Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1146.80 up $8.70 (comex closing time)

Silver $15.98 up 28 cents.

In the access market 5:15 pm

Gold $1147.10

Silver: $15.90

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very poor delivery day, registering 0 notices for nil ounces Silver saw 0 notices for 10,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 212.80 tonnes for a loss of 90 tonnes over that period.

In silver, the open interest fell by a considerable 2654 contracts despite the fact that silver was up 44 cents on yesterday. We thus must have had considerable short covering by the bankers. The total silver OI now rests at 155,397 contracts In ounces, the OI is still represented by .777 billion oz or 111% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose to 421,702 for a gain of 196 contracts. We had 0 notices filed for nil oz today.

We had no change in tonnage at the GLD thus the inventory rests tonight at 688.98 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had no change in silver inventory at the SLV / Inventory rests at 318.395 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by a considerable 2654 contracts down to 155,397 despite the fact that silver was dramatically up in price to the tune of 44 cents with respect to yesterday’s trading. The total OI for gold rose by 196 contracts to 421,702 contracts, as gold was up $1.00 yesterday. Looks like the bankers were loathe to supply the paper in silver and they must be quite concerned as they engaged in massive shortcovering.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

Asian affairs:

3. Yuan trading surpasses the Yen as this raises the possibility of inclusion in SDR’s

(zero hedge)

European affairs:

3a) Poor PMI numbers throughout Europe. German factory orders plummet due to poor orders from China/looks like Europe has entered a recession

3b) Glencore plummets again by 7.7% as copper falls. This raises the risk of default due to Glencore’s trading in derivatives and also the credit default swap on itself

(zero hedge)

3c) Glencore explains to the world what happens if their credit rating falls to junk. In a nutshell, revisit AIG 2008:

(zero hedge/Glencore)

3d) A huge commentary from Dave Kranzler of IRD on the huge increase in reverse repos by the Fed throughout September and into October. Generally these repos keep the Fed funds rate to the liking of the FOMC. However the rate has been zero for many years. The main reason for the increase in reverse repos is that it provides collateral and no doubt derivatives blew up and thus collateral was needed to plug massive holes in balance sheets of banks.

(Dave Kranzler/IRD)

Russia + USA affairs/Middle eastern affairs

4. a) After controlling the skies, and after Russia threatens with a naval blockage, the USA rhetoric against Russia increases raising the tensions/

(zero hedge)

4b) Saudi clerics now pound the table for jihad/the rhetoric gets louder and louder

(zero hedge)

Global affairs:

5a) The world’s largest sovereign wealth fund must start to liquidate its fund in order for the sovereign to pay her bills

(zero hedge)

5b) Wolf Richter explains why the entire globe has entered a recession in unison

(Wolf Richter/www.testosteronepit.com)

5c) The IMF lowers growth prospects for the globe: the main culprits are Japan and emerging markets. Strangely they state that China is constant and the USA is raised a bit

(IMF/zero hedge)

EMERGING MARKETS

6a) none

Oil related stories

7a) oil spikes on the raising of global tensions

(zeor hedge)

8 USA stories/Trading of equities NY

a) Trading today on the NY bourses 2 commentaries

(zero hedge)

b) August Trade deficit soars 16% as exports plummet and imports rise. This will put a damper on 3rd quarter GDP

(zero hedge)

c) Permabull Lavorgna throws in the towel on USA growth as he states that the economy is stagnant. (zero hedge/Lavorgna)

d Profit margins are plummeting. The last 5 out of 6 times this has happened the USA entered a deep recession (zero hedge)

e) Biotechs massacred today and turn red for 2015:

(zero hedge)

f) Ron Paul thinks that the unemployment rate in the USA is 20%

(Profit Confidential/Ron Paul/Baillieul)

9. Physical stories

- London’s Financial Times columnist admits central bank rigging of markets. (Chris Powell/GATA)

- James Turk at Kingworldnews claims that gold’s advance may be due to the conflict with Russia (Kingworldnews/James Turk)

- Peter Cooper’s Arabian money shutting down due to lack of sponsors.

- Premiums on silver coins now in priced at spot + 50% or spot + 40% depending on quantity (Nick Laird/zero hedge)

Let us head over to the comex:

October contract month:

Initial standings

Oct 6.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 4,441.710 oz

Delaware, Scotia,Brinks

|

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil

|

| No of oz served (contracts) today | 0 contracts

nil oz |

| No of oz to be served (notices) | 1477 contracts

147,700 oz |

| Total monthly oz gold served (contracts) so far this month | 126 contracts

(12,600 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 10,939.2 oz |

Total customer deposit: nil oz

***extremely unusual to have no activity of gold continually especially with 4.99 tonnes of gold standing for delivery.

October silver Initial standings

Oct 6/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,122,420.340 oz

Brinks,CNT, HSBC |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 689,385.810 oz

Scotia |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 36 contracts (180,000 oz) |

| Total monthly oz silver served (contracts) | 29 contracts (145,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,485,336.6 oz |

Today, we had 0 deposit into the dealer account:

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: 689,385.810 oz

total withdrawals from customer: 1,122,420.34 oz

And now SLV:

Oct 6/no change in silver inventory/inventory rests at 318.395 million oz

oCT 5/we had a small withdrawal of inventory at the SLV of 134,000 oz/and this is also to pay for fees/inventory rests at 318.395 million oz

Oct 2.2015: no change in silver inventory at the SLV/inventory rests at 318.529 million oz

Oct 1.2015:another addition of 1,145,000 oz of silver inventory added to the SLV inventory./inventory rests at 318.529 million oz

Sept 30/no change in silver inventory at the SLV/Inventory rests at 317.384 million oz

sept 29.2015: we had another withdrawal of 859,000 oz from the SLV/Inventory rests at 317.384 million oz

sept 28./no change in silver inventory/rests tonight at 318.243 million oz/

Sept 25./we had another 954,000 oz of silver withdrawn from the SLV/Inventory rests this weekend at 318.243 million oz

Sept 24.2015: no change in silver inventory tonight/inventory rests at 319.197 million oz

Sept 23.2015: we had a huge withdrawal of 1.718 million oz at the SLV/Inventory rests at 319.197 million oz

Sept 22/no change in inventory at the SLV/Inventory rests at 320.915 million oz

sept 21.2015: no changes in inventory at the SLV/Inventory rests at 320.915 million oz

Sept 18.2015; no changes in inventory at the SLV/inventory rests at 320.915 million oz

sept 17.2017:no change in inventory at the SLV/rest tonight at 320.915

million oz/

sept 16.2015: no change in inventory at the SLV/rests tonight at 320.915 million oz/

Sept 15./no change in inventory at the SLV/rests tonight at 320.915 million oz

Press Release OCT 6.2015

Sprott Increases Offer for Central GoldTrust and Silver Bullion Trust

Offering an Additional Premium of US$0.10 per GTU Unit payable in Sprott Physical Gold Trust Units

and US$0.025 per SBT Unit payable in Sprott Physical Silver Trust Units

When Announced on April 23, 2015, Offers Represented a Premium of US$3.06 per GTU Unit and US$0.91 per SBT Unit for Unitholders Based on Trading Value and the NAV to NAV Exchange Ratio

Premiums as of October 5, 2015 (including the Increased Consideration) are US$1.14 per GTU Unit and US$0.61 per SBT Unit

Notice of Extension and Variation to be Filed Shortly

Offers Will Now Expire on October 30, 2015 –Unitholders Urged to Tender Now

TORONTO, Oct. 6, 2015 (GLOBE NEWSWIRE) — Sprott Asset Management LP (“Sprott” or “Sprott Asset Management”), together with Sprott Physical Gold Trust (NYSE:PHYS) (TSX:PHY.U) and Sprott Physical Silver Trust (NYSE:PSLV) (TSX:PHS.U) (together the “Sprott Physical Trusts”), today announced that it has increased the consideration payable to unitholders in connection with its offers to acquire all of the outstanding units of Central GoldTrust (“GTU”) (TSX:GTU.UN) (TSX:GTU.U) (NYSEMKT:GTU) and Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (TSX:SBT.U) (the “Sprott offers”).

Unitholders will now receive an additional premium of US$0.10 per GTU unit payable in Sprott Physical Gold Trust units and US$0.025 per SBT unit payable in Sprott Physical Silver Trust units (the “Premium Consideration”), in addition to the units of Sprott Physical Gold Trust and units of Sprott Physical Silver Trust, respectively, being offered on a net asset value (NAV) to NAV exchange basis. Based on trading values and the NAV to NAV Exchange Ratio (as such term is defined in the Sprott offers) at the time Sprott announced its intention to make the Sprott offers on April 23, 2015, the offers reflected a premium of US$3.06 per GTU unit and US$0.91 per SBT unit. The premium as of October 5, 2015, based on trading values, the NAV to NAV Exchange Ratio and the Premium Consideration, represents US$1.14 per GTU unit and US$0.61 per SBT unit, respectively. In connection with this increase in consideration, the expiry time for each Sprott offer is extended to 5:00 p.m. (Toronto time) on October 30, 2015.

“Central GoldTrust and Silver Bullion Trust unitholders have been burdened for too long by a group of trustees committed to protecting the interests of the Spicer family. It is only through the public spotlight that the variety of undisclosed fees paid to supposedly independent trustees has forced public disclosures and hollow justifications. Sprott’s offers to unitholders are compelling and momentum is building as we continue to show the clear advantages of the offers. The response of the GTU and SBT trustees has been to penalize unitholders with the burden of paying for costly lawsuits and expensive advisors to protect the Spicer family and the fees they receive. We are accordingly increasing our offer to compensate unitholders for this abuse of trust, and encourage them to take advantage of this opportunity to exchange their units for an immediate premium, and trade a management committed to entrenchment to one committed to their best interests,” said John Wilson, Chief Executive Officer of Sprott Asset Management.

Added Wilson, “We have provided extensions to the offers so that no unitholders are left without this opportunity to exit an underperforming investment and enter into a high quality security that functions as intended, reflecting the value of the bullion held in the trust. Sprott appreciates the support of GTU and SBT unitholders to date and currently anticipates these extensions will be the final extensions to the Sprott offers.”

As of 5:00 p.m. (Toronto time) on October 5, 2015, there were 8,194,265 GTU units (42.46% of all outstanding GTU units) and 2,055,574 SBT units (37.60% of all outstanding SBT units) tendered into the respective Sprott offers. Total units tendered as of October 5, 2015, do not include pending units which are typically received on the date of expiration.

GTU and SBT unitholders who have questions regarding the Sprott offers, are encouraged to contact Sprott Unitholders’ Service Agent, Kingsdale Shareholder Services, at 1-888-518-6805 (toll free in North America) or at 1-416-867-2272 (outside of North America) or by e-mail at contactus@kingsdaleshareholder.com.

Gold to “double in price and surpass its inflation-adjusted high of $2,500 per ounce in the next 3 to 5 years”

The bullish outlook for gold prices was covered by Dow Jones Marketwatch yesterday.

“Gold prices may be ready to make a significant move higher as holdings of the precious metal in the SPDR Gold Trust exchange-traded fund climb to their highest level in more than two months.”

GoldCore believes that gold may have “bottomed in the summer,” and could climb to as high as $1,300 an ounce by the end of this year. Longer term, O’Byrne expects gold to “double in price and surpass its inflation-adjusted high of $2,500 per ounce in the next 3 to 5 years.”

The metal “remains undervalued when compared to assets such as stocks, bonds and property—all of which have surged in recent years,” he said.

The full article from Marketwatch can be read here – Gold may be on verge of ‘breakout’ higher as ETF holdings rise.

DAILY PRICES

Today’s Gold Prices: USD 1136.90, EUR 1014.55 and GBP 749.19 per ounce.

Yesterday’s Gold Prices: USD 1114.20, EUR 998.66 and GBP 735.69 per ounce.

(LBMA AM)

Silver in USD – 1 Month

Gold finished marginally higher yesterday, extending gains to a second straight session and consolidating on Friday’s price gains. Gold bullion is trading near $1,140 in London today after climbing to a one-week high of $1,141.80 yesterday.

Silver was a further 2.9% higher yesterday to $15.71 an ounce building on the 5.2% surge on the Friday. It is 0.15% higher to $15.80 today.

Platinum and palladium are also higher – up 0.8% and 0.3% respectively.

Download 7 Key Allocated Storage Must Haves

Silver Coin Premiums Soar Above 50%

Courtesy of Sharelynx’ Nick Laird who tracks precious metal premium by vendor, we continue our recent series showing the discrepancy between paper and physical metals, in this case silver. As Nick notes, APMEX price premiums are a lot higher than the Monex. And as can be seen in the charts below, premiums rose above 50% for 1-19 coins & above 40% for 500 plus coins.

For now, gold is stable.

end

FT columnist acknowledges ‘systematic market rigging’ by central banks

Submitted by cpowell on Mon, 2015-10-05 17:23. Section: Daily Dispatches

1:29p ET Monday, October 5, 2015

Dear Friend of GATA and Gold:

GoldCore’s Mark O’Byrne today —

http://www.goldcore.com/uk/gold-blog/bis-warns-of-major-faultlines-in-gl…

— calls attention to commentary published last month in the Financial Times about the latest quarterly report from the Bank for International Settlements, in which the BIS noted that financial markets lately have been responding mainly to interest-rate pronouncements by central banks.

The FT commentary, written by the newspaper’s veteran columnist, John Plender, published September 15 and headlined “BIS Breathes New Life into Calls for Rate Rises” —

http://www.ft.com/intl/cms/s/0/50a620ac-5b04-11e5-a28b-50226830d644.html

— said the BIS report “will also have struck a chord with those investors who are weary of trying to make sense of a world where markets have been systematically rigged by central bankers.”

Despite his subscription to the FT, your secretary/treasurer missed Plender’s commentary.

That “markets have been systematically rigged by central bankers” is a story that has yet to be pursued by the Financial Times and other mainstream financial news organizations, despite GATA’s peppering them for many years with documentation of that rigging, particularly in regard to gold but also in regard to other markets, documentation summarized here:

http://www.gata.org/node/14839

GoldCore’s O’Byrne notes that market rigging by central banks is “a charge for which we and others have been ridiculed for making in the past.”

So is Plender angling for a tinfoil hat? Would the FT permit him to wear it? Would the FT ever dare to commit actual journalism about surreptitious central bank intervention in the markets, including the gold market?

You can help try to get answers to these questions. Please e-mail Plender atjohn.plender@ft.com, congratulate him on his insight, and encourage him to urge the FT to put someone on the market-rigging beat. The newspaper already has plenty of material. It lacks only the courage and integrity to publish it.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

James Turk believes that international tensions maybe the key in the supporting of gold:

(courtesy James Turk/Kingworldnews)

International tensions may be supporting gold, Turk tells KWN

Submitted by cpowell on Mon, 2015-10-05 22:04. Section: Daily Dispatches

6:04p ET Monday, October 5, 2015

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk today tells King World News that international tensions may actually be goosing monetary metals prices. The world seldom sees that. Turk adds that silver is leading gold lately, something that happens in “the best” bull markets for the metals. The interview is excerpted at the KWN blog here:

http://kingworldnews.com/escalating-syrian-war-has-sent-gold-prices-high…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

So sad to see him go. Guys and gals, it is important to contribute to all who write on the crime committed with respect to gold and silver

(courtesy Peter cooper/Arabian money)

Why the ArabianMoney financial comment website is closing down at the end of this month

Posted on 06 October 2015

![]()

As ArabianMoney.Net editor and publisher Peter Cooper announced to his friends on social media before the weekend a decision has been taken to close this website at the end of the month. This follows the closure of its companion investment newsletter last December due to lack of subscribers.

To some extent ArabianMoney is a microcosm of the problems facing the entire business publishing industry at the moment. Over the past five years the Internet has become the dominant medium for delivering this media, and it has come at a high price in terms of lost advertising income. Blame Google and the commoditization of advertising on the Internet.

Cut-throat pricing

Media agencies increasingly buy bundles of advertising banners by the million from Google, and therefore a specialist website like ArabianMoney gets paid the same amount per banner as a tabloid news website. If say banks and brokers want an appropriate medium for their advertising to appear on then they need to pay more for it, but they are unwilling to do this and take the ‘bargain’ deal.

What websites like ArabianMoney and other business websites need are sponsors, like the ones who still support conferences specific to their industry. The MENA Mining Show we covered this morning, for example, was sponsored by government and companies from its own sector.

It is a total myth that websites are cheap to run and produce. The technology behind the site has to be updated, maintained and organized by a professional webmaster, or the whole show can come crashing down. There have to be journalists and experts to write the specialist content, search engine optimization guys and in the distant past well-paid sales executives to gather in the adverts.

Absent very much income websites have to be increasingly innovative in sourcing content which is frequently borrowed from third parties, with or without their consent. That’s a bit of a downward spiral as the lower the quality of content and the more repetitive, the smaller the audience becomes.

Disruptive technology

The bigger picture is one of a disruptive technology. Similar things have happened many times in agriculture and industry in the past, and almost always the outcome is good in terms of higher productivity. However, whether this is going to be true in the case of news and business information is less certain.

For what kind of business and financial media will Dubai or the UAE have if it can’t even support a basic financial comment website like ArabianMoney? The Financial Times is already down to one correspondent here rather than two. Bloomberg and Reuters have a virtual duopoly seeing as most of the other ‘local’ media just re-use their stuff. Business desks have had their staffing cut to the bone and the quality has suffered.

What Dubai surely needs is an independent financial journal of record in the same way that London has its FT and New York its Wall Street Journal. ArabianMoney never really came close to making the grade as commercial support failed to materialize long before we could expand as intended, and advertising banners produced such a pitifully low income that in the end it could not even cover the rising costs of its webmaster.

Is there a market?

That leaves a gap in the market. But as somebody once wrote of The Independent newspaper when it launched, is there really a market in this gap?

For the UAE such a media would be a valuable step in making Dubai a global financial hub, and a cheap way to do so. It would give the city’s financiers bankable credibility and enhance their reputation, though not if it was owned and run by the government. Independence is the bedrock of any financial media, and absent that it becomes no more than another organ of the government with a clear and understandable duty to follow its command.

This is not an easy mandate. But there is a lot for many parties to gain from it. Is anybody up to the challenge? Who will take the lead?

-END-

1 Chinese yuan vs USA dollar/yuan rises a bit in value, this time at 6.3559/Shanghai bourse: closed for holiday, hang sang: red

2 Nikkei closed up 180.61 or 1.00%

3. Europe stocks mostly in the green /USA dollar index down to 95.90/Euro up to 1.1216

3b Japan 10 year bond yield: rises slightly to .322% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.33

3c Nikkei now just above 18,000

3d USA/Yen rate now above the important 120 barrier this morning

3e WTI: 46.07 and Brent: 49.35

3f Gold up /Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .554 per cent. German bunds in negative yields from 5 years out

Greece sees its 2 year rate falls to 9.80%/Greek stocks this morning down by 0.46%: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 7.94%

3k Gold at $1139.05 /silver $15.69 (8 am est)

3l USA vs Russian rouble; (Russian rouble up 48/100 in roubles/dollar) 65.02,

3m oil into the 46 dollar handle for WTI and 49 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9745 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0929 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 5 year German bund now in negative territory with the 10 year moving further from negativity to +.554%/German 5 year rate negative%!!!

3s The ELA lowers to 89.1 billion euros, a reduction of .6 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.04% early this morning. Thirty year rate below 3% at 2.88% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Fail To Surge Despite Continuing Onslaught Of Poor Economic Data

The best headline to summarize what happened in the early part of the overnight session was the following from Bloomberg: “Asian stocks extend global rally on stimulus bets.” And following the abysmal data releases from the past three days confirming that the latest centrally-planned attempt to kickstart the global economy has failed, overnight we got even more bad data, first in the form of Australia’s trade deficit, which at A$3.1 billion, came in well wider than the S$2.8 billion expected, and up from the revised A$2.8 billion in July, the largest deficit since June as experts remained flat while imports rose by 1%.

Then moving from Asia to Europe, we got more validation for the “stimulus bets” when Germany’s factory orders which once again confirmed the recent PMI weakness, and bombed at an abysmal -1.8%, far below the 0.5% expected, while the Y/Y print was a feeble 1.9% on expectations of a 5.6% increase, with the last month revised to -1.3%, driven by a collapse in orders from outside the Euro area (coughchinacough).

This is what Goldman had to say on the terrible data: German manufacturing orders fell by 1.8%mom in August. Domestic orders decreased 2.6%mom and foreign orders 1.2%mom. Orders from the Euro area were up 2.5% on the previous month, while orders from outside the Euro area decreased 3.7%mom. Within the breakdown for type of goods, manufacturers of intermediate goods recorded decreases in new orders of 0.4% and the manufacturers of capital goods of 2.8% on the previous month. New orders of consumer goods fell by 1.5%.”

Goldman’s punchline: “the weakness in orders from outside the Euro area seems to reflect genuine weakness in China and emerging markets in general and this will weigh on the German manufacturing sector.“

The recent Volkswagen scandal will hardly boost Germany’s suddenly struggling manufacturing powerhouse.

So after all this bad data, the “bad news is good news” rally should have really gone into overdrive, right? It did in Asia: Asian equity markets traded with firm gains for a consecutive day on the back of expectations for a fed lift-off being pushed back. Nikkei 225 (+0.8%) outperformed in the region led by broad based gains as the TPP deal was clinched, while the ASX 200 (+0.3%) was led higher by gains in commodities. Hang Seng (-0.1%) pared earlier advances as Nikkei Hong Kong PMI (45.7 vs. Prey. 44.4) printed a 7th consecutive month of contraction. Participants from mainland China were away due to Golden Week holiday. JGBs traded lower amid strength in equity markets, while the weaker than prior enhanced liquidity auction initially added to losses, but then some were later pared.

And while Asia was soundly stronger, stocks in Europe swung between gains and losses (Euro Stoxx: +0.4%) as market participants used the recent upside to book profits while the pushed back expectations of rate hike by the Fed offset the resultant selling pressure. On a company specifc basis, Glencore (-2.7%) underperforms to pare back some of yesterday’s gains. In terms of US equities, PepsiCo reported Q3 EPS of $1.35 on Exp. of $1.26, with YUM Brands reporting after the closing bell.

At the same time, despite the mixed performance by equities, Bunds edged lower since the open, paring the entire opening gains . Gilts have underperformed, albeit marginally, on touted positioning linked to the 2034 tap by the DMO.

Of note, analysts at Citi forecast global equities rising 20% by Dec 2016, suggesting the global bull market is not over. At the same time, ‘unloved’ energy sector upgraded to neutral and industrials downgraded to underweight.

In commodities, energy products mimicked the price action that of European equities this morning, with prices gradually recovering following the initial move lower to trade little changed while metals markets have seen gold traded sideways overnight with prices remaining near its best levels in a week. Elsewhere copper prices were mildly lower amid subdued demand with the world’s biggest consumer not returning to the markets until Thursday and prices of lead continued their decline to fall to its lowest level since June 2010.

In FX, the biggest story overnight was the RBA keeping the overnight rate unchanged at 2.00% maintaining its neutral policy bias

by saying that economic and financial conditions are to inform its

policy stance and that leaving rates unchanged was appropriate. The

central bank also reiterated that monetary policy needs to remain

accommodative, but refrained from any jawboning of the currency. (BBG)

Despite USD/JPY trading lower on reduced expectations of a Fed rate lift-off, overnight ATM vols surged from 11.0 to above 20.0 level, as market participants began to position for potential easing by the BoJ when policy makers meet next. On that note, according to reports in Japanese press, the possibility of a stronger JPY amid reduced expectations of a Fed rate lift-off could prompt the Bank of Japan to further ease monetary policy.

On Today’s US economic calendar we get the US trade balance: for the sake of central banks with no credibility left, let’s hope it is a terrible print so the S&P can finally regain 2,000. Also notable are speeches by the Fed’s George and Williams, but the highlight will be the ECB’s Draghi speaking in Frankfurt at 1:00 pm in what many have said could be a market-moving speech.

Overnight Media Digest from Bloomberg and RanSquawk

- Stocks in Europe swung between gains and losses after Asian equities closed higher on the back of continued push back in expectations for a fed lift-off

- JPY is firmer, as pushed back expectations of Fed rate hike put unfavourable pressure on the major pair

- Today’s highlights include the latest US trade balance report, IBD/TIPP economic optimism and API crude oil inventories as well as earnings from Pepsi and Yum Brands

- Treasuries rise amid decline in stock-index futures before week’s auctions begin with $24b 3Y notes, WI yield 0.895%, lowest since April, vs 1.056% in September.

- A slowdown in output and employment may justify the Fed keeping the near zero rate policy for “much longer, well into 2016 or potentially even beyond,” Goldman’s Jan Hatzius wrote in an note

- Traders don’t see a rate increase by the Bank of England until 2017 and while the central bank might not wait as long as that, it is understandable why markets are positioned that way, said SocGen strategist Jason Simpson

- Fortress Investment Group told investors that the emerging markets are at a beginning of a bear market that could rival the Asian financial crisis of 1997 and could last at least until March 2017

- German factory orders unexpectedly fell in August, declining 1.8% after revised 2.2% drop in July

- UBS, Citi and Morgan Stanley are among banks advising clients to pay more attention to the Brexit debate as polls show diminishing support in the U.K. for staying in the bloc

- Greece shouldn’t expect the euro area to relax bailout requirements to meet next month’s deadline for unlocking money to recapitalize its banking system, Dutch Finance Minister Jeroen Dijsselbloem said

- China’s yuan overtook Japan’s yen to become the fourth most- used currency for global payments in August, boosting the nation’s bid for it to be included in the IMF’s reserves basket

- Russia rebuffed calls for a no-fly zone to be established over Syria as its warplanes extended a bombing campaign against Islamic State and other militant groups; also ruled out sending troops to take part in ground operations

- Norway could as soon as next year start making withdrawals from its massive $830b sovereign wealth fund, which it has built over the past two decades as a nest egg for “future generations,” as a slump in oil prices takes toll on economy

- $1.65b IG priced yesterday, no high yield, one deal pulled. BofAML Corporate Master Index OAS narrows 2bp to +178 from YTD wide +180bp, widest since 2012; YTD low 129. High Yield Master II OAS narrows 21bp from YTD wide +683, also widest since June 2012; YTD low 438

- Sovereign 10Y bond yields higher. Asian and European stocks gain, U.S. equity-index futures fall. Crude oil mixed, copper lower, gold gains

DB’s Jim Reid concludes the overnight recap

Markets ripped again yesterday with European stocks (Stoxx 600 +3.01%) having their best day since August and the S&P 500 (+1.83%) experiencing gains for the 5th successive session for the first time in 2015. In fact this index is up nearly 115 points from the lows early last week and 90 points above where we hit after the bad open on Friday. It was a solid start to the week for risk assets generally with credit also off to a strong start with CDX IG some 5bps tighter in the US and Crossover 20bps tighter in Europe, while EM and commodity sensitive currencies also surged higher after a decent leg up for Oil (WTI +1.58%, Brent +2.33%) and Copper (+1.51%). It’s amazing to see also that on the back of a +21% surge yesterday, Glencore is now up +72% from the intraday lows of last Monday, with the share price back to the highest level in two weeks.

Elsewhere yesterday, some slightly softer than expected US data (ISM non-manufacturing) continued to support the view of the Fed staying on hold for the foreseeable future although in fairness some of the details of the data were a little more mixed. With that said, 10y Treasury yields are now back to the pre-payrolls level after moving +6.3bps higher to 2.057% at yesterday’s close. October hike expectations were unmoved at 10% but December expectations nudged modestly higher to 35% (from 31% this time yesterday), but still remain near the lows of the recent range.

Last week we discussed our updated thoughts on the market (see Thursday’s EMR) and one small part of it was that for whatever reason the seasonals tend to be more supportive once we get into October. In today’s pdf we show a chart we’ve used before of the average path of the S&P 500 throughout a year with data going back to 1928. As can be seen the ‘average’ year sees a dip in markets in September, with October seeing stabilisation before the usual year-end rally. Interestingly though, when we look at the 1 standard deviation trendlines, October sees the biggest range of outcomes, with moves in both direction more likely in this month. There are some famous big falls in October but there have also clearly been some big rises too. So far this is looking like one of the bigger positive ones but plenty of time yet for that to be wrong!!

Turning to Asia, the rally continues with our screens generally a sea of green again as we head to print. Leading the gains are markets in Japan where the Nikkei (+1.12%) and Topix (+1.21%) have both taken a decent leg higher ahead of tomorrow’s BoJ meeting. There have been modest gains also for the Hang Seng (+0.12%), Kospi (+0.67%) and ASX (+0.35%) while credit markets in Asia, Australia and Japan are generally 3-4bps tighter. The better tone across risk assets has seen EM currencies strengthen further in Asia this morning, the Indonesian Rupiah in particular at one stage surging the most since December 2013. There’s been little in the way of data meanwhile, with the RBA leaving the cash rate on hold as expected.

Markets aside, much of yesterday’s headlines were dominated by the news that the US, Japan and ten other Pacific Rim nations have, after five years of work, come together to reach an accord on the Trans-Pacific Partnership. The trade pact, which is still subject to legislative approval by each country is set to cover 40% of the global economy and is the biggest trade deal the US has been part of since the North America Free Trade Agreement in 1994. The merits and implications of the pact will no doubt be scrutinized in due course with the finer details still to be announced, although Abenomics has been given a clear boost with the deal a key part of PM Abe’s three-arrow strategy, while the FT is suggesting that the pact will likely face parliamentary opposition in Australia and Canada in particular. There’s set to be some tension in US Congress too, with the likes of Ford Motor instead urging the Government to implement ‘strong and enforceable currency rules’ over concerns that Japanese carmakers will likely benefit under the agreement from further weakness in the Yen.

Back to markets and looking closer at yesterday’s data flow. The main focus was on the September ISM non-manufacturing reading which eased 2.1pts to 56.9, below expectations of a fall to 57.5. The details made for more mixed reading however. The new orders component grabbed some attention after dropping 6.7pts in the month to the lowest in seven months. Prices paid were also soft, dropping to the second-lowest level since July 2009 although on the other hand and seemingly in stark contrast to Friday’s NFP’s, the employment component rose 2.3pts to 58.3 and well above the six-month average of 56.4. Away from this, we also got the final September services PMI which dipped to 55.1. Finally, the September labour market conditions index was flat for the month, declining 1.2pts from August and well below hopes for a bounce to +1.4.

Closer to home, yesterday’s final September Euro area composite PMI was revised down at the last count by 0.3pts to 53.6 versus the flash reading, leaving it at the lower end of the narrow range seen since March. Much of that disappointment was driven by Spain which saw its composite notched down unexpectedly by 4.2pts to 54.6 (vs. 58.0 expected). Italy was revised down 1.3pts to 53.3, while Germany was taken down slightly to 54.1 (-0.2pts from the flash reading). Offsetting this to some extent was a 0.5pt upward revision for France to 51.9. Over in the UK meanwhile we saw the composite PMI drop 1.9pts unexpectedly to 53.3 (vs. 54.9 expected). Away from the PMI’s, the Euro area investor confidence reading dropped 1.9pts to 11.7 (vs. 11.8 expected) and retail sales for the region printed as expected at 0.0% mom for August.

Taking a look at today’s calendar, German factory orders data for August and UK house price data for September are the highlights of a relatively light calendar this morning in Europe. Over in the US however we’ve got the August trade balance print with the deficit expected to widen sharply (to $48bn from $41.9bn) in light of last week’s advance international trade data which showed a substantial deterioration in net exports. On this, our US colleagues note that assuming there are no further revisions in today’s data and little offset from the trends in services, the deterioration in Q3 net exports could subtract about two full percentage points off output. While inflation-adjusted consumer spending should help underpin Q3 growth, they note that in light of the latest data on net exports, they expect to reduce their projection of H2 real GDP growth in 2015. Away from the trade data, also expected in the US this afternoon is the IBD/TIPP economic optimism reading for October. Fedspeak today is highlighted by George (due to give a key note speech shortly after lunch) and Williams this evening while shortly after the European close we are due to hear from the ECB President Draghi.

Yuan Rising: China Surpasses Japan To Claim Number Four Spot In Most Used Global Currencies

Bungled efforts to mark a “managed” transition to a new currency regime notwithstanding, China seems generally to be doing a decent job of gradually paving the way for a world in which the yuan plays a far greater role in global trade and investment.

That is, if we look beyond the recent FX market turmoil, the picture that emerges is one in which China has managed to convince Russia to settle oil imports in renminbi and in which the AIIB and Silk Road funds are set to help establish the yuan as the funding currency for billions in development projects.

While we may still be years away from the fabled “yuan hegemony,” we got still more evidence on Tuesday that despite the currency’s rather uncertain medium-term trajectory and despite a still closed capital account, China is moving ever closer to establishing the RMB as a reserve currency. Here’s WSJ:

In August, for the first time, the yuan moved ahead of Japan’s yen for fourth place in a league table of the most-used currencies for cross-border payments compiled by Swift, the international payments provider.

A “substantial” increase in usage of the currency in the final week of August was triggered by market volatility caused by concerns about the Chinese economy and Beijing’s devaluation of the yuan, Swift said in a report.

the Chinese currency has been gaining traction. As recently as August 2012, the yuan was ranked No. 12 on Swift’s list with just a fraction of its current share of the global payments market.

Astrid Thorsen, head of business intelligence solutions at Swift, said volatile Chinese markets spurred greater use of the Chinese currency, especially toward the end of August.

China’s yuan recorded its biggest one-day loss in two decades in August after the country’s central bank surprised markets by devaluing the currency. The yuan had been strengthening for about a decade before the move, which Beijing said was meant to help shift the currency toward a more market-driven model.

The devaluation was also viewed by many investors as a sign of growing concern among Chinese authorities about the state of the country’s economy, helping to fuel fears of a slowdown.

The volume of foreign exchange trades in yuan hit more than 1 million for the first time in a single month in August, rising 50% from the same period last year and up 20% from July, “likely due to the devaluation…by the People’s Bank of China,” the Swift report said.

“Trading [in yuan] was almost nonexistent five years ago but today ranks amongst the most traded currencies globally,” said Chris Knight, head of electronic trading for Asia at Standard Chartered Bank.

“Given China’s role as a regional and global business hub at the center of economics and commerce, it has become critical for us to trade [it].”

Here’s Bloomberg with more:

China’s yuan overtook Japan’s yen to become the fourth most-used currency for global payments, shrugging off a surprise devaluation to rise to its highest ranking ever and boosting its claim for reserve status.

The proportion of transactions denominated in yuan climbed to a record 2.79 percent in August, from 2.34 percent in July, according to a Society for Worldwide Interbank Financial

Telecommunications statement on Tuesday. It was second for global issuance of letters of credit by value with a 9.1 percent share, compared with 80.1 percent for the U.S. dollar.

The report comes as the International Monetary Fund prepares to conduct a twice-a-decade review of its Special Drawing Rights basket, which currently comprises the U.S. dollar, euro, yen and the British pound. China has been pushing the yuan’s case for inclusion, which Standard Chartered Plc estimated could trigger as much as $1 trillion of inflows into the currency. The People’s Bank of China on Aug. 11 devalued the yuan reference rate by 1.9 percent and switched to a more market-oriented fixing, spurring a 2.6 percent slide in the currency in August.

“The data are positive for the probability of the yuan getting into the SDR basket,” said Nathan Chow, an economist at DBS Group Holdings Ltd. in Hong Kong who predicted in January that the currency would surpass the yen in global usage this year. “It shows that the so-called devaluation in August, which wasn’t massive in value, hasn’t driven people away from using the yuan.”

Glencore Stock Is Re-Crashing

After 5 days of CEO-confidence-inspired BTFD-ing (a la Bear Stearns), following the 30% collapse at the start of last week, Glencore’s stock price is tumbling 7.7% in the early European trading. Following a deep plunge off the open yesterday (which was rallied back to the highs) and extreme volume at the close, Tuesday’s early weakness has pushed the stock to the biggest loss since last Monday’s carnage…

The shares rebounded after the firm said its business is “robust” and it has secure access to funding.

But it’s not over…

Charts: Bloomberg

Glencore Explains What Would Happen If It Is Downgraded To Junk

As part of its ongoing scramble to defend itself against “speculators” and concerns about its balance sheet, earlier today Glencore released a 4 page “funding worksheet” detailing all of its obligations.

Among the highlights was Glencore’s disclosure of total available liquidity as of this moment, which the firm reported to be materially above its June level of $10.5 billion:

At 30 June 2015, available committed liquidity was $10.5 billion (p. 71 of 2015 Half-Year Report). As of today, committed available liquidity is materially above June’s level, given the recent $2.5 billion equity placement, the business generating positive free cashflow and the ongoing focus on delivery of the various other debt reduction measures, including lower net working capital. Further delivery of the debt reduction programme, including the $2 billion target for asset disposals, will similarly enhance liquidity levels.

It also presented its sources of funding among which the well-known $31.1 billion in bonds, as well as $20 billion in short-term funding split between a $15.25 revolver (of which a “substantial portion” is undrawn), $1.2 billion in AR/Inventory secured funding, and $3.4 billion in bilateral bank facilities. Glencore was quick to point out the gullibility of its bank lenders: “No financial covenants, no rating events of default or rating prepayment events, no material adverse change events of default or material adverse change prepayment events.”

Next Glencore details the terms of its notes and cross-guarantees which it lays out as follows:

$36.5 billion notes outstanding at 30 June 2015, including $1.9 billion maturing in October 2015. See Appendix for full details.

- Notes are issued on a pari passu basis, applying a cross guarantee structure introduced at the time of the Xstrata acquisition (see Moody’s and S&P reports dated 7 May 2013 and 19 June 2013, respectively).

- Glencore Group bonds (issued by Glencore Funding LLC, Glencore Finance (Europe) AG and Glencore Australia Holdings Pty Ltd) have guarantees from Glencore plc, Glencore International AG and Glencore (Schweiz) AG (previously Xstrata (Schweiz) AG).

- Following the Xstrata acquisition, legacy Xstrata bonds (issued by Xstrata Finance (Canada) Limited, Xstrata Canada Financial Corp, Xstrata Canada Corporation and Xstrata Finance (Dubai) Limited) also now have guarantees from Glencore plc and Glencore International AG, implemented by way of supplemental indentures.

- Similarly, the outstanding USD notes issued by Viterra Inc. in August 2010 have guarantees in place from Glencore plc and Glencore International AG.

Glencore also notes the $17.9 billion in Letter of Credit commitments it had outstanding as of June 30:

As part of Glencore’s ordinary sourcing and procurement of physical commodities and other ordinary marketing obligations, the selling party (or Glencore voluntarily) may request that a financial institution act as either a) the paying party upon the delivery of product and qualifying documents through the issuance of a letter of credit or b) the guarantor by way of issuing a bank guarantee accepting responsibility for Glencore’s contractual obligations.

The LC is not incremental exposure to that already reported in the financial statements. An LC is only a “contingent” obligation, disclosed as such in Glencore’s financial statements i.e. becomes a liability in the event that Glencore does not perform on an already recorded liability. The underlying transaction / procurement liability is recognised within “Trade Payables” in Glencore’s balance sheet. At 30 June 2015, $17.9 billion of such LC commitments have been issued on behalf of Glencore, with the respective liabilities reflected within the $28.1bn of recorded accounts payables. The contingent obligation settles simultaneously with the payment for such commodity. Availability is substantially higher, such that the vast majority of these Glencore facilities remain undrawn.

An interesting tangent is when Glencore discusses it readily marketable inventories:

Represents those marketing inventories that are contractually sold or hedged. At June 30 2015, total inventories were $23.6 billion, of which Marketing RMI were $17.7 billion.

For corporate leverage purposes Glencore accounts for RMI as being readily convertible to cash due to their very liquid nature, widely available markets and the fact that price exposure is covered by either a forward physical sale or hedge transaction.

Which brings up the very interesting question: with Glencore touting its revolver availability, and its various secured facilities, just how is Glencore marking the fair value of its inventories, because a ton of copper a year ago as collateral is worth just a little bit more than a ton of copper currently. We are confident Glencore’s banks are aware of this.

But finally, and most importantly, Glencore presents what it believes would happen if it is downgraded from Investment Grade to Junk. This is what it says:

Glencore is undertaking measures to strengthen its balance sheet, including a material debt reduction, that the company expects shall serve to protect and maintain a strong BBB/Baa credit rating.

In the event of a downgrade by Standard & Poor’s and/or Moody’s from current ratings to the level(s) immediately below, a ratings’ grid in the $6.8 billion 5-year revolving credit facility provides for a modest additional margin step-up. As this 5-year revolving credit facility is expected to remain fully undrawn, the net additional effect would only be 35% of this modest step-up margin, being the applicable commitment fee only. The maximum margin for sub-investment grade rating from either Standard & Poor’s or Moody’s is 1.10%. There is no ratings grid in relation to the $8.45 billion revolving credit facility. In addition, there are $4.5 billion of bonds outstanding, where a 125bps margin step-up would apply, in the event that the bonds were rated sub-investment grade by either major ratings agency.

Which reminds us of the waterfall analysis being shared around in the weeks before the AIG downgrade unleashed a series of events that ultimately led to the insurance company’s bail out. It took, presented glowing picture of the potential risks. In the end it was very deficient. One can only hope that Glencore’s has learned the lesson of never misrepresenting the worst case scenario.

Full letter below (link)

A Liquidity Crisis Hit The Banking System In September

Something occurred in the banking system in September that required a massive reverse repo operation in order to force the largest ever Treasury collateral injection into the repo market. Ordinarily the Fed might engage in routine reverse repos as a means of managing the Fed funds rate. However, as you can see from the graph below, there have been sudden spikes up in the amount of reverse repos that tend to correspond the some kind of crisis – the obvious one being the de facto collapse of the financial system in 2008:

You can also see from this graph that the size of the “spike” occurrences in reverse repo operations has significantly increased since 2014 relative to the spike up in 2008. In fact, the latest two-week spike is by far the largest reverse repo operation on record.

Besides using repos to manage term banking reserves in order to target the Fed funds rate, reverse repos put Treasury collateral on to bank balance sheets. We know that in 2008 there was a derivatives counter-party default melt-down. This required the Fed to “inject” Treasury collateral into the banking system which could be used as margin collateral by banks or hedge funds/financial firms holding losing derivatives positions OR to “patch up” counter-party defaults (see AIG/Goldman).

What’s eerie about the pattern in the graph above is that since 2014, the “spike” occurrences have occurred more frequently and are much larger in size than the one in 2008. This would suggest that whatever is imploding behind the scenes is far worse than what occurred in 2008.

What’s even more interesting is that the spike-up in reverse repos occurred at the same time – September 16 – that the stock market embarked on an 8-day cliff dive, with the S&P 500 falling 6% in that time period. You’ll note that this is around the same time that a crash in Glencore stock and bonds began. It has been suggested by analysts that a default on Glencore credit derivatives either by Glencore or by financial entities using derivatives to bet against that event would be analogous to the “Lehman moment” that triggered the 2008 collapse.

The blame on the general stock market plunge was cast on the Fed’s inability to raise interest rates. However that seems to be nothing more than a clever cover story for something much more catastrophic which began to develop out sight in the general liquidity functions of the global banking system.

Without a doubt, the graphs above are telling us that something “broke” in the banking system which necessitated the biggest injection of Treasury collateral in history into the global banking system by the Fed.

end

Syria Ground War Imminent? U.S. Accuses Russia Of Launching Syrian Land Campaign

While the US was been surprised and angered by the stunningly fast turn of events in Syria where in the span of less than a month Russia unleashed a massive, Syria-based airborne campaign against what it says are ISIS terrorists, even as the US accuses Putin of targeting “moderate rebels”, it has had little recourse in accusing Putin of violating Syrian sovereignty: after all Russia is the only nation that Syria has officially invited to eradicate the “terrorist threat” that is ISIS.

Then, last Friday, Syria raised the stakes once again, when as Bloomberg reported a loyalist of the Assad regime said “terrorism cannot only be fought from the air,” making an appeal for more military involvement to defeat Islamic State.

In a defiant speech at the United Nations General Assembly in New York, Syrian Foreign Minister Walid al-Muallem criticized the current approach to fighting the group that has conquered swathes of territory and was encroaching on President Bashar al-Assad’s coastal stronghold in Latakia. Those gains triggered Russian intervention.

“Air strikes are useless unless they are coordinated with the Syrian Arab army, the only force to combat terrorism,” al-Muallem, who also holds the title of deputy prime minister, told a largely empty assembly hall on Friday, the last day of speeches.

The logical implication is that Syria will next invite, if it hasn’t already done so, Russian troops to join the Russian airforce in eradicating the great ISIS strawman which until recently was the pretext for “coalition” forces to bombard Syria with complete disregard for Syrian sovereignty, and the intention of destroying Assad’s military so the CIA can conclude a regime change with a pro-western leader, one which will permit the passage of a Qatar gas pipeline.

Whether or not this assessment is accurate is irrelevant, because earlier today the US decided to jump right on it, and as CNN reported, accordint to the latest U.S. assessment of Moscow’s activity in western Syria, “Russia has moved several ground combat weapons and troops into the area to potentially back up Syrian forces in the field planning to attack anti-regime forces, according to two U.S. defense officials.”

The U.S. views the move as Russia “stepping up its ground activity” in Syria to attack those forces, rather than ISIS elements, according to one of the officials.

It’s believed the Russians are positioning the weapons to be able to support a Syrian ground offensive, the officials said.

The equipment includes several piece of artillery, as well as four BM-30 multiple-launch rocket systems — all considered to be highly accurate weapons. The latter is capable of rapid-fire rocket launches. Several weeks ago, Russia moved about half a dozen artillery pieces into Latakia port.

The U.S. originally had thought that might be for defense of the port, but the latest move is an indication of potential ground attacks in the coming days, the official said. The weapons have been spotted between Homs and Idlib and west of Idlib.

It is not clear if they’re now in final position for possible artillery strikes.

The officials also said that Russia has moved electronic jamming equipment into Syria. Both a truck-mounted system and a number of pods that can go on aircraft have been observed. This could potentially give the Russians the ability to jam electronics of coalition aircraft.

Naturally, when playing the diplomatic game, one never admits or denies one’s true intentions until well after the fact, and moments ago the speaker of the Russian Federation Valentina Matviyenko denied. According toInterfax, Matviyenko said Russia has no intention of taking part in ground operations in Syria.

“We do not intend, and we will not engage in any ground operations” said Matvienko in the meeting with the head of Jordan’s Senate president Abdelraouf al-Rawabdeh. She stressed that the Russian air campaign in Syria is to support the actions of the regular Syrian army against terrorists.

Which, ironically, is the excuse for US presence in Syria too.

What happens next? A very likely course of events is that despite Russia’s denials, the Pentagon will use the gambit of a Russian ground campaign, credible or not, to get permission from Congress to send a “small”, at first, then bigger ground force of US troops in Syria to, you guessed it, “fight ISIS“, but really to do everything to prevent Russian troops from taking over key strategic positions.

What happens then? Well, with the previously discussedRussian naval campaign of Syria as a likely next step, and with both US and Russian warplanes already flying back and forth above Syria, and now both superpowers having a legitimate, if only in the eyes of their own media, justification to dispatch land troops, what was until now a mere proxy war is about to become full blown land combat on Syrian soil, one which will soon involve both Russian and US ground, sea and airborne forces.

The last missing step will be when US cruisers, destroyers and/or battleships park next to the Syrian coastline, within earshot (and every other “shot”) away from comparable Russian warships. Keep tabs on the weekly US naval update, because once several US warships weigh anchor in the vicinity of Syria that will be the catalyst for the next and final escalation.

At that point, the world will be one false flag away from what some could call another world war, only this time one launched not in Serbia but Syria.

Saudi Clerics Call For Jihad Against Russia, Iran; NATO Warns Of Airspace “Violations”

It’s now been nearly a week since Russia began its air campaign in Syria and as we’ve documented extensively, both Moscow and the West have put their respective propaganda machines into high gear in an effort to control the narrative and thus dictate how history will remember Syria’s four-year-old, bloody civil war.

Lacking viable options in the face of Russia’s rapid military deployment at Latakia, the US has turned to the only thing left in the spin toolbox: the contention that Moscow’s airstrikes are hitting the “good” guys. Here’s WSJ:

Russia has targeted Syrian rebel groups backed by the Central Intelligence Agency in a string of airstrikes running for days, leading the U.S. to conclude that it is an intentional effort by Moscow, American officials said.

The assessment, which is shared by commanders on the ground, has deepened U.S. anger at Moscow and sparked a debate within the administration over how the U.S. can come to the aid of its proxy forces without getting sucked deeper into a proxy war that PresidentBarack Obama says he doesn’t want. The White House has so far been noncommittal about coming to the aid of CIA-backed rebels, wary of taking steps that could trigger a broader conflict.

U.S. officials said Russia’s targeting of its allies on the ground was a direct challenge to Mr. Obama’s Syria policy. Underlining the distrust, the Pentagon decided against sharing any information with Moscow about the areas where U.S. allies were located because it suspected Russia would use that information to target them more directly or provide the information to President Bashar al-Assad’s regime.

American officials and the allied commanders said several other rebel groups covertly backed by the U.S. and its coalition allies have also been targeted by the Russians. They include the First Coastal Division, whose base in northern Latakia province near the Turkish border was struck twice on Oct. 2 starting at 9:45 p.m., according to the group’s commander, Capt. Muhammad Haj Ali.

The Obama administration briefly considered asking the Russians to avoid certain areas inside Syria held by moderate opposition rebels, officials said. But they set aside the idea when it became evident the Russians could use the information to more directly target America’s allies.

There have long been skeptics within the Obama administration and the Congress about the CIA’s arm-and-train program in Syria, reflecting doubts in both branches of government about the ability and the wisdom of trying to build an anti-Assad army from scratch.

“On day one, you can say it was a one-time mistake,” a senior U.S. official said of Russia’s strike on one of the allied rebel group’s headquarters. “But on day three and day four, there’s no question it’s intentional. They know what they’re hitting.”

Yes, they indeed do “know what they’re hitting.” They’re hitting any and all targets that are strategically significant for Assad’s enemies which means that, as we’ve said repeatedly of late, this is going to be over in a matter of months if not weeks unless the US decides it’s finally time to deploy the best recession cure of all: war.

And as unlikely as you may think that is, the media seems to be preparing the American public for a possible direct confrontation with the Russians. As a reminder, Moscow’s warplanes allegedly violated NATO member Turkey’s airspace on Monday and thanks to Erdogan’s need to secure Washington’s acquiescence for Ankara’s crackdown on the PKK, the US is flying sorties out of Incirlik which means, as we noted earlier today, “close calls” between US and Russian jets are likely to increase. Here’s CBS:

U.S. pilots flying F-16s out of Turkey first picked up the Russian planes on radar. The Russians closed to within 20 miles, at which point the American pilots could visually identify them on their targeting cameras.

Lt. Gen. Charles Brown, commander of the American air campaign, said the Russians have come even closer than that to his unmanned drones.

“The closest has been within a handful of miles of our remotely piloted aircraft,” said Brown. “But to our manned aircraft they’ve not been closer than about 20 miles.”

Brown said he intends to simply work around the Russians in Syria, and he doesn’t think they will crowd out American operations.

“We’re up a lot more often than [the Russians] are so when we do have to move around [them] for safe operation, it’s for a small period of time compared to the hours and hours that we’re airborne over Iraq and Syria,” said Brown.

Indeed, NATO is apparently “not buying” Russia’s “excuse” that it violated Turkey’s airspace by accident. Here’s Reuters:

NATO on Tuesday rejected Moscow’s explanation that its warplanes violated the air space of alliance member Turkey at the weekend by mistake and said Russia was sending more ground troops to Syria.

With Russia extending its air strikes to include the ancient city of Palmyra, Turkish President Tayyip Erdogan said he was losing patience with Russian violations of his country’s air space.

“An attack on Turkey means an attack on NATO,” Erdogan warned at a Brussels news conference.

NATO Secretary-General Jens Stoltenberg said the alliance had reports of a substantial Russian military build-up in Syria, including ground troops and ships in the eastern Mediterranean.

“I will not speculate on the motives … but this does not look like an accident and we have seen two of them,” Stoltenberg said of the air incursions over Turkey’s border with Syria. He noted that they “lasted for a long time”.

The incidents, which NATO has described as “extremely dangerous” and “unacceptable”, underscore the risks of a further escalation of the Syrian civil war, as Russian and U.S. warplanes fly combat missions over the same country for the first time since World War Two.

Meanwhile, The Kremlin is being careful to preserve its image as the hero in all of this by formally rejecting calls for a no-fly zone, even as Russia’s bombing raids have effectively served to keep everyone else out of the skies. Via Bloomberg:

Russia rebuffed calls for a no-fly zone over Syria as Saudi clerics and Islamist rebels urged for retaliation against its extended bombing campaign that has targeted Islamic State and other militant groups in the Arab country.

Officials from Moscow ruled out sending troops to take part in ground operations in Syria, a day after the head of the Russian parliament’s defense committee said volunteers could go to fight, including some who took part in the conflict in Ukraine. NATO meanwhile said Russian incursions into Turkish airspace in recent days looked deliberate.

A no-fly zone would breach Syrian sovereignty and “isn’t based on the UN Charter and international law,” Deputy Foreign Minister Mikhail Bogdanov, who is Russia’s special presidential envoy to the Middle East, said in an interview published Tuesday by the Interfax news service. “Of course, we are against this. You need to respect the sovereignty of countries.”

Russia began its air campaign last week to bomb Islamic State and other jihadist groups in Syria, its first foray outside the former Soviet Union in more than three decades. Syria’s opposition groups, including Islamist rebels, and anti-Russia fighters with Islamic State have criticized the move, with many likening its intervention in Syria to the Soviet Union’s involvement in Afghanistan that began in 1979.

“Many” many ideed be likening it to the Soviet-Afghan war but one person who certainly is not is Moscow’s spin lady extraordinaire Maria Zakharova:

- RUSSIA WILL NEVER REPEAT AFGHAN EXPERIENCE IN SYRIA: ZAKHAROVA

So there you have it. But even if Russia doesn’t intend to repeat the Afghan experience, and even if the notion being propogated in the Western media that Moscow’s effort to eradicate Assad’s opponents will somehow promote terrorism is largely a myth, it looks as though the Saudis are set to promote still more violence in Syria thus creating a kind of self-fulfilling prophecy, and on that note, we close with this from Bloomberg:

More than 50 Saudi clerics called on Syrian rebels and Muslim countries on Monday to support a jihad against Syria’s government and its allies.

“This is a real war on Sunnis, their countries and their identities,” said the statement. It urged the rebels to join a “jihad against the enemy of God and your enemy and Muslims will back you every way they can.”

World’s Largest Sovereign Wealth Fund Is Forced To Begin Liquidating Assets

One of the biggest stories of this summer, as previewed originally here in November of 2014, has been the dramatic shift in the direction of capital flow from towardemerging markets (and China), to away from emerging markets (and China). The reason for this has been the double whammy of the soaring dollar, and the collapse in oil prices which as we said one year ago, would lead to the first negative global petrodollar export balance in 18 years…

… a topic which the IIF finally picked up and expanded on last week when it likewise calculated that capital outflows from emerging markets are on track to exceed inflows this year for the first time since 1988.

We first dubbed this phenomenon Reverse QE, a name which Deutsche Bank subsequently “reverse-engineering” into Quantitative Tightening, a different name for the same thing – the removal of excess liquidity from the market by way of obtaining liquidity for existing reserve assets, also known as “selling.”

However, while Reverse QE, or QT, or whatever one wants to call it has become traditionally associated with Emerging Markets and petroleum exporters, nobody had linked it with one of the most advanced Developed Markets in the world which also happens to be an oil exporter, the market with the largest sovereign wealth fun in the world: Norway.

That is about to change because as Bloomberg reports, “the future may already be here”, a future in which Norway’s gargantuan $830 billion sovereign wealth fund, the product of two decades of capital accumulation courtesy of Norway’s vast petroleum reserves and oil trade, is forced to begin liquidating its vast assets.

According to Bloomberg, Norway could as soon as next year start making withdrawals from its massive $830 billion sovereign wealth fund, which is a nest egg for “future generations.”

The start of asset sales marks a historic shift for said “nest egg” which was not supposed to be tapped for many more years. Unfortunately for Norway, which has already spent recent years using a growing chunk of its oil revenue to plug deficits while at the same time building the wealth fund…

… tax revenue from petroleum extraction are down 42% which means budget spending in 2016 will outstrip income.

The real problem for Noway is simple: the very procyclical plunge in oil prices.

As Bloomberg calculates, taxes collected on petroleum extraction reached 138 billion kroner in the first three quarters of the year, down over 40% from 238.2 billion kroner in the same period a year earlier, according to Statistics Norway. But while oil-linked revenues are plunging, spending is going nowhere but up:

The government said in May its non-oil budget deficit, or spending in real terms, would be a record 180.9 billion kroner ($21.6 billion). With its crude output waning and prices falling, the government saw petroleum income dropping to 251.6 billion kroner this year, almost 30 percent lower than its October projections. Those estimates assumed oil at about $69 a barrel.

Brent crude has averaged $56 so far this year, and has been below $50 for the past several months, presenting a huge challenge: how to tap the revenue shortfall.

The answer is simple, if unpleasant: break open the piggy bank, or in this case, start selling the securities held in the Norwegian sovereign wealth fund.

“We have reached a point where we will from now on see that the oil-corrected balance will be above the cash flow — that’s based on oil prices increasing slowly in the future,” said Kyrre Aamdal, senior economist at DNB ASA in Oslo. Tapping the fund’s returns marks a turning point that wasn’t expected to come for “several more years,” he said.

Tapping the fund to cover budget needs comes at a time when the managers of the fund, set up to safeguard the wealth of future generations, warn that it also faces diminished returns ahead amid record-low interest rates.

To be sure, government officials, terrified of revealing the unpleasant truth to the people, are pretending that the funding shortfall can be covered only with dividend and interest income:

Government officials and economists contend that only investment returns from the fund will be used for the budget, meaning it will not actually shrink in size. By using interest and dividends to cover the deficit, “no one will ever need to break the piggy bank,” said Knut Anton Mork, senior economist at Svenska Handelsbanken AB in Oslo. Oeyvind Schanke, chief investment officer for asset strategies at the Oslo-based fund, said in an interview last month it will be able to use the cash it gets from dividends and bond interest payments to make shifts in the portfolio, rather than having to sell assets.

Populist rhetoric aside, the SWF will have no choice but to sell: “capital coming into to the fund has already started to dwindle. Inflows were just 17 billion kroner in the first half of this year, compared with a quarterly average of 60 billion kroner over the past 10 years.Central bank Governor Oeystein Olsen, who oversees the fund as head of the bank’s board, said in February that oil around $60 would mean transfers to the fund “may come to a halt.”

Oil is now nearly 20% lower, and as goes the price oil, so go the inflows into the fund. Which means that any month now, if not already, Norway will shift from net buyer of global financial assets to a net seller, in the process joining the Emerging Markets and, of course, China in soaking up even more liquidity, mostly USD-denominated,out of the market, in the process removing much of the liquidity injected by the Fed and its peer central banks.

This situation will only deteriorate that much further, and force the wealth fund to sell even more assets should the Fed hike rates, pushing the dollar even higher, and sending the price of oil crashing below. In fact, the coordinated selling of US-denominated assets will be precisely the catalyst that sends the global stock market tumbling, and ultimately serve as the catalyst for NIRP and/or QE4.

The only question is whether Yellen has finally figured this out and will proceed straight to the NIRP/QE4 part or whether she will subject the market to 6-9 months of gut-wrenching volatility as the world’s largest sovereign wealth fund realizes what it means to try to sell billions of assets into an illiquid, bidless, market.

In the meantime, and completely independent of what Yellen does in the near future, what was until recently a parabolic move higher in assets…

… is about to see its first ever decline.

Last Two Times this Happened, the US Was Falling into a Recession

By Wolf Richter www.wolfstreet.com

Revenues of the companies in the S&P 500 have been declining all year. Companies and analysts blamed the strong dollar. They blamed China. They blamed oil, Greece, Japan, and a million other things. In the first quarter, revenues dropped 2.9% from a year earlier. In the second quarter they dropped 3.4%. And in the third quarter, according to FactSet, they’re expected to decline by 3.4%.

The last time year-over-year revenues declined two quarters in a row was in 2009 during the Financial Crisis [read… Revenue Recession Spreads past Dollar, Energy]. Now there have been three quarters in a row of revenue declines.

It’s tough out there.

Given this revenue debacle, corporate earnings growth has been shrinking. By Q2, it turned negative (-0.7%), according to FactSet. And in Q3, earnings “growth” dropped deeper into the negative, now estimated at -5.9%, despite all the expert financial engineering, share buybacks, and accounting tricks that companies have been leveraging with great skill and singular dedication.

But if US-based corporations blame the strong dollar, then foreign-based corporations should benefit from the strong dollar. It’s a zero-sum game: if one loses the other gains. We’ve already seen profits soar at Japanese corporations during the early phases of the yen devaluation in 2013 and 2014.

But that bonanza is over. Companies in other countries have been struggling too, despite the strong dollar that should have been beneficial to their non-dollar financial reports. And some of the deterioration has been reflected in global share prices, which have gotten hammered, including in Japan.

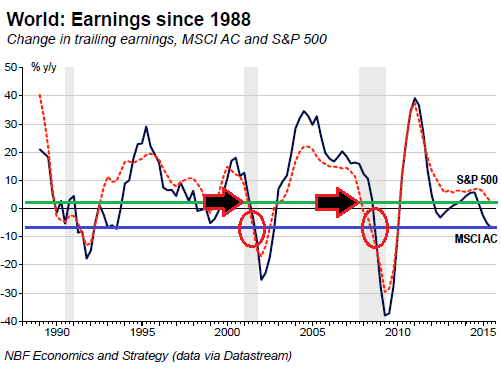

The MSCI AC world index, which captures large and mid-cap stocks across 23 developed markets and 23 emerging markets, has now been dropping for two quarters in a row – worst performance in four years.

Turns out, for the companies around the globe that comprise the MSCI AC, earnings “growth,” as measured by 12-month trailing earnings, is in even worse shape than for those in the S&P 500: by Q2, it was -7%!

So this is a global thing.

It has not primarily been triggered by the strong dollar, but by a global slowdown in revenues caused by a global slowdown in demand.