Gold: $1063.80 down $2.00 (comex closing time)

Silver $14.05 unchanged

In the access market 5:15 pm

Gold $1058.50

Silver: $14.08

At the gold comex today, we had an extremely poor delivery day, registering 38 notices for 3800 ounces. Silver saw 534 notices for 2,670,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 200.45 tonnes for a loss of 103 tonnes over that period.

In silver, the open interest fell by 2258 contracts despite the fact that silver was up by 4 cents with respect to yesterday’s trading. Generally we are witnessing a massive OI contraction once we approach the first few days of an active delivery month and they did not disappoint us today.. The total silver OI now rests at 162,306 contracts In ounces, the OI is still represented by .813 billion oz or 116% of annual global silver production (ex Russia ex China).

In silver we had 534 notices served upon for 2,670,000 oz.

In gold, the total comex gold OI fell by 4,123 contracts as the OI fell to 392,672 contracts even though gold was up by $9.60 with respect to yesterday’s trading.

We had no change in gold inventory at the GLD/ thus the inventory rests tonight at 654.80 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver, we had a huge addition of 1.144 million oz in silver inventory, / Inventory rests at 319.353 million oz.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fall by 2258 contracts down to 162,306 despite the fact that silver was up in price to the tune of 4 cents with respect to yesterday’s trading. The total OI for gold fell by 4123 contracts to 392,672 contracts despite the fact that gold was up by $9.60 with respect to yesterday’s trading.

(report Harvey)

2 Gold trading overnight, Goldcore

(Mark OByrne)

3. ASIAN AFFAIRS

ii) Europe’s very large Bluecrest hedge fund is calling it quits (almost) as 8 billion of its 9 billion in assets is being returned to shareholders. They just cannot make money!

ii) Egypt set to replace Turkey in supplying the Russian market with fruits and vegetables

ii) Canada’s GDP plunges by .5% month over month as the oil industry suffers greatly. You will see this happening to commodity countries all over the world. The reasons for the global plunge is malinvestment caused by massive printing out money which was then used to produce overcapacity

i)Can we blame the low price on oil on hedge funds

(McDonald/OilPrice.com)

ii) WTI falls as API reports another surprise inventory rise:

ii) How premiums on silver and gold bullion are calculated.

iii) Huge USA gold eagle sales and now silver sales at record levels

viii) The way bond yields have been rising indicates that if the Fed does raise rates it is policy error. Also take a look at the number of shorts on the 10 year bond. These guys have loaded the boat to one side expecting a rate hike (they went short on bonds). If it does not occur, the boat will capsize and the shorts will drown.

(courtesy zero hedge)

ix(What on earth is happening with the huge increase in USA debt!! We know that when the USA were operating under emergency measures to avoid a breach of the debt ceiling, they borrowed from Federal pension account funds. When they signed their new debt ceiling a total of 339 billion in debt was added to the previous level which is what was expected.

Let us head over to the comex:

The total gold comex open interest fell to 392,672 for a loss of 4123 contracts despite the fact that gold was up by $9.60 with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month and we are certainly witnessing both of those today. We are now entering the big December contract which saw it’s OI fall by a considerable 2018 contracts from 7849 down to 5831 contracts. We had only 2 notices filed upon yesterday, so we lost 2016 contracts or 201,600 oz of gold that will not stand for delivery in this active delivery month of December. As we indicated to you on many occasions, the bankers are cash settling as they do not have physical gold to settle upon.The next contract month of January saw it’s of rise by 67 contracts up to 566. The next big active delivery month is February and here the OI fell by 4,370 contracts down to 278,253. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 162,654 which is poor. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was very poor at 128,152 contracts.

December contract month:

INITIAL standings for DECEMBER

Dec 1/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 66,997.610 oz

HSBC |

| No of oz served (contracts) today | 38 contracts

3800 oz |

| No of oz to be served (notices) | 5793 contracts

(579,300 oz) |

| Total monthly oz gold served (contracts) so far this month | 40 contracts(4000 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | nil oz |

Total customer deposits 66,997.610 oz

we had 3 adjustments:

i) Out of Brinks: 3,641.600 oz was adjusted out of the dealer and this landed into the customer account of Brinks

ii) Out of Delaware: 578.700 oz was adjusted out of the dealer and this landed into the customer account of Delaware

iii) Out of Scotia: 9,689.41 oz was adjusted out of the dealer and this landed into the customer account of Scotia

:

DECEMBER INITIAL standings/First day notice

Dec 1/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 600,226.26 oz

(,Scotia), |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 600,725.97 oz

CNT |

| No of oz served today (contracts) | 534 contracts

2,670,000 oz |

| No of oz to be served (notices) | 708 contracts

(3,540,000 oz) |

| Total monthly oz silver served (contracts) | 3280 contracts (16,400,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 600,226.26 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

we had no dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposit:

i) into CNT: 600,725.97 oz

total customer deposits: 600,725.97 oz

total withdrawals from customer account: 600,226.26 oz

Nov 16.And now SLV/another huge addition of 2.145 million oz into the silver inventory of SLV/rests tonight at 317.256 million oz

Nov 15/no change in silver inventory at the SLV/inventory 315.111 million oz/

U.S. Mint Gold Eagles See Sales Surge, Silver at Record

“The U.S. Mint’s sales of American Eagle coins surged in November, with gold nearly tripling month-over-month and silver already reaching a new annual record as bullion prices fell to multi-year lows” reported Reuters.

The mint sold 97,000 ounces of American Eagle gold coins in November, up 185 percent from October and 62 percent higher from a year ago, after selling out of most of the 2015-dated coins as falling bullion prices attracted buyers.

Strong demand came as spot gold XAU= prices fell around 7 percent to the lowest in nearly six years. This was the gold market’s biggest monthly drop in 2-1/2 years as traders and investors widely anticipated that the U.S. Federal Reserve will raise interest rates at its next meeting in mid-December.

Higher interest rates raise the cost of holding non-yielding gold.

Toward the end of this month, the mint said it had sold out of all remaining 0.1-ounce, 0.25-ounce and 1-ounce American Eagle gold bullion coins dated 2015 and would not be making any more for the calendar year.

Demand for American Eagle silver coins has also been strong, with year-to-date sales already reaching an annual record at 44.67 million ounces, breaking the full-year record of 44 million ounces in 2014.

Prudent bullion buyers continue to accumulate gold and silver bullion coins and bars on price weakness.

DAILY PRICES

Today’s Gold Prices: USD 1069.25, EUR 1009.25 and GBP 708.55 per ounce.

Yesterday’s Gold Prices: USD 1055.65, EUR 998.20 and GBP 703.05 per ounce.

(LBMA AM)

Gold in EUR – 1 Year

Gold closed at $1065.00 yesterday, down by $6.40. Silver fell by a cent to close at $14.09. Platinum lost again, down by $5 to $828.

Comex Conundrum

For a fair and honest market, the latest developments might be significant and noteworthy, perhaps even troublesome. But remember, we’re not talking about a fair and honest market, we’re talking about The Comex, instead.

As the “delivery month” of December begins on the Comex…and before we begin another exercise detailing what a sham, charade and illusion this all is…please take a few moments to review the links below. This is hardly the first time we’ve tried to draw attention to all of this and it likely won’t be the last:

- http://www.tfmetalsreport.com/blog/7115/comex-delivery-charade

- http://www.tfmetalsreport.com/blog/7241/futures-market-fraud

- http://www.tfmetalsreport.com/blog/7249/bullion-bank-leverage-soars-near-3001

Again, the only reason that the Comex price for gold (and silver) has any relevance whatsoever is the alleged physical delivery that takes place at the price “discovered” through the trading of paper derivatives. Without physical delivery, the only “price” that is being discovered is the price of the paper derivative contract, itself. Thus, physical delivery is what gives relevance to the paper derivative price.

So, what happens when the Comex “delivery” process is exposed as a fraud, an illusion and a charade? Does this mean that the Comex paper derivative price can no longer be the basis for physical pricing worldwide? YES IT DOES! That, my friend, is the reason we so diligently chronicle this stuff month after month. And, boy oh boy, it sure looks like December 2015 is going to be a doozy.

The actual delivery phase of the December Comex gold contract began back on Friday when the Dec15 futures contract “expired”. Though it still trades through December, as of today (Monday) any entity still holding a Dec15 contract had to supply 100% margin for the full cost of the contract or about $107,000. Why? Because, as a long holder of a contract in its delivery period, you are subject to having the metal delivered to you at any time and, at a price of $1070/ounce, 100 ounces will cost you $107,000.

But the Comex market isn’t about delivery, it’s about paper derivative trading. So, by the close of business last Friday, nearly all traders had liquidated their Dec15 contracts and rolled them into the next “front month”, which is the Feb16. However, some contracts always remain open at “expiration” and a few of these actually look to “stand” and “take delivery”. For Comex gold, here’s how it has played out in 2015:

CONTRACT MONTH TOTAL OPEN AT EXPIRATION TOTAL DELIVERIES MADE

DEC14 11,507 3,381 or 29.4%

FEB15 8,455 1,174 or 13.9%

APR15 7,348 2,801 or 38.1%

JUN15 8,380 2,959 or 35.3%

AUG15 9,215 5,113 or 55.5%

OCT15 3,092 950 or 30.7%

DEC15 7,849 ?

Note the outlier and dramatic dropoff of total deliveries back in October. This was likely due to the fact that October is typically the lowest volume delivery month of the year. However, recall that total Comex registered gold has been falling to new alltime lows as 2015 progressed, too. Could this be having an impact?

Here are some random CME Gold Stocks reports. Check the date and the amount of gold listed as registered and available for delivery.

This from December of last year. Enough gold for 7,378 deliveries (if deliveries were actually made):

This from February of this year. Enough gold for 8,099 deliveries:

This from last April. Enough gold for 6,031 deliveries:

This from August. Now only enough gold for 4,888 deliveries:

And, uh-oh, this from October. Only enough gold for 1,616 deliveries. Good thing only 3,092 stood and just 950 total deliveries were made, huh?

So now here we are. The biggest and typically busiest delivery month of the year (December) is upon us and, at expiration last Friday, the Comex still had 7,849 contracts open and standing. And how many ounces of registered gold are currently available within the Comex vaulting system? As of today, total registered gold has fallen to a new all-time low of 134,877 ounces or enough gold to physically settle just 1,348 contracts!

See what I mean? What a conundrum! IF The Comex truly was a free and fair market and IF actual physical metal deliveries were taking place to “back up” the paper derivative price, The Banks and The Exchange would be in a bit of a jam. From where would they find the gold needed to physically settle all of those seeking delivery?

Ah, but no worries, I’m sure that the month of December will pass without any issues. There will be some small journal entry movements of gold back and forth between the categories and between The Banks. But no real gold will move and no real crisis will emerge. Instead, it will just be business as usual and CNBS, BBG et al will keep reporting the Comex paper price as the true “price” and “value” of gold.

And this draws us back to the questions posed at the beginning of this post:

- So, what happens when the Comex “delivery” process is exposed as a fraud, an illusion and a charade?

- Does this mean that the Comex paper derivative price can no longer be the basis for physical pricing worldwide?

The answer earlier was an emphatic “YES IT DOES!” and that’s still the case. You, as a gold investor, need to understand this important point. One day soon, this current paper derivative and fractional reserve bullion banking pricing scheme will fail. Maybe not this month and maybe not in 2016, either. But fail it will.That much is a certainty. And when it does, gold will have to be priced based upon physical availability at the offer. Call me crazy, but I suspect that physically-discovered price is going to be considerably higher than the one discovered through the current paper derivative system, a scheme that levers physical gold into paper at a ratio of nearly 300:1. How much higher will the new price be? Hmmm…well let’s just say that it’s not going to be $1070/ounce, that’s for sure.

Therefore, prepare accordingly.

TF

The Comex Is A Zombie Market: Hedge Funds Record Short Paper Gold

December 1, 2015Financial Markets, Gold, Market Manipulation, Precious Metalsbullion banks, Comex gold shorts, COT report, economic collapse, Goldman Sachs, JP Morgan, stock market crash

Gold didn’t “hit a low,” it was driven down by the bullion banks who are agents of the Fed, acting on the Fed’s orders…the price of gold is not determined in the market in which gold actually gets bought and sold, it’s determined in a paper futures market in which the contracts are settled in cash. – Paul Craig Roberts on King World News

The Comex is like a grade-B horror movie – night of the living dead. Zombies that wreak havoc on society but can’t be destroyed. The Comex is the consummate symbol of the United States. It embodies extreme fraud, corruption, wealth theft, market manipulation, regulatory capture, etc. It is the ultimate manifestation of the end of Rule of Law in this country.

Last week the “managed money” hedge fund segment of the Comex took on a record net short position in Comex paper gold. As reported to the CFTC from the CME bullion bank trading reports, hedge funds are now net short over 16,000 contracts representing over 1.6 million ozs of paper gold – over 46 tons. Conversely, the “swap dealer” segment – otherwise known as the bullion banks – have assumed a record net long position of 29.5k paper gold contracts.

Now, assuming we accept the COT report prima facie – and this can be a problematic assumption considering that the data originates from the highly corrupted bullion banks – whenever the hedge fund trader class net position has reached an extreme level in either direction, and the banks take the other side of that position, the price of gold has always eventually moved inversely to the hedge fund positioning.

Meanwhile, the amount of gold that has been declared to be available for delivery into contracts standing for delivery has diminished down to 138k ozs as of last Friday. Against the net short of the hedge funds, this implies that the hedge funds are short 11.5 ozs of paper gold for every ounce of real gold made available for delivery. If this ratio of paper to the real underlying commodity developed in any other commodity market the CFTC would step in an enforce laws on the book designed to prevent this type of market manipulation.

The reason I now reference the Comex as a “Night of the Living Dead” zombie market is because this trading pattern between the bullion banks and the hedge funds has been in repetition since at least the time I began my involvement in the precious metals market nearly 15 years ago. It never received the kind of attention it gets now until after the big smash started in 2011. By then it was too late because the CFTC, SEC, Justice Department and Oval Office advisory staff had been stuffed with Wall Street’s emissaries, primarily of the Goldman Sachs and JP Morgan variety. It’s Wall Street’s version of using pedophiles to supervise the daycare school.

Based on history, it would appear that the hedge fund/swap dealer net position is indicating that the price of gold may be in for a wild ride higher at some point. But don’t expect this to happen immediately. I expect the hedge funds to get aggressive in trying to push the price of gold lower in order to “harvest” their short position. I mentioned to colleagues last week that this would explain the erratic, volatile intra-day moves in the price of gold we started to see recently.

Today is a good example, as gold traded up overnight – in the Asian physical markets referenced at the top by Dr. Roberts – only to be smashed just before data was released showing a collapse in U.S. manufacturing – data that should have been bullish for gold. However, if you want to trade on the side of the Government insiders – the bullion banks – now is a good time to buy the price smacks and sell the ensuing push higher. At some point the banks will decide to fleece the hedge funds once again and take the price of gold higher, forcing the hedge fund black boxes to cover their shorts.

Wash, rinse, repeat. You may ask yourself, how do you kill a zombie? As a market for the trading of physical gold and silver, the Comex is already dead. At some point, the entities who have stuck around to try their hand the rigged paper game will either go broke or simply fade away. At that point, the bullion banks will be left to play only with themselves. But at that point in time I suspect the U.S. economic, financial and political system will be in a full blown collapse.

***

end

How are silver and gold bullion premiums calculated?

Submitted by cpowell on Tue, 2015-12-01 01:58. Section: Daily Dispatches

8:58p ET Monday, November 30, 2015

Dear Friend of GATA and Gold:

Our friends at J.M. Bullion in Dallas have constructed an interesting and elaborate graphic describing how premiums on gold and silver coins and bars are calculated. The graphic is titled “How Are Silver and Gold Bullion Premiums Calculated?” and it’s posted at the company’s Internet site here:

http://www.jmbullion.com/how-are-premiums-calculated/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

U.S. Mint American eagle gold coin sales surge, silver at record

Submitted by cpowell on Tue, 2015-12-01 02:24. Section: Daily Dispatches

From Reuters

Monday, November 30, 2015

The U.S. Mint’s sales of American Eagle coins surged in November, with gold nearly tripling month over month and silver already reaching a new annual record as bullion prices fell to multi-year lows, data released today showed.

The mint sold 97,000 ounces of American Eagle gold coins in November, up 185 percent from October and 62 percent higher from a year ago, after selling out of most of the 2015-dated coins as falling bullion prices attracted buyers.

Strong demand came as spot gold prices fell around 7 percent to the lowest in nearly six years. This was the gold market’s biggest monthly drop in 2 1/2 years as traders and investors widely anticipated that the U.S. Federal Reserve will raise interest rates at its next meeting in mid-December. …

… For the remainder of the report:

http://www.reuters.com/article/2015/11/30/us-usmint-coins-idUSKBN0TJ2SY2…

end

A great commentary on the huge demand for silver coins around the world

(courtesy Steve St Angelo/SRSRocco report)

Record Silver Coin Demand Signals Financial Trouble Ahead

by SRSroccco on December 1, 2015

The world doesn’t realize it, but record global silver coin demand is warning that big trouble is coming to the financial system. More investors are waking up to the fact that there is something seriously wrong with the financial industry and broader stock markets and are buying more physical gold and silver than ever.

This is especially true for silver. During the huge surge in physical silver investment demand from June to September this year, I heard from several dealers that investors were buying a lot more silver than gold. And this wasn’t just from the typical Mom & Pop buyers… there were large silver volume purchases from wealthy clients.

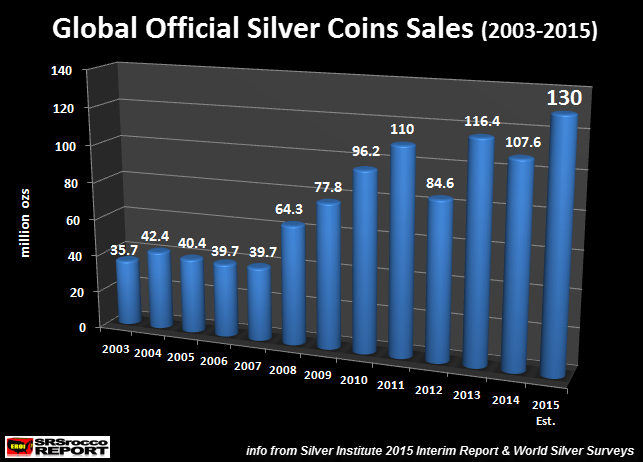

According to the Silver Institute 2015 Interim Report, total sales of official silver coins will reach 130 million oz (Moz) this year. If we look at the chart below, we can see the huge increase in official coin sales since the first collapse of the U.S. Investment Banking and Housing Industry in 2008:

Global Official Silver Coin sales ranged between 35.7 Moz and 42.4 Moz from 2003 to 2007. However, demand surged to 64.3 Moz during the 2008 financial crisis and continued to increase to 110 Moz in 2011 when the price of silver peaked at $49. Then in 2012, as investors were unsure of the silver price trend, Official coin sales declined to 84.6 Moz that year.

Well, this all changed in 2013 as the price of silver fell from $30 down to $18 in just six months, motivating investors to purchase a record 116.4 Moz of official silver coins. Even though demand fell modestly in 2014, official silver coin sales are forecasted to hit a record 130 Moz this year.

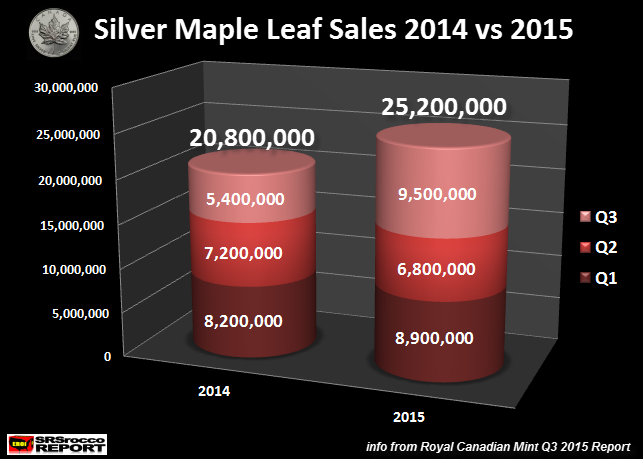

Royal Canadian Mint Silver Maple Leaf Sales Hit Record Q1-Q3 2015

The Royal Canadian Mint just released their newest Q3 Report showing a huge increase in Silver Maple sales to 9.5 Moz, up 76% compared to 5.4 Moz during the same period last year:

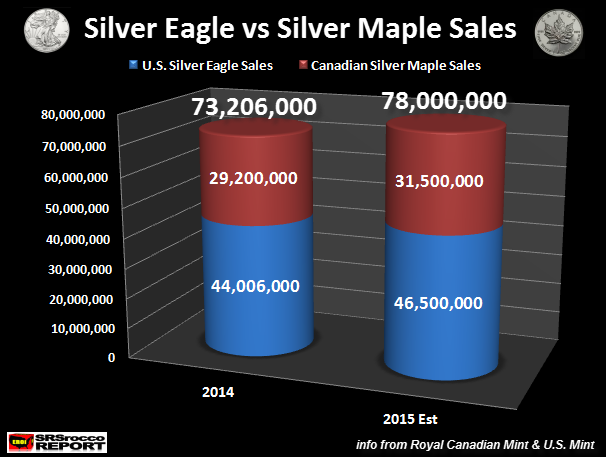

Total Silver Maple sales Q1-Q3 are 25.2 Moz versus 20.8 Moz last year… up 21%. Here is my forecast for total 2015 Silver Eagle and Maple sales:

As we can see, Silver Eagle and Maple Leaf sales are estimated to reach 78 Moz compared to 73.2 Moz last year. This is one hell of a lot of 1 oz silver coins from just these two mints. Furthermore, total sales of Silver Eagles and Maples were only 9.5 Moz in 2005. In just ten years, sales from these two official coins have increased more than 8 times.

Gresham’s Law: Bad Money Drives Out Good… Official Silver Coins

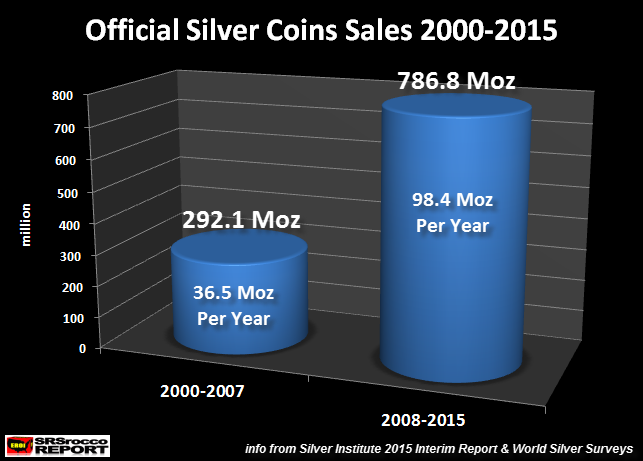

If we take the global official silver coin data from the first chart above, and divide it into two periods, we have the following result:

Before the first collapse of the U.S. financial industry and economy in 2008, total global official silver coin sales for the period 2000-2007 were 292.1 Moz. Now compare this figure to the second period from 2008 to 2015 at 786.8 Moz. If we average the annual global silver coin sales, the first period (2000-2007) shows an average of 36.1 Moz per year versus 98.4 Moz after the U.S. financial and economic meltdown (2008-2015).

This huge surge in official silver coin demand represents a percentage of investors who have decided to exchange increasing worthless paper currency for sound money.This trend started in the 1960’s when the United States sold off the majority of its huge silver stockpiles and removed silver from its coinage.

I am working on THE SILVER MARKET REPORT using figures and information starting in the 1960’s. Investors need to understand the trend change in the silver market has been going on for more than 50 years. Understanding this ongoing silver market trend is important for investors who want to protect their wealth when the next major financial crash occurs.

Even though the forecasted 130 Moz of Official Silver Coin Sales did not translate into higher silver prices, it did hammer a few more nails into the Greatest Financial Ponzi Scheme in history. That’s how investors need to look at the silver market. I realize it’s frustrating to see that record buying of silver coins does not seem to impact price.

However, investors need to understand that Greatest Financial Ponzi Scheme in history can only survive if global oil production continues to increase. Unfortunately, we are about experience a peak and decline of global oil production shortly starting first with the collapse of the U.S. shale oil industry.

I will be writing more articles explaining the connection between skyrocketing debt and rising oil production. One can not take place without the other. Which means, when the massive amount of global debt finally collapses, it will take down world oil production with it.

Some of the safest assets to own at this time will be physical gold and silver.

end

And now Bill Holter/

(courtesyHolter-Sinclair collaboration)

None of it …”can go on forever”!

Over the Thanksgiving weekend I received over 1,000 e- mails in total, many suggesting potential topics to talk about. We’ll talk about several topics on the surface, each one obvious in their own right.

First, I have been asked to speak about “climate change” as that is the current topic today for the world meeting in Paris. Let me first say this, I am no scientist and do not pretend to be one. From a big picture standpoint, didn’t what is now currently known as “climate change” used to be “global warming”? I seem to remember hearing how some scientists who revealed some of the “global warming science” was faulty were fired. I even remember calls for prosecution of anyone who denies climate change. Maybe this is just an offshoot of the new American university system advocating censorship …if what is said is contrary to the censor’s opinions? That said, I believe if you put 100 scientists with no ax to grind into a room and had them vote, a very small percentage would believe and affirm “global warming”. If you asked about “climate change”, you might have a majority affirmation but no more than 50/50 would attribute it to “man”.

In the interest of not being “prosecuted” (persecuted), I do not deny climate change. We now regularly are seeing droughts, floods, heat and cold in more severity and in more places than I can remember. I would simply ask what has changed in the last 40-50 years that might account for these changes? In the U.S., please do not tell me “carbon” because we lived in a far dirtier world in 1970 than we do today. Engines of all sorts are far more efficient (and cleaner) today than they were then. The production of electricity today is far more efficient than it was back then also. No one even considered the environment until Lake Erie actually “died”, we have steadily become more responsible since then. China, not so much but can you imagine them actually paying the Rothschilds a “carbon tax” for their pollution?

The one thing I can see (with my own eyes) are chemtrails playing tic-tac-toe across our skies. Why did we not see these in the skies when we were little kids? Are the skies different today or are jet engines so radically different now from then? Please, do not insult my intelligence as these trails have been videoed being turned on and turned off. A very good source to learn more about “geo engineering” would be from Dane Wigintonhttp://www.geoengineeringwatch.org/ads/dane- wigington/ . I would simply say this, maybe our climate is changing because the efforts of “man” to change the climate are actually having an effect? …and they want to charge a tax for these changes? Why not try the most simple? Leave the climate to God for five or ten years and let’s see what happens? Maybe the proposed global “carbon tax” (a scam in my opinion) will be “seen” as unnecessary ? One last question, who pays for or funds these sky writers anyway?

The last two subjects were both mentioned in my last article “Can you handle the ugly truth?”. First, so many e-mails sounded of capitulation …”this manipulation will go on forever”. I assure you it will not. In fact, I probably received this link two dozen times from readers http://www.kitco.com/news/2015-09- 15/Don- t-Believe-The-Hype-Comex-Gold-Warehouses-Well-Stocked- Two- Analysts.html This was posted at the (in my opinion, so I don’t get pro-ersecuted) “anti gold” site Kitco. This article is a total joke as far as I am concerned. They quote both Barclay’s and CPM Group, two leading apologists of the manipulation scheme for many years. They even disparage Peter Hambro for saying gold is very tight in London. Who would know one way or the other better than him? James Turk? He agrees! Of course his (their) opinion is supported by the backwardation in the gold market there.

I would also ask, has the registered category for deliverable gold on the COMEX EVER been this low? Something very very strange has also happened this delivery month, ONLY two contracts of over 7,800 were served on the first day. Why would this be? As I have written before, what incentive could ANY “short” possibly have to not deliver on the first day? Or even first three days? The short must pay “storage” for their physical gold right up until it is delivered and stand NO benefit whatsoever in stalling to deliver. This of course assumes the gold is actually there and “storage fees” are actually being paid…

The last topic today is the upcoming Fed meeting. Will they or won’t they raise rates? As you know, I can’t see any way they will do this, “data dependent” or not. Many say the rate hike depends on the unemployment number out this coming Friday. Really? The unemployment report has been shown by John Williams and others to be a bad joke in totally poor taste and virtually a complete fabrication. Zerohedge has come out with article after article showing the real situation in many reports and various market measures, the latest is seen here regarding ISM manufacturing http://www.zerohedge.com/news/2015-12- 01/ism-manufacturing-collapses-worst-june-2009-new- orders- prices-paid-plunge . How is it possible the Fed is even contemplating a rate hike?

It cannot be because the financial system is so flush and the “punchbowl” needs to be taken away (this should have been done 20 or more years ago). From the financial side of things, stress is again beginning to build up, this chart:

clearly shows stress in high yield debt. Please understand this does not even include debt from the energy patch. How much stress do you believe is being felt there where their product has dropped over 60% in price and many are operating at giant losses! Will the Fed hiking rates help ease this pain?

From another standpoint, the dollar has become grossly overvalued and emerging markets are finding it more and more difficult to service their dollar debt. An interest rate hike will do what exactly to this situation? In my opinion the Fed is being driven out of fear. On the one hand they absolutely MUST raise interest rates as they have been zero bound for seven years …in other words “when do we begin to move toward normal again”? On the other hand, I believe they are petrified as to what will happen if they actually do raise rates. It is not as if they have any precedent or history to look at as to how markets will react …especially the behemoth $1 quadrillion plus in derivatives!

To finish, if the Fed does raise rates I will be shocked and petrified at the same time. If the Fed does ever actually shrink their balance sheet willingly I believe it is safe to say anyone reading this will no longer be living. This of course assumes the panicked sheep who believe “this can go on forever” are correct. I assure you they are not!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

Comments welcome, bholter@Hotmail.com

end

1 Chinese yuan vs USA dollar/yuan falls in value , this time at 6.3987/ Shanghai bourse: in the green , hang sang: green

2 Nikkei closed up 264.93 or 1.34%

3. Europe stocks mixed /USA dollar index down to 100.01/Euro up to 1.0594

3b Japan 10 year bond yield: falls to .299% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 123.12

3c Nikkei now just above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 41.79 and Brent: 44.70

3f Gold up /Yen up

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .493%. German bunds in negative yields from 6 years out

Greece sees its 2 year rate rise to 7.58%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield rises to : 7.45% (yield curve inverted)

3k Gold at $1067.30/silver $14.18 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble down 15/100 in roubles/dollar) 66.58

3m oil into the 41 dollar handle for WTI and 44 handle for Brent/ China purchases huge supplies from Saudi Arabia

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0287 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0905 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/arrests 10 traders for Euribor manipulation

3r the 6 year German bund now in negative territory with the 10 year rises to +.493%/German 6 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.23% early this morning. Thirty year rate above 3% at 3.00% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Start Off December With A Bang, US Equity Futures Rebound; Yuan Drops

There was something for everyone in last night’s much anticipated Chinese PMI data, with the official number sliding to the lowest in over 3 years, suggesting the PBOC will need to do more stimulus and is thus bullish, while the unoffocial Caixin print rising to the highest since June, suggesting whatever the PBOC is doing is working, and is also bullish. Not unexpectedly, global stocks decided to take the bullish way out, and have risen across the globe led by Asia, where stocks rose as much as 1.8%, Europe also green and US equity futures up 10 points as of this writing.

“There seems to be some modest improvement in investor sentiment on the global outlook and that has supported equities and commodities,” Nick Kounis, head of macro research at ABN Amro Bank told Bloomberg. “The China data were on balance positive.” Sure enough global risk has been in a risk-on mood all morning:

- S&P 500 futures up 0.4% to 2089

- Stoxx 600 up 0.2% to 386

- MSCI Asia Pacific up 1.7% to 134

- US 10-yr yield up 2bps to 2.23%

- Dollar Index down 0.15% to 100.02

- WTI Crude futures up 0.6% to $41.90

- Brent Futures up 0.3% to $44.76

- Gold spot up 0.5% to $1,070

- Silver spot up 0.8% to $14.20

The Chinese PMI “confusion” was deftly handled by Bloomberg which in two separate pieces wrote, on one hand, that “an official manufacturing gauge sank to the lowest in more than three years” while on the other “a private gauge of Chinese factory output unexpectedly rose.” Just as watched was how China’s Yuan would react in its first day of inclusion in the IMF’s SDR basket, and instead of jumping as some strategists had expected, the freely traded offshore yuan fell 0.3% while the onshore spot rate was little changed. Others such as HSBC, said this is precisely the priced in outcome.

Also of note, there were no surprises when it came to policy decisions from the central banks of Australia and India. Both kept their benchmark lending rates unchanged. Elsewhere around the globe, U.K. banks rallied after all seven major lenders passed the Bank of England’s stress tests.

The strong December start was perhaps factored in by the algos, which are well aware that global equities have risen in the last month of the year on all but five occasions since 1988. Helping push European stocks higher was PMI data out of the EU which saw the final German PMI also rise above the flash estimate, printing at 52.9, above the 52.6 expected, while German unemployment dropping to a record low.

A closer look at regional markets starts in Asia, where MSCI Emerging Markets Index rebounded from a two-week low, climbing 1.3 percent, as benchmark gauges rallied across Asia. Hong Kong’s Hang Seng China Enterprises Index advanced for the first time in seven days and the Shanghai Composite Index increased for a second day, adding 0.3 percent.

The ASX 200 (+1.9%) outperformed following a rebound in all sectors and commodity prices, while Nikkei 225 (+1.3%) was lifted by the stellar Japanese capex and continued gains in company profits albeit at a slower pace. Mainland China lagged (Shanghai Comp +0.3%) as participants digested the latest PMI releases in which official manufacturing PMI printed its lowest since August 2012 and Caixin manufacturing PMI was at a 9th month in contractionary territory despite beating expectations. 10yr JGBs traded higher following the well-received 10yr JGB auction which saw the highest b/c since September 2014.

Asian top news:

- China’s Manufacturing PMI Gauge Weakens to Lowest in Three Years: Readings show two-speed pace of growth as services outperform

- Macau Casino Revenue Falls 32% as China Curbs Hit VIP Gaming: Decline for 18th straight month, down 35% so far this year

- Rajan Holds India Interest Rate With Eye on Inflation Target: Will use space for more accommodation when available

- Australia Holds Key Rate as Economy Expands Despite Mining Bust: RBA leaves key rate at 2.0%, as seen by all economists surveyed

- Japan Pension Whale Stands by Stocks After $64 Billion Loss: GPIF lost 5.6% last quarter as stocks slid on China surprise

- Japan 3Q Capital Spending rose 11.2% Y/y; Est. +2.2%

- S. Korea’s Nov. Exports Fall 4.7% Y/y; Est. -9%; S. Korea’s Nov. Consumer Prices Rise 1% Y/y; Est. +0.9%

- Australia Nov. Manufacturing Index Rises 2.3 Pts M/m to 52.5

- Indonesia Nov. Consumer Prices Rise 4.89% Y/y; Est. 4.85%

In Europe, equities initially drifted lower heading into the North American crossover after a relatively choppy start, while the notable outperformer today has been the FTSE-100 (+0.4%), which has been led higher by financials after the BoE announced that all UK banks passed their stress test. On the other hand Linde (-11.9%) are the notable laggard in Europe after lower their 2017 forecast and expecting 2015 earnings to be at the lower end of expectations. However, the initial weakness in Europe to an extent also driven by concerns about the ECB doing less than expected on Thursday, has since been absorbed and the Stoxx had returned back into the green at last check.

European top news:

- Bank of England Sees Countercyclical Buffer Rising on Risk: BOE said it may begin forcing banks to set aside capital as soon as March to support lending in a downturn

- Linde Drops as Lower U.S. Pricing Clips Outlook for Profit: CEO Wolfgang Buechele reduced earnings targets at the gases supplier for the third time in just over a year

- German Unemployment Rate Falls to Record Low on Domestic Demand: Sign that robust domestic demand is bolstering confidence in the growth prospects for Europe’s largest economy

- Swiss Economy Unexpectedly Stagnated in 3rd Quarter on Franc: Weak performance in energy, construction and financial sector

- Zurich Says CEO Senn Steps Down, de Swaan Takes Interim Role: CEO resigned after insurer reported a loss at general insurance unit, abandoned takeover bid for Britain’s RSA Insurance Group

- UBS Traders May Be First to Face Sanctions in Currency Probes: As many as seven UBS traders may face sanctions from Switzerland’s financial watchdog in the coming weeks

- France Nov. Manufacturing PMI unchanged at 50.6; prelim. 50.8

- U.K. Nov. Manufacturing PMI falls to 52.7, below est.

- Euro-Area Oct. Jobless Rate falls to 10.7%; median est. 10.8%

Bunds remain in negative territory after falling below the 158.00 level in early trade amid touted profit taking following recent gains, although with little new fundamental catalyst driving the move the German benchmark rebounded off worst levels and while remaining in negative territory, did rise back above the 158.00 level. While T-Notes moved in tandem with their European counterparts, initially seeing softness however heading into the US open off their worst levels.

In FX, a gauge of developing-nation currencies rose for the first time in five days after closing on Monday within 0.03 percent of a record-low. India’s rupee strengthened as the nation’s central bank kept borrowing costs on hold Tuesday. Turkey’s lira strengthened 0.8 percent, advancing for a second day as a report showed manufacturing expanded in November. In a meeting with President Recep Tayyip Erdogan on Tuesday, U.S. President Barack Obama discussed how to deescalate the situation with Russia after tension over the downing of a warplane near the Syrian border.

The AUD/USD rose after Australian building approvals smashed estimates (Y/Y 12.3% vs. Exp. 5.7%, M/M 3.9% vs. Exp. -2.5%), while AUD found additional support following the RBA’s decision to stand pat on rates and maintained a neutral bias. While also of note, the RBI kept all three of their main rates on hold as expected. In a similar fashion to yesterday, FX markets experienced volatility in early European trade, with GBP benefiting from UK/GE yield differentials and a softer USD index, as GBP/USD initially broke above the 1.5100 handle, however coming off best levels in the wake of a below expectation reading of manufacturing PM! (52.7 vs. Exp. 53.6). USD softness also benefited EUR/USD, which briefly broke above 1.0600 after reports that European names have taken off short bets today, before running into touted real money offers at 1.0620.

In commodities, Oil futures in New York erased a gain of as much as 1.3 percent to trade little changed at $41.65 a barrel before this week’s meeting of the Organization of Petroleum Exporting Countries. Gold climbed a second day. Bullion for immediate delivery climbed 0.5 percent to $1,069.69 an ounce. Copper rose 0.5 percent to at $4,606.50 a metric ton in London.

Copper clawed back some of November’s 10 percent losses, the worst month since January. It wasn’t alone. An LME gauge of six industrial metals has now sunk for seven consecutive months, the longest losing stretch since 2009. The worst might not be over for copper, which is languishing near a six-year low. Hedge funds are betting there’s more pain in store as economic growth slows to the weakest pace in more than two decades in China, the world’s top consumer. Citigroup isn’t so bearish. It forecasts many commodity markets, including copper, may strengthen in the second half of 2016 as the collapse in prices shrinks production.

Looking at today’s calendar, this morning in Europe was be all about the manufacturing PMI numbers for November, where we got the final Euro area (match), Germany (beat) and France (miss) readings along with the indicators for Italy, Spain and also the UK. We’ll also get some labour market data with the latest unemployment reads due for the Euro area and Germany. This morning will also see the release of the BoE stress tests with Governor Carney set to speak shortly after. In the US, the final manufacturing PMI will also be released for the US while the focus will be on the November ISM data (manufacturing and prices paid). October construction spending data is also set to be released, while later this evening the November vehicles data will be released. Fedspeak wise we’ve got the Chicago Fed President Evans set to discuss the economic outlook and monetary policy at 12.45pm.

Global top news:

- U.K. Banks Lead Europe’s Stock Rally After Stress-Test Results: Britain’s lenders led rally in Europe equities after Bank of England said all 7 major lenders passed stress tests

- ECB’s Split With Fed Risks Running Until Draghi Near Retirement: Market indicator shows next ECB rate hike not before Nov. 2018

- Yuan Drops as SDR Approval Seen Prompting PBOC to Reduce Support: Yuan weakened in offshore trading amid speculation China’s central bank will rein in intervention now that the IMF vote on reserve-currency status is out of the way

- Euro Area’s Modest Recovery Sets Scene for Draghi Stimulus: Factory growth in euro area accelerated amid a continued decline in unemployment, extending a tepid recovery that may require more stimulus from the European Central Bank. Euro to Bear Brunt of Yuan’s Inclusion in IMF Reserve Basket

- Oil Bulls Brace for Repeat of OPEC’s Bearish Blow at Meeting: Hedge funds are betting this week’s OPEC meeting will deliver another bearish blow to crude

- Zurich Insurance CEO Steps Down, De Swaan Named Interim CEO

- Putin Snubs Erdogan, Sees Obama in Test of Anti-Terror Front: In meeting, Obama and Putin don’t advance anti-terror alliance

- Einhorn’s Hedge Fund Plunged 5.2% in November, Set for 2015 Loss: David Einhorn’s main hedge fund at Greenlight Capital is poised for only its second losing year in almost two decades

- Power-Line Operator ITC Starts Review That May Lead to Sale: Study is part of effort to maximize value to shareholders

- Anadarko Ordered to Pay $159.5 Million for 2010 Gulf Spill: Fine due to role as part-owner of doomed Gulf of Mexico well that in 2010 caused biggest offshore oil spill in U.S. history

- Cyber Monday Sales Slow as Web Shopping Spans Holiday Season: Web-based sales climbed 17% Monday from year earlier as of 6pm in New York, after jumping 26% on Saturday and Sunday, IBM said

Bulletin Headline Summary from Bloomberg and RanSquawk

- The Asia-Pacific session saw RBA and RBI keep rates on hold, while Chinese mfg PMI printed lowest reading since Aug’12 and China Caixin mfg PMI print the highest reading since June

- FTSE-100 outperforms in Europe after financials bolster the index, with the BoE announcing that all major seven UK banks passed their stress test

- Looking ahead, today sees US manufacturing PMI, construction spending, ISM manufacturing and API crude oil inventories as well as comments from Fed’s Evans and Brainard and ECB’s Visco

- Treasuries decline led by 5Y and 7Y notes as markets wait for Yellen speech tomorrow, ECB and Draghi Wednesday, Nov. payrolls Friday and FOMC Dec. 16.

- Factory growth in the euro area accelerated amid a continued decline in unemployment, extending a tepid recovery that may require more stimulus from the ECB

- China’s manufacturing conditions slipped to the weakest level in more than three years as sluggishness in the nation’s old growth drivers add to risks facing the government’s growth target

- The euro’s worst year in a decade is looking even grimmer after the Chinese yuan’s inclusion in the IMF’s SDR basket, with its weight set to drop to 30.93% from 37.4%

- A U.K. manufacturing gauge fell more than economists forecast in November, while still signaling solid growth after reaching a 16-month high the previous month

- Obama urged Turkey and Russia to refocus their efforts on the common goal of combating terrorism, after Putin traded barbs with his Turkish counterpart, Recep Tayyip Erdogan

- Merkel’s Cabinet yesterday backed the deployment of German troops against Islamic State, including 1,200 troops along with Tornado reconnaissance planes, refueling aircraft and a frigate in support of France, according to the document obtained by Bloomberg News

- Swedes are responding to their government’s historic intake of refugees by turning to an anti-immigration group that both the ruling coalition and opposition deem too xenophobic to work with

- $110.825b IG priced yesterday, $21.405b HY. BofAML Corporate Master Index OAS narrows 1bp to +162, YTD range 180/129. High Yield Master II OAS widens 2bp to +640, YTD range 683/438

- Sovereign 10Y bond yields higher. Asian stocks rise, European stocks mixed, U.S. equity-index futures gain. Crude oil lower, copper and gold higher.

DB’s Jim Reid completes the overnight recap

Welcome to what looks set to be one of the busier December months that we can remember, certainly for central banks with the ECB and Fed very much in play. The month could be a battle between monetary policy Scrooge and Santa as we close out the year. December is rarely a bad month for risk but conditions are hardly normal at the moment. November was a month highlighted by what were huge declines across the commodity complex – Oil included – which makes this Friday’s OPEC meeting all the more important to keep a close eye on.

Although news-flow is still reasonably thin, European risk assets closed out November on a high yesterday reflecting the high hopes for this Thursday’s ECB meeting. The Stoxx 600 ended the session up +0.46% and at a three-month high while credit indices generally closed with some modest gains. The Euro continues to tumble, trading below $1.06 for all of yesterday’s session and is now at its weakest level since April. 2y Bund yields edged ever so slightly lower to -0.422% with the spread versus similar maturity Treasuries at 135bps which is the widest it’s been since 2006.

Those gains in European equities were in stark contrast to what was a generally weaker day in the US. The S&P 500 finished -0.46% having dipped lower into the close, although in reality it traded with a weaker tone for most of the session reflecting perhaps the soft second-tier data yesterday which did little to sway Fed expectations though. That said US credit indices outperformed with CDX IG finishing half a basis point tighter.

Before we go on, we’re straight to China this morning where the November PMI numbers are in. There are some mixed messages in the data, with the official reading falling 0.2pts to 49.6 (vs. 49.8 expected) which is the lowest since August 2012. This compares to a modest rise in the non-official Caixin reading, which was up 0.3pts to 48.6 (vs. 48.3 expected), albeit also in negative territory. Meanwhile and highlighting the divergence between sectors, China’s non-manufacturing PMI climbed 0.5pts to 53.6 – the highest level since July. Chinese bourses were initially weaker post the data but have rebounded for modest gains post the midday break. As we go to print, the Shanghai Comp and CSI 300 are +0.15% and +0.35% respectively.

Elsewhere, it’s been a pretty positive start for markets in December. The Nikkei is up +0.95% despite Japan’s manufacturing PMI declining a tad (52.6 from 52.8). The Hang Seng is +2.09% while the Kospi (+1.61%) and ASX (+1.93%) have also gained. The AUD is half a percent better off following some better than expected net exports data in Q3, while the RBA also left the cash rate on hold. Oil markets have made modest gains along with industrial metals this morning.

The notable newsflow from yesterday’s session was the widely expected confirmation from the IMF of the inclusion of the Chinese Yuan in its SDR basket. The currency will be added from the 1st October 2016 and will comprise 10.92% of the overall basket which was a little bit lower than the 14-16% previously drawn up from the IMF staff estimates. Speaking on the decision, IMF Chief Lagarde said that ‘the renminbi’s inclusion in the SDR is a clear indication of the reforms that have been implemented and will continue to be implemented and is a clear, stronger representation of the global economy’. In a note published this morning, DB’s China Chief Economist Zhiwei Zhang noted that the inclusion is structurally positive for China, as he believes that this may act as a catalyst to boost the momentum of reforms in China and indicates that the authorities are keen to integrate China’s economy further with the global economy. The onshore CNY was set 0.02% weaker this morning at the fix and has been little changed for much of the session.

In terms of the data flow yesterday, in the US the notable takeaway was a much softer than expected Chicago PMI for November, which fell 7.5pts to 48.7 (vs. 54.0 expected) and back to where it was in September after some falls for new orders and prices paid. The ISM Milwaukee (45.3 vs. 48 expected) also fell deeper into contractionary territory, down 1.4pts last month although there was better news for the Dallas Fed manufacturing survey which was up 7.8pts to -4.9 (vs. -10.0 expected), the highest since July albeit remaining in negative territory. These reports came before today’s ISM manufacturing print which our US economists expect slipped into negative territory in November to 49.0 (which is more bearish than the current market consensus of 50.5) having fallen to 50.1 in October. They note that this is based on the recent weakness in the NY and Philadelphia Fed surveys also, which is consistent with a decline in factory activity but not the overall economy (for the overall economy to be contracting, the level of the manufacturing ISM would have to be near 43). The other notable data point yesterday in the US was a slightly more disappointing than expected pending home sales report for October, with sales up just +0.2% mom (vs. +1.0% expected).

The economic data yesterday in Europe was focused on Germany where there was a disappointing start for Q4 retail sales with the November reading printing at -0.4% mom, which was below the +0.4% expected. It’s worth noting that this data can be very volatile, while sales do not have a strong correlation with overall consumption. Also out in Germany was the preliminary November CPI reading, although this offered no surprises at +0.1% mom for the month as expected, helping to nudge the YoY rate up one-tenth to +0.4%. Italy’s CPI print was a bit more disappointing at -0.5% mom, while in the UK mortgage approvals for the month of October nudged to 69.6k from 60.0k the previous month.

Also of interest yesterday was the news that the Fed is to adopt Dodd-Frank bailout limits, aimed at limiting the Fed’s ability to rescue individual companies during a crisis, the likes of which we saw for AIG and Bear Stearns during the financial crisis. The revised rule now means that the Fed will only be able to save companies with a ‘broad-based program’ rather than to select individual institutions.

ASIAN AFFAIRS

China Manufacturing Slumps To 3-Year Lows And Soars To 5-Month Highs

Following the earlier onslaught of weak (and strong) economic data, China has revealed its official and Caixin-based PMI surveys for Manufacturing and Services. Sure enough, while China’s official manufacturing data missed (to Aug 2012 lows), Ciaxin’s survey beat, jumping to June 2015 highs. even as China’s official Services PMI beat expectations, bouncing off 15-month lows. The question now is – given The IMF’s inclusion of the Yuan in the SDR basket – will The PBOC devalue (as offshore Yuan implies) to juice a collapsing manufacturing sector… or is China’s manufacturing now improving if one looks at the “other” PMI?

Lots of confusion, even if just as we suggested before the Caixin PMI print:

And so, behold – China Manufacturing. The official print missed expectations and heads deeper into a 4-month contraction.. but the Caixin survey surged to 5-month highs, beating expectations

And if you do not believe that the central planners know what they are doing – Dr. He Fan, Chief Economist at Caixin Insight Group explains…

“The Caixin China General Manufacturing PMI for November continued to show signs of recovery, reaching 48.6, compared to October’s 48.3. This indicates that pressure on economic growth has eased and fiscal policy has had a strong effect.

Overall, the economy is still on track to become more stable.”

Let’s get some context on this so-called “stability” – it moved up 0.3pts and is still at 48.6 – a very contractionary level! So ‘contraction’ is the new ‘killing it’.

China Services… [delayed for now – no explanation from source]

Finally we note that China services PMI is indeed likely to outperform manufacturing at every turn going forward. If we see China services PMI fall off a cliff with manufacturing, then it exposes the gaping wound that reforms are not working and that the glorious five-year plan transition away from the smokestack isn’t working…

However, someone needs to tell Chinese stocks to get with the program – following yesterday’s afternoon session rescue, Chinese equity investors are again selling to government buyers.

Because US equities are loving it – Dow Futs up over 100 points from the close – running stops above the US open cliff dive…

Charts: Bloomberg

AsiaPac Unleashes Baffle ‘Em With Bullshit Data Bonanza

From South Korean exports (beat) to Aussie PMI (multi-year highs) and from China Manufacturing PMI (2012 lows) to Japan CapEx (multi-year highs), AsiaPac was awash with the exact kind of baffle ’em with bullshit data that provides just enough “see everything is awesome after all” to balance the “umm, but what about…” less glass half full perspective. For your viewing pleasure – 5 WTF charts for AsiaPac economies.

WTF1 – Aussie PMI surprises to the upside to 2 year highs as Aussie Consumer confidence collapses…

WTF2 – While Aussie business spending collapsed at tits fastest pace on record Aussie PMI surged to near cycle highs…

WTF3 – Japanese CapEx surged by the most since 2007 as GDP dropped for the 5th time in 5 years…

WTF4 – South Korean exports dropped (again) but beat expectations notably despite not having any positive impact at all on the cost of ‘exporting’…

And finally…

WTF5 – China Services PMI jumps unexpectedly as the official manufacturing PMI just collapsed to its lowest level since August 2012, as the broad-based contraction accelerates.

Charts: Bloomberg

Confused yet? The answer is simple – if it’s bad news, buy stocks because the central bank will be forced to ease. If it’s good news, buy moar stocks because it proves central planners have fixed the problem.

end

Chinese Auto Sales Crash, Inventories Soar In November

Despite ongoing exuberance at auto sales in America (which disappointed) – as crashing credit standards enable every Tom, Dick, and Muppet to buy too much ‘depreciating asset’ for their incomes – there arenumerous problems few are talking about for automakers worldwide. Aside from “plans to buy a car” tumbling in the latest confidence surveys, and inventories-to-sales surging, China just poured ice cold water on any hope of stability in that ‘growth’ market as auto dealers issue the highest inventory alert since June. November data from China shows demand plunging, sales collapsing, and inventories soaring – a triple whammy of “no, things are not ‘stabilizing’.”

As sales begin to disappoint…

- *GM NOV. TOTAL U.S. VEHICLE SALES UP 1.5%, EST. UP 2.9%

- *FORD NOV. U.S. LIGHT-VEHICLE SALES UP 0.3%, EST. UP 3.2%

- *FIAT CHRYSLER NOV TOTAL U.S. VEHICLE SALES UP 3.0%,EST. UP 3.2%

- *TATA MOTORS: TOTAL NOV. SALES DOWN 7% YEAR OVER YEAR

First, Inventories are at record (absolute) highs and at recession-signalling ratios to current sales…

Second, and that is a problem because the much-hyped and hoped-for future sales to soak all this excess inventory up is not coming soon… As the consumer confidence survey shows the lowest level of “plans to buy an auto” since January 2013…

And finally, Third, do not look to China for any help at all… China November Vehicle Inventory Alert Index rose to 61.8% (from 54.1% in Oct.), the Beijing-based China Automobile Dealers Association says in e-mailed statement.

Automakers appear to have two options, offer buy-one-get-one-free to all new Syrian refugees or cut production dramatically in hopes of easing inventory excess. Good luck.

Charts: Bloomberg

end

Britain May Launch ISIS Strikes “Within Days”; Germany To Join With Warship, Planes, Troops

On Saturday, in “‘The Redcoats Are Coming!’ Britain Moves Closer To Launching Anti-ISIS Airstrikes,” we warned that the skies above Syria were about to get even more crowded as David Cameron pushed British lawmakers to approve RAF strikes on Raqqa.

“It is wrong for the United Kingdom to expect the aircrews of other nations to carry the burdens and the risks of striking ISIL in Syria to stop terrorism here in Britain,” Cameron said.

“I don’t think this is a country that lets others like the French or the Americans defend our interests and protect us from terrorist organizations – we should contribute to that effort,” Finance minister George Osborne added, underscoring the perception that Britain’s military prowess is but a shadow of what it once was.

We also noted that Labour leader Jeremy Corbyn would not use a party whip to influence MP’s decisions. Over the weekend, Corbyn expressed serious reservations about the number of “moderate” rebels on the ground in Syria and also suggested that to the extent there are enough fighters to occupy the territory held by Islamic State once the group is routed, the UK shouldn’t assume that the fighters can be trusted. “I seriously question the number, I seriously question the motives and loyalty of those forces,” Corbyn said.

On Monday, Corbyn apparently attempted to compel party members to vote against military action in line with his own stance on the issue but after what FT described as a “fraught meeting”, the Labour leader bowed to internal pressure and conceded that MPs would be allowed to vote as they choose. Additionally, Corbyn abandoned the idea of setting an official policy of opposing air strikes no matter how party members voted after Andy Burnham, shadow home secretary, said that was “unacceptable”. Here’s where Corbyn’s shadow cabinet stands:

Against airstrikes

- Jeremy Corbyn, leader of the Labour party

- John McDonnell, shadow chancellor

- Jon Trickett, shadow communities secretary

- Diane Abbott, shadow international development secretary

- Ian Murray, shadow Scotland secretary

- John Cryer, chairman of the parliamentary Labour party

- Nia Griffith, shadow wales secretary

For airstrikes

- Tom Watson, deputy leader (who has asked Cameron to delay the vote pending proof that there are actually 70,000 moderate rebels on the ground)

- Angela Eagle, shadow first secretary of state and shadow business secretary

- Hilary Benn, shadow foreign secretary

- Heidi Alexander, shadow health secretary

- Lucy Powell, shadow education secretary

- Chris Bryant, shadow leader of the house of commons

- Vernon Coaker, shadow northern Ireland secretary

- Michael Dugher, shadow culture secretary

With that, the stage is set for Britain to join the fray. As FT goes on to note, Corbyn’s concession to his divided party “effectively guarantees that [David Cameron] can secure a Commons majority for war.” British military action could start “within days” as the PM “reacted quickly to Corbyn’s capitulation, announcing after he returned from the Paris climate summit that he would recommend to the cabinet on Tuesday that a one-day debate and vote on military intervention in Syria be held on Wednesday.”

With the vote thus set, “RAF crews could be bombing the Isis headquarters in Raqqa by the end of the week,”The Guardian says. On Tuesday, Cameron said “the decision to take military action is one of the most serious a prime minister can make. Isis poses a very direct threat to the United Kingdom – and as we have already seen in Iraq, British airstrikes can play a key role in degrading them; but they are only part of a comprehensive strategy for Syria.

But that’s not all. Germany is now set to enter the fight as well. “German Chancellor Angela Merkel’s Cabinet approved deploying warplanes over Syria in the fight against Islamic State,”Bloomberg reported on Tuesday. Apparently, Berlin is set to send Tornado surveillance planes, a frigate to protect France’s carrier, and aerial refueling for French fighter jets.

Parliament will need to approve the deployment and a vote is expected within days. All told, around 1,200 German troops are expected to participate. This should do wonders when it comes to stemming the flow of refugees into Germany because as France explained earlier this year, by far the best way to solve a refugee crisis is to drop more bombs on the place from which the refugees are fleeing.

And with that, two more world powers will now have planes in the sky and ships in the Mediterranean. Just to be clear, this means that by the end of next week, it’s possible that American, French, Turkish, Russian, and German planes will all be flying missions above Syria, a decisively dangerous scenario now that Ankara has forced Moscow into a state of paranoia regarding the safety of The Kremlin’s aircraft. With Russian S-400s at the ready, and with Su-34s now armed with air-to-air missiles, the potential exists for another “accident.”

Additionally, it’s worth reiterating that the West and the Russians still haven’t resolved the most pressing issue when it comes to airstrikes in Syria. Namely that Moscow and Iran are still attacking the FSA and other rebel groups that are receiving guns and money on a weekly basis from the US, Turkey, Saudi Arabia, and Qatar. This means that while the West bombards Raqqa (or perhaps the better way to put is “while the West thinks they’re bombarding Raqqa based on the ‘intelligence’ they receive from Washington”), America and its regional allies are engaged in a proxy war with Moscow and Tehran in the northwest part of the country. This makes absolutely no sense and it isn’t at all compatible with David Cameron telling British lawmakers that the “moderate” opposition is in a position to hold territory formerly governed by ISIS. Not only are the rebels not in a position to secure towns and cities, they are being routed at Aleppo by the Russians and Iranians. At some point this has to be addressed but for the time being, everyone seems content with being invited to the party.

Legendary Hedge Fund Calls It (Semi) Quits: $8 Billion BlueCrest To Return Outside Client Money

Hedge funds are dropping like flies now.

Following news that both Ackman and Einhorn have suffered dramatic losses, in the -20% ballpark YTD, and after reporting that numerous metal-focused commodity hedge funds have liquidated in recent months, most notably Trafigura’s own Galena, the latest firm to wave the flag of surrender to the forced of central planning is none other than Michael Platt’s legendary $8 Billion BlueCrest Capital, which until recently was the third largest hedge fund in Europe, and as recently as two years ago was the topic of the Bloomberg profile “BlueCrest Builds a Hedge Fund Empire“, will return a whopping $7 billion of its current $8 billion AUM held currently in the form of outside money.

Just hitting the headlines:

- MICHAEL PLATT’S BLUECREST TO RETURN ALL OUTSIDE CLIENT MONEY

- BLUECREST CAPITAL MANAGEMENT TO BECOME PRIVATE INVESTMENT PARTN

- BLUECREST HAS $8B AUM, $7B IS SAID TO BE OUTSIDE MONEY

- BLUECREST: CLIENTS TO GET 75% INVESTMENT CAP BEFORE JAN END

- BLUECREST: CLIENTS TO GET 90% INVESTMENT CAPITAL BY END OF 1Q

- BLUECREST SAYS BSMA TO CONTINUE TO HOLD CERTAIN MANAGED ASSETS

From the press release:

BlueCrest Capital Management Limited “BlueCrest” announces it will, over the next several months, transition to a Private Investment Partnership, and will return to its clients the $8 billion it currently manages on their behalf. Following the transition, BlueCrest will manage assets solely on behalf of its partners and employees.

It will continue to trade all current major strategies and retain all the firm’s offices around the world and anticipates strong growth in employees and AUM over the next several years under the new business model.

During its 15 year history, BlueCrest has delivered trading profits of over $22bn for its investors, and has won numerous industry awards for excellence. It has built an industry leading global team of over 250 investment professionals in nine offices operating in fixed income, currencies, emerging markets, credit and equity trading.

However, ongoing secular changes in the industry, including trends in fee levels, the cost of hiring the best trading talent, and the challenges in tailoring investment products to meet the individual needs of a large number of investors, have weighed on hedge fund profitability. A Private Investment Partnership strategy of concentrating on a reduced number of funds, managed exclusively on behalf of BlueCrest’s partners and employees, will facilitate higher returns and greater profitability for the firm’s stakeholders, and give it greater flexibility to compete aggressively for trading talent.

BlueCrest’s existing partner fund, BSMA, will continue to hold assets managed in the fixed income, currency and credit trading strategies, and the BlueCrest Equity Strategies Fund and the BlueCrest Emerging Markets Fund will be retained as the vehicles through which partners and employees invest in equity market and emerging market trading strategies respectively. All other funds, including BlueCrest Capital International, and the AllBlue Fund, are expected to close during 2016.

The process of closing the client funds has been agreed with the Boards of Directors of those funds and communications with clients as to the timetable is now taking place. Clients are expected to receive approximately 75% of their investment capital before the end of January and 90% by the end of Q1 2016. The divestment of investment portfolios will be carried out in an orderly manner, balancing the requirements for speed and value for investors.

BlueCrest’s founder and Chief Executive, Michael Platt, said:

“Firstly, I would like to thank all of the investors who have entrusted money to the BlueCrest funds over the last 15 years and to wish them well in their future investment endeavours.”

“We are embarking on an exciting new phase in the development of BlueCrest. We will be stronger and more flexible under our new business model, and see exciting opportunities to grow significantly in terms of numbers of trading teams and assets under management. The new model provides the opportunity to create significant value for our partners, our traders and our staff, due to a step-change in our profitability. It will also allow us to enhance further our ability to attract the highest quality investment talent in markets across the globe. We have delivered industry-leading returns to our investors over the past 15 years but believe that BlueCrest is now better suited to a Private Investment Partnership model.

We have always been an industry innovator, and this transition will be no exception. We have sold and repurchased a stake in our business, we have seeded new strategies using bank loan financing, and been among the first to launch a permanent capital vehicle in the UK. We seeded and spun out BlueMountain Capital and more recently have spun out and divested of a significant stake in Systematica, a major business division. This transition, though not unique, will make us one of the largest and most diverse managers to adopt a Private Investment Partnership model.”

* * *

BlueCrest Capital Management, one of the world’s premier hedge fund managers, was founded in 2000 by Michael Platt, and manages c. $8bn of assets. With an award-winning reputation for excellence BlueCrest combines a “specialist portfolio management approach”, tight risk management and research excellence. BlueCrest has c.570 members of staff located in offices in Jersey, London, New York, Geneva, Singapore, Hong Kong, Boston, Westport and Toronto.

end

And Bluecrest’s holdings:

among thing, CNOOC and Petrochina both darlings to the Shanghai exchange!

(courtesy zero hedge)

Here Are BlueCrest’s Biggest Holdings

Following the the stunning news that BlueCrest, until recently one of the Europe’s largest and fastest growing hedge funds, will be essentially unwinding as it returns the bulk of its managed money to outside investors (according to Bloomberg $7 billion of the $8 billion in AUM will be returned), and will liquidate the vast majority of its holdings, the question is just which securities will have the overhang of a forced seller over the next few months.

The (partial) answer comes from BlueCrest’s latest 13-F, which lists some 846 securities amounting to just over $3 billion. And while the breakdown includes various fixed income investments and derivatives (both calls and puts), here are the Top 10 pure-play stock investments listed by the fund.

China’s “regulators” will hardly be pleased that one of the world’s most prominent hedge funds is about to take an axe to 2 of its three biggest holdings which just happen to be Chinese market darlings, CNOOC and Petrochina.

And a breakdown by industry courtesy of Bloomberg:

One thing stands out in the chart above: the fund’s surprising overexposure to Energy assets. Perhaps that is also the reason for its fund’s premature quasi demise?

(courtesy Keep Talking Greece)

Greeks Told To Declare Cash “Under The Mattress”, Jewelry And Precious Stones

When earlier today we read a report in the Greek Enikonomia, according to which Greek taxpayers would be forced to declare all cash “under the mattress” (including inside) or boxes that contain more than 15,000 euros as well as jewelry and precious stones (including gold) worth over 30,000 euros, starting in 2016, we assumed this has to be some early April fools joke or a mistake.

After all, this would be merely the first step toward full-blown asset confiscation, conducted so many times by insolvent governments throughout history, once the government cracks down on those who made a “mistake” in their asset declaration form or simply refuse to fill such a declaration, thereby making all their assets eligible for government confiscation.

It was not a joke.

Here is the take of Keep Talking Greece, whose stunned response mirrors ours.

Cash “under the mattress” totaling more than 15,000 euro, jewelry and other valuable items such as diamonds and gemstones, should be declared to electronic system of tax authorities, Taxisnet, as of 1 January 2016. Next to properties and vehicles and shares, now the taxpayers will also have to declare their deposits. And not only that. They will have to fill if they rent bank lockers and if yes, also the name of the bank and the branch, even if abroad.

A joint ministerial decision issued by the Ministries of Justice and Finance indicates that taxpayers in Greece should add all their valuables into a new category of the tax declaration, the “Assets declaration.”

Specifically, the decision provides that:

“Assets declarations” are submitted electronically and mandatory via Taxisnet.

Starting date for the submission is 1.1.2016

Declared must be cash money if more than 15,000 euro and precious items if their total value exceeds 30,000 euro. These amounts apply cumulatively per household (husband, wife, underage children).

To facilitate the completion of the declaration, data from the income statements (E1 and E9) will be drawn automatically.

Note that this Assets declaration process will initially apply to lawmakers, journalists, public servants etc and is the rehearsal for the creation of the electronic property & assets register that will be extended to all taxpayers.

The new assets declaration form has a total of 56 pages.