Gold: $1080.90 down $3.90 (comex closing time)

Silver $14.22 down 4 cents

In the access market 5:15 pm

Gold $1084.50

Silver: $14.30

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very poor delivery day, registering 0 notice for nil ounces. Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 209.72 tonnes for a loss of 93 tonnes over that period.

In silver, the open interest surprisingly rose by a considerable 3,553 contracts despite silver being down by 6 cents in yesterday’s trading. The total silver OI now rests at 165,988 contracts In ounces, the OI is still represented by .829 billion oz or 119% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI fell by a huge 8442 contracts to 427,984 contracts as gold was down by $0.30 yesterday. It seems the modus operandi of the bandits is to liquefy gold/silver OI as be approach first day notice on Monday, November 30. They succeeded in gold but not silver. We had 0 notices filed for nil today.

We had a huge withdrawal in gold inventory at the GLD to the tune of 1.49 tonnes / thus the inventory rests tonight at 661.94 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver, we had a huge addition in silver inventory to the tune of 1.43 milllion oz / Inventory rests at 315.111 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver rise by a considerable 3,553 contracts up to 165,988 despite the fact that silver was down by 6 cents with respect to yesterday’s trading. The total OI for gold fell by a considerable 8442 contracts to 427,984 contracts with gold down only 30 cents yesterday.

The bankers are succeeding in lowering the OI as the upcoming big December delivery month approaches. They did not have any luck in silver. First day notice is Monday, Nov 30.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

ii) China reports today on very weak lending as their debt levels and non performing loans are just too high for the Chinese to take on more debt. This should signal for QE for China:

i) A 24 hour national strike was called for today. Massive street protests brought the Greek economy to a fresh halt.

iii) The situation inside Catalonia is getting quite interesting. The government is threatening to arrest Mas and also Catalonia’s parliament refuse to elect Mas.

ii Here is one media that does not believe its nation’s report on “a stellar jobs report”(courtesy zero hedge)

(courtesy the Saker)

iii) Crude breaks into the 41 dollar column on again huge inventory gains especially in Cushing OK.

9 USA stories/Trading of equities:

i) James Bullard: we may stay at zero interest rates for quite some time

(James Bullard/zero hedge)

ii) USA comfort data just released:

two significant findings:

a) Blacks are further from comfort

b) the 25 -34 age group in the uSA also are further from comfort

remember that the consumer is 70% of GDP

iii) Janet Yellen’s favourite report the JOLTS report shows job openings rising off but hirings leveling off.

Why? find out in today’s important commentary

(zero hedge)

10. Physical stories

i) Attacks on gold are becoming for intense every day. Something is smoking behind the scenes

(John Embry/Kingworldnews)

ii) a) The big news of the day: the generally sanguine World Gold Council announces huge gold coin sales and it is at its highest levels since 2008:

very important for you to read..

(courtesy World Gold Council/zero hedge)

ii b) Reuters Jan Harvey reports on the same data from the WGC

(Jan Harvey/Reuters)

iii) N.Y Sun reports on the debate that Cruz wants to do two important things;

i) audit the Fed

ii) bring back the gold standard

a very welcome change to the debate

(New York Sun/GATA

iv) Sentiment on gold is commented upon by GATA members and others..

(Chris Powell/GATA)

v) a) Copper at 6 year lows. Glencore falls below 100 pence putting tremendous pressure on this huge derivative player

(zero hedge)

b) With copper prices retreating, Glencore and all of its derivative trading may bring down Germany, Deutsche bank and maybe set off a huge financial collapse everywhere

(Dave Kranzler/IRD)

vi Demand for silver far outstripping supply

a must read commentary tonight from Steve St Angelo

(SRSRocco report)

vii) Bill Holter’s important piece entitled: “Popular delusions …even if “popular” are still delusional.”

viii) Lawrence Williams of Lawrieongold/Sharp Pixley believes that the smuggled gold may amount up to 25% of their supply:

(Lawrie on gold)

ix) record gold exports from England to China.

(Koos Jansen)

Let us head over to the comex:

The total gold comex open interest fell from 436,426 down to 427,984 for a loss of 8,442 contracts as gold was down $0.30 with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. It looks like the latter has stopped. The November contract remained constant at 214 contracts. We had 0 notices filed yesterday, so we neither gained nor lost any gold that will stand for delivery in this non active delivery month of November. The big December contract saw it’s OI fall by a gigantic 23,009 contracts from 226,262 down to 203,253. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 192,973 which is good. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was very good at 243,050 contracts.

November contract month:

INITIAL standings for November

Nov 12/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 160.76 oz

manfra |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 32,150.000 oz

1000 kilobars Scotia |

| No of oz served (contracts) today | 0 contracts |

| No of oz to be served (notices) | 214 contracts

(21,400 oz) |

| Total monthly oz gold served (contracts) so far this month | 7 contracts

700 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 89,520.1 oz |

Total customer deposits 32,150.00 oz

we had 1 adjustments:

November initial standings/First day notice

Nov 12/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 325,802.190 oz

Brinks |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 10,834.03 oz

Delaware |

| No of oz served (contracts) | 0 contracts (nil oz) |

| No of oz to be served (notices) | 15 contracts

75,000 oz) |

| Total monthly oz silver served (contracts) | 5 contracts (25,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,996,842.3 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

total customer deposits: 10,834.03 oz

total withdrawals from customer account: 325,802.190 oz

And now SLV

nov 12/surprisingly we had a huge addition of 1.43 million oz of silver into the SLV/Inventory rests at 315.111 million oz/(my bet: it is paper silver not real silver entering the vaults)

Nov 11/no change in silver inventory at the SLV/rests tonight at 313.681 million oz/

Nov 10/no change in silver inventory at the SLV/rests tonight at 313.681 million oz/

Nov 9/no change in silver inventory/rests tonight at 313.681

Nov 6/ we had a very tiny withdrawal of 136,000 oz (probably to pay for fees)/Inventory rests tonight at 313.681 oz

Nov 5/strange no change in silver inventory/rests tonight at 313.817 million oz/

Nov 4/2015: no change in silver inventory/rests tonight at 313.817 million oz/

Nov 3.2015; no change in silver inventory/rests tonight at 313.817 million oz/

Nov 2/a withdrawal of 716,000 oz from the SLV/Inventory rests tonight at 313.817 million oz

Oct 30.no change in silver inventory at the SLV/Inventory rests at 314.532 million oz

Oct 29/a big withdrawal of 1.001 million oz from the SLV/Inventory rests at 314.532 million oz

Gold Bullion Demand Surges 27% In Q3 – New Chinese “Buying Spree”

Gold Demand Trends Q3 2015 was released by the World Gold Council today. The quarterly publication is the leading industry resource for data and opinion on global gold demand and examines demand trends by sector as well as geography.

The key findings from the report are as follows:

[Graphic source: World Gold Council]

–Overall demand increased by 8% year-on-year to 1,121t as selling of futures contracts and ETFs contributed to a price dip, 6% in July, which buoyed gold demand around the world.

–Total consumer demand – made up of jewellery demand – totalled 928t, up 14%.

–Global investment demand saw a significant rise of 27% to 230t, up from 181t in Q3 2014.

This was led by the US which saw a surge in bar and coin demand – ittripled and was up 207% to 33t from 11t on the same period last year, with massive demand from China, up 70% to 52t and Europe up 35% to 61t.

China’s sharp devaluation of the yuan this summer sparked another gold bar and coin “buying spree” in China according to the World Gold Council, as canny store of wealth buyers sought to shelter themselves from further market volatility and sharp falls in stock markets.

Much of this European demand came from Germany and Austria where demand remains very high due to heightened German concerns about the euro, the European and global economy.

–Global jewellery demand for Q3 2015 was up 6% year-on-year to 632t compared to 594t in Q3 2014. In India, demand was up 15% to 211t and China was up 4% to 188t. The US and the Middle East also saw gains, up 2% to 26t and 8% to 56t respectively.

–Central bank demand reached 175t, the 19th consecutive quarter of net purchases. Russia continued to “lead the pack” in terms of central bank purchases.

– Demand in the technology sector declined 4% to 84t as the sector continued to endure pressure, with the industry choosing to shift towards alternative, cheaper materials in technological applications.

– Total supply was 1,100t in Q3, up 1% year-on-year. Total mine supply (mine production + net producer hedging) remained relatively flat up 3% year-on-year to 848t compared to 814t in the same period last year. Year-on-year quarterly mine production shrank by 1% to 828t in Q3 2015 against 836t in Q3 2014. Recycling

Must-read guide to international bullion storage:

Download Essential Guide to Gold Storage in Singapore

Download Essential Guide To Storing Gold In Switzerland

DAILY PRICES

Today’s Gold Prices: USD 1087.60, EUR 1014.03 and GBP 716.21 per ounce.

Yesterday’s Gold Prices: USD 1088.60, EUR 1013.17 and GBP 718.36 per ounce.

(LBMA AM)

COMEX Gold in USD – 1 Year

Gold closed down $2.70 yesterday to finish the day at $1088.70. Silver closed at $14.42, down $0.14. Platinum lost $12 to $898.

Gold prices have slid in 10 of the last 10 COMEX trading sessions (see chart below) falling back to their lowest since early August – half decade lows in dollar terms. Gold looks very oversold on a few measures and is due a bounce.

The upside potential for gold and silver far outweighs the downside risk, in time. On a 5 to 10 year time horizon, the outlook for both precious metals is very positive.

Download Essential Guide To Storing Gold Offshore

end

A huge rise in silver investment demand is putting a record squeeze on supply. Also please note that with low prices for base metals and a possible curtailment of mining, this should also cause production to fall as most of silver production is a bi-product of base metal mining

(courtesy Steve St Angelo/SRSRocco Report)

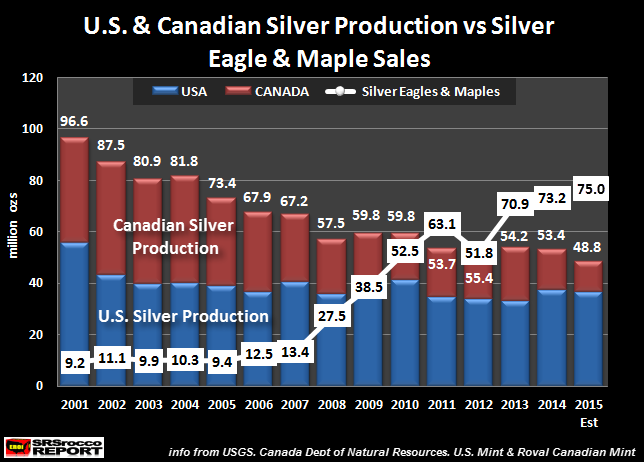

Rising Silver Investment Demand Puts Record Squeeze On North American Supply

Rising physical silver investment demand will put a record squeeze on North American supply this year. Since 2001, the United States and Canada have experience two opposite trends… surging official silver coins sales on the back of plummeting domestic mine supply.

For example, in 2001 U.S. and Canadian silver production totaled 96.6 million oz (Moz). Of that total, the U.S. produced 55.9 Moz, while Canada supplied 40.7 Moz. That year, Silver Eagle and Maple Leaf sales totaled 9.2 Moz.

Note: the red and blue bars represent Canadian and U.S. silver mine supply, while the white line and boxes show the total sales of U.S. Mint Silver Eagles and the Royal Canadian Mint Silver Maples.

Even though U.S. and Canadian silver production declined significantly to 67.2 Moz by 2007, total Silver Eagle and Maple Leaf sales only increased slightly to 13.4 Moz that year. Which means the U.S. and Canada still enjoyed a net 53.8 Moz domestic silver mine supply surplus after their official coin sales were deducted.

However, during the collapse of the U.S. Housing Market and Investment Banking System in 2008, Silver Eagle and Maple Leaf sales surged to 27.5 Moz while the combined silver production from the U.S. and Canada fell to 57.5 Moz. This pushed the combined domestic mine supply surplus from these two countries down to only 30 Moz once consumption for official silver coins were removed.

This trend counter-trend continued (except for a brief reversal in 2012) until it hit a record net deficit of 19.8 Moz in 2014. This supply deficit is a result of record sales of Silver Eagles and Maples of 73.2 Moz compared to 53.4 Moz combined silver production.

While it’s true the U.S. and Canada imports silver for industrial fabrication, jewelry, silverware and investment demand, this amount has increased significantly due to falling domestic mine supply. Let’s compare the net change since 2001:

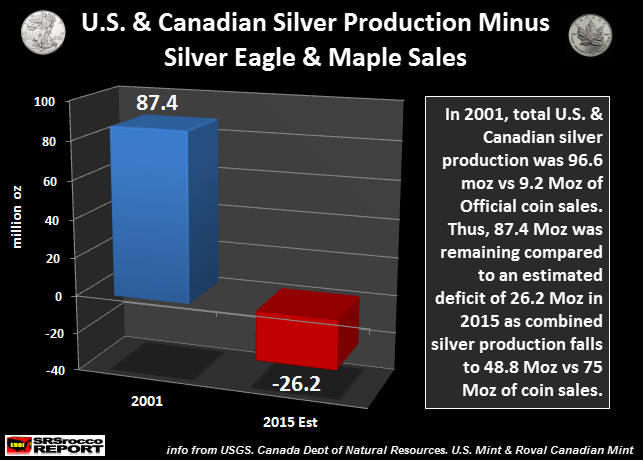

If we look at the chart above, we can see that the surplus of U.S. and Canadian silver mine supply minus consumption of their official silver coin sales was 87.4 Moz. However, this is estimated to be a net deficit of 26.2 Moz in 2015 as total Silver Eagle and Maple Leaf sales reach a record 75 Moz versus combined mine supply of 48.8 Moz.

The significance here is that the United States and Canada could use 87.4 Moz of their domestic mine supply (minus official coin consumption) for industrial, jewelry and silver ware fabrication, whereas now they have to import silver just to cover the consumption for their official coin production.

That being said, there continues to be this rumor that the U.S. Mint must use domestic silver mine supply for the production of its Silver Eagles. This used to be true when Congress authorized the U.S. Mint to use up the silver in its Strategic Stockpiles. However, after these inventories were depleted, Congress authorized the U.S. Mint to purchase silver on the open market for the production of its Silver Eagles.

Furthermore, commonsense tells us that at the estimated 37 Moz of U.S. domestic mine supply could not meet the total demand of 45 Moz of Silver Eagles this year.

Regardless, the charts in this article show just how much the surge of Silver Eagle and Maple Leaf sales have totally overwhelmed domestic silver mine supply from these two countries. While silver is still relatively cheap and abundant, there will come a time where silver producing countries such as Mexico and Peru will hold onto more of their mine supply for their own citizens.

Precious metal investors and especially the ignorant public have no clue just how little silver there is to go around when its true STORE OF WEALTH properties are realized.

Lastly, the first chart in this article was an updated chart found in my THE SILVER CHART REPORT. I am currently working on THE SILVER MARKET REPORT that will focus on the silver market going all the way back until the 1950’s.

One more thing. I have had requests from readers to add a DONATE button to the site. Some are not interested in the Paid Reports, but enjoy reading the public articles. So, after many requests, I have finally decided to add this DONATE feature to the site.

If you want to donate to the site, you can find the DONATE button at the bottom of each article or at the top right hand portion of the site. I plan on putting out more articles in the future on how best to protect one’s assets as U.S. and Global Oil production collapses. This is one of the most misunderstood concepts by the majority of analysts in both the precious metal community and Main Stream Media.

————–

end

The total amount of gold shipped from England to China this year is an astronomical 280 tonnes. (Last yr only 114 tonnes was exported).

What is fascinating here is that England does not produce any gold from any gold mines

As Koos reports, the onslaught of gold leaving the west to the east is in full swing.

Record UK Gold Export To China In September, Chinese Gold Import Reaches 156t

According to the most recent data from Eurostat the UK has net exported 37.6 tonnes of gold to China in September, an all-time record. This figure is up 25 % m/m and up 280 % y/y.

The UK started exporting gold directly to China in April 2014 when it shipped 5 tonnes to the mainland while for the first time bypassing Switzerland and Hong Kong. In total the UK net exported 114 tonnes to China in 2014. Year to date the UK has already net exported 210 tonnes of gold to China, annualized a whopping 280 tonnes, which would be 146 % more than last year. The exodus of gold from the West to the East is still in full swing.

Net export from the UK to Switzerland in September accounted for 44 tonnes, which is 45 % less than in August. Year to date the UK has net exported 417 tonnes of gold to Switzerland, down 0.3 % from 2014 and down 62 % from 2013 – all due to direct gold export to China instead of transshipping it through Switzerland for refining.

Overall the UK was a net exporter in September at 47 tonnes, which is 64 tonnes less than in August. Year to date the UK has net exported 334 tonnes in total – it has also imported gold, explaining total net export can be lower than what was net exported to China and Switzerland.

One of the greatest gold hoards on earth is located in London. The capitol of the UK has been the epicenter of the global wholesale gold market for centuries, hence many bullion banks and central banks have their physical gold stored within the M25 London ring way. It was estimated by a team of gold researchers (Ronan Manly & Nick Laird) that in early June 2015 approximately 6,256 tonnes of gold were stored in London. The composition of these holdings at the time was:

- 5,134 tonnes stored in the vaults at the Bank Of England (BOE), of which at least 3,779 tonnes were owned by central banks, the 1,355 tonnes residual were unknown holdings.

- 1,122 tonnes were stored in vaults outside the BOE, of which 1,116 tonnes in ETFs with a 6 tonnes residual in unknown holdings.

Because central banks are not likely to sell their gold (in significant quantities), what was potentially available for sale is the residual at the BOE (1,355 tonnes), the ETF gold (1,116 tonnes) and the residual outside the BOE and the ETFs (6 tonnes). Totalling at 2,477 tonnes, of which 1,116 tonnes in ETFs and 1,361 tonnes in unknown holdings.

By tracking gold export from the UK we can grasp what is happening to these stocks of gold in London. From 1 June until 30 September 2015 the UK net exported 181 tonnes in total, and GLD (the largest ETF in London) lost 27 tonnes over this period. Consequently, total ETF stocks must have declined to roughly 1,089 on 30 September, and unknown holdings in London down to 1,207 tonnes.

Here at BullionStar we have been writing withdrawals from the vaults of the Shanghai Gold Exchange (SGE), which equal Chinese wholesale gold demand, have been explosive in recent months. After the Chinese stock market plunged in June SGE withdrawals made an exceptional run up for the time of year. But, as SGE withdrawals skyrocketed we had to wait for foreign trade statistics to learn what the ratio was between recycled gold and import supplying the SGE (domestic mining supply being fairly constant), to get the best overall view on Chinese gold demand. High exports from the UK to China confirm Chinese demand has indeed been very strong this year. Although, it can still be there is more recycled gold flowing through the SGE relative to withdrawals than in previous years, because withdrawals are so exceptionally high this year.

Please read The Mechanics Of The Chinese Domestic Gold Market for a comprehensive explanation of the relationship between SGE withdrawals and Chinese wholesale gold demand.

Remember when in 2013 the gold price went down sharply and Chinese gold demand exploded? Back then Hong Kong net gold exports to China were dominating the headlines as these were thought to be the main indicator for gold going into China mainland. At the time China was importing large amounts of gold through this route, sometimes above 130 tonnes a month. More than a year later the Swiss customs department opened its gold cross-border trade book by deciding to publish gold trade statistics country specific. When we added these numbers to Hong Kong trade statistics we learned Chinese gold import had been (occasionally) more than 160 tonnes a month in 2013. Currently, we’re back at those levels. Aggregated net gold export from Hong Kong, Switzerland and the UK to China was 156 tonnes in September, which excludes gold export from Australia. The most recent data from Australia is from July and shows they have net exported 13 tonnes of gold directly to China (a record). SGE withdrawals were strong in July, but they were strong in August and September as well. I would not be surprised if Australia has exported over 10 tonnes of gold directly to China in August and September. If that appears to be true in the coming months China is importing at a tune of 166 tonnes a month. Let’s have a look at some charts.

In the chart above Australia’s gold export to China is not included for August and September, yet total Chinese gold import (derived from the countries of which I have access to the export data) has already reached 156 tonnes in September 2015.

In the chart below we can see strong SGE withdrawals from June until September have depleted the SGE vaults, which are being replenished by gold imports.

Currently, China is on track to import more than 1,400 tonnes this year, added by domestic gold mining output (476 tonnes) makes 1,876 tonnes.

Yes, it’s safe to say Chinese gold demand is very strong in 2015. We will compare these numbers with Chinese consumer gold demand as disclosed by the World Gold Council in a forthcoming post.

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

(courtesy John Embry/Kingworldnews)

Central banking’s attack on metals is more intense than ever, Embry tells KWN

Submitted by cpowell on Wed, 2015-11-11 23:53. Section: Daily Dispatches

6:53p ET Wednesday, November 11, 2015

Dear Friend of GATA and Gold:

Sprott Asset Management’s John Embry tells King World News today that central banking’s attack on the monetary metals has never been as intense as it is now. An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/the-best-antidote-to-the-chaos-that-is-happenin…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Cruz ups the ante by stating two important things:

i) audit the fed

ii) they must go back to the gold standard.

(courtesy New York Sun)

New York Sun: Silent Cal speaks

Submitted by cpowell on Thu, 2015-11-12 01:04. Section: Daily Dispatches

From the New York Sun

Wednesday, November 11, 2015

Call him Calvin Coolidge Cruz. Suddenly Senator Cruz, citing the president who delivered the full-employment economic boom known as the Roaring Twenties, is emerging as a man to watch in the Republican race. Two debates in a row, the senator from Texas declared for the gold standard and sound money, which are associated with high economic growth and low unemployment. He got in ahead of Rand Paul and any of the rest of the pack.

Two debates don’t make a campaign, of course, but the monetary issue is potentially the most transformative question in the race. It’s not just Mr. Cruz, either. Senator Paul, Governors Christie and Huckabee, and Senator Santorum all emerged on this issue last night, each adding enough savvy and subtlety to the question that it is clear the issue is starting to percolate on the hustings. No doubt this is in part because of what happened at the debate in Boulder, when CNBC’s Rick Santelli turned to the Texan and asked him to “focus on our central bank, the Federal Reserve.” …

… For the remainder of the commentary:

Sentiment means nothing in the gold ‘market,’ but GATA’s is to press on

Submitted by cpowell on Thu, 2015-11-12 03:44. Section: Daily Dispatches

11:15p ET Wednesday, November 11, 2015

Dear Friend of GATA and Gold:

Sentiment couldn’t be worse in the monetary metals sector right now. The good news and the bad news are that sentiment doesn’t matter.

Of course Mark Hulbert at MarketWatch thinks it matters, as he makes a business out of gauging the sentiment of financial letter writers, and he even calculates that sentiment for gold is good among those writers and constitutes a contrarian indicator, signifying that the metals will continue to fall, though of course those writers themselves are trying to be contrarian to market sentiment:

http://www.marketwatch.com/story/gold-investors-foolishly-think-the-yell…

And an anonymous blogger who says he attended GATA’s presentation at the New Orleans Investment conference last month writes that GATA Chairman Bill Murphy and your secretary/treasurer “both came across to me as defeated” and “have mentally lost the righteous battle they have been fighting for 15-plus years,” which he construes as another “bottom indicator” for gold:

http://news.goldseek.com/GoldSeek/1447166425.php

The guy is entitled to his impressions, and Murphy and your secretary/treasurer didargue in New Orleans that central banks are rigging markets, including the monetary metals markets, more ferociously and obviously than ever. After all, just a few days earlier an Austrian central banker had said as much himself —

http://www.gata.org/node/15878

— and Sprott Asset Management’s John Embry expressed the same thought tonight:

http://www.gata.org/node/15929

But “defeated”? Murphy and your secretary/treasurer would not have bothered going to New Orleans if we thought that. We still have enough to eat and drink at home. Nor would your secretary/treasurer, considering GATA defeated, be tapping this out on the keyboard so late at night when he could be watching old episodes of “Hill Street Blues” on TV.

* * *

GATA’s friend J.S. sounds close to defeated tonight anyway. He writes:

“Is there a point where even the noble gentlemen at GATA surrender to the inevitable and just capitulate, or can you ride out your principles to absolute ruin?

“Believe me, I’m on your side in all this, but there hasn’t been any single event — aside from the anomalous exchange-traded fund paper chase of 2010-11 — where we’ve seen any of the analysis from our side come to fruition. Ironically I would contend that the monetary metals are the worst investment precisely because they are the best investment. By this I mean they remain too much of a threat to the real beneficiaries of this country ever to be allowed to flourish.

“I think it’s apparent to all at this point that we live in a command-and-control economy and the people who are so heavily invested in the current paradigm will not hesitate to undertake the most nefarious and draconian measures to ensure that King Dollar is never dethroned. Besides, if the dollar was ever dethroned, I think we would have greater problems to contend with than the fair-market value of the monetary metals. It seems that the better the news for gold, the lower it goes.

“So here we are after another five years with nothing to show for our efforts. Market manipulation has been explained to me a thousand ways but what good is analysis based on economic fundamentals if it never yields a positive outcome? I keep joking with friends and colleagues that when I’m finally ruined by holding out to the inevitable climax for the metals I will become the most erudite homeless person in the world.

“Our blind faith in gold and silver has reached such proportions that it would make even the most zealous evangelical preacher envious, as the ‘gold rapture’ never seems to arrive. Like many others I was extremely confident about why gold and silver were the right choices, but now we are finding ourselves in for a rude awakening as we begin wondering how we will survive.

“I have nothing but praise for GATA’s efforts to bring the truth to light. But in the current political environment of warrantless wiretaps, too big to fail, undeclared wars, falsified economic statistics, whistle blowers treated like villains, and candidates who will never sincerely address the country’s real problems, we must ask: How did we manage to kid ourselves into thinking that doing the economically sound thing would ever succeed?

“My thanks to GATA for your efforts. Now if you’ll excuse me I have to ramble on over to Wal-mart to see if they’re still hiring.”

* * *

Yes, our little nonprofit educational and civil rights organization may need a bit more time to overthrow all the central banks — the creators of infinite money, the wielders of infinite power in secret — and thereby establish free and transparent markets and restore limited and accountable government in the civilized world. If mere sentiment made any difference in the face of that power, we in GATA might almost write despairing farewell notes and shoot ourselves tonight so that we could become the decisive contrarian indicators and thereby assure the success of our cause.

But our liquidation would not change central banking’s interests and objectives, which would remain the destruction of markets and the oppression of humanity.

While your secretary/treasurer would be surprised if the central banks can push gold much lower — after all, the mining industry already has been destroyed — they would not have to push gold down more to expropriate it outright or to expropriate the industry that mines it or to tax capital gains on gold at 100 percent.

But one can oppose the totalitarianism of central banking without necessarily investing in any particular way. Our cause does not require the financial ruin of its participants.

For those who want to stay invested in the monetary metals, mining entrepreneur Jim Sinclair offers some encouragement tonight on the eve of his seminar in Los Angeles:

http://www.jsmineset.com/2015/11/10/los-angeles-qa-session-announced/

As for your secretary/treasurer, he will offer hope only in the most general terms.

A little dialogue from “Casablanca” may be instructive, an exchange between the cynical but still vaguely idealistic nightclub owner Rick Blaine and the heroic if rather humorless anti-Nazi resistance leader Victor Laszlo:

BLAINE: Don’t you sometimes wonder if it’s worth all this? I mean, what you’re fighting for?

LASZLO: We might as well question why we breathe. If we stop breathing, we’ll die. If we stop fighting our enemies, the world will die.

Getting more cosmic, there’s always the Old Testament, where 1st Samuel recounts an improbable victory for the hugely overmatched side —

So David prevailed over the Philistine with a sling and a stone, and smote the Philistine, and slew him. But there was no sword in the hand of David.

And of course Isaiah says “they that wait upon the Lord shall renew their strength,” which your secretary/treasurer construes to mean that those who are doing the right thing always have at least an outside chance of divine favor.

The lights are still on and the Internet connection still works, so in the hope that weare doing the right thing we’ll press on in the morning.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Copper Plunges To Fresh 6 Years Low After Goldman Warns More Pain Ahead, Glencore Slides Back Under 100p

One month ago, when Glencore announced it latest copper production cut initiatives and mine mothballing efforts, we said that aside from the brief price spike, it would have absolutely no impact on the longer-term price dynamics of the metal which has achieved “doctor” status. The main reason we offered is that while Glencore was reducing supply, others such as Rio Tinto would gladly step in to fill the supply void. To wit:

Rio Tinto, warned that it will not cut copper production, saying it would be illogical to hold back output and leave space in the market for higher-cost rivals.

And just like that Glencore’s assumption that others in the space will act rationally, and “cooperate” with the attempt by Glencore to impose a new game theoretical equilibrium by reducing supply, and thus boosting prices, has crashed and burned.

According to the FT, Jean-Sebastien Jacques, head of copper and coal at Rio, said the Anglo-Australian mining group would not reduce output even though current prices of the industrial metal did not reflect “fundamentals”.

Rio’s CEO summarized his philosophy quite simply: “Why should I make cuts?” Mr Jacques said, in an interview ahead of LME Week, the biggest annual gathering of the metals and mining industry. “If you have marginal assets and marginal projects and you have a pretty weak balance sheet I think you may be in trouble pretty soon,” he said.

One month later, and just moments ago, we got confirmation of this prediction courtesy of the following two Bloomberg headlines:

- COPPER FALLS 1.8% TO $4,856/TON, REACHING LOWEST SINCE 2009

- NY COPPER DROPS AS MUCH AS 1.8% TO $2.177/LB, LOWEST SINCE 2009

Visually:

And intraday:

Worse for the company that as we said in early 2014 is the best proxy for both global copper demand and the Chinese industrial economy, after dead cat bouncing back to 125p in recent weeks, moments ago troubled Glencore (which alongside Volkswagen was one of the main corporate catalysts unleashing the September swoon) traded back under the psychological level of 100p.

So besides the obvious lack of actual wholesale production cuts as beggar thy higher-cost neighborstrategies are unleashed among the copper miners, did something else cause the latest overnight breakdown in prices?

The answer is yes, and it comes from a Goldman report titled simply enough “Copper poised to move even lower.”

Here is how report author Max Layton explains, in many more words than we used a month ago, what we said in early October when previewing this latest tumble in copper prices.

Supply growth has been weak, but demand has been weaker

2015 has seen slow rates of copper mine supply growth on supply disruptions and price-related closures and refurbishments. Despite the lack of supply growth, copper is now trading near its year-to-date lows and more than 20% lower than at the beginning of the year. This speaks to the ongoing demand weakness and deflationary cost environment which has driven the market into surplus and reduced cost support (the latter via a stronger dollar and weaker energy prices). Ongoing price weakness, in spite of price-related output cuts, is consistent with our view that producers do not move markets into deficit by cutting supply… rather they move markets closer to balance (than they otherwise would be). A demand recovery along with further supply discipline is required to see markets such as copper move into deficit.

Nearer term, LME and Comex net speculative positioning has picked up in recent weeks, in our view, partly on an anticipated improvement in Chinese economic data during 4Q15 (Exhibits 1 and 3). Should the Chinese data disappoint, and positioning unwind to January levels, or even lower, to August levels, copper prices may fall further than our base case forecast, which is for $4,800/t by year end. Indeed, SHFE open interest has risen across the base metals complex over the past two weeks as prices have pulled back (Exhibit 2), potentially suggesting that participants trading on the SHFE exchange are concerned about ongoing weakness in China’s commodity intensive ‘old economy’.

Importantly, we expect mine supply growth to accelerate in 2016-17 in the face of only limited demand growth. Indeed, over the coming months and throughout 2016 and 2017 investment during the prior boom period is set to bear more substantial fruit, with 5 major mines (the “big 5”) starting up or expanding output significantly, adding c.1.4mtpa of supply capacity by end 2017, and underpinning an acceleration in mine supply growth from c.1% in 2015 to at least c.3% pa in 2016/17. The “big 5” to watch are Cerro Verde (commissioning, Peru), Las Bambas (commissioning, Peru), Buenavista expansion (ramp up, Mexico), Sentinel (Commissioning, Zambia), and Grasberg (higher grades, Indonesia). We assume far less than nameplate is achieved in our supply and demand balance, in Exhibit 5, which shows pre-disruption allowance figures that we use in our model (Exhibit 4).

Stronger mine supply growth puts pressure on demand to pick up in order to absorb it. While we assume that a modest demand recovery in China will keep the copper market surplus around c.500ktpa in 2016 in our base case (Exhibit 5), our conviction level here is not high, and as a result we continue to see the risks to our supply and demand balance and price forecasts as skewed to the downside.

Overall, we continue to see the risks towards our $4,800/t year end 2015 and $4,500/t year end 2016 price forecasts as skewed to the downside, and recommend producers hedge and investors run long dated short positions.

* * *

Finally more charts than one can wave an electricity-conducting stick at.

end

Dave Kranzler on the upcoming default at Glencore:

Extremely important and a must read….

(courtesy Dave Kranzler/IRD)

Glencore Mirrors The Entire Global Financial And Economic System

- Collapsing fundamental economics

- Plunging end-user demand for its products

- Overloaded with debt

- Hidden land-mines in the form of OTC derivatives

Who said “black swans” have to be hidden? Glencore is in full view. After a dead-cat bounce from a quick descent that took Glencore stock from 310 (pounds) to 68 in 5 1/2 months, the stock is rolling over again and headed lower:

This isn’t just about the plunging price of copper, which is now back to its pre-financial system collapse price in 2008 and headed lower. Copper is responsible for generating only 36% of Glencore’s operating income. This is about the plunging prices and demand for oil and all base metals.

It’s about a company (global financial system) that hides a lot of risk, debt, derivatives, corruption and fraud. Point of example: Glencore’s funded debt level is $50 billion and it has the capability to draw on credit lines that would take it up to $100 billion. But the sleazebag snakeoil promoters cite Glencore as having $19 billion in “liquid” inventories so the debt number that gets quoted and widely accepted is $31 billion. But it’s not. It’s $50 billion. And Glencore’s “liquid” inventory is the same base metals that are plunging in price from oversupply and lack of demand.

Furthermore, over 30% of Glencore’s EBIT is derived from what the Company labels as its “marketing” business. But this is the legacy business that was originally Marc Rich’s commodities trading company. It’s a corrupted commodities trading and brokerage business. That means it’s riddled with hidden counter-party risks and derivatives. We don’t know the full extent of Glencore’s risk-exposure in this area because this an area that global financial regulators give financial firms a lot of breathing room with which to cover up the truth using insidious accounting schemes. But what I do know for sure is that you can rip and toss out any of the research reports indicating the Glencore’s derivatives exposure is limited to $5.2 billion. The real number is multiples of that.

With 50 billion (pounds) in funded debt and not including hidden off-balance sheet skeletons – Glencore’s debt to market capitalization (13 billion pounds) is nearly 4:1. That is an extreme degree of leverage for a volatile, commodities-based business which is headed into an economic depression.

Glencore is a microcosm for the entire global economic and financial system. Including and especially the United States. And here’s the kicker. Deutsche Bank is Glencore’s largest creditor. We can also very safely assume that Deutsche and Glencore are counterparties to a vast web of derivatives contracts. I’m sure Deutsche has also tried to off-load credit exposure thru the use of credit default swaps with hedge funds and other shadow banking participants. But who are those counterparties and how is the risk of default on this “insurance” Deutsche has likely “purchased.?” Glencore has the possibility of taking down Deutsche Bank, which in turn would take down the entire German system.

The rest will flow from there and there will be a lot of blood, including and especially in the United States.

Just like with Glencore, the true degree of ongoing economic collapse and financial risk exposure has been papered over with both QE and more debt issuance. It won’t take much trigger a financial nuclear explosion.

I would suggest that this is why the Central Banks and the relateve propaganda machine have shifted into full-gear in their effort to prevent the price of gold from engaging in unfettered price discovery. I would also suggest that this is why the U.S. conducted a highly visible Trident nuclear missile test along the west coast, in full view of Russia and China.

end

The big news of the day: the generally sanguine World Gold Council announces huge gold coin sales and it is at its highest levels since 2008:

very important for you to read..

(courtesy World Gold Council/zero hedge)

‘Gold’ Spikes Off 2015 Lows As Gold Coin Sales Surge To Highest Since Financial Crisis

With the ‘paper’ price of gold are a somewhat unprecedented barrage of selling currently (down 9 of the last 11 days) to 4-month lows, one could be forgiven for thinking that demand for the precious metal is dropping. However, as almost every nation in the world (ex US) is devaluing their currency, The World Gold Council reports that physical gold demand has risen dramatically with US gold Eagle coin sales at the highest levels since the financial crisis.

‘Physical’ Demand is exploding…

As ‘Paper’ prices collapse…

And then spike off 2015 lows…

As the latest report from The World Gold Council shows, gold buyers jumped on the new low prices…

“US retail investment demand jumped to 32.7 tonnes, generating growth of more than 200% year-on-year,”

“This signaled both a level of interest in gold investment not seen since the global financial crisis, and a level of price awareness on a par with that of Indian and Chinese retail investors. Nowhere was this more clearly demonstrated than in the US, where the US Mint reported rocketing sales of gold Eagle coins.”

…

“Demand for was the highest for more than five years: in volume terms, sales hit 397,000 oz.,”

“Demand for newly minted coins surged across all key product lines: sales across all denominations were many multiples of their long-term average levels. Secondary market activity was correspondingly weak as profit-taking slumped in favor of bargain hunting.”

Finally – who is buying? It’s not just those crazy retail gold bug doomers… Central Banks continue to back up the truck, taking advantage of the ‘low’ prices…Gold as a reserve asset remains firmly on the radar

Central banks continue to build their holdings of gold, adding 175t to official reserves.

Purchases by central banks and other official sector institutions almost equalled the Q3 2014 record of 179.5t as gold’s diversification benefits were increasingly recognised and sought. A couple of new countries joined the ranks of repeat buyers, the most significant of those being China.

The People’s Bank of China (PBoC) confirmed in July that its gold reserves had expanded by over 50% since its last announcement in 2009. At 1,658t, that put China at number six in the global rankings. Subsequently, the PBoC has begun regularly to report changes to its gold holdings and has confirmed an additional 50.1t of purchases between July and September.

And in another small but significant step, the central bank of the United Arab Emirates (UAE) confirmed that, between April and September it added 5t of gold to its reserve asset portfolio, having held none since 2003. The result is that the UAE makes it into the top 100 holders of gold and expands the geographical spread of central bank buyers.

Q3 saw continued buying by regular names, primarily concentrated in the CIS region. Selling was again limited and sporadic.

So it makes all the sense in the world that gold ‘prices’ are testing the lowest levels since October 2009…

Charts: Bloomberg and The World Gold Council

Global Gold Demand Hits More Than Two-Year High in Third Quarter, World Gold Council Says

By Jan Harvey

Reuters

Thursday, November 12, 2015

LONDON — Global gold demand hit its highest in more than two years in the third quarter as July’s price drop boosted buying of jewellery, coins, and bars, the World Gold Council said on Thursday.

Overall demand reached 1,121 tonnes in the last quarter, up 8 percent year on year to its highest since the second quarter of 2013. The rise was tempered by increased outflows from bullion-backed exchange-traded funds, however.

Bar and coin buying more than tripled in the United States to a five-year high of 32.7 tonnes, and rose 70 percent in China and 35 percent in Europe. That followed a more than 6 percent slide in spot gold prices in July, their biggest monthly drop in two years. …

However, outflows from gold ETFs — popular investment vehicles that issue securities backed by physical metal — increased by 24 tonnes year on year to 65.9 tonnes, helping to offset the rise in demand elsewhere. …

… For the remainder of the report:

http://www.reuters.com/article/2015/11/12/us-gold-wgc-report-idUSKCN0T110B2015111

India’s smuggled gold could be 25% of supply

New York closed at $1,084.70 down $3.70 yesterday. In Asia it rose to $1,088.05 before London opened. The LBMA price setting fixed it at $1,087.60 down from $1,088.60 over yesterday. The dollar Index is at 99.14 up from 98.95 at today. The dollar is at $1.0715 up from $1.0740 against the euro. In the euro the fixing was €1,014.795.63 down from €1,015.63. Ahead of New York’s opening gold was trading in the dollar at $1,086.85 and in the euro at €1,014.14.

The silver price closed at $14.30 down 12 cents from yesterday’s close. At New York’s opening, silver was trading at $14.42.

The currency markets, the dollar and the gold price stabilized with a weaker bias, again today. Again, the dollar has not broken through the 100 level on the dollar Index. With the Eurozone contemplating negative interests rates down as far as 0.75% [like Denmark and Sweden] we believe that the Treasury and the E.C.B. have or will agree that such stimuli not be permitted to weaken the euro. That is, if the dollar Index rises above 100, convincingly. Technically the euro should be moving to par with the dollar. We continue to watch to see if this is the new way forward. If so it will have a positive impact on the gold price.

There were no sales from the SPDR gold ETF but sales of 0.45 of a tonne from the Gold Trust. The holdings of the SPDR gold ETF stands at 663.432 tonnes in the SPDR gold ETF and at 159.85 in the Gold Trust. These sales had no impact on the gold price

Single’s Day on Alibaba was around 50% higher than last year, confirming what we said about the burgeoning growth of the middle classes in China. It is from this quarter that the future gold demand will come. The day was certain evidence of the rising disposable income among those classes. If we are to believe the Indian GDP growth figures of 7.3% we will see the urban Indian middle classes change the shape of Indian gold demand too. Currently the demand from the agricultural community is poor this year as a low quality monsoon led to lower disposable income for gold. However, the available figures on Indian demand completely ignores smuggled gold, which has to be 25% plus, of supply to the nation.

Let’s ask a few questions to put this in perspective. If your local forecaster showed you the radar of a cat5 hurricane out in the gulf moving very slowly toward you, is there anyone or anything that could get you to cancel your homeowners or flood insurance? This is the case in today’s financial and geopolitical world. You see daily where leverage has risen to previously unseen ratios. You have watched as interest rates around the world have been zeroed out and in many cases have gone negative. You see reported economic numbers that make no sense and are regularly contradicted by real world experience.

Geopolitically you see the United States losing power at every turn to the hands of China/Russia and the rest of the world. Power is being supplanted in trade, finance, manufacturing and production, socially and even militarily. This loss of power is unmistakable …but, none of this matters because the stock market is up, credit markets are still stable (on the outside), the dollar is firm versus other fiat currencies and gold has been pressed down and down. THIS is now the “new normal” and nearly everyone is extrapolating it forward “forever”.

Sorry to break the news to you but ALL of this is unsustainable. You need not even take Bill Holter’s word for this, just listen to the number crunchers and bean counters regarding Social Security, Medicaid, pensions, healthcare, military spending, the real economy and on and on. In many cases, the “bean counters” are previous federal employees like David Stockman and David Walker, who better would know?

We mathematically have the largest financial hurricane of all time coming and will be a direct hit worldwide. All of the “rigs” will be taken down and lost. Have you ever asked yourself what the world would look like should free markets price everything? Do you really believe interest rates would be where they are? Or the stock markets? Would a McDonalds hamburger only cost $3? Would you be able to get $2 gasoline when the rest of the world in many case $5 per gallon or more? When the financial storm hits, do you believe your bank or broker will survive because they are “special”?

1 Chinese yuan vs USA dollar/yuan falls badly in value , this time at 6.3678/ Shanghai bourse: in the red , hang sang:green

2 Nikkei closed up 6.38 or 0.03%

3. Europe stocks all in the red /USA dollar index up to 99.15/Euro down to 1.0719

3b Japan 10 year bond yield: falls badly to 30.8% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 122.99

3c Nikkei now just above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 42.66 and Brent: 45.56

3f Gold down /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .620 per cent. German bunds in negative yields from 6 years out

Greece sees its 2 year rate fall to 7.39%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 7.53% (yield curve flat)

3k Gold at $1084.87 /silver $14.37 (8:00 am est)

3l USA vs Russian rouble; (Russian rouble down 42/100 in roubles/dollar) 65.85

3m oil into the 42 dollar handle for WTI and 45 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0051 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0773 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/

3r the 6 year German bund now in negative territory with the 10 year falls to +.620%/German 6 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.32% early this morning. Thirty year rate above 3% at 3.11% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Euro Crushed By Draghi’s Latest “Whatever It Takes” Moment; Fed Speaker Barrage On Deck

It was a seesaw day for Chinese stocks which started off on the wrong foot despite an Australian jobs number that was so good even the Australian media and economistsaren’t buying it, perhaps aided by a Chinese new loans number that missed badly (new loans of CNY514Bn, Exp. 800Bn, aggregate financing CNY477Bn, Exp. CNY1.05Tr) and suggests the recent surge in credit creation may be tapering, however the afternoon session once again saw the arrival of the National Team with stocks recovering all losses before closing 0.48% in the red.

The intervention did not help commodities, however, as Shanghai steel futures fell more than 1% to another record low pressured by shrinking demand in top consumer China that has dented appetite for raw material iron ore. With falling prices seen forcing more Chinese steel mills to either cut output or close, demand from the biggest iron ore buyer is at risk, keeping ore prices lower for longer as top suppliers fight for more market share. Copper prices also continued their slide following a note from Goldman overnight predicting even more downside for the “Doctor” which in turn has pushed shares of Glencore back under 100p again.

But the biggest event overnight came from Europe, where Draghi managed to once again jawbone the Euro lower by over 50 pips when he told European lawmakers in a prepared testimony that downside economic risks are “clearly visible,” repeating his October press conference statement, adding that the ECB will reexamine degree of accommodation in December as “inflation dynamics have somewhat weakened.”

And the statement that crushed the Euro: “If we were to conclude that our medium-term price stability objective is at risk, we would act by using all the instruments available within our mandate to ensure that an appropriate degree of monetary accommodation is maintained.” I.e., another “whatever it takes” moment.

The immediate result:

Another immediate result:

- GERMAN TWO-YEAR NOTE YIELD DROPS TO RECORD-LOW MINUS 0.372%

This means that even if Draghi cuts to -0.30%, 2 Year bonds will still be below the yield floor and thus not eligible for purchases, which will then force the ECB to cut even more sending yields even more negative and so on in a cat and mouse game of twilight zone monetarism.

What is perhaps more disturbing is that despite the aggressive jawboning by Draghi, while the Euro obediently tumbled, neither European stocks nor US futures rebounded and the latest market snapshot can be seen below:

- S&P 500 futures down 0.1% to 2067

- Stoxx 600 down 0.7% to 376

- MSCI Asia Pacific up 0.4% to 134

- US 10-yr yield down less than 1bp to 2.32%

- Dollar Index up 0.07% to 99.08

- WTI Crude futures up 0.2% to $43.03

- Brent Futures up 0.2% to $45.90

- Gold spot up less than 0.1% to $1,087

- Silver spot up 0.5% to $14.40

One reason for the market’s lack of euphoria is that today we get another surge in Fed speakers later today, which means the risk of being caught offside to some ridiculous algo momentum ignition is very high, and why liquidity will be lower than usual. Specifically, speaking today we have Janet Yellen, No.2, Stanley Fischer, and four other Fed stooges. Look for much more December rate hike jawboning; the question is whether it will be hedged with talk focusing on the latest swoon in stocks and the resumed collapse in oil prices.

The speaker calendar:

- 9:15am: Fed’s Bullard speaks in Washington

- 9:30am: Fed’s Yellen speaks in Washington

- 9:45am: Fed’s Lacker speaks in Washington

- 10:15am: Fed’s Evans speaks in Chicago

- 12:15pm: Fed’s Dudley speaks in New York

- 6:00pm: Fed’s Fischer speaks in Washington

Another catalyst that may have prevented a rebound in Europe (and US) were earnings by engine making giant Rolls Royce whose shares sank the most in 15 years after a stark profit warning, which tumbled by 20%. Some £2 billion ($3 billion) of market value disappeared after the company said 2016 earnings will be hurt from declining demand for business jet engines and lucrative maintenance services on bigger turbines. This year’s profit will also be at the lower end of the forecast range. New CEO Warren East will unveil plans to reorganize the company on Nov.24. Shares have plummeted 37 percent in 2015, on track for the worst annual performance in seven years.

Back to the overnight markets, where in Asia stocks traded mixed, following the tepid lead from its US counterparts. ASX 200 (+0.5%) pared initial energy inspired losses after the strong Australian jobs report signalling an improvement in the economy, while the Nikkei 225 (-0.1%) oscillated between gains and losses. Shanghai Comp. (-0.5%) plunged the most in a week led by tech names with growing concerns that the recent 25% bounce back from the August low has been overdone amid a raft of weak data from the nation. JGBs rose 12 ticks amid light volumes, subsequently shrugging the relatively lacklustre 30-yr auction.

Notable was China’s monetary data which came decidedly mixed. As Goldman summarizes, October M2 growth was above market expectations while loan and TSF growth were well below market expectations. However, the weakness in TSF came in more volatile components.

- New CNY loans: Rmb 514 bn in October (RMB loans to the real economy: Rmb 557.4 bn) vs. GS forecast on loans to the real economy: Rmb 700 bn, Bloomberg consensus: Rmb 800 bn. September 2015: Rmb 1,050 bn; October 2014: Rmb 548 bn. Outstanding CNY loan growth: 15.4% yoy in October (14.3% SA ann mom, estimated by GS); September 15.4% yoy (14.6% SA ann mom).

- Strong M2 growth was supported by two factors: (1) very supportive fiscal policy with October fiscal spending at 36.1% yoy, (2) less drag from FX flows compared with September as indicated by the FX reserve data (though we would like to see more data such as FX position data to get a better sense). Both are supportive of domestic liquidity conditions.

- Loan supply was modestly weak but seasonally adjusted sequential growth remained firm.

- The downside surprise of TSF data was mainly the result of a large drop in discount bills, which tend to be a very volatile category. Despite the downside surprise the month-on-month growth of the TSF stock, after adjusting for local government bond issuance, was 14.8% annualized, only slightly slower than September.

- The mixed picture from money and credit data is broadly consistent with the lackluster activity data in October. Given activity growth is still on the soft side of officials’ comfort zone, and CPI inflation has been decelerating (it has surprised on the downside for two months in a row and is likely to remain low at least in November), policy is still likely to maintain a loosening bias. We continue to expect another cut in RRR (50 bps) and benchmark rates (25 bps) before the end of the year.

Hong Kong’s Hang Seng Index rebounded 2.4% after a five-day drop, the longest since Aug.24, becoming Asia’s best-performing stock market on Thursday. The gauge has suffered from a series of weaker-than-forecast Chinese economic data even as China’s own stocks rebounded.

The price action in the European morning session was governed by comments made by ECB’s Draghi, whereby he continued the dovish rhetoric from last month’s press conference, most notably stating that the ECB will examine monetary policy accommodation at the December meeting. As such, this leaves the door open for both an extension for the current QE program and a cut in the deposit rate.

European equities (-0.7%) also saw modest upside on the back of ECB’s Draghi’s comments, however major European indices remain in negative territory as sentiment remains downbeat after the latest soft data out of China, combined with the uncertainty with regards to the form of ECB easing in terms of whether the ECB may cut the deposit rate or expand QE . Separately for equities, multinational companies may benefit from ECB monetary easing, however may also have to contend with the possible December rate hike by the Fed, which could counter effects from the ECB action.

On a stock and sector specific basis, equities were led lower by a spate of poor earnings releases from the likes of Rolls Royce (-20%) and RWE (-8.0%), while seeing the energy sector underperform after WTI and Brent erase all their overnight gains shortly before the European cash equity open.

As a consequence, EUR is weaker across the board as market participants continue to price in further monetary easing, with significant weakness being seen this morning against both the USD and CHF; while in the more long term view and given previous rhetoric from the SNB, a sustained move lower in EUR/CHF may be a concern for the Swiss central bank.

In Asia, AUD outperformed amid positive Australian jobs data, as the headline reading topped expectations printing the highest figure since March’12 (58.6K vs. Exp. 15.0K), which also saw OIS price in as little as a 5% chance of a rate cut from the RBA in December compared with a 60% probability before the release.

In fixed income markets, Bunds also benefited from ECB’s Draghi’s comments and peripheral bond yield spreads are seen broadly tighter. However gains were capped by supply out of Italy, with the equivalent of 36k bund futures set to be issues. Front-month Euribor was also bid on the prospect of lower rates and further policy intervention.

In commodities, WTI continues to trade around 2 month lows amid the continuing supply glut, as demonstrated by Tuesday’s API crude oil inventories printing a build for the seventh straight week, which has been exacerbated by the stronger USD. Softness continues to be seen in base metals as copper continued its downward trajectory, falling for the fifth session out of six in Asia following yesterday’s weak Chinese industrial production data. Base metals continued to sell off during European trade, as a result of more weak Chinese data releases, with Chinese New Yuan Loans CNY (Y/Y 513.6B vs. Exp. 800.0B Prey. 1050.0B) and Aggregate Financing CNY (Oct 476.7B vs. Exp. 1050B Prey. 1300B, Rev. 1302B) both missing expectations. Of note, copper is now closing on the year low of USD 4,855 which it reached in August.

Today’s key events in the US this include the initial jobless claims reading, shortly followed by more employment data in the September JOLTS job openings read. Later we’ll also get the October Monthly Budget Statement. It’s a particularly busy day for Fedspeak as mentioned with Bullard (2.05pm GMT), Yellen (2.30pm GMT), Evans (3.15pm GMT), Dudley (5.10pm GMT) and Fischer (11pm GMT) all expected to speak at various points.

Top news:

- Draghi Says Inflation Weakening as December Policy Choice Nears: Likelihood of inflation returning to the ECB’s desired level has declined and economic risks are rising, Mario Draghi said at hearing in the European Parliament on Thursday

- China Credit Growth Falls as Tepid Economy Dents Loan Demand: Aggregate financing slumped to 476.7 billion yuan ($75 billion), lower than all 25 economists’ projections

- Global Banks Agree Contract Updates to Stave Off Another Lehman: Agreed to rewrite trillions of dollars of financial contracts as the industry seeks to persuade regulators that they can fail without bringing down the global economy

- Rolls-Royce Plunges as 2016 Profit to Suffer Near $1 Billion Hit: Will drop as demand for business-jet engines and lucrative maintenance services on bigger turbines declines

- Siemens Raises Dividend and Plans $3.2 Billion Share Buyback: Will buy back as much as EU3b of shares over the next 3 years

- Lenovo Loss Slimmer Than Expected Amid Shift Away From China: 2Q net loss of $714m vs $803m avg expected by analysts; sales climbed 16%, also beat ests.

- Salini Buys Lane Industries for $406 Million to Expand in U.S.: Has been looking for an acquisition in North America for more than a year as CEO seeks business in fast-growing mkts for infrastructure investments

- Russia Sees Syria War Endgame Stretch to 2017 as Talks Renew: Will propose a political transition in Syria lasting as long as 18 months at the next round of talks starting Saturday in Vienna

- Major Oil Companies Have Half-Trillion Dollars to Fund Takeovers: Exxon tops the list with total of $320 billion for potential acquisitions, followed by Chevron with $65 billion in cash and its own shares, then BP with $53 billion

- Apache’s Snub of Anadarko Approach Puts Both Explorers in Play: For Anadarko, an acquisition of the $20 billion company would have served as a defense from any potential suitors

Overnight Summary from RanSquawk and Bloomberg

- Dovish comments from ECB’s Draghi sees weakness in EUR but failed to pull equities out of negative territory

- Bunds also benefited from ECB’s Draghi’s comments and peripheral bond yield spreads are seen broadly tighter, however gains were capped by supply out of Italy

- Looking ahead, today sees US weekly jobs data, JOLTS and DoE inventories as well as a host of Fed and ECB speakers

- Treasuries gain amid as stocks decline on weak earnings, slowing credit growth in China; quarterly refunding ends today with $16b 30Y bonds, WI 3.110% (highest since June) vs 2.914% in October.

- Mario Draghi signaled that the ECB is ready to boost its stimulus programs next month as economic prospects worsen and “signs of a sustained turnaround in core inflation have somewhat weakened”. Draghi says QE “is actually working,” had “powerful effects” on banking, markets

- Industrial production in the euro area fell more than forecast in September, declining 0.3% vs -0.,1% est

- Goldman expects ECB to cut deposit rate by 10bp to -30bp in Dec., leave main refi rate unchanged at 5bp, extend QE through end of 3Q 2017

- China’s broadest measure of new credit slumped to the lowest in 15 months in October, adding to evidence six central bank interest-rate cuts in a year have yet to spur a sustained pick up in borrowing

- Hermes International SCA and Burberry Group Plc reported sputtering sales growth in America, adding to the woes of luxury-goods makers already reeling from an Asian slump

- Sweden has imposed temporary border controls to stem a record inflow of refugees as the Nordic nation pleads with the rest of Europe to help deal with the biggest migration wave seen in the region since World War II

- Russia will propose a political transition in Syria lasting as long as 18 months at the next round of talks starting Saturday in Vienna, where diplomats will resume the search for a settlement to the country’s civil war.

- $7b IG priced Tuesday, $200m HY. BofAML Corporate Master Index OAS holds at +161, YTD range 180/129. High Yield Master II OAS widens 8bp to +602, YTD range 683/438

- Sovereign 10Y bond yields lower. Asian stocks mixed, European stocks and U.S. equity-index futures decline. Crude oil and copper fall, gold gains

DB’s Jim Reid completes the overnight recap

It was fairly quiet in markets again yesterday, which was unsurprising with the US Treasury market closed for Veterans Day. As you’ll see in the day ahead at the end of the report it’s a very busy day for Fedspeak today with five officials due to comment including Fed Chair Yellen shortly after lunchtime, so expect news-flow to pick up. Yesterday US equity markets were open and traded with a bit of a softer tone for much of the session. The S&P 500, Dow and Nasdaq all finished the session -0.32%. In fact, this was an incredibly rare event. Running the numbers since the commencement of the Nasdaq in 1971, we calculate that this has only ever happened on one other day which was 15th August 1978 (assuming returns are calculated to 2dp’s). Meanwhile, prior to this European markets had actually moved higher with the Stoxx 600 +0.65% while European sovereign bond yields edged down a couple of basis points as another dovish ECB story out of Reuters made the rounds which we’ll touch on shortly.

The commodity complex was again the centre of some of the sharper moves. Metals were weak reflecting the softer than expected Chinese IP data yesterday with Silver (-0.73%), Platinum (-2.07%), Zinc (-2.25%), Copper (-0.78%) and Lead (-1.51%) all under pressure. Oil markets also tumbled which sent energy stocks sharply lower yesterday. WTI finished the session -2.90% to close back below $43/bbl for the first time since August 24th. Brent was weak too, finishing down over 3% and back below $46/bbl. It feels like most days at the moment we see fresh negative headlines suggesting the glut in prices is set to be prolonged and yesterday saw the latest American Petroleum Institute numbers show inventories increased by 6.3m barrels last week which was far higher than analyst expectations of 1.1m according to the WSJ, sparking the sell-off. On top of this, news that Iraq has loaded 10 tankers to supply US crude to American ports also weighed on sentiment, as did the EIA raising its forecast for US crude production for the remainder of the year.

Back to that Reuters story yesterday on the ECB. The article suggests that the Bank is considering the possibility of buying debt of cities and municipalities as part of its asset purchasing programme, possibly as soon as March next year. Reuters suggests that almost $500bn of bonds issued by cities and muni’s are in circulation currently, with the article suggesting that options are being studied. There was little mention of the possibility of buying corporate debt other than it being ‘much sought after and therefore difficult to buy’ according to the article. In any case, it’s another clear dovish hint from the ECB that some sort of further stimulus is likely. While the expansion into cities and muni’s for Q3 wouldn’t materially raise the overall universe, it does potentially increase the time horizon for countries seeing a shortage of assets.

Staying with the ECB, late last night we also heard from board member Coeure who, while noting that the decision is yet to have been made, confirmed that ‘the debate is open’ with regards to possible further easing. Coeure added that Euro area growth is accelerating ‘but it remains weak, while inflation expectations have stopped improving and underlying inflation has hit a ceiling’.

Turning to the latest in Asia this morning markets are somewhat mixed. The Hang Seng (+1.0%) is up for the first time in 6 days largely led by Tech and Consumer names. The Nikkei is flat but the Shanghai Composite is down just around 1% as we type partly driven by Financials and Energy stocks. Asia credit is trading reasonably firm with high quality corporates around 2-3bps tighter. Staying in China, there has been a few updates over the last 24 hours but one of the interesting macro stories was a Bloomberg article which reported that the central Government may increase the municipal debt-swap program quota up by 25% to CNY3.8-4.0trillion this year. Chinese rates are slightly higher on the back of potentially more long dated bond supply. Recall the plan was first established earlier this year to ease financing conditions at the local government level in the hope of supporting infrastructure spending.

Overall easier policy is perhaps starting to show and we got more signs of that from yesterday’s Chinese data. Indeed in a note yesterday our China Chief Economist, Zhiwei Zhang, noted that some of these indicators stabilized in October. Some of the positives that Zhiwei touches upon in particular were leading indicators for FAI. He points out that funds available for FAI rose by 7.3% yoy last month, compared to 6.8% in September having been driven by improving funds from state budget. On top of this, planned investment for new projects grew along with ongoing project investment, suggesting fiscal policy easing is working. In addition land sales as reported by the NBS improved sharply in October, jumping to -9.1% from -42.8% in September. This is consistent with other recent lands sales data and again reinforces the view that fiscal revenue will improve in Q4 and Q1. On the negative side, new housing starts failed to maintain the strong momentum of September, casting uncertainty on the property sector outlook. Overall Zhiwei maintains his growth forecast of 7.2% yoy in Q4 and 6.7% in 2016. As a baseline case he expects no more IR or RRR cuts for the rest of the year, but notes that the chance of one more IR cut is rising post the soft CPI data.

Switching tracks a little and back to markets, one of the most interesting themes we’ve been discussing with credit clients over the last few days has been the latest data from the NY Fed showing US corporate debt inventories turning negative for the first time on record. Rather like the fact that swap spreads are now deeply negative in the US, this again shows the relationships and ideas we knew from the past are changing in this heavily regulated market and financially repressed world. In both markets year-end pressures are exacerbating the issue. We still believe that when this credit cycle ends the lack of liquidity will be a major issue but for now other factors are still more dominant for the direction of spreads and we don’t think there has been an increase in the liquidity premium in recent times. In fact with inventories run down so uickly, and with the in ows we ve s een in recent weeks, had it not been for still huge US supply, credit could have gapped tighter. At the moment supply is offsetting positive inflows and remains a big issue for US credit. However in some ways it does reflect that there is still demand for the asset class. The worst periods in credit markets are when you can’t give new deals away. At the moment record supply is being taken down which is causing spread indigestion rather than anything more serious at the moment.

Trying to gauge the volume of supply in US that we’ve seen and post Tuesday’s c.$7bn of issuance, we’re standing now at nearly $57bn alone for the month of November so far and $1.4tn YTD. Putting it into perspective, that’s currently running about 17% higher YoY.

Just wrapping up yesterday and specifically the data, the only release of note was out of the UK where there some mixed signals from the latest employment rate. On the positive side the ILO unemployment rate fell in September, declining one-tenth to 5.3% (vs. 5.4%). However wages data were softer than expected. Ex-bonus earnings fell three-tenths to 2.5% yoy which was lower than expected (vs. 2.6% expected).