Gold: $1,264.50 up $35.20 (comex closing time)

Silver 16.02 up 81 cents

In the access market 5:15 pm

Gold $1256.70

silver: 15.90

At the gold comex today, we had a poor delivery day, registering 0 notices for nil ounces and for silver we had 4 notices for 20,000 oz for the active March delivery month.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 211.33 tonnes for a loss of 92 tonnes over that period.

In silver, the open interest rose by 2325 contracts up to 168,505 with silver down by 5 cents yesterday (pre announcement by Yellen). In ounces, the OI is still represented by .843 billion oz or 120% of annual global silver production (ex Russia ex China).

In silver we had 230 notices served upon for 1,150,000 oz.

In gold, the total comex gold OI rose by 8,465 contracts to 501,551 contracts as the price of gold was DOWN $1.10 with yesterday’s trading.(at comex closing). The rise in OI in gold should add considerable pressure on our bankers and thus expect future raids.

We had another big change in gold inventory at the GLD, a whopping deposit of 11.89 tonnes/ thus the inventory rests tonight at 807.09 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,/we had no changes in inventory/ and thus the Inventory rests at 325.868 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver rose by 2325 contracts up to 168,505 as the price of silver was down 5 cents with yesterday’s trading. The total OI for gold rose by 8,465 contracts to 501,551 contracts as gold was down $1.10 in price from yesterday’s level.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

3. ASIAN AFFAIRS

i) Late WEDNESDAY night/ THURSDAY morning: Shanghai closed UP BY 35.11 POINTS OR 1.22% , / Hang Sang closed UP by 246.11 points or 1.21% . The Nikkei closed DOWN 38.07 or 0.22%. Australia’s all ordinaires was UP 0.68%. Chinese yuan (ONSHORE) closed UP at 6.47800. Oil ROSE to 39.07 dollars per barrel for WTI and 40.91 for Brent. Stocks in Europe so far ALL IN THE RED . Offshore yuan trades 6.4751 yuan to the dollar vs 6.4780 for onshore yuan/yesterday China’s industrial production collapsed along with retail sales. JAPAN RE SIGNALS that they may continue with nirp a little longer which sends the USA/Yen spiraling northbound/markets in Japan tumble (see below). Japan’s exports plummet (see below).Yesterday China signals that they are going to tax financial transactions. This morning they raise the yuan trapping the shorts with huge losses (see below)

.

ii)report on Japan

Japan exports to the USA collapse. However imports collapse even more as their trade balance improves. However it is not a good sign in an economy when both exports and imports collapse!

iii)Japanese intervention saves the Nikkei from disaster as the USA/Yen plummets to the 111 handle: a complete policy failure for Kuroda.

iv) report on China

i)The following is a big story as the Syrian Kurds want a separate state. They were not invited to Geneva but they are now declaring a proto state on Turkey’s border.

This is exactly, the worst nightmare for Erdogan

(courtesy zero hedge)

ii) No words can describe what Erdogan is doing. Democracy in Turkey is non existent.

ii)the bounce that we have experienced in the Baltic Dry Index just ended:

i)A judge released wiretaps on Rousseff and Lulu and they suggest that Rousseff picked Lulu for chief of staff in order to avoid prosecution: Brazil broke into utter chaos!!

( zero hedge)

ii)VENEZUELA RUNS OUT OF ELECTRICITY/THEY SHUT DOWN FOR A WEEK

ii) Ronan Manly has written basically an encyclopedia of gold markets around the world/ trading volumes and other interesting factoids. Markets covered our South Africa, London, Singapore, Switzerland and the USA

iii)It was a foregone conclusion that all of Venezuela’s gold would end up in China after undergoing conversion to kilobars:( Ronan Manly/Bullionstar/GATA)

iv) More on our basket case country: Venezuela

(Bloomberg/GATA)

v)Tonight’s topic is on the USA election:

“The Circus We Call the Election Process!”

(courtesy Bill Holter/Holter-Sinclair collaboration)

vi)Steve St Angelo explains why silver is a great investment:

( Steve St Angelo/SRSRocco report)

vii)Lawrie Williams talks about the break out in gold:

(Lawrie Williams/Sharp’s Pixley)

USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)Very important: the impact of a dovish message from the Fed is very bad news for risk assets like financials;(Bank of America/ zero hedge)

ii)Bellwether stock Caterpillar slashes its guidance for the year as they see Q1 earnings per shore 30% below their forecast. Caterpillar is a stock to follow to give us a great idea as to how the entire globe is performing. In a nutshell: not good at all!

iii)Initial jobless claims steady. However ISM services which is 70% of uSA GDP crashes:

v)The once darling of the NYSE, Valeant sees its credit default swaps hit a record high as they scramble to avoid going bust:

vi) The JOLTS survey is certainly of concern to the Fed: lower quits/lower job openings

vii)The evidence sure looks like Hillary knew her blackberry was not secure and that she would not be allowed to pass classified stuff to various people

Let us head over to the comex:

The total gold comex open interest rose to 501,551 for a gain of 8,465 contracts despite the fact that the price of gold was down $1.10 in price. Expect our bankers to undergo relentless attacks on our two precious metals. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month or for that matter an inactive month, and 2) a continual drop in the amount of gold standing in an active month. Today, only the first scenario was in order as we actually gained in actual ounces of gold standing. The front March contract month saw its OI rise by 14 contracts up to 149.We had 0 notices filed upon yesterday, and as such we gained 14 contracts or an additional 1400 oz will stand for delivery. After March, the active delivery month of April saw it’s OI rise by 3,968 contracts up to 248,452. This high level is scaring our crooked bankers. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 270,700 which is very good.Tomorrow’s number will be extremely high. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was good at 232,762 contracts. The comex is not in backwardation .

March contract month:

INITIAL standings for MARCH

March 17/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | nil

|

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 contract (nil oz) |

| No of oz to be served (notices) | 149 contracts(14,900 oz) |

| Total monthly oz gold served (contracts) so far this month | 585 contracts (58,500 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 127,007.9 oz |

we had 1 adjustment:

out of Brinks:

200.000 oz was adjusted out of the dealer and this landed into the customer account.

Can someone explain how we can get an adjustment of exactly 200.00??

what is also interesting is that even though we had an adjustment of 200.00 oz the dealer account was not adjusted lower.

MARCH INITIAL standings/March 17/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 922,262.25 oz (Scotia,CNT/JPM) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 4 contracts 20,000 oz |

| No of oz to be served (notices) | 711 contract (3,555,000 oz) |

| Total monthly oz silver served (contracts) | 729 contracts (3,645,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 10,096,266.6 oz |

today we had 0 deposits into the dealer account

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 0 customer deposits

total customer deposits: nil oz

We had 3 customer withdrawal:

i) Out of Scotia: 12,114.960 oz

ii) Out of JPM: 299,856.400 oz

iii) Out of CNT; 610,290.89 oz

:

total customer withdrawals: 922,262.25 oz

we had 0 adjustments

And now the Gold inventory at the GLD:

March 17/we had a whopper of a deposit tonight: 11.89 tonnes/with London in backwardation this is nothing but a paper addition/inventory rests tonight at 807.09 tonnes

March 16.2016:/we had a deposit of 2.09 + 2.97(last in the evening) tonnes of gold into the GLD/Inventory rests at 795.20 tonnes

March 15/ no changes in gold inventory at the GLD/Inventory rests at 790.14 tonnes

March 14/a huge change in gold inventory at the GLD, a withdrawal of 8.63 tonnes/Inventory rests at 790.14 tonnes

March 11 /despite the high volatility of gold last night and today, somehow the GLD added 5.95 tonnes of gold without disturbing anyone./inventory rests this weekend at 798.77 tonnes

March 10/a deposit of 2.08 tonnes of gold into the GLD/Inventory rests at 702.82 tonnes

March 9/a withdrawal of 2.38 tonnes of gold from the GLD/Inventory rests at 790.74

March 8/no changes in inventory at the GLD/Inventory rests at 793.12 tonnes

MARCH 7/a tiny loss of .21 tonnes of gold probably to pay for fees/inventory 793.12 tonnes

MARCH 4/another mammoth sized deposit of 7.13 tonnes of gold into GLD/Inventory rests at 793.33 tonnes. This is no doubt a “a paper addition” and not physical

MAR 3/another good sized deposit of 2.37 tonnes of gold into the GLD/Inventory rests at 788.57 tonnes

MAR 2/another mammoth paper gold addition of 8.93 tonnes of gold into the GLD/Inventory rests at 786.20 tonnes.

March 1/a mammoth 14.87 tonnes of gold deposit into the GLD/inventory rests at 770.27 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

March 17.2016: inventory rests at 807.09 tonnes

end

And now your overnight trading in gold, THURSDAY MORNING and also physical stories that may interest you:

Happy Saint Patrick’s Day ————– Gold Surges Nearly 3% After Fed

Breaking News and Commentary

Gold jumps to $1,260/oz after Fed statement pressures dollar – Reuters

Gold Jumps After Fed Scales Back Forecasts for Interest Rates – Bloomberg

Yellen Revives Gold Rally as Fed Scales Back Rate Outlook – Bloomberg

Fed Scales Back Rate-Rise Forecasts as Global Outlook Weakens – Bloomberg

Fed under Yellen and the gold trade – CNBC

Casey Says Gold Going Over $3,000/oz – Casey Research

Yellen-era Fed hasn’t been great to gold investing …. yet – CNBC

4 Investors That Lost Combined $3.66 Bil In Valeant’s Tuesday Bloodbath – Forbes

Silver Supply under $16 Limited. Backlash If Futures Market Break – Safe Haven

SILVER: Moving From Commodity To High Quality Store Of Value – SRS Report

Read More Here

Munich Re stashes gold and cash to counter negative rates

Submitted by cpowell on Wed, 2016-03-16 17:01. Section: Daily Dispatches

From Reuters

Wednesday, March 16, 2016

MUNICH, Germany — German reinsurer Munich Re is boosting its gold and cash reserves in the face of the punishing negative interest rates from the European Central Bank, it said today.

The world’s largest reinsurer is far from alone in seeking alternative investment strategies to counter the near-zero or negative interest rates that reduce the income insurers require to pay out on policies.

Munich Re has held gold in its coffers for some time and recently added a cash sum in in the two-digit million euros, Chief Executive Nikolaus von Bomhard told a news conference. …

… For the remainder of the report:

Ronan Manly’s encyclopedia of the world’s gold markets

Submitted by cpowell on Wed, 2016-03-16 17:13. Section: Daily Dispatches

1:12p ET Wednesday, March 10, 2016

Dear Friend of GATA and Gold:

Our friend gold researcher Ronan Manly has written what is essentially an encyclopedia of gold markets around the world, detailing their mechanisms, participants, trading volumes, and many other characteristics, from London to New York to South Africa to China and in between. This is likely to become a basic reference work for the industry. It can be found at Bullion Star here —

https://www.bullionstar.com/gold-university/london-gold-market-trading

— where it starts with the London market. Sections on other markets are linked in the left column.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

It was a foregone conclusion that all of Venezuela’s gold would end up in China after undergoing conversion to kilobars:

(courtesy Ronan Manly/Bullionstar/GATA)

Ronan Manly: Venezuela’s gold keeps moving to Switzerland

Submitted by cpowell on Wed, 2016-03-16 19:23. Section: Daily Dispatches

3:20p ET Wednesday, March 16, 2016

Dear Friend of GATA and Gold:

Venezuela continues to ship its gold reserves to Switzerland as part of gold swap arrangements to finance the Venezuelan government, gold researcher Ronan Manly reports today, with 12 1/2 tonnes sent via Paris on March 8. Manly’s report is posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/venezuela-exported-12-5-to…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

More on our basket case country: Venezuela

(Bloomberg/GATA)

Imagine how much they’d save if they NEVER went back to work

Submitted by cpowell on Wed, 2016-03-16 17:22. Section: Daily Dispatches

Venezuela to Shut Down for a Week to Cope With Electricity Crisis

By Andrew Rosati

Bloomberg News

Wednesday, March 16, 2016

Venezuela is shutting down for a week as the government struggles with a deepening electricity crisis.

President Nicolas Maduro gave everyone an extra three days off work next week, extending the two-day Easter holiday, according to a statement in the Official Gazette published late Tuesday. Maduro had originally said over the weekend that the extended holiday would apply only to state employees.

The government has rationed electricity and water supplies across the country for months and urged citizens to avoid waste as Venezuela endures a prolonged drought that has slashed output at hydroelectric dams. The ruling socialists have blamed the shortage on the El Nino weather phenomena and “sabotage” by their political foes, while critics cite a lack of maintenance and poor planning.

“We’re hoping, God willing, rains will come,” Maduro said in a national address Saturday. “Look, the saving is more than 40 percent when these measures are taken. We’re reaching a difficult place that we’re trying to manage.” …

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2016-03-16/venezuela-to-shut-down..

end

Lawrie Williams talks about the break out in gold:

Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: Gold back at $1270 level after cautious Fed statement

17

Well the latest Fed deliberations appear to have favoured the so-called ‘doves’ with the consensus predictions coming about with the predicted number of any further interest rate rises this year (if indeed there are any at all) being halved to two. This suggests year end Fed interest rates of between 0.75 and 1 percent – and no immediate rate rise triggered. The whole scenario will play out again in around 6 weeks’ time. Will it be any different then?

The immediate beneficiary of the Fed non-decision was a boost to general equities, both in the U.S. and globally (apart from Japan’s Nikkei which slipped a little). This should be a little worrying for the Fed in terms of possible future rate hikes. Does this mean that equities will fall should the Fed increase rates later in the year? Equities markets are fragile at the moment amidst talk of a potential global recession. The last thing the Fed would want to do would be to take any measure that might precipitate a Wall Street crash.

An even bigger beneficiary was the gold price which gained $40 or so and is now back trading – consolidating gold bulls will hope – in the high $1,260s – low $1,270s. However it should be said that gold only fell back to the $1,230s over the past week engendered by nervousness ahead of the Fed’s statement. One doubts that the Fed takes the likely movement of the gold price into consideration when deciding whether or not to raise interest rates – but it will certainly take the likely path of U.S. equities markets into account. Sentiment is everything in maintaining any confidence in the progress of the U.S. economy and a crash in equities would be hugely counter-productive. Gold, on the other hand, may be seen as a bellwether for the U.S. dollar and the economy among some savvy investors, but in terms of the general public it remains something of an irrelevance. It accounts for too small a percentage of investment assets to be seen as having any real significance, except by those who understand its true role – and they are few and far between.

So how about the U.S. dollar (which also has an important impact on gold and dollar traded commodity prices)? Well it fell back with the Index level down at around 95 – down from over 100 back in December when the general consensus was that raising interest rates would lead to further dollar strength. This did not come about, and not raising them further appears to have led to a fairly significant fall. This may not worry the Fed too much – U.S. exporters had been suffering as the higher dollar had been making their products uncompetitive.

However, this will be a blow to other competing currencies like the Euro, the Swiss Franc, the Japanese yen and the Chinese yuan and may lead to moves by their central banks to try and devalue their currencies against the dollar, even if only by fairly small amounts. All these are the kinds of consequences the Fed will be having to take into account in its deliberations.

So where next for the Fed? Inflation remains below its target. The Fed’s inflation figures may well not tally with those of other observers, but they are the figures it bases its decisions on! Unemployment in Fed terms is on track, although again independent assessors of the true unemployment situation feel the official figures are way, way too low. But again the Fed figures are those on which it will base its future decisions. There’s a strong chance that at the next Fed Open Market Committee meeting, scheduled for late April, nothing much will have changed, but then it may find itself under stronger pressure to confirm a forthcoming rate rise, if only to try and maintains credibility in its prior forecasts. We don’t yet see it doing an about turn and cutting, or implementing a new QE phase, although some forecasters have predicted this. Such a decision would be a bitter blow to the Fed’s forecasting credibility, which is fragile enough anyway. So kicking the can further down the road would seem to be the most likely scenario failing a big upturn in the U.S. and global economies – for which there is little in the way of evidence to support this in the short term at least.

So where does this all leave gold – and silver? Poised we would reckon. Gold has moved back to the $1,270 level as I write and silver is picking up nicely pari passu with gold. If momentum continues then we see no reason why gold couldn’t move ahead towards the $1,300 level and silver to say $16.25 or higher. But gold is always tough to forecast. When you expect it to rise, something brings it back down to earth – usually strange dealings on the futures exchanges. We can probably expect to see something like this taking place in an attempt to curb, or at least control, any upwards movement. But as trading continues moving eastwards towards China with the opening of the Shanghai Gold Exchange’s new benchmarking system next month, the abilities of the U.S. futures markets to control the global gold price will become more and more limited. But will a Chinese-influenced system be any more supportive of gold while that nation continues to build its gold reserves? We will have to wait and see.

Lawrence Williams

end

Steve St Angelo explains why silver is a great investment:

(courtesy Steve St Angelo/SRSRocco report)

SILVER INVESTMENT: Switching From A Commodity To High Quality Store Of Value

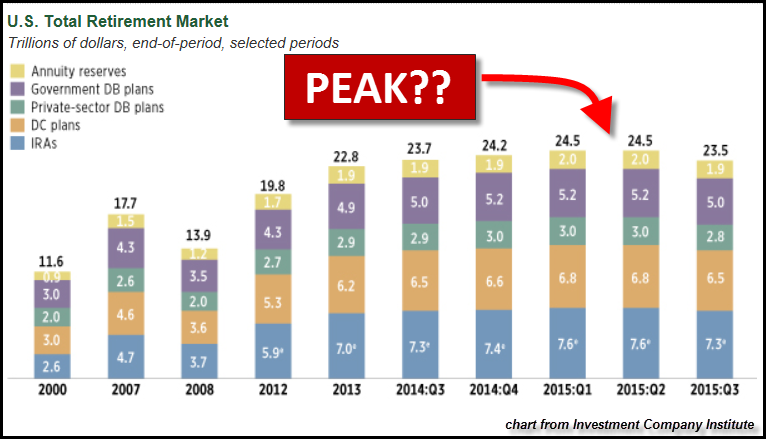

The biggest trade of a lifetime will occur when the value of silver switches from a mere commodity to a high-quality store of value. Actually, it’s not really a trade of a lifetime, but rather a fundamental repricing of real assets verses supposed assets. According to the Investment Company Institute, the supposed value of the total U.S. Retirement Market was $23.5 trillion in the third quarter of 2015:

As we can see, the value of the U.S. Retirement Market is down $1 trillion from its peak of $24.5 trillion in the previous two quarters. Could this be the peak of U.S. Retirement assets?? While the broader stock markets rebounded in the fourth quarter of 2015, they fell again during the first quarter of 2016.

If there are any investors who still believe the Fed and member banks aren’t propping up the markets, you need to get your head examined. We know many of the other Central Banks such as Japan and China have officially stated they were buying stocks, why wouldn’t the Fed and U.S. Govt?? Of course we are.

And it makes a lot of sense why they are doing it. The overwhelming majority of Americans that are invested in the markets are invested in the typical assets that comprise the U.S. Retirement Market. Only a tiny fraction of Americans are invested in physical precious metals. So, in order to keep “CALM” in the markets, the major indexes are not allowed to collapse…. well, for a while.

Look what happened to the Mainstream investor when the Dow Jones Index fell just 11% in the first two months of 2016… they moved into the Gold & Silver ETF’s and Funds in a major way. I discuss what is taking place in the Gold Market in detail in a new upcoming BULLET REPORT.

What on earth would happen to the Gold & Silver Markets if the Dow Jones Index was decimated by 30- 50%?? I believe it would cause Mainstream investors to move into gold and silver in such a forceful way, that it would totally overwhelm the supply causing the prices to shoot up much higher. And the higher the price of gold and silver would go, the more Mainstream investors would pile in.

The Fed’s worst nightmare…..

Right now the values of the major stock indexes are extremely overvalued. However, the market isn’t allowed to find their true fundamental value, but it will. This will likely happen when gold and silver switch from a commodity pricing mechanism to a high-quality store of value. Let me explain this in silver’s case.

Silver Trades As A Mere Commodity Due To The Oil Price

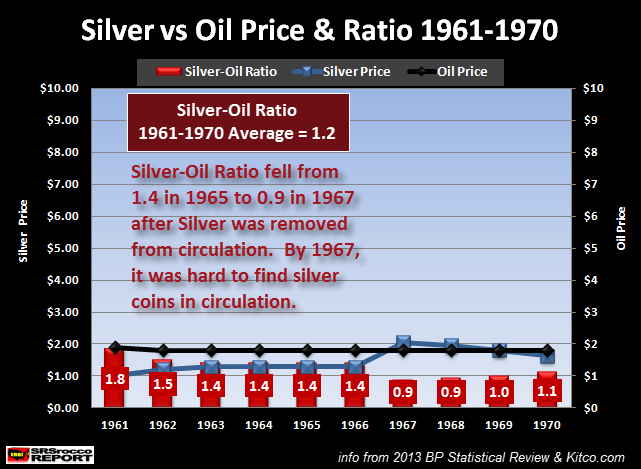

The value of silver has been tied to the price of oil for quite some time. While some analysts suggest this isn’t the case, the charts below provide ample evidence:

These charts were published in an article I wrote a couple of years ago. However, they still just as valid today. As we can see there was very little volatility in the price of oil and silver in the 1960’s. Why? Because the price of oil remained unchanged from 1962 to 1970 at $1.80. Can you imagine that? No change in the oil price for nearly a decade? Well, that all changed in 1970’s when the U.S. peaked in oil production and Nixon dropped the Dollar-Gold peg.

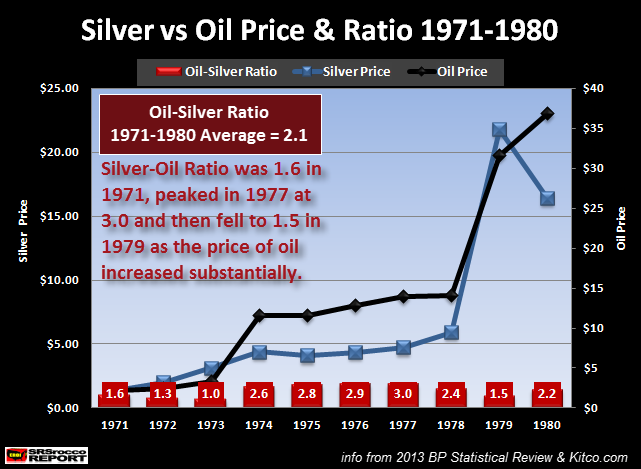

The next chart shows the change in the price of oil and silver due to two oil price shocks:

The price of oil jumped from $3.29 in 1973 to $11.58 in 1974 due to the Arab Oil Embargo. This impacted the value of silver as it increased from $1.98 in 1972 to $4.39 in 1974. Both the price of oil and silver increased slightly by 1978, but then jumped violently in 1979. This was due to the Iranian Revolution led by Ayatollah Khomeini which resulted in a huge reduction in the country’s total oil production. Total oil Iranian oil production fell from 5.3 million barrels per day (mbd) in 1978 to 1.5 mbd in 1980. This had a profound impact on the price of oil.

The price of oil jumped to $31 in 1979, up from $14 in 1978. Thus, the price of silver also skyrocketed to nearly $22 (average annual price), from $5.93 the previous year. Why did silver move up so high? Well, if silver mining costs were going to increase because of the jump in the price of oil, so would the price of silver. Of course, there was increased speculation as more investors piled into silver, but we can plainly see the rise in the price of oil was the underlying fundamental cause that impacted the silver price…. as well as gold.

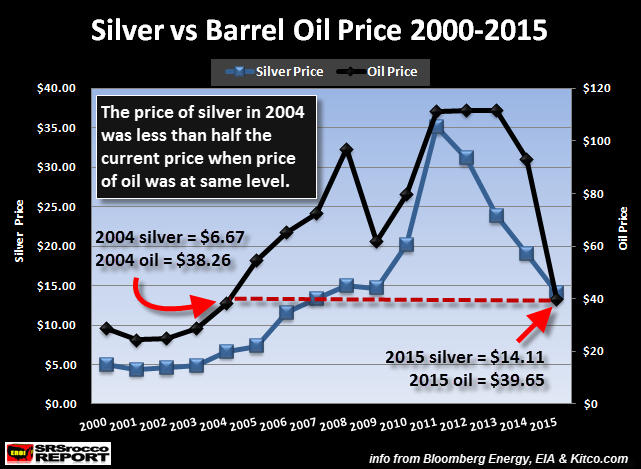

This the exact same thing that took place since 2000:

Again, the price silver moved up with the price of oil. And as we can see, it also fell with fall in the price of oil… even though prematurely. That is a discussion for another article.

The fact remains, that the cost to produce silver is based on the price of oil. This is called a “Commodity Price Mechanism.” Those folks who believe it will take a price of oil at $200 to see silver reach $50-$75, it’s likely not going to happen. Why? I don’t see a high price of oil as sustainable…. even if oil production starts to decline. That’s another topic for discussion in an upcoming report.

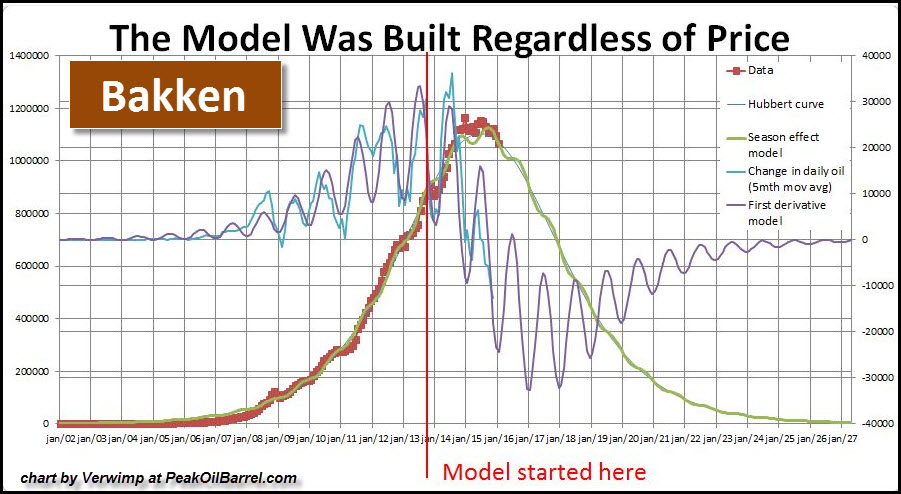

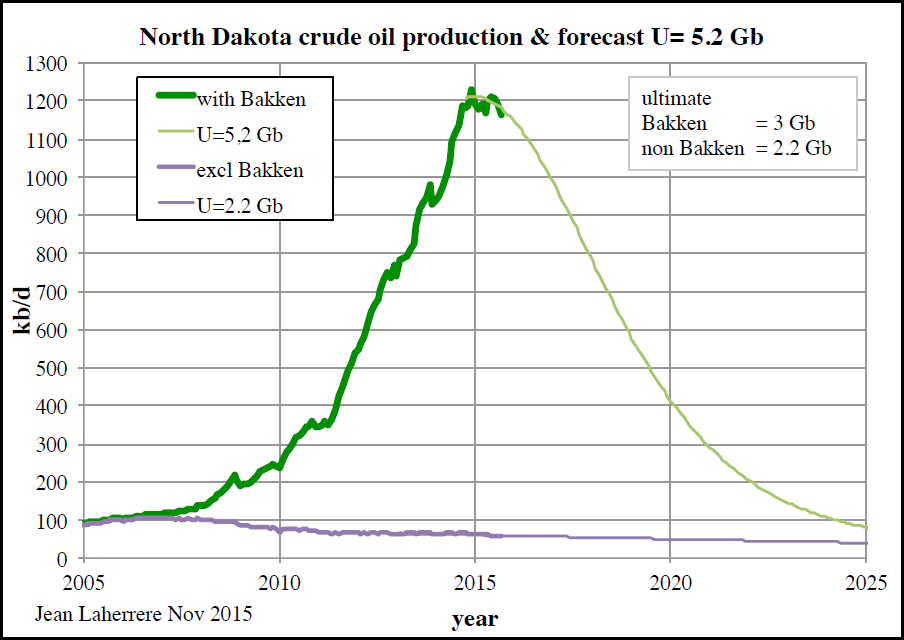

And decline it will. Especially, in the United States:

This chart is by one of the contributors (Verwimp) at the PeakOilBarrel.com website. This is an oil production profile of the Bakken, regardless of price. It has to do with the high decline rates and the amount of new wells. This isn’t the only person who believes the Bakken oil production is going to collapse. Jean Laherrere also arrives at the same production profile:

The Bakken is the second largest Shale oil field in the United States. The Eagle Ford Shale oil field is the largest, but it will suffer the same fate as the Bakken. With U.S. oil production to collapse over the next 5-10 years, this will have a profound impact on all paper assets including Stocks, Bonds and Retirement Accounts. Burning energy gives these paper assets their value. The collapse of this energy supply will cause a collapse of the paper assets.

For those who think the United States will just import more oil to make up the future shortfall… you are sadly mistaken. There is a reason why China and Russia are adding gold to the Official Reserves. They realize the value of the Dollar will be toast… and collapsing domestic oil production will be one of the leading causes.

Tonight’s topic by Bill Holter is on the USA election:

(courtesy Bill Holter/Holter-Sinclair collaboration)

The Circus We Call the Election Process!

Immediately after turning on the business news this morning, I heard an interview of a Republican National Committee member talking about “rules”. I did not catch who it was but the essence of the interview was it did not matter who had the most votes or delegates …the Republican committee would choose “their candidate” if no one had the majority leading into the convention. He was questioned with “so the will of the people doesn’t matter”? To which he answered and I will paraphrase in my own words as I understood, “it doesn’t matter who the people vote for and we will even overturn a majority if we see fit, the Republican party will choose their candidate for the good of the Republican party”. As an aside, John (buddy can you spare a Kleenex) Boehner “endorsed” Paul Ryan for presidential nominee. (Not sure I would have voted for him but I don’t recall his name on the ballot)? Upon further searching, the interview can be found here Voters don’t pick nominee, we do: GOP official . All I can say is “in your face, we make the rules, you don’t even matter”!

You might ask “what does this have to do with finance or economics”? In no particular order, it has EVERYTHING to do with economics and finance! Whatever happens will certainly affect the dollar (the currency of any nation is the equivalent of its common stock). Future policy will affect the dollar as well as how foreigners view what happens. Interest rates, stocks, real estate, everything imaginable will be affected. It does need to be said that no matter who wins or loses, the system is already toast and only “timing” may be altered. Most importantly I believe the only difference between who wins and who loses will dictate how quickly or severe the elimination of our civil rights and liberties will be.

In my opinion we are actually watching a circus that no fiction writer could have dreamed up. On one side we have a socialist/communist running against an apparent felon. On the other side we have a populist who says whatever he cares to as long as it’s something the people are thinking, running against a hardened conservative that no one in establishment Washington likes. The odds favor a Clinton/Trump matchup. I would ask a couple of questions. What will the response be if Hillary Clinton is indicted? A really far out question would be what if she is somehow pardoned and allowed to run? On the other side, what will happen if the nomination is taken away from Mr. Trump? Or better yet, what if it is taken away from both Trump and Cruz and instead given to a “preferred” candidate? The most comical thing I can think of right now is future debates between Hillary and The Donald!

Before finishing it needs to be said the old adage “it doesn’t matter who you vote for, it only matters who counts the votes” is probably quite true now more than ever before. Because of the financial backdrop I wonder whether or not we will even have an election? If the financial system were to come down prior to the election (which I believe is likely), would we have an election under martial law conditions? Financially our fate is carved in stone in my opinion, how we navigate, survive or perish with or without civil liberties is in question.

As I said at the beginning, I hesitate to write on this topic because my e-mail inbox explodes with hatred. As an admission, my candidate of choice was Ben Carson. Was he most qualified? No. Was he establishment or even a politician? No. Did he have ANY experience in government? No. In my opinion, Ben Carson is an American with his country’s best interest ahead of his own or anyone else’s. He believes in God and in Christian values, whether real or not, the world would be a pretty cool place if everyone got along and acted as Christ did according to the Bible. Mr. Carson was my choice because as I see it, our “inalienable” (or God given) rights have been frittered away and we are on the cusp of losing them altogether. Maybe I am mistaken but I view him as a man of respect for everyone and their individual rights, not someone who wants control through handouts I can only pray that we as a nation can find our way back in time when neighbor helped neighbor, and self reliance and accountability for one’s actions not only meant something but was expected. No matter the outcome, this next election will be historical!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

“Lucid” comments welcome! bholter@hotmail.com

Your early morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.4780 / Shanghai bourse IN THE GREEN, UP 35.11 OR 1.22% : / HANG SANG CLOSED UP 246.11 POINTS OR 1.22%

2 Nikkei closed DOWN 38.07 OR 0.22%

3. Europe stocks ALL in the RED /USA dollar index DOWN to 94.91/Euro DOWN to 1.1308

3b Japan 10 year bond yield: FALLS TO -.036% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.34

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 39.07 and Brent: 40.91

3f Gold UP /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS to 0.311% German bunds in negative yields from 7 years out

Greece sees its 2 year rate RISE to 9.65%/:

3j Greek 10 year bond yield RISE to : 8.88% (YIELD CURVE NOW INVERTED)

3k Gold at $1266.50/silver $15.73 (7:15 am est)

3l USA vs Russian rouble; (Russian rouble UP 68/100 in roubles/dollar) 68.54

3m oil into the 39 dollar handle for WTI and 40 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9703 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0973 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN STARTS ITS CAMPAIGN AS TO WHETHER EXIT THE EU.

3r the 7ear German bund now in negative territory with the 10 year FALLS to + .311%

/German 7 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.87% early this morning. Thirty year rate at 2.66% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Another Fed “Policy Error”? Dollar And Yields Tumble, Stocks Slide, Gold Jumps

Yesterday when summarizing the Fed’s action we said that in its latest dovish announcement which has sent the USD to a five month low, the Fed clearly sided with China which desperately wants a weaker dollar to which it is pegged (reflected promptly in the Yuan’s stronger fixing overnight) at the expense of Europe and Japan, both of which want the USD much stronger.

This morning the global markets got a rude reminder that at the end of the day it is all about currency devaluation and competitive debasement – even if it means appeasing China in the process – when the plunge in the dollar,, much to Goldman’s ongoing embarrassment, extended overnight as seen in the chart below.

This has led the USDJPY slide to just over 111 while the EURUSD was surging over 1.13 as of this moment, and in the process undoing all the recent easing by both the ECB and the ECB; furthermore an expected 25 bps rate cut by the Norway Central Bank, not only did not weaken the NOK but in fact sent it surging against the EUR, indicating that even when central bank decisions are fully priced in, few can actually trade the reaction and the implication of such moves.

Worse, after briefly spiking in the aftermath of the Fed’s decision overnight European sovereign and US Treasury yields have tumbled, commodities and especially gold have soared, and as of moments ago, European stocks hit their lows on the day now that the European currency is surging, leading to this:

- EUROPEAN STOCKS EXTEND DROP; STOXX 600 DOWN 1.4%

And since these are all the telltale signs of yet another Fed policy error, it was only a matter of time before the move also hit the Fed’s favorite asset class – equities, and sure enough, after posting modest gains overnight, US index futures have seen a sharp reversal lower, and from up 0.3% were down -0.3% at last check, as suddenly the market appears to be getting cold feet not only about the Fed’s decision to slam the Dollar at the expense of the Euro and the Yen, but also going back to that all important question which Yellen was unable to answer:has the Fed lost its credibility?

While risk assets are suddenly airpocketing, dollar-denominated oil, copper and zinc all jumped by more than 2 percent, with Brent trading above $40 a barrel, which means we can expect a rewriting of the narrative that higher gas prices are actually good for consumers, even if it also means that marginal shale production is likely to start coming back on line any moment.

And the cherry on top may have come when moments ago industrial bellwether Caterpillar slashed guidance, and now expects non-GAAP Q1 EPS of $0.65-$0.70 per share, about 25% below consensus estimates of 95 cents.

All of the above, this had led to sudden repricing of risk, which has seen equity futures stumble, and the ES is now down 10 points to 2,007, roughly where it was when the Fed unveiled its dovish surprise. Was that it for the Fed’s intervention halflife? We don’t know, but we expect much confusion today over whether even the Fed has now run out of dovish ammunition.

This is where we stand currently

- S&P 500 futures down 0.5% to 2006

- Stoxx 600 down 1.4% to 336

- FTSE 100 down 0.7% to 613

- DAX down 1.7% to 9816

- German 10Yr yield down 7bps to 0.24%

- MSCI Asia Pacific up 2.1% to 129

- US 10-yr yield down 5bps to 1.86%

- Dollar Index down 0.82% to 95.1

- WTI Crude futures up 1.6% to $39.08

- Brent Futures up 1.4% to $40.09

- Gold spot up 0.6% to $1,270

- Silver spot up 0.2% to $15.65

Top Global News

- Witty to Step Down After Tumultuous Tenure as Glaxo Chief: CEO Andrew Witty plans to step down in 2017 after almost a decade, board to begin search for a successor

- Rio Tinto Appoints Copper Chief Jacques CEO to Succeed Walsh: Copper boss Jacques replaces iron man Sam Walsh in July

- FedEx Raises Floor of Full-Year Forecast After Cutting Costs: Now sees FY16 adj. EPS $10.70-$10.90, saw $10.40- $10.90, est. $10.56; 3Q adj. EPS $2.51, est. $2.34

- Pershing Square Falls 26% Year Through March 15 on Valeant: Cut its stake in Mondelez to 5.6%

- Toshiba Said to Face U.S. Probe Over Westinghouse Accounting: Justice Department, SEC reviewing conduct in Toshiba report

- VW Said in Talks With U.S. Over Two Funds to Pay for Pollution: In talks to establish national remediation fund and a separate one for California as punishment for pollution from its cars after co. cheated on diesel- emissions tests, said people familiar with the matter

- Fed Softens Rate-Rise Urgency as Risks Abroad Cloud Outlook: FOMC cites global concerns twice as Yellen highlights in Q&A

- American Pilots Concerned by CEO Meeting on ‘Toxic’ Culture: COO Robert Isom named to deal with pilot contract concerns

- Goldman Seen Succumbing Too as Wall Street Suffers Awful Quarter: Its trading revenue may slide 17%, Credit Suisse analysts say

- New York’s Plaza Hotel Said for Sale in Foreclosure Auction: Billionaire Reuben brothers said to foreclose on mortgage

- Oil Investors See $7.4b Vanish as Dividends Are Targeted: Conoco, Kinder resort to cuts “deplored” by shareholders

- March Madness Puts Time Warner’s Big Bet on Sports to the Test: NCAA men’s championship game to air on TBS for first time

- Valeant Lenders Said to Mull New Terms in Default Talks, Reuters Says: Lender’s demands include higher interest payments, pledge to pay a larger amount of bank loans from any Valeant asset sales proceeds

- Amazon Said to Eye Office Depot’s Corporate Business Unit, NYP Report: May use some of Office Depot’s corporate accounts to jump-start its new office supply business

- Canada to Announce Bombardier Aid Decision Within Weeks, Reuters Says: Govt has finished studying co.’s request for $1b in aid

Looking at global equity markets, Asia stocks traded mostly higher in the wake of the FOMC. ASX 200 (+1.0%) was led by energy and basic materials after commodity prices benefited from USD weakness post-FOMC, while oil prices were also underpinned following yesterday’s lower than expected DoE inventory build. Nikkei 225 (-0.2%) initially surged on the prospects of lower US rates for longer, but then shrugged off majority of gains as JPY strengthened, while the Shanghai Comp (+1.2%) conformed to the picture with the PBoC also said to be gauging banks for Medium-term Lending requirements. 10yr JGBs initially tracked T-notes higher following the Fed dovishness, however JGBs pared advances after a weaker 20yr bond auction result in which b/c, tail in price and lowest accepted price all disappointed.

Top Asian News

- Li & Fung 2015 Earnings Top Estimates as New Clients Boost Sales: FY net $421m, est. $405.3m, sales down 2.4% to $18.8b

- Billionaire Li’s CK Hutchison Profit Edges Above Estimates: FY adj. net HK$31.2b; est. HK$30.9b, profit helped by earnings from Europe telecom operations

- China Mobile 2015 Profit Misses Estimates, Shares Reverse Gain: Govt request to lower mobile phone rates erodes profit

- Mr. Yen Called the Rally, Now Sees Gain Toward Intervention Zone: Ex-MOF Sakakibara correctly predicted advance

- Toshiba Gets $5.9 Billion Deal to Sell Medical Unit to Canon: Deal will be funded by existing cash and borrowings, Canon said, day after unsuccessful bidder Fujifilm questioned Toshiba about the sale

- Escape From Negative Japan Rates Wrecked by Record Hedging Costs: Swap premium for yen holders reaches record 102.5 bps

- Yuan Falls to 15-Month Low Versus Basket as Fixing Lags Dollar: Reference rate shows China doesn’t want excessive gains, DBS says

- TPG Sees Opportunity in $131 Billion India Distressed Assets: Co. would like to triple India investments in 3 yrs

In Europe, this morning has seen focus fall on the fallout from the Fed rate decision and press conference yesterday and as such, has seen much of the price action continue on from US and Asian hours. Bunds have seen significant upside during European trade, with the June future residing above 162.00 and the German curve showing many of the characteristics as its US counterparts with the curve flattening amid expectations for a shallower rate path going forward.

In tandem with this, European equities saw initial upside at the open in the wake of the dovishly interpreted Fed announcement. However stocks came off their best levels by mid-morning to see Euro Stoxx reside relatively flat as some analysts begin to focus on recent central bank commentary which appears to be relatively downbeat for global growth prospects as highlighted by the Fed statement and UK budget yesterday and the SNB and Norges Bank today.

Top European News

- Lufthansa Says Eurowings Price Cuts to Curb Profit Gains in 2016: Oper. profit will advance only “slightly” in 2016 amid deterioration in yields as Eurowings adds flights in long-haul market, where Lufthansa traditionally makes most of its money, and competition from low-cost rivals intensifies in Europe

- LafargeHolcim Sees Demand Growing After 2015 Profit Falls: Says overall demand to rise 2% to 4% in 2016, co. says it has made progress towards asset sales target; 2015 adj. operating Ebitda fell 10.7% to CHF5.75b vs est. CHF5.73b

- Swiss Keep Franc Intervention Threat Alive as Rates Left on Hold: SNB holds deposit rate at minus 0.75% as forecast by economist, repeats pledge to intervene in FX markets

- Norway Cuts Rates and Signals More Easing Ahead Amid Oil Plunge: Overnight deposit rate was lowered by 25bps to 0.50%

- HeidelbergCement Boosts Dividend Amid Expected 2016 Growth: Raises div. 73% to EU1.30/share, sees “moderate” improvement in 2016 profit

- Gulf Keystone Tumbles to Seven-Year Low as Future in Doubt: Kurdistan-focused oil company faces “material uncertainties”

- Bank of England Has Nowhere to Go With ‘Brexit’ in Limelight: Key rate will be kept at record low 0.5%, economists predict

In FX, early European flow has seen a continuation of the USD fallout from the Fed adjustment in rate hike projections for 2016. Commodities and their related currencies have benefited the most , notably USD/CAD, which is has torn through a series of support levels including 1.3000 to hit 1.2941. WTI is now looking to a move through $40.0, and the CAD seems to have pre-empted this to a degree, but near term stagnation in the Oil price sees some consolidation back around 1.3000 for now. AUD/USD took out .7600 in Asia, having previously contained the upside, but since then we have gone on to hit .7650. EUR/USD has had an easy ride on the upside and has traded to just shy of 1.1300, while EUR/GBP gains stalling at .7900 to allow for a Cable extension through 1.4300 , but lacking momentum here. USD/JPY is the one we are all watching from current levels, having taken out 112.00 to put 111.00 (double bottom) under threat. 111.45 is the low here so far, but now major pullback to note in the current climate.

The Bloomberg Dollar Spot Index, which tracks the U.S. currency against 10 major peers, sank 0.9 percent at 10:18 a.m. in London, after losing 1.1 percent in the last session.

“Currency reaction suggests market expectations for the Fed’s rate outlook were slightly more bullish,” Hiroshi Kurihara, chief U.S. economist at Bank of Tokyo-Mitsubishi UFJ Ltd. in New York. “The dollar’s been sluggish despite some positive signs over growth, hinting that it’s sensitive to negative news and that its advance may not be strong even as a rate hike approaches.”

The yen strengthened 0.8 percent versus the dollar, while the British pound rose 0.3 percent and Switzerland’s franc gained 0.4 percent. The Bank of England is forecast to leave interest rates unchanged on Thursday and maintain current stimulus levels, while the Swiss National Bank stuck with its ultra-loose monetary policy. The Norwegian krone appreciated 1.1 percent after a cut in borrowing costs.

In commodities, WTI and Brent continue to rally after yesterday’s FOMC comments with WTI close to testing the USD 40/bbl level. Gold also benefited from the FOMC reaching highs of USD 1267.60/oz while platinum and palladium are also appreciating respectively . In base metals Zinc advanced for the first time this week amid global production fell for a second month, while copper and iron ore prices were bolstered with the latter gaining over 4% amid the heightened risk sentiment. However, analysts at Jinrui futures did highlight that the market is waiting to see signs of Chinese demand given the increase in inventories and slowing physical trade.

Bulletin Headline Summary from RanSquawk and Bloomberg

- European equities fail to sustain opening gains as weakness in financials and the downbeat outlook for global growth prospects grips investor sentiment

- Early European FX flow has seen a continuation of the USD fallout from the Fed adjustment in rate hike projections for 2016

- Looking ahead, highlights include the BoE rate decision, US weekly jobs, Philadelphia Fed Business Outlook, JOLTS, and EIA Nat. Gas Storage Change

Treasuries rally overnight, global equity markets mostly lower and commodities rally after more a dovish FOMC statement and SEP than foreseen; today’s economic data includes jobless claims, JOLTS Job Openings.

Bank of England will announce their latest decision today together with minutes of their discussions. Investors are pricing in 20% chance they will cut benchmark interest rate this year

The Bank of Japan’s negative interest rate policy is making it more expensive for domestic banks to hedge dollar investments, threatening to slow their escape from negative rates into U.S. currency debt

Even with a 25% drop in the yen’s value, Japanese export volumes are basically unchanged from where they were when Prime Minister Shinzo Abe took office

Norway’s central bank cut its benchmark interest rate 25 basis points to a record low 0.50% and signaled it’s prepared to ease policy further to ward off a recession in western Europe’s biggest crude oil producer

Switzerland’s central bank held interest rates at a record low and repeated its pledge to intervene in currency markets, a threat President Thomas Jordan has used to keep the franc from strengthening

As Wall Street leaders warn publicly about this quarter’s plunging revenue from trading and deals, Goldman Sachs has provided no guidance. The mystery isn’t whether it is getting hit too — it’s how hard

$2.5b IG corporates priced yesterday; WTD $19.61b, MTD $106.03b, YTD $400.28b; $665m HY priced yesterday, MTD 13 deals for $7.315b, YTD 38 deals for $22.165b

Sovereign 10Y bond yields lower; European, Asian equity markets mostly lower; U.S. equity- index futures steady. WTI crude oil, copper, gold rise

DB’s Jim Reid concludes the overnight wrap

Although we saw the Fed closer align its rates expectations with those of the market, the market pushed Fed Funds expectations back even further with the probability of a June hike taken down to 38% (from 54%). Yellen made mention in her press conference of the April meeting being ‘live’ – which is unlikely to be surprising given her preference for optionality – although the market clearly sees that as an even longer shot now with the probability down to 8% this morning, after being at 25% just 24 hours ago.

Away from the Fed, it’s worth adding that Oil (+5.83%) rebounded hard yesterday (and is up further this morning) and in turn wiped out the heavy losses from Monday and Tuesday. That more than played its part in the price action for risk assets with the surge coming on reports that Saudi Arabia and other oil exporters will limit output levels even if Iran refuses to cooperate. According to the WSJ, Qatar have been reported as saying that they will host a meeting on April 17th for both OPEC and non-OPEC members to discuss such measures, although we highlight that this date has appeared to be pushed back on a number of occasions now.

Looking at the latest in Asia, aside from a drop in the Nikkei (-0.73%) with the stronger Yen weighing on markets there, bourses elsewhere are trading with broad based gains with the Hang Seng (+1.02%), Shanghai Comp (+0.88%), Kospi (+0.70%) and ASX (+0.96%) all up strongly. Credit indices are performing strongly too with the iTraxx Aus and Asia indices 5bps and 4bps tighter respectively. Asia FX is also posting some solid gains, while the Aussie Dollar is up over half a percent following an unexpected fall in the unemployment rate data this morning.

Back to yesterday and a quick recap of the economic data. As noted earlier, core inflation for the US in February was up a slightly better than expected +0.3% mom last month (vs. +0.2% expected) which has helped to nudge the YoY rate up one-tenth to +2.3% and the highest now in five years. Headline inflation was as expected at -0.2% mom last month, with the YoY rate down four-tenths to +1.0%. Elsewhere we saw industrial production disappoint with a -0.5% mom decline in February and more than expected (-0.3% expected) with utilities and mining output both contributing to the slump. Capacity utilization was down four-tenths to 76.7% (vs. 76.9% expected) although there was some better news in the latest manufacturing production data which showed a better than expected +0.2% mom gain last month (vs. +0.1% expected). Elsewhere, last month’s housing starts data showed a robust +5.2% mom increase (vs. +4.6% expected) although permits slipped -3.1% mom (vs. -0.2% expected).

In Europe yesterday price action was pretty benign which was of little surprise ahead of the Fed. The Stoxx 600 (+0.04%) closed barely unchanged while credit indices were flat to slightly wider (iTraxx sub fins being the notable underperformer, closing 10bps wider). Notable during the European session however was the €24bn of primary bonds issuance which priced in Europe which was the biggest volume day in two years and the week-to-date volume so far the second busiest YTD.

Looking at the day ahead now, this morning in Europe the notable data to be released will be the final revision to the February CPI report for the Euro area (no change to -0.2% yoy headline expected) along with the January trade balance. While the dataflow is light, there’s no shortage of central bank meetings however with the BoE, SNB and Norges Bank all due to announce their latest policy decisions – the latter the only one where the market is expecting a change with a 25bps cut to the deposit rate expected (to 0.5%). This afternoon in the US it’s another reasonably busy afternoon of data. The Philly Fed business outlook for March will be closely watched, while we’ll also receive employment data in the form of initial jobless claims and JOLTS job openings for January. The Conference Board’s February leading indicator will also be released.

Let us begin;

ASIAN AFFAIRS

Late WEDNESDAY night/ THURSDAY morning: Shanghai closed UP BY 35.11 POINTS OR 1.22% , / Hang Sang closed UP by 246.11 points or 1.21% . The Nikkei closed DOWN 38.07 or 0.22%. Australia’s all ordinaires was UP 0.68%. Chinese yuan (ONSHORE) closed UP at 6.47800. Oil ROSE to 39.07 dollars per barrel for WTI and 40.91 for Brent. Stocks in Europe so far ALL IN THE RED . Offshore yuan trades 6.4751 yuan to the dollar vs 6.4780 for onshore yuan/yesterday China’s industrial production collapsed along with retail sales. JAPAN RE SIGNALS that they may continue with nirp a little longer which sends the USA/Yen spiraling northbound/markets in Japan tumble (see below). Japan’s exports plummet (see below).Yesterday China signals that they are going to tax financial transactions. This morning they raise the yuan trapping the shorts with huge losses (see below)

.

report on Japan

Japan exports to the USA collapse. However imports collapse even more as their trade balance improves. However it is not a good sign in an economy when both exports and imports collapse!

Japanese Exports To US Plunge Most Since 2011 As Weak Yen Tailwind Evaporates

Japan just posted its largest trade surplus in 5 years (+JPY243bn) as exports dropped 4% YoY (worse than expected) but imports fell 14.2% (better than expected). However, the biggest standout was the ongoing deterioration in Japanese exports to the US which dropped by the most since 2011 as the ‘advantages’ of a devalued currency appear to have hit their limit. Time for some more devaluation Abe… or Peter Pan(ic).

“The tailwind from the weak yen has gone. We can’t help but hold a pessimistic view on the outlook for exports,” said Atsushi Takeda, an economist at Itochu Corp. in Tokyo, said before the figures were released. “Domestic demand won’t be dependable at all, and the same goes for exports. I can’t deny the possibility of another economic contraction this quarter.”

BOJ Intervenes After USDJPY Plunges To QQE2 Lows, Nikkei Crashes 700 Points

Nikkei futures rallied post-Fed into the Japaense open (despite weakness in USDJPY) and then when trade data struck (and exposed the utter failure of competitive devaluation), everything went into freefall. The Nikkei crashed 700 points and USDJPY plunged to its lowest since QQE2… and then – on cue – “someone” started panic selling JPY…

And just as USDJPY hit QQE2 lows – so someone stepped in large…

Which juiced NKY back up…

Report on China

P2P Property Lending Explodes In China; Officials Panic

PBoC governor Zhou Xiaochuan thought about it, and decided it’s probably not a good idea for borrowers to get P2P loans for down payments on homes.

In fact, he said last weekend, it’s illegal: “Funds used for down payments cannot be borrowed.”

Vice-governor Pan Gongsheng, one of Zhou’s deputies, echoed his sentiments. “Property agencies and developers are not qualified to conduct financial business. They are illegally doing financial business,” he explained. “This business they are engaged in, and jointly with peer-to-peer lenders and down payment credit firms, has not only raised the leverage of residents’ house purchases, worn down the effectiveness of macro policy controls and added to financial risks, but has also increased risk in the property market.”

Now you might think that what’s implied there is too bad to be true – even in the increasingly ludicrous world of P2P and marketplace lending. But in fact, P2P lenders in China have indeed been funding down payments on homes, embedding an enormous amount of excess leverage into the market while simultaneously driving up prices in Tier-1 cities.

“Home sales in Beijing, Shanghai, Guangzhou and Shenzhen, China’s ‘first-tier’ cities, grew 14% last year compared with about 7% nationwide,” FT reports. “In Shenzhen, the average price per square meter in February increased by about 50% compared with a year earlier, according to Soufun, a real estate consultancy.”

Theoretically, this shouldn’t be happening. Although Beijing has gradually relaxed the rules on down payment requirements for both first- and second-homes in an effort to boost the economy, FT reminds us that “in the wake of the collapse of the US housing market in 2008, China launched restrictions on mortgages to rein in the country’s then red hot property market, which was part-fuelled by speculation on borrowed money.”

But as we noted late last month, shadow banking has a way of creeping into every market in China and as soon as you stamp out one conduit, another pops up in an endless game of Whack-a-Mole. Somehow, leverage always finds a way.

Over the past year or so, a new phenomenon has emerged: P2P lending for down payments on homes, and as we alluded to above, it’s just as utterly insane as it sounds. Bloombergrecounts one borrower’s experience:

When Fu Songtao found his ideal home in the suburbs of Shanghai, he faced the typical problem of would-be homebuyers: Coming up with enough cash for a down payment. So Fu turned to an online solution. His property agent offered him a zero-interest loan, funded entirely online by peer-to-peer lenders, that covered almost half his deposit.

“Everybody I know took out these loans,” said Fu, a 29-year-old employee of a state-owned enterprise, who borrowed 380,000 yuan ($58,000) a year ago, with interest payments to lenders subsidized by the property agent, for his 3 million yuan apartment, and has seen its value increase to 3.3 million yuan since. “If you can borrow like that, why not?”

Right, “why not?” One reason is because you are effectively taking out a zero down payment mortgage. If you can’t figure out the problem with that then you probably have no business buying a home in the first place.

In any event, this type of lending is proliferating – at a rapid clip. In fact, according to Bloomberg, “peer-to-peer lending for property in China grew more than six times fasterthan loans extended through banks last year” to $18 billion. That’s up 163% over 2014 and dwarfs the 21% increase in outstanding mortgages.

In some ways this is a self-fulfilling prophecy. That is, borrowers (and speculators) see the price gains the practice is fuelling and, not wanting to miss out, dive in as well, driving prices still higher and perpetuating a kind of greater fool boom. Have a look, for instance, at the following chart which shows that China’s housing bubble – at least in Tier-1 cities – is alive and well:

As we put it last month, “now that the Chinese stock market bubble has burst, the local population has to find a new asset class which to chase for the next few months, and for the time being that asset is housing; and since the politburo gets to boast that the Chinese economy is ‘improving’ as a result of this scramble, no ‘macroprudential brakes’ will be deployed before it is again too late.”

Well, when it comes to macroprudential brakes, the Politburo might be prepared to make an exception for P2P down payment loans. Just as P2P lenders were forbidden from loaning money for stock purchases last summer, so too is Beijing set to ban P2P loans for down payments. “New rules being drafted by the central bank, the China Banking Regulatory Commission and other bodies would bar developers, peer-to-peer networks and other non-banks from offering down-payment loans,” Bloomberg writes. “Banks would be required to scrutinize mortgage applications and reject those with deposits funded by loans.”

“[External financing] started to boom in 2014, helped by online and mobile technologies,” Clement Luk, chief executive officer for eastern China at realtor Centaline, told Reuters, who also notes that “property loans account for around 15 percent of all online financing in China, according to Xu Hongwei, chairman of a data provider on the business, Wangdaizhijia.” Shanghai-based Yingcan says the number is far higher, at 23%.

And while at least one broker is already under investigation for facilitating down payment loans, analysts say the sector will be difficult to police, given the fact that lenders brand them with innocuous names that would not immediately indicate that they were made for down payments on property. Here’s BofAML with a bit of color on the market:

The overall property market recovery that began in the spring of 2015 has been supported by a string of monetary-easing measures and supportive property policies. Moreover, the pursuit of capital gain and lack of attractive alternative investments amid the economic downturn have stimulated purchase demand in Tier-1 cities and helped fueling up prices while the supply remains tight. A recent Xinhua News article has warned about housing speculation, especially in Shenzhen, suggesting speculative purchases account for 30% home transactions at present. Home mortgages loan as a percentage of total loans are still relatively low, at 10.1% in Beijing, 14.5% in Shanghai and 22.9% in Shenzhen, vs. 15.4% nationwide. However, there are some other forms of leverage gaining its popularity to speculate in the Tier-1 housing markets, such as mortgage down-payment loans provided by some property agents and P2P platforms. But the size of such loans should still be quite small. For example, the outstanding loans by Lianjia (a leading player in this field) are at RMB2.9bn currently, with typical maturity of 90 days.

If the typical maturity is 90 days and with interest rates sometimes running as high as 2% per month, it seems rather clear to us that borrowers might indeed default en masse should the economy take a decisive turn for the worst and should Beijing live up to its promise of stripping excess capacity from the industrial sector.

On the other side of the equation, lenders are promised returns of up to 10% per year for financing this madness.

Of course this is, like the rest of China’s shadow banking sector, a Catch-22 for Beijing. If China cracks down on down payment loans, it may curtail the property market and thus dent the economy. If they don’t crackdown, more and more leverage will be embedded into the system making the eventual collapse that much more spectacular. Summing up the government’s dilemma is Hu Xingdou, an economics professor at the Beijing Institute of Technology:

“China has learned a lesson from the U.S. subprime crisis. The Chinese government understands that they have to solve problems like housing and overcapacity. At the same time, they can’t bring further risks to the financial system, as the banks already have a lot of bad debt.”

END

RUSSIAN AND MIDDLE EASTERN AFFAIRS

The following is a big story as the Syrian Kurds want a separate state. They were not invited to Geneva but they are now declaring a proto state on Turkey’s border.

This is exactly, the worst nightmare for Erdogan

(courtesy zero hedge)

In Dramatic Move, Syrian Kurds Set To Declare Proto-State On Erdogan’s Border

Well, Turkish President Recep Tayyip Erdogan’s worst nightmare is about to come true.

For days there have been rumors that Syria might attempt to adopt some manner of federal system at peace talks in Geneva as a kind of compromise on the way to negotiating a political solution to the country’s five-year conflict that’s killed some 300,000 people and created the worst refugee crisis Europe has seen since World War II.

But one of the problems with the “peace talks” is that no one who really matters in terms of the opposition was invited. The High Negotiations Committee (which represents a collection of Saudi-backed anti-Assad elements) is only comprised of representatives from the “moderate” rebels and let’s face it: Russia and Hezbollah just rolled most of them up in five short months, all but forcing them to surrender at Aleppo.

So it’s not even clear what a federal system would look like with the FSA and the other “moderates.” How would they administer anything in their current depleted condition especially considering they’d live under constant threat of attack from the half dozen (at least) jihadist elements operating in the country?

The groups who are actually still capable from an operational perspective are al-Nusra, ISIS, and of course, the Kurds (the YPG). Now obviously, you can’t exactly invite ISIS or al-Nusra to Geneva (even though you can, apparently, arm them and send them money), but you could certainly have invited the Syrian Kurds who have been exceptionally effective at battling extremists and who control the entire northern part of the border with Turkey save one small strip west of the Euphrates.

(Kurdish controlled areas are in purple)

But when the Kurds checked the mail for their Geneva invitation they discovered that as usual, they got the short end of the stick (no doubt thanks to Erdogan). But that’s ok. Because now,they are simply going to take matters into their own hands and declare a federal system.

“After being excluded from the talks in Geneva, which began on Monday, [the Kurds] are drawing up plans to combine three Kurdish-led autonomous areas of northern Syrian into a federal arrangement,”Reuters reports, adding that “Aldar Khalil, a Kurdish official and one of the organizers, said he anticipated the approval of a new system, and ‘democratic federalism’ was the best one.”

Idris Nassan, another Kurdish official, told Reuters he also expected a declaration of federalism.

According to a document seen by Reuters, the Kurds felt the step was necessary because they “envision the failure of U.N.-led peace talks in Geneva.”

“The system envisions areas of democratic self-administration that will manage their own economic, security and defense affairs,” the document asserts. The details, Kurdish officials said, would be worked out later. The name of the new proto-state: “The Federal Democratic System of Rojava-North Syria.”

“Now the conference has just started in Rmelan, about 200 representatives of Rojava have joined [the event]. They represent different ethnicities and nationalities. There are Kurds, Arabs, Assyrians, Syriacs, Turkomans, Armenians, Circassians and Chechens,” Barzan Iso, a Kurdish journalist, told RT. “Also we have representatives from the Syrian democratic forces, YPG, women defense units.”

“Within days, probably today, self-governing [bodies] of three Kurdish cantons in Syria’s north will declare a federation,” Abd Salam Ali, a PYD party rep in Moscow, told RIA Novosti “Separation of Rojava [Western Kurdistan] from Syria is not an option. We remain [a part of Syria], but declare a federation,” he said.

From a common sense perspective this makes perfect sense. The Kurds have been defending themselves against virtually everyone for years in Syria and not only that, they managed to make territorial gains while fending off random shelling from inside of Turkey. They’re certainly in a better position to govern themselves than any other group operating in the country including the Alawite government and those who are still loyal to it.

Of course this is just about the last thing Erdogan wants to see. Ankara equates the YPG with the PKK and thus with terrorism and worse, Erdogan fears that a Kurdish state on his border will embolden Kurds in southeast Turkey – who, you’re reminded are under bloody seige by government forces that allegedly burned 150 people alive in Cizre last month – to declare autonomy, something the pro-Kurdish HDP supports.

For their part Russia is firmly on the side of the Kurds after demanding that they be invited to Geneva.

“If the Kurds are ‘thrown out’ of the negotiations on Syria’s future, how can you expect them to want to remain within this state?” Sergei Lavrov asked in an interview with Russian REN TV channel that aired on Sunday.

Good question.

“The second round of inter-Syrian talks is underway in Geneva, but Syrian Kurds were not invited. It means that the future of Syria and its society is decided without Kurds. In fact, we are pushed back into a conservative, old-fashioned system which does not fit well with us,” Rodi Osman, the head of Syrian Kurdistan’s office in Moscow, told RIA Novosti. “In light of this, we see only one solution which is to declare the creation of [Kurdish] federation. It will serve the interests of the Kurds, but also those of Arabs, Turks, Assyrians, Chechens and Turkomans – all parts of Syria’s multinational society.

And with that, we can start to see how the next conflict in Syria begins. Erdogan has already shelled the Syrian Kurds in the past month and he’s made it very clear that a Kurdish state on his borders would not be tolerated. “Unilateral moves carry no validity,” the Turkish foreign ministry said, in a terse statement. Ankara will now use every PKK attack and every suicide bombing as an excuse to attack the new proto-state and Erdogan will probably invade later on down the road on the excuse that he’s not invading Syria, but rather a hostile country that supports terrorist elements in southeast Turkey.

Note that you heard it here first.

Turkey’s Erdogan Goes Full-Dictator: Designates Journalists And Teachers As “Terrorists”; Arrests Lawyers

“It is not only the person who pulls the trigger, but those who made that possible who should be defined as terrorists, regardless of their title,” Turkish President Tayyip Recep Erdogan said on Monday, in an attempt to convince parliament to include journalists, politicians, academics, and activists under the country’s anti-extremism laws.

Erdogan’s comments came a day after the latest in a string of suicide bombings ripped through Ankara, killing 34 and wounding more than 100 in Kizilay. Since then, Turkey has arrested nearly 50 people with “suspected ties” to the PKK against which Erdogan is waging a highly personal crusade.

Apparently, the President doesn’t think parliament is moving fast enough on his “request” to expand the definition of “terrorist” because in a speech on Wednesday, he effectively instructed lawmakers to get moving before also urging parliament to deal with “the issue of immunities.”

Erdogan desperately wants to prosecute HDP members who he says are guilty of “inciting terrorism.” “We must swiftly finalize the issue of immunities,” he said. “Parliament must take steps on this issue swiftly,” he added, as if the first statement was in some way unclear.

(Erdogan gets it, why don’t you?)

But frankly, we’re not even sure why he bothers parliament with these things. Erdogan is going to do whatever Erdogan wants to do. We’re talking about a man who arrested two of the country’s preeminent journalists and had the nerve to charge them with “deliberately aiding a terrorist organization” when what they were in fact doing was exposing Erdogan for… wait for it… deliberately aiding a terrorist organization.

And if that’s not absurd enough for you, there are countless other examples including an incident which saw a medical doctor put on trial for posting a picture of the President next to a picture of a fictional creature from a Tolkein novel on social media.

Turks are in fact so scared of their “leader” that just last month, a Turkish truck driver literally sued his own wife for cursing at Erdogan when he spoke on television. “I warned her,” the man later said.

True to form, Erdogan didn’t wait on parliament to expand the definition of “terrorist” before he went ahead and arrested three academics for “terrorist propaganda” after they made the mistake of publicly asking the government to stop the siege on Cizre and other cities in the predominantly Kurdish southeast.

“More than 2,000 academics signed a petition in January criticizing military action in the southeast, including round-the-clock curfews aimed at rooting out PKK militants who have barricaded themselves in residential areas in southeastern cities,” Reuters notes. “The petition outraged President Erdogan, who said the academics would pay a price for their ‘treachery’“.

A few days ago, a group of lawyers made the mistake of holding a press conference to defend the academics who signed the aforementioned petition. On Tuesday, Erdogan arrested the lawyers too.

Finally, when a British citizen who teaches at Bilgi University showed up at the courthouse to support the lawyers, he was also arrested. His crime, in his own words: “I am accused because I had several invitations to Kurdish new year (celebrations on March 21) published by the HDP – the third-largest party in the Turkish parliament – in my bag.”

So there you go. Lessons learned all around we suppose.

Better still, the President says he plans to start campaigning in April for his long-planned push to expand the powers of the presidency (because clearly he’s not powerful enough). Erdogan will look to rewrite the constitution (literally) in order that it might, inBloomberg’s words, “feature a strengthened presidency while retaining a key role for the parliament.”

Yes, “a key role for parliament,” where the third largest party is about to have their immunity stripped away so that Erdogan can prosecute the whole lot of them for being terrorists.

Erdogan, Bloomberg goes on to write, “has devoted much energy to expanding the executive role of what’s traditionally been a largely ceremonial post, arguing that strong leadership will help extend a record of economic growth [but] only holds 317 seats in the 550-member parliament, short of the 330 votes needed to take a new charter to a public vote.”

Trust us. He’ll get it to a referendum. Votes or no votes. And then he’ll rig the referendum.

Clearly, Nihat Ali Ozcan at the Economic Policy Research Foundation in Ankara (who spoke to Bloomberg) doesn’t get it: “The PKK is engaged in a direct confrontation with Erdogan with the aim of preventing him from turning his office into an executive presidency. However,Erdogan may benefit from a growing nationalist backlash in his campaign for a presidential system, as long as he maintains his crackdown on the PKK.”

Gee, do you think so?

That’s been the entire gambit since last June’s elections. Erdogan lost ground to the pro-Kurdish HDP and so, he used the war on ISIS as an excuse to deliberately restart the conflict with the PKK in order to convince the public that it needs his protection lest the entire country should descend into chaos. Three months and a whole lot of lost lives later, AKP performed better in a November redo election that Erdogan – gun to his head – was “forced” to call when the coalition building process was sabotaged fell apart in August.

We have no doubt that Erdogan will succeed one way or another in his bid to rewrite the constitution. Even if it kills him. Or wait. No. Even if it kills you.

GLOBAL ISSUES

Norway Cuts Rates, Hints At NIRP, QE As Central Bank Falls (Way) Behind In FX Wars

We’ve long said the Norges Bank would ease in March in the face of falling crude prices and the continuation of the negative rates regime at the ECB, the Riksbank, and the NationalBank.

Indeed by the time of today’s announcement, the market was pricing in a ~75% chance that Oystein Olsen would cut rates by 25 bps. And he didn’t disappoint, slashing the depo rate to 0.50%. Incidentally, we’d hate to be the 1 economist out of 20 surveyed by Bloomberg that managed to miss this one.

The picture in Norway is clouded by a number of factors.

Obviously, the economy is heavily dependent on oil, and the sharp decline in prices has taken a significant bite out of revenue. At the same time, falling crude has also put pressure on the NOK, which has naturally adjusted downward with oil, providing somewhat of a cushion for the country’s economy.

Still, there are two factors that prevent the currency from adjusting as much as it otherwise might: 1) competitive easing from the ECB, the Riksbank, the NationalBank, and 2) the fact that when Norway taps into oil revenues to provide fiscal stimulus to the economy, the Norges Bank becomes a buyer of NOK. We explained the latter dynamic in detail here, but suffice to say that in February, the bank bought 900 million kroner per day, a marked increase from previous purchases. Here are two simple graphics which show that when the budget deficit began to catch up with oil revenues, the Norges Bank began buying NOK: