Gold: $1135.80 down $5.70 (comex closing time)

Silver $15.41 down 16 cents

In the access market 5:15 pm

Gold $1133.70

Silver: $15.41

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very poor delivery day, registering 0 notices for nil ounces. Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 208.42 tonnes for a loss of 95 tonnes over that period.

In silver, the open interest fell by 3440 contracts despite silver being up 5 cents in Friday’s trading. The total silver OI now rests at 168,945 contracts In ounces, the OI is still represented by .844 billion oz or 120% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI fell by a rather large 7,683 to 451,117 contracts as gold was down $5.70 on Friday. We had 0 notices filed for nil oz today.

We had a huge withdrawal in gold inventory at the GLD to the tune of 2.98 tonnes / thus the inventory rests tonight at 689.28 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver,a big withdrawal of 716,000 oz in silver inventory / Inventory rests at 313.817 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fell by 3440 contracts down to 168,945 despite the fact that silver was up 3 cents with respect to Friday’s trading. The total OI for gold fell by 7,683 contracts to 451,117 contracts as gold was down $5.70 on Friday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. FRB gold report

(Harvey)

b) zero hedge discusses the above FRBNY

(zero hedge)

iii) China is dumping German bunds:

9 USA stories/Trading of equities NY

i) ISM PMI’s in the USA weakest in 3 years and totally at odds with the Markit PMI

(ISM PMI/zero hedge)

ii) Federal Co op insurance providers for Obamacare dropping like flies

(zero hedge)

iii) Fed admits that something is going on in the economy that they do not understand

(zero hedge)

iv) Goldman Sachs downgrades Valeant

(Goldman Sachs/zero hedge)

v) David Stockman takes on Valeant

(courtesy David Stockman/ContraCornerBlog)

vi Atlanta Fed lowers 4th quarter GDP from 2.5% down to 1.9%

(Atlanta Fed/zero hedge)

10. Physical stories

Let us head over to the comex:

October contract month:

INITIAL standings for November/First day notice

Nov 2/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil

|

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 contracts

nil oz |

| No of oz to be served (notices) | 293 contracts

(29,300 oz) |

| Total monthly oz gold served (contracts) so far this month | 6 contracts

600 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | nil |

Total customer deposits nil oz

we had 0 adjustment:

November initial standings/First day notice

Nov 2/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 360,783.940 oz

(Brinks) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1,082,711.58 oz

Scotia |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 11 contracts

55,000 oz) |

| Total monthly oz silver served (contracts) | 3 contracts (15,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 424,645.6 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: 1,082,711.58 oz

total withdrawals from customer: 360,783.94 oz

And now SLV

Nov 2/a withdrawal of 716,000 oz from the SLV/Inventory rests tonight at 313.817 million oz

Oct 30.no change in silver inventory at the SLV/Inventory rests at 314.532 million oz

Oct 29/a big withdrawal of 1.001 million oz from the SLV/Inventory rests at 314.532 million oz

Oct 28.2015: no change in silver inventory at the SLV//inventory rests at 315.533 million oz.

Oct 27/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 26/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 23./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 22./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 21:a we had a small addition in silver ETF inventory of 381,000 oz/inventory rests tonight at 315.533 million oz

Oct 20.2015/ no change in silver ETF/Inventory rests at 315.152 million oz

Oct 19.2016: no change in silver ETF/Inventory rests at 315.152 million oz

Oct 16/no change in silver ETF/inventory rests tonight at 315.152 million oz

Oct 15./no change in silver ETF inventory/rests tonight at 315.152

Oct 14/no change in silver ETF/silver inventory/rests tonight at 315.152 million oz

oct 13/no change in silver ETF /silver inventory/rests tonight at 315.152 million oz

:oct 12/ no change in the silver ETF/silver inventory rests tonight at 315.152 million oz

Press Release OCT 6.2015

Sprott Increases Offer for Central GoldTrust and Silver Bullion Trust

Offering an Additional Premium of US$0.10 per GTU Unit payable in Sprott Physical Gold Trust Units

and US$0.025 per SBT Unit payable in Sprott Physical Silver Trust Units

When Announced on April 23, 2015, Offers Represented a Premium of US$3.06 per GTU Unit and US$0.91 per SBT Unit for Unitholders Based on Trading Value and the NAV to NAV Exchange Ratio

Premiums as of October 5, 2015 (including the Increased Consideration) are US$1.14 per GTU Unit and US$0.61 per SBT Unit

Notice of Extension and Variation to be Filed Shortly

Offers Will Now Expire on October 30, 2015 –Unitholders Urged to Tender Now

TORONTO, Oct. 6, 2015 (GLOBE NEWSWIRE) — Sprott Asset Management LP (“Sprott” or “Sprott Asset Management”), together with Sprott Physical Gold Trust (NYSE:PHYS) (TSX:PHY.U) and Sprott Physical Silver Trust (NYSE:PSLV) (TSX:PHS.U) (together the “Sprott Physical Trusts”), today announced that it has increased the consideration payable to unitholders in connection with its offers to acquire all of the outstanding units of Central GoldTrust (“GTU”) (TSX:GTU.UN) (TSX:GTU.U) (NYSEMKT:GTU) and Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (TSX:SBT.U) (the “Sprott offers”).

Unitholders will now receive an additional premium of US$0.10 per GTU unit payable in Sprott Physical Gold Trust units and US$0.025 per SBT unit payable in Sprott Physical Silver Trust units (the “Premium Consideration”), in addition to the units of Sprott Physical Gold Trust and units of Sprott Physical Silver Trust, respectively, being offered on a net asset value (NAV) to NAV exchange basis. Based on trading values and the NAV to NAV Exchange Ratio (as such term is defined in the Sprott offers) at the time Sprott announced its intention to make the Sprott offers on April 23, 2015, the offers reflected a premium of US$3.06 per GTU unit and US$0.91 per SBT unit. The premium as of October 5, 2015, based on trading values, the NAV to NAV Exchange Ratio and the Premium Consideration, represents US$1.14 per GTU unit and US$0.61 per SBT unit, respectively. In connection with this increase in consideration, the expiry time for each Sprott offer is extended to 5:00 p.m. (Toronto time) on October 30, 2015.

“Central GoldTrust and Silver Bullion Trust unitholders have been burdened for too long by a group of trustees committed to protecting the interests of the Spicer family. It is only through the public spotlight that the variety of undisclosed fees paid to supposedly independent trustees has forced public disclosures and hollow justifications. Sprott’s offers to unitholders are compelling and momentum is building as we continue to show the clear advantages of the offers. The response of the GTU and SBT trustees has been to penalize unitholders with the burden of paying for costly lawsuits and expensive advisors to protect the Spicer family and the fees they receive. We are accordingly increasing our offer to compensate unitholders for this abuse of trust, and encourage them to take advantage of this opportunity to exchange their units for an immediate premium, and trade a management committed to entrenchment to one committed to their best interests,” said John Wilson, Chief Executive Officer of Sprott Asset Management.

Added Wilson, “We have provided extensions to the offers so that no unitholders are left without this opportunity to exit an underperforming investment and enter into a high quality security that functions as intended, reflecting the value of the bullion held in the trust. Sprott appreciates the support of GTU and SBT unitholders to date and currently anticipates these extensions will be the final extensions to the Sprott offers.”

As of 5:00 p.m. (Toronto time) on October 5, 2015, there were 8,194,265 GTU units (42.46% of all outstanding GTU units) and 2,055,574 SBT units (37.60% of all outstanding SBT units) tendered into the respective Sprott offers. Total units tendered as of October 5, 2015, do not include pending units which are typically received on the date of expiration.

GTU and SBT unitholders who have questions regarding the Sprott offers, are encouraged to contact Sprott Unitholders’ Service Agent, Kingsdale Shareholder Services, at 1-888-518-6805 (toll free in North America) or at 1-416-867-2272 (outside of North America) or by e-mail atcontactus@kingsdaleshareholder.com.

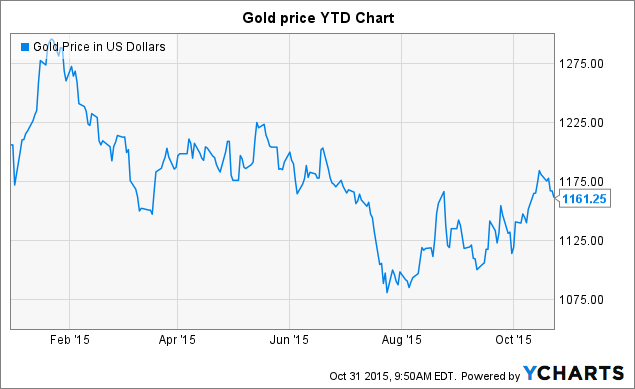

Gold Selling “Malevolent Force”? – Dennis Gartman

Dennis Gartman, author of the institutionally well followed ‘The Gartman Letter,’ has asked questions about gold’s peculiar price action last week and raised the question as to whether there was official central bank manipulation of gold prices.

Gold was 2.4% higher in October but fell 2% last week as the Fed again suggested they may soon increase interest rates. Gartman’s assertion is significant as he is no so-called ‘goldbug’. In fact, he is the darling of Wall Street, Bloomberg, CNBC and is highly respected and followed by large hedge funds and financial institutions.

Gold in USD – 1 Month

He has been bearish on gold in recent months but the recent turmoil in currency markets has Gartman bullish on gold also in dollar terms since August.

“I think for the first time in a while, you can actually say the lows may have been in dollar-dominated gold,” Dennis Gartman told CNBC’s “Fast Money.”

Gartman is on record regarding his belief that gold is in a long term bull market in all currencies.

Here is the key extract regarding potential gold manipulation from the Gartman Letter on Friday:

“As for the precious metals, the selling late Wednesday and all day yesterday was indeed severe, and even our positions in gold/euro and gold/yen have seen severe damage wrought upon them.

We find it hard to believe that the mere suggestion by the Federal Open Market Committee in its post-meeting communique on Friday that “liftoff” on the overnight Fed funds rate may take place at its December meeting can be responsible for this sort of egregious, serious, and now relentless selling, and we are almost of the mindset associated with the likes of the gold bugs and GATA that some malevolent “force” was behind the selling.

However, we are not going to travel down that road at the moment and sit tight with our positions, believing that the continued “experiments” with QE undertaken by the Bank of Japan and the European Central Bank shall work to the detriment of their currencies and to the support of gold. Nonetheless, the last 36 hours have been terribly dismaying …”

GoldCore Note: As ever, we view such manipulation as an opportunity for investors as it allows them to accumulate gold at artificially depressed prices.

The history of manipulation of the gold market is of short term success followed by ultimate failure and then much higher prices as was seen after the failure of the “London Gold Pool” in the late 1960s and gold’s massive bull market in the 1970s.

The golden beach ball has been pushed near the bottom of the ‘gold pool.’ The lower it is pushed in the short term, the higher it will surge in the long term.

DAILY PRICES

Today’s Gold Prices: USD 1135.80 , EURO 1030.86 and GBP 733.86 per ounce

Friday’s Gold Prices: USD 1147.75, EUR 1042.70 and GBP 748.04 per ounce.

(LBMA AM)

Gold closed at $1141.50 on Friday a loss of $4.30 and -1.98% overall for the week. Silver lost $0.08 to close at $15.52, showing a -2.14% loss for the week. Platinum lost $6 to $982.

Gold fell 2% last week as the Fed again suggested they may soon increase interest rates. However, it was 2.4% higher in October due to strong demand for physical gold bullion globally and especially in Germany, India and China.

We are now entering gold’s seasonal sweet spot from early November to the end of February as we enter the Indian festival and Chinese New Year periods.

Download Essential Guide To Storing Gold Offshore

FRBNY report came out today Oct 31.2015 ( two days late)

Withdrawals Of Gold From NY Fed Jump To 20 Tons In September, Total 276 Tons Since 2014

First it was Germany who redeemed 120 tons of physical gold in 2014; then it was the Netherlands who “secretly” redomiciled 122 tons of gold; then this past May, we learned that Austria would be the third “core” European nation to repatriate most of its offshore gold, held primarily in the Bank of England, redepositing it in Vienna and Switzerland.

Thanks to the latest NY Fed data released yesterday, we now know that beginning in 2014 and continuing through yesterday, the gold “bleeding” from the vault located 90 feet below street level at 33 Liberty Street (and which may or may not be connected by a tunnel to the JPM gold vault located just across the street at 1 Chase Manhattan Plaza) is not only continuing but accelerating.

As the chart below shows, while central banks assure the population that there is nothing to worry about when it comes to paper money, and in fact it is the evil ISIS terrorists who plot and scheme to crush the benevolent Fed with their terroristy “gold dinars” and if not that then their made in Hollywood propaganda movies, they have been quietly pulling gold from the biggest centralized depository of global gold in the world: the New York Federal Reserve.

According to the latest just released monthly update of foreign official assets held in custody at the NY Fed, in July the total holdings of foreign earmarked, i.e., physical, gold declined to just over $8 billion when evaluated at the legacy “price” of $42.22 per ounce. In ton terms, this means that after declining below 6000 tons in January, for the first time since FDR’s infamous gold confiscation spree…

… the total physical gold held at the NY Fed dropped another 19.9 tons in September, down to 5,919.5 tons.

This was a doubling in gold withdrawals from 10 tons in August, and

is the highest withdrawal since January.

At just under 5,920 total tons in NY Fed inventory, this is the lowest amount of gold held in NY Fed custody in decades, and is the 20th consecutive month of flat or declining gold, and when added to previous outflows, amounts to 199 tons of gold withdrawn in the past 12 months, and a whopping 276 tons pulled since the start of 2014.

Indicatively, during the last crisis period, starting in March 2007 and lasting through November 2008, foreign central banks withdrew gold for a total of 20 out of 21 consecutive months, repatriating a grand total of 409 tons of gold. The last period of peak redemption culminated with the failure of Lehman in September 2008, the near failure of AIG in October and November 2008, coupled with the Fed’s bailout of the western financial system.

If past is prologue, one should ask: what current or future event is driving the ongoing redemption of gold from the NY Fed this time?

Russia’s VTB Bank Joins As SGE Member. Chinese Direct Gold Imports Increase

Another strong week for gold demand at the Shanghai Gold Exchange – China’s main physical gold bourse. From 19 until 23 October 57 tonnes have been withdrawn from the vaults of the Shanghai Gold Exchange (SGE), according to data released on Friday by the SGE. Year to date 2,119 tonnes have been withdrawn. With a little over two months left in 2015 SGE withdrawals, which capture the amount of Chinese wholesale gold demand, are set to reach more than 2,500 tonnes in 2015, breaking the record of 2013 at 2,197 tonnes.

SGE withdrawals have made a spectacular run up this year since the Chinese stock market came crumbling down in June. In between June and October SGE withdrawals have been 1,138 tonnes, up 37 % year on year.

The People’s Republic of China does not publish the amount of gold imported, however, from foreign trade statistics provided by other nations and physical turnover at the SGE we can estimate China will net import at least 1,300 tonnes of gold in 2015 – transcending net import in 2014, which was an estimated 1,250 tonnes.

Whilst the SGE releases withdrawal data every week, foreign trade statistics are released on a monthly basis. Wholesale gold demand in China mainland was elevated in recent months, but it always remains to be seen exactly how much gold was net imported in order to supply the SGE.

Let’s have a look at what gold trade data has already been released for the past months: Switzerland has net exported 21.69 tonnes of gold to China in September – up 28 % month on month – according to the most recent data from the Swiss Customs department. This is the largest amount of gold export to China from Switzerland in six months.

Trade data from the Hong Kong Census And Statistics Department has not yet officially been released, but Reuters gave us a sneak preview. Net export from Hong Kong to China mainland in September was 97 tonnes, up 63 % month on month and the largest amount of gold export to China in ten months.

Foreign Trade statistics from the UK and other major gold trading hubs has not yet been published. Although not all gold trade data can be collected, we can see in the chart below, that displays currently known Chinese physical gold supply, gold import into China is steadily rising along side strong SGE withdrawals.

As usual, apparent physical gold supply in China is much more than what the mainstream media would like you to believe. Most notably, since 2013 gold supply in China has been thousands of tonnes more than what consultancy firms like the World Gold Council and GFMS disclose as Chinese gold demand. On the LBMA conference in Vienna (18 – 20 October) it was discussed, again, that Chinese Commodity Financing Deals are the sole reason for the missing gold in China.

This is not true. Chinese Commodity Financing Deals (CCFDs) with respect to gold can be either conducted throughround tripping or gold leasing. Round tripping has got nothing to do with the Chinese domestic gold market and gold leasing can never have ‘swallowed’ a few thousand tonnes of gold from reaching genuine demand. Because the myths about CCFDs keep being repeated I will write a new extensive post on CCFDs.

VTB Bank Has Been Granted SGE Member Status

On the website of VTB Bank it was announced it has been granted SGE member status, with the right to participate in trading on the Shanghai International Gold Exchange (SGEI). VTB is the first Russian bank to enjoy member status of the Chinese exchange.

Russia has hardly been exporting non-monetary gold directly to China in recent years. Now VTB is an SGE member this will change, as Russian banks are often the exporters of mined gold of Russian mining companies. I will closely watch the foreign trade statistics provided by Russia’s customs department.

“Access to trading on China’s domestic precious metals market will give VTB Bank, which also trades on Western exchanges, more opportunities to sign gold deals in Shanghai. As an important element of our Chinese strategy, we continue working to develop the bank’s business and that of our clients in the Shanghai Free Trade Zone.…” saidHerbert Moos, Chairman of VTB Bank’s Management Board.

The biggest part of Russia’s mining output is sold to VTB and Sberbank, who sell it to the Russian central bank and foreign buyers – according to newswire EM Goldex.

Russia’s largest gold mining company Polyus Group, that mined 53 tonnes in 2014, announced in early May it would start cooperating with China’s largest mining company China National Gold Group Corporation in resource exploration, technical exchanges and materials supply. Shortly after, we learned this cooperation is part of theSilk Road economic project that was initiated by China.

Polyus sells the lion share of its mine output through Russian banks. If we look at the 2014 Polyus Annual Report we can see it sold most if its gold (38 %) through VTB Bank.

In 2014 Polyus sold gold valued at 841 million US dollars through VTB Bank. In the past this gold has probably not been sold directly to China or through the SGEI. This is about to change since VTB is now SGE member.

VTB Bank’s SGE membership is significant, as it can been seen as more cooperation in the gold industry on the Eurasian continent along the Silk Road between Russia and China.

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

TF Metals Report on Comex fraud; Maguire sees division among bullion banks

Submitted by cpowell on Fri, 2015-10-30 20:20. Section: Daily Dispatches

3:20p CT Friday, October 30, 2015

Dear Friend of GATA and Gold:

The TF Metals Report’s Turd Ferguson today explains again how the Comex gold futures market is fraudulent:

http://www.tfmetalsreport.com/blog/7241/futures-market-fraud

And London metals trader Andrew Maguire tells King World News that a split is developing among London bullion banks, as some of the banks are concluding that the paperizing scheme of bullion banking is running out of time:

http://kingworldnews.com/andrew-maguire-this-historic-event-is-about-to-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This is huge news: Andrew Maguire who is well versed in affairs with respect to LBMA as he is a member comments that Goldman Sachs + other cartel members are separating itself from the gold cartel, namely the bullion bankers JPMorgan and HSBC

Andrew Maguire – This Historic Event Is About To Shock The World And The Gold Market

Today whistleblower and London metals trader Andrew Maguire gave one of his most important interviews ever. Maguire warned King World News about a stunning event that is going to shock the world and the gold market.

October 30 – (King World News)

Andrew Maguire: “Eric , there is so much going on under the radar in the gold and silver markets. If you recall, I made a prediction that gold and silver would end the year strong and I am still a firm believer that they will…

We can see by the current stale-dated published Commitment of Traders (COT) open interest structure that gold is at a similar bearish structure as the January highs, and a lot has been made of this. However, there are differences. This time, the downside range scale is limited by strong seasonality, tight supply, rising wholesale bid interest, the FED backed into a corner, ECB QE, and the concern of more Chinese rate cuts, etc.

But a much more important factor is flying under the radar — namely, a division between the two primary market making bullion banks, (who have vaulting operations here in London), and the rest of the collusive bullion bank cabal. This is a definite game-changer and a very big deal that will begin to unwind a 30-year collusive relationship.

A Crack In The Cabal’s Resolve

I have been hearing reliable rumors of this split since mid-June, but the LBMA conference last week exposed this crack in the cabal’s resolve to continue to work together. In order to assess the immediate impact of this split, it is best to first take a look at the cabal’s history and mechanisms, and then analyze how this split in their ranks is about to challenge the historical wash and rinse setups.

The Gold cabal was born under the wing of Robert Rubin, who ran the gold trading desk at Goldman Sachs in the 1980’s.

This is when the gold carry trade was born, which given the large interest differentials between gold and Treasuries at that time, was a slam dunk win for Western central banks looking to contain gold vs the dollar, while drawing the proceeds of the sale of large tranches of central bank leased gold flowing through the bullion banks into Treasuries. This created the synthetic markets as we see them today. The result of being subsidized through the central banks gave the green light for the bullion banks and central banks to leverage up a multi-billion dollar fractional-reserve gold position they never thought would need to be unwound.

The primary bullion banks, acting as agents for the central banks, who have had a free pass to naked short large volumes of synthetic gold and over a long period of time, became accustomed to exploiting the advantages of colluding together to create and protect mutually beneficial position concentrations in the paper gold and silver markets. In the process, they accrued an embedded naked short position that they thought could be infinitely rolled forward. This created a fractional reserve gold/silver position that directly mirrored the cash banking system, where it is assumed that not more than 10% of cash depositors at any one time would ever ask for the money they had deposited back…

Unallocated gold accounts are also deemed to be cash investments in the receiving bank, giving the gold investor no right to ever receive delivery. The bullion banks operating these fractional-reserve gold positions are geared even more aggressively than their more tightly regulated cash banking operations. These multi billon dollar unallocated gold accounts were independently verified in a Reserve Bank of India report to be leveraged at a 92/1 level, far greater than the 10/1 governing other banking operations.

When analyzing many years of positioning data in the COT report, the footprints are easy to read. And when connecting the dots through the options and OCC reports, it is well established that the two primary market making bullion banks that have vaulting operations — HSBC and JPM — have for many years primarily worked directly in synch with the four non-vaulting market-making bullion banks, who are also privileged to operate gold bank accounts with the Bank of England.

This small cabal of bullion banks operating with the blessing and insider advantages of acting as agents for Western central banks, have concentrated their mutually agreed positioning against a very diverse range of hedge funds and speculators who are easy to pick off, as they are not coordinated. The resulting action is what I refer to and is now commonly known as ‘the Wash and Rinse Cycle.’

What Is Changing Will Shock The World

So what is changing? The physical element to this synthetic open interest positioning is changing the critical point where the paper market rubber hits the physical road. In fact, the physical markets have already migrated out of the hands of these few collusive bullion banks. But with regulators now finally forced to act against a full range of gold and silver market manipulation cases, this is resulting in an exit of traditional liquidity providers. These were the banks financing the unallocated markets. Right now, critical liquidity is exiting the Loco London market, and this is unprecedented.

This is where the split is occurring. The two primary bullion banks, who have large vaulting operations here in London, are also the primary agents for the central banks who want to keep the OTC gold trade opaque and off a proposed centrally-cleared exchange.

Synthetic Gold Market House Of Cards To Collapse

However, the aggressive and predatory bullion banks that largely infest the swap dealer category of the COT report recognize the gold market has changed and are about to split ranks and reposition more bullishly, a position they would already have if they had not accrued such large underwater proprietary positions. The head of this pack of wolves is Goldman Sachs. These banks read the changes coming and see an incentive to compete against the two primary bullion banks forced to keep this game going for as long as possible. This is a big deal because without collusive cooperation of all of the cabal, the whole synthetic gold market house of cards collapses.

This market change is now underway. The glass is cracked and cannot be repaired. Goldman Sachs and at least ten other trading banks are breaking rank because they see the writing on the wall and are pre-positioning for a post-cash settlement. And once released from their underwater unallocated gold liabilities, they will benefit from an embedded long position in physical as well as paper gold.

No one understands the bifurcation of the capped synthetic markets and underpriced physical markets better than these trading banks. JP Morgan has already cornered the silver physical market and Goldman Sachs plans to front-run the increasingly illiquid paper gold market against its rival bullion banks. This split in the ranks will speed up…To continue listening to the incredible audio interview with London metals trader and whistleblower Andrew Maguire, where he discuses the great unwind that is going to take place in the gold and silver markets, what traders should expect next, and where gold and silver prices are headed, CLICK HERE OR ON THE IMAGE BELOW.

end

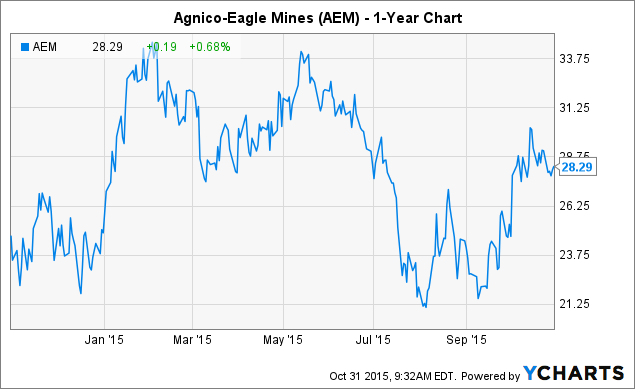

With all gold mines having trouble with the low price of gold/silver yet costs rising, Agnico Eagle is perhaps the best run company struggling with all the hardships thrown at them.

(courtesy seeking alpha)

Summary

Agnico-Eagle released its third-quarter results on October 28, 2015 which was followed by a conference call. Again a solid and impressive quarter.

Agnico-Eagle is delivering a strong production, thereby generating an operating cash flow of $143.7 million this quarter — in spite of a gold price at record low of $1,119/ Oz.

I recommend AEM as a buy and accumulate on any weakness.

Agnico Eagle Mines Ltd.(NYSE:AEM)

Source: Meadowbank picture taken from company website.

This article is following a preceding article on AEM published on Sept. 21, 2015, about the company update on its Mexican operations and a quick look at the 2Q’15 results.

A Quick Q3’15 Financial Snapshot:

| Q3 2015 | Q2 2015 | Q1 2015 | Q4 2014 | Q3 2014 | |

| Revenue

in $ million |

508.795 | 510.109 | 483.596 | 503.1 | 463.388 |

| Gold Production

in Oz |

441,124 | 403,678 | 404,210 | 387,538 | 349,273 |

| Realized gold price

in $ |

1,119 | 1,196 | 1,202 | 1,202 | 1,249 |

| Cash provided by operating activities

in $ million |

143.7 | – | – | – | 71.2 |

| Net income

$ Million |

1.29 | 10.08 | 28.7 | (21.3) | (15.1) |

| Adjusted Net income

$ Million |

39.2 | – | – | – | – |

| EPS – basic | 0.01 | 0.05 | 0.13 | (0.10) | (0.07) |

| Adjusted EPS | 0.18 | – | – | – | – |

| AISC (by-product)

$/Oz |

759 | 864 | 804 | 954

(2014) |

1,059 |

| CapEx

in $ million |

72.0 | 81.9 | 82.9 | 133.4 | – |

| Cash and Cash equivalent (including restricted cash)

in $ Million |

208.1 | 158.3 | 172.1 | 215.3 | 164.0 |

| Outstanding Debt

in $ Million |

1,203.3 | 1,180.3 | 1,220.1 | 1,322.5 | – |

| Dividend per share

In $/share |

0.08 | 0.08 | 0.08 | 0.08 | 0.08 |

| Shares outstanding

in million |

217.2 | 215.426 | 214.6 | 213.3 | – |

Available credit facilities:

The outstanding balance on the Company’s $1.2 billion credit facility was reduced from $375 million at June 30, 2015 to $350 million at September 30, 2015. This results in available credit lines of approximately $850 million, not including the $300 million accordion facility.

TB1 – Payable production per quarter and per metal:

| Gold

Oz |

Silver

K Oz |

Zinc

Tonne |

Copper

Tonne |

|

| Q3 2015 | 441,124 | 1,037 | 650 | 1,302 |

| Q2 2015 | 403,672 | 1,106 | 733 | 1,131 |

| Q1 2015 | 404,210 | 1,032 | 936 | 1,167 |

| Q4 2014 | 387,538 | 1,043 | 2,467 | 1,399 |

| Q3 2014 | 349,272 | 830 | 2,225 | 989 |

| Q2 2014 | 326,058 | 870 | 3,788 | 1,060 |

| Q1 2014 | 366,420 | 890 | 2,060 | 1,554 |

TB2 – Breakdown of the geographical distribution of the three-year future gold production:

| Canada | Europe | Mexico | |

| % gold production | 70 | 10 | 20 |

TB3 – Production and cost/cash cost per segment.

| Mine | Total production cost per Mine

in $ |

Production of gold

Oz |

Cash cost

on a By-product basis $/Oz |

|

| LaRonde | 2Q’15 | 45,133 | 64,007 | 613 |

| 3Q’15 | 49,243 | 71,860 | 558 | |

| Lapa | 2Q’15 | 13,656 | 19,450 | 678 |

| 3Q’15 | 12,279 | 25,668 | 522 | |

| Goldex | 2Q’15 | 16,913 | 26,462 | 633 |

| 3Q’15 | 16,120 | 32,068 | 479 | |

| MeadowBank | 2Q’15 | 66,888 | 91,276 | 688 |

| 3Q’15 | 57,404 | 99,425 | 598 | |

| Canadian Malartic | 2Q’15 | 42,185 | 68,441 | 609 |

| 3Q’15 | 42,008 | 76,603 | 544 | |

| Kittila | 2Q’15 | 30,777 | 41,986 | 776 |

| 3Q’15 | 31,116 | 46,455 | 639 | |

| Pinos Altos | 2Q’15 | 29,768 | 50,647 | 384 |

| 3Q’15 | 26,845 | 47,725 | 392 | |

| Creston Mascota | 2Q’15 | 7,501 | 15,606 | 402 |

| 3Q’15 | 6,101 | 12,716 | 436 | |

| La India | 2Q’15 | 10,791 | 25,803 | 410 |

| 3Q’15 | 13,468 | 28,604 | 436 | |

| TOTAL 3Q’2015 | 254,584 | 441,124 Oz | $536

AISC $759 |

|

| TOTAL 2Q’2015 | 263,612 | 403,672 Oz | ||

| TOTAL 1Q’2015 | 247,280 | 404,210 Oz |

Revised 2015 Guidance – Production Increased and Costs Lowered — from the press release.

As a result of strong operational performance in the third quarter of 2015, production guidance for 2015 has been increased to approximately1.65 million ounces of gold (previously 1.6 million ounces) with total cash costs on a by-product basis of approximately $590 to $610 per ounce (previously $600 to $620) and AISC of approximately $840 to $860 per ounce (previously $870 to $890).

Commentary:Agnico-Eagle released its third-quarter results on October 28, 2015 which was followed by a conference call. Again a solid and impressive quarter.

I will not comment again on the results that I have displayed in detail above. Just one simple conclusion is that the numbers were impressive, and covering every segment. Production increased by 9.3% quarter over quarter, while AISC went down to $759/ Oz.

Production has been strong in the Abitibi, particularly for the Canadian Malartic, and the company decided to increase production guidance to another50K Oz with an AISC at $850 for 2015, despite some lower mining grade in Meadowbank mine.

The two projects that are being developed now, are the Barqueno project in Mexico and the Nunavut at Amaruq (Satellite of Meadowbank operations).

In short, Agnico-Eagle is a Canadian gold miner with a clear future potential, that delivers a steady production at low costs.

Unlike, Barrick Gold (NYSE:ABX) for example, that I covered yesterday, which seems “too big” and cumbersome with a large debt, the AEM shareholders can grasp, in a few minutes, the entire AEM mining model and its basic strategy.

It is a very important detail for an investor like me, who wants to invest in a gold mining industry, and add a few strong leaders in his portfolio, with a time horizon of a few years.

Agnico-Eagle is delivering a strong production — See Tab3 — and even increased its production guidance for 2015 again, thereby generating an operating cash flow of $143.7 million this quarter — in spite of a gold price at record low of $1,119/ Oz. This is nearly a double year over year, and while paying a 1.1% per year dividend. The debt of $1.2 billion is also very manageable.

Of course, nothing is perfect, especially when we are talking about gold, and investment in gold has not been the best return on investment (‘ROI’) lately, and for the past two years as a matter of fact. The jury is still out for 2016, and analysts seem divided on the direction of the gold price.

However, it is very important to have a “presence” in the gold sector, through a good quality gold miners like AEM or Newmont Mining (NYSE:NEM) that Icovered yesterday, because the market is essentially cyclical, which means that this segment in your portfolio, will turn to profit, in due time.

Thus, a good balanced portfolio with a long-term perspective is paramount, and to build-up such a winner requires to recognize the true leaders, when they are still cheap and not so appealing.

If we look at the 1-year Chart, we can see what I mean.

Conclusion:

AEM is a well managed gold miner that should be part of your long portfolio. I recommend AEM as a buy and accumulate on any weakness.

(courtesy Mike Kosares/GATA)

Mike Kosares: You will hear the roar of the printing presses from Mars

Submitted by cpowell on Sat, 2015-10-31 18:19. Section: Daily Dispatches

1:15p CT Saturday, October 31, 2015

Dear Friend of GATA and Gold:

Gold prices and bond yields, USAGold’s Mike Kosares writes today, are “telling us that the global economy is in the grip of disinflation and perhaps on the verge of going over the cliff — to a full-blown deflation.” Kosares agrees with the analysis who says that, as central banks respond, “you will hear the roar of the printing presses from Mars.” Kosares’ commentary is headlined just that — “You Will Hear the Roar of the Printing Presses from Mars” — and it’s posted at USAGold’s Internet site here:

http://www.usagold.com/cpmforum/2015/10/31/you-will-hear-the-roar-of-the…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy Chris Powell/GATA)

Martin Armstrong is too brilliant to understand that time is money

Submitted by cpowell on Sun, 2015-11-01 05:07. Section: Daily Dispatches

12:14a CT Sunday, November 1, 2015

Dear Friend of GATA and Gold:

Claiming breathtaking omniscience with his latest commentary, the economist and market analyst Martin Armstrong asserts that market manipulation is nothing to worry about and that complaints of manipulation of the gold market are nonsense.

Armstrong’s commentary —

http://www.armstrongeconomics.com/archives/38757

— is headlined “Market Manipulations: The Greatest Scam of All Time,” that headline being his first claim to omniscience, a claim to comprehensive knowledge of every scam in history:

He elaborates: “Throughout history, there has never been a market manipulated to alter its long-term trend — period.”

Armstrong thereby claims comprehensive knowledge of every market going back to caveman times when Og of the Rock People became the first commodity trader, offering to sell his tribe 10 pterodactyl feathers he didn’t own in the hope that this would intimidate Zug to reduce the price of the feather he was trying to exchange for a dozen mastodon-bone fish hooks, Og having only five fish hooks to trade.Armstrong’s knowledge may be especially impressive because no record of Og’s trade was kept. But Armstrong claims to know the history of all markets for thousands of years before records were kept.

Armstrong’s commentary then descends to a lot of chest thumping about how two decades ago he was right about the silver market when some other bigshots were wrong. Apparently this assertion too is supposed to be dispositive about everything in history.

Armstrong’s mighty conclusion: “There is no secret plot to keep gold down to pretend inflation is lower.”

Armstrong thereby claims to know the minds of every market participant in the world, from central bankers right down to the Chinese “aunties” trying to put a little metal away for the grandchildren.

In the old days an assertion like the ones Armstrong makes was called an “ipse dixit,” Latin for “he himself said it,” as if the speaker presumed that his authority would be taken for granted without the slightest need for evidence. Armstrong may be a prodigy but he didn’t invent the swelled head. He’s just wearing one.

One doesn’t need to be omniscient like Armstrong to note the flaw in his premise: “Throughout history, there has never been a market manipulated to alter its long-term trend — period.”

That is, for starters, Armstrong fails to define his terms. For what is a “long-term trend” and what is a “short-term” one? And even if Armstrong defined those terms, would those definitions necessary hold for other people?

Armstrong acknowledges the possibility of short-term market manipulations contrary to long-term trends. He cites Soviet communism, a vast market manipulation that destroyed markets altogether. He might not deny that the U.S. government held the gold price at $20.67 and then $35 an ounce for many years, preventing any market in gold from developing.

Yes, market pressures helped bust Soviet communism as well as the U.S. dollar’s gold peg and a lot of other market manipulations, and the prices that followed might be called vindication of the “long-term trend.” But vindication for what and for whom?

For as Keynes noted, thinking of people like Armstrong: “The long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can tell us only that when the storm is past the ocean is flat again.”

After all, while Armstrong may consider the history of the Soviet Union to have been short-term, it nevertheless encompassed 70 years and damaged or ruined millions of lives. Even a market manipulation of much shorter duration — a few weeks or months, or just a few days — can cheat people substantially and do great harm.

Transcending space and time, Armstrong is too brilliant to understand that for mere mortals time is money. His empty pontifications evoke Mark Twain: “The less a man knows, the bigger the noise he makes and the higher the salary he commands.”

Armstrong’s analysis of the gold market — indeed, given the gold market’s connection to other major markets, his analysis of all markets — would be more useful if it addressed these questions:

— Are central banks in the gold market surreptitiously or not?

— If central banks are in the gold market surreptitiously, is it just for fun — for example, to see which central bank’s trading desk can make the most money by cheating the most investors — or is it for policy purposes?

— If central banks are in the gold market for policy purposes, are these the traditional purposes of defeating a potentially competitive world reserve currency, or have these purposes expanded?

— If central banks, creators of infinite money, are surreptitiously trading a market, how can it be considered a market at all, and how can any country or the world ever enjoy a market economy again?

Of course just a week ago another central banker actually volunteered that certain central banks are intervening in the gold market surreptitiously even as they are trying to increase their gold reserves, the intervention apparently meant to help keep the price down to facilitate their acquisition of gold:

http://www.gata.org/node/15878

http://www.gata.org/node/15892

http://www.gata.org/node/15897

http://www.gata.org/node/15898

More documentation responsive to these questions can be found in GATA’s archive here:

http://www.gata.org/node/14839

A summary of that documentation and the history behind it is in GATA’s archive here:

http://www.gata.org/node/14839

In his omniscience Armstrong may dismiss this stuff as being from another universe, but those who live in that universe may find it useful.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Ronan Manly and I both agree, that Venezuela has lost all of its gold reserves.

(courtesy Ronan Manley/Bullionstar.com)

Ronan Manly: Venezuela says adios to its gold reserves

Submitted by cpowell on Sun, 2015-11-01 05:58. Section: Daily Dispatches

12:57a CT Sunday, November 1, 2015

Dear Friend of GATA and Gold:

Venezuela lately has probably sold, leased, swapped, or otherwise encumbered more gold than reported, gold researcher Ronan Manly writes today after a painstaking review of the records of the country’s central bank.

Venezuela’s gold reserves, Manly writes, fell by about 61 tonnes from February to April even though the International Monetary Fund and World Gold Council did not note the decline. This decline, Manly writes, was distinct from the gold swap Venezuela was reported to be undertaking with Citigroup and might have been a sale to other investment banks or even to China.

Shipping documents at the Caracas airport, Manly adds, suggest strongly that more gold from the central bank’s vaults was flown to Europe in July.

Manly concludes that Venezuela’s gold reserves may be substantially lower than analysts believe are available to help service the country’s external debt into 2016 and indeed may already be oversubscribed.

Manly’s analysis is headlined “Venezuela Says Adios to Her Gold Reserves” and it’s posted at the Bullion Star blog here:

https://www.bullionstar.com/blogs/ronan-manly/venezuela-says-adios-to-he…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy Egon von Greyerz/GATA)

Central banks’ only policy is to inflate money supply, von Greyerz tells KWN

Submitted by cpowell on Mon, 2015-11-02 00:51. Section: Daily Dispatches

7:50p ET Sunday, November 1, 2015

Dear Friend of GATA and Gold:

The stock market is dictating Federal Reserve policy, gold fund manager Egon von Greyerz tells King World News today, and as a result the Fed and other central banks really have no policy at all except to keep expanding the money supply to support the markets while using derivatives to suppress the gold price. He credits GATA for producing “innumerable pieces of proof” of gold price suppression by central banks. An excerpt from von Greyerz’s interview is posted at the KWN blog here:

http://kingworldnews.com/get-ready-for-the-total-destruction-of-the-fina…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

1 Chinese yuan vs USA dollar/yuan falls , this time at 6.3365 Shanghai bourse: in the red, hang sang:red

2 Nikkei down 399.65 or 2.08%

3. Europe stocks mostly in the green /USA dollar index up to 96.87/Euro up to 1.1013

3b Japan 10 year bond yield: rises to .316% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.64

3c Nikkei now just above 18,000

3d USA/Yen rate now just above the important 120 barrier this morning

3e WTI: 45.80 and Brent: 48.73

3f Gold down /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .516 per cent. German bunds in negative yields from 6 years out

Greece sees its 2 year rate rises to 8.91%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 7.91% (yield curve inverted)

3k Gold at $1137.60 /silver $15.42 (8:00 am est)

3l USA vs Russian rouble; (Russian rouble down 3/10 in roubles/dollar) 64.25

3m oil into the 45 dollar handle for WTI and 48 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9865 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0867 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 6 year German bund now in negative territory with the 10 year rises to +.516%/German 6 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.17% early this morning. Thirty year rate below 3% at 2.95% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Rebound From Overnight Lows On Stronger European Manufacturing Surveys, Dovish ECB

On a day full of Manufacturing/PMI surveys from around the globe, the numbers everyone was looking at came out of China, where first the official, NBS PMI data disappointed after missing Mfg PMI expectations (3rd month in a row of contraction), with the Non-mfg PMI sliding to the lowest since 2008, however this was promptly “corrected” after the other Caixin manufacturing PMI soared to 48.3 in October from 47.2 in September – the biggest monthly rise of 2015 – and far better than the median estimate of 47.6, once again leading to the usual questions about China’s Schrodinger economy, first defined here, which is continues to expand and contract at the same time.

Unrelated to China’s PMI, was the biggest plunge in the onshore Yuan which after soaring the most since 2005 on Friday (followed by the appropriate surge in the fix overnight) proceeded to tumble by nearly 0.5%, the biggest plunge since the Yuan devaluation, on even more PBOC intervention. This followed a statement that China’s central bank is finalizing revisions to its foreign-exchange rules that would loosen some capital controls while preserving its ability to intervene in times of volatility, according to people familiar with the matter. In other words, keep its SDR cake while eating “malicious short sellers” too and intervening at will.

Certainly unrelated to China’s PMI, but even more market moving, was overnight news that Chinese authorities had arrested China’s “Carl Icahn”, Xu Xiang on insider trading charges, head of the $1.5 billion Zexi Investment fund (with concurrent news from both China National Radio and Xinhua that his partner Wu Shuang had been shot by local police after attempting to flee from arrest). Here are the highlights from Bloomberg’s report:

Shanghai police raided hedge fund Zexi Investment on Sunday, taking away computers and other materials, according to a person familiar with the matter, in the latest attempt by Chinese authorities to crack down on strategies blamed for exacerbating a $5 trillion stock-market rout.

Xu Xiang, the general manager of top-performing Zexi, was detained on charges including insider trading and stock manipulation, the official Xinhua news agency reported. Two executives at Jiangsu-based Yishidun International Trading and the technical director at Shanghai-based Huaxin Futures were arrested after a police investigation showed they made 2 billion yuan ($316 million) in “illegal profit”, Xinhua reported separately, citing the Ministry of Public Security. Agricultural Bank of China Ltd. President Zhang Yun was taken away to assist authorities with an investigation, people familiar with the matter said on Monday, who didn’t give details.

Highlighting the tense environment sparked by the probes, Chinese social media was set abuzz Monday morning by an unconfirmed report of a man associated with the insider trading probe who was shot and killed by police while trying to escape apprehension. The report was retracted less than an hour after being posted to various websites, including that of China National Radio. A person at China National Radio’s news department, who refused to give their name, said the police had informed the broadcaster that the information was untrue.

One easy way to confirm whether or not Wu is alive: present him to the public. Somehow we doubt this will happen.

Continuing the overnight news, following China’s bad/good PMI data, it was Europe’s turn where at least the manufacturing surveys are improving, if not the economy, which sadly is the reason why Draghi is preparing to unleash even more QE. Specifically, the Final October Manufacturing PMI printed 52.3, vs Ex. 52.0 and a Previous print of 52.0.

Here was Goldman’s rundown:

BOTTOM LINE: The final Euro area manufacturing PMI came in at 52.3 in October, 0.3pt above the flash estimate. With this revision, the Euro area manufacturing PMI gained 0.3pt on the month. On a country basis, the German manufacturing PMI edged down on the month by 0.2pt, while the Spanish PMI fell by 0.4pt. The French PMI was flat, and the Italian PMI experienced a robust gain of 1.4pt.

- The final Euro area manufacturing PMI came in at 52.3 in October, 0.3pt above the flash. Relative to the flash, the German manufacturing PMI was revised up (from 51.6 to 52.1), whilst the French reading was revised down marginally (from 50.7 to 50.6). Between September and October, the Euro area manufacturing PMI rose by 0.3pt (Exhibit 1).

- The PMI breakdown across subcomponents in October was mixed. Manufacturing output rose (+0.2pt to 53.6), whilst employment fell (-0.5pt to 51.1). The order-to-stock difference fell marginally by 0.4pt in October, reflecting a large increase in the stocks of finished goods.

- On a country basis, following the upward revision, the German manufacturing PMI now only fell slightly on the month (from 52.3 to 52.1). The Spanish PMI also nudged down in October (from 51.7 to 51.3). The French print was flat on the month (50.6), whilst the Italian value increased robustly (52.7 to 54.1).

- Outside the ‘big 4’, the manufacturing PMI in Greece rose by 4.0pt (43.3 to 47.3), while the Irish figure edged down from 53.8 to 53.6.

Additionally, UK Mfg PMI also unexpectedly surging from 51.8 to a print of 55.5, above expectations of 51.3 boosted sentiment as well.

But perhaps the biggest reason why both Europe and the US wiped out all overnight losses in equities and futures was the latest baffle with BS moment out of Europe, where following this weekend’s unexpectedly hawkish interview by Mario Draghi to Il Sole, it was again Ewald Nowotny’s turn to bring the doves home, after saying the ECB’s 2% inflation target “clearly missed,” “therefore, the ECB has to act,” according to interview with Austria’s Kleine Zeitung. He then proceeded to engage in an economist’s favorite activity: stating what can not proven, namely that “without QE we’d be stuck in much bigger difficulties.” Well, one can just as easily state the opposite and have just the same “accuracy.”

A quick run through markets starts in Asia, where stocks traded mostly lower following the weak close on Wall St. coupled with discouraging official Chinese PMI figures over the weekend where manufacturing PMI (49.8 vs. Exp. 50.0) was in contractionary territory for a 3rd month, while services PMI (53.1 vs. Prey. 53.4) was at its lowest since 2008. This pressured Chinese markets from the open, however Shanghai Comp. (-1.3%). then recovered after China Caixin manufacturing PMI (48.3 vs. Exp. 47.6) beat expectations, although Chinese equities took another leg lower heading into the European open following news on the Zexi Investment crackdown.

Nikkei 225 (-2.1%) underperformed to trade back below 19,000 as JPY strength weighed on exporters, while ASX 200 (-1.4%) was pressured by financials after big-4 bank Westpac’s disappointing update. 10yr JGBs traded lower amid lack of buying by the BoJ ahead of tomorrow’s Culture day public holiday.

Despite opening lower on the back of another round of weak macroeconomic data from China, stocks in Europe staged a dramatic turnaround following dovish comments by ECB’s Nowotny who said that the central bank has to act given that inflation target is being missed. Bunds have failed to benefit from the above and instead traded lower amid FT reports over the weekend which suggested that China are selling some of its holdings of German government bonds to help assist the ECB’s QE programme. Also, somewhat non-committal comments by ECB’s Draghi who suggested that it is too early to pass judgement on depo-rate cut resulted in partial unwind of aggressive flattening of the Euribor curve which took place following very dovish press conference by Draghi last month.

In FX, GBP outperformed its peers, with the major pair rising above the 100DMA line following the release of much better than expected UK Manufacturing PMI report, which also comes ahead of the eagerly awaited MPC policy decision and the latest Quarterly Inflation Report. Elsewhere, USD/JPY recovered overnight losses and edged into positive territory to test the key 200DMA line, aided by higher US bond yields that’s as USTs were dragged lower by German Bunds. As noted previously, the Turkish Lira has exploded overnight on news that Erdogan’s rule is assured for years to come.

The release of yet another round of weak macroeconomic data from China meant that energy and metals markets remained under pressure in Europe this morning. Furthermore, reports that Russian October oil output has risen to record of 10.78mbpd, as well as reports that Iran it to seek 500kbpd output rise at OPEC meeting exacerbated the downside bias by WTI and Brent crude prices.

Top Weekend News:

- Erdogan Party Sweeps Back to Power in Surprise Turkey Win: AK Party sweeps back into office, defying polls, strengthening President Recep Tayyip Erdogan’s 13-year rule following divisive campaign.

- Russian Plane’s Midair Breakup a Puzzle in Modern Jet Era: Wreckage found in area ~8km long, 4km wide, suggesting aircraft broke up at high altitude.

- Macau Casino Shares Advance as Gambling Revenue Slump Eased: Gross gaming revenue fell 28% in Oct., decline was at slowest since Jan.

- ‘Martian’ Holds at No. 1 at Box Office Over Slow Halloween: Film generated $11.4m at U.S., Canadian theaters; Weinstein Co.’s “Burnt,” with Bradley Cooper, landed in fifth, while Warner Bros.’ “Our Brand Is Crisis,” with Sandra Bullock, opened in eighth place; Paramount’s “Scouts Guide to the Zombie Apocalypse” was 12th.

- Citron’s Left Won’t Have ‘Earth-Shattering’ News on Valeant: WSJ: Short seller Andrew Left to issue new Valeant report today

- Pfizer, Allergan Said to Aim to Agree on Deal by Thanksgiving: Cos. keen on friendly deal, hope to agree on the terms of takeover, incl. who will lead combined co., by Thanksgiving: people familiar

- Nissan Raises FY Profit Forecast as Demand Rises in U.S.: Net income may rise to JPY535bin 12 months through March vs JPY457.6b year ago.

- Chipotle Shuts Restaurants in Seattle, Portland on Health Risk: Co. closed 43 restaurants in Seattle, Portland, as health officials investigate E. coli outbreak

- China Factory Gauge Signals Contraction Continued a Third Month: Manufacturing PMI remained at 49.8 in Oct., below ests.

Market Wrap

- S&P 500 futures up 0.1% to 2076

- Stoxx 600 up 0.2% to 376

- MSCI Asia Pacific down 1.2% to 133

- US 10-yr yield up 3bps to 2.17%

- Dollar Index down 0.09% to 96.86

- WTI Crude futures down 1.5% to $45.88

- Brent Futures down 1.5% to $48.84

- Gold spot down 0.4% to $1,138

- Silver spot down 0.9% to $15.41

Bulletin Headline Summary From RanSquawk and Bloomberg

- Stocks in Europe staged a dramatic turnaround following dovish comments by ECB’s Nowotny who said that the central bank has to act given that inflation target is being missed

- Bunds have failed to benefit from further dovish rhetoric and instead traded lower amid FT reports over the weekend which suggested that China are selling some of its holdings of German government bonds to help assist the ECB’s QE programme

- Finally, going forward market participants will get to digest the release of the latest US manufacturing PMI, manufacturing ISM reports, as well as comments by Fed’s Williams.

- Treasuries drop in overnight trading as U.K manufacturing growth accelerated and sends equities higher; this week’s data will be dominated by nonfarm payroll release on Friday.

- Manufacturing in the euro area unexpectedly accelerated in October as German companies fared better than initially reported, according to Markit Economics

- The odds that the Federal Reserve will increase interest rates before year-end climbed to 50%, suggesting Treasuries are poised to extend October’s biggest monthly loss since June

- A 16-month oil rout and growing talk of recessionary risks have led economists tracking monetary policy in Norway to wonder whether zero — or even negative — rates are in store for western Europe’s biggest crude producer

- Asian hedge-fund managers are putting more money into their funds, seeking to project confidence after the industry’s worst performance streak since the 2008 financial crisis spurred redemptions

- China is signaling that it’s not letting record outflows this year deter capital-market reforms; changes to foreign- exchange rules will loosen some capital controls while preserving its ability to intervene in times of volatility

- Shanghai police raided hedge fund Zexi Investment on Sunday, according to a person familiar with the matter, in the latest attempt by Chinese authorities to crack down on strategies blamed for exacerbating a $5t stock- market rout

- German Chancellor Angela Merkel faces further coalition discord over the refugee crisis after weekend talks with fellow party leaders failed to identify a common government stance on tackling the biggest influx of migrants since World War II

- The Royals beat the Mets with a come-from-behind 7-2 victory in 12 innings to give them their first championship since 1985

- Sovereign 10Y bond yields mixed, with Greek 10Y yield 12bp higher. Asian and European stocks mixed; U.S. equity- index futures rise. Crude oil, gold and copper fall

DB’s Jim Reid completes the overnight wrap

Before we get to the weekend’s China numbers its worth highlighting that the strong October kicked into life with the 57 point S&P 500 turnaround on October 2nd just a few minutes after the weak payroll number. So it’s interesting that the end of this week sees the latest instalment in this random number generator of a series. The risk rally took a pause for breath over the last few days of last week not helped by a hawkish FOMC. So lots to play for in the data.

Looking now at the China data from the weekend and this morning. The official manufacturing PMI number for October has failed to show signs of a pickup in the sector, holding steady at 49.8 after expectations for a rise to 50.0. That was the third straight month of contraction in the sector and while the new orders component nudged up, there was some softness to be seen in the employment index in particular. Meanwhile the official non-manufacturing PMI declined three-tenths last month to 53.1, the lowest print now since December 2008.

There was a hint of more positive news in this morning’s Caixin manufacturing PMI. Although the 48.3 reading for last month supported the evidence from the weekend that the sector is still struggling, the reading was up 1.1pts from September and ahead of expectations of 47.6. DB’s Zhiwei Zhang notes that the rise in the non-official reading was the biggest this year. He reports that this rise, combined with some of the strength in key subcomponents (namely output and new orders) is consistent with his expectation that economic activities are picking up in Q4. Zhiwei reiterates his view that Q4 GDP will rebound to 7.2% from 6.9% in Q3.

There looks set to continue to be a reasonable amount of focus on China this week with the remaining Caixin PMI numbers due on Wednesday, foreign reserves data on Saturday and trade data on Sunday. On top of this we should also hear about the IMF’s decision on including the Chinese Yuan in its SDR basket with a decision due sometime early this month (with an exact date yet to be announced). Our Asia FX colleagues think that the likelihood of inclusion has increased in recent weeks reflecting better fulfillment of several of the SDR technical conditionalities and strong reporting from the Europe and the US during President Xi’s visit.

It’s been a volatile start to markets in China this morning following the latest data. The Shanghai Comp initially opened down -1.6%, although the slight upside surprise in the non-official PMI data has seen the index pare almost all of those losses to currently sit at -0.14%. It’s been a similar start also for the CSI 300 (-0.11%) although the Shenzhen (+1.03%) has rallied back strongly. Elsewhere it’s been a pretty weak start for bourses in Asia. The Nikkei is -1.94% after Japan’s final Nikkei manufacturing PMI nudged down one-tenth to 52.4. The Hang Seng (-0.65%) and ASX (-1.41%) have also seen losses. Asia credit indices are around a basis point wider while some of the more interesting moves have been in FX where the Chinese Yuan was set 0.54% stronger versus the USD this morning, the most the fix has been strengthened since 2005. This follows a 0.62% gain for the Yuan on Friday after the PBoC said it was to loosen capital controls around Yuan convertibility.

Turkey is also attracting plenty of headlines this morning following the parliamentary elections yesterday in which the ruling AK party gained what was seen as a surprise victory after taking about 49% of the total votes and a seat majority in parliament, having lost support in polls just five-months ago. The result may come as relief after previous polls had pointed towards the possibility of a hung parliament and heightened uncertainty. The Turkish Lira has jumped nearly 3% against the USD this morning in early trading – the most since January 2014.

Also of note from the weekend were comments from ECB President Draghi which keeps open the argument for more ECB stimulus as soon as next month. In an interview published in Italian Press Il Sole 24 Ore on Saturday, Draghi was quoted as saying that ‘if we are convinced that our medium-term inflation target is at risk, we will take the necessary actions’ and that ‘we will see whether a further stimulus necessary’. With expectations rising that another cut in the deposit rate might be necessary as soon as December, Draghi said that it is ‘too early’ to make that judgment, but that ‘the interest rate on deposits could be one of the instruments that we use again’.

These comments came a day after US equity markets faded into the close on Friday, although not enough to stop the S&P 500 posting its fifth consecutive weekly gain. The index finished -0.48% on Friday, while there were similar declines for the Dow (-0.52%) and Nasdaq (-0.40%) after stocks softened up in the final half hour of the US session. It had previously been a much more mixed session in Europe with the Stoxx 600 (-0.06%) finishing more or less unchanged, but the Dax (+0.46%) having a better day. Moves were pretty muted in credit but the bigger story continues to be one of a buoyant US primary market. Last week saw nearly $37bn price in US IG, the eleventh busiest week YTD but the $105bn priced in the month of October the busiest October on record. YTD volumes are actually now sitting at about the same as the total for 2014 and there looks set to be no let up with another $25-$30bn expected to come to market this week.

Earnings season continues with another 20 S&P 500 companies reporting on Friday. The overall trend was generally disappointing relative to what we’ve seen so far with just 13 (65%) beating earnings expectations (and 2 matching) and 9 (45%) beating revenue expectations. That was despite some better than expected numbers from the bellwether oil names on Friday after Chevron and Exxon Mobil exceeded analyst expectations, although the former in particular announcing that it expects to cut up to 11% of its workforce as well as scale back production guidance. With that the overall numbers now with 341 S&P 500 companies having now reported shows 73% have beat earnings expectations (similar to the 75% and 73% in the previous two quarters this year) but just 44% have beat revenue expectations (compared to 49% and 48%). Digging deeper, DB’s David Bianco notes that YoY EPS growth so far is standing at +1.7%, although this rises to +9.6% when you strip out the energy names, but equally declines to -1.7% excluding the financials stocks. The obvious weakness has been in revenues however where YoY growth is -5.8%. Again energy stocks have been a large driver of this, with the YoY growth rate actually +0.6% excluding these names.

In Europe meanwhile we’ve now seen quarterly reports from 213 Stoxx 600 companies. The trend so far continues to be one of notable weakness relative to prior periods with just 47% beating earnings expectations and 44% beating revenue expectations. That compares to 66% and 61% respectively in Q2 and 72% and 57% in Q1.

Friday’s dataflow in the US was a fairly mixed bag. It was hard to get too excited about the inflation numbers. The PCE core for September rose a less than expected +0.1% mom (vs. +0.2% expected) during the month, with the YoY staying put at +1.3%. The PCE deflator matched expectations at -0.1% mom, with the YoY rate nudging down one-tenth to +0.2% to match the lowest reading this year. The Q3 employment cost index also offered no surprises relative to expectations after printing at +0.6% qoq, which was up from a particularly soft Q2 (+0.2%). Meanwhile the final University of Michigan consumer sentiment reading for October revealed a 2.1pt downward revision to 90.0. Of more interest was the downgrade in 5-10y inflation expectations to 2.5% (from 2.6%) which matched the lowest level since the data series started in 1979. That helped take US Treasury yields lower, the benchmark 10y closing 3bps down at 2.143% while the USD softened with the Dollar index falling -0.35%.

Elsewhere, there was an impressive bounce-back in the October Chicago PMI which rebounded 7.5pts to 56.2 (vs. 49.5 expected) and to the highest level since January this year. The October ISM Milwaukee print was supportive too, rising 7pts to 46.7 (vs. 44 expected). Our US colleagues still expect this afternoon’s ISM manufacturing reading to print sub-50 however, consistent with the contraction in the manufacturing sector.

There was also some chatter out of Fed officials on Friday. The San Francisco Fed President Williams said he needs to see more economic data in the coming weeks to decide whether or not a December hike is warranted, although he did acknowledge that the mentioning of December in the minutes was meant as a signal that its ‘very much a live meeting’. Richmond Fed President Lacker confirmed that he voted against the FOMC’s decision to hold rates in October, noting that rates should be higher in his eyes given ‘the steady growth in output and household spending that we have been observing and expect to continue’. Finally the Kansas City Fed President George, while giving little away on her view of the potential for a December move, said that recent jobs and housing market improvement should ‘continue to see optimism on the part of consumers’ and that economic growth this year should largely keep pace with its longer-term trend.

Prior to this in Europe on Friday, the latest Euro area CPI estimate for October revealed a modest pickup as expected to 0.0% yoy, up one-tenth of a percent from September. There was a similar edge up for the core to +1.0% yoy, while the latest unemployment rate reading for the Euro area in September revealed an improvement to 10.8% from an already downwardly revised 10.9% in August. German retail sales for September disappointed (0.0% mom vs. +0.4% expected) as did the latest consumer spending report out of France (0.0% mom vs. +0.3% expected).

end

PBOC Fixes Chinese Yuan Higher By 0.54%, Most Since 2005

On Friday morning, after the biggest surge in the onshore Yuan in a decade, we explained it as follows: “capital controls are to some extent counterintuitive. That is, the stricter the capital controls, the more people want to move their money out of the country. Here’s how we put it last month: “What better way to spark a capital exodus than with very vocal, and very effective capital controls. Just look at Greece.”

Indeed, China will likely need to completely liberalize the capital account in the coming years in order to pacify the IMF which is poised to throw Beijing a bone and grant its RMB SDR bid. Inclusion could lead to some $500 billion in reserve demand.

That helps to explain why overnight, the yuan soared the most in a decade after Chinamoved to loosen capital controls with a trial program in the Shanghai free trade zone that would allow domestic individuals to directly buy overseas assets. The move marks another step towards capital account convertibility, thus bolstering Beijing’s bid for yuan internationalization.

Ironically, this did absolutely nothing to ease the local population’s concerns that capital outflows are accelerating, and certainly did nothing at all to help the Chinese export economy, which as we saw from the overnight PMI numbers, deteriorated once more to new cycle lows.

Fast forward to today when Westpac strategist Sean Callow said that the Froday jump in yuan’ spot rate on Friday and weaker dollar since last week’s close could mean largest daily gain in yuan fixing in several years, adding that the obvious policy priority for stronger yuan essentially sidelines fixing models for time being.

Sure enough, as per the fixing limits established as part of the August 11 Yuan devaluation, moments ago the PBOC announced that it had set the Yuan at a USDCNY fixing of 6.3154, a strengthening of a massive 0.54% – the most since 2005 – following the manic end of trading PBOC intervention on Friday that sent the Yuan soaring some 300 pips from 6.3475 to 6.3175.

So while the Chinese capital outflow is accelerating with every passing day, and which may now be best seen in the daily surge in the price of Bitcoin which has become a preferred means of circumventing China’s strengthened capital controls…

… China is well on its way to not only filling the entire devaluation gap, but slamming its export industries with an increasingly stronger currency, and thus assuring that any stabilization in the Chinese economy is promptly wiped away.

end

Nikkei falters badly last night but Turkish lira advances on Erodgan’s election victory

(courtesy zero hedge)

US, Japanese Stocks Extend Losses; Turkish Lira Soars Most In 7 Years As Gold Mini-Flash-Crashes

Despite the world seemingly exuberant at Turkey’s fraudelection, sparking the biggest rally in the Lira since Nov 2008(confirming once again that “markets love totalitarian governments,”) it appears the centrally-planned machinations of the US equity markets are not living up to their promises of wealth for all (and rate-hikes don’t matter). US and Japanese equity futures are opening notably lower, erasing all of the post-Fed exuberance with Dow Futs down over 200 points from pre-BoJ hope highs. Finally, gold futures were hammered lower at the Asia open (on heavy volume) only to rip back to practically unchanged.

Lira loves the ‘fix’…

Biggest daily jump since Lehman…

Someone decided the thinly-traded pre-open markets on a Sunday night was an opportune time to flush 10s of thousands of ounce of paper gold (around $228 million notional) into the market…

And maybe higher rates are bad after all…

Japanese stocks are tumbling

As the world, contrary to a surge in pent up expectations that China is finally fine, realize that it isn’t following this weekend’s miss in both the Manufacturing PMI, and slide in the non-manufacturing PMi to the lowest level since 2008.

Finally, was the hawkish Fed hawkish not just to punk another iteration of Eurodollar/FF traders, but because its FRB/US model actually believes that there is no more slack in the economy and a December rate hike is imminent as reported earlier?

China’s Manufacturing Misses; Nonmanufacturing Worst Since 2008 Despite Unprecedented $1 Trillion “Debt Injection”