Gold: $1,211.10 up $3.60 (comex closing time)

Silver 15.37 up 4 cents

In the access market 5:15 pm

Gold $1208.50

silver: $15.29

At the gold comex today, we had a poor delivery day, registering 43 notices for 4,300 ounces. Silver saw 3 notices for 15,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 207.36 tonnes for a loss of 96 tonnes over that period.

In silver, the open interest fell by 1843 contracts down to 166,645. In ounces, the OI is still represented by .834 billion oz or 119% of annual global silver production (ex Russia ex China).

In silver we had 3 notices served upon for 15,000 oz.

In gold, the total comex gold OI rose by 4,247 contracts to 428,912 contracts despite the fact that the price of gold was down $30.60 with yesterday’s trading.

We had no change in gold inventory at the GLD, / thus the inventory rests tonight at 710.95 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,/we had another change in inventory and this time a huge withdrawal of 1.237 million oz/ and thus the Inventory rests at 310.952 million oz.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fell by 1843 contracts down to 166,645 as the price of silver was down 45 cents with yesterday’s trading. The total OI for gold rose by 4,247 contracts to 428,912 contracts despite the fact that gold fell by $30.60 in price from yesterday’s level.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

3. ASIAN AFFAIRS

i) Late TUESDAY night/ WEDNESDAY morning: Shanghai closed up only after a huge government intervention in the last hour / Hang Sang closed down by 197.51 points or 1.03% . The Nikkei was closed down 218.07 or 1.36%. Australia’s all ordinaires was down 0.57%. Chinese yuan (ONSHORE) closed 6.5260 on a bigger than usual devaluation by POBC and yet they still desire further devaluation throughout this year. Oil gained to 29.74 dollars per barrel for WTI and 33.14 for Brent. Stocks in Europe so far deeply in the green . Offshore yuan trades yuan to the dollar vs 6.5298 for onshore yuan/

Japanese trading TUESDAY night: the Nikkei falls 218.07 or 1.36% finally reacting to news of a drop in GDP by 1.8% year over year. China saw their exports tumbling… which causes fear in Japan of continual yuan devaluations.

Last night: China weakens the yuan again

ii)On top of the problems in Syria, this will go over good:

China is moving missiles into the Spratly islands

ii) Massive explosion in Ankara and this might be the ammunition that Erdogan needs to infiltrate Syria and bomb the Syrian Kurds:

iii) S and P downgrades Saudi Arabia for the second time in 4 months as it also downgrades Oman and Bahrain:

GLOBAL AFFAIRS

i)Canadians are within 200 dollars per month on not paying their bills

(zero hedge)

ii) Huge disparity of home prices in Canada’s 3 major cities:

a) Vancouver..hot price

b) Toronto..semi hot

c) Calgary: prices plummeting

iii) After receiving 1 billion dollars in October, Bombardier is to let go of 7,000 workers

(zero hedge)

iii)The Central Bank of Mexico crushed shorts by raising overnight rate by 50 basis points as the Peso soars from 19.00 to 18.00 to the dollar.

i)Oil tumbles below 30 dollars as Iran refuses the Doha proposal and wants to increase production. Goldman Sachs warns that the freeze in production will not help at all (zero hedge)

ii)The one area that has been quite good for the past year has been the refining sector due to the good crack spreads. (the cracking of oil to produce gasoline, jet fuel etc). Now increase of supply from China et al is now causing crack spreads to fall:

( Michael McDonald/Oil Price.com)

iii) what an absolute joke: WTI rallies as Iran supports the freeze of everyone except themselves:

PHYSICAL STORIES

i)We have for quite a while provided you with our thoughts that it is the Chinese that are whacking the paper price of gold and silver. Since the bankers are in full knowledge of this, they support the Chinese by also providing the necessary non backed paper gold/silver (for them) driving their prices downward while at the same time China picks up the physical metal. I also believe that the Chinese have lent their official silver to the uSA in order that they could carry on in their suppression schemes.

iii) From award winning author William Engdahl as he discusses intrigue on the Freeport McMoRan property in Indonesia:

(courtesy Steve St Angelo/SRSRocco report)

v)A very important commentary tonight from Bill Holter on the threats of us becoming a cashless society and its implications:

i) The USA TIC report was released showing a monthly outflow of 41 billion USA of treasuries stored at the Fed (NY) and this is tracking quite nicely the total outflow of USA dollars from China (at roughly 100 billion per month)

ii)The Fed is not going to like this: core inflation rose faster than expected. If you include food costs, that inflation is surely heating up:

vi) the beige book confirms the confusion at the fed:

( zero hedge)

vii)And the above was confirmed by the mouthpiece of the Fed, Jon Hilsenrath:

Let us head over to the comex:

The total gold comex open interest rose to 428,912 for a gain of 4,247 contracts despite the fact that the price of gold was down $30.60 in price with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. Today, both scenarios were in order. In February the OI fell by 142 contracts down to 574. We had 0 notices filed on yesterday, so we lost 142 contracts or an additional 14,200 oz will not stand for delivery as they were cash settled.The next non active delivery month of March saw its OI rose by 65 contracts up to 2024. After March, the active delivery month of April saw it’s OI rose by 1,768 contracts up to 302,120. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 174,617 which is poor but includes the access trading for 4 days. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was enormous at 362,639 contracts. The comex is in backwardation until April.

Feb contract month:

INITIAL standings for FEBRUARY

Feb 17/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 26,003.128 oz

Scotia |

| Deposits to the Dealer Inventory in oz | 4000.000 pz

Brinks???? |

| Deposits to the Customer Inventory, in oz | 122,453.128 oz

HSBC,Scotia |

| No of oz served (contracts) today | 43 contracts (4300 oz) |

| No of oz to be served (notices) | 531 contracts (53,100 oz ) |

| Total monthly oz gold served (contracts) so far this month | 2005 contracts (200,500 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 529,775.8 oz |

we had 0 adjustments.

FEBRUARY INITIAL standings/

feb 17/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 577,689.001 oz

Brinks CNT,Delaware,Scotia,HSBC |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 321,387,590 (JPM) |

| No of oz served today (contracts) | 3 contracts 15,000 oz |

| No of oz to be served (notices) | 1 contract (5,000 oz) |

| Total monthly oz silver served (contracts) | 165 contracts (825,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 10,252,791.3 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit;nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposits:

i) Into JPM: 321,387.590 oz

total customer deposits: 321,387.590 oz

total withdrawals from customer account 577.689/001 oz

we had 0 adjustments:

And now the Gold inventory at the GLD:

fEB 17/no change in gold inventory at the GLD/Inventory rests at 710.95 tonnes

Feb 16.a huge withdrawal of 5.06 tonnes from the GLD/the loss was probably a paper loss/inventory at 710.95 tonnes

fEB 12/ a huge deposit of 11.98 tonnes/inventory rests at 716.01 tonnes. With gold in severe backwardation in London, I really believe that the gold added was paper gold and not real pbhysical/

Feb 11/no change in inventory/inventory rests at 702.03 tonnes

Feb 10/ a withdrawal of 1.49 tonnes of gold from the GLD/Inventory rests at 702.03 tonnes

Feb 9./a huge addition of 5.06 tonnes of gold into the GLD/Inventory rests at 703.52 tonnes/ (no doubt that this addition is paper gold/not physical/

Feb 8/no change in inventory/inventory rests at 698.46 tonnes

FEB 5/another massive 4.84 tonnes added to the GLD/Inventory rests at 698.46 tonnes/this is a paper gold addition and this vehicle is nothing but a fraud. There is no metal behind it.

FEB 4/another massive 8.03 tonnes added to the GLD/Inventory rests at 693.62 tonnes.

in a little over a week we have had 29.43 tonnes added to the GLD. Judging from the backwardation of gold in London, it would be impossible to bring that quantity into the GLD. No doubt that the entry is a “paper” gold deposit.

Feb 3.2016: a massive 4.16 tonnes deposit of gold at the GLD/Inventory rests at 685.59 tonnes.. In a little over a week, we have had 21.42 tonnes enter the GLD. Without a doubt that this entry is paper gold. It would be impossible to find 21 tonnes of physical gold and load the GLD.

Feb 2.2016: no changes in inventory at the GLD/inventory rests at 681.43 tonnes

Feb 1/a massive deposit of 12.20 tonnes of gold inventory/Inventory rests at 681.43

Feb 17.2016: inventory rests at 710.95 tonnes

end

And now your overnight trading in gold, WEDNESDAY MORNING and also physical stories that may interest you:

Gold Stabilises Above $1,200; Asia Markets Run Out Of Steam

Global economic turmoil continues to rumble on as major economies seek to come to grips with a changing monetary environment, sagging growth, low inflation, pockets of deflation and uncertainty over the future of Europe post Brexit. Japanese shares sold off after their gains on Monday, falling 1.8% in today’s trading sessions. European shares rising 1.6% this morning on the back of an expectation that volatility in the markets may begin to stabilise, feels more like a dead cat bounce to be honest.

In a wonderful example of poor timing, China is ruffling global security circles by placing advanced ground-to-air missiles in the South China Sea in what many see as an antagonistic move. Russians and Saudis have decided to freeze production of oil, which smacks of desperation as oil output rates are at recent highs and economic demand is lagging so it is likely that such a move will actually suppress prices further.

One statistic we like to follow and we think is indicative of the global post debt binge slowdown is the Chinese Container Freight Export, which is showing a 28% drop since February 2015. For a large industrialised nation like China that is a akin to an economic cardiac arrest. The good news is that the index seems to be stabilising, albeit slowly.

I am the CEO of GoldCore. We help investors buy and store gold and silver easily and cost effectively. We work with clients of every variety from wealth family offices to everyday people. We provide the very best market data and client service and we care deeply for our clients interests.

We have for quite a while provided you with our thoughts that it is the Chinese that are whacking the paper price of gold and silver. Since the bankers are in full knowledge of this, they support the Chinese by also providing the necessary non backed paper gold/silver (for them) driving their prices downward while at the same time China picks up the physical metal. I also believe that the Chinese have lent their official silver to the uSA in order that they could carry on in their suppression schemes.

China is likely capping Comex gold to facilitate metal’s eastward flow

Submitted by cpowell on Wed, 2016-02-17 01:34. Section: Daily Dispatches

8:43p ET Tuesday, February 16, 2016

Dear Friend of GATA and Gold:

In analysis posted tonight at GATA Chairman Bill Murphy’s LeMetropoleCafe.com, Toronto securities broker Mike Ballanger elaborates on a point made by a number of GATA’s friends since the big gold smash of April 2013 — friends like Koos Jansen, Jim Rickards, and Andrew Maguire, among others. That is, China almost certainly is very active keeping gold futures prices down so that it might acquire more real metal as it reduces the U.S. dollar component of its foreign-exchange reserves.

Your secretary/treasurer put it this way in November 2013:

http://www.gata.org/node/13256

“China is the gold market as well as the U.S. government bond market and any market China wants to be — China’s foreign exchange surplus is that huge. If China had not been at least complicit in the April smashdown of gold, it would not have occurred — China would have bought the dip at a much higher level. So much for the ‘Chinese put’ many gold investors thought they enjoyed.

“China and the United States have great leverage over the other. Each knows what the other wants.

“The United States wants to devalue the dollar gradually and gracefully to reduce its debt burden and improve its trade balance.

“Understanding the U.S. objective of gradual dollar devaluation, China wants to hedge its insane dollar exposure and is doing so by acquiring gold and other hard assets around the world.

“Each side could blow up the other at any time — China by dumping U.S. debt instruments and buying gold abruptly, the United States by devaluing abruptly.

“So the two governments probably are talking to each other in detail every day and acting cooperatively in the markets in pursuit of their objectives, which really are not so contradictory.

“The advice often given by market analysts, some of whom just shrug off the unfairness of gold price suppression and market rigging — advice to purchase gold steadily at the market rigging’s ‘discount’ and just wait for the great international currency reset (and pray that you have time to wait) — is probably being followed most of all by China itself, which is as well situated as any other nation to push gold futures prices down to facilitate its acquisition of real metal.”

Last October the Austrian central banker Peter Mooslechner more or less confirmed all this, if inadvertently, in an interview with Kitco News on the sidelines of the LBMA conference in Vienna, volunteering that Asian central banks were surreptitiously intervening in the gold market as the price declined:

http://www.gata.org/node/15897

Pressed by the German financial journalist Lars Schall about his remarks to Kitco News, Mooslechner disappeared and the Austrian central bank clammed up, confident that no mainstream financial news organization would make anything of Mooslechner’s admission.

An excerpt from Ballanger’s elaboration tonight is appended.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@gata.org

The Ballanger commentary:

Gold and Gold Miners Analysis for February 16, 2016

By Michael Ballanger

www.LeMetropoleCafe.com

Tuesday, February 16, 2016

Last night I was sitting in my reading room (which substitutes as a “libation room” most evenings) and I was trying to go over the “coincidence” of a strong gold market during the Chinese Lunar New Year holiday and sudden and dramatic weakness Sunday evening with the Chinese traders back at work.

I have alluded to that famous quote by Mark Twain mentioned here a few weeks back that goes like this: “It ain’t what you don’t know that gets you into trouble; it’s what you know for sure that just ain’t so. …”

I mention this because one of the most classic cases of recency bias is the natural assumption that the Chinese are constant, perpetual buyers of gold day in, day out, week after week, and never sell. We all know “for sure” that it could not have been Chinese selling that has been suppressing the gold market — but what if that “just ain’t so”? What if the Chinese are using the phony, synthetic paper market called the Crimex to set the price for physical purchases that never get seen until months later?

In other words, the Chinese central planning traders are capping the Crimex price to secure physical gold and silver prices advantageous to their long-term national objective.

Dumping trillions of ever-depreciating U.S. dollars for price-capped physical gold sounds like a brilliant idea and it really is nothing more than disguised arbitrage, masterfully executed and wonderfully discreet. They have even perfected the “false flag” concept seen in military campaigns throughout history by making it appear that it is other central bank entities that are perpetrating this heinous financial folly.

Dreaming, am I?

Well, when you drill down into it, there are a great many nuances that point to the Red Menace as the master manipulator, such as the 3 a.m. ET smashes that have always occurred in the thin trading sessions of the European opening, but it was last Sunday evening (morning in China) when the gold market was immediately marked down by as much as $28 an ounce on the Asian opening, the first day back at work after a week of fun and frivolity.

Don’t forget that the average Chinese citizen has loved these low prices, as has the People’s Bank of China for most of last six months. Since the yuan has been declining against the U.S. dollar lately, the double whammy of weak yuan and strong dollar exchange rate for gold has created some nice profits for the Chinese gold buyer.

In the final analysis, it really doesn’t matter that much who the buyers are and who the sellers are, but if my speculative thinking is on the money, it is even more bullish for gold because the level of foreign exchange reserves held by the People’s Bank of China has been drastically reduced by massive stock market and currency interventions of late, and since this is the funding source for People’s Bank of China gold accumulation, once the central bank’s vault is empty of U.S. dollars and full of gold, the need for suppression vaporizes and that phony, synthetic paper market is allowed to levitate. …

end

Steve St Angelo of SRSRocco report gives us a dandy report on gold demand from the USA and gold supply. It certainly gives you a good picture of what the USA is doing as they need to supply gold to China and to do that, they must import much of that gold.

(courtesy Steve St Angelo/SRSRocco report)

2012-2015 U.S. GOLD SUPPLY DEFICIT: One Hell Of A Lot Of Gold

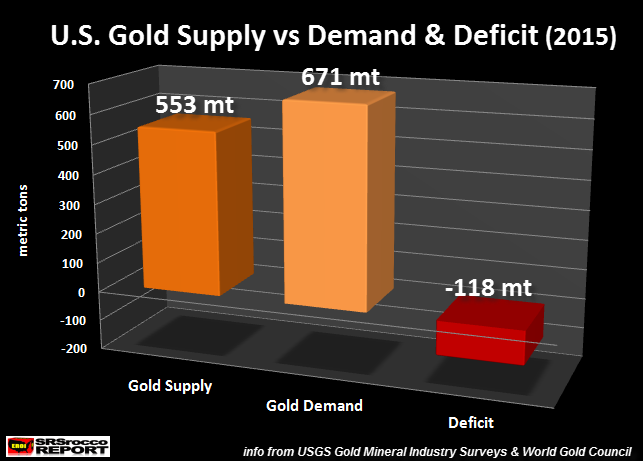

According to figures put out by the USGS, World Gold Council and Thomson Reuters GFMS, the U.S. had a total of 553 mt of gold supply compared to 671 mt of total demand… leaving a 118 mt shortfall for 2015 :

Here is how I arrived at the figures shown in the chart above:

U.S. Gold Supply & Demand Figures 2015

Domestic Mine Supply = 213 mt

Gold Imports = 265 mt

Estimated Scrap = 75 mt

Total Supply = 553 mt

Gold Exports = 478 mt

Domestic Consumption = 193 mt

Total Demand = 671 mt

Total Deficit = 118 mt

American gold consumption increased from 179 mt in 2014 to 193 mt in 2015. The majority of the increase was due to higher Gold Bar & Coin investment. According to the World Gold Council Full Year 2015 Report, Americans purchased 132 mt of Gold Jewelry and 47 mt of Bar & Coin in 2014 versus 120 mt of Gold Jewelry and 73 mt of Bar & Coin investment in 2015.

What was interesting was the huge spike of U.S. Gold Bar & Coin demand during the third quarter of 2015. This was at the same time when the retail silver market suffered extensive shortages with upwards of two month wait times on certain products. Americans purchased 33 mt of Gold Bar & Coin in Q3 2015, 45% of the total for the year.

While some precious metal investors do not trust any of the data that comes from the World Gold Council or Thomson Reuters GFMS, I believe the figures for the U.S. are pretty accurate. If we look at Gold Eagle sales from July-Sept 2015, they totaled 397,000 oz while Gold Buffalo sales were 74,000 oz. Thus, total sales of these two official gold coins equaled 471,000 oz or 14.6 metric tons. The remaining 18.4 mt of Gold & Bar & Coin for Q3 2015 was in from other official coins and bars (such as Gold Maples) and private bars and rounds.

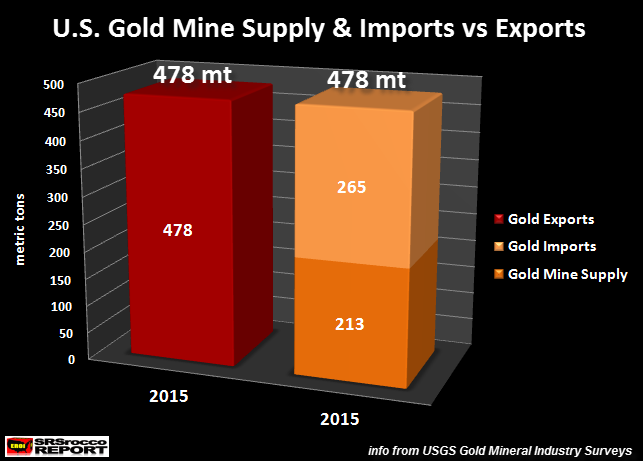

U.S. Exports Every Bit Of Its Gold Supply In 2015

Now, if we were to exclude U.S. gold scrap supply and domestic consumption, this would be the result:

U.S. domestic gold mine supply of 213 mt and imports of 265 mt (478 mt) is the same total of gold exports at 478 mt. Basically, the United States exported every bit of its mine supply and imports abroad.

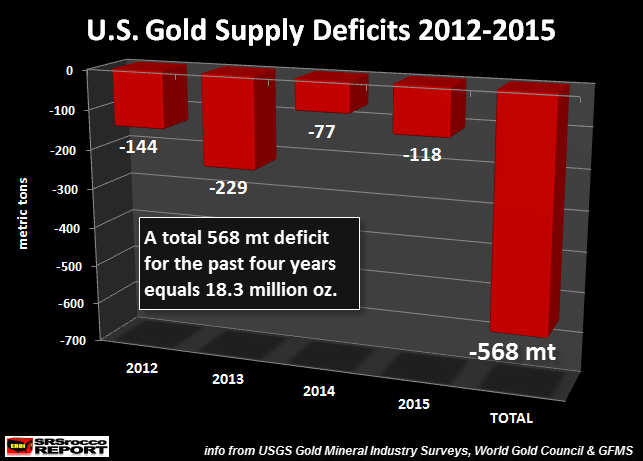

U.S. Four-Year Gold Supply Deficit Equals One Hell Of A Lot Of Gold

If we add up total gold supply and subtract total demand since 2012, the United States suffered one hell of a deficit:

As we can see from the chart above, the U.S. experienced annual gold supply deficits since 2012. In 2011, the U.S. actually enjoyed a 215 mt surplus. What was interesting is that during the years when the price of gold surged (2009-2011), the U.S. reported more annual surplus. However, since the price of gold peaked (2011), it has been one annual deficit after another. I believe this is due to a significant “Trend Change” by the Eastern countries to acquire as much gold as they can get.

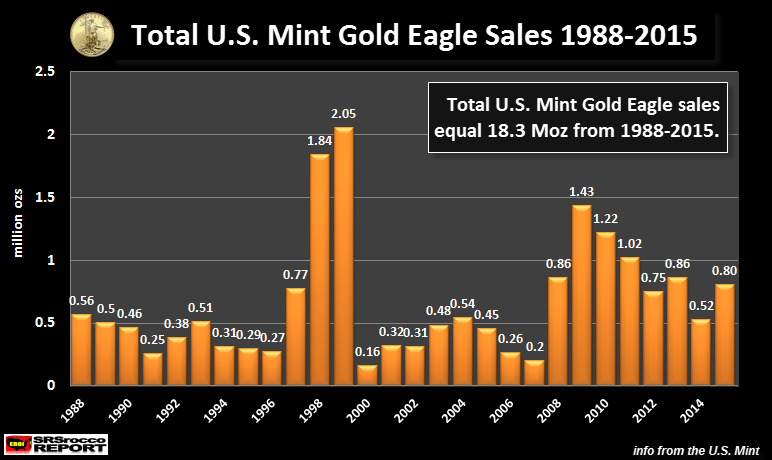

If we add up the annual gold supply deficits from 2012 to 2015, it totals 568 mt, or a massive 18.3 million oz (Moz). To give you an idea of how much gold that is, it equals all the Gold Eagles sold by the U.S. Mint from 1988-2015, 18.3 Moz:

So, in just the past four years, the total U.S. gold supply deficit equals all the U.S. Gold Eagle sales for the past 28 years. That’s a one hell of a lot of gold. It amounts to a $22 billion gold supply deficit, based on a $1,200 current market price multiplied by 18.3 Moz.

I will be writing more articles on the U.S. and Global gold supply-demand forces. However, the basic takeaway is this… physical gold continues to be drained from the WEST and shipped to the EAST. As we can see from the data in this article, the U.S. continues to export all of its domestic mine supply and imports abroad, while using its scrap supply for consumption purposes.

Which means, the present American Gold Ownership Strategy is to EXPORT IT ALL, JUST LET US KEEP THE SCRAPS.

-END-

Should you believe “the Squid” on selling gold? Answer: do not go anywhere near these crooks!

(courtesy Jim Quinn/the Burning Platform)

Should You Believe The Vampire Squid On Gold?

Submitted by Tyler Durden on 02/17/2016 15:15 -0500

Submitted by Jim Quinn via The Burning Platform blog,

I find it fascinating the mainstream corporate media and Wall Street shysters spend SO MUCH time talking down gold and spending an inordinate amount of electronic ink trying to convince the masses that only nutjobs would buy it.I believe less than 2% of people have gold in their investment portfolio, so why the endless articles bashing it?

The suppression of gold prices through the paper market since 2011 by the Fed and their Wall Street bank co-conspirators has thus far been successful, but it is fraying at the edges as China continues to accumulate physical gold and pushing the ponzi scheme towards its inevitable conclusion. Soaring gold prices tells the masses central bankers are a fraud, that’s why they are desperate to keep the price capped.

With zero and negative interest rates throughout the world, gold should be skyrocketing. It is showing signs of calling the central banker bluff. Jesse’s comments below should be heeded. The stock market dead cat bounce and the holiday manipulation of gold down $30 will fail.

Gold Daily and Silver Weekly Charts – Goldman Says Have No Fear and Buy Our Paper

Goldman analyst Jeffrey Currie came out this morning with a ‘sell gold’ recommendation for Ma and Pa Muppet.

I was fortunate enough to hear his explanation for this in his own words on Bloomberg TV, which had touted his gold call about every fifteen minutes all day.

The net summary of Mr. Currie’s forecast is that Goldman’s economists think that there ought to be no fear in the financial paper markets, since there is an historically low chance of a recession, less than fifteen percent, and he sees no real possibility of negative interest rates.

Therefore, since in his mind gold is strictly a ‘fear trade’ and since Goldman says to have no fear one ought to therefore sell gold.

Do with that what you will.

As for my own forecasts, I see the world economy fraying substantially throughout the year, with the domestic risk of inflation unusually high relatively speaking, and the geopolitical risks to be also rather elevated.

But at the end of the day, gold is now trading as a currency, and Uncle Buck was on a no fear tear this morning. And no matter what Mr. Currie may be saying, I am watching what Asia is doing.

So far so good on the charts as noted below.

It may be a bit of time before one might determine whether the lip of the cup is straight horizontal or slanted IF the chart continues to develop.

There was very little action at The Bucket Shop on the PM delivery front, and some silver was shoved around the plate and taken out of the warehouses. Not much happened in other words. What a surprise. The Bucket Shop is a monumental mausoleum for what has gone wrong in the US markets.

* * *

If there is a lesson from the Big Short, do the opposite of what Goldman says to do.

Indonesia, China, Gold and ISIS

At first glance it’s a strange title for an article. What does Indonesia, China, Gold and the Islamic State or ISIS have to do with one another? That might begin to become clearer when we look more closely at the foreign economic policy actions of the Indonesian government of President Joko Widodo.

At first glance it’s a strange title for an article. What does Indonesia, China, Gold and the Islamic State or ISIS have to do with one another? That might begin to become clearer when we look more closely at the foreign economic policy actions of the Indonesian government of President Joko Widodo.

On January 14, an Indonesian terrorist group connected with ISIS in Syria claimed responsibility for a series of suicide bombings and terror attacks in Jakarta, killing two civilians and ending in the death by police of five terrorists. The attackers apparently were not the most professional. The first was a suicide bomber who entered a Starbucks café, detonated the device killing only himself, along perhaps with a few thousand calories worth of Starbucks muffins and cups of Latte. The terror attacks were the first in Indonesia since 2009.

Now, if we take the basic fact that all major international terrorist organizations must have at least one or more state sponsors to remain in existence, and that the blood from ISIS atrocities lies on the hands of the CIA, the Turkish government of Recep Erdogan, and on Saudi King Salman and his princeling Salman, with some drops finding their way to the hands of Israel’s Netanyahu, we must ask what it is that suddenly, after a calm of almost seven years, makes Indonesia a terror target?

China and Jokowi

Joko “Jokowi” Widodo, Indonesia’s president, who was voted in October 2014 for his appeal as a clean, new face in the traditionally corrupt Indonesian politics, has followed a mixed course, seemingly trying to be friends with all, at least in foreign relations.

To please Washington he agreed to the disastrous Trans-Pacific Partnership trade swindle. He backed Obama’s agenda on the fraudulent Global Warming. But he also has taken very concrete steps to improve relations with China, and here is where it becomes interesting.

Since a CIA-backed military coup in the late 1960’s, Indonesia has had a mixed relationship with Beijing. The CIA backed a military coup in 1967 to oust the nationalist leader of the revolution that overthrew Dutch rule, Sukarno, placing in power General Suharto, whose army launched mass slaughters of hundreds of thousands of pro-Chinese communists. With the US-backed coup regime of Suharto, diplomatic ties to Beijing were cut, a state of affairs lasting until 1990. The Suharto coup had a lot to do with controlling Indonesia’s oil and locking her into America’s Asian sphere of influence.

Today Indonesia, under the populist Jokowi as he is called, is concerned with developing the nation economically. That, in today’s Asia, inevitably means working with China. And this is precisely what Jokowi has been also doing.

Financing Major Infrastructure

Over the past decade, Indonesia trade with China has assumed growing importance. In November, 2014, newly elected President Joko Widodo paid his first official overseas visit. It was to China where he met with China President Xi Jinping and Prime Minister Li Keqiang. Then in April 2015, President Xi Jinping met in Bandung with Jokowi at the commemoration of the 60th anniversary of the Asian-African Conference.

By 2010, China had overtaken the US as Indonesia’s second-largest export destination after Japan. China has also become Indonesia’s most important source of imports. Now, under Jokowi, Indonesia has recently turned to China to finance major domestic infrastructure projects to link the most important of the country’s thousands of islands.

Last October, Jokowi’s government announced that it had decided to accept China’s revised offer to construct a major high-speed rail linking Jakarta to Indonesia’s third-largest city, Bandung. China beat a rival Japanese bid for the project, to cost an estimated $5-6 billion. The railway will be completed by 2018.

The Jakarta-Bandung rail project is a part of President Xi’s economic diversification strategy of focusing high-tech China companies on developing export markets and also of developing the needed infrastructure along China’s One Belt, One Road routes across Asia and Eurasia. Good relations with Indonesia is also important for China in developing stronger ties with the ASEAN countries of southeast Asia, where Washington is hard at work trying to stir friction against China’s presence in the islands of the South China Sea.

For the Jokowi government it’s clear that they see China as the essential partner in helping meet the goal of a vast infrastructure investment plan. Japan is de facto bankrupt.

The Jakarta government needs to invest an estimated $740 billion in the coming five years for infrastructure development projects to achieve the targeted 7%-a-year growth in its economy. The government expects 5.8% growth this year, lower than the 6.3% target. Jokowi has also requested Chinese president Xi Jinping increase involvement of Chinese state companies in developing Indonesia’s infrastructure. He also proposed a bigger role for Indonesia in the China-led Asian Infrastructure Investment Bank (AIIB).

The golden hills of Papua

The Jokowi government needs to get Chinese financing, a lot of it to reach its significant infrastructure targets, seen as bringing the huge economic potential of the country of some 255 million. Now things get interesting. To collateralize infrastructure borrowing from China, Jokowi’s government is looking more closely at a project high in the mountains of Papua. There, inside Indonesia, lies the world’s largest gold mine. It also happens to have the world’s largest reserves of copper. One beautiful collateral to use to borrow the estimated $85 billion needed from China to get the further infrastructure moving. Only problem is that the gold is controlled by an American multinational, not Indonesia.

The Papua gold mine known as Grasberg, is situated some 14,000 feet high in the Sudiman Mountain Range, in the Indonesian part of the New Guinea island. It is not only the world’s largest gold mine. It is also the world’s most profitable gold mine. Since 1989 the mine has been mined by a very well-connected corporation now based in Phoenix, Arizona called Freeport McMoRan.

Freeport McMoRan’s Grasberg gold mine is the world’s largest and the most profitable gold mine

Freeport McMoRan, a firm that in the past has had Rockefellers, Whitneys Stillmans, Goodrichs and Lovetts on its board, is one of the most influential of global US corporations. It got control of the mining rights for Grasberg in the usual way for such giant US mining multinationals—by hook and crook, fraud and bribery. A 2005 New York Times investigation revealed documents showing that from 1998 through 2004, Freeport gave Indonesian military and police generals, colonels, majors and captains, and military units, nearly $20 million to insure “security” at the huge Grasberg mine. The military and police were used to put down protests and riots by locals and workers protesting the unchecked environmental toxins resulting from Grasberg. To get mining rights at the start Freeport chairman James R. Moffett reportedly made Indonesian President Suharto bribes that made him rich. Freeport has become one of the largest sources of revenue for the government.

Freeport has a brutal record at Grasberg. On October 17, 2011 the company halted operations in Papua amid a strike that led to a deteriorating security situation and intensified calls for Papuan independence. Seventy percent of Grasberg workers joined the strike, appealing for higher pay, blocking roads, clashing with police and cutting the pipeline in several places.

Now, the new Jokowi government has looked more closely at the terms of Freeport McMoRan’s lease on Grasberg, a lease expiring in 2021. The government is demanding that Freeport give it a share double as large as the 10% it holds today, up to 20%, to be finally raised to 30% in 2019. As well it demands more revenue from the mining proceeds and wants the mining company to comply with a new Mining Law, which limits concession areas for miners, in addition to the greater government ownership. The company valued the Grasberg asset at a total of $16.2 billion. That is amusing to say the least. The company admits in another filing that it will invest $18 billion to turn the Grasberg complex from open pit to underground mining in late 2017. Invest $18 billion in a property only worth $16.2 billion?

According to Indonesian sources, geological estimates are that Grasberg holds a total gold of possible 16,000 tons. That would be fully half of all world official central bank gold holdings in that one mine. At today’s price of gold at $1,107 a troy ounce, that translates into a gold mountain worth of some $516,000,000,000, or more than half a trillion dollars. That’s money some would say worth killing for.

Now this all is hardly proof that Freeport McMoRan went and hired some “ISIS” suicide bombers to wreak chaos and death in Indonesia’s Jakarta capital as a warning. It is worth noting, nonetheless, that the very same day Freeport published its offer for the settlement of the 2021 Grasberg mine lease renewal, bombs went off in Jakarta.

In my humble opinion, were I Jokowi, I would look for links between Grasberg and the Jakarta bombings. Or better yet, find another reason to not renew the Freeport lease in 2021 on grounds of massive bribery, illegal environmental degradation and such that is already known and proven. That 16,000 tons of gold would collateralize the lion’s share of Indonesia’s planned infrastructure. And with China rapidly becoming the world gold trading hub, the Beijing-Jakarta economic friendship could have a golden future.

F. William Engdahl is strategic risk consultant and lecturer, he holds a degree in politics from Princeton University and is a best-selling author on oil and geopolitics, exclusively for the online magazine “New Eastern Outlook”.

http://journal-neo.org/2016/02/14/indonesia-china-gold-and-isis/

end

Such crookedness!!

(courtesy Nanex/zero hedge)

The Gold Spoofer Is Back

Overnight action saw gold jerked lower as Europe opened and Asia closed. Thanks to Nanex, we now see ‘how’ this occurred as the “gold spoofer” has returned. Once the spoofer disappeared, gold has rallied back up to the overnight highs… rigged?

75 gold futures contracts used to “spoof” prices lower…

And once the spoofer left the building…

It seems $1200 is the line in the sand once again.

And now your overnight TUESDAY NIGHT/ WEDNESDAY morning trades in bourses, currencies and interest rate from Asia and Europe:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.5260 / Shanghai bourse IN THE GREEN: / HANG SANG CLOSED DOWN 197.51 POINTS OR 1.03%

2 Nikkei closed DOWN 218.07 OR 1.36

3. Europe stocks all in the GREEN /USA dollar index DOWN to 96.83/Euro UP to 1.1144

3b Japan 10 year bond yield: RISES TO +.066 !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.14

3c Nikkei now well below 18,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 29.61 and Brent: 33.11

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to 0.252% German bunds in negative yields from 8 years out

Greece sees its 2 year rate fall to 12.88%/:

3j Greek 10 year bond yield FALL to : 10.93% (yield curve deeply inverted)

3k Gold at $1206.60/silver $15.29 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble up 1 rouble and 5/100 in roubles/dollar) 76.92

3m oil into the 29 dollar handle for WTI and 33 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9900 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1037 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/arrests 10 traders for Euribor manipulation

3r the 8 year German bund now in negative territory with the 10 year rises to + .252%/German 8 year rate negative%!!!

3s The Greece ELA at 71.5 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.78% early this morning. Thirty year rate at 2.65% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Storm Above 1900, Europe Jumps Despite Gloomy Asian Session

It has been a morning session of two halves.

In Asia, the mood was somber, and stocks fell with the Shanghai Composite (+1.1%) outperforming on another late session binge-fest by the National Team, and the Nikkei 225 (-1.4%), Hang Seng -1%, Kospi -0.2%, ASX -0.6%, Sensex -0.4% and the South Korean Won all down following news of the biggest Chinese Yuan devaluation in five weeks.

The European session, on the other hand was a different matter and after the USDJPY slid as low as 113.35 at the European open, it then proceeded to soar 100 pips and push European stocks (Stoxx 600 +1.7%) and US equity futures up with it, with the ES trading above 1900 as of this posting, adding to the best 2-day rally in the S&P in five months.

Shares in Europe also rose as companies including Credit Agricole SA and Schneider Electric SE reported better-than-estimated results.

Among the key corporate news, Glencore Plc pushed a gauge of commodity stocks higher, advancing 8.6 percent after the Swiss trader said it won new loan commitments from banks to replace an existing $8.45 billion revolving credit facility. Its bonds also gained. Total SA dropped 1.7 percent after a shareholder sold a stake at a discount. ABN Amro Group NV bucked the banking industry trend, sliding 2.2 percent after its quarterly profit missed analysts’ projections as regulatory costs rose.

Some observations were optimistic, such as this one by Justin Urquhart Stewart, co-founder of Seven Investment Management in London: “I’d love to think this is the start of a lasting rebound but it’s too early to tell. Any gains have been pretty fragile and short-lived lately, even though earnings haven’t been all that bad and economic figures have been quite supportive.”

Others less so, such as this UBS technical analyst note: “We see Europe starting our suggested multi-week corrective/volatile rebound into later 1Q/early 2Q before resuming its underlying bear trend into deeper summer on the back of the recent break down in small and mid-caps. After the undershooting in banks, we expect a bounce in the Euro Stoxx 50 to remain capped at 3050 to best case 3200. On the sector front, a bounce should be led by autos, chemicals, industry, energy and miners, whereas a rebound in financials should sooner or later lose momentum.”

But ultimately it all remains about oil, which after sliding to $29 yesterday after the disappointing summit between Russia and Saudi Arabia, has rebounded on hope that today’s follow up meeting between Iran, Iraq and Venezuela may provide something actionable. It won’t, as the following tweet from a WSJ correspondent indicates, and instead the stage for the fingerpoint is now set.

Focusing on regional markets, we start in Asia where stocks shrugged off Wall St. gains to trade negative with energy losses weighing bourses. Nikkei 225 (-1.4%) underperformed on JPY strength, while the biggest decline in machine orders in over a year also added to the gloom. ASX 200 (-0.6%) saw energy names heavily pressured after crude retreated back below the USD 30/bbl level, while Woodside Petroleum shares also dragged the sector lower following a 99% decline in profits. Elsewhere, the Shanghai Comp (+1.1%) fluctuated between gains and losses after an early upbeat tone following reports of increased funds for infrastructure spending and officials also discussing a reduction in bad loan provision ratios, was counter-balanced by a somewhat reserved PBoC liquidity operation. Finally, 10yr JGBs saw spillover selling from T-Notes where large corporate issuances and firm US stock momentum weighed on US paper while the BoJ’s presence in the market today was for a relatively modest amount. Japanese PM Abe adviser Honda says the BoJ may increase stimulus at the March meeting and that the tax hike should be delayed until 2019.

In Europe, European equities started the session off on the front-foot with a slew of earnings reports and a paring of yesterday’s losses enough to out-muscle underperformance in energy names amid the latest OPEC/Non-OPEC¬related headlines. Furthermore, financials have also been dealt a helping hand by stellar earnings from Credit Agricole (+11.1%) and elsewhere to the downside, utilities are seen softer in the wake of RWE suspending their dividend for ordinary shares. From a fixed income perspective, Bunds trade modestly higher with no real sustained direction as participants awaited supply from both the UK and Germany for much of the morning, which was technically uncovered when auctioned. Portugal spent the European morning wider to the German benchmark as has often been the case over the past few week. Elsewhere in the periphery, concerns continue to linger for Spain as to whether or not the nation would be able to obtain a definitive outcome if they were to hold a fresh round of elections.

In FX, much of the focus has been on GBP this morning, with the backdrop of the EU renegotiations added to by the UK employment report. The jobless rate was unchanged at 5.1% which caused and immediate hit on the Pound, led by Cable. Earlier in the day, we saw losses through 1.4250 limited to 1.4242, held up by some strong bids at these levels, which then formed the basis of a sharp turnaround as the rest of the numbers proved very healthy. Claims fell by a much larger than expected 14.8k and once digested, saw Cable taking out 1.4300 and pushing the GBP to session highs against the rest of its major counterparts. Elsewhere, early stock market jitters saw USD/JPY dipping below 113.50, but as sentiment eased, we saw a slow grind back to 114.00 and above, but the Asia highs ahead of 114.40 cap for now. Oil prices moving higher despite ongoing wrangling over the production freeze (Iran), and this has given CAD some relief to send the spot rate back towards 1.3800.

In commodities, energy markets traded relatively unchanged through most of the session as participants await further headlines regarding any success/breakdown in negotiations regarding a co-orindated production freeze. However, in the lead up to the beginning of the 1030GMT meeting between Qatar, Venezuela, Iraq and Iran WTI and Brent futures both saw a bid, with the former heading higher, towards the USD 30/bbl level, although with no fundamental catalyst immediately behind the move. In terms of metals markets, Gold traded higher overnight amid weakness in Asia-Pac stocks and a pull-back in the USD, however, prices have since retreated from their best levels alongside the upside seen in European equities.

* * *

Bulletin Headline Summary from RanSqawk and Bloomberg

- FX markets have seen USD/JPY and GBP/USD retrace earlier losses with both heading into US crossover seeing a bid, as participants shrug off mixed UK employment release and sentiment strengthens through the European morning

- While Asian equities failed to benefit from the positive Wall St close, European equities have traded higher this morning, benefitting from stock specific news as well as an uptick in sentiment

- Today’s highlight is the release of the FOMC Minutes, while participants will also be looking out for US housing starts, building permits, industrial production and API Crude Oil Inventories

- Treasury yields little changed as European equities and oil rally during overnight trading; Fed minutes to Jan. 26-27 meeting to be released at 2pm ET.

- The yuan posted the biggest two-day decline in more than a month as the central bank’s fixing for the currency tracked an overnight advance in the dollar and official media voiced concern that capital outflows will increase

- China’s unprecedented jump in new loans at the start of 2016 is fueling concern that excessive credit growth is piling up risks in the nation’s financial system. The increase could pressure the country’s credit rating, S&P said Tuesday

- China is stepping up support for the economy by ramping up spending and considering new measures to boost bank lending. The nation’s chief planning agency is making more money available to local governments

- The BOJ should act preemptively to change the deflationary mindset in Japan and this action could come as soon as March, said Etsuro Honda, an adviser to Prime Minister Shinzo Abe

- Wall Street firms are readying themselves for a provision of the 2010 Dodd-Frank law that takes effect in December that forces banks to keep a stake in the commercial-property loans they package into securities and sell off to investors

- Syria’s five-year war has turned into a tangled web of proxy conflicts between global and regional powers, with a growing risk that some of them could clash directly. Right now the most dangerous flashpoint is between Russia and NATO member Turkey

- Apple rejected a court order to help the Justice Department unlock an iPhone used by one of the shooters in a terrorist attack in California, accusing the U.S. government of “overreach” that will set a dangerous precedent

- $23.425b IG corporates priced yesterday (YTD volume $206b) and $350m priced yesterday (YTD volume $9.625b)

- Sovereign 10Y bond yields little changed; European stocks higher, Asian markets drop; U.S. equity-index futures higher. Crude oil, copper and gold rally

DB’s Jim Reid concludes the overnight wrap

While the rally in Europe succumbed to a bit of fatigue yesterday with the Stoxx 600 closing with -0.43% after a day of whippy price action, the US reopened after Monday’s holiday with a fairly positive tone to build on the momentum generated from the end of last week, culminating with the S&P 500 closing with a +1.65% gain. Much of the focus however was on oil markets and specifically the meeting between Saudi Arabia and Russia. The initial headlines appeared positive and saw WTI spike as high as $31.50/bbl before disappointment set in that actually there was little fundamental change from the meeting and instead realization set in that talks had moved from cuts to a freeze in production. WTI closed -1.36% on the day at $29.04/bbl.

In terms of the details, it emerged that Saudi Arabia and Russia, along with Venezuela and Qatar had agreed to freeze current production at January levels. As our Commodity strategy colleagues highlighted yesterday in their note, the Russia Oil Ministry stated that this freeze would only take effect if other producers participate, without specifying how many or which countries would be required to join the agreement. While a credible agreement to hold production flat by all OPEC members at the January level would be quite meaningful in tightening forward expectations of market balance, a lot of this would hinge on the need for the inclusion of Iran and Iraq. Talks are expected to continue in Tehran today but expectation levels are low given that Iran has publicly stated that it will restore production to pre-sanctions levels regardless of price.

A silver lining is that the talks are overall a positive step forward for sentiment in advance of the scheduled June OPEC meeting. Clearly though there is the need for negotiations to progress to achieve any sort of coordinated agreement in production cuts between OPEC and non-OPEC members however.

Glancing at our screens this morning it appears that weakness in energy names following the news yesterday is to blame for a broadly weaker start in Asia this morning. Bourses in Japan in particular have seen the greatest losses with the Nikkei currently -1.88%. Elsewhere the Hang Seng (-0.50%), Kospi (-0.27%) and ASX (-0.57%) are also in the red as we go to print, while Chinese bourses (Shanghai Comp +0.31%) have just nudged back into positive territory. Oil markets are actually about half a percent firmer while US equity index futures are unchanged.

Away from the focus on Oil yesterday there was also some data and Fedspeak for us to digest. With regards to the former first of all there was a notable downturn in this month’s German ZEW survey. The current situations index plunged 7.4pts to a below-market 52.3 (vs. 55.0 expected) which is the lowest in 12 months and clearly a reflection of the European banks, global growth and China woes which have played their part this year. The expectations survey fared little better, tumbling 9.2pts to 1.0 (vs. 0 expected). In the UK meanwhile the January CPI print was lower than expected at -0.8% mom (vs. -0.7% expected). That said the YoY rate did nudge up one-tenth to +0.3% with the core sitting at +1.2%. In the US we saw the February Empire manufacturing survey continue to remain weak this month at -16.6 (vs. -10.0) despite improving nearly 3pts from January. Meanwhile the NAHB housing market index declined 3pts to 58 which came as a slight surprise with consensus expectations having been at 60, although it still remains close to its cyclical high.

In terms of the Fedspeak, Philadelphia Fed President Harker (non-voter) provided a fairly cautious overview of the US economy. Harker opined that ‘it might prove prudent to wait until the inflation data are stronger before we undertake a second rate hike’ and that ‘I am approaching near-term policy a bit more cautiously than I did a few months ago’. Harker did highlight that his overall view of the US economy is upbeat, but that risks to his outlook are very much tilted to the downside. New Minneapolis Fed President Kashkari also made some interesting comments yesterday. The former US Treasury official was fairly up front with his views on US Banks, saying that ‘the biggest banks are still too big to fail and continue to pose a significant risk to our economy’. He remarked that ‘now is the right time for Congress to consider going further than Dodd-Frank with bold, transformational solutions to solve this problem once and for all’.

Recapping the rest of the price action yesterday, Gold extended its move lower for a third day, finishing -0.73% at $1200. US Treasury yields were a smidgen higher with the benchmark 10y in particular up 2.4bps to 1.773%. European credit indices and financials in particular were a touch wider, while US indices finished 1bp tighter although the real news was in the primary market with the new issue market in the US reopening with a bang. Indeed over $23bn of deals were said to have been raised yesterday in the second busiest day of the year, led by a bumper nine-part $12bn deal for Apple while IBM and Toyota Motor Corp were also out with sizeable deals of their own. Despite the volatility in credit markets of late, clearly demand hasn’t waned too much with the order book for Apple in particular said to have reached $28bn.

Taking a look at today’s calendar now, the only data of note in the European session this morning will again come from the UK where we get the latest employment report where focus will be on the December unemployment and weekly earnings prints in particular. This afternoon in the US we’ll see the January housing starts and building permits data. Last month’s PPI print will also be worth keeping an eye on before we get the January IP report where expectations are currently running for +0.4% mom. Capacity utilization and manufacturing production data is also due before we get the January FOMC minutes this evening (7pm GMT) although as we’ve since heard from Fed Chair Yellen at her semi-annual testimony so the minutes will now look a little outdated. There’s no Fedspeak due today while earnings wise we’ve got 13 S&P 500 companies set to report.

end

Let us begin:

ASIAN AFFAIRS

Late TUESDAY night/ WEDNESDAY morning: Shanghai closed up only after a huge government intervention in the last hour / Hang Sang closed down by 197.51 points or 1.03% . The Nikkei was closed down 218.07 or 1.36%. Australia’s all ordinaires was down 0.57%. Chinese yuan (ONSHORE) closed 6.5260 on a bigger than usual devaluation by POBC and yet they still desire further devaluation throughout this year. Oil gained to 29.74 dollars per barrel for WTI and 33.14 for Brent. Stocks in Europe so far deeply in the green . Offshore yuan trades yuan to the dollar vs 6.5298 for onshore yuan/

Japanese trading TUESDAY night: the Nikkei falls 218.07 or 1.36% finally reacting to news of a drop in GDP by 1.8% year over year. China saw their exports tumbling! which causes fear in Japan of continual yuan devaluations.

Last night: China weakens the yuan again

Yuan Extends Slide As China Weakens Fix By Most In 5 Weeks

It appears last night’s terrible trade data has reawoken the beats of Chinese devaluation. Amid offshore Yuan’s slide since China came back from vacation, PBOC fixed the Yuan 107 pips weaker against the USD – the biggest ‘devaluation’ since the first week of January. Chinese stocks are opening modestly lower (despite exuberant panic-buying in Japan at the open which spiked Nikkei 200 points).

The biggest Fix weakening since the first week of January…

as Offshore Yuan extends its post-holiday decline…

This has pushed CNH “cheap” once again to CNY as outflows rise and shorts rebuild positions.

Charts: Bloomberg

China Puts Missiles On Disputed Islands, Says West Should Ignore Them, Focus On Lighthouses

China may not have troops or planes in Syria but that doesn’t mean it won’t be a part of World War III.

Even as the eyes of the world are now trained squarely on the Mid-East where the Russian and Iranian assault on Aleppo is set to draw the Saudis and the Turks into a ground war, the dispute over a tiny chain of islands in the South China Sea is still simmering.

Beijing has built some 3,000 acres of new sovereign territory atop reefs in the Spratlys, in what is now a long-running effort to expand the country’s maritime capabilities in waters China claims as its own.

The world began to take notice early last year and before you knew it, Washington’s regional allies were exceptionally upset with China’s “sandcastle” construction, which some view as an illegitimate attempt to militarize the island chain at the expense of peace and stability.

For its part, China says it has every right to do as it pleases in the Spratlys and in fact, at least one Chinese official has said that the PLA would be well within its rights to forcibly expel any country who seeks to occupy islands China doesn’t control.

Tensions escalated in May when China threatened a Poseidon spy plane with a CNN crew aboard and the situation was exacerbated further in October when the US finally “went there” and sent a warship to the islands in what the US dubbed a “freedom of navigation” exercise.

Through it all, China has indicated that it may establish what amounts to a no-fly zone over the islands and now, it appears the PLA is ready to make good on that threat because as Fox News first reported(yes, that’s right, Fox News somehow managed to get an exclusive) last night, China has deployed surface-to-air missile system on Woody Island.

“The imagery from ImageSat International (ISI) shows two batteries of eight surface-to-air missile launchers as well as a radar system on Woody Island, part of the Paracel Island chain in the South China Sea,” Fox said, adding that “the missiles arrived over the past week [as] the beach on the island was empty on Feb. 3, but the missiles were visible by Feb. 14.”

“A U.S. official confirmed the accuracy of the photos,” Fox goes on to claim. “The official said the imagery viewed appears to show the HQ-9 air defense system, which closely resembles Russia’s S-300 missile system [and] has a range of 125 miles.”

Here are the images:

“Asked about the missiles at a briefing in Beijing, Foreign Minister Wang Yi said that limited self-defense facilities on Woody Island are consistent with China’s self-protection policies and international law,”Bloomberg reports. “He described the report as Western media hype.” He also said the West should focus more on the lighthouses China has built on the islands which should help to protect the $5 trillion in shipping that moves through the region each year.

Right. It’s all “Western media hype.” This is just the PLA putting air defense systems in place on islands that China is definitely not militarizing. Nothing to see here, move along…

“This calls into direct question the seriousness of President Xi’s statement [that China doesn’t seek to militarize The South China Sea],” U.S. Pacific Command chief Harry Harris said.

Yes, it most certainly does and now that the HQ-9s are in place, you can expect to see more incidents like the one recorded below.

end

“Highly Dangerous” Radioactive Material Stolen In Iraq, “Could Be Used For ISIS Dirty Bomb”

Just when it seemed that the Syria’s proxy war would remain confined within the “comfortable” realm of conventional weaponry, moments ago Reuters gave the first hint of a potential, and radioactive escalation, when it reported that Iraq is searching for “highly dangerous” radioactive material stolen last year, according to an environment ministry document and seven security, environmental and provincial officials. The loss is significant because in already setting the next steps of the narrative, Reuters reportsthat the same officials “fear it could be used as a weapon if acquired by Islamic State.”

It is unclear why a “highly dangerous” radioactive substance was located in Iraq, but as Reuters adds, the material, stored in a protective case the size of a laptop computer, went missing in November from a storage facility near the southern city of Basra belonging to U.S. oilfield services company Weatherford, the document obtained by Reuters showed and officials confirmed (incidentally this is the same Weatherford which two weeks ago fired 15% of its employees after warning of “lower for longer” oil prices).

Reuters attempts to probe further were promptly contained: a spokesman for Iraq’s environment ministry said he could not discuss the issue, citing national security concerns. A Weatherford spokesman in Iraq declined to comment, and the company’s Houston headquarters did not respond to repeated requests for comment.

More details on the theft from Reuters:

The material, which uses gamma rays to test flaws in materials used for oil and gas pipelines in a process called industrial gamma radiography, is owned by Istanbul-based SGS Turkey, according to the document and officials.

An SGS official in Iraq declined to comment and referred Reuters to its Turkish headquarters, which did not respond to phone calls.

The document, dated Nov. 30 and addressed to the ministry’s Centre for Prevention of Radiation, describes “the theft of a highly dangerous radioactive source of Ir-192 with highly radioactive activity belonging to SGS from a depot belonging to Weatherford in the Rafidhia area of Basra province“.

A senior environment ministry official based in Basra, who declined to be named as he is not authorized to speak publicly, told Reuters the device contained up to 10 grams (0.35 ounces) of Ir-192 “capsules”, a radioactive isotope of iridium also used to treat cancer.

The material is classed as a Category 2 radioactive source by the International Atomic Energy Agency, meaning if not managed properly it could cause permanent injury to a person in close proximity to it for minutes or hours, and could be fatal to someone exposed for a period of hours to days.

Reuters adds that the ministry document said it posed a risk of bodily and environmental harm as well as a national security threat.

And with this highly radioactive substance stolen, concerns arise that it may have fallen in the hands of ISIS, from where it could promptly be used to make a dirty bomb.

According to Reuters, large quantities of Ir-192 have gone missing before in the United States, Britain and other countries, stoking fears among security officials that it could be used to make a dirty bomb.

“We are afraid the radioactive element will fall into the hands of Daesh,” Reuters cited a senior security official with knowledge of the theft, using an Arabic acronym for Islamic State.

“They could simply attach it to explosives to make a dirty bomb,” said the official, who works at the interior ministry and spoke on condition of anonymity as he is also not authorized to speak publicly.

For now, there has been no indication the material had come into the possession of Islamic State, which seized territory in Iraq and Syria in 2014 but does not control areas near Basra. However, in case of a dirty bomb going off somewhere on the Syria-Turkey border, in close proximity to a battalion of Russian solders, well…

Attempts to contain a potential panic appears somewhat muted: the security official, based in Baghdad, told Reuters there were no immediate suspects for the theft. But the official said the initial investigation suggested the perpetrators had specific knowledge of the material and the facility: “No broken locks, no smashed doors and no evidence of forced entry,” he said.

Almost as if it wasn’t actually “stolen.”

Meanwhile, everyone is searing for the deadly substance: “a spokesman for Basra operations command, responsible for security in Basra province, said army, police and intelligence forces were working “day and night” to locate the material. The army and police have responsibility for security in the country’s south, where Iranian-backed Shi’ite militias and criminal gangs also operate.”

Reuters also notes that ISIS does not actually have to make a dirty bomb with the material: besides the risk of a dirty bomb, the radioactive material could cause harm simply by being left exposed in a public place for several days, said David Albright, a physicist and president of the Washington-based Institute for Science and International Security.

The senior environmental official said authorities were worried that whoever stole the material would mishandle it, leading to radioactive pollution of “catastrophic proportions”.

A second senior environment ministry official, also based in Basra, said counter-radiation teams had begun inspecting oil sites, scrap yards and border crossings to locate the device after an emergency task force raised the alarm on Nov. 13.

Two Basra provincial government officials said they were directed on Nov. 25 to coordinate with local hospitals. “We instructed hospitals in Basra to be alert to any burn cases caused by radioactivity and inform security forces immediately,” said one.

Something tells us any burn cases will not afflict local Iraqis; however if we were Russian soliders in Syria or Iraq’s vicinity, we would be concerned.

The final word belongs to the abovementioned David Albright who said that “if they left it in some crowded place, that would be more of the risk. If they kept it together but without shielding,” he said. “Certainly it’s not insignificant. You could cause some panic with this. They would want to get this back.”

Unless causing some panic, and a panicked counterresponse, is precisely the intention.

\

At Least 5 Dead After Massive Explosion In Turkish Capital, Military Dormitory Targeted

With Turkey on the brink of going to war with Russia and, implicitly, Iran, President Recep Tayyip Erdogan is looking for an excuse to invade Syria.

The rebels Turkey and Saudi Arabia back are staging what amounts to a last stand at Aleppo and the Kurdish YPG is moving to cut the Azaz corridor, which would effectively mean that Turkey has no way of resupplying the insurgency.

For the past five days, Ankara has been shelling the YPG in a futile attempt to stop their advance.

The only thing that can save the rebellion against Bashar al-Assad is an outright ground operation by the rebels’ Sunni benefactors, including Turkey.

All Erdogan needs is a pretext and he may have just gotten one as reports indicate there’s been a huge explosion in Ankara near parliament and at least 5 people are dead.

Early indications are that military barracks were targeted. A “large number of casulaties” are rumored. Expect this to be pinned on either ISIS or the PKK. If it’s the latter, Ankara will once again claim that the group is working in concert with the YPG and that will be all the evidence Erdogan needs to march across the border.

- EXPLOSION REPORTED IN TURKISH CAPITAL ANKARA, AHABER SAYS

- ANKARA EXPLOSION OCCURRED NEAR MILITARY RESIDENCES: OFFICIAL

- 5 PEOPLE KILLED IN ANKARA BLAST: T24 CITES ANKARA GOVERNOR

- ANKARA BLAST WAS SUSPECTED CAR BOMB: CNN-TURK CITES GOVERNOR

????2huge explosions targetting area of Military Command Staff,Parliament, Houses of Military.Massive smoke/casualties! pic.twitter.com/IbwzwGOBQM

— taylieli (@taylieli) February 17, 2016

S&P Downgrades Saudi Arabia For Second Time In 4 Months, Also Cuts Oman, Bahrain

For the second time in four months, S&P has downgraded Saudi Arabia.

In late October, the ratings agency flagged sharply lower oil prices and the attendant fiscal deficit (16% in 2015) on the way to cutting the kingdom to A+ outlook negative.

At the time, S&P projected the deficit would amount to 10% of GDP in 2016. That turned out to be optimistic as the shortfall is now projected to be around 13% and that’s assuming crude doesn’t fall below $30 and stay there.

Riyadh has cut subsidies in an effort to shore up the books, but between the war in Yemen and defending the riyal peg, there’s no stopping the red ink, especially not while the kingdom remains determined to wage a war of attrition with the US shale complex.

Moments ago, S&P downgraded Saudi Arabia again, to A-.

On the bright side, the outlook is now “stable” (chuckle).

* * *

From S&P

Oil prices have fallen further since our last review of Saudi Arabia in October 2015, and we have cut our oil price assumptions for 2016-2019 by about $20 per barrel. In our view, the decline in oil prices will have a marked and lasting impact on Saudi Arabia’s fiscal and economic indicators given its high dependence on oil.

We now expect that Saudi Arabia’s growth in real per capita GDP will fall below that of peers and project that the annual average increase in the government’s debt burden could exceed 7% of GDP in 2016-2019.

We are therefore lowering our foreign- and local-currency sovereign creditratings on Saudi Arabia to ‘A-/A-2’ from ‘A+/A-1’.

The stable outlook reflects our expectation that the Saudi Arabian authorities will take steps to prevent any further deterioration in the government’s fiscal position beyond our current expectations.

RATING ACTION

On Feb. 17, 2016, Standard & Poor’s Ratings Services lowered its unsolicited long- and short-term foreign- and local-currency sovereign credit ratings on the Kingdom of Saudi Arabia to ‘A-/A-2’ from ‘A+/A-1’. The outlook is stable.

At the same time, we revised downward our transfer and convertibility (T&C) assessment on Saudi Arabia to ‘A’ from ‘AA-‘.

We now anticipate a current account deficit, equivalent to 14% of Saudi GDP in 2016, compared with 6% of GDP in our October review.

* * *

Other Gulf oil producers got the knife as well as Oman and Bahrain were cut to BBB- and junk, respectively.

- S&P: OMAN CUT TO BBB-FROM BBB+; OUTLOOK TO STABLE FROM NEG

- BAHRAIN CUT TO JUNK BY S&P ON LOWER OIL PRICE ASSUMPTIONS

Here’s the punchline from S&P: “We do not expect the agreement on Feb. 16 between oil ministers from Qatar, Russia, Saudi Arabia, and Venezuela to freeze oil output.”

We don’t either.

Finally, we ask “who knew what yesterday?”

Average:

MXN Shorts Crushed Soars After Mexcian Central Bank Unexpectedly Hikes Rate By 50 bps, Peso Soars

It was already a torrid day for commodity currencies, among which the MXN, or Mexican Peso, which were surging on today’s latest crude short squeeze and then as if pulling a PBOC with just one intention – to crush the shorts – the Mexican Central Bank or Banxico, dealt a crushing blow on anyone short the MXN when it announced an unexpected 50 bps rate hike in the overnight rate to 3.75%.

From the central bank: “The target for the overnight interbank funding rate is increased by 50 basis points.”

Perhaps the reason for the dramatic move is that Banxico, like the PBOC, no longer wants to be selling dollars to keep the currency stronger, so it resorted to the nuclear option. Sure enough:

- BANXICO INCREASES OVERNIGHT RATE BY 50 BPS

- VIDEGARAY SAYS FX COMMISSION ENDING DOLLARS SALES

- BANXICO MAY CONTINUE DISCRETIONARY DOLLAR SALES: CARSTENS

- CARSTENS: IT WAS A FORM OF PROTEST

- CARSTENS: FX RATE ‘MISALIGNED’ W/MACROECON FUNDAMENTALS

- CARSTENS: CEN BANK COULD MAKE EXCEPTIONAL INTERVENTIONS

Carstens also added that the decision for Banxico rate increase was unanimous.

Now whether the strengthening effect persists is another matter, but for now one look at the chart below shows that anyone who was long the USDMXN just had a Swiss National Bank moment.

And now we begin the countdown until the effect from this latest desperate central bank intervention is wiped out.

Read more here from Banxico.

50% Of Canadians Say They Are Within $200/Month Of Being Unable To Pay Their Bills

It was just last month when we profiled Canada’s “other problem”: record high household debt.

Canada is struggling to cope with falling crude prices which have put enormous amounts of pressure on some parts of the country, most notably Alberta, where suicide rates are on the rise, as is property crime and foodbank usage.

Amid the malaise, households are also being pressured by persistent CAD weakness – which is of course a symptom of falling crude. The currency’s decline has driven up prices for things like fresh fruits and vegetables, 75% of which Canada imports. That puts an extra burden on households that are already laboring under record debt.

As we showed three weeks ago, household debt relative to disposable income is sitting at 171% in Canada meaning that for every $100 in disposable income, households have debt obligations of $171. That’s the highest figure for any G7 country.

That’s disconcerting for any number of reasons. As we wrote, “this would be bad enough in a favorable economic environment with a benign outlook for rates, but it’s a veritable nightmare when the economy is sliding headlong into recession and central planners are hell bent on trying to normalize policy some time in the next five or so years.”

In other words, the outlook for Canada’s economy isn’t good, and that means joblessness is likely to rise going forward…

But interest rates have virtually nowhere to go but up – at least in the medium to long-term. Sure Stephen Poloz may cut rates one or two more times to try and help the oil patch avert certain insolvency, but at 50 bps, there’s only so much lower Canada can go unless the BoC intends to experiment with NIRP.

This means that households could face the disastrous prospect of rising rates in an unfavorable economic environment. Think a monetary policy mistake like hiking into a recession can’t happen? Just look at what the Fed did in December. Throw in the fact that many families are overburdened thanks to the astronomical cost of housing in places like Vancouver and Toronto and one is inclined to think that some Canadian households may find themselves in quite a bit of trouble going forward.

But don’t take our word for it, just ask Canadians, half of whom said in response to a new Ipsos Reid survey that they are within $200 per month of not being able to pay their bills and make their debt payments.

“Ipsos Reid conducted the poll about a week after the Parliamentary Budget Office issued a report on Jan. 19 that said Canada has seen the largest increase in household debt relative to income of any G7 country since 2000,” The Calgary Herald writes, adding that “31 per cent of respondents said any increase in interest rates could move them towards bankruptcy“.

The survey also found that 25% of Canadians are already unable to cover their bills and service their debt.

So what do you do if you’re the BoC? Cut rates to boost the economy and rescue the oil patch at the risk of driving the cost of imported goods through the roof, thus pressuring consumer spending and thereby creating another headwind for the economy? Or hike to bolster the loonie at the risk of tanking not only the oil patch but also the 31% of the country that say they’ll slip into bankruptcy it rates rise?

Your guess is as good as ours.

end

Calgary’s Housing Market Collapses While “Three-Alarm Blaze” Burns Next Door In Vancouver

In Waterloo, Ontario, the property market is red hot.

Dubbed “Canada’s Silicon Valley,” the city of just 140,000 people is drawing interest from real estate investors far and wide. Waterloo is around 70 miles west of Toronto and is home to a Google office as well as two universities and “dozens” of startups.

One-bedroom apartments in a new development being pitched to investors are going forCAD$270,000 while a two-bedroom will run you CAD$340,000. Rents in the building are as high as $2,000/month.

Vacancy rates are running at just 1.5%.

Meanwhile, in Vancouver, housing has gone full-retard. Average home prices for detached residences rose to an astronomical $1.82 million in January. It’s not as insane in Toronto, but at $631,092, there aren’t too many “bargains” to be had.

(Vancouver prices)

New data out on Tuesday shows average property values on resold homes in the Greater Vancouver area rising by 30.9% in January while average prices in the Greater Toronto Area and in the abovementioned Waterloo rose 14.2% and 9% for the month, respectively.

But oh what a difference a province makes.

While the Canadian housing bubble is alive and well in Ontario and British Columbia, in the heart of Canada’s dying oil patch the picture isn’t pretty. We’ve documented the glut of vacant office space in downtown Calgary on a number of occasions. Here’s a visual for those who missed it.