Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1177.20 up $4.70 (comex closing time)

Silver $15.91 up 8 cents.

In the access market 5:15 pm

Gold $1176.00

Silver: $15.92

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very good delivery day, registering 108 notices for 10,800 ounces Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 208.52 tonnes for a loss of 94 tonnes over that period.

In silver, the open interest fell by a small amount of 569 contracts as silver was down by 27 cents yesterday. I guess in silver nobody of importance wants to leave the arena. The total silver OI now rests at 167,617 contracts In ounces, the OI is still represented by .838 billion oz or 120% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose to 462,744 for a gain of 2,454 contracts. We had 108 notices filed for 10,800 oz today.

We had no change in tonnage at the GLD / thus the inventory rests tonight at 697.32 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had no changes in silver inventory at the SLV / Inventory rests at 315.152 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by a small 569 contracts down to 167,617 despite the fact that silver was down by a considerable 27 cents with respect to yesterday’s trading. The total OI for gold rose by a large 2,452 contracts to 462,744 contracts, despite the fact that gold was down $11.10 yesterday.

No wonder we continue have raids on our precious metals as the OI for both silver and gold have been rising too fast for our criminal bankers.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

8 USA stories/Trading of equities NY

i) the juicing of the USA /Jap Yen trying to get the stock markets higher this morning

(zero hedge)

ii) Housing permits plummet

(zero hedge)

iii) Treasury bill yields skyrocket on fears of a debt default in two weeks

(zero hedge)

iv) the treasury bill auction was a failure due to the above debt ceiling fiasco (zero hedge)

9. Physical stories

i)Bron Suchecki states that last night’s smoking gun article by David Fairfax did not enough enough data to prove manipulation..

In my opinion, it did.

(Bron Suchecki/GATA)

ii) Jim Sinclair and Bill Holter and David Schectman of Miles Franklin are going on the road to explain to all of us what is going to happen

(GATA/Holter-Sinclair)

iii) Will the press ask the correct questions on gold manipulation at the LBMA conference (GATA)

iv)New rules making it tougher for the banks to trade in gold will force these banks out of the gold trading business. Couldn’t happen to a better group of guys..good riddance

(LBMA/Reuters/GATA)

v) Hugo Salinas Price discusses:

“The Fundamental Flaw of ‘Mainstream Economics'”

vi)Bix Weir writes on his blogsite that the USA Mint is breaking the law by not mining enough silver coins to satisfy demand

(Bix Weir/Road to Rooota!!)

Let us head over to the comex:

October contract month:

Initial standings

Oct 20/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 108 contracts

10,800 oz |

| No of oz to be served (notices) | 662 contract (66,200 oz) |

| Total monthly oz gold served (contracts) so far this month | 351 contracts(35,100 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 184,991.8 oz |

Total customer deposit nil oz

we had 0 adjustments:

October silver Initial standings

Oct 20/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 68,161/74 oz

Brinks,CNT,Scotia |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| nilNo of oz served (contracts) | 0 contract (nil oz) |

| No of oz to be served (notices) | 18 contracts (90,000 oz) |

| Total monthly oz silver served (contracts) | 64 contracts (320,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 9,288,181.7 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: nil oz

total withdrawals from customer: 68,161.74. oz

And now SLV

Oct 20.2015/ no change in silver ETF/Inventory rests at 315.152 million oz

Oct 19.2016: no change in silver ETF/Inventory rests at 315.152 million oz

Oct 16/no change in silver ETF/inventory rests tonight at 315.152 million oz

Oct 15./no change in silver ETF inventory/rests tonight at 315.152

Oct 14/no change in silver ETF/silver inventory/rests tonight at 315.152 million oz

oct 13/no change in silver ETF /silver inventory/rests tonight at 315.152 million oz

:oct 12/ no change in the silver ETF/silver inventory rests tonight at 315.152 million oz

Oct 9.2015:/no change in the silver ETF SLV inventory/rests tonight at 315.152 million oz/

Oct 8.2015/no changes in the silver ETF SLV/Inventory rests tonight at 315.152 million oz

Oct 7/a huge withdrawal of 3.243 million oz from the SLV/Inventory rests tonight at 315.152 million oz

Oct 6/no change in silver inventory/inventory rests at 318.395 million oz

oCT 5/we had a small withdrawal of inventory at the SLV of 134,000 oz/and this is also to pay for fees/inventory rests at 318.395 million oz

Oct 2.2015: no change in silver inventory at the SLV/inventory rests at 318.529 million oz

Oct 1.2015:another addition of 1,145,000 oz of silver inventory added to the SLV inventory./inventory rests at 318.529 million oz

Sept 30/no change in silver inventory at the SLV/Inventory rests at 317.384 million oz

sept 29.2015: we had another withdrawal of 859,000 oz from the SLV/Inventory rests at 317.384 million oz

Press Release OCT 6.2015

Sprott Increases Offer for Central GoldTrust and Silver Bullion Trust

Offering an Additional Premium of US$0.10 per GTU Unit payable in Sprott Physical Gold Trust Units

and US$0.025 per SBT Unit payable in Sprott Physical Silver Trust Units

When Announced on April 23, 2015, Offers Represented a Premium of US$3.06 per GTU Unit and US$0.91 per SBT Unit for Unitholders Based on Trading Value and the NAV to NAV Exchange Ratio

Premiums as of October 5, 2015 (including the Increased Consideration) are US$1.14 per GTU Unit and US$0.61 per SBT Unit

Notice of Extension and Variation to be Filed Shortly

Offers Will Now Expire on October 30, 2015 –Unitholders Urged to Tender Now

TORONTO, Oct. 6, 2015 (GLOBE NEWSWIRE) — Sprott Asset Management LP (“Sprott” or “Sprott Asset Management”), together with Sprott Physical Gold Trust (NYSE:PHYS) (TSX:PHY.U) and Sprott Physical Silver Trust (NYSE:PSLV) (TSX:PHS.U) (together the “Sprott Physical Trusts”), today announced that it has increased the consideration payable to unitholders in connection with its offers to acquire all of the outstanding units of Central GoldTrust (“GTU”) (TSX:GTU.UN) (TSX:GTU.U) (NYSEMKT:GTU) and Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (TSX:SBT.U) (the “Sprott offers”).

Unitholders will now receive an additional premium of US$0.10 per GTU unit payable in Sprott Physical Gold Trust units and US$0.025 per SBT unit payable in Sprott Physical Silver Trust units (the “Premium Consideration”), in addition to the units of Sprott Physical Gold Trust and units of Sprott Physical Silver Trust, respectively, being offered on a net asset value (NAV) to NAV exchange basis. Based on trading values and the NAV to NAV Exchange Ratio (as such term is defined in the Sprott offers) at the time Sprott announced its intention to make the Sprott offers on April 23, 2015, the offers reflected a premium of US$3.06 per GTU unit and US$0.91 per SBT unit. The premium as of October 5, 2015, based on trading values, the NAV to NAV Exchange Ratio and the Premium Consideration, represents US$1.14 per GTU unit and US$0.61 per SBT unit, respectively. In connection with this increase in consideration, the expiry time for each Sprott offer is extended to 5:00 p.m. (Toronto time) on October 30, 2015.

“Central GoldTrust and Silver Bullion Trust unitholders have been burdened for too long by a group of trustees committed to protecting the interests of the Spicer family. It is only through the public spotlight that the variety of undisclosed fees paid to supposedly independent trustees has forced public disclosures and hollow justifications. Sprott’s offers to unitholders are compelling and momentum is building as we continue to show the clear advantages of the offers. The response of the GTU and SBT trustees has been to penalize unitholders with the burden of paying for costly lawsuits and expensive advisors to protect the Spicer family and the fees they receive. We are accordingly increasing our offer to compensate unitholders for this abuse of trust, and encourage them to take advantage of this opportunity to exchange their units for an immediate premium, and trade a management committed to entrenchment to one committed to their best interests,” said John Wilson, Chief Executive Officer of Sprott Asset Management.

Added Wilson, “We have provided extensions to the offers so that no unitholders are left without this opportunity to exit an underperforming investment and enter into a high quality security that functions as intended, reflecting the value of the bullion held in the trust. Sprott appreciates the support of GTU and SBT unitholders to date and currently anticipates these extensions will be the final extensions to the Sprott offers.”

As of 5:00 p.m. (Toronto time) on October 5, 2015, there were 8,194,265 GTU units (42.46% of all outstanding GTU units) and 2,055,574 SBT units (37.60% of all outstanding SBT units) tendered into the respective Sprott offers. Total units tendered as of October 5, 2015, do not include pending units which are typically received on the date of expiration.

GTU and SBT unitholders who have questions regarding the Sprott offers, are encouraged to contact Sprott Unitholders’ Service Agent, Kingsdale Shareholder Services, at 1-888-518-6805 (toll free in North America) or at 1-416-867-2272 (outside of North America) or by e-mail atcontactus@kingsdaleshareholder.com.

Gold On Verge Of Posting First Positive Year Since 2012

Gold is looking likely to finish the year positive for the first time since 2012, according to Frank Holmes writing in Forbes today. Holmes points to the weaker US dollar, the probability of near-zero interest rates for the remainder of the year and a seasonal increase in demand as underpinning the positive momentum.

“…the yellow metal broke above its 200-day moving average and is close to erasing its 2015 losses. This could be the price reversal many gold bulls have been expecting”.

Holmes highlights the so-called US dollar “death-cross” which occurs when the 50-day moving average crosses below the 200-day moving average, an indicator that is “widely recognized as the start of a bearish trend” and not seen since September 2013.

This may be indicative of a downward trend for the dollar that would be good news for gold, allowing it “the breathing room it needs to reach the important $1,200 resistance level”.

Read the full article: “Gold On Verge Of Posting First Positive Year Since 2012”

DAILY PRICES

Today’s Gold Prices: USD 1173.70 , EUR 1032.87 and GBP 747.86 per ounce.

Yesterday’s Gold Prices: USD 1171.65 , EUR 1032.93 and GBP 757.86 per ounce.

(LBMA AM)

Gold in USD – 1 Year

Gold closed down $5.00 yesterday, ending with a loss of 0.43% for the day. Silver slipped to as low as $15.761 and ended with a loss of 1.12% closing at $15.83. Euro gold fell to about €1033, platinum lost $6 to $1009.

GoldCore will be conducting a Webinar next Thursday, October 22nd at 1600 (BST/ London/ UK time) in which we will open up the floor to attendees in our ever popular Question and Answer session.

Register Now and have your question answered byJohn Butler ofAmphora Capital.

![]()

John will be giving a keynote speech at the Precious Metals Symposium in Sydney, Australia on October 26th and 27th and we are scheduling meetings with HNW clients for him while he is in Sydney.

Contact us at sales@goldcore.com if you wish to meet John in Sydney to discuss optimal strategies to access and allocate funds to the gold market today.

end

Bron Suchecki: Gold, silver manipulation study lacked enough data

Submitted by cpowell on Mon, 2015-10-19 17:12. Section: Daily Dispatches

1:10p ET Monday, October 19, 2015

Dear Friend of GATA and Gold:

Perth Mint research director Bron Suchecki is not terribly impressed by the study by Peak Prosperity’s Dave Fairtex, called to your attention Sunday —

http://www.gata.org/node/15863

— concluding that the gold and silver markets are disproportionately manipulated downward in hours of thin trading. Suchecki sees key omissions in the study and hopes that Fairtex will run the data again with broader parameters. Suchecki’s commentary is headlined “A Manipulation Smoking Gun?” and it’s posted at the Perth Mint’s Internet site here:

http://research.perthmint.com.au/2015/10/19/a-manipulation-smoking-gun/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy GATA)

Correction: Sinclair takes seminar on the road again, this time with Holter and Schectman

Submitted by cpowell on Mon, 2015-10-19 17:50. Section: Daily Dispatches

8:52p ET Monday, October 19, 2015

Dear Friend of GATA and Gold:

Mining entrepreneur Jim Sinclair is resuming his gold market seminars, this time in Los Angeles on Saturday, November 14, and his bringing his partner in commentary at JSMineSet.com, Bill Holter, whose work also appears at GATA Chairman Bill Murphy’s LeMetropoleCafe.com, and Andrew Schectman of the Miles Franklin bullion shop, not Andy Hoffman, as mistakenly reported earlier today. Information about the new seminar is posted at JSMineSet.com here:

http://www.jsmineset.com/2015/10/19/upcoming-qa-sessions-4/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Will critical questions be raised about central banks at LBMA conference?

Submitted by cpowell on Mon, 2015-10-19 18:14. Section: Daily Dispatches

2:15p ET Monday, October 19, 2015

Dear Friend of GATA and Gold:

Reporting from the London Bullion Market Association conference in Vienna, Bullion Vault’s Adrian Ash writes that LBMA chief executive Ruth Crowell is talking about incorporating all four precious metals in an organization with much wider scope. Ash wonders if she means a “World Bullion Market Association.”

That might make worldwide market rigging easier for the central banks using the London bullion banks as their agents.

Ash adds that the delegates were welcomed to Vienna by Peter Mooslechner, a member of the board of directors of Austria’s central bank, and that the conference is to include a “central bank session.” The involvement of central banks in the gold market — public and surreptitious — sure would be an interesting subject for critical questioning. Will Ash or anyone else be allowed to pose critical questions to central bank representatives and to report the answers or refusals to answer?

Or do members of the LBMA and representatives of central banks get together like this because they are basically members of the same fraternity if not the same organization and thus not inclined to discomfort each other?

Ash’s dispatch is headlined “Gloomy on Gold at LBMA 2015” and it’s posted at Bullion Vault’s Internet site here:

https://www.bullionvault.com/gold-news/Gloomy-on-Gold-10192015

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATa.org

end

New rules making it tougher for the banks to trade in gold will force these banks out of the gold trading business. Couldn’t happen to a better group of guys..good riddance

(courtesy LBMA/GATA/Reuters)

Tough liquidity rules could push more banks out of gold, LBMA says

Submitted by cpowell on Mon, 2015-10-19 18:32. Section: Daily Dispatches

By Clara Denina

Reuters

Monday, October 19, 2015

VIENNA, Austria — New liquidity rules for banks in the European Union could raise costs for those trading gold by up to 300 percent, forcing them to withdraw from the market, the head of the London Bullion Association said.

Banks were found to be undercapitalised after the financial crisis began in 2007, forcing taxpayers to bail out many lenders and prompting the development of a global set of tougher rules known as Basel III.

The rules treat physically traded gold the same as other commodities, meaning banks trading the metal would have to carry more cash and cash equivalents as a proportion of their gold exposures to act as a buffer if there is an adverse move in the gold price. …

This, the LBMA and other industry bodies argue, makes funding gold transactions for commercial banks difficult and increases the cost of doing business. …

… For the remainder of the report:

http://www.reuters.com/article/2015/10/19/lbma-gold-regulations-idUSL8N1…

end

Hugo…..

(courtesy Hugo Salinas Price/GATA)

Hugo Salinas Price: The fundamental flaw of ‘mainstream economics’

Submitted by cpowell on Tue, 2015-10-20 00:40. Section: Daily Dispatches

8:40p ET Monday, October 19, 2015

Dear Friend of GATA and Gold:

Modern economics is getting everything wrong and merely performing experiments on humanity, Hugo Salinas Price of the Mexican Civic Association for Silver writes today, because it is using the wrong scientific method. Or as Plato said — or was it Yogi Berra? — garbage in, garbage out. Salinas Price’s commentary is headlined “The Fundamental Flaw of ‘Mainstream Economics'” and it’s posted at the association’s Internet site, Plata.com.mx, here:

http://www.plata.com.mx/Mplata/articulos/articlesFilt.asp?fiidarticulo=2…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy Bix Weir/GATA)

Bix Weir: Another smoking gun — U.S. silver eagle allocation conspiracy

Submitted by cpowell on Tue, 2015-10-20 00:49. Section: Daily Dispatches

8:48p ET Monday, October 19, 2015

Dear Friend of GATA and Gold:

Bix Weir of the Road to Roota Internet site today published an open letter to the director of the U.S. Mint and the U.S. Treasury secretary, calling attention to their violation of the federal law requiring the mint to issue as many silver eagle bullion coins as necessary to meet public demand. Claims of a shortage of metal are no good, Weir writes, since the mint simply could outbid other buyers for the metal it needs to follow the law.

Weir’s letter is headlined “Another Smoking Gun: U.S. Silver Eagle Allocation Conspiracy” and it’s posted at the Road to Roota site here:

http://www.roadtoroota.com/public/1663.cfm?awt_l=8YlKQ&awt_m=3WKlURsUflb…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

1 Chinese yuan vs USA dollar/yuan travels higher, this time at 6.3480 Shanghai bourse: slightly green, hang sang:red

2 Nikkei closed up 75.92 or 0.42%.

3. Europe stocks all in the red /USA dollar index down to 94.66/Euro up to 1.1374

3b Japan 10 year bond yield: falls slightly to .324% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 119.63

3c Nikkei now just above 18,000

3d USA/Yen rate now below the important 120 barrier this morning

3e WTI: 46.38 and Brent: 48.59

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund remains constant at .551 per cent. German bunds in negative yields from 5 years out

Greece sees its 2 year rate rises to 8.32%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 7.68%

3k Gold at $1174.60 /silver $15.89 (8 am est)

3l USA vs Russian rouble; (Russian rouble up 1/4 in roubles/dollar) 62.10

3m oil into the 46dollar handle for WTI and 48 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9512 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0819 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 5 year German bund now in negative territory with the 10 year remaining constant +.551%/German 5 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.05% early this morning. Thirty year rate below 3% at 2.90% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Halt Three-Day Rally, Drop On Energy Weakness, IBM Earnings

After yesterday’s closing ramp “prudently” just ahead of an abysmal IBM earnings report with the lowest revenues since 2002, and the latest rally in capital markets which sent European stocks to their highest level since August on the back of a barrage of global bad data which has unleashed the Pavlovian liquidity dogs screaming formoar central bank bailouts, this morning has seen a modest decline in the Stoxx 600 driven by energy names, while S&P500 futures are set to open lower on IBM’s disappointment at least until the latest massive BOJ USDJPY buying spree sends the pair to 120 and the S&P solidly in the green. The biggest political event overnight was the Canadian election, where Trudeau’s liberals swept PM Harper from power, capping the biggest political comeback in the country’s history; the Canadian dollar is largely unchanged after initially weakening then rising.

Asian equity markets traded mixed with subdued price action due to a lack of tier 1 data or speakers . Nikkei 225 (+0.3%) outperformed lifted by gains in tech names after the 4th largest weighted stock KDDI (+6%) was supported by a favourable broker move, while ASX 200 (-0.7%) underperformed amid pressure from commodity names and losses in large banks, which face an increase in capital requirements. Shanghai Comp. (+1.1%) returned back to its old “government intervention, last-minute ramp” ways, spikinmg 1.1% in the last 30 minutes of trading, despite declines in the energy sector. 10yr JGBs tracked the rebound seen in USTs, with a better than prior 20yr JGB auction also supporting the 10yr.

European equities retraced their initial gains to trade firmly in the red (Euro Stoxx: -0.8%), weighed on my energy names in tandem with the energy complex coming off its highs while exporters were weighed on by strength in EUR. on a company specific breakdown, the likes of InterContinental Hotels (+4.7%), Actelion (+3.1%) and Whitbread (+2.0%) are among the best performers after reporting earnings premarket. In line with the pullback in stocks, Bunds have come off their worst levels since the open to trade relatively flat on the day, with macro news fairly light. While orders for UK 2065 Gilt have exceeded GBP 16.5b1n, with price guidance set at 1.5 bps over 2068 Gilt.

The European session kicked off seeing volatility in FX markets, with GBP/JPY breaking above its 200 DMA, with the upside also attributed to by some desks to a touted large order in the cross. The initial upside in GBP/JPY filtered through to both GBP/USD and USD/JPY as well as commodity currencies. This saw AUD build on its gains from overnight on the back of the neutral RBA minutes from overnight and aided CAD in paring back some of the losses seen after the results of the Canadian election showed a victory for the Liberals, although CAD went on to see weakness heading into the North American crossover.

RBA Minutes from October 6th meeting stated that economic and financial conditions are to be considered in the RBA’s policy stance. Members also stated that earlier rate cuts were supportive of aggregate demand and that the RBA expects Q3 GDP to improve from Q2. (BBG/RTRS)

The energy complex heads into the NYMEX pit open relatively flat after paring its upside from overnight after yesterday’s comments after from Libya and Iran regarding prospects of increased output. This comes ahead of API crude oil inventories (Prey. 9300K), which are set to be at 2135BST/1535CDT.

In the metals complex, gold has come off overnight lows, trading in close proximity to its 200 DMA at 1175.70. Elsewhere, copper prices were weaker amid continued concerns over global demand and increased Chinese production of the metal, while iron ore remains range bound with prices failing to be bolstered following a 4.4% decline in China iron ore output last month.

On today’s US docket we have September housing starts and building permits data as the notable releases, while Dudley and Powell are due to speak at the NY Fed Conference at 9:00 am, shortly followed by Fed Chair Yellen at 11:00 am BST who is scheduled to make brief opening remarks at an induction ceremony. Corporate earnings will again be closely watched with 22 S&P 500 companies due to report including Verizon, Yahoo and United Technologies. In Europe we’ve got 6 Stoxx 600 companies set to report. Today’s large cap US earnings include Verizon, United Technologies, VMware, Bank of New York Mellon, ACE, Travelers Cos, Lockheed Martin, Yahoo, Discover Financial Services, Chubb, Chipotle and Illumina.

Market Wrap

- S&P 500 futures down 0.3% to 2021

- Stoxx 600 down 0.7% to 362

- MSCI Asia Pacific down 0.1% to 134

- US 10-yr yieldunchanged at 2.02%

- Dollar Index down 0.19% to 94.74

- WTI Crude futures up less than 0.1% to $45.90

- Brent Futures down 0.7% to $48.28

- Gold spot up 0.2% to $1,173

- Silver spot up 0.1% to $15.87

Bulletin Headline Summary from RanSquawk and Bloomberg

- Upside in GBP/JPY as European participants arrived at their desks filtered through to both GBP/USD and USD/JPY

- European equities retraced their initial gains to trade firmly in the red, weighed on my energy names in tandem with the softness in the energy complex while exporters were weighed on by strength in EUR

- Looking ahead, today’s highlights include US housing starts and building permits, GDT auction and API crude oil inventories, while speakers include BoE’s McCafferty & Carney, ECB’s Nowotny, Fed’s Dudley & Yellen

- Trudeau’s Liberals Oust Harper With Surprise Canada Majority: Liberal Party swept into office, capping the biggest political comeback in the country’s history

- The day of reckoning for many debt-heavy oil drillers has been postponed as lenders are giving energy producers more time to cut costs and raise cash

- The U.S. dropped its view that China’s currency is “significantly undervalued” while saying that forces driving appreciation in the longer term remain and China needs to allow such strengthening eventually

- United Picks Counsel as Acting CEO With Munoz on Medical Leave: Brett Hart named acting CEO; says it’s still too early to determine “course and treatment” of Munoz’s recovery

- When Wal-Mart Stores Inc. raises its minimum wage to $10 an hour next year, Target Corp. and other competitors are going to face a dilemma: follow along and jeopardize profits or risk losing their best workers

- SanDisk Said in Advanced Talks to Sell to Western Digital: Co. said to be discussing price of $80-$90 per SanDisk share; SanDisk closed at $72 in NY trading on Monday

- ECB Says Credit Standards Improve as QE Program Supports Lending: Credit standards on loans to cos. eased for 6th consecutive qtr, ECB’s Bank Lending Survey showed on Tuesday

- Blackstone in Deal to Buy New York’s Stuyvesant Town Complex: Private equity firm said to pay $5.3 billion for complex

- Goldman Sees Treasuries Rally Overdone as Inflation to Pick Up: Investment bank sees Fed interest-rate increase in Dec.

- Apple CEO Defends Encryption, Opposes Govt Back Door: Cook and director of NSA squared off on Monday in debate over how much access tech cos. should afford U.S. intelligence agencies

- Yum Said in Advanced Preparations to Separate Chinese Business: Plans to break up business could be announced before end of month

- VW’s 12-Brand Behemoth Under Scrutiny as Costs of Scandal Mount: While VW in the past could afford to prop up financially struggling divisions with profit from Porsche and Audi, that money will now need to help cover costs linked to the crisis

- U.S. Softens Criticism of Yuan Level Amid Currency Pressures: Treasury says yuan now below “appropriate medium-term valuation”

- ‘Star Wars’ Demand Crashes Websites as Fans Rush for Tickets: Attempts on Fandango to buy tickets to the movie, which opens on Dec. 18, during the first few hours of availability produced the notice “Error 500: Technical Difficulties”

DB’s Jim Reid completes the overnight event wrap

It’s a scary 38 years since the first Star Wars film and yesterday it was the 28th anniversary of Black Monday where the DOW fell -22.61% in a fraught trading session. Last night the DOW closed a slightly less earth shattering +0.08% higher (S&P 500 +0.03%) on fairly light volumes as markets took a breather. The early Chinese data dump we discussed yesterday didn’t really seem to change anyone’s opinion on the country’s fortunes but as we’ll highlight later our economist thinks there are some important signs of more positive momentum under the surface. If anything, the main market reaction was for commodities to fall on concerns about the strength of the recovery overall. It was a tough session for Oil in particular as we saw Brent fall back below $50 after tumbling -3.03% to $48.93/bbl. WTI closed the session down -2.26% and is now sitting just above $46 as the record Saudi Arabia stockpile data from the weekend also weighed on prices. Gold closed down -0.55%, dragging most of the precious metal space with it, while Copper (-1.49%), Aluminum (-1.46%) and Lead (-1.13%) also slid lower. Those moves helped put some pressure on EM FX too, with falls of at least a percent for currencies in Russia, South Africa, Egypt and Colombia in particular.

Back to China and the latest update from our China Chief Economist Zhiwei Zhang (Data Flash – China: lackluster Q3, Q4 looks encouraging dated Oct, 19th). On the back of yesterday’s data, Zhiwei noted that there are signs from some of the leading indicators that seem to suggest that there will be an investment-led growth rebound in Q4. In particular, the notable developments include both a strong pickup in floor space starts in the property markets and secondly an improvement of the fiscal situation. On the property market, floor space starts strengthened in September with monthly growth at +15.3% yoy, which compares to -16.7% and -21.3% in August and July respectively. Meanwhile, government revenues improved on the back of the land sales recovery. Local government land sales revenues declined only -27.2% yoy in Q3, better than the -36% in Q1 and -41% in Q2. As a result, general government revenues dropped only -0.5% yoy in Q3, also better than the -3.6% in H1 2015. Zhiwei also points out that there were stronger government expenditure numbers last quarter. Added to this, strong new RMB loans and new total social financing in September are also indicating a possible recovery of investment in Q4. As a result, Zhiwei reiterates his view that GDP growth will pick up modestly in Q4 to 7.2%, led by an investment recovery. With regards to monetary policy, he does not expect an IR cut until the end of 2016, but expects one RRR cut this quarter followed by one for each quarter of 2016. On the FX front, Zhiwei believes that the CNY rate should remain stable at around 6.4 this year, before depreciating modestly to 6.7 by the end of 2016.

Moving on. The relatively benign trading session in the US last night has filtered through to the Asia session where there’s little obvious direction in markets this morning. There’s modest gains for the Nikkei (+0.27%) and Kospi (+0.19%), while China is mixed (Shanghai Comp -0.09%, Shenzhen Comp +0.94%) but the Hang Seng (-0.48%) and ASX (-0.65%) are lower. Oil (WTI +0.46%) is a touch higher after yesterday’s heavy losses while Asian credit is mostly weaker, the Asia iTraxx in particular 4bps wider as we go to print. Elsewhere, moments ago the news has emerged that the Liberals have won a surprise majority in the Canadian election, ending 10 years of Conservative ruling with the latter’s leader Stephen Harper resigning following the result as per FT.

Meanwhile, the story on the Chinese SOE Sinosteel that we mentioned yesterday is gathering steam with a Bloomberg article noting moments ago that the company delayed an interest payment on its Yuan dominated bonds due today. The same story suggests that the Chinese regulator and State Council are working with all related parties in order to try to prevent a default. Certainly a noteworthy story testing China’s commitment to allowing market reform.

It was very much a mixed day on the earnings front yesterday. Of the 7 S&P 500 companies to report, all seven names reported a miss at the top line in a similar theme to much of what we’ve seen so far this quarter. However it was a different story at the profit level where 4 of the 7 (57%) companies beat analyst expectations. After that and with 65 companies now reporting so far this season, that’s taken the earnings beats number to 74%, which compares to just 43% of beats for the top line.

Yesterday we saw Morgan Stanley join Goldman Sachs and JP Morgan in putting out a largely disappointing Q3 report. Revenues in the quarter tumbled with the drop exceeding analyst estimates by nearly $1bn after fixed income revenues in particular were down over 40%. EPS of 48c was well below the 63c market estimate, helping to send the bank’s share price down nearly 5% by the close. IBM was another to disappoint investors. After reporting a fourteenth consecutive quarter of declining sales, the company also cut its full year profit guidance, causing its share price to slide a couple of percent in after-hours trading.

It was a very quiet day for data yesterday, but the one print of note was the October NAHB housing market index print which was up 3pts from last month to 64 (vs. 62 expected), reaching the highest level since October 2005. Away from this, there was more Fedspeak for us to digest with the San Francisco Fed President Williams the latest to opine. Without pinning down any particular timing and although acknowledging that the decision is a close call, Williams noted that he expects economic conditions in the US to allow the Fed to act ‘in the near future’. While making claim that the decision will be data dependent, Williams did say that the recent data has been ‘all over the map’.

Of interest also yesterday was the Treasury’s semiannual report on economic and currency policies of major trade partners. In particular, it was the commentary around China and its devaluation of the Yuan which stood out. The report noted that further currency appreciation of the Yuan is key to the process of China rebalancing its economy in shifting its domestic economy towards greater reliance on household consumption. The report did however suggest that the near-term trajectory of China’s currency is difficult to assess given economic uncertainties, volatile capital flows and prospects for slower growth. At current levels the Treasury determined that the Yuan remains ‘below its appropriate medium-term valuation’, a change in language and notably softer than prior releases where the Treasury determined that the Chinese currency was ‘significantly undervalued’.

There wasn’t a whole lot to report in the European session yesterday. The Stoxx 600 finished up +0.31% along with the bulk of core European bourses yesterday. The underperformer was the FTSE 100 which finished down -0.40% as miners dragged the index lower. Ahead of the ECB meeting on Thursday, there were some moderately hawkish comments from ECB official Noyer, saying that the ECB’s QE program is ‘well calibrated’ and that ‘it’s already bearing fruits’.

Looking at today’s calendar, it’s another particularly quiet day for data in Europe this morning with just German PPI the notable release. It’ll be worth keeping an eye on various comments from BoE officials however with Bailey due to speak at 10am BST, followed by McCafferty at 10.45am BST and Governor Carney shortly after at 11am BST. Over in the US this afternoon September housing starts and building permits data are the notable releases, while Dudley and Powell are due to speak at 2pm BST at the NY Fed Conference, shortly followed by Fed Chair Yellen at 4pm BST who is scheduled to make brief opening remarks at an induction ceremony. Corporate earnings will again be closely watched with 22 S&P 500 companies due to report including Verizon, Yahoo and United Technologies. In Europe we’ve got 6 Stoxx 600 companies set to report.

May the force be with you today!!

end

Chinese Officials Say “Unnecessary To Be Anxious” About Economy As Margin Debt Rises Most Since June Bubble Peak

As everyone opined on China’s ‘goldilocks’ GDP data all day long, perhaps the biggest news this evening was US Treasury’s softer stance towards China’s currency ‘manipulation’, as we noted earlier, saying Yuan is merely “below appropriate medium-term valuation,” and sure enough offshore Yuan has strengthened since the report. China’s ‘official’ mouthpiece Xinhua told the people it is “unnecessary to be anxious about China’s economic growth.”And finally, for the 8th straight day, Chinese margin debt rose today to its highest in over a month. This is the longest stretch of releveraging in 4 months – since the peak of the bubble. “Will they never learn?”

He’s back…

- GEITHNER: YUAN CAN BE SIGNIFICANT RESERVE CURRENCY IN LONG TERM

- *GEITHNER: CHINA CAN TRANSITION ITS ECONOMY WITHOUT CRISIS

Offshore Yuan is strengthening since US Treasuries Yuan Report…

But PBOC weakened the Yuan fix for the 3rd day in a row…

- *CHINA SETS YUAN REFERENCE RATE AT 6.3614 AGAINST U.S. DOLLAR

Another day, another liquidity injection…

- *PBOC TO INJECT 25B YUAN WITH 7-DAY REVERSE REPOS: TRADER

And then the China propaganda flowed:

It is unnecessary to be anxious as China’s economic growth in the first 9 mos. was within expectations and adjustment directions, the official Xinhua News Agency says in a commentary on website.

Chinese economy has enormous growth flexibility, market space and leeway

And ironically, given the worst GDP print in over 6 years (and a 10 year low in Industrial Production)…Officials aid economic fundamentals are unchanged…

Positive economic signs are increasing and economy has momentum, Xinhua reports, citing a meeting by the National Committee of the Chinese People’s Political Consultative Conference.

Equity markets are lower (modestly)

- *FTSE CHINA A50 INDEX FUTURES FALL 0.2% IN SINGAPORE

Shanghai Composite has retraced 50% of the post-Devaluation plunge…

As US Futures drift on the back if IBM’s collapse… (Dow -50 points)

Weak China GDP sparked weakness in Aussie miners overnight and that is extending in today’s market(following Glencore’s tumble)…

And finally, it appears another crash is needed to remind the Chinese of the perils of levering up in a bubble…

- *SHANGHAI MARGIN DEBT RISE HITS LONGEST STRETCH IN FOUR MONTHS

“Will they never learn?”

Charts: Bloomberg

end

New calculations suggest that the net capital outflow of dollars from China top 500 billion USA

(courtesy London’s financial Times and special thanks to Robert H for sending this to us)

http://www.ft.com/intl/cms/s/0/84aa4dbe-76a3-11e5-933d-efcdc3c11c89.html

October 19, 2015 11:04 pm

China’s capital outflows top $500bn

Shawn Donnan in Washington

©EPA

Capital outflows from China topped $500bn in the first eight months of this year, according to new calculations by the US Treasury that highlight the shifting fortunes in the global economy.

The outflows, which peaked at about $200bn during the market turmoil in August according to the estimates released on Monday, have also contributed to a shift by Washington in its assessment of the valuation of China’s currency, the renminbi.

In its latest semi-annual report to Congress on the global economy, the US Treasury dropped its previous assessment that the renminbi was “significantly undervalued”. Instead, the Treasury said the Chinese currency was “below its appropriate medium-term valuation”.

“Given economic uncertainties, volatile capital flows and prospects for slower growth in China, the near-term trajectory of the RMB is difficult to assess,” Treasury economists wrote. “However, our judgment is that the RMB remains below its appropriate medium-term valuation.”

The new language reflects the cautious welcome that the Obama administration has given to Beijing’s efforts in recent months to prop up the renminbi since China announced onAugust 11 that it would allow a greater role for the market in setting the currency’s exchange rate.

It is also a sign of the recognition in Washington that even as it believes China’s currency should strengthen in the longer term, in the short term the renminbi is facing downward pressures because of several factors including what amount to historic outflows from China and other emerging economies.

“Market factors are exerting downward pressure on the RMB at present, but these are likely to be transitory,” the Treasury said. Among those factors, Treasury economists wrote, was the unwinding of carry trades betting on the appreciation of the renminbi.

Beijing’s August announcement of the change in its currency regime provoked fears that, after years of letting the renminbi appreciate, Beijing was intent on pursuing a devaluation to help exporters and boost flagging growth. The move to change the way in which the midpoint for the renminbi’s daily trading band is set also provoked the two biggest shifts downward in China’s currency against the dollar in 20 years.

In its report, the Treasury said it was still reserving judgment on Beijing’s longer-term intentions.

“Ultimately, the implementation of the [new foreign exchange] mechanism — and specifically, whether China allows the RMB to respond flexibly to appreciation as well as depreciation pressures — will indicate how responsive the new mechanism is to market forces,” the Treasury said.

But the report also recognised the fact that the People’s Bank of China has been spending heavily to prop up the currency. In just three months — July, August and September — the PBOC spent a total of almost $230bn to support the renminbi, the Treasury said.

The spending by China’s central bank was at least partly in response to the vast capital outflows from the country. In the first six months of 2014, capital outflows from China, not including foreign direct investment, amounted to $26bn. In the first half of this year, according to the US Treasury estimates, they were $250bn. That was followed by an estimated $70bn-$80bn in July and a further $200bn in August following the shift in Beijing’s exchange rate regime.

Eswar Prasad, a Cornell University economist who used to be the International Monetary Fund’s China mission chief, said the new report highlighted the difficult position in which Beijing’s summer foreign exchange move had left the US.

“The US Treasury is clearly in an awkward position as a falling renminbi and a rising bilateral US trade deficit with China will stoke further domestic criticism of China’s currency policy,” he said.

“However, Treasury has little economic basis for criticising China’s move towards greater exchange rate flexibility. Indeed, preventing the yuan from depreciating further would run counter to Treasury’s calls for China to have a more market-determined exchange rate.

end

Japanese important stories:

A sorry state of affairs in Japan:

(courtesy zero hedge)

Japan’s Fukushima Lies Blow Up With Admission Of First Radiation Cancer Casualty

The main reason why Japan has been able to successfully push the 2011 Fukushima nuclear power plant disaster far out of the public eye, is for the simple reason that the tragic fallout from said disaster would take many years to materialize: after all, it takes a long time between the initial irradiation to the first cancer symptoms, to the sad terminal outcome.

However, for the biggest, and most criminal, cover up by a Japanese government in recent history, the irradiated chickens are coming home to roost and earlier today Japan finally acknowledged the first “possible casualty” from radiation at the wrecked Fukushima nuclear power plant, a worker who was diagnosed with cancer after the crisis broke out in 2011.

According to Reuters, “the health ministry’s recognition of radiation as a possible cause may set back efforts to recover from the disaster, as the government and the nuclear industry have been at pains to say that the health effects from radiation have been minimal.”

A more accurate way of putting is that after lying for nearly 5 years that there is nothing to worry about and people should just go about their business, and that Fukushima is nothing to worry about, an unknown number of people were being exposed to deadly radiation, and only now are the consequences of the government’s lies starting to appear.

Reuters also adds that this announcement may also add to compensation payments that had reached more than 7 trillion yen ($59 billion) by July this year. That, however for those morbidly wondering, is bullish for stocks: it means Japan will need to issue more debt, thus giving the BOJ even more debt to monetize, thus pushing the Nikkei higher.

Reuters has more on Japan’s lies:

Hundreds of deaths have been attributed to the chaos of evacuations during the crisis and because of the hardship and mental trauma refugees have experienced since then, but the government had said that radiation was not a cause.

The male worker in his 30s, who was employed by a construction contractor, worked at Tokyo Electric Power Co’s Fukushima Daiichi plant and other nuclear facilities, a health ministry official said.

And yet, even when it partially admits the truth, Japan is still lying: according to the Japanese ministry official, of total radiation exposure of 19.8 millisieverts (mSv), the worker received a dose of 15.7 (mSv) between October 2012 and December 2013 working at Fukushima. As the pursits will repeatedly point out, this exposure is well lower than the annual 50 mSv limit for nuclear industry workers, suggesting that the government was not only lying about the risk of death by radiation, but also about the total exposure innocent civilians had been exposed to while believing the government’s lies.

The good news is that with Japan’s blatant disregard for human life now exposed, Japan’s civilians can finally take the protective measures they should have taken years ago.

The bad news, is that this is only the first tragic death resulting from Fukushima (with countless many more covered up). And now that the government has admitted the truth (which it likely did as it had no other choice as the bodies were piling up rapidly), expect hundreds if not thousands more Fukushima-related casualties to “make the news” in the months ahead.

end

Late this afternoon, Reuters reports that the Chinese yuan is to included in the iMF basket:

(courtesy Reuters/Economic Times)

Chinese yuan on track to be included in IMF basket: HSBC

A must read…the truth behind the real economy inside China!!

STOCKMAN’S CORNER

Red Swan Descending

by David Stockman • October 20, 2015

The proverbial peddlers of Florida swampland can now move over. They can’t hold a candle to the red suzerains of Beijing.

The latter had drawn a line in the sand at 7.0% GDP growth. Conveniently enough, the “consensus” estimate of so-called street economists was pegged at 6.8% for Q3, thereby giving authorities one thin decimal point through which to thread a “beat” at 6.9%.

By golly they did it!

Even then, China’s Ministry of Truth had to fiddle down the GDP deflator to negative 0.5% (for the second time this year) in order to hit the bulls eye. And that’s exactly the point.

No real world $10 trillion economy plagued with all of the turmoil evident in China’s whipsawing trade data or its volatile real estate development sector or its faltering rust belt and commodity-based industries can possibly deliver absolutely stable GDP numbers to the exact decimal point quarter after quarter.

In fact, the odds that these reports represent anything other than goal-seeked propaganda are so overwhelmingly high that they perforce raise another more important question. Why does Wall Street and its servile financial press not issue a loud collective guffaw when they are released?

But no, the Wall Street Journal took it all very seriously, noting both the “beat” and China’s claim that the “miss” wasn’t a miss at all:

The better-than-expected result—a Wall Street Journal survey of 13 economists forecast a median 6.8% gain—is likely to renew debate over the accuracy of China’s growth statistics…….Speaking at an event to promote entrepreneurism in Beijing on Monday, Premier Li Keqiang said “even though it was 6.9%, it is still a growth rate of around 7%.”

Right. China’s #2 communist boss is out promoting the “enterprenurial spirit” while emitting central planning propaganda to the decimal point.

You might find the irony exceptionally rich, but there is a larger message. Namely, the true size of China’s economy is unknowable to the nearest trillion or even several trillions. But that does not prevent most of Wall Street from taking seriously each and every word of China’s self-evidently clueless statist rulers spouting growth rates to the decimal point.

In truth, Wall Street has become so intellectually addled from its addiction to central bank enabled gambling that it no longer has a clue about what really matters. That’s why the next crash will come as an even greater surprise than the Lehman meltdown, and will be far more brutal and uncontainable, as well.

Yet the evidence that a China-led crash is on its way is hiding in plain sight. And what is being blithely ignored is not merely the blatant inconsistencies in its economic numbers—–such as the fact that electricity consumption has grown at only a 1.3% rate over the past year——or that its commerce with the outside world has shrunk drastically, with imports down by 23% and exports off by 3-6% in recent months.

Instead, the evidence that China is a slow-motion trainwreck lies in the very consistency of its Beijing-cooked numbers. Apparently, no one has told its credit-happy rulers that printing precise amounts of new GDP quarter after quarter by issuing credit at double the rate of nominal income growth will eventually result in the mother of all deflationary collapses.

Stated differently, if the pattern of debt versus GDP shown below is pursued long enough, the world’s greatest open air construction site will fall silent. Everything which can be built will have been delivered; any cash flow which can be encumbered with more debt will have been levered-up; any pretense that financial institutions are solvent will have given way too soaring defaults; and the Wall Street delusion that the primitive central planners of red capitalism had a iron grip on China’s runaway expansion will have been revealed as a snare and delusion.

Accordingly, the only thing that really counted in yesterday’s release was that credit is still growing at nearly 12% or at 2X the 6.2% gain in nominal GDP. And as is also evident in the chart, this massive and aberrational debt versus income gap has been underway as far back as the eye can see.

Indeed, its goes all the way back to Mr. Deng’s moment of enlightenment 25 years ago. That’s when he discovered a printing press in the basement of the PBOC and concluded that communist party power might better be preserved by running these presses red hot than by Mao’s failed dictum that power descends from the white hot barrel of a gun.

In any event, why in the world would anyone in their right mind think this crucial chart can be extended toward the right axis much longer. Assume 10 more years of 12% credit growth, for example, and China will have $90 trillion of total debt or 50% more than the already staggering amount carried by the US economy.

At the same time and given that China’s nominal GDP growth is descending in Gartman fashion from the upper left to the lower right, assume the very best outcome for nominal income. That is, posit that somehow China manages to achieve ten more years of this quarters’ 6% nominal growth. So doing, you get a mere $17 trillion of GDP.

Everywhere and always, however, a 5X total leverage ratio on an economy is a recipe for crushing deflation. In fact, it has never happened before in modern times except for Japan after 1990; and Japan at least had some semblance of functioning markets separate from the state and the rule of commercial law, contracts and bankruptcy.

By contrast, when China fully plunges into its inexorable deflationary spiral the rulers of red capitalism will have no choice except to resort to Mao’s preferred instruments of rule—–paddy wagons and machine guns—-in order to quell an outraged citizenry. After all, Mr. Deng told China’s newly ascendant capitalists that it is glorious to be rich, but did not explain that printing press prosperity ultimately results in a crack-up boom.

Stated differently, the recent 18-month rise and then overnight collapse of $5 trillion of phony market cap in the Chinese stock market gave rise to utter panic and mindless expediency in Beijing, including a de facto bailout of billionaires. China’s red rulers apparently feared that the 90 million angry stock market speculators would be no match for its 70 million party cadres——especially since most of the latter were foremost among the former.

Yet what will happen when China’s hideously inflated real estate and land values succumb to the deflationary wringer? And hideous is not too strong a word: in many urban areas housing prices have reached 15-30X the median income.

Well, there are 65 million drastically over-priced, empty apartments in China because its rulers told speculators and the rising middle class that housing prices could never fall——that they were the next best thing to a piggy bank. Accordingly, the last phase of China’s madcap construction boom is likely to be a manic spurt of prison building to accommodate the millions of irate citizens who are destined to experience China’s turbo-charged version of 1929.

The other number number in the Q3 release that has been drastically misinterpreted is the reported 10.6% growth of fixed asset investment. Needless to say, this was described as “disappointing” when it is actually a screaming symptom of China’s terminally deformed economy. If it had any hope of avoiding a crash landing, fixed investment in its fantastically overbuilt public facilities and industrial capacity would be sharply negative, not still growing in double digits.

Owing to the cardinal error embodied in Wall Street’s self-serving rendition of Keynesian economics, however, China’s fatal dependence on erecting economic white elephants and what amount to public pyramids in the form of unused airports, train stations, highways and bridges, is given hardly a passing nod. That’s because it is assumed that some way or another China will make the transition to a services and consumption based economy just like the good old shop-till-they-drop US of A.

Let’s see. When China finally stops its borrowing binge, these putative shoppers will need to finance their purchases out of current incomes. Yet is not the overwhelming share of household income in China currently earned from the supply chain for fixed asset investment and construction and from the export of cheap goods to already saturated and debt-besotted DM markets?

Just consider the fantastical reality that China’s 2 billion ton cement industry produced more in three years than did the US industry during the entire 20th century. When they finally stop building roads, apartments and factories, therefore, it is not just the cement kilns which will shutdown, but a whole network of gravel haulers, chemical plants, cement truck fleets, construction equipment suppliers, work site service vendors and much more reaching deep into the interstices of China’s hothouse economy.

Likewise, when rebar and other construction steel demand collapses and the rest of the world throws up barriers to China’s surging steel exports, as it surely will and is already doing, the ricochet effects on China massively overbuilt 1.1 billion ton steel industry will be far-reaching. The incomes of coal barons and blast furnaces workers alike have already taken a pasting, and the downward spiral is just getting started.

And wait until China’s newly minted auto dealer lots become backed-up with unsold cars as far as the eye can see. Then its 25 million unit auto industry will tumble into a depression unlike anything since 1929 when Detroit’s production plunged from 6 million cars/year to less than 2 million.

All of those suddenly unemployed auto, steel, rubber, glass, upholstery etc. workers did, in fact, economically “drop”. But it wasn’t from an excess of shopping!

In short, the affliction of Keynesian economics brought many ills to the modern world, but repeal of Say’s Law was not among them. You can have a one-time credit party, but when it inevitably ends, consumption spending defaults to that which can be financed from current incomes. Consumption is the consequence of production and income, not its cause.

Yet crack-up booms eventually destroy the bloated and unsustainable incomes generated in the raw materials, capital goods and consumer durables sectors during the boom phase. Accordingly, even the red suzerains of Beijing can not get from here to there. The phantom incomes that resulted from paving nearly half of the Asian continent occupied by 20% of the world’s population must inevitably shrink, meaning that China’s consumption and service spending will falter, too.

Stated differently, China’s red capitalism is the new black swan. There is nothing rational, stable or sustainable about it. Moreover, the consequence of its pending collapse will be literally earth shattering.

That’s because in recent years it has accounted for a lot more than the one-third of global GDP growth conventionally cited. The latter is just a measure of border-to-border economic statistics.

But the second and third order effects are equally large. From the bowels of Australia’s iron ore mines to the top of Dubai’s pointless 100 story office towers, the entire warp and woof of the global economy has been distorted and bloated by the central bank money printing spree of the last two decades, led by the red credit machines of Beijing. Everywhere economies have succumbed to over-building, over-consumption, over-financialization and endless dangerous, unstable speculation.

So forget the cleanest dirty shirt meme or the preposterous Wall Street nostrum that the US economy has been “decoupled” from the rest of the world. That’s unadulterated hogwash, and its means that the stock market and risk assets are heading for a thundering crash.

After the fact, of course, Wall Street will discover that the world economy was unexpectedly taken down when the suzerains of Beijing were unable to perpetuate the Red Ponzi.

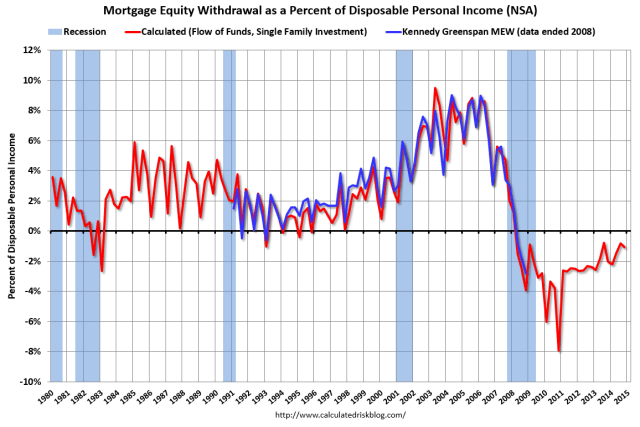

But just like last time during the mortgage and housing meltdown it was starring them in the face all along. Here is what happened to the home ATM piggy-bank that fueled the Greenspan Boom and that gave rise to the Wall Street illusion that consumption spending is the motor force of economic life.

From a peak mortgage equity withdrawal rate (MEW) at 9% of DPI or nearly $1 trillion per year prior to the crisis, MEW has been negative ever since. That is, it has subtracted from consumption, not added. Not one in one hundred Wall Street economists could have correctly projected this chart in 2007 when they were slobbering about the goldilocks economy.

Needless to say, when it comes to the wounded elephant in the room this time around—-the tottering edifice of the Red Ponzi——they are still slobbering.

end

EUROPEAN AFFAIRS

Anti islam protests are raging throughout Germany:

(courtesy zero hedge)

Furious Germans Stage Massive Anti-Islam Protest: “The Concentration Camps Are Unfortunately Out Of Action”

Over the past several months, we’ve warned repeatedly that Europe’s escalating migrant crisis threatens to set off a dangerous bout of scapegoating xenophobia.

Germany’s open door policy to asylum seekers has effectively been forced on other countries by decree, a move which could very well engender intense and possibly dangerous feelings of nationalism among citizens who disagree with Berlin’s approach to the crisis. We’ve already seen Hungary resort to razor wire fences, water cannons, and tear gas to keep migrants out and Budapest’s move to close its border with Croatia and Serbia has set off a Balkan border battle wherein no one can quite figure out the most efficient way to get the refugees to Germany without allowing their countries to be used as migrant superhighways.

Meanwhile, German Chancellor Angela Merkel is beginning to feel the heat at home. Recall the followingfrom AFP:

Germany’s Angela Merkel is used to owning the room when she speaks to her party faithful, but the mood turned hostile when she defended her open-door refugee policy this week.

In a heated atmosphere, some of the 1,000-odd members at the meeting warned of a “national disaster” and demanded shuttering the borders as Germany expects up to one million migrants this year.

“Stop the refugee chaos — save German culture + values — dethrone Merkel,” read a banner at the congress late Wednesday in the eastern state of Saxony, the home base for the anti-foreigner PEGIDA movement.

As Reuters notes, PEGIDA (which stands for Patriotic Europeans Against the Islamization of the West,) almost “fizzled out” earlier this year when the group’s leader Lutz Bachmann posted the following picture of himself on Facebook with the caption “He’s Back”:

Now, thanks to the refugee crisis, PEGIDA is apparently “back” as well, as attendance at the group’s Monday night “gatherings” swells amid the influx of Syrian asylum seekers. Here’s Reuters:

The German anti-Islam movement PEGIDA staged its biggest rally in months on Monday, sparked into fresh life on its first anniversary by anger at the government’s decision to take in hundreds of thousands of migrants from the Middle East.

But it has swelled again as Germany implements Chancellor Angela Merkel’s decision to accept a tide of refugees that could exceed a million this year, as she argues that Germany can not only cope but, with its aging population, will benefit in the long term.

Police declined to estimate the number of protesters but media put it at 15-20,000, somewhat below a peak of around 25,000 in January. Around 14,000 counter-demonstrators urged people to welcome refugees rather than whip up opposition.

PEGIDA supporters waved the national flag and carried posters bearing slogans such as “Hell comes with fake refugees” and “Every people should have its country, not every people a piece of Germany”.

Gathering outside Dresden’s historic opera house, the Semperoper, PEGIDA supporters chanted “Deport! Deport!” and “Merkel must go!”.

“We’re just normal people who are scared of what’s coming,” said 37-year-old Patrick, a car mechanic. “As a German citizen who pays taxes, you feel like you’re being taken for a ride.”

And Bachmann was there on Monday, not dressed as Hitler. Here’s what he had to say to the crowd which reportedly handed him bouquets of flowers:

“Politicians attack and defame us and the lowest tricks are used to keep our mouths shut. We are threatened with death, there are attacks on our vehicles and houses and we are dragged through the mud, but we are still here … And we will triumph!”

While it’s not entirely clear what “triumph” means in this context, you can get a clue or two by simply taking a look at the following homemade sign which showed up at last Monday’s rally in Dresden:

More from Deutsche Welle:

The anti-“Islamization” movement PEGIDA marked its first birthday with a significant resurgence – and what many observers saw as a new radicalization. The new influx of refugees over the summer and a significant backlash against Merkel’s decision to open the borders to Syrians has apparently given the racist elements in the PEGIDA movement new confidence.

Police put the attendance at Monday’s PEGIDA rally at between 15,000 and 20,000 people, with an equal number of counterdemonstrators, making this the largest turnout since the movement’s previous high point in February. But there was also a new aggression in the crowds: a Saxony police statement said the two sides threw “objects and fireworks” at one another, and said there were several attacks on officers themselves, who deployed pepper spray.

The media’s attention was particularly drawn to a 25-minute speech by the German-Turkish writer Akif Pirincci,otherwise known for a cat-based crime fiction series and a libertarian blog called “The Axis of Good,” which has often been accused of racism.

Pirincci’s extraordinary and occasionally vulgar ramble, all read from notes, included references to refugees as “invaders,” politicians as “gauleiters against their own people,” Muslims “who pump infidels with their Muslim juice” and a threat that Germany would become a “Muslim garbage dump.”

After the crowd responded with shouts of “resistance, resistance,” Pirincci said, “Of course there are other alternatives – but the concentration camps are unfortunately out of action at the moment.”

You read that correctly, the man who stood up in front of 10-15,000 people and delivered a 25-minute rant complete with the suggestion that Germany should fire back up the concentration camps writes cat detective novels in his spare time…

In any event, this is precisely what we meant when we said that feelings of intense nationalism could well lead directly to dangerous bouts of scapegoating xenophobia, and don’t expect anyone at a PEGIDA rally to be persuaded by the argument that the influx of Syrian refugees may help Germany overcome the economic hurdles it will soon face from challenging demographic shifts.

We’ll leave you with a quote from Hungary’s Viktor Orban and some visuals from Monday’s rally.

“Spiritually, Islam was never part of Europe. It’s the rulebook of another world.”

And more:

(courtesy Dave Kranzler/IRD)

Glencore Stock Is Tanking Again

After a hearty dead-cat short-cover bounce, Glencore – aka “Glenron” – stock appears to be headed quickly south again:

After a flurry of rumors about debt buybacks, asset sales and possible buyouts, it looks like the reality of gravity has gripped Glencore’s stock again, as Glencore’s stock bounced up to its plunging 50-day moving average and quickly headed south again.

A lot of unfounded assertions and articles written without factual references have surfaced, so I did a quick “drive-by” view of Glencore’s financials and recent presentations to get some truth. To begin with, 36% of Glencore’s operating income (EBIT) is derived from copper. Here’s what a long term copper chart looks like:

I don’t know about anyone else, but it appears to me that the global economic conditions are headed back down to where they were in 2008/2009 and probably even lower. That implies that the price of copper has a lot further to fall. Another 17% of Glencore’s EBIT is derived from zinc, nickel and coal. All three commodities are close to or at very long term lows, with no bottom in sight.

I think it’s fair to say that the downside risk to Glencore’s cash flow is greater than the likelihood of upside potential at this point.

As for Glencore’s debt load. In the latest management presentation, management stated the one of its goals is to maintain a “strong investment grade rating.” This made me laugh. Why? Because Glencore’s debt rating is triple-B flat (BBB/Baa). This is two downgrades away from being considered “junk.”

Original reports were that Glencore had “net debt” of $29 billion at the end of June. But let’s examine the truth before we become poisoned with propaganda. As it turns out, Glencore was carrying $50 billion of funded debt at the end of June (bonds + funded credit lines):

The graphic above is from Glencore’s 1st Half financial report. As you can see, the “$29 billion” is derived by netting out Glencore’s “readily marketable inventories.” It’s a number used by Wall Street’s snakeoil salesmen and their financial media propaganda vassals (Steve Liesman, Joe Lavorgna, Jim Cramer, Mark Zandi, etc). If these inventories are “readily marketable,” then how come Glencore does not readily sell them and pay down its debt?

Because the answer is that the inventory consists of copper, zinc, nickel and coal, all of which are in abundant supply with falling prices. The “net debt” number is therefore highly misleading and the real debt level is $50 billion, which means that Glencore is de facto a junk bond credit.

As an aside, the other day some dweeb from BlackRock, Evy Hambro, announced publicly that he backs Glencore’s big debt reduction “plan.” Of course he backs it – BlackRock is the fourth biggest holder of Glencore’s stock and undoubtedly one of its largest non-bank creditors. Tell me Evy, if Glencore’s plans are executable, why don’t they start by raising $17 billion from the “readily marketable inventory?” “Readily” means you can sell it all into a deep market bid now.

$50 billion in debt on top of what will likely be about $8.5 billion of EBITDA and likely about $2.5 billion after CAPEX for all of 2015. Glencore’s debt level, in other words, is In other words, is 20x cash flow after capex. This is a staggering ratio. It is likely that Glencore’s cash flow will continue to decline along with commodities prices and the economic contraction in China. Glencore has thus entered the realm of the Irreversible Debt Spiral.

I remember the Enron saga vividly because I was short the stock from about $42 down to where it bounced. At which point I covered and after the bounce was over I re-shorted Enron until it went below $10. I’m not suggesting that Glencore is going to be completely incinerated the way Enron was, but there’s certainly a lot of questionable events behind the “curtain” that covers Glencore, going all the way back to the time when Glencore existed as Marc Rich’s commodity trading company. I would suggest that anyone who might be exposed to the stock or the debt of Glencore should get out of the way, because Glencore certainly does not pass the “smell test.”

bounced. At which point I covered and after the bounce was over I re-shorted Enron until it went below $10. I’m not suggesting that Glencore is going to be completely incinerated the way Enron was, but there’s certainly a lot of questionable events behind the “curtain” that covers Glencore, going all the way back to the time when Glencore existed as Marc Rich’s commodity trading company. I would suggest that anyone who might be exposed to the stock or the debt of Glencore should get out of the way, because Glencore certainly does not pass the “smell test.”

end

RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia confirms that eliminating ISIS is not their only priority. Keeping and restoring Assad’s government in Syria is its primary objective:

(courtesy zero hedge)

Russia “Confirms” It Has Plans To Restore Assad Government In Syria

Watching the US attempt to explain to the public why Washington can’t join the Russians in targeting extremists in Syria has been entertainment gold. The fundamental PR problem revolves around the fact that the West has gone out of its way to hold up ISIS as the quintessential example of pure, unadulterated evil that must be eradicated at all costs and yet when Moscow began bombing ISIS targets and publicly implored the US to join in, Washington said no.

If you’re the public that seems strange. To be sure, everyday Westerners are accustomed to Russophobic propaganda in the news and in cinema and the public is thoroughly conditioned to think of The Kremlin as a weird, multi-colored palace complex staffed with hundreds of James Bond villains in a country where it’s always dark, and always snowing. That said, Western leaders have had a difficult time explaining why that’s somehow worse than ISIS, whose slickly-produced videos have so far depicted a series of beheadings, a Jordanian pilot being burned alive, “spies” being drowned in a cage, and four men being packed into a Toyota Corolla which is then destroyed at close range by a rocket launcher.

The answer, of course, is that ISIS and the various other extremist groups battling for control of Syria have almost all received training and funding from the US and its regional allies at one point or another and at the end of the day, destroying ISIS nets nothing for Washington in terms of geopolitics. In fact, were the group to go the way of the dinosaurs, it would help to restore the Assad regime which is the worst possible outcome in the eyes of the US, Saudi Arabia, and Qatar.

In short: from a geopolitical perspective, deterring Assad, Russia, and Iran is much more important than fighting any ragtag band of extremists, but that’s a tough sell to a public that’s grown weary of watching Westerners having their heads chopped off on the nightly news.

Moscow’s position is simple. The Russians are in Syria to restore Assad which means waging war on his enemies and because some of his enemies are terrorists, that means Russia is at war with terror. Putin has made no secret of this, but the US has been forced to act as though he has because without the whole “we can’t be sure what his aims are” line, an impatient public might start to demand answers as to why Washington is so obstinate when it comes to cooperation on anti-terror ops.

Now, Bloomberg reports that Russian officials have “admitted” that Moscow’s goals in Syria go beyond ISIS. Here’s more:

As Russia’s air war in Syria nears its fourth week, officials now admit that Moscow’s aim is far broader than the publicly announced fight against terrorist groups.

The Kremlin’s real goal is to help Syrian President Bashar al-Assad retake as much as possible of the territory his forces have lost to opponents, including U.S.-backed rebels, Russian officials told Bloomberg News. Moscow’s deployment of several dozen planes, as well as ships in the Black and Caspian Seas, could last a year or more, one official said.

President Vladimir Putin is willing to run the risk of falling into the kind of quagmire that helped sink the Soviet Union a generation ago for the chance to roll back U.S. influence and demonstrate he can dictate terms to Washington. If the strategy is successful, Russia’s largest military drive in decades outside the former Soviet Union would force the

U.S. and its allies to choose between Assad, whom they oppose for his human-rights abuses, and the brutal extremists of Islamic State.

A top Russian military official said on Friday that the Kremlin sees no moderate opposition in Syria, leaving only terrorists and the pro-Assad forces Moscow is backing.

“In the West, they talk about ‘moderate opposition,’ but we so far haven’t seen any in Syria,” General Andrey Kartapolov, commander of the Russian operation in Syria, told the Komsomolskaya Pravda newspaper.

“Any person who takes up arms and fights the legal authorities, how moderate can he be?”