Gold: $1088.20 up $.30 (comex closing time)

Silver $14.36 down 6 cents

In the access market 5:15 pm

Gold $1089.90

Silver: $14.42

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very poor delivery day, registering 0 notice for nil ounces. Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 208.60 tonnes for a loss of 94 tonnes over that period.

In silver, the open interest surprisingly fell by only 1462 contracts despite silver being down 27 cents in yesterday’s trading. The total silver OI now rests at 165.289 contracts In ounces, the OI is still represented by .826 billion oz or 118% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI fell by 1581 contracts to 438,385 contracts despite the fact that gold was only down by $0.30 yesterday. it seems the modus operandi of the bandits is to liquefy gold/silver OI. We had 0 notices filed for 100 oz today.

We had a slight addition in gold inventory at the GLD to the tune of 0.32 tonnes / thus the inventory rests tonight at 666.43 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,no change in silver inventory / Inventory rests at 313.681 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by only 1,462 contracts down to 165,278 despite the fact that silver was down 27 cents with respect to yesterday’s trading. The total OI for gold fell by a rather large 1,581 contracts to 436,804 contracts despite the fact that gold was down only 30 cents yesterday.

The fact that OI continues to remain high in silver necessitates the bankers to continue raiding hoping to shake the leaves from both the gold and silver trees. Remember that December is generally a big delivery month for both gold and silver

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

9 USA stories/Trading of equities:

i) Apple cuts component orders by 10% as global aggregate demand softens

(zero hedge)

ii) Looks what happens when China sends her deflation to the rest of the world:

(zero hedge)

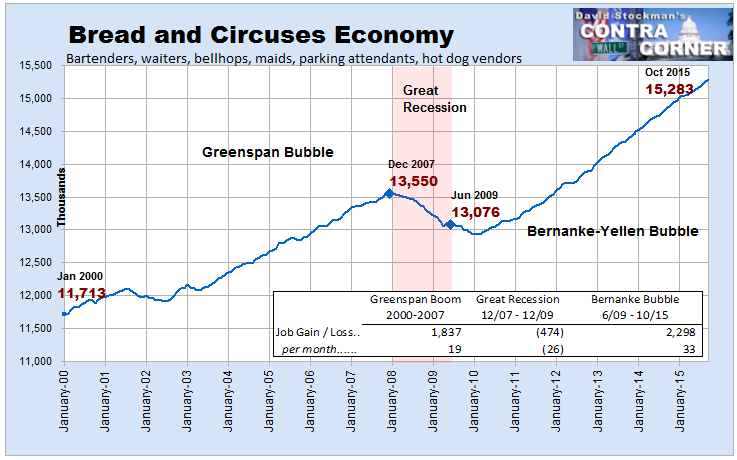

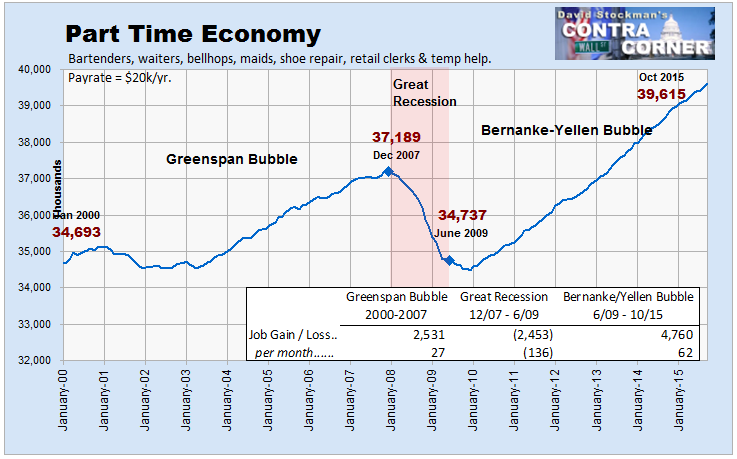

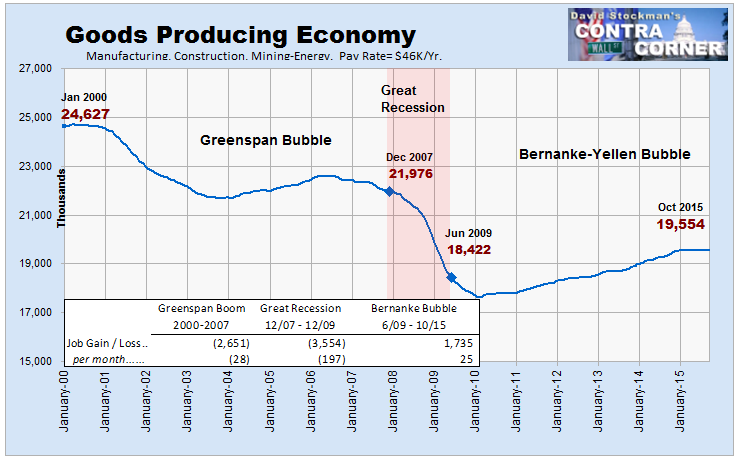

iii) The real truth behind the jobs report: the declining manufacturing jobs vs leisure time part time gains

generated through the factitious B/D and further adjustments

( David Stockman)

iv) The Fed is worried about the soundness of the USA banks

(Simon Black/Sovereign Man)

v) The phoniness is the retail jobs and the construction jobs in the latest jobs report

(zero hedge)

vi Something to worry about: the spread between retail sales and inventories have never been greater

(zero hedge)

vii) Fast food workers are going on strike. With automation here, just why on earth are they striking?

(zero hedge)

viii) Continuing with the fast food industry:

10. Physical stories

i) Koos Jansen reports on gold demand (SGE withdrawal) in the latest weekly report: 47 tonnes.

He compares gold deliveries at the SGE vs comex. It is nutshell, they are totally different

(Koos Jansen)

ii) James Turk believes (as do I) that the gold that has been fed by the uSA into the market is from the FRBNY

(James Turk/Kingworldnews)

iii) Hugo Salinas Price… what is Bitcoin?

(Hugo Salinas Price)

iv) China now allows the direct conversion from yuan into Swiss francs and visa versa, totally by-passing the dollar

(Bloomberg/GATA)

v) Bill Holter interview by Palisades Radio

(Bill Holter0

vi) Dave Kranzler on the looting of GLD gold:

(Dave Kranzler/iRD)

vii Nyrstar does a rights offering and 20% owned Trafigura is buying 50% of the rights offering raising their level to 30% of the company. They are contemplating removing 400,000 tonnes of zinc concentrate from the market to order to raise the price of zinc

(zinc news)

viii Dave Kranzler talks about that other base metal company is trouble;

Glencore

(Dave Kranzler/IRD)

Take a look at the discrepancy in silver production reporting from our major country producers!!

looks to me like the supply of silver is coming down!!!

a great paper!!

(courtesy Steve St Angelo/SRSRocco report)

Let us head over to the comex:

The total gold comex open interest fell from 438,385 down to 436,804 for a loss of 1,581 contracts despite the fact that gold was down by only $0.30 with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. The November contract fell by 0 contracts remaining at 211. We had 0 notices filed yesterday, so we neither lost nor gained any gold contracts that will stand for delivery in this non active delivery month of November. The big December contract saw it’s OI fall by 10,338 contracts from 247,319 down to 164,476. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 164,476 which is good. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was good at 172,212 contracts and aided by copious HFT trading.

November contract month:

INITIAL standings for November

Nov 10/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 7,046.878 oz

(Scotia, Brinks,Manfra |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today | 0 contracts

|

| No of oz to be served (notices) | 211 contracts

(21,100 oz) |

| Total monthly oz gold served (contracts) so far this month | 7 contracts

700 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 89,423.6 oz

|

Total customer deposits nil oz

we had 0 adjustments:

November initial standings/First day notice

Nov 10/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 95,399.720 oz |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 5 contracts

25,000 oz) |

| Total monthly oz silver served (contracts) | 5 contracts (25,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,512,989.6 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: nil oz

total withdrawals from customer account: 803,216.592 oz

And now SLV

Nov 10/no change in silver inventory at the SLV/rests tonight at 313.681 million oz/

Nov 9/no change in silver inventory/rests tonight at 313.681

Nov 6/ we had a very tiny withdrawal of 136,000 oz (probably to pay for fees)/Inventory rests tonight at 313.681 oz

Nov 5/strange no change in silver inventory/rests tonight at 313.817 million oz/

Nov 4/2015: no change in silver inventory/rests tonight at 313.817 million oz/

Nov 3.2015; no change in silver inventory/rests tonight at 313.817 million oz/

Nov 2/a withdrawal of 716,000 oz from the SLV/Inventory rests tonight at 313.817 million oz

Oct 30.no change in silver inventory at the SLV/Inventory rests at 314.532 million oz

Oct 29/a big withdrawal of 1.001 million oz from the SLV/Inventory rests at 314.532 million oz

Oct 28.2015: no change in silver inventory at the SLV//inventory rests at 315.533 million oz.

Oct 27/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 26/no change in silver inventory at the SLV/Inventory rests at 315.533 million oz/

Oct 23./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 22./no change in silver inventory at the SLV/Inventory rests at 315.533 million oz

Oct 21:a we had a small addition in silver ETF inventory of 381,000 oz/inventory rests tonight at 315.533 million oz

Oct 20.2015/ no change in silver ETF/Inventory rests at 315.152 million oz

One of America’s Largest Online Retailers Is Stockpiling Gold and Silver Coins to Pay Employees In Coming Crisis

One of America’s largest companies is preparing for problems in the banking and financial system and another financial crisis.

Online retail giant Overstock.com (OSTK), publicly stated that the company has stockpiled gold and silver coins in preparation for another U.S. financial crisis. Patrick Byrne, its founder and chief executive, is a libertarian who champions crypto currencies, bitcoin and gold and silver bullion as financial insurance against risk in the financial and monetary system.

Patrick Byrne, CEO of e-commerce giant Overstock.com

Overstock Chairman, Jonathan Johnson recently told an audience at the United Precious Metals Association:

“We are not big fans of Wall Street and we don’t trust them. We foresaw the financial crisis, we fought against the financial crisis that happened in 2008; we don’t trust the banks still and we foresee that with QE3, and QE4 and QE n that at some point there is going to be another significant financial crisis.”

Quantitative easing (QE) is when central banks create billions and trillions worth of fiat currency out of thin air and inject it into the financial system rising currency debasement and inflation in the long term.

Johnson went on to explain the company’s preparations:

“So what do we do as a business so that we would be prepared when that happens? One thing that we do that is fairly unique: we have about $10 million in gold, mostly the small button-sized coins, that we keep outside of the banking system. We expect that when there is a financial crisis there will be a banking holiday. I don’t know if it will be two days, or two weeks, or two months. We have $10 million in gold and silver in denominations small enough that we can use for payroll. We want to be able to keep our employees paid, safe, and our site up and running during a financial crisis.

We also happen to have three months of food supply for every employee that we can live on.”

A further insight into the company’s preparations for a crisis can be seen in the company’s latest 10-Q filed with the SEC:

“Our precious metals consisted of $6.3 million in gold and $4.6 million in silver at June 30, 2015 and December 31, 2014. We store our precious metals at an off-site secure facility. Because these assets consist of actual precious metals, rather than financial instruments, we account for them as a cost method investment initially recorded at cost (including transaction fees) and then adjusted to the lower of cost or market based on an average unit cost”.

![]()

Johnson, Overstock’s anti-establishment chairman, told the Financial Times it holds the bullion coins outside the banking system so the company could pay employees even if banks close for a period of time in a crisis – as was seen in Cyprus and Greece in recent months:

“We thought there’s a decent chance that there could be a banking holiday at some point caused by a crisis and it could last for two days or two weeks or who knows how long, and we wanted to be in a position where we could continue to operate during any such crisis,” he said.

GoldCore is advising companies internationally to allocate capital to gold and silver bullion as a way to diversify their assets. This is prudent given the risks of today and need for financial insurance to protect against bank bail-ins, capital controls, “bank holidays”, currency debasement and other risks posed by another financial crisis.

DAILY PRICES

Today’s Gold Prices: USD 1092.50, EUR 1017.23 and GBP 723.50 per ounce.

Yesterday’s Gold Prices: USD 1095.60 , EUR 1015.90 and GBP 725.95 per ounce.

(LBMA AM)

Gold closed higher yesterday up $3.10 to $1091.10. Silver lost $0.18 to close at $14.56. Platinum lost $28 to $910.

Gold in USD – 5 Years

Gold has eked out small gains and appears to be stabilising at just above five-year lows reached in July, after last week’s nearly 5% plunge.

Less than two weeks ago – on October 28th – gold was trading at $1180 per ounce and has declined a sharp 8 per cent in just two weeks. Value buyers and those dollar cost averaging into position are taking advantage of the price weakness.

Indian demand for gold and silver remains robust as we had into the Indian festival season. Gold and silver coins saw good demand on Dhanteras in India today instead of jewellery. It was noted that consumers were on a buying spree due to lower prices.

According to jewellers and bullion dealers MMTC-PAMP India, the buying activity remained robust in the first half of the day at most places. But more sales are expected later in the day, with office-goers coming in for buying late in the evening.

Dhanteras is considered to be an auspicious day for buying gold and silver and is largely celebrated in North and West India.

Essential Guide to Gold Storage in Singapore

end

Here is Steve St Angelo’s latest piece of silver

Take a look at the discrepancy in silver production reporting from our major country producers!!

looks to me like the supply of silver is coming down!!!

a great paper!!

(courtesy Steve St Angelo/SRSRocco report)

Biggest Silver Supply Losers For 2015

As the financial and economic systems continue to disintegrate, this will put more stress will on the silver market. Why? Because elevated physical silver investment demand will likely exceed available silver supply in the future. Even though physical silver investment demand has fallen off since the huge spike starting in June, market conditions have impacted supply in a negative way.

According to the most recently released data, three of the top five silver producing countries are showing large declines in production compared to the same period last year. When I researched the mine supply figures, I came up with some conflicting data. For some strange reason, my data showed a decline in Mexican silver production, while figures from another source stated an increase.

I wrote the organization responsible for providing silver production figures to the Chile Copper Commission. You see, the Chile Copper Commission (Cochilco.cl) provides global production data on many metals. They use data from World Metal Statistics.

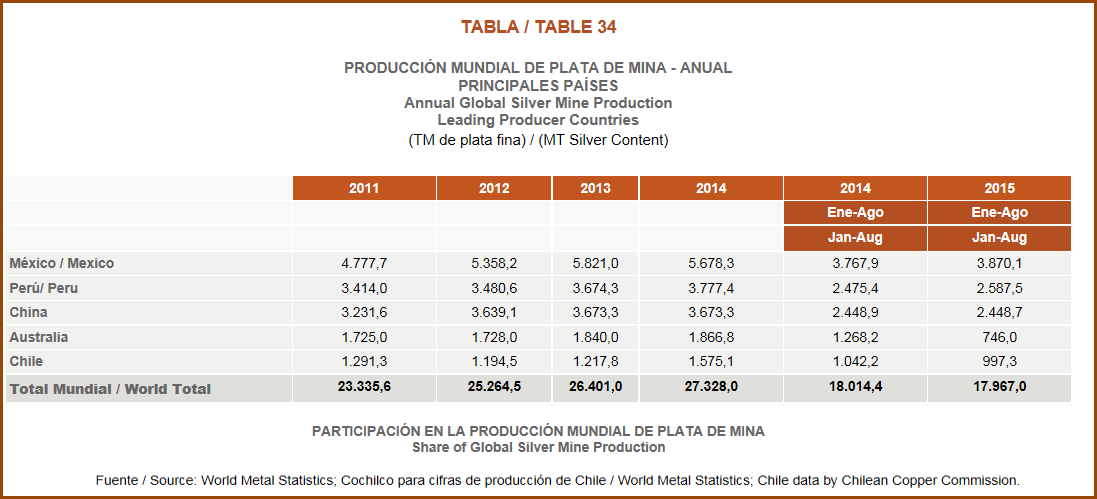

Here is a snapshot of their monthly world silver production update:

Please click on the table to see a larger image. If you look at Mexico silver production, they show an increase to 3,870.1 metric tons (mt) JAN-AUG 2015 up from 3,767.9 mt during the same period in 2014. From this report, Mexico’s silver production JAN-AUG 2015 increased 102 mt, or 3% year over year (yoy).

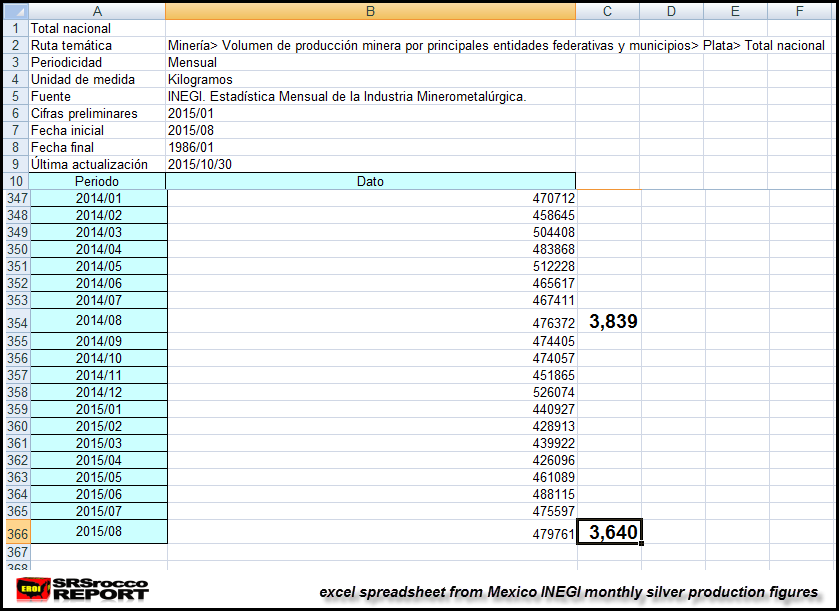

However, I spoke with a person at Mexico’s Department of Mineral Resources (INEGI), and they sent me the link to their monthly silver production figures. I downloaded the excel spreadsheet and made a screenshot show below:

I added the total of Mexican silver production from JAN-AUG 2014 and 2015 and put the figures in the next column. As you can see from Mexico’s official INEGI monthly data, silver production is down from 3,839 mt in JAN-AUG 2014 to 3,640 mt during the same period this year.

So, instead of Mexican silver production being up 3% this year (according to data from World Metal Statistics), it’s actually down 6% if we go by official Mexican INEGI figures.

When I contacted World Metal Statistics about this inconsistency, they were nice enough to reply. I asked them why was their Mexican silver production showing an increase while Mexico’s official data reports a decline? They stated that they do use INEGI data for their silver production figures, but they use different data for the Chile Copper Commission.

That being said, they were surprised that Mexico showed a decline in silver production in 2015. I sent them the excel spreadsheet from Mexico’s INEGI, and they told me that their data was different. They replied to me stating that they had to update all their Mexican silver production data back to 2011… as it was revised and I gather they revised it using incorrect data. How interesting.

I find this quite interesting because it costs an individual 2,240 Euros to purchase 12 monthly metal production reports from World Metal Statistics. Readers on my site, get to find out this information for FREE.

NOTE: I will be including a DONATE BUTTON on the site shortly. After many requests from readers, I decided to finally add this function for the individuals who would like to donate for the public research and articles on the site.

While I used some of the silver production data (in the chart below) from the Copper Commission Table shown above, I double checked Peru’s and Australia’s silver production from their official state figures.. and they matched up. That being said, I also have a problem with World Metals Statistics “Total World Silver Production Figures” shown at 17,967 metric tons (mt) JAN-AUG 2015 compared to 18,014 mt during same period in 2014. These figures come from the Chile Copper Commission table above.

Basically, World Metal Statistics shows a small reduction in total global silver supply JAN-AUG 2015 compared to last year. Even if we adjust the revised lower Mexican silver production data, total world silver production is only down 2.5%… again, according to their figures.

However, if we just go by the top five producers (Mexico, Peru, China, Australia & Chile), overall silver production in down 6%. I gather World Metal Statistics is saying the rest of the countries are reporting increases to show just an average loss of 3% worldwide. Unfortunately, some of the other countries such as Canada are reporting declines in silver production.

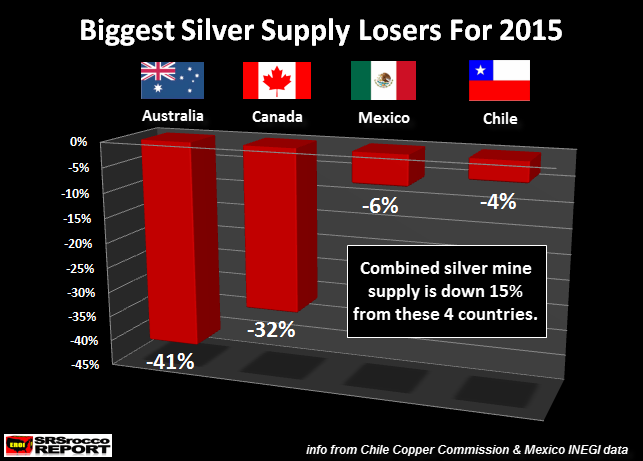

Here are the biggest silver supply losers for 2015:

As we can see from the chart above, Australian silver production JAN-AUG 2015 is down a whopping 41% compared to the same period last year, followed by Canada down 32%, Mexico down 6% and Chile down 4%. The combined silver production from these four countries is down 15% compared to last year.

Here is additional silver production data from three countries:

Russia’s Polymetal Jan-Sep 2015 = +53 mt

Poland’s KGHM Polska Jan-Jun 2015 = + 6 mt

United States Jan-Aug 2015 = -22 mt

If we just add up these three producers, we find a net increase of about 37 metric tons. Of course, these show different periods, but an increase of even 40-50 mt for these producers won’t change the overall decline of the top five down 684 mt JAN-AUG 2015.

I would imagine the low metal prices going forward will continue to impact global silver production. Chile, the largest copper producer in the world, is showing a 4% decline in silver production this year. The majority of silver production from Chile is a by-product of copper mine supply. As the price of copper continues to fall, we will see more companies shut down copper mines. This will have a negative impact on global silver supply going forward.

I will be writing future articles on how the future silver supply, demand and price will impact the market in the next several weeks and months.

—————-

If you haven’t checked out THE SILVER CHART REPORT, there’s a great deal of information on the Silver Industry & Market not found in any single publication on the internet. There is one chart in this report (Chart #19) that I can guarantee that 99.9% of precious metal investors haven’t seen before.

I use this bird’s-eye approach when I create my easy to understand charts. The Silver Chart Report is a collection of my top silver charts from articles published over the past six years, and includes in-depth, never-before-seen charts and content that indicate that silver is on the rise. There are 48 charts in the report, broken down in five sections.

Please check back for new articles and updates at the SRSrocco Report. You can also follow us at Twitter below:

end

This morning:

China allows the direct conversion between yuan and Swiss francs totally by-passing the dollar

(Bloomberg/GATA)

China to allow direct conversion between yuan and Swiss franc

Submitted by cpowell on Mon, 2015-11-09 16:17. Section: Daily Dispatches

By Fion Li

Bloomberg News

Monday, November 9, 2015

China took another step to boost the yuan’s global usage, saying it will start direct trading with the Swiss franc, as the nation pushes its case for reserve-currency status at the International Monetary Fund.

The link will start on Tuesday, the China Foreign Exchange Trade System said in a statement, making the franc the seventh major currency that can bypass a conversion into the U.S. dollar and be directly exchanged for yuan. The rate will be allowed to fluctuate a maximum 5 percent on either side of a daily fixing, according to CFETS. …

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2015-11-09/china-to-allow-direct-…

end

Dave Kranzler on the looting of GLD gold:

I agree with Dave in that with huge troubles in the steel industry, the base metals industry, and the oil industry there must be huge derivative train wrecks.

a must read…

(courtesy Dave Kranzler/IRD)

GLD Is Being Looted To Help Banks Manipulate The Price Of Gold

The choke hold put on the precious metals the past several days has been relentless, Eric. It was so forceful, it might even have been unprecedented…the selling is being driven by the paper-gold market and the central planners no doubt have had a hand in it. The paper-gold they sell needs to be matched from day to day with a show of force, and the only way to do that is being able to deliver physical metal when the buyer of your paper promise asks for physical metal rather than cash settlement. – James Turk on King World News

The price of gold pushed through its 200 dma and hit a high of $1191 on October 15. It appeared ready to assault $1200 (click to enlarge):

But over the next 17 trading days 36 tonnes of gold was removed from the GLD Trust. Most of the gold – 29 tonnes – was removed in the last 9 trading days to facilitate manipulating the price back below 200 day moving average (red line in the graph above).

There’s unquestionably something wrong behind the “curtain.” With the increasing meltdown in various areas of the global financial system (energy, commodities, high yield debt, leveraged loan portfolios, biotech stock, Glencore/Lonmin, emerging market currencies, etc) the OTC derivatives market must be littered with train wrecks.

At a time when the price of gold should be soaring to reflect the increasing financial, economic and political turmoil brewing, the western Central Banks/banks are relentlessly manipulating the price. Without a doubt they have had to resort to raiding GLD in order to make the deliveries referenced at the top by James Turk.

Now we have to endure another round of the “we’re going to raise rates this time, we promise” game. How many times can the Fed get away with hammering Wall Street’s calcified brain trust and the financial media over the head with this farce?

With the level of systemic debt in the U.S. (Federal, State, corporate, individual and pension debt in the form of underfunding) going parabolic, economic activity quickly fading, financial landmines going off behind the scenes and geopolitical risk escalating, the only way the Fed can maintain any level of credibility is to prevent the price of gold from engaging in bona fide, market-determined price discovery.

At some point the Central Banks will lose their ability to contain the price of gold. We’re already starting to sense their level desperation in this endeavor as reflected in the paper gold to deliverable ratio on the Comex, the gold being drained from the Fed’s vaults and the removal of gold from GLD.

Remember that we told you about the troubles in Nyrstar. They hare undergoing a rights offering and 20% owned Trafigura is taking half of the issue which will raise their share to 30%. They are also looking to take 400,000 tonnes oz zinc concentrate off the market which will hurt their bottom line:

(courtesy Zinc news)

On Monday, debt-laden Nyrstar (EBR:NYR)announced that Trafigura will purchase up to half of the shares it’s selling in a rights offering for 250 to 275 million euros. The news has raised red flags for those concerned that Trafigura is seeking to gain control of Nyrstar.

As the Financial Times explains, Trafigura, a multinational commodities trading company, amassed a 20-percent stake in Nyrstar last year and “pushed successfully to get two directors appointed to its board.” The rights offering could raise Trafigura’s interest in Nyrstar to 30 percent, and will likely attract further scrutiny from the European Commission, which is already looking at whether Trafigura “has taken de facto control of the zinc company.”

However, Bill Scotting, CEO of Nyrstar, has denied that is happening, commenting, “[t]his is not a takeover by stealth. Trafigura is a supportive shareholder.”

Market watchers too seem unconcerned about the growing relationship between Nyrstar and Trafigura, and have instead latched onto other aspects of Nyrstar’s Monday release. In particular, the following statement from the company has raised eyebrows:

Following a detailed review of the performance, near term cash needs, medium term capital requirements and exploration potential of the Mining segment, Nyrstar management is now pursuing strategic alternatives for its mining assets, individually and as a portfolio, which may include additional suspensions, asset disposals and a full exit from mining and has appointed financial advisors to assist with that process. Where appropriate, offtake agreements will be put in place to maintain Nyrstar’s access to concentrates.

Nyrstar will consider further suspensions of its mines if the current depressed commodity price environment continues; such suspensions would potentially reduce global supply by up to a further 400,000 tonnes of zinc concentrate (in addition to the 100,000 tonnes removed by the Myra Falls and Campo Morado suspensions).

Many have honed in on the fact that Nyrstar is considering “a full exit from mining,” while those in the zinc space are taking heart from the news that the company is looking at suspensions that could take 400,000 tonnes of zinc concentrate off the market.

end

And now Dave Kranzler talks about that other copper giant Glencore:

(courtesy Dave Kranzler/IRD)

Glencore Stock Is Down 16% In Three Days

Glencore stock popped up last week after it announced a $900 million dollar streaming deal with Silver Wheaton. It involves Glencore’s share of the silver that is produced from the Antimina mine in Peru. But Glencore leveraged up to buy Xstrata in 2012, when silver was $32/oz. The amount of debt that Glencore was able to access for this transaction without doubt assumed a $32/oz valuation on Glencore’s silver assets. It only took 3 days for reality to reassert control over Glencore’s stock:

The stock has plunged 16% since hitting 130 (British pounds) last Wednesday after the streaming deal was announced.

Glencore’s business is a general reflection of the entire global economy: A massive cesspool of too much debt supported by economic fundamentals which are quickly collapsing. Glencore’s stock has been repriced downward by 65% since May, when it hit 318 pounds.

This one is going to be a wild ride because the big banks with derivatives and debt exposure to Glencore will do their best to proliferate disinformation designed to cause upward spikes in the stock. But ultimately they can’t support of a collapsing economy and base metals commodities market.

Glencore derives 37% of operating income from copper. When the price of copper dives below $2, which appears to be inevitable, it will be a disaster for Glencore. Citibank and Blackrock are among Glencore’s largest shareholders.

appears to be inevitable, it will be a disaster for Glencore. Citibank and Blackrock are among Glencore’s largest shareholders.

At some point in time the Fed is going to lose control of its ability to keep the U.S. stock market propped up. That reality is inevitable but placing a bet on the timing of that reality is not easy. However when the event occurs which triggers a complete re-pricing of the U.S. stock market, I suspect that the graph of the S&P 500 will look quite similar to graph of Glencore above. The best advice I can give is that you should prepare accordingly, especially if you have the ability to get out of your retirement asset vehicles.

Bitcoin explained by Hugo…

(courtesy Hugo Salinas Price

Hugo Salinas Price: What is a bitcoin?

Submitted by cpowell on Tue, 2015-11-10 01:31. Section: Daily Dispatches

8:30p ET Monday, November 9, 2015

Dear Friend of GATA and Gold:

Bitcoins, Mexican Civic Association for Silver President Hugo Salinas Price writes today, are no more real than government-issued currency, both being little more than computer entries. Salinas Price’s commentary is headlined “What Is a Bitcoin?” and it’s posted at the association’s Internet site, Plata.com, here:

http://www.plata.com.mx/Mplata/articulos/articlesFilt.asp?fiidarticulo=2…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

James Turk is in my camp when he explains that gold from the FRBNY is feeding China et al

(courtesy James Turk/Kingworldnews)

Fed’s outflows likely being used to lock gold down, Turk tells KWN

Submitted by cpowell on Tue, 2015-11-10 01:35. Section: Daily Dispatches

8:35p ET Monday, November 9, 2015

Dear Friend of GATA and Gold:

Gold flows reported out of the Federal Reserve Bank of New York are likely the mechanism of the “choke hold” that governments lately have put on the gold price, GoldMoney founder and GATA consultant James Turk tells King World News today. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/gold-hemorrhaging-out-of-u-s-feds-vault-as-ecb-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Last reporting week for Shanghai demand: 47 tonnes.

(courtesy Koos Jansen)

COMEX Deliveries vs SGE Withdrawals

Withdrawals from the vaults of the Shanghai Gold Exchange, a number by which we can measure Chinese wholesale gold demand, accounted for 47 tonnes in week 42 (26 – 30 October 2015). Strangely, this is a weak number if we compare it to the rest of this year. Still, 47 tonnes of gold equals 47,000 one-kilogram bars, or 3,760 London Good Delivery bars – withdrawn from the vaults in just one week.

Year to date, an astonishing 2,165 tonnes of gold have been withdrawn from the vaults. The yearly record for withdrawals from the vaults of the Shanghai Gold Exchange (SGE) stands at 2,197 tonnes, set in 2013. Probably this record has already been surpassed by 6 November, though the numbers have yet to be released on 13 November. With 8 more weeks left on the calendar SGE withdrawals are set to reach 2,680 tonnes in 2015.

This year’s strong SGE withdrawals have likely been supplied by a higher share of recycled gold than in previous years, which doesn’t mean Chinese gold import was not robust in recent months. Cross-border trade statistics from around the world are slowly being released and all data signals elevated gold exports to China, matching strong SGE withdrawals. Total Chinese gold import 2015 is likely to transcend 1,350 tonnes of gold.

Last week we learned Australia has net exported 17 tonnes of gold to China in July, of which 13 tonnes were shipped directly to the mainland (an all time record) and 4 tonnes have been transported through Hong Kong.

Known Chinese non-monetary gold import (YTD) stands at 985 tonnes and Chinese domestic mining supply has reached 357 tonnes. Without counting scrap, apparent physical gold supply in China in the first three quarters of 2015 has been at least 1,342 tonnes.

Kindly note, in the chart above Chinese gold import from the UK is not included for September and Chinese gold import from Australia is not included for August en September.

China’s central bank, the PBOC, increased its official gold reserves by 14 tonnes in October, now totalling 1,722.5 tonnes. Vey likely the PBOC owns far more gold than 1,723 tonnes, but they don’t disclose this or they would disturb the US and renminbi inclusion into the SDR could be sabotaged.

China’s Foreign Exchange reserves increased for the first time in six months, from 3,514 billion US dollars to 3,525 billion US dollars.

COMEX Deliveries vs SGE Withdrawals

Across the pond at the COMEX gold futures exchange in New York there is a lot less physical gold going through the vaults. Year to date COMEX deliveries have reached a mere 40 tonnes. Though, in my opinion comparing COMEX deliveries to SGE Withdrawals is meaningless.

Frequently I receive inquires from gold investors around the world that like to verify their Chinese gold demand numbers. Some of the numbers they present are totally outrages, ranging from 20 to 60 tonnes of Chinese gold demand a day. Often, this is based on a misunderstanding regarding the term “delivery”. The same misunderstanding explains why we can’t compare COMEX deliveries to SGE withdrawals.

On any gold (futures) exchange in the world “deliveries” reflect the amount of physical gold that traders prefer to hold over a derivative contract, which requires the long contract holder (buyer) to to pay short contract holder (seller) the notional value of the futures contract in full in a addition to the margin (down payment). When physical gold is delivered through a futures exchange this is not automatically dropped off at the buyer’s doorstep. The amount of gold delivered is the amount of gold inside the vaults of the exchange that changes ownership from ashort to a long. The process of delivery inside the vaults of the exchange can be repeated indefinitely, ownership of gold can change from person X to Y, from owner Y to Z, from Z to X, etc. Delivery captures gold demand to a certain extent – traders at an exchange opting for physical gold instead of a derivative contract – but delivery cannot be compared to SGE withdrawals that capture wholesale gold demand for China.

(SGE) Withdrawals reflect the amount of gold that leaves the vaults of the exchange. Because of the unique structure of the Chinese gold market (nearly) all physical gold in China is traded through the SGE and therefor SGE withdrawals are an indicator for Chinese wholesale gold demand. Note, foreigners cannot buy, withdrawal and export gold from the SGE system. International investors have little incentive to purchase physical gold on the COMEX (or any other futures exchange) as delivery and withdrawing metal from the vaults in New York is a devious process compared to buying gold at a local bullion distributor. International investors looking to buy physical gold are more likely to buy spot gold contracts or directly call a refinery. In China delivery of gold futures contacts on the Shanghai Futures Exchange is practically nothing, as futures contracts are not a convenient way to buy physical gold.

COMEX withdrawals are neither an indicator for (US) gold demand because the structure of the US gold market is different form the market in China. Consequently, it makes no sense to compare COMEX withdrawals or deliveries, to SGE withdrawals.

Some gold blogs depict COMEX deliveries to resemble anything more than “change in ownership of gold in the vaults of the COMEX in New York”. Furthermore, some look at SGE deliveries as if this has anything to do with Chinese gold demand – while only SGE withdrawals are an indicator that can be used to measure gold demand.

At the SGE all Chinese citizens are able to buy spot gold through an SGE account that can be opened at a Chinese commercial bank. The spot gold contracts, officially called physical contracts in the SGE rulebook, which are offered by the SGE are Au99.5, Au99.95, Au99.99, Au100g and Au50g. These physical contracts are not derivatives so the buyers and sellers do not have the option to take or make delivery; change in ownership of in the metal is mandatory when the contracts are traded. Physical contracts can’t be traded on margin and when they are exchanged the physical gold always immediately changes hands.

The SGE also offers spot deferred contracts, which can be described as futures contracts without any predetermined delivery date. Every day traders of SGE spot deferred contracts have the option to take or make delivery. The spot deferred contracts offered by the SGE are Au(T+D), mAu(T+D), Au(T+N1) and Au(T+N2). On the English website of the SGE we can see the delivery volume of the spot deferred contracts in the daily reports – click here to view. Let’s have a look at an example, below is the daily report of 9 November 2015.

We can see the spot deferred contracts show delivery volume and the physical contracts not. The delivery volume reflects the amount of physical gold in the SGE vaults that has changed ownership between traders of spot deferred contracts; it has nothing to do with Chinese gold demand. Though, this delivery volume is erroneously used by some to measure Chinese gold demand.

Also important to mention is that this delivery volume on the SGE is counted bilaterally. So, if one contract is delivered (1 short hands over gold to 1 long) the volume will show “2” (1 short + 1 long). In contrast, COMEX delivery is countedunilaterally (“1″ contract delivered means 1 short hands over gold to 1 long). In the example above SGE delivery volume is 43.248 tonnes, this volume would be displayed on the COMEX website as 21.624 tonnes.

SGE withdrawals are only published in the Chinese weekly reports. Below we can see a screen shot of the most recent report.

The number framed in red is the amount of gold withdrawn from the vaults in the current week denominated in Kg’s counted unilaterally (46.5651 tonnes in between 26 – 30 October 2015). The number framed in blue is the amount of gold withdrawn from the vaults year to date (2,165.4422 tonnes) counted unilaterally.

The misunderstanding regarding COMEX deliveries versus SGE withdrawals is fuelled by some blogs that disclose SGE withdrawals labeled as SGE deliveries. Confusing readers to think deliveries are an indicator for demand. While, deliveries are not the same as withdrawals.

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

end

(courtesy Bill Holter/Palisade Radio)

My latest interview http://palisaderadio.com/bill-holter-gold-is-cheap-gold-stocks-are-cheaper/

Bill Holter: Gold Is Cheap. Gold Stocks Are Cheaper!

Physical gold is a necessary part of one’s portfolio, but investors should also look towards mining stocks. That is according to Bill Holter, who contends that ounces in the ground are so deeply discounted today, that buying mining shares is like getting gold for free!

Bill Holter writes and is partnered with Jim Sinclair at the newly formed Holter/Sinclair collaboration. Prior, he wrote for Miles Franklin from 2012-15. Bill worked as a retail stockbroker for 23 years, including 12 as a branch manager at A.G. Edwards. He left Wall Street in late 2006 to avoid potential liabilities related to management of paper assets. In retirement he and his family moved to Costa Rica where he lived until 2011 when he moved back to the United States. Bill was a well-known contributor to the Gold Anti-Trust Action Committee (GATA) commentaries from 2007-present.

Talking points for this week’s interview –

• Why buying mining shares gives you a deep discount on your gold?

• How to get your gold mining share certificates out of the system?

• Geopolitical events that may cause global economic shifts? Russia, Saudia Arabia, and more…

• And you don’t want to miss Bill’s view on BITCOIN!

end

1 Chinese yuan vs USA dollar/yuan rises slightly in value , this time at 6.3618 Shanghai bourse: in the red, hang sang:red

2 Nikkei closed up 28.32 or 0.15%

3. Europe stocks all in the red /USA dollar index up to 99.13/Euro down to 1.0733

3b Japan 10 year bond yield: falls to .319% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 123.46

3c Nikkei now just above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 43.96 and Brent: 47.13

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .673 per cent. German bunds in negative yields from 5 years out

Greece sees its 2 year rate rise to 7.99%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 7.68% (yield curve flat)

3k Gold at $1094.00 /silver $14.53 (8:00 am est)

3l USA vs Russian rouble; (Russian rouble up 1/4 in roubles/dollar) 64.37

3m oil into the 44 dollar handle for WTI and 47 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0041 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0778 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 5 year German bund now in negative territory with the 10 year rises to +.673%/German 5 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.33% early this morning. Thirty year rate above 3% at 3.09% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Fall For 5th Day On Disturbing Chinese Inflation Data; Renewed Rate Hike Fears; Copper At 6 Year Low

A day after China reported another month of disappointing trade data, overnight it confirmed that all that communist talk of “recovery”, and “for make benefit glorious concept of central planning” is hot air when overnight not only its CPI missed, rising just 1.3% and below the 1.5% expected, but PPI tumbled by -5.9%, which was the 44th (!) consecutive month of declines and at the current accelerating pace, China may have another 44 months of gate deflation before anything improves.

And with both trade weak, and inflation disappointing, it meant one thing: demand for industrial metals was slumping, leading to another day of tumbling prices overnight, led by nickel…

… and copper, both of which dropped to their lowest levels since before 2010.

It would appear all those Glencore copper production cuts didn’t do anything after all, just as predicted.

Stocks, however, were a different matter and more bad news out of China’s economy is just what the market wanted at least initially, and resulting in the following Bloomberg headline: China Deflation Threat Gives PBOC Room for More Monetary Easing. However, it appears the latest bad news wasn’t bad enough as the Composite failed to continue its 4-day winning streak, and closing down fractionally just 0.2% on the session, despite expectations of another imminent stimulus from someone.

Mockery of central planning aside, the ongoing failure of China to achieve any stabilization in its economy, after already cutting interest rates six times in the past year, and the prospect of a U.S. interest rate hike in December, had made markets increasingly jittery and worried which is not only why the S&P 500 Index had its biggest drop in a month, but thanks to the soaring dollar emerging market stocks are falling for a fourth day – led by China – bringing their decline in that period to almost 4 percent, and the global stock index down for a 5th consecutive day.

Elsewhere in Asia, Asian equity markets traded mostly lower following the lacklustre close on Wall St. which saw the worst intraday decline in a month, amid fears over a Fed December rate hike coupled with the OECD downgrading their global growth forecast. The Shanghai Comp. (-0.1%) fluctuated between gains and losses amid increased speculation of further easing after the latest Chinese CPI figure printed a 5-month low, signalling concerns of slowing demand in China. Hang Seng (-1.4%) was weighed on by weakness in casino names after Wells Fargo cut Macau’s November gaming gross revenue guidance. Nikkei 225 (+0.2%) has seen a relatively mixed session, tracking the fluctuations in Chinese stocks with modest support provided by the healthcare sector. 10yr JGBs traded higher amid risk-off sentiment which prompted inflows into Japanese paper.

Asia Wrap:

- MSCI Asia Pacific down 0.7% to 133

- Nikkei 225 up 0.1% to 19671

- Hang Seng down 1.4% to 22402

- Shanghai Composite down 0.2% to 3640

- S&P/ASX 200 down 0.4% to 5099

Key Asain News:

- Tencent Profit Rises to Record as Online Gaming Lures Users: 3Q net income 7.45b yuan vs est. 7.51b yuan

- Aussie Business Loan Bonanza as Bank Margins Slide May Stall RBA: Borrowing rates for corporates have dropped by at least 57 basis points since Jan.

- Short Sellers’ No. 1 Target Is Surging in Hong Kong as CEO Buys: Shrs of China Huishan Dairy have soared 90% since early Jul., despite highest level of short interest in HK and analyst price targets implying 46% tumble over next 12- mos.

- Morgan Stanley Sees BOJ Shift in Easing Methods as Bonds Run Out: BoJ will be forced to change its stimulus strategy as soon as next autumn as it runs out of gov’t debt to buy from market, Robert Feldman said

In Europe, equities (Euro Stoxx -0.36%) have continued the trend set in the US and Asia and reside in negative territory , led higher initially by stock specific gains, but subsequently led lower by the materials and energy sectors. The aforementioned sectors have underperformed as a result of disappointing data out of China, as highlighted by the latest CPI and PPI data overnight . The FTSE 100 (-0.35%%) underperforms in Europe, weighed upon by mining names, after Barclays downgraded both BHP Biliton (-1.4%) and the sector as a whole. Telecoms is the outperforming sector after Vodafone (+4.2%) reported positive earnings including organic service growth of 1.2% for the quarter, beating expectations. Utilities is the second best performing sector, coming off the back of National Grid’s (+1.8%) announcement that it has begun the process for its stake sale in the UK’s gas grid. The pharma heavy CAC 40 (-0.37%) outperforms its major counterparts in Europe, as a flight to quality ensues.

Fixed income has trended higher, with Bunds supported by the growing consensus suggested by source comments yesterday that some members of the ECB are pushing for a larger than 10bps depo cut as they think that 10bps is already priced in.

European Wrap:

- Stoxx 600 down 0.4% to 374

- FTSE 100 down 0.4% to 6272

- DAX down 0.5% to 10766

- German 10Yr yield down 3bps to 0.63%

- Italian 10Yr yield down 5bps to 1.7%

- Spanish 10Yr yield down 6bps to 1.9%

- S&P GSCI Index up 0.3% to 351.9

European Top News:

- ABN Amro Seeks Up to $4.6 Billion in IPO as State Cuts Stake: Dutch govt is selling a 23% stake in ABN at EU16- EU20/shr, valuing the co. at >EU18.8b at the high end of the range

- Portuguese Premier Set to Be Ousted as Socialists Eye Power: Loose alliance of Portuguese opposition parties poised to vote PM Coelho’s govt out of power on Tuesday

- Asda Calls Time on Black Friday as U.K. Turns Back on U.S. Rite: Instead of having customers line up all night for a limited number of heavily discounted items, Asda plans to cut prices by GBP26m across the season

FX markets have remained quiet amid no tier one data releases from Europe . Price action continues to be subdued in the wake of NFP report last Friday, with the USD remaining firm as FFR futures are now pricing in a 70% probability of a fed rate hike at the December meeting. As such, USD/JPY continues to trade above the 123.00 handle. EUR/USD now trades in negative territory however, with hawkish comments by ECB’s Weidmann failing to bolster EUR.

The commodity complex remains quiet for the session with WTI and Brent trading flat, with precious metals continuing to be maintained in range by the firmer USD and industrial metals being weighed upon by the aforementioned weak Chinese inflation data overnight.

Looking ahead data is light on the US calendar, with Import Prices and Wholesale Inventories at 8:30 and 10:00 am respecitvely, and a 10Y auction at 1pm; we are expecting comments from ECB’s Coeure, BoE’s Cunliffe and Fed’s Evan’s.

Top News:

- China Deflation Threat Gives PBOC Room for More Monetary Easing: Consumer price index rose 1.3% in Oct. from yr earlier, missing the 1.5% median est.

- ECB Faces Three Suits Over Quantitative Easing in German Court: EU1.1 trillion asset-purchase program the target of lawsuits pending in Germany’s top constitutional court that challenge the country’s role in the policy

- Obama Immigration Plan Stymied as States Win Again on Appeal: Court refuses to let program begin while 26 states fight to derail it

- Battle for Asciano Intensifies as Qube Makes Counteroffer: Qube and its North American backers made a A$9b counteroffer for Asciano, rivaling bid from Brookfield Asset Management

- Synchrony Financial Will Be Added to S&P 500, Replacing Genworth: Genworth will take Rovi’s place in S&P MidCap 400

- Goldman Sachs Sees 60% Chance U.S. Expansion Lives to See Ten: U.S. economic upswing now the 5th longest since 1900

- Loomis Avoids Treasuries on View Fed to Lift Rates Twice by June: Loomis Sayles portfolio manager Matt Eagan predicts Fed will raise interest rates in Dec. and again in June

- Gundlach Says December Rate Increase a Threat to Stocks, Bonds: Would potentially drive up the value of the dollar to the point where it weakens the economy, Jeffrey Gundlach, CEO of DoubleLine Capital, said late yday on call with investors

- Vodafone Service Revenue Beats Estimates on Europe Recovery: 2Q organic service rev. growth 1.2% vs est. 0.8%, boosts lower end of FY2015/2016 Ebitda range

- VW Starts Talks to Win Worker Backing for Post-Scandal Cutbacks: Two sides sought to present a unified front after a daylong board meeting on Monday, saying they’re starting 10 days of talks

Bulletin Headline Summary from Bloomberg adn RanSquawk

- Treasuries gain for first time in over a week after weaker than expected Chinese inflation data sparked global stock selloff; quarterly refunding continues with $24b 10Y, WI 2.305%, highest since June, vs. 2.066% in Oct.

- China’s CPI rose 1.3% in October from a year earlier, below 1.5% median forecast in Bloomberg survey; producer prices fell 5.9%, its 44th straight monthly decline

- China’s giant banks got a nine-year breather to issue the securities they need to meet standards for loss absorbency laid down by the FSB, an acknowledgment of the challenge this implies for the largely deposit-funded lenders.

- The EC has proposed that the EU’s overhaul of financial markets regulation — MiFID II — be delayed by a year, according to the European Parliament’s lead rapporteur on the dossier, Markus Ferber

- German politicians who failed in previous attempts to have courts derail EU monetary policy filed lawsuits at the country’s top court challenging the ECB’s EU1.1t asset- purchase program

- Obama’s plan to shield more than 5m undocumented immigrants from deportation before he leaves office was dealt another blow by an appeals court’s refusal to let the program begin while 26 states fight to derail it

- A London judge ruled former Deutsche Bank AG trader Christian Bittar was improperly identified in a regulatory sanction notice against the bank over Libor in a significant setback for the Financial Conduct Authority

- In a speech today, U.K.’s David Cameron outlined for key demands for reforms as he seems to keep Britain in the EU; U.K. Independence Party leader Nigel Farage said speech shows there is no major renegotiation and there should be no delay in holding a referendum on membership

- Chinese police slapped a two-year freeze on more than $670m of shares owned by the mother of Xu Xiang, the Shanghai hedge fund boss under investigation for alleged insider trading and stock manipulation

- $16.95b IG priced yesterday, $1.08b HY. BofAML Corporate Master Index OAS holds at +161, YTD range 180/129. High Yield Master II OAS widens 4bp to +594, YTD range 683/438

- Sovereign 10Y bond yields lower. Asian, European stocks fall, U.S. equity-index futures decline. Crude oil gains, gold little changed. copper falls

DB’s Jim Reid completes the overnight wrap

It’s straight to China this morning where soft inflation data is dominating the headlines. CPI in the month of October was -0.3% mom, the first monthly decline in prices since May. That’s seen the YoY rate fall to +1.3% (vs. +1.5% expected) following a +1.6% reading in September with food prices in particular appearing to be a large contributor to the decline having fallen to 1.9% yoy from 2.7% yoy in the month prior. Prices at the factory gate continue to remain under pressure meanwhile with PPI of -5.9% as expected and unchanged from last month, marking the 44th straight monthly decline.

Chinese equity markets had initially fallen as much as 1% immediately following the data, only to then rebound and trade as much as +0.5%, but have since declined again following the midday break with the Shanghai Comp and CSI 300 both down -0.41%. The Nikkei is +0.08% while the Hang Seng -1.27%, Kospi -1.50% and ASX -0.40% have fallen and base metals have all sold off following the data. US equity markets are a touch firmer while Oil markets are half a percent stronger after the International Energy Agency forecasted that supply outside of OPEC is set to stop growth by 2020.

Friday’s strong US employment report and subsequent Fed rate hike re-pricing dominated much of the tone in markets again yesterday as risk assets starting the week on the back foot with the S&P 500 retreating -0.98%, Dow closing -1.00% and European equity markets down a bit more. The OECD added to the softer tone, joining the IMF in cutting its growth forecast for this year (2.9% from 3.0% previously) and next year (3.3% from 3.6% previously). Meanwhile, Oil markets slid through the afternoon session with WTI eventually closing the session -0.95%, its sixth consecutive down day. Treasury yields nudged a bit higher, the 10y eventually closing up +1.8bps at 2.344%. Credit markets weakened with CDX IG a couple of basis points wider but again the primary market shrugged off any concern as 11 issuers were out with new deals in the US, with nearly $17bn of bonds getting priced. Estimates for supply this week are running at around $25-$30bn.

Yesterday’s Fedspeak didn’t offer a whole lot of new information. Chicago Fed President Evans said that he is not predisposed against liftoff in December while the Boston Fed President Rosengren said that all future meetings, including December’s, could be an ‘appropriate time for raising rates’ should the economy continue to improve as expected. Like his Fed colleagues, Rosengren also highlighted that he prefers a path that involves only a gradual increase in interest rates.

So given the renewed focus on the higher probability of a Fed rate hike we thought it was worth re-highlighting this year’s Long-Term Study (Scaling the Peaks – 07/09/2015 –http://pull.db-gmresearch.com/p/6523-08FD/52242465/LT_Study.pdf) where we looked at the impact of Fed hikes on various financial and economic indicators using 12 hiking cycles since 1950. The results are on pages 10-14 of the document with data from the first hike in the cycle on page 11. Generally the results emphasize the traditional lag of monetary policy on financial and economic variables.

If we look at the first hike in the cycle, real GDP growth has tended to steadily climb into the move and then actually accelerate in the half-year afterwards. From 6 months to three years after, the pace of growth incrementally slows as the long lag of monetary policy and subsequent rate hikes bite. For equities performance in the 6 months before the first hike and 6 months after are fairly similar. It does seem though that there is a trend for equity returns to stall 12-24 months after the first hike which again perhaps reflects the lag in monetary policy. For credit spreads, we see tightening for around 12 months after the first hike. However after this for the next two years this tightening is fully and progressively reversed hinting again at the lag.

While we think there are good reasons to think this cycle is different to the last twelve it’s a useful reminder that we may not know the consequences of any imminent Fed move until maybe 2017. We have a bias to believe that a rate hike now would be a policy error mainly because global growth and inflation are so low that you risk activity tipping over into a recession in say 2017. Clearly a lot can happen between now and then but that’s our current thinking.

Moving on, the Euro was under some pressure yesterday following a report released by Reuters suggesting that the ECB was considering more aggressive easing (relative to market expectations) in December. The article, quoting four governing council members, suggested that a consensus is forming at the ECB to move the deposit rate further into negative territory at the December meeting, although the article noting that the move might be even greater than the 10bp cut currently expected by markets according to the policymakers. Interestingly the article quoted one Governing Council member as going so far as to say that ‘there is no bottom to the deposit rate in the near term’ and that ‘it could be lowered quite sharply still’. The Euro was off as much as -0.6% from the day’s highs but closed pretty much unchanged. 10y Bund yields ended down just over 3bps in at 0.660%. The same couldn’t be said for yields in the periphery however as political headlines dominated markets there.

Portuguese government bond yields moved quite sharply wider yesterday (10yr +16bps) as the main opposition Socialist party reached an agreement with radical-left parties over the weekend. This makes it almost certain that the minority centre-right government will be defeated – a no confidence vote is expected on Tuesday – and increases the likelihood of a leftist government outcome. Although the Socialists’ revised economic programme remains moderate, our economists expect stasis on the structural front with risks tilted towards greater fiscal slippage.

Spanish government bond yields also increased (by a lesser +4bps in 10yrs) as the Catalan pro-independence parties approved in the Catalan Parliament a resolution to begin working on a separate social security system and treasury with the aim to secure independence as early as 2017. This is not a surprise. The pro-independence parties come from a very heterogeneous political spectrum. Hence, they have only the pro-independence battle to unite them. The likely next step is for the Constitutional Court to annul the Catalan resolution although this is unlikely to stop the pro-independence parties. But political risk in Spain is not uniformly increasing, opinion polls ahead of the general election on 20 December in Spain are painting a slightly less fragmented picture, with a slightly higher probability of a pro-business government coalition.

Wrapping up yesterday and specifically the economic data that we got, Germany’s trade balance reading for September revealed a slightly better than expected trade surplus (€22.9bn vs. €20.0bn expected) after exports rose +2.6% mom (vs. +2.0% expected) during the month. French business sentiment for October was up a point last month to 99, while Euro area investor confidence rose +3.4pts to 15.1 (vs. 13.1 expected) for November. In a quiet day for data, the only release of note in the US was the October labour market conditions index which rose 0.3pts to a slightly below-market 1.6 (vs. 1.9 expected).

In terms of the day ahead now, this morning in Europe see’s more industrial production prints out of France and Italy, along with the monthly manufacturing production read in the former. The calendar picks up a bit in the US this afternoon starting with the October NFIB small business optimism index reading, followed by last month’s import price index and then the September wholesale inventories and trade sales data later this afternoon. Meanwhile it’s a busy day for Central Bank speak. The ECB’s Coeure, Weidmann and Nouy are all scheduled to speak at various points, while over at the Fed we’re due to hear from Evans (at 10.15pm GMT) after the US close.

end

Chinese Stocks Longest Win Streak Since Bubble Peak After CPI, Commodities Tumble; Philippines Exports Crash

A busy night in Asia began with a total collapse in Philippines Exports (-24.7% YoY – the biggest miss since Lehman). This was quickly followed by a 0.3% drop (deflation) in CPI MoM (thanks to a drop in pork -1.9%, eggs -6.9%, and veggies -5.6%) which sparked buying in stocks (because moar stimulus). Chatter of a few large fund houses under investigation stymied the rally quickly but as nobody was summoned stocks recovered, then rallied strongly back into the green on renewed chatter of Stock Connect occurring sooner than expected. With CSI-300 (China’s S&P 500), up at the break, this is the longest winning streak since the peak of the bubble in May. And finally Shanghai Copper and Nickel tumbled to new multi-year lows, dragging Bloomberg’s Commodity Index to fresh 16-year lows.

Philippines Exports crash, miss by most since Lehman..

Then China inflation data hit… CPI missed +1.3% YoY, the lowest since January (with a 0.3% drop MoM – the most since March) ; PPI tumbled 5.9% – its 44th monthly decline in a row...

A choppy morning in China leaves Shanghai Composite higher at the break…

Leaving CSI-300 set for the longest win streak since the peak of the bubble…

Shanghai Copper hit a new 6-year low (and nickel tumbled)…

Leaving Bloomberg’s Commodity Index at fresh 16 year lows…

Charts: Bloomberg

h/t @SimonTing

China Sends Fighter Jets To Island, Demands No Mention Of “Contentious Issues” At Summit

When Washington sent the USS Lassen to Subi Reef last month, it represented the most meaningful escalation yet in what has become an incredibly tense standoff in The South China Sea.

America’s friends in the region – most notably, The Philippines – seem convinced that Beijing has designs on using its newly constructed islands in the Spratlys as forward operating bases for future military operations. China of course denies this, but has nevertheless built 10,000 foot airstrips capable of landing fighter jets and surveillance aircraft, cement factories, and ports atop the reefs, and when a US Poseidon spy plane went to have a look back in May, the PLA told it to “Go now!”

There are conflicting accounts of just how “forceful” a message the US actually sent by sending a guided missile destroyer to Subi (some say the exercise wasn’t “convincing” enough), but it did serve to antagonize Beijing and indeed, Admiral Wu Shengli told US chief of naval operations Admiral John Richardson that this needs to stop now unless the US wants to go to war.

But by all accounts, the patrols aren’t going to cease because Washington needs to save face and reassure its allies in the South Pacific and so, the stage is set for an “accident.”

Now, reports indicate that China has sent J-11BH/BHS fighter jets to Woody Island, south of Hainan in what one could be forgiven for believing is an attempt to discourage US military flyovers. Here’s The Diplomat:

The People’s Liberation Army Air Force (PLAAF) has dispatched an unknown number of fourth-generation J-11BH/BHS fighter aircraft to Woody Island (known as Yongxing Island in Chinese), the largest of the Paracel Islands administered by the People’s Republic of China in the South China Sea, according to Chinese media reports.

Woody Island, located around 200 miles (321 kilometers) south of Hainan Island, boasts the only operational airstrip in the South China Sea, although China is in the process of construction of at least two more airstrips in the Spratly Islands.

The J-11BH/BHS fighter aircraft are most likely part of the People’s Liberation Army Navy’s 8th Aviation Division stationed in Hainan Province. As my colleague, Ankit Panda, reported at the beginning of the month, J-11BH/BHS fighter jets armed with missiles have recently carried out exercises in the South China Sea rehearsing “real air battle tactics,” according to the PLA Daily.

Yes, “real air battle tactics”, which certainly leads you to wonder if they aren’t preparing to establish a no-fly zone above the islands in the Spratlys. After all, moving the jets to Woody gets them closer to Beijing’s new islands:

Here’s more from Defense News:

The new location could prove troublesome for US surveillance aircraft, such as the EP-3 Aries and the P-8 Poseidon, that fly through the area on a regular basis. In 2001, a collision between a Chinese fighter and EP-3 resulted in the death of a Chinese fighter pilot and the forced landing of the EP-3 on Hainan Island. In 2014, a Chinese fighter harassed a P-8 in the vicinity of Woody Island, which followed with a strong verbal protest by the Pentagon.

Bonnie Glaser, director of the China Power Project, Center for Strategic and International Studies, said the Chinese are demonstrating to the US, other claimants to the South China Sea and their domestic audience that they intend to protect their sovereignty.

As noted above, we’ve already seen what happens when a P-8 Poseidon gets near China’s sandcastles:

Fortunately for the US, these particular fighters apparently have trouble with “salty sea air.” Back to Defense News:

Taiwan-based Alexander Huang, chairman, Council on Strategic and Wargaming Studies, said that it might be too early to focus on military implications. Citing the problems Taiwan’s Air Force faces with the operational and seasonal deployment of fighter aircraft at Magong Air Force Base, Penghu Island, Huang said weather and the salty sea air makes deployment on off-shore islands difficult for advanced fighter aircraft.

“If they intend to place J-11 on Woody Island around the year, it would be an ‘all-weather’ test to the airframe, parts and combat systems onboard before I do military implication analysis.”

Glaser agrees. “My understanding is that fighters are likely only to be deployed for short time frames in the Spratlys – the salty sea air would cause havoc to the aircraft over long periods.”

Maybe, but that’s really not the point. The issue is whether Beijing is ramping up its capability to “cause havoc” to the US and its regional allies should they continue to antagonize the PLA in the Spratlys.

Stay tuned…

And meanwhile (via ABC):

China’s top diplomat asked the Philippines Tuesday not to raise contentious issues — an obvious reference to the Asian neighbors’ territorial spats — in an annual economic summit of Asia-Pacific leaders in Manila next week, a Filipino official said.

Chinese Foreign Minister Wang Yi’s request, relayed to his Philippine counterpart Albert del Rosario during talks in Manila, underscored Beijing’s objection to any effort to bring the long-raging disputes to an international arena, where rivals like Washington could use it to criticize Beijing.

Non-inclusion of the thorny topic would also shield Chinese President Xi Jinping, who is expected to attend the Nov. 18-19 Asia-Pacific Economic Cooperation forum in Manila, from a potentially embarrassing confrontation.

EURUSD Crashes To 1.06 Handle – 7-Month Lows

It appears the stop sbelow yesterday’s lows (following The ECB’s jawboning of “big cuts” in rates) have been run, sparking a 40 pip waterfall to a 1.06 handle in EURUSD (and there are more ECB speakers to come). These are 7-month lows in EURUSD and are pressing The USD Index to break April’s highs.

Charts: Bloomberg

Portuguese Government Falls As Socialists, Communists Topple PM

Well it wasn’t hard to see this coming.

As detailed here on Tuesday, Antonio Costa and the Socialists have fulfilled their promise of ousting Portuguese PM Pedro Passos Coelho’s government just days after President Anibal Cavaco Silva reappointed the premier on the heels of largely inconclusive elections.

- PORTUGUESE PARLIAMENT REJECTS PM COELHO’S GOVERNMENT PROGRAM

- PORTUGAL GOVERNMENT FALLS AFTER LAWMAKERS BLOCK COELHO PLAN

For those who missed it, the Socialists moved to form a government with the Left Bloc and the Communists and when Silva decided to give them the political equivalent of a swift slap in the face by reappointing Coelho, the stage was set for a veritable mutiny.

Today’s events validate Communist leader Jerónimo de Sousa’s contention that Silva’s decision would amount to a “manifest waste of time.”

Here’s AP:

Anti-austerity lawmakers have forced Portugal’s new center-right government to resign by rejecting its policy proposals.

The showdown comes less than two weeks after the center-right government was sworn in.

The moderate Socialist Party forged an unprecedented alliance with the Communist Party and the radical Left Bloc to get a majority in the 230-seat Parliament and vote down the proposals Tuesday.

After four years in power the government lost its parliamentary majority in an Oct. 4 general election, which saw a public backlash against austerity measures adopted following a 78 billion-euro ($84 billion) bailout in 2011.

Socialist leader Antonio Costa is expected to become prime minister in coming weeks, supported by the Communists and Left Bloc. The have promised to alleviate austerity, though critics fear a return to borrow-and-spend policies.

So get ready Brussels and Berlin, because you might be in for another anti-austerity battle only this time, the country in question “matters.”

But then again, the “smartest” guy on the Street doesn’t think there’s anything to worry about…

We close with the following, from AFP:

Finance Minister Maria Luis Albuquerque, from the centre-right coalition which won the most votes in last month’s polls but lost the absolute majority it had enjoyed since 2011, warned that the rival bloc would derail Portugal’s economic recovery.

“If investor confidence is shattered, the threat of bankruptcy is real,” she told parliament.

Son Of Billionaire Steel Magnate Plunges To His Death Amid Demise Of UK Industry

Angad Paul, chief executive of Caparo Holdings, had done a lot of things in his 45 years.

He created the world’s fastest road-legal car, for instance. The Caparo T1.

He also executive produced the classic “Lock, Stock, and Two Smoking Barrels“:

Aside from supercars and gangster movies, Paul was, to quote FT, one of the Midlands’ leading industrialists as the head of Caparo Holdings. He was the son of Lord Paul, the 84 year old billionaire steel magnate who’s one the UK’s wealthiest people. Paul replaced his father as CEO nearly two decades ago. He was married to lawyer Michelle Bonn, 40, in 2005, and lived at his family’s home in Marylebone with his parents, Lord and Lady Paul

We’re using the past tense here because on Sunday, Paul tragically fell from “high up” at his home in London. He was pronounced dead at the scene. Here’s the statement from a Met spokesperson:

“London ambulance service and London’s air ambulance both attended and the man, believed to be in his mid-40s, was pronounced dead at the scene.

“London fire brigade have also been called to the scene to assist with the recovery of the body. The man’s next of kin has been informed, although we still await formal identification. Enquiries into the circumstances of the incident continue but it is being treated as non-suspicious at this stage.”

The timing of the “accident” raises questions. Caparo was placed in administration last month in what was characterized as a “shattering, devasting hammer blow” to the UK’s steel industry. For those who might have missed it, The Telegraph reported the following in mid-October:

“The crisis in Britain’s steel industry could be about to claim another victim, with parts of Labour peer Lord Paul’s Caparo empire under enormous pressure.

Caparo Industries, a major producer of steel products with 1,800 staff across 20 sites, was understood to be looking at all funding options over the weekend.

Lord Paul – one of the country’s 50 wealthiest people, with a fortune estimated at £2bn – has a large stake in the privately-owned business through its parent company, Caparo Group.

And then, two days later, there was this (again from The Telegraph):

Britain’s beleaguered steel industry has been dealt a “shattering” and “devastating hammer” blow after Caparo Industries went into administration, with doubts over the future of its 1,700 staff.

The global business, which has about 20 sites in the Midlands as well as operations sites in India and the US, filed for administration as pressure on the steel industry intensifies.

The problems at Caparo, first revealed on Monday by The Telegraph, came ahead of an announcement expected on Tuesday from Tata that it will slash up to 1,200 jobs at its steel plants in Scunthorpe and Scotland. It follows the closure of SSI in Redcar with the loss of 2,000 jobs.

Britain’s largest union, Unite, warned of a “domino effect” in the steel industry, as it renewed calls for the Government to step in to support the sector following Caparo Industries’ collapse.

“This is yet another hammer blow for steel and manufacturing communities already reeling from the closure of Redcar and job losses at Tata,” said Tony Burke, the union’s general secretary. “Ministers need to ask themselves how many more steel firms need to go to the wall before they step in. Failure to act could lead to a ‘domino effect’ taking hold across the industry.”

Finally, more color from FT:

Caparo, which comprises about 20 companies, was placed in administration last month, leading to the loss of 323 jobs and the closure of Black Country plants at Darlaston, Dudley and West Bromwich.

Its activities range from the forging and pressing of metal products for aerospace, automotive and other industries. It also produces fastenings, wire, tubes and other accessories.

The UK company is part of a global network of businesses under the Caparo name, with operations in China, India and the US.

In addition to steel, Caparo’s global business is also involved in product development, materials testing services, hotels, media, furniture and interior design, financial services, energy and private equity investment.

PwC, the administrators, said at the time of their appointment that 1,700 West Midlands jobs were at risk.

It isn’t difficult to guess how this came about. Excess capacity in China (a topic we’ve covered exhaustively) and the now ubiquitous exported deflation effectivelykilled the industry:

Business Secretary Sajid Javid has called for an EU-wide emergency summit on steel. This is due to be held with the next fortnight. At the event he is expected to campaign for European consent to the UK’s early introduction of the energy compensation package and for co-ordinated EU action to stop China dumping excess steel on international markets.

From BNP, earlier this year:

As a reminder, ArcelorMittal just reported a massive loss attributable to the same dynamic. As we noted on Friday, the obvious implication of China’s excess capacity problem is that the country will simply export its deflation...

Given that, it shouldn’t come as any surprise that the world’s biggest steelmaker suspended its dividend and cut its outlook.

Here’s more from Bloomberg:

The world’s biggest steelmaker on Friday cut its full-year profit target and suspended its dividend, putting the blame on the flood of cheap steel from China’s loss-making mills. The market is being overwhelmed with material coming from the nation’s state-owned and state-supported producers, a collection of industry associations said Thursday.