Gold: $1078.00 up $15.10 (comex closing time)

Silver $14.22 up 48 cents

In the access market 5:15 pm

Gold $1073.40

Silver: $14.17

At the gold comex today, we had a good delivery day, registering 265 notices for 26,500 ounces.Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 195.86 tonnes for a loss of 107 tonnes over that period.

In silver, the open interest fell by 2303 contracts even though silver was up in price by 8 cents with respect to Tuesday’s trading and thus we must have had some short covering. We have an extremely low price of silver and a very high OI coupled with backwardation in silver at the LBMA. (negative SIFO rates). The total silver OI now rests at 166,864 contracts. In ounces, the OI is still represented by .834 billion oz or 119% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI fell by 4492 contracts to 390,944 contracts as gold was down $1.80 in price with respect to yesterday’s trading.

We had no changes in gold inventory at the GLD, / thus the inventory rests tonight at 634.63 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver, we had no changes,in silver inventory at the SLV/Inventory rests at 323.509 million oz

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fall by 2303 contracts down to 166,864 despite the fact that silver was up in price to the tune of 8 cents with respect to yesterday’s trading. The total OI for gold fell by 4492 contracts to 390,944 contracts as gold was down $1.80 in price

(report Harvey)

2 a) Gold trading overnight, Goldcore

a very important audio with Grant Williams of Hmmm fame

(Mark OByrne)

3. ASIAN AFFAIRS

4. EUROPEAN AFFAIRS

Denmark is to confiscate jewelry, diamonds and money from refugees

(zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. EMERGING MARKETS

8. OIL MARKETS

i Last night:

Oil breaks below 37 dollars again after the huge buildup in API inventories:

(courtesy API/zero hedge)

ii)Today: DOE also reports a huge December inventory build. It was the biggest gain in inventory levels in 22 years:

(courtesy DOE/zero hedge)

9. PHYSICAL MARKETS

i) This morning gold and silver jump as the dollar is the most crowded trade in the world at 9 trillion usa:

(courtesy zero hedge)

ii) How the USA forces the world to store USA dollars. In essence the USA buys stuff and exports only one major thing: USA dollars.

10 IMPORTANT USA STORIES WHICH WILL INFLUENCE GOLD AND SILVER

iii Markit’s USA Manufacturing PMI plunges to its lowest level since 2012/ Factory orders, a big component collapses to 2009 level.

v) Here is the next hammer to fall: Collateratized leverage loans are getting hammers due to the low oil price:(courtesy Idzelis/Bloomberg)

vi) Bill Ackman of Pershing Square had a awful month as he reports his earnings

Old rusted pipes in Flint Michigan has caused lead levels in the water to be at disastrous levels

(courtesy Carey Wedler/The AntiMedia.org)

ix) The Fed is out of dry powder..

x) Fed raises rates by 1/4%

(zero hedge)

xi the Mouthpiece, Hilserath explains the above

(Hilsenrath/WallStreet Journal)

xii) Real estate guru Sam Zell warns that the Fed is too late in raising rates:

Let us head over to the comex:

The total gold comex open interest fell to 390,944 for a loss of 4492 contracts despite the fact that gold was down by only $1.80 in price with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. Today, both scenarios were in force but only a very tiny contraction in front month OI. We are now in the big December contract which saw it’s OI fall by 199 contracts from 1768 down to 1569. We had 186 notices filed yesterday, so we lost a tiny 13 gold contracts or an additional 1300 oz will not stand for delivery in this active delivery month of December. The next contract month of January saw it’s OI rise by 24 contracts up to 647. The next big active delivery month is February and here the OI fell by 3946 contracts down to 278,288. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 110,059 which is poor. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was also poor at 120,211 contracts. The comex was in backwardation in gold up to April

December contract month:

INITIAL standings for DECEMBER

Dec 16/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 32,150.000 (1ooo kilobars) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 265 contracts

26500 oz |

| No of oz to be served (notices) | 1304 contracts

(130,400 oz) |

| Total monthly oz gold served (contracts) so far this month | 761 contracts(76,100 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 189,048.5 oz |

Total customer deposits nil oz

DECEMBER INITIAL standings/

Dec 16/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 159,189.32 oz

Brinks,CNT,Scotia), |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 150,679.17 oz

Scotia |

| No of oz served today (contracts) | 0 contract

nil oz |

| No of oz to be served (notices) | 329 contracts

(1,645,000 oz) |

| Total monthly oz silver served (contracts) | 3599 contracts (17,995,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,631,771.6 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

we had no dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposit:

i) Into Scotia:150,679.17

total customer deposits: 150,679/17 oz

total withdrawals from customer account: 159,189.320 oz

we had 2 adjustments:

Out of CNT:

we had 4983.46 oz leave the customer account and this landed into the dealer account of CNT

Out of Brinks:

4931.300 oz leaves the dealer account and this landed into the customer account of Brinks

And now the Gold inventory at the GLD:

dec 16/no changes in gold inventory at the GLD/inventory rests at 643.63 tonnes.

Dec 15.2105/no changes in gold inventory at the GLD/Inventory rests at 643.63 tonnes

Dec 14.no change in gold inventory at the GLD/Inventory rests at 634.63 tonnes

DEC 11/no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

Dec 10.2015/no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

DEC 9/no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

Dec 8/ no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

Dec 7/another huge withdrawal of 4.23 tonnes of gold/inventory rests at 634.63 tonnes

Dec 4/no change in gold inventory at the GLD/Inventory rests this weekend at 638.80

And now your overnight trading in gold and also physical stories that may interest you:

Federal Reserve At End Of Monetary Road

The all important context for Federal Reserve’s interest rate decision, where the Federal Reserve is widely expected to hike interest rates for the first time in nearly a decade has been examined by the insightful Grant Williams. He is very skeptical of the Fed’s ability to continue to control markets much longer … and this is a gross understatement:

None of this has been tried before and, to me, that just demonstrates the dangers. Once you get into a situation like the central banks did in ’08 with this panicking — everyone calls it the Hotel California — you can’t get out. And, so incrementally, they have to keep doing something. Instead of stepping back and letting free markets and business cycles and forces of nature have their way and flush out all of the impurities in the system, this is what happens. And, yet, this time, for whatever reason, I think since post-Volker, Greenspan has basically started this ball rolling with this knee-jerk reaction to slash interest rates. And, you can kind of understand it, because everyone was still traumatized by the high inflation of the ‘70s. But, they started and they started down that road.

Click the play button above to listen to Chris’ interview with Grant Williams (59m:06s)

DAILY PRICES

Today’s LBMA Gold Prices: USD 1065.75, EUR 975.65 and GBP 710.33 per ounce.

Yesterday’s LBMA Gold Prices: USD 1069.15, EUR 969.53 and GBP 705.31 per ounce.

BREAKING GOLD NEWS and COMMENTARY (16 December, 2015) – Click here

end

This morning gold and silver jump as the dollar is the most crowded trade in the world at 9 trillion usa:

(courtesy zero hedge)

Gold & Silver Jump Ahead Of Fed On Concerns About “World’s Most Crowded Trade”

Is this supposed to happen on the day the Fed’s rate hike is “boosting

confidence in the economy” and telegraphs more gains for the dollar?

Or perhaps these are just early hints that the world’s most crowded trade, being long the USD, is starting to crack?

(courtesy Koos Jansen and Willem Middelkoop)

Koos Jansen interviews Willem Middelkoop about dollar imperialism

Submitted by cpowell on Wed, 2015-12-16 04:38. Section: Daily Dispatches

11:36p ET Tuesday, December 15, 2015

Dear Friend of GATA and Gold:

Financial journalist and fund manager Willem Middelkoop, interviewed by gold researcher and GATA consultant Koos Jansen, tonight explains, as GATA long has tried to explain, how control of the currency markets and particularly the world reserve currency remains the primary mechanism of imperialism.

“Because it can print the world currency,” Middelkoop says, “the United States can buy anything it wishes without having to worry about its liabilities. … By ‘obliging’ foreign central banks to keep their monetary reserves in Treasury bonds, the United States in fact forced them to finance U.S. military spending abroad, as Michael Hudson explains in his book ‘Super Imperialism.’

“In this new form of imperialism, the United States is able to rule not through its position as world creditor but as world debtor. … A Chinese market commentator remarked: ‘World trade is now a game in which the United States produces dollars and the rest of the world produces things that dollars can buy … a dollar hegemony that forces the world to export not only goods but also dollar earnings from trade to the United States. … Everyone accepts dollars because dollars can buy oil.’

“Only when dollar-holding nations decide to buy natural resources instead of U.S. Treasuries is the dollar’s reserve currency status in danger. This is exactly the exit strategy China and Russia seem to be playing right now.”

Jansen’s interview with Middelkoop is headlined “Interview with Willem Middelkoop about the Big Reset” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/koos-jansen/interview-willem-middelkoo…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

And now your overnight WEDNESDAY morning trading in bourses, currencies, and interest rates from Europe and Asia

1 Chinese yuan vs USA dollar/yuan falls in value , this time to 6.4748/ Shanghai bourse: in the green (even though last hr sell off), hang sang: green

2 Nikkei closed up 484.01 or 2.61%

3. Europe stocks all in the green /USA dollar index up to 97.24/Euro down to 1.0921

3b Japan 10 year bond yield: rises to .304 !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 121.43

3c Nikkei now just above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 37.15 and Brent: 37.90

3f Gold up /Yen down

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .643% German bunds in negative yields from 5 years out

Greece sees its 2 year rate fall sharply to 7.65%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield rises to : 8.62% (yield curve upward sloping)

3k Gold at $1065.10/silver $13.86 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble down 30/100 in roubles/dollar) 70.25

3m oil into the 37 dollar handle for WTI and 38 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9905 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0822 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/arrests 10 traders for Euribor manipulation

3r the 5 year German bund now in negative territory with the 10 year rises to + .643%/German 5 year rate negative%!!!

3s The ELA lowers to 82.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.27% early this morning. Thirty year rate at 3% at 2.99% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, US Futures Greet Historic Fed Day With Euphoria

The day has come when the boxed-in Fed has no choice: with the vast majority of the market expecting a rate hike, Yellen has to deliver or suffer a crushing confidence blow like no other. And deliver she will, with expectations that said hike will be “as dovish as possible”, which however as we explained yesterday, is not really possible. For now however, the market is desperate to convince itself that just as more easing and more QE were bullish for the market, so rate hikes are just as bullish. Recall from late 2013: “tapering is not tightening,” then the 2015 version of this refrain is “tightening is not tightening.”

It remains to be seen just what happens after the Fed’s announcement but in the last few hours before it, the surge higher in global stocks and equity futures continues as the last ounces of a “dovish rate hike” are fully priced in. Asian and European stocks, S&P futures all rise ahead of Federal Reserve’s rate decision. The Dollar is little changed vs euro. Oil, however, has held its losses after late news last night that the U.S. plans to lift the 40-year-old ban on crude oil exports, which in itself will have little impact on oil prices, but as Virendra Chauhan at Energy Aspects in Singapore says “The deal to lift the crude ban is a significant change in U.S. policy, but in terms of the near-term impact on prices, we expect that to be blotchy and sentiment driven. All that you’re doing is transferring the glut from the U.S., where most of the storage capacity is, to elsewhere in the world.“

So with less than 8 hours until the Fed’s historic announcement – and for the best indicator of how the market will respond to the Fed’s announcement at 2pm just keep an eye on the USDJPY as it will dictate every other class, this is where we stand.

- S&P 500 futures up 0.6% to 2049

- Stoxx 600 up 0.5% to 361

- FTSE 100 up 0.6% to 6055

- DAX up 0.3% to 10484

- German 10Yr yield up less than 1bp to 0.64%

- Italian 10Yr yield down 1bp to 1.67%

- MSCI Asia Pacific up 2.1% to 129

- Nikkei 225 up 2.6% to 19050

- Hang Seng up 2% to 21701

- Shanghai Composite up 0.2% to 3516

- S&P/ASX 200 up 2.4% to 5028

- US 10-yr yield up less than 1bp to 2.27%

- Dollar Index up 0.09% to 98.31

- WTI Crude futures down 1.1% to $36.94

- Brent Futures down 2.3% to $37.55

- Gold spot up 0.4% to $1,065

- Silver spot up 0.3% to $13.83

Aside from the Fed countdown, here are some of main overnight news:

- Congress Reaches Fiscal Agreement That Ends U.S. Oil Export Ban: Plan extends solar, wind energy credits backed by Democrats

- Global Payments to Buy Heartland Payment for About $4.3b: Stock and cash deal has transaction value of $100 per share

- Pershing Square Lost 19.7% YTD, Ackman Says in Holder Letter: 3Q net redemptions totaled $39m, or 0.2% of capital

- Third Avenue Bled Managers, Billions of Assets Before Fund Shut: Assets plunged to $8b from $26b in 2006

- GE Capital Prepares to Sell Spain Credit Business: Expansion; Business mostly made up of mortgages, volume of ~EU600m

- Pichai Says Google Making Changes to Suit Non-English Speakers: Google starting program to train 2m Android developers

- Valeant CEO Said to Be on List for Drug Price Hearing: Lawmaker writes Valeant CEO threatening subpoena for documents

- Norfolk Southern Says CP Response ‘Flatly Wrong’ on Facts, Law: Canadian Pacific hasn’t sought declaratory order from Surface Transportation Board on proposed voting trust structure, Norfolk Southern says

- Constant Contact Gets SEC Subpoena: SEC seeks documents on sales, marketing, customer retention practices, disclosure of financial and operating metrics

As noted above, overnight markets were in a euphoric state, starting in Asia where stocks traded higher tracking the positive close on Wall St., following the continued rebound seen in energy prices ahead of the FOMC meeting later on today. The energy sector outperformed across all bourses, particularly in China where the sector rose by more than 6% in the Hang Seng (+2.0%) index.

Nikkei 225 (+2.6%) was led higher by telecom stocks, which were supported after Japan’s communication ministry panel did not push for mobile carrier rate cuts.

“Markets had time to prepare for this day, with investors winding back risks ahead of the event,” Tim Schroeders, a portfolio manager who helps oversee about $1 billion in equities at Pengana Capital Ltd. in Melbourne, said by phone. “What happens after the Fed rate hike is difficult to tell, especially since we’re coming into a quiet period around Christmas and New Year.”

10yr JGBs traded lower as the firm risk sentiment in markets dampened demand for safer assets, while the BoJ entered the market to purchase JPY 1.1trl in government bonds.

Top Asian News

- MSCI Asia Pacific rises for first time in 7 days. The gauge lost more than 4% in the previous six sessions, reaching the lowest level since Oct. 2.

- China Growth May Slow to 6.6 Percent in 2016, Researchers Say: Chinese Academy of Social Sciences predicted “slow bull” market

- Developing Asian Bond Market Set to Top Japan as Funds Go Global: Philippines, Indonesia yield spreads widen versus Japan

- Rupee Faces Moment of Truth With $2.6 Billion Outflow Before Fed: Currency has weakened 2.4% percent since end of Oct.

- Saudi Arabia Spends Billions to Get Asia Hooked on Its Crude Oil: Aramco has invested in 3 processing facilities in Asia

- Packer Said in Talks to Take Crown Resorts Assets Private: Billionaire speaks with PE firms, pension funds on possible bid

- Piquant Hedge Fund Closes After Failing to Attract Investors: The $20m Singapore quant fund stopped trading in June

In Europe, despite opening in the green, European equities (Euro Stoxx: +0.6%) briefly slipped into the red before then moving higher again in what has been a choppy session so far. In terms of a sector specific breakdown, defensive sectors lead the way higher, namely healthcare, while the energy sector continues to outperform after WTI and Brent managed to avoid fresh multiyear lows in the wake of yesterday’s build in API crude oil inventories.

Despite the early lack of direction in equity markets, with sentiment on edge today Bunds have moved higher throughout the European morning and reside in positive territory with analysts at Informa noting that bund options have been attracting some mixed put interest, while the curve steepening has slowed ahead of the FOMC decision later today. This comes after heavy losses seen in the German benchmark yesterday, and amid light supply today.

Top European News

- Julius Baer Will Buy Commerzbank’s Luxembourg Unit to Add Assets: Adds EU3b in assets under management

- Casino to Cut Debt by More Than EU2b in 2016: Plans to sell some of its real estate in Thailand and Colombia

- Rolls-Royce Culls Top Managers as East Responds to Profit Slump: CEO takes direct charge of business divided into five units

- SSAB Falls to 14-Year Low After Warning of 4Q Loss: European, North America steel volumes significantly weaker than forecast

- Carney Says Conditions for a U.K. Rate Hike Aren’t Yet in Place: U.K. is in a ‘low-for-long’ interest-rate environment

In FX markets, the USD dictated play this morning, with the greenback gaining against EUR, GBP and JPY, with levels being broken in the form of the 122.00 level to the upside in USD/JPY and 1.5000 to the downside in GBP/USD. This morning has seen a number of data points out of Europe (Manufacturing PMI 53.10 vs. Exp. 52.80) and the UK (Jobless Claims Change 3.9K vs. Exp. 0.8K), however with reactions relatively muted given the focus on the FOMC later.

Asia-Pacific hours saw the continued divergence between CNH and CNY, with analysts at Informa noting that according to Citi data, short positions in CNH fell marginally last week, while contrasting data from BofAML shows that real money names have resumed selling after a brief spell of being net buyers.

The energy complex heads into the North American crossover seeing softness across the board, with WTI and Brent both in the red on the day, with the former residing around the USD 37.00/bbl handle and the latter below the USD 38.00/bbl handle. This comes after API crude oil inventories showed a build of 2300k (Prey. -1900k) and ahead of DoE crude oil inventories later today (Exp. -1500k, Prey. -3568k).

Gold was stable overnight and trades in modest positive territory as participants remained tentative ahead of today’s much awaited, key-risk FOMC decision. Elsewhere, copper and iron prices were mildly supported amid short-covering and an improvement in global risk sentiment. Finally, steel rebar futures showed some signs on stabilising overnight after the May future rose 1 %, although analysts warn that gains could be short-lived due to a lack of demand in China.

As well as the aforementioned Fed rate decision, today sees US housing starts, building permits and manufacturing PMI.

Bulletin Headline Summary from Bloomberg and RanSquawk

- European equities drift higher after early choppiness to trade in positive territory in line with their US and Asian counterparts

- USD heads into the North American crossover near intraday highs, with gains seen against GBP and JPY

- Today sees one of the biggest events of the year in the form of the Fed rate decision, with housing starts, building permits, manufacturing PMI and DoE’s also scheduled from the US

- Treasuries little changed as market awaits FOMC rate decision and Yellen presser amid expectations Fed will increase interest rates for first time in almost a decade.

- Barring a shock, investors are about to find out how much stocks are worth in the absence of Fed support that has helped restore $15 trillion to share values since 2009

- Currency traders are on alert for a repeat of dollar declines that followed the start of tightening cycles in 2004, 1999 and 1994 on speculation that a boost is already in the price

- Merkel’s party colleagues expressed growing dismay at the prospect of a British exit from the European Union, with one lawmaker portraying Cameron’s planned referendum as an “existential risk” for Europe

- U.K. wage growth slowed more than economists forecast, reinforcing the case for the Bank of England to keep borrowing costs at a record-low for now

- Congressional leaders unveiled a broad package of spending and tax legislation that would avert a U.S. government shutdown and lift the 40-year-old ban on crude oil exports

- Donald Trump’s rivals still haven’t figured out how to land a fatal blow against their party’s front-runner. That was true again on Tuesday, as the New York businessman survived the latest meeting of the party’s White House contenders

- No IG or HY deals yesterday. BofAML Corporate Master Index OAS holds at +174, YTD range 180/129. High Yield Master II OAS tightens 24bp to +709 after reaching new YTD wide Tuesday; YTD low 438

- Sovereign 10Y bond yields mostly lower. Asian stocks gain, European stocks and U.S. equity- index futures rise. Crude oil lower, gold and copper higher

US Event Calendar

- 7:00am: MBA Mortgage Applications, Dec. 11 (prior 1.2%)

- 8:30am: Housing Starts, Nov., est. 1.130m (1.060m)

- Housing Starts m/m, Nov., est. 6.6% (prior -11%)

- Building Permits, Nov., est. 1.150m (prior 1.150m, revised 1.161m)

- Building Permits m/m, Nov., est. -1% (prior 4.1%, revised 5.1%)

- 9:15am: Industrial Production, Nov., est. -0.2% (prior -0.2%)

- Capacity Utilization, Nov., est. 77.4% (prior 77.5%)

- Manufacturing (SIC) Production, Nov., est. 0.0% (prior 0.4%)

- 9:45am: Markit US Manufacturing PMI, Dec. P, est. 52.6 (prior 52.8)

- 2:00pm: FOMC Rate Decision, est. 0.25% to 0.5% range (prior 0% to 0.25% range)

- 2:30pm: Fed’s Yellen holds news conference in Washington

DB’s Jim Reid concludes the rest of the overnight wrap

Despite Oil markets down around half a percent this morning, bourses in Asia are following much of the strength from yesterday’s showing in the US and Europe. There are broad-based gains across the bulk of the region with +2% gains for the Nikkei, Hang Seng, Kospi and ASX. Markets in China haven’t quite been as impressive although the Shanghai Comp and CSI 300 are still up +0.71% and +0.41% respectively. Credit markets across Asia, Australia and Japan are generally 2-3bps tighter also. US politics is also attracting a bit of attention with the news that US congressional leaders have agreed on a plan that will see the 40-year old ban on crude oil exports lifted. According to the FT the new spending plan would also avoid a looming possible government shutdown. The House is due to vote on the bill on Thursday.

On another day yesterday’s data would have probably garnered more attention than it perhaps got. That being said, yesterday’s inflation numbers in the US coming in more or less in line with expectations will have given FOMC policymakers one last sigh of relief. Headline CPI for November printed at 0.0% mom which was in-line with expectations, while the YoY rate nudged up to the highest this year at +0.5% (vs. +0.4% expected), a rise of three-tenths from October as some of the energy price reductions rolled out from last year. The monthly core reading also met expectations at +0.2% mom which has helped to push the YoY rate up one-tenth to +2.0%. Meanwhile, the December Empire manufacturing reading improved to -4.6 from -10.7 in November, with the new orders and inventories components also showing improvement. Elsewhere the NAHB housing market index was down 1pt this month to 61 (vs. 63 expected) and has dipped lower for two consecutive months now.

Over in Europe we saw the German ZEW survey for December rise 0.6pts to 55.0 (vs. 54.2) with the expectations survey also up, rising 5.7pts to 16.1. Over in the UK, headline CPI was a bit better than expected last month although still at a lowly 0.0% mom (vs. -0.1% expected). The YoY rate edged up two-tenths to +0.1% while the core was up one-tenth to +1.2% as expected. Sweden also generated a few headlines after the Riksbank made no change to its current policy rate of -0.35% and its current asset purchasing program, while also coming across a bit more hawkish than anticipated in its post-meeting statement.

Looking at the day ahead, the focus in the European session this morning is set to be on the flash December PMI’s where we’ll get the manufacturing, services and composite prints for the Euro area, Germany and France. The latest batch of UK employment indicators are also expected this morning, along with the November Euro area CPI reading. It goes without saying that the focus this afternoon will be on the conclusion of the two-day FOMC meeting where we’ll get the decision at 7pm GMT. The associated dot plots and any potential revisions will be closely scrutinized, while Fed Chair Yellen’s post meeting press-conference will also be in the spotlight. Prior to this, the economic data due out in the US today includes November housing starts and building permits, industrial and manufacturing production, capacity utilization and finally the flash December manufacturing PMI.

See you all on the other side.

ASIAN AFFAIRS

Denmark To Confiscate Gold, Jewelry, & Valuables From Refugees

Submitted by Simon Black via SovereignMan.com,

It started on December 8, 1931.

Germany was in a world of pain at the time. They were still financially debilitated from having to make reparation payments after losing World War I, and had just barely recovered from one of the worst bouts of hyperinflation in recorded history.

By the early 1930s, the onset of the Great Depression had taken hold in Germany, driving the government to desperation once again.

They needed cash. And rather than go back to the printing press and risk hyperinflation again, German President Paul von Hindenburg signed a decree to create a new tax called the Reichsfluchtsteuer, nearly 84 years ago to the day.

It was an exit tax… a type of capital control to dissuade people from leaving with their savings.

So any German citizen with a certain level of income or assets who left the country would be charged a 25% wealth tax.

The following year, in 1932, the government generated about 1 million marks in revenue from the tax.

Of course since the tax was a ‘temporary’ measure, it was set to expire at the end of 1932.

But they extended it. And kept extending it.

By 1938, the German government collected an astounding 346 million marks from this tax.

This nearly 350x increase in tax revenue over 6 years is incredible, making the Reichsfluchtsteuer one of the fastest growing taxes in human history.

(By comparison, income tax receipts in the United States grew about 9-fold in the first six years of its history.)

So what was the German government’s secret in having so much success with this tax?

Simple. Their secret was the Secret Police.

By the late 1930s, the Nazis had taken over.

And even though there was no longer a reason to keep the Reichsfluchtsteuer on the books since the Depression had largely subsided, the Nazi regime kept extending the law, using it almost exclusively to target Jewish citizens.

In fact, the Reichsfluchtsteuer became one of the core components of the Nazi’s confiscation strategy to plunder Jewish wealth.

Now, I couldn’t help but think of the Reichsfluchtsteuer when I heard about the government of Denmark’s latest tactic against refugees today.

This isn’t even something that has made the international, English-language news. We just happen to have a Danish-speaking member of our team.

As he explained to me, Danish Justice Minister Soren Pind recently announced his intention to have border guards confiscate gold, jewelry, diamonds, and other valuables from refugees as they enter the country.

After a bit of popular backlash, wedding rings are now off limits.

But just about anything else ranging from cash to expensive wristwatches, is fair game for confiscation, as long as the ‘loot’ (as they call it) is valuable.

So apparently Danish border guards are expected to discern whether a refugee is wearing a $15,000 IWC Schaffhausen or a $15 knock-off.

(Clearly they spent a lot of time thinking about this policy and how to implement it.)

Having armed men indiscriminately seize refugees’ personal belongings doesn’t strike me as the best representation of a free society. Not that this matters anymore.

The Danish government’s excuse is that they need to confiscate assets from refugees in order to pay for the services they’re providing to those same refugees.

This might even sound reasonable… until you realize that a government could make the same argument for every other public service they provide.

It’s the same logic as confiscating funds from your bank account in order to provide you with the FDIC. Or seizing other assets to provide ‘free’ healthcare or education.

When a government awards itself the authority to attack one particular group, they give themselves that same power to attack everyone.

In the Land of the Free, they call it Civil Asset Forfeiture– a legal form of theft in which the government can administratively steal your assets with no Constitutionally guaranteed due process.

The US government stole $4.5 billion worth of private property from its citizens last year alone, far more than the $3.9 billion stolen by common thieves according to FBI data.

The trend is pretty obvious—governments are not shy at awarding themselves the authority to take whatever they want, whenever they want, from whomever they want.

And they’ll always come up with a good excuse to justify it.

This risk is not negligible. So as an insurance policy, it makes sense to ensure that you’re not holding 100% of your assets and savings within the control of a single government.

After all, they may one day be so desperate that they’ll steal from you in the name of protecting you.

END

The Humiliation Is Complete: Assad Can Stay, Kerry Concedes After Meeting With Putin

Back on September 20 (so, a full ten days before a three star Russian general strolled into the US Embassy in Baghdad to let the US know that airstrikes in Syria “start in 1 hour”), we said that the US strategy in Syria had officially unraveled.

At the time, John Kerry had just concluded a meeting with British Foreign Secretary Philip Hammond in London. “For the last year and a half we have said Assad has to go, but how long and what the modality is, that’s a decision that has to be made in the context of the Geneva process and negotiation,” Kerry told reporters after the meeting. “It doesn’t have to be on day one or month one [and] there is a process by which all the parties have to come together and reach an understanding of how this can best be achieved.”

“That this a far, far cry from the hardline rhetoric the US was still clinging to just months ago,” we said, adding that “it marks a tacit recognition of what should have been obvious from the very beginning: the US backed effort to assist Qatar and the Saudis in destabilizing the Assad regime was doomed from the start.”

About a month later, ahead of talks in Vienna, WSJ said the following about Washington’s plans for Assad:

The Obama administration entered a crucial round of international talks on Syria’s war prepared to accept a deal that leaves President Bashar al-Assad in place for several months or more during the transition to a new government.

The U.S. shift on the dictator’s future caps months of backtracking on the most significant obstacle to a resolution of the Syrian conflict. While U.S. officials once argued Mr. Assad couldn’t take part in a political transition, they have gradually eased that stance, eventually signaling he wouldn’t have to step down immediately. Now they are planning to negotiate the question of his future in talks being held Friday in Vienna.

The solution Washington sought to broker would “not prejudge the Assad question,” a senior administration official told The Journal.

Of course the Assad “question” has already been “prejudged” – only not by Washington or any of its regional allies. As we’ve been at pains to explain, Tehran isn’t going to allow a US puppet government to be installed in Damascus. It’s out of the question. Losing Damascus to Washington and worse, to Riyadh, would severely impair Iran’s supply lines to Hezbollah and roll back Iranian influence in the region. For Russia, the stakes are also high. Moscow now has an air base and a naval base in Syria and establishing a foothold in Syria is the first step for The Kremlin on the way to supplanting the US as Mid-East superpower puppet master. In short, even is Assad himself ultimately abdicate, the regime (and our apologies for anyone who finds that term pejorative) will remain in one form or another.

On Tuesday, Kerry was in Russia for talks with Vladimir Putin. As Foreign Policy notes, America’s top diplomat was “wicked psyched” that he found a Dunkin Donuts in Moscow:

As for negotiations with Putin over Syria, it appears the humiliation is now complete.

As AP reports, “U.S. Secretary of State John Kerry on Tuesday accepted Russia’s long-standing demand that President Bashar Assad’s future be determined by his own people, as Washington and Moscow edged toward putting aside years of disagreement over how to end Syria’s civil war.”

“The United States and our partners are not seeking so-called regime change,” Kerry said, adding that the focus is no longer “on our differences about what can or cannot be done immediately about Assad.”

In a testament to the fact that mainstream media is beginning to understand just how weak America’s negotiating position has become, AP offered the following rather sarcastic assessment:

President Barack Obama first called on Assad to leave power in the summer of 2011, with “Assad must go” being a consistent rallying cry. Later, American officials allowed that he wouldn’t have to resign on “Day One” of a transition. Now, no one can say when Assad might step down

Kerry also called demands by the “moderate” opposition that Assad step down before peace negotiations begin an “obvious nonstarter.”

http://graphics8.nytimes.com/video/players/offsite/index.html?videoId=100000004094144

But even as Kerry and Sergei Lavrov hailed the talks as a “big negotiating day,” Lavrov’s de facto deputy, the sharp-tongued Maria Zakharova, stressed that “serious differences” remain between the US and Russia with regard to Syria.

One point of contention is Washington’s insistence on differentiating between “moderate” and “non-moderate” elements operating to oust the Assad government.

That and other pressing issues are expected to be discussed next week in New York at what Kerry says will be a “major international conference” on Syria.

As for relations between Moscow and Washington, Kerry said this: “There is no policy of the United States, per se, to isolate Russia.”

Right. No “per se” policy. So in other words, it may not be an explicit, de jure mandate, but it sure as hell seems like a tacit, de facto foreign policy position.

Caught On Tape: Chaotic Aftermath Of A Russian Strike On ISIS Oil Tankers

On Tuesday, Lieutenant General Sergey Rudskoy, chief of the main operations department of the Russian General Staff, gave reporters an update on Moscow’s efforts to squeeze ISIS by dismantling the group’s illicit oil trade from the air.

“The intensity of air strikes at Islamic State and other terrorist targets has been increased, Rudskoy told reporters, adding that The Kremlin’s warplanes have destroyed six oil production facilities and seven truck convoys in the past three days alone.

The Russian MoD – which had made a habit of documenting Moscow’s military exploits in Syria on the way to making Washington’s 15-month effort look ineffectual by comparison – was also out with some fresh commentary on the effort to cripple Islamic State’s illegal crude trafficking business. “Russian air strikes have helped to halve the Islamic State’s proceeds from illegal oil trade from $3 million to $1.5 million,” TASS reported, citing the defense ministry.

According to the Syrian Observatory For Human Rights – which, you’re reminded, is essentially one man operating from London on tips he receives from a network of “sources” on the ground – Russian warplanes struck “a fuel market in Idlib on Tuesday, destroying tanker trucks, setting huge fires and killing 16 people.”

While it’s impossible to conclusively verify the death toll or who actually conducted the strikes, it does indeed appear that someone “struck oil” (so to speak) in Idlib yesterday and for those wondering what the situation on the ground looks like after the Russians hit terrorist oil convoys, we present the following video with no further comment:

Baltic Dry Crashes To New Record Low As China “Demand Is Collapsing”

Despite a brief dead-cat-bounce late November, which Jim Cramer heralded as evidence of stabilization in China, the world’s best known freight index has collapsed to new all-time record lows this morning. Amid a persistent glut of ships and ongoing concerns about Chinese steel imports, The Baltic Dry has tumbled to 471 – the lowest level in at least 30 years.

Worst. Ever.

As Bloomberg adds, China, which makes about half the world’s steel, is on track for the biggest drop in output for more than two decades, according to data compiled by Bloomberg Intelligence…

Owners are reeling as China’s combined seaborne imports of iron ore and coal — commodities that helped fuel a manufacturing boom — record the first annual declines in at least a decade. While demand next year may be a little better, slower-than-anticipated growth in 2015 has led to almost perpetual disappointment for rates, after analysts’ predictions at the end of 2014 for a rebound proved wrong.

“It doesn’t help that Chinese steel production is about to see the most dramatic decline to the lowest in 20 years,” said Herman Hildan, a shipping-equity analyst at Clarksons Platou Securities in Oslo. “Demand growth is collapsing.”

* * *

Sounds like a perfect time to hike rates and exaggerate the deflationary tsunami and monetary outflows from the world’s potentially growing economies.

Brazil Stocks, Currency Tumble After Fitch Downgrade To Junk

It was just last Thursday when we previewed what we said would likely be further downgrades for Brazil on the heels of S&P’s move to cut the country to junk in September.

Here’s what we said:

On the heels of the S&P move, the political “dynamics” have become less favorable despite some observers’ contention that the further we move down the road to a Rousseff impeachment, the happier the market will be given her track record. House Speaker Eduardo Cunha faces an investigation by the ethics committee in connection with his alleged role in the Carwash scandal while the relationship between Rousseff and VP Michel Temer looks increasingly tenuous. Meanwhile, the arrest of Delcidio Amaral seemed to have ushered in a new era wherein sitting lawmakers aren’t above the law and may be too busy looking over their shoulders going forward to legislate. All of this casts considerable doubt on the country’s ability to overcome fractious politics on the way to adopting some semblance of fiscal rectitude.

As for “economic turmoil,” well, Brazil has effectively descended into a depression since S&P’s downgrade. GDP is collapsing, inflation is sitting at 10.5%, a 12-year high, and unemployment is soaring. Everything that could possibly go wrong economically is going wrong and thanks to rising prices and the incipient threat of lagged FX pass through, Copom is powerless to adopt counter-cyclical policies and will in fact be forced to hike in January.

We then proceeded to go agency by agency courtesy of four graphics from Credit Suisse. Here’s the visual for Fitch:

Sure enough, just moments ago, the ratings agency cut Brazil to junk. Here’s the bullet point summary:

- FITCH SAYS BRAZIL GENL GOVT DEBT TO INCREASE FURTHER IN 2017

- FITCH: BRAZIL GENL GOVT DEBT TO REACH OVER 70% GDP IN 2016

- FITCH DOWNGRADES BRAZIL TO ‘BB+’; OUTLOOK NEGATIVE

- BRAZIL CUT TO BB+ FROM BBB- BY FITCH

- FITCH SAYS BRAZIL’S ECONOMIC SLUMP ISN’T ABATING

- FITCH NOW SEES BRAZIL’S GROWTH OF -3.7% IN ’15

- FITCH NOW SEES BRAZIL’S GROWTH OF -2.5% ’16

- FITCH SEES BRAZIL GENERAL GOVT FISCAL DEFICIT OVER 10% GDP ’15

- FITCH: BRAZIL GENL GOVT FISCAL DEFICIT AVG OVER 7% GDP ’16-’17

The reaction in the beleaguered BRL:

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings/WEDNESDAY morning 7:00 am

Euro/USA 1.0921 down .0012

USA/JAPAN YEN 121.80 up .121

GBP/USA 1.5017 down .0028

USA/CAN 1.3750 up .0021

Early this morning in Europe, the Euro fell by 12 basis points, trading now just above the 1.09 level rising to 1.0986; Europe is still reacting to deflation, announcements of massive stimulation (QE), a proxy middle east war, and the ramifications of a default at the Austrian Hypo bank, an imminent default of Greece, Glencore, Nysmark and the Ukraine, along with rising peripheral bond yield, further stimulation as the EU is moving more into NIRP and moving in the opposite direction that they were suppose to with the USA tightening on Dec 16. Last night the Chinese yuan was down in value (onshore). The USA/CNY up in rate at closing last night: 6.4748 / (yuan down)

In Japan Abe went all in with Abenomics with another round of QE purchasing 80 trillion yen from 70 trillion on Oct 31/2014. The yen now trades in a southbound trajectory as settled down again in Japan by 12 basis points and trading now further to that all important 120 level to 121.80 yen to the dollar.

The pound was down this morning by 27 basis points as it now trades just below the 1.51 level at 1.5017.

The Canadian dollar is now trading down 21 in basis points to 1.3750 to the dollar.

We are seeing that the 3 major global carry trades are being unwound. The BIGGY is the first one;

1. the total dollar global short is 9 trillion USA and as such we are now witnessing a sea of red blood on the streets as derivatives blow up with the massive rise in the rise in the dollar against all paper currencies and especially with the fall of the yuan carry trade. The emerging market which house close to 50% of the 9 trillion dollar short is feeling the massive pain as their debt is quite unmanageable.

2, the Nikkei average vs gold carry trade (blowing up)

3. Short Swiss franc/long assets (European housing/Nikkei etc. This has partly blown up (see Hypo bank failure).(blew up)

These massive carry trades are terribly offside as they are being unwound. It is causing global deflation ( we are at debt saturation already) as the world reacts to lack of demand and a scarcity of debt collateral. Bourses around the globe are reacting in kind to these events as well as the potential for a GREXIT>

AND NOW WE AWAIT THE DECISION OF THE USA TO RAISE RATES AND THE DILEMMA THEY FACE. SOMEONE ELSE MUST DO QE TO REPLACE LOST LIQUIDITY (800 billion of liquidity will be withdrawn on a 1/4% rise in rates)

The NIKKEI: this WEDNESDAY morning: up 481.08 or 2.61%

Trading from Europe and Asia:

1. Europe stocks all in the green

2/ Asian bourses all in the green… Chinese bourses: Hang Sang green (massive bubble forming) ,Shanghai in the green barely/last hr sell off/ / (massive bubble ready to burst), Australia in the green: /Nikkei (Japan) green/India’s Sensex in the green /

Gold very early morning trading: $1064.00

silver:$13.81

Early WEDNESDAY morning USA 10 year bond yield: 2.27% !!! par in basis points from TUESDAY night and it is trading at resistance at 2.27-2.32%. The 30 yr bond yield falls to 2.99 par in basis points.

USA dollar index early WEDNESDAY morning: 98.24 up 11 cents from TUESDAY’s close. ( Now below resistance at a DXY of 100)

This ends early morning numbers WEDNESDAY MORNING

end

OIL RELATED STORIES

Last night:

Oil breaks below 37 dollars again after the huge buildup in API inventories:

(courtesy API/zero hedge)

WTI Slumps Under $37 After API Reports Unexpected, Large Inventory Build

Following last week’s huge draw, total crude inventories were expected to drop 1 million barrels this week driven by expectations that refinery utilization rose last week. When API reported a hugely surprising 2.3 million barrel build, crude prices, which had drifted off highs after NYMEX close, dropped further as disappointment set in, back under $37.

A majorly unexpected build…

Ansd crude prices slumped back under $27…

Charts: Bloomberg

end

Today: DOE also reports a huge December inventory build. It was the biggest gain in inventory levels in 22 years:

(courtesy DOE/zero hedge)

Crude Crashes To $35 Handle After Biggest December Inventory Build In 22 Years

Following last night’s surprising 2.3mm barrel inventory build, reported by API, DOE reports a massive 4.8mm build against expectations of a 1.5mm barrel draw and way above the highest estimate of a 2.6mm draw. This is the biggest build in 2 months at a seasonally ‘weak’ time of year (and biggest December build since 1993). Crude ramped overnight to regain the losses from the API dump, but dropped back to lows (under $37) before the DOE data, then crashed below $36. Furthermore, production was up in the lower 48.

Biggest build in 2 months…

This is the biggest Mid-December build sicne 1993…

And production rose…

Crude prices collapsed lower…

Charts: Bloomberg

Fed’s First Rate Hike In 9 Years Sparks “Goldilocks” Buying Of Risk Assets

What else is there to say…

Despite an initial disappointment in stocks, once Janet started speaking, traders started panic-buying… coz everything is awesome…

Best 3 days since October…

Panic-Buying NFLX as soon as Yellen started speaking…

Oil dumped and stocks pumped post-Yellen… (it looks like the move was all pegged on her jawboning beginning at 1130)…

Leaving stocks soaring on the week…

Energy credit market continued to collapse (and energy stocks fell)…

And bond yields were considerably higher heading in to the decision, the long-end dumped right after the decision (policy error) before yields surged back higher along with every risk-on asset as Yellen spoke… 2s30s was ucnhanged!!

Bond started dumping as soon as Yellen spoke…

Commodities were mixed with some big swings around 8amET (PMs surged) but crude tumbled after the DOE data and copper faded…

Crude plunged…

Charts: Bloomberg

Fed Hikes Rates, Unleashing First Tightening Cycle In Over 11 Years

On the 7th anniversary of entering ZIRP, and for the first time since June 29th 2006, The Federal Reserve announced today that it will try and raise interest rates:

*FED RAISES INTEREST RATES 0.25 POINT IN UNANIMOUS VOTE

Of course, the flowery language and dots are as dovish as possible while maintaining some semblance of credibility with regard growth expectations as The Fed unleashes a tightening cycle for the first time in over 11 years.

Pre-FOMC: S&P Futs 2050, 2Y 98bps, 10Y 2.29%, Gold $1072, Oil $36, EURUSD 1.0960

Heading into the decision, gold and silver suddenly started to fade, bond yields slid notably, and the USD jerked lower.

Fed Headlines:

* * *

What’s happened since The Fed folded in September? Macro “data” got worse… Market “data” got better…

The Fed has never raised rates in December when stocks were down over the last 6 months…

h/t @RyanDetrick

And when it has raised rates in December, stocks have pushed lower.

The Fed is raising rates today with the VIX above 20 for the first time since 2000…

That did not end well…

The Fed is also raising rates with Junk bonds trading worse that after Lehman…

* * *

Full Redline below:

end

Fed Mouthpiece Reads Liftoff Tea Leaves

Well, liftoff has officially begun.

Assuming 25 bps doesn’t tip EM into crisis and/or trigger some kind of dramatic, unforeseen meltdown elsewhere, the Fed is about to embark on the first rate hike cycle in over a decade.

Of course the hike itself isn’t what’s interesting – virtually no one thought the Fed would fold again, even as China did its best to create a bit of pre-Yellen drama by stirring up the deval fears with a nod to a new trade-weighted index for the yuan.

In short, it’s now all about reading the “flight path” tea leaves and when it comes to the FOMC and tea leaf reading, there’s only one man for the job.

The latest from WSJ’s Jon Hilsenrath is below.

The Federal Reserve said it would raise its benchmark interest rate from near zero for the first time since December 2008, and emphasized it will likely lift it gradually thereafter in a test of the economy’s capacity to stand on its own with less support from super-easy monetary policy.

Fed officials said they would move up the federal funds rate by a quarter percentage point on Thursday, to between 0.25% and 0.5%, and would adjust their strategy as they see how the economy performs. At these low rates, they added, policy remains accommodative.

“The [Fed] expects economic conditions will evolve in a manner that will warrant only gradual increases in the fed funds rate,” the Fed said in a statement following its two-day meeting. To hammer home this point, officials added in a second place in their statement that they anticipated “gradual adjustments” in rates.

Fed Chairwoman Janet Yellen won a unanimous vote.

New projections show officials expect their benchmark rate to creep up to 1.375% by the end of 2016, according to the median projection of 17 officials, to 2.375% by the end of 2017 and 3.25% in three years. That implies four quarter-percentage-point interest rate increases next year, four the next and three or four the following.

That is a slower pace than projected by officials in September and much slower compared to earlier series of Fed rate increases. In the 2004-06 period, for example, the Fed raised rates 17 times in succession, an approach Fed officials don’t intend to repeat. In September seven Fed officials believed the fed funds rate could rise to 3% or higher by 2017; now just four do.

When the Fed moves next will depend importantly on how inflation evolves. The Fed’s preferred measure of inflation has run below its 2% objective for more than three years. The central bank focused extra attention on the inflation outlook in its statement, saying it would “carefully monitor” actual and expected progress toward the goal. This point implied the Fed will be reluctant to raise rates again unless it sees inflation actually moving up. For now, officials said they were “reasonably confident” inflation would rise.

Ms. Yellen, in a speech and in testimony earlier this month, said a rate increase represented a vote of confidence in the U.S. economy after the deep 2007-09 recession and a long, often-disappointing recovery. Still, uncertainties abound about how markets and the economy will respond in the months ahead.

Any number of factors might throw the central bank off its plans. Persistently low inflation, a shock to the financial system or slowing growth from abroad could force the Fed to delay further rate increases or even reverse course. An unexpected acceleration in economic growth or inflation, or a new financial boom could lead officials to lift borrowing costs more quickly.

For the moment, however, Fed officials see an economy that has made enough progress to warrant a slow retreat from easy money. The jobless rate has fallen to 5% in November from 10% in 2009. Inflation has run below the Fed’s 2% goal for more than three years, but officials believe it will rise in 2016 as slack in the job market diminishes and oil prices stabilize.

“There has been considerable improvement in the labor market,” the Fed said.

Officials predicted the economy would expand at an annual pace between 2.4% in 2016 and 2.0% in 2018, in the process taking the expansion to a decade in length. They saw their preferred measure of inflation rising from 0.4% in 2015 to 1.6% in 2016 and then to 2% by 2018. The jobless rate is seen stabilizing at 4.7% during the next three years. These projections were largely in line with earlier estimates.

Whether other interest rates—on savings accounts, mortgages, car loans, credit cards, corporate loans and beyond—rise as well depends on how investors, businesses and households respond.

Stocks surged in the minutes after the Fed announcement, with the Dow Jones Industrial Average up by triple digits.

The market doesn’t always follow the Fed’s lead. Between 2004 and 2006, when the Fed raised its benchmark short-term rate 4.25 percentage points, yields on 10-year U.S. Treasury notes and corporate bonds and mortgage rates barely budged because of strong global appetite for U.S. securities.

Michael Lussier, chief executive of Webster First Federal Credit Union in Worcester, Mass., said banks and credit unions now could be slow to adjust rates on certificates of deposits and other savings accounts, potentially bad news for retirees looking for higher returns on their fixed income investments.

“You are not going to see an instant change in CDs on Thursday, that’s a guarantee,” he said in an interview ahead of the Fed’s release. A 12-month CD at First Federal yields 0.4%.

The central bank has been telegraphing the rate increase for months. In September it looked close to acting, but turbulence in financial markets and uncertainties about the global growth outlook, particularly in China, caused officials to hold off.

By moving now, the Fed could put new pressure on emerging markets, particularly corporate borrowers in these countries that took out U.S. dollar loans which have gotten more expensive as the dollar rises in value.

The junk bond market is already reeling. Yields on low-rate junk bonds have jumped from 6.61% at the beginning of the year to 8.79%. In the process investors have retreated from junk bond funds, a development that prompted Third Avenue Management LLC last week to suspend withdrawals, which added to investor anxiety about the sector.

To ensure it doesn’t disrupt markets too much, officials noted in their statement that they intended to keep their portfolio of mortgage and Treasury securities large for the time being, avoiding selling securities or letting them mature without rolling them over. It said it wouldn’t reduce its holdings until rate increases were “well under way.” The Fed has assets of $4.5 trillion and shrinking the portfolio could shake up markets.

The Fed’s rate increase goes into effect Thursday. That is when the central bank will begin moving two new levers. One is an interest rate it pays on deposits—known as reserves—which banks keep with the central bank. This rate will move to 0.50% from 0.25%. The other is a rate the Fed pays to money market mutual funds and others on trades known as overnight reverse repurchase agreements, or repos. That rate will move to 0.25% from 0.050%.

Officials expect their benchmark rate, the federal funds rate, which is what banks pay each other for overnight loans, to move toward the middle of the 0.25% to 0.50% channel it is creating with these two other rates.

Officials in 2014 set a $300 billion limit on the amount of reverse repo trades they would conduct with Wall Street firms to maintain the lower bound of the channel. In a technical step to ensure there are no constraints on getting rates where they want them, the Fed on Wednesday said it would lift that cap to around $2 trillion.

The central bank also raised the rate it charges banks on emergency loans, by a quarter percentage point to 1%.

end

Market Confidence In The Fed’s Policy Error (Summed Up In 1 Chart)

While The Fed is confidently rising rates, the market is signalling its belief that this is a policy error. Not only are longer-dated bond yields lower but short-term money-marketexpectations for January now see a higher chance of a rate-cut, than a rate-hike.

Fed Reveals Rate Hike “Plumbing” Details: Removes Cap On Reverse Repos, Limits Each Counterparty To $30 Billion

Perhaps even more important than the actual rate hike announcement, the one statement the market was particularly focused on was the Fed’s “implementation note“, which lays out the Fed’s thought process on how it will actually raise rates in order to maintain the Fed Funds in the 0.25%-0.50% range. What it reveals is that in addition to removing the daily limit on aggregate borrowings through its overnight reverse repurchase facility, previously set at $300 billion (recall that according to Citi, the Fed may need to drain up to $1 trillion in excess liquidity to effect the 25 bps hike), it will have a per counterparty limit of $30 billion per day, which may or may not be enough.

Separately, the Simon Potter’s desk at the NY Fed announced “that the Desk anticipates that around $2 trillion of Treasury securities will be available for ON RRP operations to fulfill the FOMC’s domestic policy directive.”

What is missing from the analysis is how the Fed will approach the fact that securities pledged to the Fed remain outside of the traditional repo pathway, and thus the liquidity shortage among the treasury market is likely to continue if not worsen.

Most of these are in line with expectations. Now it remains to be seen if these theoretically necessary measures will also be practically sufficient.

The full details from the FED:

Decisions Regarding Monetary Policy Implementation

- The Federal Reserve has made the following decisions to implement the monetary policy stance announced by the Federal Open Market Committee in its statement on December 16, 2015:

- The Board of Governors of the Federal Reserve System voted unanimously to raise the interest rate paid on required and excess reserve balances to 0.50 percent, effective December 17, 2015.

As part of its policy decision, the Federal Open Market Committee voted to authorize and direct the Open Market Desk at the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive:

“Effective December 17, 2015, the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1/4 to 1/2 percent, including: (1) overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 0.25 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day; and (2) term reverse repurchase operations to the extent approved in the resolution on term RRP operations approved by the Committee at its March 17-18, 2015, meeting.

The Committee directs the Desk to continue rolling over maturing Treasury securities at auction and to continue reinvesting principal payments on all agency debt and agency mortgage-backed securities in agency mortgage-backed securities. The Committee also directs the Desk to engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve’s agency mortgage-backed securities transactions.”

More information regarding open market operations may be found on the Federal Reserve Bank of New York’s website.

In a related action, the Board of Governors of the Federal Reserve System voted unanimously to approve a 1/4 percentage point increase in the discount rate (the primary credit rate) to 1.00 percent, effective December 17, 2015. In taking this action, the Board approved requests submitted by the Boards of Directors of the Federal Reserve Banks of Boston, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Kansas City, Dallas, and San Francisco.

This information will be updated as appropriate to reflect decisions of the Federal Open Market Committee or the Board of Governors regarding details of the Federal Reserve’s operational tools and approach used to implement monetary policy.

And from the NY Fed:

During its meeting on December 15–16, 2015, the Federal Open Market Committee (FOMC) directed the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York (New York Fed), effective December 17, 2015, to undertake open market operations as necessary to maintain the federal funds rate in a target range of ¼ to ½ percent, including overnight reverse repurchase operations (ON RRPs) at an offering rate of 0.25 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account (SOMA) that are available for such operations and by a per-counterparty limit of $30 billion per day.

To determine the value of Treasury securities available for ON RRP operations, several factors need to be taken into account, as not all Treasury securities held outright in the SOMA will be available for use in such operations. First, some of the Treasury securities held outright in the SOMA are needed to conduct reverse repurchase agreements with foreign official and international accounts. Second, some Treasury securities are needed to support the securities lending operations conducted by the Desk. Additionally, buffers are needed to provide for possible changes in demand for these activities and for possible changes in the market value of the SOMA’s holdings of Treasury securities.

Taking these factors into account, the Desk anticipates that around $2 trillion of Treasury securities will

be available for ON RRP operations to fulfill the FOMC’s domestic

policy directive. In the highly unlikely event that the value of bids received in an ON RRP operation exceeds the amount of available securities, the Desk will allocate awards using a single-price auction based on the stop-out rate at which the overall size limit is reached, with all bids below this rate awarded in full at the stop-out rate and all bids at this rate awarded on a pro rata basis at the stop-out rate.

These ON RRP operations will be open to all eligible RRP counterparties, will settle same-day, and will have an overnight tenor unless a longer term is warranted to accommodate weekend, holiday, and other similar trading conventions. Each eligible counterparty is permitted to submit one proposition for each ON RRP operation, in a size not to exceed $30 billion and at a rate not to exceed the specified offering rate. The operations will take place from 12:45 p.m. to 1:15 p.m. (Eastern Time). Any changes to these terms will be announced with at least one business day’s prior notice on the New York Fed’s website.

The results of these operations will be posted on the New York Fed’s website. The outstanding amounts of RRPs are reported on the Federal Reserve’s H.4.1 statistical release as a factor absorbing reserves in Table 1 and as a liability item in Tables 5 and 6.

Billionaire Sam Zell Warns Fed Too Late, “Recession Likely In Next 12 Months”

When last we checked in with billionaire Sam Zell, the real estate mogul was busy offloading some $5.4 billion in apartments from Equity Residential’s portfolio. The 23,000 units were sold to Barry Sternlicht’s Starwood Capital and as we noted at the time, Zell has traditionally had a very keen nose about such things as “market peaks”: the 74 years old is credited with calling the top of the real-estate market in 2007, when he sold another one of his companies, Equity Office Properties Trust, to Blackstone for $23 billion.

Despite his penchant for getting it right, Zell warned last September that when it comes to calling market peaks, “you’ve got to tiptoe [because] if you’re wrong on when, that’s a problem.”

Well on Wednesday, Zell “tiptoed” into an interview on Bloomberg TV and made a rather decisive prediction about where the economy is headed now that the Fed has waited too long to hike.

“I think this interest rate hike is too late,” Zell said, before suggesting that “this economy is closer to falling over than it is to going up.”

Zell’s conclusion: “I think there’s a high probability that we’re looking at a recession in the next twelve months.”

Note that this is entirely consistent with the notion that if, as a result of the Fed missing its window, NAIRU undershoots, if (or, more appropriately “when”) it snaps back, a recession is a virtual certainty if history is any guide. Recall what BNP said last month: “NY Fed Fed President William Dudley recently pointed out that whenever the US unemployment rate has increased by more than 0.3-0.4pp from its low, there has always been a recession. Knowing this, it is perhaps not surprising that the median Fed forecast always shows the unemployment rate levelling off close to its equilibrium. The Fed would presumably be reluctant to forecast that its actions (or lack of them) would cause an undershoot in the unemployment rate, which would more than likely end in a recession.”

“The central bank has been too cautious and the economy would already be adjusting if it raised rates six to nine months ago, giving Chair Janet Yellen ‘more room if a recession is on the way,'”, Zell says.

Again we see the old “hike so we have room to cut after we cause a recession” argument.

In any event, the interview touches on a number of topics from energy, to the slump in world trade, to real estate. Watch below.

http://www.bloomberg.com/api/embed/iframe?id=nCqxX~MsR_e8ZBJkb4XCFw

Housing Starts Bounce As Permits Surge Most In 5 Years On Multi-Family Spike

Housing Starts rose 10.5% in November (after plunging 12% in October) as it appears weather-weakened construction caught back up with single-family starts recovering from the plunge in October.The South saw the biggest spike (up 21%) and Northeast fell 8.5%. Building Permits rose 11% MoM (after a 5.1% last month) as multi-family spiked from 446 to 566 (driven by a 22% spike in The Midwest and The West). This is the biggest MoM gain since Dec 2010.

Permits spiked most in 5 years, Starts surged…

Starts driven by single-family…

Permits driven by multi-family…

Welcome to the post-Fed rate-hike renter nation?

Charts: Bloomberg

end

Industrial Production Crashes Most Since 2009, Weather Blamed

For the third month in a row US Industrial Production dropped MoM, crashing 0.6% in November (against expectations of a mere 0.2% drop). This is the 9th month of 2015 with no MoM increase in industrial production and is the biggest MoM drop since March 2012. However, for the first time since Dec 2009, Industrial Production fell YoY (down 1.2%) signalling America is deep in recession. The excuse, blame, is “unusually warm weather” which sent the utilities index down 4.3% as demand for heating tumbled.

So if the wealther was to blame for November, what was to blame for January, February, March, April, May, June, September, and October?

Charts: Bloomberg

US Manufacturing PMI Plunges To Lowest Since 2012 As Factory Orders Collapse To 2009 Lows

Following the collapse in industrial production, it is no surprise that Markit’s Manufacturing PMI has plunged to 51.3, its lowest since October 2012. Under the surface it is a disaster with production volume growth the softest since October 2013, and new orders crashed to worst since September 2009.

But do not ignore manufacturing because, as Markit notes,

“Although manufacturing only accounts for around one-tenth of the economy, theManufacturing PMI exhibits a high correlation of 77% with GDP as industrial activity has an important cyclical impact on other parts of the economy.

With many sectors such as transport and business services dependent upon the manufacturing economy’s health, the downturn in the survey data sends a warning signal that the US upturn appears to be rapidly losing momentum as we move into 2016. However, the picture will become clearer with the publication of services PMI numbers on Friday.”

Seems like the perfect time to raise rates.

Charts: Bloomberg

Foreigners Sell A Record $55.2 Billion In US Treasuries In October

After several months of significant reserves liquidations by China (specifically by its Euroclear proxy “Belgium”) which tracked the drop in China’s reserves practically tick for tick, in October Chinese+Belgian holdings were virtually unchanged according to the latest TIC data, as China moderated its defense of its sliding currency. Of course, putting this in context still shows a China which has sold $600 billion of US paper since 2014, as this website was first to note over half a year ago.

And while we expect a prompt resumption of Treasury selling in the coming months following China’s recent aggressive devaluation of its currency, what was more notable in today’s TIC data was the consolidated total change of all foreign US Treasury holdings.

As shown in the chart below, following an increase of $17.4 billion in September, foreign net sales of Treasuries hit an all time high of $55.2 billion, surpassing the previous record of $55.0 billion set in January. In absolute terms, October’s total foreign holdings by major holders declined to $6,046.3 trillion the lowest since the summer of 2014.

What is the reason? There are two possible explanations, the first being that foreigners are unloading US paper (ostensibly to domestic accounts) ahead of what they perceive an imminent Fed rate hike which would pressure prices lower, or more likely, the ongoing surge in the dollar and collapse in commodity prices continues to pressures foreign reserve managers to liquidate US Treasury holdings as they scramble to satisfy surging dollar demand domestically and unable to obtain this much needed USD-denominated funding, are selling what US assets they have.

Should this selling continue or accelerate in the coming months and if it has an adverse impact on TSY yields, it may also force the Fed’s tightening hand if, as some expect, the liquidation of foreign reserves becomes a self-fulfilling prophecy and leads to a material drop in Treasury prices.

Source: Treasury International Capital

end

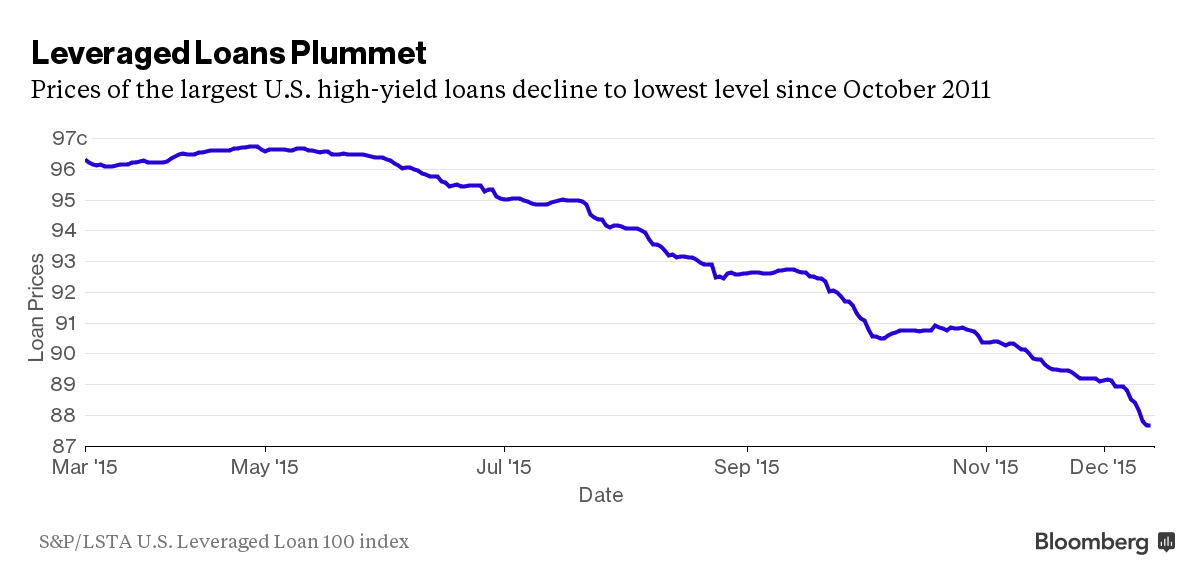

Here is the next hammer to fall: Collateratized leverage loans are getting hammers due to the low oil price:

(courtesy Idzelis/Bloomberg)

CLOs Hammered as Energy Rout Plays Havoc With Other Markets

by Bloomberg Business • December 15, 2015

By Christine Idzelis at Bloomberg

The bust in commodities that’s roiling junk bonds is also taking its toll on funds that bundle corporate loans used to finance buyouts.

The riskiest slices of collateralized loan obligations raised after the financial crisis plunged 9 cents on the dollar since September to about 58 cents at the end of last month, down from 84 cents a year ago, according to JPMorgan Chase & Co. Intensifying price declines in recent months have led to one of the “more challenging years in recent memory,” JPMorgan analysts Rishad Ahluwalia and Jacob Kurosaki wrote in a Dec. 11 note to clients.

CLOs purchase high-yield, high-risk loans and bundle them into securities of varying risk and return. Investors in the lowest-ranked CLO slices, also called the equity tranche, are first in line to absorb any potential losses. The sell-off comes amid concern about the creditworthiness of speculative-grade borrowers as volatility spreads beyond the energy sector.

“The price declines are alarming and worrying,” Ahluwalia, JPMorgan’s head of global CLO research, said in a telephone interview.

While CLO equity holders have continued to receive cash flow payments, the price drop signals investors are worried that their returns are imperiled by “stress” in the corporate credit markets, according to London-based Ahluwalia.

Commodity Exposure

Since the end of October, loans have seen losses in all but the chemicals sector, according to JPMorgan. A typical portfolio of hardest-hit CLO managers has “above-average exposure to commodity sectors and potentially also low-priced credits in other sectors including healthcare and technology,” the analysts wrote.

Oil has tumbled below $37 a barrel, down more than 65 percent from last year’s peak.

Leveraged loans have lost 2.6 percent this year in the U.S. and are heading for their first annual decline since 2008, according to the Standard & Poor’s/LSTA U.S. Leveraged Loan 100 index. U.S. junk bonds have tumbled about 4.7 percent, Bank of America Merrill Lynch index data show.