Gold: $1166.80 down $0.20 (comex closing time)

Silver $15.86 down 4 cents

In the access market 5:15 pm

Gold $1166.80

Silver: $15.87

We are now entering options expiry week: EXPECT GOLD AND SILVER PRICES TO BE SUBDUED FOR THE REST OF THE WEEK

for the Comex gold and silver: OPTIONS EXPIRE tonight Oct 27.

for the LBMA contracts: OPTIONS EXPIRE ON Friday/Oct 30

for OTC contracts:OPTIONS EXPIRE ON Friday Oct 30.

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very good delivery day, registering 38 notices for 3800 ounces Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 208.51 tonnes for a loss of 94 tonnes over that period.

In silver, the open interest rose by 268 contracts as silver was up 8 cents. The total silver OI now rests at 169,879 contracts In ounces, the OI is still represented by .850 billion oz or 121% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose by a considerable 1,229 to reach 469,097 contracts. We had 38 notices filed for 3800 oz today.

We had no change in gold inventory at the GLD / thus the inventory rests tonight at 695.54 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver,no change in silver inventory / Inventory rests at 315.553 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver rose by 268 contracts up to 169,879 as silver was up 8 cents with respect to Monday’s trading. The total OI for gold rose by 1229 contracts to 469,097 contracts as gold was up $3.70 yesterday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

iv) And this is probably what China will do with respect to the USA transgression according to newspaper China’s Global Times

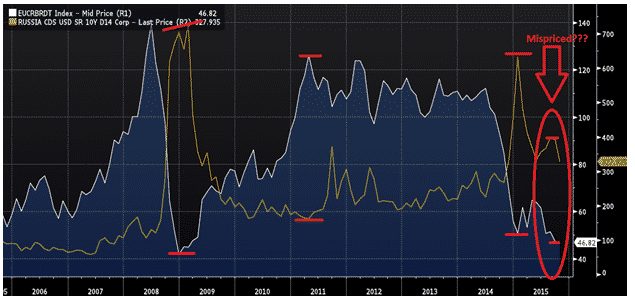

iii) An excellent scholar on Russian affairs, Marin Katusa writes that it is quite possible for a Russian default: why? a default will not hurt them but only hurt the west:

iii ) Oil jumps a bit at the end of the day despite higher ATI inventory build

(zero hedge)

9 USA stories/Trading of equities NY

i) Durable goods orders tumble for the 6th month in a row

(zero hedge)

ii) Case Shiller home prices remain stagnant for the past 6 months at 5% rise. San Francisco continues to lead home prices higher.

(Case Shiller/zero hedge)

iii) USA service index falls the most since January 2015

(zero hedge)

iv) USA consumer confidence drops to 3 month lows despite the higher stock market and lower gas prices

(zero hedge)

v) Sam Zell sells 23,000 apartments in the USA or 25% of his portfolio indicating a top

(zero hedge)

vi Rent a center stock plummeting: If we are starting to witness trouble in the secondary smart phone sector, you know that the economy is falling into an abyss!!

(courtesy zero hedge)

vii More troubles for Valeant as it was hit with a downgrade warning by S and P. These guys did their acquisitions through debt and that debt totals 30 billion USA. A downgrade will force them to delever exactly like Glencore.

(courtesy zero hedge)

10. Physical stories

i) John Embry discusses gold and China’s huge banking problems together with huge amounts of accumulated debt (public and private)

(Kingworldnews/John Embry/Kingworldnews)

ii) James Turk discusses how central banks destroy capital. However due to the fragility in finances around the world, the uSA cannot raise rates.

(James Turk/Kingworldnews/GATA)

iii) Craig Hemke of TFMetals, reports that due to the high amount of net short position by the commercials expect a raid on our precious metals such that the bankers can cover. Also expect subdued pricing on gold and silver due to options expiry this week

(Craig Hemke/TFMetals)

iv) Lars Schall and Chris Powell on how central bankers refuse to tell how they secretly intervene in the gold market

(Lars Schall/Chris Powell/GATA)

v) Bill Holter’s commentary for today is entitled: “Respected Like a Banana Republic?

Let us head over to the comex:

October contract month:

Initial standings

Oct 27/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 300.245 oz

Delaware |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 38 contracts

3800 oz |

| No of oz to be served (notices) | 425 contract (42,500 oz) |

| Total monthly oz gold served (contracts) so far this month | 525 contracts

52,500 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 185,291.0 oz |

Total customer deposit nil oz

we had 0 adjustment:

October silver Initial standings

Oct 27/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 461,791.440 oz

Delaware,Scotia |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 0 contract (nil oz) |

| No of oz to be served (notices) | 4 contracts (20,000 oz) |

| Total monthly oz silver served (contracts) | 85 contracts (425,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 10,373,722.8 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: nil oz

total withdrawals from customer: 461,791.44 oz

And now SLV

Oct 27/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 26/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 23./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 22./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 21:a we had a small addition in silver ETF inventory of 381,000 oz/inventory rests tonight at 315.533 million oz

Oct 20.2015/ no change in silver ETF/Inventory rests at 315.152 million oz

Oct 19.2016: no change in silver ETF/Inventory rests at 315.152 million oz

Oct 16/no change in silver ETF/inventory rests tonight at 315.152 million oz

Oct 15./no change in silver ETF inventory/rests tonight at 315.152

Oct 14/no change in silver ETF/silver inventory/rests tonight at 315.152 million oz

oct 13/no change in silver ETF /silver inventory/rests tonight at 315.152 million oz

:oct 12/ no change in the silver ETF/silver inventory rests tonight at 315.152 million oz

Press Release OCT 6.2015

Sprott Increases Offer for Central GoldTrust and Silver Bullion Trust

Offering an Additional Premium of US$0.10 per GTU Unit payable in Sprott Physical Gold Trust Units

and US$0.025 per SBT Unit payable in Sprott Physical Silver Trust Units

When Announced on April 23, 2015, Offers Represented a Premium of US$3.06 per GTU Unit and US$0.91 per SBT Unit for Unitholders Based on Trading Value and the NAV to NAV Exchange Ratio

Premiums as of October 5, 2015 (including the Increased Consideration) are US$1.14 per GTU Unit and US$0.61 per SBT Unit

Notice of Extension and Variation to be Filed Shortly

Offers Will Now Expire on October 30, 2015 –Unitholders Urged to Tender Now

TORONTO, Oct. 6, 2015 (GLOBE NEWSWIRE) — Sprott Asset Management LP (“Sprott” or “Sprott Asset Management”), together with Sprott Physical Gold Trust (NYSE:PHYS) (TSX:PHY.U) and Sprott Physical Silver Trust (NYSE:PSLV) (TSX:PHS.U) (together the “Sprott Physical Trusts”), today announced that it has increased the consideration payable to unitholders in connection with its offers to acquire all of the outstanding units of Central GoldTrust (“GTU”) (TSX:GTU.UN) (TSX:GTU.U) (NYSEMKT:GTU) and Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (TSX:SBT.U) (the “Sprott offers”).

Unitholders will now receive an additional premium of US$0.10 per GTU unit payable in Sprott Physical Gold Trust units and US$0.025 per SBT unit payable in Sprott Physical Silver Trust units (the “Premium Consideration”), in addition to the units of Sprott Physical Gold Trust and units of Sprott Physical Silver Trust, respectively, being offered on a net asset value (NAV) to NAV exchange basis. Based on trading values and the NAV to NAV Exchange Ratio (as such term is defined in the Sprott offers) at the time Sprott announced its intention to make the Sprott offers on April 23, 2015, the offers reflected a premium of US$3.06 per GTU unit and US$0.91 per SBT unit. The premium as of October 5, 2015, based on trading values, the NAV to NAV Exchange Ratio and the Premium Consideration, represents US$1.14 per GTU unit and US$0.61 per SBT unit, respectively. In connection with this increase in consideration, the expiry time for each Sprott offer is extended to 5:00 p.m. (Toronto time) on October 30, 2015.

“Central GoldTrust and Silver Bullion Trust unitholders have been burdened for too long by a group of trustees committed to protecting the interests of the Spicer family. It is only through the public spotlight that the variety of undisclosed fees paid to supposedly independent trustees has forced public disclosures and hollow justifications. Sprott’s offers to unitholders are compelling and momentum is building as we continue to show the clear advantages of the offers. The response of the GTU and SBT trustees has been to penalize unitholders with the burden of paying for costly lawsuits and expensive advisors to protect the Spicer family and the fees they receive. We are accordingly increasing our offer to compensate unitholders for this abuse of trust, and encourage them to take advantage of this opportunity to exchange their units for an immediate premium, and trade a management committed to entrenchment to one committed to their best interests,” said John Wilson, Chief Executive Officer of Sprott Asset Management.

Added Wilson, “We have provided extensions to the offers so that no unitholders are left without this opportunity to exit an underperforming investment and enter into a high quality security that functions as intended, reflecting the value of the bullion held in the trust. Sprott appreciates the support of GTU and SBT unitholders to date and currently anticipates these extensions will be the final extensions to the Sprott offers.”

As of 5:00 p.m. (Toronto time) on October 5, 2015, there were 8,194,265 GTU units (42.46% of all outstanding GTU units) and 2,055,574 SBT units (37.60% of all outstanding SBT units) tendered into the respective Sprott offers. Total units tendered as of October 5, 2015, do not include pending units which are typically received on the date of expiration.

GTU and SBT unitholders who have questions regarding the Sprott offers, are encouraged to contact Sprott Unitholders’ Service Agent, Kingsdale Shareholder Services, at 1-888-518-6805 (toll free in North America) or at 1-416-867-2272 (outside of North America) or by e-mail atcontactus@kingsdaleshareholder.com.

EU Takes Countries To Court Over ‘Bail-In’ Laws

The European Commission is taking legal action against six European countries, including the Netherlands and Luxembourg, after they failed to implement rules that would allow for depositors to have their cash confiscated.

Six countries will be referred to the European Court of Justice (ECJ) for their continued failure to transpose the EU’s “bail-in” laws into national legislation, the European Commission said last Thursday according to The Telegraph.

Taxpayers bailed out banks in the first global financial crisis. Depositors will be in the firing line the next time. Photo: AFP

Most EU countries, UK, the U.S., Canada, Australia and New Zealand all have plans for bail-ins in the event of banks and other large financial institutions getting into difficulty. It is now the case that in the event of bank failure, personal and corporate deposits could be confiscated.

The referral comes after the EU issued a warning against Poland, the Netherlands, Luxembourg, Sweden, Romania and the Czech Republic for their non-compliance earlier this year.

The rules – known as the Bank Recovery and Resolution Directive (BRRD) – are designed to stop governments from having to foot the bill for saving banks from going bust by instead forcing savers and deposit holders to foot the bill in an attempt to further protect banks from insolvency.

Brussels will refer six countries to the European Court of Justice over their failure to apply the new, very radical “bail-in” rules. Deposits of less than €100,000 should be protected under the new regime but in reality these limits are arbitrary and would likely be reduced to lower levels in the event of banks being insolvent again in another European and global financial crisis.

In the event of a systemic European banking crisis, however, laws could be changed at the stroke of a pen and “bail-in” mechanisms could become fully operational. Also, the comforting guarantee of €100,000 ($100,000 or £80,000) would likely be reduced in such a crisis.

The era of depositor bail-ins is coming and preparations are in place by the international monetary and financial authorities for bank bail ins. Financial interests of banks are once again being placed over those of small and medium businesses and taxpayers in general. The majority of the public is unaware of these developments, the risks and ramifications, and how they can protect their money.

Download Guide – Protecting Your Savings In The Coming Bail-In Era (11 pages)

Download Guide – From Bail-Outs to Bail-Ins: Risks and Ramifications(51 pages)

DAILY PRICES

Today’s Gold Prices: USD 1165.74, EUR 1054.55 and GBP 759.52 per ounce.

Yesterday’s Gold Prices: USD 1168.50, EUR 1058.86 and GBP 761.96 per ounce.

(LBMA AM)

Gold closed at $1,163.70/oz yesterday, having lost a small 0.08% or $0.90. Silver was unchanged for the day, remaining at $15.86/oz.

Gold in EUR – 1 Year

Gold is 0.3% higher in euros, pounds and dollars this morning, snapping four straight days of losses that have pulled prices further from this month’s near four-month high. This morning’s trading range has been narrow, with less than $5/oz between its lows and highs of the day so far.

Silver’s also 0.4% higher, but platinum and palladium are both down by more than 0.5%. For the month of October, silver and platinum have outperformed, up 9.4% and 9.5% respectively. If it holds its ground until the end of the month, platinum will post its biggest monthly gain since January 2012.

In KWN interview, Embry covers China, insolvency, gold suppression

Submitted by cpowell on Mon, 2015-10-26 19:30. Section: Daily Dispatches

3:30p ET Monday, October 26, 2015

Dear Friend of GATA and Gold:

China’s official figures for economic growth are belied by power-consumption data, Sprott Asset Management’s John Embry tells King World News today, adding that central banks keep trying to paper over the insolvency of national economies with mere liquidity. Meanwhile, Embry adds, the central planners keep shorting gold to prevent its price from giving the game away, but he wonders whether the shortage of real metal will sustain this scheme much longer. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/bankster-manipulation-continues-as-excess-debt-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(James Turk/Kingworldnews/Eric King)

Central banks destroy capital but Fed won’t raise rates, Turk tells KWN

Submitted by cpowell on Mon, 2015-10-26 20:52. Section: Daily Dispatches

3:50p CT Monday, October 26, 2015

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk tells King World News today why he doesn’t think the Federal Reserve can raise interest rates even though central bank policy around the world is destroying capital and creating crazy outcomes, like two-year Italian bonds carrying negative rates. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/we-are-witnessing-unprecedented-madness-as-u-s-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The boys will no doubt raid this week. Here is why!!

(courtesy Craig Hemke/TFMetals Report)

TF Metals Report: Mental preparation

Submitted by cpowell on Tue, 2015-10-27 02:44. Section: Daily Dispatches

9:40p CT Monday, October 26, 2015

Dear Friend of GATA and Gold:

If trader positioning in gold and silver futures continues to determine the prices of the monetary metals, both are about to suffer another big smashing from the bullion banks, the TF Metals Report’s Turd Ferguson writes today, in perfect coordination with the Federal Reserve’s meetings this week. Ferguson’s commentary is headlined “Mental Preparation” and it’s posted at the TF Metals Report’s Internet site here:

http://www.tfmetalsreport.com/blog/7232/mental-preparation

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

An excellent report on Chinese demand for gold:

As Williams states, there are 6 ways gold enters China:

- through her own production

- SGE deliveries

- importation through Hong Kong

- importation through Switzerland creating kilobars

- importation from England and the rest of the world (e.g. USA)

- gold imported for financial transactions

courtesy Lawrie Williams/Sharp Pixley

LAWRIE WILLIAMS: New Hong Kong gold exports support record high China demand forecast

OCT

27

Lawrie Williams

Whatever the major mainstream analysts and the World Gold Council may say we would put Chinese domestic gold demand as running very high this year – almost certainly exceptionally so. Shanghai Gold Exchange (SGE) deliveries would certainly support this premise, running around 312 tonnes higher year to date than in China’s record 2013 consumption year at the same time as we have already reported (See:Another 53.4 t gold withdrawn from SGE. YTD 2061.9 t) and heading for an annual figure of probably well over 2,600 tonnes. Now we see reported net Hong Kong gold deliveries to the mainland at a 10 month high of a considerable 97.42 tonnes in September. Hong Kong remains one of the principal import routes for gold into mainland China but is no longer so dominant in those terms for its figures to be taken as a proxy for total Chinese gold imports.

So, Shanghai Gold Exchange deliveries, imports via Hong Kong, direct imports from Switzerland and the UK, direct imports from the rest of the world, the apparent build-up of Chinese Central Bank gold holdings, China’s own annual gold production, the amount of gold tied up in financial transactions etc. – all these are either known knowns or unknown knowns in trying to assess he true level of Chinese gold imports and demand. While some of this is reported by the countries exporting gold to China, the country does not itself quantify its imports. It is thus difficult, if not impossible, to assess what is the real nature and size of true Chinese gold demand, but all indications are that 2015 will indeed be a record year – and keep China comfortably ahead of India as the world’s top consumer whatever GFMS may say in its latest analysis report for the first three quarters of the year.

There are a number of professional analysts out there who earn a living out of their own researched assessments of what is going on – and are adamant that they are correct in their assumptions and calculations, but their figures often don’t seem to add up in the light of what seems to be overwhelming statistical evidence which may contradict their figures. We also feel that some of their assumptions are mostly speculative in trying to make sense of their sometimes contradictory figures.

The biggest fly in the ointment of the analytical assumptions is the enormous level of deliveries to the Chinese market out of the Shanghai Gold Exchange this year. Whatever the analysts say this has to be a strong indicator of overall demand, although perhaps not of consumption as they measure it. As we have pointed out before, the analysts do not include the use of gold in Chinese financial transactions as being part of their demand assessments. To us this is still gold being consumed in China – even if it does not meet the analysts’ strict interpretations of what is consumption. Yes, it can be returned to the markets when these transactions unwind, although it tends to be rolled over instead – but then other forms of traditionally-consumed gold may also find their way back to the market through gold for investment sales and scrap supplies. With extremely low mark-ups for most gold jewellery in China (and India too), the jewellery market is very different from that in the West.

What is perhaps only now coming to light is the enormous level of the ‘financial’ gold involved in Chinese transactions. Speaking at last week’s LBMA meeting in Vienna, Jiang Shu, Chief Analyst of the Shandong Group, noted that over 1,300 tonnes of gold is tied up in such transactions. This would account for much of the differential between SGE deliveries and analysts’ ‘gold consumption’ figures. Gold imports from known sources, plus China’s own gold production, plus scrap looks to be heading for the 2,000 tonne mark or more this year, while SGE deliveries have already exceeded this level. With India adding between 800 and 1,000 tonnes of imported gold to the equation this accounts for virtually all the world’s newly mined gold leaving the rest of the world (which according to the analysts consumes about as much gold as India and China together) to be supplied from the balance of global supply – notably from scrap – but given the relatively low gold price and thus falling scrap supply – this is insufficient to meet the balance of demand. This physical gold is coming from somewhere – if not from privately held vaulted gold, then perhaps from central bank holdings in the form of leased or swapped gold. But, leased and swapped gold remains in central bank accounts as though it is being held as physical metal – an obscurity which more than matches any Chinese obfuscation of its gold import and demand figures.

As an aside, much is made in the West of China’s supposedly collapsing economy – yet figures from Chinese online giant Alibaba out today would seem to belie this. Alibaba revenues to end-September have risen 32% year on year. While there may have been something of a slowdown in gross merchandise volumes it would seem that reports of a collapsing Chinese economy are somewhat overdone.

-END-

(courtesy Lars Schall/GATA)

Austrian central bank refuses questions about executive’s assertion of gold interventions

Submitted by cpowell on Tue, 2015-10-27 12:25. Section: Documentation

7:24a CT Tuesday, October 27, 2015

Dear Friend of GATA and Gold:

The German freelance financial journalist Lars Schall has done again what no mainstream financial journalist in the world dares to do: put critical questions about gold to a central bank.

This time Schall has directed his questions to Peter Mooslechner, executive director of the central bank of Austria, who a week ago let slip in an interview with Daniela Cambone of Kitco News that central banks are using their gold reserves for secret intervention in the gold and currency markets:

http://www.gata.org/node/15878

Seeming oblivious, Cambone did not pursue the relevation. Today Schall reports how he did pursue it with some very specific and critical questions and that Mooslechner and the Austrian central bank refused to respond to him.

Schall’s report is headlined “Again and Again: No Answers from Central Banks to Critical Questions about Gold” and it’s posted at his Internet site here:

http://www.larsschall.com/2015/10/27/again-and-again-no-answers-from-cen…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

2015-10-27 13:06 GMT+01:00 Lars Schall <larsschall@googlemail.com>:

friends, romans, countrymen!

oops!…i did it again:

Again and Again: No Answers from Central Banks to Critical Questions about Gold

Oktober 27th, 2015

So, how do central banks exactly intervene in the gold market? Well, you can ask central bankers this question and they won’t tell you – even those central bankers that do mention interventions in the gold market during superficial interviews. Recent example: Peter Mooslechner, executive director of Austria’s central bank.

Respected Like a Banana Republic?

Calling your attention to two recent stories, the debate over the debt limit

1 Chinese yuan vs USA dollar/yuan falls as expected with a rate cut, this time at 6.3530 Shanghai bourse: in the green (manipulated), hang sang:red

2 Nikkei closed down 170.08 or 0.90%.

3. Europe stocks mostly in the red /USA dollar index down to 96.74/Euro up to 1.1055

3b Japan 10 year bond yield: falls to .305% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.33

3c Nikkei now just above 18,000

3d USA/Yen rate now above the important 120 barrier this morning

3e WTI: 43.34 and Brent: 47.24

3f Gold up /Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .500 per cent. German bunds in negative yields from 6 years out

Greece sees its 2 year rate rises to 8.03%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield rises to : 7.66% (yield curve inverted)

3k Gold at $1166.00 /silver $15.89 (8 am est)

3l USA vs Russian rouble; (Russian rouble down 1 & 1/5 in roubles/dollar) 64.17

3m oil into the 43 dollar handle for WTI and 47 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9842 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0880 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 6 year German bund now in negative territory with the 10 year falling to +.500%/German 6 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.05% early this morning. Thirty year rate below 3% at 2.85% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Flat After Yen Carry Tremors As Fed Starts 2-Day Policy Meeting

Two biggest move overnight came from everyone’s favorite carry pair, the USDJPY, which may have finally read what we said yesterday, namely that with the Fed and ECB both doing its job, there is little need for the Bank of Japan to repeat its Halloween massacre for the second year in a row, and as a result will keep its QQE program unchanged. It promptly tumbled from its 121 tractor level, to just above 120.25, where BOJ bids were said to be found.

With the FOMC October meeting starting today, the other overnight catalyst was not surprisingly the latest Hilsenrath scribe in which he removed any uncertainty about a Wednesday hike, “leaving mid-December as the central bank’s last chance to raise rates this year.”

The timetable poses twin challenges for Fed Chairwoman Janet Yellen: Deciding whether the U.S. economy is ready for an interest-rate increase, and signaling central bank intentions without causing further market confusion.

The problem is that not even Hilsenrath’s Fed “source” has any idea what will happen in December. “The Fed’s uncertainty is contagious. A Wall Street Journal survey of market economists this month found that 64% believe the Fed will raise rates by December. Futures markets put the odds at 35%.” Who’s wrong? Well, the Fed’s model of the economy, and the “dot plot” are certainly accurate, so it has to be the economy’s fault for not complying with the central planners’ vision:

One cause of the confusion isn’t the fault of the central bank. The economy isn’t cooperating. With unemployment falling rapidly, Ms. Yellen and most of her colleagues began the year thinking the economy would be strong enough to lift rates.

One of these years the Fed will realize that the reason the “economy isn’t cooperating” is because of the Fed. But don’t hold your breath, we give it at least another 24-36 months before the S&P is at 3000 and Yellen is still “confused.”

In other news, there was the usual macro disappointment, when UK Q3 GDP printed at 0.5%, below the 0.6% expected, and down from 0.7% in Q2, driven by the weakest construction sector contribution to GDP in years. Are the Chinese no longer buying?

Speaking of Chinese buying, perhaps they were not too excited about stocks, but with the SHCOMP down most of the day, we were relieved to see the National team stage its usual last hour intervention, and drag the Chinese stock market from down -2% to close up 0.14% with the traditional furious last hour ramp to eliminate the bitter aftertaste from the latest drop in industrial profits which dropped -0.1% Y/Y, following a -8.8% drop in August.

One thing the Chinese were definitely not buying was natgas which overnight dropped continued their steep descent and dropped below $2.00 for the first time since 2012 and just the 4th time in the 21st century.

Elsewhere in Asian equity markets traded lower led by the slump in Chinese stocks as they shrugged off the recent easing measures by the PBoC , while subdued trade was also observed as participants await the FOMC and BoJ policy decisions. Shanghai Comp. (+0.1%) retreated from 2-month highs amid a continued decline in industrial profits (-0.10% vs. Prey. -8.80%), however, heading into the European open some losses have been pared. Nikkei 225 (-0.9%) was pressured by losses in the energy sector which also weighed on the ASX 200 (0.0%). JGBs traded higher as the lacklustre risk sentiment drove inflows into the safer asset, while a stronger than prior 40yr auction added support.

European equities kicked off the session firmly in negative territory before paring the losses throughout the morning (Euro Stoxx: -0.1%). Equities have been weighed on notably by healthcare and materials names in the wake of downbeat earnings from Novartis (-1.4%) and BASF (-4.1%). While fixed income markets have seen Bunds continue to be supported by softer stocks, with Dutch 4.0% 2019 and 2.5% 2033 Bonds (equiv to approx 20k Bund futures) seeing a relatively successful auction. Of note, there is a fair amount of supply today, with ESM expected to issue 5y syndication and Cyprus’ lOy syndication.

In FX, as noted above, markets saw JPY outperform once again, in line with yesterday’s move on the back of comments from the likes of Honda and Hamada out of Japan, suggesting that the BoJ do not need to increase QQE when they meet on Friday. Elsewhere, EUR underperforms the USD, with ECB’s Praet adding to the dampened sentiment for EUR this morning by suggesting the ECB is examining short-term rates and its asset-buying program as well as stating the inflation target could be delayed. GBP also underperforms against the USD, weakening heading into the release of the advanced Q3 GDP release out of the UK (Q/Q 0.50% vs. Exp. 0.60%).

In the commodity space, the energy complex remains soft, with WTI and Brent remaining in negative territory, although off their worst levels, while NatGas has fallen below USD 2.00/MMBTU for the first time since 2012 , as forecasts predicting warmer than average weather continue to weigh upon the commodity. Looking ahead, today sees the release of API crude oil inventories (Prey. 7100K).

Elsewhere, the metals complex has seen relatively muted price action overnight, with gold outperforming other precious metals underpinned by increased demand for safer assets as Chinese markets initially shrugged off last week’s PBoC rate cuts

Looking ahead, today sees durable goods orders, S&P/Case Shiller report and services PM! out of the US, as well as comments from ECB’s Nowotny and Coeure and BoE’s Shafik. It’s a busy day for corporate earnings too. In the US 43 S&P 500 companies are due to report with the highlights including Pfizer, Ford, UPS and Merck all before the open and then Apple’s numbers after the closing bell.

Market Wrap:

- S&P 500 futures down 0.1% at 2060

- Equities: Nikkei 225 (-0.9%), IBEX (-0.7%), Euro Stoxx 50 down 0.2%, FTSE 100 down 0.3%, DAX down 0.1%, CAC 40 down 0.3%, IBEX 35 down 0.7%, FTSE MIB little changed, SMI down 0.6%

- Bonds: German 10Yr yield (-2.4%), French 10Yr yield (-1.4%)

- Commodities: Natural Gas Futures (-2.7%), WTI Futures (-1.2%)

- FX: Yen spot (+0.5%), EUR/CHF (+0.1%)

- Vstoxx Index up 0.5% at 20.74

- For a detailed market snapshot click here

- U.S. consumer confidence, durable goods orders, capital goods orders, Markit U.S. composite PMI, Markit U.S. services PMI, due later

Bulletin Headline Summary from RanSquawk and Bloomberg

- Stocks in Europe opened lower, with DAX and SMI underperforming following weak earnings by BASF (BAS GY) and also Novartis (NOVN VX)

- JPY continued to strengthen in a similar manner to the move seen yesterday with EUR/JPY and USD/JPY lower ahead of this week’s BoJ decision with figures such as Hamada and Honda downplaying the likelihood of additional imminent easing

- Looking ahead, today sees durable goods orders, S&P/Case Shiller report and services PM! out of the US, as well as API crude oil inventories and comments from ECB’s Nowotny and Coeure and BoE’s Shafik

ASIA - Treasuries steady before two-day FOMC meeting begins in Washington and before week’s auctions begin tomorrow with $29b 5Y, $15b 2Y FRN; 2Y notes sales scheduled for today was postponed.

- The White House and top lawmakers from both parties reached a deal to avoid a debt default after Nov. 3, putting lawmakers on course to stave off a fiscal calamity

- China said it will take “all necessary measures” to defend its territory after the U.S. sailed a warship through waters claimed by China in the disputed South China Sea, a move Beijing called a threat to peace and stability in Asia

- The U.S. plans to sell millions of barrels of crude oil from its Strategic Petroleum Reserve from 2018 until 2025 under a budget deal reached on Monday night by the White House and top lawmakers from both parties

- Iran’s crude exports are likely to remain restricted until the first half of next year, when it’s “reasonable” to expect international sanctions against the OPEC producer to be lifted, according to a U.S. government official

- U.S. natural gas traded below $2/mBTU for the first time since April 2012 as a glut of the power-plant and heating fuel expands toward a record

- Some officials at Abe’s office and the finance ministry see no need now for the Bank of Japan to expand its monetary stimulus program amid concern it would harm consumers, according to people with knowledge of talks inside the government

- China’s official 6.9% y/y print for 3Q GDP is at odds with models used by researchers at Bloomberg Intelligence and financial firms, Bloomberg economists Tom Orlik and Fielding Chen write

- $7.1b IG priced yesterday, no HY. BofAML Corporate Master Index OAS narrows 1bp to +166, YTD range 180/129. High Yield Master II OAS widens 3bp to +600, YTD range 683/438

- Sovereign 10Y bond yields lower. Asian and European stocks mostly lower, U.S. equity-index futures decline. Crude oil lower, gold and copper higher

DB’s Jim Reid completes the overnight summary

Looking now at the latest in Asia this morning. Any post-PBoC easing euphoria which supported an, albeit modest, rise in Chinese equities markets yesterday has come to a sudden halt this morning with falls across Chinese bourses. The Shanghai Comp is down -1.05%, while the CSI 300 and Shenzhen are -1.17% and -0.76% respectively. That’s actually despite a rebound in China industrial profits data this morning, with the September print improving to (a still however soft) -0.1% yoy from -8.8% in August. Meanwhile, it’s broadly weaker across much of the Asia region this morning. The Nikkei (-0.64%), Hang Seng (-0.48%) and Kospi (-0.38%) all taking a leg lower, while the ASX is the relative outperformer, down just -0.03%. Credit indices in Asia and Australia are generally 2bps wider this morning too.

A slide in commodity markets was the big story yesterday. After falling nearly 10% in the last two weeks, Brent (-0.94%) continued to march lower yesterday, closing at $47.54/bbl. It was a similar story for WTI (-1.39%) which closed back below $44 for the first time since August 26th and is now nearly $8 off the MTD highs reached just 17 days ago. Both markets are down another 1% in trading this morning too. Natural Gas was the big mover yesterday though after tumbling -9.80% and to the lowest since April 2012. While the continued concerns around record-high inventory levels are still front and centre, concern for a strong el Nino this winter is also weighing on the energy complex at the moment and being attributed for much of the latest leg lower.

Those moves kept energy stocks on the back foot yesterday with the likes of Chevron, Exxon Mobil, Shell, Total and ConocoPhillips down between 1% and 3%. That was enough to see equity markets run out of steam following the recent dovish CB relief rally. The Stoxx 600 finished -0.39% while in the US the S&P 500 finished down -0.19% and the Dow closed -0.13%. The Nasdaq continues to be the relative outperformer however with the index yesterday just about closing in positive territory (+0.06%), taking it to just 2% off the August highs prior to the huge sell-off mid-way through the month.

Apple was a notable drag for US equities yesterday too after falling 3% following some weak results out of the company’s semi-conductor supplier. Apple will be the attention of most analysts this evening when the tech giant is due to release its latest quarterly earnings report. Yesterday was in fact a fairly quiet day for earnings on the whole. Just 11 S&P 500 companies released their latest quarterly report, with 7 (64%) beating earnings expectations and 5 (45%) beating revenue estimates. That means with 185 companies having reported, 74% have beaten earnings expectations but just 42% beating top line estimates (73% and 42% respectively this time yesterday).

Treasury yields nudged lower yesterday, the benchmark 10y down 3bps to 2.057% and the US Dollar came under some pressure (Dollar index -0.27%) following a strong 3-day run after some fairly softish US economic data yesterday. New home sales for September were weak, falling -11.5% mom during the month (vs. -0.6% expected) after a downward revision to August and July, taking the annualized rate down to 468k and the lowest since November last year. Following this we got the latest Dallas Fed manufacturing activity index with the October print of -12.7 (vs. -6.5 expected) a 3.2pt fall from September. The index has in fact failed to print in positive territory this year, while there was more softness in the new orders component, down 3pts to -7.6pts.

Over in Europe the only data to note was out of Germany with the October IFO survey. The headline index reading fell (-0.3pts) less than expected to 108.2 (vs. 107.8 expected). The expectations print rose 0.5pts to 103.8 (vs. 102.4 expected) but the current assessment reading declined 1.4pts to 112.6 (vs. 113.5 expected). Our colleagues in Europe noted that the expectations print points to +0.6% qoq GDP growth in Q4 which compares to the composite PMI which points to +0.5% growth – both an upside risk to their +0.3% estimate currently for Q4.

Before we turn to today’s calendar, headlines on the wires are suggesting that we may be moving one step closer to a budget agreement in the US. According to the WSJ, the White House and congressional leaders were said to be nearing a two-year budget plan deal this week and ahead of the November 3rd deadline. The article suggests that the deal would suspend the debt limit into early 2017 while also establishing new spending levels through September 2017.

Turning now to today’s calendar. Data flow this morning in Europe kick starts with the latest Euro area money and credit aggregates. That’s before we get the advanced Q3 GDP reading in the UK with market expectations currently sitting at +0.6% qoq. This afternoon in the US we’ve got a bumper session for economic data. Capital and durable goods orders for September will warrant much of the attention, with the data helping to sharpen this Thursday’s Q3 GDP report. Shortly following this we’ll get the August S&P/Case Shiller house price index reading, before the October flash composite and services PMI’s. Later on we’ll then get the October consumer confidence print and Richmond Fed manufacturing survey. It’s a busy day for corporate earnings too. In the US 43 S&P 500 companies are due to report with the highlights including Pfizer, Ford, UPS and Merck all before the open and then Apple’s numbers after the closing bell. In Europe we’re due to hear from 13 Stoxx 600 names with BP looking like the notable highlight.

As China ‘Buys Low’ To Build SPR, Washington Forced To Sell Strategic Crude To Meet Budget

The signs of regime change are everywhere. From embarrassment by Russia’s success in Syria to China’s creation of its own ‘World Bank’ and SWIFT alternative, the trend of de-empirization are growing, but tonight’s news that Washington will sell oil from its strategic reserve in order to meet budget constraints and avoid default (as China takes advantage of low prices to build its own reserves) is simply stunning in its analogy of the shifting world order.

Bipartisan congressional leaders and the White House struck a major fiscal deal in principle Monday that would raise the debt ceiling and lift budget caps on both defense and domestic programs, according to congressional sources familiar with the deal.

…

This deal would avoid a potential debt default on November 3, and it would reduce the chances of a government shutdown on December 11.

…

The deal includes $80 billion in increased defense and domestic spending over two years, a senior House source told CNN.

…

That new spending would be offset by sales from the strategic petroleum oil reserve, use of public airwaves for telecommunications companies and changes to the crop insurance program — among other measures. Moreover, the deal would spread out increases in Medicare premiums over time so beneficiaries don’t feel them acutely. It would also aim to preserve the Social Security disability trust fund, sources said.

Conservatives sharply panned the deal.

“It’s emblematic of five years of failed leadership,” said Rep. Justin Amash, R-Michigan.

So, to summarize, ‘Murica – the world’s reserve currency superpower and “cleanest dirty sheet in a brothel” economy is about to sell its “strategic” petroleum reserves at multi-year low prices in order to meet an ever-expanding welfare state’s needs…

As China “buys low” adding to its reserves amid the multi-year low prices…

* * *

Of course this move by The US is echoing what many Petrodollar States are being forced to do to (sell ‘reserves’ to meet social welfare needs); however, in this case, it is not some massively indebted banana republic, but The Unites States of America (oh wait!).

* * *

As we recently pointed out,there are two general schools of thought amongst noted contrarians and libertarians regarding China’s overriding objectives.

One school has it that China is very much a part of the One World Government philosophy and their primary goal is to acquire a more powerful seat at the IMF. Having done so, they will settle in and be content to be one of the leading jurisdictions that run the world collectively.

The other school suggests that China means to become the most powerful nation in the world – to replace the US in every way as the world’s dominant nation.

My own appraisal is a combination of the two. China’s behaviour – not only their public stance, but their massive economic infrastructural development efforts indicate to me that they intend to go full-bore with their new economic infrastructure, giving them powers that rival and even overtake the EU and US. At that point, they will be unconcerned as to whether they will be welcomed into the “club” that is presently dominated by the EU and US. They will be an unstoppable freight train passing through town. The western world can either get on board, or fall by the wayside. The Chinese will prefer the former, as it would be more profitable and would avoid conflicts (both military and economic), but they will not be deterred.

At this moment in time, we’re observing a part of that effort. The old structure is being slowly bulldozed and a new structure is underway. It’s very likely that, in order to assure its success, it will be a better one – one which offers its users greater freedom. We can be certain that, like all governmental constructs, it will eventually become corrupted and be just as oppressive as the one it hopes to replace. However, in its early years (and hopefully beyond that) the people of the world will enjoy a period of increased economic freedom.

Some time ago, when we first predicted that China would create such a system, it seemed almost a fairy tale – a highly unlikely development. Yet, China has gotten there even faster than I’d expected. Let’s hope that the day when its benefits trickle down to the street level, worldwide, will also arrive more quickly than we had expected.

Charts: Bloomberg

end

Something Just Snapped – Sudden Yen Strength Sends Crude, Copper & China, US Stocks Sliding

Catalysts are unclear for now – whether it was stronger than expected industrial profits in China, tensions growing in the South China Sea, or more chatter of no imminent increased easing from BoJ – but broadly speaking, JPY strength (lower USDJPY) is weighing on risk assets across the world as US, Japanese, and Chinese stocks tumbles (US Treasuries bid) and crude and copper prices slump.

USDJPY broke back below 120.50 (erasing its post-PBOC move)…

And as goes JPY, so goes US equities… with the S&P giving up all its post-PBOC gains…

JPY strength (left) and a sudden safety bid to US Treasuries (right)

Sparking derisking in Japanese stocks (left), US equities (middle), and Crude (rightz-0

For now paper gold prices have yet to react but Bitcoin jumped notably…

Charts: Bloomberg

end

Then this morning this happened:

Furious China Summons U.S. Ambassador, Slams Obama Decision To “Threaten Peace” With Warship Challenge

Update: CHINA SUMMONS U.S. AMBASSADOR OVER SOUTH CHINA SEA PATROL: CCTV

Well, the USS Lassen sailed within 12-nautical miles of Subi Reef and surprisingly, World War III did not break out overnight.

(USS Lassen)

(Subi reef)

Nine months of tension between Washington and Beijing over the latter’s land reclamation efforts in The South China Sea culminated on Monday with President Obama’s decision to send a guided missile destroyer to China’s man-made military outposts on a “freedom of navigation” exercise. As we put it on Monday evening:

“The ball is now squarely in China’s court. The question now is whether Beijing will back down and concede that “sovereignty” somehow means something different with regard to the islands than it does with respect to the mainland or whether Xi will stick to his guns (no pun intended) and take a pot shot at a US destroyer.”

In short, some feared that based on recent rhetoric out of Beijing (e.g. the PLA will “stand up and use force”) that China might actually fire upon the US-flagged vessel or at least move to surround it in what might mark the first step on the road to war.

Ultimately, that didn’t happen as China apparently decided to take the high road for now and avoid an escalation that might have had far-reaching consequences.

That said, Beijing isn’t happy. Here’s more from Bloomberg:

China said it will take “all necessary measures” to defend its territory after the U.S. sailed a warship through waters claimed by China in the disputed South China Sea, a move the government in Beijing called a threat to peace and stability in Asia.

“The behavior of the U.S. warship threatened China’s sovereignty and national interest, endangered the safety of the island’s staff and facilities, and harmed the regional peace and stability,” Foreign Ministry spokesman Lu Kang said in a statement today. “The Chinese side expressed its strong discontent and firm opposition.”

The comments came hours after the USS Lassen passed within 12-nautical miles of Subi Reef, an island built by China as a platform to assert its claim to almost 80 percent of one of the world’s busiest waterways. By passing so close to the man-made island, the U.S. is showing it doesn’t recognize that the feature qualifies for a 12-nautical mile territorial zone under international law.

The patrol marks the most direct attempt by the U.S. to challenge China’s territorial claims and comes weeks after President Barack Obama told President Xi Jinping at a Washington summit that the U.S. would enforce freedom of navigation and that China should refrain from militarizing the waterway.

In a strongly-worded statement, Lu said the USS Lassen had “illegally” entered Chinese waters and that “relevant Chinese departments monitored, shadowed and warned the U.S. ship.” China has “indisputable” sovereignty over the Spratly Islands and surrounding waters, Lu said.

“What the U.S. is doing now will only damage the stability in the South China Sea, and send the wrong message to neighboring nations such as the Philippines and encourage them to take some risky behavior,” said Xu Liping, a professor of Southeast Asian studies at the Chinese Academy of Social Sciences, a government-linked institute.

While it’s not entirely clear what professor Xu Liping means by “encourage the Philippines to take some risky behavior,” it’s worth noting that Washington’s provocation is in some respects explicity designed to embolden America’s regional allies. That is, this isn’t going on in Washington’s backyard. This is simply the US responding to calls from its friends in the South Pacific to counter what they view as Chinese aggression by letting Beijing know that Big Brother isn’t going to stand for any bullying from the PLA. That gambit appears to have paid off – for the time being.

As for what comes next, Malcolm Davis, an assistant professor in China-Western relations at Bond University on Australia’s Gold Coast tells Bloomberg China could move to set up a no-fly zone:

China may choose to respond without directly challenging U.S. ships with its Navy or coast guard. It could declare an Air Defense Identification Zone over the South China Sea, or speed up the militarization of the area by deploying extra forces, including combat aircraft, to the islands.

“The ball would then be back in the U.S.’s court,” Davis said. “A Chinese attempt to enforce an ADIZ over the South China Sea would increase tensions with its neighbors, most notably Vietnam, the Philippines and Malaysia, and they would place increasing pressure on Washington not to back down.”

In other words, China doesn’t need to fire on a US destroyer to ratchet up the pressure. Beijing can simply continue to do what it’s done up until now; that is, militarize the region and essentially dare the US to take action beyond sailing by and waving.

We suspect we’ll see plenty of new satellite images over the coming weeks and months which purport to show the extent to which the PLA is beefing up its defenses in the face of unnecessary (not to mention extremely petty) posturing on Washington’s part.

China Unleashes The Jingoist Rhetoric: “If U.S. Ships Stop, We Should Lock Them By Fire-Control Radar”

Now that the U.S. has sailed the guided missile destroyer USS Lassen within 12 miles of the disputed islands in the South China Sea as “an assertion of freedom of navigation and as a means to balance power in the region”, it was time for China to offer its “diplomatic” response.

And the best place to do that would be ultranationalistic Global Times, a newspaper described as “a Chinese tabloid under the auspices of the People’s Daily newspaper, focusing on international issues at a communist Chinese perspective. The Global Times differentiates itself from other Chinese newspapers in part through its more populist approach to journalism, coupled with a tendency to court controversy.”

Here is what the editors said in an agitated, jingoist Op-Ed published earlier today.

After the show, it’s time for US destroyer to leave

According to Reuters and the Wall Street Journal, the US Navy sent the guided-missile destroyer USS Lassen within 12 nautical miles of islands built by China in the South China Sea. US officials claimed that the action is aimed at safeguarding the freedom of navigation and did not target China. The patrols could also be conducted around features that Vietnam and the Philippines have built up in the South China Sea. According to the US side, the action has been approved by President Barack Obama, but with no notification for China.

Washington hinted long ago that it would send ships within 12 nautical miles of China’s islands, but it didn’t say explicitly what it would do. The US said the action would last several hours. According to Western media, Chinese navy ships are closely watching the Lassen. The Pentagon is obviously provoking China. It is time to test the wisdom and determination of the Chinese people.

We should stay calm. If we feel disgraced and utter some furious words, it will only make the US achieve its goal of irritating us.

We should analyze the actual condition of the US harassment. It seems that the US only wants to display its presence as it didn’t raise the imprudent demand that China stops island-building. It has no intention to launch a military clash with China. It is just the US’ political show. The UN Convention of the Law of the Sea provides three categories. The first is islands, which are naturally formed, habitable areas above water at high tide, and are therefore entitled to 12 nautical miles of territorial waters and a 200 nautical mile exclusive economic zones (EEZs). The second is reefs that have portions above water at low tide, and are uninhabitable, which have territorial waters but no EEZs. Finally, completely submerged “low tide elevations” have no territorial waters.

The islands and reefs in the Nansha Islands under the control of the Chinese mainland belong to the latter two categories. China did not elaborate whether it will expand its territorial seas after land construction. This is where the ambiguity of the international law. In addition, China hasn’t announced its territorial baseline in the South China Sea, making the legal meaning of Sino-US contention in the South China Sea vague.

China and the US have no conflicting views over the international law. Instead, the two are competing with each other over the rules and orders in the South China Sea. Beijing’s construction work in the area is completely legal, and there is nothing Washington can blame it for.Yet, from Washington’s perspective, the geopolitical situation in the area will be changed following China’s island reclamation. Beijing may seize the advantage to control the Nansha Islands and their adjacent seas. The US also conjectures that China will gain strategic pivots for power projection to the south in the future. Therefore, Washington, annoyed and anxious, has taken actions in order to balance Beijing’s clout and to consolidate its dominance in the South China Sea.

It has to be noticed that China has already carried out construction work in the area. This is the concrete achievements Beijing has gained. Completing building the islands still remains as a major task for China in the future. At present, no country, the US included, is able to obstruct Beijing’s island reclamation in the region.

In face of the US harassment, Beijing should deal with Washington tactfully and prepare for the worst. This can convince the White House that China, despite its unwillingness, is not frightened to fight a war with the US in the region, and is determined to safeguard its national interests and dignity.

Beijing ought to carry out anti-harassment operations. We should first track the US warships. If they, instead of passing by, stop for further actions, it is necessary for us to launch electronic interventions, and even send out warships, lock them by fire-control radar and fly over the US vessels.

Chinese should be aware that the US harassment is only a common challenge in China’s rise. We should regard it with calm and be confident of our government and troops.It is certain that the Chinese government, ordering the land reclamation, is able and determined to safeguard the islands. China is gradually recovering its justified rights in the South China Sea. China has not emphasized the “12 nautical miles.” It is the US that helps us to build and reinforce this concept. Then, it is fine for us to accept the “12 nautical miles” and we have no intention to accept 13 or more than 13 nautical miles.

end

“Giant Wave Of Money” Heads For Sweden, As Draghi Creates “Nightmare” For Riksbank

Early on September 3, we warned that the Riksbank was at risk of making a meaningful policy “error” by not cutting rates ahead of the ECB announcement expected later that morning.

It wasn’t that we were anxious to see Sweden plunge further into the Keynesian Twilight Zone by taking the repo rate further into negative territory. Indeed, we never recommend going full-Krugman as Sweden did starting late in 2011 after marking a sharp policy reversal. For its trouble, the Riksbank has been left with a massive housing bubble and successive rate cuts have had only a minimal effect on inflation expectations.

But alas, in a world that’s gone Keynesian crazy, it’s either ease or be eased upon (so to speak) and when the Riksbank decided not to cut at its September meeting, it set up the possibility that a dovish Mario Draghi would cause the krona to rise, further jeopardizing Sweden’s inflation target. In other words, the Riksbank was setting itself up to take a loss in the ongoing global currency wars.

Sure enough, Draghi raised the PSPP issue limit from 25% to 33% and then, last week, the ECB telegraphed more easing in December either in the form of a depo rate cut, an expansion of PSPP, or both.

As we discussed in “How Mario Draghi Can Force The Swiss National Bank To Go “Nuclear” On Depositors”, this puts the Riksbank and the SNB in a tough spot. Sweden’s policy options are limited. The repo rate is already deeply negative and the Riksbank is bumping up against the upper limit in terms of how many bonds it can buy without breaking the market. Meanwhile, thanks to the fact that the SNB only applies NIRP to a fraction of reserves, rate cuts by the ECB may have an outsized impact on the EURCHF cross, a decisively undesirable outcome for Switzerland.

Now, ahead of this week’s Riksbank policy announcement, Robert Bergqvist, chief economist at SEB in Stockholm is out warning that thanks to Mario Draghi, Sweden faces a veritable “nightmare.” Here’s more, via Bloomberg:

European Central Bank President Mario Draghi said boo last week and the krona jumped.

With the ECB signaling a new wave of stimulus to prop up the euro zone, the question is how Sweden’s central bank can fight the monetary expansion coming from the south with its own, much smaller toolbox as it tries to stop the krona appreciating.

“The nightmare for the Riksbank board is maybe something like this: they are gathered in the south of Sweden, looking out over the Baltic Sea, when they see a giant wave of money coming in from the euro zone and try to fight it with a hose,”Robert Bergqvist, chief economist at SEB in Stockholm and a former researcher at the Riksbank, said by phone.

The Riksbank is due to announce its next rate decision on Oct. 28. Most economists surveyed by Bloomberg see the bank keeping its repo rate at minus 0.35 percent, though there’s speculation policy makers will need to expand their quantitative easing program. Failure to do so would lead to the krona strengthening “markedly,” Nordea Bank says.

Draghi’s stimulus measures to date have already forced his Swedish counterpart, Stefan Ingves, to resort to unprecedented measures to drive up consumer prices in Scandinavia’s largest economy. He cut Sweden’s main rate below zero for the first time in February and started buying bonds, expanding the QE program several times since. Underlying price growth has stayed below the Riksbank’s 2 percent target since the beginning of 2011.

And so, we’re now beginning to see the results of the beggar-thy-neighbor monetary insanity that grips DM central banks. It’s a never-ending race to the bottom and now that everyone is moving further and further into NIRP, it’s not even clear that there is a bottom. After all, even if negative rates finally do make their way to household deposits causing rationale actors to simply withdraw their money, the monetary authorities can always just ban cash, which would effectively obliterate the idea of a “lower bound.”

In any event, perhaps the more pressing concern here is the combination of a massive housing bubble, NIRP, and a QE program that’s all but exhausted. As we noted last week when discussing Denmark, Copenhagen home prices are rising at 12% per year (or more) and yet the Danish central bank is operating on the assumption that headline inflation is half of 1%. Obviously that borders on the insane. Central banks are deliberately ignoring a sure sign of inflation on the way to citing disinflation as an excuse for doubling, tripling, and quadrupling down on the same policies that have driven housing prices into the stratosphere. The question then becomes this: when these housing bubbles burst (and they will), how do central banks in Denmark, Sweden, and Norway intend to fight the ensuing deep recessions now that they’ve exhausted their counter-cyclical capacity?

Greek Creditors Refuse To Make Next Loan Payment – German Press

At first it was cute: when Greece got its first “dramatic” bailout in 2010 sending the global markets and the EUR first plunging then soaring, it was a melodrama of sorts – people still cared.

Then, by the time the second and third bailouts rolled around, especially in the aftermath of the most ridiculous referendum in modern history, where a majority of Greeks voted for one thing only to get the other, it became a tragicomedy in what everyone hoped would be its final, “German colonial” season.

It wasn’t.

Moments ago, Germany’s Suddeutsche Zeitung reported that just two (or is it three, this past summer is one big blur) months after Greece voted through its third bailout, one which will raise its debt/GDP to over 200% on a fleeting promise that someone, somewhere just may grant Greece a debt extension (which will do absolutely nothing about the nominal amount of debt), its creditors have already grown tired with the game and are refusing to pay the next Greek loan tranche of €2 billion.

Specifically, the payment of the first €2b tranche of €3b is now said to bedelayed because Greek Prime Minister Alexis Tsipras failed to implement reforms on schedule, Sueddeutsche Zeitung reports, citing unidentified senior EU official.

Wait, you mean the Greeks (over)promised and never delivered? Who could have possibly seen this coming?

Not the unidentified EU official who blasts Athens as having implemented only a third of the required projects.

As a result, the transferprobably will only take place in November, if then, since only 14 of the 48 “milestones” linked to payments have been decided on.

The report goes on to tell us what we already knew: talks between the government in Athens and the Troika + the ESM (or Quadriga, or whatever it’s called) ended last week without success.

SZ goes into the unpleasant details, noting that there are inconsistencies in how the banks deal with bad loans, estimated that 320 000 apartment owners have mortgage payments in arrears, threatened with foreclosures, evictions, and so on.

In other words, the Greek holiday from being held accountable for anything which started in July and lasted until October is over.

* * *

Yet, there is still hope: in a separate report, Germany’s Bild tabloid cites Deutsche Bank analysts as anticipating a debt reduction for Greece of €200 billion by year-end, and amount which Bild conveniently calculates corresponds to €700 per inhabitant of the Eurozone.

It adds that, as noted above, Greek debt would total €340b by year-end, or 200% of Greek GDP, some 140% higher than allowed by European treaties.

It concludes by citing Lueder Gerken, Chairman of the Centre for European Policy, as saying that a Greek “haircut is economically inevitable, as well as a fourth rescue package.”

That much is known.

What is not known is why, out of the blue, the German press decided to remind the public of the Greek disaster story. After all, thanks to the refugee crisis and Volkswagen, Germany has a whole new set of problems to worry about. Or perhaps, it is time to find a diversion from those, and what better antagonist to focus on than the recently annexed Mediterranean colony which is the European ground zero of so many refugee adventures.

* * *

That said, the endless Greek default fiasco is no longer funny, or sad, or tragic, or exciting, or anything – the Greek people eagerly voted for their own doom; they only have themselves to blame this time.

end

(courtesy supersation95.com)

4th Largest Private Bank in Switzerland FAILS

- Post by Newsroom

- – Oct 26, 2015

- Banque Hottinger & Cie SA, a Swiss private bank headquartered in Zurich has FAILED. This is a critical and completely unexpected bank collapse.-

The Swiss Financial Market Supervisory Authority (FINMA) has initiated Bankruptcy proceedings against Hottinger because the bank is so utterly unsustainable.

Hottinger is the successor of the banking firm established in Paris by Hans-Konrad Hottinger (under the name of Banque Hottinguer). it is the fourth largest private bank in Switzerland, behind:

- Rothschild Bank

- E. Gutzwiller & Cie, Banquiers

- Union Bancaire Privée

Since its foundation in 1786 Banque Hottinguer has been very active in European economic life. For example, it took part in the creation of Compagnie Générale des Eaux, as well as that of the Insurance company Drouot (at the origin of the group AXA). Banque Hottinguer in France was sold to Credit Suisse in 1997. Banque Hottinger & Cie SA in Switzerland continued its activities independently.

end

GLOBAL AFFAIRS

Sweden Warns That Government Debt Can Be Risky… Unless It’s Swedish Government Debt

On Wednesday, Sweden’s Riksbank will announce its decision on whether to cut the repo rate further into NIRP-dom and on whether to expand QE.

Who’s excited?

Ok, so it may not sound as compelling as “US sails guided missile destroyer around man-made Chinese military outposts,” but tomorrow’s decision by Sweden’s central bank actually has serious implications for the global currency wars.

As we explained on Monday (and on several prior occasions, here and here for instance) the Riksbank is in a tough spot. They’ve driven rates into negative territory and virtually exhausted the market’s capacity to absorb central bank purchases of government bonds and yet they’re still falling behind in the race to the bottom (i.e. incipient krona strength is still jeopardizing the inflation target).

An uber dovish Mario Draghi and the attendant threat of an ECB depo rate cut in December isn’t helping matters.

And so, the Riksbank’s decision on Wednesday will be watched closely to see if Sweden will once again take a wait and see approach to the ECB or attempt to get out ahead by either cutting the repo rate or expanding the country’s already broken QE.

This is well worn territory and we’re sure we’ll be revisiting it tomorrow, so we won’t delve further into it here other than to say that if the Riksbank does expand QE, they’d better revise the list of eligible paper lest the lack of market depth for government bonds should once again cause investors to reconsider the trade off between liquidity and the benefits of frontrunning central bank asset purchases on the way to sending yields in the wrong direction.

So while we await Stefan Ingves’ decision, we thought it worthwhile to draw your attention to a particularly amusing contradiction in policy recommendations. Consider first this from Bloomberg:

Sweden has told its banks to stop pretending all government bonds are safe.

With Greece on the verge of bankruptcy numerous times over the past five years, the cat’s out of the bag: it is possible to lose money on sovereign debt. That means banks should no longer be free to operate as though that weren’t the case, according to Sweden’s Financial Supervisory Authority.

Though European regulators have been trying to address this issue, Sweden didn’t want to wait for a region-wide decision before acting, Uldis Cerps, executive director of banking at the FSA in Stockholm, said in an interview.

It makes little sense that while “sovereign risk is being priced in markets on a daily basis,” banks “would be, by the regulatory framework, allowed not to take this into account in their capital planning,” he said.

Sweden has told its four biggest banks that they can’t adopt the standardized models, which would allow them to use risk weights as low as zero on sovereign debt. Instead, they must come up with internal ratings systems and assign realistic loss probabilities to the assets. The models also need to apply to municipal debt, Cerps said.

Got that? Sweden doesn’t think banks should stick to an across-the-board policy of assigning a zero risk weighting to the sovereign debt they hold on their books because as it turns out, governments can and do default.

No argument there.

The punchline however, comes from Swedbank whose chief credit strategist notes that while banks shouldn’t always assign a 0% risk weighting to sovereign debt, when they do, they should make that debt Swedish. Again, via Bloomberg:

- 0% Risk Weight Likely for Swedish Govt Debt Post-FSA Rule: Bank

- Risk weight models for sovereign debt that Swedish FSA has required of biggest banks probably will give Swedish government bonds and rated municipal debt a 0% risk weight,Linus Thand, chief credit strategist at Swedbank, says in note.

- Says all rated municipalities currently rated AAA or AA+ with a strong implicit government backing so that even if risk weighted higher than zero, “they are still considered Level 1 from an LCR perspective and we maintain that they are attractive in such a portfolio”

So, although Sweden admits that sovereign debt is in factnot risk-free, it’s nonetheless likely to contend its own debt is without risk and not only that, the FSA will “probably” deem Swedish muni debt riskless too.

That’s extremely convenient for the Riksbank considering i) they’re targeting SEK135 billion in government bond purchases, and ii) they’ve considered expanding the list of eligible assets to muni bonds.

In other words, Sweden thinks sovereign debt can be risky – only not Swedish sovereign debt – because that would be bad – especially if you’re the Swedish central bank – and you’re buying close to the top…

Washington’s Syria “Strategy” In Complete Disarray As “Ally” Turkey Bombs US-Armed Rebels

A little over a week ago in “Full Metal Retard: US Launches ‘Performance-Based’ Ammo Paradrop Program For Make-Believe ‘Syrian Arabs’” we outlined what is perhaps the most hilarious Pentagon scheme designed to arm rebels in Syria to date (and that’s saying something).

Following the comical demise of the latest “train and equip” program, the US is out of options for supporting the opposition in Syria and so Washington decided to go back to Old Faithful: the Kurds.

But that presents a problem.

The US is now flying sorties from Incirlik and Turkish autocrat President Recep Tayyip Erdogan hates the Kurds and has gone out of his way to make it clear that Ankara doesn’t distinguish between the PKK and the YPG. For the uninitiated, here’s the problem broken down in bullet points:

- The US is flying from a Turkish airbase

- Access to that airbase came with NATO’s tacit approval of Erdogan’s move to crack down on the Kurdish PKK operating in Turkey (that crackdown is designed to bolster support for the government ahead of elections next month)

- Both the US and Turkey designate PKK as a “terrorist” group

- BUT while Ankara equates the PKK with the Kurdish rebels battling ISIS in Syria, Washington actually supports those same rebels, setting up a conflict of interest

Now clearly, this is beyond absurd. That is, Turkey only got NATOs support for the politically motivated crackdown on the PKK because Ankara agreed to bundle said crackdown with a military campaign against ISIS. But the Syrian Kurds are the most effective ground force of them all when it comes to combating Islamic State. Because those Syrian Kurds are aligned with the PKK, Turkey is effectively trying to say its army is fighting ISIS, the PKK, and YPG all at once even as both the PKK and the YPG are also fighting ISIS.

And so, in an unbelievably silly attempt to keep from angering Erdogan, the US effectively created a fictional group of “Syrain Arabs” and then claimed that YPG had formed an alliance with the made-up army. Next, Washington dropped 50 tons of ammo into the desert (literally) and claimed that the “Syrian Arab Coalition” had retrieved it. Of course it was the Kurds who actually picked it up, the Pentagon just needed a cover story to feed to Ankara in case Erdogan lost his mind. Which he did.

As noted above, all of this comes in the context of what is supposed to be a cooperative effort between the US and Turkey to fight ISIS.

When the deal was struck a few months back (following a suspect suicide bombing in Suruc that served as the pretense for Erdogan’s “war on terror”), the two countries agreed to establish an “ISIS-free zone” near Aleppo. Here’s the map:

Note that when the US-Turkey alliance was formally established, the Kurds were set to squeeze ISIS from the east and west, meaning that if Washington and Ankara had just left the YPG to their business, the “ISIS-free zone” would have probably been rid of Islamic State in a matter of months. But alas, Turkey convinced the US to tell the YPG to halt their advance and the ensuing awkwardness put Washington in a tough spot, as the US had previously backed the Kurds with airstrikes.

Well now, just days ahead of elections in Turkey which Erdogan is banking on to restore AKP’s absolute majority at the expense of popular support for the pro-Kurdish HDP, the Turkish army has now attacked the very same Kurdish fighters that the US just supplied with 50 tons of ammo two weeks ago. Here’s The New York Times:

Turkey has confirmed that it struck positions in Syria held by Kurdish militias that over the last year have become the most important allies within Syria of the American-led coalition fighting the Islamic State.

The confirmation of the strikes, which the Kurds said took place over the weekend, adds a new level of complexity to the United States’ struggle to put together a coherent strategy to fight the Islamic State in Syria. It also increases tensions between the United States and Turkey, which are nominally allies in the battle against the militant group, but whose interests diverge substantially.

In an interview on a Turkish news channel Monday night, Prime Minister Ahmet Davutoglu of Turkey did not specify when the strikes had taken place, but he said they came after Ankara warned Kurdish fighters not to move west of the Euphrates River.

“We struck them twice,” Mr. Davutoglu said.