Gold: $1,230.40 up 4.30 (comex closing time)

Silver 15.37 down 6 cents

In the access market 5:15 pm

Gold $1226.50

silver: $15.34

At the gold comex today, we had a POOR delivery day, registering 3 notices for 300 ounces. Silver saw 0 notices for NIL oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 207.44 tonnes for a loss of 96 tonnes over that period.

In silver, the open interest rose by a whopping 5721 contracts up to 174900. In ounces, the OI is still represented by .875 billion oz or 125% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose by a large 10,001 contracts to 440,453 contracts as the price of gold was up $15.00 with yesterday’s trading.

We had another change in gold inventory at the GLD,this time a huge deposit of 2.68 tonnes of gold / thus the inventory rests tonight at 713.63 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,/we had no change in inventory and thus the Inventory rests at 310.952 million oz.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver rose by 5721 contracts up to 174,900 as the price of silver was up 6 cents with yesterday’s trading. The total OI for gold rose by 10,001 contracts to 440,453 contracts as gold rose by $15.00 in price from yesterday’s level.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

2b) COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/ FRIDAY morning: Shanghai closed DOWN slightly / Hang Sang closed down by 77.58 points or 0.40% . The Nikkei closed down 229.63 or 1.42%. Australia’s all ordinaires was down 0.79%. Chinese yuan (ONSHORE) closed down at 6.5202 on another bigger than usual intervention by POBC of cash through 7 day REPOS in support of the currency, and yet they still desire further devaluation throughout this year. Oil lost to 30.28 dollars per barrel for WTI and 33.68 for Brent. Stocks in Europe so far deeply in the red . Offshore yuan trades 6.52708 yuan to the dollar vs 6.5201 for onshore yuan/

Japanese trading THURSDAY night: the Nikkei falls badly by 229 points reacting finally to their trade data crumbling as their exports fall 12.9% year over year. The 10 yr interest rate plummeted to only .01% sending shivers down the spines of Abe and Kuroda.The drop in the 10 yr yield to .01% (totally unbelievable) is driving the Central Bank of Japan crazy. What is shocking the boys of the rising sun is the rise in the yen value: instead of falling to the level of 122 it has risen to the 112 handle:

Last night: China weakened the yuan again. Data released show continuing deflation in all sectors. The big story saw money market rates rise to as high as 9.6%. There is also trouble in the shadow banking sector where B. of America believes that China will no longer bail out deficient entities.

(zero hedge)

ii)Up until now, the government has been bailing out deficient entities for failure to pay interest on vehicles set up in China. Bank of America believes that China will now let these guys fail setting off an avalanche of defaults and many dominoes cascading:

iii) China will no longer report on a key data which shows the size of capital outflows from its country. This will make our life a little more difficult as this data is essential in understanding what is going on globally. However, China will need to fudge just about every other capital account.(courtesy zero hedge)

i a) The Prime Minister of Great Britain, Cameron does an all nighter as he pushes for reforms so that he can sell it to his citizens.

( zero hedge)

i b) If Great Britain leaves the EU, then Paris and Frankfurt cannot wait to tackle the English’s stranglehold on financial trading. England is the hub of financial trading throughout the world.

ii) Consumer confidence levels plunge in Eurozone

(zero hedge)

RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia is demanding an end to Turkey’s efforts in Syria. Russia has called an emergency meeting of the UN Security council to discuss what to do with Turkey’s aggression. We will watch developments on this front quite closely.

( zero hedge)

ii) It seems that Erdogan’s son Bilal Erdogan (of Turkey) has set up residency in Bologna Italy. Today he has been accused of money laundering as there is a full investigation on him;

( zero hedge)

iii)The USA are claiming that with direct hits on ISIS “banks” in Mosul they have effectively destroyed 1/2 billion of USA cash.

( zero hedge)

OIL MARKETS

i)It did not take oil long to tumble back below 30.00 dollars: exactly what we told you would happen!

( zero hedge)

ii) USA rig count drops heavily down 26 rigs following last week;s 28 and the week before at 31. This is the fastest 3 week plunge at over 17%. The rig count seems to track very nicely the falling oil price. However rig productivity is increasing and thus production is still steady!

(courtesy zero hedge)

PHYSICAL MARKETS;

i)Ray Dalio of Bridgewater, believes that the next fix on the horizon is helicopter money as it goes directly where it is needed: to the spenders:

ii)Jim Sinclair and Bill Holter discuss many aspects of gold and silver( JSMinset/Holter-Sinclair collaboration/GATA)

iii)Bank runs anybody? Are we close to having them?

( Robin Wigglesworth/London’s Financial Times/GATA)

iv)Our quant specialist now tells us why our two hedge funds, Bridgewater and Citadel are facing problems: lack of momentum (volume) in stocks. He suggests that it is harder for stocks to rise due to lower S and P earnings forecast this year will be down and thus the reason for our two hedge funds getting whacked. Interesting enough, our quant man from JPMorgan went long gold as he suggests it does have the mo jo behind it and it is time to load the boat.

(courtesy zero hedge/JPMorgan)

v)Miners are reacting to the lower gold price by cutting costs

( Lawrence Williams/Sharp Pixley)

vi)The dishoarding of gold by western central banks and the purchase of that hoard by Eastern nations:

USA STORIES WHICH WILL INFLUENCE THE PRICE OF GOLD AND SILVER

i)Our Fed doves are certainly not going to like the consumer core prices and then prices with food and energy. It rose at a rate of 2.2% which is higher than expected. Shelter rose 3.7%. It sure looks like Yellen will have her hands full if she tries QE4 down the road

ii) Just take a look at the problems facing public pension entities. They are so underfunded that they are now trying to cut benefits today by 50% to save the systeam.

Let us head over to the comex:

The total gold comex open interest rose to 440,453 for a gain of 10,000 contracts as the price of gold was up $15.00 in price with respect to yesterday’s trading. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month. Today, only the first scenario was in order as we actually gained in gold ounces standing for delivery. In February the OI fell by 256 contracts down to 278. We had 327 notices filed on yesterday, so we gained 71 contracts or an additional 7100 oz will stand for delivery. The next non active delivery month of March saw its OI fall by 105 contracts down to 1982. After March, the active delivery month of April saw it’s OI rise by 5023 contracts up to 306,818. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 219,802 which is fair. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was fair at 200,328 contracts. The comex is in backwardation until April.

Feb contract month:

INITIAL standings for FEBRUARY

Feb 19/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil |

| Deposits to the Dealer Inventory in oz | nil

|

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 3 contracts (300 oz) |

| No of oz to be served (notices) | 275 contracts (27,500 oz ) |

| Total monthly oz gold served (contracts) so far this month | 2335 contracts (233,500 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 531,585.1 oz |

we had 1 adjustment

i) Out of HSBC:

384.815 oz was adjusted out of the customer and this landed in the dealer account of HSBC;

.

FEBRUARY INITIAL standings/

feb 19/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 780,103.425 oz

Delaware CNT,Scotia |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 2042.190 CNT |

| No of oz served today (contracts) | 0 contracts nil oz |

| No of oz to be served (notices) | 1 contract (5,000 oz) |

| Total monthly oz silver served (contracts) | 165 contracts (825,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 13,362,972.7 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit;nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposits:

i) Into CNT: 2042.190 oz

total customer deposits: 2042.190 oz

total withdrawals from customer account 780,103.425 oz

we had 0 adjustments:

| COT Gold, Silver – February 19, 2016 |

| Tweet LinkedIn Google + | Disqus — Published: Friday, 19 February 2016 | E-Mail | Print

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 80,249 | 21,532 | 18,689 | 44,638 | 114,700 | |

| 2,141 | -3,894 | 766 | 201 | 8,554 | |

| Traders | |||||

| 97 | 48 | 50 | 37 | 46 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 166,645 | Long | Short | |

| 23,069 | 11,724 | 143,576 | 154,921 | ||

| -1,127 | -3,445 | 1,981 | 3,108 | 5,426 | |

| non reportable positions | Positions as of: | 161 | 126 | ||

| Tuesday, February 16, 2016 | © SilverSe | ||||

And now the Gold inventory at the GLD:

FEB 19/a huge deposit of 2.68 tonnes of gold into the GLD/Inventory rests at 713.63 tonnes

fEB 18/no change in gold inventory at the GLD/Inventory rests at 710.95 tonnes

fEB 17/no change in gold inventory at the GLD/Inventory rests at 710.95 tonnes

Feb 16.a huge withdrawal of 5.06 tonnes from the GLD/the loss was probably a paper loss/inventory at 710.95 tonnes

fEB 12/ a huge deposit of 11.98 tonnes/inventory rests at 716.01 tonnes. With gold in severe backwardation in London, I really believe that the gold added was paper gold and not real pbhysical/

Feb 11/no change in inventory/inventory rests at 702.03 tonnes

Feb 10/ a withdrawal of 1.49 tonnes of gold from the GLD/Inventory rests at 702.03 tonnes

Feb 9./a huge addition of 5.06 tonnes of gold into the GLD/Inventory rests at 703.52 tonnes/ (no doubt that this addition is paper gold/not physical/

Feb 8/no change in inventory/inventory rests at 698.46 tonnes

FEB 5/another massive 4.84 tonnes added to the GLD/Inventory rests at 698.46 tonnes/this is a paper gold addition and this vehicle is nothing but a fraud. There is no metal behind it.

Feb 19.2016: inventory rests at 713.63 tonnes

end

And now your overnight trading in gold, THURSDAY MORNING and also physical stories that may interest you:

“Own Some Solid Currency, In Other Words … Gold” Warns Faber

“Leave a million dollars with a bank, and in a year, you get only something like $990,000 back,” Marc Faber, respected publisher of the Gloom, Boom & Doom Report, told Bloomberg by phone yesterday.

“I would rather want to own some solid currency, in other words … gold” warned Faber.

Gold bears for years fed off the prospects for higher borrowing costs. Now bulls are thriving in a world where negative rates are becoming commonplace.

The Bank of Japan adopted negative rates last month to spur growth, joining central banks in Denmark, the euro area, Sweden and Switzerland. With about a quarter of the world economy facing negative rates in some form and growth faltering, gold has become one of this year’s best investments.

It’s a big turnaround for the metal which slid to a five-year low in December as the Federal Reserve readied for its first rate increase in almost a decade. With China’s slowdown roiling markets, there’s less chance the Fed will move again until next year. Negative rates mean depositing cash would leave investors with less than when they started, making traditional stores of value such as gold more appealing.

You can read the full article on Bloomberg here

Marc Faber is an eloquent advocate of owning physical gold which he describes as being a way to become “your own central bank.” He believes an allocation to physical gold will serve as vital financial insurance and that Singapore is the safest place to own gold in the world today.

Marc Faber Webinar on Storing Gold in Singapore

Essential Guide To Storing Gold In Singapore

LBMA Gold Prices

19 Feb: USD 1,221.50, EUR 1,101.14 and GBP 853.35 per ounce

18 Feb: USD 1,204.40, EUR 1,082.41 and GBP 841.19 per ounce

17 Feb: USD 1,202.40, EUR 1,080.57 and GBP 838.84 per ounce

16 Feb: USD 1,212.00, EUR 1,083.75 and GBP 838.04 per ounce

15 Feb: USD 1,208.45, EUR 1,078.94 and GBP 834.57 per ounce

For the week, gold is 0.4% lower and gold appears to have recovered from the falls seen on Sunday night and Monday morning.

For the week, silver is 0.7% lower and also appears to have recovered from the falls seen at the start of the week.

Both appear over valued in the short term and under valued in the medium and long term.

Smart money will continue to accumulate and dollar cost average into bullion.

Gold and Silver News and Commentary

“Bullion brokers GoldCore declared a bull market” – South China Morning Post

Gold sparkles amid global gloom to brighten mining sector – South China Morning Post

Gold firm above $1,200 as lower equities stoke safe-haven bids – Reuters

Gold Resumes Rally as ETP Assets Swell Amid Demand for Haven – Bloomberg

Gold rises, reverses earlier losses as equities pull back – Reuters

‘Helicopter money’ on the horizon, fund manager Dalio says – Finfacts

Gold Set to be the Most Popular Investment in 2016 – Prague Post

Questions and Answers with Bill Holter and Jim Sinclair – GoldSeek

New York Fed Suggests Large Asset Managers Are Systemic Risk Due To Runs – Value Walk

Negative interest rates a ‘dangerous experiment’ for the world as monetary policy hits buffers – Telegraph

Click here

‘Helicopter money’ on the horizon, fund manager Dalio says

Submitted by cpowell on Thu, 2016-02-18 20:52. Section: Daily Dispatches

Robin Wigglesworth

Financial Times, London

Thursday, February 18, 2016

Bridgewater’s Ray Dalio has argued that central banks’ ability to invigorate economic growth has atrophied, and he predicts a new era of radical monetary policy possibly involving “helicopter money.”

Central banks around the world have been attempting to revive durable economic growth and combat deflationary forces through conventional measures like interest rate cuts and unconventional policies such as quantitative easing — or bond buying — and even negative interest rates.

But Mr Dalio, by one measure the most successful hedge fund manager of all time, argued in a note to clients that these measures have been exhausted and are increasingly ineffective.

“While QE will push asset prices somewhat higher, investors/savers will still want to save, lenders will still be cautious lenders, and cautious borrowers will remain cautious, so we will still have ‘pushing on a string,'” he wrote.

He therefore predicts that central banks will eventually have to usher in what he calls “monetary policy 3” — where rate cuts were the first stage and quantitative easing the second phase — which will more directly and forcefully encourage spending.

The Bridgewater founder says this third era of monetary policy will range from central banks directly financing government spending through electronic money-printing to what the famous economist Milton Friedman coined “helicopter money” in 1969 — in other words, central banks disbursing cash directly to households. …

… For the remainder of the report:

http://www.ft.com/intl/cms/s/0/5bc2c2be-d666-11e5-829b-8564e7528e54.html

END

Jim Sinclair and Bill Holter discuss many aspects of gold and silver

(courtesy JSMinset/Holter-Sinclair collaboration/GATA)

Sinclair and Holter discuss gold- and silver-related issues

Submitted by cpowell on Thu, 2016-02-18 21:07. Section: Daily Dispatches

4:05p ET Thursday, January 18, 2016

Dear Friend of GATA and Gold:

Mining entrepreneur and gold advocate Jim Sinclair and his partner at JSMineSet.com, Bill Holter, have recorded a half-hour discussion addressing questions from readers about the world economy; the prospects for government currencies, gold, and silver; and other issues. The interview can be heard at JSMineSet.com here:

http://www.jsmineset.com/2016/02/18/questions-and-answers-from-readersfe…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Bank runs anybody?

(courtesy Robin Wigglesworth/London’s Financial Times/GATA)

New York Fed warns that asset managers are vulnerable to ‘runs’

Submitted by cpowell on Thu, 2016-02-18 21:20. Section: Daily Dispatches

By Robin Wigglesworth

Financial Times, London

Thursday, February 18, 2016

The New York Federal Reserve has warned that asset managers are vulnerable to quasi-bank runs that can cause “significant negative spillovers” across financial markets.

The combination of deteriorating trading conditions — especially in corporate bonds — and the swelling of the US mutual fund industry that promises investors the ability to redeem money at a moment’s notice has become an increasing concern for some policymakers, fund managers, and analysts.

While the New York Fed’s researchers have argued that bond market “liquidity” is not as bad as many traders and analysts maintain, they have examined the vulnerability of mutual funds to a sudden spurt of investor withdrawals, and concluded that they are indeed susceptible to “runs” despite not using leverage.

“The price dislocations that follow after large redemptions and liquidations are quite significant and have market-wide implication,” the New York Fed’s researchers said on the central bank’s Liberty Street Economics blog. “Investors seem to have become more skittish since the crisis and are quicker to redeem shares, and in larger amounts, for a given degree of underperformance.” …

… For the remainder of the report:

http://www.ft.com/intl/cms/s/0/4c000bba-d662-11e5-829b-8564e7528e54.html

END

Miners are reacting to the lower gold price by cutting costs

(courtesy Lawrence Williams/Sharp Pixley)

Gold miners cutting debt and production, improving margins

We speculated nine months ago that gold mining companies’ successes in cutting costs might be coming to an end as most of the easy cuts had been made and anything beyond that would largely be window dressing – See: Has Gold Mine Cost Cutting Gone As Far As It Can Go?. However we were wrong, although some of the key reasons that most gold miners have continued to be able to show both lower operating costs and better margins than the up-to-now falling gold price would suggest have been from factors completely outside the companies’ controls, with the oil price suffering a huge decline, which may only now be bottoming, and from the strength of the US dollar against producer nations’ own domestic currencies.

An interesting analysis from precious metals consultancy Metals Focus in a recent client newsletter, goes a little further. It opens by pointing out that a few years ago when gold had started its decline from its 2011 high point of around $1,900 an ounce, a speaker from a prominent resource fund at one of the numerous gold conferences, expressed a wish to see the price fall further (it was around $1600 at the time), on the grounds that this would force the mining companies to tackle the then ever-rising operating cost scenario and ultimately make the companies financially stronger in the longer term.

A complex industry like mining can weather many storms. It tends to get lax in its controls in good times, carried away by euphoria and pressures from greedy institutional shareholders who always want more, but who will then knife the miners in the back if things turn around adversely and their ever-growing profits start to fade. But, as the resource fund speaker noted above suggested, such occasional severe setbacks do force the companies to at least start to put their houses in order and ultimately make their companies stronger. That is until the cycle reverts and these things are long forgotten by a new generation of directors and managers and a degree of profligacy returns along with higher metal prices.

We are currently in the repair stages in the gold mining industry, but again we are of the opinion that there may no longer be much leeway in further operating cost cutting, as some of the external factors which have enabled many gold miners to stay afloat despite the big US dollar revenue falls, could be beginning to bottom or reverse. Metals Focus notes that ‘looking at the industry as a whole, the average total cash cost has fallen $130/oz from the peak reached in Q2.13 down to $652/oz as of Q3.15. The average all-in sustaining cost (AISC) over the same period has been cut from $1,128/oz to $824/oz. In spite of the much lower price, this has resulted in improved margins. Basic margin between gold price received and AISC stood at $302/oz in Q3.15 which is actually higher than that recorded in Q2.13, $289/oz, when gold prices averaged $1,417/oz.’

But a large part of the industry’s problem has been that, in addition to allowing operating costs to rise faster than they should have done, many of the major miners had been embarking on hugely costly big low grade new gold mine capital programmes which, while looking potentially very profitable at a higher gold price will have led to real profit margins (in terms of free cash flow) decline sharply with the lower one. A switch to mining higher grade sections of orebodies may have been possible in some cases (although this impacts adversely on future profitability and mine life) – but the real problem here was the massive build-up of the debt needed to finance the capital programs in the first place.

Debt servicing thus became an intolerable burden at the lower metal price, so it is no surprise perhaps that the biggest turnaround in the miners’ financial restructuring has been in reducing these huge debt levels, often by selling off non-core and low profit assets, and cutting back or eliminating any major future such expenditures. This debt restructuring continues to have a significant positive impact in helping reduce All In Sustaining Cost (AISC) figures.

Companies like world No. 1 gold miner Barrick, for example, which had been building up enormous debt levels have very successfully been reducing these substantially – at a cost to the balance sheet, but providing a significant benefit to operating margins and lowering unit costs. This will likely carry on at least until the miners see debt servicing costs returning to sensible levels and the finance sector may again be prepared to provide the wherewithal to develop big new projects again. This may not be for some years yet.

One suspects that the asset disposals and more circumspect capital spending patterns will continue for the time being, all helping make for leaner and meaner mining companies, but it does also mean that output growth is now plateauing, and beginning to turn down according to the most recent available data. Barrick, in demonstrating this, is targeting a production fall of around half a million ounces of gold in the current year compared with 2015, and more cuts looking further ahead. With cuts in exploration and in building new operations to replace aging mines which would need to close anyway, output is set now for a continuing fall at many gold mining companies – perhaps for several years yet.

Now whether a fall in new mined output will seriously impact the gold price positively is debatable. There are many other factors out there which can have an even bigger effect, at least in the short to medium term – See a recent article I’ve written on this subject:What does peak gold mean for the gold price. However a fall in global gold output will at least have an effect on sentiment towards gold investment while, as we see it, demand, particularly from the East where the ever-growing numbers of middle class consumers, with a traditional inbuilt propensity to use gold as a store of value against hard times, is continually growing. Falling gold inventories in the West suggest that there is a looming crunch on physical gold supply as a result of continuously rising demand and potentially falling supply. This will positively impact the gold price, and that of silver and the other precious metals, at some point in time. It may already have started, but with a metal where the price is so dependent on the futures markets where sentiment and vested interest big money rule, we can’t be sure yet. Gold and silver’s time will come – but when?

But back to the beginning of this article. Can gold miners continue to cut costs further – indeed do they now need to given the recent gold price recovery if this is sustained? Many analysts had predicted the demise of perhaps 50% of the global gold mining sector by now. This hasn’t happened. Indeed many look at gold’s 40% plus fall from its 2011 peak forgetting that the peak was a brief one and gold only averaged $1,572 that year – so the fall to the current price level from the 2011 average has only been 25%. This has thus been a less serious fall than generally reckoned. We suspect operating margins will still come down further, with the miners in cost-cutting mode, failing a decent gold price increase, despite oil prices beginning to pick up (but bear in mind many miners buy oil forward which means they can lock in current prices for a number of months ahead). Cutting debt levels will also continue. Meanwhile the huge cuts in capital programmes and exploration will mean there will be little new production coming on stream to replace shuttered operations.

Currency movements against the dollar are harder to predict. For resource economies, low metal prices could still mean further depreciations against the US dollar, even though the Dollar Index itself could fall back given that this is most heavily weighted against non-resource currencies like the Euro, the Swiss Franc, the Japanese Yen and the British Pound. There is no simple answer here.

Some major asset disposals will likely continue for the next year or so further bringing down debt and improving margins at the expense of balance sheet impairments. So the outlook for the gold miners is perhaps more positive than many might imagine in terms of overall day to day profitability and free cash flow – even at current lower gold prices. However there will be a continuing emphasis on improving margins which will lead to more low profit, or unprofitable, mines being shut or divested to smaller companies which may be more flexible in their approach.

As the fund manager quoted earlier was predicting, the shock of a falling gold price after 11 years of continuous rises, has certainly focused gold mining company management’s minds, while the stresses involved in doing so will continue to bear fruit for some years ahead. The industry is definitely already meaner and leaner and now may well be the time for investors to climb back in – even though actual operating costs may start to trend upwards again as inflationary pressures begin to impact.

Article first published on www.sharpspixley.com

end

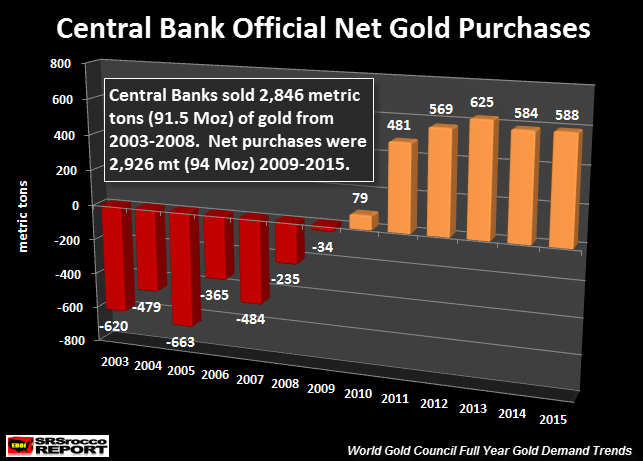

The dishoarding of gold by western central banks and the purchase of that hoard by Eastern nations:

(courtesy Steve St Angelo/SRSRocco Reprot)

Two Gold Charts Western Central Banks Are Worried About

There’s been a significant trend change in the gold market and it has the Western Central Banks worried. Before the collapse of the U.S. Investment Banking system in 2008, annual net physical gold investment was negligible. However, the present situation has changed considerably, putting severe stress on Western Central Bank policy makers.

Prior to 2008, many Central Banks (mostly Western) were net sellers of gold into the market. This official Central Bank policy was designed to keep the gold price from moving up higher. According to the figures from the World Gold Council, from 2003 to 2009, net sales of Central Bank gold totaled 2,846 metric tons (mt), or 91.5 million oz (Moz):

Central Bank gold sales peaked in 2005 at 663 mt and accounted for 21% of total demand that year. What would have been the market price of gold if the Central Banks didn’t dump 91.5 Moz over the seven-year period (2003-2009)?

Then something changed in 2010. As the United States and other Western Central Banks (Japan & then the EU) continued their massive QE (Quantitative Easing – money printing) policies, Eastern and various Central Banks became net buyers of gold.

Net Central Bank gold buying started at only 79 mt in 2010, surged to 625 mt in 2011 and is estimated to be 588 mt for 2015. Again, the majority of Central Bank gold purchases were from Eastern governments, especially in 2015. Russia and China accounted for majority of Central Bank gold purchases last year.

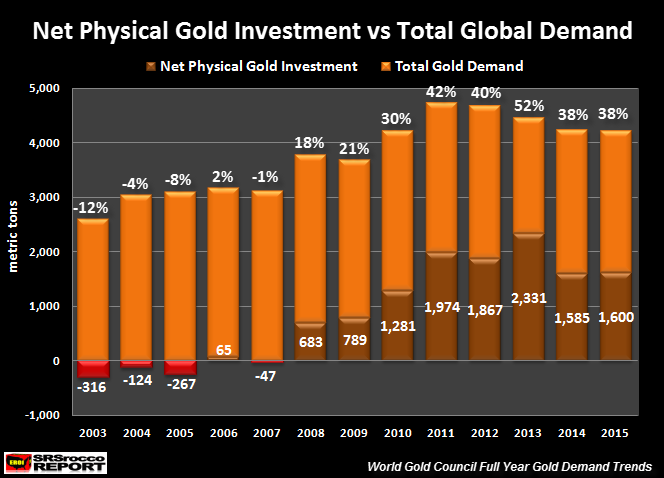

What a trend change… aye? From 2003-2009, Central Banks dumped 91.5 Moz of gold into the market. However, this totally reversed as Central Banks were net buyers, acquiring 94 Moz of gold from 2010-2015.

While Western Central Banks dumped gold onto the market to suppress the price, Eastern Central Banks are doing the opposite. Thus, Eastern Central Bank gold purchases have put more stress on “Net Physical Gold Investment.” I say physical gold investment as I have excluded changes in Global Gold ETF inventories. While Gold ETF’s are a gold investment vehicle, there is speculation that some (or a large percentage) of the Global Gold ETF inventories may be fictitious or oversubscribed. By the term oversubscribed… it refers to the notion that there are more than one owner for each ounce.

To get an idea just how significant the trend change of net physical gold investment has been over the past several years, I created the chart below:

Basically, I took total physical Gold Bar & Coin demand for the year, subtracted or added Central Bank net purchases and divided it by total demand. In 2003, total world Gold Bar & Coin demand was 304 mt and Central Bank gold sales were 620 mt for a net decline of total physical gold investment of 316 mt for the year. Thus, net physical gold investment for 2003 was a negative 12%. Which means, there was a 12% net disinvestment of physical gold in 2003.

I know this may sound a bit obtuse, but Central Bank gold sales are a liquidation of Central Bank reserves. Furthermore, most of this Central Bank gold sales were used to supplement the overall market including Jewelry, Bar-Coin and Technology demand.

For example, here is the breakdown for 2003:

2003 Global Gold Demand

Jewelry = 2,484 mt

Technology = 386 mt

Bar & Coin = 304 mt

Total = 3,174 mt

Central Bank sales = -620 mt

Total Demand = 2,554 mt

Even though total world gold demand was 3,174 mt in 2003, Central Bank sales of 620 mt had a negative impact and lowered overall demand down to 2,554 mt.

As we can see from the chart above, net physical gold investment was actually negative or very low (2% in 2006) before the U.S. and World financial and economic markets collapsed in 2008-2009. As Central Bank gold purchases increased after 2010, so did Gold Bar & Coin demand.

Let’s look at the peak year… 2013:

2013 Global Gold Demand

Jewelry = 2,673 mt

Bar & Coin = 1,706 mt

Central Bank = 625 mt

Technology = 354 mt

Global ETF change = -915 mt

Total = 4,443 mt

Here we can see that in ten years, there has been a significant increase in Gold Bar & Coin and Central Bank purchases. In 2003, net physical gold investment (Bar & Coin – Central Bank sales) was a negative 318 mt versus a positive 2,331 mt in 2013. Thus, net physical gold investment in 2013 accounted for a record 52% of total demand.

NOTE: I did not use changes in Global Gold ETF’s in creating the “Net Physical Gold Investment” in the chart above, but I did use the total demand figures from the World Gold Council which were adjusted due to builds or declines of Global Gold ETFs.

Why is this so important? Before 2008, net physical gold investment was minuscule or actually negative when we factor in Central Bank gold sales. Even if we took total Gold Bar & Coin demand of 304 mt in 2003 and divide it by total demand of 2,594 mt, it would only equal 12% of total gold demand that year.

Regardless, Central Banks dumped gold onto the market to suppress the price and help supplement the market. Now that Eastern Central Banks are net buyers of gold as well as the elevated Gold Bar & Coin demand, total net physical gold investment is consuming nearly 40% of total demand compared to the single digits prior to 2008.

Western Central Banks realize the price of gold determines demand, which is why they had to resort to knocking the price down from $1,600 to $1,150 at the beginning of 2013. Even though demand picked up significantly in 2013, there was available stocks to loot from above ground stocks such as the GLD ETF to meet this demand.

However, I believe the real Western Central Bank strategy was to continue slowly pushing the price down lower to keep gold off the RADAR from the Main Street Investor. There is speculation that China may be apart of the market rigging of gold, but it’s to their benefit in the long run, not the Western Central Banks.

There is one thing that I have not factored into the equation. A lot of global jewelry demand is by Indians. India consumed 654 mt of gold jewelry in 2015. I would imagine most of this would be considered a “Store of Wealth”, rather than something used for adornment purposes only. Yes, it’s true that the Chinese (and to lessor extent, Americans) purchased a lot of gold jewelry in 2015. And yes, this gold can be sold back into the market at close to spot price if the owner is clever.

That being said, Indians view gold jewelry more as a store of wealth, than do the Chinese or Americans. While some Chinese may be buying gold jewelry as a store of wealth, more Chinese have become like Americans and enjoy wearing gold more as adornment purposes.

Lastly, we must remember, nothing has changed since Lehman Brothers and Bear Stearns went bankrupt in 2008. The situation in the financial system is much worse than it was in 2008. I hear from several precious metal dealers that the wealthy investors are buying a lot of gold since the price spiked 5% in one day last week.

I believe 2016 will turn out to be an interesting year for the precious metals. Today, the price of gold is up $30 at $1,238. While the bullion banks continue to control the paper price, the new ABX fully allocated precious metal exchange will likely cause some real trouble for the Western Central Banks.

It wouldn’t take much of an increase of physical gold investment buying to totally overwhelm the market. Keep an eye out for possible fireworks in the precious metal markets this year. If this occurs, there is a good change that it may become impossible to acquire physical gold and silver.

end

And now your overnight THURSDAY NIGHT/ FRIDAY morning trades in bourses, currencies and interest rate from Asia and Europe:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.5202 / Shanghai bourse IN THE RED: / HANG SANG CLOSED DOWN 77.58 POINTS OR 0.40%

2 Nikkei closed DOWN 229.63 OR 1.42%

3. Europe stocks all in the RED /USA dollar index DOWN to 96.81/Euro DOWN to 1.1100

3b Japan 10 year bond yield: FALLS TO +.01 !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.88

3c Nikkei now well below 18,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 30.12 and Brent: 33.68

3f Gold UP /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS to 0.196% German bunds in negative yields from 8 years out

Greece sees its 2 year rate RISE to 12.05%/:

3j Greek 10 year bond yield FALL to : 10.75% (yield curve deeply inverted)

3k Gold at $1233.55/silver $15.45 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble DOWN 49/100 in roubles/dollar) 76.89

3m oil into the 30 dollar handle for WTI and 33 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9936 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1029 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England on criminal charges/arrests 10 traders for Euribor manipulation

3r the 8 year German bund now in negative territory with the 10 year FALLS to + .196%

/German 8 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.72% early this morning. Thirty year rate at 2.59% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Sink To Session Lows, Europe Slides Following Chinese RRR Hike Confusion, Brexit Concerns

Not even this morning’s mandatory European open ramp has been able to push US equity futures higher, and as a result moments ago the E-mini hit session lows on rising concerns about Brexit as talks drag on in Brussles, but mostly as a result of overnight confusion about China’s loan explosion and whether the PBOC has lost control over its maniacally-lending banks.

The biggest news overnight, in addition to the endless Brexit negotiations, was a report that the PBOC will hike RRR-rates on some banks, a move that may contain credit growth after advances by smaller lenders jumped in January. It also suggests that any incremental easing in China may be off the table for some time.

As a reminder, following January’s CNY3.42 trillion ( HARVEY : = 520 BILLION USA EQUIVALENT) surge in Total Social Financing, one estimate showed that February is already run-rating at roughly the same number, suggesting a total credit injection in the first two months of roughly $1 trillion. It is this surge that has apparently spooked the PBOC.

The central bank said in a Friday statement that some banks no longer meet criteria for preferential reserve requirement ratios and will have those levels increased. Prior to the announcement, Bloomberg News reported that some lenders will face a higher ratio as officials seek to limit the risks associated with last month’s jump in credit. The PBOC said its action wasn’t driven by the speed of lending.

A notable item is that the collective loan market share for ICBC, China Construction Bank, Agri Bank and Bank of China dropped to 20% last month from almost 40% in December, the figures show. This suggests that China’s four biggest banks weren’t the driving force behind last month’s credit binge. Small- and medium-sized lenders extended a combined 1.45 trillion yuan ($222 billion) of the new loans in January, accounting for 60 percent of the total increase.

While big banks are showing caution, smaller banks “are desperate to lend,” said Mu Hua, a Guangzhou-based analyst at GF Securities Co. “I just can’t figure out where would they find so many good projects to lend to. That’s probably raising some red flag to the central bank.”

What was truly bizzare is that between the first Bloomberg report and the subsequent PBOC confirmation, PBOC governor Zhou Xiaochuan said during a forum in Beijing that he “didn’t hear about” raising reserve-ratio rate for some banks, China Business News reported, opening up questions about just what is going on with monetary policy in China and who is making the decisions.

As a result of this PBOC confusion, US equity futures’ attempt to stage an overnight breakout failed, and the E-mini was trading down 9 points sessions lows at 1906 moments ago, while stocks in Europe and Asia trimmed weekly gains as oil fell for the first time in three days, denting optimism that this year’s rout in commodities was easing: as of this moment the European Stoxx 600 was down precisely 1.1%, while Spain’s IBEX was down 2%.

As Bloomberg adds, a global equities gauge fell for the first time in six days, bringing to an end a rally fueled by the first signs that producers may consider steps to rein in a record crude glut. Friday’s drop in energy prices dragged the Bloomberg Commodity Index lower even as industrial metals rose. Britain’s pound declined as David Cameron negotiated with European Union leaders over the U.K.’s membership of the bloc, while German bonds rose. The yen strengthened against all of its 31 major peers, with the biggest gains coming versus Asian counterparts.

“It’s a bumpy stabilization on oil, currency, spreads and equities,” said Didier Duret, who oversees about $219 billion as chief investment officer of ABN Amro Bank NV’s wealth-management unit. “The tail of energy has moved the psychology of the market.”

* * *

Looking at regional markets, we start in Asia, where stocks declined following from the negative lead from Wall St where stocks snapped a 3-day gain as oil weakness dampened sentiment. This saw the energy sector underperform across the region with the ASX 200 (-0.79%) further pressured by poor results from Santos. Nikkei 225 (-1.42%) is the laggard amid JPY strength, while the Shanghai Comp (-0.1%) saw indecisive trade as participants, however fell late in Asian trade amid source reports that the PBoC is said to have increased RRR for banks that bolstered lending too fast following the record lending data in China. 10yr JGBs tracked the gains seen in UST’s as the risk off sentiment globally spurred demand for safe-haven assets.

As noted above, the PBoC stated it has reviewed banks regarding RRR cuts, with some banks not meeting standards on targeted RRR cuts and as a result cannot enjoy the preferential RRR ratios beginning Feb 25th. This comes after PBoC’s Governor Zhou denied knowledge of source reports that the central bank have increased RRR for banks that bolstered lending too fast.

Asian stocks fall with the Kospi outperforming and the Nikkei 225 underperforming; The Nikkei 225 -1.4%, Hang Seng -0.4%, Kospi +0.4%, Shanghai Composite -0.1%, ASX -0.8%, Sensex +0%; 2 out of 10 sectors rise with utilities and health care outperforming and energy and consumer discretionary underperforming.

European markets have seen somewhat of a Friday lull so far, with newsflow particularly light and much of the price action relatively range bound. Price action has been somewhat guided by WTI and Brent futures, which both saw a bid in early European trade to retrace some of the losses in the wake of yesterday’s DoE inventories. As such WTI Apr’16 futures rose to test USD 33.00/bbl but failed to make a firm break and as such have come off their best levels in recent trade.

The Stoxx Europe 600 Index slid 0.5 percent at 11:14 a.m. London time, after rising as much as 0.3 percent. While the equity benchmark was set for a 4.7 percent gain this week, it’s still down more than 10 percent this year amid concerns ranging from global growth and the deepening oil slump, to the creditworthiness of lenders and dissipating faith in central-bank support.

Bunds have also been relatively range bound today, trading modestly higher after closing the opening gap shortly after the Eurex open, with little price action seen in the periphery. Additionally, analysts at Mizuho note that increase in average duration of EGB indexes this month-end will be a large 0.13yrs, which should be supportive for cash bonds. They also state that Austria, Italy and France will be the main beneficiaries from extension flows

“We remain reasonably confident that Europe can avoid a major macro slowdown, but current market pricing suggests otherwise.”, UBS says in note. “The markets seem to have taken a more negative view than we have on the severity of problems in the financial sector and their likely fallout on the European credit channel. The markets also seem to suspect that the ECB is running out of options to lift the economy.”

In commodities, West Texas Intermediate crude slipped 1.8 percent to $30.21 a barrel after rising the past two days on statements by the Saudis, Russians and Iranians. Brent fell 1.8 percent to $33.67.

U.S. crude stockpiles rose by 2.15 million barrels to 504.1 million last week, according to the Energy Information Administration. That’s the highest level in EIA data going back to 1930. In another sign of the glut, supplies at Cushing, Oklahoma, the biggest U.S. oil-storage hub, rose to a record 64.7 million barrels. The site, which is the delivery point for WTI, has a working capacity of 73 million, according to the EIA.

Gold lost 0.6 percent to $1,223.93 an ounce after posting a two-day, 2.5 percent jump. Copper rose 0.3 percent to $4,589 a metric ton while zinc, aluminum, tin and lead all gained more than 1 percent. Zinc is poised for its first five-week run of gains since last May and nickel is set for its biggest weekly increase since May 2014.

In FX, all the action has been in GBP this morning, with the UK retail sales numbers adding event risk to the overhang of the EU summit this morning. Early reports of selling vs the SEK fed through Cable, knocking the latter spot rate from 1.4335-40 levels down to just below 1.4300. Strong buying resumed ahead of the consumer numbers, but despite a strong read, the lack of upside progress saw the intra market turn tail to send Cable back to new lows on the day. Elsewhere, CAD and the rest of the Oil related currencies remain on the back foot, though Oil prices are relatively stable, albeit at lower levels. Euro bourses and S&P futures pretty flat on the day, helping to support USD/JPY off the earlier lows, but the heavy tone is clear to see. AUD on the back foot also, though finding some support below .7100.

The key event in the US January will be January’s CPI print where current expectations are for a -0.1% mom headline and +0.2% mom core readings which would take the YoY rates to +1.3% (up-six tenths from December) and +2.1% (unchanged versus December) respectively. In terms of Fedspeak we are due to hear from Mester at 1.30pm GMT on her economic outlook. EU leaders are also set to conclude their summit in Brussels (with Brexit discussions high on the agenda) while the ECB’s Constancio is due to speak this afternoon.

Bulletin Headline Summary from RanSquawk and Bloomberg

- European stocks trade broadly in negative territory in what has been somewhat of a quiet end to the week.

- UK retail sales beat expectations across the board, however downward revisions sees GBP pressured, while participants keep a close eye on the EU summit for any developments regarding Brexit talks.

- Looking ahead, highlights include US CPI, ECB’s Draghi (Soft Dove) and Fed’s Mester (Voter, Soft Hawk)

- Treasury yields mostly steady overnight as global equity markets and oil lower; CPI and average weekly earnings reports to be released at 8:30am ET.

- Central banks embrace negative rates that economists scorn as just 27% of respondents in a Bloomberg survey say negative rates will help the BOJ boost feeble inflation and only 42% say the policy is succeeding in the euro area

- U.K. retail sales surged the most in more than two years in January, boosted by demand for clothing and computers. The 2.3% jump in the volume of sales was almost three times the pace of growth forecast by economists in a Bloomberg survey

- David Cameron pleaded for a deal on the U.K.’s EU membership that he can sell to British voters. The prime minister ran into resistance from eastern European states over demands for more welfare curbs on non-British citizens

- Wall Street’s biggest banks boosted their Treasury holdings to the highest level in more than two years, and one of them says that’s a warning sign for the market

- China’s central bank said some banks will be forced to lock away more reserves, a move that may contain credit growth after advances by smaller lenders jumped in January

- Milan prosecutors are probing whether Credit Suisse engaged in money laundering and evaded taxes when it sold billions of euros of insurance policies that clients from Italy used to shield funds from tax authorities

- In a secret meeting convened by the White House around Thanksgiving, senior national security officials ordered agencies across the U.S. government to gain access to the most heavily protected user data on the most secure consumer devices, including Apple’s iPhone

- $8.1b IG corporates priced yesterday (YTD volume $221.45b) and $1b HY priced yesterday (YTD volume $11.125b)

Sovereign 10Y bond yields mostly lower led except Greece (+11bp); European, Asian markets mostly lower; U.S. equity- index futures mixed. Crude oil and gold drop, copper higher

DB’s Jim Reid concludes thes overnight wrap

With newsflow taking a bit of a breather, there hasn’t been a lot to drive markets over the last 24 hours or so. US equity markets in particular saw the strong 3-day rally come to a bit of a stuttering and unspectacular end yesterday. Some bleak Wal-Mart numbers certainly weighed on the retail sector, while the latest swing in the daily oil rollercoaster moved from hope around the Iran and Saudi Arabia/Russia production meetings back to the reality of the current fundamental picture following the latest set of bearish US crude inventory numbers. WTI was up as high as $32/bbl prior to the data and the highest in 9 days, before paring the bulk of the day’s gains to close at $30.77/bbl after data showed that crude stockpiles extended an 86-year high in the US. The S&P 500 eventually closed -0.47% while in Europe we saw the Stoxx 600 (+0.04%) finish pretty much unchanged having got off to a reasonable start prior to that oil data. Peripherals (IBEX -0.83%, FTSE MIB -1.53%) were notable under-performers though.

Away from this, various US economic surprise indicators improved again yesterday with both initial jobless claims (262k vs. 275k expected) and the Philly Fed manufacturing index (-2.8 vs. -3.0 expected) ahead of expectations. The improvement in the four-week moving average for claims to 273k (from 281k) in the NFP survey week was seen as particularly positive although the details in the breakdown of the Philly Fed data was less so. Prices paid (-2.2 vs. -1.1 previously), new orders (-5.3 vs. -1.4), inventories (-17.1 vs. -15.7) and number of employees (-5.0 vs. -1.9) in particular increase the risk that the next manufacturing ISM survey remains in contractionary territory when we receive the latest data in a couple of weeks.

US Treasury yields marched lower across the curve although the moves were essentially tracking the fall in oil from mid-afternoon. The benchmark 10y finished 8bps lower at 1.740% and is back to more or less where it closed last week. Credit markets reflected the lack of direction with indices in the US finishing flat, while weakness in European financials (iTraxx Senior +4bps, Sub +6bps) drove Main and Crossover 2bps and 4bps wider. Reassuring however was another strong day of primary across the pond with over $8bn of deals said to have priced. This shows that there is still demand for the asset class in spite of everything thrown at it of late. Elsewhere Anglo American, which has been in the news a fair bit this week, came out with a bond buyback announcement which helped sentiment for the asset class.

Refreshing our screens this morning, it’s looking like a bit of a mixed ending to the week for markets in Asia. After a strong week, bourses in Japan are ending on a down note with the Nikkei and Topix -1.43% and -1.47% respectively. The ASX (-0.79%) is also lower however there’s a modest gain for the Kospi (+0.31%) while bourses in China are flat. Oil markets are down around half a percent while credit indices are generally a tad wider. As we go to print Bloomberg headlines are suggesting that the PBoC is to raise the required reserve ratio for some banks having determined that some had increased lending too quickly with regional banks said to be targeted. One to keep an eye on as more details emerge.

In terms of the rest of the economic data yesterday, in the US the Conference Board’s leading index revealed an as expected -0.2% mom decline last month to mark the second consecutive negative monthly reading. Prior to this in France we saw no change to the final January CPI print of -1.0% mom with the YoY staying unchanged at a lowly +0.2%. Yesterday’s ECB minutes didn’t offer a whole lot new with the text revealing that the governing council was unanimous that policy ‘needed to be reviewed and possibly reconsidered’ at the March meeting, although there were some hints from certain policymakers that it would be ‘preferable to act pre-emptively’ rather than ‘wait after risks had fully materialized’.

Over at the Fed the latest set of comments came from San Francisco Fed President Williams who stuck to his view that ‘a gradual pace of policy normalization as being the best course’. Williams said that the US economy ‘still needs a gentle shove’ from monetary policy headwinds but that the economy is ‘all in all, looking pretty good’. On the popular topic of negative rates, Williams said that the chances of the Fed cutting rates below zero were ‘very remote’.

Before we look at today’s calendar, the OECD became the latest agency to cut global growth forecasts yesterday. The think-tank now see’s the world economy growing by 3% this year which is three-tenths lower than its previous forecast three months ago and the same pace as 2015. That included a five-tenths downgrade to its US forecast to 2% this year while China is expected to grow 6.5%. The biggest revision was reserved for Brazil however, who the agency expects to contract 4% this year, a downward revision of 2.8 percentage points.

Looking at today’s calendar, this morning in Europe the early data is out of Germany where we’ll see the January PPI numbers. That’s closely followed by UK retail sales covering the month of January where expectations are for a relatively robust +0.7% mom print excluding fuel. UK public sector net borrowing data is also expected. In the US this afternoon much of the focus will be on the January CPI print where current expectations are for a -0.1% mom headline and +0.2% mom core readings which would take the YoY rates to +1.3% (up-six tenths from December) and +2.1% (unchanged versus December) respectively. In terms of Fedspeak we are due to hear from Mester at 1.30pm GMT on her economic outlook. EU leaders are also set to conclude their summit in Brussels (with Brexit discussions high on the agenda) while the ECB’s Constancio is due to speak this afternoon.

Let us begin:

ASIAN AFFAIRS

Late THURSDAY night/ FRIDAY morning: Shanghai closed DOWN slightly / Hang Sang closed down by 77.58 points or 0.40% . The Nikkei closed down 229.63 or 1.42%. Australia’s all ordinaires was down 0.79%. Chinese yuan (ONSHORE) closed down at 6.5202 on another bigger than usual intervention by POBC of cash through 7 day REPOS in support of the currency, and yet they still desire further devaluation throughout this year. Oil lost to 30.28 dollars per barrel for WTI and 33.68 for Brent. Stocks in Europe so far deeply in the red . Offshore yuan trades 6.52708 yuan to the dollar vs 6.5201 for onshore yuan/

Japanese trading THURSDAY night: the Nikkei falls badly by 229 points reacting finally to their trade data crumbling as their exports fall 12.9% year over year. The 10 yr interest rate plummeted to only .01% sending shivers down the spines of Abe and Kuroda.

(see story below)

Last night: China weakened the yuan again. Data released show continuing deflation in all sectors. The big story saw money market rates rise to as high as 9.6%. There is also trouble in the shadow banking sector where B. of America believes that China will no longer bail out deficient entities.

(see story below)

First Japan: the drop in the 10 yr yield to .01% (totally unbelievable). What is shocking the boys of the rising sun is the rise in the yen: instead of falling to the level of 122 it has risen to the 112 handle:

A “Baffled” Bank Of Japan Is Shocked By Its “Message Of Despair”

One look at Japan’s bond yields, which moments ago hit a fresh record low for the 20Y maturity as the curve slowly but surely inverts…

…. and one would think Haruhiko Kuroda would be delighted.

After all, when he launched NIRP three weeks ago, a world in which negative rates are now a reality, it should have been clear to everyone even children, that yields would collapse as the scramble for any positive yield was unleashed.

The only problem is that Kuroda did not care about yields – positive or negative: what he wanted was to crush the currency and to send the Nikkei soaring – the only two actual “arrows” of Abenomics. Sadly for the BOJ, this time it failed as precisely the opposite of what was expected happened.

But, as the WSJ wrote earlier today in an article explaining why the BOJ is baffled (at least before a call from the BOJ forced it to change the title to the far more politically correct “Bank of Japan Faces a New Opponent on Negative Rates: Main Street“)…

… Kuroda’s confusion has nothing to do with the market’s reaction; it has everything to do with the reaction by the public.

An appropriately very negative reaction.

Just yesterday, shortly after the BOJ’s shocking announcement, Kuroda found himself dodging a concerted attack in Parliament from lawmakers who charged the policy was “victimizing consumers and sending a message of despair“, the WSJ writes.

Even a ruling-party member, Masahiro Ishida, called the policy hard to grasp. “It could have the opposite effect of confusing the market,” he said.

It already has. But the problem is not that the market is confused; it is that the market’s reaction to the BOJ’s NIRP, which as we explained previously was largely due to central banker “peer pressure” during this year’s Davos meeting, has led to a global revulsion against negative rates in general, thus validating the BOJ’s error.

The criticism has come as a surprise to central-bank officials who thought their efforts to spark lending and faster economic growth would gain more public support. “Those who understand this policy are criticizing us, and those who do not are also criticizing us,” said one official this week.

Here the WSJ adds something that is patenly wrong: “It is a symptom of a global problem. The more central banks move into unconventional policies, the harder it becomes to get their message across. That is a particular problem when the policies are supposed to work in part by inspiring confidence.”

Dead wrong: central bank policies are supposed to work by boosting the market; the narrative follows from there. It goes without sayinng that had Japan’s NIRP somehow sent stocks soaring and the Yen crashing, the avalanche of praise would have been constant and Kuroda would be deemed a hero in parliament. Alas for the BOJ – which failed at the simple task of manipulating the market higher in the initial kneejerk reaction – that did not happen, and now Kuroda is suddenly fighting for his professional life.

And since the BOJ’s market domination had finally cracked, a new narrative emerged: one which demonstrated the BOJ as being a bunch of “clueless losers”, with no understand of what they are doing.

Although negative interest rates have existed for some time in Europe, the idea was unfamiliar to most Japanese when it burst onto the front pages late last month. Initial accounts focused on what could happen to bank deposit rates. That is a sensitive issue in a society where wages have barely risen since the 1990s and where one in three citizens receives pension income.

“Deposit one million yen and earn annual interest of ¥10,” said the headline of an online article Tuesday by Japan’s biggest daily newspaper, the Yomiuri Shimbun, telling savers with nearly $10,000 in the bank that they could expect less than a dime in interest

But nothing demonstrates Kuroda’s bafflement quite as much as the outright hostile reception he got during his speech before parliament on Thursday:

In Parliament on Thursday, opposition lawmaker Shinkun Haku squared off with the Bank of Japan’s Gov. Kuroda on whether commercial banks would effectively introduce negative rates by hitting consumers with fees in excess of the tiny amount of interest paid. “Can you deny that banks will put an additional burden on average depositors?” Mr. Haku said. “If you can’t deny it, don’t. It’s a yes or no.”

Mr. Kuroda said he didn’t want to speculate about fees, but “there’s no chance that deposit interest rates will turn negative.”

Which is a lie – not only will deposit rates ultimately turn negative, the only questions are when and by how much.

He said negative interest rates had helped spur lending in Europe with few harmful effects. “Europe has much larger minus interest than the Bank of Japan, and I haven’t heard of minus interest rates being applied to individual depositors there,” he said.

Someone please inform the Credit Suisse or Deutsche Bank stock about the “few harmful effects”, or the fact that Europe’s economy is once again slowly relapsing into a recession, only this time with some 1.5 million Syrian refugees to partake in the festivities.

It didn’t stop there:

“Mr. Kuroda’s responses merely inspired further attacks from the opposition, which has been looking with little success for an issue with which to dent Prime Minister Shinzo Abe’s popularity…. a Communist Party lawmaker, Akira Koike, said negative interest rates were bad public relations. “You have sent a message to the people that they had better watch out because Japan’s economy is in trouble,” Mr. Koike said.

Which in itself is a stunning of just how stupid communists, or anyone else for that matter, still are and are utterly incapable of grasping the most simple equality of the post-crisis era, namely that any central banks intervening = the economy is in trouble.

And of course Japan’s economy is in trouble: it has had 6 recessions in the past 6 years as it rushes toward a demographic singularity in which there is simply no longer a Japanese population. Japan’s economy is in so much trouble, the only question is when does it disintegrate into a Venezuela-style supernova.

But we can see where the confusion comes from. As the WSJ conveniently notes, central banks “policies are supposed to work in part by inspiring confidence” and instead “lawmakers charged the policy was victimizing consumers and sending a message of despair.”

No: the message is one of reality, because the can kicking for Japan, having gone on for 40 years, is almost over. The good news about a central bank-free future is that it will hurt – a lot – for a while, and then normal growth can resume, but not before trillions in fake paper wealth are wiped out and quadrillions (in Yen terms) in debt is swept away.

As for Kuroda, we will fondly remember him forever as Peter Panic. There was also this pearl in the WSJ piece: “opposition lawmaker Motoyuki Odachi accused Mr. Kuroda of sounding like a World War II propaganda broadcast.”

Dear Motoyuki, all central bankers sound like a World War II propaganda broadcast, one on which the time has long ago come to pull the plug.

Chinese Money-Market Rates Are Spiking As Post-New-Year Liquidity Hangover Hits

It would appear the Chinese central bank currency squeeze is back as money-market rates are exploding higher once again. With the outpuring of liquidity heading into the new-year holiday, the post-celebration hangover was always likely unless PBOC just kept pumping but judging by the 500bps spike in overnight Yuan interbank rates to 9.3%, more than a few banks are desperate for some liquidity. We note that the last six times that Chinese banks have suffered liquidity constraints, US equities have tumbled…

While not at the extremes of mid December or mid-January’s catastrophes, O/N Yuan depo rates are soaring…

As it seems PBOC is not quite as liberal with its liquidty post-new-year…

and that bodes ill for US equities as the global liquidity problems this signals send ripples through every conduit (and their corresponding risk asset)…

Still 9.3% overnight deposit rates are probably nothing, right?

BofA Asks: Is This The Chinese Shadow Bank Failure That Will This Trigger The Chain Reaction

The reason why this particular bubble has proven so resilient is because up to this point the government has been willing to directly or indirectly bail out the participants. However, as Bank of America’s David Cui writes today, that may not be the case for much longer.

Take the case of Shanxi-based shadow bank Xinsheng. As CBN writes today, this is the latest shadow bank to collapse, a bank whose Shanghai subsidiary alone sold RMB1.9 billion in wealth management products to over 5,000 investors and is now unable to return the funds. As Chiecon writes, the company marketed “asset securitisation” wealth management productspromising annual returns between 13%-24%. In reality, client funds were diverted into real estate projects, mainly office buildings, in lower tier cities, where chronic oversupply has depressed local property prices. Some investors are now protesting outside the company’s Shanghai branch office.

As Bank of America adds, as large as Xinsheng’s sounds, it pales against some of the other recent defaults in the lightly regulated P2P and private wealth management product markets. For example, in July 2015, a commodity exchange, Fanya, defaulted on Rmb43bn, involving some 220k investors nationwide (Yunnan News, Feb 5); in Nov, a P2P platform, Caifu Milestone, defaulted on Rmb5bn from some 75k individuals (China Business News, Jan 11); in Dec, a P2P platform, eZubao, defaulted on Rmb50bn from some 900k investors (New Beijing News, Feb 1); in Jan, a P2P platform, Rongzicheng, defaulted on Rmb1.5bn (Economic Information, Jan 26); another P2P player, Shengshi Caifu, defaulted on Rmb2bn from some 7k investors (Rong360, Jan 21).

The charts below show BofA’s estimates related to the default cases in the shadow banking sector, based on media reports of high profile actual default cases. What is notable is that while the number of reported cases has remained relatively low, the size of the blow ups has soared in recent months.

So far, none of the six cases mentioned above in the P2P and private wealth management product markets have been resolved, and there has been no clarification from the companies or local governments on potential solutions. Unless the government decides to bail investors out, large losses could ensue, Cui warns.

Previously, defaults mainly occurred in more stringently regulated areas e.g. trust and bond, and involved financial institutions with large balance sheets. The cases were often resolved in investors’ favor.

In a scenario in which investors are not bailed out and thus become more cautious, eg, rolling over some of the debt instruments in the shadow banking sector, some borrowers may struggle to obtain credit, for example, developers and coal miners.

Whether this scenario would trigger a chain reaction is a key risk that needs to be monitored.

Moreover, given the default pressure in the trust and bond market markets as detailed in the list of defaults at the end of this article, cases may emerge there eventually.

The paradox, as Cui concludes, is that if shadow banking investors continue to be bailed out, this would imply a further strengthening of the implicit guarantee, and potentially, put pressure on growth, increase the debt burden and hurt RMB stability.

BofA’s conclusion: “financial system risk is arguably the most important risk facing market this year. Until the debt issue is addressed, we believe it is unlikely we will see the bottom of the market.”

We don’t know, but we find it disturbing that suddenly a whole lot of banks around the globe – from Germany to China – are being watched very closely as a potential catalyst that will spark the next crisis. Wasn’t the entire point of the 2008/9 bailout and subsequent injection of trillions in central bank liquidity to ensure that precisely this scenario does not occur?

And speaking of defaults of either plain vanilla companies, or shadow bank trusts, here is a brief list of all recent Chinese defaults: how long until the the losses from any one of these – or some upcoming default – are simply too large for the government to pocket, and the inevitable “chain reaction” is finally triggered.

END

China will no longer report on a key data which shows the size of capital outflows from its country. This will make our life a little more difficult as this data is essential in understanding what is going on globally. However, China will need to fudge just about every other capital account.

(courtesy zero hedge)

China No Longer Reports Key Data Showing Size Of Its Capital Outflows

When it comes to following China’s capital outflows, the traditional place to keep track has been China’s official reserve data released monthly, which however as we showed previously can and often is manipulated to give the impression of generally smalle numbers. We noted one example in October when China disclosed an official outflow of $43 billion, yet this number was largely incomplete, and short of the total, due to the PBOC’s recent adoption of using currency forwards to manipulate the Yuan, something not tracked by the official reserve number.

This is what Goldman said at the time about a relatively more reliable data set which provides a more accurate snapshot of China’s capital position:

In our view, a preferred gauge of FX-RMB conversion trend amongst onshore non-banks would be SAFE data on banks’ FX settlement on behalf of their onshore clients (to be out on October 22nd). That report captures banks’ FX transactions vis-à-vis non-banks through both spot and forward transactions (for August this data showed an FX outflow of $178bn). But to assess the overall FX-RMB trend, including in the offshore RMB (CNH) market, other FX data sets such as the position for FX purchase would be useful supplements—these are not affected by valuation effects and include FX settlement between the onshore banking system and offshore banks, although they do not account for forward transactions. Data on the position for FX purchase covering the PBOC should be out on October 14, and similar data covering the whole onshore banking system (PBOC plus banks) should be released at around the same date, although this is not completely clear.

It appears that China has finally figured out this loophole to track the PBOC’s attempts at masking the sheer size of its outflows, because as SCMP reported overnight, “sensitive data is missing from a regular central bank report in China amid concerns about the flow of cash out of the country as its economy slows and currency weakens.”

More from SCMP:

Financial analysts say the sudden lack of clear information makes it difficult for markets to assess the scale of capital flows out of China.

Figures on the “position for forex purchase” are regularly published in a monthly report issued by the People’s Bank of China.

The data, however, is missing from its latest report on the “Sources and Uses of Credit Funds of Financial Institutions in Foreign Currencies”.

Another key item of potentially sensitive financial data has also been altered in the latest report.

As SCMP adds, the central bank regularly publishes data on the ‘foreign exchange purchase” position, which covers all financial institutions including the central bank. The figure was 26.6 trillion yuan (HK$31.7 trillion) in December. The data published in January, however, only gives information on forex purchases by the central bank and details the lower figure of 24.2 trillion for last month.

The report (source) and line item in question are shown below:

Why the dramatic change in what is arguable one of the most important data series about the Chinese capital situation, one which comes at a time when China has been outflowing around $100 billion every month, shringking its total reserve holdings to dangerous levels? We don’t know: SCMP writes that the press office at the People’s Bank of China bank has yet to respond to telephone calls or a faxed request for comment about the changes.

As it also adds, “the central bank has tweaked items on its financial statements before, but the latest unannounced change comes at a particularly sensitive time when Beijing is trying hard to stabilise the yuan exchange rate. It is also just a week ahead of the G20 central bankers and finance ministers meeting in Shanghai.”

As a reminder, many expect that China may announce a major devaluation at the upcoming G-20 meeting, which some such as Bank of America have dubbed the “Shanghai Accord.”

The result is that China’s already opaque and manipulated economic picture, will become even more so:

“The central bank used a non-transparent method which makes the market unable to have a clear picture about capital flows,” said Liu Li-Gang, chief China economist at ANZ in Hong Kong.

“Given current circumstances, the move will fuel more speculation that the country is under great pressure from capital outflows. It will hurt the central bank’s credibility.”

An in-house analyst at an investment bank in Beijing, who declined to be named, said the changes were technical, but reflected the central bank’s intention to hide China’s real capital flows.

As we noted above, SCMP explains that according to analysts it was common practise to calculate China’s capital outflows by looking at the gap between positions on the yuan throughout the financial system and at the central bank alone, but the changes by the central bank would make this calculation impossible.

All data related to foreign exchange released by the central bank is closely monitored by financial analysts. They often read item by item from the dozens of tables and statistics released by the People’s Bank of China to spot new trends and changes.

What makes matters worse for China is that as Xie Yaxuan, chief economist at China Merchants Securities, says the central bank was unable to conceal data as there were many ways to obtain and assess information on capital movements.

“We are waiting for more data releases such as the central bank’s balance sheet and commercial banks’ purchase and sales of foreign exchange released by the State Administration of Foreign Exchange for a better understanding of the capital movement and interpreting the motive of the central bank for such change,” said Xie.

This means that if China truly intends to cover up how much capital is fleeing the mainland on any given month, it will have to fudge, delete, adjust and otherwise manipulate virtually every other capital account series, making a complete mockery of its already laughable economic reporting.

We wonder what the IMF will have to say about this significant occlusion to a critical currency data series by the newest member of the SDR basket.