Gold: $1106.50 down $7.70 (comex closing time)

Silver $15.06 down 18 cents

In the access market 5:15 pm

Gold $1108.00

Silver: $15.08

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very poor delivery day, registering 0 notices for nil ounces. Silver saw 3 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 208.30 tonnes for a loss of 95 tonnes over that period.

In silver, the open interest fell by only 801 contracts despite silver being down 27 cents in Tuesday’s trading. The total silver OI now rests at 166,942 contracts In ounces, the OI is still represented by .835 billion oz or 119% of annual global silver production (ex Russia ex China).

In silver we had 3 notices served upon for 300 oz.

In gold, the total comex gold OI fell by a rather large 6684 contracts to 443,900 contracts as gold was down $21.60 yesterday. We had 0 notices filed for nil oz today.

We had no change in gold inventory at the GLD / thus the inventory rests tonight at 686.30 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver,no change in silver inventory / Inventory rests at 313.817 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fell by a tiny 801 contracts down to 166,942 despite the fact that silver was down 16 cents with respect to yesterday’s trading. The total OI for gold fell by a rather large 6684 contracts to 443,900 contracts as gold was down $21.60 yesterday.

The fact that OI continues to remain high in silver necessitates the bankers to continue raiding hoping to shake the leaves from both the gold and silver trees. Remember that December is generally a big delivery month for both gold and silver

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

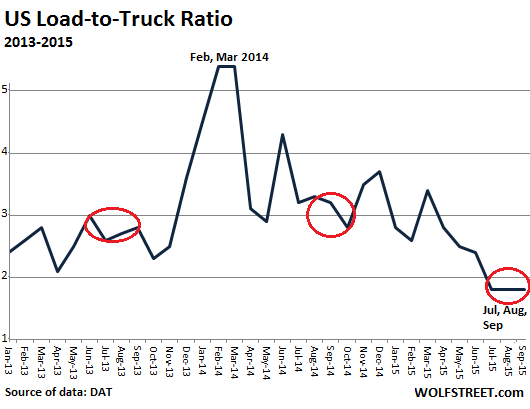

iii Now we are witnessing 3 big transportation vehicles that show that global trade is in one big freefall:

a) Shipping container rates

b) Train freight

c) Trucking

(courtesy zero hedge)

iii) Now British Prime Minister weighs in on the possible cause of the downing of the Russian airliner and he suspects a bomb

v) This is a big story…the aquifers that have been supplying water to Saudi Arabia to grow wheat etc has now run dry.

ii) Just look at which Middle Eastern oil nations are going broke:

9 USA stories/Trading of equities NY

i) ADP shows slower growth in employment in both manufacturing and service sector

(ADP)

ii) Senators to probe USA drug pricing especially for Valeant and Turing

(zero hedge)

iii The USA deficit narrows a bit signifying the global drop in output. If one excludes petroleum the deficit is far worse. When the shale industry finally halts, the deficit will skyrocket and the need for more monetization will be demanded

iv) a) US Services report is down badly, yet ISM services up.

Baffle them with BS

iv b) The last time we have a bifurcation between ISM manufacturing and ISM service reports, markets tanked 2001 and 2008

(ISM/zero hedge)

(zero hedge)

vii) Interesting!! Yesterday we witness the first criminal conviction on spoofing, yet HFT’s are free to do their illegal stuff.

They warn: if you outsmart us, yo go to jail!!”

(zero hedge)

viii FHFA’s Mel Watt warns that Fannie and Free may need another taxpayer bailout despite the low interest rates

(courtesy Mike Krieger)

ix) Dave Kranzler talks about the upcoming jobs report:

As everybody know, Friday is the jobs report

Dave Kranzler warns that gold and silver will be whacked on phony job gains. According to Mark Zandi they will use the B/D plug of 145,000 jobs to show a 190,000 job gain. Then they will whack gold and silver down from which the shorts will cover their shortfall.

Criminal activity at its finest…

(courtesy Dave Kranzler/IRD)

x) the economy must be booming: Kraft Heinz to layoff 10% of its workforce(courtesy zero hedge)

10. Physical stories

i) Koos Jansen on the important reason why the central bank of Austria is repatriating her gold.

(Governor of central Bank of Austria/Kitco/Koos Jansen)

ii) Bill Holter interview with Greg Hunter/USA Watchdog)

iii) Kingworldnews interviews John Embry

iv) India’s plan to monetize gold is falling on deaf ears

(Reuters/GATA)

Let us head over to the comex:

November contract month:

INITIAL standings for November/First day notice

Nov 4/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 356.424 oz

(HSBC,Manfra) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 contracts

nil oz |

| No of oz to be served (notices) | 293 contracts

(29,300 oz) |

| Total monthly oz gold served (contracts) so far this month | 6 contracts

600 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 3271.4 oz

(Scotia) |

Total customer deposits nil oz

we had 0 adjustments:

November initial standings/First day notice

Nov 4/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 46,817.606 oz

(Delaware, CNT,Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | |

| No of oz served (contracts) | 3 contracts (15,000 oz) |

| No of oz to be served (notices) | 11 contracts

55,000 oz) |

| Total monthly oz silver served (contracts) | 5 contracts (25,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 902,423.7 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: nil oz

total withdrawals from customer: 46,817.606 oz

And now SLV

Nov 4/2015: no change in silver inventory/rests tonight at 313.817 million oz/

Nov 3.2015; no change in silver inventory/rests tonight at 313.817 million oz/

Nov 2/a withdrawal of 716,000 oz from the SLV/Inventory rests tonight at 313.817 million oz

Oct 30.no change in silver inventory at the SLV/Inventory rests at 314.532 million oz

Oct 29/a big withdrawal of 1.001 million oz from the SLV/Inventory rests at 314.532 million oz

Oct 28.2015: no change in silver inventory at the SLV//inventory rests at 315.533 million oz.

Oct 27/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 26/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 23./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 22./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 21:a we had a small addition in silver ETF inventory of 381,000 oz/inventory rests tonight at 315.533 million oz

Oct 20.2015/ no change in silver ETF/Inventory rests at 315.152 million oz

“Great Optimist” Faber Says “I Added To My Gold Position”

Marc Faber, Swiss economist, forecaster, renowned investor and the original Dr. Doom, may need a new nickname.

In an interview on CNBC’s “Trading Nation,” the Gloom, Boom & Doom Report editor revealed he may not be as bearish as some may think and that he is actually a “great optimist.”

Marc Faber on one of his five motorcycles

“I always tell people, ‘I am a great optimist … because one of the most dangerous things to do is to drive motorcycles in Thailand and I have five motorcycles.”

The blunt-spoken, truth-telling Faber may have helped people understand that one may be worried about the economic outlook and bearish on stocks and other markets and yet be an optimist about life and all the wonderful things it has to offer and on the human spirit and our capacity to overcome even the worst financial and economic crashes.

On the risks of being a perma bull, he warned:

“You can’t be always sitting there and saying ‘Stocks always go up, real estate always goes up’ and so forth and so on”.

“You could have zero interest rates and stocks go down – as they’ve done in Japan until three years ago. Even at these very low interest rates, something can happen and dampen the enthusiasm for equities.”

Faber admits that he is bearish on the global economy. “I’m most gloomy about the prospects of the global economy, but it doesn’t mean that markets will go down,” he told CNBC. But on the other hand, he says “you have the mad professors at central banks around the world who think that because of a weakening economy they have to do more [quantitative easing].”

On a more positive note, Faber says he is most optimistic about the Indochinese region, which he likens to Los Angeles.

“Provided there is peace and not tensions that explode, I think the region of Indochina is right now like Newport Beach and Huntington Beach and Manhattan Beach, where I’m at right now,” he told CNBC. “It’s a boom region, Indochina. It includes Vietnam, Cambodia, Laos, Thailand – which is not booming right now – Myanmar, Malaysia, Singapore.”

According to Faber, this region could “easily” grow at 6%-8% per annum for the next 10 years as long as there is peace.

“Cambodian exports were up 20% this year,” he added. “Vietnamese exports are up approximately 10% this year. So relative to the rest of the world, this is a boom region.”

Faber said he would invest in both this region’s stock and real estate markets. Faber believes that U.S. equities are fully priced. And while he says it’s possible that indexes could make a new high, he thinks that the majority of shares would not.

When asked if he’d bought any U.S. stocks recently, Faber said he’s done very little.

“The only thing I’ve really done recently is I added to my gold position about two months ago, and I bought some gold-related equities.” “But other than that, I’ve done very little because I believe that in this extreme volatility where markets suddenly drop 10%, individual stocks drop 10% or 20% in one day – it’s a very difficult environment to make a lot of money unless you take huge risks.”

The shrewd investment adviser is staunch advocate of owning physical gold bullion which he describes as being a way to become “your own central bank.”

He believes an allocation to bullion is vital financial insurance and that the biggest question is where to store your gold? He believes that Singapore is the safest place to own gold in the world today.

Watch the complete interview with Marc Faber on CNBC

Marc Faber Webinar on Storing Gold in Singapore

Essential Guide To Storing Gold In Singapore

DAILY PRICES

Today’s Gold Prices: USD 1118.00, EURO 1024.09 and GBP 724.99 per ounce.

Yesterday’s Gold Prices: USD 1130.90, EURO 1029.82 and GBP 733.95 per ounce.

(LBMA AM)

Gold lost $16.60 yesterday to close at $1117.70. Silver closed at $15.29, down $0.14. Platinum lost $13 to $961.

Why Austria Is Repatriating Gold From London

At the LBMA conference in Vienna, which was held from 18 – 20 October 2015, the Executive Director of the Austrian central bank, Peter Mooslechner, was interviewed by Editor-in-Chief for Kitco News, Daniele Cambone. You can watch the interview here. This particular interview is interesting because the central banker from Austria made some exceptional remarks about repatriating gold and indirectly about gold management by central banks around the world in our current economic climate. Central bankers have a long history of keeping silent about anything related to their gold policy, and this interview suits the tradition in part, though Mooslechner by accident told us what’s happening behind the scenes.

Many central banks around the world are aware the international monetary system is moving away from the US dollar and that the role of gold will (officially) be much greater in the future. In this development central banks benefit from a smooth and slow transition to a new system, as sudden shocks will bring the global economy in a free fall and more time provides better preparations. Central bankers prefer slow and attentive change. Signs of the slow development towards gold by central banks can be seen across several continents. In Europe slowly more and more countries are repatriating their gold from the UK (Bank Of England) and the US (Federal Reserve Bank Of New York). Certainly not all their gold but weighed amounts and in the case of Germany and Austria the gold is repatriated over several years. If all European countries would repatriate all their gold at once it would cause a panic in financial markets. In the East, Russia and China are increasing their gold reserves every single month by relative small amounts, respecting the slow development towards gold. Asian central bankers differ from their European colleagues because they verbally acknowledge the role of gold in finance. In 2004 Zhou Xiaochuan, governor of the People’s Bank Of China, said:

… China’s gold market should move from commodity trade to financial product trade. Gold is a commodity that combines the attributes of a currency, financial commodity and general commodity. … gold still has a strong financial nature and remains an indispensable investment tool. In financial centers in the world, the gold market – together with the money market, securities market and FX market – constitutes the main part of the financial market.

Obviously all these central banks are aware what the future will hold. How else can we explain Europe’s repatriating gold policy and Asia’s buying gold policy?

Candid statements from European central bankers regarding their gold policy are scarce. The slow development towards gold previously described is usually covered in excuses by European policy makers. I can recall the Dutch Minister Of Finance, Jeroen Dijsselbloem, was asked in a television interview why the Dutch central bank (DNB) had covertly repatriated 123 tonnes of gold from the Federal Reserve Bank of New York in 2014. Dijsselbloem answered with a condescending smile, saying, “ the decision was made by DNB to spread its gold stock in a more balanced way, but it was of little importance”. Of course the military operation that DNB had carefully planned and executed over the course of two years was of utmost importance for the financial well being of the Netherlands, but Dijsselbloem could not openly acknowledge this importance because of the sensitivity of the subject. Just like Jean-Claude Juncker said in 2011:

When it becomes serious, you have to lie.

With the slow developmenttowards gold in mind, let us analyze the interview with Mooslechner in order to distil the genuine reason why Austria is repatriating its gold from London. Below is the transcript of the interview supplemented by my comments.

Cambone:

I want to talk to you about the role of gold in a central bank. Is it loosing appeal in the role it plays in a central bank, or is it gaining ground? How do see you gold.

Mooslechner:

I think it differs a lot. For a small central bank like we are, and we have joined the Eurosystem some time ago, the role of gold has significantly changed. It was of big importance during the period of the Bretton Woods System, it played a key active role also in the management of our over all reserves. But having become now part of a much greater monetary and economic area, it has transformed into something like the basic part of reserves to be hold for as a liquidity buffer or for security reasons, but not so much an active part of management of gold reserves anymore.

Interesting. Mooslechner states that his central bank views its 280 tonnes of gold as “the basic part of reserves”. This is in line with the Balance of Payments and International Investment Position Manual (BPM6) drafted by the IMF, in which gold is regarded as “the only case of a financial asset with no counterpart liability” and is therefor listed at the top of all reserve assets – above SDRs.

…

Cambone:

Does the Austrian central bank have plans to increase its gold reserves? Last estimates were 43.9 %.

Mooslechner:

We don’t think so that we have to increase, because we are now part of the much bigger intervening power of the Eurosystem and the ECB. But what we have decided in the last strategic …. uhm … documents, is to keep the share of gold and the amount of gold constant for the time being.

Apparently, the Austrian central bank’s gold policy is communicated in strategic “uhm… … documents”. I wonder if these documents are publicly accessible? I guess not.

Cambone:

You want to repatriate 3.5 billion pounds of the gold, which is currently in the UK, moving it back to Austria over the course of five years. Why did you decide on this move?

Mooslechner:

This goes back to a request by our general court of auditors, they thought that the concentration of our gold holdings at the Bank Of England [BOE] is a little bit too high and they wanted us to reduce concentration risk there. Frankly speaking, we didn’t see much of a concentration risk because the Bank Of England is the best place to be, but we decided to go a little bit more in the direction of diversification, so we’ll bring a little bit back to Austria, in fact, in the end 50 % of our gold holdings should be kept in Austria and we will also stock up our holdings in Switzerland, from the original part, which is held by the Bank Of England in London.

Mooslechner states the Austrian central bank (OeNB) will repatriate its gold from the BOE because of a concentration risk in London, while at the same time he states the BOE is the best place to store gold. This contradiction indicates his answer is nonsense. The BOE cannot be the best place for foreign central banks to store official gold reserves or Mooslechner wouldn’t take the effort to repatriate. Aside from the contradiction, in 1976 there were more than 12,000 tonnes of gold stored at the Federal Reserve Bank of New York for foreign central banks. Did anybody complain about a concentration risk at the time? Why are European countries currently repatriating official gold reserves due to concentration risks, but they didn’t complain about concentration risks in the past decades when their gold was stored in London and New York as well? The argument to repatriate gold because of concentration risks is an excuse.

One aspect of the genuine reason for the Austrian central bank to repatriate gold from the UK was passingly disclosed by the Austrian general court of auditors in February 2015:

… the gold depository contract with the depository in England [BOE] contained deficiencies. As regards the gold reserves stored abroad, internal auditing measures were lacking.

…

The OeNB had no appropriate concept to perform audits of its gold reserves. … The lack of audit measures represented a gap in the internal control procedures of the OeNB.

The problem was not the concentration risk of gold in London, but the fact OeNB couldn’t audit its gold abroad.

Carry in your mind, a few years before the report by the general court of auditors was published in 2015, the Austrian central bank started to unwind its gold leases. Its conventional gold leases to commercial banks stood at 116 tonnes in 2009, but brought down to 24 tonnes in 2013.

And since January 2013 OeNB has moved 59 tonnes of gold from unallocated gold accounts to allocated gold accounts (gold bullion). In January 2013 OeNB’s unallocated gold accounted for 74.62 tonnes, in August 2015 it was at 15.58 tonnes. Total OeNB official gold reserves are flat at 280 tonnes since 2007.

The fact Austria started securing its gold bullion in 2009 demonstrates the decision by OeNB to repatriate was not simply because the general court of auditors saw a concentration risk in 2015. As, the decision to repatriate was taken a long time ago, likely when the global economic crisis and the eurocrisis erupted – Germany and the Netherlands decided to repatriate in 2012.

Mooslechner used the concentration risk argument by the general court of auditors as an excuse to repatriate. As we know by now, there have been safety issues with the Austrian gold in London, one example that we know of is that OeNB was not able to audit the gold until 2013. But if Mooslechner would have used this argument as the sole reason to repatriate all hell would break loose. And so he used an excuse, the concentration risk.

Note, the concentration risk excuse was also used by the Netherlands. Apparently this was communicated among European central bankers. Nice teamwork.

Cambone:

It seems that Germany started the movement one day asked for the gold back that was held in New York, you think that had anything to do with it? Because we so many other countries follow suit after Germany’s announcement.

Yes, Daniela ask him! In 2011 Germany’s central bank Executive Board Member Carl-Ludwig Thiele testified to the German parliament’s budget committee, “We’re in negotiations with our partner central banks [the Federal Reserve Bank of New York and the Bank Of England] to develop auditing rights”, according to Bloomberg. This sounds like the exact same problem the Austrians ran into in London. Maybe, just maybe, this is all connected. Let’s read what Mooslechner answered:

Mooslechner:

Perhaps this could be also be labeled as some sort of economic nationalism, which has risen politically in I think a lot of countries. …

A few seconds ago Mooslechner stated OeNB is repatriating because the Austrian general court of auditors observed concentration risks at the BOE. Now, he turns around and states Austria is repatriating because of economic nationalism. If we take into account OeNB has been working on securing its gold bullion since at least 2009 and tried to audit its gold in vain, economic nationalism sounds more like the genuine reason to repatriate than concentration risks. Mooslechner is actually saying OeNB prefers to store its gold on its own soil, instead of storing it abroad and risk a foreign institution (BOE) to use the gold at its own discretion. If the BOE would be capable of doing such things no wonder OeNB was not granted any auditing rights.

Also note, by revealing the genuine reason to repatriate Mooslechner confirms the ‘official reason’ (concentration risk) is nonsense.

…

Cambone:

If we see continued easing in Europe however, what impact do you feel that would have on gold?

Mooslechner:

It depends, if uncertainty increases in parallel, for whatever reason, for example reasons which are situated in Asia in the Chinese situation, then perhaps gold might become more attractive even in Europe. On the other hand if Europe, as it’s the view form the US for example, at the moment if Europe can improve its economic situation as planned in our forecast, then this might not have a big impact on the situation of the gold market.

Cambone:

Peter, thank you so much for your thoughts today.

Thanks indeed Peter, that’s very honest, but in fact common knowledge, when the shit hits the fan “gold might become more attractive even in Europe”. Let’s hope Austria has a fair share of its gold repatriated in due time.

In conclusion, European countries are repatriating gold from the UK and US simply because the abroad depositories are not considered safe. Therefor, gently the gold is being repatriated in segments, respecting the slow development towards gold.

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

end

(courtesy John Embry/Kingworldnews)

Fed knows but won’t admit that the problem is debt, Embry tells KWN

Submitted by cpowell on Wed, 2015-11-04 13:07. Section: Daily Dispatches

8:06a ET Wednesday, November 4, 2015

Dear Friend of GATA and Gold:

The Federal Reserve knows that the world financial system’s big problem is too much debt and that higher interest rates will sink the world economy but can’t admit it, Sprott Asset Management’s John Embry tells King World News. Instead, Embry says, the Fed merely talks about raising rates and issues bogus economic data. An excerpt from his interview is posted at the KWN blog here:

http://kingworldnews.com/the-unsuspecting-public-is-being-led-into-immen…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

As we told you on countless occasions India’s plan to monetize gold will not work

(courtesy Reuters/GATA)

India launches gold monetization scheme, response seen muted

Submitted by cpowell on Wed, 2015-11-04 13:19. Section: Daily Dispatches

By Manoj Kumar

Reuters

Wednesday, November 4, 2015

NEW DELHI, India — Prime Minister Narendra Modi will launch on Thursday a programme to lure tonnes of gold from households into the banking system, but low returns and concerns over tax authorities hounding depositors may hinder a scheme aimed at cutting imports.

India’s obsession with gold is rivaled only by China, with the metal used widely in wedding gifts, religious donations, and as an investment. The country has amassed about 20,000 tonnes of gold worth over $800 billion in family lockers and temples.

Previous attempts at mobilising this gold have been unsuccessful, but the prime minister is hoping higher interest rates paid will help it to succeed this time.

“The government wants to reduce the reliance on gold imports over time,” a finance ministry official said.

Banks will collect gold for up to 15 years to auction it off or lend it to jewellers from time to time. They will pay 2.25-2.50 percent interest a year, higher than previous rates of around 1 percent.

But industry experts and bankers said many prospective depositors will not take up the scheme due to concerns that the tax department could question the source of gold, while others may find conventional bank deposit rates of 8 percent more attractive. …

… For the remainder of the report:

http://in.reuters.com/article/2015/11/04/india-gold-modi-monetisation-id…

end

Lawrie on Gold updates WGC official gold reserves:

the big surprise is the big addition of gold to Jordan’s official reserves

Probable increase in central bank purchases amount to 440 tonnes this year.

(courtesy Lawrie on Gold

Significant Changes YTD in World Gold Holdings

The World Gold Council has just updated its tabulation of global gold reserves country-by country – and the accompanying table of country-by-country reported changes year to date makes for interesting reading at looking at gold flows in and out of global central banks. The tabulation of significant (+1 tonne total) changes in gold holdings on a month by month basis is set out below:

| Country | Jan | Feb | Mar | Apr | May | June | Jul | Aug | Sept | Net Total |

| Belarus | -1 | 3 | 2.5 | -3 | 1.5 | |||||

| China* | 604.3 | 19 | 16.2 | 14.9 | 654.4 | |||||

| El Salvador | -5.4 | -5.4 | ||||||||

| Germany | -0.8 | -2.4 | -3.2 | |||||||

| Jordan | 3.4 | 8.1 | 2.5 | 0.9 | 7.5 | 22.4 | ||||

| Kazakhstan | 1.7 | 2.7 | 2.3 | 2.4 | 2.6 | 2.3 | 2.5 | 2.1 | 3.2 | 21.8 |

| Malaysia | 0.6 | 0.6 | 0.3 | 0.6 | 2.1 | |||||

| Mauritius | 1 | 1 | ||||||||

| Mongolia | -1 | -0.1 | -0.3 | 0.7 | 1.0 | -0.9 | -0.6 | -1.2 | ||

| Russia | -0.5 | 30.5 | 8.3 | 4.3 | 24.1 | 13.1 | 29.6 | 34.5 | 143.9 | |

| Turkey** | -14.2 | -4.6 | 2.7 | -6.5 | -1.9 | -4.8 | 17.2 | 0.6 | -13.2 | -24.7 |

| Ukraine | 0.3 | 2.2 | 0.9 | 3.4 | ||||||

| UAE | 2.6 | -0.1 | 2.4 | 0.1 | 0.1 | 5.1 |

Source: World Gold Council, IMF, lawrieongold

*China figure includes big gold reserve accumulation reported in July, but applicable to an unreported reserve build-up over the previous 6 years.

** Turkey’s reserve figures are somewhat anomalous as they include holding held in the country’s commercial banking system and are thus prone to be far more volatile on a month-by-month basis.

Looking at annual Central Bank gold purchases, if we strip out the big Chinese reported addition to reserves reported in June (which was an accumulation built up over the prior 6 years) and replace that with a nominal 15 tonnes a month for the first nine months of the year – the kind of level it is reporting now on a month by month basis. And also strip out the anomalous Turkey total, we look to be heading for total central bank purchases, net of sales, for the full year of around 440 tonnes which is pretty much on target from analysts forecasts.

With the major monthly buyers – Russia, China, Kazakhstan, and perhaps Jordan – seemingly committed to ongoing gold reserve increases there seems to be little reason why these shouldn’t continue into 2016 and beyond.

end

great interview of Bill Holter with Greg Hunter of USA Watchdog:

(courtesy Bill Holter/Greg Hunter)

China Could Reprice Gold to $100,000 per Ounce-Bill Holter

By Greg Hunter On November 4, 2015

Financial writer and gold expert Bill Holter contends China has enormous debt problems, but a very good plan. B. Holter explains, “China used fiat debt to build real infrastructure, and when the system blows up, the fiat debt blows away and they are left with infrastructure. Do they have 20% bad loans? They very well could and probably do. If it is true that they are going to have a debt blow up, don’t forget China has been importing big tonnage of gold for years now. Over the last five years, they have imported 9,000 tons of gold. Their way out is the old way out. The old way out was to revalue gold higher. They could revalue gold and step up and say they will pay $50,000 or $100,000 per ounce for any and all ounces for sale. You can’t say there is not enough gold. What you can say is that it’s not priced correctly to support the system. If they have an implosion of debt which leaves their balance sheets impaired, the way to recapitalize the balance sheets is to revalue the price of gold higher. It creates capital, in other words.”

How about the U.S. debt problem? Holter says, “That does not and cannot work for the U.S. because we have offloaded our gold. Simple math tells you the gold that China received has to come from somewhere, and that only somewhere in the world is Western U.S. vaults.”

Could the U.S. still have its more than 8,000 tons of gold? Holter says, “That’s pure ‘hopium’ that the U.S. still has their gold. Common sense and logic tells you that the gold is gone.”

So, has the U.S. budget and debt ceiling deal fixed anything? Holter says, “If they didn’t raise the debt ceiling, there would have been an immediate implosion. You have to understand, Americans are the only people on earth that aren’t laughing at the debt ceiling. Foreigners are laughing at it. You are talking about $20 trillion. It can’t be paid. We are at 110% of GDP already, and we’re the reserve currency.”

Holter goes on to say, “It’s another bubble. It’s going to burst, and the banks are in worse condition now from a debt to equity standpoint. Nothing has changed–it’s just bigger.”

Holter worries about possible deals between Saudi Arabia and Russia that could impair the petro-dollar. Holter says, “The (dollar) dam is leaking, at this point, because there is less and less use of the dollars around the world. . . . If Saudi Arabia were to say we’ll accept euros, yuan or rubles for oil or if they said we won’t accept dollars anymore, that’s like pulling a center piece out of a dam. It will break, and it’s over for the dollar. They could do that, and they could get bombed back to the stone-age, but I am sure it’s been talked about.”

Holter says there is “no rule of law,” and criminal activity has suppressed the price of physical gold. Holter says, “We have been through a four year period of time where paper gold has been pounding the price of physical gold. You have people who were strong legged, hard money guys who are weak in the knees now, and they shouldn’t be. My hope is we can strengthen some weak knees, to not sell you only insurance in a financial Armageddon. It is mathematically coming. There is absolutely no possible exit with the system intact and the rule of law.”

Join Greg Hunter as he goes One-on-One with Bill Holter of JSMineset.com.

(There is much more in the video interview.)

Video Link

http://usawatchdog.com/china-could-reprice-gold-to-100000-per-ounce-bill-holter

or this link:

1 Chinese yuan vs USA dollar/yuan rises , this time at 6.3355 Shanghai bourse: in the green, hang sang:green

2 Nikkei closed up 243.67 or 1.30%

3. Europe stocks mostly in the green /USA dollar index up to 97.36/Euro up to 1.0934

3b Japan 10 year bond yield: rises slightly to .319% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 121.21

3c Nikkei now just above 18,000

3d USA/Yen rate now just above the important 120 barrier this morning

3e WTI: 48.13 and Brent: 50.72

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .566 per cent. German bunds in negative yields from 5 years out

Greece sees its 2 year rate fall to 8.02%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 7.74% (yield curve inverted)

3k Gold at $1118.00 /silver $15.28 (8:00 am est)

3l USA vs Russian rouble; (Russian rouble up 1/100 in roubles/dollar) 62.58

3m oil into the 48 dollar handle for WTI and 50 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9895 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0821 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 5 year German bund now in negative territory with the 10 year rises to +.566%/German 5 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.21% early this morning. Thirty year rate below 3% at 2.99% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Rally Continues After PBOC “Unintentionally” Sparks Market Surge With Stale News, Largest 2015 IPO Prices

The most entertaining overnight story has to do with the latest farcical development in the Chinese “market” when just after open, it was reported that PBOC Governor Zhou said a trading link with Shenzhen will start this year which promptly sent all Chinese brokerages soaring, and the Shanghai Composite jumped over 3%. And then, out of the blue, the PBOC said the undated comments were actually as of May. As Bloomberg put it, “China’s central bank unintentionally sparked a surge in the nation’s stock market by publishing five-month-old comments from governor Zhou Xiaochuan that said a link between exchanges in Shenzhen and Hong Kong would start in 2015.”

Zhou’s comments appeared in a lengthy article dated Tuesday that focused on the need for Communist Party discipline. It was published on the PBOC’s website without any indication that the statements were old. The central bank later said via text message that the comments were taken from a speech on May 27, while Hong Kong’s bourse said the link is still subject to regulatory approval. The clarifications came after a 3.3 percent surge in the Shenzhen Composite Index and a 3.1 percent gain in Hong Kong’s Hang Seng Index in early trading.

AS Bloomberg further adds, the PBOC article moved markets because it came as a surprise to many investors who had anticipated the link would be delayed after a $5 trillion rout in Chinese shares. As a result of the non-news, everything jumped, and while there was some retracing in stock prices after the PBOC correction…

… soon thereafter the refutation was forgotten and only the original non-news remained, allowing the PBOC to achieve its mission of sparking a marketwide ramp on a 5-month-old statement, with all the brokerages closing limit up (Pacific Sec +10%, Citic Sec +10%, Haitong Sec +10%, Guotai Junan +10%, Shenwan Hongyuan +10%), even as the Composite closed at its highs, up 4.3% on the day.

The other main event in Asia was the IPO of Japan Post which soared after going public in a $12 billion, three part deal which also included its banking and insurance divisions, making it the biggest IPO of 2015 and the largest since Alibaba’s $25 deal in 2014. It was also the Japanese government’s largest asset sale in nearly three decades.

Japan Post Holdings opened at 1,631 yen per share, 16.5% above the IPO price of 1,400 yen. The banking unit started at 1,680 yen, up almost 16% from its IPO price, while the insurance unit was 33% higher.

Shares in the parent company Japan Post Holdings closed up 20%; shares of Japan Post Bank closed up 15% while Japan Post Insurance soared 56%.

Angus Nicholson, market analyst at trading firm IG, said the “blockbuster” IPO was helping to drive the rally in Japanese markets as they returned from a holiday on Tuesday. And indeed, the euphoria surrounding the issue also helped push both the USDJPY higher, and closed the Nikkei up some 1.3%.

The Japanese government plans to raise a total of 4tn yen in additional asset sales in the coming years. It has said the funds will be used to help reconstruct areas hit by the 2011 earthquake and tsunami disaster.

Other Asian headline news:

- China’s Latest Bond Scare Burns Holdouts as Default Risks Spread: Hidili has said it can’t pay $190.6m due Wednesday.

- Historic China-Taiwan Meeting Shakes Up Island’s President Race:: Leaders of China and Taiwan plan to meet Saturday for the first time since their civil war seven decades ago.

- Rajan Sees Rupee as Investment Currency; Dollar Debt Curbed: Monetary policy ‘just right’ to reach 2017 inflation target.

- Standard Chartered’s Bad Loans Show Cracks in Asia Economies: Bank had gambled on success in emerging markets such as India, which instead saddled the lender with delinquent loans.

Moving to Europe, recently infamous heavyweight Volkswagen (-8.5%) is once again the notable underperformer as the emissions scandal is further fuelled by recent reports suggesting that it was not only diesel engines which have been implicated. As such, the carmaker has gone on to weigh on the DAX (-0.2%), which is the laggard compared to other major European indices (Euro Stoxx +0.7%). Separately, energy and material names are the best performing sectors today as yesterday’s API inventories showed a lower than previous build 2800K (Prey. 4100K), while materials trade in the green after Glencore (+5.4%) reported they are to increase the planned cuts to copper production and reiterated their FY forecast.

We also got European Service PMI data, which came in better than expected in Spain 55.9, exp. 55.4, (last 55.1), France 52.6, exp. 52.3 (last 52.3), while it disappointed in Italy 53.4, exp. 53.5 (last 52.3), and Germany at 54.2, exp. 55.2 (last 55.2). The combinedf Euro-area composite PMI rose to 53.9 from 53.6, slightly missing expectations; U.K. services rose to 54.9 from 53.3, better than forecast.

Fixed income markets see Bunds in modest positive territory, aided by small real money buying, while the 5s/30s German curve is close to its September high at 146bps. Portuguese bonds are currently outperforming their EU counterparts with the PO/GE spread tighter after PM Coehlo has said he would be willing to lead a caretaker govt, a step that is seen as a measure of stability for Portuguese politics. Finally of note, for USD swaps, the curve is seen flatter after a deal hedge position, with November expected to see plenty of issuance as treasurers look to close off all funding ahead of a potential Fed lift off in December.

Despite the latest Volkswagen snafu, European stocks gain for third day to highest since late Aug. after ECB President Draghi’s comments last night reiterated commitment to euro-area recovery, with Norwegian, Swiss bourses outperforming. “The degree of monetary policy accommodation will need to be re-examined at the Governing Council’s December meeting,” Draghi said at in Frankfurt last night; “The Governing Council is willing and able to act by using all the instruments available within its mandate if warranted in order to maintain an appropriate degree of monetary accommodation.”

As a result, 18 out of 19 Stoxx 600 sectors rise with basic resources, oil & gas outperforming and autos underperforming with 72% of Stoxx 600 members gain, 26% decline.

Other European key news:

- VW Scandal Deepens as Emissions Woes Spread to Gasoline Cars: Co. says internal probe showed 800,000 gasoline- powered cars had “unexplained inconsistencies” concerning their carbon-dioxide output.

- Bank of England Will Raise Key Rate in Early 2016, Niesr Says: BoE will probably raise its benchmark interest rate in Feb., according to National Institute for Economic and Social Research.

- Merkel’s Coalition Will Survive Refugee Turmoil, Ally Says: Asked whether Merkel’s govt could collapse, Deputy Foreign Minister Michael Roth said: “No, not at all.”

- Iceland Raises Rates as It Moves Closer to Capital Controls Exit: 7-day term deposits rate was raised to 5.75% from 5.5%.

- Lonmin May ’Cease Trading’ If $400 Million Share Sale Fails: World’s third-largest platinum miner said shareholders risk losses if they block a $770m refinancing plan that includes sale of shares.

In FX markets, the EUR underperformed both USD and GBP after further dovish comments from ECB’s Draghi overnight , suggesting that the degree of accommodation within monetary policy required will need to be re-examined at the December meeting and is willing to act if necessary. However losses were capped by generally better than expected services and composite PMIs from across Europe, although the German and Eurozone readings both missed on expectations. GBP did see modest strength on the back of the UK release of services and composite PMIs (Services PMI 54.9 vs. Exp. 54.5) however is still relatively unchanged on the day against the USD..

The commodity complex heads into the North American crossover relatively flat, with WTI and Brent having seen strength after API crude inventories (W/W 2800K Prey. 4100K) showing a smaller build than the previous week . Looking ahead, today sees the DoE crude oil inventories, which are expected to show a build of 2500k (Prey. 3376k). The metals complex has seen copper outperform after reports from Glencore that they are going to cut production of the metal by a further 55,000, for a total cut of 455,000 by the end of 2017.

And now we look forward to the main even in th US market, where in addition to notable US earnings including Facebook, Allergan and Time Warner, as well as US ADP employment change, services and composite PMIs and ISM Non-manufacturing composite, the most important thing everyone will be watching is the deluge of Fed commentators which include the Fed’s Brainard, Harker, Dudley, Lockhart, Fischer while Janet Yellen herself will address Congress this morning on bank regulatory matters.

In short, prepares for a deluge of Fed speakers to prepare the equity, and the Fed Fund futures markets, for a December rate hike now that the Fed again has a green light to hike rates with the S&P is back at its all time highs. Here is the schedule:

- 5:30am: Fed’s Brainard speaks in Frankfurt

- 8:00am: Fed’s Harker speaks in Philadelphia

- 10:00am: Fed’s Yellen testifies before House Financial Services Committee

- 2:30pm: Fed’s Dudley speaks in New York

- 7:30pm: Fed’s Fischer speaks in Washington

Market Wrap:

S&P 500 futures up 0.1% to 2105

Stoxx 600 up 0.8% to 382

MSCI Asia Pacific up 1.1% to 135

US 10-yr yield up less than 1bp to 2.21%

Dollar Index up 0.29% to 97.44

WTI Crude futures up 0.2% to $47.99

Brent Futures up 0.2% to $50.66

Gold spot up less than 0.1% to $1,118

Silver spot up less than 0.1% to $15.29

Top Overnight News:

- Tesla’s ‘Aspiration’ to Have Positive FCF in 1Q 2016: Sees production rate of “several hundred” Model X per week by next month.

- PBOC Inadvertently Boosts China Stocks With Dated Zhou Comments: 2015 target for Shenzhen-Hong Kong link surprises investors.

- Japan Post Bank May Shift Some Investment Funds to Stocks: Stock listed Wednesday after three-pronged $12b IPO.

- Takata to Pay Up to Record $200 Million Over Faulty Air- Bags: Under 5-year consent decree with NHTSA, co. agreed to pay $70m, plus up to $130m more in fines if it doesn’t adhere to settlement terms.

- San Francisco Voters Reject Ballot Measure to Curb AirbnbP: Measure would have imposed 75-day/yr limit on Airbnb rentals, forcing hosts to register with city; its was losing 55% to 45% with all precincts reporting.

- Ohio Voters Reject Legalizing Pot Controlled by Investors

- Druckenmiller Says He’s Short the Euro, Stocks Could Be Next: Says Draghi has “pretty much pre-announced step two,” signaling either further discount rate cut, more quantitative easing or both.

Bulletin Headline Summary from RanSquawk and Bloomberg

- European heavyweight Volkswagen (-8.3%) is once again the notable underperformer as the emissions scandal is further fuelled by recent reports suggesting that it was not only diesel engines which have been implicated

- FX markets have seen EUR underperform both USD and GBP after further dovish comments from ECB’s Draghi overnight

- Looking ahead, notable highlights include the US ADP employment change, services and composite PMIs and ISM Non-manufacturing composite as well as a number of FED and ECB speakers and earnings from Facebook and Allergan

- Treasuries little changed as stocks, crude oil and copper gain; today brings ADP for first look at October employment (est. 180k) and $26b 2Y sale. WI 0.79%, highest since 2010, vs 0.699% last month.

- At 8:30am ET, U.S. to announce plans for Quarterly Refunding auctions of 3Y/10Y notes, 30Y bonds (See Treasury link)

- Volkswagen said late Tuesday that an internal probe showed 800,000 cars had “unexplained inconsistencies” concerning their output of CO2, with affected vehicles include gas- powered models for the first time

- Euro-area composite PMI rose to 53.9 from 53.6, below expectations; U.K. services rose to 54.9 from 53.3, better than forecast

- Standard Chartered Plc became the third European bank in less than two weeks to announce sweeping job cuts, bringing the total planned reductions to more than 30,000, or almost one in seven positions

- Less than three months after its sudden yuan devaluation roiled global markets, the PBOC sowed confusion among stock traders by presenting five-month-old comments from governor Zhou Xiaochuan as if they were fresh in an article on the PBOC’s website Tuesday

- Stan Druckenmiller, who boasts one of the best investor track records over the past three decades, said he’s betting against the euro again and could see himself becoming bearish on stocks

- Sovereign 10Y bond yields lower. Asian, European stocks gain; U.S. equity- index futures rise. Crude oil and copper higher, gold little changed

DB’s Jim Reid completes the overnight wrap

The last 24 hours or so in markets has largely seen a continuation of the trend that we got for the most part during Monday’s session. The positive tone for risk assets extended yesterday with US equities edging closer to their YTD highs. Indeed, despite softening into the close, the S&P 500 finished +0.27% after energy stocks again led the charge following a strong day in Oil markets. The S&P 500 has in fact now rebounded 13% from the August 25th low and is just 1% off the YTD high we reached back in May. European equity markets generally nudged a bit higher despite financials taking a knock following the latest quarterly reports from UBS and Standard Chartered (more on that later). Meanwhile Treasury yields continue to creep up. 10y Treasuries were another 4bps higher at the close yesterday at 2.211% and are now at their highest since September 16th.

The big event this week is Friday’s payroll report for which analysts will get a final chance to fine tune their estimates after today’s October ADP employment change reading where market expectations are currently sitting at 180k after printing at 200k in September. There’s plenty of Fedspeak for us to keep an eye on as well today including Fed Chair Yellen who is due to testify in front of Congress at 3pm London time. While the official topic is on financial regulation, it’s possible that we see Congress also pick the Fed Chair’s brain on her current economic outlook in what will be her first public comments since last week’s FOMC meeting.

Before we get there though, it’s been a strong start for bourses in Asia this morning with decent gains across the board. In China the Shanghai Comp has rallied +2.67% while the Shenzhen is +3.52% and supported by the news out of the PBoC that the much-anticipated Hong Kong-Shenzhen connect is set to be accelerated in a bid to open as soon as this year, although a subsequent release from the PBoC suggests this comment was made earlier this year which is seemingly causing come confusion. In Japan and having reopened from a public holiday yesterday the Nikkei is +1.94% and the Topix is +1.37% while elsewhere this morning, the Hang Seng is +2.38% and ASX +0.10%. Asia credit is around 5bps tighter, while Aus credit is 3.5bps tighter.

Meanwhile, there’s been more data out of China this morning. The non-official services PMI for October has come in at 52.0 which is up 1.5pts from September and the best reading since July. That’s also helped lift the composite PMI up 1.9pts to 49.9. Staying in China, there’s also a story doing the rounds on Bloomberg this morning of another potential Chinese corporate default on the horizon. The article suggests that on October 20th Chinese coal miner Hidili Industry and Development said it was unable be repay $191m of bond interest and principal that was due. One to keep an eye on.

Yesterday evening, ECB President Mario Draghi did little to move the dial following comments which were largely a repeat of what we heard post the ECB meeting nearly 3 weeks ago. Draghi reiterated that ‘the degree of monetary policy accommodation will need to be re-examined at the Governing Council’s December meeting’ and that the Council is willing and able to act by using all the instruments available within its mandate if warranted in order to maintain an appropriate degree of monetary accommodation. This came after the ECB President warned that even though domestic demand remains resilient, downside risks are being created, affecting the outlook for growth and inflation as a result of concerns over growth prospects in emerging markets and other external factors.

The comments actually came as Oil markets were staging a decent rally yesterday. WTI closed +3.81% and just shy of $48, while Brent finished +2.95% and back above $50 for the first time since October 16th. A couple of factors appeared to help support the leg up in prices. A fall in production out of Libya by as much as 70k barrels a day is expected after a force majeure was declared and the Eastern export terminal of Zueitina blocked. Meanwhile there was also some expectation that we may also see a drop in production out of Brazil according to the WSJ, after the nation’s biggest oil-sector union commenced a strike on Sunday.

Moving on, it was a reasonably light day for economic data yesterday. With nothing out in Europe, the main data of note was in the US where we saw factory orders fall during September (-1.0% mom vs. -0.9% expected) more or less in line with expectorations. The November IBD/TIPP economic optimism reading declined 1.8pts and below market to 45.5 (vs. 47.4 expected) but there was better news in the autos sector where total vehicle sales in October rose to 18.1m saar (vs. 17.7m expected) during the month, a second consecutive monthly +18m read. Finally the ISM NY was up a robust 21.3pts to 65.8 (vs. 45.7 expected).

As noted earlier, headlines out of Standard Chartered and UBS attracted plenty of attention yesterday. As part of its restructuring program aimed at shrinking costs, the former announced that it expects to cut up to 15,000 jobs, equivalent to 17% of its workforce. The bank also outlined plans looking at either restructuring or exiting $100bn of assets, while also announcing a sizeable rights issue. Meanwhile UBS, despite reporting some better than expected Q3 earnings yesterday, announced that it expects to take a year longer than expected to reach profitability targets.

Meanwhile VW continues to remain firmly in the spotlight. After we noted yesterday that the scandal looks set to spread to Porsche and Audi, the episode appears to have taken another twist after an internal probe showed that VW also found problems involving carbon dioxide emissions, including petrol-powered vehicles. This latest finding is said to have found ‘unexplained inconsistencies’ on 800k vehicles according to the automaker.

Before we take a look at the day ahead, quickly recapping the latest from earnings season yesterday saw 27 S&P 500 companies report their latest quarterly numbers, with 16 (59%) beating earnings expectations, but just 8 (30%) above revenue expectations. That was a lot softer than the overall trend so far and with nearly 80% of the S&P 500 now having reported (388 companies), 73% having beaten earnings expectations and 44% revenue expectations, down from 74% and 45% respectively this time yesterday.

In terms of the day ahead, data-wise in Europe it’ll be all eyes on the final October services and composite PMI readings for the Euro area, Germany and France. We’ll also get readings for the UK and Italy while Euro area PPI data is also expected. Over in the US this afternoon the main data of note will be the October ADP employment change reading ahead of Friday’s payrolls, while the October non-manufacturing ISM reading will also be closely watched with markets expectations for a 0.4pt fall to 56.5. The full September trade report is also due, while the final October PMI’s are also scheduled to be released. It’s a busy day for Fedspeak also. Fed Chair Yellen is set to address Congress at around 3pm GMT on bank regulatory matters, while Brainard (at 10am GMT) is speaking on financial stability and Dudley (7.30pm) speaking on income inequality. Earnings wise we’ve got 26 S&P 500 companies due to report, headlined by Facebook. 18 Stoxx 600 companies are due to report also.

end

China’s Fixed? Stocks Pop But Yuan Drops After Services PMI Surge

Following Caixin China Manufacturing’s ‘surprise’ jump higher (in the face of the official PMI flat), Caixin Services PMI just beat expectations and bounced considerably to ‘healthy expanding’ 52.0, bringing the Composite PMI to 49.9 – thus proving that billions of dollars of liquidity injections, market interventions, debt transfers to SOEs, arrests, shootings, and general thuggery has fixed China. For now stocks are rallying on this news but offshore Yuan is continuing to leak back to Friday’s lows.

Is China Fixed?

Who knows?

Chinese stocks are recovering on the ‘good’ news…

But it seems the Yuan continues to weaken...

Charts: Bloomberg

Bitcoin Soars To 14-Month Highs As Major Exchange Eases Access For Chinese

Bitcoin, at $444, is now up over 100% since we suggested, in early September, it would become the conduit for Chinese capital outflows following China’s crackdown on capital controls. This afternoon’s sudden BIS-induced plunge, taking the virtual currency down $50, has been entirely retraced and more as BTCC (China’s leading Bitcoin Exchange) announced it will now accept direct deposits (making it significantly easier for Chinese to rotate their Yuan deposits into the virtual currency and out of the potential clutches of capital controlling communists).

As BTCC details,

Recent bitcoin price increases have reignited enthusiasm in buying bitcoin. BTCC is confident this trend will continue. As such, we are pleased to announce that we now accept direct deposits.

Customers now need only log in, click on “Account,” then “Fund,” and then select the “Bank Deposit” option to fund their BTCC accounts through their bank accounts. All customers who have Chinese bank accounts will be able to make direct deposits through ATM transfers or online banking.

And adds, even more crucially…

BTCC will stop accepting customer deposits through agents on November 15.

Which appeared to provide further dip-buying impetus to the recovery off the day’s earlier mysterious plunge...

Lifting BTC to $444 highs, more than double the September levels when we suggested it. Notice the rally is on rapidly increasingly volumes also (as word spreads and ease of access is enabled)…

As we noted previously, this is the validation that, just as predicted here two months ago, bitcoin has become the go-to asset class for millions of Chinese savers seeking to quietly and under the radar transfer funds from point A to point B, whatever that may be, in the process circumventing the recently expanded governmental capital controls:

While he didn’t provide any concrete numbers, he did comment last week on what was driving the adoption. “Some Chinese traders are expressing a view on the CNY exchange rate after the last devaluation and you have interest by mainland speculators to move to other assets after the stock market fallout,” he explained in an interview with Bitcoin Magazine.

Which again brings us back to our conclusion from two months ago:

… if a few hundred million Chinese decide that the time has come to use bitcoin as the capital controls bypassing currency of choice, and decide to invest even a tiny fraction of the $22 trillion in Chinese deposits in bitcoin (whose total market cap at last check was just over $3 billion), sit back and watch as we witness the second coming of the bitcoin bubble, one which could make the previous all time highs in the digital currency, seems like a low print.

As of this moment, the total value of bitcoin is up from the $3 billion two months ago to a little over $5 billion. That means the ratio of Chinese deposits (at around $22 trillion) to bitcoin, is down to a far more “conservative” 4,400x.

And now, again, imagine what could happen if these same Chinese depositors realize they have been lied about the non-performing loans “backing” their deposits and that instead of the official 1.5% bad debt ratio, the real number is really far greater, somewhere in the 20% ballpark as we will show shortly, suggesting major deposit impairments are no longer the stuff of Cypriot nightmares but just the thing hundreds of millions of Chinese depositors have to look forward to, and that they have just two possible choices to avoid said impairment: reallocating their savings into bitcoin or, of course, gold.

* * *

How will the Chinese regulators and government react to this? Especially as the volumes are start to become relevant.

end

Volkswagen Tumbles Again As Emissions Scandal Deepens, Gasoline Engines Dragged In: Wall Street’s Reaction

The thing about sweeping corporate scandals is that once you start finding out where all the bodies are buried you usually discover that whatever event or revelation served as the impetus for the investigation was in fact just the tip of the proverbial iceberg.

Indeed, it now looks as though that assessment will certainly apply to the Volkswagen emissions scandal because as it turns out, in addition to software installed on some 11 million diesel vehicles designed to game nitrogen oxide tests, Germany’s largest carmaker has also been habitually understating CO2 output on around 800,000 cars sold in Europe.

As Bloomberg reports, the company found “unexplained inconsistencies” while conducting an internal probe related to carbon-dioxide output.

For the first time, gasoline engines are also said to be affected.

“VW is leaving us all speechless,” Evercore ISI’s Arndt Ellinghorst said. “It seems to us that this is another issue triggered by VW’s internal investigation and potentially related to Europe.”

It “seems” that way to us as well. Meanwhile, the company is fighting allegations by the EPA that some SUVs sold in the US are also equipped with questionable “software.” From Reuters:

U.S. environmental regulators said on Monday that similar “defeat devices” were installed on larger 3.0 litre engines used in luxury sport utility vehicles from Porsche and Audi, although VW has denied those allegations.

Porsche’s North American unit said it was discontinuing sales of Porsche Cayenne diesel sport utility vehicles until further notice, citing the allegations.

And from BofAML:

The EPA issued a second notice of violation of the Clean Air Act to VW, potentially increasing the fines the company is liable for. Under the Clean Air Act, the EPA can fine a car manufacturer up to $37,500 per vehicle for violations. The EPA held a press conference yesterday to announce the results. The EPA (along with counterparts in California and Canada) found that, when the defeat device was deactivated, total emissions of nitrogen oxide were up to nine times the amount permitted. Since the VW diesel scandal broke in September, the EPA has been testing all the new diesel models available in the US. So far, only VW has been implicated.

Finally, from Bloomberg:

The 3.0-liter diesel motors targeted on Monday by the EPA probe aren’t part of the latest company finding. Volkswagen rejected allegations that its cheating on diesel-emissions tests included the Porsche Cayenne and VW Touareg sport utility vehicles and as well as larger sedans and the Q5 SUV from Audi, setting up a showdown with the regulator.

“You’re fighting against the biggest regulator in the world,” Arndt Ellinghorst, a London-based analyst in Evercore ISI, said on Bloomberg TV. “This can get pretty ugly.”

Yes it sure can. And speaking of ugly, here’s a look at the reaction in VW shares:

As far as the new findings regarding CO2 emissions are concerned, the company said the issue could add some €2 billion to the nearly €7 billion already earmarked for vehicle “repairs.” Here’s a peak at the sellside reactions:

- Exane BNP Paribas (neutral, PT EU116)

- Adding EU4b in VW recall/compensation costs for the latest 800k cars to previous est. EU12b costs

- Reducing 2016 EPS by 10%, may affect customer behavior more than diesel engine recall

- See potential ramifications across sector; sees CO2 risks greatest at Daimler and least at Renault

- Tire makers may be safest place in sector

- JPMorgan (neutral)

- Latest news brings total provisioning to EU8.7b, JPM est. total liability now EU13.2b including legal claims

- Co. leaving “no stone unturned,” has EU27.8b net cash to face crisis

- Credit Suisse (underperform)

- New EU2b provision implies cost of EU2,500/car for gasoline engine vehicles affected vs EU609/car for diesels

- “Key question” remains whether there will be other disclosures

- See VW’s credibility deteriorating; uncertainty not priced in

- UBS (buy)

- Will add to pressure on VW shares and concern about costs and governance

- Reiterates investment case; sees EU32b negative value after EU35b in total fixing and litigation costs, co can cope with those costs over 5+ yrs without raising capital

So yeah, bad news all around. Barclays is also out with a bit of commentary on the near-term implications:

According to Automotive News Europe, the models affected are VW, Seat and Skoda vehicles that use 1.4-, 1.6- and 2.0-liter diesels built in 2012 and later. These so far include VW Golf, Polo, Passat, Audi A1 and A3, Seat Ibiza and Skoda Octavia models. VW’s 1.4-liter ACT gasoline engine in the Polo that has cylinder on demand technology is also affected. The issue of potentially false CO2 levels mainly affects Europe, the biggest market for diesel cars, where a model’s carbon emissions are always communicated to consumers.

We believe that this latest development increases the risk of a downgrade at Moody’s (A2 negative) given that the agency only changed the outlook from stable to negative so far. Fitch (A Watch negative) could also decide to act on its negative watch and cut by one notch and keep the company on watch negative, as S&P did in October 2015 (A- Watch negative).

As for the longer-term implications, just about the last thing Germany needs is for its exports to be crippled by the demise of the largest player in the country’s proud auto industry just as demand from China collapses. On that note, we remind you that the surest sign of a problem is when officials and policymakers start telling the public there’s no problem and with that, we close with comments out today from German Economy Minister Sigmar Gabriel:

“I’m firmly convinced, with more than 100 years of experience in quality from the ‘Made in Germany’ label in industrial production, that this problem will be overcome. I’m very certain that this won’t mean sustained damage to German industry.”

* * *

“Stability in volatile times”…

end

The Volkswagen scandal and more talk from Draghi of further QE softens the Euro/USA cross. A huge dagger into the heart of USA multinationals:

(courtesy zero hedge)

EURUSD Hammered To 1.08 Handle, 3-Month Lows

After Draghi’s moar dovishness yesterday, this morning’s “meh” US data has sparked another leg lower in EURUSD (as December rate-hike odds rise modestly from 52% to 55%). EURUSD is now trading with a 1.08 handle for the first time since early August... more pain for US corporate earnings…

Just keeps falling…

Banging EURUSD to 3-month lows, drastically lower since Draghi said The ECB GC had talked about easing more…

Dogfights Next? US Sends F-15 Jets To “Counter” Russian Air Force Over Syria

When the Obama administration announced it would soon put 50 (er… 100 we guess, since soldiers generally have two feet) boots on the ground in Syria, the US media immediately asked the wrong set of questions.

As we noted in “US Sends Troops To Syria: Here Are The Questions The Media Should Be Asking,” the Josh Earnest presser was nothing short of a joke, as the media peppered the Press Secretary with question after question about whether the President had gone back on his promise (made to the American people at least 16 times) to not put US ground troops into combat in Syria.

Of course that completely misses the point. And here’s why:

There have been boots on the ground in Syria and Iraq for years and indeed, the public seems to have forgotten that just five months ago, US commandos executed a raid in Syria that purportedly killed Islamic State’s “gas minister” (and yes, that’s just as absurd as it sounds).

Additionally, Washington has made no secret of the now defunct “train and equip” program for Syrian rebels – clearly, the American public hadn’t thought very hard about who was doing the on-the-ground “training.”

Finally, there’s no telling how many CIA operatives and black ops have been running around in Syria assisisting Saudi Arabia and Qatar’s proxy armies from the very beginning.

Given that, there are two questions everyone should be asking: 1) how does Washington plan to explain to Ankara that the Pentagon is set to embed US ground troops with the YPG in Syria and fly sorties from Incirlik in support of those ground troops when Turkey is literally flying from the exact same airbase on the way to bombing the exact same YPG forces with whom the US is set to embed?, and 2) how does the US intend to make sure that Russia doesn’t end up “accidentally” bombing US positions?

Well, one way to answer both of those questions is to send US dogfighters to Syria. The Daily Beast reports:

The U.S. Air Force is deploying to Turkey up to a dozen jet fighters specializing in air-to-air combat—apparently to help protect other U.S. and allied jets from Russia’s own warplanes flying over Syria.

Officially, the deployment of F-15C Eagle twin-engine fighters to Incirlik, Turkey—which the Pentagon announced late last week—is meant to “ensure the safety” of America’s NATO allies, Laura Seal, a Defense Department spokesperson, told The Daily Beast.

That could mean that the single-seat F-15s and the eight air-to-air missiles they routinely carry will help the Turkish air force patrol Turkey’s border with Syria, intercepting Syrian planes and helicopters that periodically stray into Turkish territory.

But more likely, the F-15s will be escorting attack planes and bombers as they strike ISIS militants in close proximity to Syrian regime forces and the Russian warplanes that, since early October, have bombed ISIS and U.S.-backed rebels fighting the Syrian troops.

Well, kind of. We could always be wrong, but it seems unlikely that The Pentagon is going to send F-15s into battle against Russian fighter pilots in western Syria. What’s pretty clearly going on here is that Washington is sending just enough air support to ensure that once the Russians and Iranians secure Syria’s major cities in the west, the US has the capability to shoot down Russian jets should they threaten whatever the hell Washington’s spec ops are trying to accomplish near Raqqa in conjunction with the YPG. Anyway, back to The Daily Beast:

Seal declined to discuss the deployment in detail, but hinted at its true purpose. “I didn’t say it wasn’t about Russia,” she said.

Russia’s air wing in western Syria is notable for including several Su-30 fighters that are primarily air-to-air fighters. The Su-30s’ arrival in Syria raised eyebrows, as Moscow insists its forces are only fighting ISIS, but ISIS has no aircraft of its own for the Su-30s to engage.

The F-15s the U.S. Air Force is sending to Turkey will be the first American warplanes in the region that are strictly aerial fighters. The other fighters, attack planes and bombers the Pentagon has deployed—including F-22s, F-16s, A-10s and B-1s—carry bombs and air-to-ground missiles and have focused on striking militants on the ground.

In stark contrast, the F-15s only carry air-to-air weaponry, and their pilots train exclusively for shooting down enemy warplanes. It’s worth noting that F-15Cs have never deployed to Afghanistan, nor did they participate in the U.S.-led occupation of Iraq. The war in Syria is different.

And while that is indeed interesting, the following is nonsense:

Incirlik and its growing contingent of warplanes is the key to a new northern strategy in the U.S. campaign against ISIS, an unnamed Pentagon official said on Oct. 30. “One of the principal things we will do to put pressure in the border area and into Syria is, quote, ‘thicken’ air operations in northern Syria.”

“That means we want a greater density of planes striking. We need a greater density of intelligence assets developing targets. You—the White House announced A-10s, which are already on the ground at Incirlik, and F-15s forthcoming on—in Incirlik, to help in the counter-ISIL campaign,” the official added, using another acronym for ISIS.

As we’ve said on too many occasions to count, if Washington and Ankara (both of which are flying from Incirlik) were that concerned about ISIS in the “border area”, then they wouldn’t have explicitly forbidden the YPG from advancing on ISIS west of the Euphrates.

In the final analysis, Washington has absolutely no idea what’s going to happen now that i) the PKK has suffered a bitter electoral defeat at the hands of Erdogan in Turkey, and ii) it’s just a matter of time before Hezbollah advances on Raqqa supported by Russian warplanes and so, the Pentagon is sending in the dogfighters to make sure that in case something goes horribly wrong, the US can shoot down whoever happens to be in the sky before the “50” spec ops get bombed.

In New Audio, Video ISIS Says “We Downed” Russian Plane, Threatens Putin With Bowie Knife From Front Yard

The thing about the ongoing “war” on terror is that it seems to get more surreal by the day and indeed, the videos, pictures, and claims that emanate from ISIS’ media arm are at times so outlandish, violent, and outright bizarre that quite a few observers have questioned how they can possibly be authentic.

There was the clip purporting to show members building flying landmines out of condoms for instance and let’s not forget the nearly hour long video (that at times appeared as though it walked right out of a high school social studies class) explaining why ISIS intended to wean the world off of fiat money and transition back to the gold dinar.

And of course no critique of ISIS propaganda would be complete without mentioning their uncanny ability to produce Hollywood-esque murder montages violent enough to make Quentin Tarantino blush (a few installments back, ISIS filmed the drowning of a handful of “spies” and judging from the video, high quality underwater video cameras are something you regularly come across in the Syrian countryside).

Finally, in what has to be considered the silliest terror-related story of the year, al-Qaeda was out this week calling ISIS leader Bakr al-Baghdadi a “feeble, failure person.” ISIS responded by calling al-Qaeda a bunch of “donkeys.” If you want to understand just how surreal the whole thing is, look no further than the following picture (note that everyone looks to be wearing white, high top Nikes):

Well, the story took a further turn for the ridiculous on Wednesday after IS Sinai, apparently aggravated by claims that their video of an exploding plane doesn’t actually depict the destruction of the Russian passenger jet that crashed in the Sinai Peninsula last Saturday, released an audio message to confirm that they did indeed “down” the plane and that they’ll prove it when they’re good and ready and not a minute prior.

Some highlights:

- “We downed Russia plane, so die in your rage.”

- “Bring your black box, and do your analysis...prove we didn’t down it...we will reveal the way at the time we wish.”

- “We are the ones who downed it thank to God and we are not forced to reveal how we downed it.”

The group says that for now, the proof is that the attack coincided with the one-year anniversary of IS Sinai’s pledge of allegiance to Baghdadi (Ayman al-Zawahiri’s “feeble, failure person”) but the dates appear to be questionable.

Whatever the case, it doesn’t seem to have occurred to IS Sinai that they are asking the world to prove a negative.

Meanwhile, the home office in Raqqa is out praising the supposed “downing.” In a new video, five ISIS members praise the actions of their “Sinai brothers” and then go the extra mile by directly threatening Vladimir Putin. The video:

Here’s a screenshot for your amusement:

And yes, that is an actual still shot from the video.

Five guys sitting in the front yard waving a bowie knife at The Kremlin.

There you go Moscow. Your move.

Bomb May Have Brought Down Russian Plane Over Egypt, U.K. Says

-

U.K.-bound flights halted from Sharm el-Sheikh for security

-

David Cameron calls emergency meeting of COBRA committee

U.K. Prime Minister David Cameron’s office said that a bomb may have brought down the Russian plane that crashed in Egypt on Saturday.

The statement from the usually cautious British government is the strongest indicator yet that terrorists may have been responsible for the crash of the Metrojet Airbus Group SE A321, which was carrying 224 people. So far there haven’t been any findings released by investigators suggesting whether a bomb, some other explosion or a structural failure caused the plane to break into pieces and fall to the ground.

“While the investigation is still ongoing we cannot say categorically why the Russian jet crashed,” Cameron’s office said in an e-mailed statement on Wednesday. “But as more information has come to light we have become concerned that the plane may well have been brought down by an explosive device.”

Britain isn’t formally a party to the probe and the government statement didn’t say whether its actions are based on findings from the crash investigators or an interpretation of information already in the public domain. Egypt said Wednesday that the Airbus’s cockpit-voice recorder was damaged in the crash and that work is required to access its final few minutes. The flight-data device has been decoded and work will begin on that information shortly.