Gold: $1,258.70 down $13.30 (comex closing time)

Silver 15.61 up 6 cents

In the access market 5:15 pm

Gold $1250.80

silver: 15.48

At the gold comex today, we had a poor delivery day, registering 8 notices for 800 ounces and for silver we had 101 notices for 505,000 oz for the active March delivery month.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 212.04 tonnes for a loss of 91 tonnes over that period.

In silver, the open interest fell by 358 contracts to 169,264 despite the outside/upside reversal yesterday with silver advancing by 19 cents . In ounces, the OI is still represented by .846 billion oz or 122% of annual global silver production (ex Russia ex China).

In silver we had 101 notices served upon for 505,000 oz.

In gold, the total comex gold OI rose by an enormous 15,074 contracts to 504,118 contracts as the price of gold was up $15.40 with yesterday’s trading.(at comex closing).

We had another rather large change in gold inventory at the GLD, a deposit of 5.95 tonnes of gold from the GLD/ thus the inventory rests tonight at 798.77 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,/we had a huge change in inventory/this time a huge deposit of 1.333 million oz and thus the Inventory rests at 323.965 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fell by 358 contracts down to 169,264 despite the fact that the price of silver was up 19 cents with yesterday’s trading. The total OI for gold rose by 15,074 contracts to 504,118 contracts as gold was up $15.40 in price from yesterday’s level. The high OI in gold necessitated our criminal bankers to raid gold/silver today.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

b COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/ FRIDAY morning: Shanghai closed UP BY 5.58 POINTS OR 0.20% , / Hang Sang closed UP by 215.18 points or 1.08% . The Nikkei closed UP 86.52 or 0.51%. Australia’s all ordinaires was UP 0.14%. Chinese yuan (ONSHORE) closed UP at 6.5003. Oil GAINED to 38.68 dollars per barrel for WTI and 40.70 for Brent. Stocks in Europe so far ALL IN THE GREEN RESPONDING TO THE OIL RAMP UP. Offshore yuan trades 6.4976 yuan to the dollar vs 6.5003 for onshore yuan/ LAST WEDNESDAY, MOODYS DOWNGRADES CHINA’S CREDIT FROM STABLE TO NEGATIVE. At the big people’s congress where they meet to set a 5 year plan, the leaders failed to deliver a major fiscal stimulus package.

ii)report on Japan

Two days ago we witnessed panic buying into the Japanese 10 year bond sending yields down to negative 0.10%. Last evening it was panic selling which again caused a flash crash as yields rose to +0.003%.

Points of interest: because China is focusing on a basket of currencies instead of just the USA dollar, the offshore yuan has just jumped 300 basis points to 6.494 and its strongest level since mid December. Gold is rising and at 9 pm est it is trading at 1278. Goldman Sachs is within 13 dollars of being stopped out of its gold contracts

iv) For 18 months in a row, USA import prices have fallen year over year. However we are beginning to see the first rise in prices since May 2014. China is still exporting its deflation to the entire globe:( zero hedge)

v)After a dramatic increase in social lending in January, February witnesses a total collapse

EUROPEAN AFFAIRS

i)Draghi warns about the rising inequality, even hours after boosting QE which rewards bankers and hurts Main Street:

( zero hedge)

ii)David Stockman talks about yesterday’s ECB announcement and what it means:

OIL STORIES

i)The EIA states that oil may have bottomed as non OPEC cut production. However Goldman Sachs has come out with another report where they warn of lower prices as storage fills last remaining spaces:

( zero hedge)

ii)Crude reacts to the EIA report stating that we are at the bottom with respect to WTI pricing/ and ignores Goldman’s dire warning on oil:

iii)However the low WTI price is causing many Texas towns to undergo huge hardships as credit is downgraded at municipalities and West Texas Governments.

iv)first it was gold that was slammed. Then late in the morning, they whacked oi:

v)Production higher, yet rig counts continue to collapse.

i)Alasdair Macleod talks about gold as the only sound money:( Alasdair Macleod/GATA)

ii)Ambrose Evans Pritchard comments on yesterday’s ECB decision, basically saying the Euro zone is extremely worried on the mounting deflation heading its way:

( Ambrose Evans Pritchard/UKTelegraph)

iii) Steve St Angelo takes on Jeff Christian on the true figures for silver demand

and destroys him!

(Steve St Angelo/SRSRocco)

USA STORIES WHICH WILL INFLUENCE THE PRICE OF GOLD/SILVER

i)the big story of the day: the bond market is broken to smitherines

Treasury failures soaring to multi year highs as collateral disappears:

Not only is the 10 year treasury in trouble but also the 30 yr treasury is also disappeariny in collateral.. the 10 yr repo rate -3% and the 30 yr repo rate -2.40%

(COURTESY ZERO HEDGE)

ii) This week’s wrap up with Greg Hunter

(Greg Hunter/USAWatchdog)

Let us head over to the comex:

The total gold comex open interest rose to 504,118 for a gain of 15,074 contracts as the price of gold was up $15.40 in price with respect to yesterday’s huge advance and an outside/upside gold price reversal and thus why the bankers raided today. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month or for that matter an inactive month, and 2) a continual drop in the amount of gold standing in an active month. Today, only the first scenario was in order as we actually gained in number of ounces standing for March. The front March contract month saw its OI rise by 33 contracts up to 146.We had 0 notices filed upon yesterday, and as such we gained 33 contracts or an additional 3300 oz will stand for delivery. Somebody must be in urgent need of physical gold. After March, the active delivery month of April saw it’s OI rise by 5026 contracts up to 281,676. This high level is also scaring our crooked bankers. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 251,772 which is good. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was excellent at 340,016 contracts. The comex is not in backwardation .

March contract month:

INITIAL standings for MARCH

March 11/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 196.15 oz(

SCOTIA

|

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 8 contract (800 oz) |

| No of oz to be served (notices) | 138 contracts(13,800 oz) |

| Total monthly oz gold served (contracts) so far this month | 584 contracts (58,400 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 106,013.9 oz |

we had 2 adjustments

i) Out of Brinks: 701.67 oz was adjusted out of the dealer and this landed into the customer account. This is probably a settlement of a delivery

ii) Out of JPMorgan; 404.984 oz was adjusted out of the dealer and this landed into the customer account of jPM and it also is a probable settlement.

.

MARCH INITIAL standings/

March 11/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 47,091.110 oz (Delaware,Brinks

CNT) |

| Deposits to the Dealer Inventory | 458,229.970 ozCNT

|

| Deposits to the Customer Inventory | 142,384.000 oz ??? (CNT) |

| No of oz served today (contracts) | 101 contracts 505,000 oz |

| No of oz to be served (notices) | 1238 contract (6,190,000 oz) |

| Total monthly oz silver served (contracts) | 447 contracts (2,235,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 8,462,724.3 oz |

Today, we had 1 deposits into the dealer account:

i) Into CNT: 458,229.970 oz

total dealer deposit; 458,229.970 oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposit

i) Into CNT: 142,384.000 oz ??????

total customer deposit; exactly 142,384.000 oz

We had 3 customer withdrawals:

i) Into CNT: 36,326.960 oz

2. Into Delaware; 5,893.05 oz

3. Into Brinks: 4871.100 oz

:

total customer withdrawals: 47,091.110 oz

we had 2 adjustments

i) Out of CNT:

40,079.45 oz was adjusted out of the customer account and this landed into the dealer account of CNT

ii) Out of the International Depository Services of Delaware:

20,409.580 oz was adjusted out of the customer Delaware and into the dealer Delaware.

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 252,895 | 78,085 | 76,202 | 116,493 | 311,865 | 445,590 | 466,152 |

| Change from Prior Reporting Period | ||||||

| 29,709 | 7,312 | 15,552 | 922 | 24,863 | 46,183 | 47,727 |

| Traders | ||||||

| 184 | 106 | 96 | 45 | 58 | 276 | 218 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 53,520 | 32,958 | 499,110 | ||||

| 2,372 | 828 | 48,555 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, March 08, 2016 | |||||

Those large specs who have been short in gold added a tiny 828 contracts to their short side

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 79,879 | 19,995 | 18,527 | 47,434 | 118,249 | |

| 1,272 | -3,132 | 4,997 | -591 | 4,987 | |

| Traders | |||||

| 93 | 49 | 43 | 37 | 43 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 169,875 | Long | Short | |

| 24,035 | 13,104 | 145,840 | 156,771 | ||

| 1,904 | 730 | 7,582 | 5,678 | 6,852 | |

| non reportable positions | Positions as of: | 150 | 122 | ||

| Tuesday, March 08, 2016 | © Silver | ||||

Our small specs;

And now the Gold inventory at the GLD:

March 11 /despite the high volatility of gold last night and today, somehow the GLD added 5.95 tonnes of gold without disturbing anyone./inventory rests this weekend at 798.77 tonnes

March 10/a deposit of 2.08 tonnes of gold into the GLD/Inventory rests at 702.82 tonnes

March 9/a withdrawal of 2.38 tonnes of gold from the GLD/Inventory rests at 790.74

March 8/no changes in inventory at the GLD/Inventory rests at 793.12 tonnes

MARCH 7/a tiny loss of .21 tonnes of gold probably to pay for fees/inventory 793.12 tonnes

MARCH 4/another mammoth sized deposit of 7.13 tonnes of gold into GLD/Inventory rests at 793.33 tonnes. This is no doubt a “a paper addition” and not physical

MAR 3/another good sized deposit of 2.37 tonnes of gold into the GLD/Inventory rests at 788.57 tonnes

MAR 2/another mammoth paper gold addition of 8.93 tonnes of gold into the GLD/Inventory rests at 786.20 tonnes.

March 1/a mammoth 14.87 tonnes of gold deposit into the GLD/inventory rests at 770.27 tonnes

FEB 29/another deposit of 2.08 tonnes of gold into the GLD/Inventory rests at 762.40 tonnes

Feb 26./no change in gold inventory at the GLD/Inventory rests at 760.32 tonnes

Feb 25./we had a huge deposit of 7.33 tonnes of gold into the GLD/Inventory rests at 760.32 tonnes. No doubt that this is a paper gold deposit/not real as the price of gold hardly moved on that huge amount of deposit.

FEB 24/no change in gold inventory at the GLD/Inventory rests at 752.29 tonnes

FEB 23./another huge addition of 19.3 tonnes of gold into its inventory/Inventory rests at 752.29 tonnes. Again how could they accumulate this quantity of gold with backwardation in London/this vehicle is nothing but a fraud

Feb 22/A huge addition of 19.33 tonnes of gold to its inventory/Inventory rests at 732.96 tonnes/ How could this happen: a huge addition of gold coupled with a huge downfall of 20 dollars in gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

March 11.2016: inventory rests at 798.77 tonnes

end

end

And now your overnight trading in gold, FRIDAY MORNING and also physical stories that may interest you:

Gold Prices Hit 13 Month High as ECB ‘Bazooka’ Shoots Blanks

Gold prices climbed to a 13-month high in dollar terms overnight ($1,282.51) after the increasingly adventurous, dare one say reckless, European Central Bank unleashed its latest ‘bazooka’ and initiated more interest-rate cuts, a significant extension in currency printing and bond purchases and also a potential subsidy to banks lending.

Gold in EUR – 1 Year

Draghi cut the ECB’s deposit rate by a further 10 basis points to minus 0.40 percent, and its main refinancing rate to zero and announced that the ECB may buy nearly a whopping €1 trillion in corporate debt.

The move was even more dovish than expected and confirmed, if any confirmation was necessary , that the ultra loose monetary policy adventure has intensified and will actually deepen in the short term.

Gold reached 3 year highs in euro terms at €1,161.40 per ounce on Monday after 4% gains last week – likely anticipating ‘Super Mario’ Draghi’s latest attempt at pulling a rabbit out of the hat. There is likely an element of ‘buy the rumour and sell the news’ as year to date euro gold has already eked out strong gains of 17%.

On the announcement yesterday, the euro fell initially versus gold from €1,135 per ounce to €1,155 per ounce prior to reversing and falling back to €1,135 per ounce as the euro strengthened. Gold in euro terms was actually marginally lower by the close yesterday and is marginally lower this week after the multi-month record high on Monday.

Huge volatility was seen in all markets as Draghi surprised even the monetary doves by making already ultra loose monetary policies even looser. This was most evident in the foreign exchange markets where despite deepening currency debasement the euro surged in value. Versus the dollar, the euro surged from 1.082 to over 1.11 in minutes or a near 3% surge. By the end of the day, the euro had surged from 1.082 to over 1.121 or a move of over 3.6% in a few hours.

Such volatility is more akin to a casino rather than a stable foreign exchange market between two leading international mediums of exchange. It is great for and welcomed by CFD providers, spread betters, brokers, hedge funds and speculative banks. But it has real world economic consequences for small and medium enterprises and all EU companies and international companies trading in the EU. Such volatility and extremely rapid moves in the value of the two world’s leading trading currencies is a sign that something is very wrong with the monetary system.

It will likely badly impact many employment generating companies in the import and export sectors and is not good for the trading of goods and services internationally and for world trade. Trade and commerce, the backbone of the economy is being put at risk in order to protect the interests of banks and a dysfunctional banking, financial and monetary system. This is a simplification, but it is largely the truth.

The strength of the euro yesterday was counter intuitive and given the scale of manipulation in markets today may have been due to intervention. A collapse in the value of the euro during and immediately after Draghi’s speech would not be welcomed by monetary moderates – labelled hawks – in the Bundesbank, in Germany and elsewhere in Europe and indeed by savers and depositors throughout the monetary dis-union.

Stocks moved higher briefly prior to giving up gains as did bonds. This is likely due to Mario Draghi saying that he didn’t anticipate further rate cuts. Stock and bond markets are now hopelessly addicted to the cocaine of cheap money and currency debasement. Something that will not end well and bodes ill for these markets.

The ECB’s drastic action reeks of panic and was not the panacea that “cheap money” addicted banks and markets had hoped for.

“Insanity is doing the same thing over and over again and expecting a different result.” So said Albert Einstein and the ECB is in danger of not realising that its QE programme and ultra loose monetary policies are failing. You cannot print your way to prosperity and it may be slowly dawning on market participants that you cannot print your way out of deflation.

Markets remain subject to a weird combination of irrational complacency and significant denial. But beneath this comes a deepening concern amongst the smart money that the imbalances that brought the global financial system to its knees in the first financial crisis remain and are in many cases worse today.

There is a distinct whiff of 2008 in the air. However today, the belief in central banks as monetary saviours of the universe is increasingly in doubt. Indeed, there are real and growing concerns that they are contributing to the creation of much bigger financial bubbles with similar if not worse consequences.

The financial insurance that is physical gold has never been more important to own.

LBMA Gold Prices

11 Mar: USD 1,262.25, EUR 1,136.50 and GBP 883.03 per ounce

10 Mar: USD 1,247.25, EUR 1,137.04 and GBP 876.67 per ounce

09 Mar: USD 1,258.25, EUR 1,146.69 and GBP 884.16 per ounce

08 Mar: USD 1,274.10, EUR 1,155.69 and GBP 894.35 per ounce

07 Mar: USD 1,267.60, EUR 1,156.96 and GBP 896.13 per ounce

Gold News and Commentary

Gold Surges to One-Year High After European Stimulus – WSJ via Nasdaq

Gold Climbs to One-Year High as Dollar Weakens on ECB Rate View – Bloomberg

Gold rises more than 1 percent as euro rebounds on ECB comments – Reuters

Gold Rallies as Base Metals Slip Amid Dimmed ECB Growth Outlook – Bloomberg

Gold futures settle at 13-month high – Marketwatch

Draghi ECB Gamble – “It Is All Going To End In Chaos” – Telegraph

Europe Presses the Panic Button – Gilbert – Bloomberg View

The Germans React To Draghi’s Monetary “Tidal Wave” – Zero Hedge

The End? Draghi Fires His Bazooka And Markets Fall – Dollar Collapse

Largest Primary Silver Mine Productivity Falls To Lowest Ever – Silver Seek

Read more here

‘7 Real Risks To Your Gold Ownership’ – New Must Read Gold Guide Here

Please share our website with friends, family and colleagues who you think may benefit from it.

Thank you

END

Alasdair Macleod talks about gold as the only sound money:

(courtesy Alasdair Macleod/GATA)

Alasdair Macleod: Gold is the only sound money

Submitted by cpowell on Thu, 2016-03-10 18:28. Section: Daily Dispatches

1:28p ET Thursday, March 10, 2016

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod writes today that technical analysis of gold price trends is “notoriously fallible” and that the most important fundamental analysis of the gold price doesn’t involve gold itself but rather the steady debasement of government currencies. Macleod’s analysis is headlined “Gold Is the Only Sound Money” and it’s posted at GoldMoney’s Internet site here:

https://www.goldmoney.com/our-research/goldmoney-insights/gold-is-the-on…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Ambrose Evans Pritchard comments on yesterday’s ECB decision, basically saying the Euro zone is extremely worried on the mounting deflation heading its way:

(courtesy Ambrose Evans Pritchard/UKTelegraph)

Ambrose Evans-Pritchard: ECB’s Draghi plays his last card to stave off deflation

Submitted by cpowell on Fri, 2016-03-11 00:56. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Thursday, March 10, 2016

The European Central Bank has pulled out all the stops to avert a dangerous deflation trap, launching a blast of triple stimulus despite angry criticism from Germany that it is entirely unnecessary and will do more harm than good.

The markets reacted wildly to the package of measures, surging at first and then plummeting on creeping fears that the bank has exhausted its policy options and may be defenseless against a fresh shock.

Mario Draghi, the ECB’s president, no longer seems able to conjure confidence with his former panache. His magic has, for now, deserted him.

The ECB cut the deposit rate by 10 basis points to a historic low of -0.4 percent and stepped up the pace of quantitative easing from E60 billion to E80 billion a month. It buttressed the effect with unlimited four-year loans to banks at near-zero cost, hoping this will limit the damaging side-effects of negative rates for banks. …

… For the remainder of the commentary:

http://www.telegraph.co.uk/business/2016/03/10/ecbs-draghi-plays-his-las…

end

And now a great report on silver as Steve St Angelo takes on my nemesis Jeff Christian:

(courtesy Steve St Angelo/SRSRocco Report)

SILVER OUTBREAK: Investment Demand Will Totally Overwhelm The Market

Submitted by SRSrocco on 03/11/2016 15:11 -0500

![]()

It’s no secret to the precious metal community that silver is one of the most undervalued assets in the market, however 99% of Mainstream investors are still in the dark. This was done on purpose to keep the majority of individuals invested in Wall Street’s Greatest Financial Ponzi Scheme in history.

You see, this is the classic PUMP & DUMP strategy. Unfortunately, it’s not a lousy penny stock that Wall Street is pumping, rather it’s the entire market. Most pump & dump stock campaigns last a day, week or a few months. Sadly, this one has gone on for decades and the outcome will be disastrous for the typical American.

The problem is quite simple… there are way too many PAPER ASSETS floating around backed by very little PHYSICAL ASSETS. Or, let me put it another way. There are way too many DEBTS in the market masquerading as assets, while very few investors hold true STORES OF WEALTH.

And one of the best stores of wealth in the market is SILVER. Yes, gold is also another excellent store of wealth, but silver will outperform gold spectacularly when the Mainstream investor finally gets precious metal religion.

I was inspired to write this article due to a recent announcement by one of the well known silver analyst in the Mainstream and alternative media. Jeff Christian of the CPM Group made this statement which was reported in a recent Bloomberg article, Why Poor Man’s Gold May About To Get More Investor Love:

Not everyone is convinced.

“There’s a lot of bullishness forming around silver,” said Jeffrey Christian, managing director at New York-based CPM Group, a precious metals adviser. “We are of mixed minds. Silver is in surplus, plain and simple.”

Investors will only increase their purchases if there are more worrying economic, financial and political developments, Christian said in an e-mail dated March 3. CPM Group data on supply and demand show annual surpluses from 34 million ounces to 177 million ounces stretching back to 2006.

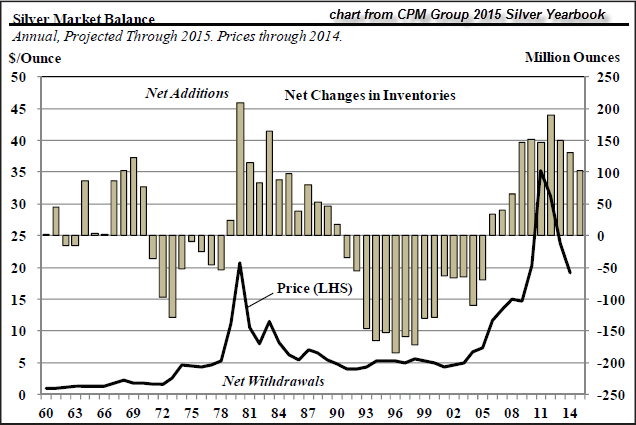

As many of you know, Jeff Christian’s CPM Group publishes the Silver Yearbook. According to their figures, the global silver market has enjoyed annual surpluses since 2006. Several of my readers forwarded this statement to me and asked me what I thought of it.

Here is the CPM Group’s chart showing annual silver surpluses since 2006:

Well, there you have it… the silver market did enjoy annual surpluses since 2006. Or did it?? If you were from the Mainstream media and you only read the CPM Group’s Silver Yearbook you would have been bamboozled by the data in this chart. Why? Because Jeff Christian’s CPM group cleverly OMITS silver investment demand from this calculation… LOL.

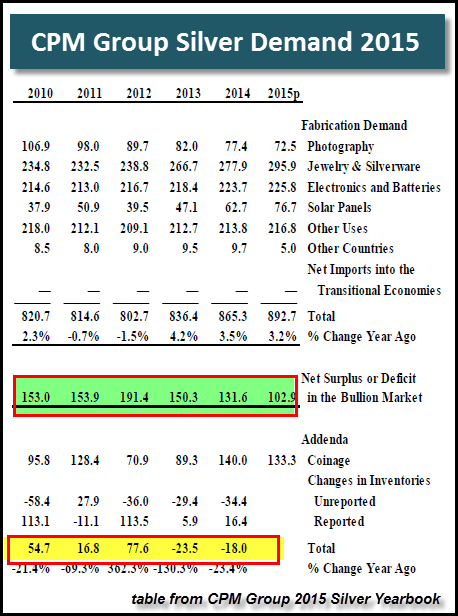

Here is part of the CPM Groups Silver Demand table showing how they arrive at their supposed surplus:

On the top is total supply, then they subtract out Photography, Jewelry & Silverware, Electronics & Batteries, Solar Panels and Other Uses to arrive at their surplus figure highlighted in green. They take that figure to make the annual silver surplus chart above it.

Then they QUIETLY subtract Official Silver Coin demand below it and make adjustments for changes in inventory. The figure highlighted on the bottom is the real annual net silver market balance. If we go by the CPM Groups figures here, they actually show a deficit for 2013 and 2014. How Mr. Christian can call this a surplus is beyond me.

You see, the CPM Group’s Investment calculation is titled as an “Addenda”. Why an addenda??? And where is Silver Investment Bar demand? I hate to say it, but CPM Group’s Supply & Demand figures receive a POOR GRADE compared to the data put out by the GFMS Team at Thomson Reuters who publishes the World Silver Surveys.

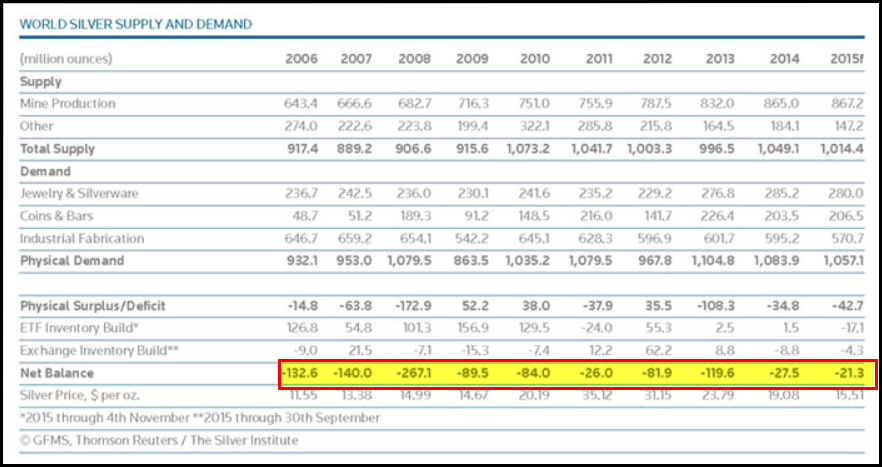

According to the Silver Institute news release on the Silver Interim Report, the GFMS Team at Thomson Reuters published the following Silver Supply & Demand table:

As we can see, they do a much better BANG UP job with their data by also subtracting Silver Bar & Coin demand from their total supply figures. Then first arrive at an annual Physical Surplus or Deficit. I didn’t highlight this but it’s located right below total Physical Demand. Once they get that figure they adjust for any ETF or Exchange Inventory Build, positive or negative. Lastly, they end up with a NET BALANCE which is highlighted in yellow.

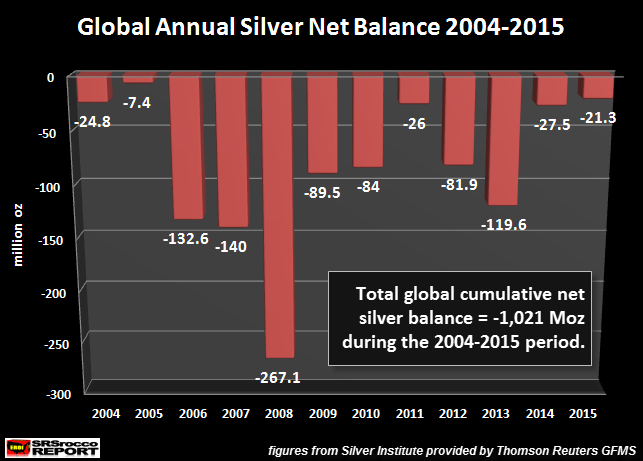

This is the true overall surplus or deficit figure for the silver market. As we can see, the GFMS Team shows annual silver deficits as far as they eye can see. Okay at least for the past decade. I took these figures and made the chart below (also included data for 2004):

So, if we are going to use real professional data, the silver market suffered a 1 billion oz net deficit since 2004. How Mr. Christian can say, “The silver market is in surplus” is beyond me. Of course Jeff Christian is probably guilty of using semantics in his official statements to the press. There is probably some excellent reason why Mr. Christian tends to ignore silver investment demand in his surplus-deficit figures and is more negative about silver than other analysts. However, we can plainly see from the data above, Jeff Christian is most certainly talking out of a different part of his body than the folks at GFMS.

Sorry to be blunt here, but the evidence proves who the guilty party is here.

SILVER OUTBREAK: Investment Demand Will Totally Overwhelm The Market

Some readers may think that is a hyped title. Sure, it may be… but it’s true. I have said countless times in articles and interviews that investment demand will be the driving force for silver price in the future, not industrial demand.

Jeff Christian tends to harp on industrial demand.

Yes, it’s true… industrial demand has been falling and WILL CONTINUE TO FALL. According to the figures by the GFMS Team, industrial silver demand was 645 million oz (Moz) in 2010, but has fallen to 570 Moz in 2015. Sure, that might include the falling Photography demand, but that’s part of industrial consumption. And remember this, a lot of silver used in photography is recycled. So, as silver photography demand declines, so does the amount of recycled silver.

So once again, for all of the Mainstream silver analysts out there… forget about INDUSTRIAL SILVER DEMAND as a determining factor for price going forward. It’s a non issue. The key will be investment demand and I have a chart to prove it:

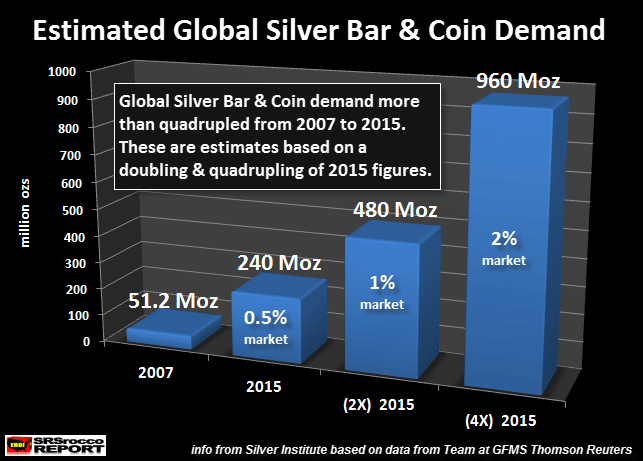

According to the data by the GFMS Team, total Silver Bar & Coin demand was a paltry 51.2 Moz in 2007. This surged after the U.S. Investment Banking & Housing Market collapse to 240 Moz in 2015. While GFMS reports a total of 206 Moz for Silver Bar & Coin demand, they do not include private rounds and bar demand.

In an email exchange with the GFMS Team, they told me that getting figures for private silver rounds and bars was quite difficult. However, they were working on a system and would be publishing this figure in the future. They “unofficially” stated in the email that estimated private silver rounds and bars was likely 30-40 Moz in 2015. This is how I came up with the 240 Moz figure shown in the graph above.

In discussions with many analysts, I came up with a figure of 0.5% of the market was buying silver. Official estimates put the figures of global precious metal buying at approximately 1%. So, in all reality… global silver buying is probably less than 0.5%. But, let’s just use that figure as a ballpark.

So, once the world starts to wake up to the fact that they are the BIGGEST PAPER BAG HOLDERS of increasing worthless paper assets, there will be a mad rush into the silver market. Thus, if we had just a doubling to 1%, it would be 480 Moz of physical Silver Bar & Coin demand. And a quadrupling of 2015 demand would equate to 960 Moz. Just think about how that would impact the annual surplus-deficit figure… LOL.

I actually believe just a doubling to 1% and 480 Moz of physical Silver Bar & Coin demand would totally overwhelm the market. Why? Because I haven’t even included the huge inflows from the Mainstream Investors. The same Bloomberg article linked above published the chart called Silver Hoarding- ETF Demand:

As we can see, global Silver ETF’s added a whopping 500 metric tons in the past several weeks. That turns out to be 16 Moz. I would imagine Mr. Christian will also omit this data when he regurgitates his 2016 silver surplus figures next year.

I believe the reason Christian suggests that the silver markets has been in a surplus because he doesn’t see investment as true demand like industrial consumption. Most of industrial silver is lost forever, while a Silver Eagle coin is likely held in private hands waiting for the opportunity to sell it at a much higher price. However, most physical silver investment is being held TIGHTLY and will enter back into the market because its owners realize the Global Financial System will get flushed down the toilet when the Central Banks lose control.

While we have no idea if all of this silver is actually being deposited at these ETF’s, it is a sign that the Mainstream investor has a lot of leverage in the market. Actually, the Mainstream investor has more leverage because they comprise 99% of the market while the precious metals investor is 1%.

It makes a great deal of sense why the Fed and Wall Street continue to downplay gold and silver. Because a small percentage switch of investors into these metals would totally overwhelm the market and price.

Fortunately for precious metals investors, this is only a matter of time. While Ponzi Schemes can go on for many years, they all end in a disaster. The present insanity and extreme volatility in the markets provides us a clue that the END maybe coming a lot sooner than we realize.

Please check back for new articles and updates at the SRSrocco Report. You can also follow us at Twitter below:

![]()

end

:

1 Chinese yuan vs USA dollar/yuan UP to 6.5003 / Shanghai bourse IN THE GREEN, UP 5.58 OR 20.20% : / HANG SANG CLOSED UP 215.18 POINTS OR 1.08%

2 Nikkei closed UP 86.52 OR 0.51%

3. Europe stocks ALL IN THE GREEN /USA dollar index UP to 96.34/Euro DOWN to 1.1102

3b Japan 10 year bond yield: RISES TO +.005% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.75

3c Nikkei now JUST below 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 37.01 and Brent: 40.34

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES to 0.303% German bunds in negative yields from 7 years out

Greece sees its 2 year rate FALL to 7.84%/:

3j Greek 10 year bond yield FALL to : 9.26% (YIELD CURVE NOW BACK TO BEING DEEPLY INVERTED)

3k Gold at $1265.60/silver $15.55 (7:15 am est)

3l USA vs Russian rouble; (Russian rouble UP 1 AND 97/100 in roubles/dollar) 69.77

3m oil into the 38 dollar handle for WTI and 40 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9867 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0955 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN STARTS ITS CAMPAIGN AS TO WHETHER EXIT THE EU.

3r the 7 year German bund now in negative territory with the 10 year RISES to + .303%

/German 8 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.87% early this morning. Thirty year rate at 2.66% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets Surge After Traders “Reassess” ECB Stimulus

Three months ago, on December 4, when the ECB clearly disappointed markets and European stocks tumbled as the Euro soared, it took a speech by Mario Draghi at the Economic Club in NY to send stocks soaring…

… when Draghi explained that the ECB’s announcement was not at all “disappointing”, and subsequently held this exchange with former BOE head Mervyn King who asked “was today’s speech deliberately designed to try offset some of the reaction yesterday?” to which Draghi responded “Not really… well, of course.” As shown in the chart above, stocks promptly soared if only briefly.

Fast forward to the price action over the past 24 hours, when markets again stumbled into a world of mayhem after stocks first soared and the EUR tumbled, only for the move to reverse itself after Draghi hinted that there would be no more rate cuts. The markets clearly ignored the fact that at the same time, Draghi announced a far more important expansion of QE, one including corporate bonds to unclog what had been a largely blocked bond issuance pipeline together with 4 TLTROs which would end up paying banks to lend money.

It took a while, but market participants got it: “Draghi made the mistake of essentially saying that the ECB was done with stimulus, and the market overreacted to this,” said Teis Knuthsen, CIO at Saxo Bank’s private- banking unit. “At the end of the day, the ECB delivered more than expected and is pumping a lot of money into the system. A few years ago this would have marked the start of a significant rally, but now there seems to be a widespread fatigue with monetary policy.”

Maybe, but not today, because the result has been that after “reassessing” – in Bloomberg’s parlance – what the ECB did, following yesterday’s plunge, risk has soared overnight with both Asian and European stocks surging, sparing Draghi the indignity of having to explain why he did what he did, and that it was all to prop stocks higher. Sure enough, as of this moment European bourses are all broadly higher led by banks, with the DAX and FTSE both up over 2.7%, while the Stoxx 600 is higher by 2.3% as of this writing.

Nowhere is the return of euphoria clearer, however, than in bank stocks, which as seen below are soaring.

Still, as Bloomberg notes, despite today’s advances, European equities are heading for their first weekly drop in four, with the Stoxx 600 down 0.6 percent. Commodity producers, automakers and banks – the most battered in the recent selloff – had led a 13 percent rebound from February’s low through a five-week high on March 4. As of yesterday, the index traded at 14.6 times estimated earnings, still far below the 16.7 multiple reached last April.

As Bloomberg adds, “investors have had to deal with increased volatility this year, and Thursday’s market reaction exemplifies a trend that’s been intensifying in recent months: central banks are increasingly powerless when it comes to calming markets. The Euro Stoxx 50 Index of the biggest euro-area companies moved more than 5 percent intraday, its wildest swings since August, and the most on an ECB day since 2011. A measure of volatility expectations increased for four straight days, its longest streak this year. It tumbled 10 percent on Friday.”

For now, the markets have contained the damage, filling yesterday’s gaps on what still remains the ECB’s kitchen sink. The question remains where will the incremental stimulus come from?

Elsewhere, oil is higher by over 2% after the latest reported by the IEA which predicted that oil prices may have finally bottomed.

In any case, this is where the markets stand currently:

- S&P 500 futures up 1% to 2000

- Stoxx 600 up 2.3% to 341

- FTSE 100 up 1.5% to 6126

- DAX up 2.7% to 9757

- German 10Yr yield down 3bps to 0.28%

- Italian 10Yr yield down 11bps to 1.35%

- Spanish 10Yr yield down 8bps to 1.51%

- MSCI Asia Pacific up 0.7% to 126

- Nikkei 225 up 0.5% to 16939

- Hang Seng up 1.1% to 20200

- Shanghai Composite up 0.2% to 2810

- S&P/ASX 200 up 0.3% to 5166

- US 10-yr yield up 1bp to 1.94%

- Dollar Index up 0.54% to 96.59

- WTI Crude futures up 2.7% to $38.87

- Brent Futures up 2.2% to $40.95

- Gold spot down 0.5% to $1,265

- Silver spot down 0.1% to $15.58

Top Global News

- JPMorgan Said to Cut Credit Traders Amid Emerging-Market Swings: Bank cut several EM credit traders, including global head Robert Milam, due to volatility in asset class.

- United Technologies Weighing Acquisitions in Fire, Aerospace: “I wouldn’t be afraid to do a big deal, but it’s got to be something that’s actionable,” CEO Gregory Hayes said.

- Yahoo’s Mayer Hopes to Stay in Job Even If Changes Hands: Under pressure from investors, facing potential proxy fight, CEO Marissa Mayer has pledged to do what’s best for shareholders.

- Buffett’s Gen Re Shuts Operations in Hong Kong, Melbourne:

Reinsurer said it’s exiting property-casualty operations at 6 smaller locations amid a global reorganization. - AmEx Targets Loan Growth as Rivals Cut Fees in Partnerships: Focus on financing may help co. bolster revenue amid increasingly aggressive bidding on deals with retailers, airlines that bring in customers, fee-generating spending.

- Trump Embraces Unity; Bats Away Rivals in Subdued Debate: Final four candidates for Republican nomination mostly got along during the first half of the latest debate.

- Apple Announces March 21 Event to Update Smaller IPhone: Co. will introduce updated iPhone with 4-inch screen: person familiar.

- Oil Price May Have Bottomed as High-Cost Output Falls: IEA: Non-OPEC production to decline by 750kbbl/d this year, higher than last month’s est. by 150kbbl/d.

- Iron Ore Sags Toward $50 as ‘Insane’ Advance Gets Rolled Back: Analysts said that price leap at start of week simply wasn’t justified given poor fundamentals.

Looking at regional markets, we start as usual in Asia, where equity markets shrugged off the early dampened sentiment triggered by comments from ECB President Draghi that signalled a possible end to the ECB’s rate cut cycle, with the region recovering as it digests ECB’s looser policy and gains in oil prices. ASX 200 (+0.3%) and Nikkei 225 (+0.5%) were initially led lower by the energy sector, but then rebounded in late trade as oil re-approached 3-month highs, while Japanese stocks were also supported as JPY pared some of yesterday’s strength. Shanghai Comp (+0.2%) was also pressured at the open following a consecutive net weekly drain by the PBoC and a 3rd straight decline in margin trading, before reversing alongside the regional improvement in risk-tone. 10yr JGBs traded lower following spill-over selling in T-notes with demand also subdued amid recent volatility in Japanese bonds. The PBoC injected CNY 20bIn via 7-day reverse repos for a net weekly drain of CNY 205b1n vs. CNY 840b1n drain last week; PBoC set the CNY mid-point at 6.4905 vs. last close. 6.5075 (Prey. mid-point 6.5127); its strongest reference rate YTD.

Top Asian News

- Yuan Erases 2016 Drop as PBOC Raises Fixing Most in Four Months: Move follows advance in euro after Draghi’s says he didn’t see need to cut rates further

- Hong Kong Regulator Bans Hedge Fund Matchpoint Founder Raaj Shah: Shah failed to disclose all his personal trading accounts in line with firm’s policy

- BSI Singapore Banker Involved in 1MDB Investigation Leaves: Yak’s financial accounts were frozen as part of probe related to a Malaysian government fund

- China Said to Plan New Rules Facilitating Debt-to-Equity Swaps: Central bank and country’s top economic planning agency are tasked with outlining rules

- Hedge Fund Effissimo Ups Ante, Buying 25% of Japan Shipper: Kawasaki Kisen Kaisha shares have dropped almost 40% in past year

- Cyberdyne Plans Nasdaq Listing Next Year for U.S. Expansion: Maker of robot exoskeletons for physical therapy aims to boost its investor base

- Hedge Funds Bet on the Decline of Japanese Technology Giants: Oxford, Vinva and Stats among funds shorting technology stocks

In Europe, this morning has very much had a feel of ‘the day after the night before’, with markets continuing to feel the fallout from yesterday’s ECB meeting but with little other newsflow guiding price action. In tandem with the bazooka released by Draghi and Co. yesterday, European stocks trade significantly higher today (Euro Stoxx: +2.5%), with the FTSE and SMI underperforming given the lack of direct impact from the ECB action . Financials outperform today on a sector specific basis, with particular outperformance in the periphery from the typically volatile Italian banking names. Elsewhere, Bunds are also benefitting from the ECB action yesterday with the German benchmark higher today and back above 161.50, while the periphery remaining tighter today in light of the new easing measures.

Top European News

- Old Mutual to Be Broken Up as CEO Hemphill Chases Growth: Co. to split into 4 units.

- Deutsche Bank Sees Industry-Wide Trading Revenue Drop in 2016: Securities firms will see debt trading revenue fall “slightly” from a year earlier; Deutsche Bank Cuts Bonus Pool 11% to Spreads Legal Costs

- ArcelorMittal to Sell Stock at 2.20 Euros in $3b Offering: Co. will sell seven new shares for every 10.

- Porsche Profit Rises 25% to Record as Macan SUV Lifts Sales: Revamp of brand’s 911 segment, robust demand for its SUVs should help Porsche meet its 15% operating profit margin target in 2016.

In FX, some temperance seen in EUR/USD this morning, with the 1.1200 breach yesterday topping out some 17 ticks through the figure but seeing profit taking bringing us back into low 1.1100’s — briefly dipped below here. No major recovery seen as the USD index is edging higher tentatively, but what we did see is some notable EUR/GBP sales going through to lift Cable back to 1.4300, with a view to testing the Thursday highs at 1.4317. UK trade data saw the headline deficit narrowing — this the only reason we could see for sudden GBP focus. Elsewhere, USD/JPY is looking to 114.00 again, but we ran into strong resistance ahead of 114.55 Thursday, so we may see a little struggle up here, but will need a strong stock market performance to do so. USD/CAD is back testing the 1.3220 level, with Oil eyeing $39.0. Canadian jobs data later on today. AUD/USD through .7500 again, but momentum has faded here of late.

In commodities, oil markets are still trading at a relatively high levels as Brent stays above USD 40bbl with WTI above USD 38bb1 respectively with the spread differential tightening over the last 24 hours. Gold has been retracing after gains following the ECB rate decision and press conference. Base metals have all been trading slightly lower with many analysts touting profit taking after recent rallies. IEA have said that monthly production dips on outages in Iraq and Nigeria and Iran’s market return more modest than forecast. World oil demand was revised to 94.6m from 94.4m bpd by the EIA. And they have also commented on the price of oil saying it may have bottomed out as high cost producers have cut production. (BBG/RTRS)

This afternoon in the light US calendar we get the February import price reading due up. There’s little in the way of Central Bank speakers today, while the latest Baker Hughes rig count will be closely watched in the commodity space.

Bulletin Headline Summary from RanSquawk and Bloomberg

- Markets continue to digest yesterday’s ECB-inspired mayhem with European equities trading higher across the board in a pull-back of some of Thursday’s losses

- Some temperance seen in EUR/USD this morning, with the 1.1200 breach yesterday topping out

- some 17 pips through the figure but seeing profit taking bringing us back into low 1.1100’s

- Looking ahead, highlights include US Import Price Index, Canadian Net Change in Employme

- Treasuries slightly lower, global equity markets and U.S. futures rally overnight “as traders warmed to President Mario Draghi’s policy measures;” economic data calendar today features Import Price Index.

- Whether Draghi’s latest barrage of stimulus works or not, the ECB president made one thing clear: he won’t be the one to clean up afterward. Instead, ultra-low interest rates are now potentially locked in until after he retires in 2019

- ECB’s new series of TLTRO will be a welcome boost to liquidity for Spanish lenders that have been among the largest users of these programs so far. They have collectively drawn more than €74 billion ($82 billion) from previous rounds, just behind Italian lenders that have taken €97.2 billion

- Deutsche Bank, which runs Europe’s biggest investment bank, said it expects the industry’s revenue to decline this year as clients consider pulling back from trading some fixed- income securities and refrain from doing deals; The bank also cut its bonus pool by 11% after rising legal expenses hurt earnings last year and said volatility in financial markets means the first quarter may be challenging

- Investment banks worldwide have been cutting jobs in recent months as stock-market turmoil and a slowing Chinese economy put the brakes on dealmaking and trading

- The world’s largest banks are incorrectly accounting for their swaps trades, locking up money that could otherwise be paid out as dividends to their shareholders, according to a bold new academic paper

- Italian industrial output rose more than twice the economists’ forecast in January to 1.9% from December, which registered a 0.6% fall, signaling that the pace of economic growth may accelerate in the coming months

- Sovereign 10Y bond yields mostly lower, led by Greece (-15bp), Italy (-13bp) and Spain (-10bp); European, Asian equity markets higher; U.S. equity-index futures rise. WTI crude oil, copper rise, gold drops

US Event Calendar

- 8:30am: Import Price Index m/m, Feb., est. -0.7% (prior -1.1%)

- Import Price Index y/y, Feb., est. -6.5% (prior -6.2%)

DB’s Jim Reid concludes the overnight wrap

With regards to the price action which ensued, the most impressive way to show the sheer swing in sentiment is by detailing some of the massive high to low ranges after that early rally faded fast. The Stoxx 600 peak-to-trough amounted to 4.07%, with the index eventually closing -1.66%. The range on the DAX was 4.98% and the closing level -2.31%. Peripheral bourses were actually the relative outperformers from an equities perspective, although that also reflects the fact that they rallied so hard on the initial headlines. The FTSE MIB closed -0.50% but not without a 4.69% range, while the IBEX (+0.07%) actually closed just in positive territory, again with a large 3.70% range however. European Banks were at the centre of the volatile moves with the Stoxx 600 Banks Index closing -0.52% and out-performing but the daily range amounting to 6.00%. It’s worth noting that we’ve also added an update piece from our European Banks team at the end of the report touching on some potential impacts for the sector post the announcements.

Elsewhere, the moves for the Euro seemed to cause some of the greatest debate. The single currency initially weakened over 1.5% in the minutes post the news, touching a low of 1.082 (and the lowest since the start of February) before then staging one heck of a rebound to rally off the lows and finish up +1.62% on the day at 1.118. The intraday high-to-low range of 3.66% lower than what we saw on December 3rd last year (when the ECB ‘under delivered’) but still the 10th highest daily range that we’ve seen in the currency in the last 10 years (especially impressive when you consider some of the massive swings in 2008/09 which account for seven of the top ten).

Rates markets were in major reversal mode too. 10y Bund yields initially tumbled 8bps lower to strike an intraday low of 0.156%, before spiking higher and closing at 0.304%, up 6.4bps on the day but the high-to-low range an impressive 17bps. Unsurprisingly moves in the peripheral bond market were even more exaggerated. 10y BTP’s were as much as 18bps lower on the day but closed 5bps higher with a range of 24bps. 10y Portugal yields actually closed 3bps tighter but again not without a 33bp range.

Along with the Euro, it was credit markets which were the other big outperformer on the day which is unsurprising given the news of the inclusion of corporate bonds in the ECB’s expanded asset purchases. The iTraxx Main index was as much as 12bps tighter at one stage before paring a bit of that into the close to finish 7bps tighter. Crossover ended 18bps tighter although again was a huge 40bps tighter at its best. Senior and Sub iTraxx financials closed 7bps and 17bps tighter respectively with the peripherals names leading the charge.

The inclusion of non-financial corporate bonds was a surprise and it marks another landmark moment for the ECB. This is the first time they’ve entered the private unsecured market. Longer term this might be significant as it paves the way for other non-government or unsecured risk purchases at a later date. For now we’ll have a good 3 months of speculation as to what they might buy and how successful they’ll be. In the note my team have just published we take a look at what the potential universe looks like, as well as discuss how the ECB’s market of eligibility could grow through looking at issuance, redemptions and net issuance trends over the past decade or so. Ultimately we expect ECB purchases to be positive for IG credit, although clearly there is still a certain amount of execution risk, while the liquidity of the market is also a big consideration. Experience from ABS purchases has not been great but whatever the risks from a performance/liquidity perspective it’s hard to imagine investors wanting to be short corporate bonds at least until the program starts in a few months or until more details are known.

Back to the bigger picture. Overall perhaps the eventual negative market reaction was due to the increasing realisation that this meeting might mark the point where focus shifts from easing being solely for the financial markets to one where it’s aimed at improving credit in the economy. By association this may explain the significant rally in the Euro as markets feel that the game of trying to weaken the currency is shifting. Elsewhere if the sell-off in core rates yesterday reflected reflation then this would have been a positive. However the move in breakevens didn’t suggest that this was the case so one has to be a bit concerned at the move. As a last word, clearly one has to be skeptical as to whether the package will work for the wider economy but it terms of having a go it’s hard for us to say that it’s not an impressive attempt.

It’s a rare occurrence – this year at least – for us to mention this so far along, but a selloff for oil markets (WTI -1.18%, Brent -2.48%) also coincided with the timing of Draghi’s negatively perceived comments and so certainly contributed to some of that risk-off move. That said, a bit of a rebound into the close for energy did eventually result in US equities bouncing off their lows to finish pretty much unchanged by the close of play (S&P 500 +0.02%), with US credit markets (CDX IG -5bps) enjoying similar gains to those in Europe.

This morning in Asia we’ve seen bourses rally back after an early weak opening which saw most markets open in the red. A big reversal for Oil (which has wiped out yesterday’s losses) has seen the Hang Seng (+1.06%), Shanghai Comp (+0.29%), Kospi (+0.28%), ASX (+0.32%) and Nikkei (+0.76%) all move back into positive territory. Market have also seemingly put to one side the latest CNY fix which was strengthened (+0.34%) by the most since November. Elsewhere credit markets are playing catch up in Asia this morning with iTraxx Asia and Australia indices 7bps and 5bps tighter respectively.

Before we look at today’s calendar and away from the ECB focus, labour market data in the US continues to remain supportive with last week’s initial jobless claims falling 18k to 259k (vs. 275k expected) and a new five-month low. Prior to this we saw Germany report a shrinking in their trade surplus in January, aided by an unexpected fall in exports (-0.5% mom vs. +0.8% expected). Finally in France the January industrial production print was up a much better than expected +1.3% mom (vs. +0.8% expected).

Looking at the day ahead, today we begin in Germany where shortly after this is out we’ll receive the final revision to the February CPI print (no change from the +0.4% mom expected). That’s before we turn to the UK where we’ll see the January trade numbers. This afternoon in the US the calendar continues to remain light with just the February import price reading due up. There’s little in the way of Central Bank speakers today, while the latest Baker Hughes rig count will be closely watched in the commodity space.

It’s worth keeping an eye out on some important China data over the weekend too (Saturday morning to be specific) where we’ll get the February industrial production, retail sales and fixed asset investment data. If that wasn’t enough, we’ll also hear from PBoC Governor Zhou tomorrow morning who is set to hold a press conference on ‘financial reform and development’. And if that still wasn’t enough, three regional elections in Germany this weekend will also prove an early test for German Chancellor Merkel’s refugee policy. Expect all this to help set the tone for the open on Monday.

Let us begin;

ASIAN AFFAIRS

Late THURSDAY night/ FRIDAY morning: Shanghai closed UP BY 5.58 POINTS OR 0.20% , / Hang Sang closed UP by 215.18 points or 1.08% . The Nikkei closed UP 86.52 or 0.51%. Australia’s all ordinaires was UP 0.14%. Chinese yuan (ONSHORE) closed UP at 6.5003. Oil GAINED to 38.68 dollars per barrel for WTI and 40.70 for Brent. Stocks in Europe so far ALL IN THE GREEN RESPONDING TO THE OIL RAMP UP. Offshore yuan trades 6.4976 yuan to the dollar vs 6.5003 for onshore yuan/ LAST WEDNESDAY, MOODYS DOWNGRADES CHINA’S CREDIT FROM STABLE TO NEGATIVE. At the big people’s congress where they meet to set a 5 year plan, the leaders failed to deliver a major fiscal stimulus package

.

report on Japan

Two days ago we witnessed panic buying into the Japanese 10 year bond sending yields down to negative 0.10%. Last evening it was panic selling which again caused a flash crash as yields rose to +0.003%.

Japanese Government Bond Futures Are Flash-Crashing (Again)

Remember that once-in-a-lifetime, “don’t worry there’s plenty of liquidity” flash-crash in japanese Government Bond futures on Tuesday night (Wednesday morning Japan time)… well it happened again…

JGB Futures to be halted any minute…

And so the market chaos even among the “safest” of securities, the result of central bank intervention, continues. Bloomberg’s Richard Breslow summarized it best:

Even with QEs creating what look an awful lot like bubbles, it’s been fair to say, those distortions reflected the reaction function of how central bankers interpreted the state of play. Yield levels, let alone negative rates, and volatility are making these guideposts increasingly questionable.

If you look at the yield curves of much of the world, you’d be hard pressed not to conclude we are very much still experiencing a severe global recession. Central bankers may strongly disagree, yet Japanese 10-year JGBs haven’t seen 2% this century. German bunds have backed up to 21bps. Both are likely to increase QE. The U.S. is tightening (?) and 10- year yields are still down 42bps on the year

The Fed wants to raise rates but insists on re-investing the take on its massive portfolio. They act like fund managers protecting their AUM.

The Osaka Stock Exchange had to invoke circuit breakers today on the March JGB future for excessive volatility. Buying panic yesterday to front-run today’s QE buying led to panic selling today into BOJ bids 22 bps through Monday’s close. Oh, and did I mention, ahead of an auction tomorrow. The take-away is mayhem, not analysis.

And now we look forward to an even greater surge in volatility first ahead of the Fed and BOJ next week, who – just like everyone else – have no idea what is going on any more.

Tonight’s debate comes just five days ahead of the next week’s “Super Tuesday 3,” when there are more than 350 delegates up for grabs, including in winner-take-all contests in Florida and Ohio.

Some wonder just who it is that is selling JGBs so aggressively and in such entirely economically irrational a manner? Well we got hints who has been dumping Bunds from Goldman recently, which makes us think, as MNI ‘hints’ at, if The BoJ is not trying to “Goldilocks it”…

BOJ officials recognize that any upward pressure on JGB yields stemming from a brighter view on economic growth and inflation would be impeded by the BOJ’s massive purchases of JGBs, which also have been restricting risk premiums.

But some of them worry that the drop in the 10-year yield into negative territory may reflect undue pessimism by market players.

Just how much the negative yields are influenced by that pessimism and how much by the BOJ bond buying can’t be determined.

At this point it is also unclear how a gradual return to a steeper yield curve will happen, although BOJ officials must assume it will. It may be that changing sentiment in the market will be enough to overpower the other factors and begin to push up yields.

If it isn’t, things may become much more complicated, since it would then take some move toward an unwinding of the BOJ’s bond-buying policy to shift yields, and that would bring officials uncomfortably close to a knife edge of trying to edge up yields without making them spike.

In other words – rates not too low (or signals pessimism for growth) and not too high (because the entire fiscal balance will implode) – good luck centrally planning that.

report on China:

\

Points of interest: because China is focusing on a basket of currencies instead of just the USA dollar, the offshore yuan has just jumped 300 basis points to 6.494 and its strongest level since mid December. Gold is rising and at 9 pm est it is trading at 1278. Goldman Sachs is within 13 dollars of being stopped out of its gold contracts.

Goldman Is About To Be Stopped Out Of Its Gold Short

Given China’s new focus on a basket of currencies, rather than pegging to the dollar alone, today’s record-breaking reversal in EUR has sparked a yuuge 300 pips rally in Offshore Yuan (from 6.5270 to 6.4940) pushing to its strongest level since mid-December. At the same time, Gold is accelerating as China opens, pushing up to $1278 – new 13-month highs.Most critical is we are within $5 of Goldman Sachs “short gold” stop at $1291…

Yuan surges to 3-month highs…

As Gold spikes to fresh 13-month highs…

Goldman went short gold on 2/15 at around $1205…

We also maintain our bearish view on gold that has rallied along with the other commodities. Our short gold recommendation (which we opened with a 17% upside, in line with our $1000/toz 12-m forecast) is currently at a c.5% loss, with a stop loss at 7%.

This gold rally was driven by a lack of conviction in divergence in US growth as a weak US dollar has been highly correlated with a higher gold price.

We believe this realignment view of weak global growth is not supported by the US data, which will likely reinforce higher US yields, a stronger US dollar and the return of divergence, particularly should strong US consumer growth dissolve market fears regarding US growth. This in turn will likely put downward pressure on gold prices towards our near-term target of $1100/toz

Tonight we are getting very close to Goldman’s stop-loss…

Leaving Goldman clients pensive…

end

For 18 months in a row, USA import prices have fallen year over year. However we are beginning to see the first rise in prices since May 2014. China is still exporting its deflation to the entire globe:

(courtesy zero hedge)

China Exports Most Deflation To US Since 2010

For the 18th month in a row, US Import prices fell YoY (down 6.1% vs expectations of a 6.5% drop). This is the longest deflationary streak since 1999. Under the hood we see the first first rise in prices (ex food, fuel) since May 2014. Fuel price dropped 3.9% – the 8th consecutive drop – and foreign food product prices dropped 2% – the most since Feb 2012. Perhaps most crucially, China’s forced deflationary wave continues to build with the index at its lowest since 2010.

Longest losing streak since 1999…

With China exporting deflation at the fastest pace since 2010…

The Labor Department’s accompanying cheat sheet for reporters repeated the phrase “The index has not recorded a monthly increase since…” ten times. The range of sustained declines ranged from March 2014 for non-petroleum imports, to September 2015 for natural gas

Charts: Bloomberg

After January Scramble, Chinese Lending Collapses

After January’s record-smashing CNY3.4 trillion (half a trillion dollars!) surge in aggregate credit expansion in China, the post-lunar-new-year hangover hit hard in February as credit growth tumbled 77% from Janaury’s level to just CNY780 ($112bn). This is the weakest February loan growth since 2011. Drastically missing expectations, and following authorities comments on the need to “monitor” excess credit growth, all categories of total social finance registered a sharp drop.

After a huge spike in loan growth in January (which appeared to have absolutely no marginally positive impact on any real economic data)…

China total loan growth collapses….

As it appears massive amounts of loan issuance were pulled forward (before the new year), promptingthe People’s Bank of China to crack down on excess lending at some banks always making the slump in February a possibility. But as Bloomberg notes, looking at the data for the first two months of the year together, credit growth remains on a rapid upward trend, and the government is targeting a faster credit expansion for 2016 as a whole. Industrial output data for January and February, slated for release Saturday, will be critical in determining the immediate policy outlook.

In the details of today’s data release, all categories of total social finance registered a sharp drop. Yuan bank loans fell to 810 billion yuan in February from 2.5 trillion yuan in January. Corporate bond issuance fell to 86 billion yuan from 454 billion yuan. Bankers acceptances dropped 370 billion yuan, after registering a 130 billion-yuan increase in January. Trust loans and entrusted loans, the other major “shadow banking” categories, fell from January’s level but remained in positive territory.

Goldman Sachs explains…

February credit data was weak. Part of the fall in the level of credit supply was because of seasonality — February credit supply is always substantially lower than that in January. However, normal seasonality certainly cannot explain the magnitude of the fall, as the level of RMB loans last February was only around Rmb 500 bn less than that in January. Another perspective on seasonality is to compare this February with last. Since the outstanding loan growth rate is in the teens, the newly increased amount is normally larger than that of the same month the prior year–but this February’s level is clearly below last year’s, pointing to factors other than seasonality as playing an important role. TSF flows were weak, although there was around RMB 167 bn net issuance in local government bonds in February. After adjusting for local government bonds, TSF growth was still relatively weak, with sequential (month-over-month) growth at the lowest level since mid 2015. Among the components under TSF, bank acceptance bills declined RMB 371 bn, which likely reflected the impact from discount bill frauds that surfaced in late January.

However, sequential M2 growth accelerated in February. Fiscal policy stance was supportive, although not quite as supportive as February last year, and FX flows likely became less of a drag.

The weakness in February credit data was policy driven, in our view, and should be viewed in light of exceedingly strong January data. Although the government likely wanted to loosen policy in light of renewed downward pressures on growth, which are due in large part to weak exports, the actual amount of loosening in January may have breached policymakers’ comfort zone (consistent with reports on PBOC guidance to slow lending in mid January).

Concerns about rising CPI inflation, leverage and public perception remain key constraints on the extent of monetary policy loosening. Although doves tend to dismiss the rise in CPI inflation, which has been mostly food driven, as driven by temporary factors especially adverse weather conditions, hawks may view it differently as the result of the very loose monetary conditions in January. Historically, China’s CPI inflation is almost always mainly food driven and its behavior is very pro-cyclical, contrary to that in many developed economies. As food prices continue to be high in March, CPI is likely to remain at above 2% in March, in our opinion, limiting the extent of short-term policy loosening. There also is a rising number of media comments on policy stance questioning whether the high credit growth in January is turning out to be another Rmb 4 trillion stimulus, which may make the case for loosening more difficult for policymakers who are in favor of this.

Strong January money and credit data led to overly high market expectations about future liquidity supply, which likely gave domestic equity market and commodities market a boost recently. Today’s downside surprise may raise questions about whether the government still intends to loosen. Our view is it still does, just not as aggressively as it appeared after the release of January data. The combined level of liquidity supply in the first two months of the year was still around RMB 700 bn, higher than during the same period of last year, which should support domestic demand growth, especially fixed asset investment, and partially offset the weakness in external demand. While the problem of “policy laziness” (a phrase coined by PM Li to describe the lack of action by officials tasked with implementing stimulus) certainly has not been eliminated, the severity likely has lessened amid heightened administrative pressures from the leadership. Aggregate demand growth on the other hand likely weakened from the high level reached in November and December (based on IP sequential growth). As such, we think reaching the annual GDP growth target of 6.5-7.0% will be a challenging task and will require continued policy support, including monetary policy.

What is potentially most troubling is that despite all this yuuge issuance and declining credit quality, yields on China corporate bonds continue to compress in the biggest bubble that no one is talking about…

And as Bloomberg concludes, the signals from China’s policy makers remain somewhat confused.Ahead of the National People’s Congress, the PBOC flagged a shift to a “slight easing bias” in monetary policy. In the last few days they have appeared to try to row that back, saying the “prudent” policy stance remains essentially unchanged. That said, a target for 13% growth in M2 in 2016, up from 12% in 2015, and a 13% target for expanding aggregate finance, suggests the government is preparing to continue the credit stimulus. A 13% expansion in aggregate finance implies 17.9 trillion yuan in new lending and equity issuance in 2016, up from 15.3 trillion yuan in 2015.

Which is notable since M1 growth and M2 growth missed expectations significantly in February (M1 +17.4% vs +18.09% exp and M2 +13.3% vs 13.7% exp.)

Charts: Bloomberg

EUROPEAN AFFAIRS

Draghi warns about the rising inequality, even hours after boosting QE which rewards bankers and hurts Main Street:

(courtesy zero hedge)

Draghi Warns About Rising Inequality Hours After Boosting QE, As BIS Warns QE Leads To Inequality

Just hours after Mario Draghi unveiled another €20 billion in monthly QE, bringing the total in “unconventional monetary policy” asset purchases to €80 billion per month, and entering the market for corporate bond purchases for the first time, the ECB released the text of an interview that was conducted with the Guardian on February 18, in which the central banker not only lamented youth unemployment but said he is “worried about increasing inequality.”

Here are the selected excerpts:

Are you worried about the position of young adults in Europe and is this an increasingly urgent issue?

Youth unemployment is a tragedy and prevents people from playing a full and meaningful part in society. If every second young person is out of work – as is still the case in some countries in Europe – it seriously harms the economy, because people willing to work cannot work and skills are not developed. And it threatens social harmony. Unemployment can lead in the long run to increased social problems and ill-health.

What might be the forces at work here – demographics / changing workplaces / fiscal-monetary policy – that mean that young adults appear to be receiving little of the rewards of two and half decades of average economic growth?

Nobody stays young forever. The crucial question is whether a person can participate fully in the economy over his or her life-time – get a good education, find a job, buy a home for the family. Income and wealth follow. What makes me worry is that increasing inequality might prevent people from doing that. This is an issue all our societies need to look at carefully. The ECB’s role in that is to maintain price stability, which prevents unfair redistribution. For example, our research shows that in the euro area too low inflation results in redistribution from younger, more indebted households to older households that are typically net creditors.

Naturally, what is particularly ironic about the head of the ECB complaining about inequality after doing everything in his power to make the rich even richer, is that one doesn’t have to read fringe websites to get to that conclusion. One just has to read a paper issued just a few days ago by none other than his “superior”, the Bank of International Settlements, titled “Wealth inequality and monetary policy” which explicitly states that monetary policy, i.e., more QE, is unambiguously responsible for the recent surge in inequality.

The highlights:

Our results suggest that the impact of low interest rates and rising bond prices on wealth inequality may have been small, while rising equity prices may have added to wealth inequality. A recovery of house prices appears to have only partly offset this effect… Since 2010, high equity returns have been the main driver of faster growth of net wealth at the top of the distribution.

Frost and Saiki (2014) study the impact of unconventional monetary policy on income inequality in Japan in a vector autoregression (VAR) framework. Using household survey data,they find that quantitative easing widened income inequality, especially after 2008 when policy became more aggressive. They identify capital gains resulting from higher asset prices as the main driver.

Yes, ironic, but we certainly expect Draghi to have even more heartfelt lamentations about how increasing inequality is preventing young people from getting an “education, finding a job, or buying a home for the family.” Courtesy of none other than Mario Draghi of course.

Draghi’s Deadly Derangement

by David Stockman • March 10, 2016

Yes, the man is totally deranged, and so is the entire eurozone policy apparatus. Like much of officialdom elsewhere in the world, the ECB is attempting to fight low growth and low inflation with monetary nitroglycerin. Its only a matter of time before they blow the whole financial works sky high.

Low real GDP growth in the eurozone has absolutely nothing to do with the difference between –0.3% on the ECB deposit rate versus the new -0.4%dictate announced this morning; nor does QE bond purchases of EUR 80 billion per month compared to the prior EUR 60 billion rate have anything to do with it, either. The only purpose of such heavy handed financial intrusion is to make borrowing cheaper for households and businesses.

But here’s what the moronic Mario doesn’t get. The European private sector don’t want no more stinkin’ debt; they are up to their eyeballs in it already, and have been for the better part of a decade.

The growth problem in Europe is due to too much socialist welfare and too much statist taxation and regulation, not too little private borrowing. These are issues for fiscal policy and elected politicians, not central bank apparatchiks.

As shown in the chart below, the eurozone private sector had its final borrowing binge during the initial decade of the single currency regime through 2008; debts outstanding grew at the unsustainable rate of 7.5% annually. But since then the eurozone private sector has self-evidently been stranded on the shoals of Peak Debt.

Outstandings have flat-lined for the past eight years—-not withstanding increasingly heavy doses of ECB interest rate repression that have finally taken money market rates into the netherworld of subzero.

Nor has the approximate EUR $700 billion of bond purchases since QE’s inception last March made one wit of difference. Bank loans outstanding to the private sector were EUR 10.24 trillion at the end of January or exactly where they stood in March 2015 when Draghi and his merry band of money printers went all in.

By the same token, it is damn obvious that low inflation is not a problem, and that, in any event, it is not caused by lack of money printing and insufficient interest rate repression by the goofballs assembled at the ECB’s swell new headquarters in Frankfurt. The eurozone’s respite from its normal 1-2% annual dose of headline inflation is entirely imported via the global tide of plunging oil, commodities, steel and other industrial prices.

That welcome tide of imported deflation, in turn, is actually improving the eurozone’s terms of trade and raising consumer living standards; and it is not remotely connected to anything the ECB has done or not done in the last year or even four years.

Instead, the global deflation is a consequence of the massive malinvestment in mining, energy, industry, transportation and distribution which has resulted from the 20-year global credit binge enabled by the world’s convoy of money printing central banks. Incremental debt of $185 trillion or nearly 4X GDP growth during that period has crushed the world’s capacity for investment and production led growth.

The overhang of excess capacity everywhere on the planet is also drastically compressing prices, margins and profits, but the major impact is in the Red Ponzi and its EM supply chain; and the secondary impact is on engineered machinery, high tech and luxury goods exporters, including Germany and other eurozone export strongholds.

It goes without saying, however, that today’s new round of monetary quackery by the ECB will have no impact whatsoever on eurozone export demand from China and the EM. Not only did Draghi fail to send the Euro careening lower, but it wouldn’t matter anyway. The barrier is not FX; the problem is investment saturation in foreign markets that have run out of borrowing capacity.