Gold: $1,220.90 down $1.50 (comex closing time)

Silver 15.19 UNCHANGED

In the access market 5:15 pm

Gold $1221.50.00

silver: 15.23

Let us have a look at the data for today.

At the gold comex today, we had a poor delivery day, registering 0 notices for nil ounces and for silver we had 0 notices for nil oz for the active March delivery month.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 212.17 tonnes for a loss of 91 tonnes over that period.

In silver, the open interest FELL by only 1333 contracts DOWN to 170,580 as the silver price was down by 7 cents with respect to Thursday’s trading . In ounces, the OI is still represented by .852 billion oz or 122% of annual global silver production (ex Russia ex China).

In silver we had 0 notices served upon for nil oz.

In gold, the total comex gold OI rose by 306 contracts to 497,522 contracts despite the fact that the price of gold was down $2.30 with Thursday’s trading.(at comex closing). I was expecting a larger contraction in OI in both gold and silver and as such expect continual raids in both metals

we had no changes in the GLD despite gold’s drubbing for the past 3 days/ thus the inventory rests tonight at 823.74 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,/we had no changes in inventory tonight, and thus the Inventory rests at 328.914 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fell by 1333 contracts down to 170,580 as the price of silver was down 7 cents with Thursday’s trading. The total OI for gold rose by 306 contracts to 497,522 contracts despite the fact that gold was down $2.30 in price from Thursday’s level.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

off today

2b COT report/

(Harvey)

2c) FRBNY

Harvey

3. ASIAN AFFAIRS

i)Late SUNDAY night/ MONDAY morning: Shanghai closed DOWN BY 21.61 POINTS OR 0.73% , / Hang Sang closed FOR HOLIDAY The Nikkei closed UP 131.62 POINTS OR 0.71% . Australia’s all ordinaires was CLOSED FOR THE HOLIDAY. Chinese yuan (ONSHORE) closed DOWN at 6.5161. Oil ROSE to 39.62 dollars per barrel for WTI and 40.46 for Brent. Stocks in Europe MOSTLY CLOSED FOR HOLIDAY . Offshore yuan trades 6.5222 yuan to the dollar vs 6.5161 for onshore yuan.

.

REPORT ON JAPAN

none today

REPORT ON CHINA

Friday trading in China:

ii)Yuan weakens for the 6th straight day as China sends a signal to the USA not to raise rates once or less they will massively devalue sending shock waves around the globe.

( zero hedge)

iv) It sure looks like China is preparing for massive layoffs. However they do not want social unrest, so they warn officials that their jobs are on the line with citizens protest:

( zero hedge)

v)Sunday night/Monday morning

Early this morning, we get a report from New York based China Beige Book International, a corporation which tries to give an honest assessment of what is going on in China. It revealed a huge plunge in their unemployment rate to a 4 yr low as China desperately tries to adjust from a smoke-stack export model to a domestic consumption model. Their problem is that they will have million of people unemployed and if China cannot get these people relocated, there will be massive, social unrest:

( zero hedge)

vi)Hugh Hendry is another extremely bright individual and we must always pay attention to what he says. He was invited for a conversation with another brilliant individual by the name of Raoul Pal, a close friend of Grant Williams (Hmmm fame). They have a paid webcast and their thoughts are always enlightening.

Today’s talk was about China. Strangely Hendry went against his host as stated that if China devalues by 20% (to 8 yuan/dollar)” the world is over, everything hits the wall”. He states that the USA dollar will rise to astronomical heights, causing scarcity of that currency together with a collapse of all commodity prices and in turn, a collapse in emerging markets with huge defaults on their sovereign bonds etc.He describes if that happens, China will be king of a MAD MAX world and who would want that? Hendry states that the only way out for China is for a stronger yuan, yet with a high Debt to GDP ratio of 350% he does not know how this is possible.

We now have two competing forces out there on China:

a) Kyle Bass who states that China must devalue

b) Huge Hendry who believes that China can muddle along at current yuan levels as the percentage of world trade has not been hurt at all, despite the lower amounts of world trade.

this is a must see/read.

( zero hedge)

EUROPEAN AFFAIRS

i)SCARY!! Belgian nuclear guard murdered Thursday night and had his access badge stolen.

( ZERO HEDGE)

ii)Like Japan the demographics in Europe is just awful as the birth rate is around 1.5 children per woman. There is just not enough new workers to pay for the retirees

Russian and Middle Eastern Affairs

i) Interesting!!! Jordan blames Turkey for terror in Europe as Erdogan supplied the necessary stuff to ISIS. They also blames Israel for not attacking ISIS on their borders. The Israelis had two enemies right on their border with Syria, Hezbollah and ISIS. Israeli did the correct strategy by letting both of them attack each other and they stayed out of their way:

( zero hedge)

ii) The ancient city of Palmyra has been rescued by Hezbollah forces and Iran. Putin congratulated ASSAD but no congratulatory message was sent by Obama:

( zero hedge)

GLOBAL ISSUES

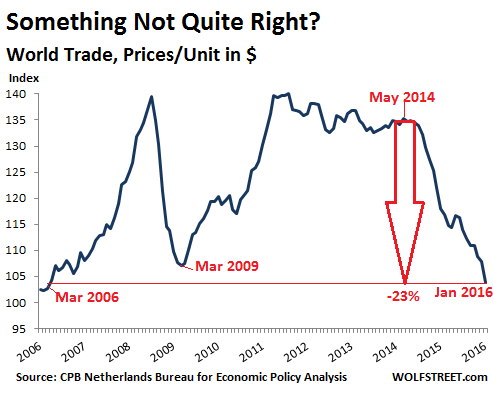

i) A very important warning from Deutsche bank. They are stating that global trade has lagged behind GDP growth. They actually state that peak global trade occurred in 2007 and has been downhill since. I have always used the Baltic Dry Index as a barometer of global trade and with the index at just above 400, having fallen from 10,000 in 2009, you can visually see the writing on the wall. Thus currency wars to get a little bigger piece of a declining trade is futile

OIL MARKETS

It is now official, the entire surge in price of oil was nothing but the biggest short squeeze ever

( zero hedge)

PHYSICAL MARKETS

i)Our good friends over at Barrick are being continuing to be plagued with lawsuits over their failure to bring Pasqua Lama into production.

( Reuters/GATA)

ii)Doorknobs!! These idiots (New Gold) are hedging again:

( Kovan/NationalPost Toronto)

iii)We have Ted Butler’s latest piece. I am not in agreement with his thesis that JPMorgan has acquired over 500 million physical oz. However if he is right, it is criminal activity to the highest degree: knocking down the price of a commodity so as to acquire it cheaply.

( Ted Butler)

iv) Bill Holter’s latest piece is entitled:

“THE RALLY YOU NEVER SELL!!”

USA STORIES WHICH WILL INFLUENCE THE PRICE OF GOLD/SILVER

i)The final figures for 2015 are now in and the USA GDP came it as expected at 1.4% Corporate profits plunged. However first quarter 2016 is heading southbound in a hurry:

( zero hedge)

ii)Although the TVIX or the double levered long VIX complex falls to record lows, something unusual is happening in that the number of shares outstanding for the TVIX has risen remarkably in a similar fashion to the Blackrock ETF of a few weeks ago. VIX is a volatility index and a rise in volatility means trouble for the market. Is the Dow/NYSE reaching an airpocket?

(zero hedge)

iii) The so called “restaurant recovery” is now over in the USA as casual dining sales tumble for the 4th straight month. It will be interesting if the BLS reports a higher bartender and waiter increase in jobs to be announced next week

iv)Personal income growth reported early this morning, is the weakest since Q3 last yr at 0.2%. However spending growth slowed 3.8% year over year. Spending was revised downward from that big spike in January. The consumer is just not spending because they ran out of money..( zero hedge)

v)Because spending fell with the revised first quarter report, the Atlanta Fed has no choice but to lower its GDP for first quarter to 1% or less:

vi)And as expected the Atlanta Fed lowered its expectation of first quarter GDP to only .6%. Janet Yellen has a severe problem!( zero hedge)

vii)Thanks to Obamacare, the USA citizens spent the most on health care this last year:

( zero hedge)

viii)The Illinois supreme court rejects Chicago’s Pension reform bid and this sets the stage for Chicago and Illinois’s insolvency:

ix)California raises its minimum wage to 15 dollars per hr. This will be phased in over 5 yrs:( zero hedge)

x)As Connecticut has a huge funding problem as the budget defict surges, they are seeking to tax the Yale University Endowment as a plug:

xii)The hits just keep on coming:

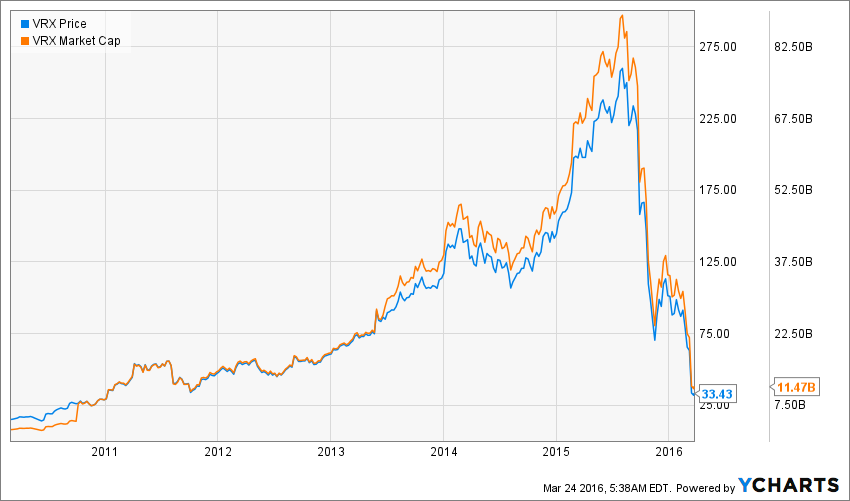

First Valeant must testify under oath

Second: the firm may have a merger agreement violation on that 1 billion pharmaceutical acquisition of a female libido drug

( zero hedge)

xiii)For your enjoyment a full account of who Valeant rose to great heights from its infancy in 2009 to its now probable ultimate collapse. Stockman states that there are other Valeants trading on the NYSE ready to blow

( David Stockman/ContraCorner)

xiv) Wrap up with Greg Hunter and Dr Paul Craig Roberts

(Greg Hunter/Craig Roberts

Let us head over to the comex:

The total gold comex open interest rose to 497,522 for a gain of 306 contracts despite the fact that the price of gold was down $2.30 in price with respect to Thursday’s trading. I expected a much deeper slide in OI. As I stated before the holiday weekend: “Expect our bankers to undergo relentless attacks on our two precious metals.” They have not disappointed us with their antics. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month or for that matter an inactive month, and 2) a continual drop in the amount of gold standing in an active month. Today, both scenarios were in order. The front March contract month saw its OI fall by 24 contracts down to 28.We had 0 notice filed upon yesterday, and as such we lost 24 contracts or an additional 2400 oz will not stand for delivery. .After March, the active delivery month of April saw it’s OI fall by 26,977 contracts down to 125,328. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was fair at 208,167. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was good at 242,029 contracts. The comex is not in backwardation. First day notice is this Thursday, March 31. The options for the comex is over today. However we still have LBMA options and OTC options which expire March 31.2016.

Today we had 0 notices filed for nil oz in gold.

March contract month:

INITIAL standings for MARCH

March 28/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 64.30 oz

brinks |

| Deposits to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 4639.228 oz

Delaware,HSBC Scotia |

| No of oz served (contracts) today | 0 contracts (nil oz) |

| No of oz to be served (notices) | 28 contracts(2800 oz) |

| Total monthly oz gold served (contracts) so far this month | 696 contracts (69,600 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 192,293.3 oz |

Today we had 0 dealer deposits

Total dealer deposits; nil oz

Today we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

Today we had 3 customer deposits:

i) Into Delaware: 1812.651 oz

ii) Into HSBC: 897.577 oz

iii) Into Scotia: 1929.000 oz (60 kilobars)

total customer deposits: 4,639.228 oz

Today we had 1 customer withdrawals:

i) Out of Brinks; 64.30 oz 92 kilobars

total customer withdrawals; 64.30 oz

Today we had 0 adjustment:

MARCH INITIAL standings

/March 28/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 218,179.480. oz

Scotia,CNT, Brinks |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served today (contracts) | 0 contractsnil oz |

| No of oz to be served (notices) | 116 contracts (580,000, oz) |

| Total monthly oz silver served (contracts) | 1199 contracts (5,995,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 11,136,487.2 oz |

today we had 0 deposits into the dealer account

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 0 customer deposits

total customer deposits: nil oz

We had 3 customer withdrawals:

i) Out of Scotia:

60,480.190 oz

ii) Out of CNT: 181,749.000 oz??? How can this be possible?

iii) Out of Brinks:

5950.29 oz

:

total customer withdrawals: 218,179.480 oz

we had 1 adjustment

i) Out of CNT: 29,505.43 oz was adjusted out of the customer account and this landed into the dealer account of CNT

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 258,646 | 79,815 | 73,290 | 127,081 | 327,075 | 459,017 | 480,180 |

| Change from Prior Reporting Period | ||||||

| 10,987 | 1,668 | -3,717 | 8,471 | 22,934 | 15,741 | 20,885 |

| Traders | ||||||

| 172 | 102 | 103 | 48 | 59 | 273 | 220 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 51,562 | 30,399 | 510,579 | ||||

| 1,752 | -3,392 | 17,493 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, March 22, 2016 | |||||

And now for our silver COT:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 82,933 | 19,504 | 18,377 | 47,743 | 124,985 | |

| 6,327 | 971 | -741 | 1,296 | 8,514 | |

| Traders | |||||

| 99 | 50 | 47 | 34 | 42 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 175,775 | Long | Short | |

| 26,722 | 12,909 | 149,053 | 162,866 | ||

| 2,713 | 851 | 9,595 | 6,882 | 8,744 | |

| non reportable positions | Positions as of: | 154 | 123 | ||

| Tuesday, March 22, 2016 | © SilverSeek.com | ||||

And now the Gold inventory at the GLD

March 28/no change in inventory at the GLD/Inventory rests at 823.74 tonnes

March 24.2016: a deposit of 2.08 tonnes of gold into its inventory/and this after a big drubbing these past two days??/Inventory rests at 823.74 tones

March 23/no changes at the GLD today despite the gold drubbing. Inventory rests at 821.66 tonnes

March 22./no changes in inventory at the GLD/Inventory rests at 821.66 tonnes

MARCH 21/another big deposit of 2.68 tonnes/inventory rests tonight at 821.66 tonnes

(and this was done with gold down $10.00 today!!)

March 18.I GIVE UP!! WITH GOLD DOWN TODAY, THE CROOKS OVER AT GLD ADDED ANOTHER IDENTICAL 11.89 TONNES OF PAPER GOLD INTO THEIR INVENTORY.

INVENTORY RESTS THIS WEEKEND AT 818.98 TONNES. IF I WAS A SHAREHOLDER OF THIS ENTITY I WOULD BE VERY WORRIED.

March 17/we had a whopper of a deposit tonight: 11.89 tonnes/with London in backwardation this is nothing but a paper addition/inventory rests tonight at 807.09 tonnes

March 16.2016:/we had a deposit of 2.09 + 2.97(last in the evening) tonnes of gold into the GLD/Inventory rests at 795.20 tonnes

March 15/ no changes in gold inventory at the GLD/Inventory rests at 790.14 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

March 28.2016: inventory rests at 823.74 tonnes

end

And now your overnight trading in gold, MONDAY MORNING and also physical stories that may interest you:

By Mark O’Byre

off today

end

Our good friends over at Barrick are being continuing to be plagued with lawsuits over their failure to bring Pasqua Lama into production.

(courtesy Reuters)_

Barrick Gold to face U.S. group lawsuit over South American mine

Submitted by cpowell on Fri, 2016-03-25 06:04. Section: Daily Dispatches

By Amrutha Penumudi

Reuters

Thursday, March 24, 2016

A federal judge on Wednesday granted class certification for a U.S. class-action lawsuit filed against Barrick Gold Corp claiming that Barrick misstated facts of its now-halted Pascua-Lama gold-mine project on the border of Argentina and Chile.

The class certification means the world’s largest gold producer will have to face the U.S. lawsuit.

U.S. District Judge Shira Scheindlin in Manhattan said that shareholders who purchased Barrick shares from May 7, 2009, through Nov. 1, 2013 are a part of the class-action lawsuit.

Investors who bought Barrick’s common stock during this period have said Barrick touted Pascua-Lama as a world-class project even as it became clear that the project would fall short of expectations. …

… For the remainder of the report:

http://www.reuters.com/article/us-barrick-gold-lawsuit-idUSKCN0WQ0E5

end

Doorknobs!! These idiots are hedging again:

(courtesy Kovan/NationalPost Toronto)

Once reviled, gold hedging makes an unexpected return

Submitted by cpowell on Fri, 2016-03-25 06:24. Section: Daily Dispatches

By Peter Kovan

National Post, Toronto

Thursday, March 24, 2016

New Gold Inc. was braced for a vicious backlash from the investment community when it decided to hedge some gold production earlier this month.

After all, hedging is the gold industry’s ultimate dirty word. It became such a toxic subject during the last decade that most chief executives decided that even talking about it was off-limits. And New Gold is led by Randall Oliphant, who headed up Barrick Gold Corp. back when it had the biggest — and most reviled — hedge book in the business.

But the response to New Gold’s move wasn’t negative. Instead, almost everyone cheered.

“We’ve heard nothing but positive reactions from shareholders, analysts, and media people to what we did,” said Oliphant, New Gold’s executive chairman. “So that will give other people who want to do this sort of stuff some ammunition.” …

… For the remainder of the report:

http://business.financialpost.com/news/mining/once-reviled-gold-hedging-…

* * *

Australian Gold Miners Are Starting to Embrace Hedging Amid Strong Prices

By Peter Ker

Sydney Morning Herald

Thursday, March 24, 2016

Once upon a time, Newcrest Mining was adamant that shareholders did not want the company to hedge its gold production.

“Our investors are looking for spot price exposure,” former chief executive Greg Robinson said in 2013, insisting that shareholders could hedge their own positions by purchasing shares in other companies and commodities.

However, with the gold price near record highs in Australian dollar terms, the largest gold miner on the ASX has decided to embrace hedging.

Newcrest confirmed on Thursday a portion of the gold produced at the Telfer mine in Western Australia had been hedged until June 2018. …

… For the remainder of the report:

http://www.smh.com.au/business/mining-and-resources/newcrest-mining-chan…

end

Here is Ted Butler’s latest piece. I am not in agreement with his thesis that JPmorgan has acquired over 500 million oz. If he is right, it is criminal activity to the highest degree: knocking down the price of a commodity so as to acquire it cheaply.

(courtesy Ted Butler)

Five Years That Changed Silver Forever

|

March 24, 2016 – 8:14am

Ask any casual observer of the silver market what happened to the metal over the past five years and you’re likely to hear how the price fell from nearly $50 in April 2011 to under $14 at recent lows – a stunning decline of 70%. If you inquire further, you’ll likely hear a number of reasons for the decline, ranging from an oversupply of the metal, a strengthening dollar, falling inflation rates, and the collapse of the commodities markets.

What you will not hear is how a specific development has transpired over the past five years that ensures a coming explosion in the future price of silver beyond the most bullish predictions and optimistic upside targets. You’re also not likely to hear that the stunning decline in the price of silver over the past five years was a deliberate feature of an unusually bullish development that promises to change forever the future price landscape.

While I have closely researched the silver market for more than 30 years, uncovering more original findings (including silver’s price manipulation) than anyone, I fully admit that I did not immediately see the monumental change that began to occur five years ago. This astonishing development that had begun in 2011 did not come clear to me until late 2013.

I discovered that the largest U.S. bank, JPMorgan Chase, began to accumulate massive amounts of physical silver starting in 2011 and has continued that accumulation to this day. All told, I believe JPMorgan has acquired somewhere between 400 and 500 million ounces, the largest privately held stockpile of silver in history.

What this means is that the future price of silver is now destined to move far higher in price than anyone can imagine. I wasn’t looking for something to come along that would supersede my already ultra-bullish outlook on silver, but that is what occurred. That’s because the obvious motive JPMorgan has whenever it acquires a large investment position is to profit on that position to the greatest degree possible. And since JPMorgan is now in position to profit enormously when silver prices soar, that means anyone holding silver will profit as well.

How did JPMorgan come to acquire hundreds of millions of ounces of physical silver? It was a circuitous route, beginning in the financial crisis of 2008 when JPMorgan took over a failing Bear Stearns, then the largest short seller in COMEX gold and silver futures contracts. JPMorgan stepped smoothly into Bear Stearns’ role as the main silver and gold price manipulator and proceeded to drive the price of silver from $21 in March 2008 to under $9 through massive short sales on the COMEX. In the years that followed, JPMorgan continued its new role as the largest short seller in COMEX silver and reaped billions of dollars in ongoing profits by shorting silver on price rallies and buying back those short positions after it rigged the prices lower.

With manipulative intent and practice, JPMorgan continued to make illicit profits on the short side of COMEX silver until late 2010. Then a developing physical shortage in silver drove prices to almost $50 by the end of April 2011. JPMorgan was not prepared for the developing physical shortage and the price run up nearly crippled the bank. That’s when it dawned on JPM that it was on the wrong side (the short side) of silver and the bank resolved to get on the right side – the long side. But first, JPMorgan had to get off the short side.

JPM did this by causing silver futures prices to plummet with the full consent of the COMEX and government regulators at the CFTC, a process that has continued to this day. JPM regained control of silver prices on May 1, 2011 and by driving prices sharply lower killed off the developing investment demand that was causing the physical shortage. But while JPMorgan regained control of silver prices on the COMEX, it could not buy as many futures contracts as it desired without causing prices to soar – it needed another angle. That other angle was for the bank to begin to buy physical silver while it continued to sell short COMEX paper futures contracts. This way, JPMorgan could have its cake and eat it too – continuing to profit on paper short sales while acquiring physical silver at the depressed prices it had created. I labeled JPMorgan’s actions as the perfect crime in a public article in December 2014.

http://www.silverseek.com/commentary/perfect-crime-13944

JPMorgan behaved illegally in manipulating prices lower while accumulating all the physical silver it could. However, there is no limitation on what any entity can hold in a physical commodity position. Limitations exist (loosely enforced) on what traders can hold in futures and other derivatives, but no such limitations apply to physical positions. This cleared the way for JPMorgan to hold as much physical silver as it could. Since the price of COMEX silver determines the price for silver throughout the world, this put JPMorgan in the catbird’s seat, by enabling it to depress the COMEX price and then scooping up physical silver in prodigious quantities and at ridiculously depressed prices.

As far as the forms of physical silver that JPMorgan has acquired over the past five years, the simple answer is in any form that could be acquired in size. Most of the silver that JPMorgan acquired was in the form of 1,000 ounce bars, the industry standard for silver and the kind deliverable on COMEX futures and held in the worlds silver ETFs and other investment vehicles. JPMorgan has secured hundreds of millions of ounces from the big silver ETF, SLV, and in deliveries against COMEX futures contracts, some of it held in JPM’s own COMEX warehouse, which opened for business in May 2011 and is now the largest COMEX silver warehouse (confirming my timeline). Their warehouse now holds 70 million ounces and is their most visible holding. Harder to see is the 100 million ounces they likely have in their London warehouse where they moved out 100 million ounces of other people’s silver to make room for their own in 2012.

But JPMorgan has also bought silver in the form of American Silver Eagles and Canadian Maple Leafs to the tune of 150 million ounces over the past five years, quickly re-melting the coins into 1,000 ounces bars because it would be impossible to sell so many coins in coin form. In fact, the curious riddle of record sales of Silver Eagles and Maple Leafs over the past five years coupled with bona fide reports of weak retail sales of these coins was an important clue that someone big was buying many of the coins, roughly 50% of all such coins sold.

When I say I wasn’t looking to uncover the most bullish development ever in silver that is an understatement. But as an analyst, I look to the data first and foremost. Not only has that data tipped me off to what JPMorgan has been up to, the continuing flow of public data confirm my conclusion daily. Everything from COMEX silver warehouse movement, deliveries against futures contracts, changes in the big silver ETF, SLV, sales of silver coins from the U.S. and Royal Canadian Mints point to the massive accumulation of silver by JPMorgan. They are positioned to make $100 billion or more in a runaway silver market. They will make $1 billion on a $2 rise in silver.

The very last thing I would be interested in at this stage of my life, is to come up with some wacky premise that threatened to undermine many of my previous findings. I studiously avoid anything that would damage a reputation I have spent decades constructing. On the other hand, if I have discovered the most shockingly bullish silver development ever, how could I not proclaim it far and wide?

I have discovered that JPMorgan has accumulated more physical silver than any private entity in history and I don’t care if great numbers of observers come to agree with me or not. I will openly discuss this with anyone who has questions, but most importantly I would remind you that if I am correct in my assertion anyone who aligns themselves with what JPMorgan has done and buys silver will most likely reap financial rewards of truly amazing proportions.

Ted Butler

March 24, 2016

end

And now Bill Holter with his very important piece:

THE RALLY YOU NEVER SELL!!

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.5161 / Shanghai bourse IN THE RED, DOWN 21.61 OR 0.73%/: / HANG SANG CLOSED FOR THE HOLIDAY

2 Nikkei closed UP 131.62 or down .77%

3. Europe stocks MOSTLY CLOSED FOR THE HOLIDAY /USA dollar index UP to 96.30/Euro DOWN to 1.1158

3b Japan 10 year bond yield: FALLS TO -.084% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.52

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 38.86 and Brent: 39.65

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS to 0.180% German bunds in negative yields from 8 years out

Greece sees its 2 year rate RISE to 9.97%/:

3j Greek 10 year bond yield RISE to : 8.77% (YIELD CURVE NOW INVERTED)

3k Gold at $1217.60/silver $15.25 (7:15 am est)

3l USA vs Russian rouble; (Russian rouble UP 5/100 in roubles/dollar) 68.12

3m oil into the 39 dollar handle for WTI and 40 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9774 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0906 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN STARTS ITS CAMPAIGN AS TO WHETHER EXIT THE EU.

3r the 8 Year German bund now in negative territory with the 10 year FALLS to + .180%

/German 8 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.91% early this morning. Thirty year rate at 2.68% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Rise In Thin Trading On Back Of Yen Weakness; Europe Closed

With European markets closed across the continent on Monday as the Easter holiday continues, overnight Asia was busy with the Shanghai Composite letting off some steam, and closing down 0.7% at session lows on concerns the Shanghai and Shenzhen home bubble have been popped prematurely by the politburo.

Japan was a different story with the Yen sliding following a report by the Sankei newspaperthat Abe will announce in May his intention to delay the planned April 2017 sales tax hike from 8% to 10%, coupled with additional reports that Japan will unveil a major fiscal stimulus (and just on Friday Abe said he is “not thinking at all about supplemental budget” at this time).

This turned out to be nothing but the latest Japanese market trial balloon, because hours after the report, Abe reiterated that Japan’s sales tax will indeed be raised as scheduled in April 2017 “barring a crisis like the one caused by the collapse of Lehman Brothers”, while cabinet secretary Suga said there is no truth in the report that the government has decided to delaythe sales tax hike. By the time these denials hit, however, the FX momentum algos were engaged, and the USDJPY jumped, leading to seven straight days of Yen losses, the longest losing streak since October 23 and in the process sending the Nikkei higher by 0.8%.

And thanks to the low volume, illiquid futures market, U.S. equity index futures followed the Japanese rebound, with the E-Mini rising 0.3% to 2034.5 in the thin premarket trade. Dollar falls slightly, reversing earlier gains, while gold also declines. Oil rises for first day in 3. Traders are pricing in a 6% chance of a U.S. rate increase in April, and about 38% probability of a boost in June, according to Fed funds futures. Increasingly many strategists are concerned that the market is underplaying the risk of a June rate cut and as a result odds will have to rise substantially in the coming weeks so the Fed will avoid a “surprise.”

Markets Snapshot

- S&P 500 futures up 0.3% to 2035

- Stoxx 600 closed

- MSCI Asia Pacific up less than 0.1% to 128

- Nikkei 225 up 0.8% to 17134

- Hang Seng closed

- Shanghai Composite down 0.7% to 2958

- S&P/ASX 200 closed

- US 10-yr yield up less than 1bp to 1.91%

- Dollar Index down 0.06% to 96.22

- WTI Crude futures up 1.1% to $39.88

- Brent Futures up 0.8% to $40.78

- Gold spot down less than 0.1% to $1,216

- Silver spot up 0.3% to $15.23

Top Global News

- Japan’s NTT to Acquire Dell Units for $3.055b: NTT Data to acquire Dell Systems Corp. and other units related to IT services.

- Sanders Says He’s Seized Momentum After Crushing Caucus Wins: Sanders received 73% in Washington state, day’s biggest delegate prize, 70% in Hawaii, 82% in Alaska.

- Bull Market in U.S. Stocks Goes AWOL as History Rewards Patience: S&P 500 Index hasn’t seen a new high in 10 months, longest streak outside a bear market since 1995.

- Avon Activists Near Deal to Call Off Proxy Fight: WSJ: Deal would allow Barington Capital, NuOrion Partners to approve new independent director.

- Third Point Warns Seven & I Against Nepotism Deciding CEO: Seven & i CEO Toshifumi Suzuki, 83, is having chronic health problems; investors fear he may try to name his son, Yasuhiro Suzuki, to lead Seven?Eleven Japan, eventually become president of Seven & i, Loeb wrote.

- Microsoft Said to Meet With Possible Yahoo Bidders Seeking Funds: MSFT met with possible bidders for Yahoo! such as Verizon, private equity firms, who may seek backing from the software maker for their offers.

- Fed’s Williams Sees ’Huge Impact’ on U.S. From China, Brazil: “The real issue is the global financial and economic developments. There’s uncertainty about what’s happening around the world and how that feeds back to the dollar and the U.S. economy,” Williams, who doesn’t vote on monetary policy this year, told CNBC.

- ‘Batman v Superman’ Soars in Boost to Warner’s DC Franchise: Film opened with weekend sales of $170.1m in North American theaters, meeting estimates, giving studio a new foundation to build on.

- Qlik Tech Said to Hire Morgan Stanley for Possible Sale: Reuters: Co. has begun exploring strategic alternatives.

- Oil Halts Two-Day Slide After U.S. Rig Count Resumes Decline: Rigs targeting oil in the U.S. fell by 15 to 372, according to Baker Hughes.

Looking quickly at regional markets, we start in Asia where equities traded mixed with Topix, Nikkei 400 outperforming and CSI 300, Sensex 30 underperforming. As noted earlier the Chinese weakness was led by concerned about the potential bursting of the housing bubble: “developers are facing some headwinds as these measures are likely to cause immediate negative impact on the demand side,” said Wu Kan, fund manager at JK Life Insurance in Shanghai. “The market is in the stage of building a bottom so we’ll see lots of ups and downs.” 8 out of 10 sectors rise with health care, utilities outperforming and finance, energy underperforming.

Over the weekend, we got the latest China Jan.-Feb. Industrial Profit data, which rose 4.8% Y/y while China Feb. Diesel Stocks Increased 38.26% M/m; Shanghai New Home Sales Rise 48% on Week, Uwin Says.

Asian Top News

- Online Property Companies Soar on China’s Real Estate Recovery: Leju’s ADRs jump most on Bloomberg China-US Equity Index

- Woes Descend on Japanese IPOs as Stocks Tank on First Day: 6 of 21 cos. this year opened below their offer price

- Amazon to Flipkart Clash in India’s Nascent E-Commerce Market: Battlefield challenges accelerate pace of innovation

- Indian Paradox: As Economy Soars Modi Reforms Face Big Headwinds: IMF warns prosperity at risk without structural reforms

- Pakistan Vows to Hunt Terrorists After Easter Sunday Carnage: At least 65 people killed, death toll may rise further

European markets are closed today due to the Easter holiday.

European Top News

- Belgium Conducts More Raids in Aftermath of Terror Attacks: Authorities conducted 13 raids in Belgium on Sunday, detaining nine people as part of their efforts to prevent further terrorist attacks.

- Abengoa Wins Support of Creditors for Extension: Europa Press: Co. lined up enough support from creditors to ask court in Seville for an extension of several months in process of negotiation of financial restructuring; Abengoa Presents Standstill Request, Has 75% Creditor Support

FX markets are in consolidation mode for the most part, with the run up to US payrolls on Friday a usually quiet affair. This should keep many specs on the side-lines for now, but there looks to be some respite for GBP despite the uncertainty over the Brexit vote overwhelmingly restrictive. Nevertheless, Cable has recovered towards 1.4200, but any move through the figure should find plenty of sellers from 1.4225-50. EUR/GBP should find some support from the mid .7800’s also, though larger support not until the mid-.7700’s.

USD/JPY has made some decent gains from the mid 111.00’s, but will start to find better offers ahead of 114.00, with 113.65¬70 capping the Asian session today. The commodity currencies are still looking heavy, but with Oil up off the lows, USD/CAD is threatening a return through 1.3200. All very tight so far, with much of Europe away, but North American players may take advantage of thin markets.

In Commodities, the energy complex was in a consolidation mode amid holiday thinned trading volumes and ahead of the eagerly awaited meeting by oil producing countries on April 17th to discuss the output freeze plan.

Bulletin Headline Summary from Bloomberg

- Treasuries fall in overnight trading while European markets closed for holiday and Asian equity markets mixed; week’s U.S. auctions begin today with $26b 2Y notes, WI yield 0.87%, compares with 0.752% awarded in Feb., was 21st straight 2Y auction to stop through or even with WI yield at bidding deadline.

- Hedge funds are crowding into U.S. Treasuries, and that has bond traders bracing for more turbulence. While the Federal Reserve doesn’t break out hedge-fund ownership, a group seen as a proxy increased its holdings to a record $1.27 trillion

- Japanese primary dealers say negative bond yields are here to stay in 2016; bond investors are still trying to adjust to the conditions that have turned yields on 70% of the market negative; Japanese banks are sitting on profits made last year and can withstand the impact of negative rates, according to the Bank of Japan

- Gold has been thrown onto the defensive by a resurgent dollar, sinking to the lowest in more than a month as the U.S. currency’s rally hurts the allure of the metal that’s been the best-performing commodity of 2016

- Oil’s rebound to about $40 a barrel means some investors are nursing losses after betting that Saudi Arabia would abandon its three-decade-old currency peg

- It’s been barely a month since investors first started betting on a copper rally, and they’re already on the retreat. Money managers cut their wagers on price gains for a second week, pulling back just before futures capped the worst slump in a month

- Terrorism probes advanced across Europe in the wake of last week’s deadly bombings in Brussels, with suspects arrested in Italy and the Netherlands, and Belgium carrying out police raids in several areas

- Sovereign 10Y bond yields mostly unchanged; European equity markets closed, Asian mixed; U.S. equity-index futures rise. WTI crude oil higher; gold and copper fall

end

In order to catch up here is a summary of Friday trading in China:

Holiday Market Summary

With all of Europe and the Americas closed for holiday, what little market action there was overnight came out of Asia, where China once again was engaged in its last hour “National Team” market manipulation, which saved the SHCOMP from a red close after the now traditional last hour buying spree, pushed the Shanghai Composite from red on the session an hour before close to near the highs of the day.

Elsewhere Japan’s Nikkei rose 0.7% after tracking the weakening yen as it always does tick for tick, which in turn dropped on some more BOJ jawboning (BOJ board member Harada says negative rate can go lower and there is room for more easing), although the biggest weekly gain in the USDJPY in two months was driven by news that Japanese investors bought record sum of foreign bonds and stocks last week as local investors continue their “silent bank run” (first noted two months ago) in an attempt to get away from Japan’s oppressive negative rates.

And since this, by definition, is Yen-negative, and since the entire Japane stock market is a function of currency strength, Japan’s capital flight from local stocks was…. bullish for local stocks.

Ah, the magic of centrally-planned markets.

To summarize, the MSCI Asia-Pacific Index adds 0.2%, as gains in consumer shares across the continent outweighed weakness in telecom and health care stks.

Away from Asia, in less than an hour the BEA will release its final revision to Q4 GDP; as a reminder the second revision was for a 1.0% print but since this data is woefully old, the markest will certainly ignore it – especially since it is closed – and will be far more focused on the Q1 GDP which yesterday the Atlanta Fed estimated has tumbled as low as 1.4% after hitting 2.7% just over a month ago.

end

i)Late SUNDAY night/ MONDAY morning: Shanghai closed DOWN BY 21.61 POINTS OR 0.73% , / Hang Sang closed FOR HOLIDAY The Nikkei closed UP 131.62 POINTS OR 0.71% . Australia’s all ordinaires was CLOSED FOR THE HOLIDAY. Chinese yuan (ONSHORE) closed DOWN at 6.5161. Oil ROSE to 39.62 dollars per barrel for WTI and 40.46 for Brent. Stocks in Europe MOSTLY CLOSED FOR HOLIDAY . Offshore yuan trades 6.5222 yuan to the dollar vs 6.5161 for onshore yuan.

FIRST: report on Japan

none today

SECOND: report on China

Friday trading in China:

Yuan weakens for the 6th straight day as China sends a signal to the USA not to raise rates once or less they will massively devalue sending shock waves around the globe.

(courtesy zero hedge)

The Threat Continues: Yuan Weakens For 6th Straight Day – Longest Losing Streak In 2 Years

PBOC fixed the Yuan at its weakest in 3 weeks, pushing the devaluation streak to its longest since early January. However, Offshore Yuan has now dropped over 1.1% against the USD, extending losses for the 6th straight day to 3-week lows. This is the longest streak of weakness in the offshore Yuan since April 2014.

It appears EUR and JPY took enough pain so the basket is reverting to the USD again…

What’s the opposite of passive-aggressive as a clear message is being sent to The Fed –tighten and we unleash the Yuan-weakness-driven turmoil…

Chairman Of Insolvent Chinese Steel Company Hangs Himself Day Before Bond Maturity

Back in October when we first looked at ground zero of the commodity price collapse, we found something striking: as of the end of 2014, one half of China’s commodity companies with corporate debt were totally insolvent – based on Macquarie data they were unable to cover even one interest payment (let along debt maturity) with existing cash creation.

And since in the intervening time period, both commodity prices have dropped far lower, while Chinese corporate debt has proceeded to soar exponentially, we said it was “safe to assume that up to two-thirds of Chinese commodity companies are now at imminent danger of default, as they can’t even generate the cash to pay down the interest on their debt, let alone fund repayments.”

We concluded that “we fully expect this to be the source of the next market freakout: when the punditry turns its attention away from macro China, which has more than enough problems to begin with, and starts to focus on the cash flow devastation in China at the micro, or corporate, level.”

To be sure, the Chinese government has done everything in its power to delay this day of reckoning and mask just how extensive the devastation at the local level is, by having its entire focus on the recently concluded People’s Congress on the topic of sustainability and debt leverage, going so far as to propose a wholesale, and utterly mind-boggling, debt-for-equity exchange at the bank level, one which would involve the nationalization of China’s insolvent commodity enterprises. Alas, we along with most rational observers, are skeptical this plan would ever get off the ground, as it would mean encumbering banks not with secured if impaired loans, but with unsecured equity in still insolvent companies, in the process making China’s solvency problems even worse.

That said, the punditry has indeed started to focus away from macro China and to the “devastation at the corporate level”, most notably in a recent Reuters article which suggested that “China’s campaign to slim down its bloated industries could be derailed by more than $1.5 trillion of debt in its steel, coal, cement and non-ferrous metal sectors, which threatens to overwhelm local banks.”

The story is well known: China is providing more than 100 billion yuan ($15 billion) in the next two years to handle layoffs from coal and steel, but that will only be made available once debts have been settled. Critics say there is no clear mechanism for tackling the debt burden, which will put huge strain on the weakest sections of the banking sector.

The debt figures, revealed in papers submitted to China’s parliament this month, highlight the dilemma facing state firms grappling with surplus capacity and how difficult it will be to pull off this central plank of Beijing’s economic reform plans.

Costs for the estimated 1.3 million coal-sector layoffs alone are as much as 195 billion yuan, and coal industry delegates attending parliament urged government to provide more support to deal with the mounting debts of hundreds of stricken “zombie” firms.

* * *

A lawyer who handles steel industry non-performing loans for mid-sized Chinese banks said: “Banks’ fear is not without reason. The steel sector’s continued slump increases the difficulty of disposing of outstanding non-performing loans.”

The four sectors targeted in the battle against overcapacity owe around 10.2 trillion yuan ($1.56 trillion), according to documents submitted to parliament by Wang Mingsheng, head of Anhui-based coal firm Huaibei Mining.

China’s statistics bureau puts coal and steel debts alone at 8 trillion yuan, of which about a third is bank debt. If 20 percent of that were to go bad in 2016, which industry analysts say is not unrealistic, it would raise Chinese banks’ non-performing loans by nearly half.

Therein, as the bard said, lies the rub, and explains why China will continue jawboning and talking instead of taking any decisive action as there is simply no effective way out: once the debt starts being marked to something resembling fair value, it will unleash a tsunami of insolvencies which Beijing will be helpless to stop, which would then lead to mass layoffs in the tens of millions, social unrest and possibly culminating with civil war as tens of millions of angry workers are no longer able to make enough money to feed their families.

* * *

And while Beijing dithers, and does its best to kick the can as far as it can without doing anything, it was too late for one person: on Friday morning, Dongbei Special Steel Group reported that the company’s Chairman Yang Hua, 53, was found dead after hanging himself in his residence.

We tried to find if the company is at or near insolvency and were unable to confirm this suspicion until last night, when a Chinese news report confirmed that as we expected, the company is indeed insolvent and will most likely be unable to make a 800 million yuan bond payment. To wit:

Dongbei Special Steel announced on the evening of March 25 that, due to tight liquidity, deposit principal and interest payment uncertainty, 800 million yuan bonds maturing 27 15 Eastern Steel CP001 (called the Northeast special steel Group Co., Ltd. 2015 year the first phase of short-term bonds) or face default.

It is reported that the current short margin issue size of 800 million yuan, 6.5% interest rate, the total amount of principal and interest payable of 852 million yuan, the lead underwriter for the China Development Bank.

Joint credit 25 afternoon announcement in Chinese currency network, in view of the Northeast Special Steel, chairman of death by hanging and 15 Eastern Steel CP001 is about to expire payment of principal and interest, will be included in the Northeast Special Steel lowered the credit rating watch list.

At 13:20 on the 24th, the Dalian City Public Security Bureau received a report, found that the chairman Dongbei Special Steel Group Co., Ltd., party secretary Yang Hua (male, 53 years old) Death by hanging at his residence. At present, the authorities are conducting investigations.

But why is this a problem: historically the Chinese government, either directly or indirectly through state-owned banks has mostly bailed out insolvent companies, especially those in the commodity sector. Has something changed this time? It appears the answer is yes.

Earlier this week, Caixin reported that Guangxi Nonferrous Metals Group Co., a state-owned enterprise in the southern region of Guangxi, said in a statement given to the Shanghai Clearing House, on February 22 that it filed an application for bankruptcy in Nanning Intermediate People’s Court in December. What makes this bankruptcy particularly notable is that Shanghai Clearing House is a state-backed financial institution for the interbank market.In other words, the government is now allowing even state-backed companies to go under, a radical departure from its recent bailout ways.

Guangxi Nonferrous owed 14.51 billion yuan to 108 creditors, namely subsidiaries, financial institutions, suppliers, construction companies and private bondholders. The largest creditors are a subsidiary named Guangxi China Tin Group Co. Ltd., which is owed 1.63 billion yuan, and China Development Bank, which holds a debt of 1.60 billion yuan.

The firm has received government subsidies but still reported a loss of 2.29 billion yuan from 2012 to 2014, its financial reports show. In June last year, Guangxi Nonferrous said it was having difficulty repaying its bonds, citing excess capacity and falling prices.

Guangxi Nonferrous was founded in 2008 in Nanning by the State-owned Assets Supervision and Administration Commission, a central government agency that oversees state-owned enterprises, with registered capital of 1.16 billion yuan. The Guangxi government wants to protect its nonferrous metals industry.

“The nonferrous industry is facing downward pressure and the company had limited return on new investments in the past few years,” a person close to Guangxi Nonferrous said. “These factors have resulted in tight cash flow.”

All of this was expected and is proceeding just as we warned last October: after all there is only so far you can stretch reality before the lack of cash flow catches up to you.

But what makes this default especially curious, in addition to the fact that the bankrupt company is an SOE, is that the lender in the case of Guangxi is the same as that behind the imminent, and now tragic bankruptcy, of Dongbei: China Development Bank.

The problem was solved when China Development Bank agreed to help, a bank employee told Caixin. But Guangxi Nonferrous defaulted on two other bond payments that were due in November and February, he said. The company is being restructured, several people with the knowledge of the matter said.

Guangxi Nonferrous’ executives met with creditors on March 18 to discuss restructuring, but no detailed plans were drawn up, the sources said. The management team said at the meeting that the Guangxi government promised to see that the restructuring was done in six months.

And while we lament that there is no way to buy CDS on China Development Bank, these two defaults hint at big trouble ahead for insolvent corporate China.

For the past four years China had effectively bailed out and otherwise “saved” all of its insolvent companies, but that period of wholesale rescues now appears to be over: are these two defaults confirmation that the tipping point in how Beijing handles bankruptcies, has finally arrived.

If so, how many more suicides by hanging (or otherwise) are imminent for China’s commodity, and financial, sectors. One thing we know is that courtesy of $36 trillion in Chinese bank “assets”, amounting a whopping 367% of GDP…

…. the short answer is “a lot.”

end

It sure looks like China is preparing for massive layoffs. However they do not want social unrest, so they warn officials that their jobs are on the line with citizens protest:

(courtesy zero hedge)

China Warns Officials: Allow Social Unrest, Lose Your Job

To be sure, there are always going to be financial and geopolitical landmines and every once in awhile we – and by “we” we’re referring to the market, or the country, or humanity, or whatever collective you want to choose – are going to step on one on the way to ushering in a black swan event.

But when we look out across markets and across the political landscape it’s difficult to escape the feeling that there are more black swans waiting in the wings – so to speak – than usual. There’s the threat of a dirty bomb being detonated in a crowded Western European urban center for instance. Or the chance that Turkey ends up “accidentally” killing a Russian or Iranian soldier while shelling the Azaz corridor. And how about the possibility that China tries to save its economy by chancing a 30% devaluation of the yuan and inadvertently plunges the world into a crisis far worse than 2008?

The interesting thing to note about the third crisis event listed above is that an economic implosion in China may spawn a black swan far larger than that which would emanate from a crisis in the country’s banking sector and/or a deeper devaluation of the RMB.

As we’ve discussed on multiple occasions of late, China desperately needs to purge its economy of excess capacity. The industrial sector is weighed down by too much debt and too little demand, but an acute overcapacity problem prevents the market from getting anywhere close to clearing. Either Beijing moves quickly to ameliorate this, or else a wave of defaults will ripple through the industrial complex on the way to crippling the country’s banking sector, where NPLs are probably at least five times greater than the official numbers suggest.

The big question is this: how will China manage to restructure or otherwise wind down insolvent SOEs without triggering a wave of layoffs that will leave millions of Chinese jobless, destitute, and, most importantly, furious? In other words, the biggest black swan of them all – with the possible exception of terrorists detonating an actual nuclear weapon – may be a coup in China stemming from the sweeping layoffs the country must implement to restore the industrial sector to some semblance of solvency.

Indeed we’re already hearing the rumblings of social unrest. Thousands of miners in China’s coal-rich (or poor depending on one’s perspective) north have gone on strike over months of unpaid wages and fears that government calls to restructure their state-owned employer will lead to mass layoffs. Earlier this month, protesters marched through the streets of Shuangyashan city in Heilongjiang province, venting their frustration at Longmay Mining Holding Group, the biggest coal firm in northeast China.

Subsequently, in the country’s southwest, eight construction workers tied to a protest held in Langzhong last August were subjected to a 1950’s-style public sentencing. Their crime: protesting unpaid wages. Their charge: obstructing official business. The verdict: guilty.

“Don’t take the public for fools,” one citizen wrote on Chinese social media. “You think the people don’t understand your purpose in using public sentencing?”

Just to be clear the “purpose” is this: discouraging protests which the politburo rightly views as the precursor to social unrest.

Just this week, “the Communist Party’s Central Committee and the State Council, China’s cabinet, warned party and state officials that they will lose their jobs if they fail to control public unrest,” WSJ writes. And while “that’s not altogether surprising [as it is] on one level, just a restatement of longstanding practice, [it] marks the first time authorities have come up with a definitive public statement explicitly warning party and state officials ‘at all levels’ that their jobs are on the line.’”

The warning from the politburo is likely tied directly to the abovementioned protests in what The Journal describes as the “gritty” streets of Shuangyashan. “Government officials are likely worried that the Shuangyashan incident and others could inflict a political cost on the leadership by highlighting issues such as the deficit of labor rights in China,” WSJ continues, before delivering the following summary of everything outlined above:

Party chiefs face a difficult task. Over the next five years, they need to shut down millions of tons of industrial capacity that’s making China’s economy inefficient. This means downsizing scores of steel, coal and other large industries that currently employ hundreds of thousands of workers. They have promised to do this without large-scale layoffs. Those displaced, Mr. Li said, would be given new jobs or government assistance.

These promises now hang in the balance.

Yes they do, and as we outlined a week ago, reassigning steelworkers and miners to lower paying jobs in sanitation, logging, and other industries may keep the official unemployment rate subdued, but it will do very little to appease workers who are forced to take a 60% pay cut. Strikes, The Journal goes on to note citing China Labour Bulletin, have risen by 200% from July 2015 to January of this year. Click the image below for an interactive map.

Needless to say, we’re highly skeptical that Beijing will be able to avert widespread protests. The question is whether those protests coalesce into an organized, political movement or whether the frustration simply manifests itself in disparate, ad hoc demonstrations against specific SOEs and/or local governments.

Of course manifestos like that which appeared on March 4 on Wujie News may help to galvanize public opinion and focus frustrations on the central government. On that note we’ll close with what we said earlier this month: “The Party had better figure something out quick. Because while you can make an example out of a handful of construction workers, and while you can “disappear” dissident journalists, the only thing you can do when millions of furious Chinese descend on Zhongnanhai is start shooting.”

* * *

end

Sunday night/Monday morning

Early this morning, we get a report from New York based China Beige Book International, a corporation which tries to give an honest assessment of what is going on in China. It revealed a huge plunge in the unemployment rate to a 4 yr low as China desperately tries to adjust from a smoke-stack export model to a domestic consumption model. Their problem is that they will have million of people unemployed and if China cannot get these people relocated, there will be massive, social unrest:

(courtesy zero hedge)

China Beige Book Reveals Employment Plunges To 4-Year Low, Capex Worst In History

Back in December, New York-based China Beige Book International released what they called a “disturbing” set of data that pointed to pronounced weakness in the Chinese economy.

“National sales revenue, volumes, output, prices, profits, hiring, borrowing, and capital expenditure were all weaker than the prior three months,” the firm – whose CBB is modeled on the Fed’s survey of US economic conditions and is supposed to provide a more objective assessment of China’s economic health than the goalseeked figures that emanate from the NBS – remarked.

In the three months since the CBB’s last report, we haven’t seen a whole lot in the way of positive data that would have caused us to believe that things are looking up. Exports, for instance, cratered more than 20% in RMB terms last month and 25% in USD terms – the third worst performance in history.

Sure enough, the CBB’s latest quarterly read on the Chinese economy betrays more pervasive problems including a persistent lack of hiring and a disheartening dearth of capex. “Only 33% of firms reported capital expenditure growth in the first quarter, the lowest in the survey’s five-year history,” Reuters reports, adding that “the share of firms reporting capex growth has fallen by over 40 percent since the second quarter of 2014.”

The CBB’s survey, which includes 2,200 companies and 160 bankers, showed that although profits have risen, hiring has collapsed to a four-year low and that poses a very real problem for the Party which is perpetually concerned with optics. “The weakness in the job market hits at a paramount concern for the Chinese Communist Party,” WSJ notes, before quoting CBB president Leland Miller, who said the following in the report:

“The party cares very much about the state of the labor market. The first quarter may therefore be one of the rare occasions when investors see the data and react mostly with relief, while the results cause some mild panic back in Beijing.”

“Our data show that firms first stopped borrowing, then cut spending and now are becoming allergic to hiring,” Miller continues.

Right. And if there’s anything the politburo does not need in the current environment, it’s for firms to develop a hiring “allergy.”

As we’ve documented exhaustively of late, China is staring down what may end up being a catastrophic employment crisis as the government must choose between allowing an acute industrial overcapacity problem to sink the entire economy or else move to implement a massive restructuring of elephantine SOEs.

Reforming grossly inefficient government enterprises will likely cost hundreds of thousands if not millions of jobs and if Beijing can’t manage to mitigate the situation by reassigning workers or otherwise providing some manner of social safety net, they’ll be widespread social unrest.

Of course besides the whole “popular revolt”/ “angry coup” issue, mass layoffs also do not bode well for China’s nascent transition from a smokestack economy to an economic model that revolves around consumption and services. As we put it earlier this month, “if, as the PBoC says, China intends to depend on domestic consumption rather than exports to fuel growth, then someone had better get to explaining how exactly it is that hundreds of thousands of recently jobless factory workers are going to be able to power the hoped-for but still nascent transformation.”

On that note, we close with the following from WSJ’s take on the latest CBB survey:

The government’s bid to regear the economy toward consumption and services and away from manufacturing and investment is having mixed results, at least this quarter, the survey found. Revenue growth in services and in retail – especially furniture, appliances and clothing — slowed in the first quarter, while holding steady in manufacturing.

Mission accomplished?

Hugh Hendry is another extremely bright individual and we must always pay attention to what he says. He was invited for a conversation with another brilliant individual by the name of Raoul Pal, a close friend of Grant Williams (Hmmm fame). They have a paid webcast and their thoughts are always enlightening.

Today’s talk was about China. Strangely Hendry went against his host as stated that if China devalues by 20% (to 8 yuan/dollar)” the world is over, everything hits the wall”. He states that the USA dollar will rise to astronomical heights, causing scarcity of that currency together with a collapse of all commodity prices and in turn, a collapse in emerging markets with huge defaults on their sovereign bonds etc.He describes if that happens, China will be king of a MAD MAX world and who would want that? Hendry states that the only way out for China is for a stronger yuan, yet with a high Debt to GDP ratio of 350% he does not know how this is possible.

We now have two competing forces out there on China:

a) Kyle Bass who states that China must devalue

B) Huge Hendry who believes that China can muddle along at current yuan levels as the percentage of world trade has not been hurt at all, despite the lower amounts of world trade.

this is a must see.

(courtesy zero hedge)

Hugh Hendry: “If China Devalues By 20% The World Is Over, Everything Hits A Wall”

Once upon a time Hugh Hendry was one of the world’s most prominent financial skeptics, arguing with anyone who would listen that the status quo is doomed and that central planning will never work.

Most famously, back in 2010 during a BBC round table discussion with Jeffrey Sachs and Gillian Tett when discussing Europe’s crashing experiment with the single currency, he said that we should “purge this system of its rottenness. Let’s take on a recession. It’s going to be tough, people are gonna lose their jobs. They are going to lose their jobs anyway. We can spread this over 20 years, or we can get rid of it over 3 years” before concluding “I recommend you panic.”

Ultimately everyone did panic, which led to the single biggest episode of global QE and negative rates ever seen, resulting in ever louder speculation even among the most “serious” people that central bankers are now powerless.

But perhaps most notably, Hendry was one of the biggest China bears, certain that the country’s massive overcapacity, insolvency and bad debt problems will result in disaster (back then China only had about 200% debt/GDP, it has since risen to over 350%). His Chinese skepticism led to his fund generating a 40% profit by late 2011.

And then after a poor two year performance spell, Hendry had a historic burnout and threw in the towel on bearishness, infamously saying he can no longer “look at himself in the mirror“:

“I may be providing a public utility here, as the last bear to capitulate. You are well within your rights to say ‘sell’. The S&P 500 is up 30% over the past year: I wish I had thought this last year… Crashing is the least of my concerns. I can deal with that, but I cannot risk my reputation because we are in this virtuous loop where the market is trending.”

He proceeded to buy momentum stocks and 3D printer companies.

Fast forward to the present, when countless hedge funds – key among them Kyle Bass’ Hayman Capital and Mark Hart’s Corriente – have become China megabears, expecting the country’s financial collapse and trading it by shorting the Yuan expecting a massive Yuan devaluation.

It is here that Hugh Hendry has once again proven contrarian, even if it means agreeing with the dominant textbook meme of the day, namely that China can contain its economic hard landing, and in his most recent interview with RealVision’s Raoul Pal, he cautions against a Chinese devaluation saying that “tomorrow we wake up, I mean, I would jump out the hotel window if this was the scenario, but we wake up and China has devalued 20%. The world is over. The world is over.”

What makes this interview doubly ironic is not just that Hendry is wildly contradicting everything he himself believed in a few short years ago, but disagrees with his interview host himself – recall that one month ago, we showed an excerpt from a Raoul Pal interview in which he previewed “the Big Reset” and laid out how the Kondratieff Winter would unwind, one in which China would play a prominent part.

Whether Hendry is right or wrong remains to be seen: for now he has the powerful People’s Bank of China at his back which has been especially active recently especially after the PBOC stated recently it intends to crush all hedge funds who have shorted the Yuan even if it means slamming Chinese trade and the economy once again (as a reminder, one of the biggest reasons why China needs a weaker Yuan is not just the stronger dollar to which it is pegged but because its exports have been crashing against all of its trading partners making the need for a weak currency paramount).

For now, as we showed just ten days ago, those short the Yuan have swung from wildly profitable to losing money as both the USD has slid and the Yuan has spiked, although both of these trades appear to be reversing now.

Needless to say, Hendry disagrees with the China contrarians and believes that the way to fix the Chinese economy is through a stronger currency, even if there is no logical way how that could possibly work when China’s debt load is 350% of GDP while its NPLs are over 10% and rising.

So, borrowing from a favorite Keynesian trope, one where the counterfactual to his prevailing – if incorrect – view of the world finally emerges, Hendry is convinced that a 20% devaluation would lead to global devastation; the same way if Paulson did not get Congress to sign off on his three page term sheet that would lead to the “apocalypse.” Only unlike Paulson who only hinted at a Mad Max world, for Hendry the alternative to him being right is a very explicit doomsday scenario, as he explains in the following excerpt from his RealVision interview:

Tomorrow we wake up and China has devalued 20%, the world is over. The world is over. Euro breaks up. The world is over. The euro breaks up. Everything hits a wall. There’s no euro in that scenario. The US economy, I mean everything hits a wall! Everything hits a wall!

The dollar strength that you imagined is devastation because you just eliminated dollars. They’re a scarce commodity. You’ve wiped them out. And China is a pariah state.

It’s a ‘Mad Max’ movie, right. OK, China gets to be the king in ‘Mad Max’ world. How appealing is that? There is no world after the tomorrow where China devalues by 20%. There is no world. Yeah, it’s looney tunes to believe that, people say, ‘oh wow, they needed to catch a break.’

Their share of world trade has never been higher. They’re facing no pressure, immense terms of trade improvement, and you would destroy world trade. World trade is down 25%. You would probably have passport restrictions, the world is over.

And while it is clear on which side of the Yuan Hugh is currently positioned (Hendry’s Eclectica is down 2.1% through March 18 and -5.9% YTD) either directly or synthetically, we can’t wait to see who is right in the end: China and its central bank (as well as Hugh Hendry) or reason and common sense (as well as some of the smartest hedge funds in the world).

The RealVisionTV interview excerpt is below:

To view the full interview, subscribe to Real Vision Television, which offers Zero Hedge readers a 7-day free trial.

EUROPEAN AFFAIRS

SCARY!! Belgian nuclear guard murdered Thursday night and had his access badge stolen.

(COURTESY ZERO HEDGE)

“Dirty Bomb” Fears Rise After Belgian Nuclear Guard Murdered, Access Badge Stolen

Hours after brothers Khalid and Ibrahim El-Bakraoui and two other men (one of whom may or may not have been bombmaker Najim Laachraoui) detonated explosives-laden vests and luggage at the Brussels airport and metro murdering nearly two dozen people and wounding scores more, we were alarmed but not entirely surprised to see Belgium evacuate the Tihange nuclear power plant.

We say we weren’t entirely surprised because way back on November 30, a raid on an Auvelais home rented by Mohamed Bakkali – who was arrested four days earlier and may have used the residence to shelter the Paris attackers including the supposed leader of the Brussels cell Abdelhamid Abaaoud – turned up an hours-long (some reports had suggested it was a mere 10 minutes long, an apparently incorrect assessment) surveillance tape that appeared to show a top Belgian nuclear official (see here).

“A small video camera stashed in a row of bushes silently recorded the comings and goings of the family of a Brussels-area man with an important scientific pedigree last year, producing a detailed chronology of the family’s movements,” Foreign Policy wrote, late last month. “At one point, two men came under cover of darkness to retrieve the camera, before driving away with their headlamps off, a separate surveillance camera in the area revealed later.”

If, as some suspect, those two men were the Bakraoui brothers, it would suggest that the Brussels cell which is now well on its way to going down in jihadist lore as the most “successful” sleeper cell in the history of radical Islam, was in the advanced stages of trying to procure the materials needed to build a dirty bomb.

Belgian lawmakers were beside themselves when they learned of the video, as it was apparently kept secret for months. “Your services possessed this videotape since Nov. 30, and the nuclear control agency was informed immediately,” said Jean-Marc Nollet, a Parliament member from Ecolo, told interior minister, Jan Jambon. “So I don’t understand how you could have been in possession of this video since Nov. 30, but on Jan. 13, when I questioned you on this, you answered, ‘There is no specific threat to the nuclear facilities.’”

We don’t really understand that either, but we imagine Belgian authorities will be discussing the issue quite a bit in the weeks and months ahead because it’s now emerged that on Thursday, Didier Prospero was shot and killed while walking his dog in Charleroi (about an hour drive from Brussels). Why should you care about Didier? Well, because he is (or “was”) a security guard at Tihange. His security pass was stolen as he lay dying.

“The murder was completely ignored and was committed on Thursday night in the judicial district of Charleroi,” Derniere Heure reported. “A security guard, accompanied by his dog, was shot in the early evening. His badge was stolen.”

![]()

The badge itself was immediately deactivated. It’s as yet unclear whether this is connected to Belgian jihadists, but it would certainly be difficult to write it off as a coincidence. Well, it would be difficult to write it off as a coincidence unless you are a Belgian prosecutor. In that case it would be easy. “”A terrorist track is not considered in the case,” the Charleroi prosecutor’s office told TASS on Saturday.

Meanwhile, the mainstream media is beginning to sound the alarm bells on the threat to Belgium’s nuclear infrastructure. Here, for instance, is The New York Times:

The investigation into this week’s deadly attacks in Brussels has prompted worries that the Islamic State is seeking to attack, infiltrate or sabotage nuclear installations or obtain nuclear or radioactive material. This is especially worrying in a country with a history of security lapses at its nuclear facilities, a weak intelligence apparatus and a deeply rooted terrorist network.

On Friday, the authorities stripped security badges from several workers at one of two plants where all nonessential employees had been sent home hours after the attacks at the Brussels airport and one of the city’s busiest subway stations three days earlier. Video footage of a top official at another Belgian nuclear facility was discovered last year in the apartment of a suspected militant linked to the extremists who unleashed the horror in Paris in November.

Asked on Thursday at a London think tank whether there was a danger of the Islamic State’s obtaining a nuclear weapon, the British defense secretary, Michael Fallon, said that “was a new and emerging threat.”

While the prospect that terrorists can obtain enough highly enriched uranium and then turn it into a nuclear fission bomb seems far-fetched to many experts, they say the fabrication of some kind of dirty bomb from radioactive waste or byproducts is more conceivable. There are a variety of other risks involving Belgium’s facilities, including that terrorists somehow shut down the privately operated plants, which provide nearly half of Belgium’s power.