Gold: $1066.20 up $15.40 (comex closing time)

Silver $14.08 up 40 cents

In the access market 5:15 pm

Gold $1066.00

Silver: $14.09

At the gold comex today, we had a good delivery day, registering 94 notices for 9400 ounces.Silver saw 11 notices for 55,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 199.08 tonnes for a loss of 104 tonnes over that period.

In silver, the open interest rose by 2595 contracts even though silver was down in price by 54 cents with respect to Thursday’s trading and thus we had more investors piling into silver. We have an extremely low price of silver and a very high OI coupled with backwardation in silver at the LBMA. (negative SIFO rates). The total silver OI now rests at 165,994 contracts. In ounces, the OI is still represented by .829 billion oz or 118% of annual global silver production (ex Russia ex China).

In silver we had 11 notices served upon for 55,000 oz.

In gold, the total comex gold OI rose by a whopping 9962 contracts to 402,962 contracts despite the fact that gold was down $27.20 in price with respect to yesterday’s trading.

We had a huge change late last night in gold inventory at the GLD, a massive withdrawal of 4.46 tonnes of gold and this gold is heading straight to Shanghai/ thus the inventory rests tonight at 630.17 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver, we had no changes,in silver inventory at the SLV/Inventory rests at 323.509 million oz

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver rise by 2595 contracts up to 165,884 despite the fact that silver was down in price to the tune of 54 cents with respect to yesterday’s trading. The total OI for gold rose by 9,962 contracts to 402,962 contracts despite the fact that gold was down $27.20 in price

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

b) COT report

Harvey

3. ASIAN AFFAIRS

i) Last night, THURSDAY night, FRIDAY morning: Shanghai down , Hang Sang falls, Chinese yuan finally rises a bit to 6.4813. Stocks in Asia down, including a huge downfall in Japan . Oil falls in the morning,. Stocks in Europe way down. Beige book for China shows deterioration. (see below/2 commentaries)

ii) Jawboning fails to stop the plummeting in the Nikkei

(zero hedge)

iii) Japan prepares for a missile blockade in the East China Sea as they try and halt Chinese aggression. China will not be amused!

ii) This is a real shocker!! Germany now moving closer to Russia, isolating the USA: they are now heading back to Damascus returning to their embassy.

iii) Huge amounts of Ammonium nitrate, used in explosives, entered Turkey. Also a secret Norwegian report details clearly the ISIS Turkey oil trading. The UN now vows to cut off terrorist funding sources:

iv) Russia sets a no fly zone and then the USA immediately halts flights over northern Syria

Not good for Canada: a surge in inventories coupled with a huge decline in business inventories. This sent the Dollar to 1.40 not seen since 2003:

(courtesy zero hedge)

i) Oil crashes back into the 34 dollar column after the oil rig counts surges!!

iii A very important commentary tonight from Andrew Maguire. He is stating that the gold fix in London has less and less physical coming in, not because of low production, but due to the fact that miners are realizing Singapore and Shanghai are better places to sell their physical.

He states that the gold trade is continually migrating away from London to Asia. The nail in the coffin will be when Shanghai begins its gold fix in yuan in April. Arbitrage will destroy the London paper markets.

An extremely important commentary from Andrew Maguire

(courtesy Andrew Maguire/kingworldnews)

i). The St Louis Fed, a research facility for the entire USA saw the largest surge in their Financial Stress Index (FSI).

ii) Last night huge fund liquidations will create havoc on Wall Street:

(courtesy zero hedge)

iii) The house passes their 1.15 trillion spending bill and this will also be passed by the senate and signed the Obama.

iv) the service sector is dominant in the final calculations to USA GDP. It faltered badly following on the footsteps of the manufacturing PMI:

v) Largest restructuring deal with the Puerto Rico Power authority avoids default:

(courtesy zero hedge)

vi) another good reason for the Fed to raise rates; Kansas City Fed survey collapses to negative 9 from a positive 1:

viii) Citibank sees the writing on the wall as it decides to slash 2,000 jobs. These will be middle or back office positions

Let us head over to the comex:

The total gold comex open interest rose to 402,962 for a gain of 9962 contracts despite the fact that gold was down by $27.20 in price with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. Today, the latter scenario stopped as the outstanding OI in that front month remained relatively constant. We are now in the big December contract which saw it’s OI fall by 184 contracts from 1305 down to 1121. We had 183 notices filed yesterday, so we lost a tiny 1 gold contracts or an additional 100 oz will not stand for delivery in this active delivery month of December. The next contract month of January saw it’s OI fall by 29 contracts down to 592. The next big active delivery month is February and here the OI rose by 6040 contracts up to 285,395. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 115,882 which is poor. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was also poor at 186,112 contracts. The comex was in backwardation in gold up to April

December contract month:

INITIAL standings for DECEMBER

Dec 18/2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 4822.500 oz

(150 Kilobars)

Scotia |

| Deposits to the Dealer Inventory in oz | 4,000.000 oz

???? (Brinks) |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 94 contracts

9,400 oz |

| No of oz to be served (notices) | 1027 contracts

(102,700 oz) |

| Total monthly oz gold served (contracts) so far this month | 1038 contracts(103,800 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 193,871.0 oz |

Total customer deposits nil oz

DECEMBER INITIAL standings/

Dec 18/2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 630,541.410 oz

(CNT), |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 299,800.15 oz

(,CNT) |

| No of oz served today (contracts) | 11 contracts

55,000 oz |

| No of oz to be served (notices) | 351 contracts

(1,755,000 oz) |

| Total monthly oz silver served (contracts) | 3613 contracts (18,065,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,718,858.0 oz |

Today, we had 0 deposit into the dealer account:

total dealer deposit; nil oz

we had no dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposit:

i) Into CNT: 299,800.15oz

total customer deposits: 299,800.15 oz

total withdrawals from customer account: 630,541.41 oz

we had 1 adjustments:

Out of CNT:

we had 15,828.49 oz leave the customer account and this landed into the dealer account of CNT

And now the Gold inventory at the GLD:

Dec 18.2015: late last night: a huge withdrawal of 4.46 tonnes of gold/Inventory tonight rests at 630.17 tonnes

DEC 17.no changes in gold inventory at the GLD/Inventory rests at 634.63 tonnes/

dec 16/no changes in gold inventory at the GLD/inventory rests at 634.63 tonnes.

Dec 15.2105/no changes in gold inventory at the GLD/Inventory rests at 634.63 tonnes

Dec 14.no change in gold inventory at the GLD/Inventory rests at 634.63 tonnes

DEC 11/no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

Dec 10.2015/no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 155,934 | 142,278 | 48,714 | 151,012 | 159,278 | 355,660 | 350,270 |

| Change from Prior Reporting Period | ||||||

| -6,830 | -863 | 2,689 | 1,395 | -4,336 | -2,746 | -2,510 |

| Traders | ||||||

| 126 | 125 | 85 | 42 | 50 | 214 | 224 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 35,284 | 40,674 | 390,944 | ||||

| -438 | -674 | -3,184 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, December 15, 2015 | |||||

Our large specs:

Those large specs who have been long in gold liquidated a huge 6830 contracts from their long side

Those large specs who have been short in gold pitched 863 contracts from their short side.

Our commercials;

Those commercials who have been long in gold added 1395 contracts to their long side

Those commercials who have been short in gold covered a large 4336 contracts from their short side.

Our small specs:

Those small specs that have been long in gold covered a smallish 438 contracts from their long side

Those small specs that have been short in gold pitched a tiny 674 contracts from their short side.

Conclusions;

bullish as the commercials went net long again after only a one week hiatus. (5731 contracts)

and again they are within a whisker of going net long with all of their contracts.

And now for silver COT:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 71,479 | 55,902 | 16,805 | 54,707 | 78,249 | |

| 888 | 6,571 | 702 | 2,422 | -5,063 | |

| Traders | |||||

| 86 | 65 | 40 | 37 | 35 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 166,864 | Long | Short | |

| 23,873 | 15,908 | 142,991 | 150,956 | ||

| 94 | 1,896 | 4,106 | 4,012 | 2,210 | |

| non reportable positions | Positions as of: | 143 | 126 | ||

| Tuesday, December 15, 2015 | © Silver | ||||

Our large specs:

Those large specs that have been long in silver added 888 contracts to their long side.

Those large specs that have been short in silver added 6571 contracts to their short side

Our commercials:

Those commercials that have been long in silver added 2422 contracts to their long side

Those commercials that have been short in silver pitched a huge 5063 contracts from their short side

Our small specs;

Those small specs that have been long in silver added a tiny 94 contracts to their long side

Those small specs that have been short in silver added 1896 contracts to their short side.

Conclusions:

extremely bullish as the commercials go net long again by 7485 contracts.

end

And now your overnight trading in gold and also physical stories that may interest you:

5 Key Charts Show Rising Interest Rates Good For Gold Bullion

Gold fell to the lowest level in dollar terms since 2009 yesterday after the Fed’s “historic” 25 basis point interest rate rise on Wednesday. The rate hike has been heralded as the “end of cheap money.” This may or may not be the case but what is more important for precious metal buyers is the impact of potential rising rates on gold prices.

Most pundits on Wall Street are nearly universal in seeing the rate increase as negative for gold. Especially vocal in this regard has been Goldman Sachs. One headline this week, screamed ‘Gold sags as higher U.S. rates are ‘very negative’ for bullion’. However, the consensus is likely once again wrong and it is important to examine the widely held belief that rising rates are bad for gold, by looking at the data and the historical record.

Source: New York Federal Reserve for Fed Funds Rate, LBMA.org.uk for Gold (PM fix)

Firstly, let’s look at the basis for the simplistic “rising rates will lead to lower gold prices” narrative. It comes about due to the belief that rising rates will lead to higher yields and thus investors allocating more funds to bonds and deposits. As gold is a non yielding asset, this therefore is negative for gold or so the narrative goes.

Goldman Sachs is the leading propagator of the narrative and is unquestioningly quoted in the media as seen in this article from Bloomberg in October:

“The Federal Reserve will probably raise interest rates in December and follow that with a further 100 basis points of increases over 2016, according to Goldman Sachs Group Inc., which said the shift in U.S. monetary policy will hurt gold”

As with all narratives, there is a small degree of truth to it. However, as ever the devil is in the detail. Janet Yellen increased the Fed’s key interest rate by a meager 25 basis points to between 0.25 percent and 0.50 percent. Thus, ultra loose monetary policies will continue for the foreseeable future – an environment that is unquestionably favourable to gold.

Fed Funds Rate and Gold Price (USD) – 2003 to 2007

Despite the rate rise, depositors are not getting the benefit of the rate rise. Quite the opposite, immediately after the decision, many of America’s leading banks announced that they were increasing their prime lending rates — the rate at which individual banks lend to their most creditworthy customers — to 3.5 percent effective the following day. Already, many American companies are being impacted by the rate rise. The deposit rate, however, which is the interest rate banks pay to its account holders, will remain unchanged.

The average interest rate on a savings account is a tiny 0.5 percent right now, according to Bankrate. Even after the rate hike, interest on deposits will remain near zero and are negative when inflation is taken into account. Thus, savers are losing money keeping their cash on deposit and today they are also at risk of having their savings expropriated due to the real risk of bail-ins in most G20 nations.

Negative real interest rates is positive for non-yielding, but counterparty risk free gold bullion.

Having looked at the basis for the simplistic narrative, lets now look at the data and historical record.

The most recent example we have of rising interest rates is when the Fed increased interest rates from 2003 to 2006. As can be seen in the charts and table above, in June 2003, the Fed funds rate was at 1% and by June 2006, it had been increased to over 5.5%.

At the time, there was a similar narrative that rising interest rates would scupper the gains gold had seen in 2001 and 2002. Instead, the period of rising interest rates saw gold rise from $361/oz in June 2003 to $633/oz in June 2006 – a gain of 75%.

The other data set and a second clear example of a rising interest rate environment and rising gold prices is from the 1970s. The Federal Funds Rate rose from below 4% in 1971 to over 18% in 1980. During the same period, gold rose by 2,400% – from $35/oz to $850/oz.

Gold and US 10 Year – 1970 to 1980 (GoldCore via Bloomberg)

In the short term, increases in interest rates can be negative for gold. But, in the medium to long term rising interest rates are positive for gold as they were in the 1970s and the 2003 to 2006 period. When interest rates return to more normal levels – above 5% – and positive real returns, only then gold will be vulnerable to weakness as savers and investors become enticed by higher yields.

We are a long way from there yet and gold is likely to be correlated with rising interest rates and only fall towards the end of an interest rate hiking cycle. It is important to remember that the 1970s gold bull market only ended with interest rates close to 20%.

Also rising interest rates are not positive for margin and debt-dependent, equities and property and volatility or further falls in these asset classes should lead to renewed safe haven demand for gold.

As long as central banks continue to debase their currencies by trying to inflate their way out of weak economic growth and recessions through zero interest rate policies and massive digital currency creation, gold will be supported and should indeed begin to make new gains.

Today, interest rates remain close to zero not just in the U.S but in most major economies. Thus, there is no opportunity cost to owning the non yielding gold. Indeed there remains significant counterparty and systemic risk in keeping one’s savings in a bank and government bonds look like a bubble that is being supported by money printing and debt monetisation.

Today, after a near 50% correction in recent years, gold again has significant potential for substantial capital gains. This and gold’s important safe haven diversification attributes make gold increasingly attractive for investors internationally.

DAILY PRICES

Today’s LBMA Gold Prices: USD 1065.85, EUR 982.71 and GBP 713.06 per ounce.

Yesterday’s LBMA Gold Prices: USD 1065.75, EUR 975.65 and GBP 710.33 per ounce.

BREAKING GOLD NEWS and COMMENTARY TODAY – CLICK HERE

Gold Bars At 2% Premium and Free Storage For Six Months On Orders Before December 31st

- 2016 looks set to be stormy – arguably it has never been a better time to buy gold

- Gold bars (1 oz, LBMA) at just 2% on orders placed prior to December 31st

- One of lowest premiums in market today for one ounce bullion coins and bars

- Currently sell gold bars (1 oz) at 3.75% so this is nearly 50% reduction in premium

Free storage for six months – allocated and segregated storage of your bars in safest vaults in world

* This is a phone offer only

** A minimum order of 5 gold bars applies

*** Gold coins and bars are tax free – no stamp duty, VAT or sales tax

Call Us Today To Secure Your Allocation

IRL +353 (0)1 632 5010

UK +44 (0)203 086 9200

US +1 (302) 635 1160

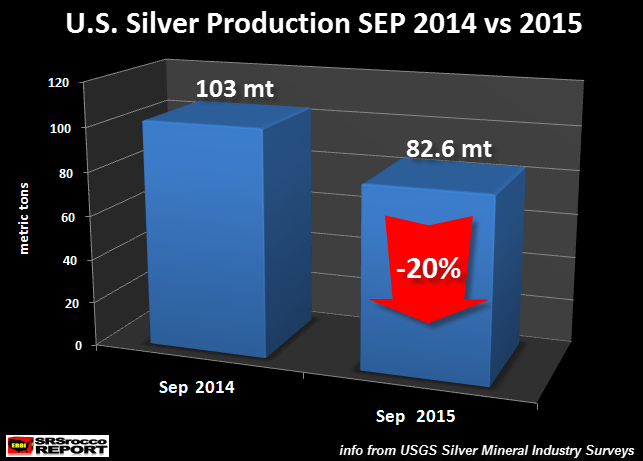

BREAKING NEWS: U.S. Silver Production Plunges

According to the U.S. Geological Survey (USGS), overall domestic silver production for 2015 has trended lower compared to last year. However, the recent data for September show a much larger decline.

U.S. silver production for September fell a staggering 20% compared to the same month last year:

As we can see from the chart U.S. silver production fell to 82.6 metric tons (mt) in September compared to 103 mt during the same month last year. This amounts to a decline of 20.4 metric tons or a 20% plunge versus last year.

This is a large amount if we compare the total decline year to date in 2015 (JAN-SEP) is only 41 mt (5%). I asked the USGS silver specialist if he thought the September’s production figures would be revised higher in the following months. He responded by saying, “Probably not.”

Falling silver production is also taking place in several of the top producers in the world:

Mexico = -4% (Jan-Sep)

Chile = -4% (Jan- Aug)

Canada = -23% (Jan-Oct)

Australia = -41% (Jan-Aug)

(data from Canada Dept of Natural Resources, Mexico INEGI & Chilean Copper Commission)

As I have stated in many articles and interviews, PEAK SILVER will occur first in the base metal mining industry where the majority of by-product silver is produced.According to the data from the 2015 World Silver Survey, 55% of all silver produced in 2014 came as a by-product of zinc, lead and copper production. Furthermore, 13% came as a by-product of gold mining, while the remaining 31% was from primary silver production.

Global silver production will fall more rapidly in the following years as an increasing number of base metal mines shut down due to lower copper, lead and zinc prices.This will occur right at a time when investors finally realize just how undervalued silver is compared to most of the highly overvalued paper garbage the world is invested in.

Lastly, something changed in the U.S. Silver Market this year. Please look for my article, Something Broke In The U.S. Silver Market This Year to be published tomorrow.

end

(courtesy Chris Powell/GATA)

Failing to support his charge against GATA, financial letter writer changes subject

Submitted by cpowell on Thu, 2015-12-17 13:54. Section: Daily Dispatches

9a ET Thursday, December 17, 2015

Dear Friend of GATA and Gold:

Financial letter writer Avi Gilburt today offers a rebuttal to your secretary/treasurer’s response Tuesday (http://www.gata.org/node/16034) to his charge Monday (http://www.kitco.com/commentaries/2015-12-14/Confessions-of-a-Gold-Analy…) that GATA has taken out of context its documentation of largely surreptitious intervention in the gold market by central banks.

Rather than defend his charge by reviewing any of the supposedly misconstrued documents, which would require a little effort, Gilburt changes the subject and himself misconstrues GATA in several respects:

— Gilburt criticizes GATA for not being an investment adviser when your secretary/treasurer, rebutting him, proclaimed that GATA is not an investment adviser but an organization advocating free, transparent, and fair markets

— Gilburt says GATA is mistaken to assert that fundamentals should control markets. But GATA has not asserted that. While fundamentals often do control markets, as when a commodity is exhausted and higher prices are necessary to spur supply, of course there may be other factors. GATA strives to identify another factor in the gold market, intervention by central banks.

— Gilburt charges that GATA maintains that there is no manipulation of the gold market when gold prices are rising. This charge discloses that Gilburt really pays no attention at all to what GATA says. As recently as Monday your secretary/treasurer again called attention to a study speculating that central banks mean to push the gold price way up eventually to help monetize assets and devalue debt:

http://www.gata.org/node/16030

— Gilburt writes that GATA “lacks any real perspective of how financial markets work,” and yet he never mentions central banks, as if central bank policy lately has not been widely acknowledged to determine most market action, if not gold market action.

— Gilburt’s conclusion is that “investor sentiment is the main controlling factor” in markets. GATA can agree with that assertion if central banks are included among “investors.” But Gilburt does not include them.

Gilburt’s basic position seems to echo the position expressed by market analyst Doug Casey at last year’s New Orleans Investment Conference: that central banks are irrelevant to markets and so what they do doesn’t matter, though they create infinite money and throw much of it around in secret. But Gilburt seems most interested in touting the profitability of the technical analysis of markets provided by his financial letter. If he can make money, either by trading or selling his letter, Gilburt apparently couldn’t care less whether markets are free, transparent, and fair. That’s his right but he has run away from his original criticism of GATA: that GATA has misconstrued the documentation of central bank intervention in the gold market.

Gilburt’s rebuttal is headlined “Avi Gilburt’s Response to GATA” and it’s posted at GoldSeek here:

http://news.goldseek.com/GoldSeek/1450364820.php

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A very important commentary tonight from Andrew Maguire. He is stating that the gold fix in London has less and less physical coming in, not because of low production, but due to the fact that miners are realizing Singapore and Shanghai are better places to sell their physical.

He states that the gold trade is continually migrating away from London to Asia. The nail in the coffin will be when Shanghai begins its gold fix in yuan in April. Arbitrage will destroy the London paper markets.

An extremely important commentary from Andrew Maguire

(courtesy Andrew Maguire/kingworldnews)

Hugo…….

Hugo Salinas Price: Is Bloomberg hiding something?

Submitted by cpowell on Fri, 2015-12-18 20:31. Section: Daily Dispatches

3:30p Friday, December 18, 2015

Dear Friend of GATA and Gold:

Hugo Salinas Price of the Mexican Civic Association for Silver, who two weeks ago noted the steady decline in international reserves held by central banks —

— notes today that Bloomberg News seems to have stopped publishing its weekly accounting of those reserves.

Salinas Price writes that “the contraction of international reserves announces a secular change of trend to liquidation of international debt and consequently to depression.”

His analysis is headlined “Is Bloomberg Hiding Something?” and it’s posted at the association’s Internet site, Plata.com.mx, here:

http://www.plata.com.mx/Mplata/articulos/articlesFilt.asp?fiidarticulo=2…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

1 Chinese yuan vs USA dollar/yuan rises in value , this time to 6.4813/ Shanghai bourse: in the red , hang sang: red

2 Nikkei closed down 366.76 or 1.90%

3. Europe stocks all in the red /USA dollar index up to 98.90/Euro down to 1.0832

3b Japan 10 year bond yield: falls to .285 !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 121.43

3c Nikkei now just above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 34.56 and Brent: 36.71

3f Gold up /Yen up

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .589% German bunds in negative yields from 5 years out

Greece sees its 2 year rate rise sharply to 7.75%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield rises to : 8.22% (yield curve flattening)

3k Gold at $1057.00/silver $13.82 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble down 6/100 in roubles/dollar) 71.09

3m oil into the 34 dollar handle for WTI and 36 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9890 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0773 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/arrests 10 traders for Euribor manipulation

3r the 5 year German bund now in negative territory with the 10 year rises to + .646%/German 5 year rate negative%!!!

3s The ELA at 75.8 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.20% early this morning. Thirty year rate at 3% at 2.90% /POLICY ERROR

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Slide As Quad-Witching Has A Violently Volatile Start After Massive BOJ FX Headfake; Oil Tumbles

Arguably the biggest event overnight was yesterday’s BOJ announcement which was widely expected to be non-event, yet ended up being anything but, when, as expected, the Bank of Japan did announce it would keep overall JPY80 trillion monthly QE unchanged, as forecast by 41 of 42 economists, however it also announced it would extend the average maturity of JGB holdings to 7-12 yrs, would establish a new program for ETF purchases targeting the stocks issued by companies “proactively making investment in physical and human capital”, and lastly would boost the maximum issue amount of each J-Reit to be bought from current 5% to 10%.

And so the market was suddenly wrongfooted assuming the BOJ was actually launching another episode of easing, sending the USDJPY soaring, until suddenly the realization swept the market that not only was the incremental action not really material, but even Kuroda spoke shortly after the announcement, confirming that “today’s decision wasn’t additional easing.”

The result was one of the biggest FX headfakes in recent days, perhaps on par with that from December 4 when EUR shorts were crushed, as the biggest carry pair first soared then tumbled...

… and since the Yen correlation drives so many risk assets, also pulled down not only Japanese stocks but US equity futures. Specifically, the Nikkei initially surged as much as +2.50% immediately post the headlines, but has actually faded since and closed down 1.90%. The Yen was also nearly 1% weaker but it is actually a touch firmer on the day now as we go to print, while 10y JGB yields are down 1bp

The second most important overnight event was the release of the latest Chinese “Beige Book“, which revealed that China’s economic conditions deteriorated across the board in the fourth quarter, raising doubts over “whether it’s successfully transitioning from manufacturing to services-led growth, according to a private survey from a New York-based research group.” (HARVEY: see below)

As Bloomberg reports, “national sales revenue, volumes, output, prices, profits, hiring, borrowing, and capital expenditure were all weaker than the prior three months, according to the fourth-quarter China Beige Book, published by CBB International and modeled on the survey compiled by the Federal Reserve on the U.S. economy.”

The profit reading is “particularly disturbing,” with the share of firms reporting profit gains slipping to the lowest level recorded, CBB President Leland Miller wrote in the report. While retail and real estate held up reasonably well, manufacturing and services performed poorly, with revenues, employment, capital expenditure and profits weakening.

And then, the cherry on top of a turbulent pre quad-witching session, was the announcement by Ukraine that it would default on a $3 billion bond to Russia, largely as expected. (Harvey: see below)

What was not expected was the continuing tremors in commodities, which contrary to endless calls that this dip is to be bought, continued sliding:

- WTI CRUDE EXTENDS LOSS, TRADES 46 CENTS LOWER AT $34.49/BBL

- WTI UNDERCUTS DEC. 14 LOW, DROPS TO $34.43/BBL

And while it’s not news as we have been warning about it for the past two weeks (and again last night), today’s quad-witching with the biggest S&P options expiration in years (mostly puts) will assure a violently volatile, illiquid session.

Looking closer at regional markets, Asian stocks traded mostly lower following the weak close on Wall St. amid continued weakness in the commodities complex coupled with a reversal of the post¬FOMC rally, while volatility was observed among Japanese asset classes after the BoJ decided to stand pat on policy but announced new ETF asset measures. As a result, the Nikkei 225 (-1.9%) swung between gains and losses before ultimately trading in negative territory as some viewed the measures as not that significant, while large mining names capped gains in the ASX 200 (+0.1%). Elsewhere, Chinese bourses pared their commodity triggered slump with the Shanghai Comp. (0.0%) relatively flat after gains in developers, who benefitted on the back of better than prior Chinese property prices, offset material weakness in the index. Finally 10yr JGBs tracked USTs higher, while the risk off sentiment in the region also supported inflows into the safe asset.

All China November New Home Prices rose 0.9% vs. Prey. 0.1% in October. China New Home Prices rose M/M in 33 cities vs. 27 in October and rose Y/Y in 21 cities vs. 16 in October.

In terms of the BoJ decision, they kept monetary policy steady at a JPY 80trl annual rise in monetary base as expected, but announced a new program to purchase additional ETFs. The BoJ extended growth lending programs by a year and extend the average maturity of JGB holdings to 7-12yrs, while under the new ETF program it will purchase JPY 300bIn annually in addition to the current ETF purchases.

Elsewhere, it also added that it will begin selling stocks purchased from financial institutions from April next year. Volatility was observed across Japanese asset classes, with initial upside being seen in both the Nikkei and USD/JPY before paring the move shortly after.In equity markets, Europe has continued the trend set by US and Asian markets, with Euro Stoxx residing in negative territory (-0.7%) to pare back some of the recent, post-FOMC gains. The FTSE outperforms in Europe so far (-0.0%), with the index benefitting from strength seen in energy and utility names, with the former bolstered by a bid this morning in the energy complex.

Fixed income markets have also seen a retracement of recent price action, with Bund futures trading higher today after significant losses on the back of the FOMC rate decision. Given the holiday-thinned volumes, month-end flows are expected to come into play earlier and analysts at Citi expect the effective duration for EGBI to increase by 0.04 years and month-ends to be particularly supportive for French and Spanish bonds.

FX markets have taken focus in the European morning and continue to be dominated by holiday-thinned markets and optionality plays. As such, GBP regained ground against USD to pare earlier losses seen following the EU cash open amid no new fundamental catalysts. Separately USD/JPY has also continued to ebb lower in the wake of the latest BoJ policy decision which left some doves in the market slightly disappointed with the pair now residing below all three key 50,100 and 200DMAs.

Looking ahead, the final Friday before Christmas sees a relatively light schedule with today’s highlights including Canadian CPI and US services PMI.

Bulletin Headline Summary From RanSquawk and Bloomberg

- USD/JPY has ebbed lower in the wake of the latest BoJ policy decision which left some doves in the market slightly disappointed with the pair now residing below all three key 50,100 and 200DMAs

- Europe has continued the trend set by US and Asian markets, with Euro Stoxx residing in negative territory (-0.7%) to pare back some of the recent, post-FOMC gains

- Today has a relatively light economic calendar, with highlights including Canadian CPI and US services PMI

- Treasuries gain, 5/30 curve narrowest since April, as EGBs rally, stocks decline around the world; all maturities lower on the week amid Fed’s first rate hike since 2006.

- Overnight, long tenors lead as EGBs extend post-Fed rally, bull flattening curves; futures outperform cash, while continued large flows in long-end EUR swaps draw some attention

- China’s economic conditions deteriorated across the board in the 4Q, according to a private survey from a New York-based research group that contrasted with recent official indicators that signaled some stabilization in the country’s slowdown

- U.S. high-yield funds saw outflows of $3.811b in the week ended Dec. 16, highest YTD and third-highest on record, vs outflows of $3.463b in the previous week, according to Lipper

- Oil traded near $35/bbl and headed for a third weekly decline amid a worsening U.S. supply glut and the Fed’s rate hike

- The Bank of Japan kept its main monetary stimulus target unchanged Friday while outlining operational changes for its purchases of government bonds, ETFs and REITs

- The bank plans to lengthen the average maturities of the JGBs it buys to 7-12 years from current 7-10 years currently

- U.K.’s Cameron said his bid to change Britain’s relationship with the EU is gathering momentum after fellow leaders signaled they are willing to find compromises on his demand for curbs on welfare

- Ukraine defaulted on a $3b bond payment due to Russia on Sunday, deepening a dispute over the debt as the two sides move closer to legal action

- Casino mogul Sheldon Adelson acknowledged presidential candidate Donald Trump’s “incredible” support among the Republican base and said he might let some primaries pass before deciding whom to back

- Trump has criticized the influence of big donors like Adelson and mocked Marco Rubio for courting the casino tycoon’s money

- Sovereign 10Y bond yields lower. Asia, European stocks and U.S. equity-index futures slide. Crude oil mixed, gold and copper fall

US Event Calendar

- 9:45am: Markit US Services PMI, Dec. P, est. 55.9 (prior 56.1)

- Markit US Composite PMI, Dec. P (prior 55.9)

- 11:00am: Kansas City Fed Mfg Activity, Dec., est. 2 (prior 1)

- 1:00pm: Fed’s Lacker to speak in Charlotte, N.C.

DB’s Jim Reid concludes the overnight wrap

Before the holidays, just when you thought it was safe to emerge from the non-zirp waters, yesterday wiped out all of Wednesday’s gains with the S&P 500 (-1.50%) and now -0.60% below the pre-rate hike levels. It has been a tough year to achieve positive returns whatever the asset class you’re in. Even in markets that are up in local currency terms, often it’s been wiped out in dollar terms. With that in mind I couldn’t help get excited by a possible trade yesterday. Apparently some of the old original Star Wars figures from 30-35 years ago are now worth up to £18,000. The word is that at the time one stockist was extremely oversupplied and his whole inventory got dumped into a landfill site in the Midlands here in the UK. So find your shovels and follow me up the motorway this weekend!!

The force has been with the BoJ this morning. While the current ¥80tn expansion of the monetary base was kept unchanged as expected, markets initially reacted positively to the more surprising news that the BoJ is to make additional purchases of ETF’s on top of the current ¥3tn of purchases that the BoJ currently makes each year. The accompanying statement shows that the Bank’s new additional program will have an annual budget of ¥300bn and will be initially tied to the JPX-Nikkei 400 index. It’s also been announced that the BoJ is to increase the maximum amount of each issue of Japanese REIT’s it can buy. These measures were passed with a 6-3 majority. On top of this, the BoJ also announced that it is to extend the average remaining maturing of JGB purchases to about 7-12 years from the beginning of next year, from 7-10 years currently. The price action has been interesting. The Nikkei initially surged as much as +2.50% immediately post the headlines, but has actually faded since and is now down -1.20%. The Yen was also nearly 1% weaker but it is actually a touch firmer on the day now as we go to print, while 10y JGB yields are down 1bp. We await Kuroda’s press conference for more details behind the move but it’s another small piece of plate spinning as 2015 draws to an end.

It’s fairly unexciting in markets elsewhere in Asia this morning. The Hang Seng is +0.11%, the Shanghai Comp is +0.25% and the Kospi and ASX are lower post the losses in the US yesterday. Credit markets are the notable underperformer however, with indices 1-3bps wider. Meanwhile there was some encouraging property prices data out of China this morning where 33 of the 70 cities tracked saw new home prices rise in November, compared to just 27 companies in October.

Moving on. Oversupply still hangs over the oil market but yesterday the stronger dollar post-FOMC sunk commodities to fresh multi year lows. Oil dominated the headlines as WTI sank -1.60% and closed back below $35 for the first time since February 2009. Brent was also down nearly 1% to hover around $37, while Natural Gas finished -2% and at levels not seen since 1999 (it’s also down another 1% this morning). It was the moves in precious metals which also caught the eye. Gold closed down -1.98% which was the biggest daily loss since July and at $1051/oz is holding the five-year lows reached briefly earlier this month. Silver and Platinum were each down well over 3% with both also hovering around multi-year low levels again. Industrial metals finished generally 1-2% lower. This all came as the Dollar index recorded a sharp +1.43% gain yesterday which was the highest daily return this year. In particular, currencies in Russia, Hungary, Canada, Australia, New Zealand and South Africa were down at least 1% by the close. The biggest slide however was reserved for the Argentinean Peso which depreciated some 26% after the lifting of currency controls late on Wednesday night.

In the end it was a very weak day for US credit also. Of particular focus, CDX HY finished 27bps wider by the close of play and wiped out a decent chunk of the gains that we had seen in the prior two days. The two big US HY ETF’s both finished -1.11% and are pretty much back to where they closed last week. Meanwhile US HY energy spreads blew out 40bps wider yesterday to a new record wide at 1,310bps. US IG wasn’t immune to the moves either, CDX IG in fact finished 5bps wider which was the third weakest day this year. Rates markets rallied back as 2y yields dipped back below 1% and 10y yields finished over 7bps lower at 2.224%.

There wasn’t too much to take away from yesterday’s data which largely played second fiddle to those commodity moves. In the US we learnt that initial jobless claims fell 11k last week to 271k (vs. 275k expected) although there was less good news to come out of the December Philly Fed which fell 7.8pts this month to -5.9 (vs. +1.0 expected). The print was the second-lowest this year although it was noted that the six-month outlook print fell to the lowest since November 2012 after plunging more than 20pts. Finally the Conference Board’s leading index for November rose a better than expected +0.4% mom last month (vs. +0.1% expected).

Just wrapping up the rest of yesterday’s economic data. In Germany the IFO dipped slightly in December following some slightly weaker readings out of the domestic sectors and despite the uptick in sentiment in the manufacturing sector. The index declined a fairly modest 0.3pts to 108.7 (vs. 109.0 expected) with the current assessment reading in particular down 0.6pts this month. UK retail sales were impressive last month however, with the ex auto and fuel print rising a much better than expected +1.7% mom in November, well above expectations of +0.5%. That helped nudge the YoY rate up seven-tenths to +3.9%. Elsewhere, as expected the Norges Bank left the current policy rate of 0.75% although hinted at a possible cut in the first half of next year.

Staying with central banks, yesterday saw Mexico follow the Fed in raising its benchmark interest by 25bps. That was in fact the first hike by the nation since 2008 although it was widely anticipated. Mexico now joins Chile, Hong Kong, Kuwait and the UAE in tightening policy since the Fed on Wednesday. Despite this, in a note yesterday our Asia Macro colleagues highlighted that they do not necessarily expect other central banks in Asia to follow suit, reflective of weaker business cycles, slowing growth and in particular negative export growth. They are of the view that Asian central banks will not be able to keep up with even a gradual Fed and front-end rate differentials will narrow. They highlight that Philippines is perhaps the only central bank that they think could hike next year.

Looking ahead to what’s set to be a relatively quiet end to the week for data. In the European session this morning the only data of note is out of France where we’ll get the November PPI data. In the US this afternoon we’ll get the flash December services and composite PMI prints along with the Kansas City Fed manufacturing activity index reading for December. Of more interest perhaps will be comments from the Fed’s Lacker who is due to speak on the 2016 economic outlook at 6pm GMT tonight. He will be the first Fed speaker other than Yellen to have spoken since the rate hike.

Before we wrap up, it’s worth also reminding readers of the Spanish General Election this Sunday. We gave a bit of a rundown yesterday but just recapping again, while a central case scenario is probably still a PP minority government with external support from Citizens, recent swings in opinion polls means the main risk remains political impasse through a fragmented parliament. It’s certainly worth keeping an eye on Sunday’s outcome.

ASIAN AFFAIRS

let us begin:

Last night, THURSDAY night, FRIDAY morning: Shanghai down , Hang Sang falls, Chinese yuan finally rises a bit to 6.4813. Stocks in Asia down, including a huge downfall in Japan . Oil falls in the morning,. Stocks in Europe way down. Beige book for China shows deterioration. (see below)

(courtesy zero hedge)

Japanese Jawboning Fail – Nikkei Crashes 1000 Points From Overnight Highs

For a brief few minutes, overnight saw exactly the reaction that central planners had hoped for when The Bank Of Japan announced it would buy ‘moar’ stock ETFs and extend bond duration buying ad nauseum. However, within just 15 minutes something happened that we haven’t seen since the world embarked on this experimental nightmare. Despite the front-ran promises to buy Japanese stocks “whatever it takes” traders sold… and sold large.

After a 500 point “business as usual” spike, Nikkeie 225 crashes over 1000 points as traders recognized The BoJ’s desperation…

As Bloomberg reports,

The new program is in addition to the 3 trillion yen the bank already spends on ETFs each year, the BOJ said on Friday. The BOJ also said it would extend the average maturity of holdings of Japanese government bonds to seven to 12 years, and increase the amount of individual Japanese real estate investment trusts it can own. The Topix index sank 1.8 percent to 1,537.10 at the close in Tokyo, reversing a gain of as much as 2 percent.

“At 300 billion yen, it’s on the scale of margin of error. The impact to the stock market will not be big,” said Soichiro Monji, chief strategist at Tokyo-based Daiwa SB Investments Ltd. “If it’s this small, some investors will think this is the best they can do. Kuroda himself says he never does anything half-baked, but frankly speaking this is half-baked.”

…

“Investors were buying on hope,” said Hiroaki Hiwada, a Tokyo-based strategist at Toyo Securities Co. “But they are realizing now that it’s not actually a big deal,” he said. “People are disappointed after looking at the details closely.”

As Kuroda loses his magic touch, the overwhelming sense of panic washes across every carry trader and algo hesdline reader in the world.

end

China Beige Book Shows ‘Disturbing’ Economic Deterioration

-

Survey results weaken across the board; profits disturbing

-

Successful manufacturing-to-services transition may be on hold

China’s economic conditions deteriorated across the board in the fourth quarter, according to a private survey from a New York-based research group that contrasted with recent official indicators that signaled some stabilization in the country’s slowdown.

National sales revenue, volumes, output, prices, profits, hiring, borrowing, and capital expenditure were all weaker than the prior three months, according to the fourth-quarter China Beige Book, published by CBB International. The indicator is modeled on the survey compiled by the Federal Reserve on the U.S. economy, and was first published in 2012.

The world’s second-largest economy lacks the kind of comprehensive data available on developed nations, making it harder for investors to get a clear read — particularly as China transitions from reliance on manufacturing and investment toward services and consumption. Official data on industrial production, retail sales and fixed-asset investment all exceeded forecasts for November, while consumer inflation perked up and a slide in imports moderated.

Earnings Deterioration

The Beige Book’s profit reading is “particularly disturbing,” with the share of firms reporting earnings gains slipping to the lowest level recorded, CBB President Leland Miller wrote in the release. While retail and real estate held up reasonably well, manufacturing and services performed poorly, with revenues, employment, capital expenditure and profits weakening.

The survey shows “pervasive weakness,” Miller wrote in the report. “The popular rush to find a successful manufacturing-to-services transition will have to be put on hold for a bit. Only the part about struggling manufacturing held true.”

After efforts including six interest-rate cuts since late 2014 failed to revive growth, policy makers are switching focus to fix problems like overcapacity on the supply side. President Xi Jinping — seeking to keep growth at a minimum 6.5 percent a year through 2020 — is juggling short-term stimulus with long-term prescriptions to avoid the middle-income trap that has ensnared developing nations after bouts of rapid growth before they became wealthy.

China’s leaders convene their annual economic work meeting Friday, according to the People’s Daily. Officials typically set the growth target for the coming year at the conference, which lasts a few days.

Survey Description

The report was based on surveys of more than 2,100 firms across China and interviews with bankers, managers and executives. CBB began the series in mid-2012, when its inaugural survey indicated a pick-up in growth from early that year, a forecast later borne out.

Geographically, the three most high-profile regions performed the worst, with Shanghai’s “dismal” showing outpacing Guangdong’s and Beijing’s. Every region weakened on-quarter except for the Center and West, the report showed.

“More concerning than overall growth weakness was degradation of two components of the economy that were previously overlooked as sources of strength: the labor market and the impact of inflation,” Miller wrote. Given growth in input prices and sales prices slipped to record-lows while firm performance metrics fell, “it looked like firms were encountering genuinely harmful deflation,” he wrote.

If labor market weakness persists, policy makers in Beijing will feel “increasing pressure” to ramp up the policy response, according to the report.

With official indicators picking up in November, Bloomberg’s monthly China gross domestic product tracker rose to a 6.85 percent estimated growth pace for the month, the best reading since June.

In a worrying sign for the effectiveness of monetary easing to date, the share of companies borrowing declined to a record low, the survey showed.

“The interest of firms in both borrowing and spending continues to decline, suggesting it’s past time the ‘stimulus mafia’ rethinks its Pavlovian responses,” Miller wrote. “Reform or bust.”

“Alarming” Chinese Beige Book Reveals Dire Economic Situation, Fewest Profitable Companies On Record

It’s notoriously difficult to get a read on the health of China’s economy.

The ambiguity is in large part attributable to the NBR’s tendency to goalseek the data in order to ensure that growth remains in line with the Party’s “targets.” To be sure, virtually no one believes the official numbers and when it comes to GDP, the situation is complicated by what we’ve called Beijing’s deficient deflator math, which causes China to habitually overstate economic growth during times of rapidly falling commodity prices.

Although sellside estimates are useless (the Street is effectively forced to produce forecasts they know are erroneous because trying to estimate actual output in China would mean missing the “official” mark every single time) we can get a decent approximation of how the country is really doing by looking at the Li Keqiang index, which tracks electricity consumption, rail cargo, and loans.

Another way to assess the health (or lack thereof) of the world’s engine of global growth and trade is the CBB, or, China Beige Book which is modeled on the Fed’s survey of the U.S. economy. According to the CBB, the Chinese economy deteriorated markedly in Q4 and the weakness was broad-based.

Despite the fact that “official data on industrial production, retail sales and fixed-asset investment all exceeded forecasts for November, while consumer inflation perked up and a slide in imports moderated,”the CBB suggests “national sales revenue, volumes, output, prices, profits, hiring, borrowing, and capital expenditure were all weaker than the prior three months,”Bloomberg reports.

The profit reading is “particularly disturbing,” with the share of firms reporting earnings gains slipping to the lowest level recorded, CBB President Leland Miller said. Although retail and real estate weren’t terrible (and that’s pretty much all you can hope for these days), manufacturing and services slumped, as revenues, employment, capital expenditure and profits all came in weaker.

http://www.bloomberg.com/api/embed/iframe?id=yMw3KJ1RQ0SCix~yUU9FhA

China is of course attempting to mark a difficult transition from an investment-led, smokestack economy to a consumption and services-driven model. That’s proving to be easier said than done, a point Miller underscored in the CBB’s report. There’s “pervasive weakness,” he said. “The popular rush to find a successful manufacturing-to-services transition will have to be put on hold for a bit. Only the part about struggling manufacturing held true.”

Miller continues:

“More concerning than overall growth weakness was degradation of two components of the economy that were previously overlooked as sources of strength: the labor market and the impact of inflation. Given growth in input prices and sales prices slipped to record-lows while firm performance metrics fell, it looked like firms were encountering genuinely harmful deflation.”

“The interest of firms in both borrowing and spending continues to decline, suggesting it’s past time the ‘stimulus mafia’ rethinks its Pavlovian responses. Reform or bust.”

In other words, both fiscal stimulus and monetary easing have failed to rescue the Chinese economy from the dreaded “hard landing” and from a deflationary death trap. Recall also that the credit impulse simplyrolled over and died in October as an acute overcapacity problem combined with a negative overall economic outlook stifled demand for credit while rising NPLs made banks wary of lending.

Note that this is entirely consistent with what we said in “Credit Suisse Warns On China: “Some Companies Are Having To Borrow To Pay Staff Salaries.” “The government has become more active in terms of counter-cyclical measures since late summer [and] the PBoC has injected liquidity into the policy banks, through its selective easing program, and policy banks have invested in special infrastructure projects approved by planning agency NDRC,” Credit Suisse wrote earlier this month. Here’s the bank’s assessment of how effective Miller’s “stimulus mafia” has been: “However, the impact of these stimulus measures on the real economy has been weak.”

And so it is, as Miller writes, “reform or bust.” We’ll leave it to readers to determine which is more likely.

Japan Prepares Missile Blockade In East China Sea To Halt Chinese “Maritime Aggression”

Late last month in “South Pacific Showdown? Japan May Send Warships To China Islands,” we documented a meeting between Japanese PM Shinzo Abe and Philippines President Benigno Aquino on the sidelines of the Asia-Pacific Economic Cooperation summit held in Manila.

The two leaders discussed the possibility that Japan could provide Manila with “large ships” that the Philippines can use to patrol the South China Sea.

This was, of course, a direct response to China, whose land reclamation efforts in the Spratlys have ruffled more than a few feathers in the South Pacific.

“The deal will mark the first time Japan has agreed to directly donate military equipment to another country, and is the latest example of Abe’s more muscular security agenda,” Reuters reported on at the time, before adding that “rather than challenge Beijing directly by sending warships or planes to patrol the South China Sea, Japan is helping to build the military capacity of friendly nations with claims to parts of the waterway.”

Despite the contention that Abe has no immediate plans to “directly challenge” the PLA navy, the PM also told Obama that Japan would consider conducting “freedom of navigation” patrols in conjunction with the US around China’s man-made islands.

Recall that Washington has committed to sailing warships by the islands several times per year in a repeat of the pass-by the navy conducted in late October.

As we said last month, “if Japan starts to conduct the same type of exercises near the Spratlys that the US has now pledged to carry out at least twice per quarter, it will be more than Beijing can bear.”

Of course Japan is also at odds with China over the latter’s construction of rigs near a demarcation line that separates the two countries’ exclusive economic zones in the East China Sea:

Well, speaking of the East China Sea, Reuters is out reporting that in response to pressure from Washington, Japan is set to “fortify its far-flung island chain in the East China Sea under an evolving strategy that aims to turn the tables on China’s navy and keep it from ever dominating the Western Pacific Ocean.”

The US believes Japan “must help contain growing Chinese military power” and is pushing Abe “to abandon his country’s decades-old bare-bones home island defense in favor of exerting its military power in Asia,” Reuters continues. According to “a dozen military planners and government policymakers … Tokyo is responding by stringing a line of anti-ship, anti-aircraft missile batteries along 200 islands in the East China Sea stretching 1,400 km (870 miles) from the country’s mainland toward Taiwan.”

Apparently, the deployment will act as a kind of blockade as “Chinese ships sailing from their eastern seaboard must pass through this seamless barrier of Japanese missile batteries to reach the Western Pacific, access to which is vital to Beijing both as a supply line to the rest of the world’s oceans and for the projection of its naval power.” Recall that from the PLA’s surprise appearance at the Yemeni port city of Aden to the Chinese navy’s trip to Alaska, Xi is keen on projecting China’s growing maritime prowess. The missile battery is an attempt to deter Beijing’s ambitions.

The idea is to establish the string of islands stretching through Japan’s East China Sea territory and south through the Philippines as a kind of demarcation line separating Beijing’s sphere of regional influence from Washington’s. “In the next five or six years the first island chain will be crucial in the military balance between China and the U.S.- Japan,” said Satoshi Morimoto, a Takushoku University professor who was defense minister in 2012 told Reuters.

This purportedly marks the beginning of a concerted effort to challenge China’s attempt to exert complete control over the South and East China Seas (which the US and its allies swear is Beijing’s endgame). “The growing influence of China and the relative decline of the U.S. [is] a factor. We wanted to do what we could and help ensure the sustainability of the U.S. forward deployment” Akihisa Nagashima, a DPJ lawmaker says, explaining a shift in Abe’s maritime defense strategy that began in 2010.

So, as we anxiously await the (likely angry and invariably indignant) response from Beijing, we’ll close with the following rather ominous quote, from an official who spoke to Reuters:

“To be sure, there is nothing to stop Chinese warships from sailing through under international law, but they will have to do so in within the crosshairs of Japanese missiles.”

Moody’s Downgrades Glencore To Lowest Investment Grade Rating As CDS Trade A Multi-Year Highs

One of the corporate catalysts which unleashed the market “wobble” in August, in addition to the confluence of macro and geopolitical events, was the dramatic repricing of risk for all the commodity traders in general and for Glencore in particular as the market caught up with what we had cautioned since early 2014: Glencore is the closest (and most readily tradeable) proxy to China’s commodity and credit crunch, due to its extensive and direct exposure to copper prices.

So as commodity prices tumbled, the market looked to find a (levered) hedge and discovered it courtesy of Glencore CDS (in the process sending it wider by 600 points since our preview of just this event nearly two years ago), which as the chart below shows, may have been the single best liquid trade of 2015, as the probability of a Glencore default in the next 5 years has surpassed 50%.

More importantly, it was in early September that the rating agencies started noticing Glencore, which was bad news for the commodity trader as a junk bond rating would effective mean a collateral margin call cascade, requiring billions in additional liquidity. On September 2: S&P announced: GLENCORE TO BBB/NEGATIVE FROM BBB/STABLE, which was unexpected as Glencore had just announced its first of many deleveraging program. It has since promised it would cut much more debt, even if it hasn’t executed on any of these promises.

Then moments ago, it was the other rating agencies, Moody’s which reminded Glencore that it is living on borrowed time and that it should move from mere deleveraging promises to actual actions when it downgraded Glencore from Baa2 to Baa3, the lowest investment grade category. The good news is that the outlook is stable, so Moody’s won’t proceed with another downgrade in the immediate future.

However, as Moody’s writes, the downgrade may be inevitable as a result of the following conditions which would be sufficient to downgrade the giant commodity trader: “Weak earnings performance in marketing operations below the current EBIT guidance of $2.4-$2.7 billion could place negative pressure on the Baa3 ratings in the absence of any mitigating measures.A weakening of the company’s liquidity position, delays with the planned divestments in 2016 or a material reduction in its working capital funding capacities by the banks, as well as sustained high leverage with adjusted debt/EBITDA exceeding 4x, will also put negative pressure on the Baa3 ratings.”

In other words, unlike central banks which can get away with jawboning indefinitely, the raters have just started the countdown for Glencore which now has a few months in which to deliver asset divestment results, and enjoy a rebound in commodity prices, or else the worst case scenario for the company may unfold.

Full Moody’s note:

Moody’s downgrades Glencore’s ratings to Baa3; stable outlook

London, 18 December 2015 — Moody’s Investors Service has today downgraded the long term ratings and short term ratings of Glencore International AG (Glencore) and its related entities to Baa3/(P)Baa3/P-3 from Baa2/(P)Baa2/P-2. The outlook on the ratings is stable.

“Our decision to downgrade Glencore’s ratings by one notch to Baa3 primarily reflects our expectations that the pricing environment in mining will remain unfavorable in 2016-17, making a return to the previous level of earnings unlikely,” says Elena Nadtotchi, Vice President Senior Credit Officer and Moody’s lead analyst of Glencore. “However, we believe that Glencore has the capacity to adjust its balance sheet to a reduced earnings level in order to maintain its investment grade ratings.”

RATINGS RATIONALE

— DOWNGRADE OF RATINGS TO Baa3/P-3

Today’s downgrade of Glencore’s ratings to Baa3 reflects Moody’s view that market conditions in the mining industry will not improve for a prolonged period of time. Weak metal prices have significantly reduced the earnings capability of the industrial division. However, Moody’s expects that Glencore’s substantial commodity marketing franchise will continue to contribute strongly to the earnings and free cash flow generation.

The rating agency expects that Glencore’s adjusted EBITDA will have fallen by about 25% year-on-year in 2015 and will continue to decline by around 10% in 2016 on the back of Moody’s lower metal price assumptions for the next year. The rating agency now assumes an average copper price of $2.15/lb in 2016 and only a modest recovery in the copper price to $2.35/lb average in 2017, compared to around $2.1/lb spot price today. While the rating agency bases its analysis on average metal price assumptions, it expects that metal prices will be highly volatile and as a result it will continue to review its price assumptions in 2016.

Given the deterioration in earnings, Glencore’s debt/EBITDA (as adjusted by Moody’s) is expected to have deteriorated to around 4x at the end of 2015. Moody’s expects some improvement for 2016, however, metrics will likely stay above the 3.5x threshold compatible with a Baa2 rating.

RATIONALE FOR STABLE OUTLOOK

The stable outlook on the ratings reflects Moody’s opinion that the company has the ability to manage its debt levels down to match the lower earnings levels.

Glencore’s industrial operations remain robust, notwithstanding the adverse pricing environment. Over the last months of 2015, the company executed a number of operating measures in its industrial division, including suspending unprofitable production, improving cash cost positions across its key metals and minerals and announcing substantial capex cuts for 2016-17. These actions have improved the resilience of the industrial portfolio.

Moody’s views the commodity marketing operations as a positive differentiating credit factor, given the relative stability in its earnings and its high FCF generation capability due to its low capex requirements. Glencore expects that its marketing operations will contribute $2.4-$2.7 billion of EBIT in 2016. This diversity of the operating model allows Glencore greater financial flexibility, compared to its mining peers. In the declining price environment, marketing operations release significant working capital, as seen in 2015, and help to repay debt to match the lower level of the earnings. Moody’s recognises that the marketing business model relies on the availability of working capital financing. The rating agency has no indication that this has significantly deteriorated in the current commodity pricing environment.

The Baa3 rating and the stable outlook also recognises that the company is managing its balance sheet proactively. In H2 2015, Glencore placed $2.5 billion in equity, made divestments and delivered a substantial release of working capital, including from its marketing operations. Moody’s expects that these measures will have arrested the deterioration in the company’s financial metrics, with adjusted debt/EBITDA projected to peak at around 4x at end-2015, despite the accelerated decline in copper prices in the last quarter of this year.

In December 2015, Glencore also confirmed plans to further reduce debt in 2016, targeting about $3 billion of additional debt reduction compared to its September plans. Assuming lower metal prices, these plans will be in part supported by a further release of working capital, as well as the expected divestments. Moody’s views the plan as credible and as a result factors some further improvement in Glencore’s debt/EBITDA leverage metrics in 2016.

Finally, the Baa3 ratings and the stable outlook are supported by the company’s financial policy that prioritises the investment grade rating, as demonstrated by the proactive execution of balance sheet strengthening measures in 2015, including equity placement, suspension of dividends and the accelerated repayment of debt.

LIQUIDITY

Glencore maintains a strong liquidity position, even as it continues to reduce its debt. In 2015, debt reduction was primarily funded by a substantial working capital inflow on the back of decline in metal prices and the release of capital from its commodity marketing operations, as well as by proceeds from its $2.5 billion equity placement and $0.9 billion streaming deal.

The company maintains substantial funding lines, which underpin its commodity marketing operations. Glencore has a $15.3 billion committed syndicated bank facility, comprising an $8.45 billion 12-month revolving credit facility maturing in May 2016 (with the term-out option to May 2017) and a $6.8 billion five-year 2020 revolving credit facility. At the end of September 2015, the company reported $13.8 billion in available liquidity, including cash balances and funds available under the revolving credit facilities.

STABLE OUTLOOK

The stable outlook on the Baa3 ratings factors the expectation that Glencore will improve its leverage profile in 2016 and will continue to maintain strong liquidity. The rating agency expects that Glencore retains sufficient financial and operating capacity and will execute additional measures to maintain its Baa3 credit profile, in particular if copper prices were to decline to $1.9/lb for a period of time, which is the rating agency’s current stress case price assumption for 2016.

WHAT WOULD CHANGE THE RATING DOWN/UP

Large moves in commodity prices, and copper prices in particular, will continue to have an impact on the ratings.

Weak earnings performance in marketing operations below the current EBIT guidance of $2.4-$2.7 billion could place negative pressure on the Baa3 ratings in the absence of any mitigating measures. A weakening of the company’s liquidity position, delays with the planned divestments in 2016 or a material reduction in its working capital funding capacities by the banks, as well as sustained high leverage with adjusted debt/EBITDA exceeding 4x, will also put negative pressure on the Baa3 ratings.

In the medium term, an upgrade of Glencore’s ratings to Baa2 would be considered once leverage is sustainably reduced to the point where the company is able to build some headroom and maintain solid credit metrics. We expect that adjusted debt/EBITDA below 3.5x, backed by strong free cash flow generation and solid liquidity position will put positive pressure on the Baa3 ratings.

end

(courtesy LSE)

no change in Glencore’s stock price today: 80.86 pence.

GLEN GLENCORE PLC ORD USD0.01

| Price (GBX) | 80.86 | Var % (+/-) | +0.00% ( 0.00) |

| High | 83.59 | Low | 79.75 |

| Volume | 112,565,941 | Last close | 80.86 on 18-Dec-2015 |

| Bid | 80.46 | Offer | 80.50 |

| Trading status | Market Close | Special conditions | NONE |

Ukraine “Crooks” Default On $3 Billion Bond To Putin

Back in August, Ukraine struck a restructuring agreement on some $18 billion in Eurobonds with a group of creditors headed by Franklin Templeton.

Under the terms of the deal, Kiev should save around $4 billion once everything is said and done. That was the good news. The bad news was that Ukraine still owed $3 billion to Vladimir Putin. Here’s what we said at the time:

“..owing Vladimir Putin $3 billion is not a situation one ever wants to find themselves in, but this particular case is exacerbated by the fact that Putin did not loan the money to Ukraine as we know it now, he loaned the money to a Ukraine that was governed by Russian-backed Viktor Yanukovych. Of course Yanukovych was run out of the country last year following a wave of protests (recall John McCain’s infamous speech at Maidan).”

Ukrainian finance minister Natalie Jaresko offered the same restructuring terms to Russia that it offered to Franklin Templeton and T. Rowe. In effect, Jaresko was attempting to tell Vladimir Putin that Ukraine would allow him to take a 20% upfront loss on the $3 billion he loaned to Yanukovych who was overthrown by the current Ukrainian government with whom Moscow is effectively at war.

As you might imagine, Putin was not at all interested. Last month, Moscow “generously” offered to accept $1 billion per year from now until 2018 (so, a “restructuring” at par). Kiev refused, noting that such a deal would violate the country’s agreement with its other creditors.

Earlier this week, the IMF ruled that the debt to Russia was intergovernmental (as opposed to private). “In the case of the Eurobond, the Russian authorities have represented that this claim is official. The information available regarding the history of the claim supports this representation,” the Fund said, in a statement.

“The decision means that under new IMF rules Ukraine will now have to demonstrate ‘good faith’ in at least attempting to negotiate a restructuring of its debt with Russia if it wants to secure the next instalment of a $17bn IMF-led rescue programme,” FT noted at the time. “But the ‘good faith’ bar is one that senior IMF officials do not believe Ukraine has yet met.”

That ruling effectively set the stage for Ukraine to declare a default and that’s precisely what happened just moments ago.

As Bloomberg reports, “Prime Minister Arseniy Yatsenyuk said Kiev is imposing a moratorium on the note due Dec. 20. Yatsenyuk announced the payment freeze at a government meeting in Kiev on Friday.”The finance ministry warned Russia on Thursday evening that it could not make the payment (due by Sunday).

“Considering that Russia has refused, despite our efforts, to sign an agreement on restructuring and to accept our proposals, the cabinet is imposing a moratorium on payment of the Russian debt worth $3 billion,” Yatsenyuk said, adding that Kiev “is also imposing a moratorium on the $507 million debt payment to Russian banks of two Ukrainian companies Yuzhnoe and Ukravtodor. From today all payments are suspended till our government or a court makes a decision.”

And it looks like a court will have to make “a decision” because Putin is probably going to sue. “Russia said as recently as last week it would take Ukraine to court if the payment was missed,” Bloomberg notes.

Earlier this month, Putin ordered Finance Minister Anton Siluanov to file a lawsuit against Ukraine in the event Kiev defaults. “It is strange. If they are so confident in the country’s solvency for the next year, then they could somehow participate during the last four years to share the risks,” Putin said, referencing Washington’s unwillingness to back Ukraine’s guarantees. “Fine. File the lawsuit,” he concluded.

So, the stage is now set for what will surely be an amusing court battle between Russia and Ukraine which, you’re reminded, are still essentially at war. In a preview of the kind of chuckle-inducing soundbites you’re likely to hear in the months ahead, we close with the following quote from PM Dmitry Medvedev:

“I have a feeling that they will not pay us back because they are crooks.”

Syria Stunner: German Intelligence “Cooperating” With Assad, Berlin May Reopen Embassy In Damascus

John Kerry went to Moscow on Tuesday and was absolutely elated when he stumbled on a Dunkin Donuts:

But America’s top diplomat didn’t travel halfway around the world just to get coffee (we don’t think). He also met with Sergei Lavrov and Vladimir Putin to discuss (what else?) Syria. You can get a decent idea of which side prevailed by taking a quick look at the following priceless image captured during a discussion between three of the world’s most powerful government officials:

In short, Kerry ended up conceding once and for all that the fate of Bashar al-Assad has effectively been backburnered for the time being. That’s a painful concession for Washington to make. After all, the whole idea was to topple the Assad government by arming, funding, and training a hodgepodge of Sunni extremists. Now, the US is effectively being forced into a situation where the proxy armies of America’s regional allies will be systematically dismantled only instead of destroying them after Assad fell and a puppet government was installed in Damascus (which was likely to original plan), they’re being routed by Assad himself with the help of the Russians and the Iranians.

Put simply: Assad isn’t going anywhere in the near-term.

On Friday we get still more evidence that the West is begrudgingly coming to terms with the fact that Assad will be sticking around for the foreseeable future, as Bild (citing anonymous sources) saysGermany is set to establish an intelligence cell in Damascus. Note the characterization of Assad as a “torturer”:

“Germany’s spy agency is working again with Syrian President Bashar al-Assad’s secret service to swap information on Islamist militants,” Reuters writes, citing the German daily.

Reuters continues: “Citing well-informed sources, the mass-circulation newspaper said German foreign intelligence BND agents had been traveling regularly to Damascus for some time for consultations with Syrian colleagues.”