Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1138.10 up $20.10 (comex closing time)

Silver $15.15 up 18 cents.

In the access market 5:15 pm

Gold $1138.95

Silver: $15.16

First, here is an outline of what will be discussed tonight:

At the gold comex today we had a poor delivery day, registering 0 notices for nil ounces Silver saw 112 notice for 560,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 213.926 tonnes for a loss of 89 tonnes over that period.

In silver, the open interest fell by 2,061 contracts despite the fact that silver was up in price by 10 cents yesterday. Again, our banker friends tried to use the opportunity to cover as many silver shorts. They must be really frightened as to what might happen in a default situation. The total silver OI now rests at 152,327 contracts In ounces, the OI is still represented by .761 billion oz or 109% of annual global silver production (ex Russia ex China).

In silver we had 112 notices served upon for 560,000 oz.

In gold, the total comex gold OI fell to 414,115 for a loss of 174 contracts. We had 0 notices filed for nil oz today.

We had no changes in tonnage at the GLD, thus the inventory rests tonight at 678.18 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had no change in silver inventory at the SLV/Inventory rests at 320.915 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by 2,061 contracts down to 152,327 despite the fact that silver was up by 10 cents in price with respect to yesterday’s trading. The total OI for gold fell by 174 contracts to 414,115 contracts, as gold was down $1.90 yesterday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. COT report (Harvey)

4. China opens for trading 9:30 pm est Thursday night/Friday morning 9:30 Shanghai time

(zero hedge)

12. USA stories/Trading of equities NY

a) Futures on NY drop immediately after Gartman signals that he is going long!

(zero hedge)

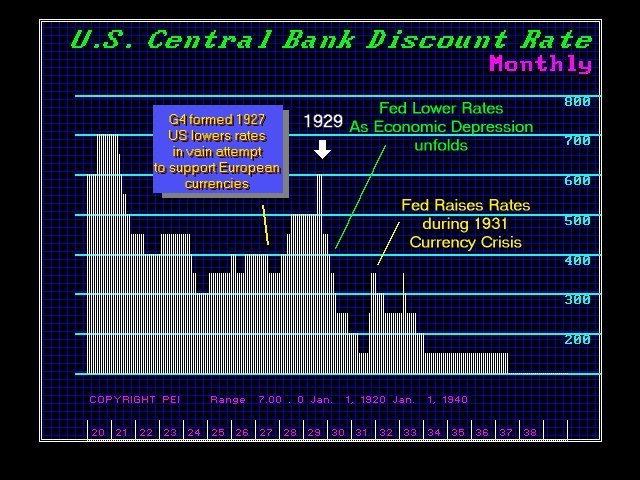

b Martin Armstrong believes that the USA has made a terrible policy error with their FOMC no rate cut similar to that of 1927

(Armstrong)

c)

13. Physical stories

i)Another lawsuit on the rigging of treasuries, libor etc

(Bloomberg)

ii) Jessie of Americain cafe: why you must own gold

iii) Alasdair Macleod comments on gold as money

(Alasdair Macleod)

iv) Another example of devastation in the gold mining area:

(Helen Thomas/Wall Street Journal)

v) Peter Cooper/Arabian money/the perfect storm for gold and silver brewing.

vi) Bill Holter comments as he responds to Bron Sucheki

(Bill Holter-Holter Sinclair collaboration)

14. This week’s wrap courtesy of Greg Hunter/USAWatchdog/

and well as other commentaries…

Let us head over and see the comex results for today.

September contract month:

Initial standings

September 17.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 95.110 oz Delaware |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz (nil) | |

| No of oz served (contracts) today | 0 contracts (nil oz) |

| No of oz to be served (notices) | 91 contracts (9,100 oz) |

| Total monthly oz gold served (contracts) so far this month | 24 contracts(2,400 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 380,912.81 oz |

Total customer deposit: nil oz

JPMorgan has only 0.3350 tonnes left in its registered or dealer inventory. (10,777.29 oz) and only 874,018.71 oz in its customer (eligible) account or 27.18 tonnes

September silver initial standings

September 17/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 101,140.35 oz(CNT,Brinks) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1,123,379.715 oz JPMorgan, HSBC,Brinks,CNTDelaware |

| No of oz served (contracts) | 112 contracts (560,000 oz) |

| No of oz to be served (notices) | 259 contracts (1,285,000 oz) |

| Total monthly oz silver served (contracts) | 1206 contracts (6,030,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 603,500.075 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 17,747,362.5 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: 1,123,379.715 oz

total withdrawals from customer: 101,140.35 oz

And now SLV:

Sept 18.2015; no changes in inventory at the SLV/inventory rests at 320.915 million oz

sept 17.2017:no change in inventory at the SLV/rest tonight at 320.915

million oz/

sept 16.2015: no change in inventory at the SLV/rests tonight at 320.915 million oz/

Sept 15./no change in inventory at the SLV/rests tonight at 320.915 million oz

Sept 14./we had another withdrawal of 1.145 million oz from the SLV/Inventory rests at 320.915 million oz

Sept 11.2015: no changes in silver inventory at the SLV/inventory rests at 322.06 million oz

Sept 10.2015: we had no changes in silver inventory at the SLV/rests tonight at 322.06 million oz

Sept 9.2015:

we had another huge withdrawal of 1.336 million oz of silver from the vaults of the SLV/Inventory rests at 322.06 million oz

Sept 8/we had a huge withdrawal of 1.524 million oz of silver from the SLV/Inventory rests tonight at 323.396 million oz.

Sept 4.2015:no changes in inventory at the SLV/rests tonight at 324.923 million oz

sept 3/we had a small withdrawal of 140,000 oz of silver from the SLV/Inventory rests at 324.923 million oz

Sept 2: we had a small withdrawal of 859,000 oz of silver from the SLV vaults/inventory rests tonight at 325.063 million oz

September 1/no change in inventory over at the SLV/Inventory rests tonight at 325.922 million oz

August 31.a huge addition of 954,000 oz were added to inventory today at the SLV/Inventory rests at 325.922 million oz

August 28.2015: no change in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 27.no change in inventory at the SLV/Inventory rests at 324.698 million oz

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 174,225 | 134,678 | 51,513 | 154,988 | 187,967 | 380,726 | 374,158 |

| Change from Prior Reporting Period | ||||||

| -9,390 | 10,356 | 2,630 | -632 | -23,632 | -7,392 | -10,646 |

| Traders | ||||||

| 118 | 119 | 96 | 44 | 52 | 209 | 227 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 32,607 | 39,175 | 413,333 | ||||

| -1,007 | 2,247 | -8,399 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, September 15, 2015 | |||||

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 60,443 | 46,180 | 14,576 | 61,170 | 82,527 | |

| 1,682 | 6,160 | -368 | 175 | -4,028 | |

| Traders | |||||

| 83 | 57 | 35 | 45 | 39 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 158,007 | Long | Short | |

| 21,818 | 14,724 | 136,189 | 143,283 | ||

| 903 | 628 | 2,392 | 1,489 | 1,764 | |

| non reportable positions | Positions as of: | 142 | 120 | ||

| Tuesday, September 15, 2015 | © Silv | ||||

just take a look at the premiums on gold/silver coins!!

(courtesy/Mark O’Byrne/Goldcore)

Gold and Silver Coins, Bars See Very Robust Demand – Delays and Premiums Rising

- Demand for physical gold this month at “a historically high level” – HSBC

- Q3 U.S. Mint gold sales set to dwarf those of previous two quarters

- Supply of physical silver “continues to be tight” and premiums rising

- China and India demand remains very strong

- Seasonal Asian buyers to add to demand in coming weeks

- Dovish Fed bullish for gold

Demand for physical gold and silver in August and September has been exceptionally strong as investors seek a safe-haven from market turmoil, as the global economy slows down and as it becomes clear that the Federal Reserve and central banks generally are slowly losing credibility and ultra loose monetary policies are set to continue for the foreseeable future.

BULLION COIN & BAR PREMIUMS & AVAILABILITY – September 18, 2015

| GOLD | PREMIUMS | AVAILABILITY |

| Gold Bars (1 oz – Perth Mint) | 3.75% | In Stock |

| Gold Bars (1 oz) | 4% | In Stock |

| Gold Bars (10 oz) | 3.75% | Delivery Delay – 5 Days |

| Gold Bars (1 kilo) | 2.00% | Delivery Delay – 5 Days |

| Gold Maples (1 oz) | 4.25% | Delivery Delay – 5 Days |

| Gold Eagles (1 oz) | 5% | Delivery Delay – 5 Days |

| Gold Krugerrands (1 oz) | 4.25% | In Stock |

| Gold Philharmonics (1 oz) | 5.00% | In Stock |

| Gold Buffalos ( 1 oz) | 5.00% | In Stock |

| Gold Sovereigns (0.2354 oz) | 8.50% | 2015 In Stock |

| Gold Sovereigns (0.2354 oz – Pre 1933) | 9.00% | Not available in volume |

| SILVER | PREMIUMS | AVAILABILITY |

| Silver Bars (100 oz Generic) | 9.50% | Delivery Delay – October 4 |

| Silver Bars (100 oz LBMA – Asahi Refinery) | 9% | Delivery Delay – Nov 9 |

| Silver Bars (1000 oz) | 5.50% | Delivery Delay – 1 to 15 Days |

| Silver Eagles (1 oz) | 35% | Not Available |

| Silver Maples (1 oz) | 25% | Delivery Delay – Unknown |

Note: Given continuing and deepening delays for certain popular bullion coins and bars and rising premiums we believe it is important to keep our clients and subscribers aware of the most up to date premiums and availability. The prices quoted are indicative and can change at any time. We continue to be one of the most competitive bullion dealers internationally. The premiums quoted are for smaller orders and there are volume discounts and lower premiums on larger orders..

HSBC described gold demand from the U.S. Mint as being at a “historically high level” which indeed it has been. The bank report that the Mint has sold 322,000 ounces of gold in the first half of this month.

Of this, only 91,000 ounces were made up of Gold Eagle coins – the most popular coin with retail investors – although some market participants believe that some of the stock may be being accumulated by large institutional investors.

And yet, demand for gold eagles is still very strong with demand in Q3 set to dwarf demand of the previous two quarters. With two weeks still to go, total Gold Eagle coin sales have been a staggering 352,500 ounces.

That compares with sales of 146,000 oz in Q1 and 127,000 oz in Q2. So far this year Gold Eagle sales are almost 20% higher than last years total sales of 524,500 oz.

Silver eagle supply continues to be very tight with long delays and a lack of clarity about when supply will be available again. Premiums on Eagles have surged and some are selling for as much as 40% or more than $6 per coin over spot. Dealers report “unprecedented” demand for large silver bars.

Silver maples are on small weekly allocations and silver bars are also becoming difficult to source in volume. The release of the 2016 Australian 1 oz silver .9999 Kangaroo, intended to compete with the Eagle/Maple is already in such demand that the Perth Mint is rationing supply to large dealers.

Production on other 2016 silver products has been delayed by the Australian mint to maintain production levels on the Kangaroo due to very strong global demand.

At the same time the traditional months of strong demand from Asia are now ahead of us which will add even greater demand for gold in the coming weeks. In India, gold demand will reach its peak later than usual this year as Diwali falls in the second week of November.

Premiums for physical gold in China have risen from $4 per ounce to as high as $6 this indicating very strong demand in China. As do withdrawals from the Shanghai Gold Exchange.

The incredibly strong demand for physical precious metals around the world continues to be obscured by institutional selling of futures contracts on the COMEX. The paper or electronic market continues to dominate the spot price for now. But rising premiums and delays for popular bullion products suggests that proper price discovery reflecting real world supply and demand may be at hand.

However, it is clear both from the enormous demand and from the shortages in the precious metals markets that many investors are becoming nervous about the markets and the state of the global economy.

We advise our readers, as always, to acquire physical gold and to store it outside of the banking system in safer jurisdictions internationally.

DAILY PRICES

Today’s Gold Prices: USD 1136.00, EUR 992.31 and GBP 726.25 per ounce.

Yesterday’s Gold Prices: 1118.15, EUR 987.46 and GBP 720.64 per ounce.

(LBMA AM)

Gold rose nearly 1% or $11.60 to $1,131.30 while silver gained 1.4% or 20 cents to $15.11 an ounce on the COMEX just before the Federal Reserve interest rate announcement yesterday.

Gold in Singapore dipped lower but in European trade gold was moved higher again and is now above $1,140 per ounce. Silver bullion has ticked another 0.8% higher to $15.35 today. Platinum and palladium are slightly lower today.

Gold is headed for a 3 percent weekly gain and silver for a 5.5% weekly gain.

The Federal Reserve kept interest rates unchanged yesterday due to increasing concerns about the global economy and financial market volatility. The sluggish U.S. economy may also have played a role in the decision but this was not signalled.

In what amounted to a somewhat embarrassing volte face, Yellen said developments in a tightly linked global economy had in effect forced the U.S. central bank’s hand. “The outlook abroad appears to have become less certain,” Yellen understatedly told a news conference as gold prices ticked higher.

Yellen was more dovish than expected which is bullish for gold and suggests that the long awaited for bottom for gold may have occurred in early August prior to recent market volatility.

The longer interest rates stay at these record low levels, the better for gold.

IMPORTANT NEWS

FTSE falters after Fed but gold shines as dollar falls – The Guardian

Gold Gets Saved (This Time) by the Fed as Rate Rise Is Deferred – Bloomberg

Gold jumps to 2-week high as Fed holds U.S. rates steady – Reuters

Gold prices head higher after Fed stands pat on rates – MarketWatch

Gold price rallies after Fed holds rates steady – Mining.com

IMPORTANT COMMENTARY

World May Soon Need “QE For The People” – The Telegraph

Corbyn’s QE for the people is exactly what the world may need – The Telegraph

This Is What Yellen Said About Negative Rates Coming To The US – Zero Hedge

VIX Crushed As Bonds & Bullion Rip, USDollar & Stocks Slip – Zero Hedge

Britain’s economic Achilles heel – MoneyWeek

end

For those of you who want to get a handle on what on earth is going on this conference should be just the place to attend.

(courtesy Chris Powell/GATA)

Please join GATA in New Orleans in October — you really can’t lose

Submitted by cpowell on Thu, 2015-09-17 20:29. Section: Daily Dispatches

4:28p ET Thursday, September 17, 2015

Dear Friend of GATA and Gold:

With recent equity market crashes, China’s devaluation, Greece’s bankruptcy, the European Union’s dissolution, the collapse of commodity prices and world trade, and ever-more-obvious central bank interventions against gold, the world financial system may be approaching a turning point — just as the annual New Orleans Investment Conference convenes, from Wednesday through Saturday, October 28-31. If, as some observers suspect, the monetary metals are turning around and about to start exacting their revenge on market-rigging central banks and their investment bank agents, New Orleans will be the place to be.

Once again GATA Chairman Bill Murphy and your secretary/treasurer will be speaking in New Orleans. We’ll be joined by many renowned market analysts and critical thinkers, including the columnists Mark Steyn and Charles Krauthammer; fund manager, best-selling author, geopolitical strategist, and gold market analyst Jim Rickards; newsletter editor Marc Faber; contrarian and provocateur Doug Casey; and Adrian Day, Frank Holmes, Marin Katusa, Brent Cook, Mary Anne and Pamela Aden, Mark Skousen, Eric Coffin, Ian McAvity, and many others.

But of course New Orleans itself is always one of the stars of the show. The conference again will be held at the Hilton New Orleans Riverside hotel, on the Riverwalk along the Mississippi, across the street from Harrah’s casino, adjacent to the city’s trolley line, and a short walk from the French Quarter, beautiful Jackson Square, and many wonderful restaurants and museums.

New Orleans is not a free conference, but GATA supporters really can’t lose on it.

In the first place, if you use the GATA-aligned link below for registration and enter “FREEGOLDCLUB” in the promotional field, you’ll be given free membership in the conference’s Gold Club, entitling you to entry to the conference’s special private viewing area with day-long coffee service, exclusive question-and-answer sessions with select speakers following their presentations, copies of special reports and investment information, discounts on conference compact discs and video discs, and more.

Further, the conference offers you a financial guarantee: If you attend and within six months have not earned back, because of your attendance, at least four times your registration fee, the conference will refund it to you. (Of course you’d still be out your lodging expenses, but you’ll have had a great time in New Orleans.)

There’s another special reason for GATA supporters to attend the conference: The conference will make a donation to GATA for every GATA supporter who attends.

The New Orleans Investment Conference long has been important to GATA, giving us a forum among some hugely influential people. It’s more important than ever for us to show that the cause of free and transparent markets and limited and accountable government endures and indeed still offers the world its best hope for prosperity.

So please consider joining GATA in New Orleans by learning about and registering for the conference here:

https://jeffersoncompanies.com/landing/gata

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy Peter Cooper/Arabian money)

‘Mini-perfect storm’ for gold and a positive hurricane brewing for silver

Posted on 18 September 2015 with no comments from readers

Gold futures climbed again on Friday and eyed a solid weekly gain of around three per cent or higher, with analysts giving the credit to the Federal Reserve’s decision to keep interest rates at historically low levels.

‘Gold seems to be holding on to gains, and perhaps this is a mini-perfect storm for gold,’ said William Adams, head of research for Fastmarkets, explaining that ‘prices are low, other asset classes are relative high and interest rates will stay down for longer.’

Silver hurricane?

But then if gold was doing well its volatile sister was outperforming to the upside with prices set for gains of more than five per cent for the week, and a positive hurricane seems to be brewing in the silver camp. Remember 2008-11 when silver jumped from $8 to $48.50 an ounce?

Gold for December delivery was up two per cent to $1,140 an ounce at the time of writing on Friday, while December silver had leapt to $15.40 an ounce.

Analysts led by Goldman Sachs had previously emphasized that higher interest rates would hurt gold because it doesn’t pay interest, meaning some investors would step away from it. Plus, higher rates lift the dollar and a stronger greenback can weigh on dollar-denominated commodities as they become pricier for holders of other currencies.

In the event the Fed was having none of this, and the weary business of trying to anticipate when it will finally raise rates must start again. However, more stormy global economic clouds ahead could now kick rate rises into the very long grass.

Great expectations

To turn Goldman’s somewhat dubious logic – as gold has often risen with interest rates in the past – on its head, then surely gold and silver prices have only one way to go absent interest rate rises.

Hedge funds and other momentum traders are always on the look out for trading positions like this, where you just buy and ride the momentum upwards. Could it be that stocks will now continue to head downwards while precious metals step up into the great blue yonder?

The trend is your friend, until it is not.

end

Of course it is rigged!! Everything is rigged!!

(courtesy Bloomberg)

Primary dealers rigged Treasury auctions, investor lawsuit says

Submitted by cpowell on Thu, 2015-09-17 17:04. Section: Daily Dispatches

By Alexandra Scaggs Matthew Leising

Bloomberg News

Thursday, September 17, 2015

The same analytical technique that uncovered cheating in currency markets and the Libor rates benchmark — resulting in about $20 billion of fines — suggests that the dealers who control the U.S. Treasury market rigged bond auctions for years, according to a lawsuit.

The analysis was part of a 115-page lawsuit filed in Manhattan federal court on Aug. 26 by Quinn Emmanuel Urquhart & Sullivan LLP and other law firms. The plaintiffs built their case against the 22 primary dealers who serve as the backbone of Treasury trading — including Goldman Sachs Group Inc., JPMorgan Chase & Co., and Morgan Stanley — using data from Rosa Abrantes-Metz, an adjunct associate professor at New York University who has provided expert testimony in rigging cases.

Her conclusion: More than two-thirds of a certain type of Treasury auction appear to have been rigged. She found issues with other auctions too. …

The new case is Cleveland Bakers and Teamsters Pension Fund v. Bank of Nova Scotia, 15-cv-06782, U.S. District Court, Southern District of New York (Manhattan).

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2015-09-17/primary-dealers-rigged

end

Alasdair Macleod’s commentary for the week, a must…

(courtesy Alasdair Macleod/GATA)

Gold remains money

- By Alasdair Macleod

- Posted 17 September 2015

We think we know that gold is no longer money, because Keynesians and monetarists insist it is so.

Furthermore, it has been replaced by government currencies, which we use to buy and sell, do our accounts and pay our taxes. While it is undoubtedly true that gold is no longer used for transactions in all but a few places in Asia, this common assumption has no basis in fact.

It is one thing for macroeconomists of all veins to theorise about the contents of the dustbin of history, but the choice people make is what really matters. Humanity has an infinite capacity for adapting and using what is either made available or forced upon them. But just because they have adapted and used government currencies as their circulating media, they have not always given up on gold as the money of choice to retain a store of value.

This article is written in the parochial confines of a welfare state that has advanced beyond regarding gold as money. The views of the people in Britain on this subject are probably similar to those in the other welfare states of Europe, North America and Japan. Those in the finance industries trained in macroeconomics and subscribing hook line and sinker to the relegation of gold to the rank of a plain commodity are relatively few: probably a few million world-wide at most. There are a greater number so dependent on the fiat money system that they would rather dismiss the issue instead of properly considering it, which to a lesser extent must also be true of the wider population which benefits from government welfare and spending.

The welfare system, based as it is on anything other than free markets, conflicts with the concept of sound money. People would rather not pay for everything through taxes, and money and credit inflation as a means of funding are a convenient cop-out. But it is plainly wrong to say the uncaring masses are anti-gold; it is more correct to describe them as not bothered one way or the other. Even most western gold-bugs, which in numbers probably balance the aforementioned macroeconomist establishment, vaguely regard gold as an insurance policy or speculative investment, rather than sound money only driven out of circulation by Gresham’s law.

So the combined population of the welfare states is not anti-gold at all, and the argument that progress in economic thinking has reduced its status to a plain commodity is not true. Nor is it true in South and Central America, where the US dollar is regarded as the sound money alternative to local currencies, only because people have adapted to what is available to them. Nor is it true in sub-Saharan Africa, where the majority of the population has its roots in subsistence farming and tribal communities. However, in Asia, where civilisations have long histories, the story is very different.

For centuries ordinary people from all walks of life are painfully aware that government money is ephemeral, and true money is gold. When the cumulative debasement of a currency leads to its replacement by another debasing currency, you continue to dump the government stuff for gold. This is the experience of the Turks, who faced a million-to-one consolidation of the lira in 2005. According to Wikipedia one gold lira coin could be sold for 154,400,000 old paper lira towards the end, and the new lira is still going down. Indian farmers and traders put their savings into gold, a wisdom borne out by the rupee’s continual devaluation over the years. Even the Chinese, after decades of communism and the brain-washing of the cultural revolution still persist in accumulating gold as the only sound money to tuck away for a rainy day.

To understand why the belief persists that gold is the ultimate money, you have to look back in time to appreciate its value before it was used as money. Anyone who has not been to Cairo and seen the 3,300 year old gold mask of Tutankhamen, and is unable to understand the feeling of awe that overcomes one’s emotions in its presence, must be devoid of all imagination. Not only has it endured an extraordinary length of time, it is in itself timeless, and unchanged from when it was fashioned: that’s some store of value.

Max Keiser of the eponymous show on RT told me of an occasion when he joined a debate on BBC Television about this very subject. He argued the case for gold, while an economist representing the prestigious Economist weekly journal argued against. Off-camera after the debate, the young economist was just as eager as anyone else in the studio to touch and feel the gold bar that had been brought into the studio as a prop.

That is the point: despite the theorising of macroeconomists and what governments with a vested interest force us to believe, gold has an enduring fascination for and a value to humanity. The majority of above-ground stocks are still wrought in the form of jewellery and the highest classification of ornaments. Gold’s durability and fungibility makes this unique material eminently suitable as the only sound money available to the human race.

The welfare states’ denial of this simple fact, and their insistence that their own inflating currencies are superior, is leading them towards economic disaster. They have committed themselves to the destruction of a basic human value, which they will never supress. Asian governments, many of which would undoubtedly like to take this route are forced by their people to be more realistic. Even government officials privately acknowledge the superiority of gold, and in the case of China they have actually encouraged their population to accumulate it.

This matters to us all, because the process of wealth creation is declining in the west, and accelerating in Asia. Furthermore, there are four billion Asians, the majority of which are either directly or indirectly involved in the economic union of the Shanghai Cooperation Organisation, and who have overwhelmingly become the world’s savers and wealth creators.

Government currencies come and go while human values endure. The adaptability of the human race will allow it to continue to use whatever is most convenient for day-to-day transactions. But the days of ordinary people in the welfare states blindly accepting fiat currencies as valid for storing the product of their labour, however temporary, are probably drawing to a close. The impossibility of our debt obligations, including the net present value of future welfare commitments, is catching up with us, and the requirement to debase these obligations is becoming paramount.

When this becomes obvious to growing numbers of the public in the welfare states, as it is bound to do, they will switch from no opinion on gold to having one. The derisory term for gold-bugs will disappear as their prescience emerges, and the price of physical metal measured in government currencies will reflect more properly its unique monetary quality.

end

Another example of devastation in the mining sector

(courtesy Helen Thomas/WallStreet/GATA)

Gold is so cheap, it’s being given away

Submitted by cpowell on Thu, 2015-09-17 15:47. Section: Daily Dispatches

By Helen Thomas

The Wall Street Journal

Thursday, September 17, 2015

It is a sign of the beleaguered state of the gold sector that people are effectively giving the stuff away for nothing.

Consider Randgold’s agreement to form a 50/50 joint venture with AngloGold Ashanti, aimed at redeveloping the Obuasi mine in Ghana, which AngloGold largely closed last year. Details weren’t disclosed, but it doesn’t appear Randgold is paying anything upfront for the mine, which offers 5.3 million ounces of reserves. Instead, the pair will share development costs and rehabilitation liabilities.

Mark Bristow, chief executive of Randgold, seems to have parlayed his reputation as the best operator in the business into a cut-price option on a sizable gold mine. AngloGold has already laid off thousands of workers at the loss-making mine. Near-term, Randgold need only shell out a few million to study if the mine can be overhauled and mechanized. …

… For the remainder of the report:

http://www.wsj.com/articles/gold-is-so-cheap-its-being-given-away-144249…

end

Why you must own gold:

(courtesy Jessie/Americain cafe)

The Misguided Paperati & Bifurcated ‘Gold’ Markets

Submitted by Jesse via Jesse’s Cafe Americain,

There is a short excerpt of a video interview with hedge fund titan Ray Dalio at the Council on Foreign Relations below.I think it is priceless. Ray lays out his thoughts on wealth and hedging with gold to the chuckles and sniggers of the pampered ruling class in a very clear and straightforward manner.

There is also another video interview in which Dalio discusses his views with the smirking chimps from CNBC. It is almost a scene out of Huxley’s Brave New World, with Dalio as some kind of monetary savage trying to explain reality to those who have been incubated in an artificial currency regime of King Dollar and know nothing else.

* * *

Here is why I think that this is important.

The gold market in particular seems to have bifurcated, or split into two: one market for largely paper speculation and high leverage, and another for the purchase and distribution of actual physical bullion.

Is this a problem?

Yes it is. Because the attitude towards gold among the status quo in the West has become rigidly dogmatic, supported by years of lazy thinking and a determined the campaign of ridicule and propaganda to try and extend the unsustainable.

You can see it emerge every so often in sites and media outlets and analysts who can be considered as creatures of the establishment, to use an older phrase, for whatever reason they may have. Some of the economist manservants of the ruling class talk about gold with the same sneering manner that a Victorian aristocrat might have discussed the ‘rights’ of the peoples of India or of China.

And I do not necessarily think they are bad motives, in the dishonest sense at least. Some may actually believe what they say, although for the most part I don’t think that the fortunate care what is good or what is true, if it serves their own special interests. This is how they have been taught to be, how life is.

If you have been brought up, bred, and bombarded with certain points of view for most of your life, it is no surprise that you may reflexively tend to adhere to and promote those views without regard to any intervening facts, past or present. You have been programmed by your education and, dare I say it, class. I see it all the time.

And it can sometimes lead to odd divergences in reasoning. This is why certain Founding Fathers found it perfectly acceptable to declare that ‘all men are created equal’ and also own slaves. Or to seek to curtail the rights of the non-landed and women in terms of ruling and voting. They are running on what they knew, without proper and rigorous examination.

It is hard for someone who has come from outside that system to understand how they can rationalize such a glaring discrepancy. But if you put yourself in their place, and honestly examine some of your own habitual thinking, it is not so hard.

Hypocrisy, maybe. And maybe it is just the unexamined prejudices of the fortunate. Sometimes even what seems to be an obvious truth can only be seen clearly through tears. And we have quite a surplus of the exceptionally fortunate these days, who have been pampered and privileged by an order which care very well for them, but that seems to be passing.

A big change is what we are heading for. We have a financial system that still holds a vast amount of gold in the central banks, including the US and Europe according to their reports at least. And more importantly, it is on a mad increase in the East with the central banks and the people buying in ever increasing amounts. Those who serve the power circles of New York, Washington, and London do not want to hear about it, anymore than Winston Churchill had a regard for the thoughts of Mr. Gandhi.

And despite the huge change in the global supply and demand for bullion, we have a holdover, a significant price discovery mechanism in New York and London that is increasingly diverging from the physical realities of supply and demand.

There is going to be a reconciliation of attitudes and realities at some point. And it may be quite impressive. The longer that the status quo and their courtiers try to maintain their modern aristocracy, like vast tectonic plates unable to move but building greater and greater pressure, the more dramatic that change may be when it finally comes.

And alas, so many of our politicians are servants, although well paid and well taken, of the moneyed interests. So they will do nothing that would perturb their true lords and masters, if they wish to also become fabulously rich and rise within the existing system.

The thought of the harm that this careless disregard for justice and right reason is doing to a very large group of relative bystanders and innocents, whose proper role is to be protected by those who have been gifted with greater talents accompanied by oaths of office, is almost disheartening.

end

Bill Holter responds to bron Suchecki/director of the Perth Mint

(courtesy Bill Holter/Holter-Sinclair collaboration)

Bron Suchecki is a Gentleman

Bron did not refute my logic but disagrees about the cause for the current retail coin shortages. He believes the shortages exist because the mints cannot keep up with demand, it is not a problem getting the raw metal he says. I would simply ask this, “why is gold in London in severe backwardation?” This condition should NEVER exist.

What he did disagree with is paying a large premium to own coins in hand. I would again simply ask, what is the cost to own a coin and have it in your hand? It is the physical price, not the pooled price nor any other paper price. We clearly saw an example of HUGE premiums of physical over paper in 2008, while COMEX briefly traded under $9, no physical metal changed hands under $15. So, what was the “real” price back then?

He went on to say he was surprised at my statement “if you hold metal in hand, you have no question as to whether you own it” because that as he said “implied I did not trust Eric Sprott’s funds or James Turk’s services”. Let me say this, I know Mr. Sprott very well and I know James Turk via e-mail and his writitngs, I trust them both. That said, I trust my own eyes more than I trust ANYTHING OR ANYONE (even though age is taking its toll and it’s time for glasses). One final point he agreed with to my shock was “there will be future cases of fraud and empty vaults” even citing the latest at Bullion Direct as an example. (As a side note, the biggest example of “empty vaults” was Morgan Stanley charging full storage fees for nonexistent metal. Only to be slapped on the wrist because they had the paper to pay clients with) I believe his thought process here reinforces much of what I wrote yesterday. Mr. Suchecki finished his e-mail by pointing out Perth Mint has been in business for 116 years, is still owned by the government and provided a bar list http://www.perthmint.com.au//documents/PABarlist.pdf for perusal.

To finish I must say thank you for the reply Bron. You showed me you are a gentleman and a class act with your response! Now I will do something I have hesitated to do because I never want to appear self serving or like a carnival barker. Since joining forces with Jim, I have retained my business relationship with Miles Franklin, still broker metals and can help with storage of metals via Brink’s in Montreal. We also have “non bank” storage agreements in Switzerland, Hong Kong, and Singapore. While I cannot comment first hand on the Swiss, Hong Kong or Singapore facilities, I have been personally to the Brink’s vault and observed while they audited the holdings. I saw with my own eyes how and where the metals are stored and how they are audited. This process is done every six months by an independent auditor. If segregated storage is something you feel necessary because you hold too much metal to be safely secured personally, please feel free to contact me.

1 Chinese yuan vs USA dollar/yuan rises a bit in value, this time at 6.3664/Shanghai bourse: barely in the green and Hang Sang: green

2 Nikkei down 362.06 or 1.96.%

3. Europe stocks all in the red /USA dollar index down to 94.20/Euro up to 1.1430

3b Japan 10 year bond yield: falls to .340% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 119.15

3c Nikkei now just above 18,000

3d USA/Yen rate now below the important 120 barrier this morning

3e WTI: 46.30 and Brent: 48.85

3f Gold up /Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .699 per cent. German bunds in negative yields from 4 years out

Greece sees its 2 year rate falls to 10.83%/Greek stocks this morning down by 0.75%: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield falls to : 8.46%

3k Gold at $1136.00 /silver $15.26 (8 am est)

3l USA vs Russian rouble; (Russian rouble down 22/100 in roubles/dollar) 65.70,

3m oil into the 46 dollar handle for WTI and 48 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9543 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0905 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund now enters in negative territory with the 10 year moving closer to negativity to +.699%

3s The ELA lowers to 89.1 billion euros, a reduction of .6 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.15% early this morning. Thirty year rate below 3% at 2.07% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Slide, Futures Tumble On Confusion Unleashed By “Uber-Dovish” Fed

What was one “one and done“, just became “none and done“ as the Fed will no longer hike in 2015 and will certainly think twice before hiking ahead of the presidential election in 2016. By then the inventory liquidation-driven recession will be upon the US and the Fed will be looking at either NIRP or QE4. Worse, the Fed just admitted it is as, if not more concerned, with the market than with the economy. Worst, suddenly the market no longer wants a… dovish Fed?

* * *

While consensus was split if the Fed was going to hike or keep rates the same (although with Goldman pushing for the latter and even urging further easing, it is no surprise for the first time ever a FOMC member suggested negative rate), everyone was expecting some hawkish component to yesterday’s FOMC announcement: either the hike itself, or a hawkish “hold” in which the Fed would promise a hike is imminent any moment. After all, 7 years later, the market needed at least a little confirmation that the economy is finally starting to pick up through the lens of the Fed. Nobody expected that dovish mess that was unleashed at 2pm yesterday, in which the Fed explicitly made it clear that it now has a third mandate: responding to Chinese and global events, and that a rate hike is virtually impossible any time emerging markets are “tantruming” due to the same dollar strength that accompanies any pre-hiking intentions, thus proving what we have said all along: the Fed is trapped in a catch 22.

This is how JPM’s chief economist Michael Feroli summarized the confusion unleashed by the Fed:

“While that outcome wasn’t too much of a surprise – we were leaning toward a hike but thought it was basically a coin flip – what was a surprise was the dovish statement and dovish tone of Yellen’s remarks in her post-meeting press conference. Rather than reinforce the message that a rate hike before year-end is highly likely, she gave little sense of growing confidence that inflation will return to its 2% objective over time.”

As for the Fed admitting it is now trapped by the market, here is Vanguard’s senior economist Roger Aliaga-Diaz:

“We are concerned with the Fed’s acknowledgement of recent market volatility in its decision. The Fed runs the risk of being held captive to the markets as, paradoxically, much of that volatility is due to the anticipation and uncertainty around when the Fed will move.”

What’s worse, said Catch 22 also confirms that just like all other central banks who hiked just to ease promptly thereafter, starting with Japan’s failed attempt to escape ZIRP in 2000 and continuing through all the aborted rate hikes in the New Normal, a reflexive attempt to stimulate confidence, and thus inflation, by hiking rates first and hoping inflation follows, will not work forcing central banks to consider the “last option” (hyper)inflationary paradigm – direct monetary injections to the general population bypassing the bank transmission mechanism, where money creation is trapped in capital markets. In other words, monetary paradrops. That, of course, would be the final event before central banks lose all confidence, and incidentally is precisely why the market is trading as it is right now: down big in response to the most dovish Fed we have seen in over two years.

In the meanwhile, the market itself is stunned with its response to the Fed decision: while dovish holds such as this one has previously been almost inevitably bullish for risk assets, the selloff following 2pm’s kneejerk response and the ongoing selling overnight, confirms something is very wrong not only with the global economy, but the market’s “reaction function” to the Fed’s “reaction function.” Just as bad, the debate remains: when will the Fed hike, bringing with it the attendant volatility; and if the Fed does not hike, will it at least go NIRP or launch QE?

For now, all these are seen as dollar negative which is bad news for the ‘recovery’ narrative but good news for emerging markets for the time being.

As a result, while Emerging Markets are enjoying a brief but acute rally on the heels of dollar weakness overnight, developed market stocks are currently tumbling in virtually every market, from Japan which was down 2%, to Europe, to US equity futures which were up early but have since followed the USDJPY far lower as markets are now “tantruming” and demanding that if the Fed will not hike rates, then at least the BOJ or ECB will provide more QE.

The somewhat bright spot was Asian development markets where equities traded mostly higher as the region digested the Fed’s decision to keep rates unchanged but reiterated that a 2015 rate lift-off remained on the table. ASX 200 (+0.5%) and Shanghai. Comp. (+0.4%) traded in positive territory following the FOMC decision, while an improvement in Chinese new home prices (Y/Y -2.3% vs. Prey. -3.7%) further supported sentiment. Nikkei 225 (-2.0%) underperformed ahead of its extended 5-day closure with the index weighed on by a stronger JPY. JGBs tracked the firm gains seen in USTs as domestic pension funds were said to be in bids for bonds in the super long end, while the BoJ also entered the market to purchase JPY 820b1n in government debt.

Cautious sentiment dominated the price action in early trade, as market participants re-position following the decision by the Fed to leave rates unchanged . At the same time, Fed’s Yellen put particular emphasis on China and the recent market volatility in her press conference. As a result of the cautious tone European equities opened in the red (Euro Stoxx: -1.8%), with defensive sectors outperforming. Despite coming off the best levels of the session, both Bunds and Gilts are trading sharply higher, with Euribor and Short-Sterling curves flattening as market participants re-price rate hike expectations.

In FX, it has been a dollarpocalypse the hours following the FOMC announcement with the EUR gaining across the board, as the currency is now viewed as a slightly less attractive option for carry related trades and as such some unwinding has been observed. On that note, analysts at Bank of America have increased their EUR/USD forecast to 1.05 by the end of the year. The USD has continued to soften overnight (USD-Index: -0.5%) to see strength in major pairs, while safe haven flows to JPY have seen USD/JPY fall over a point to below the 119.50 level. At the same time, high-yielding currencies have been the main beneficiary with CAD and AUD seeing strength overnight despite the bleak outlook for metals and energy markets.

The commodity complex has seen further strength on the back of the week USD overnight with gold higher by over USD20.00 since the release of the FOMC rate decision. Elsewhere, copper and iron ore prices were mildly pressured with the latter on course for its worst week in over 2 months as a lack of demand from the world’s largest consumer China continues to weigh. WTI and Brent futures both reside near intraday highs heading into the North American crossover and on course to finish the week in positive territory.

There is nothing on the US calendar today, which gives markets even more time to digest the confusion the Fed unleashed yesterday.

Bulletin Headline Summary

- Cautious sentiment dominated the price action in early trade, and as such European equities opened in the red with defensive sectors outperforming

- EUR gained across the board, as the currency is now viewed as a slightly less attractive option for carry related trades and as such some unwinding has been observed

- Looking ahead, notable events on the calendar include Canadian CPI as well as comments from BoE’s Haldane and ECB’s Coeure

- Treasuries extend post-Fed rally, move to gain on week after Yellen cited concern over slowing growth in China and turbulence in global markets for keeping rates unchanged.

- Fresh charges in the U.K. Libor rigging investigation may target traders linked to the benchmark’s euro counterpart, with prosecutors focusing efforts on that strand of the probe in recent weeks

- Greece’s election remains too close to call as a three-week campaign wraps up on Friday with no clear front-runner in a vote that may put Europe’s most indebted state on course for thorny coalition talks as of next week

- China’s stocks capped their steepest weekly loss this month as turnover shrank amid growing concern government measures to support the world’s second-largest equity market and economy are failing

- Life is getting better in the U.S. even with stagnating wages for some workers, thanks to improvements in technology and cars, according to JPM’s Jamie Dimon

- Abe’s fiscal policy is backfiring again: More than a year after a sales-tax increase tipped Japan into a recession, efforts to clamp down on soaring pension payments are suppressing a recovery in consumer spending

- PBOC orders banks to tighten supervision of their clients’ FX deals, Reuters reports, citing unidentified people with direct knowledge of the matter

- Sovereign 10Y bond yields lower. Asian stocks higher with the exception of Japan. European stocks, U.S. equity-index futures decline. Crude oil, gold and copper rise

DB concludes the overnight wrap

So the Fed stands pat and the spell of record low rates continues as concerns about developments abroad and the fragility of markets proved to be enough of a red flag for policymakers. The overall tone and message from both the statement and Fed Chair Yellen certainly felt like it was weighed more towards the dovish end of the scale. Median dot plot estimates were lowered by a quarter basis point for the next three years (leaving one hike for 2015), while the LT rate was also notched down by the same proportion to 3.5%. Growth and inflation expectations for 2016 and 2017 were revised down, while the 2% core inflation target was moved back to 2018. The stronger Dollar and the disinflationary impact that this is having was an overriding theme. There was some support from Yellen on the improvements in domestic activity with both business spending and the labour market in particular highlighted. She also kept the door open for a move this year, including October, but once again the timing was downplayed with the expected path of rate rises re-emphasized as the more important factor.

In terms of the market reaction, the price action in Treasuries actually started about 45 minutes pre-FOMC as yields moved south in a hurry. The most notable move was in the 2y which was already down about 5bps prior to the release. The yield then plummeted a further 8bps post-decision and Yellen conference, finishing the day 13.1bps lower at 0.682% and in turn marking the biggest single day move lower since March 2009 when the Fed announced its QE program. The 10y closed just over 10bps lower at 2.191%, although it’s worth noting that it’s pretty much back to where it was at last Friday’s close. Meanwhile, the Dollar unsurprisingly came under decent pressure, the Dollar index finishing down 0.91%. Some of the more interesting price action came in risk assets. Equities initially rallied on the decision, the S&P 500 jumping as high as +1.3% before nerves crept in as Yellen’s press conference got underway, with the index eventually paring all of that move and more, closing down -0.26%. Credit indices saw a similar trend, CDX IG finishing about half a basis point tighter after trading nearly 3bps tighter.

While there weren’t huge changes to the statement put out by the committee, the main focus was on the paragraph ‘recent global economic and financial developments may restrain economic activity somewhat and are likely to put downward pressure on inflation in the near term’. This was followed up by Yellen in her press conference saying that officials had decided to stay put ‘in light of the heightened uncertainties abroad’. Yellen balanced this with supportive comments around the state of the domestic economy, but that was already overshadowed somewhat by a cut in growth estimates by the committee for 2016 (to 2.3% from 2.5% previously) and 2017 (2.2% from 2.3%), while core PCE projections were notched down to 1.7% (from 1.8%) and 1.9% (from 2.0%) respectively. The proportion of Fed officials now expecting a move by the year end has dropped to 13 out of the 17 officials, down from 15 who expected such at June. As mentioned median dot plots were nudged down 25bps and one committee member is now advocating for a rate cut.

As DB’s Peter Hooper notes, the Fed has now added considerable complexity to the task of divining when conditions will be ‘right’ in their view by stressing the importance of economic and financial market developments abroad as well as at home. The door has been kept open for now, but one has to think that that door is slowly starting to creak shut and a lot will rest on how markets react over the next month or so. As we stand, market pricing for an October hike is at just 18%, while December is currently at 44%.

In terms of trading in Asia this morning, with the exception of Japan – which has been weighed down by a stronger Yen – most major equity bourses have followed up in a positive manner, although not without some early swings. In China the Shanghai Comp and CSI 300 are up +0.40% and +0.62% respectively at the midday break, although the former has crossed between gains and losses eight times already. Elsewhere the Hang Seng (+0.42%), Kospi (+0.63%) and ASX (+0.88%) have all taken a leg up, although in Japan we’ve seen both the Nikkei (-1.39%) and Topix (-1.62%) tumble. Oil markets are more or less unchanged after falling over a percent yesterday, while Gold (-0.30%) has given back some of yesterday’s post FOMC gains. S&P 500 futures are currently up +0.2%, while Treasuries have seen little change. EM currencies have firmed although no more than three-tenths of a percent while Asia credit is generally a couple basis points tighter. Meanwhile, August home price data out of China this morning was reasonably supportive with prices rising in 35 of the 70 cities from the previous month.

Unsurprisingly there wasn’t much to report in the European session prior to the Fed yesterday. Equity markets were fairly mixed. The Stoxx 600 closed -0.18% while there were some modest gains for the DAX (+0.02%) and CAC (+0.20%) although in fairness there was little conviction for most of the session. It was a decent day for European credit though. Crossover closed some 7bps tighter and Main finished 1.5bps tighter.

Despite the obvious main event of the Fed taking up most of the attention there was also some data out yesterday. The highlight was a soft headline Philly Fed business outlook print for September which declined over 14pts to -6.0 (vs. +5.9 expected). The reading was the lowest since February 2013, although there were some positives in the details. Notable was a decent leg higher for capex expectations, while there were also firmer new orders and employment indices numbers. The six-month ahead outlook also rose relative to last month. Elsewhere, both housing starts (-3.0% mom vs. -3.8% expected) and building permits (+3.5% mom vs. +2.5% expected) readings recorded beats. Finally initial jobless claims declined 11k last month to 264k after expectations of no change. Meanwhile, in the UK we got an in-line +0.2% mom gain for retail sales for August, with the ex auto and fuel reading also printed as expected at +0.1% mom.

Before we get onto the day ahead, one event which has somewhat flown under the radar is Greece’s general election this Sunday. The recent polls have been too close to call, with fairly evenly split support for Syriza and New Democracy although neither is likely to control a majority in parliament. The successful conclusion of the 3rd ESM package and broad-based political support to meet creditors’ demands eliminated a lot of the political risk however and as DB’s George Saravelos pointed out previously the eventual outcome of the vote may not entail particularly different paths ahead. The bigger picture is the popular support towards underlying Eurozone membership as the key underlying factor behind ensuring that Greece’s path towards stabilization is in place.

It’s a quiet day for data today, with the focus set to be more on the price action following the Fed. There’s nothing of note in Europe this morning, while over in the US we’ve got the Conference Board’s leading indicator as the only notable release. Tomorrow we get the first Fedspeak post yesterday’s decision with Williams and Bullard both due to speak on the US economic outlook, so it’ll be worth keeping an eye on that.

end

Your opening of Japan and Shanghai stock markets, Thursday night 9:30 pm/Thursday morning 9:30 Shanghai time:

USA/Yen continues to plummet/Japanese stocks falter badly. China raises value of yuan which will cause more USA dollar outflows. Margin debt increases. The big news: the minister believes the USA/Yen rate will fall to 115: this would be the death blow to the yen carry traders.

(courtesy zero hedge)

Japanese Stocks/USDJPY Plunge As China Cracks Down On Aggressive-Buying By “Sinister Stock Squads”

Despite the approval of various Asian nation officials (e.g.Japan’s Amari: “Fed decision appropriate”), it appears non-hawkishness is not enough to keep the dream alive. Japan’s Nikkei 225 is down over 600 points from its post-FOMC spike highs, and USDJPY has tumbled over 1 handle – back below 120.00. Chinese stocks are extending losses after last night’s late tumble, as ironically, China’s securities regulator has uncovered a number of market manipulators who boosted prices of some stocks to sky-high levels during the peak of the bull market, attracting numerous followers who have suffered heavy losses in the recent market crash. The PBOC strengthened the Yuan fix for the 2nd day in a row (by the most in 2 weeks).

A sigh of relief from Japan’s leadership:

- *AMARI: FED DECISION APPROPRIATE IN VIEW OF WORLD, U.S. ECONOMY

- *AMARI: IMPACT FROM RESULTS OF FED DECISION WASN’T BAD

But it is not enough, as USDJPY and Nikkei 225 are tumbling…

And this did not help…

- *FORMER JAPAN MOF OFFICIAL EISUKE SAKAKIBARA SPOKE IN TOKYO

- *SAKAKIBARA SAYS DOLLAR-YEN MAY MOVE TOWARD 115-120 RANGE

- *SAKAKIBARA SAYS DOLLAR-YEN RATE UNLIKELY TO BE TOWARD 125

Which legged USDJPY lower still.

* * *

Broad asian equity markets weaker…

- *MSCI ASIA PACIFIC INDEX DROPS 0.6%, EXTENDING LOSS

And China is opening lower, extending last night’s closing weakness…

- *CHINA’S CSI 300 STOCK-INDEX FUTURES FALL 0.4% TO 3,143.8

Despite a 2nd day of releveraging…

- *SHANGHAI MARGIN DEBT BALANCE RISES FOR SECOND DAY

Which is ironic since China’s securities regulator has uncovered a number of market manipulators who boosted prices of some stocks to sky-high levels during the peak of the bull market, attracting numerous followers who have suffered heavy losses in the recent market crash,according to Shanghai’s China Business News.

The China Securities Regulatory Commission (CSRC) has penalized two such manipulators, announcing on Sept. 11 the confiscation of 47 million yuan (US$7.3 million) of the illegal gains Ma Xinqi and Sun Guodong made from stock manipulation.

In its announcement, the comission described how Ma Xinqi jacked up the stock price of Beijing Baofeng Technology, an internet video company, by placing massive orders which were canceled shortly afterwards before selling off his original holdings of the stock, making huge gains.

Sun Guodong repeatedly bolstered the stock prices of Guangdong Qtone Education and 12 other listed companies by placing orders for those stocks before selling off his original holdings the following day.

Insiders pointed out that Ma and Sun are members of 10-dd “stock squads” focusing on investments in high-flyers, China Business News said.

“These stock squads, each boasting several hundreds of millions of yuan in funds, carefully study technical market charts and profit from investments of extremely short duration,” remarked an executive of a private equity fund, adding that in addition to their own money the squads also solicit funds to boost their clout in manipulating stock prices.

The private equity fund executive said both Ma and Sun are but minor players among the stock squads, however, pointing to their limited profits, according to the announcement of CSRC.

Market insiders suspect that Ma and Sun are followers of much greater forces manipulating stock prices, perhaps involving fund managers, which were behind the stock price rise at daily ceiling of Baofeng Technology for 34 trading sessions consecutively in March this year, according to China Business News.

“Institutional investors have driven the prices of many stocks with shaky fundamentals to sky-high level,” the private equity fund executive said.

So – it appears – in China, do not be an over-aggressive buyer or a seller of stocks. We love the smell of free markets in the morning.

China strengthened the Yuan fix fior the 2nd day in a row..

- *CHINA SETS YUAN REFERENCE RATE AT 6.3607 AGAINST U.S. DOLLAR

That was the biggest rise in 2 weeks:

- *CHINA RAISES YUAN REFERENCE RATE BY 0.1%, MOST IN 2 WEEKS

Charts: Bloomberg

end

Over in England, another flash crash!!

(courtesy zero hedge)

UK Stocks Flash-Crash As BP, Banks Plunge

Chatter of a fat-finger trade, then exaggerated by the algos, has smashed UK’s FTSE 100 lower instantly this morning, dragging major firms with it…

- *HSBC DROPS 4.8% IN UK TRADING, QUICKLY REBOUNDS TO 2.3% LOSS

- *BP DROPS 4.7% IN UK TRADING, QUICKLY REBOUNDS TO 1.8% LOSS

As with all these plunges, the machines BTFD but the rebound is weak.

As Bloomberg noted:

- *FTSE 100 SUDDENLY DROPS TO LOWS, FALLS 1.9%

Charts: Bloomberg

end

We now have Bank of England’s Andy Haldane, who seemed to have a head on his shoulders and was the lone voice of sanity inside the Bank of England has just gone to the dark side by proposing:

i) negative interest rates in England

ii) a ban on all cash.

Ladies and Gentlemen; the wheels are coming off the entire globe’s finances:

(courtesy zero hedge)

Bank Of England Economist Calls For Cash Ban, Urges Negative Rates

Just three short years ago, Bank of England chief economist Andy Haldane appeared a lone voice of sanity in a world fanatically-religious Keynesian-esque worshippers. Admissions in2013 (on blowing bubbles) and 2014 (on Too Big To Fail “problems from hell”) also gave us pause that maybe someone in charge of central planning might actually do something to return the world to some semblance of rational ‘free’ markets. We were wrong! Haldane appears to have fully transitioned to the dark side, as The Telegraph reports, he made the case for the “radical” option of supporting the economy with negative interest rates, and even suggested that cash could have to be abolished.

Speaking at the Portadown Chamber of Commerce in Northern Ireland, as The Telegraph reports, Mr Haldane’s support for a possible cut in rates came as the Bank as a whole has signalled that the next move in rates would be up.

Andy Haldane, one of the Bank’s nine interest rate setters, made the case for the “radical” option of supporting the economy with negative interest rates, and even suggested that cash could have to be abolished.

He said that the “the balance of risks to UK growth, and to UK inflation at the two-year horizon, is skewed squarely and significantly to the downside”.

As a result, “there could be a need to loosen rather than tighten the monetary reinsas a next step to support UK growth and return inflation to target”.

But recent volatility in financial markets, prompted by China, and a decision by the US Federal Reserve to delay rate hikes, have pushed back expectations of the Bank’s first rate rise to November 2016.

Traditionally policymakers have resisted cutting rates below zero because when the returns on savings fall into negative territory, it encourages people to take their savings out of the bank and hoard them in cash.

This could slow, rather than boost, the economy. It would be possible to get around the problem of hoarding by abolishing cash, Mr Haldane said

Interestingly, one idea, Haldane told an audience of business owners in Northern Ireland, could be to scrap cash and adopt a state-issued digital currency like Bitcoin. Although widely reviled as the currency for drug dealers and criminals, Haldane said Bitcoin’s distributed payment technology had ‘real potential’. Which may explain the Fed’s sudden fascination in the virtual currency.

NIRP – it would appear – is about to global.

So Haldane has gone from worrying that “financial markets were detaching themselves too materially from fundamentals” and fearing the “biggest risk to global financial stability right now it would be a disorderly reversion in the yields of government bonds globally,” the BoE’s chief economist has not only called for policies which will enable an even bigger bond bubble but will also remove freedom from the people to do what ‘they’ think is best with their capital. Indoctrination is complete (or more ominously, is there something Haldane sees that has driven him to this extremist perspective?)

The ECB may have to react as the world now perceives that the USA policy to leave the rates unchanged is a blunder.

ECB board member Coeure suggests that more QE may be in the hopper. Europe is frightened to see the Euro rise which will dampen exports, the only saving grace for them. The one problem, of course, is the one we highlighted to you on several occasions:

they just do not have enough bonds to monetize!!

(courtesy zero hedge)

ECB May Launch More QE In Response To Fed Inaction, Board Member Hints

As noted earlier, the very simple calculus of yesterday’s Fed announcement boils down to the following: “markets are now “tantruming” and demanding that if the Fed will not hike rates, then at least the BOJ or ECB will provide more QE.” Moments ago the EURUSD briefly hit 1.1450, a 150 pip increase since the Fed statement, and an unwelcome development for Europe’s economy which has been treading water only due to its weak currency which has supported the European trade balance.

So now that the Fed appears to have made a grave policy error judging by the market’s initial reaction, it is up to the ECB and BOJ to step up (even if as we warned two weeks ago both are running out of monetizable material) and try to preserve some confidence, i.e., halt the selling.

Sure enough, that is precisely what happened earlier today when infamous ECB board member and hedge fund leaker Benoit Coeure hinted that if only the market drives 5Y5Y’s even lower, i.e., inflation expectations, the ECB will have no choice but to boost QE.

To wit:

- ECB’S COEURE SAYS ECB CAN ADAPT QE ASSET PURCHASE PROGRAMME IF DOWNWARD RISKS TO INFLATION ENTRENCH

- ECB’S COEURE SAYS WHATEVER U.S. FED DECIDES, EURO ZONE AND U.S. MONETARY POLICY ARE ON VERY DIFFERENT PATHS

This is happening even as the much touted European recovery is supposedly now faltering:

- ECB’S COEURE SAYS GLOBAL GROWTH PROSPECTS HAVE DARKENED, HAVE WORSENED MARKEDLY IN EMERGING MARKET ECONOMIES

- ECB’S COEURE SAYS EURO ZONE ECONOMIC ACTIVITY SHOULD CONTINUE TO IMPROVE BUT AT A SLOWER RATE THAN PREVIOUSLY THOUGHT

- ECB’S COEURE SAYS WHATEVER HAPPENS INFLATION WILL ONLY RISE VERY SLOWLY IN THE EURO ZONE

Better yet, Coeure came this close to admitting that which shall never be admitted by central bankers in polite company, namely that QE is nothing but a mechanism to manipulate exchange rates (and boost stocks in the process):

- ECB’S COEURE SAYS EXCHANGE RATE IS NOT A TARGET BUT IS A VARIABLE IN ECB ANALYSIS OF PRICE DEVELOPMENTS

And yet all the wrath of the world is focused on China’s and its “massive” 3% devaluation when the Yen has gone from 80 to 120 in three years simply due to printing money?

The ironic conclusion: ECB’S COEURE SAYS MONETARY POLICY CANNOT RESTORE GROWTH IN LONG TERM

But it sure will try, and quite soon at that – just push those 5Y5Y fwds low enough, and sit back awaiting more Q€.

end

Late this afternoon: Moody’s cuts France’s rating to Aa2 from Aa1

(courtesy Moodys/zero hedge)

Moody’s Downgrades France, Blames “Political Constraints”, Sees No Material Reduction In Debt Burden

Citing “continuing weakness in the medium-term growth outlook,” Moody’s has downgraded France:

- *FRANCE CUT TO Aa2 FROM Aa1 BY MOODY’S, OUTLOOK TO STABLE

Apearing to blame The EU’s “institutional and political constraints,” Moody’s expects French growth to be at most 1.5% and does not expect the debt burden to be materially reduced this decade.

1. The continuing weakness in France’s medium-term growth outlook, which Moody’s expects will extend through the remainder of this decade; and2. The challenges that low growth, coupled with institutional and political constraints, poses for the material reduction in the government’s high debt burden over the remainder of this decade.

The following is very worrisome. Netanyahu is heading to Moscow worried that weapons will be given to Syria. The fear is that these weapons will be given to Israel’s enemy, Hezbollah:

(courtesy zero hedge)

Russia Says It May Send Troops Into Combat In Syria As A Worried Netanyahu Heads To Moscow

On Thursday evening, we detailed a Reuters report which suggested that the influx of Russian technical and logistical support to Bashar al-Assad’s depleted army at Latakia might have breathed new life into the regime as it seeks to rout Islamic State and a whole host of other armed groups fighting for control of Syria. “Foreign Minister Walid al-Moualem said on Thursday Russia had provided new weapons and trained Syrian troops how to use them,” Reuters said, before describing what certainly sounds like an invigorated air campaign against the de facto ISIS capital at Raqqa.

Importantly, al-Moualem also indicated that Syria would be willing to make an official request for Russian combat troops “if needed.”

Now clearly, it seems likely that Russian troops have already joined the battle and indeed, when the bullets start flying, the distinction between “logistical” support and “combat” support quickly becomes blurred, but through all the sabre rattling and back-and-forth banter between Kerry and Lavrov, both sides are still keen to at least pay lip service to the unwritten rules of international diplomacy which is why before Russia can admit that its troops are actually on the ground to fight, they’ll be a charade where Syria will pretend to be raising the issue with the Kremlin for the first time at which point the Kremlin will take a few days to “consider” things. As of Friday, it appears as though that process has begun. Here’sBloomberg:

Russia said it’s willing to consider sending troops into combat operations in Syria if President Bashar al-Assad’s government requests assistance.

While the possibility is hypothetical now, “if there is a request, it will be discussed as part of bilateral contacts,” Kremlin spokesman Dmitry Peskov told reporters on a conference call on Friday. “Of course it will be discussed and considered.”

The prospect of direct Russian involvement in the country’s civil war, in which more than 250,000 people have died since 2011, would mark a sharp escalation in President Vladimir Putin’s support for the embattled Assad government. The U.S. has accused Russia of increasing military aid to Syria in recent weeks by sending tanks, artillery and personnel, as well as setting up what the Pentagon says might be a forward airbase near the coastal city of Latakia. Syria also hosts Russia’s only naval facility outside the former Soviet Union at Tartus.

The possibility of troop involvement emerged before a visit to Moscow by Israeli Prime Minister Benjamin Netanyahu on Monday for talks with Putin about Russia’s growing military involvement in Syria. Netanyahu “will present the threats posed to Israel as a result of the increased flow of advanced war material to the Syrian arena and the transfer of deadly weapons to Hezbollah and other terror organizations,” the Israeli government said in an e-mailed statement on Wednesday.

To be sure, Netanyahu’s Russian visit comes at an interesting time. In the US, the last challenge to the Iran nuclear deal was defeated in the Senate on Thursday, paving the way for the agreement’s implementation. Needless to say, Netanyahu isn’t particularly pleased with The White House’s stance on Iran’s nuclear ambitions and US-Israeli relations have deteriorated markedly this year thanks in large part to the Iran deal. But the Israeli PM is also concerned that Russia’s move to reinforce Assad could have implications for Hezbollah, something Netanyahu and Putin will discuss on Monday. Here’s Reuters:

Western officials and a Russian source said last week that Russia was sending an advanced anti-aircraft missile system to Syria in support of Assad.

The Western officials said the SA-22 system would be operated by Russian troops. A U.S. official, who confirmed the information, said the system may be part of a Russian effort to bolster defences at an airfield near Latakia, an Assad stronghold.

Even if Russians operated the missiles and kept them out of the hands of the Syrian army, the arrival of such an advanced anti-aircraft system could unsettle Israel, which in the past has bombed sophisticated arms it suspected were being handed to Assad’s Lebanese guerrilla allies, Hezbollah.

(Hezbollah chief Hassan Nasrallah)

Worried about accidentally coming to blows with Russian reinforcements in Syria, Israeli officials said last week they were in contact with Moscow. But Israel also made clear it would continue its policy of stopping advanced arms reaching Hezbollah.

And let’s not forget that just one month ago, Israel hit targets inside Syria after Damascus-based Islamic Jihad lobbed rockets at a village in Northern Israel. Netanyahu claimed the militants were acting on order from an “Iranian general.”

“This is another clear and blatant demonstration of Iran’s continued and unabating support and involvement in terrorist attacks against Israel and in the region in general. This attack has also occurred before the ink on the . . . nuclear agreement has even dried, and provided a clear indication of how Iran intends to continue to pursue its destabilising actions and policies as the international sanctions regime is withdrawn in the near future,” Israel’s foreign ministry said at the time.