Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1115.50 down $11.60 (comex closing time)

Silver $14.51 down 5 cents.

In the access market 5:15 pm

Gold $1127.50

Silver: $14.66

I wrote the following last Thursday:

“On the 24th of September, the comex options expired but we still have the LBMA options as well as the OTC options. Expect gold and silver to be relatively subdued until Oct 1.2015.”

still holds true today! Tomorrow the curse of the bankers will be off until next month’s expiry options.

First, here is an outline of what will be discussed tonight:

At the gold comex today, on first day notice we had a good delivery day, registering 121 notices for 12,100 ounces Silver saw 11 notices for 55,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 213.14 tonnes for a loss of 90 tonnes over that period.

In silver, the open interest fell by 620 contracts despite the fact that silver was up in price by 3 cents yesterday. The total silver OI now rests at 156,905 contracts In ounces, the OI is still represented by .784 billion oz or 113% of annual global silver production (ex Russia ex China).

In silver we had 93 notices served upon for 465,000 oz.

In gold, the total comex gold OI fell to 415,700 for a loss of 2070 contracts. This is par for the course as we always see a contraction as we approach an active delivery month. We had 121 notices filed for 12,100 oz today.

We had no changes in tonnage at the GLD; thus the inventory rests tonight at 684.14 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had no changes in silver inventory at the SLV to the tune of 859,000 oz/Inventory rests at 317.384 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fell by 620 contracts down to 156,905 despite the fact that silver was up by 3 cents in price with respect to yesterday’s trading. The total OI for gold fell by 2070 contracts to 415,700 contracts, as gold was down $4.60 yesterday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

Asian affairs:

3. a) China opens for trading 9:30 pm est Tuesday night/Wednesday morning 9:30 Shanghai time/More bad news from Japan where deflation is getting a stranglehold on the economy/factory output and retail sales also plummet/China revalues yuan again as more USA treasuries are sold/

(zero hedge)

3b) Southern China whacked today by 31 explosions leveling many buildings

(zero hedge)

c) Japanese pension funds lost 80 billion usa (10 trillion yen) because of the stock market collapse. On top of this, the morons are now buying junk bonds

(zero hedge)

European affairs:

4a) S and P now state that the ECB will need to increase QE by 120% to 2.4 trillion euros. Problem: where are they going to find the bonds to monetize?

(zero hedge/S andP)

b) Trifugura chief died of cancer this morning

(zero hedge)

The Global EConomy

a) Losses have wiped out 13 trillions of dollars from equity/now stands below 60 trillion.

(zero hedge)

Russia + USA affairs/Middle eastern affairs

5a) Russia bombs various sites in Syria

5b) Propaganda begins as the USA et al state that Russia is not hitting ISIS targets.

(zero hedge)

EMERGING MARKETS

6a) Emerging markets now witnessing credit default swaps risk rising!

(zero hedge)

. Oil related stories

6a)Both DOE and API report huge inventory buildups. However production levels are now at 2014 levels. Oil initially plummeted and then rebounded

(zero hedge)

7 USA stories/Trading of equities NY

a) Trading today on the NY bourses 1 commentary

(zero hedge)

b) The phony private ADP jobs report is out showing good gains in job growth. However it does show manufacturing jobs disappearing

(ADP/zero hedge)

c) Milwaukee PMI shows big decline

(Milwaukee PMI)

d) The huge Chicago PMI declines from 52 down to 48.1 verifying all regional PMI’s that the USA is in recession

(Chicago PMI/two commentaries)

e)Michael Snyder comments to those who think nothing has happened in September

(Michael Snyder/EconomicCollapse Blog)

f) Bill Dudley lying through his teeth

(zero hedge)

g) Gartman doubles down on going short the market/today he was stopped out but he continues to go short (zero hedge)

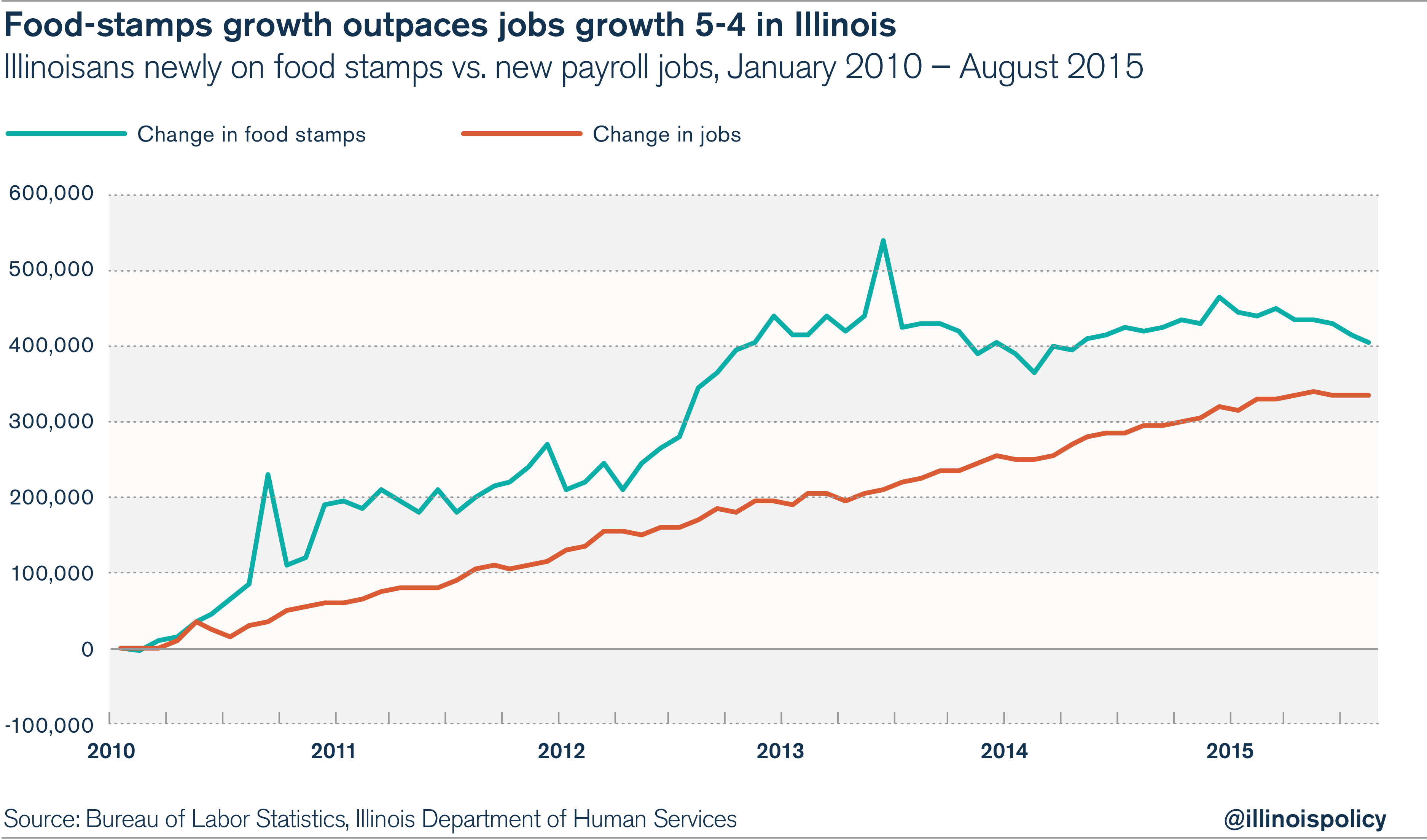

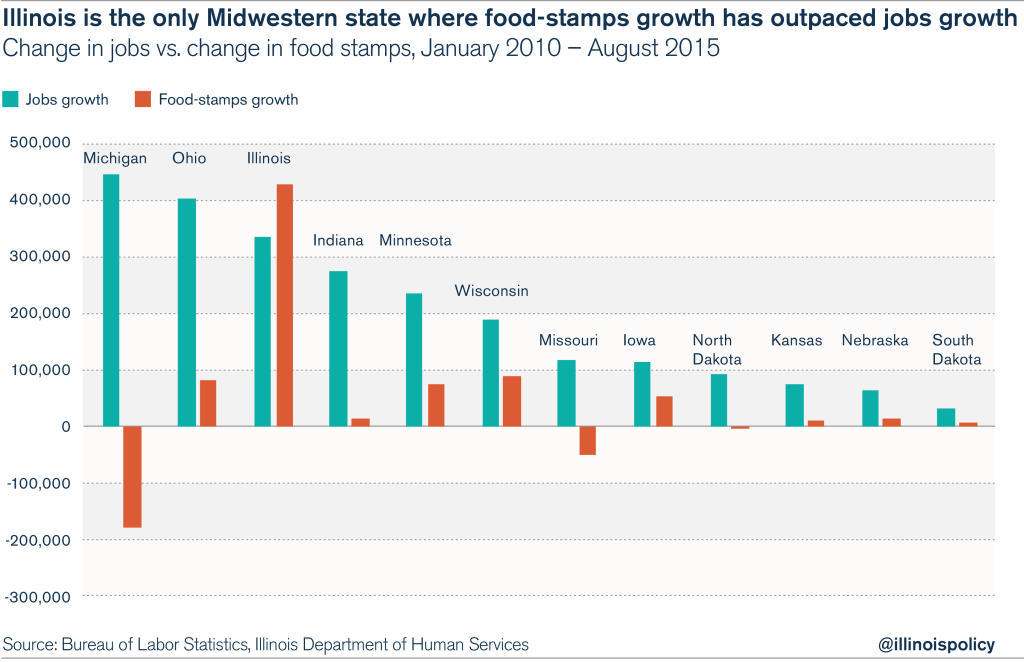

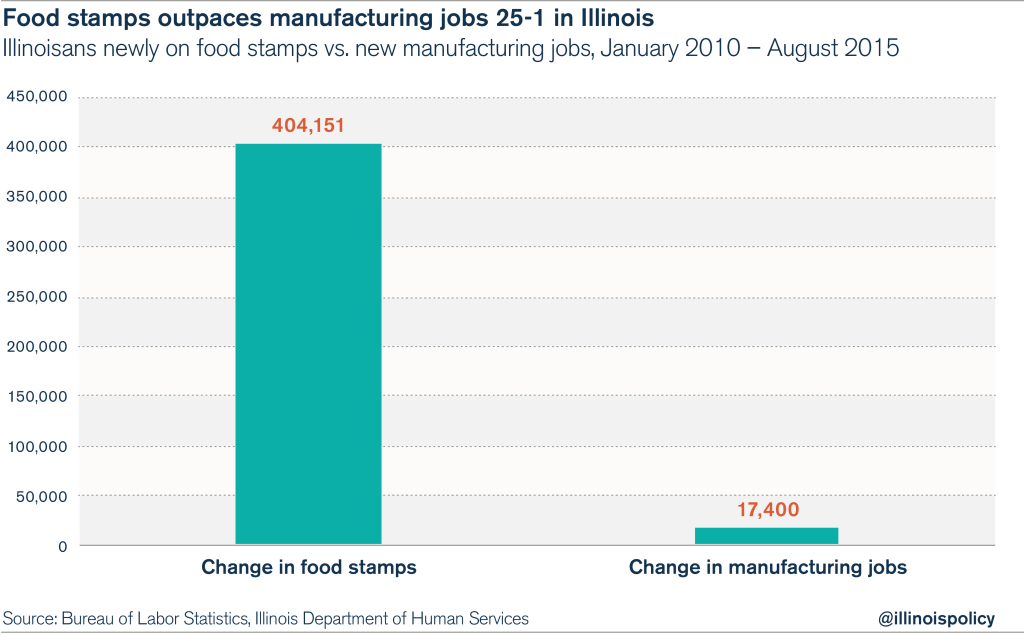

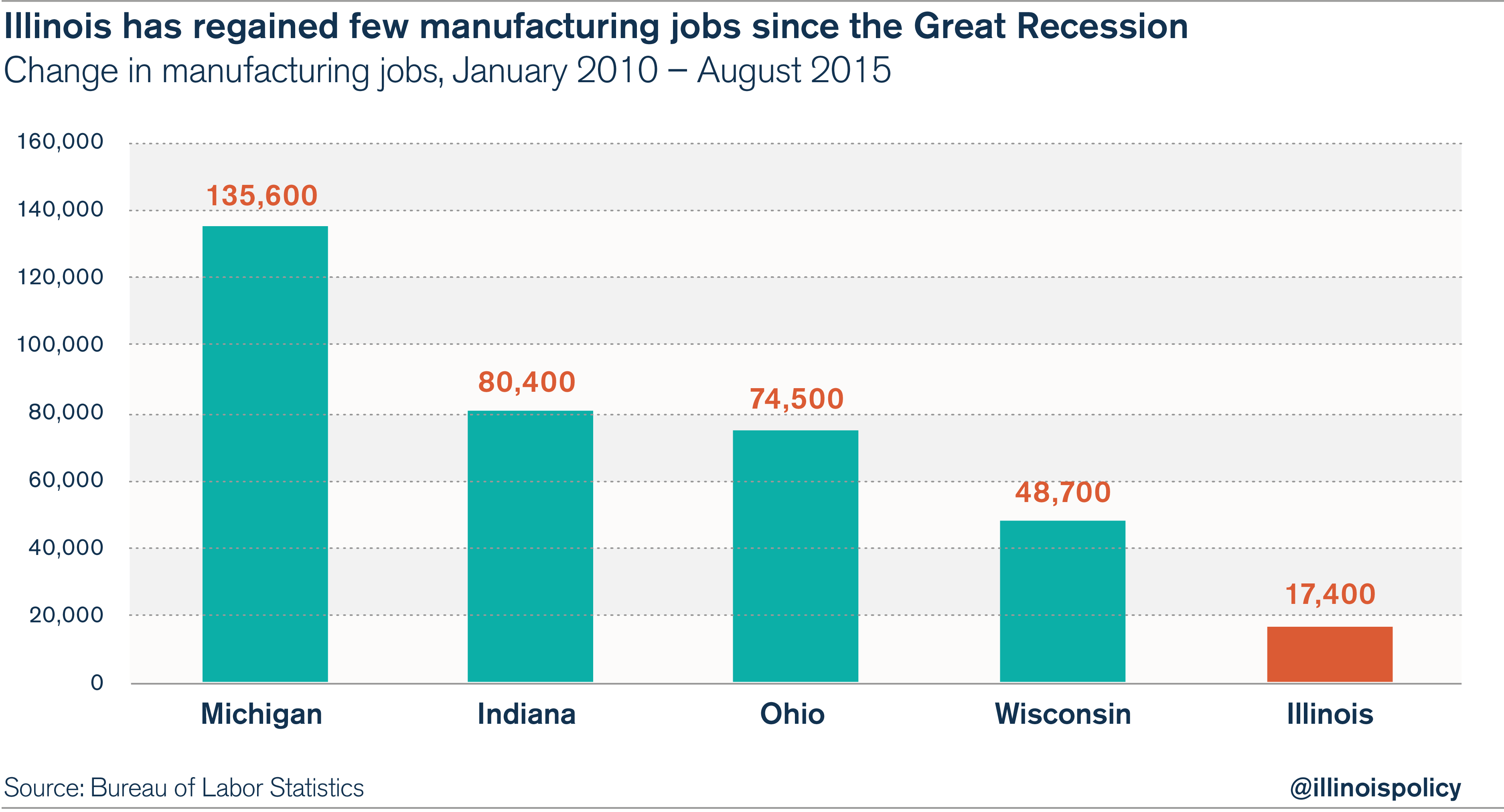

h) In Illinois, food stamp growth, did better than job growth from 2007 to now (Lucci)

10. Physical stories

- Goldcore/China officially adds 16.2 tonnes to official reserves. Zero hedge also discusses the purchase of Chinese gold in conjunction with Russia’s 19 tonnes of official gold addition.

- Simon Black: “What it means if gold is selling at a negative price!” (Simon Black)

- Ronan Manley discusses the secrecy behind official gold storage and Central banks’ silence on this/ (Ronan Manly)

- James Turk believes the USA will allow the dollar to sink to provide the impetus for stocks to continue to rise (Turk/Kingworldnews)

- GoldSeek interviews Bill Murphy (GATA/Goldseek)

- Steven St Angelo gives a great commentary on the huge demand for silver. He also discusses the problems facing the shale boys in the uSA (Steve St.Angelo/SRSRocco report)

- Wall Street Journal reports that so far this year with week ending Sept 19/gold withdrawals from SGE totaled 1819 tonnes or averaging 64.9 tonnes per week. (Wall Street Journal)

Let us head over to the comex:

October contract month:

Initial standings

September 29.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 121 contracts

12100 oz |

| No of oz to be served (notices) | 2971 contracts

297,100 oz |

| Total monthly oz gold served (contracts) so far this month | 121 contracts

(12,100 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | nil oz |

Total customer deposit: nil oz

***extremely unusual to have no activity of gold on first day notice especially with 9.6 tonnes of gold standing for delivery.

October silver Initial standings

September 30/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,239,823.09 oz

Brinks,CNT |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1001.000 oz (Delaware)

nil; |

| No of oz served (contracts) | 11 contracts (55,000 oz) |

| No of oz to be served (notices) | 47 contracts (255,000 oz) |

| Total monthly oz silver served (contracts) | 11 contracts (55,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,239,823.09 oz |

Today, we had 0 deposit into the dealer account:

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: 1001.000 oz

total withdrawals from customer: 1,239,823.09 oz

And now SLV:

Sept 30/no change in silver inventory at the SLV/Inventory rests at 317.384 million oz

sept 29.2015: we had another withdrawal of 859,000 oz from the SLV/Inventory rests at 317.384 million oz

sept 28./no change in silver inventory/rests tonight at 318.243 million oz/

Sept 25./we had another 954,000 oz of silver withdrawn from the SLV/Inventory rests this weekend at 318.243 million oz

Sept 24.2015: no change in silver inventory tonight/inventory rests at 319.197 million oz

Sept 23.2015: we had a huge withdrawal of 1.718 million oz at the SLV/Inventory rests at 319.197 million oz

Sept 22/no change in inventory at the SLV/Inventory rests at 320.915 million oz

sept 21.2015: no changes in inventory at the SLV/Inventory rests at 320.915 million oz

Sept 18.2015; no changes in inventory at the SLV/inventory rests at 320.915 million oz

sept 17.2017:no change in inventory at the SLV/rest tonight at 320.915

million oz/

sept 16.2015: no change in inventory at the SLV/rests tonight at 320.915 million oz/

Sept 15./no change in inventory at the SLV/rests tonight at 320.915 million oz

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

China Boosts Gold Reserves 1% in August, Diversifying Assets

In his article for Bloomberg Business Ranjeetha Pakiam takes a look at China’s recent accumulations in gold and how the country now compares in the world league table on gold holdings. He observes that there is a deliberate policy of increased transparency in China “as the country improves data quality, increases its presence in commodities trading and promotes the international role of the yuan”.

- China has overtaken Russia to become the country with the fifth-largest gold hoard

- China’s accumulation of physical gold is being tipped to continue by market experts

- Monthly reporting increases Chinese transparency after years of mystery

You can read the full article on Bloomberg Business

DAILY PRICES

Today’s Gold Prices: USD 1122.50, EUR 1000.08 and GBP 739.12 per ounce.

Yesterday’s Gold Prices: USD 1124.60, EUR 1001.16 and GBP 741.36 per ounce.

(LBMA AM)

Gold in GBP – 1 month

Gold closed at $1127.50 yesterday with a $4.40 loss on the day. Silver was up $0.05 at close to $14.64, a gain of 0.34%. Euro gold fell to about €1002, platinum remained at $914.

Download 7 Key Allocated Storage Must Haves

China Bought Gold With Proceeds From Record Sale Of US Treasurys

Two months ago, when China stunned the world in announcing it had officially “bought” 604 tons of gold for the first time since 2009 (this was untrue: China merely admitted to the world what we had reported for years, namely that it had been patiently accumulating gold via untraceable accounts and only now decided to reveal a fraction of its total holdings), we said that, contrary to the wrong “one-and-done” pundit assessment, China would continue “adding” to its gold holdings. To wit:

… now that the seal has been finally broken after so many years, and since today’s update indicates that Chinese gold numbers are clearly goal-seeked with a specific policy purpose – to boost confidence – we await for the PBOC to start leaking incremental gold holding data every month (and especially in months when the market crashes) which will bring us ever closer to what China’s true gold holdings are.

One month ago, we were proven correct when China indeed announced it had “added” another 19.3 tons of gold in July – even as it was dumping record amounts of Treasurys at the time as we previously reported.

Then, overnight, we got a second confirmation when the PBOC announced that China’s official gold holdings had risen again in August, increasing by 520,000 troy ounces, or 16.2 tons (which is more than 3 times the entire registered gold inventory in the Comex vault system), and bringing the new total to 54.5 million ounces, or 1,694 tons of gold. In dollar terms, Chinese gold holdings rose from $59.2 billion at the end of July to $61.8 billion.

However, even as China is “buying” gold, it is still doing so at half the pace of neighbor Russia, which as reported several days ago added 1,000,000 ounces or about 31 tons in the same month, bringing its total to 42.4 million ounces, or 78% of China’s holdings. Between China and Russia, some 47 tons of gold were purchased in the open market in past month.

Naturally, as has been the curious case for the past several months, the confirmation that China keeps buying gold merely served to push gold lower, and as of this moment gold was down to $1,117/ounce: the lowest level in two weeks.

A Commerzbank analyst had this to say about China’s ongoing gold buying spree: “Given the size of Chinese currency reserves and the extent of its domestic gold production, even higher gold purchases might have been assumed. That said, the decrease in currency reserves may have put the brakes on buying interest of late, in August, currency reserves declined to a two-year low of $3,557.4 billion.”

This is almost correct. The real message here is that in a month in which China (together with its Euroclear-held Belgium holdings) sold a record $83 billion in Treasurys…

… it had no qualms about rotating the sale proceeds into gold.

end

The total amount of gold withdrawals at the SGE for the year with the week ending Sept 19: 1819.00 tonnes. Thus for the 28 weeks, the average demand is 64.96 tonnes and it is up a huge 560 tonnes y/y.

(courtesy Wall Street Journal)

China gold purchases accelerating – WSJ

WSJ reports gold withdrawals from the Shanghai Gold Exchange have totaled 1819.9 tonnes so far in 2015, up 560.9 tons y/y. The piece cites analyst data that showed China imported 53.9 tonnes of gold from Hong Kong in August, more than double the amount imported in August 2014.

Analysts attributed demand to seasonal buying ahead of the festival season, the yuan’s devaluation and stockmarket turmoil. Demand from India was also likely to pick up ahead of the Hindu festival. Analysts added that price support is expected once the Fed rate decision removes uncertainty around gold’s outlook.

http://www.wsj.com/articles/gold-stays-low-despite-china-buying-1443555480

* * * * *

end

(courtesy Simon Black/GATA)

Simon Black: What it means when gold sells at a negative price

Submitted by cpowell on Wed, 2015-09-30 00:43. Section: Daily Dispatches

8:41p ET Tuesday, September 29, 2015

Dear Friend of GATA and Gold:

In his commentary tonight, “What It Means When Gold Sells at a Negative Price,” Sovereign Man’s Simon Black seems to assume that the whole world knows now that all major markets are rigged by central banks and their investment bank agents. He well may be right, but mainstream financial news organizations and even supposed gold-oriented Internet sites seem determined to pretend otherwise. Black’s commentary is posted at Sovereign Man here:

http://www.sovereignman.com/trends/what-it-means-when-gold-sells-at-a-ne…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy Ronan Manly/GATA)

Ronan Manly: Central banks’ secrecy and silence on gold storage arrangements

Submitted by cpowell on Wed, 2015-09-30 01:01. Section: Documentation

9:13p ET Tuesday, September 29, 2015

Dear Friend of GATA and Gold:

Gold researcher and GATA consultant Ronan Manly today identifies eight central banks that refuse to disclose where they are storing their countries’ gold reserves, including one — Finland — that refused to disclose the information but changed its mind nine months later. Also among the unaccountable central banks is the Bank for International Settlements, whose 2007 presentation to the Peruvian central bank boasted of the BIS’s “transparency” and “accountability.”

This secrecy almost surely involves the desire of central banks to intervene surreptitiously in the gold and currency markets or to assist such intervention surreptitiously.

Manly’s efforts show what financial journalism can achieve when it dares to confront primary sources, the most august of which are central banks. If only mainstream financial news organizations dared to attempt ordinary journalism like this.

Manly’s report is headlined “Central Banks’ Secrecy and Silence on Gold Storage Arrangements” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/central-banks-secrecy-and-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Huge demand for silver as buying intensity increases. Also a great report on the coming collapse of the shale business in the USA

(courtesy Steve St Angelo/SRSRocco report

PREPARING FOR COLLAPSE: Record Eight-Year Silver Buying Intensity Continues

by SRSrocco on September 29, 2015

While the Mainstream Media and Financial Network hacks delude Americans into believing the Fed and U.S. Treasury are in control of the financial and economic system, investors continue on a record eight-year buying spree of silver. This multi-year silver buying trend is unprecedented in history.

Precious metal investors need to understand just how different this current trend of elevated physical silver demand is compared to previous periods in history. Very few individuals realize that during the rise in the price of silver during the 1970’s, investors were net sellers of silver:

Total new silver supplies fell far short of meeting these requirements. From 1971 through 1978 there was a cumulative deficit of new supply over demand of 415.8 million ounces. The silver that filled this gap came from the 620.5 million ounces of silver inventories – many held by investors – built up during the previous seven years. By becoming net sellers of silver, investors replaced the U.S. Treasury as the source of silver to make up for a major, ongoing shortage of silver.

So, the price of silver rose from $1.5 to over $5 even though 620.5 million oz (Moz) were supplied from inventory stockpiles during 1971-1978… mainly from investors. The main drivers behind the price rise were skyrocketing oil prices and large buying by the Hunt Brothers and other institutions.

The public didn’t get involved in buying silver until the later part of 1979 and 1980. Unfortunately, this was at the time the price of silver peaked at $49 an ounce. As the price of silver fell to $4.98 in June 1982, so did silver investment demand. However, buying picked up once again later that year due to several circumstances:

In late 1982 investor interest in silver was rekindled by several forces, all of which emerged at roughly the same time. The international financial market panic led some investors to turn to silver. Others were attracted by what they saw as unsustainably low prices. Investment demand also was encouraged by a rapid easing of credit market conditions by monetary authorities in most industrialized nations; this easing led to an immediate revival of inflation fears. As a result of all of these forces coming to bear at once, investment demand picked up during the second half of 1982 and the first quarter of 1983. This influx of investor buying helped take silver prices from the June 1982 low of $4.98 to a peak of $14.72 in March 1983.

Here we can see, that when investors returned back into the silver market, the price of silver increased from $4.98 in June 1982 to a high of $14.72 in March 1983. The difference in the 1982-1983 silver buying trend compared to the previous decade (1971-1978), is that the public was the main driving force in silver demand, while large individual buyers (Hunt Brothers & etc) were the dominant players.

Furthermore, the public’s buying of physical silver during this time occurred during brief periods (1979-1980 & 1982-1983). This is much different from the current trend that started in 2008…. the year the U.S. banking industry died.

This can be seen in the following chart:

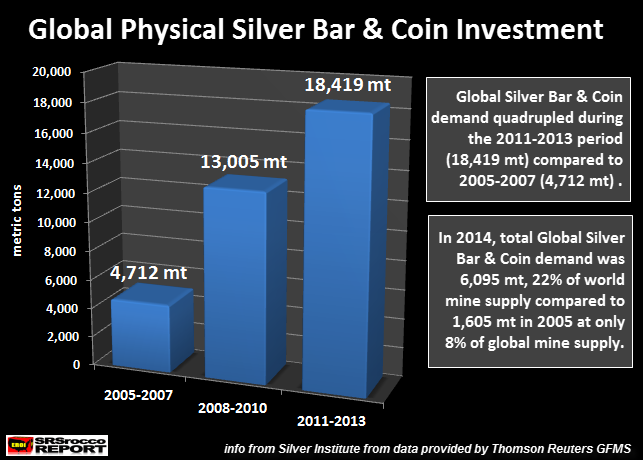

Total Silver Bar & Coin demand in 2007 was 51.2 Moz. This picked up significantly in 2008 to 187.3 Moz and remained elevated for the next seven years. Silver Bar & Coin demand hit a record 243.6 Moz in 2013, due to low prices, declined in 2014 to 196 Moz, but will likely jump substantially in 2015 to over 240 Moz.

Investors purchased a stunning 1.2 billion ounces of silver from 2008 to 2013. Of the 1.2 billion oz in Silver Bar & Coin demand, Official Coin sales accounted for 657 Moz or 55% of the total.

Even though the price of silver has declined since 2011, investors continue to purchase record amounts of physical metal. This is a much different situation than the previous buying periods of 1979-1980 and 1982-1983. In both of these buying periods, the price of silver rose considerably. However, in this four-year period since the price of silver peaked in 2011, investors are buying more silver than ever.

Silver Product Shortage With Three Times The Product Supply

I discussed this topic in my previous article BEWARE: What If This Retail Silver Investment Shortage Doesn’t End:

SilverDoctors interviewed Tom Power, CEO of the Sunshine Mint back on Sept 7th. If you haven’t listened to that interview, I highly recommend you do. The Sunshine Mint is one of the largest silver mints in the United States. They provide a good portion of the silver blanks for the U.S. Mint.

One of the interesting things Tom said during the interview was that the Sunshine Mint’s annual silver production level increased three times from 25 Moz in 2008 to an estimated 75-80 Moz this year. We must remember, there was a huge spike of retail silver investment demand in 2008 when the price of silver fell from $20 to $8.50. There were huge product delays and high premiums… much like the present conditions today.

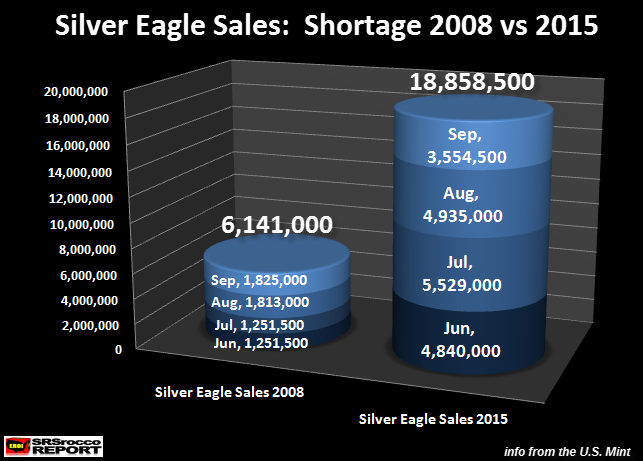

Now, what I didn’t include in that article is the chart below. Clearly, we can see just how much more Silver Eagle buying is taking place this year compared to 2008:

The Silver Eagle shortage in 2008 started in June after the price peaked in March at $21 due to the bankruptcy of Bear Stearns. Even though the price of silver declined until October after a hitting second peak in July 2008 of $19, investors continued to purchase record amounts of silver. This caused more retail shortages, thus pushing premiums to extremely high levels.

Interestingly, the same jump in Silver Eagle buying also took place in June this year due to the possible Greek Exit of the European Union and the Chinese market crash. Although, the amount of Silver Eagle buying of 18.8 Moz (Jun-Jul-Aug-Sep 2015) was more than three-times the 2008 period of 6.1 Moz.

Thus, the silver product shortages are taking place even with three-times the silver product supply. This is an important factor to understand.

While silver product shortages are taking place, they are not yet widespread. So, for all the precious metal investors who like to leave comments on various blogs that they could buy 30 Silver Eagles on Ebay with no wait, or from another dealer with with only a week or two delivery time… there are still shortages taking place in many areas in the retail market.

Short-sighted investors need to realize that country, or worldwide shortages don’t happen overnight. They start in certain areas and move throughout the system. If financial and economic conditions deteriorate by the end of 2015 and into 2016, silver product shortages will only get worse. Which means, we could see retail product shortages extend into the wholesale 1,000 oz bar market.

Present Silver Buying Trend Is Unprecedented

The present eight-year silver buying trend by the public signifies a much different situation than what took place during the 1979-1980 and 1982-83 periods. Investors bought record amounts of physical silver during the 2008-2011 price rise period and even more during the price decline period from 2012-2015.

Silver Bar & Coin Buying Trends

2008-2011 = 628.5 Moz

2012-2015 = 817.6 Moz (based on 2015 estimated 24o Moz)

Investment demand 1981-early 1982 and 1984 and onward, declined as the price of silver fell. However, the 2012-2015 silver price decline period will actually show an increase in buying (817.6 Moz estimated) compared to the price-rise period (2008-2011) of 628.5 Moz.

Thus, the present silver buying trend is unprecedented. Why? It’s taking place during a four-year price decline period while the previous surges occurred as prices spiked or increased (1979-1980, 1982-1983 & 2008-2011).

I believe investors are still buying silver even though the price has continued to fall because they realize the GREAT FINANCIAL COLLAPSE is still coming. Furthermore,the highly leveraged debt-based financial system is taking place as the world peaks in global oil production. A perfect example of this forecasted rapid decline is U.S. Shale oil production.

The Coming Collapse Of U.S. Shale Oil Production

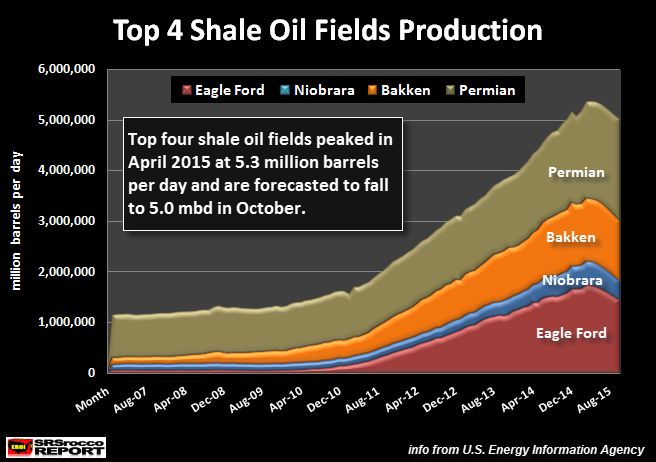

According to the EIA – U.S. Energy Information Agency, U.S. oil production peaked in June at 9.6 million barrels per day (mbd) and is currently at 9.1 mbd. However, production from the top shale oil fields peaked in April at 5.3 mbd and is forecasted to fall to 5.0 mbd in October:

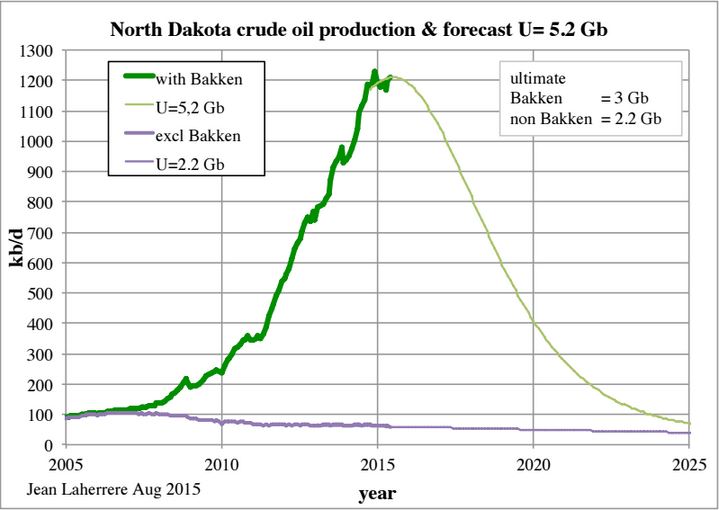

To get an idea of just how bad the coming collapse in U.S. shale oil production will be, let’s take a look at two charts by Jean Laherrere based on ultimate recoverable reserves from the Bakken and North Dakota:

The GREEN LINE in the chart represents Bakken oil production (inside North Dakota, as small percentage is from Montana), while the purple line denotes the rest of North Dakota. As you can see, Jean’s chart shows Bakken oil production peaking and falling to 400,000 barrels per day (bd) by 2020 and less than 100,000 bd by 2025.

This is a huge drop from the 1.2 mbd of oil the Bakken is producing currently. If we assume the same kind of declines in the Eagle Ford and other shale oil fields, U.S. domestic oil production will likely fall 30-40% by 2020 and 60-70% by 2025. This will be the nail that finally destroys the U.S. Empire and economy.

Unfortunately, there are still many analysts and investors who are completely clueless to the coming energy crisis. I still receive countless emails from readers informing me that there are trillions of barrels of oil still out there in LaLa Land or there are new energy technologies that will solve all our problems.

Actually, I wish this was true, but it isn’t. This sort of wishful thinking takes place because individuals do not want to face the reality…. a reality that is just too damn horrible to swallow. So, instead of facing reality, many continue dream of SUGAR PLUMS DANCING IN THEIR HEADS.

As precious metal analysts-investors bicker about whether THIS IS A SILVER SHORTAGE or not, the U.S. and world move closer to the worst collapse in human history. This is actually much worse than musicians playing music on the Titanic as it sinks. Why? There were 713 survivors on the Titanic of the total 2,229 passengers and crew. Thus, 32% survived the sinking of the Titanic, whereas only 1-2% of investors have gold and silver lifeboats.

end

(courtesy James Turk/GATA)

Turk thinks Fed will let dollar fall to sustain stock prices

Submitted by cpowell on Wed, 2015-09-30 01:18. Section: Daily Dispatches

9:17p ET Tuesday, September 29, 2015

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk tells King World News that he thinks the Federal Reserve will let the U.S. dollar sink to help sustain stock prices. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/is-the-global-house-of-cards-finally-going-to-c…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy Bill Murphy/GATA/Goldseek)

GoldSeek Radio interviews GATA Chairman Bill Murphy

Submitted by cpowell on Wed, 2015-09-30 01:42. Section: Daily Dispatches

9:40p ET Tuesday, September 29, 2015

Dear Friend of GATA and Gold:

GoldSeek Radio’s Chris Waltzek today interviewed GATA Chairman Bill Murphy, who welcomed financial analyst Chris Martenson to the ranks of those who acknowledge central bank rigging of the gold market. Murphy speculated that a derivatives problem likely will spark the gold market’s liberation. The interview is 10 minutes long and can be heard at GoldSeek Radio here:

http://radio.goldseek.com/nuggets/murphy.09.28.15.mp3

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

1 Chinese yuan vs USA dollar/yuan rises quite a bit in value, this time at 6.3555/Shanghai bourse: in the green, hang sang: green

2 Nikkei closed up 457.31 or 2.70%

3. Europe stocks in the green /USA dollar index up to 96.13/Euro down to 1.1211

3b Japan 10 year bond yield: rises to .352% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.27

3c Nikkei now well below 18,000

3d USA/Yen rate now above the important 120 barrier this morning

and thus supplying the necessary ramp for bourses.

3e WTI: 45.09 and Brent: 48.15

3f Gold down /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises slightly to .589 per cent. German bunds in negative yields from 4 years out

Greece sees its 2 year rate rises to 11.12%/Greek stocks this morning down by 0.26%: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 8.25%

3k Gold at $1123.70 /silver $14.66 (8 am est)

3l USA vs Russian rouble; (Russian rouble up 57/100 in roubles/dollar) 65.35,

3m oil into the 45 dollar handle for WTI and 47 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9728 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0906 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund now in negative territory with the 10 year moving further from negativity to +.589%/5 year rate at 0.00%!!!

3s The ELA lowers to 89.1 billion euros, a reduction of .6 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.10% early this morning. Thirty year rate below 3% at 2.89% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks, Futures Soar As Europe Joins Japan In Deflation, Surge Driven By Hopes For More Japan, ECB QE

Terrible economic news is wonderful news for markets, all over again, and with the worst S&P500 quarter since 2011 set to close today, some horribly “great” news is just what the window-dressing hedge funds, most of whom are deeply underperforming the broader market (not to mention Dennis Gartman) ordered.

Days after Japan returned to deflation for the first time since 2013, confirming Abenomics 1.0 was a failure (hence Abe’s launch of Abenomics 2.0 which will be even worse)…

… and after reporting even more abysmal industrial production and retail sales data, which in turn prompted a bevy of banks to cut their Q3 GDP forecasts to negative (JPM now expected Q3 GDP of -1.0%) and unleash yet another technical recession for Japan, the fifth since the financial crisis, the Yen plunged following the latest round of loud, renewed calls for a boost to the BOJ QE, and JPM in fact made the October 30 BOJ meeting its base case for further central bank easing. Abe advisors Honda and Takenaka both confirmed more BOJ easing is just a matter of time, as a result pushing the USDJPY solidly above the market critical 120 level.

And then, just a few hours later, we got the latest inflation, or rather deflation, data out of Europe, where consensus hoping for an unchanged print was once again disappointed when the September CPI print came in negative once again on the back of a drop in commodity prices, confirming the latest inflationary impulse from the March launch of QE is officially over.

As a result of Europe’s relapse into deflation, hours ago S&P announced that it believes the ECB will more than double its QE program from €1.1bn to €2.4 bn: “We believe the ECB will extend its QE program beyond September 2016, most likely until mid-2018, and that it could reach €2.4 trillion–more than twice the original €1.1 trillion commitment.“

Nothing new here, just more people piling onto the more stimulus train before this too fail, and the now inevitable monetary paradrops begin.

Finally, jumping on board the “moar stimulus” train, was China which whose central bank and banking regulators just announced today that down payment requirement for first mortgage will be lowered from 30% to 25%, while additionally China would also cut in half the taxes on small car purchases in a bid to stimulate its sputtering auto market. How this latest attempt to reflate the previously burst housing bubble will help the proper allocation of capital is anyone’s guess, but for now markets are loving this trifecta of “bad news is good news” from around the globe, even as such “hawks” as Bill Dudley and Janet Yellen are set to speak later today in the US.

Looking at markets it was blast off from the beginning entirely on the back of the diagonal move in the USDJPY: Asian equity markets traded mostly higher as they rebounded from yesterday’s substantial declines. The Nikkei 225 (+2.7%) recovered from 8-month lows and yesterday’s 4% slump, to return back above 17,000 as JPY softened, while the ASX 200 (+2.1%) was lifted by strength in large banks. Shanghai Comp. (+0.5%) was supported by gains in the auto sector, after China announced it is to halve taxes on small car purchases. JGBs tracked the losses seen in USTs on the last day of fiscal H1 trade amid gains in equities with investors side-lined until tomorrow’s 10yr auction, while the BoJ entered the market to purchase JPY 1.18trl as expected.

Equities in Europe traded higher since the open (Euro Stoxx: +2.4%), largely in reaction to stock specific news flow, which in turn meant that Bunds traded lower, albeit marginally. Glencore (+11.0%) shares surged as it continued to reaffirm that it is financially sound, while VW (+2.7%) shares advanced in reaction to reports that China is to halve taxes in small car purchases, together with WSJ reports, which suggested that the company could avoid criminal prosecution. At the same time, shares of UK retailer Sainsbury’s jumped over 10% after it said full-year profits were set to be better than expected.

Bonds are understandably weaker as T-Notes head into the pit open firmly in negative territory in line with the pickup in sentiment and strength in global equities , while over in Europe the latest LTRO auction saw ECB allot EUR 11.842bIn with 92 bidders and long end peripherals have outperformed after long end Bunds have lead the way lower throughout the European morning.

In commodities, softness in the metals complex has been observed in early European trade, weighed upon by a stronger USD with platinum set for its worst performing quarter in nearly seven years, on fears of falling demand from the VW scandal, while gold is set for its worst quarter in nearly a year as participants continue to look ahead to a Fed rate hike. Elsewhere Brent and WTI crude futures have pared back some of yesterday’s losses after API crude oil inventories showed a build of 4600K (Prey. drawdown on 3700K), seeing the 2nd biggest weekly build in over 5 months.

In FX, month and quarter-end related flows proved supportive for the USD index, which in turn ensured that USD/JPY reclaimed 120.00 level, while EUR/USD was also weighed on by carry related flows amid better bid stocks, as well as lower EUR/GBP amid a large payment from the EU to UK farmers. Elsewhere, despite the mixed performance by energy and metals markets, commodity sensitive currencies rose, in part benefiting from the alleviation of fears regarding the future of the troubled mining and trading giant Glencore. While the upside by NZD was aided by comments from Westland Milk who lifted their 2016 forecast pay-out and said they see some signs of increasing demand and price recovery.

On today’s US calendar, we have the Milwaukee ISM (expected to improve to 48.5), the Chicago Purchasing Managers index (expected to fall to 53) and the September ADP employment change number (expected in steady at 190k) to set us up nicely for Friday’s NFP number. We also have a fair amount of Fed speak with Dudley, Bullard and Yellen all scheduled to opine on things with the latter two due to make opening remarks at the Fed’s annual Community Banking conference.

* * *

Bulletin Headline Summary from Bloomberg and RanSquawk

- Month and quarter-end related flows support the USD to see USD/JPY break back above 120.00

- Equities in Europe trade higher since the open (Euro Stoxx: +2.4%), largely in reaction to stock specific news flow, which in turn meant that Bunds trade lower, albeit marginally

- Today sees the release of the latest US ADP employment change report, Chicago PMI and the weekly DOE inventories update as well as comments from Fed’s Dudley, Yellen and Brainard

- Treasuries drop in overnight trading as equity markets see robust gains as ECB begins to debate expanding QE after consumer prices declined y/y.

- Glencore has recouped most of the losses from Monday’s 29 percent plunge as the shares rebounded for a second day on higher metal prices and speculation the stock is cheap

- Glencore is unlikely to lose access to its $15 billion of syndicated loans, even as liquidity concerns weigh on its stock and bond prices, according to Macquarie Group

- Chesapeake Energy is letting go of about one in six employees, the latest blow to a workforce that enjoyed boom years under shale wildcatter Aubrey McClendon and shrank since his departure as the natural gas producer grapples with a downturn

- A key gauge of wealth in Britain has risen above its pre- recession peak and workers are seeing their compensation grow at the fastest pace in eight years

- China cut the minimum down payment requirement for first- time homebuyers, stepping up support for the property market amid an economic slowdown

- Sovereign 10Y bond yields mostly higher. Asian and European stocks gain, U.S. equity-index futures gain. Crude oil drops, copper rises, gold lower

Central Banks

- 8:30am: Fed’s Dudley speaks in New York

- 3:00pm: Fed’s Yellen, Bullard speak in St. Louis

- 8:00pm: Fed’s Brainard speaks in St. Louis

DB’s Jim Reid completes the overnight wrap

Its been an action packed last two weeks in markets and there’s plenty to consider what with the Fed, VW, Glencore and a general uneasiness in markets all contributing to the risk off. I’ll be trying to make some sense of it all in tomorrow’s EMR with some comments so watch this space.

For now today ends what is likely to be one of the worst quarters for global risk for 4 years and at the moment we’re all looking for the catalyst as to what brings this extended period of volatility and uncertainty to an end. Yesterday was a quieter day but despite there being little in the way of new news or headlines, the S&P 500 capped a 1.5% intraday range but finally snapped five days of consecutive losses and nudged into positive territory in the final minutes of trading, closing up a modest +0.12% after being supported by a rebound in healthcare names. That was after having traded between gains and losses over a dozen times during the session. Credit markets, or more specifically primary markets continue to be weighed down by the lack of stability with yesterday case in point after no deals were done in the Dollar market and up to six issuers were said to have stood down in the European session.

Volatility was the dominating feature for European equity markets as well and despite buyers re-emerging for Glencore and sending the stock soaring +17%, the Stoxx 600 failed to fully recover from an early 2% fall, eventually closing -0.69%. There were similar falls for other DM bourses but it’s the peripherals which are outperforming at the moment with the Spanish IBEX in particular having closed the session flat. VW tumbled another 4% but much of the focus in Germany was on a disappointing headline CPI, stoking the ECB stimulus fire some more.

More on that shortly, but refreshing our screens this morning, the risk tone is generally firmer in Asia as we prepare ourselves for quarter end. The Hang Seng, HSCEI and Shanghai Composite indices are up +1.4%, +2.4% and +0.7%, respectively as we go to print. The KOSPI (+0.3%) resumed its trading session with modest gains while interestingly the Nikkei (+2.6%) is doing well despite some weak industrial data. Japan’s industrial production fell unexpectedly (-0.5% mom v +1.0% expected) in August. Retail sales were also flat month-over-month versus consensus forecast of a 0.5% gain. The disappointing data perhaps strengthens the case for more policy stimulus in Japan. Turning to credit markets, new issuance activity in has been fairly muted in Asia which has been a trend for some time now given the uncertainties around EM Asia/China although it does seem that the onshore CNY bond market is offering Chinese corporate an alternative source of funding. Secondary credit spreads retraced some of the widening yesterday with Asia iTraxx and benchmark IG cash spreads around 3-5bps tighter as we type. The UST 10yr yield is a smidgen higher but still wrapped around the 2.06% area as we type.

Back to markets yesterday. The highlight of yesterday’s economic data was out of Germany where more energy-price related weakness resulted in the headline September CPI reading falling a greater than expected -0.2% mom (vs. -0.1% expected). That was enough to nudge down the annualized rate two-tenths to 0.0% (vs. +0.1% expected) while the harmonized rate dipped into negative territory at -0.2% yoy, heightening concerns for today’s Euro area inflation reading. Despite the softer than expected headline reading, our colleagues in Europe calculate the core print to have remained stable around +1.2% yoy, which is easily inside the tight band it has stayed in since 2012. ECB Governing Council member, Weidmann, speaking shortly after the data said that the ECB should ‘look through’ the energy-price swings on inflation, saying also that deflation fears are overstated and have instead dissipated. Its probably fair to say he is again not in an immediate rush to vote for more QE!

Away from this, Euro area consumer confidence was unchanged at the final reading for September as expected at -7.1. There was better news elsewhere however with better than expected indicator prints for economic (105.6 vs. 104.1 expected), business climate (0.34 vs. 0.21 expected), industrial (-2.2 vs. -3.8 expected) and services (12.4 vs. 10.0 expected) confidence. Meanwhile, over in the UK we saw mortgage approvals tick up 2k to 71k (vs. 69.8k expected) in August.

Over in the US, the highlight of the dataflow was the September consumer confidence reading which rose 1.7pts to 103.0 (vs. 96.8 expected), driven by the present situation index, and to the second-highest level in eight years. Elsewhere, the July S&P/Case Shiller house price index declined 0.2% mom in July after expectations for a slight rise of +0.1%. A downward revision to the previous month however saw the annualized rate nudge up slightly to +4.96% (vs. +5.15% expected). Meanwhile, speaking to the Nikkei, Cleveland Fed President Mester largely re-affirmed what we already knew in saying that the decision of the Fed to ‘not raise rates in September was really a decision about risk management’.

Looking to the day ahead and it looks set to be a busy one. In the UK we have the latest house price data (with the rate of appreciation expected to rise to +3.8% YoY), the latest consumer confidence (expected to fall) and the final read on Q2 GDP (no change expected). We have the latest CPI inflation from Italy (expected to fall to +0.3%) and the Euro area (expected to fall to 0%). The Euro area core inflation is expected to remain steady at +0.9%. We also have September unemployment from Germany (expected in steady at 6.4%), Italy (expected steady at 12%) and the Euro area (expected at 10.9%). We also have the August retail sales number from Germany (expected steady at +3.3%) and French consumer spending. Over in the US we have the Milwaukee ISM (expected to improve to 48.5), the Chicago Purchasing Managers index (expected to fall to 53) and the September ADP employment change number (expected in steady at 190k) to set us up nicely for Friday’s NFP number. We also have a fair amount of Fed speak with Dudley, Bullard and Yellen all scheduled to opine on things with the latter two due to make opening remarks at the Fed’s annual Community Banking conference.

(courtesy zero hedge)

Peak Japaganda: Advisers Call For More QE (But Admit Failure Of QE); China’s Yuan Hits 3-Week High

Asian markets are bouncing modestly off a weak US session, buoyed by more unbelievable propaganda from Japan. Abe’s proclamations that “deflationary mindset” has been shrugged off was met with calls for more stimulus, more debt monetization, and an admission by Etsuro Honda (Abe’s closest adviser) that Japan “is not growing positively” and more QE is required despite trillions of Yen in money-printing having failed miserably, warning that raising taxes to pay for extra budget “would be suicidal.” Japanese data was a disaster with factory output unexpectedly dropping 0.5% and retail trade missing. Markets are relatively stable at the open as China margin debt drops to a 9-month low. PBOC strengthened the Yuan fix for the 3rd day in a row to its strongest in 3 weeks.

We begin the evening in Asia with some exceptional double-talk from who else but the Japanese leadership.

First Abe:

- *ABE: WILL RESHUFFLE CABINET ON OCT. 7(should fix everything)

- *ABE: WOMEN AND ELDERLY SHOULD BE TAPPED BEFORE IMMIGRANTS (not quite sure what he means there)

- *ABE: CLOSE TO ESCAPING DEFLATION (nope!)

- *JAPAN HAS SHRUGGED OFF `DEFLATIONARY MINDSET,’ ABE SAYS (nope!)

- *JAPAN’S CPI HAS `MADE A TURNAROUND,’ PRIME MINISTER ABE SAYS (nope!)

Japan just dipped back into deflation…

Then came Former Economy Minister Takenaka:

- *TAKENAKA: JAPAN SHOULD COMPILE 5T YEN EXTRA BUDGET IN AUTUMN(fiscal stimulus, ok)

- *TAKENAKA: FOLLOWED BY MORE BOJ EASING (well who else is going to monetize that debt?)

- *TAKENAKA: YEN IN ‘COMFORTABLE RANGE’ OF 115-120 VS DOLLAR

Then one of Abe’s closest advisers accidentally spilled some truthiness (as The FT reports):

Japan needs more economic stimulus to stave off a serious shock from China,according to one of Prime Minister Shinzo Abe’s closest advisers.

Etsuro Honda, an architect of Abenomics in his role as special adviser to Mr Abe, said passing a supplementary budget to boost the stagnant economy was an “urgent task”.

“I don’t think we should call it a technical recession yet, but generally speaking, the Japanese economy is in a static situation,” Mr Honda said in an interview with the Financial Times. “It is not growing positively.”

And he is right – as Japan heads for Quintuple Dip recession…

and it appears, despite China’s reassurance, all is not well…

“I’m sure that something serious is happening in China,” he said, arguing that a shift towards the service industry in China could not explain how far its imports have fallen, or other measures such as electricity consumption.

And do not even think about raising taxes to cover this additional budget…

Mr Honda said: “Definitely if something serious happens outside of Japan, like the Lehman shock, we cannot raise consumption tax. It would be suicidal.

“At this moment, all that I can say is ‘I don’t know’.”

And then Japanese data hit – and it was a disaster…

- Japan Aug. Industrial Production Falls 0.5% M/m; Est. +1% (oops!)

- *JAPAN AUG. RETAIL SALES UNCHANGED M/M (Exp. +0.5%)

* * *

Following Daiichi Chuo’s bankruptcy:

- *DAIICHI CHUO SAYS FILED FOR BANKRUPTCY AFTER OVER INVESTING

- *DAIICHI CHUO TRADES IN TOKYO, FALLS TO AS LOW AS 1 YEN

Other shipbuilders are under pressure:

- *DAEWOO SHIPBUILDING FALLS 8% IN SEOUL TRADING

And today’s bounce in Glencore has the rest of the commodity/miner sector in confidence-boostingh mode…

- *FORTESCUE CEO SAYS CO. CAN WEATHER VOLATILITY IN MARKETS

- *FORTESCUE IN ‘FANTASTIC POSITION’ AFTER CUTTING COSTS: CEO

- *FORTESCUE COULD BRING IN INVESTOR TO SPEED DEBT PAYMENT: CEO

And Aussie miners are bouncing modestly (apart from South32)

* * *

China opened with more de-dollarization...

- *PBOC TO PROMOTE CURRENCY SWAP COOPRATION W/ KYRGYZSTAN C. BANK

- Central banks of two countries agree to promote cooperation in currency swap and local currency settlement, according to a statement posted on People’s Bank of China website.

And some good news on deleveraging…

- *SHANGHAI MARGIN DEBT BALANCE FALLS TO NINE-MONTH LOW

- Outstanding balance of Shanghai margin lending dropped for fifth day, falling 0.8%, or 4.7b yuan, to 573.4b yuan on Tuesday, lowest level since Dec. 4.

The PBOC fixed The Yuan stronger for the 3rd day in a row (under pressure from offshore Yuan) to its strongest in 3 weeks

- *CHINA SETS YUAN REFERENCE RATE AT 6.3613 AGAINST U.S. DOLLAR

But offshore Yuan remains notably stronger than onshore still…

Chinese stocks are modestly higher pre-market…

- *FTSE CHINA A50 OCTOBER FUTURES RISE 0.6% IN SINGAPORE

- *CHINA’S CSI 300 STOCK-INDEX FUTURES RISE 0.8% TO 3,103.4

And Interbank lending markets remain entirely suppressed...

Here’s why you may want to care about that…

Simply put – as the mainland squeeze bleeds out to Hong Kong, it creates a liquidity suck out from the rest of the world, reducing carry trade ‘power’ and thus derisking any and every leveraged portfolio’s exposure to US equities. When (or if) SHIBOR finally snaps then we will see the real impact (just as we saw shockwaves after CNY devalued unexpectedly).

* * *

Crude has faded as Asia opens after the bigger than expected API inventory build…

Charts: Bloomberg

end

China’s unrest? Are citizens starting to revolt?

(courtesy zero hedge)

The Start Of China’s Unrest? Southern China City Rocked By “Massive” Bomb Explosions, At Least 6 Dead

Over the weekend when we reported that one of China’s largest coal miners had laid off 100,000, or 40% of its workforce, we noted that China’s hard-landing is starting to hit where it really hurt: employment, or rather the lack thereof, and the one logical consequence: “now, many migrant workers struggle to find their footing in a downshifting economy. As factories run out of money and construction projects turn idle across China, there has been a rise in the last thing Beijing wants to see: unrest.“

Moments ago we may have witnessed the first direct, and deadly, manifestation of this unrest when as Xinhua reported, a series of “massive” explosions rocked the southern Chinese city of Liuzhou on Wednesday, killing at least three people and injuring more than a dozen, state media reported.

According to NBC, a local police chief told state news agency Xinhua that the 13 explosions hit locations including a hospital, a food market and a bus station, state news agency Xinhua reported.

State-run broadcaster CCTV cited a police chief saying the blasts were caused by “parcels containing explosives,” without providing further information.

In other words, for the first time in recent years, someone in China proactively sent out mailbombs to heavily populated areas including a hospital, a market, and a bus station.

CCTV said at least 6 people had been killed and at least 13 injured. NBC News could not immediately confirm that tally.

Images posted to Twitter by the Chinese media outlets appeared to show partially collapsed buildings, rubble in the streets, and at least one plume of smoke above the city.

According to Xinhua, the incident is being investigated as a criminal act. Which brings us back to our conclusion from Sunday:

if there is one thing China’s politburo simply can not afford right now, is to layer public unrest and civil violence on top of an economy which is already in “hard-landing” move. Forget black – this would be the bloody swan that nobody could “possibly have seen coming.

Three days later we may have the first manifestation of precisely this civil violence “bloody swan.” Will today’s deadly bombing be the end of it, or is it just starting?

Japanese Pension Funds Find New Ways To Lose Money, Will Blow Retirement Funds On Junk Bonds

Following yesterday’s collapse in the Nikkei, when a 4% drop pushed it red for the year below 17,000, down 20% from a high of 21,000 hit just over a month ago, we had just one question for Japan’s pension fund “fudiciaries” who have been “greatly rotating” out of bonds for the past few years as the primary sources for BOJ debt monetization, dumping trillions in fixed income yen, and promptly buying up equities: equities which have gone nowhere in 2015, and which have posted massive losses in the third quarter. The question was:

Less than 24 hours we got the answer, when moments ago Nikkei reported thatQ3 losses at (at least one) pension funds were just under JPY 10 trillion in the third quarter.

- JAPAN PENSION FUND JULY-SEPT. LOSS LIKELY 9.4T YEN: NIKKEI

With Japan’s economy already sliding into its 5th recession of the past decade, once pensioners open their retirement statements in a few weeks and find a 15% plunge in their purchasing power, Japan can skip recession and proceed straight to a consumer-driven recession.

But wait, there’s more: because if pensioners are angry now, wait until they learn that they have lost everything, after buying all those junk bonds that Carl Icahn is now actively selling with both hands and feet, because…

- JAPAN PENSION FUND TO INVEST IN JUNK BONDS, NIKKEI SAYS

And just like that, with or without Krugman’s active economic advice, Japan’s fate is sealed because much to Japan’s dismay, “junk” bonds are called that for a reason.

The good news for US shale companies: they just got a 6-9 month reprieve thanks to millions of Japanese pensioners who will starve to death in a few years. This is probably bad news for oil as the scramble to issue junk bonds in the coming weeks to take advantage of Japanese idiocy means taht the oil spigots will be turned on full blast.

ECB Will Boost QE By 120% To €2.4 Trillion, S&P Predicts

- Earlier this month, when we previewed the September ECB meeting and subsequent Draghi presser, we noted that the “the deflationary boogeyman still lurks” in Europe and as Richard Breslow wrote that morning, “the five year/five year inflation gauge that Draghi has said the ECB watches very carefully remains at very depressed levels [with] no sign from the swaps market that inflation is expected to hit target as far as the eye can see.”Breslow continued, “say what you will about the market being wrong, but the market has had a better track record on predictions than many central bankers.”

Well, sure enough, on Wednesday we learned that less than a week after the Krugman “success” story that is Japan stumbled back into deflation…

Well, sure enough, on Wednesday we learned that less than a week after the Krugman “success” story that is Japan stumbled back into deflation… …inflation has officially turned negative (again) in Europe where consensus hopes for an unchanged print were once again disappointed when the September CPI print came in negative on the back of a drop in commodity prices, confirming the latest inflationary impulse from the March launch of QE is officially over.

…inflation has officially turned negative (again) in Europe where consensus hopes for an unchanged print were once again disappointed when the September CPI print came in negative on the back of a drop in commodity prices, confirming the latest inflationary impulse from the March launch of QE is officially over.

The message being sent here is fairly straightforward, but for what it’s worth, here’s a bit of color from Bloomberg:

The message being sent here is fairly straightforward, but for what it’s worth, here’s a bit of color from Bloomberg:

The euro area’s inflation rate unexpectedly turned negative in September for the first time in six months, adding pressure on the European Central Bank to bolster stimulus.

Consumer prices in the 19-nation currency bloc fell 0.1 percent from a year earlier, according to a preliminary report published by the European Union’s statistics office in Luxembourg on Wednesday. Economists predicted an inflation rate of zero, according to the median estimate of 38 analysts in a Bloomberg survey. Unemployment in the region remained unchanged in August at 11 percent, Eurostat said in a separate release.

Data “was broadly driven by the energy component,” said Giada Giani, an economist at Citigroup Inc. in London. “There are very little inflationary pressures even aside from the oil-price shock. It should be bottom for the year.”

Brent oil has plunged by a quarter since the end of June amid speculation a global glut will be prolonged. Oil is poised for its lowest quarterly average price since the start of 2009.

Energy prices fell 8.9 percent in September from the previous year, Eurostat said. Core inflation, which strips out volatile elements such as food and energy, remained unchanged at 0.9 percent.

The setback comes as the euro area’s recovery shows signs of strengthening. Economic confidence unexpectedly increased in September to the highest in more than four years as sentiment in the industrial and services sectors improved. A gauge of economic activity points to a 0.4 percent rate of expansion in the third quarter amid rising orders and backlogs of work.

Even so, unemployment is only falling slowly from the 12.1 percent peak reached in 2013. The region’s jobless rate fell less than initially reported in July and remained unchanged in August, according to Eurostat’s report.

Wages will only increase at a moderate pace amid weak growth and a gradual decline in unemployment, said Michael Schubert, an economist at Commerzbank AG in Frankfurt. That argues against noticeably stronger underlying price pressure.

In other words, the promise of €1.1 trillion in asset purchases (i.e. money printing) has not only failed to engineer a robust recovery complete with the promised dramatic declines in unemployment and/or dramatic increases in wages, it hasn’t even managed to keep Europe out of deflation. The most hilariously absurd thing about it all is that it is indeed unconventional monetary policy that has helped to keep otherwise bankrupt US drillers in business thus perpetuating the very same low crude prices that everyone now blames for the disinflationary impulse.

Of course these are post-crisis central bankers we’re talking about here, which menas that when a lot of Keynesian cowbell doesn’t work, the only cure for the deflationary fever must be more Keynesian cowbell which explains why Japan is about to double down on Abenomics (from JPM: economist Masaaki Kanno says in report that Bank of Japan will announce additional easing on Oct. 30), and why the ECB will almost invariably expand PSPP. Indeed, S&P is now out calling for ECB Q€ to last for nearly two years longer than originally planned and for the size of the program to be expanded to a Dr. Evil-ish €2,400,000,000,000. Here are the main points via Bloomberg:

- CB will extend its QE program beyond Sept. 2016, most likely until mid-2018, and it could reach EUR2.4t, S&P says in report.

- Expected amount is more than twice the original EUR1.1t commitment

- As EM currencies have declined, the euro has begun to appreciate again, complicating the ECB’s QE program

Note the last bullet there. This has become a self-perpetuating nightmare. Global QE is forestalling the creative destruction that in normal times serves to purge speculative exccess and correct capital misallocation, contributing the very same global deflationary supply glut that’s tanking commodity currencies. The resultant pressure on EM FX then leads to relative strength for DM crosses jeopardizing inflation targets and leading to still more advanced economy QE. Of course when one DM central bank eases, the immediate effect is to trigger easing by a neighbor. The best example of this is probably the ECB-SNB-Riksbank connection and it means that this a never-ending Keynesian insanity loop, and in case the self-feeding dynamic wasn’t strong enough as it is, when the EM meltdown finally filters back into DM markets, the attendant turmoil will also be used to justify more easing.

Summing it all up in one horrifying image…

- Summing it all up in one horrifying image…

- end

-

-

-

(courtesy zero hedge)

-

-

Global ‘Wealth’ Destruction – World Market Cap Plunges $13 Trillion To 2 Year Lows

Since the start of June, global equity markets have lost over $13 trillion.

(The last time global market dropped this much – Bernanke unleashed QE2)

World market capitalization has fallen back below $60 trillion for the first time since February 2014 as it appears the world’s central planners’ print-or-die policy to create wealth (and in some magical thinking – economic growth) has failed – and failed dramatically.

To rub more salt in the wounds of monetray policy mumbo-jumbo, despite endless rate cuts and balance sheet expansion around the world, the last 4 months have seen an 18% collapse – the largest since Lehman.

It appears “Wealth” creation is just as transitory as The Fed thinks every other outlier is.

Charts: Bloomberg

end

Oh dear!!

Trafigura’s founder Claude Dauphin has died of cancer.

Its bonds have plummeted more:

(courtesy zero hedge)

Commodity Giant Trafigura Founder, Top Shareholder Claude Dauphin Has Died

In a tragic, if very odd coincidence, a day after we postulated that the real “commodity-trader” risk may not be Glencore after all, but its just as vast, if even more levered competitor, Trafigura, moments ago the privately-held company (with publicly traded bonds), announced that its founder and biggest shareholder, french billionaire Claude Dauphin has died at the age of 64.

From the press release:

It is with great sadness and regret we have to announce that Trafigura’s Founder and Executive Chairman, Claude Dauphin, passed away peacefully in the early hours of this morning in a hospital in Bogota, Colombia after a hard-fought battle with cancer.

Claude Dauphin (64) has been a leading figure in the global commodities trading industry for more than three decades. He founded Trafigura together with five partners in 1993, and as Chairman and CEO built the company into its current position as one of the world’s leading traders of oil, metals and minerals.

“Claude will be greatly missed by his family, friends, and vast network of business partners, as well as by us all,” said Jeremy Weir, CEO Trafigura. “We owe him an enormous debt of gratitude for a career full of achievement and entrepreneurial endeavour and for his energy, inspirational leadership, generosity of spirit, humility and humour.”

Our deepest condolences go to his wife and children.

Dauphin’s bio from Wikipedia:

Dauphin worked for nearly 22 years as an oil executive at Victoria Trading Services (UK) Ltd. In 1990, at the age of 39, he assumed his first directorship. The following year he became a director at A.O.I. (UK) Ltd. He moved to Marc Rich & Co. (now Glencore) from 1991 to 1992. In 1993 Dauphin and several other senior traders at Marc Rich founded Trafigura.

Trafigura is known for its role in the 2006 Ivory Coast toxic waste dump environmental disaster. Dauphin and four others were imprisoned in Ivory Coast for five months on charges of dumping toxic waste; afterward they were released and all charges were dropped. While Trafigura denied responsibility and culpability, it paid €1.3 million in an out-of-court settlement.

Dauphin communicates with lenders and bondholders in the company’s annual report, but does not speak publically. He is married and has three children.

And some more on the highly secretive Dauphin from the Telegraph:

Little is known about Mr Dauphin, except that he was previously a senior trader for secretive commodities firm Marc Rich & Co, which later became Switzerland-based Glencore.

However, Mr Dauphin hit the headlines in 2006 when he was arrested with four colleagues and spent five months in jail in Ivory Coast on charges related to the toxic waste. He was later released and the authorities dropped all allegations of wrongdoing. In a statement, Mr Dauphin described it as “a terrible ordeal… [to spend] five months in jail as innocent men”.

The oil trader settled out of court over the toxic waste last September by giving 31,000 Ivory Coast residents £30m, without admitting any liability for the “slops” that ended up in their country in 2006.

Our condolences go to his friends and family, even as our eyes are following the impact of this news on Trafigura’s bonds.

Russia + Middle eastern affairs:

Russia strikes ISIS inside Syria:

(courtesy zero hedge)

Moscow Approves Military Action In Syria, Video Captures First Russian Air Strikes

A week ago in “Endgame: Putin Plans To Strike ISIS With Or Without US,” we reported that Russia was set to launch unilateral airstrikes against ISIS targets in Syria even if it does not receive the support of the US-led “coalition.” These will of course be real airstrikes, designed to hit real targets, and kill real extremists because after all, preserving the Assad regime means Moscow has an incentive to wipe out terror in Syria. On the other hand, the US and its regional allies have an incentive to merely contain terror in Syria – if terrorist elements work to destabilize a regime that’s unfriendly towards the West then they serve a purpose even if that purpose is transient and limited, making it necessary to conduct bombing sorties not to “degrade and defeat”, but merely to make sure Frankenstein doesn’t escape the lab, so to speak.

On the heels of Vladimir Putin’s speech at the UN and amusing interviews with Western media (in which he made his intentions in Syria clear beyond a shadow of a doubt, making it virtually impossible for Washington to keep up the “we don’t know what the Russians are doing at Latakia” narrative), Russian lawmakers have now officially approved the use of force abroad, setting the stage for airstrikes on Islamic State (and any other anti-regime “terrorists”). Here’s WSJ with more:

Russian lawmakers Wednesday approved the use of military force abroad following a request by President Vladimir Putin, paving the way for possible airstrikes in Syria.

The authorization—passed unanimously by Russia’s Federation Council— comes after a request for military assistance by Syrian President Bashar al-Assad, according to a top aide to Mr. Putin.

It comes as Russia has built up forces on the ground in Syria, including deploying combat aircraft, moves that have placed Moscow at odds with Washington. Sergei Ivanov, the Kremlin chief of staff, said Russia’s military involvement would be limited to an air campaign targeting Islamic State, or ISIL.

“As our president already said, the use of military forces in ground combat has been ruled out,” Mr. Ivanov said. “The military goal of these operations is exclusively limited to air support for the Syrian government forces in their campaign against ISIL.”

Through it all, both sides will desperately cling to their stories even as the words and actions of their respective leaders tell a completely different story. For instance, here’s WSJ parroting the “we’re just shocked at Russia’s actions” theme:

The authorization for the use of force represents something of an about-face for the Kremlin.

And here’s Russia denying the fact that this is a very clear attempt to exploit ISIS and the regional ambitions of Moscow’s allies in Tehran on the way to securing a more prominent geopolitical role for The Kremlin in the Mid-East:

Mr. Ivanov said that thousands of Russian citizens and others from the former Soviet Union are fighting on the side of Islamic State, and that many have returned home, presenting a direct threat.

“The point here is not in achieving any foreign policy goals or satisfying ambitions,” Mr. Ivanov said.

Of course Ivanov immediately qualified that assessment by saying that “we’re talking exclusively about Russia’s national interests.”

Now obviously, that kind of doublespeak makes it possible to completely reinterpret the first statement. That is, if one equates Russia’s “foreign policy goals” and regional “ambitions” with the country’s “national interests” (and really, you couldn’t possibly separate those things) then the first statement doesn’t mean what Ivanov wants you to believe it means.

Meanwhile, foreign minister Sergei Lavrov met with his permanent Security Council member counterparts on Tuesday to discuss Syria. Here’s the official line from the Russian Foreign Ministry:

On September 29, Foreign Minister Sergey Lavrov attended a traditional lunch for the foreign ministers of the five permanent UN Security Council members with UN Secretary-General Ban Ki-moon held in New York.

The lunch participants focused on Syria in light of the increasing terrorist threat coming from the so-called Islamic State (ISIS). The Russian minster pointed to the need to create a broad counterterrorism front based on a solid foundation of international law and uniting all countries that provide a practical contribution to this struggle, including Syria’s armed forces.

They also discussed the settlement process in Yemen, where the military-political and humanitarian situation has seriously deteriorated in the past few months, as well as the possibilities of a peaceful solution to the conflict in South Sudan.

We’d be curious to know what the Chinese side had to say at the luncheon.

In any event, it’s now official. Russia has cleared up any legal ambiguity around airstrikes in Syria and one can expect to see planes in the sky (they’re already on the ground) in Syria in short order and if the following is any indication, they may have already started:

Somehow we suspect Russia’s brand of anti-militant airstrikes will be far more effective than the Western brand has been over the course of the past year. Additionally, it’s worth noting that at this juncture, the rumor mill will move from focusing on whether the planes overhead are Russian to whether the troops on the ground are Russian and while we can’t know for sure, we certainly imagine that if any Russian pilots wind up being burned alive in a slickly-produced propaganda video, Putin’s official line on combat troops might change rather quickly.

end

I was waiting for this: the propaganda begins:

Propaganda War Begins: Russia’s Syria Strikes Targeted US-Backed “Moderate” Rebels, West Says

With the US having officially lost control of the narrative in Syria now that The Kremlin has called Washington’s bluff on the battle to eradicate ISIS and eliminate the Sunni extremist elements that threaten to wrest control of Syria from President Bashar al-Assad, the only remaining question after Russian lawmakers officially cleared the way for airstrikes was how long it would be before the Western media began shouting about Russian warplanes bombing targets that aren’t affiliated with ISIS.

As we reported earlier today, Moscow wasted no time in launching its first round of air raids.

In turn, the West wasted no time in contending that Russia is targeting areas that aren’t known to be strategically significant for ISIS. Here’s a look at two headlines which do a nice job of summarizing all of the rhetoric which you’re about to hear emanating ceaselessly from every corner of the Western world in the coming days and weeks:

- U.S. IS CONCERNED RUSSIA’S INTENT IS PROTECTING ASSAD: KERRY

- U.S. HAS ‘GRAVE CONCERNS’ IF RUSSIA STRIKES OUTSIDE ISIL AREAS

And here’s WSJ with a sneak peek at the new narrative which Washington will be working hard to refine:

Russian President Vladimir Putin inserted his country directly into Syria’s war Wednesday, as Russian forces launched their first airstrikes against what Moscow said were Islamic State targets in the Middle Eastern nation.

But Western leaders raised doubts about whether Russia really intended to take the fight to Islamic State, or merely broaden the Syrian regime’s offensive against a wide range of other opponents.

For the U.S., the Russian strikes add new questions about the role of Russian forces in Syria. “While we would welcome a constructive role by Russia in this effort, today’s [meeting in Baghdad] hardly seems indicative of that sort of role and will in no way alter our operations,” a U.S. official said.

Warplanes targeted Islamic State military hardware and weapons stores, a spokesman for Russia’s Ministry of Defense told official news agencies hours after Russian lawmakers approved a request by Mr. Putin to allow the use of force abroad.

Framing the attacks as part of a fight against terrorism, Mr. Putin said that Russia will support the Syrian army from the air, without any ground operations, for the duration of the Syrian offensive.

“The only real way to fight international terrorism…is to act pre-emptively. and not wait till they [terrorists] come to our home,” Mr. Putin said in televised comments. He called for antiterror cooperation with other states through the Russian coordination center in Baghdad.

The official Syrian Arab News Agency reported Wednesday that Russian airstrikes hit areas under Islamic State control in Homs and Hama provinces, including the cities of Al Rastan and Talbiseh, near the town of Salamiyah, and the villages of al-Za’faran, al-Humr Hills, Eidoun, Salamiyah and Deir Fol. The strikes had successfully targeted Islamic State, SANA said, without elaborating.

But with the exception of the area east of the town of Salamiyah in Hama province, none of the areas listed by the Syrian regime have a known presence of Islamic State fighters. They are largely dominated by relatively moderate rebel factions and Islamist groups like Ahrar al-Sham and the al Qaeda affiliate the Nusra Front.

Yes, “relatively moderate rebel factions like al-Qaeda” (check the above, WSJ actually said that) which in July kidnapped the commander and deputy commander of the Pentagon’s ragtag group of US-trained rebels that was supposed to number in the thousands by now but has been reduced to just “four or five” men and which was humiliated last Friday when the remaining fighters were forced to surrender their pickup trucks and ammo to al-Nusra in order to “secure safe passage” to who knows where.

Considering that, and considering the “solid” relationship the US has always maintained with al-Qaeda, it sure would be a shame if a few al-Nusra operatives wound up as collateral damage in Russia’s air campaign.

Then there’s The Telegraph with an epic attempt to spin the news with a single headline: “Putin defies West as Russia bomb ‘Syrian rebel targets instead of Isil‘”.

Meanwhile, France – who recently went full-propaganda by using “self defense” to justify its newly launched Syrian bombing campaign – is out expressing its consternation about which groups Russia is bombing. Via Reuters:

France said it was “curious” that Russian air strikes in Syria on Wednesday had not targeted Islamic State militants and a diplomatic source added that Moscow’s action appeared aimed at supporting President Bashar al-Assad against other opposition groups in the country’s civil war.

The diplomatic source said it was in line with Russia’s stance since 2012 that until there was a viable alternative to Assad, Moscow would not drop its support for him in the war that began in 2011 after a government crackdown on anti-Assad protests.

“Russian forces struck Syria and curiously didn’t hit Islamic State,” Defence Minister Jean-Yves Le Drian told lawmakers.