Gold: $1091.90 up $13.50 (comex closing time)

Silver $13.96 up 1 cent

In the access market 5:15 pm

Gold $1094.00

Silver: $14.02

Today, gold broke above the critical resistance level of 1080.00 and once that level was cleared, gold was off to the races. But not silver.

At the gold comex today, we had a poor delivery day, registering 0 notices for nil ounces.Silver saw 0 notices for nil oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 199.48 tonnes for a loss of 103 tonnes over that period.

In silver, the open interest fell by 674 contracts even though silver was well up in price to the tune of 13 cents with respect to yesterday’s trading and without a doubt we had more short covering. We have an extremely low price of silver and a very high OI. However we moved back into backwardation in silver at the comex up until March. The total silver OI now rests at 167,520 contracts. In ounces, the OI is still represented by .838 billion oz or 120% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose by 3860 contracts to 413,688 contracts as gold was up $3.30 in yesterday’s trading.

we had a 1.90 tonnes withdrawal in gold inventory at the GLD, and his gold headed straight for Shanghai / thus the inventory rests tonight at 640.97 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver, we had huge changes in inventory at the SLV/we had massive withdrawals of 4.28 million oz /Inventory rests at 317.797 million oz.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fell slightly by 674 contracts down to 167,510 despite the fact that silver was up in price with respect to yesterday’s trading to the tune of 13 cents. The total OI for gold rose by 3,860 contracts to 413,688 contracts as gold was up $3.30 in price yesterday

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

b) Federal Reserve Bank of NY report of gold movement last month.

(Harvey)

3. ASIAN AFFAIRS

EARLY LAST NIGHT:

Last night, MONDAY night, TUESDAY morning: Shanghai closes down sharply throughout the day with an attempted relief rally into the close , Hang Sang falls, Chinese yuan rises a bit after a big devaluation over the holiday season. Stocks in Asia all in the red, . Oil falls slightly in the morning,. Stocks in Europe mixed. Offshore yuan continues to collapse as it trades at 6.64 yuan to the dollar vs 6.515 for onshore yuan:

4.EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

the Saudi currency the Riyal takes a nasty fall after ties are cut with Iran

( Press TV)

2, if you think that Syria is a mess just look at see what is going on in Libya:

( zero hedge)

6. GLOBAL ISSUES

i) North Korea claims a successful Hydrogen bomb. However it looks like more of an atomic blast than a H. Bomb

ii) An excellent commentary by Nomi Prins on the chaotic roadmap for 2016:

7. EMERGING MARKETS

none

8. OIL MARKETS

i)Crude drops into the 34 dollar column after record gasoline inventory build up plus Cushing increase;

( zero hedge)

ii)In 12 to 18 months you will find these 25 shale companies under default status:

9. PHYSICAL MARKETS

i) Steve St Angelo describes the huge fall in registered silver at the comex

(Steve St Angelo/Chris Powell)

ii) Bron Suchecki comments that we should pay more attention to central bank gold inventories instead

of Comex gold inventories

(Bron Suchecki/Perth Mint)

iii) China’s rigged markets will no doubt fall much further

v) Bill Holter’s important commentary tonight is entitled:

“Why would he say this?”

vi) The author is correct that once they initiate a gold price fix in yuan in April, that would be a game changer:

10 USA STORIES WHICH WILL INFLUENCE GOLD AND SILVER.

i) what a joke!! The ADP payrolls report shows highest employment in the private sector since 2014. And yet a load of this;

ii) zero hedge responds to the report why asking the ADP adjusters to explain why the USA ISM manufacturing at post recession lows along with the uSA Mfg PMI, plus the huge inventories to sales ratio at record levels, why on earth are the goods producers hiring at such a frantic pace?

iii) Although the trade deficit improved last month, it did so on the back of both exports and imports decreasing.

iv) ISM services collapses, lowest level since March 2014: (follows ISM mfg to a tee)

v) Total USA factory orders tumble for the 13th month in a row:

vi) the next company in the USA to fall on its sword: Chipotle as its December sales per same store falls 30%. They are also in receipt of a FDA subpoena:

vii) And now it is Apple’s turn to collapse

viii) Beige book is now out and the Fed is showing lack of confidence:

x) Another Macy’s Massacre: earnings down badly/an another 600 workers to be fire:

Let us head over to the comex:

The total gold comex open interest rose to 413,688 for a gain of 3860 contracts as gold was up by over $3.30 in price with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. Today, both scenarios were in full force.. We are now in the non active January contract which saw it’s OI fall by 50 contracts to 260. We had 0 notices filed upon yesterday, so we lost 50 contracts or an additional 5000 oz will not stand for delivery in this non active delivery month of January. The next big active delivery month is February and here the OI rose by 69 contracts up to 272,978. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 213,978 which is good. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was also poor at 112,122 contracts. The comex is in backwardation in gold up to April.

December contract month:

INITIAL standings for January

Jan 6/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 9709.300 oz

Scotia, Brinks, Manfra 302 kilobars |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 64,300.000 oz

Scotia

2,000 kilobars

|

| No of oz served (contracts) today | 0 contracts

oz |

| No of oz to be served (notices) | 260 contracts

(31000 oz) |

| Total monthly oz gold served (contracts) so far this month | contracts(nil oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 10,866.3 oz |

Total customer deposits 64,300.000 oz

January INITIAL standings/

Jan 6/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 76,963.83 oz

Brinks,CNT,Scotia |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 102,820.359 oz

SCOTIA |

| No of oz served today (contracts) | 0 contracts

nil oz |

| No of oz to be served (notices) | 361 contracts

(1,805,000 oz) |

| Total monthly oz silver served (contracts) | 12 contracts (60,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 76,963.83 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit;nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposit:

i) Into CNT: 600,411.06 oz

total customer deposits: 600,411.06 oz

total withdrawals from customer account: nil oz

we had 2 adjustments:

i) Out of Brinks:

150,860.900 oz was removed from the dealer side and placed into the customer side (probably a settlement)

ii) Out of CNT:

132,969.140 oz was removed from the dealer side of CNT and placed into the customer side of CNT

(probably a settlement)

And now the Gold inventory at the GLD:

Jan 6/2016/we had a withdrawal of 1.6 tonnes of gold from the GLD/Inventory rests at 640.97 tonnes/

Jan 5/2016: since my last report we had a total of 3.57 tonnes of gold withdrawal from the GLD/Inventory rests at 642.37 tonnes

Dec 23. will update GLD inventory tomorrow

Dec 22.no change in inventory tonight/inventory rests at 645.94 tonnes/

Dec 21/tonight a huge deposit of 15.77 tonnes of gold was added to the GLD/Inventory rests tonight at 645.94 tonnes

(With gold in backwardation it is highly unlikely that physical gold was added/probably a paper gold addition.)

Dec 18.2015: late last night: a huge withdrawal of 4.46 tonnes of gold/Inventory tonight rests at 630.17 tonnes

DEC 17.no changes in gold inventory at the GLD/Inventory rests at 634.63 tonnes/

dec 16/no changes in gold inventory at the GLD/inventory rests at 634.63 tonnes.

Dec 15.2105/no changes in gold inventory at the GLD/Inventory rests at 634.63 tonnes

Dec 14.no change in gold inventory at the GLD/Inventory rests at 634.63 tonnes

DEC 11/no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

Dec 10.2015/no change in gold inventory at the GLD/inventory rests at 634.63 tonnes

And now your overnight trading in gold and also physical stories that may interest you:

Gold Price Up On Mid East, Asia Risk – January Best Monthly Performance

– Gold up 2.5% in January on stock falls, Korea nuclear test, Middle East tensions

– Gold up an average of 4.4% in January over past decade

– January positive month for gold and silver

Gold prices hit a four-week high today over $1,088 per ounce, extending gains for the third day and leading to a 2.5% gain year to date. Deepening concerns over the indebted Chinese economy saw falls in stock markets again and tensions rose in Asia and the Middle East.

Stocks globally fell for a fifth day as China added to fears about its economy by allowing the yuan to weaken further in the ongoing currency war, and a nuclear test by North Korea added to a growing list of geopolitical worries.

Stocks globally fell for a fifth day as China added to fears about its economy by allowing the yuan to weaken further in the ongoing currency war, and a nuclear test by North Korea added to a growing list of geopolitical worries.

Overnight, North Korea said it successfully tested a miniaturised hydrogen nuclear device on Wednesday, setting off alarm bells in Japan and South Korea. Relations between Saudi Arabia and Iran collapsed over the weekend after the Kingdom’s execution of nearly 50 people including a Shi’ite cleric, a prominent critic of Saudi policy, set off violent protests and condemnation from Tehran.

Bullion has has been one of the best months for gold in terms of monthly performance in the last 10 years. Bloomberg confirms that today:

Bullion has advanced 4.4 percent on average in January over the past 10 years, climbing in all but three cases. Its performance in the first month beats that in any other. January is a time when Chinese shoppers stock up on gold in anticipation of the Lunar New Year.

Seasonally, the months of November, December, January and February have historically been positive months for gold. October often sees declines in the gold price followed by strong gains in November, December, January and February (see table above and chart below).

Risk aversion has seen gold move closer to key chart levels, including the December high at $1,088.70. A push above $1,088 would indicate that gold may have bottomed out for now after twice rebounding from the $1,045 area in December, a technical analyst told Reuters.

Silver is up 0.3 percent at $14.11 an ounce, while platinum is up 0.1 percent at $893.75 an ounce and palladium was down 0.6 percent lower at $533.40 an ounce.

Daily Prices

6 Jan LBMA Gold Prices: USD 1083.85, EUR 1,009.66 and GBP 739.84 per ounce

5 Jan LBMA Gold Prices: USD 1078.00, EUR 1,000.75 and GBP 734.31 per ounce

4 Jan LBMA Gold Prices: USD 1072.70, EUR 982.30 and GBP 725.02 per ounce

31 Dec LBMA Gold Prices: USD 1062.25, EUR 974.32 and GBP 716.36 per ounce

Breaking Gold News and Commentary Today – Click here

Must-Read Guide: Gold and Silver Storage Must Haves

China’s rigged markets could fall much further, much faster

Submitted by cpowell on Tue, 2016-01-05 13:10. Section: Daily Dispatches

Good thing the West’s markets aren’t rigged — or that they seldom suffer critical journalism like this.

* * *

China’s Rigged Markets Could Fall Much Further, Much Faster

By Craig Stephen

MarketWatch.com, New York

Monday, January 4, 2015

HONG KONG — Those fearing that China is the big risk in the year ahead for global markets hope that the first trading day of 2016 does not set the tone for the rest of the year.

Between a 7-percent fall in shares that triggered new circuit breakers on the Shanghai and Shenzhen stock exchanges and accelerated weakness in the yuan, there is ample fodder for China bears.

The question being posed anew is whether 2016 will be the year Beijing finally throws in the towel on its attempts to coerce multiple asset markets upward while its economy continues to sink in a sea of debt.

While yet more weak industrial activity numbers from the Caixin China December PMI got the new year off to a flat start, the bigger concern is whether the leadership still has the will or the ability to continue holding up stock prices as its confronts ever more painful policy choices. …

… For the remainder of the report:

http://www.marketwatch.com/story/chinas-rigged-markets-could-fall-much-f…

END

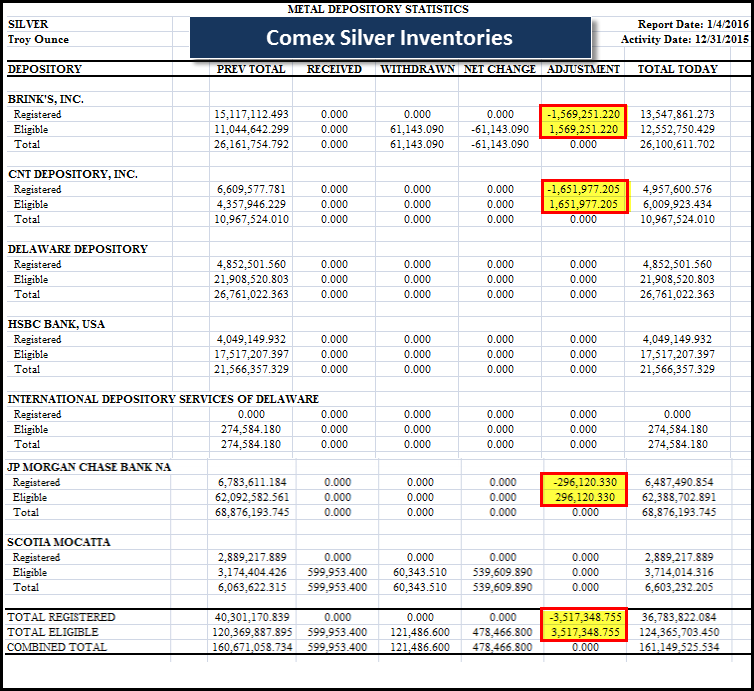

Yesterday, I alerted you on the huge drop in registered or dealer silver. Last night, Steve St Angelo commented on this huge reduction and what it means. He also comments on the huge increase in the Shanghai silver exchange

(courtesy Steve St Angelo/SRSRocco report)

In a stunning development, the Comex Registered Silver inventories experienced a large one day decline yesterday. Nearly 10% of total Comex Registered Silver inventories were removed from the exchange on the last day of the year and reported on Jan 4th.

According to the CME Group’s Metal Depository Statistics, 3.5 million ounces (Moz) of Registered Silver Inventories were withdrawn and transferred to the Eligible category:

As we can see, there was 1.5 Moz transferred out of Brinks, 1.6 Moz from the CNT Depository and nearly 300,000 oz removed from JP Morgan for a total of 3,517,348 oz. At the end of 2015 (Dec 31st), there were 40.3 Moz held in Registered Silver inventories at the Comex. After this large one day transfer, only 36.7 Moz remains.

This is an interesting development for two reasons:

- This is the lowest level the Comex Registered Silver inventories have been for the past three years and,

- The motivation for depositories to transfer that much silver out of its deliverable category.

First, the last time the Comex Registered Silver inventories were this low was in Feb 8th, 2013 at 36.2 Moz. The lowest the Registered Silver inventories fell to was 26.6 Moz in July 2011. However, the overall trend of the Registered Silver inventories was up until April, 2015… where they peaked at 70.5 Moz.

In just the past eight months, Registered Silver inventories at the Comex have fallen be nearly 50%. Again, Registered Silver inventories are those that are ready to be delivered into the market.

Second, something has motivated the holders of this silver to remove it so it is no longer able to be delivered into the market. If we assume that industrial silver demand has fallen due to a weaker U.S. and global economic activity and there is no longer a retail shortage of silver (as there was from June-Sept 2015), why are we continuing to see silver removed from the Registered Category?

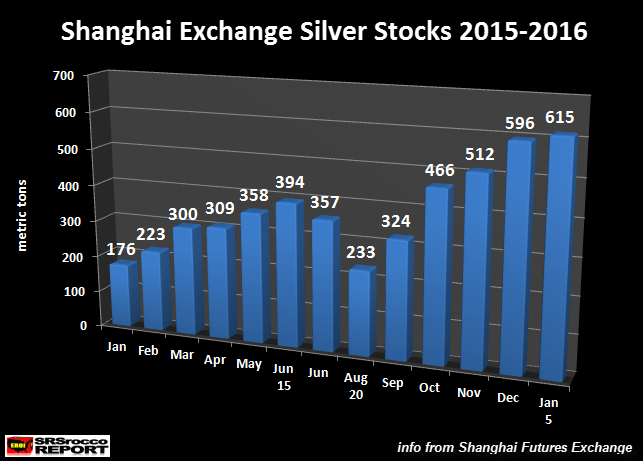

You would think we would be seeing the opposite as the Registered Silver inventories started to build in August, 2011… after the peak and decline of the silver price and investment demand. And interestingly, the opposite is taking place at the Shanghai Future Exchange.

Shanghai Future Exchange Silver Inventories Surge End Of Year

Silver inventories at the Shanghai Futures Exchange (SHFE) grew from a low of 176 metric tons (mt) in January 2015 to 394 mt in June. They bottomed in August at 233 mt and then continued to build steadily until spiking at the end of the year:

What is really interesting about the build of SHFE silver inventories is the rapid increase since Dec 28th. On Dec 28th, there were 535 mt of silver at the SHFE, only 23 mt higher than the beginning of the month. Then over the next week and including the first few days in 2016, total inventories at the Shanghai Futures Exchange jumped 80 mt to 615.

Precious metal investors need to realize the Chinese view gold more as an investment than silver. Furthermore, the Chinese also have to pay a 17% vat tax on silver investment. According to the 2015 World Silver Survey, Chinese silver bar investment demand was only 6.2 Moz in 2014 while Official Coins sales were 5.9 Moz. The notion that the Chinese are buying a lot of physical silver investment is not true… however, they are buying one hell of a lot of gold.

So, this spike of SHFE silver inventories must be motivated more by the decline of industrial silver demand in China than investment demand. China is the largest silver fabricator in the world as they consumed 5,788 mt (186 million oz) of silver in 2014 via industrial applications (2015 World Silver Survey).

Again, something very strange is happening here. The Comex continues to see a drain of its Registered Silver inventories (for delivery), while the SHFE inventories are showing a rapid increase.

It will be interesting to see what happens to the silver inventories at these two exchanges over the next 6 months. If Comex Registered Silver inventories continue to fall (just like the Gold Registered inventories), this could spell more trouble for the highly leveraged paper based precious metal markets going forward.

Please check back for new articles and updates at the SRSrocco Report. You can also follow us at Twitter below:

![]()

END

(courtesy Bron Suchecki/Perth Mint and Chris Powell/GATA)

important for you to read

Comex gold inventories don’t matter as much as central bank inventories do

Submitted by cpowell on Wed, 2016-01-06 15:37. Section: Daily Dispatches

10:42a ET Wednesday, January 6, 2016

Dear Friend of GATA and Gold:

The Perth Mint’s Bron Suchecki today notes that gold inventories on the New York Commodities Exchange are not necessarily a good indicator of tightness in the gold market, since “eliglble” gold — gold in Comex warehouses — easily can be converted to “registered,” gold available for delivery against Comex contracts. Suchecki’s analysis is headlined “Issuers Can Make Deliveries Using Eligible” and it’s posted at the Perth Mint’s research page here:

http://research.perthmint.com.au/2016/01/06/issuers-can-make-deliveries-…

This is a point GATA often has made, though in different ways and for different purposes.

That is, if, as GATA has maintained from its inception, central banks are intervening surreptitiously in the gold market to control currency values, interest rates, bond prices, and equity prices, central bank gold inventories are far more relevant to the gold price than mere Comex inventories. For through intermediary bullion banks, central bank gold inventories may become Comex inventories as quickly as “eligible” gold in Comex warehouses may be reclassified as “registered.”

That’s why, as the International Monetary Fund discerned in a secret report in March 1999, central banks intervening surreptitiously in the gold market insist on concealing their gold swaps and leases, lest the market get an idea of the real supply of gold, the supply available for intervention:

http://www.gata.org/node/12016

Indeed, studying Comex data last June, securities lawyer Avery B. Goodman concluded that bullion bank JPMorganChase was administering the U.S. government’s gold leasing and swapping operations and that the U.S. gold reserve was effectively guaranteeing Comex gold contracts, at least for the time being:

http://www.gata.org/node/15441

Yes, as Suchecki writes, some gold bugs make far too much of the decline of “registered” Comex gold stocks. But then many gold market analysts, including Suchecki himself, make far too little of the overwhelming documentation of surreptitious intervention in the gold market by central banks, since doing that can get one in trouble with the authorities. In fairness to Suchecki particularly, it must be noted that the Perth Mint is an agency of the government of Western Australia.

A summary of the documentation of central bank rigging of the gold market can be found at GATA’s Internet site here:

There’s a lot more of it here:

http://gata.org/taxonomy/term/21

GATA pleads for it to be analyzed, concurred in, or disputed — anything but ignored.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This is a strange one!! UBS says that we should buy gold because a 30% downfall in S and P is coming!

(courtesy UBS/zero hedge)

A Disturbing Warning From UBS: “Buy Gold” Because A 30% Bear Market Is Coming

As Wall Street axioms (Santa rally, January effect, as goes January etc.) are rapidly falling by the wayside at the start of 2016, following a chaotic but return-less 2015, the UBS analysts who correctly forecast last year’s volatility are out with their forecast for 2016. It’s simple – Sell Stocks, Buy Gold.

UBS Technical Analysts Michael Riesner and Marc Müller warn the seven-year cycle in equities is rolling over.

UBS expects S&P 500 to move into a 2Q top and fall into a full size bear market, with risk of a 20% to 30% correction into minimum later 2016 and worst case early 2017

“The comeback of volatility was the title of our 2015 strategy. Last year’s rise in volatility was in our view just the beginning for a dramatic rise in cross-asset volatility over the next few years,”

Noting that while equities have had a good run, Risener and Muller warn, “we are definitely more in the late stages of a bull market instead of being at the beginning of a new major breakout.”

Our key message for 2016 is that even if we were to see another extension in price and time, we see the 2009 bull cycle in a mature stage, which suggests the risk of seeing a significant bear cycle event in one to two years.

S&P-500 trades in 4th longest bull market since 1900 Bear markets are defined by a market decline of 20% and more. It’s a fact that since its March 2009 low, with 82 months and a performance of 220%, the S&P-500 now trades in its 4th longest and 5th strongest bull market since 1900. So from this angle alone we suggest the 2009 bull cycle has reached a mature stage.

Keep in mind, since 1937 the average downside in a 7-year cycle decline was 34%…

Having said that, if we look at equities globally the picture looks more diverse. Last year we said we think the May top in the MSCI World represents a major equity top. Our view is unchanged, and in this context it is important to understand and sort in the extent of last year’s summer correction. In the MSCI World universe, we saw in 20 out of 48 markets a correction of 20% and more (DAX -25%), which is per definition bear market territory. The MSCI Emerging Market has been factually trading in a bear market since 2011 but from its May top alone the EM complex lost another 28% into its late August low!

Together with the 200-day moving averages rolling over in more and more markets globally, the break of the 2011 bull trend in the Russell-2000 and the equally weighted Valueline-100 index in the US, as well as intact sell signals in our monthly trend work, we can clearly say that globally, a bear market is already underway in more and more markets; whereas the S&P- 500 has just corrected 13% from its May top, and where into H1 2016 we can still see the large and mega cap driven S&P-500, Dow Jones Industrial and Nasdaq Composite to hit a new all-time high.

In 2013, high yields topped out and particularly since 2014, we have a real bear market underway in the high yield segment, which in the meantime is forming a multi-year divergence versus the S&P-500, similar as prior to the major market tops in 2000 and 2007.

The bear market started with the energy complex but it is a trend, which is filtering through into other commodity themes, as well as Emerging Markets, Asia and at the end of the day into the Western world, which translated means we are running through a very classic credit cycle.

2016 is a Presidential Election year, which usually have a rather bullish track record in the 4-year cycle. However, if we look more selectively into this cycle there is a big divergence between a normal Presidential Election year and the 8th year of a presidential turn, which we highlighted red in chart 9.

Since 1920, more or less all 8th years of a presidential turn were amongst the worst election years.

Also, pattern-wise the two cycles have a very contrarian message where the average of all 8th years of a presidential turn is actually outright negative for next year, which we think would be quite a big surprise for most investors.

So if stocks are due for a 30% correction – what to do? Buy Gold…

Gold has been trading in a cyclical bear market since 2011.

In 2016, we expect gold and gold mines moving into an eight-year cycle bottom as the basis for the next multi-year bull market.

Initially, we see gold profiting as a safe haven and as of 2017, gold could profit from the US dollar moving in a major top and starting a bear market.

Tactically, over the last three years, we’ve tried playing bear market rallies in gold and gold mines several times. In 2013 and 2014, our targets were reached.

In 2015, the bounce in gold was weaker than expected. However, in all these cases we made it clear that we just expect a bear market rally before resuming its dominant cyclical bear trend. Generally, our cyclical roadmap and our long-term call on gold of the last few years has not changed.

A potential bottom in 2016 bottom could be a rather powerful bottom, since together with a four-year cycle low we have also an eight-year cycle low projection for this year. In this context we expect a potential 2016 low in gold to be the basis of a new multi-year bull market.

In contrast to the underlying secular trend in commodities (which has turned bearish) UBS sees gold (which is in our view a currency and not a commodity) still trading in a secular bull market.

Pattern wise we continue to see the 2011/2016 cyclical bear market in the same context as the 1975/1976 bear cycle in gold. Keep in mind, in the mid-70s gold lost 43% of its value from its January 1975 top before another gold bull market started into the January 1980 bubble peak. It is amazing to see that with a loss of 45% from its August 2011 top into the early December 2015 low, the decline in gold has more or less exactly the same proportion as in the mid-70s.

Furthermore, there are still a lot of market commentators who say that the August 2011 top in gold was the top of a bubble. According to the average gains we have seen in historical financial bubbles, the gold bull run from 2001 into 2011 (760%) was far away from any bubble territory. In the first gold bubble, gold gained 2400%. In the 1903 to 1929 Dow bubble, the Dow Jones Industrial gained 1200%. The 1979 – 1989 Nikkei bubble came in at around 2000% and the 1980 – 2000 Nasdaq bubble topped out a +3900%.

So if gold moves into a bubble, we would need to see a gold price of minimum $3300, and in this case we would still talk about a low bubble phenomena such as the 1903 – 1929 Dow Jones bubble!!

What kind of macro environment could justify such a gold bull market in the end of the decade?

In December we saw the Fed’s first rate hike. Even if we were to see another 1 or 2 rate hikes in H1 2016, with a 20% to 30% bear market event in later 2016 or into early 2017, it would bevery likely to see a big U-turn in the Fed policy where initially we should see a negation of the rate hikes and at the end of the day we would expect the Fed to move into QE4.

Our call is, that at the point where we see a Fed u-turn, we get the top of the decade in the US Dollar, and together with the accommodative stance of the ECB, BOJ and the PBOC, this would be the trigger for the ultimate reflationary trade, where equities, commodities and finally also gold could rally hard on the back of a big recovery in inflation towards the end of the decade.

And judging by the market so far this year – and post FOMC – the Buy Gold, Sell Stocks plan is already being implemented…

Preview YouTube video Fisher Fed At Fault

China to Start Yuan-Based Gold Price Fix in April: Game Changer?

China has been quietly accumulating a significant amount of gold bullion in recent years. They are now the top producer and top consumer of gold in the world. They are believed to keep all of their domestic production, plus import significant amounts from other nations. In addition, they have been buying up gold mines around the globe at steep discounts and bringing home gold they had stored in London, New York and Switzerland.

China has been quietly accumulating a significant amount of gold bullion in recent years. They are now the top producer and top consumer of gold in the world. They are believed to keep all of their domestic production, plus import significant amounts from other nations. In addition, they have been buying up gold mines around the globe at steep discounts and bringing home gold they had stored in London, New York and Switzerland.

After accumulating all of this gold, along with their close ally Russia, many believe they will eventually break the metal free from the price manipulation undertaken by the banks/governments in the United States and United Kingdom. Once price discovery moves from West to East, they will allow the price to float to free-market levels and the value of all the gold they have been accumulating will skyrocket.

Removing the gold price suppression will be accompanied by wholesale dumping of U.S. treasury bonds and test the world’s faith in the US dollar debt-based fiat currency system. This will give China, Russia and others a greater influence in world financial markets and better stability in their currencies. It may give them a considerable strategic advantage over the United States, a nation that many believe no longer has the gold that they claim. Indeed, with a lack of a comprehensive audit and unwillingness of officials to allow one, many believe the gold is no longer in Fort Knox.

Now we move to the really interesting part of this story. Not only has China been accumulating huge amounts of gold (on and off record), but they also launched their own international gold trading platform on the SGE. It has become the largest physical gold exchange in the world, with an estimated 52 times more physical gold withdrawals versus the predominantly paper exchange of the COMEX.

Fast forward to the first week of 2016 and China is warning foreign banks that they must participate in Yuan-based gold price fixing or lose their Chinese gold import rights. This first-ever Chinese benchmark is set to launch in April of this year and could be a game-changer for gold prices moving forward.

Reuters reported today that:

China has warned foreign banks it could curb their operations in the world’s biggest bullion market if they refuse to participate in the planned launch of ayuan-denominated benchmark price for the metal, sources said.

The world’s top producer and consumer of gold has been pushing to be a price-setter for bullion as part of a broader drive to boost its influence on global markets.

Derived from a contract to be traded on the state-run Shanghai Gold Exchange,the Chinese benchmark is set to launch in April, potentially denting the relevance of the current global standard, the U.S. dollar-denominated London price.

In a trial run for the fix in April 2015, some foreign banks participated along with many major Chinese banks. Traders at those banks said earlier that while they were interested in the benchmarking process, their legal and compliance teams may be reluctant.

Perhaps a little sensationalized, but Jim Willie recently commented:

The Gold market cannot be fixed by paper gold on a repeated basis, surely not in perpuity. When the Shanghai shock comes, all the Paper Gold structures will fall, all the FOREX derivatives will collapse, all the control rooms will go into panic mode.

The Shanghai shock is not likely to materialize all at once and cause an immediate collapse of the dollar, the COMEX or our fiat monetary system. However, it is another nail in the proverbial coffin and significantly increases the odds of more honest price discovery in precious metals as it moves from West to East.

The red line in the chart below shows Asian gold reserves as a percentage of total gold reserves. The percentage has been rising steadily for decades, but the pace of the increase has picked up significantly since the 2008/09 financial crisis.

If you believe that the gold price has been suppressed in order to maintain faith in fiat money and allow governments to continue deficit spending to secure their power, it is logical to conclude that gold prices may rise sharply as the disconnect between paper and physical pricing intensifies. And it would make sense for China, Russia and other BRICS nations to push for such a transition, as it would diminish the dominance of the United States in global trade and finance, leveling the playing field.

In any event, it will be an interesting development to watch during 2016. I believe it could be another catalyst in a long list that could cause a spike in gold and silver prices.

1 Chinese yuan vs USA dollar/yuan falls badly in value , this time to 6.5527/ Shanghai bourse: in the green with a late rally , hang sang: red

2 Nikkei closed down 182.68 or .99%

3. Europe stocks down badly /USA dollar index up to 99.39/Euro down to 1.0746

3b Japan 10 year bond yield: falls to .250 !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 118.37

3c Nikkei now just above 18,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI: 35.05 and Brent: 35.05

3f Gold up /Yen up

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to .538% German bunds in negative yields from 6 years out

Greece sees its 2 year rate rise to 8.80%/: still expect continual bank runs on Greek banks

3j Greek 10 year bond yield rises to : 8.31% (yield curve inverted)

3k Gold at $1085.30/silver $14.00 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble down 72/100 in roubles/dollar) 74.07

3m oil into the 35 dollar handle for WTI and 35 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0089 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0845 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/arrests 10 traders for Euribor manipulation

3r the 6 year German bund now in negative territory with the 10 year falls to + .538%/German 6 year rate negative%!!!

3s The ELA at 75.8 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.19% early this morning. Thirty year rate at 3% at 2.95% /POLICY ERROR

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

The Carnage Returns: Stocks Tumble After Sharp Chinese Devaluation; Brent At 2004 Lows; Gold Surges

On the first trading day of the year, stocks crashed after China shocked the world with a circuit-breaking market slide that was not contained by the government. On the second trading day, after the Chinese government intervened drastically, global equities stabilized if just barely.

Then overnight, even as Chinese stocks surged higher by 2.3% after the ban on major shareholder selling was extended, the global market was far more focused with what was going on in China’s currency, which as previously reported, plunged to new 5 year lows, while the spread between the onshore and offshore Yuan rose to a record wide, suggesting the depreciation in the currency is only going to accelerate from here, and a big payday for Kyle Bass is coming. Then again, how this is surprising since China’s December 11 announcement it would devalue against a basket of currencies, not just the USD, is not exactly clear to us.

“China is for sure back in focus,” said Didier Duret, chief investment officer at ABN Amro NV’s wealth-management unit. “I’d say this is an echo of what happened in August maybe more than a replay. It’s making people nervous.”

This accelerating depreciation, despite constant official lies to the contrary, such as this one from yesterday….

- CHINA’S YUAN WON’T SEE SHARP DEPRECIATION: SECURITIES JOURNAL.

… has clearly spooked traders and heightened concerns that the outlook for global growth is dimming. To be sure, North Korea’s first hydrogen bomb test overnight even as geopolitical tensions in the Mideast refuse to go away, have not helped risk sentiment. The MSCI All-Country World Index fell 0.4 percent at 10:49 a.m. London time. The Stoxx Europe 600 Index slid 1.1 percent and futures on the Standard & Poor’s 500 Index dropped 1.4 percent.

As a result, the sharp weakness seen early in the session in US equity futures has growing worse, and while global equities are down across the board, today’s session could be as bad as that of Monday if not worse, especially since moments ago Brent tumbled below $35 for the first time since 2004.

Elsewhere, the yen reached its strongest level since October and Treasuries rose for a fifth session on demand for haven assets. Finally, despite or perhaps due to the broad risk-off sentiment, gold has finally woken up and as of this morning was trading at the highest price in over a month.

Before we go into details of the overnight carnage, this is where we stand currently: S&P futures now down 33 points or 1.63% while 2Y Treasury rallies pushing its yield back below 1% as EU stocks extend their drop after China weakened its currency, North Korea says it tested a hydrogen bomb; Brent crude falls to lowest level since 2004.

Equity Futures:

- S&P 500 futures down 33pts or 1.63% to 1978; (high 2012; low 1976)

- DJIA futures -266pts or 1.5%

- Nasdaq 100 futures -79pts or 1.8%

- Stoxx 600 down 1.5% to 354

- MSCI Asia Pacific down 0.9% to 127

- Brent Futures down 3.1% to $35.09

- Gold spot up 0.5% to $1,083

- Silver spot up less than 0.1% to $13.99

Commodities:

- WTI Crude -2.5% to $35.09/bbl (range $34.80 to $36.39)

- Brent Crude -3.6% to $35.12/bbl

- Gold +0.8% to $1,087/oz

- Copper -1.1% to $2.07/lb

Rates/FX:

- 30-yr -5.92bps to 2.9359%

- 10-yr -5.31bps to 2.1826%

- 2-yr -2.19bps to 0.992%

- Dollar Index Spot little changed at 99.43

- Euro/Dollar -0.1% to $1.074

- GBP/Dollar -0.1% to $1.4659

- Dollar/Yen +0.6% to 118.37

Looking at regional markets, Asian stocks traded mostly lower following the subdued lead from Wall St., with further weak Chinese data, more aggressive CNY softening by the PBoC and a North Korea nuclear bomb test adding to the risk averse tone. ASX 200 (-1.2%) was led lower by commodity-linked weakness, while Nikkei 225 (-1.0%) declined as JPY strength dampened exporter sentiment, with poor Chinese services PM! which posted a 17-month low, adding to the region’s gloom . Elsewhere, US equity futures also saw a bout of pressure overnight in the wake of a North Korean nuclear bomb test and further softness in the CNH which was perceived as a negative signal from the world’s second largest economy, while the MSCI emerging market index reached its lowest level since July 2008. However, the Shanghai Comp (+2.3%) outperformed on reports that China is to extend the ban on major shareholders from selling shares. Finally, 10yr JGBs gained as the negative sentiment in the region spurred demand for safer assets, while the BoJ were also in the market for 1.27tr1 of government debt.

A quick reminder why China’s devaluation is bad – in a zero sum world, China’s export gains, mean everyone else’s export loses: “This isn’t good for the rest of the world. Until China stops weakening the yuan, global markets will struggle to stabilize,” said Koichi Kurose, Tokyo-based chief market strategist at Resona Bank Ltd. “The Chinese authorities may be trying to prop up the economy by boosting exports, but while that’ll help one part of China’s economy, it comes at the sacrifice of someone else.”

“There’s word spreading in the market that state funds are buying, but the idea is to hold up the market, not to bolster it by a large margin,” said Dai Ming, a fund manager at Hengsheng Asset Management Co. in Shanghai.

Top Asian News:

- Caixin China Services PMI Falls to Second Lowest in Decade: Gauge fell to 50.2 in Dec. vs 51.2 in Nov.

- Chinese Brokerage Head Targeted in Probe by Communist Party: Changjiang Securities case adds to wave of probes in finance

- Rupee Bonds Cheaper Than Loans Make Arrangers Bullish for 2016: Offerings will probably rise to a record this year

- Huawei Starts Selling Honor-Brand Smartphone in U.S. Market: Available for pre-order on Amazon and Newegg.com

European equities sank after emerging-market stocks dropped to a six-year low and developing-nation currencies slid on concern a weaker yuan may spark a wave of global turmoil similar to what followed China’s shock depreciation in August. Indeed, sentiment in Europe today has once again been dictated by events in Asia overnight, with China remaining in focus, while elsewhere sentiment has been shaken by North Korean hydrogen bomb tests . European equities spent the morning in the red, with Euro Stoxx down over 1% on the day and around 3.8% for the week. Dialog Semiconductor (-4.2%) is the worst performer in Europe today after reports that Apple are to reduce output of its latest iPhone by 30%.

Amid the concerns surrounding China, the materials sector is the notable underperformer amid growth concerns, while the metals complex sees gold as the notable outperformer amid risk off sentiment. Separately, the energy complex has seen further softness this morning to pare yesterday’s API inventory inspired gains, with the weakness attributed to USD strength.

“It could be a difficult year,” said Fredrik Nerbrand, HSBC’s London-based head of asset allocation. “We believe 2016 is a year for capital protection rather than appreciation. The increased focus on uncertain and volatile economic data releases is likely to cause markets to overreact.”

Top European News:

- John Lewis Provides Holiday Cheer as Store’s Online Sales Soar: Web sales rose 21% in six weeks ended Jan. 2

- U.K. Services Cool in December as Confidence Hits 3-Year Low: Markit said report together with its latest surveys of manufacturing and construction indicates U.K. economy grew 0.5% in 4Q, down from 0.6% it estimated last month.

- ‘Brexit’ Gamble Enters Crunch Phase as Cameron Returns to Merkel: Cameron travels to Bavaria on Wednesday to meet with German Chancellor Angela Merkel

Dialog Semiconductor Plc, the chipmaker whose biggest client is Apple Inc., dropped 4.3 percent as Nikkei Asian Review reported the U.S. company would reduce the first quarter output of its latest iPhones by about 30 percent. AMS AG and ARM Holdings Plc, also Apple suppliers, lost at least 3 percent.

Taiwan’s Largan Precision Co. and Catcher Technology Co. led declines among Apple suppliers, slumping more than 5 percent and sending Taiex index to a four-month low.

In FX, today’s session was again dominated by the JPY pairs, with Asia once again providing the major drivers of trade. China Caixin services PMI contract dropped significantly, and with the CNH weakening to fresh multi year highs, growth and instability concerns dominated. North Korea added to global woes with its first H-bomb test, so it was no surprise to see spot and cross JPY extending recent lows, though notable was USD/JPY finding strong support comfortably ahead of 118.00. As a result, the yen appreciated 0.5 percent to 118.46 per U.S. dollar and reached 118.34, the strongest since Oct. 15. Japan’s currency surged more than 1 percent against the yuan to the highest level since October 2014, just before the Bank of Japan expanded monetary easing.

EUR/JPY has tested 127.00 and AUD/JPY to sub 84.00, dragging the respective spot rates lower, though anticipated EUR/USD bids ahead of 1.0700 continue to support. CAD has raced through 1.4000 on broader risk sentiment, with fresh losses in Oil adding to weakness here. AUD now eyeing a fresh move on .7000. GBP largely ignored the small miss in UK services PMI (55.5 vs 55.6 exp).

In commodoties, Brent crude for February settlement fell as much as $1.59, or 4.4 percent, to $34.83 a barrel on the London-based ICE Futures Europe exchange. West Texas Intermediate declined 2.5 percent after dropping 2.2 percent Tuesday. U.S. oil inventories probably increased by 500,000 barrels last week, according to a Bloomberg survey before Energy Information Administration data Wednesday. The industry-funded American Petroleum Institute was said to report stockpiles fell by 5.6 million barrels while fuel supplies gained.

Gold for immediate delivery advanced 0.6 percent to $1,084.52 an ounce following two days of gains. Demand for the precious metal has been bolstered as gyrations in global stock markets enhance its allure as a haven investment. Zinc on the London Metal Exchange dropped 2.2 percent to the lowest since Dec. 29. Copper fell 0.9 percent.

It’s a busy session on the US calendar today, where the session kicks off firstly with the December ADP employment change print, followed closely by the November trade balance. The final December services and composite PMI’s follow this before we get the all-important ISM non-manufacturing where market expectations are currently sitting for little change at 56.0. November factory orders data along with the final revisions to durable and capital goods orders are also due out before we get the Fed’s FOMC minutes from its first rate hike in 9 years at 2pm.

Top Global News:

- Yuan Sinks to Five-Year Low as PBOC Surprises With Weaker Fixing: China sending out confusing policy signals, Macquarie says

- Valeant Said to Name New CEO With Pearson Still Hospitalized: Schiller, Rosiello may be candidates, Wall Street Journal says

- North Korea Says It Successfully Tested First Hydrogen Bomb: Regime in Pyongyang says won’t give up nuclear development. North Korea’s Hydrogen Bomb Claim Disputed by Weapons Experts: Data show explosion yield lower or similar to previous blasts

- Apple Suppliers Drop in Asia After IPhone Output Cut Report: Nikkei Asian Review reports cut of 30% in first quarter

- Brent Crude Drops to 11-Year Low Before U.S. Oil-Stockpile Data: Citigroup, UBS see possible slide in prices toward $30

- Halliburton Faces Longer EU Probe on Missing Early Offer Slot: Co. will likely face protracted antitrust review of its plan to buy oil services rival Baker Hughes for $26b

- Verizon Said to Start Process to Sell Data Centers, Reuters Says: Co. hopes to get more than $2.5b from sale

- NuVasive to Acquire Ellipse Technologies in $410m Deal: Elipse develops surgical implants to treat skeletal deformities

Bulletin Headline Summary from RanSquawk and Bloomberg

- Aggressive CNY softening by the PBoC and a North Korea nuclear bomb test have added to the weeks risk averse tone

- In FX markets, today’s session was again dominated by the JPY pairs, with Asia providing the major drivers of trade

- Highlights today include, US ADP employment change, ISM non-manufacturing composite, factory orders, durable goods and the release of FOMC minutes

- Treasuries gain for a fifth day as China devalues yuan, North Korea says it successfully tested its first hydrogen bomb and a report said Apple would reduce 1Q output of iPhones.

North Korea’s hydrogen bomb test risks reigniting tensions with China and the U.S. after months of calm even as some experts cast doubt on the full extent of Pyongyang’s claim - The yuan sank to a five-year low and tumbled 1.1% in Hong Kong after the PBOC set the reference rate at an unexpectedly weak level, a sign that policy makers are becoming more tolerant of depreciation

- A private Chinese services gauge slumped to the second- lowest reading since the series began a decade ago and close to a level signaling contraction, suggesting conditions may be weaker than the government’s official index indicates

- The Chinese economy may be headed for a “hard landing” as borrowers are taking on record amounts of debt to repay interest on their existing obligations, said Marc Faber

- Apple Inc. suppliers from Asia to Europe fell after a report saying the world’s most valuable company would reduce 1Q production of its latest iPhones by about 30%

- S&P 500 will fall into a full-sized bear market this year as seven-year cycle in equities is rolling over, UBS technical analysts wrote in a note

- Merkel’s government said about 1.1m asylum seekers entered Germany last year, reaching a record as Europe struggles to manage the influx of refugees from the Middle East and beyond

- A U.K. services gauge eased in December as risks including a British exit from the EU weighed on hiring and business expectations fell to a three-year low

- $25.75b IG priced yesterday, no HY. BofAML Corporate Master Index OAS holds at +173, YTD range 180/129. High Yield Master II OAS narrows 7bp to +703; YTD range 733/438

- Sovereign bond yields lower. Asian and European stocks lower, U.S. equity-index futures slide. Crude oil lower and copper lower, gold gains

US Event Calendar

- 2:00pm: FOMC Minutes, Dec. 15-16

DB’s Jim Reid concludes the overnight wrap

With the exception of bourses in China, it’s been a broadly weak start for risk assets for most of the region as concerns reverberate around further weakening of the Chinese Yuan, while headlines of nuclear testing in North Korea are not helping sentiment. Losses are being led out of Japan where the Nikkei is -1.15%, while there’s been falls also for the Hang Seng (-0.92%), Kospi (-0.50%) and ASX (-1.07%). In credit the Asia iTraxx is currently +3bps wider. This is in contrast to moves in China however where the Shanghai Comp (+0.69%), CSI 300 (+0.35%) and Shenzhen (+0.56%) are all up at the midday break and more than likely a sign of those government support measures yesterday. Much of the newsflow this morning however is being dominated by the latest moves in China’s currency. The PBoC set the Yuan fix 0.22% weaker this morning (lower for the seventh day in a row) to the weakest level since 2011 while the spread between the onshore and offshore currencies at one stage widened to the largest on record. The offshore Yuan is currently down -0.48% as we type and at its weakest level since 2010. That’s seen EM currencies come under similar pressure this morning where there are declines of around half a percent for most.

Meanwhile we’ve also had some data out this morning and it’s made for more disappointing news. The non-official Caixin services PMI in China revealed a 1pt fall to 50.2, the lowest reading since July 2014. Combined with the soft manufacturing print from earlier in the week, the composite dipped below 50 last month to 49.4, a fall of 1.1pts. China was cited as a big risk for markets in most 2016 outlook publications and while it’s very early days, events there are dominating markets and price action for now.

Recapping the rest of the news and price action yesterday. 2016 hasn’t been too kind for Oil markets so far and yesterday saw WTI (-2.15%) take another dip lower, at one stage falling below $36 only to finish slightly above that by the closing bell. Despite that US HY spreads actually closed more or less flat although still underperformed relative to the modest gains over in Europe. With markets a bit more stable, yesterday saw the new issue market get going, with over $25bn pricing in the IG space alone.

Meanwhile, yesterday saw our US economists slash their Q4 GDP forecast. They now expect Q4 real GDP to be just 0.5%, a full percentage point cut from the previous forecast while at the same time highlighting that this still might be too high in light of what could be a much larger inventory liquidation than what they have assumed. This downward adjustment has the effect of now lowering their projected Q4-over-Q4 rate of real GDP growth by 30bps to 1.7%. They highlight however that some of the expected Q4 GDP softness may carry over into the current quarter and so have also trimmed their current quarter growth projection by 50bps to 1.5%. Highlighting the reasons for the downward changes to the forecasts, our team highlight that the data released over the last couple of weeks (i.e. durable goods, international trade, constructing spending and manufacturing ISM) have been softer than expected with most of this adjustment due to less stockpiling. They point out that there is a high correlation between the change in private inventories and the inventory component of the manufacturing ISM (nearly 0.8). In fact, last quarter ISM inventories fell to 44.3 from 48.8, the lowest since Q4 2009, when inventory liquidation totaled nearly -$50bn. This raises the possibility that inventories could in fact be lower than what they predict and raising the possibility of taking GDP temporarily into negative territory. It’s worth reminding, as we noted yesterday, that the Atlanta Fed recently downgraded their Q4 GDP forecast to just 0.7%.

Staying on the data theme, after Monday’s disappointing German inflation numbers, Euro area CPI failed to meet hopes for a modest rise after the core reading came in unchanged at +0.9% yoy in December (vs. +1.0% expected), with an estimate for the headline at +0.2% yoy. Italian CPI (-0.1% mom vs. +0.2% expected) also missed to the downside, while Germany’s unemployment rate held steady at 6.3% in December as expected. Meanwhile in the US we saw the ISM NY print rise 1.3pts in December to 62.0, while the total vehicle sales reading for last month showed a slightly disappointing pullback in sales to 17.2m on an annualized basis (from 18.1m).

It’s set to be a busy day ahead with a packed calendar for us to get through. This morning in Europe will be all about the PMI’s with the final services and composite prints due for the Euro area, Germany and France as well as indicators out of the UK, Italy and Spain. French consumer confidence data and Euro area PPI is also due out in the European session this morning. The US session kicks off firstly with the December ADP employment change print, followed closely by the November trade balance. The final December services and composite PMI’s follow this before we get the all-important ISM non-manufacturing where market expectations are currently sitting for little change at 56.0, although our US economists are less optimistic and expect a drop to 54.0 (from 55.9). November factory orders data along with the final revisions to durable and capital goods orders are also due out before we get the aforementioned FOMC minutes at 7pm GMT.

ASIA AFFAIRS

let us begin:

Last night, TUESDAY night, WEDNESDAY morning: Shanghai closes UP with an relief rally into the close, the only bourse to rise , Hang Sang falls badly, Chinese yuan sharply down with another big devaluation. Stocks in Asia all in the red, . Oil falls again in the morning,. Stocks in Europe deeply in the red. Offshore yuan continues to collapse as it trades at 6.67 yuan to the dollar vs 6.5527 for onshore yuan:

A Shocked Wall Street Reacts To China’s “Surprising” Devaluation

Less than a month ago, and just days after the Yuan was finally inducted into the IMF’s hall of reserve currency fame, the Chinese Foreign Exchange Trade System, a part of the PBOC, made it very clear that what was about to happen would not be pretty, when it announced – in a statement which clearly everyone ignored – that going forward it would index the relative strength of the CNY not to the USD but the a basket of currencies (against which the USD to which it is pegged has been soaring).

At the time we explained that “what this means is that for anyone who thought the Yuan devaluation is over, now that the currency is at the lowest level relative to the dollar since 2011, the reality is that the devaluation relative to everyone else is only just starting.

And, with the PBOC’s warning that the “RMB is relatively a strong currency among the major international currencies” the real devaluation is, just as we warned four months ago, about to be unleashed. Expect at least a 15% reduction in Trade-Weighted terms in the coming weeks and months, especially if the Fed hikes.

One month later, it appears that not a single person heeded this warning, and now that the PBOC has unleashed a whopper of a devaluation round…

… precisely as we warned a month ago, everyone is panicking. So, more for comic relief than anything, here are Wall Street’s reactions to last night’s latest “shocking” PBOC devaluation, which nobody could have possibly seen coming.

Sean Callow, Sydney-based FX strategist at Westpac:

- Today’s fixing was a big surprise, and impression is that upside risks to USD/CNY have grown

- Allowing the yuan to trend lower against the dollar this year is consistent with the need to loosen domestic financial conditions to support growth

- PBOC may not tolerate widening CNY-CNH spread for long since it will encourage capital outflows

Tommy Xie, Singapore-based economist at OCBC:

- PBOC’s actions are conflicting: there was suspected intervention yesterday and sentiment stabilized, but it set such a low fixing today

- PBOC may be taking dollar demand into consideration: usually at the start of a new year, retailers’ and corporates’ foreign-exchange requirements are higher

- Central bank may be using the fixing to convey a message to the market that it doesn’t want the RMB index to be too strong

Zhou Hao, Singapore-based senior economist at Commerzbank:

- Lowered-than-expected yuan fixing today shows authorities will tolerate more weakness for the time being

- Will help loosen monetary conditions; still, risk of capital outflows could increase concurrently

- Increasing outflow pressures may rule out excessive drop in yuan

Liu Dongliang, Shenzhen-based senior analyst at China Merchants Bank:

- Yuan depreciation this week aims to stabilize the yuan index amid a stronger dollar environment

- Expects 5%-10% depreciation by end of the year, though this depends on the pace of PBOC’s intervention and health of macroeconomy

So to avoid any further surprise, here is a preview of what happens next: China continues to devalue, and does so aggressively. But don’t believe us. Here is what Kyle Bass said over the weekend:

“Given our views on credit contraction in Asia, and in China in particular, let’s say they are going to go through a banking loss cycle like we went through during the Great Financial Crisis, there’s one thing that is going to happen: China is going to have to dramatically devalue its currency.”

His full thoughts here.

end

Eyewitness Account Of The “Monstrous” Migrant Attacks In Germany: “It’s Like Civil War”

On Tuesday, we documented multiple reports that suggest as many as 1,000 men “of Arab or North African origin” participated in what appeared to be coordinated attacks on German women in Cologne.

“About 90 women have reported being robbed, threatened or sexually molested at New Year celebrations outside [the city’s] cathedral,” Reuters writes, adding that the men were “between 18 and 35” and appeared to be “mostly drunk.”

Cologne mayor Henriette Reker called the incident “unbelievable and intolerable” while Justice Minister Heiko Maas described the attacks as “a new scale of organized crime.”

For her part, Reker has been variously criticized for comments which seem to place some of the blame with the victims. “The Mayor of Cologne said today that women should adopt a “code of conduct” to prevent future assault at a crisis meeting following the sexual attack of women by 1000 men on New Year’s eve,” The Independent reports. “The suggested code of conduct includes maintaining an arm’s length distance from strangers, to stick within your own group, to ask bystanders for help or to intervene as a witness, or to inform the police if you are the victim of such an assault.”

“We need to prevent confusion [among asylum seekers] about what constitutes happy behaviour and what is utterly separate from openness, especially in sexual behaviour,” Reker said, as though this might all be one big misunderstading.

“Ms Merkel where are you? What do you say? This scares us!,” read a sign held by one of hundreds of protesters who gathered outside the cathedral on Tuesday. Here are some images from the demonstrations:

“A spokeswoman for the interior ministry in North-Rhine Westphalia, the state in which Cologne is located, said there were three suspects but declined to give further details,” Dow Jones says, before detailing the alleged attacks: “Police have said the women reported small groups of men attacking them among a crowd of around 1,000 people that had gathered in front of the station to set off fireworks. Women were allegedly cornered by groups of 20 to 30 men, mugged and in some cases sexually assaulted.”

Assaults were also reported in Hamburg and Stuttgart. Authorities are attempting to discern if there’s a connection.

“Mrs Merkel, is Germany ‘colorful and cosmopolitan’ enough for you after the wave of crimes and sexual attacks?,” AfD party leader Frauke Petry tweeted, taunting the iron chancellor’s open-door policy for Mid-East asylum seekers, more than 1.1 million of whom streamed into the country in 2015.

While Integration commissioner Aydan Ozoguz warned Germans to avoid putting migrants under “blanket suspicion” for the attacks, it is precisely these types of incidents that trigger dangerous bouts of scapegoating xenophobia, embolden right-wing political movements, and provoke violent responses from otherwise peaceful people who feel their home is being invaded by hostile foreigners. As we put it on Tuesday, “at this point it is too late for damage control, however, as this has become a case of guilty until proven innocent.”

Below, find a first-hand account of the New Year’s Eve assaults in Cologne from Ivan Jurcevic, a hotel club bouncer who was on the job (literally) as the melee unfolded. “These people that we welcomed just three months ago with teddy bears and water bottles … started shooting at the cathedral dome and started shooting at police,” Jurcevic says. “Well seasoned police officers then confessed to me that they never saw something like this in their entire lives,” he adds. “They called it a ‘civil war like situation.'”

‘Saudi currency takes a tumble after ties cut with Iran’

-

The Saudi riyal has taken a nosedive after Riyadh cut its ties with Iran. (file photo)

Saudi Arabia’s national currency, the riyal, has fallen sharply in the wake of Riyadh’s move to sever ties with Tehran, according to Reuters.

The Saudi money dropped against the US dollar in the forward foreign exchange market early on Monday, raising concern in the Persian Gulf monarchy that dollar funding for the kingdom could become more expensive, the report said.

On Sunday, Saudi Foreign Minister Adel al-Jubeir announced the kingdom’s severing of diplomatic relations with Iran following Tehran’s strong condemnation of the Riyadh regime’s Saturday execution of prominent Shia cleric Sheikh Nimr al-Nimr.

On Monday, one-year dollar/Saudi riyal forwards jumped to 680 points, near a 16-year high, from a close of 425 points on Thursday.

The riyal has little scope to move in the spot foreign exchange market because of its peg of 3.75 to the dollar, so banks use the forwards market to hedge against risks, the report said.

In the last few months, the riyal dropped in the forwards market to its lowest level since 1999 because of fears that huge Saudi budget deficits due to low oil prices might eventually force Riyadh to abandon the currency peg.

An austerity budget for 2016, which Riyadh announced last week appeared to partly ease such fears, but geopolitical tensions may now increase them.

According to Reuters, the breaking of diplomatic ties will not necessarily have a direct impact on the economies of Iran and Saudi Arabia, which have ‘minimal’ trade and investment ties.

But geopolitics could make foreign banks and investors more wary of funding Saudi Arabia, at a time when Riyadh is considering borrowing abroad to ease the pressure of funding its fiscal deficit on the domestic banking system.

“One-year forwards will likely touch 800 points levels this week, depending on the level of escalation of the events between Saudi and Iran,” Reuters quoted a senior bank trader from the region, who spoke on condition of anonymity.

A recent report said Saudi Arabia’s economic growth is expected to further slow down in 2016 after the country announced record budget deficits due to slumping oil prices.

Jadwa Investment’s forecast report, released last month, said the Saudi economy will grow by only 1.9 percent this year, down from 3.3 percent in 2015.

end

\

if you think that Syria is a mess just look at see what is going on in Libya:

(courtesy zero hedge)

“Pray For Us”: Libya Issues “Cry For Help” As ISIS Advances On Oil Fields

“We are helpless and not being able to do anything against this deliberate destruction to the oil installations. NOC urges all faithful and honorable people of this homeland to hurry to rescue what is left from our resources before it is too late.”

That’s from Libya’s National Oil Corp and as you might have guessed, it references the seizure of state oil assets by Islamic State, whose influence in the country has grown over the past year amid the power vacuum the West created by engineering the demise of Moammar Qaddafi.

The latest attacks occurred in Es Sider, a large oil port that’s been closed for at least a year.

Seven guards were killed on Monday in suicide bombings while two more lost their lives on Tuesday as ISIS attacked checkpoints some 20 miles from the port. “Es Sider and Ras Lanuf, Libya’s biggest oil ports, have been closed since December 2014,” Reuters notes. “They are located between the city of Sirte, which is controlled by Islamic State, and the eastern city of Benghazi.”

ISIS also set fire to oil tanks holding hundreds of thousands of barrels of crude. “Four tanks in Es Sider caught fire on Tuesday, and a fifth one in Ras Lanuf the day before,” Ali al-Hassi, a spokesman for the the Petroleum Facilities Guard told Bloomberg over the phone.

(a fire at Ras Lanuf)

(a smoking storage tank in Es Sider)

Ludovico Carlino, senior analyst at IHS Country Risk says the attacks are “likely diversionary operations” during Islamic State’s takeover of the town of Bin Jawad, a seizure that may enable the group to expand and connect “its controlled territory around Sirte to the ‘oil crescent.’”

Islamic State is pushing east from Sirte in an effort to seize control of the country’s oil infrastructure, much as the group has done in Syria and Iraq. As Middle East Eye wrote last summer, “the desert region to the south of the oil ports has been strategically cleared in a series of attacks by IS militants on security personnel and oil fields, where employees have been killed and kidnapped, and vehicles and equipment seized.”

“I expect they will try and take Sidra and Ras Lanuf and the oil fields on the west side of the oil crescent,” one oil worker said. “There are few people left to protect the oil fields apart from local security from isolated towns.”

Efforts to protect Libya’s oil are complicated immeasurably by the fractious (and that’s putting it nicely) political environment.

In short: the country is a modern day Wild West and a strong central government is now a distant memory. This makes administering the country’s resources nearly impossible. Oil production is now just a quarter of what it was under Qaddafi. Essentially, both of Libya’s two governments have what they call a National Oil Corp. The eastern NOC is run by the exiled government in Tobruk (which is internationally recognized), where the House of Representatives was exiled in 2014 after elections produced an outcome that wasn’t agreeable to Islamist elements in Tripoli.

Unfortunately, large foreign oil companies won’t work with Tobruk’s NOC which sets up the following ridiculous scenario: the internationally recognized government in Tobruk has an NOC no one wants to work with, while Tripoli’s NOC (which foreign oil companies will do business with) is run by a government that the world doesn’t deem legitimate.

To top it all off, there’s every reason to believe that neither Tobruk nor Tripoli actually control the country’s oil. Here’s Foreign Policy:

On the ground, the conflict involves far more than just the two bickering governments. Libya is composed of dozens of tribes, each with its own shifting interests and allegiances. “There’s a question about the extent to which the political forces actually have control over the important militias on the ground,” said Chivvis. “I think all this comes down to who controls the oil; it comes down to alliances on the ground. Which political forces control which sites within Libya.”

Ibrahim Jadhran is a perfect — and crucial — example. The 35-year-old was a militia leader during the 2011 revolution, and was appointed commander of the Petroleum Defense Guards by the still-unified transitional government in 2012. Originally from the eastern city of Ajdabiya, the rogue militia leader is an outspoken advocate of a federal system for Libya and frequently uses his power to open or close oil ports, shutting off oil exports — and therefore salaries — when he disagrees with either government.

“One of the initial causes for the plummeting of Libyan oil production was the blockade imposed by Ibrahim Jadhran in August of 2013,” said Porter. The commander has continued the tactic of stoppages in defiance of both regimes, even trying to steal a tanker full of crude to sell on the black market. The ship was finally stopped by the U.S. Navy off the coast of Cyprus.

Jadhran’s power is not to be underestimated. In fact, according to local media reports, it was actually him, and not the Tobruk government, that closed the Zuetina port. As Porter points out, it is Jadhran — not Tripoli or Tobruk — who truly controls exports.

Got that? There are two governments and two NOCs, but that doesn’t really matter because the whole show is run by a militia leader. “Jadhran is a mystery even to us. We have not yet understood what he really is, apart from an oil thief,” Misrata Military Council head Ibrahim Beitemal told Middle East Eye last year.

Ali al-Hassi (quoted above) is a spokesperson for Jadhran’s forces.

Islamic State then, is apparently at war with Jadhran which is interesting for a number of reasons.

First, Jadhran’s brother is in ISIS. “ISIS’ Libya branch released an online statement earlier in the week claiming to have taken control of the coastal city of Bin Jawed, about 120 miles east of Sirte,” CBS reported on Monday. “Bin Jawed is the last city before the oil town of Sidra and the huge oil port of Ras Lanouf, both currently witnessing fierce clashes between ISIS and al-Jadhran’s men.” And more: “ISIS fighters were reportedly attacking Siddra from three directions, aided by al-Jadhran’s own brother, who apparently joined the ISIS camp.”

Additionally, some say Jadhran once tried to broker a deal with the group and it’s not entirely clear what, if any, relationship he has with the militants. “We have been told that Jadhran proposed some reinforcements to ISIS but on the condition that he kept control of the oil ports and fields, but this was rejected,” a source told Middle East Eye.

So Libya’s vast oil wealth is effectively up for grabs and the person guarding it has a brother who not only joined ISIS, but is actually participating in the battle for key ports and facilities. Now, Britain is apparently on the verge of sending in thousands of troops to halt the ISIS advance in yet another example of the West engineering regime change only to go back in later in a futile attempt to clean up the mess.”Crack SAS troops are in Libya preparing for the arrival of around 1,000 British infantrymen to be sent against ISIS there in early 2016,” The Mirror reports. “The operation will involve around 6,000 American and European soldiers and marines – led by Italian forces and supported mainly by Britain and France.”

Of course that wouldn’t be necessary if the West hadn’t thrown out the government in Tripoli back in 2011. Now, the stepped up ISIS attacks threaten to derail the formation of a unitary governing body.

“In December, representatives of Libya’s two rival powers signed a United Nations-brokered power-sharing pact that called for the formation of a national unity government by mid-January,” WSJ notes, adding that the violence could “undermine the financial viability of a peace agreement by destroying the country’s main source of revenue.”

“I urge the swift formation of a national unity government and the establishment of a unified force structure capable of bringing peace to this country and protecting its natural resources,” Mustafa Sanallah, chairman of National Oil Co., said, in a statement posted on the company’s website on Wednesday.

Now that Russia has begun to dismantle Islamic State’s oil operation in Syria and now that the link with the Turks has been revealed, it might very well be that ISIS is turning to Libya as an alternative source of financing. Taking control of the country’s oil crescent would be a good start.

Will the country’s rival governments unite in time to stop the assault? Will Jadhran resort to some manner of negotiated settlement with ISIS if it means retaining his influence over Libya’s oil riches? How will ISIS get its captured crude to market without a cross-border state sponsor?

All good questions that will be answered soon enough. For now, we close with one final quote from Jadhran’s spokesperson:

“Pray for us.”

* * *

“Miss me yet?”

North Korea Confirms It Conducted “Successful Hydrogen Bomb Test” As “Act Of Self-Defense” Against US

North Korea has confirmed that it has “successfully tested a hydrogen bomb.” The test was “an act of self-defense” against threats like the US.

This is the 3rd test during Obama’s administration…

As we detailed earlier…

A 5.1-magnitude earthquake detected near North Korea’s nuclear test site appears to have been artificial, according to South Korea’s meteorological service, raising the prospect the isolated regime tested a nuclear device. As Bloomberg reports, the “earthquake” follows North Korea’s threat in September that it is ready to use atomic weapons against the U.S. at any time and that its main nuclear facility was fully operational. The Pentagon is reportedly “looking into” the quake reports.

Coincidence?

As AP reports,

South Korean officials detected an “artificial earthquake” near North Korea’s main nuclear test site Wednesday, a strong indication that nuclear-armed Pyongyang had conducted its fourth atomic test. North Korea said it planned an “important announcement” later Wednesday.

A confirmed test would mark another big step toward Pyongyang’s goal of buildinga warhead that can be mounted on a missile capable of reaching the U.S. mainland.