIES: 21ST

As authorities begin wide-scale crackdowns on rumor-mongers and nay-sayers…

- *CHINA DETAINS REPORTER ON SUSPECTED SPREADING RUMORS: XINHUA

- *CHINA DETAINS CSRC OFFICIAL ON SUSPECTED INSIDER TRADING:XINHUA

In a worrying signal for global investors with a presence in China, some officials have argued strongly for a crackdown on “foreign forces”, which they say have intentionally unsettled the market.

“If our own people have collaborated with foreign forces to attack the soft underbelly of the market and bet against the government’s stabilisation measures then they should be suspected of harming national financial security and we must take resolute measures to subdue them,”said an editorial in the state-controlled Securities Daily newspaper last week.

As SCMP’s Goerge Chen details…

Chinese authorities have held several people, including a journalist, an official of China’s securities watchdog and four senior executives of China’s major securities dealer for stock market violations.

Wang Xiaolu, journalist of Caijing Magazine, has been placed under “criminal compulsory measures” for suspected violations of colluding with others and fabricating and spreading fake information on securities and futures market, Xinhua learned on Sunday.

Wang confessed that he wrote fake report on Chinese stock market based on hearsay and his own subjective guesses without conducting due verifications.

He admitted that the false information have “caused panics and disorder at stock market, seriously undermined the market confidence, and inflicted huge losses on the country and investors.”

Also put under “criminal compulsory measures” were Liu Shufan, an official with China Securities Regulatory Commission.He is held over suspicions of insider dealings, taking bribes and forging official seals.

According to Liu’s confession during the investigation, he has taken advantage of his position to secure an approval from the securities authorities for a public company and help the growth of the company’s shares.

In return, the head of the company offered bribes worth several million yuan to him.

Also, Liu has used insider information from the above-mentioned company and another company and obtained millions of yuan of illegal gains, according to his confession.

Liu confessed that he has forged official seals to fake a court ruling on divorce and taxation certificates for his mistress.

Xinhua also learned from authorities that Xu Gang, Liu Wei, Fang Qingli and Chen Rongjie, senior executives of the Citic Securities, China’s leading securities dealer, have been put under “criminal compulsory measures” for suspected insider trading. They have also confessed to their violations.

“Compulsory measures” may include arrest, detention, issuing a warrant to compel a suspect to appear, bail pending trial, or residential surveillance.

* * *

Way to go China – “open” those markets up to anyone (as long as they are buying)

Charts: Bloomberg

end

Evercore reports that the real GDP of China is -1.1%

(courtesy Evercore/zero hedge)

China Stunner: Real GDP Is Now A Negative -1.1%, Evercore ISI Calculates

With Chinese data now an official farce even among Wall Street economists, tenured academics, and all others whose job obligation it is to accept and never question the lies they are fed, the biggest question over the past year has been just what is China’s real, and rapidly slowing, GDP – which alongside the Fed, is the primary catalyst of the global risk shakeout experienced in recent weeks.

One thing that everyone knows and can agree on, is that it isnot the official 7% number, or whatever goalseeked fabrication the communist party tries to push to a world that has realized China can’t even manipulate its stock market higher, let alone its economy.

But what is it? Over the past few months we have shown various unpleasant estimates, the lowest of which was 1.6% back in April.

Today we got the worst one yet, courtesy of Evercore ISI, which using its own GDP equivalent index – the Synthetic Growth Index (SGI) – gets a vastly different result from the official one, namely Chinese growth of -1.1% annually. Or rather, contraction.

To wit, from Evercore:

Our proprietary Synthetic Growth Index (SG!) fell 1.1% mim in July, and was also down 1.1% y/y. No wonderglobal commodities are so weak. The most recent 18 months have been much weakerthan the 2011-13 period. Even if we adjust our SG I upward (for too-little representation of Services — lack of data), we believe actual economic growth in China is far below the official 7.0% yly. And, it is not improving, Most worrisome to us; the ‘equipment’ portion of Plant & Equipment spending is very weak, a bad sign for any company or country. Expect more monetary and fiscal steps to lift growth.

And here is why the world is in big trouble.

Citigroup Chief Economist Thinks Only “Helicopter Money” Can Save The World Now

Having recently explained (in great detail) why QE4 (and 5, 6 & 7) were inevitable (despite the protestations of all central planners, except for perhaps Kocharlakota – who never met an economy he didn’t want to throw free money at), we found it fascinating that no lessor purveyor of the status quo’s view of the world – Citigroup’s chief economist Willem Buiter – that a global recession is imminent and nothing but a major blast of fiscal spending financed by outright “helicopter” money from the central banks will avert the deepening crisis. Faced with China’s ‘Quantitative Tightening’, the economist who proclaimed “gold is a 6000-year old bubble” and cash should be banned, concludes ominously,“everybody will be adversely affected.”

China has bungled its attempt to slow the economy gently and is sliding into “imminent recession”, threatening to take the world with it over coming months, Citigroup has warned. As The Telegraph’s Ambrose Evans-Pritchard reports, Willem Buiter, the bank’s chief economist, said the country needs a major blast of fiscal spending financed by outright “helicopter” money from the bank to avert a deepening crisis.

Speaking on a panel at the Council of Foreign Relations in New York, Mr Buiter said the dollar will “go through the roof” if the US Federal Reserve lifts interest rates this year, compounding the crisis for emerging markets.

“So why it matters is that the competence of the Chinese authorities as managers of the macro economy is really in question – the messing around with monetary policy, the hinting on doing things on the fiscal side through the policy banks. But I think the only thing that is likely to stop China from going into, I think, recession – which is, you know, 4 percent growth on the official data, the mendacious official data, for a year or so – is a large consumption-oriented fiscal stimulus, funded through the central government and preferably monetized by the People’s Bank of China.

Well, they’re not ready for that yet. Despite, I think, the economy crying out for it, the Chinese leadership is not ready for this.

So I think they will respond, but they will respond too late to avoid a recession, and which is likely to drag the global economy with it down to a global growth rate below 2 percent, which is my definition of a global recession. Not every country needs go into recession. The U.S. might well avoid it. But everybody will be adversely affected.”

Or translated from ‘economist’ to English – a massive helicopter drop of cash (well 1s and 0s) into the inflating hands of Chinese soon-to-be-consumers is all that can the world from another recession… and The Chinese leadership may need to stare into the abyss before they actually pull the trigger. Just think of the pork prices?

Mr Buiter had some more to add on the idiocy of Chinese Equity markets. He said the stock market crash in Shanghai and Shenzhen…

…is a sideshow. Consumption effects, you know, wealth effects, minor. Almost no capex in China is funded through share issue. And so it is a symbol of the policy failure rather than intrinsically economically important.

China’s problems are excessive leverage in the corporate sector, in the local government sector, and the very fragile banking system, and shadow banking system. As Chen pointed out, it won’t be allowed to collapse because it is underwritten by the government, but it won’t be a source of great funding strength.

There is excess capacity and a pathetically low rate of return on capital expenditure, right?Invest 50 percent of GDP and get, even in the official data, 7 percent growth. The true data is probably something closer to 4 ½ percent or less. So it is an economy that, I think, is sliding into recession.

And what the stock market reminds us of, I think, especially this sequence of thegovernment first cheerleading the stock market boom and bubble – because quite a few of the local pundits believed that this was a great way of deleveraging without paying for the corporate sector, to have a stock market bubble. And then, of course, the rather panicky and incompetent reaction in response.

So, once again, why it matters is that the competence of the Chinese authorities as managers of the macro economy is really in question.

* * *

So, it seems, all of a sudden – despite the permabulls, asset-gatherers, and commission-takers saying otherwise – China matters! As Bloomberg notes,China’s deepening struggles are starting to make a bigger dent in the global economic outlook.

“We’re seeing evidence that the slowdown is broader than expected” in China, saidMarie Diron, a London-based senior vice president at Moody’s and one of the report’s authors. “It’s long been clear that there’s a slowdown in the manufacturing and construction sector, but the service sector was more resilient. That’s still the case, but we’re seeing some signs of weakness in the labor market.”

“We continue to believe that the greatest risks to our growth forecasts remain to the downside,” Schofield wrote. Actual growth is “probably even lower” because of “likely mis-measurement in China’s official data,” he wrote.

* * *

Which, is exactly what we have been saying for the last 2 years as the rolling collapse of China’s ponzi becomes ever more evident (and hidden by ever more manipulation)…

Here, for those curious, are links to previous discussions:

- China Dumps Record $143 Billion In US Treasurys In Three Months Via Belgium

- China’s Record Dumping Of US Treasuries Leaves Goldman Speechless

- How The Petrodollar Quietly Died And Nobody Noticed

- Why It Really All Comes Down To The Death Of The Petrodollar

- Devaluation Stunner: China Has Dumped $100 Billion In Treasurys In The Past Two Weeks

- What China’s Treasury Liquidation Means: $1 Trillion QE In Reverse

- It’s Official: China Confirms It Has Begun Liquidating Treasuries, Warns Washington

And so on and so forth.

In short, stabilizing the currency in the wake of the August 11 devaluation has precipitated the liquidation of more than $100 billion in USTs in the space of just two weeks, doubling the total sold during the first half of the year.

In the end, the estimated size of the RMB carry trade could mean that before it’s all over, China will liquidate as much as $1 trillion in US paper, which, as we noted on Thursday evening, would effectively negate 60% of QE3 and put somewhere in the neighborhood of 200bps worth of upward pressure on 10Y yields.

And don’t forget, this is just China.

…

The potential for more China outflows is huge: set against 3.6trio of reserves (recorded as an “asset” in the international investment position data), China has around 2trillion of “non-sticky” liabilities including speculative carry trades, debt and equity inflows, deposits by and loans from foreigners that could be a source of outflows . The bottom line is that markets may fear that QT has much more to go.

What could turn sentiment more positive? The first is other central banks coming in to fill the gap that the PBoC is leaving. China’s QT would need to be replaced by higher QE elsewhere, with the ECB and BoJ being the most notable candidates. The alternative would be for China’s capital outflows to stop or at least slow down. Perhaps a combination of aggressive PBoC easing and more confidence in the domestic economy would be sufficient, absent a sharp devaluation of the currency to a new stable. Either way, it is hard to become very optimistic on global risk appetite until a solution is found to China’s evolving QT.

* * *

China “Punishes” Hundreds For “Maliciously” Manipulating The Market

The deadly chemical blast in the Chinese port of Tianjin was a preventable catastrophe in which more than 100 people lost their lives thanks in part to what looks like the political connections of the warehouse’s owners and although an upfront, transparent investigation and honest assessment of the environmental impact is likely the only way to safeguard the public and ensure it doesn’t happen again, no one believes the Chinese government has the will to conduct such an investigation.

But whatever you do, do not say any of the above if you live in China.

Similarly, China’s stock market collapse was an entirely preventable financial catastrophe caused by the unchecked accumulation of margin debt and the encouragement of speculation, and the bursting of the equity bubble which began in June has been nothing short of a debacle that’s led to international condemnation and accusations that, even in a centrally planned world, Beijing’s particular brand of intervention is so egregious as to stray outside the bounds of manipulated market decorum.

But if you live in China, don’t say that either.

Over the last two months there were signs that Beijing would soon resort to outright, sweeping censorship as it relates to both the stock market and the Tianjin blast. For instance, in July, phrases like “rescue the market” were reportedly banned and in the wake of the Tianjin disaster, hundreds of social media accounts were shut down for spreading “blast rumors.”

Now, ahead of a military parade that Xi Jinping will allegedly use to show the world that the Chinese lion “has woken up” (albeit with the amusing caveat that the lion is “peaceful, pleasant and civilized”), the Politburo apparently has seen just about enough criticism for its handling of the stock market collapse and the Tianjin blasts and as WSJ reports, more than 200 people have now been “punished” for their alleged role in “mislead[ing] society and the public, generat[ing] and spread[ing] fearful sentiment, and even us[ing] the opportunity to maliciously concoct rumors to attack [the] Party and national leaders.” Here’s more:

The sweep targeted people who the government said spread false Internet rumors regarding events such as the stock-market turmoil and deadly explosions earlier this month in the port city of Tianjin, the Ministry of Public Security said Sunday.

The government is facing intense public scrutiny in China over its management of the slowing economy and turbulent markets, as well as public anger over the blasts at a hazardous-chemical warehouse in Tianjin.

In its statement, the public-security ministry didn’t identify most of the 197 alleged offenders, giving only surnames for some of them. The statement quoted four people, identified only by their surnames, as expressing regret for spreading false information. It didn’t elaborate further on individual offenses and punishment, except to note that 165 online websites and accounts were shut down.

Statements described by the ministry as false included rumors that a man jumped to his death in Beijing because of the stock market slump, claims that at least 1,300 people were killed in the Tianjin blasts, and inflammatory rumors related to China’s commemorations of the 70th anniversary of victory in World War II.

Sunday’s statement came just weeks after the Cyberspace Administration of China said it shut down 18 websites permanently and suspended another 32 websites for a month for allegedly publishing unverified information or letting users spread groundless gossip related to the Aug. 12 explosions in Tianjin, which killed at least 150 people and injured more than 700.

China has also officially confirmed what multiple news outlets reported late last week. Namely that a journalist at Caixin and a prominent investment banker had been detained in connection with spreading “rumors” and “illegal trading.”From WSJ again:

In the case of Mr. Wang, the Caijing reporter, Xinhua said an alleged fabrication was a July 20 report saying the China Securities Regulatory Commission was studying a withdrawal of government funds used to stabilize the domestic stock market amid a broad-based slump.

Mr. Wang told investigators he wrote the report by combining market-related information with his own “subjective assessment.” More specifically, Wang says he“obtained the information [about the possible scaling back of CSF’s plunge protection buying] through the abnormal channel of gleaning, in private, information about the market.”

So essentially, Wang’s criminal behavior amounted to reading publicly available information in “private” (which we presume means “at his desk”), drawing conclusions, and writing a story, which is of course contrary to the tried and true method of journalism in China wherein Beijing sends journalists a dispatch telling them what to say and then journalists just regurgitate it.