Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1153.80 up $22.20 (comex closing time)

Silver $15.13 up 35 cents.

In the access market 5:15 pm

Gold $1154.00

Silver: $15.13

First, here is an outline of what will be discussed tonight:

At the gold comex today we had a poor delivery day, registering 0 notices for nil ounces Silver saw 9 notices for 45000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 213.27 tonnes for a loss of 90 tonnes over that period.

In silver, the open interest fell by 298 contracts despite the fact that silver was up in price by 3 cents yesterday. The total silver OI now rests at 151,842 contracts In ounces, the OI is still represented by .759 billion oz or 108% of annual global silver production (ex Russia ex China).

In silver we had 9 notices served upon for 45,000 oz.

In gold, the total comex gold OI fell to 417,564 for a loss of 1740 contracts. We had 0 notices filed for nil oz today.

We had no change in tonnage at the GLD; thus the inventory rests tonight at 674.61 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had no change in silver inventory at the SLV/Inventory rests at 319.197 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by 298 contracts down to 151,842 as silver was up by 3 cents in price with respect to yesterday’s trading. The total OI for gold fell by 1740 contracts to 417,564 contracts, as gold was up $6.60 yesterday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

Asian affairs:

3. a) China opens for trading 9:30 pm est Monday night/Tuesday morning 9:30 Shanghai time

The Nikkei ends up down 498 points. Europe implodes.

European affairs:

4) Black Swan events? German auto industry spreads to BMW and is this the next deflationary wave to whack us

(zero hedge)

5, The Chart has has everybody in Europe worried: the markets react positively to no QE and negative when

QE is possible!

(zero hedge)

6. Portugal fiscal budget skyrockets as its bad bank purchase falls apart.

Portugal has to go back to the drawing board

(zero hedge)

7. France: joblessness rising to record heights

(zero hedge)

Scandinavia and Taiwan

8 Both Norway and Taiwan cut their interest rates as we have a race to the bottom

(zero hedge)

Russian affairs

9. a)Putin tells the uSA to either join us as they engage to knock out ISIS

b) Ukraine is now deciding to enter NATO totally against the wishes of Russia. Putin will react.

Middle East:

Saudi Arabia

10. 717 people killed in a stampede to enter Mecca

(zero hedge)

EMERGING MARKETS

11. Currency carnage continues unabated

(zero hedge)

12. a) Petrobras credit default swaps rise signifying risk of collapse. It has a total of 134 billion dollars worth of debt and

billion of USA denominated debt. As China’s currency the yuan devalues, this causes massive liquidation of dollars leaving the sovereign. We are close to a default in Brazil and its main jewel: Petrobras

(zero hedge)

b) Brazilian real collapses to 4;21 to the dollar (3 commentaries)

13. Oil related stories

Shale boys are having difficulty tapping the bond market

(zero hedge)

14 USA stories/Trading of equities NY

a) Trading today on the NY bourses 3 commentaries

b) Caterpillar reports that they are going to layoff another 10,000 staff as global sales plummet

(zerohedge)

c) The Chicago Activity Index (the National Mfg index) goes negative and crashes

(Chicago Activity Index/zero hedg)

d) The 6th Regional Fed survey shows another collapse in the region of Kansas City

(Kansas City Fed survey/zero hedge)

e)Durable goods orders collapse signalling a massive recession is upon us and maybe depression like conditions

(zerohedge)

f) New home sales rise against existing home sales plummeting. Wealthy Chinese are taking their unwanted yuan and buying USA homes

g) WalMart demanding savings from suppliers of Chinese origin because of their devaluation!

(zero hedge)

15 Physical stories

i) Is the Bank of Spain pulling gold out of Catalonia, afraid of Sunday’s independence vote?

(Bloomberg/GATA)

and the Bank of Spain responds to zero hedge!!

ii). Bron Suchecki ‘s commentary tonight is gold fractional banking

(Bron Suchecki/Perth Mint Part iii)

iii) Ronan Manly and Jessie of Americain cafe tackle how much gold is really behind London’s LBMA and the Bankof England

(Ronan Manly,Jessie/American cafe/two commentaries)

iv) The price suppression of gold and silver will end once everybody takes delivery/a new brainer

(GATA)

v)Mike Kosares on gold today vs 15 years ago vs stocks

(Mike Kosares)

vi) The huge Nadera (Dutch) commodity firm reports huge losses in biofuels as a rogue trader went wild. This has been going on for several years. What is interesting is the firm was 51% bought out by Chinese interests last year.

(zero hedge)

vi) Bill Holter’s commentary tonight is titled: “Look no further than international trade!”

(Bill Holter/Holter-Sinclair collaboration)

Let us head over to the comex:

September contract month:

Initial standings

September 24.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 5,608.20 oz

Scotia |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz (nil) | |

| No of oz served (contracts) today | 0 contracts (nil oz) |

| No of oz to be served (notices) | 71 contracts (7100 oz) |

| Total monthly oz gold served (contracts) so far this month | 24 contracts(2,400 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 401,985.6 oz |

Total customer deposit: nil oz

September silver initial standings

September 24/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 343,849.93, oz

Brinks |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 622,338.600 oz

CNT,JPM |

| No of oz served (contracts) | 9 contracts (45,000 oz) |

| No of oz to be served (notices) | 213 contracts (1,065,000 oz) |

| Total monthly oz silver served (contracts) | 1223 contracts (6,115,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 603,500.075 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 19,705,280.0 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: 622,338.600 oz

total withdrawals from customer: 343,849.93 oz

And now SLV:

Sept 24.2015: no change in silver inventory tonight/inventory rests at 319.197 million oz

Sept 23.2015: we had a huge withdrawal of 1.718 million oz at the SLV/Inventory rests at 319.197 million oz

Sept 22/no change in inventory at the SLV/Inventory rests at 320.915 million oz

sept 21.2015: no changes in inventory at the SLV/Inventory rests at 320.915 million oz

Sept 18.2015; no changes in inventory at the SLV/inventory rests at 320.915 million oz

sept 17.2017:no change in inventory at the SLV/rest tonight at 320.915

million oz/

sept 16.2015: no change in inventory at the SLV/rests tonight at 320.915 million oz/

Sept 15./no change in inventory at the SLV/rests tonight at 320.915 million oz

Sept 14./we had another withdrawal of 1.145 million oz from the SLV/Inventory rests at 320.915 million oz

Sept 11.2015: no changes in silver inventory at the SLV/inventory rests at 322.06 million oz

Sept 10.2015: we had no changes in silver inventory at the SLV/rests tonight at 322.06 million oz

Sept 9.2015:

we had another huge withdrawal of 1.336 million oz of silver from the vaults of the SLV/Inventory rests at 322.06 million oz

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

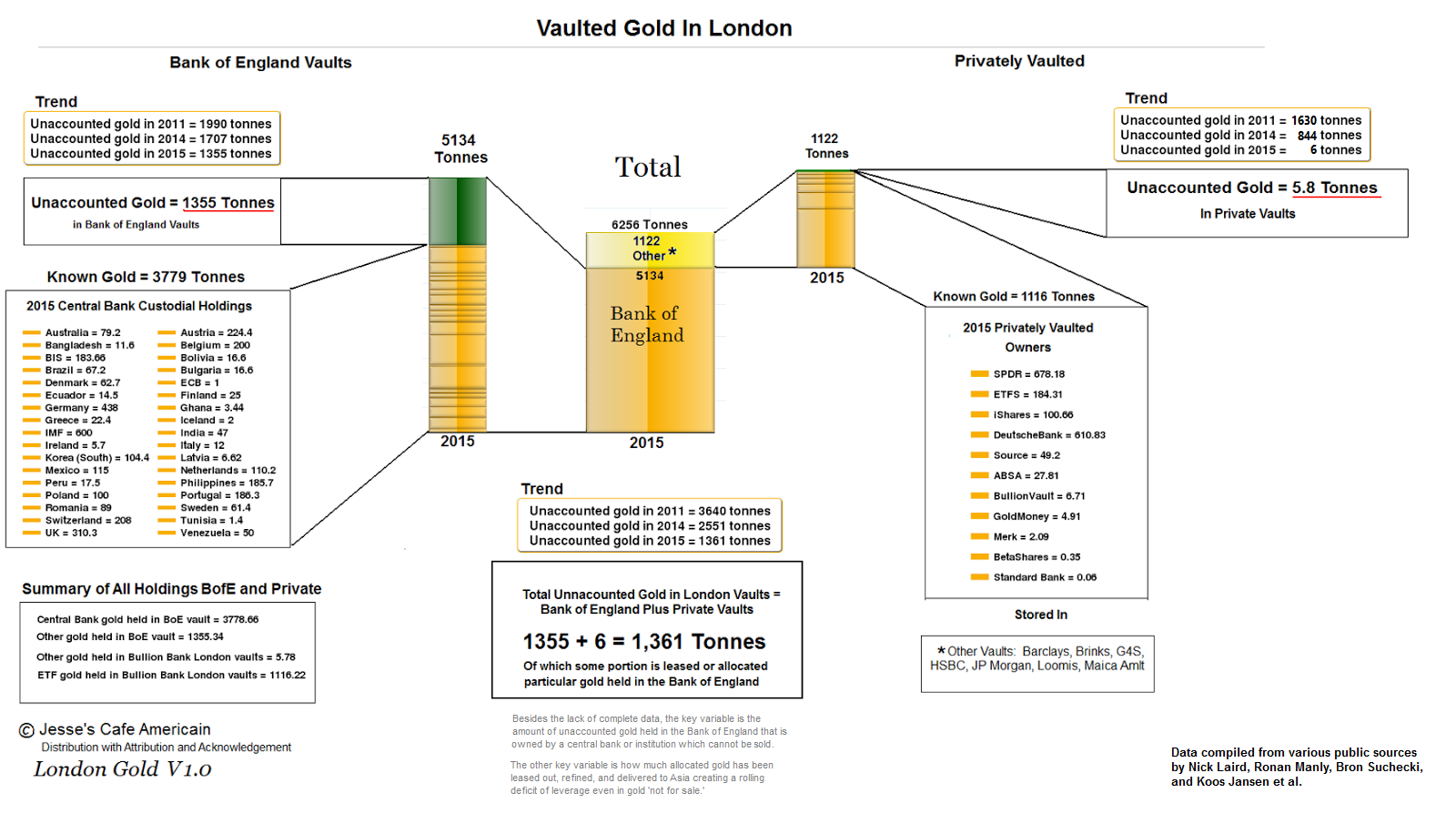

Bank of England and LBMA Gold Vaults – The “London Float”

A case study of physical gold stored in London Vaults in LBMA 400 troy ounce gold bars has been undertaken by Ronan Manly, Koos Jansen, Bron Suchecki and Nick Laird.

Nick Laird has just completed a great article replete with many interesting and important charts which further illuminate the size of the “London Float” which is the working supply of gold available to meet the gold markets daily needs and huge international demand for gold today – especially from Germany, India and China.

The size of the “London Float” is examined and brought “out of the shadows and into the light of day”.

[Please click chart to expand]

Jesse’s Cafe Americain via Sharelynx – please click image to expand

Laird concludes that there is an increasing shortage of physical gold bullion in LBMA vaults and on the COMEX due to the continuing flows of gold east to “satisfy the current rampant Asian demand”.

The full article and excellent charts can be accessed here.

DAILY PRICES

Today’s Gold Prices: USD 1134.45, EUR 1012.31 and GBP 742.73 per ounce.

Yesterday’s Gold Prices: USD 1124.60, EUR 1010.97 and GBP 734.77 per ounce.

(LBMA AM)

Gold in Australian Dollars – 3 Months (Reuters Eikon)

Gold rose 0.4% or $4.70 to $1,130.10 per ounce yesterday while silver fell 2 cents to $14.79 per ounce. Gold also eked out further gains in euros, pounds and most major currencies. Gold in Australian dollars has been particularly strong.

In Singapore, gold bullion ticked a little higher and maintained those gains in London, hovering just above the $1,135 per ounce level. Silver prices are another 0.3% higher to $14.94 today, while platinum is 1% higher

Palladium surged another 6% yesterday and is 0.3% down today. The move appeared to be a short squeeze and may be the precursor for the long awaited short squeeze higher in gold and silver.

end

Is The Bank Of Spain Quietly Pulling Its Gold From Catalonia Ahead Of This Weekend’s Vote?

This weekend, Catalonia’s long-running push for independence from Spain could get a boost if separatists manage to secure an absolute parliamentary majority in regional elections. Here’s a brief summary via FT for those unfamiliar:

If the independence movement has its way, the Catalan regional election on Sunday will bring [the independence process] to a dramatic climax. Should the pro-secession parties gain an absolute majority in parliament, they will press ahead with a plan to separate the prosperous region from the rest of Spain within 18 months.

Both the pro- and anti-independence sides look to Barcelona as the crucial battleground. Global tourist magnet, former Olympic host city and all-round architectural jewel, the city has traditionally been seen as an uphill climb for the independence campaign. Supporters of the union with Spain expect Barcelona and its densely populated suburbs to act as their main line of defence against the secessionist onslaught.

“What happens to Catalonia on September 27 will not depend on the independentistas. It will depend on the men and women in the metropolitan area of Barcelona who are not independentistas, and who traditionally don’t vote in the regional elections. If they vote this time, no one will be able to break Catalonia away from the rest of Spain,” Xavier García Albiol, the leader of the conservative Popular party in Catalonia, said this week.

As for how likely it is that CDC and ERC will be able to secure the 68 seats they need to move forward with independence, Citi thinks they’ll ultimately come up short, but as the following graphs show, it’s a close call:

Against that backdrop, we present the following with no further comment other than to ask if perhaps the Bank of Spain knows something everyone else doesn’t and is preparing for every contingency.

Via VilaWeb (Google translated):

This afternoon held an unusual movement in the branch of the Bank of Spain, Barcelona, ??Catalonia Square. Over thirty armored vans were entering and leaving the building shortly after an unknown direction. Many people have the photographed. The Bank of Spain has refused to comment on the operation or indicate that it was but people working in the area have said that is not a normal deployment.

Several readers VilaWeb explained that Monday early morning was a similar deployment.

Bank of Spain Responds, Promises It Is Not Confiscating Catalonia’s Gold

On Wednesday, some were curious to know why a line of armored vans was stationed outside the Bank of Spain’s Barcelona branch.

Our interest was piqued when we remembered that on Sunday, Catalans will vote in what might as well be an independence referendum.

We’ll spare readers a lengthy discussion of the history behind the independence movement and just note that CDC and ERC need 68 seats for an absolute parliamentary majority. If they hit that threshold, they’ll push quickly for an independent Catalonia. Based on the latest polls, it looks like it’s going to be close:

It doesn’t require a leap of logic to draw a connection between what looked like unusual activity at a central bank branch in the Catalan capital and this Sunday’s vote and so, we took the opportunity to ask the following: “Is the Bank Of Spain quietly pulling its gold from Catalonia ahead of this weekend’s vote?”

The answer, according to The Bank Of Spain itself who was kind enough to send us a letter this morning, is “no.” We present their response below without further comment:

Good morning,

Regarding the story posted by Tyler Darden on 09/23/2015 under the headline Is The Bank Of Spain Quietly Pulling Its Gold From Catalonia Ahead Of This Weekend’s Vote?, we want to point out the following:

Nothing extraordinary happened yesterday in the building of Banco de España in Barcelona. A number of armoured vans were stationed for a while in the street because of the increased movement of cash being distributed to the commercial banks prior to the banking holiday in Barcelona today (followed in many cases by another non-working day tomorrow or “Puente” as it is called in Spanish).

We gladly provided this explanation yesterday to the media which happened to ask us about the matter (which was not the case of VilaWeb, that did not contact the Banco de España regarding this –or any other- matter).

And, by the way, there is no gold in this site of Banco de España in Barcelona.

| Ronan Manly: Central bank gold at the Bank of England |  |

Submitted by cpowell on 08:21PM ET Tuesday, September 22, 2015. Section: Daily Dispatches

11:29p ET Tuesday, September 22, 2015

Dear Friend of GATA and Gold:

Gold researcher and GATA consultant Ronan Manly tonight publishes a huge research project — an attempt not only to quantify the gold vaulted in the London bullion market and at the Bank of England but also to calculate the gold reserves held at the bank by individual countries.

Manly concludes that gold vaulting in London has been in steady decline for years and that some nations, though far from all, are candid about their gold leasing.

Your secretary/treasurer infers from Manly’s report that gold leasing in London by central banks is a pretty big business even though it pays them very little. This in turn suggests that the purpose of gold leasing is not to earn a return on a supposedly dead asset but rather to protect central banking itself by controlling or regulating the value of the sole potentially independent international currency, a currency emitted not by any central bank but by Mother Earth herself, the only currency without counterparty risk. This control or regulation is undertaken through largely surreptitious market rigging and is facilitated by gold leasing’s creation of a vast imaginary supply of gold, gold that can seem to be in a dozen places at once, or maybe even a hundred.

Let anyone try to deny this when the International Monetary Fund has confirmed as much here:

http://www.gata.org/node/12016

Manly’s report is titled “Central Bank Gold at the Bank of England” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/central-bank-gold-at-the-b…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Extremely important stuff from Jessie last night. His data suggests correctly that physical gold in London is depleting fast. he author also suggests that gold in London is being hypothecated and rehypothecated many times over as there is probably north of 90 oz claims per one physical oz.

(Courtesy/Jessie/Americain cafe)

23 SEPTEMBER 2015

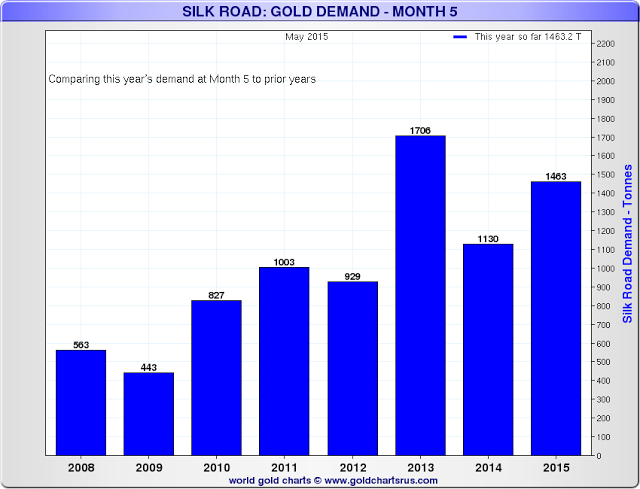

Shrinking Supply of Available Gold In London For World Demand – Timely Caution

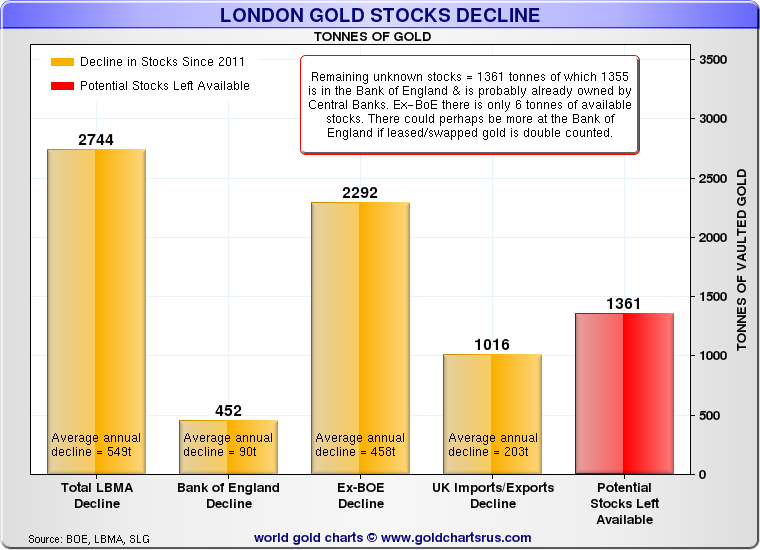

It is reasonable to estimate that London, in all the vaults, has only about 900 to 250 tonnes of gold available for physical delivery, which is a shockingly low figure given the current demand from ‘The Silk Road’ nations alone that is running about 1,700 tonnes per year. And even that 250 number is questionably high, depending on the status of the gold in the Bank of England.The objective is to attempt to determine how much available physical gold for delivery can be wrung out of London and New York, in excess of what can be had from scrap, minining and leasing. We are calling that ‘the gold float,’ and it is feeding the demand for bullion in Asia. At that point we might estimate when the pressure on price becomes irresistible.

We are thinking months, not years, at least with things as they are.

I wish to acknowledge up front the debt that is owed to Ronan Manly and Nick Laird especially for the data contained herein, as well as Koos Jansen for his ground breaking work in estimating Asian gold demand, and Bron Sucheki for his participation.. I have listed some of the pertinent published articles below.

It is regretful that one can only provide estimates. But that is the nature of this beast that operates with secrecy of supply and distortion of actual demand.

What manner of business is this to enable price discovery in a public market, by covering so many fundamentals with secrecy? Where is the mining community in all this?

The LBMA is said by those who are in a position to know these things to be running 90:1 or more leverage to each of its unallocated ounces of gold, which according to Jim Rickards is all of them.

The potential claims per deliverable ounce at the Comex right now is at an historic nosebleed high by of about 255:1, supposedly because the owners which to avoid a ‘short squeeze’ in bullion, although the party who said this did not say ‘where.’ London probably, maybe Switzerland.

Peter Hambro says that “there is not enough physical about. There are endless promises.”

In a nutshell, we now know that physical gold for global delivery, of which the London vaults are a major supplier, are rather tight, especially given the increasing demand for physical bullion in the East.

There is plenty of room for questioning the numbers and casting doubt on them, while hiding behind a curtain of exchange secrecy. One might suppose that the gold bullion bank apologists will be hard at it soon enough again.

They too often do not help to advance the understanding of the public, preferring to selectively twist the data to say ‘all is well.’ They deride the supply problems that people in the industry are encountering, always saying they are not real. And they like to include all the gold that exists in the warehouses for their calculations, whether someone else already owns it and is clearly not interested in selling at these prices.

More details would be useful, because if we could obtain a better idea on the extent of central bank leasing, we would be better able to estimate the risks and the relative fragility in the highly leveraged and hypothecated supply of gold in New York and London.

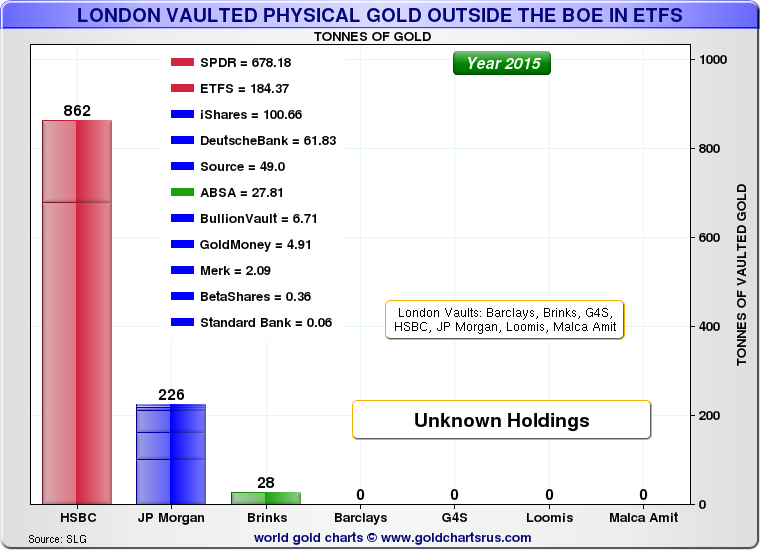

One would think from the known data that the unallocated gold in London is counter-claimed many times, and even the allocated and custodial gold is likely to have multiple claims upon it. So the actual ‘gold float’ is probably quite a bit less than 1,361 tonnes. Each of us has our own favorite ballpark number ranging from 900 to 250 tonnes and less, not fully accounting for leases and leverage on the remaining stock.

Nick Laird had a secondary outlier estimate which he expressed in colloquial Australian, which I dare not repeat here. But it was quite low. lol. Maybe four months worth of float left.

And it would certainly be nice to have more information about silver, especially since to my knowledge the central banks have dealt their own supply away some years ago and there are quite a few indications of tightness of supply, although not in the Comex yet.

I do consider this analysis to be a work in progress, Nick Laird and Ronan Manly are the key data organizers I believe, with help from Koos Jansen and Bron Suchecki, and the odd bit from Jesse the consulting detective. So I would look to their sites for explication of their methods and sources. Ronan Manly in particular is a public source and he goes into quite a bit of detail.

Given the struggle it has been to obtain the data, and the refusal of central bank personnel to discuss their own supplies on orders from above, there may surely be gaps and errors in this, but not for lack of effort.

If I have any major concern it is that the management, the exchanges and the regulators, will allow the traders to sleep walk themselves into a rather serious situation. And don’t we know how little self-restraint these traders have been showing.

The remedy for this situation is not even more leverage, or more hypothecation of the unallocated stock, or even more leasing by the central banks, or more programs in India to dampen demand.

The longer they allow this price rigging and leveraging up, the slower productive mines will come on line, and the worse the tightness on the remaining physical supply will become. But as they say in New York and London, ‘nothing is broken yet.’

The market solution for this tightness of supply is HIGHER PRICES and not increasingly ludicrous jawboning, spin, and bear raids.

And if higher prices might inconvenience the policy and perception management aspirations of the Wall Street financiers, their enablers and associated hirelings, well then too bad. Try to behave more responsibly, and stop attempting to make the rest of the world pay for your excessive gambling losses and poor judgement.

Related:

On the LBMA and Their Unallocated Holdings

Lions and Tigers and Deriding the Tightness of Gold Supply

How Many Good Delivery Bars Are In the London Vaults – Ronan Manly

Central Bank Gold at the Bank of England – Ronan Manly* (detailed sourcing of this data)

The London Bullion Market and International Gold Trade – Koos Jansen

Detailed London Charts and much data gathering – Nick Laird (available to the public)

Here are a few additional charts from Nick Laird’s site at goldchartsrus.com to break out a bit more detail and to provide some context for the estimated physical supply compared to physical demand.

end

(courtesy GATA)

Price suppression ends if buyers take delivery, Swiss refiner tells Physical Gold Fund

Submitted by cpowell on Thu, 2015-09-24 01:20. Section: Daily Dispatches

9:19p ET Wednesday, September 23, 2015

Dear Friend of GATA and Gold:

Physical Gold Fund’s John Ward today interviews an unidentified director of a large Swiss gold refinery who asserts, among other things, that gold is heading from West to East in huge volumes; that the gold price at the moment has no correlation to the physical market, which is tight; that if gold buyers ever start taking delivery of metal instead of leaving their metal on deposit with bullion banks, the situation could become dangerous; but that as long as buyers don’t take delivery, the current price mechanism — that is, price suppression by central banks and their bullion bank agents — can continue forever.

Of course this is pretty much the account that GATA and others, like JSMineset’s Jim Sinclair, have been providing for a long time.

The interview is 23 minutes long and can be heard at the Physical Gold Fund’s Internet site here:

http://www.physicalgoldfund.com/physical-gold-fund-interviews-director-o…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Mike Kosares: A note from an old friend and client

Submitted by cpowell on Thu, 2015-09-24 00:17. Section: Daily Dispatches

8:15p ET Wednesday, September 23, 2015

Dear Friend of GATA and Gold:

USAGold’s Mike Kosares today writes about “A Note from an Old Friend and Client” who is worried about “the social, political, and economic framework of our society.” Kosares likens the present time to 15 years ago “when gold was taking a beating in the mainstream financial media, stocks were being glorified, and everyone was talking about the Goldilocks economy (not too hot, not too cold, just right). That was just before the roof caved in … and gold began its long ascent.”

The exchange is headlined “A Note from an Old Friend and Client” and it’s posted at USAGold’s Internet site here:

http://www.usagold.com/cpmforum/2015/09/23/a-note-from-an-old-friend-and…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy Bron Suchecki/Part III Fractional Reserve Bullion banking)

Bron Suchecki: Fractional-reserve bullion banking, Part 3

Submitted by cpowell on Wed, 2015-09-23 15:55. Section: Daily Dispatches

11:53a ET Wednesday, September 23, 2015

Dear Friend of GATA and Gold:

In the third installment of his series on fractional-reserve gold banking, Perth Mint research director Bron Suchecki describes how the association formed by London-based bullion banks, London Precious Metals Clearing Ltd., reduces risk among bullion banks and regulates their credit with each other.

Suchecki writes that in some ways the London bullion banking system resembles a “free banking” system, in which financial institutions issue their own competing forms of money. But, he adds, the analogy is far from complete because of the involvement of central banks in gold lending.

The credit extended by bullion banks to each other, Suchecki writes, in effect increases what is perceived as the gold supply and thus tends to suppress gold’s price in terms of government currencies. He adds that gold lending by central banks tends to do this as well.

Suchecki writes: “So in our semi-free bullion banking system, the lending of gold to the bullion banks by a central bank increases the bullion banks’ reserves and thus increases the bullion banks’ ability to create more gold credit (unallocated). This inflation in gold supply naturally results in its fiat price falling. If so, why then would a central bank actually sell its precious physical gold if it wanted to manipulate the gold price when it can do so via reserve expansion instead? An answer to this rhetorical question tomorrow.”

Suchecki’s analysis is headlined “Fractional-Reserve Bullion Banking, Part 3,” and it’s posted at the Perth Mint’s Internet site here:

http://research.perthmint.com.au/2015/09/23/fractional-reserve-bullion-b…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Oh ! OH! this one is a dandy. We have another massive loss with the huge Nadera commodity firm announcing a rogue trader and significant losses!!!!

What is interesting here is the fact that 51% interest in the commodity company was bought by Chinese interests last year.

The original partners still own 49% and are now doubt seeking asylum somewhere!!

(courtesy zero hedg)

Dutch Commodity Trading Firm Suffers Massive Loss, Blames It On “Rogue Trader”

Two months ago, weeks before the carnage in Glencore started in earnest, we asked a simple question:

Judging by today’s collapse in Glencore price – a company whose CDS we said in March 2014 should be aggressively bought – which is now trading at an all time low below 100p on a Goldman report which confirmed what we have been saying all along (more on that shortly), it does appear that the Swiss commodity giant and copper miner will be the first mega-commodity trader with trillions in counterparty exposure to be “Lehmaned.”

But going back to July 22, what our tweet hinted at was not so much that one of the three commodity traders would be the first to blow up, as that the entire commodity-trading space is in jeopardy as a result of the collapse in commodity prices and carried inventory which has not been market to market in months (see the recent implosion in Jefferies fixed income results).

Indeed, one of the most surprising developments in recent months has been the relative scarcity of any high-profile commodity blow-ups or trader snafus, despite the tumbling commodity prices.

That changed today when Dutch grain-trading firm, Nidera BV (whose name is an acronym consisting of the countries in which it operates: Netherlands, India, Deutschland, England, Russia, Argentina) has suffered a crushing blow as a result of a “rogue trader” whose actions led to “significant losses” in the company’s biofuels business.

According to a Bloomberg report, that Nidera CEO Ton van der Laan said the grain-trading house has since exited the biofuels business and closed all the deals linked to the losses. “There is a significant loss,” he said on Thursday in a phone interview from Singapore, declining to provide a figure. He said Nidera will still post a profit for the company’s fiscal year, ending this month.

The actions of the trader “probably lasted for a prolonged time,” and the company only “found out earlier this year,” he said. Nidera notified the Dutch police because the trader “was involved in fraudulent action,” he said, declining to elaborate.

What makes this case even more interesting is that Nidera is controlled by Cofco Corp., China’s largest food company, which took control of Nidera last year after buying 51% of the company to create a global agricultural commodities trading house. The deal valued Nidera at $4 billion, including debt, a person with knowledge of the matter said at the time. The rest of the Rotterdam-based company, established in 1920, is controlled by the founding families.

While the firm did not quantify the size of the loss (the number will surely leak over the next few days) but it is virtually assured that the company’s profitability was massively impaired if not entirely wiped out: Nidera reported 2014 net income of $116.2 million, up from $72.7 million the year before.

The biofuel losses emerged after global prices plunged earlier this year, said van der Laan. Biofuels, made from crops including soybeans and corn, are closely linked to the price of crude oil.

Strange how “rogue traders” only emerge when trades go against them: we have yet to encounter a “rogue trader” case who was caught doing something illegal after generating a profit.

Those curious to learn more about Nidera’s now defunct biofuels business are out of luck. As Bloomberg’s Javier Blas shows, the webpage placeholder for the division is now 404-ing.

Finally, as Bloomberg reminds us while scarce in the past year, commodity trading houses have been hit by rogue traders in the past, causing big losses. In one of the most notorious cases, Yasuo Hamanaka, a top copper trader for Sumitomo Corp., hid $2.6 billion in losses trading the metal from its Japanese employer in 1996. In another case, a trader in the soybean market caused significant losses in 1999 to Andre & Cie SA that ultimately pushed the company, at the time one of the world’s largest grain traders, to its collapse in 2001.

Expect many more commodity blow ups in the coming months, all of which will be blamed on, you guessed it, rogue traders.

end

And now for our other problem child: Glencore

A default at Glencore will set off derivatives and according to zero hedge, may necessitate huge QE from the Fed to rescue the globe:

Glencore closed today at 98 pence:

(courtesy zero hedge)

Is Goldman Preparing To Sacrifice The Next “Lehman”

One of the more “unmentionable” conspiracy theories surrounding the demise of Lehman Brothers in 2008 is that this “shocking” event was in fact a well-choreographed and carefully scripted “controlled demolition”, with the Lehman Bankruptcy – the event that officially unleashed the Great Financial Crisis – getting the express prior permission of both Ben Bernanke and Hank Paulson, a former Goldman employee, whose motive was the elimination of the one firm that was then Goldman’s biggest competitor in the FICC space, and whose subsequent bailout of his former employer (Goldman Sachs and all other insolvent banks) would lead to the preservation of trillions in worthless equity courtesy of the biggest taxpayer funded bailout in history, and with billions in excess reserves parked on Goldman’s balance sheet smoothing the bank’s transition through a historic recession.Fast forward to this week when as we reported previously, following a surge in its Credit Default Swaps, the “doomsday” scenario for Glencore was suddenly on the table, because the market was suddenly warning Glencore that its most valuable asset, not its mines, or its trading operations, but its investment grade rating could be stripped away.

This is what we said, after we noted that GLEN CDS had just hit a multi-year wide of 464bps (precisely as we said it would over a year ago):

We expect this CDS blowout to continue.

What’s worse, if the company is downgraded from investment grade to junk, watch as the “commodity Lehman” scenario for Glencore, which much more than a simple copper miner just happens to be one of the world’s biggest commodity trading desks, comes full circle leading to waterfall collateral liquidations and counterparty freeze-outs as suddenly the world is reminded that there is a vast difference between a real and a rehypothecated commodity, and that all collateral rehypothecation chains are only as strong as the weakest counterparty!

Long story short: if and when Glencore loses its Investment Grade rating, it’s more or less game over, if not for the company’s already mothballed mining operation then certainly for its trading group, where “junking” would lead to numerous collateral shortfalls and margin call waterfalls, reminiscent of the ratings agency downgrade of AIG that culminated with the US bailout of the insurer.

Therefore we were not surprised earlier today to see Glencore stock crash to a new record low below 100p even as the CDS blow out continued.

We were, however, very surprised by the catalyst, because the company that managed to successfully hammer Glencore, which in our view is nothing short of the commodity “Lehman” (or perhaps AIG) was none other than Goldman, which earlier today released a report which is essentially blueprint for not only how to take away Glencore’s precious investment grade rating, but taken a few steps further, how to unleash this cycle’s commodity “Lehman event” (once again, Glencore is first and foremost a trading desk which serves as a counterparty with trillions in derivatives notional exposure to virtually every other commodity using and trading entity in the world) and taken to the extreme, how to “force” the Fed to finally unleash the helicopter money should Glencore’s failure be the catalyst the pushes the entire world into a deflationary recession, if not outright depression.

This is what Goldman said earlier in a note titled “Much progress made but the song remains the same”

We update our estimates for Glencore following the completion of its equity placement on September 16, in which it raised its target of $2.5bn. We also update our estimates to incorporate our commodity analysts’ lower thermal coal forecasts ($58/54/52/t for 2015/16/17E) and lower met coal forecasts ($91/85/90/t), which impacts Glencore’s 2016/17/18E EBITDA by c.15-18%… On lower estimates we reduce our 12-month price target to 130p (was 170p).

Implications

Since announcing c.$10bn of debt reduction measures on September 7 and completing a 9.9% equity placing, shares have retreated a further 14%. In our view investors are not yet convinced that Glencore has gone far enough to totally allay fears that the industrial assets can service the new lower debt level. Our scenario analysis suggests that using GS estimates for commodities prices and FX rates, Glencore’s IG rating would be secure in the medium term, but our estimates for zinc, nickel and coal prices are higher than spot prices.When we run the same analysis using spot commodity prices and spot FX rates, most of Glencore’s credit metrics would be at the border of required ranges to maintain its IG rating. Finally, a 5% drop in spot commodity and flat FX would see most of Glencore’s credit rating metrics fall well outside the required range to maintain its IG rating, suggesting concerns would quickly resurface.Glencore has a few levers left – further lowering capex, signing streaming deals and releasing more working capital. Recent underperformance suggests that the measures exercised are insufficient and more is needed. We remain Neutral rated but expect continued volatility in the near term.

Why is Glencore’s IG rating so critical? As explained above, Glencore is really not so much the Lehman as the AIG of the commodity world: without an investment grade rating, a self-reinforcing collapse will begin that could ultimately terminate Glencore’s trading desk, in the process liquidating one of the world’s biggest commodity trading counterparties.

From Goldman:

Glencore’s trading business relies heavily on short-term credit to finance commodity deals and its financing costs would increase if it were to lose its Investment Grade credit rating. In addition, it could even lose some counterparties due to increased counterparty risk.

That’s putting it mildly: what a junking of Glencore would do, is start a collateral demand waterfall cascade that the cash-strapped company simply would not be able to sustain.

So having laid out the strawman, Goldman next, very conveniently, explains just what would take for the Investment Grade trap to slam shut:

it would only take a c.5% fall in spot commodities prices for concerns about its credit rating to resurface

While Glencore’s announced measures have allayed near-term concerns about the potential for its credit rating to be downgraded, its high leverage to commodity prices is demonstrated in our scenario analysis, where we estimate just a c.5% drop in spot commodity prices would see concerns resurface about the potential for its credit rating to be downgraded. In addition, given the latest guidance on capex of c.$4bn in FY17, we believe there is limited flexibility for the company to make any further cuts while maintaining its production targets.

Wait, high leverage to commodity prices as the biggest risk factor? Where have we seen this before? Oh yes, in our March 2014 post (saying to buy GLEN CDS) which showed the one thing nobody was looking at at the time; Glencore’s, wait for it, high leverage to commodity prices!

For those who enjoy playing with numbers, here is Goldman’s real “Doomsday” scenario: the one which sees Glencore’s IG rating stripped. As Goldman admits,all it would take is a small 5% drop in commodity prices from here:

If commodity prices were to fall 5% from current levels – which we do not consider to be a far-fetched assumption given the downside risk to commodity consumption in China – we believe that concerns about its IG credit rating would quickly resurface. Under this scenario, we estimate that most of Glencore’s credit rating metrics would fall well outside the required ranges to maintain its IG rating, and as early as the next reporting period (FY15).

Although Glencore has a few levers left in the event commodity prices continue their leg down (such as deferring capex and executing streaming deals), the key point to highlight is that executing these options would take time. That said the recent announcement by Silver Wheaton that it is working with Glencore on the streaming deal highlights that management is focused on bolstering its balance sheet.

Charted:

It goes without saying that courtesy of HFTs and China’s hard landing, a 5% drop in commodities could happen overnight.

So if one is so inclined, and puts on the conspiracy theory hat mentioned at the beginning of this post, Goldman may have just laid out the strawman for the next mega bailout which goes roughly as follows:

- Commodity prices drop another 5%

- The rating agencies get a tap on their shoulder and downgrade Glencore to Junk.

- Waterfall cascade of margin and collateral calls promptly liquidates Glencore’s trading desk and depletes the company’s cash, leaving trillions of derivative contracts in limbo. Always remember:the strongest collateral chain is only as strong as its weakest conterparty. If a counterparty liquidates, net exposure becomes gross, and suddenly everyone starts wondering where all those “physical” commodities are.

- Contagion spreads as self-reinforcing commodities collapse launches deflationary shock wave around the globe.

- Fed and global central banks are called in to come up with a “more powerful” form of stimulus

- The money paradrop scenario proposed by Citigroup yesterday, becomes reality

Too far-fetched? Perhaps. But keep an eye out for a Glencore downgrade from Investment Grade. If that happens, it may be a good time to quietly get out of Dodge for the time being. Just in case.

end

A good one tonight from Bill Holter

(courtesy Bill Holter/Sinclair-Holter collaboration)

Look no further than international trade!

Last week the clock ran out on the Fed’s latest bluff. They have gone 55 meetings over 80 months without a single tightening or rise in interest rates. Last week was supposed to be “different” and a tightening of credit was predicted by something like 82% of economists polled. We of course now know that no tightening occurred and a trial balloon was even floated about instituting a new round of QE …

This of course was an easy one to call. Look at what the markets have done since that meeting, how much worse would it be had the Fed actually raised rates? Look all around the world and especially at China beginning to unwind, do they need a tightening of credit? They just devalued the yuan again yesterday (without any mysterious plant explosions …yet), had the Fed tightened you must ask yourself how much bigger the devaluation would have been by market forces?

Leading into last week, I think the easiest way to know that credit did not need to be tightened was by looking at international trade. This is one area where the “numbers are the numbers” and are not massaged (annihilated) by government reporters (not to mention mainstream reporters!). You see, the trade numbers pretty much need to match up and the freight rates are extremely hard to hide. Pretty much, they are what they are and if lied about are too easy to debunk. Last week, Zerohedge wrote on this topic when they penned WTO’s Stark Warning On Global Trade: “The Timing Belt On The Global Growth Engine Is Off” .

Further, if you look below at the Baltic Dry index, do you see a “recovery” from 2008 or a dead cat bounce which is now waning? THIS is indicative of global GDP, anything different from individual countries is an outlier and must be seriously questioned (including China).

http://www.zerohedge.com/sites/default/files/image

s/user5/imageroot/2015/08/bdiy.png

But why is this even important? First, because it is the REAL PICTURE but more importantly it is a very strong clue to actual rather than “made up” GDP. Spelled out for you, GDP is not growing enough (or at all) to create and bring new capital into the system. “The system” being one which has far more debt than it did during the 2007-09 event. Do you see where I am going with this? Clearly not enough growth exists globally to create the new capital necessary …yes that’s right…to carry a much larger debt load than we had back then!

Maybe it would be a good thing to remind you, one of the big problems back in 2008 was “too much debt”. Not only did the world not “liquidate” debt, it has taken on much more with an underlying economy that has been weakening for several years.

Going back to the top and full turn, how could the Fed have tightened last week? Or better, how can they ever tighten? The next move will be further additions of liquidity …at least as long as markets are open to do the “add”. Of course, just pulling the plug on the computers is another option!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

Comments welcome!

bholter@Hotmail.com

1 Chinese yuan vs USA dollar/yuan falls a bit in value, this time at 6.3825/Shanghai bourse: in the green and Hang Sang: deeply in the red

2 Nikkei closed down 498.38 or 2.76%

3. Europe stocks all deeply in the red /USA dollar index down to 95.85/Euro up to 1.1242

3b Japan 10 year bond yield: rises to .333% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 119.62

3c Nikkei now well below 18,000

3d USA/Yen rate now below the important 120 barrier this morning

(providing the necessary ramp for all bourses)

3e WTI: 44.55 and Brent: 47.85

3f Gold up /Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls badly to .599 per cent. German bunds in negative yields from 4 years out

Greece sees its 2 year rate rises to 11.12%/Greek stocks this morning down by 0.51%: still expect continual bank runs on Greek banks /Greek bank stocks plummet Wednesday and again on Thursday

3j Greek 10 year bond yield rises to : 8.23%

3k Gold at $1135.90 /silver $14.80 (8 am est)

3l USA vs Russian rouble; (Russian rouble up 19/100 in roubles/dollar) 66.54,

3m oil into the 44 dollar handle for WTI and 47 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9730 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0935 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund now deeper in negative territory with the 10 year moving closer to negativity to +.599%/5 year rate at 0.00%!!!

3s The ELA lowers to 89.1 billion euros, a reduction of .6 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.11% early this morning. Thirty year rate below 3% at 2.91% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Tumble As Emissions Scandal Spreads To BMW; NOK Plunges On Unexpected Norway Rate Cut

Two days ago, when observing how the Volkswagen scandal could become a systemic threat to both the German and the European economies we quoted Theo Vermaelen, a finance professor at INSEAD who said “if nobody else has done it, the damage would be limited. If it looks like it’s more companies, not just Volkswagen, it would be a major problem for the German car industry, and the German economy overall.“ We added “that’s the question German investors are wrestling with: was it just one cockroach. If it was more, the ultimate outcome WILL (not may) be more QE from the ECB because with Europe tentative recovery also sputtering after 6 months of ECB QE, a stake through the heart of Germany’s most important industry, will be just the black swan that sends Europe into a recession.”

Earlier this morning it seems the case for more ECB easing is pretty much set following a report by German Autobild that BMW’s X3 xDrive 20d sport utility vehicle “emitted as much as 11 times the European limit for air pollution in a road test, adding to concern that the investigation weighing on Volkswagen AG may spread to other manufacturers.”

According to Bloomberg the SUV was road-tested by the International Council on Clean Transportation, the same group whose tipoff led U.S. regulators to investigate a gap between Volkswagen AG diesels’ emissions in tests and on the road.

The company denied: “There is no function to recognize emissions testing cycles at BMW,” the Munich-based company said in a statement in response to the report. “All emissions systems remain active outside the testing cycles” adding that BMW said that there’s no system in its cars that responds to tests differently than it would operate on the road, but by then the damage was done and

BMW shares traded down 6.2 percent to 74.9 euros at 11:59 a.m. in Frankfurt after dropping as much as 9.3% earlier.

“There’s no suggestion BMW has done anything illegal,” said Juergen Pieper, an Frankfurt-based analyst with Bankhaus Metzler. “However, there are concerns for the long-term damage on the business with diesel cars for every manufacturer that builds cars with these engines.”

Perhaps now we know the reason why BMW’s new CEO Harald Krueger fainted last week during the Frankfurt motor show.

Shares of other German carmakers also declined. Daimler AG tumbled below €63 for the first time since November 2014. Volkswagen, which is at the heart of the probe and has lost about 20 billion euros in market value since Monday, recovered some of its losses, rising as much as 7.8 percent.

The news promptly ended the brief kneejerk rebound higher in European equities, which had rebounded earlier on positive German IFO data with expectations and business climate beating surveyed expectations, while current assessment missed expectation, however this failed to have a sustained reaction in the EUR, while elsewhere the USD-index heads into the North American crossover lower by around 0.1 % after seeing relatively muted price action overnight. Finally of note, NZD/USD saw strength after Fonterra revised its 2015/16 milk forecast upward, however mixed trade figures capped further advances in the pair.

In global central bank news – because lately that’s all that matters – ahead of Janet Yellen’s first post-FOMC speech in Amherst, MA on Inflation Dynamics and Monetary Policy in which the Fed chair will be expected to elaborate on last week’s disappointing FOMC announcement, overnight two central banks lowered their interest rates with the Norges Bank unexpectedly lowering their deposit rate by 25bps to a record low 0.75%. 7 of the 17 surveyed analysts forecast a rate cut, citing weaker consumer and business surveys as well as a weaker oil outlook, however the majority of analysts believed that the central bank would hold off until later in the year.

As a result of the rate decision, NOK saw substantial weakness on the back of the release, slumping to its weakest level in more than 13 years versus the dollar after the nation’s central bank unexpectedly cut interest rates to an all-time low and said it may ease monetary policy further to support an economy that’s been battered by the collapse in oil prices.

The krone slid 2.1 percent to 8.4471 per dollar as of 10:11 a.m. London time after reaching 8.4861, the weakest since April 2002. It fell 2.3 percent to 9.4636 per euro, having touched 9.5076, the weakest level since Aug. 26. The Norwegian currency dropped the most against the Swiss franc among its major peers, slumping 2.7 percent. “The move is logical given what they did today,” Carl Hammer, chief foreign-exchange strategist at SEB AB in Stockholm, told Bloomberg. “I thought it was equally likely that they would remain on hold and send a very dovish message, because the krone is already weak. The rate path was reduced substantially. It’s a very dovish message.”

Elsewhere the Taiwan central bank also unexpectedly cut their key interest rate by 12.5 bps to 1.75%, with the news reported by sources ahead of the official release.

So much for all that under appreciated global growth. As a result of the two latest rate cuts, expect the US to import even more deflation, making any case for a US rate hike that much more improbable.

Asian equity markets traded mixed following the tepid close on Wall Street, with Japan underperforming on return from the elongated weekend . Nikkei 225 (-2.8%) played catch up to the recent weakness seen in global equities as Japanese manufacturing PMI (50.9 vs. 51.2) missed expectations, with the auto sector also pressured as it reacts to the Volkswagen emission scandal. ASX 200 (+1.5%) was underpinned by gains in banking names, while Shanghai Comp. (+0.9%) is mildly positive, albeit off its best levels after the PBoC injected CNY 80Bn at a longer term of 14 days which resulted to a net weekly injection of CNY 40Bn vs. Prev. CNY 140Bn drain. JGBs traded higher amid softness in Japanese equities, while the BoJ also entered the market to purchase JPY 780b1n in government debt.

As noted above, European equity markets (Euro Stoxx: -0.7%) have swung between gains and losses, initially moving higher after the IFO data, before moving back into negative territory, weighed on by BMW (-8.5%) after reports in German press that BMW emission tests for their X3 model could show worse results than that of the Volkswagen Passat . Elsewhere, notable US earning reports today include Accenture before the open on Wall St and Nike after the closing bell.

Fixed income markets have seen muted price action so far in today’s session, with T-notes heading into US hours in modest negative territory ahead of the US USD 29b1n 7y Note auction, with the most recent auction saw the highest B/C since Nov’14.

The commodity market has seen strength this morning, bolstered by USD weakness with gold stronger by over USD 5, while WTI trades around the USD 45.00 handle to retrace some of the losses seen after yesterday’s DoE inventories saw a smaller drawdown than yesterday’s API headline, allied to an increase in US crude output. Looking ahead, today sees the EIA NatGas storage change data, expected to come in at 99bcf.

Of note Platinum fell to a 6-1/2-year low on Wednesday, on fears about reduced demand from the auto sector, where it is used in diesel catalysts to clean up exhaust emissions, while palladium, used in gasoline vehicles, surged 7 percent. Platinum has been hurt by news of Volkswagen AG’s falsification of U.S. vehicle emission tests as investors believed it could affect demand for diesel cars. The price of palladium, the predominant metal used in gasoline catalysts, rose on speculation that the Volkswagen scandal could increase demand for gasoline vehicles.

Key events on today’s calendar include US weekly jobs data and durable goods orders as well as comments from ECB’s Praet and Fed’s Yellen. Of note US data, including jobless claims, durables and home sales will be delayed today & not released to newswires 1st due to Pope’s visit.

Bulletin Headline Summary

- European equity have been weighed on by BMW after reports in German press that the Co.’s emission tests for their X3 model could show worse results than that of the Volkswagen Passat

- The Norwegian and Taiwanese central banks have both cut interest rates, taking the number of central banks to cut rates this year to 40

- Today’s highlights include US weekly jobs data and durable goods orders as well as comments from ECB’s Praet and Fed’s Yellen. Of note US data, including jobless claims, durables and home sales will be delayed today & not released to newswires 1st due to Pope’s visit

- Treasuries steady with global markets in disarray before Yellen speech at 5pm ET; week’s auctions conclude with $29b 7Y notes, WI yield 1.859% vs 1.930% in August.

- Global stocks have fallen every day since Fed refrained from hike last week, with emerging market stocks falling more today, ZAR approaches record low, NOK tumbles after surprise rate cut

- Norway’s central bank cut rates to an all-time low and said it may ease policy further as it seeks to rescue an expansion in western Europe’s biggest petroleum producer amid a plunge in oil prices

- Germany’s Ifo institute business climate index climbed to 108.5, more than forecast, from a revised 108.4 in August; almost all responses were received before the news of Volkswagen AG’s emissions scandal

- BMW AG fell as much as 9.3% after a German magazine reported that the X3 xDrive 20d sport utility vehicle emitted as much as 11 times the European limit for air pollution in a road test, adding to concern that the investigation weighing on Volkswagen AG may spread to other manufacturers

- Martin Winterkorn amassed a $32 million pension before stepping down as CEO of VBW Wednesday, and may reap millions more in severance depending on how the supervisory board classifies his exit.

- China’ leaders will further cut growth objective to 6.5%-7% for 2016, according to eight of 15 economists in a Bloomberg News survey conducted Sept. 17-22. Four said they expect a 6.5 percent goal.

- Japan’s Abe unveiled a new economic growth target, switching his policy focus to children and the elderly after the passage of unpopular defense bills last week sparked scuffles in parliament and undermined public support

- ECB handed EU15.5b to euro-area lenders in the fifth round of its long-term loan program to funnel money into the real economy; estimates in Bloomberg survey ranged from $35b- $120b

- Wall Street is close to cutting billions of dollars from the cost of a derivatives rule as a debate among regulators over how tough the provision should be shifts in banks’ favor

- Up and down the West Coast, home to the nation’s first $15 minimum wage laws, business owners are grappling with higher labor costs by experimenting with no-tip policies, employee ownership and trimming part-timers’ hours by working longer themselves

- $7.7b IG priced yesterday, no HY. BofAML Corporate Master Index widens 1bp to +168; YTD range 172/129. High Yield Master II OAS holds at +598; YTD range 614/438

- Sovereign 10Y bond yields mostly lower. Asian stocks mostly lower led by Nikkei, European stocks and U.S. equity-index futures decline. Crude oil, gold and copper gain

DB Conludes the overnight wrap

There wasn’t a whole lot of direction in markets yesterday. The initial soft opening we got in European equities on the back of the weak China manufacturing data was quickly cancelled out as the sectors which had tumbled on Tuesday, namely autos and miners, reversed course. ECB President Draghi made mention that the asset purchase programme has sufficient flexibility to increase the scope or size of purchases if necessary, but ultimately struck a somewhat cautious tone around emerging markets in particular. The US session was characterized by a decent selloff in the energy complex, while Atlanta Fed President Lockhart – who’s been busy of late – highlighted some concern around the divergence of market pricing of Fed liftoff timing versus what committee members think and also suggested that markets are overreacting to developments in China.

The end result was one of modest gains in European equity markets with the Stoxx 600 closing +0.09%, but markets across the pond failing to recover from the energy related weakness with the S&P 500 (-0.20%) and Dow (-0.31%) declining for the fourth session in the last five post last week’s FOMC decision. It’s been fairly quiet so far in terms of data but with capital and durable goods orders and new home sales data this afternoon in the US there should be a bit more for markets to sink their teeth into. Arguably, the bigger focus however will be on Fed Chair Yellen who is set to speak this evening (10pm BST). The speech is due to be on ‘inflation dynamics and monetary policy’ and while no Q&A is scheduled, given the uncertainty in markets since the Fed last week there will be a lot of investors hoping for some calming words from the Fed Chair. Before we get there, it’s straight to the latest in Asia.

Refreshing our screens, it’s been a fairly mixed start across bourses in Asia this morning. Mainland China bourses have seen modest gains, with the Shanghai Comp and CSI 300 up +0.27% and +0.20% respectively at the midday break. The Kospi (+0.07%) is also up a tad while the ASX (+1.15%) is leading gains this morning. Elsewhere, it’s been a weaker start for the Hang Seng (-0.93%), while Japanese equities appear to be playing catch up with the rest of the region after markets opened for the first trading session this week following a public holiday. The Nikkei and Topix have tumbled -2.11% and -1.66% respectively as we go to print. Not helping sentiment in Japan this morning was a softer than expected flash manufacturing PMI (50.9 vs. 51.2 expected), down 0.8pts from August.

Back to yesterday and starting with ECB President Draghi first of all. In his quarterly testimony to European Parliament lawmakers, Draghi’s comments came across as one which highlighted a sense of patience and caution most of all. Specifically he said that ‘more time is needed to determine in particular whether the loss of growth momentum in emerging markets is of a temporary or permanent nature’. He then went on to say that the ECB needs to look closer at assessing the driving forces behind the recent slump in commodities and market turbulence. There were however some more reassuring words with regards to the ECB’s reaction function. Draghi told the audience that the ‘asset purchase programme has sufficient in-built flexibility’ and that ‘we will adjust its size, composition and duration as appropriate, if more monetary policy impulse should become necessary’.

Meanwhile and speaking for the third time this week, the Fed’s Lockhart largely reiterated much of what we had already heard this week, although the policymaker highlighted that with regards to market pricing of Fed liftoff, ‘if the probabilities put on various dates are way out of whack with what the committee members seem to be thinking, I would be concerned about that’. On the subject of China, Lockhart was of the view that ‘China is slowing to a still respectable pace of growth’ and that ‘there is a decent chance that the world is overreacting’.

Price action in the rates space was fairly muted yesterday. 10y Treasury yields closed the session 1.6bps higher at 2.151%, while 2y yields finished up 2.5bps at 0.701%. It was a similar story in Europe with 10y Bunds up just shy up a basis point to 0.594%. Draghi’s comments supported a stronger day for the Euro which finished firmed 0.59%. Much of the price action was in the Oil complex however where WTI (-4.06%) tumbled back below $45/bbl. Brent (-2.71%) also fell and the latest leg lower came despite a decent drop in US crude stockpiles, although a buildup in Gasoline stockpiles seems to be largely attributed to yesterday’s weakness. That helped lead energy stocks lower in the US while closer to home there was a decent rebound for the bulk of European carmakers, led by Volkswagen which closed up over 5%.

Yesterday was also flash PMI day with the September composite reading for the Euro area coming in a tad softer than expected (-0.4pts to 53.9; 54.0 expected) but as our European Economics colleagues note, still broadly consistent with a quarterly growth projection in Q3 of +0.5% qoq. There were almost identical falls for both the manufacturing (-0.3pts to 52.0; 52.0 expected) and services (-0.4pts to 54.0; 54.2 expected) prints while regionally a fall in the German composite (-0.7pts to 54.3; 54.6 expected) was offset by a larger than expected rise in France (+1.2pts to 51.4; 50.4 expected). Our colleagues note that the monthly fall in the Euro area PMI was driven by the non-core countries and they calculate that the flash reading implies a one point decline in the composite PMI’s of Italy, Spain and Ireland on average. Over in the US, the flash manufacturing PMI showed no change relative to last month’s print at 53.0, although the data was a touch ahead of expectations of a fall to 52.8.

Looking ahead to today’s calendar now. Much of the focus this morning in the European timezone will be on Germany’s IFO survey for September. Elsewhere we’ll also get French confidence indicators out this morning as well as German consumer confidence. It’s a busy day for US data this afternoon. As mentioned the highlights are durable and capital goods orders and new home sales. On top of this, initial jobless claims, the Chicago Fed national activity index and the Kansas City Fed manufacturing activity index are also due. The aforementioned speech from Fed Chair Yellen this evening will also be a closely watched affair.

end

Let us begin: Japanese stocks tumble right at the get go. Chinese default risks rise and for the 4th day in a row, China lowers the value of the Yuan. By the end of the day, Japan closes down 498 points.

Wednesday night at 9:30/Thursday morning 9:30 am Shanghai time

(courtesy zero hedge)

Japanese Stocks Tumble After Holiday, China Default Risk Hits 2 Year Highs As Yuan Weakens For 4th Day

AsiaPac stocks are broadly lower at the open, following US’ lead as after being closed for 3 days, Japanese stocks open and catch down to global weakness with Nikkei 225 at 2-week lows. It appears it is time to “get back to work Mr.Kuroda,” as stocks are below Black Monday’s lows. Following last night’s dismal data, China credit risk rose once again to new 2 year highs. Once again, industrial metals are under pressure with iron ore, copper, and aluminum all lower (following “peak steel” comments). After 3 days of weakening (and Xi’s comments that China won’t weaken), PBOC weakend the Yuan fix again, pushing the offshore-onshore spread to 2-week wides (over 500 pips apart).

After 3 days of holidaying, selling resumes in Japanese stocks… ahead of tonight’s Japan PMI.

The good news to start the day in China, delveraging begins again…

- *SHANGHAI MARGIN DEBT BALANCE FALLS FIRST TIME IN THREE DAYS

As it appears the excitement of high beta fraud is back with ChiNext and Shenzhen outperforming this week…

But the path remains similar (albeit a little faster)…

Once again China injects more liquidity…

- *PBOC TO INJECT 80B YUAN WITH 14-DAY REVERSE REPOS: TRADER

And industrial metals are all lower after…

- *CHINA STEEL OUTPUT TO DROP TO 810 MLN TONS IN `15: CUSTEEL

- *CHINA STEEL OUTPUT HAS PEAKED, CUSTEEL’S YANG SAYS IN I’VIEW

But China default risk continues to leak higher…

Following Xi’s comments that China will not devalue the Yuan (and 3 days of devaluing the Yuan), PBOC weakened the Yuan fix again tonight…

- *CHINA SETS YUAN REFERENCE RATE AT 6.3791 AGAINST U.S. DOLLAR

Notably the spread between Onshore and Offshore Yuan has pushed to a 2-week high...

Charts: Bloomberg

“Why Has It Suddenly Stopped Working”: The Chart Every Trader Is Losing Sleep Over

In a must-read report which we will deconstruct shortly, Citi’s Matt King (who, as a reminder, is the person whose “Are the Brokers Broken” report issued in the first week of September 2008 was, according to many, one of the catalysts for Lehman’s failure simply by explaining to a largely clueless Wall Street just how broken the US financial system had become in late 2008) hits it out of the park with just one chart from his latest presentation, the chart which every market bull – whether they know it or not – is losing sleep over: has the only thing that has worked in the past 7 years, namely the central bank QE transmission channel, broken down.

Or, as Citi’s Matt King notes in what may be the only chart which traders should be obsessing over, “why has it suddenly stopped working“, by which he means the market’s favorable reaction to central bank liquidity injections.

His question: “have central banks lost their touch” and points out that while in the past QE injections have always resulted in improving risk asset prices (in this case represented by junk bond returns), this time is different.

The answer will determine whether the next move in the market is 20% higher or lower.

end

European affairs:

First Portugal

It seems that our good bank/bad bank scenario in Portugal just went south. The government could not sell the bad stuff.

This caused their budgets to skyrocket northbound and now Portugal is in trouble.

(courtesy zero hedge)

Budget Deficit Explodes Higher In Portugal After Government Throws In Towel On Bad Bank Sale

Just over a year ago, Portugal (which, you’re reminded,was just upgraded by S&P last week to BB+ stable) was forced to bailout the country’s second largest bank by assets Banco Espirito Santo. Here were the details, as dileneated by Bloomberg at the time:

- Portugal may use the Resolution Fund to recapitalize Banco Espirito Santo, Diario Economico reports, citing unidentified people linked to the process.

- Resolution Fund may inject more than €3 billion

- A “bad bank” may be created for the toxic assets of the credit portfolio

- Solution aims to rescue Banco Espirito Santo without spending taxpayers’ money, and is being prepared by the government and the Bank of Portugal

- From Aug. 4, Banco Espirito Santo will leave the stock market and will be 100% owned by the Resolution Fund, an entity created in 2012 and financed by Portuguese banks and by revenue from the special contribution that the banking sector pays the Portuguese state

- Resolution Fund will have to be given enough resources to capitalize Banco Espirito Santo, and according to legislation this can be done through a state loan or through a new special contribution imposed on the 84 institutions that contribute to the fund

- Part of the €6.4b that the Portuguese state still has available in the bank recapitalization facility that was included in Portugal’s bailout program may also be used to give the Resolution Fund the necessary resources to capitalize Banco Espirito Santo

- Portuguese authorities’ plans predict that the bank will be sold in the stock market within six months, with the proceeds from the sale being used to repay the Resolution Fund

The idea, basically, was to sell off Novo Banco SA (the “good bank” that was spun out of BES) and use the proceeds to pay back the nearly €5 billion injected by the Resolution Fund.

Unsurprisingly, the auction process hasn’t gone so well for any number of reasons, not the least of which is that two potential bidders (China’s Anbang Insurance Group and Fosun International) suddenly became far more risk-averse in the wake of the financial market turmoil in China. Talks with US PE (Apollo specifically) also went south, presumably because no one knows if this “good” bank will actually turn out to need more capital going forward given that NPLs sit at something like 20% while the H1 loss totaled €250 million thanks to higher provisioning for said NPLs.

As WSJ reported a week ago, Portugal finally threw in the towel and with the future now entirely uncertain, the government’s contention that the bailout won’t end up costing taxpayers looks increasingly dubious. Indeed, today we learn that Portugal has revised its 2014 budget deficit higher by a whopping 60% thanks to the failure to liquidate Novo. Here’s Reuters:

Portugal on Wednesday reported a budget deficit of 7.2 percent of gross domestic product for 2014 after including the cost of a state rescue of Banco Espirito Santo, which raised the gap from 4.5 percent reported previously.

The Bank of Portugal has so far failed to sell Novo Banco – the “good bank” successor of Banco Espirito Santo – and recover the rescue funds after bids came in too low earlier this month.

INE said the Novo Banco cost was included as the bank was not sold within a year from the rescue in August 2014.

The government had previously insisted that the rescue loans should not be counted towards the deficit, but it was up to Eurostat to make the final decision.

The government argues that there will be no impact on public finances or a cost to tax payers because the bank had not been nationalised but received the money via the Bank Resolution Fund, which is the joint responsibility of all Portuguese banks.

As Reuters also notes, the country “faces a general election on Oct. 4, completed an international bailout in May last year and the government has pledged to keep its budget tight and cut the deficit below 3 percent in 2015.” Indeed, the opposition is set to use the deficit issue to show that the policies Portugal has adopted in an effort to appease the troika have been for nothing. Here’s Reuters again:

Campaigning for an Oct. 4 national election, Prime Minister Pedro Passos Coelho dismissed the revision from a previously reported 4.5 percent as a “statistical correction, without any influence on this year’s deficit prospects or impact on debt”.

But a spokesman for the main opposition Socialist party, which is neck and neck with the ruling coalition in opinion polls, said the new figure showed Passos Coelho had failed both to meet budget targets and to sell the rescued bank quickly.

The Socialists say the data showing the budget gap back at levels last seen in 2011, the peak of Portugal’s debt crisis, shows sacrifices made by its people under a bailout that imposed sharp austerity and exacerbated recession were in vain.

And although one certainly imagines that Brussels would consider the extraordinary circumstances before seeking to tighten the proverbial screws on Lisbon much as it did on Athens, an “undesirable” political outcome may mean the troika is less forgiving than they otherwise would be.

Finally, it’s worth noting that the relationship between Novo’s predecessor and a certain nefarious cephalopod (detailed exhaustively here) has predictably come back to haunt the bank as one reason for the fraught nature of the auction process this year was the uncertain fate of the infamous Oak Finance Luxembourg SPV which, as Portugal’s central bank so eloquently put it in April, was disrupting the liquidation effort “at a crucial stage of collecting definitive offers from potential buyers, [creating] uncertainty as to the configuration of the balance sheet” and creating a situation wherein bidders might be “subject to significant future risks of litigation.”

So in the end, taxpayers will likely be on the hook for the BES debacle despite all assurances to the contrary delivered by the government last year, and because we would hate for anyone to let this go without appreciating how truly absurd the backstory is, we’ve included the background below for those interested to know more.

* * *(for the background of the story/see zero hedge)

end

And now Germany:

Is Volkswagen about to unless the next huge deflationary wave throughout the globe as inventory levels at the peak maximum and then trouble throughout this mega exporting country due to the cheating at WV

(courtesy zero hedge)

Is Volkswagen About To Unleash The Next Deflationary Wave?

With the new car bubble peaking, and the world’s automakers having ramped up production across the globe after seeing Fed-driven signals that all is well and all is going to get better…

…the slowdown in China already has many hitting the panic button (with production plunging, capacity utilization tumbling, and workweeks tumbling).

With this week’s ‘exogenous’ diesel-defect ‘event’, the inventory-problem that US automakers are facing…