Gold: $1076.40 down $1.60 (comex closing time)

Silver $14.10 down 14 cents

In the access market 5:15 pm

Gold $1078.40

Silver: $14.20

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a very poor delivery day, registering 0 notice for nil ounces. Silver saw 8 notices for 40,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 200.01 tonnes for a loss of 103 tonnes over that period.

In silver, the open interest fell by 1454 contracts despite silver being up by 16 cents in yesterday’s trading. We probably had some short covering. The total silver OI now rests at 170,549 contracts In ounces, the OI is still represented by .852 billion oz or 122% of annual global silver production (ex Russia ex China).

In silver we had 8 notices served upon for 40,000 oz.

In gold, the total comex gold OI was hit again with this time 1182 contracts removed as the OI fell to 423,392 contracts despite gold being up by $9.20 in yesterday’s trading. It seems the modus operandi of the bandits is to try and liquefy gold/silver OI as we approach first day notice on Monday, November 30. The bankers get very nervous when OI is rising despite awful prices for the metals. We had 0 notices filed for nil today.

We had a huge withdrawal in gold inventory at the GLD to the tune of 1.19 tonnes/ thus the inventory rests tonight at 660.75 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver, we had no change in silver inventory to the tune of / Inventory rests at 317.256 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by 1454 contracts down to 170,549 despite the fact that silver was up by 16 cents with respect to yesterday’s trading. The total OI for gold surprisingly fell by 1182 contracts to 423,392 contracts despite the fact that gold was up by $9.20 with respect to yesterday’s trading.

(report Harvey)

2 a)Gold trading overnight, Goldcore

(Mark OByrne)

b) COT report

(Harvey)

3. ASIAN AFFAIRS

4. EUROPEAN AFFAIRS

i) Draghi gives a speech early this morning and he states that he will do anything possible to raise INFLATION

That ought to be good for gold except our crooked bankers decided it best to whack again

(zero hedge)

ii The German 2 year bund goes deeper into the negative at -.39%. This also causes much grief to Draghi as he has less “good” bonds to monetize. He is not allowed to monetize bonds that are deeper into the negative

(zero hedge)

iii) Europe is set to outlaw Bitcoin and any virtual currency

(courtesy zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i Russia shows its power by obliterating ISIS in Syria

50 oil trucks totally demolished

(2 commentaries/zero hedge/Inside Russia)

6 GLOBAL AFFAIRS

i) The Baltic Dry Shipping Index just collapsed again and it is at an all time record low

(courtesy Michael Snyder/Economic CollapseBlog)

ii)Islamic Gunmen storm a luxury hotel in Mali. USA special forces and French forces will be coming to the aid of Mali

( zero hedge/3 commentaries)

iii) Suicide bomber hits Yemen

(zero hedge)

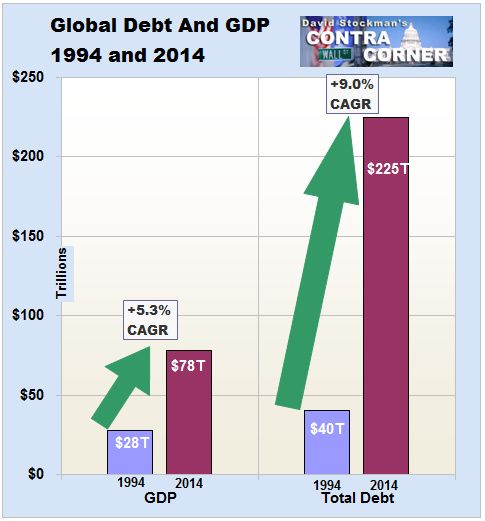

iv) David Stockman writes a terrific commentary showing the plight of the global economy. Through Caterpillar, Stockman illustrates that the next victim in global growth is “cap -ex depression”

7 EMERGING MARKETS

none today

8 OIL RELATED STORIES

i) Oil spikes higher on lower rig counts

(zero hedge)

9 USA MAJOR STORIES

i) USA 30 yr bond yield initially breaks below 3.00%. With the Dow rising this makes no sense unless:

a) the upcoming rate hike is deemed by many to be a policy error

b) a flight to quality due to the many Islamist blasts during the past 7 days.

(zero hedge)

ii) The subprime auto loans continue to climb in a parallel bubble to the 2007 subprime housing bubble

this is an accident waiting to happen

(zero hedge)

iii) Tesla recalls 90,000 vehicles due to a seat belt problem:

(zerohedge)

iv) Chipotle Restaurants fall badly with announcements of E coli found in 3 restaurants

(zero hedge)0

v) Puerto Rico has big payments due on Dec 1 and it looks like it may default. Congress has not come up with any plan on how to bail these guys out:

(courtesy zero hedge)

vi/ Fed to have an emergency meeting on Monday!!

what could this be??

Fed To Hold An “Expedited, Closed” Meeting On Monday

10. PHYSICAL STORIES

i) The house passes to bill such as to provide for more transparency at the Fed. It has no chance of becoming law as Obama will veto it.

(GATA)

ii) New York Sun also comments on the above story

(New York Sun)

Let us head over to the comex:

The total gold comex open interest fell from 424,574 down to 423,392 for a loss of 1182 contracts despite the fact that gold was up by $9.20 in yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. For today, both were in force especially the former. The November contract lost 2 contracts lowering to 210 contracts. We had 0 notices filed yesterday, so we lost 2 gold contracts or an additional 200 oz will not stand for delivery in this non active delivery month of November. The big December contract saw it’s OI fall by a monstrous 13,019 contracts from 173,288 down to 166,541. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 166,541 which is fair. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was good at 210,611 contracts.

November contract month:

INITIAL standings for November

Nov 20/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 100.04 oz

Delaware |

| Deposits to the Dealer Inventory in oz | 98.10 oz

Brinks first deposit in a year and a half |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 contracts |

| No of oz to be served (notices) | 210 contracts

(210,00oz |

| Total monthly oz gold served (contracts) so far this month | 7 contracts

700 oz |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 267,403.2 oz |

Total customer deposits 0 oz

we had 0 adjustments:

November initial standings/First day notice

Nov 20/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 262,114.730 oz

(Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 600,005.200

Brinks |

| No of oz served (contracts) | 8 contracts (40,000 oz) |

| No of oz to be served (notices) | 25 contracts

150,000 oz) |

| Total monthly oz silver served (contracts) | 56 contracts (280,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 7,858,232.3 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

we had no dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposit:

i) Into Brinks; 600,005.200 oz

total customer deposits: 600,005.200 oz

total withdrawals from customer account: 262,114.73 oz

Nov 16.And now SLV/another huge addition of 2.145 million oz into the silver inventory of SLV/rests tonight at 317.256 million oz

Nov 15/no change in silver inventory at the SLV/inventory 315.111 million oz/

nov 12/surprisingly we had a huge addition of 1.43 million oz of silver into the SLV/Inventory rests at 315.111 million oz/(my bet: it is paper silver not real silver entering the vaults)

Nov 11/no change in silver inventory at the SLV/rests tonight at 313.681 million oz/

Nov 10/no change in silver inventory at the SLV/rests tonight at 313.681 million oz/

Nov 9/no change in silver inventory/rests tonight at 313.681

Nov 6/ we had a very tiny withdrawal of 136,000 oz (probably to pay for fees)/Inventory rests tonight at 313.681 oz

Nov 5/strange no change in silver inventory/rests tonight at 313.817 million oz/

Nov 4/2015: no change in silver inventory/rests tonight at 313.817 million oz/

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 173,395 | 138,996 | 52,408 | 170,494 | 198,967 | 396,297 | 390,371 |

| Change from Prior Reporting Period | ||||||

| -1,166 | 32,824 | -13,252 | 14,548 | -28,873 | 130 | -9,301 |

| Traders | ||||||

| 138 | 127 | 102 | 52 | 48 | 238 | 237 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 39,079 | 45,005 | 435,376 | ||||

| -1,180 | 8,251 | -1,050 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, November 17, 2015 | |||||

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 72,282 | 47,028 | 14,945 | 57,596 | 93,120 | |

| -22 | 13,714 | -1,007 | 9,215 | -5,390 | |

| Traders | |||||

| 89 | 56 | 43 | 44 | 46 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 170,721 | Long | Short | |

| 25,898 | 15,628 | 144,823 | 155,093 | ||

| 100 | 969 | 8,286 | 8,186 | 7,317 | |

| non reportable positions | Positions as of: | 153 | 133 | ||

| Tuesday, November 17, 2015 | © Si | ||||

Dark Days: Vulnerable Europe faces crisis of confidence

Europe is in a very dark place. Under the cloud of on-going terrorist threats there is widespread fear of what the future holds – economically, socially and politically.

Jeremy Warner writing for the Telegraph yesterday describes the ‘abyss’ into which we are sliding and how this is precisely the reaction that the terrorists had hoped to elicit, despite the fact that – “even in Israel, citizens are far more likely to be the victim of a car accident than a terrorist outrage”.

Despite the initial bravado and defiance of the population in the immediate wake of such attacks, there is inevitably always a knock-on effect. “Most people will indeed carry on as before, but it only takes a 10pc reduction in footfall to have quite marked economic effects.”

Despite the initial bravado and defiance of the population in the immediate wake of such attacks, there is inevitably always a knock-on effect. “Most people will indeed carry on as before, but it only takes a 10pc reduction in footfall to have quite marked economic effects.”

“Yet it is to the wider geo-political impact of terrorism that we must look for the longer-term economic consequences.

In providing a pretext for war in Afghanistan and Iraq, 9/11 ended up having a massive economic impact far beyond any immediate behavioural changes.”

“The fiscal costs alone of these wars were vast. On its own, Iraq is estimated to have cost the US $1.1 trillion, and that’s ignoring myriad after conflict costs, which compound over time.”

“The wars also triggered a series of interest rate cuts in the US and beyond, helping to unleash a dangerous degree of credit expansion which ultimately culminated in the Global Financial Crisis (GFC). You can have guns or butter, it is sometimes said, but not both. America and Britain tried to have both, and paid the price.”

Read the full article: “Europe is sliding towards the abyss, and the terrorists know it”

You can follow Jeremy Warner on twitter

DAILY PRICES

Today’s Gold Prices: USD 1073.10, EUR 1004.18 and GBP 703.05 per ounce.

Yesterday’s Gold Prices: USD 1070.50, EUR 1002.95 and GBP 702.74 per ounce.

(LBMA AM)

Gold in EUR – 1 Month

Gold gained yesterday closing up $0.60 to $1070.10. Silver lost slightly on the day closing at $14.17, down $0.04. Platinum lost $5 to $84.

Download your guide to Protecting Your Savings in the Coming Bail-in Era

The Rats and The Sinking Ship

Yes, what we are about to show you is simply a collection of anecdotal data points. Taken separately, perhaps they can all be written off and marginalized. Taken collectively, however…well, maybe there’s something to consider here.

This site has been around for over five years now and, for most of that time, we’ve preached about how fractional reserve bullion banking is a scheme that is destined to fail. By pricing a physical commodity upon the oversupply of paper derivatives, shortages become inevitable. The market recognizes the value of the mispricing and drives up demand. At the same time, the lower price affects supply as producers of the commodity limit or shut down production due to the economics and declining/negative margins.

What eventually happens is a physical supply shortage that manifests itself in smaller global stockpiles. This is evident in the increasing abundance of stories about the tight global gold market, particularly in London. This has also become apparent in silver as, just this week, Thomson Reuters GFMS released their latest Silver Interim Report, which projected the third consecutive year of a global shortfall in the supply of physical silver. Check these links for details:

- http://www.cpifinancial.net/news/post/33686/mine-production-stagnates-as-silver-coin-demand-hits-record-high

- https://srsroccoreport.com/official-release-world-silver-deficits-12-years-running/

- https://smaulgld.com/silver-coin-and-bar-demand-2015/

As we all know, the global “price” of physical gold and silver is largely derived by trading on highly-leveraged futures exchanges such as The Comex in New York. On these exchanges, a modern form of alchemy has been perfected, whereby a relatively small amount of metal can be leveraged multiple times in the creation of paper metal derivative contracts. If after five years we are, in fact, seeing the first real physical cracks in the global paper metal bullion banking scheme, logic would compel us to expect those cracks to appear at The Comex first.

And that may be what we are seeing play out in real time. Below are those “anecdotal data points” mentioned above. Consider them independently but also take time to view them collectively, as well.

COMEX BANK LEVERAGE AT RECORD LEVELS

This site and others have been documenting this trend for weeks. What we’re talking about here is not margin leverage. Instead, this is The Banks’ ability to lever their existing supply of readily-deliverable gold. On the Comex, this is gold classified as “registered” and it is this registered stockpile that has been at record lows for over two months. As of Thursday, the amount of gold shown in this category was just 151,384 troy ounces. When you divide this amount of available gold into the total amount of “paper gold” outstanding…as measured by a total open interest of 424,000 contracts (100 paper ounces per contract)…we get a historically high and unprecedented leverage ratio that is nearing 300:1. We’ve repeatedly written about this here and you can also see this displayed on the chart below from ZeroHedge:http://www.tfmetalsreport.com/blog/7249/bullion-bank-leverage-soars-near-3001

TOTAL COMEX GOLD STOCKS

However, it’s not just registered gold on The Comex that is dwindling, it’s also the total amount of gold held in the bullion bank vaults. The chart below was published yesterday by Dave Kranzler, at his excellent site called Investment Research Dynamics:http://investmentresearchdynamics.com/did-greshams-law-invade-jp-morgans-comex-gold-vault/ Note that over the past five years the total amount of gold held within the Comex vaulting system has declined from over 12,000,000 troy ounces to yesterday’s new low of 6,436,404 troy ounces. Of course, this hasn’t limited The Banks ability to create paper metal to meet occasional speculator demand, but that’s a topic for another day. http://www.tfmetalsreport.com/blog/7214/inherent-unfairness-comex

THE GOLD HELD BY JP MORGAN

But let’s dig even deeper and look at the gold held by individual Bullion Banks within the Comex vaulting system. Every day, the CME puts out a “Gold Stocks Report” which attempts to show the total amount of gold held within the Comex vaults, though the CME added a major disclaimer to the report back in 2013 (http://jessescrossroadscafe.blogspot.com/2013/06/caveat-emptor-another-level-of-risk.html)

On the Gold Stocks report below, dated July 27 of this year, note that JPM reported a total vault of nearly 1,398,215 ounces. In that vault were 115,755 ounces categorized as registered and 1,282,460 ounces listed as eligible.

Next is a chart from about two weeks ago. Note that JPM’s total vault has been more than cut in half. Total registered gold has fallen to just 10,777 ounces and total eligible gold was shown to only be 657,721 ounces. Hmmm.

But now look at what has transpired in just the past week. The total amount of gold held in the vaults of JPM has been cut in half again! As of Monday, JPM showed a total of 668,498 ounces of gold in their Comex vault. After two separate withdrawals of nearly five metric tonnes, JPM’s vault was down to just 347,898 ounces as of yesterday:

So, after including the massive withdrawals of just this week, the total amount of gold held by JPMorgan in their Comex vault has fallen by 1,050,317 troy ounces…or 32.7 metric tonnes…that’s a cumulative 75.1%…in just the past four months.

SCOTIA MOCATTA’S GOLD AND SILVER VAULTS

And if you’re beginning to feel as I do…that all of these points are connected…then what is going on at The Scoshe might be the most important as the Canadian bank, Scotia Mocatta, is the “oldest” gold dealer and bullion bank in the world.

One might think that, as the world’s oldest bullion bank, The Scoshe is pretty well wired into what’s going on in the global gold market. Additionally, you don’t get to be the longest-tenured bullion bank without recognizing/anticipating change and then positioning yourself for future profits…and, as importantly, avoiding current losses.

We’ve detailed what appears to be a slow-burning “bank run” that is ongoing at Scotia Mocatta’s Comex vault. We most recently wrote about the trend here: http://www.tfmetalsreport.com/blog/7170/comex-bank-run-scotia-mocatta Note that The Scoshe (or their clients) almost appears to be exiting the Comex system…similar to what we’re now seeing at JPMorgan. As you can see on the report below, back on March 5 of this year The Scoshe allegedly held 3,066,169 troy ounces of gold in their Comex vault. (You might also note the total amount of gold held by all six banks at that time and compare it to the 6,436,404 ounces reported yesterday.)

Now let’s look again at the CME Gold Stocks report from yesterday. Notice that The Scoshe currently shows just 79,096 ounces of registered gold and about 1,008,831 ounces of eligible gold for a total vault of 1,167,927 troy ounces. This means that, over the course of the past 8+ months, Scotia Mocatta has lost 77% of its registered gold and 60% of its eligible gold. As measured by its total vault, the drop has been 1,898,242 troy ounces…or 59.4 metric tonnes…that’s a cumulative 61.9%…in a little over eight months.

And here’s where the intrigue regarding The Scoshe gets even deeper. They’re losing (moving?) silver, too.

Below is a CME Silver Stocks report from September of 2013. Note that the total amount of silver held with Scotia Mocatta’s Comex vault was well over 22MM ounces or about 695 metric tonnes.

By May of this year, Scotia’s silver vault was down to about 15MM ounces or about 468 metric tonnes:

And after yesterday’s posted withdrawal of over 1MM ounces, Scotia’s Comex vault held only 5,148,700 troy ounces of silver.

So, measuring from September of 2013, the drop in Scotia Mocatta’s Comex silver vault has been 17,188,272 troy ounces…or about 535 metric tonnes…that’s a cumulative 76.9%…in about 26 months.

SUMMARY

Again, we’ll leave it up to you, the reader, to decide if something significant is happening behind the scenes OR if what has been displayed above is simply a collection of disparate data points. Maybe ponder these questions over the weekend, though:

- Is the world’s most important bullion bank (JPMorgan) moving gold away from a Comex system that is leveraged to a degree not seen before in its history?

- Is the world’s oldest bullion bank (Scotia Mocatta) relocating gold AND silver away from and out of the same Comex vaulting system?

- If they are doing so, are these banks signaling that they, too, understand that the days of the current fractional reserve and derivative-based pricing scheme are numbered?

- As gold and silver exit the Comex system…and as reports continue about physical tightness in London…and as the world continues to run physical silver supply deficits…it at safe to conclude that the system’s ultimate collapse is, at a minimum, an eventuality?

I don’t know about you, but I think I’ll buy some more gold and silver today…and take immediate delivery. The current pricing scheme may not collapse next week or next month (as stated above, we’ve been writing about this for over five years), but it’s not going to last forever, either. And when change does come…and a new system emerges that determines price on the trading of physical and not synthetic metal…I’m quite confident that the prices “discovered” are going to be a little bit higher than $1100/ounce for gold and $14/ounce for silver.

Prepare accordingly.

TF

end

and now Dave Kranzler on the same subject as above:

Did Gresham’s Law Invade JP Morgans Comex Gold Vault?

Gresham’s Law states that bad money drives good money out of the system. People will use inferior money in their daily “bartering” for goods, services, investments etc and hoard good money.

We are seeing Gresham’s Law work in the gold market, where eastern hemisphere Central Banks, investors and populations are in the process of hoarding all the gold the west will send their way in exchange for the constituent country fiat currencies. “Here, take our currency and convert it to dollars and sell us your gold.”

And the gold seems to disappear from sight. Can anyone hazard a guess how much gold the People’s Bank of China controls or where it’s safekept?

Recently my friend and colleague Craig “Turd Ferguson” Hemke – TFMetals Report – noticed an usual amount of gold was being removed from the “registered”/investor account in JP Morgan’s Comex vault. Last Friday, for instance, 24% of the eligible gold disappeared from JPM’s registered vault account and disappeared to destinations unknown: LINK

Again yesterday another chunky 160,750 ozs of gold fled the questionable custody of JP Morgan’s eligible account (click on image to enlarge):

The amount of gold removed yesterday represented 32% of the amount of gold remaining the eligible account after last Friday. In total, this entity or entities has/have removed 49% of the gold that was sitting in “investor safekeeping” section of JP Morgan’s Comex custodial vault.

We can only speculate what might of “spooked” the entitled owners of that gold to take it away from the Comex.

However, I will say this confidence: whomever removed that gold decided that they no longer trusted JP Morgan to safekeep it. It’s interesting because the Comex offers storage rates that are a significant discount to market rates to investors who take delivery off the Comex and use the Comex vaults for safekeeping.

Whatever the case may be, nearly 50% of ALL of the gold in Comex vaults has been removed since 2011 (source: 24hgold.com, edits are mine – click to enlarge):

(courtesy GATA)

House passes bill calling for rule-based monetary policy

Submitted by cpowell on Thu, 2015-11-19 21:01. Section: Daily Dispatches

By Jason Lange and David Lawder

Reuters

Thursday, November 11, 2015

WASHINGTON — The U.S. House of Representatives on Thursday approved a bill that would make the Federal Reserve set interest rate policy using a mathematical rule, a proposal that has little chance of becoming law given a White House veto threat.

The House approved the Fed Oversight Reform and Modernization Act in a 241 to 185 vote thanks to overwhelming Republican support.

The bill is a sign of the deep suspicion many Republican lawmakers hold against the U.S. central bank, which played a major role in America’s policy response to fight the 2007-09 recession. …

… For the remainder of the report:

http://www.reuters.com/article/2015/11/19/us-usa-fed-house-idUSKCN0T82HD…

New York Sun: House bill on Fed includes audit provision and monetary commission

Submitted by cpowell on Fri, 2015-11-20 01:03. Section: Daily Dispatches

From the New York Sun

Thursday, November 19, 2015

We’d like to think it’s no coincidence that less than a month after Paul Ryan of Wisconsin became speaker, the House of Representatives passed the most important monetary reform bill since Humphrey Hawkins in 1978. This happened today with the decision to send to the Senate the Federal Oversight, Reform, and Modernization Act. Mark it well that the Ryan era is about substance, and the most representative body in the American government is unhappy with the performance of the Federal Reserve and is ready for reform. …

The measure passed today would require the Fed to set a monetary rule of its choosing and let the Congress and the American people know what it is. It also includes Audit the Fed, which would give Congress continuing oversight into the Fed’s operations. And, importantly, it would establish the Centennial Monetary Commission, a formal body to review the various monetary regimes the Fed has pursued and make recommendations for reform as it begins, as it does this year, the second century of its operations. …

… For the remainder of the commentary:

1 Chinese yuan vs USA dollar/yuan falls in value , this time at 6.3875/ Shanghai bourse: in the green , hang sang: green

2 Nikkei closed up 20.00 or 0.10%

3. Europe stocks mixed /USA dollar index up to 99.33/Euro down to 1.0682

3b Japan 10 year bond yield: rises to .319% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 123.12

3c Nikkei now just above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 41.43 and Brent: 44.17

3f Gold up /Yen up

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .483 per cent. German bunds in negative yields from 6 years out

Greece sees its 2 year rate rise to 6.75%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield falls to : 6.93% (yield curve close to inversion)

3k Gold at $1084.20/silver $14.31 (8:00 am est)

3l USA vs Russian rouble; (Russian rouble down 44/100 in roubles/dollar) 64.96

3m oil into the 41 dollar handle for WTI and 44 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0161 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0853 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/arrests 10 traders for Euribor manipulation

3r the 6 year German bund now in negative territory with the 10 year falls to +.483%/German 6 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.25% early this morning. Thirty year rate above 3% at 3.01% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Rise, Global Stocks Set For Best Week In Six Unfazed By Terrorism Concerns

Futures are modestly higher in early trading having tracked the USDJPY once again almost tick for tick, with the carry trade of choice rising to 123 shortly after Mario Draghi’s latest speech pushed the dollar strong initially only to see most gains promptly evaporate against both the Yen and the Euro. European shares are likewise little changed, after gaining earlier, while Asian stocks rise; oil also advanced in early trading only to drop to its lowest overnight level moments ago, a few dimes over $40, with aluminum and copper both posting modest increases.

Perhaps it is worth noting that a week which many predicted would be bad for risk assets has been precisely the opposite and nowhere more so than in France, where as Bloomberg reports, after Europe’s worst terror attack in more than a decade hasn’t deterred equity investors this week, with France’s CAC 40 Index rising as much as 2.5 percent. Fewer than 10 stocks have fallen, among them Accor, Europe’s biggest hotel operator, which dropped 4.7 percent on Monday on concern about tourist flows. Since then it’s clawed back more than half of those losses. The CAC 40 Index remains one of Western Europe’s best performing equity indexes this year.Only Denmark, Ireland, Italy and Austria have fared better

As Bloomberg also notes, while global stocks are little changed so today, the MSCI All Country World Index is on track for its best week in six. Investors have a new-found belief the path of U.S. interest rate increases will be gradual even if the Federal Reserve embarks on tighter monetary policy next month for the first time in nine years. The MSCI Asia Pacific Index has risen 1.6 percent this week, while the MSCI Emerging Markets Index has jumped 2.4 percent.

Perhaps more notable is that despite the Fed’s tightening rhetoric, emerging market currencies are set for their first weekly gain in five. The JPMorgan Emerging Market Currency Index has risen 0.5 percent over the past five days, the most since Oct. 9. This week some of the year’s worst-performing emerging market currencies have rallied against the dollar. The Brazilian real has risen 3.5 percent, having dropped 28 percent in 2015. The South African rand has jumped 3 percent after falling 17 percent this year.

This is where we stand currently:

- S&P 500 futures up 0.2% to 2084

- Stoxx 600 down less than 0.1% to 381

- MSCI Asia Pacific up 0.4% to 135

- US 10-yr yield up less than 1bp to 2.26%

- Dollar Index up 0.2% to 99.19

- WTI Crude futures up 0.1% to $40.60

- Brent Futures up 0.9% to $44.58

- Gold spot up 0.3% to $1,085

- Silver spot up 0.6% to $14.36

Among the top overnight news: Obama, Putin Agree on One Thing: Bombing Islamic State’s Oil: French leader to push for consensus in Washington, Moscow; France Scrutinizes EU’s Terror Failings a Week After Attacks: Hollande presses ahead on military cooperation with Russia; Swedish Prosecutor Detains Suspected Terrorist: suspect affiliated with Islamic State in Iraq, Swedish media says; Pfizer Said Near Allergan Deal as U.S. Targets Inversions: U.S. drugmaker may pay as much as $380 per share for Allergan; Draghi Says ECB Will Do What It Must to Raise Inflation Quickly: ECB President spoke in speech in Frankfurt; ABN Amro IPO Raises $3.6b as Government Cuts Stake: IPO values ABN at EU16.7b as bank returns to market; 1MDB Said to Near $2.3b Power Sale to Chinese-Led Group: deal with group may be announced as soon as this weekend; Gap Cuts Annual Profit Forecast as Sales Continue to Slide: Sees FY2016 adj. EPS $2.38-$2.42 vs prior view $2.75-$2.80; Goldman Said to Raise $1.3 Billion to Buy Stakes in Hedge Funds: bank started raising money for Petershill II in 2013, initially aiming to raise $1b, according to person familiar.

A closer look at the markets shows Asian stocks rose, with the regional benchmark index extending its biggest weekly advance in 6 weeks; equities traded mixed in a tepid fashion following the flat lead from US bourses. ASX 200 (+0.1%) extended on gains led higher by financials, subsequently on course for the 2nd best week of 2015, while the Nikkei 225 (+0.1%) initially fell as Japanese exporters continued to feel the squeeze from a stronger JPY before recovering heading into the close. Shanghai Comp. (+0.1 %) traded with mild gains following reports that the PBoC reduced the SLF rates in an attempt to combat deflationary pressures., JGBs fell following a lacklustre enhanced liquidity auction which drew a lower than prior b/c.

Key Asian Data:

- MSCI Asia Pacific up 0.4% to 135

- Nikkei 225 up 0.1% to 19880

- Hang Seng up 1.1% to 22755

- Shanghai Composite up 0.4% to 3631

- S&P/ASX 200 up 0.3% to 5256

In Europe, the reaction to Draghi’s latest “whatever it takes to boost inflation” speech in fixed income was somewhat more muted with Bunds relatively unmoved immediately preceding the speech, however we have seen a leg lower in 2 year yield subsequently touching new record lows of -0.39%, while it is worth noting that the Euribor curve has continued to flatten, with the front strip adding between 1.5 and 2 ticks, while the red and green strips remain in the black. Of interest, Portuguese bonds are underperforming their European counterparts this morning amid continued political uncertainty with the Socialists still unable to form a stable government and subsequently unable to guarantee passing their budget. Greek yields also trade notably wider to the German benchmark amid concerns over the fragility of the Syriza government, following yesterday’s expulsion of several members

Key European Data:

- Stoxx 600 up less than 0.1% to 381

- FTSE 100 up less than 0.1% to 6332

- DAX down less than 0.1% to 11077

- German 10Yr yield up less than 1bp to 0.49%

- Italian 10Yr yield down 1bp to 1.5%

- Spanish 10Yr yield down 2bps to 1.67%

- S&P GSCI Index up 0.4% to 338.7

Equity markets have seen a choppy start to the session (Euro Stoxx: -0.5%), with energy names the session’s laggard given that the stronger USD (USD-index: +0.10%) is keeping commodities near their lows as WTI Jan’15 futures remain below USD 42.00/bbl and spot gold continues to reside around USD 1080.00/oz. Stocks continue to edge lower in Europe, from a technical perspective the CAC (-0.50%) and Dax (0.0%) broke their 200DMA’s to the downside.

In commodites, WTI and Brent trade relatively flat, with a lack of fundamental news driving price action. However, WTI is on course to post its 3rd consecutive week of decline, with US supplies sustaining the glut especially following a drop in the front month contract which has seen a drop of 1.1% to the lows of the session.

Gold traded range bound overnight with the USD-index remaining in a tight range after comments from Fed’s Fischer who reaffirmed December hike expectations. Of note, FFR futures are currently pricing in a 68% chance of hike in December. Elsewhere, most LME metals have fallen to multi year lows this week, however copper and Zinc for 3 month delivery have attempted to claw some ground back in recent trade.

Bulletin Headline Summary from Bloomberg and RanSquawk

- Comments from ECB’s Draghi saw immediate downside in EUR, underlying the significance of the December meeting. However moves in EUR/USD were not overtly pronounced, highlighting the dovishness of the market

- Stocks have sold off with CAC and Dax both breaking 200DMA’s to the downside, with financials and energy underperforming

- Looking ahead, highlights include Canadian Retail Sales and CPI, Coeure and Constancio, Fed’s Bullard and Dudley

- Treasuries little changed, 5/30 extends flattening amid expectations Fed to hike rates in Dec; Fed’s Dudley to speak today; yesterday Vice Chairman Fischer said Fed trying not to surprise markets at liftoff.

- Draghi set the scene for further stimulus at the ECB’s next meeting in two weeks’ time, saying it will do what’s necessary to reach its inflation goal rapidly

- A year of ABS purchases by the ECB has left investors underwhelmed and confused as the purchases have been dwarfed by other stimulus efforts and failed to prevent an issuance slowdown; a shortage of detail has led to complaints about transparency

- Chinese borrowers are taking on record amounts of debt to repay interest on existing obligations, raising the risk of defaults and adding pressure on policy makers to keep financing costs low

- China’s slowdown is already playing out across the world, dragging down commodity prices and weighing on trade partners — and that’s while the economy is still growing at about 7%, according to government data. So imagine what happens in a hard-landing scenario

- Federal regulators have started to intensify their scrutiny of risky company loans extended by Wall Street’s biggest banks, just weeks after completing an annual audit of corporate lending, according to people with knowledge of the matter

- France pressed its European partners to toughen security and intelligence across the continent, saying other countries’ shortcomings were to blame for the failure to prevent last week’s terror attacks

- U.S. and French military forces entered a hotel in the Malian capital of Bamako where gunmen took 170 hostages in an attack on the Radisson Blu Hotel

- Sovereign 10Y bond yields higher. Asian stocks gain, European stocks lower, U.S. equity-index futures decline. Crude oil mixed, gold and copper gain

DB’s Jim Reid completes the overnight wrap

After Wednesday’s rally it felt like a bit of winter-related fatigue crept into US equities yesterday with the S&P 500 failing to break out of a tight 8pt range during the session, crossing between gains and losses multiple times and eventually finishing down -0.11%. That was actually the 4th smallest trading range this year (by points) for the index. The steadiness masked what were some steep falls for healthcare stocks (driven by a profit warning from UnitedHealth) and energy names as WTI – although closing the session down ‘only’ -0.64% – broke below $40 again temporarily for the second consecutive day after more bearish inventory data. Meanwhile, the latest October machine sales numbers from Caterpillar failed to inspire much hope for a near-term rebound in the mining sector after reporting sales down double-digits in all regions, with Asia in particular seeing sharp drop-off.

Prior to this European stocks had previously closed broadly higher (Stoxx 600 +0.43%) although off their earlier intraday highs while the ECB minutes didn’t offer a whole lot of new information but continued to hint towards a possible further easing in December (more on that below). The notable underperformer yesterday was US credit where CDX IG finished +3bps wider with the commentary suggesting that book builds for new issues were slightly underwhelming and suggestive of supply indigestion. Still, weekly volumes for US IG has again topped $30bn, marking the fourth consecutive week above that mark.

Meanwhile, the Atlanta Fed President Lockhart was vocal again yesterday, reiterating his view that the Fed is ready for liftoff but continuing to warn that ‘the pace of increases may be somewhat slow and possibly more halting than historic episodes of rising rates’. While the prospect of a December move is looking more and more likely, the likelihood for a gradual pace of moves thereafter appears to be weighing on the USD slightly with the Dollar index finishing -0.69% lower yesterday with sharp gains across the board for currencies in emerging markets in particular (Brazil +1.3%, Malaysia +1.1%, South Africa +1.0%, Colombia +1.0%). US Treasury yields generally nudged lower at the longer end of the curve for the same reason, the benchmark 10y closed 2.5bps lower at 2.248% and 30y yields closed over 3bps down.

Near the end of the US session we also heard from Fed Vice-Chair Fischer who said that the Fed has ‘done everything we can to avoid surprising the markets and governments when we move, to the extent that several emerging market (and other) central bankers have, for some time, been telling the Fed to just do it’.

It’s a bit of a mixed end to the week for bourses in Asia this morning, with little newsflow in the region. The Nikkei (-0.09%) and Hang Seng (-0.23%) are both lower as we go to print, while there’s been a modest gain for the Shanghai Comp (+0.50%), Kospi (+0.08%) and ASX (+0.26%). Asia credit is unchanged, while credit indices in Australia are wider and US equity futures are near flat. The only data of note has come from China where the Conference Board leading economic index was up +0.6% mom in October.

Yesterday’s US data was generally pretty supportive. Initial jobless claims were down 5k last week to 271k (vs. 270k expected) which is pretty much consistent with the current four-week average. The November Philly Fed manufacturing survey was up 6.4pts this month to 1.9 (vs. -0.5 expected) at the headline and back in positive territory after two successive negative prints. In the details, while still negative, new orders and shipments components were up, while the employment index edged back up into positive territory. Shortly following this, the October Conference Board’s leading index printed a +0.6% mom gain, bettering expectations by a tenth.

Over in Europe the main data of note was out of the UK where we saw retail sales come in slightly below expectations for October (excluding fuel -0.9% mom vs. -0.6% expected), although that was on the back of a strong September reading. Meanwhile, the ECB minutes showed that it was argued that the ‘risk of deflation remained relevant’ and that ‘against this background, the view was put forward that a case could be made for considering reinforcing the ECB’s accommodative monetary policy stance already at the current meeting and, in any case, to act sooner rather than later’. Governing Council members also found it ‘necessary to step up communication and underscore the Governing Council’s determination and readiness to act’. Notably, the accounts also highlighted that ‘reference was made to the experience in other jurisdictions, where negative rates had not appeared to result in major difficulties or widespread substitution into cash’.

One other snippet worth highlighting emerged late last night with the news that the Treasury Department has issued new rules which is set to discourage US corporate inversions. According to the WSJ, the rules will restrain US companies from putting their addresses in foreign countries with the aim of benefiting through lower tax bills. Significantly, one of the aspects of the rules is set to apply retroactively to inversions since September 2014, impacting the likes of big headline M&A deals including Medtronic and Mylan and creating issues for Pfizer’s potential deal with Allergan. An interesting story to keep an eye on.

Wrapping up, yesterday also saw the confirmation in Greek parliament of the passing of the vote for the measures required to disburse the bailout funds from creditors. The pass means €2bn will be disbursed to pay state arrears and a further €10bn for bank recapitalisation. Focus will now turn to the progress for the bank recaps, with the FT reporting that three of the four eligible banks said earlier this week that they have reached the thresholds required.

Looking at the day ahead, the Fed’s Bullard is set to speak on the US economy while Dudley will later speak on the same subject later. Over the weekend the San Francisco Fed’s Williams is due to speak on a panel focused on US monetary policy developments which could be of some interest.

end

Let us begin:

ASIAN AFFAIRS

“People Are Worried” – Chinese Authorities Arrest ‘King Of IPOs’ & ‘Hedge Fund Brother No. 1’

The arrests or investigations targeting the finance industry in the aftermath of China’s summer market crash have intensified in recent weeksaccording to Bloomberg,creating a climate of fear among China’s finance firms and chilling their investment strategies. As one professor of Chinese economy noted, “some in the political leadership sought to find scapegoats to blame”for the market crash which along with massive intervention “created uncertainty and anxiety that can only undermine the effort to make these markets work better.” :

1.The high-drama highway arrest of a prominent hedge fund manager. 2.Seizures of computers and phones at Chinese mutual funds. 3.The investigations of the president of Citic Securities Co. and 4. at least six other employees. Now,5) add the probe of China’s former gatekeeper of the IPO process himself.

About a third of China’s futures-focused hedge funds had to stop trading as regulators restricted practices such as short-selling,but as Bloomberg details,

Howbuy Investment Management Co. in September said it stopped providing data on premature fund liquidations because the information was too sensitive. The Shanghai-based fund research firm had previously said almost 1,300 hedge funds closed this year amid the stock rout.

The authorities’ goal was to root out practices such as insider trading as part of China’s anti-corruption campaign, and a desire by “some in the political leadership to find scapegoats to blame” for the market crash, according to Barry Naughton, a professor of Chinese economy at the University of California in San Diego.

“Together these are creating uncertainty and anxiety that can only undermine the effort to make these markets work better,” he said by e-mail.

The government’s response to the market crash was intervention: state-directed purchases of shares, a ban on initial public offerings and restrictions on previously allowed practices, such as short selling and trading in stock-index futures. Next, high-ranking industry figures came under scrutiny as officials investigated trading strategies, decried “malicious short sellers” and vowed to “purify” the market.

Policy makers say “now we’re innovating, so you can all come in — using high-frequency trading, hedging, whatever — to play in our markets,” Gao Xiqing, a former vice chairman of the China Securities Regulatory Commission, told a forum in Beijing on Nov. 6. “A few days later, you say no, the rules we made are not right, there are problems with your trading, and we’re putting you in jail for a while first.”

At least 16 people have been arrested, are being investigated or have been taken away from their job duties to assist authorities, according to statements and announcements compiled by Bloomberg News.

In the latest probe announced last week, Yao Gang, a vice chairman at the CSRC, is under investigation for “alleged serious disciplinary violations,” the Communist Party’s Central Commission for Discipline Inspection said.Known as China’s “King of IPOs,” he supervised China’s initial public offerings until earlier this year, when he changed to approve bonds and futures, according to Caixin magazine. He joins two other CSRC officials being investigated, one of whom, Zhang Yujun, was formerly the general manager of the Shanghai and Shenzhen stock exchanges.

The securities regulator carried out unannounced inspections of several Chinese investment firms including Harvest Fund Management earlier this month, taking away hard drives and mobile phones, according to people familiar with the seizures. Police in Shanghai also confiscated computers and froze $1 billion of shares in listed companies connected to Xu Xiang, the manager of Zexi Investment known as “hedge fund brother No. 1,” who was arrested Nov. 1 on a highway between Shanghai and Ningbo.

Among Xu’s fellow money managers who performed well this year, anxiety has been palpable following his arrest,according to hedge fund manager Lu Weidong, chairman of Xinhong Investment based in China’s southern city of Dongguan. Lu’s Fuguo No. 1 fund was the best-performer among the 236 Chinese multi-strategy hedge funds from June to August, according to Shenzhen Rongzhi Investment Consultant Co., which tracks the data.

It isn’t uncommon for Chinese money managers to trade on unpublished information, according to Lu. Everybody that ever traded on such tips would “restrain themselves a bit” going forward, Lu said by phone.

“People are worried,” he said.

“The extent of this round of clampdown in the financial industry has surpassed everybody’s expectations,” Hao Hong, chief China strategist at Bocom International Holdings Co. in Hong Kong.said. “Over the longer term, the clampdown on corruption in the financial industry will level the playing field in the market for smaller investors.”

However, the arrests or investigations targeting the finance industry are creating a climate of fear among China’s finance firms and chilling their investment strategies.

China’s “Minksy Moment” – $1.2 Trillion In Ponzi Financing

Early last month in “Chinese Cash Flow Shocker: More Than Half Of Commodity Companies Can’t Pay The Interest On Their Debt,” we highlighted a report from Macquarie which showed that for many Chinese corporates, debt service payments have simply become too much to bear in the current environment.

As Macquarie put it “more than half of the cumulative debt in [the commodities space] was EBIT-uncovered in 2014, and all sub-sectors have their share in the uncovered part, particularly for base metals (the big gray bar on the right stands for Chalco), coal, and steel.”

In short, last year about CNY2 trillion in debt was in danger of imminent default.

To be sure, this shouldn’t exactly come as a surprise. Lackluster demand (both domestic and international) combined with an acute excess capacity problem and an enormous amount of leverage spells disaster and as the growing number of defaults we’ve seen in China this year underscores, Beijing’s habit of bailing out anyone and everyone and the unspoken directive that compels Chinese banks to roll bad debt may no longer be enough to keep a lid on things. Meanwhile, multiple rate cuts are proving to be too little, too late.

So what do you do when you can’t service your debt? Well, you either default or you go into full ponzi mode and take out new loans to pay the interest on your old loans. Don’t look now, but that’s exactly what’s happening in China.

As Bloomberg reports, Chinese borrowers are set to take out some CNY7.6 trillion in new loans this year just to pay interest on their existing borrowings.That’s according to Beijing-based Hua Chuang Securities Co., whose data Bloomberg used to construct the following chart:

Here’s more:

Chinese companies are struggling to generate the cash flow needed to service their obligations as economic growth slows to the weakest pace in 25 years and corporate profits shrink. While the debt burden has been eased by six central bank interest-rate cuts in 12 months and a tumble in corporate borrowing costs to five-year lows, the number of defaults in China’s onshore corporate bond market has increased to six this year from just one in 2014.

China Shanshui Cement Group Ltd. became the latest company to default on yuan-denominated domestic notes last week as overcapacity in the industry hurt profits and a shareholder dispute stymied financing. State-owned steelmaker Sinosteel Co., which pushed back an interest payment on a bond last month, postponed it again this week.

And so, as we pointed out more than 18 months ago, China is about to reach its Minsky Moment. Recall what Morgan Stanley said last March:

It is clear to us that speculative and Ponzi finance dominate China’s economy at this stage. The question is when and how the system’s current instability resolves itself.The Minsky Moment refers to the moment at which a credit boom driven by speculative and Ponzi borrowers begins to unwind. It is the point at which Ponzi and speculative borrowers are no longer able to roll over their debts or borrow additional capital to make interest payments. Minsky states this usually occurs when monetary authorities, in order to control inflationary impulses in the economy, begin to tighten monetary policy. We would add that this monetary tightening often begins to occur at the time when the size of speculative and Ponzi borrowings have become so large that the demand for additional capital to keep these borrowers afloat becomes greater than the supply of such capital. We believe that China finds itself today at exactly this juncture.

To be sure China is is certainly doing its best to forestall this eventuality. The PBoC for instance, is not seeking to tighten monetary policy and deflation is a bigger risk than inflation. Additionally, the local government debt swap program is a sweeping effort to address provincial governments’ inability to make interest payments on LGVF financing which in many cases came with punitive rates.

So while we may not have reached the breaking point just yet (i.e. the point at which borrowers can no longer obtain new financing to pay the interest on their existing obligations), we’re getting there and were it not for the flood of liquidity (the tightening effect of PBoC FX interventions notwithstanding) unleashed by a series of RRR cuts and the implementation of various short- and medium-term lending ops, China probably would have gone over the edge long ago. For a preview of what comes next (and some of what you’ll read below is already happening), here’s Morgan Stanley again:

The unwind of this credit boom is likely in progress, and we expect it to pick up speed over the coming months and quarters. It will likely involve a steady drip of defaults and near-defaults as insolvent borrowers finally become illiquid. Market rates for all assets except central government bonds and central bank bills will likely continue to rise, reflecting increasing market fears of default by shaky borrowers. Asset values will likely begin to deteriorate as stressed borrowers attempt to sell assets to stay afloat. As a result, banks and other financial entities could begin to increase provisioning for bad debts and to reduce credit availability by gradually tightening credit standards. This could lead to a credit crunch where credit to the economy is choked off for all but the safest borrowers.

Xi’s determination to show the world that China is set to liberalize capital markets will only serve to accelerate this dynamic as a free(er) market means allowing for more defaults.

You were warned.

We close with a quote from Shi Lei, the Beijing-based head of fixed-income research at Ping An Securities Co. who spoke to Bloomberg and who we imagine may be “summoned” for daring to offer the following assessment of the situation:

“Some Chinese firms have entered the Ponzi stage because return on investment has come down very fast. As a result, leverage will be rising and zombie companies increasing.”

In $64 Billion Bust, China Nabs “Underground Bank” Kingpin

Late last month, we introduced you to “Mr. Chen”, a catch-all for the operators of tiny storefronts and kiosks in China who can either get you some tea and a Snickers bar, or smuggle millions out of the country, whichever you prefer.

“Mr. Chen” is part and parcel of China’s vast underground bank network which Chinese use to circumvent Beijing’s capital controls.

Officially, you’re only allowed to move $50,000 per year out of China, but there are any number of ways to get around that limit. One popular method – until Xi began to crack down that is – was the UnionPay end-around, which entails making what amounts to a fake purchase for something like, say, an expensive watch, and receiving cash from the merchant instead of merchandise. The underground bank method is more complex than that, but not by much. As WSJ explained in October, “large sums are divided into legally allowed amounts and then channeled out of the mainland via hundreds of bank accounts controlled by the underground banker.” Alternatively, “underground banks can match yuan deposited with them on the mainland with equivalent amounts in foreign currency paid into a client’s bank account elsewhere:Give the underground bank a sum, and a matching sum appears in Hong Kong, minus a cut of anywhere between 0.3% and 3%. No money physically or electronically crosses the border; the match is built on networks on both sides controlled by the underground bank.”

As we mentioned earlier this month when, courtesy of Bloomberg, we presented “5+1 Ways To Smuggle Billions Out Of China,” this is an underground business and so things don’t always go as planned, something a “Mr. Chan” (with an “a”) discovered when he attempted to move CNY63 million out of the country via “Mr. Chen” (with an “e”) only to find that once the transaction was complete, he only had CNY8 million left. That’s a pretty hefty fee even in the world of money laundering and so, Chan reported “Chen” to the authorities. The subsequent investigation led to the arrest of some 31 people and netted 1,087 accounts holding some CNY12 billion.

Those arrested were never heard from again.

Well, we’re not sure if some other “Chan” got robbed and subsequently ratted on “Chen”, but whatever the case, Chinese authorities have broken up another underground bank – more specifically, the largest such operation in the country which allegedly handled some $64 billion in illicit FX transactions.

As Bloomberg reports, “more than 370 people have been arrested or face lawsuits or other punishment in the case centered in eastern Zhejiang province.” According to the details from Xinhua, it took police more than a year to sort the whole thing out, but by the time it was all said and done, 1.3 million transactions were scrutinized and 3,000 accounts were frozen. According to Jinhua City Public Security Bureau of Economic Investigation Detachment Vice Captain Zhang Hui, it took 35,000 sheets of paper to print out all of the evidence.

The group’s “Mr. Chen” is a guy called Zhao Mouyi, and as Bloomberg goes on to detail, he “set up more than 10 companies in Hong Kong from 2013 and transferring more than 100 billion yuan through so-called non-resident accounts, which are used by offshore companies in China when they are transferring money abroad.”

Amusingly, HSBC – the global bastion of money laundering – assissted Zhao in exchanging yuan for foreign currency. Here’s the account from The People’s Daily (Google translated):

Hui said that unlike traditional underground banks by domestic and foreign “knock” level account transfer of funds approach, this is the first case of the use of the case to commit the crime of domestic accounts NRA found that the use of NRA accounts management loopholes and no foreign exchange purchase limit features, bypassing the foreign exchange regulation, the RMB cross-border transfer accounts directly through the NRA, hit the accounts provided by the “customer” in the settlement after HSBC and other banks.

Well, if you’re going to launder money (because that’s basically what this is… you’re taking an illicit sum and via a series of transactions rendering it free and clear) we suppose you might as well go with the guys who have the most experience.

HSBC didn’t comment.

We suppose the only question now is whether anyone will ever hear from “Zhao” or any of his accomplices again.

You can expect this crackdown to continue unabated. The market believes (rightly) that Beijing is targeting a much larger deval going forward as the economy continues to falter. That means the pressure on the yuan isn’t likely to dissipate in a meaningful way. Indeed, as Goldman noted a few days ago, based on the sum of outright spot transactions and freshly entered (but unsettled) forward contracts, FX outflow was about US$26bn in China during October, composed of US$24bn in net outright spot transactions and US$2bn via net forward transactions. In other words: capital is still flowing out of China.

As long as the pressure on the yuan is there, “Mr. Chen” will be around, white-haired, peering out from behind the candy and trinkets – and Xi will keep trying to stop him.

P.S. If you need to get money out of China and Chen isn’t your style, there’s always bitcoin…

end

EUROPEAN AFFAIRS

Early this morning: 3 am est 9 am local time

(courtesy zero hedge)

Euro Tumbles As Draghi Says “ECB Will Do What It Must To Raise Inflation” But Drop May Not Last

Yesterday, there was pent up expectation that the ECB’s latest minutes, by being structurally dovish and thus the opposite of the Fed’s own minutes, would unleash another round of EUR weakness. This did not happen, and instead not only did the EUR jump during the day, but the USD saw an unexpected round of all day weakness. Many were surprised by this response. It turns out Mario Draghi was merely biding his time, and in a speech released moments ago, titled “Monetary Policy: Past, Present and Future” delivered at the European Banking Congress, Draghi pulled another “whatever it takes” card, and promptly sent the Euro currency reeling, if only for the time being.

Here are the key highlights:

- DRAGHI SAYS ECB WILL DO WHAT IT MUST TO RAISE INFLATION QUICKLY

- DRAGHI: ECONOMY NEEDS MORE AID IF RECOVERY NOT SELF-SUSTAINING

- DRAGHI: BALANCE OF RISKS TO PRICE STABILITY SKEWED TO DOWNSIDE

Some of the key excerpts:

- “If we decide that the current trajectory of our policy is not sufficient to achieve that objective, we will do what we must to raise inflation as quickly as possible. That is what our price stability mandate requires of us,” ECB President Mario Draghi says in speech in Frankfurt.

- “In making our assessment of the risks to price stability, we will not ignore the fact that inflation has already been low for some time”

- “If we conclude that the balance of risks to our medium- term price stability objective is skewed to the downside, we will act by using all the instruments available within our mandate”

- “Low core inflation is not something we can be relaxed about, as it has in the past been a good forecaster for where inflation will stabilise in the medium-term”

- “The question we face now is not therefore whether we have the tools available to provide the appropriate degree of monetary stimulus. We have proven that. The question is one of calibration”

“Moar” is coming:

“growth momentum remains weak and inflation remains well below our objective of below but close to 2%.“

Much “moar”:

“The Governing Council is committed – unanimously – to using both unconventional and conventional instruments to deal effectively with the risks of a too prolonged period of low inflation.”

For those who skip straight to the conclusion, it doubled-down:

“So let me reiterate what I said here last year: if we decide that the current trajectory of our policy is not sufficient to achieve that objective, we will do what we must to raise inflation as quickly as possible. That is what our price stability mandate requires of us.”

The impact on the Euro was predictable:

… But the reaction may be shortlived. Here is CA’s Valentin Marinov explaining why:

So we got yet another ‘…do what it takes speech’ by Draghi. I guess the expression was put in there to evoke the spirit of the, by now, famous speech from July 2012, which helped to solve the sovereign debt crisis.

EUR went promptly lower presumably on the back of Draghi’s signal that the ECB will do what it must to lift the EZ inflation quickly. For some that maybe the tantamount of aggressive easing on December 3. The thing is, however, there is not much new in there to suggest that the ECB will actually exceed the already dovish market expectations.

Indeed, it seems that, by now, everyone we talk to is expecting a 10bps deposit rate cut and QE-extension (even an increase in the monthly purchases). I am struggling to see how the ECB will exceed the already dovish expectations. In addition, one potential mistake people are making thinking about the ECB is that they will go and fire their bullets in one go. I disagree with that. I think that they realize this is a long-term process and they don’t want to corner themselves like the BoJ by acting too aggressively.

I was also thinking about how people like to compare EUR and JPY all the time. By implication, they like to think of ECB QE2 as having the same impact on EUR as it BoJ QE2 had on JPY. I think that there are at least two important differences there:

1/ The BoJ QE2 came on the back of the GPIF reform which had set in motion a massive outflows abroad

2/ Europe is far behind Japan in terms of institutional set up to support the so called EUR-funded carry trades. In other words there are no uridashi bonds or double decker funds for the EZ investors to export EUR. These have been available in Japan for years

Our call for EUR/USD is a grind lower from here towards the lows of the year. I think, however, extreme moves on the downside maybe less likely for now

end

The German Bund is now deeply into the negative at -.39% as the world believes the only way that Draghi can get inflation going is to monetize more debt. The deeper into the negative makes it more difficult for Draghi to find enough bonds (bunds) to monetize.

(courtesy zero hedge)

German Bunds Give Draghi The Finger: 2-Year Hits Record Negative Low -0.39%

As we reported moments ago, Mario Draghi just unleashed another “whatever it takes” speech, this time focusing on the ECB’s fight with the “deflation monster” and explaining how the central bank plans to boost inflation and inflation expectations, saying that “while inflation will remain low for a prolonged period, we see it gradually rising back to 2%. The delay is largely explained by the impairments in the transmission mechanism that lengthen the lag between our accommodative policy stance and price developments.”

And while the initial EUR response was as expected, dropping about 30 pips (but already rebounding on concerns that the Draghi bazooka may truly be empty this time – after all what else can he surprise with as CA’s Valentin Marinov said), German Bunds, especially the short-end, were quick to give Mario Draghi the middle finger and the 2Y has dropped to a quite deflationary all time record low of -0.389%, because all they heard was that the ECB will monetize even more debt.

And a longer view:

However, as a reminder, the ECB has a monetization floor: recall “purchases of nominal marketable debt instruments at a negative yield to maturity are permissible as long as the yield is above the deposit facility rate.”

In fact, based on recent calculations some 30-40% of the entire German curve is now trading with too negative yields to be eligible for the ECB’s current formulation of QE, and we don’t have to remind readers that the biggest risk the ECB’s QE faces is running out of eligible securities it can purchase. The private market is scarce enough as is, and explains why Europe is desperate to find politically correct ways to issue much more debt (hint: refugee crisis).

In effect what the German short end is saying is that not only will the ECB slash the deposit rate, from -0.20% to as low as -0.40% or more, but that another massive wave of QE will be unleashed. What this means, of course, is that the ECB will also unleashe another massive deflation-exporting tsunami, which in turn will force not only Japan and China, but soon, the Fed as well, to respond in kind and expand their own “unconventional monetary policy measures” because in the race to the bottom, all that matters is if just one central bank is doing it.

Finally, as for Draghi’s contention that more negative rates will stop savers from hoarding money at the bank, he is as usual, completely wrong: as the actual data shows, what happens is that the lower the deposit rate across Switzerland, Denmark and Sweden, the greater the eagerenss of savers to, well, save instead of spend.

end

Glencore falls to 91 pence today, putting tremendous pressure on their derivatives.

(courtesy LSE/Harvey)

GLEN GLENCORE PLC ORD USD0.01

| Price (GBX) | 92.33 | Var % (+/-) | -1.83% ( |

| High | 97.44 | Low | 91.77 |

| Volume | 72,137,178 | Last close | 92.33 on 20-Nov-2015 |

| Bid | 92.14 | Offer | 92.17 |

| Trading status | Market Close | Special conditions | NONE |

end

Europe is set to outlaw Bitcoin and any virtual currency:

(courtesy zero hedge)

Europe Cracks Down On Bitcoin, Virtual Currencies To “Curb Terrorism Funding”

In the past we have explained why when it comes to circumventing capital controls, primarily in the context of China, there are few as simple and as efficient alternatives to Bitcoin – contrary to what Bernanke may think, gold is concentrated money (and in India it now pays interest) but when it comes to transferring it across borders, it tends to be rather problematic. And now Europe appears to have figured this out, and as Reuters reports, European Union countries are preparing to crackdown on virtual currencies such as bitcoin, and anonymous payments made online and via pre-paid cards “in a bid to tackle terrorism financing after the Paris attacks, acording to a draft document.”

Just a week after the Paris terrorist attack, showing a dramatic ability for coordinated work by a continent that is known for anything but, today EU interior and justice ministers are gathering in Brussels for a crisis meeting called after the Paris carnage of last weekend. This happens days after the European Commission already announced it would make procurement of weapons across Europe virtually impossible, if only for citizens who wish to obtain protection legally.

According to Reuters, the justice minister will urge the European Commission, the EU executive arm, to propose measures to “strengthen controls of non-banking payment methods such as electronic/anonymous payments and virtual currencies and transfers of gold, precious metals, by pre-paid cards,” draft conclusions of the meeting said.

Conveniently, Reuters reminds us that “Bitcoin is the most common virtual currency and is used as a vehicle for moving money around the world quickly and anonymously via the web without the need for third-party verification. Electronic anonymous payments can be made also with pre-paid debit cards purchased in stores as gift cards.”

But no more: “EU ministers also plan “to curb more effectively the illicit trade in cultural goods,” the draft document said.”

And with all of Europe sliding ever deeper into negative rates, and where a ban on cash bank notes is an all too realistic possibility, the easiest mechanism to evade the ECB’s creeping financial oppression is about to be made illegal.

Finally, there was no word about the true source of terrorism funding: those mysterious “third parties” which keep pumping the Islamic State with hundreds of millions in cash in exchange for its crude oil. Perhaps Europe is so unwilling to dig down into this most important question (which as we said last night nobody is willing to ask) because it either already knows the answer, or realizes that the people implicated just may be some of the wealthiest and most respected Europeans, and the resulting stench could spread all the way to the various unelected politicians and ex-Goldmanite central bankers?

EU’s Founding Treaty To Be “Reconsidered”, Seeking End To Passport-Free Travel

Between the French (Interior Minister Cazeneuve: “we’re face with a new kind of terrorism”, and Hungary (PM Orban: “allowing people into our own back yard” who may then commit acts of terrorism was irresponsible), AP reports that the EU’s founding treaty with regard to passport-free travel – the so-called Schengen Agreement – is to be reformed. “We want Europe, which has lost too much time on a certain number of questions, to note the urgency and take decisions today,” exclaimed Cazeneuve, with Orban adding “the founding treaty is currently an obstacle to this and I believe it needs to be reconsidered.” According to Cazeneuve, the reforms will happen by year-end.

AP reports The Schengen Agreement is to be reformed..

- *EU SEEKING CHANGE TO PASSPORT-FREE BORDER AREA RULES, AP SAYS

Member states must fully apply the rules of the border-free Schengen zone to carry out systematic controls on EU citizens at the bloc’s external borders, he says, adding, “It’s not an option, it’s an obligation.”The bloc’s internal and justice ministers have also requested a strengthening of the existing Schengen rules, he adds.The move is one of several aimed at “considerably reinforcing our tools in the fight against terrorism,” Schneider says.

- *CAZENEUVE: WE’RE FACED WITH A NEW TYPE OF TERRORISM

- *CAZENEUVE: FRANCE TO KEEP CONTROLS AS LONG AS THREAT REMAINS

- *CAZENEUVE: DRAFT SCHENGEN REFORM PLAN SEEN BY YEAR END

On one hand, “we cannot close Europe,” de Maizière said in an interview on Friday with the Washington Post.

But on the other hand, “we cannot open Europe totally for millions and millions of poor people in the world or even for all of those coming from conflict zones. Impossible,”he stated, calling for a change to the European refugee system.

Berlin intends to slash cash benefits to refugees, providing them with food instead, and engage in a “reunification of families” practice, promising “years” of efforts to those who would like to bring their relatives to Germany after settling there with refugee status.

“The number is too big,” the official said. “It has to be checked.”

And as MTI reports, Hungary’s Orban is calling for more aggressive external borders also...

The European Union’s founding treaty should be reconsidered, Prime Minister Viktor Orban said after meeting Macedonian counterpart Nikola Gruevski on Friday.

The prime minister said European should face up to the fact that migrants come from areas involved in military conflict with EU members. “We are considered enemies in those countries, and the acts of terror committed in our areas are considered war successes over there”, he said, adding that “allowing people into our own back yard” who may then commit acts of terrorism was irresponsible.

The EU should protect its borders, culture, economic interests and its democracy, Orban said.

“The founding treaty is currently an obstacle to this and I believe it needs to be reconsidered,” Orban said.

In order to make Europe effective, basic questions need to be reevaluated, he added. It is increasingly obvious that the EU is capable only of responding to crises rather than taking preventive measures. Citing the Paris terror attacks, he said it was only afterwards that European politicians started assigning security its proper role.

Orban said it was the British who first pushed the issue in connection with the EU’s founding treaty, and they want to make changes to European regulations that will be impossible without amending them.

In response to a query about whether he considered the Schengen system dead, similarly to the Dublin agreement, he said “Dublin is dead, Schengen is alive”. An increasing number of EU countries neglect the Dublin agreement but everybody is trying to uphold Schengen because if it fails then “walls and fences will rise and border controls will be put in place between countries where they have not been used.” The possibility of free travel between Schengen members needs to be maintained, and this is only possible if external Schengen borders are protected, he added.

“One should either be a Schengen member and protect its borders or if they do not protect the borders, they should not be a Schengen member,” Orban said.

* * *

As we detailed repviously, on The Future of Schengen

The European Union probably will not abandon the Schengen Agreement anytime soon. Despite the criticisms, the treaty has reduced the time and cost of moving goods across Europe because trucks no longer have to wait for hours to cross an international border. It also benefits tourists and people living on border towns, because passports and visas are no longer needed. Finally, the agreement allows countries to save money, because governments no longer need to patrol their land borders.