Gold: $1,248.20 up $4.40 (comex closing time)

Silver 15.87 up 3 cents

In the access market 5:15 pm

Gold $1248.40

silver: 15.87

Let us have a look at the data for today.

At the gold comex today, we had a good delivery day, registering 61 notices for 6100 ounces and for silver we had 65 notices for 325,000 oz for the active March delivery month.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 212.48 tonnes for a loss of 90 tonnes over that period.

In silver, the open interest rose by 487 contracts up to 177,016 despite the fact that the silver price was up by 3 cents with respect to yesterday’s trading . In ounces, the OI is still represented by .885 billion oz or 127% of annual global silver production (ex Russia ex China).

In silver we had 65 notices served upon for 325,000 oz.

In gold, the total comex gold OI rose 840 contracts to 504,152 contracts despite the fact that the price of gold was DOWN $10.00 with yesterday’s trading.(at comex closing). .

No changes tonight in the GLD/ thus the inventory rests tonight at 821.66 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,/we had a huge deposit of 1.809 million oz in inventory, and thus the Inventory rests at 330.342 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver rose by 487 contracts up to 177,016 as the price of silver was up 3 cents with yesterday’s trading. The total OI for gold rose by 840 contracts to 504,152 contracts despite the fact that gold was down $10.00 in price from yesterday’s level.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

3. ASIAN AFFAIRS

i)Late MONDAY night/ TUESDAY morning: Shanghai closed DOWN BY 18.13 POINTS OR 1.94% , / Hang Sang closed DOWN by 17.40 points or 0.08% . The Nikkei closed UP 323.74 . Australia’s all ordinaires was DOWN 0.32%. Chinese yuan (ONSHORE) closed DOWN at 6.4923. Oil ROSE to 41.36 dollars per barrel for WTI and 41.46 for Brent. Stocks in Europe so far ALL IN THE RED . Offshore yuan trades 6.49310 yuan to the dollar vs 6.4923 for onshore yuan/LAST WEDNESDAY, China’s industrial production collapsed along with retail sales. JAPAN RE SIGNALS that they may continue with nirp a little longer which sends the USA/Yen spiraling northbound/markets in Japan tumble . Japan’s exports plummet.LAST WEDNESDAY, China signals that they are going to tax financial transactions. Since nobody has a handle on Chinese foreign exchange, the IMF politely asks how large is its forward book on currencies. Many believe it is over 300 billion and that would be a future payment

.

report on Japan

non today

.

ii) report on China

We have been pointing this out to you on several occasions. The Chinese are using forwards to hide their exposure to depleting USA reserves. Basically by using derivatives they delay the exit of USA dollars by the length of derivative contracts. It is believed that China has in excess of 300 billion of USA exit exposure.

(courtesy zero hedge)

ii)Three blasts, two at the Belgium airport and one at subway stations: Maelbeek,

The terror attack in Belgium heightens Brexit risk as UK wants no part of the European mess with the migrants

( zero hedge)

OIL MARKETS

i)Canada’s regulators are warning banks with their under reserves with respect to energy losses:

( zero hedge)

ii)Oil rises on another freeze moment

iii)Crude drops on huge inventory build

i)Confidence in Europe falling apart after the Belgium bomb blast.

ii)India resumes gold purchases(Dave Forrest/Piece Points)

iii)Craig mirrors my thoughts exactly how the crooks are manipulating gold at the comex//a must read….

i)It is now 8 straight weeks, that the “smart money” has sold stocks as they do not believe the rally. They must have read David Stockman. (see next article after this one)( zero hedge/Bank of America)

ii) David Stockman continues with his rant on the phony earnings report on the S and P and the very dangerous Keynesian, Janet Yellen:

iii)Bill Gross: the collapse of Valeant is a preview of the failure of global monetary policy:( zero hedge/Bill Gross)

iv)This confirms the Chicago National Mfg index which shows manufacturing on a national level falling apart.

( zero hedge)

v)What an absolute joke!! Richmond Fed spikes the most in HISTORY

( zero hedge)

vi)Very respected journalist,William Engdahl writes on the Clinton emails:

And now for the wild silver comex results. Silver OI rose by 487 contracts from 176,529 up to 177,016 despite the fact that the price of silver was up by 3 cents with yesterday’s trading. The next big active contract month is March and here the OI fell by 82 contracts down to 347 contracts. We had 78 notices served upon yesterday, so we lost 4 contracts or an additional 20,000 ounces will not stand for delivery. The next contract month after March is April and here the OI rose by 46 contracts up to 408. The next active contract month is May and here the OI rose by 498 contracts up to 122,954. This level is exceedingly high. The volume on the comex tod

Let us head over to the comex:

The total gold comex open interest rose to 504,152 for a gain of 840 contracts as the price of gold was down $10.00 in price. Expect our bankers to undergo relentless attacks on our two precious metals. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month or for that matter an inactive month, and 2) a continual drop in the amount of gold standing in an active month. Today, both scenarios were in order. The front March contract month saw its OI fall by 517 contract down to 132.We had 37 notices filed upon yesterday, and as such we lost 480 contracts or an additional 48,000 oz will not stand for delivery. .After March, the active delivery month of April saw it’s OI fall by 29,016 contracts down to 208,851. This high level is scaring our crooked bankers. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was 284,501 which is very good.. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was very good at 250,736 contracts. The comex is in backwardation until April .

And now for the wild silver comex results. Silver OI rose by 487 contracts from 176,529 up to 177,016 as the price of silver was up by 3 cents with Monday’s trading. The next big active contract month is March and here the OI fell by 82 contracts down to 347 contracts. We had 78 notices served upon yesterday, so we lost 4 contracts or an additional 20,000 ounces will not stand for delivery. The next contract month after March is April and here the OI rose by 46 contracts up to 408. The next active contract month is May and here the OI rose by 498 contracts up to 122,954. This level is exceedingly high. The volume on the comex today (just comex) came in at 47,745 , which is very good. The confirmed volume yesterday (comex + globex) was good at 36,639. Silver is now in backwardation until April at the comex. In London it is in backwardation for several months.

March contract month:

INITIAL standings for MARCH

March 22/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 2,573.623 Oz manfra,Scotia

brinks,JPM, Delaware |

| Deposits to the Dealer Inventory in oz | 2999.99 oz Brinks |

| Deposits to the Customer Inventory, in oz | nil

|

| No of oz served (contracts) today | 61 contract (6100 oz) |

| No of oz to be served (notices) | 71 contracts(71,000 oz) |

| Total monthly oz gold served (contracts) so far this month | 683 contracts (68,300 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 181,826.5 oz |

Today we had 1 dealer deposit

i) Into Brinks: 2999.99 oz

Total dealer deposits; 2999.99 oz

Today we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

Today we had 0 customer deposits:

total customer deposits: nil oz

Today we had 5 customer withdrawals:

i) Out of Manfra: 64.30 oz

ii) Out of Brinks: 1,403.19 oz

iii) Out of HSBC: 304.377 oz

iv) Out of JPM: 404.984

v) Out of Delaware; 396.772 opz

total customer withdrawals; 2,573.623 oz

Today we had 0 adjustment:

MARCH INITIAL standings

/March 22/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 600,713.49 oz

Scotia |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 634,919.57 oz

CNT,Delaware |

| No of oz served today (contracts) | 65 contracts325,000 oz |

| No of oz to be served (notices) | 282 contract (1,410,000 oz) |

| Total monthly oz silver served (contracts) | 1114 contracts (5,570,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 10,751,457.1 oz |

today we had 0 deposits into the dealer account

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 2 customer deposits

i) Into CNT: 600,329.340 oz

ii) into Delaware: 34,590.23 oz

total customer deposits: 634,919.57 oz

We had 1 customer withdrawal:

i) Out of Scotia:

600,713.49 oz

:

total customer withdrawals: 600,713.49 oz

we had 1 adjustment

i) Out of Brinks: 5,032.810 oz was adjusted out of the dealer account and this landed into the customer account of Brinks

And now the Gold inventory at the GLD

March 22./no changes in inventory at the GLD/Inventory rests at 821.66 tonnes

MARCH 21/another big deposit of 2.68 tonnes/inventory rests tonight at 821.66 tonnes

(and this was done with gold down $10.00 today!!)

March 18.I GIVE UP!! WITH GOLD DOWN TODAY, THE CROOKS OVER AT GLD ADDED ANOTHER IDENTICAL 11.89 TONNES OF PAPER GOLD INTO THEIR INVENTORY.

INVENTORY RESTS THIS WEEKEND AT 818.98 TONNES. IF I WAS A SHAREHOLDER OF THIS ENTITY I WOULD BE VERY WORRIED.

March 17/we had a whopper of a deposit tonight: 11.89 tonnes/with London in backwardation this is nothing but a paper addition/inventory rests tonight at 807.09 tonnes

March 16.2016:/we had a deposit of 2.09 + 2.97(last in the evening) tonnes of gold into the GLD/Inventory rests at 795.20 tonnes

March 15/ no changes in gold inventory at the GLD/Inventory rests at 790.14 tonnes

March 14/a huge change in gold inventory at the GLD, a withdrawal of 8.63 tonnes/Inventory rests at 790.14 tonnes

March 11 /despite the high volatility of gold last night and today, somehow the GLD added 5.95 tonnes of gold without disturbing anyone./inventory rests this weekend at 798.77 tonnes

March 10/a deposit of 2.08 tonnes of gold into the GLD/Inventory rests at 702.82 tonnes

March 9/a withdrawal of 2.38 tonnes of gold from the GLD/Inventory rests at 790.74

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

March 22.2016: inventory rests at 821.66 tonnes

end

And now your overnight trading in gold, TUESDAY MORNING and also physical stories that may interest you:

By Mark O’Byre

Global Stocks Fall, Bonds and Gold Rise After Terrorist Attacks In Brussels

Safe haven assets, gold, silver and German bonds rose, while European stocks and global stock futures fell, after explosions rocked Brussels airport departure hall and a subway station near the EU parliament and other important EU institutions. At least 26 people are reported to have been killed after the explosions which the Belgian prosecutor has alleged are terrorist attacks.

Asset Performance – March 22, 2016 (Finviz)

Gold in dollar terms rose 0.8% but the gains were greater in euro and sterling terms. Gold in euros terms rose from €1,108/oz to €1,123/oz or 1.3% and gold in sterling rose from £865/oz to £881.50/oz or nearly 2%.

Silver also saw a safe haven bid and moved higher with gold to reach $16.oo/oz again. Silver also saw a safe haven bid and moved higher with gold to reach $16.00/oz again. Silver in euro and sterling terms rose to multi month highs.

The German DAX fell by nearly 1% and the Stoxx Europe 600 Index fell the most in a week as the attacks caused deaths and injuries and spurred fears of imminent follow-up attacks in the capital of the European Union and internationally.

Travel and leisure shares including airlines and hotels led the slide and futures on the Standard & Poor’s 500 Index also declined. Global stock markets fell from multi-week, month and annual highs as reports on the scale of the carnage in the Belgian capital unfolded.

Gold in EUR – 24 Hours (GoldCore)

The yield on 10-year bunds touched the lowest in almost two weeks, while gold gained for the first time in four days as investors sought safer assets.

The pound dropped by even more than than the euro and against all its major peers amid increasing concerns about the UK electing to ‘BREXIT’ and the ramifications of BREXIT for UK companies, the wider economy and indeed sterling.

Gold Prices (LBMA)

22 Mar: USD 1,251.80, EUR 1,117.35 and GBP 876.96 per ounce

21 Mar: USD 1,244.25, EUR 1,104.47 and GBP 863.60 per ounce

18 Mar: USD 1,254.50, EUR 1,112.93 and GBP 868.78 per ounce

17 Mar: USD 1,269.60, EUR 1,119.40 and GBP 883.17 per ounce

16 Mar: USD 1,233.10, EUR 1,111.79 and GBP 874.09 per ounce

Silver Prices (LBMA)

22 Mar: USD 15.89, EUR 14.16 and GBP 11.12 per ounce

21 Mar: USD 15.81, EUR 14.02 and GBP 10.99 per ounce

18 Mar: USD 15.94, EUR 14.13 and GBP 11.02 per ounce

17 Mar: USD 15.78, EUR 13.86 and GBP 10.93 per ounce

16 Mar: USD 15.29, EUR 13.78 and GBP 10.84 per ounce

Gold News and Commentary

Global stocks fall, gold and govt bonds rise after Brussels explosions (Reuters)

Global stocks fall, gold rises after Brussels explosions (Marketwatch)

Gold ends below $1,250 as Fed officials float April rate hike (Marketwatch)

Germany Continues Repatriation of Gold Reserves From Abroad (Sputnick)

Germany wants its gold back (Russia Today)

Gold’s appeal grows in era of volatile markets (PI Online)

What to avoid and what to buy as inflation makes a comeback (MoneyWeek)

These Eight EU Countries Are in the Budget Danger Zone (BBG)

Ireland gain a little but suffer most from Brexit – Moody’s (Independent)

`Brexit’ May Lead to Downgrades and Slower Economy, Moody’s Says (BBG)

Read More Here

Silver Coins – VAT Free Delivered In UK and EU

We are now delivering legal tender silver coins, VAT free, throughout the EU. Meaning US clients can take delivery of silver bullion coins anywhere in the EU and not pay VAT or sales tax. Silver coins and bars can also be owned tax free with GoldCore in vaults in Zurich, Singapore and Hong Kong.

2016 Silver Nuggets or Kangaroos (1 oz)

Silver bullion coins – like Silver Nuggets (Kangaroos), Eagles, Maples, Philharmonics and Britannias are great forms of insurance against currency debasement and financial collapse. They also make very nice gifts for loved ones and are a great way to pass on wealth to the next generation.

We have very competitive prices – some of the most competitive internationally. Secure your allocation of silver bullion coins by contacting us today.

Stock Dip-Buyers Active After Belgium Terror Attack Sparks Gold Pop, Oil Drop

While stock markets are modestly lower, and “off the lows”, perhaps in anticipation of the quite unbelievable panic-buying that occurred after the French terrorist attacks, investors have seemingly rotated from black gold to pet rocks for safety as the former drops back below $41 and the latterbounces back above $1250.

Gold up, Oil down… (notably gold appeared to rise notably ahead of the main headlines at around 430am ET)

And dip-buyers were piling-in after the initial plunge in stocks…

because remember what happened after Paris…

Because nothing says confidence-inspiration like the biggest terrorist attack in Europe in decades. It appeared someone wanted to “prove” that this attack was not meaningful. After Belgium now, we suspect it may be harder to suggest it is a one-off drop to be bought.

end

The Donald speaketh:

(courtesy Kitco/Donald Trump)

Gold at Fort Knox?

Donald Trump Doesn’t Think So

Tuesday March 22, 2016 13:20

(Kitco News) – Although he made this assumption nearly one year ago, the Donald’s comments on gold at Fort Knox – or lack thereof – are making the rounds on Twitter again Tuesday.

Republican frontrunner Donald Trump hinted at the idea that there just might be no gold in the U.S. “I like the gold standard and there is something very nice about it,” he said, in March 2015, in an interview with Josh McElveen, host of Conversation with the Candidate on ABC affiliate WMUR9. “We used to have a very solid country because it was based on a gold standard.”

However, according to the real estate mogul, it would be difficult to back the dollar by gold again. “It would be very hard to do at this point and one of the problems is we do not have the gold. Other places have the gold,” he said.

end

Strengths and weaknesses for gold and silver. The most important of these is negative interest rates and that should boost gold demand overseas.

(courtesy Lawrie on Gold/Lawrence Williams/Sharp’s Pixley)

Negative Interest Rates Boost Gold Demand Overseas – The Holmes SWOT

Frank Holme of U.S. Global Investors‘ weekly roundup of perceived Strengths, Weaknesses, Opportunities and Threats for Precious Metals

Strengths

- The best performing precious metal for last week was silver, up 2.87 percent. Investors own the most silver in exchange-traded products in seven months, boosting holdings from a three-year low, according to ZeroHedge. This rebound comes as hedge funds and other money managers hold a near-record bet on further price gains.

- Physical gold ETF holdings have increased by over 270 tonnes since reaching their cycle-low in early January, reports TD Securities, coinciding with an 18 percent rally in the gold price. In contrast, only three tons of gold have been collected so far in India’s newly announced deposit plan. Macquarie raised its 2016 gold forecast for the precious metal by 4.8 percent, while Morgan Stanley announced its gold price outlook for the year up 8 percent to $1,173 per ounce.

- Calico Resources Corp. and Paramount Gold Nevada Corp. announced this week that Paramount has agreed to acquire all of the issued and outstanding common shares of Calico. Particulars of the transaction show that holders of Calico Shares will be entitled to 0.07 of a share of common stock of Paramount, in exchange for each Calico Share held. This represents an implied offer premium of 49.2 percent per share.

Weaknesses

- The worst performing precious metal for the week was gold, still up 0.34 percent. Gold consolidation is underway says UBS, adding that this should be healthy for the market. In its Global Precious Metals Comment this week, the group points out that pullbacks in gold so far this year have been relatively shallow and short-lived, not really offering investors many opportunities to enter at better levels.

- While the Indian jewelry trade continues its stir for withdrawal of the 1 percent excise duty announced in the Union Budget, the finance ministry does not indicate a compromise, reports the Business Standard. The strike entered its seventeenth day on Thursday. One ministry official said, “There is no question of a rollback.”

- B2Gold Corp. announced this week its approval for Gold Prepaid Sales Financing Arrangement, or prepaid sales, of up to $120 million. As stated in the company’s release, the prepaid sales (in the form of metal sales forward contracts) allow B2Gold to deliver pre-determined volumes of gold on agreed future delivery dates in exchange for upfront cash pre-payment. These financing arrangements will help fully fund the Fekola Mine Construction.

Opportunities

- CLSA’s Christopher Wood believes that the European Central Bank’s meeting last week reinforces the fact that central banks globally are addicted to unconventional monetary policies, reports Barron’s. Prior to the Bank of Japan meeting this week, Wood said that pension funds should have 70 percent exposure to the precious metal. Wood’s logic says that as we adjust for rising income, gold could peak again at $4,212 an ounce in an ultimate bull market.

- Bloomberg reports that in Japan, negative interest rates are boosting gold demand (according to the nation’s biggest bullion retailer). The same is true in Germany, where reinsurer Munich Re has boosted its gold and cash reserves in the face of the negative interest rates imposed by the ECB, reports Reuters. Last week the ECB cut its main interest rate to zero and dropped the rate on its deposit facility to -0.4 percent from -0.3 percent.

- Roxgold Inc. announced results from its latest drilling project this week from the QV1 structure at the Bagassi South regional exploration target, 1.8 kilometers to the south of the 55 zone. “Results from this program further confirm the potential at QV1,” stated John Dorward, President and CEO of Roxgold. These results make a stronger case for owning Roxgold and likely increased the prospect of Roxgold as a significant take out candidate.

Threats

- The CSFB “Fear Indicator” (specifically designed to measure investor sentiment, and represented by the index prices zero-premium collars that expire in three months) has never been higher, writes ZeroHedge. This could indicate that institutional investors are not believers in the equity rally and that there is more demand for put protection, continues the article, a sign of fear in the marketplace.

- Total business inventories have ballooned to crisis levels, according to a report from Macro Strategy Partnership. This can be seen in the chart below which shows the inventory-to-sales ratio. Inventories are up another 1.8 percent year-over-year to $1.81 trillion, and are up 18.5 percent from the prior peak in August 2008 while sales are only up 5.8 percent over the period.

- Barclays thinks that the rally in commodities is overdone, and although economic data has improved, it is not enough to support current prices. With a fragile global economy still in place, the group believes that a turning point for commodities is still some way away.

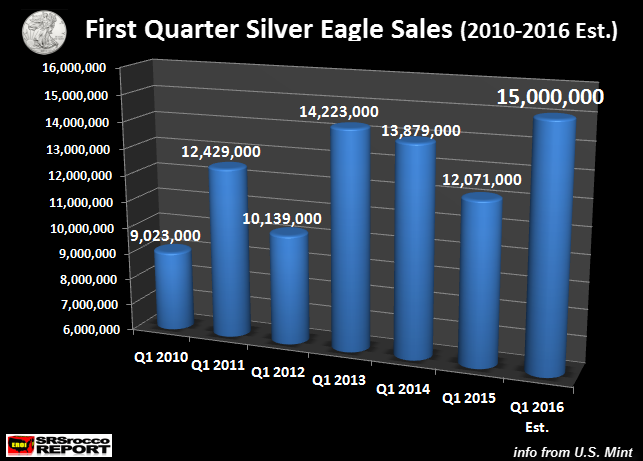

Huge increase in silver eagle sales:

It looks like the first quarter will see 15 million oz. Thus they will be heading for 60 million oz for this year. They produce only 32 million which means they must import 28 million oz from Mexico just to satisfy the silver eagle sales. How about all of the other important uses for silver like TV screens, pharmaceuticals etc?

(courtesy Steve St Angelo/SRSRocco report)

Silver Eagle Sales To Jump 25% Due To Deteriorating Market Conditions

|

March 20, 2016 – 10:09am

Silver Eagle sales will likely jump by 25% in the first quarter due to deteriorating market conditions. During the first three months last year the U.S. Mint sold 12 million Silver Eagles. Already, sales of Silver Eagles have reached 13 million. There are two weeks remaining in March and the U.S. Mint will likely sell another two million. This will put total Silver Eagle sales for the first quarter at 15 million….. the highest ever.

The last record was set in 2013 as the U.S. Mint sold 14.2 million Silver Eagles as the price of silver fell from $32 down to $25 in the first three months of the year. Regardless, the Authorized Purchasers have been on a one million week allocation for the past two months, so there was no way to acquire more Silver Eagles.

Demand for Silver Eagles this year has hit a record due to deteriorated market conditions. Even though the Dow Jones Index has added 2,000 points from its low last month at 15,500, this is not a sustainable rally. Each day, there are more indicators pointing to a worsening economic fundamentals.

Total Silver Eagle sales in 2016 could easily reach 50 million and possibly 55 million if demand remains strong for the remainder of the year.

I believe a certain amount of investors understand that nothing has been fixed in the financial system since the collapse of U.S. Investment Banking and Housing Market in 2008. This is why we continue to see record buying of Silver Eagles.

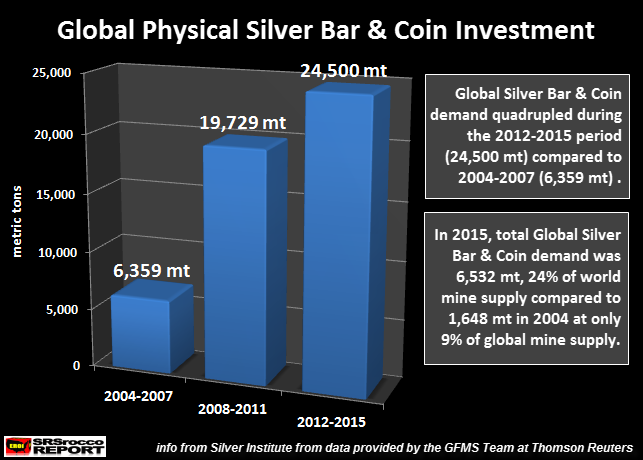

I published this chart in a prior article, but it’s worth taking another look… especially if you haven’t seen it yet. What is interesting about this chart is that cumulative physical Silver Bar & Coin demand is higher in the past four years even though the price has fallen in half:

As we can see, cumulative Silver Bar & Coin demand from 2012-2015 was 24,500 mt (788 Moz) versus 19,729 mt (634 Moz) from 2008-2011 (Moz = million oz).

Again, a percentage of investors realize the system continues to get weaker even though the stock and bond markets look good on paper. This is why silver investment demand continues to be strong even though the price has declined 67% from its $49 high in 2011.

Lastly, even though the Dow Jones Index has increased 2,000 points from its low, the price of silver is at its high for the year. We have to remember, silver jumped from a low of $13.75 in the beginning of the year to $16 when the Dow Jones fell 11%. To see the price of silver continue to move higher along with the Dow Jones suggests that something has fundamentally changed in the silver market.

I will be soon releasing a new BULLET REPORT on the Gold Market. It provides charts and data on how the recent flows are setting up the Gold Market for a big move in the future.

-END-

India resumes gold purchases

(Dave Forrest/Piece Points)

This Critical Consumer Is Buying Gold For The First Time In Three Weeks

Submitted by Dave Forrest of Pierce Points

The First Gold Buying In 3 Weeks Happening For This Critical Consumer

Major news in the gold market over the weekend. With the world’s largest gold-consuming nation reaching an agreement to resume metal sales for the first time in nearly three weeks.

That’s in India. A critical gold consumer globally, where buying had been idled since the beginning of March by a nation-wide strike by the jewelry sector.

But that strike is now officially over. With the president of India Bullion and Jewelers Association, Mohit Kamboj, announcing late Saturday that jewellers have reached an agreement with the government to return to work.

Details are still emerging, but here’s one of the most critical takeaways: as part of the back-to-work deal, the Indian government will not roll back the 1% sales tax on gold that it announced in a surprise move as part of its February 29 budget.

That sales tax had been the major trigger for the jewellers strike. But it appears that India’s gold sellers have relented on demands that the government shelve the extra levy.

Instead, reports suggest that jewellers had been appeased by assurances from the government that they would not be “harassed” over the collection of the new tax.

It’s difficult to know exactly what this means. Although it could suggest that tax officials may not push collection of the sales tax — rendering this more of a cosmetic measure than a practical one.

Whatever the case, the good news for the gold market is that India will now be buying again — for the first time since February. Which should give a lift to gold prices — especially with reports suggesting there is a lot of “pent up” demand here after the 19-day strike.

Watch for imports into India to rise for the coming weeks, and potentially lift the gold price. And keep an eye out for more details on how the 1% sales tax will be implemented — with this measure having the potential to dampen gold sales here in the longer term.

Here’s to a triumphant return.

TF Metals Report: Bullion bank desperation and motive

Submitted by cpowell on Mon, 2016-03-21 20:11. Section: Daily Dispatches

4:15p ET Monday, March 21, 2016

Dear Friend of GATA and Gold:

Bullion banks last week seemed especially desperate to drive speculative money out of gold, the TF Metal Report’s Turd Ferguson writes today. While he writes that the bullion banks also seem firmly in control of gold futures, he adds that the effort is requiring ever more paper creation from them and that another price smashing is not necessarily imminent. Ferguson’s analysis is headlined “Bullion Bank Desperation and Motive” and it is posted at the TF Metals Report here:

http://www.tfmetalsreport.com/blog/7518/bullion-bank-desperation-and-mot…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.4775 / Shanghai bourse IN THE GREEN, UP 63.65 OR 2,15% : / HANG SANG CLOSED UP 12.52 POINTS OR 0.06%

2 Nikkei closed FOR HOLIDAY

3. Europe stocks MIXED /USA dollar index UP to 95.11/Euro UP to 1.1276

3b Japan 10 year bond yield: RISES TO -..093% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.48

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 38.91 and Brent: 41.15

3f Gold DOWN /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS to 0.212% German bunds in negative yields from 8 years out

Greece sees its 2 year rate RISE to 9.68%/:

3j Greek 10 year bond yield FALL to : 8.61% (YIELD CURVE NOW INVERTED)

3k Gold at $1247.50/silver $15.88 (7:15 am est)

3l USA vs Russian rouble; (Russian rouble DOWN 1/100 in roubles/dollar) 68.25

3m oil into the 38 dollar handle for WTI and 41 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9687 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0923 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN STARTS ITS CAMPAIGN AS TO WHETHER EXIT THE EU.

3r the 8 Year German bund now in negative territory with the 10 year FALLS to + .212%

/German 8 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.88% early this morning. Thirty year rate at 2.67% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets, S&P500 Futures Fall After Brussels Bombings

This morning’s Brussels bomb attacks have led to risk-off sentiment across European asset classes, with Bunds higher and equities firmly in the red, although if the Paris terrorist attacks of November are any indication, today’s tragic events may be just the catalyst the S&P500 needs to surge back to all time highs. FX markets have also been dominated by events in Brussels, with USD and JPY strengthening, while EUR and GBP softening throughout the European morning.

Losses today would disrupt a five-week rally bolstered by improving economic data, rising crude prices and “optimism that central banks around the world will continue to support growth” as Bloomberg puts it clearly not aware of the irony that the world is no longer able to grow precisely due to decades of central bank “stimulus.”

This is where global markets stand as of this morning.

- S&P 500 futures down 0.4% to 2034

- Stoxx 600 down 0.9% to 338

- FTSE 100 down 0.6% to 6149

- DAX down 0.9% to 9854

- German 10Yr yield down 3bps to 0.2%

- Italian 10Yr yield down less than 1bp to 1.25%

- Spanish 10Yr yield up 2bps to 1.46%

- S&P GSCI Index down less than 0.1% to 336

- MSCI Asia Pacific up 0.7% to 130

- Nikkei 225 up 1.9% to 17049

- Hang Seng down less than 0.1% to 20667

- Shanghai Composite down 0.6% to 2999

- S&P/ASX 200 down 0.3% to 5167

Global top news

- Brussels Rocked by Deadly Attacks With Blasts at Airport, Subway: Two explosions ripped through Brussels airport departure hall, third hit a downtown subway station on Tuesday morning; VTM news put toll at 11, citing local fire department.

- IPhone Hearing Canceled as FBI Tests Hack Without Apple Help: Court hearing was canceled at DoJ’s request, as govt said in Monday court filing that it wanted to test a possible method for accessing phone data.

- Apple Unveils Smaller IPhone SE, New IPad Pro to Aid Sales: iPhone SE has a 4-inch-screen, incorporates faster A9 processor that also runs larger iPhone 6S handsets.

- Cooperman, Omega Said to Get Wells Notice Over 2010 Trade: Leon Cooperman said regulators are considering taking action against both him, Omega Advisors over certain trades, according to person familiar.

- Express Scripts Incoming CEO Wants Anthem to Stay Amid Suit: Incoming CEO Tim Wentworth trying to keep its biggest customer, after health insurer Anthem sued to recoup billions.

- Carnival Wins Cuban Government’s OK to Begin Cruises to Island: Decision allows co.’s Fathom division to become first U.S. cruise line to dock there in >50 years.

- Ackman Said to Address Valeant Side-by-Side With Pearson: Ackman, with chairman Ingram, outgoing CEO Pearson answered questions, made proclamations about co.’s future.

- BlackRock Says There Won’t Be a U.S. Recession, Cut Treasuries: “Economic indicators this week may show the U.S. economy experienced a mild slowdown but is not headed for a recession,” Richard Turnill, global chief investment strategist, wrote in a report Monday.

- Boeing Likely to Miss Delivery Date for Tankers: Pentagon: Co. likely to miss first major requirement of its $51b tanker program for U.S. Air Force; delivering firrt 18 aerial refueling planes by August 2017.

- Apache Unlikely to Seek M&A Until More Restructuring Occurs: Co. has higher bar for purchasing assets, given that it already has deferred activity, CEO John Christmann said Monday.?Transocean, Schlumberger See Oil Industry Recovery Delayed ?National Oilwell Considering Billion-Dollar Deals in Oil Slump

Looking at regional markets, Asian stocks traded mixed despite the mild positive lead from Wall St., as commodities retreated and demand for risky assets remained subdued ahead of the Easter season. Nikkei 225 (+1.9%) outperformed on return from a long weekend to snap a 4-day losing streak with JPY weakness driving price-action, while ASX 200 (-0.3%) saw indecisive trade as losses in financials and materials capped upside momentum. Elsewhere, Chinese markets were subdued with the Shanghai Comp (-0.6%) on course for its first loss in 8 days following weakness in commodity-related sectors, while there were also reports that China’s regulator urged banks to reduce their risk and curb dividend pay-outs. Finally, 10r JGBs traded relatively flat despite the heightened risk-appetite in Japan as real money accounts were seen to be mostly side-lined, while there was also notable curve-flattening as yields in the super-long-end dropped to fresh record lows. BoJ’s Nakaso said would like to watch for some time to evaluate how negative rates work throughout the Japanese economy and added that it is technically possible for the BOJ to go deeper into negative territory.

Top Asian News

- Hong Kong Property Crash Averted, If Stock Traders Are Right: Hang Seng Properties Index has climbed 18% from January low.

- Ringgit Gains to Seven-Month High on 1MDB Asset Sale Report, Oil: Currency’s break of 4/$ puts 3.9 in sight, Macquarie says.

- China’s Rising Sway Seen in Korea Bonds as Holdings Top U.S.: Chinese funds are now biggest holder of won- denominated debt.

- Botched Rules Trip Modi Dream of Shipping Hub Rivaling Singapore: Curbs, costs mean shippers prefer Colombo, Singapore, Dubai.

- ANZ Bank Plans to Eliminate 12 Positions in its Markets Division: Unit includes foreign exchange, syndicated loans, fixed income.

The price action in Europe has been dictated by the tragic events in Belgium, in which explosions at the Brussels airport and metro stations has prompted risk off sentiment. As such, equities (Eurostoxx -0.40%) are deeply entrenched in negative territory with underperformance seen in airline names such as IAG (-4.2%) and Ryanair (-4.3%), this comes alongside other tourist related names feeling the brunt such as Accor (-4.4%). The risk off tone has seen Bunds move higher with volume also spiking, while yields continue to bull flatten across the curve with peripheral spreads slightly wider.

Top European News

- European Hotel Stocks Fall After Explosions at Brussels Airport: Bloomberg Europe Lodging Index, composed of seven leading lodging stocks, fell 4.1%, most since Feb. 11.?Air, Train Travel Slows in Europe After Brussels Airport Blasts

- Bank Drops as Moody’s Signals Risk of Cut Amid Overhaul: “Since changing leadership last June and recalibrating its strategic plan last November, the operating environment has worsened for Deutsche Bank,” ratings firm said in statement late Monday.

- German Business Confidence Rebounds on Resilient Domestic Demand: Indicator improved for the first time in four months.

- Wal-Mart Loses Everyday Low Price Edge as Aldi Opens Across U.S.: Family-owned German grocery-store chain is beating WMT at its own game: selling food at rock-bottom prices.

- Bang & Olufsen in Takeover Talks With China’s Sparkle Roll: Several elements in the discussions remain to be resolved, B&O said Tuesday in statement.

- OMV Said in Talks to Hire Morgan Stanley for Turkey Disposal: Sale may raise as little as $1.3b, according to Bloomberg Intelligence calculations.

In FX, this morning’s FX trade has also been dominated by the confirmed suicide attacks on Belgium. All the familiar risk currencies were hit, with spot and cross JPY taking a dive; the USD rate falling to lows around 111.36 having pushed through to 112.20 highs prior to this. GBP/JPY was a key loser on the day, as Cable was hit hard prior to news of the above — pre 1.4400 pounced up as London players came in. EUR/GBP was also edging higher, but with EUR/USD also coming under fire, the USD won out against all currencies with the exception of the JPY. AUD and CAD were slow to react, and were only marginally weakened in the risk off climate — as was NZD. The CHF made some progress against the EUR, less so against the USD. Limited impact on emerging FX. German Ifo (106.7 vs. Exp. 106) beat expectations on all counts although with ZEW (4.3 vs. Exp. 5.4) lower and UK inflation (Y/Y 0.30% vs. Exp. 0.40%) was softer than forecast.

In commodities, gold has seen the biggest move in commodities, rising USD 9.00/oz after the terror attacks in Brussels, meanwhile WTI and Brent are trading relatively flat for the day. In Base metals, copper and iron ore prices declined amid weak sentiment in China, with Dalian iron ore futures further pressured by profit-taking after prices hit limit-up in the prior 2 consecutive days.

On the US calendar today, markets will focus on the latest Markit manufacturing flash PMI for March (51.9 expected; 51.3 prior) and the Richmond Fed Manufacturing index (0.0 expected; -4 prior). We also get more housing data with the FHFA house price index for January due (+0.5% expected) ahead of the manufacturing data as well as API Crude Oil Inventories data.

Bulletin Headline Summary From Bloomberg

- Treasuries slightly higher in overnight trading, global equity markets drop, gold rises; Brussels airport and subway system hit by explosions in possible terrorist attacks.

- The pound suffered the biggest impact in the currency market of the Brussels explosions amid speculation the tragedy boosts the case of campaigners who want Britain to quit the European Union

- The U.K.’s inflation rate was unexpectedly unchanged in February, remaining far below the BOE’s 2% goal. Annual consumer-price growth was at 0.3%; economists had forecast an acceleration to 0.4%

- Deutsche Bank extended declines after Moody’s Investors Service signaled it may cut the German lender’s credit rating amid concern that it will struggle to restructure businesses

- German business confidence improved for the first time in four months in a sign that domestic demand is helping shield companies in Europe’s largest economy from slowing global growth

- The Australian central bank’s attempts to talk the local currency lower last year ran afoul of the U.S. Treasury, which chided officials by reminding them of their commitment to a freely floating exchange rate

- Prime Minister Justin Trudeau will put the Canadian government back in business when he introduces a debut budget Tuesday that reverses a decade of restraint

- In 2016, for the first time in years, drillers will add less oil from new fields than they lose to natural decline in old ones

- $2.7b IG corporates priced yesterday; MTD $132.505b, YTD $426.755b; $1.75b HY priced yesterday, MTD 17 deals for $9.965b, YTD 42 deals for $24.82b

- Sovereign 10Y bond yields mostly steady; European, Asian equity markets lower; U.S. equity-index futures drop. WTI crude oil and copper fall, gold rallies

Let us begin;

ASIAN AFFAIRS

Late MONDAY night/ TUESDAY morning: Shanghai closed DOWN BY 18.13 POINTS OR 1.94% , / Hang Sang closed DOWN by 17.40 points or 0.08% . The Nikkei closed UP 323.74 . Australia’s all ordinaires was DOWN 0.32%. Chinese yuan (ONSHORE) closed DOWN at 6.4923. Oil ROSE to 41.36 dollars per barrel for WTI and 41.46 for Brent. Stocks in Europe so far ALL IN THE RED . Offshore yuan trades 6.49310 yuan to the dollar vs 6.4923 for onshore yuan/LAST WEDNESDAY, China’s industrial production collapsed along with retail sales. JAPAN RE SIGNALS that they may continue with nirp a little longer which sends the USA/Yen spiraling northbound/markets in Japan tumble . Japan’s exports plummet.LAST WEDNESDAY, China signals that they are going to tax financial transactions. Since nobody has a handle on Chinese foreign exchange, the IMF politely asks how large is its forward book on currencies. Many believe it is over 300 billion and that would be a future payment

(see below)

.

REPORT ON JAPAN

none today.

END

report on China:

We have been pointing this out to you on several occasions. The Chinese are using forwards to hide their exposure to depleting USA reserves. Basically by using derivatives they delay the exit of USA dollars by the length of derivative contracts. It is believed that China has in excess of 300 billion of USA exit exposure.

(courtesy zero hedge)

IMF Politely Asks China To Explain Exactly How Large Its FX Forwards Book Is

On the heels of China’s move to devalue the yuan on August 11, the market’s attention abruptly shifted to something we’d been discussing for quite some time. Namely, China’s rapidly depleting FX reserves.

The problem for China was that they wanted to devalue, but they wanted to do it on their terms and that’s not something that was particularly agreeable to the market. What was immediately apparent to us, but what it took weeks for most observers to understand, was that the PBoC actually transitioned to an FX regime that afforded the market less of a role in determining the exchange rate, not more. Before, China would reset the daily fix to dictate where the spot traded. In the new system, the PBoC simply manipulates the spot in order to dictate the fix, which from August 12 was supposed to “better reflect” the previous day’s trading. But if the previous day’s trading was dictated by PBoC intervention, then the entire endeavor is meaningless.

Of course daily spot interventions cost money. Lots of it. Especially if the market smells a rat and thinks you may be angling for a larger devaluation down the road but are unwilling to just rip the band-aid off and move to a free float now.

China blew through nearly $100 billion in the month of August alone supporting the yuan and soon enough, FX reserve data out of Beijing became the market’s new risk on/risk off trigger. The data also became a rather public proxy for capital flight and before long, China got uncomfortable with the amount of attention the headline figure received.

So, the PBoC decided to find other ways to intervene to both support the onshore spot and ensure that the CNY/CNH spread didn’t widen too much (the weaker the offshore yuan trades relative to the onshore spot, the more depreciation pressure there is). Dabbling in forwards became one of the bank’s go-to strategies.

What Beijing has been doing actually isn’t all that complicated. The PBoC simply asks policy banks to borrow dollars in the swap market, sell them, and then enter into a forward contract with Beijing which effectively squares the trade for the banks as the PBoC takes everything onto its own balance sheet.

The problem is that this makes it difficult for the market to get a read on capital outflows and on how much downward pressure the RMB is experiencing (and obscuring those two things is precisely the point for China). And it’s not just the market that’s having a hard time reading the tea leaves, it’s the IMF as well.

“The International Monetary Fund is pressing China to disclose more data on its currency operations according to the standards the Chinese central bank pledged to follow,” WSJ reported on Monday. Here’s more:

In recent months, the People’s Bank of China has increasingly turned to the derivatives market to help prop up the currency—a shift from its traditional approach of dipping into its dollar pile to buy yuan.

The new tactic has several advantages for the central bank: It allows it to burn through its foreign-exchange reserves more slowly and drain smaller amounts of yuan from the financial system at a time of economic slowdown. It also leaves less evidence of intervention.

Currency traders and investors, however, complain that the strategy is making it even harder to figure out Beijing’s intentions for the yuan. Now, the IMF is calling on the Chinese central bank to release more data on its holdings of derivatives such as forwards—which have become the main financial instrument used by the PBOC for currency intervention these days, the people said.

The step would be in keeping with China’s pledge in October to adhere to the IMF’s special-data-dissemination standards as part of its effort to win the yuan its long-coveted reserve-currency status. Disclosing the data could also shed more light on how much firepower China has to keep defending the yuan.

The data being sought by the IMF concerns the total holdings of forwards and futures by the PBOC, according to the people. Such data sets reflect future claims to a country’s foreign-exchange reserves; many of the world’s central banks, including those of Thailand, Malaysia and India, have frequently disclosed this data to the fund.

Some market participants estimate that China’s current holdings of forwards range between $150 billion and $300 billion.

You really needn’t think too hard about all of the above because there are two very simple takeaways: 1) the IMF is going to hold China to its promises of transparency and market oriented reforms now that the Fund has agreed to include the yuan in the SDR basket, and 2) these have to be settled at some point, so just know that the strategy outlined above is just about near-term optics.

Perhaps Citi summed it up best last autumn: “If you have a transaction that settles down the road, the actual liquidity impact in the short term may not be as dramatic. Down the road you can’t avoid it.”

You can see why the IMF and the market more generally want full transparency out of Beijing and given the fear of capital flight, you can probably also understand why China would want to adopt strategies that make the PBoC’s FX intervention as opaque as possible. Unfortunately for the PBoC, the IMF looks set to play the SDR trump card.

end

EUROPEAN AFFAIRS

Belgium Cancels All Air, Rail Traffic Into/ Out Of Brussels; Military Deployed

In the wake of the three (and now possibly four) explosions that rocked Brussels on Tuesday morning, Belgium has cancelled all air and rail traffic to the city.

Eurostar has suspended all service to Brussels following a deadly explosion at Maelbeek metro station were more than 20 were reportedly killed this morning.

Meanwhile, all flights from the Brussels airport are cancelled.

The airport says it will remain closed until at least Wednesday. “The blasts add to the woes of the travel industry in Europe, the Middle East and Africa, which already has seen tourism drop after two terrorism attacks in Paris last year, the destruction of a Russian airliner in Egypt, bombings in Ankara and Istanbul in Turkey, and a deadly assault on tourists on a Tunisian beach,” Bloomberg notes.

Meanwhile, the Belgian army will deploy an additional 275 troops to Brussels as the city will once again come to resemble a war zone in the aftermath of an apparent coordinated suicide attack that authorities believe may well be linked to last week’s anti-terror raid that ended with the capture of Paris fugitive Salah Abdeslam.

Expect more trouble in Molenbeek over the next 24-48 hours.

Dozens Killed After Massive Bomb Explosions Rip Through Belgium Airport, Subway – Live Feed

Update: The latest reports indicate 28 dead, 55 injured, 1 bomb at the metro and 2 suicide bombers at the Brussels Airport.

Update: Belgian media have reported a fourth explosion apparently at Rue De La Loi. It may be a controlled detonation. Police are also evacuating Royal Park.

Update: The Belgian army will deploy 275 more troops to Brussels as the city will once again come to resemble a war zone.

Update: Reports indicate the death toll from the twin airport blasts sits at 13 while casualties in the metro number 20. Cell phone networks are congested and authorities are encouraging Belgians to use messaging apps and social media to contact friends and family.

Obviously, officials believe there could be a connection to networks cultivated by Paris suspect Salah Abdeslam who was captured in a Molenbeek anti-terror raid last week. On theory says that cells connected to Abdeslam might have pulled forward plans to bomb soft targets fearing more raids were imminent.

* * *

Just four months after the tragic attacks in Paris, Europe was once again the epicenter of a terrorist mass murder, when several deadly explosions this morning rocked Brussels, first hitting the international airport and then a metro station near the European Union institutions, resulting in dozens of casualties and over a hundred wounded in what Belgian authorities moments ago labeled as terrorist attacks.

The first explosions Tuesday morning hit the city’s main airport outside a security check.According to Reuters, at least 10 people have reportedly been killed although estimates in social media range as high as 17, and dozens were wounded after two blasts ripped through Zaventem airport. Brussels police said that Zaventem’s great hall was targeted in the blast, but they couldn’t confirm the number of the victims in the attack. “There was an explosion, but we cannot say more,” a police spokesperson said.

“It was atrocious. The ceilings collapsed,” Zach Mouzoun, who arrived on a flight from Geneva about 10 minutes before the first blast, told BFM television. “There was blood everywhere, injured people, bags everywhere.”

“It was a war scene,” he added, for emphasis.

A suicide bomber was responsible for one of the blasts, Belgian broadcaster VRT said. Three suicide belts packed with explosives have been found at the Brussels airport by police, local TV reported.

Reports also suggest that first there was a shot fired in the departure hall, then something was called out in Arabic, and only afterward, two explosions rocked the facility.

http://www.dailymail.co.uk/embed/video/1276217.html

A person briefed on the incident said two devices exploded inside the airport outside the security check and that more than 100 people had been injured. Smoke could be seen rising from the airport in the aftermath of the explosions.

According to preliminary reports, one of the explosions took place near the American Airlines check-in desk. A government source confirmed to VRT broadcaster that it was an attack, while Anke Fransen, spokeswoman for Brussels Airport, said there were multiple injuries. “We can confirm that there have been two explosions in the departure hall. We called the emergency services on the ground – they [are] now provid[ing] first aid to the injured.”

Niels Caignau, flight watcher at Swissport, told Radio 1 that he heard an explosion at around 8:00 a.m. local time. “The windows outside the departure hall are completely shattered. Many people have run out with tears in [their] eyes. We were advised to stay indoors.”

No planes are landing at Brussels Airport which is in lockdown, and planes are being diverted to Antwerp. Planes are circling over the city of Liege. Sky News Middle East correspondent Alex Rossi, who was at the airport en route to Tel Aviv, has tweeted that he could “feel the buildings move.”

Belgian officials immediately raised the terror alert across the country. As the WSJ adds, police have closed the access road leading to the airport and police and ambulances were rushing to the scene. The airport began evacuating the building where the explosions took place and an official warned people not to come to the area. “Don’t come to the airport—airport is being evacuated. Avoid the airport area. Flights have been cancelled,” the airport said.

Airlines said they were diverting inbound flights. Europe’s air-traffic management organization Eurocontrol on Tuesday warned airlines that the airport was unavailable “until further notice.”

* * *

The third explosion struck just after 9 a.m. local time struck Maelbeek metro station, very near the heart of the European quarter in Brussels, home to the EU institutions.

According to preliminary local police reports cited by RT, at least 10 people were killed. The explosion took place less than an hour after a deadly airport bombing, which killed at least 17 people. Large amounts of smoke have been seen coming out of the metro station in the Belgian capital. Brussels’ transport authority says all metro stations in the city have been closed, Reuters reports.

Minutes after the blast at Maalbeek, a second explosion is reported to have taken place at the near-by Schuman metro station. Images on social media have shown passengers being evacuated from inside the metro and walking along the train tracks. The Maalbeek station is also near a number of important EU buildings such as Berlaymont building, which houses the EU Commission and the Council of the European Union.

Staff working at the EU commission have also been told to stay indoors. Belgian authorities have raised the security alert to the highest level following blasts at the Zaventem Airport and Maalbeek Metro station.

All trains to and from Brussels have been suspended and the airport will remain closed until at least Wednesday.

A video summary of this morning’s events:

And a live feed of events in Belgium and across Europe which wakes up to another bloody terrorist morning, courtesy of SkyNews:

RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

GLOBAL ISSUES

The terror attack in Belgium heightens Brexit risk as UK wants no part of the European mess with the migrants

(courtesy zero hedge)

FX Market Chaos Signals Brexit Risk Surge Post-Belgium

The markets’ various indicators of ‘Brexit Risk’ are all elevated this morning post-Belgium-attacks.

GBPUSD is tumbling…

But most crucially, the cost of protection against pound currency swings over EU currency swings has jumped to the highest ever signalling the highest market-impled risk of Brexit so far.

As Fed’s Lockhart warned yesterday, the contagious risk of Brexit will likely spread to the US economy – so this is not to be ignored.

end

EMERGING MARKETS

OIL MARKETS

Canada’s regulators are warning banks with their under reserves with respect to energy losses:

(courtesy zero hedge)

Soon After We Sounded The Alarm, Canada’s Regulator Warns Local Banks Are Under reserved To Energy Losses

Back in early February, Zero Hedge laid out what was the biggest crisis facing Canada’s banks: a chronic under reserving to potential (and soon, realized) oil and gas loan losses.

As we said nearly two months ago, “for Canada, it’s not only raining, it’s pouring for the country’s energy industry, a downpour which is about to migrate into its banking sector. Which is why it is indeed time to take a somewhat deeper dive into the Canadian banks’ balance sheets, where we find something very troubling, and something which prompts us to wonder if the time of freaking out about European banks is about to be replaced with comparable panic about Canadian banks.

The following chart from an analysis by RBC shows that when compared to US banks’ (artificially low) reserves for oil and gas exposure, Canadian banks are…not. Here is the one chart showing why the time to panic about Canadian banks may have finally arrived:

Two months later, we are happy to announce that Canada’s regulator has caught up to our warning, and as the WSJ reported, “Canada’s banking regulator is urging the country’s major banks to review their accounting practices to ensure they have sufficient reserves as the commodity-price collapse takes a toll on the economy.”

As we first suggested in early February, Canada’s Office of the Superintendent of Financial Institutions is now warning local lenders should scrutinize their collective allowances and reserve funds that act as cushions to absorb potential future loan losses, the regulator’s chief said in an interview.

“We want them to take a good look at their accounting practices,” said Superintendent of Financial Institutions Jeremy Rudin. “They should support loss-absorbing capacity and the ability to manage through difficult times in general,” he added.

Some of the banks laughed at us when we suggested they are purposefully masking their exposure to distressed loans; we wonder if they will also laugh when their regulator tells them to do precisely that. As the WSJ further writes, “Canada’s regulator is giving the country’s six biggest banks this guidance on their accounting as they face mounting criticism from some analysts that they haven’t amassed enough reserves to cover soured loans to the energy sector. That criticism was a recurring theme during calls following their fiscal first-quarter results, in which many banks warned of rising provisions for credit losses but assured investors their rainy-day cushions were adequate.”

Here is the WSJ chart released today which is oddly identical to the one we showed many weeks ago:

Next, the WSJ summarizes the details of what is known about Canadian loan exposure:

Energy loans totaled 49.7 billion Canadian dollars ($38.2 billion) for the country’s six biggest banks during the November-to-January quarter, according to a report by TD Securities Inc. Bank of Nova Scotia, Canada’s third-largest bank by assets, has the biggest direct oil and gas exposure at 3.6% of total loans.

Some analysts are skeptical about the lenders’ reserving practices in part because U.S. banks, including J.P. Morgan Chase & Co. and Wells Fargo & Co., have set aside millions more for their reserves as they brace for bigger energy-related losses.

Mr. Rudin declined to say whether Canadian banks are under-reserved compared with their U.S. peers. Nor did he offer an opinion on whether analysts voicing such criticisms were misinformed.

Actually, that is only half the picture: as we explained in “The Next Cockroach Emerges: Including Undrawn Loans, Canadian Banks Exposure To Oil Doubles” if one includes undrawn (but committed) bank exposure, the number doubles. Indeed, when adding “untapped loans in the form of undrawn revolvers and other committed but unused credit facilities, Canadian banks’ exposure to the struggling oil-and-gas industry more than doubles from the current C$50 billion in outstanding loans generally highlighted by Royal Bank of Canada, Toronto-Dominion Bank and the country’s four other large lenders in quarterly earnings calls and presentations, to C$107 billion ($80 billion).”

We expect the WSJ to catch up with this critical angle of the story in the next 4-weeks, one which would imply the all-in loss reserves are about 50% lower than the already alarming estimates. For now, however, what we do know is that most banks declined to comment, including on how they have responded to the regulator’s guidance. “We have no comment on this specifically, but are confident in our current provisioning practices,” said Ali Duncan Martin, a spokeswoman for Toronto-Dominion Bank, Canada’s No. 2 lender by assets, in an email.

For their part, Canada’s banks did what they also do: float in a sea of denial. A spokeswoman for an industry group representing the lenders, the Canadian Bankers Association, said that Canadian banks aren’t under-reserved. Well, they clearly are, but admitting as much would unleash the market’s realization just how wrong its valuation of Canadian banks has been.

Not only are Canadian banks under-reserved, they are also purposefully opaque to prevent investors from making a comprehensive health assessment:

Canadian banks tend to disclose their energy exposures as a percentage of total loans, but it is difficult to make a direct comparison with U.S. lenders. For instance, Canadian portfolios include large amounts of insured residential loans that are essentially risk-free because they are backstopped by the federal government.

Canada’s banks have also been criticized by analysts for providing varying degrees of detail about their energy lending books—such as the proportion of reserve-based loans and the amount considered “investment grade”—and about their stress-testing of loan portfolios.

“I’m concerned about this,” said James Shanahan, an equity analyst with Edward Jones, in a recent interview. “The banks aren’t really saying a whole lot about the true underlying quality of these [energy] portfolios,” he later added. He’s among the analysts calling on Canadian banks to provide more disclosure on their energy exposure, including how much covenant relief is being provided to distressed borrowers.

He almost certainly won’t get it, unless for some reason, the Dallas Fed make it explicit that Canadian banks have to be more transparent in a few weeks when bank borrowing base redeterminations are made in negotiations which will include not only Canadian and US commercial banks, but the Dallas Fed as well as the US OCC.

That could prove to be a key issue in the spring borrowing base redeterminations.Mr. Rudin declined to specify what role, if any, OSFI would play in those upcoming reviews, saying only banks are expected to have a “robust credit assessment process” that is frequently reviewed by the regulator. Issues, such as covenant relief, are “business decisions” best left to the individual banks, he added.

We can tell Mr. Rudin what will happen: the OSFI will play the same role that the US OCC played in recent preliminary, if quite definitive, discussions between US lenders and shale producers, the same discussions which the Dallas Fed denied ever took place even though both Credit Suisse and the WSJ confirmed our story: discussions which made it clear to US banks not to force defaults, but to suspend MTM until the local lenders can force the underlying company to issue debt (just like Weatherford) and use the proceeds to take out the secured lender bank.

Expect precisely the same in Canada over the next few months as Canada’s lenders are told to quietly, if aggressively, unwind their exposure to all Canadian oil and gas companies.

Oil Rips On Yet Another Doha “Freeze” Meeting Headline (As Predicted)

Around 915ET we tweeted the need for an OPEC meeting headline as oil prices started to accelerate losses. 70 minutes later, the market’s “wish” was granted when Algeria (yes, seriously) announced they will attend, Nigeria is hopeful, and Libya said it would not attend… of course any headline is a buying opportunity and the algos went wild…

We tweeted…

And then, headlines hit…

- *LIBYA SAID TO SKIP DOHA OIL-OUTPUT FREEZE MEETING ON APRIL 17

- *ALGERIA’S SONATRACH SAYS OIL FOUND AT HASSI BIR REKAIZ WELL

- Algeria Said to Attend Doha Meeting on Oil-Output Freeze Talks

- Nigerian oil minister welcomes Doha meeting of oil producers and wants OPEC to take binding action to stabilize oil prices

And the machines went wild…

One wonders how many more times oil can rally on the same (or even less newsworthy) headlines.

It would appear that Reuters needs another narrative…

Crude Drops On Yuuge Inventory Build

Overall crude inventories rose for the 6th week in a row according to API. Despite draws in Gasoline, Distillates, and Cushing; Crude inventories surged 8.8mm barrels – the 2nd biggest weekly build in a year.

API, according to RTRS:

- Crude +8.796mm

- Cushing -1.37mm (confirming Genscape’s data)

- Gasoline -4.3mm

- Distillates -391k

This was a big draw in Cushing but appears to be dominated by the surge in overall inventories…

Crude is giving back some of the bounce gains on the news…

Charts: Bloomberg

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings/TUESDAY morning 7:00 am

Euro/USA 1.1206 DOWN .0026 ( STILL REACTING TO USA FAILED POLICY)

USA/JAPAN YEN 111.74 DOWN 0.382 (Abe’s new negative interest rate (NIRP)a total bust/SIGNALS U TURN WITH INCREASED NEGATIVITY IN NIRP)

GBP/USA 1.4273 DOWN .0091 (THREAT OF BREXIT)

USA/CAN 1.3074 DOWN.0018

Early THIS MONDAY morning in Europe, the Euro FELL by 26 basis points, trading now WELL above the important 1.08 level RISING to 1.1102; Europe is still reacting to deflation, announcements of massive stimulation (QE), a proxy middle east war, and the ramifications of a default at the Austrian Hypo bank, an imminent default of Greece, Glencore, Nysmark and the Ukraine, along with rising peripheral bond yield further stimulation as the EU is moving more into NIRP, and NOW THE USA’S NON tightening by FAILING TO RAISE THEIR INTEREST RATE / Last night the Chinese yuan was DOWN in value (onshore) The USA/CNY UP in rate at closing last night: 6.4923 / (yuan DOWN AND will still undergo massive devaluation/ which will cause deflation to spread throughout the globe)

In Japan Abe went BESERK with NEW ARROWS FOR HIS Abenomics WITH THIS TIME INITIATING NIRP . The yen now trades in a SOUTHBOUND trajectory RAMP as IT settled UP in Japan by 38 basis points and trading now well BELOW that all important 120 level to 111.44 yen to the dollar. NIRP POLICY IS A COMPLETE FAILURE AND ALL OF OUR YEN CARRY TRADERS HAVE BEEN BLOWN UP/SIGNALS TO THE MARKET THAT THEY MAY DO A U TURN ON NIRP AND INCREASE NEGATIVITY

The pound was DOWN this morning by 91 basis points as it now trades WELL BELOW the 1.44 level at 1.4273.

The Canadian dollar is now trading UP 18 in basis points to 1.3049 to the dollar.

Last night, Chinese bourses AND jAPAN were MIXED/Japan NIKKEI CLOSED UP 323.74 , OR 1.94%HANG SANG DOWN 17.40 OR 0.08% SHANGHAI DOWN 18.13 OR 1.94% / AUSTRALIA IS LOWER / ALL EUROPEAN BOURSES ARE IN THE RED, as they start their morning/.

We are seeing that the 3 major global carry trades are being unwound. The BIGGY is the first one;

1. the total dollar global short is 9 trillion USA and as such we are now witnessing a sea of red blood on the streets as derivatives blow up with the massive rise in the rise in the dollar against all paper currencies and especially with the fall of the yuan carry trade. The emerging market which house close to 50% of the 9 trillion dollar short is feeling the massive pain as their debt is quite unmanageable.

2, the Nikkei average vs gold carry trade (blowing up and the yen carry trade HAS BLOWN up/and now NIRP)

3. Short Swiss franc/long assets blew up ( Eastern European housing/Nikkei etc.

These massive carry trades are terribly offside as they are being unwound. It is causing global deflation ( we are at debt saturation already) as the world reacts to lack of demand and a scarcity of debt collateral. Bourses around the globe are reacting in kind to these events as well as the potential for a GREXIT>

The NIKKEI: this TUESDAY morning: closed UP 323.74 OR 1.94%

Trading from Europe and Asia:

1. Europe stocks ALL IN THE RED

2/ CHINESE BOURSES RED/ : Hang Sang CLOSED IN THE RED. ,Shanghai IN THE RED/ Australia BOURSE IN THE RED: /Nikkei (Japan)CLOSED/IN THE GREEN/India’s Sensex in the RED /

Gold very early morning trading: $1251.30

silver:$15.94

Early TUESDAY morning USA 10 year bond yield: 1.90% !!! UP ONE in basis points from MONDAY night in basis points and it is trading WELL BELOW resistance at 2.27-2.32%. The 30 yr bond yield falls to 2.71 DOWN 1 in basis points from MONDAY night.

USA dollar index early TUESDAY morning: 95.61 UP 21 cents from MONDAY’s close.(Now below resistance at a DXY of 100)

This ends early morning numbers TUESDAY MORNING

end

And now your closing TUESDAY NUMBERS

Portuguese 10 year bond yield: 2.92% UP 19 in basis points from MONDAY

JAPANESE BOND YIELD: -.097% UP A BIT in basis points from MONDAY

SPANISH 10 YR BOND YIELD:1.43% DOWN 1 IN basis points from MONDAY

ITALIAN 10 YR BOND YIELD: 1.25 DOWN 1 basis points from MONDAY

the Italian 10 yr bond yield is trading 18 points lower than Spain.

GERMAN 10 YR BOND YIELD: .210%

end

IMPORTANT CURRENCY CLOSES FOR TUESDAY

Closing currency crosses for TUESDAY night/USA dollar index/USA 10 yr bond: 2:30 pm

Euro/USA 1.1213 DOWN .0021 (Euro DOWN 21 basis points and for DRAGHI A COMPLETE POLICY FAILURE/

USA/Japn: 112.40 UP .264 (Yen DOWN 26 basis points) and still a major disappointment to our yen carry traders and Kuroda’s NIRP. They stated that NIRP would continue.

Great Britain/USA 1.4207 DOWN .0158 (Pound DOWN 158 basis points.

USA/Canada: 1.3043 down .0.0048 (Canadian dollar DOWN 48 basis points EVEN THOUGH oil was HIGHER IN PRICE (WTI = $41.41)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

This afternoon, the Euro was DOWN by 21 basis points to trade at 1.1213 AS THE MARKETS REACTED TO THE BRUSSELS BOMBING TODAY.

The Yen FELL to 112.40 for a LOSS of 26 basis pints as NIRP is still a big failure for the Japanese central bank/also all our yen carry traders are being fried.

The pound was DOWN 158 basis points, trading at 1.4207 (HUGE BREXIT CONCERNS)

The Canadian dollar ROSE by 48 basis points to 1.3043 AS the price of oil was UP today (as WTI finished at $41.41 per barrel)

the 10 yr Japanese bond yield closed at -.097% UP A BIT IN basis points in yield

Your closing 10 yr USA bond yield: UP 3 basis point from MONDAY at 1.94% //trading well below the resistance level of 2.27-2.32%) policy error

USA 30 yr bond yield: 2.72 UP 1 in basis points on the day and will be worrisome as China/Emerging countries continues to liquidate USA treasuries (policy error)

Your closing USA dollar index, 95.68 UP 27 cents on the day at 2:30 pm

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for TUESDAY

London: UP 8.16 points or 0.13%

German Dax :UP 41.36 points or 0.42%

Paris Cac UP 4.17 points or 0,09%

Spain IBEX DOWN 29.00 or 0.32%

Italian MIB: UP 1.89 points or 0.01%

The Dow was down 41.30 points or 0.23%

Nasdaq :up 12.79 points or 0.27%

WTI Oil price; 41.41 at 2:30 pm;

Brent Oil: 41.76

USA dollar vs Russian Rouble dollar index: 67.26 (Rouble is UP 57 /100 roubles per dollar from yesterday)AS the price of Brent and WTI OIL ROSE

end

This ends the stock indices, oil price, currency crosses and interest rate closes for today

Closing Price for OIl, 5 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 5 PM: $41.21

BRENT: 41.60

USA 10 YR BOND YIELD: 1.95%

USA DOLLAR INDEX:95.65 up 25 cents

END

And now your more important USA stories which will influence the price of gold/silver

Stocks Stumble As Fed Hawks Tamp Down Terror-Attack Exuberance

Belgian PM Charles Michel said earlier that “this is the deadliest attack on Brussels ever,” andas we noted in this morning’s pre-open wrap:

This morning’s Brussels bomb attacks have led to risk-off sentiment across European asset classes, with Bunds higher and equities firmly in the red, although if the Paris terrorist attacks of November are any indication, today’s tragic events may be just the catalyst the S&P500 needs to surge back to all time highs

So it should be no surprise that panic-buying ensued off the reaction lows of a terror attack…

From BTFPTAD to BTFBTAD

Because whoever is buying knows that if stock sell-off then the terrorists win… which can be summed up as…

European “investors” bought the deadliest terror attack dip…

Because in the new normal – It’s easy…

BUT… The Fed had different views and unleashed The Hawks to tamp down the terror attack exuberance:

- *EVANS: I THINK THE FUNDAMENTALS ARE REALLY QUITE GOOD

- *EVANS: MARCH PROJECTED FED HIKE PATH IS `A PRETTY GOOD SETTING’

Across asset classes, only The USD Index maintained the reaction (stocks, bonds, and gold reverted)

On the day, in The US, Nasdaq was bid (thank sto Biotechs) and Trannie whacked (airlines) but Dow and S&P batteled between bullish terrorism and hawkish fed…

Dow Futures show exactly what happened – machines ran stops off the lows but were unable to maintain momentum (no matter what JPY did) to new highs and so collapsed into the close…

As USDJPY and Stocks tracked each other perfectly…

Traders rushed for the safety of Biotechs..

VIX was slammed to a 13 handle once again but Fed’s Evans’ hawkish comments sparked a lift in VIX…

Treasury yields and stocks decoupled early, then yields spiked after EU closed…

until Europe closed then a flood of selling struck…

The USD Index was bid led by EUR weakness and a plunge in cable… as Brexit odds rose…

Commodities all rallied on the Brussels headlines then spent the rest of the day giving it all back as the dollar rallied…

Charts: Bloomberg

END

It is now 8 straight weeks, that the “smart money” has sold stocks as they do not believe the rally. They must have read David Stockman. (see next article after this one)

(courtesy zero hedge/Bank of America)

“This Is Unprecedented”: Smart Money Throws Up All Over “Rally”, Sells Stocks For Eight Straight Weeks

First it was five weeks; then it was six straight weeks; then a whopping seven weeks of selling in a row even as the market rose 1.1% higher. And now, in an unprecedented for a bear market rally move, the “smart money”, i.e., BofA’s hedge funds, institutional, and private clients, havbe sold stocks for a whopping 8 consecutive weeks.

As BofA’s Jill Hall writes, “last week, during which the S&P 500 climbed 1.4%, BofAML clients were net sellers of US stocks for the eighth consecutive week, in the amount of $1.4bn—suggesting clients still doubt the sustainability of the rally. This is the longest selling streak since Oct-Dec 2010, when clients sold stocks for 12 consecutive weeks. (Following this, they were cumulative net buyers during the first quarter of 2011 and for the year as a whole). Similar to the prior week, all three client groups (hedge funds, private clients and institutional clients) were net sellers, led by institutional clients. Net sales were chiefly in large caps, while small caps saw inflows.”

So as insiders continues to throw up all over the rally, who is buying? The usual IG debt-funded suspect of course: