Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1163.30 down $3.30 (comex closing time)

Silver $15.82 unchanged.

In the access market 5:15 pm

Gold $1164.30

Silver: $15.83

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very good delivery day, registering 45 notices for 4500 ounces Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 208.52 tonnes for a loss of 94 tonnes over that period.

In silver, the open interest roe by 813 contracts as silver was up by 12 cents yesterday. The total silver OI now rests at 167,321 contracts In ounces, the OI is still represented by .836 billion oz or 120% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose to 467,776 for a gain of 3,419 contracts. We had 45 notices filed for 4500 oz today.

We had a rather large withdrawal of 1.78 tonnes of gold at the GLD / thus the inventory rests tonight at 695.54 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver,no change in silver inventory / Inventory rests at 315.553 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver rose by 813 contracts up to 167,321 as silver was up by 12 cents with respect to yesterday’s trading. The total OI for gold rose by a large 3,419 contracts to 467,776 contracts despite the fact that gold was down $1.00 yesterday.

No wonder we continue have raids on our precious metals as the OI for both silver and gold have been rising too fast for our criminal bankers.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. COT report/Massive increase in gold and silver commercial short positions as they supply unbacked paper/can only be construed as fraudulent misrepresentation.

Harvey

iii) by the end of the day, the Euro plunges into the 1.09 handle briefly

we notice two potential problems:

- Multinational USA corporations and their CEO’s are not happy as earnings will fall again.

- The off shore yuan fell badly to 6.39 yuan to the dollar suggesting huge outflows of more dollars.

( zero hedge)

iv) The big question: how far will the ECB go towards monetization:

10 USA stories/Trading of equities NY

i) Good PMI numbers from the USA today. Problem: how did this occur with all 6 regional Fed showing big declines in Mfg

(zero hedge)

ii) Puerto Rico demanding a bailout: meaning bondholders being made hole and USA taxpayers suffering

(zero hedge)

iii) Bill Ackman’s Pershing square in trouble again with another holding suffering at the stock market.

(zero hedge)

iv) Dave Kranzler talks about two companies with sketchy accounting:

11. Physical stories

i) China’s Construction Bank becomes the second Chinese bank to enter the Gold fix in London

(Jan Harvey/Reuters/GATA)

ii) The seven big lies on gold/Guy Chrisopher/Money Metals Exchange

iii) Museum of American Finance will have a gold exhibit in New York

(CoinWeekly)

iv) Alasdair Macleod’s commentary for this week is entitled:

“The decline of the dollar–the consequences”

v) Bill Holter’s huge commentary tonight is entitled:

“The Crime of the Century”

vi Another 54. tonnes of gold demand from China/Lawrie on Gold

Let us head over to the comex:

October contract month:

Initial standings

Oct 23/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 45 contracts

4500 oz |

| No of oz to be served (notices) | 561 contract (56,100 oz) |

| Total monthly oz gold served (contracts) so far this month | 453 contracts

45,300 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 184,991.8 oz |

Total customer deposit nil oz

we had 1 adjustment:

October silver Initial standings

Oct 23/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 52,390.47 oz

Brinks |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 0 contract (nil oz) |

| No of oz to be served (notices) | 12 contracts (60,000 oz) |

| Total monthly oz silver served (contracts) | 81 contracts (405,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 9,450,366.0 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: nil oz

total withdrawals from customer: 52,390.47 oz

And now SLV

Oct 23./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 22./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 21:a we had a small addition in silver ETF inventory of 381,000 oz/inventory rests tonight at 315.533 million oz

Oct 20.2015/ no change in silver ETF/Inventory rests at 315.152 million oz

Oct 19.2016: no change in silver ETF/Inventory rests at 315.152 million oz

Oct 16/no change in silver ETF/inventory rests tonight at 315.152 million oz

Oct 15./no change in silver ETF inventory/rests tonight at 315.152

Oct 14/no change in silver ETF/silver inventory/rests tonight at 315.152 million oz

oct 13/no change in silver ETF /silver inventory/rests tonight at 315.152 million oz

:oct 12/ no change in the silver ETF/silver inventory rests tonight at 315.152 million oz

Oct 9.2015:/no change in the silver ETF SLV inventory/rests tonight at 315.152 million oz/

Oct 8.2015/no changes in the silver ETF SLV/Inventory rests tonight at 315.152 million oz

Oct 7/a huge withdrawal of 3.243 million oz from the SLV/Inventory rests tonight at 315.152 million oz

Press Release OCT 6.2015

Sprott Increases Offer for Central GoldTrust and Silver Bullion Trust

Offering an Additional Premium of US$0.10 per GTU Unit payable in Sprott Physical Gold Trust Units

and US$0.025 per SBT Unit payable in Sprott Physical Silver Trust Units

When Announced on April 23, 2015, Offers Represented a Premium of US$3.06 per GTU Unit and US$0.91 per SBT Unit for Unitholders Based on Trading Value and the NAV to NAV Exchange Ratio

Premiums as of October 5, 2015 (including the Increased Consideration) are US$1.14 per GTU Unit and US$0.61 per SBT Unit

Notice of Extension and Variation to be Filed Shortly

Offers Will Now Expire on October 30, 2015 –Unitholders Urged to Tender Now

TORONTO, Oct. 6, 2015 (GLOBE NEWSWIRE) — Sprott Asset Management LP (“Sprott” or “Sprott Asset Management”), together with Sprott Physical Gold Trust (NYSE:PHYS) (TSX:PHY.U) and Sprott Physical Silver Trust (NYSE:PSLV) (TSX:PHS.U) (together the “Sprott Physical Trusts”), today announced that it has increased the consideration payable to unitholders in connection with its offers to acquire all of the outstanding units of Central GoldTrust (“GTU”) (TSX:GTU.UN) (TSX:GTU.U) (NYSEMKT:GTU) and Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (TSX:SBT.U) (the “Sprott offers”).

Unitholders will now receive an additional premium of US$0.10 per GTU unit payable in Sprott Physical Gold Trust units and US$0.025 per SBT unit payable in Sprott Physical Silver Trust units (the “Premium Consideration”), in addition to the units of Sprott Physical Gold Trust and units of Sprott Physical Silver Trust, respectively, being offered on a net asset value (NAV) to NAV exchange basis. Based on trading values and the NAV to NAV Exchange Ratio (as such term is defined in the Sprott offers) at the time Sprott announced its intention to make the Sprott offers on April 23, 2015, the offers reflected a premium of US$3.06 per GTU unit and US$0.91 per SBT unit. The premium as of October 5, 2015, based on trading values, the NAV to NAV Exchange Ratio and the Premium Consideration, represents US$1.14 per GTU unit and US$0.61 per SBT unit, respectively. In connection with this increase in consideration, the expiry time for each Sprott offer is extended to 5:00 p.m. (Toronto time) on October 30, 2015.

“Central GoldTrust and Silver Bullion Trust unitholders have been burdened for too long by a group of trustees committed to protecting the interests of the Spicer family. It is only through the public spotlight that the variety of undisclosed fees paid to supposedly independent trustees has forced public disclosures and hollow justifications. Sprott’s offers to unitholders are compelling and momentum is building as we continue to show the clear advantages of the offers. The response of the GTU and SBT trustees has been to penalize unitholders with the burden of paying for costly lawsuits and expensive advisors to protect the Spicer family and the fees they receive. We are accordingly increasing our offer to compensate unitholders for this abuse of trust, and encourage them to take advantage of this opportunity to exchange their units for an immediate premium, and trade a management committed to entrenchment to one committed to their best interests,” said John Wilson, Chief Executive Officer of Sprott Asset Management.

Added Wilson, “We have provided extensions to the offers so that no unitholders are left without this opportunity to exit an underperforming investment and enter into a high quality security that functions as intended, reflecting the value of the bullion held in the trust. Sprott appreciates the support of GTU and SBT unitholders to date and currently anticipates these extensions will be the final extensions to the Sprott offers.”

As of 5:00 p.m. (Toronto time) on October 5, 2015, there were 8,194,265 GTU units (42.46% of all outstanding GTU units) and 2,055,574 SBT units (37.60% of all outstanding SBT units) tendered into the respective Sprott offers. Total units tendered as of October 5, 2015, do not include pending units which are typically received on the date of expiration.

GTU and SBT unitholders who have questions regarding the Sprott offers, are encouraged to contact Sprott Unitholders’ Service Agent, Kingsdale Shareholder Services, at 1-888-518-6805 (toll free in North America) or at 1-416-867-2272 (outside of North America) or by e-mail atcontactus@kingsdaleshareholder.com.

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 233,227 | 81,926 | 57,126 | 134,966 | 298,266 | 425,319 | 437,318 |

| Change from Prior Reporting Period | ||||||

| 29,928 | -4,214 | 4,084 | -9,276 | 35,530 | 24,736 | 35,400 |

| Traders | ||||||

| 164 | 101 | 87 | 44 | 58 | 248 | 216 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 42,473 | 30,474 | 467,792 | ||||

| 7,128 | -3,536 | 31,864 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, October 20, 2015 | |||||

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 79,449 | 22,151 | 23,381 | 42,189 | 108,989 | |

| 4,874 | -714 | 3,171 | -2,833 | 5,341 | |

| Traders | |||||

| 94 | 45 | 41 | 33 | 42 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 167,574 | Long | Short | |

| 22,555 | 13,053 | 145,019 | 154,521 | ||

| 1,016 | -1,570 | 6,228 | 5,212 | 7,798 | |

| non reportable positions | Positions as of: | 143 | 119 | ||

| Tuesday, October 20, 2015 | © Silve | ||||

Our small specs;

Those small specs that have been short in silver covered 1570 contracts from their short side.

Gold Q&A – How To Allocate, Dollar Cost Average, Rebalance and Store Where?

- Global Economic Outlook

- History and Role of Gold in Portfolios Today

- Asset Allocation – Higher Allocations to Gold Justified

- Dollar Cost Average – Need to Front End Financial Insurance

- An “ETF Is No Substitute for Physical Allocated Gold in the Vault”

- Switzerland, Singapore and London are Safest Places to Store Gold

- Q&A

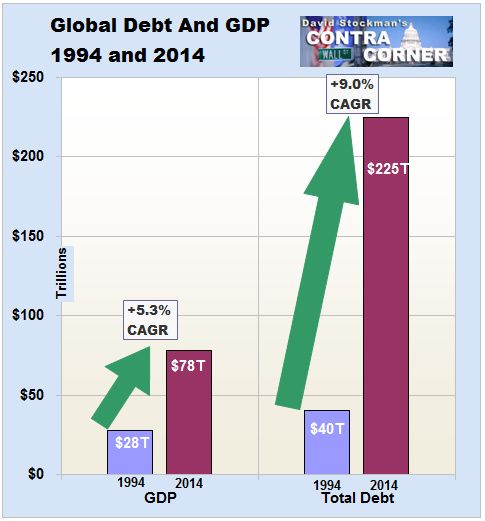

Global Debt to GDP – New GFC and Currency Reset Likely

John Butler was interviewed by Mark O’Byrne about gold and the vitally important but little covered aspects of investing in gold such as – higher allocations, how to geometrically dollar cost average, re-balancing gold and of course geographic diversification and the safest locations to own gold.

Butler believes that since the end of the Bretton Woods monetary system, there is a strong case for having higher allocations to physical gold. He warns of the risk inherent in gold ETFs due to the levels of indemnification and legal indemnifications.

“If you read the prospectuses carefully” the gold ETFs are“subject to various forms of force majeures and unforeseen circumstances” and “the gold is not even fully insured.”

“They could be susceptible to fraud” and “there may be no recourse.”Hence the importance of physical, allocated and segregated gold “outside the banking system”.

The webinar had the ever popular ‘question and answer’ section which is always well received and saw some interesting questions from the participants. Some of which included:

Q: How should an investor approach portfolio rebalancing and gold, should it ever be sold down?

Q: I am a 65 year old retiree. I have much of my pension in stocks and small amount in physical coins (2%), should I buy the Gold ETF and if so what is a good allocation?

Q: If rates start to rise in 2016, what will gold do?

Q: What do you see as the greatest threat to the world economy over the next 5 years, systematic, market, geo political?

Q: Where is the safest place to store metal?

The webinar is a must listen for anyone who owns gold or is considering allocating funds to gold.

John Butler is now a consultant for GoldCore and advising high net worth and family offices with regard to allocating funds to physical gold and institutions with regard to offering their clients precious metals services.

Butler has worked as a global investment strategist for more than 20 years and has advised many of the world’s largest institutional investors, sovereign wealth funds and central banks. He is giving the opening address at the Precious Metals Symposium in Sydney Australia on October 26th and 27th.

He is giving keynote addresses at the Mines and Money Conference in London and at the Gulf Financial Forum in December. He is available to meet to discuss optimal strategies to allocate funds to the gold market today.

Watch Video of the Webinar here

DAILY PRICES

Today’s Gold Prices: USD 1171.55 , EUR 1052.84 and GBP 760.70 per ounce.

Yesterday’s Gold Prices: USD 1166.45 , EUR 1031.30 and GBP 753.94 per ounce.

(LBMA AM)

Gold in USD – 1 Week

Gold fell by an even $1.00 yesterday to close at $1166.30. Silver fell by $0.13 to close at $15.84. Euro gold rose to about €1050, platinum gained $7 to $1008.

Gold climbed for the first time in three days after the European Central Bank signaled it will likely engage in more QE and may even move to negative interest rates. Draghi’s comments are gold bullish – particularly in euro terms.

Gold in EUR – 1 Week

Markets took ECB President Mario Draghi’s comments as a signal that additional easing was coming as soon as December. That weakened the euro against the dollar and gold. Gold in euros priced rose to the highest in three months.

Gold has risen about 5 percent this month as patchy economic data lessened expectations of a U.S. rate increase any time soon. Indeed, there are increasing noises suggesting negative interest rates may be coming in the U.S. and EU.

Gold is now just 0.2% lower for the week in dollar terms and is nearly 2% higher in euro terms. Gold is on track for its best monthly performance since January, with a rise of 5.5%.

Silver’s outperforming again today and is up 1% – it has broken above its 200-day simple moving average at $15.94/oz above the $16/oz level again at $16.08/oz.

Government-owned Chinese bank joins London gold price auction

Submitted by cpowell on Thu, 2015-10-22 15:47. Section: Daily Dispatches

The government of China is owns a majority of shares in China Construction Bank. Presumably the Chinese government now will be able to affect the London gold benchmark price directly, without having to act through Western intermediaries that can front-run Chinese buy and sell orders.

* * *

China Construction Bank Joins London Gold Price Auction

By Jan Harvey

Reuters

Thursday, October 22, 2015

China Construction Bank will join the twice-daily electronic auction process to set the benchmark price of gold, its operator Intercontinental Exchange said in a statement on Thursday.

CCB on Wednesday confirmed it would be the second Chinese company to gain access to the 138-year old London Metal Exchange’s trading floor with the acquisition of a majority stake in UK metals trading firm Metdist Trading Ltd.

The gold auction, which takes place each day at 10:30 and 15″00 London time, sets the London Bullion Market Association Gold Price, a benchmark used by producers, traders and end-users globally in contracts and transactions. …

… For the remainder of the report:

http://www.reuters.com/article/2015/10/22/china-gold-ccb-idUSL8N12M44H20…

end

(courtesy Guy Christopher/Money Metals Exchange/GATA)

Guy Christopher: The seven biggest lies told (and believed) about gold

Submitted by cpowell on Fri, 2015-10-23 01:18. Section: Daily Dispatches

9:15p ET Thursday, October 22, 2015

Dear Friend of GATA and Gold:

Writing for Money Metals Exchange, retired investigative journalist Guy Christopher itemizes and refutes what he calls the seven biggest lies about gold, starting with the lie that gold is a “barbarous relic,” something John Maynard Keynes never said, though it is commonly attributed to him. Christopher’s commentary is headlined “The Seven Biggest Lies Told (and Believed) about Gold” and it’s posted at the Money Metals Exchange Internet site here:

https://www.moneymetals.com/news/2015/10/22/lies-about-gold-000778

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy CoinsWeekly/Lorrach Germany/GATA)

Museum of American Finance in New York City will open gold exhibition Nov. 19

Submitted by cpowell on Fri, 2015-10-23 01:38. Section: Daily Dispatches

From Coins Weekly

Lorrach, Germany

Thursday, October 22, 2015

On November 19 the Museum of American Finance in New York City will open “Worth Its Weight: Gold from the Ground Up,” an exhibit that will captivate visitors with the many spectacular and unexpected ways gold has influenced our lives — from science and technology to entertainment and pop culture to finance and economics. The exhibit will be featured in three galleries and the museum’s theater and will be on view through December 2016.

“We are excited to showcase more than 100 stunning gold objects from over a dozen public and private collections in this unique exhibit on Wall Street,” said David Cowen, the museum’s president. …

… For the remainder of the report:

end

Alasdair Macleod…

Alasdair Macleod: The decline of the dollar — the consequences

Submitted by cpowell on Fri, 2015-10-23 01:56. Section: Daily Dispatches

By Alasdair Macleod

Research Director

GoldMoney, St. Helier, Jersey, Channel Islands

Thursday, October 22, 2015

There are signs that the U.S. dollar, instead of consolidating the sharp rise that peaked last March, might be reversing its previously rising trend.

Certainly a weakening dollar fits with the Federal Reserve Board’s deferring attempts to raise interest rates from the zero bound, and reflects the growing chatter that negative rates cannot be ruled out. It should also interest us that there is evidence the Americans are beginning to take seriously the threats to the dollar’s hegemonic status, and this is no longer just seen as a speculative possibility. …

… For the remainder of the commentary:

https://www.goldmoney.com/decline-of-the-dollar-the-consequences?gmrefco…

end

(courtesy Lawrie Williams/Sharp Pixley)

LAWRIE WILLIAMS: Another 53.4 t gold withdrawn from SGE. YTD 2061.9 t

Oct 23.2015:

We are continuing to monitor Shanghai Gold Exchange withdrawals following the Golden Week holiday and they do seem to be a little down from their peak, but still remain at an impressive 53.4 tonnes delivered in the week ending October 16th – week 40 – the first full week after the holiday. The year to date figure is a fraction short of 2,062 tonnes.

Looking at past years, demand does tend to fall off by a little at this time, but then picks up again as the year-end nears and stocks are built up ahead of the Chinese New Year buying spree. Next year the Chinese New Year – a Monkey year under the Chinese zodiac – falls on Monday February 8th, suggesting strong gold demand in December and January In Chinese astrology, the Monkey is a symbol of health and wealth and those born under the influence of this sign are said to be intelligent, quick-witted and adventurous.

Already the UK’s Royal Mint and Australia’s Perth Mint, in expectation of Chinese gold coin demand, have announced limited edition ‘Monkey’ gold coin mintings aimed at Chinese gift givers.

On the figures to date, we stand by our prediction that Shanghai Gold exchange withdrawals for the full 2015 year will likely reach 2,600 tonnes or more – a huge new record, probably over 400 tonnes more that the previous record year of 2012 when 2,181 tonnes were withdrawn from the Exchange. The year to date figure will probably already surpass last year’s full year total of 2,102 tonnes by the time next week’s SGE figures are announced – and last year was the second highest year ever for SGE withdrawals. Chinese demand, as represented by SGE withdrawals thus remains enormous.

As we have noted before there is considerable disagreement over what actually constitutes Chinese gold demand, with figures calculated by mainstream analysts hugely lower than the SGE withdrawal figures might suggest. The big difference is that the mainstream analysts do not take into account the vast volumes of gold used in internal financial transactions mostly in gold leasing activities.

We recently put forward the viewpoint that a significant proportion of this may be being used by Chinese entities using gold as collateral for obtaining low cost dollar loans and utilising the money so borrowed to take advantage of significantly higher Chinese rates for interest bearing notes. However, according to a presentation at the recent LBMA meeting in Vienna by Jiang Shu, Chief Analyst of the Shandong Group, while this may be true of using iron ore and base metals as such collateral, it was not so true of gold due to export restrictions on bullion, but that huge amounts of gold were indeed tied up in internal gold leasing transactions – and quoted a figure of around 1,370 tonnes so employed. With the analysts not counting this as consumption, this would therefore almost wholly account for the differences between the analysts figures and those of the SGE.

Whichever way you look at this though, this all represents gold flows from West to East, despite which it remains the Comex gold futures market which is largely setting the gold price. But the more and more the Chinese become involved in the nitty-gritty of the gold pricing mechanism the more their influence will rise in determining the actual price given these massive gold flows. Perhaps we will just see the determination of the price by the big money-manipulated Comex futures market replaced by a gold price capable of being manipulated by the Chinese to their own benefit. Whether this would be positive or negative for the gold investor we do not know. However we would err on the side of the former given the huge amounts of gold held by the Chinese public and the moves by the Chinese to switch from an export dominated economy to one which relies on internal domestic demand, which will itself be determined by public wealth.

-END-

Bill Holter tackles something dear to my heart: the fraud inside the comex

(courtesy Bill Holter/Holter-Sinclair collaboration)

The Crime of the Century!

We will no doubt look back upon the current era as the “crime of the century” for so many different reasons. Actually, current times represent the worst financial crimes of ALL TIME! The various crimes and how they are operated are too numerous to list and would probably fill a three volume set of books, let’s concentrate on just one. Central to everything is the U.S. issuing the global reserve currency by fiat knowing full well it truly means “non payment”. The absolute cornerstone to the dollar retaining confidence and thus value has been the suppression of the price of gold.

Before getting to specifically what I’d like to point out, let’s look at a couple common sense points which beg questions. How is it China has been importing 2,400 tons of gold over the past two and a half years without any upward push to the gold price? This amount equals almost EXACTLY the TOTAL amount of gold mined annually around the world! How is it possible that ALL production has been purchased by China and yet the price goes down? The answer of course is quite simple unless you purposely close your eyes or disingenuously “apologize”.

The argument from the apologists is that “traders” on COMEX and LBMA believe gold will go lower so they are sellers and this is where the downward pressure has come from. You as a reader already know that much of the “selling” is done at midnight (or off hours) in the U.S. which is the lunch break in Asia, China specifically. The massive selling (as much as total global production in less than two trading days) has usually taken place during off hours when the volume is lightest and price moves the most, especially with any significant volume. The result has been gold now trades at or very near the cost of production and silver well below production costs. None of this is new, only a refresher. The reaction in the actual physical markets is backwardation, premiums over spot prices and actual shortages. Put simply, low price has brought out additional physical demand.

To the point, the following is a snapshot of inventory movement (or the lack of) within the COMEX gold vaults this month:

Initial standings

Oct 21/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 13 contracts1300 oz |

| No of oz to be served (notices) | 650 contract (65,000 oz) |

| Total monthly oz gold served (contracts) so far this month | 364 contracts

36,400 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 184,991.8 oz |

end

1 Chinese yuan vs USA dollar/yuan rises a tiny bit, this time at 6.3490 Shanghai bourse: in the green, hang sang:green

2 Nikkei closed up 389.43 or 2.11%.

3. Europe stocks all in the green /USA dollar index down to 96.39/Euro up to 1.1095

3b Japan 10 year bond yield: falls to .305% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.73

3c Nikkei now just above 18,000

3d USA/Yen rate now above the important 120 barrier this morning

3e WTI: 45.56 and Brent: 48.44

3f Gold up /Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .499 per cent. German bunds in negative yields from 6 years out

Greece sees its 2 year rate falls to 7.60%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield rises to : 7.77% (yield curve flattening)

3k Gold at $1178.80 /silver $16.05 (8 am est)

3l USA vs Russian rouble; (Russian rouble up 2/3 in roubles/dollar) 61.88

3m oil into the 45dollar handle for WTI and 48 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9740 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0812 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 6 year German bund now in negative territory with the 10 year rising to +.499%/German 6 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.07% early this morning. Thirty year rate below 3% at 2.89% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Continue Surge On Global Draghi Euphoria, Tech Earnings

Yesterday morning, when previewing the day’s tumultuous events, we said that “Futures Are Firm On Hope Draghi Will Give Green Light To BTFD.” And boy did Draghi give a green light, that and then some, when his press conference unleashed one of the biggest one-day US equity rallies in 2015. However we also said that Draghi “faces the paradox of reflexivity“: how does he intervene and demonstrate he is readier than ever to set up stimulus, without panicking investors over euro area’s health because remember: more ECB intervention means Europe’s economy is once again far weaker than consensus admits.

We got the answer to that too when Draghi did absolutely nothing, but merely jawboned to a level unseen since his infamous “whatever it takes” speech in July 2012, sending the EURUSD down by 250 pips on the day on nothing but more cajoling and hints of both boosting or extending QE as well as hinting at NIRP.

And thanks to reflexivity, now that Draghi has achieved his FX goal of pushing EURUSD to the ECB’s stated Euro forecast ceiling of 1.10, he no longer even has to do anything, and most likely won’t in December when the market expects the ECB to unleash savers’ hell. Golf clap.

Confirming that central banks are far more eager to talk than to actually do anything, were comments overnight from that “other” country which is expected to boost QE, Japan, where Etsuro Honda, adviser to Japanese PM Shinzo Abe, said that “immediate additional easing by Bank of Japan is not necessary”, Kyodo reports, citing an interview. Honda says if BOJ carried out additional easing it could be to increase annual JGB purchases to 100t yen from 80t yen; says “next additional easing would be last one.” Of note was his claim that economic measures to aid low income workers was needed due to weak individual consumption; and that fiscal measures are more effective than monetary easing.

Indeed, with the USDJPY surging overnight to 121 on Draghi’s comments, if not actions, suddenly the BOJ too has far less of a reason to act. And, as expected, the USDJPY promptly tumbled down to 120.20 once it became clear that the BOJ, just like the ECB, was merely talking and has no intention to actually act.

Which is why we would not be at all surprised to see absolutely nothing from either the BOJ next Friday, or from the ECB on December 3 – after all the bulk of the FX intervention already took place, and the S&P500 has ramped to just shy of its all time highs once again.

And in fact, following overnight’s glowing PMI data out of Europe, we would also not be at all surprised if Draghi won’t back off entirely from his uber-bearish commentary at the next public statement opportunity he gets, launching a rocket under the EURUSD.

Overnight Marketi reported Euro area flash composite PMI which surprisingly rose 0.4pt to 54.0 in October. This was stronger than consensus expectations of a moderate decline to 53.4. The manufacturing sector PMI was flat at 52.0 (Cons. 51.7), while the services sector PMI increased 0.5pt to 54.2 (Cons. 53.5). At the country level, the German and the French composite PMI made similar robust gains.

The breakdown was mixed. Within the manufacturing PMI, new orders edged down 0.1pt, while stocks of finished goods rose 0.8pt, leading to a 1.0pt reduction in the order-stock difference. Among other subcomponents of the manufacturing PMI, output and employment fell (-0.2pt to 53.3 and -0.6pt to 50.9, respectively). More positively, in services, the forward-looking subcomponents (which are not part of the headline services PMI figure) showed ‘incoming new business’ rising from 53.6 to 54.1, while ‘business expectations’ fell from a high level (-1.2pt to 61.0).

The German composite PMI rose in a similar fashion to the area-wide improvement (+0.5pt to 54.5), reflecting an increase in the services PMI (+1.1pt to 55.2), while the manufacturing PMI fell (-0.6pt to 51.6). The French composite PMI showed similar developments in October (+0.4pt to 52.3), with gains both in the services PMI (+0.4pt to 52.3) and the manufacturing PMI, even if very moderate (+0.1pt to 50.7).

A quick walk through the markets reveals that Asian stocks traded higher in conjunction with gains seen in its global counterparts after ECB President Draghi’s dovish comments. Nikkei 225 (+2.1%) outperformed amid broad based gains with USD/JPY remaining near yesterday’s highs supporting exporters, while ASX 200 (+1.7%) was underpinned by mining names and large banks after NAB and ANZ followed both Westpac and Commonwealth Bank in raising mortgage rates. China’s Shanghai Comp. (+1.3%) benefitted from better property figures, margin debt reaching 6-week highs and reports that China is to increase the amount of funds available to local governments by 100% for infrastructure projects, as an improvement in the property sector is seen to dampen demand for stocks. JGBs tracked Bunds and USTs higher with the paper also supported by the BoJ entering the market to purchase JPY 1.2trl in 1-10yr bonds.

An interesting data point out of China was that September New Home Prices rose in 39 cities vs. 35 in August and in 12 cities Y/Y vs. 9 in August. This was the first time Chinese home prices rose in more than half of 70 major cities in 17 months, driven by mortgage restrictions easing and PBOC rate cuts.

It is very possible that now that China is once again reflating its housing bubble it may allow the stock bubble, which was merely an interim step to hold the economy over for a period of time, to fully burst.

The final European session of the week has kicked off with sentiment continuing on from yesterday as markets continue to digest the dovish press conference from ECB’s Draghi. As such equities (Euro Stoxx: +1.2%) bolstered this morning, while fixed income products experienced initial strength to see yields reach lows across Europe as Italian and Spanish 2y yields go negative for first time, joining German, French, Austrian,

Dutch and Finnish 2yr yields, before Bunds retraced their gains later in the session. While over in equity markets, price action has been bolstered through German automakers (Daimler: 2.0%), who have seen upside today on the back of the weaker EUR.

In FX, EUR/USD spent much of the overnight session trading around the 1.1100 handle after yesterday’s sharp losses, with EUR seeing modest gains ahead of the North American crossover to par some of yesterday’s losses , with sentiment supported by generally better than expected manufacturing and services PMI from France, Germany and the Eurozone (Eurozone Manufacturing PMI 52.0 vs. Exp. 51.). Elsewhere, USD-index (-0.3%) resides in negative territory, weighed on by JPY strength on the back of comments from Japan PM adviser Honda who stated that there is no need for additional easing by the BoJ at this stage.

Of note, as well as initial weakness in EUR, the dovish comments also saw a bout of carry trade and supported countries with higher yields with NZD/USD breaking above 0.6800, coinciding with AUD/NZD retreating below 1.0600. AUD/USD was stronger, although did see some mild paring after NAB and ANZ increased home loan rates, which put pressure for the RBA to act at the November meeting.

Gold prices saw mild support overnight following yesterday’s dovish ECB press conference, although gains were capped by USD strength, however the European morning saw gold move higher, breaking out of its overnight range and eyeing its 200DMA to the upside at USD 1174.59, benefitting from the aforementioned weaker USD. Elsewhere copper and iron ore prices saw mild weakness with the latter near 3-month lows and on course for a 5th weekly loss in 6 weeks, while aluminium prices extended on declines to print its weakest level since 2009. In the commodity complex. WTI and Brent futures both head into US hours modestly higher on the back of USD softness and amid relatively light nesflow.

Looking ahead, highlights include Canadian CPI and US manufacturing PMI. Following yesterday’s tech earnings barrage, today we get P&G, Altera, LyondellBasell Industries, State Street, VF and Ventas.

Market Wrap

- S&P 500 futures up 0.2% to 2057

- Stoxx 600 up 1% to 374

- FTSE 100 up 0.8% to 6425

- DAX up 1.4% to 10639

- S&P GSCI Index up 0.5% to 361.7

- MSCI Asia Pacific up 1.7% to 136

- Nikkei 225 up 2.1% to 18825

- Hang Seng up 1.3% to 23152

- Shanghai Composite up 1.3% to 3412

- S&P/ASX 200 up 1.7% to 5352

- US 10-yr yield up 2bps to 2.05%

- Dollar Index down 0.2% to 96.18

- WTI Crude futures up 0.3% to $45.53

- Brent Futures up 0.7% to $48.41

- Gold spot up 0.6% to $1,173

- German 10Yr yield up 1bp to 0.51%

- Italian 10Yr yield up 2bps to 1.47%

- Spanish 10Yr yield up 2bps to 1.62%

Bulletin Headline Summary from Bloomberg and RanSquawk

- The final European session of the week has kicked off with sentiment continuing on from yesterday as markets continue to digest the dovish press conference from ECB’s Draghi

- USD-index resides in negative territory, weighed on by JPY strength on the back of comments from Japan PM adviser Honda who stated that there is no need for additional easing by the BoJ at this stage

- Looking ahead, highlights include Canadian CPI, US manufacturing PM! as well a host of US earnings including P&G, Altera and LyondellBasell Industries

- Falling Prices Meet Weakening Growth as ECB Prepares for Action: While a PMI for manufacturing and services unexpectedly rose to 54 in Oct. from 53.6 in Sept., forward- looking indicators point to a risk of a slowdown, Markit said

- Treasuries decline as global stocks and commodities extend rally sparked by prospect of more QE from the ECB.

- BOJ Said to See Output Data as Crucial Before Policy Meeting: Sept. industrial production data due a day before the policy board meets on Oct. 30 to consider adjusting monetary stimulus

- While Markit’s euro-area PMI increased to 54 in October from 53.6 the previous month, forward-looking indicators point to a risk of a slowdown, with service-sector expectations for the year ahead fell to a 10-month low

- Jack Dorsey Gives a Third of His Twitter Stock Back to Employees: Shares amount to 1% of the co., worth ~$200m

- A.P. Moeller-Maersk cut its 2015 profit forecast to ~$3.4b vs previous expectations for $4b, citing weaker container shipping market as the outlook for global growth becomes gloomier

- With oil prices still wobbling around $50, Norway is in danger of a recession that could drive its benchmark interest rates, already at a record low, to zero

- China’s home prices rose in September in more than half of the 70 major cities monitored by the government for the first time in 17 months, as home-purchase restrictions were loosened and interest rates cut

- The towns that became synonymous with Volkswagen AG’s rise to the pinnacle of the auto industry are feeling the pinch of the diesel-emissions scandal, freezing spending on projects such as playgrounds amid the carmaker’s abrupt fall from grace

- Merkel is signaling to Putin that she’ll stand firm on defending Ukraine, even at the risk of denying herself a possible ally in stemming Europe’s refugee crisis

- Sovereign 10Y bond yields mixed. Asian and European stocks gain, U.S. equity-index futures rise. Crude oil, copper and gold higher

DB’s Jim Reid completes the overnight recap

With the new James Bond film opening on Monday and continuing the film theme in the EMR this week I felt I had to share my own personal Bond anecdote. In 1998 I lived in Wapping and walked to work in Canary Wharf by a canal. One day I walked home to find a new small boat house installed alongside the canal with canoes in it and London Canoe Club painted on the entrance. I was quite excited and made a note that I was going to come back at the weekend to join the new club. Not that I had ever done it before but I was still at an age where trying new things once was still exciting! I didn’t go back past for a couple of days as I was travelling but on my return at the weekend the boats and clubhouse were completely gone with no trace they ever existed. Part of me thought I’d gone crazy and part of me wondered whether there wasn’t enough interest and they had decided against setting up there. I therefore regretted not joining immediately. I thought little of it for the next year and then I went to the cinema to see “The World is Not Enough”. Imagine my surprise when in the movie James Bond drove a speedboat at high speed into the London Canoe Club sending boats and the building scattered everywhere. Only then did I realise what had happened.

Yesterday Mario Draghi gave the financial community licence to be thrilled as he ended up shaking and stirring markets with the Stoxx 600 (+2.03%) closing at a 2-month high. It’s been pretty obvious to us that with inflation so low, the ECB and BoJ have plenty of excuse to give the plates another big spin and expand current monetary policy further and thus give assets another dose of supportive fairy dust. Whilst we didn’t expect action yesterday from the ECB its fair to say we got more certainty than we would have expected that the December 3rd meeting is set to yield more stimulus. As a result our economists have amended their QE extension call and included a small (10bps) further deposit rate cut into their forecasts. They think such a small cut might now risk market disappointment but this will be compensated by signalling that the lower bound has not yet been reached.

Digging deeper into Draghi’s comments. Concerns over growth prospects in emerging markets, as well as possible repercussions for the economy from developments in financial and commodity markets were well flagged as downside risks for the outlook for growth and inflation for the Euro area. On inflation, Draghi warned that ‘most notably, the strength and persistence of the factors that are currently slowing the return of inflation to levels below, but close to, 2% in the medium term require thorough analysis’.

With this, Draghi said that ‘the degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting’. Also ‘the Governing Council is willing and able to act by using all the instruments available within its mandate’ and that in particular ‘the asset purchase programme provides sufficient flexibility in terms of adjusting its size, composition and duration’. Interestingly and as highlighted by our European economists, Draghi also used his predecessor code word ‘vigilance’ that previously had used to signal imminent action.

European equity markets were up across the board. The DAX (+2.48%), CAC (+2.28%), IBEX (+2.05%) and FTSE MIB (+2.00%) all with gains of at least 2%. Unsurprisingly the Euro was heavy hit and finished down 2.03% against the Dollar, the lowest closing level since August 18th. Credit markets got a boost with Crossover and Main 14bps and 4bps tighter respectively. Meanwhile European sovereign bond yields marched lower. Peripherals were the relative outperformer with 10y yields in Italy, Spain and Portugal dropping 15.6bps, 15.6bps and 12.7bps respectively. 10y Bunds ended the session down 7.3bps at 0.494%, the lowest yield since May 29th. There were some decent moves at the shorter end of the curve too. Having declined over 6bps, 2y Bund yields finished down at -0.320% and the lowest level on record, while the Bund curve has moved back into negative territory again up to 6yrs in maturity.

Draghi’s comments helped boost equity markets across the pond too. The S&P 500 closed up +1.66% while the Dow and Nasdaq ended +1.87% and +1.65% despite some more weakness in the healthcare space after Valeant fell another 7%. Some productive earnings reports also helped much of the better tone in the US. After reporting post the closing bell on Wednesday, EBay surged 14% yesterday. Meanwhile, during the day investors were also buoyed by earnings beats for McDonalds (+8%), Dow Chemical (+5%) and 3M (+4%) during the session. Better news was to come after the close however with some material beats from a few bellwethers in the tech space. Microsoft shares surged to a 15-year high in extending trading after earnings came in above expectations, bouncing back strongly from one of its worst losses in history last quarter. Amazon shares jumped as much as 11% after the close, notching a beat in both earnings and sales for the quarter after some robust performance in its cloud-computing division. Finally Google parent company Alphabet was also up double digits in extended trading after beating profit expectations and announcing the group’s first share buyback.

Updating our beat/miss monitor then, yesterday saw 45 S&P 500 companies release results with 34 (76%) reporting a beat in earnings but just 19 (42%) beating at the top-line. While yesterday’s beat ratio in earnings was a touch better than what we’ve seen this earnings season so far (75%), the trend in beats for the top-line was slightly worse than the overall trend so far, currently sitting at 45%. It’s quite clear from the earnings season so far that revenues are struggling more than EPS relative to expectations. This has been the case for many quarters now but seems to be especially so this season.

Just staying on earnings, Caterpillar’s numbers are always worth keeping an eye on with regards to insights in global demand and commodity and investment cycles. Earnings came in a tad below expectations with revenue declines across construction and resources industries. Regionally the biggest declines were in Latin America and Asia Pacific, with mention of declining demand out of China. The company’s outlook was mixed. Profit guidance was revised down for 2015, while revenues are expected to decline 5%. The company did however suggest that they expect world economic growth to be up next year, from 2.4% this year to 2.8% in 2016 with growth in the US and Europe offsetting slower growth in China and Russia. They do however expect key commodity prices to remain largely unchanged.

The prospect of more ECB stimulus is supporting a decent session in Asia this morning. The Nikkei (+2.20%), Hang Seng (+1.34%), Kospi (+0.79%) and ASX (+1.67%) have all moved higher. Markets in Korea have also been buoyed by better than expected GDP data this morning. Credit markets have rallied strongly. Asia and Australia iTraxx indices are 5bps and 4.5bps tighter respectively. EM FX is off to a flyer too. In particular, currencies in Malaysia, Korea and Indonesia are up over a percent in early trading. Meanwhile, equity bourses in China are seemingly trading to their own beat. Both the Shanghai Comp (+0.02%) and CSI 300 (+0.00%) are little moved, but the Shenzhen (+0.93%) has seen a decent gain. September house price data in China showed prices were up in 39 cities last month (out of 70) versus August. This is the first time in 17 month prices have risen in more than half of Chinese cities. This compared to the previous two months when house prices rose in 35 cities in August and 31 cities in July. Elsewhere, S&P 500 (+0.2%) and Nasdaq (+0.4%) futures are pointing towards to decent start post last night’s earnings.

Just wrapping up yesterday, economic data was relatively mixed on the whole in the US. Initial jobless rose 3k to 259k (vs. 265k expected) last week. The Conference Board’s leading index was down a slightly softer than expected -0.2% mom (vs. -0.1% expected) last month. There was some improvement in the Kansas City Fed’s manufacturing activity index during October however, rising 7pts to -1 (vs. -9 expected) and to the highest level since February. The Chicago Fed’s national activity index was a touch below market (-0.37 vs. -0.29 expected), albeit more or less in line with last month. Meanwhile, on the housing front existing home sales were up a robust +4.7% mom (vs. +1.5% expected) in September, the annualized rate of 5.55m just below the 8-year high of July.

Prior to this in Europe, French business confidence rose 1pt to 101 (vs. 100 expected) in October, while an indicator of manufacturing confidence was a touch softer relative to last month. UK retail sales data was supportive. Excluding autos, retail sales rose +1.7% mom in September (vs. +0.4% expected) helping to lift the YoY rate to +5.9%.

Onto today’s calendar now. Economic data today is dominated by the release of the October flash PMI’s where we’ll get the manufacturing, services and composite readings for the Euro area, France and Germany and the manufacturing print in the US this afternoon. With no Fedspeak scheduled again today, corporate earnings will again be closely watched with 10 S&P 500 companies due to release results, including Procter & Gamble and American Airlines (both due before the open). 16 Stoxx 600 companies will report also, including Volvo and Ericsson.

ASIAN AFFAIRS

Let us begin; 9;30 pm Thursday night/9;30 Friday am Shanghai time)

US Dollar Dumped Against Asian FX As Releveraging Chinese Send Margin-Debt To 6-Week Highs

Chinese stocks are not as exuberant as European, Japanese (which are rolling over), and US markets at the open as they cling to unchanged for the day and week(despite margin debt rising to a six-week high). The main event in AsiaPac trading appears to be a huge re-entry into the EUR-ANY-EM-FX carry trade as The USDollar gets pummeled against Asian FX (despite EUR weakness). PBOC weakened the Yuan fix by the most in 8 days to its lowest in 2 weeks.

Japanese stocks soared during the US session but are fading at the open…

Chinese stocks flat in the pre-open…

Even as Margin Debt hits a 6-week high...

As The Dollar gets pummeled against Asian FX...

and PBOC weakens the Yuan Fix…

With Offshore Yuan pushing to 1-month lows...

Finally, it’s almost as if China never shook up the world’s carry trading malarkey… only Chinese stocks are still feeling the pain…

Charts: Bloomberg

Breaking: China Cuts Interest Rate By 25 bps, Cuts RRR by 50 bps; Futures Soar; Fed December Rate Hike Back In Play

Just two days ago, we noted that according to Citi’s Willem Buiter, there would be “Imminent Easing From Central Banks Of China, Australia, Japan And Europe.” Fast forward 48 hours when he is already half right – not only did Europe confirm it is about to cut, but moments ago none other than China joined the global easing orgy when in a completely unexpected development as it happened on a Friday (we are scouring various databases to find the last time, if ever this happened) China announced it has cut not only its 1 year lending rate and 1 year deposit rate by 25 bps, but also its reserve requirement ratio by 50 bps.

- CHINA CUTS BANKS’ RESERVE REQUIREMENT RATIO

- CHINA CUTS INTEREST RATES

- CHINA CUTS 1-YEAR LENDING RATE BY 0.25 PPT

- CHINA CUTS 1-YEAR DEPOSIT RATE BY 0.25 PPT

- CHINA REMOVES DEPOSIT RATE CEILING FOR BANKS

- CHINA CUTS RESERVE RATIO BY 0.5 PPT

- CHINA INTEREST RATE CUT EFFECTIVE FROM OCT. 24

The PBOC’s statement in its google-translated entirety:

People’s Bank of China, from October 24, 2015, down financial institutions RMB benchmark lending and deposit interest rates, in order to further reduce the social cost of financing. Among them, one-year benchmark lending rate by 0.25 percentage point to 4.35%; year benchmark deposit rate by 0.25 percentage point to 1.5%; adjusted for each other grade benchmark interest rate loans and deposits, the People’s Bank lending rates of financial institutions ; personal housing accumulation fund loan interest rates remain unchanged. Meanwhile, commercial banks and rural cooperative financial institutions are no longer set the upper limit of the floating interest rates on deposits, and pay close attention to improve the market-oriented interest rate formation and regulation mechanism, strengthen the central bank interest rate system of regulation and supervision, improve the efficiency of monetary policy transmission.

Since the same date, down financial institutions RMB deposit reserve ratio by 0.5 percentage points, in order to maintain reasonably adequate liquidity in the banking system, guide steady moderate growth of money and credit. Meanwhile, to increase financial support for the “three rural” and small businesses a positive incentive for additional standards-compliant financial institutions to reduce the deposit reserve ratio by 0.5 percentage points. (Finish)

S&P futures surge nearly 20 points on this latest scramble to ease, which is just the latest green light by central banks to take on more risk, and as a result fresh all-time highs in the S&P500 are now just a matter of time.

But the real take home message here is that both the ECB and the PBOC just confirmed a December Fed rate hike is suddenly in play once again, especially since this move by China should remove Yellen’s concerns about Chinese growth.

end

Initial reaction:

China Rate Cut Reaction – Bullion Best, Bonds Bruised, Exuberance Everywhere Else

For now, the biggest loser is Treasury bonds – which are up 2-4bps in yields post-China. As for everything else – buy it with both hands and feet. US equities are extending tech gains (Nasdaq up 3% post-cash close), Gold has surged back above its 200DMA, Commodities are all loving it and the USD is bid…

The last two days have been quite impresive…

US Equities are exuberant…

As VXX tumbles over 3% in the pre-market (heralding 13 handle VIX today)

But bonds are suffering as gold leads the reaction

With gold breaking back above its 200-day moving-average…

Europe is loving it too… DAX +300 today, +600 in 2 days

Credit markets are higher, but remain notably decoupled from equity exuberance…

Charts: Bloomberg

Reactions To China Rate Cut Trickle In: “China Is Getting More And More Desperate”

To say that China, which a few days ago reported GDP of 6.9% which “beat” expectations and which a few hours ago reported Chinese home prices rose in more than half of tracked cities for the first time in 17 months, stunned everyone with its rate cut on Friday night, meant clearly for the benefit of US stocks, as well as the global commodity market, is an understatement: nobody expected this.

As a result strategists have been scrambling to put China’s 6th rate cut in the past year (one taking place just ahead of this weekend’s Fifth plenum) in context. Here are the first responses we have seen this morning.

First, from Vikas Gupta, executive vice president at Mumbai-based Arthveda Fund Management Pvt., who told Bloomberg that “China rate cut will spur fund flows to EMs.” He adds that “the move rules out U.S. rate increase this yr; Fed’s “hands are getting tied” concluding that “easing shows China is “getting more and more desperate” and that “things are really bad there.“

While there is no debate on just how bad things in China are, one can disagree that the Fed’s hands are tied – after all the Fed’s biggest “global” concern was China. The PBOC should have just taken that concern off the table.

The second reaction comes from Citi’s Richard Cochinos:

Bottom line: Impacts of China rate announcements on the G10 are falling. Investors remain cautious ahead of this weekend’s announcements, and what policy cuts imply for the region.

One day after a dovish ECB, China cuts interest rates by 25bp and RRR cut by 50bps.Accommodative policy begets accommodative policy it seems. Our economics team has been expecting further policy accommodation out of China, the issue was just a matter of timing. Unlike other major central banks, the PBOC doesn’t announce policy on a set schedule – but this doesn’t mean there isn’t a pattern to it. Before today, it had announced cuts to the RRR or interest rate six times in 2015 – the last being on 25 August. So today was a surprise in terms of action, but not completely unexpected. We prefer to see the easing can be seen in the larger picture of China adjusting to weaker growth in a systematic and controlled manner, rather than a reaction to a new economic shock.

This view helps explain the muted reaction in the G10. So far, AUDUSD (0.27%) and USDJPY (0.18%) have borne the bulk of price action, but we note price action so far is muted relative to April, June or August. Clearly stimulus is beneficial to both Japan and Australia – but we are cautious not to sound too optimistic.Today’s rate cut comes ahead of this weekend’s Fifth plenum, and previous ones haven’t been sufficient to reverse the economic slowdown. Additionally, this weekend it has been expected GDP targets for the next 5-years will be announced (currently at 7%, but broadly expected to fall), along with other fiscal plans and goals. Without knowing the full baseline of what China expects and is working towards, it is difficult to chase price action. The main drivers of EM Asia lower has been poor growth and trade in the region – hence we main cautious. Policy adjustments now could be a way to soften the impact of further weak economic growth.

And finally, from MarketNews:

The PBOC will cut its key one-year lending rate by 25 basis points to 4.35%, the bank said on its website, and make a similar reduction to its one-year deposit rate, taking it to 1.5%. Reserve ratio requirements for China’s domestic lenders were also trimmed by 50 basis points and the PBOC abolished a ceiling on banks’ deposit rates, the so-called final step of China’s interest rate reform.

The triple-set of moves provides a much better assessment of the impending weakness in China’s economy, it seems, than the various indicators scrutinized in Europe over the past few weeks, which continue to suggest minimal impact from the slowdown.

They may also better explain the surprisingly dovish stance articulated Thursday by ECB President Mario Draghi, who emphatically flung the door to further monetary easing measures wide open and suggested the Bank might even consider a re-think of its “lower bound” assessment on key interest rates.

And therein lies the question: just how bad are things in China (and Europe for that matter) for the PBOC to act (and the ECB to hint) with the urgency of a world hanging on the edge of a global recession. We’ll find out next Friday when the BOJ become the third bank to join the global easing train.

end

Commodities, Precious Metals Are Tumbling – Give Up China Rate-Cut “Hope” Gains & More

That’s not supposed to happen…

If rate cuts create “growth” and stocks are discounting that “growth” then why are “growth”-oriented commodities dumping?

Or did China just admit by action that its economy is much more screwed-er than its GDP data suggests…?

Crude even lower no – 2 month lows…

Charts: Bloomberg

end

Then this: the market intervention lasts only 4 hours. The new equity owners of stock looked over their shoulder and saw bond yields falling and not rising which caused them to shiver!!

(courtesy zero hedge)

Peak Intervention? China Rate-Cut Stock Gains Erased In Under 4 Hours

Did the age of central bank omnipotence just come to an end?

After 3 USDJPY driven rescues, the China Cut gains are gone for the S&P 500…

Of course, from the close yesterday, markets are still holding gains…

Even as VXX surges back into the green

Maybe stock traders glanced at the un-exuberance in credit markets…

Charts: Bloomberg

end

This story is a biggy!!

The IMF is seen as approving the yuan as a reserve currency.. The meeting is set for the first week of November.

As you can see, the offshore yuan is falling as dollars continue to vacate China

(courtesy zero hedge)

IMF Seen Approving Yuan As “Reserve Currency”

Just a few short weeks after The IMF appeared to snub China by delaying its decision on Yuan inclusion in the SDR basket, Bloomberg reports that Otaviano Canuto, executive director at the IMF for 11 countries including Brazil, said “prospects for approval seem to be favorable,” adding that the story “is going in the direction of the renminbi becoming a necessary component of the SDR.” China is taking that as a ‘yes’ and is preparing statements celebrating IMF SDR approval.

As Bloomberg reports,

International Monetary Fund representatives have told China that yuan is likely to join the fund’s basket of reserve currencies soon, according to Chinese officials with knowledge of the matter.

IMF has given Chinese officials strong signals in meetings that yuan is likely to win inclusion in current review of Special Drawing Rights, said three people who asked not to be identified because talks were private

Chinese officials are so confident of winning approval that they have begun preparing statements to celebrate the decision, according to two people

Board has requested that IMF staff members look into some operational challenges of including yuan in the basket, such as ability of fund’s 188 member nations to quickly convert SDRs into yuan, according to another person familiar with the matter.

“We realize that although we’ve done a lot, it’s really first up to the staff, and second up to the board, to make a final judgment,” Jin Zhongxia, China’s representative to the IMF executive board, said in interview Friday. “We have to fully respect their decision”

Of course, as one analyst notes, “I think a political decision has already been made,” said Domenico Lombardi, director of the global economy program at the Centre for International Governance Innovation in Waterloo, Ontario.

“The Chinese have invested considerable political capital. They’ve mobilized their intellectual and political resources to this purpose, and it’s a case that’s difficult to argue against.”

“The most probable outcome is the board will vote to include the renminbi in the SDR basket,” said Meg Lundsager, who served as the U.S. representative on the IMF’s executive board from 2007 to 2014. “I really haven’t heard any big opposition. If there were countries which had real problems with it, they would have been raising their concerns.”

The U.S. took a step toward backing China’s SDR bid last month, when it softened its insistence that the Chinese implement financial reforms to win support. The U.S. now says it will support inclusion of the yuan if it demonstrates it meets the IMF’s technical criteria.

“This is going to make it very hard for the Chinese to undo a lot of these reforms,”said Lundsager, now a public-policy fellow at the Woodrow Wilson International Center for Scholars in Washington. “Once you move into this group of major currencies, it becomes pretty much impossible to backslide.”

* * *

The bottom line is that this appears bearish for The Yuan… and likely means more outflows…

Several days ago, Citi announced that it “expects the upcoming IMF review (scheduled for early-November) will probably lead to China’s inclusion in the SDR basket from late-2016. But we expect that the CNY will over time weaken versus the USD either way — either because of a poor outcome from SDR review or (if China joins the SDR) because of gradual (and limited) FX liberalization.“

which is fascinating as China’s offshore Yuan has plunged to 1-month lows in the last few days…(and decoupled – for now – from the onshore market suggesting outflows are accelerating)

While it remains to be seen just how negative the impact on the CNY will be as a result of any possible SDR inclusion, and the definition of China’s currency as a reserve currency, it now appears virtually assured that the IMF will include the CNY in its SDR basket, “validating efforts by President Xi Jinping to push through policies aimed at making the world’s second-biggest economy more market oriented, boosting China’s prestige as it prepares to host Group of 20 gatherings next year.”

EUROPEAN AFFAIRS

Draghi announced that NIRP was discussed in yesterday’s Euro area banking meeting. Once Europe plunges into negative rates, the Euro/Swiss Franc cross will plummet causing more havoc to the Swissy. Coupled with today’s announcement by the Chinese, the world is now in total turmoil and a race to the bottom

(courtesy zero hedge)

Why Europe Is About To Plunge Further Into The NIRP Twilight Zone, And What It Means For Depositors

In some respects, today’s ECB presser was a snoozer. Reporters asked the same old questions (some of which we’ve been asking for years) and, more importantly, there were no glitter attacks.

Our ears did perk up however, when Mario Draghi admitted that, unlike the governing council’s last meeting, cutting the depo rate further into negative territory was indeed discussed.

This is significant for a number of reasons. At the general level, it shows that DM central bankers are ready and willing to plunge the world further into the Keynesian Twilight Zone. As we outlined last month, this means the Riksbank and the SNB are now on watch. If the ECB cuts again, the Riksbank will be forced to act as well and as Barclays recently opined, the SNB may be compelled to go nuclear on depositors, as removing the negative rate exemption for domestic banks would force them to pass along the “cost” to customers:

“In contrast, a cut in the ECB’s deposit rate further into negative territory likely would have a significant impact on the EURCHF exchange rate and provoke a more immediate response from the SNB.Indeed, we expect that a cut in the ECB’s deposit rate may have a greater effect on EURCHF than on other EUR crosses. Switzerland applies its negative deposit rate to only a fraction of reserves, currently about 1/3rd of sight deposits by our calculation. In contrast, negative deposit rates apply to all reserves held at the ECB, Riksbank and Denmark’s Nationalbank. Consequently, a cut to the ECB’s deposit rate likely has a larger impact both on the economy and on the exchange rate than a proportionate cut by the SNB. An SNB response to an ECB deposit rate cut could take one of two forms: 1) a further cut in its deposit rate and CHF Libor target range; or 2) the ‘nuclear’ option, removing all exemptions from the negative deposit rate. We think the latter is more likely and would have major implications for EURCHF.” Most retail (private) depositors at domestic Swiss banks still do not face negative interest rates, but we would expect that to change if the SNB removed exemptions of domestic banks on sight deposits at the SNB. A removal of domestic banks’ exemption from negative deposit rates likely would force Swiss banks to pass on negative deposit rates as it would increase the proportion of assets charged negative rates to over 20%.

This is an important concept not only for what it says about the never-ending, tit-for-tat, beggar- thy-neighbor monetary policies that now pervade developed markets, but also for the degree to which it explains why NIRP has not yet led to a sharp increase in the demand for physical banknotes. Put simply: depositors haven’t yet felt the effects of the monetary insanity engendered by the global currency wars.

Deutsche Bank’s Abhishek Singhania and Oliver Harvey have taken a close look at the proliferation of NIRP at the Riksbank, the SNB, the Nationalbank, and the ECB on the way to positing that not only is zero not the lower bound, but in fact no one has hit the lower limit for rates as of yet.

First, there’s the obvious problem with negative rates. Namely, depositors will just take it to the mattresses (so to speak):

The main concern with further cuts to policy rates is the problem of the zero lower bound. In academic literature, the challenge for central banks operating near or at zero interest rates is that it is technically unfeasible to impose interest rates on cash. Depositors charged at negative rates can simply exchange electronic reserves into paper currency.

Of course because fractional reserve banking is nothing more than a giant ponzi scheme wherein banks are perpetually borrowing short to lend long, instituting a rate negative enough to trigger a run on deposits would have the exact opposite effect from what central banks intended. That is, banks would be forced to sell assets to meet the outflows:

As well as losing control over monetary policy, central banks would see financial conditions tighten as banks were forced to sell assets to meet depositor withdrawals. In extremis, the effect could be compared to a bank-run preceding capital controls or large scale currency devaluation. However, due to the more incremental nature of the impact of negative rates (e.g. 25bp charge on deposit holdings rather than a multi percent devaluation), interest rates would need to be slashed deeply negative for depositor withdrawals to resemble much more than a jog.

Obviously, if rates go negative enough to trigger a run that (literally) breaks the banks, then the lower limit will definitively have been reached, but at that point it will be too late. Back to Deutsche Bank:

So far, the experiences of the four European economies under negative interest rates, including the Eurozone, suggest that this theoretical constraint has not been reached. The demand for coins and notes has ticked up slightly in recent months, but remains at fairly muted levels.

Why the lower bound constraint has yet to be reached, and how much more room there is to maneuver, is obviously crucial for the ECB and the three other central banks imposing negative rates. The main reason is that banks have not passed on negative policy rates to depositors. In none of the four economies are household deposit rates in negative territory, either for outstanding balances or new business. Why have negative nominal rates not passed through to depositors?

Banks are of course hesitant to charge depositors for deposits for fear of damaging relationships. Or, in Deutsche Bank’s more condescending parlance, “banks are very reluctant to pass on negative rates to households [because] retail depositors [are] least likely to understand the wider monetary policy context behind such a decision.” Right, they aren’t likely to understand why they should have to pay the bank to lend out their money at a spread that nets the bank a profit and the reason they aren’t likely to understand it is because, frankly, it makes absolutely no sense.

But the bank has to preserve its margins. With long-end rates falling on the asset side thanks to unconventional monetary policy, you either have to pass that along by reducing the rate you pay on your liabilities (i.e. deposits) or else your margins are going to get pinched – unless you find some other way to make up the difference, that is.

The indirect cost of negative rates for banks is through margins. In theory, as unconventional monetary policy pushes down yields on the asset side of the balance sheet, banks need to cut rates on the liability side to preserve margins. As banks are reluctant to cut deposit rates into negative territory for the reasons above, their net interest margin may suffer.

Right. So what’s the solution if it’s not passing along NIRP to depositors?

The SNB have noted that the consequence of introducing negative rates earlier this year was rising, not falling, mortgage rates as banks sought to protect falling liability margins by raising long-end rates. In a similar vein, Danish banks appeared to raise administration fees on new mortgages after rates first turned negative back in 2012. An analysis of long-end mortgage rates offered by banks across Sweden, Denmark and Switzerland suggests that at the long-end, rates have actually risen since the introduction of negative interest rates.

Got that? NIRP is paradoxically causing mortgage rates to rise because banks fear a depositor backlash from negative rates. So, this is yet another example of the unintended consequences of unconventional monetary policy.

We saw something akin to this in Sweden back in July when the Riksbank had sucked up so much high quality collateral via QE that the liquidity premium demanded by investors ended up pushing yields on 10-year govieshigher in what amounted to the exact opposite of what the central bank intended.

Note once again that there’s no end to this. If the ECB cuts the depo rate further, then other NIRP countries will have to respond. If they don’t, their currencies will soar, threatening inflation targets. Case in point, from this morning:

This means going deeper into NIRP, which, in light of the above, means rising borrowing costs right up until the breaking point when the hit to margins can no longer be offset. At that juncture, NIRP will have to be passed on to depositors lest NIM should simply flatline.

What happens next is anyone’s guess but if depositors revolt and begin asking for their money back, banks’ maturity mismatched business model means there are only three available options, i) sell assets to meet withdrawals, ii) institute capital controls, or iii) ban cash. Welcome to the future.

end

The first nation to undergo NIRP was Denmark. Just take a look at its new huge housing bubble. Home prices have risen 60% in 3 years.

(courtesy zero hedge)

This Is What Happens After Three Years Of Negative Interest Rates

It may seem extraordinary that in the aftermath of the infamous Kocherlakota “dots” the Fed is actively contemplating negative interest rates, but some may have forgotten that Europe has had NIRP since last June. In fact, the reason for today’s global risk-on rally, was Draghi’s hint – remember: Draghi did absolutely nothing, just suggested he may do more – that in addition to extending the ECB’s QE program, the ECB may cut its deposit rate, already at -0.20%, to -0.30% or more.

But when it comes to negative rates, the ECB is merely a late adopter. For the real pioneer one has to look further north in Denmark, where the central bank first adopted negative rates in the middle of 2012 to defend the krone’s peg to the Euro. And, as documented here before, Denmark cut rates not once, not twice, but three times in early 2015 in anticipation of the EUR collapse, pushing its interest rate to a record negative -0.75%.

Denmark’s descent into NIRPdom is shown in the Bloomberg chart below.

So what happens after 3 years of NIRP?

Well, according to Bloomberg, you get the mother of all housing bubbles, one which makes even China blush:

“Property prices in Copenhagen have risen 40-60 percent since the middle of 2012, when the central bank first resorted to negative interest rates to defend the krone’s peg to the euro.”

This should come as no surprise: recall that there are documented cases where Danish borrowers are paid to take on debt and buy houses as we explained in January in “In Denmark You Are Now Paid To Take Out A Mortgage“, so between rewarding debtors and punishing savers, this outcome is hardly shocking. Yet it is the negative rates that have made this unprecedented surge in home prices feel relatively benign on broader price levels, since the source of housing funds is not savings but cash, usually cash belonging to the bank.

What is disturbing is that Denmark is reflating a gargantuan housing bubble less than 7 years since its last housing bubble popped: