Gold: $1,226.90 down $8.90 (comex closing time)

Silver 15.21 down 9 cents

In the access market 5:15 pm

Gold $1224.50

silver: 15.23

Yesterday, I promised you that the bankers would attack today in both gold and silver. My boys did not disappoint me with their antics.

Let us have a look at the data for today.

At the gold comex today, we had a good delivery day, registering 20 notices for 2000 ounces and for silver we had 9 notices for 45,000 oz for the active March delivery month.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 213.04 tonnes for a loss of 90 tonnes over that period.

In silver, the open interest ROSE by 3373 contracts UP to 175,245 as the silver price was up 4 cents with respect to yesterday’s trading . In ounces, the OI is still represented by .876 billion oz or 125% of annual global silver production (ex Russia ex China).

In silver we had 9 notices served upon for 45,000 oz.

In gold, the total comex gold OI fell slightly by 2195 contracts to 480,441 contracts as the price of gold was UP $15.70 with yesterday’s trading.(at comex closing) which should have caused the OI to rise. However, we also are entering the new active month of April and that usually causes an obliteration of OI. The two cancelled each other out and we had a net loss of 2195 contracts.

We had a no changes in the GLD/ thus the inventory rests tonight at 820.47 tonnes. No doubt that will change tomorrow considering Yellen’s dovish comments today with regards to the raising of rates. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,we had no changes in inventory tonight and thus the Inventory rests at 330.389 million oz.

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver rose by 3373 contracts up to 175,245 as the price of silver was up 4 cents with yesterday’s trading.Investors flocked into silver on the dovish Yellen speech where she indicated that she is reticent to raise rates. The total OI for gold fell by 2,195 contracts to 480,441 contracts as gold was up $15.70 in price from yesterday’s level and we are now entering a new active delivery month.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

off today

2b COT report/

(Harvey)

2c) FRBNY

Harvey

3. ASIAN AFFAIRS

i)Late TUESDAY night/ WEDNESDAY morning: Shanghai closed UP BY 80.81 POINTS OR 2.77% , / Hang Sang closed UP 437.09 POINTS OR 2.15% / The Nikkei closed DOWN 224.57 POINTS OR 1.31% . Australia’s all ordinaires was CLOSED UP 0.11%. Chinese yuan (ONSHORE) closed UP at 6.4774. Oil ROSE to 38.99 dollars per barrel for WTI and 39.66 for Brent. Stocks in Europe ALL IN THE GREEN . Offshore yuan trades 6.4808 yuan to the dollar vs 6.4774 for onshore yuan. Japanese INDUSTRIAL PRODUCTION plunges the most in almost 5 years as negative interest rates ARE KILLING BUSINESS. (see below)

.

REPORT ON JAPAN

Industrial production collapses by the most in 5 yrs

(zero hedge)

REPORT ON CHINA

POBC responds to Yellen by raising yuan value

(Harvey)

EUROPEAN AFFAIRS

GLOBAL ISSUES

Amazing, 1/3 of all sales in Vancouver, Canada came from wealthy Chinese who are desperate to take their yuan and buy assets like homes and gold. It did not help Alberta as their housing market is dead as can be:

( zero hedge)

OIL MARKETS

i)Oil pops in price as USA production tumbles to 16 month lows:

( zero hedge)

PHYSICAL MARKETS

i)My goodness these guys are good. They can buy 846 tonnes of silver (27.1 million oz) in March so far without causing the price to rise.

( zero hedge)

ii)A must read…James Turk describes the gold options manipulation from Europe and the manipulation is even worse than in the uSA

( James turk/Kingworldnews)

iii)Quite a good article. Rickards states that as the world continues to advance the theory and use negative interest rates, the more gold will be used. Why? gold does not pay out an interest rate. Rickards states that the Swiss refiners are working 24/7 at great speed to produce kilobars

( James Rickards/GATA)

iv)Very unusual that Chris Powell was granted an interview to talk about gold manipulation on a Toronto radio station

(Chris Powell/GATA/CFMJ ratio station)

v)Strange!!: we now hear that Germany wants 1/2 of its gold back by 2020. For the past 3 months they got zero from the FRBNY.

We wish Germany all the luck in the world:

( Lawrie on Gold/Lawrie Williams/Sharp’s Pixley)

vi)Steve St Angelo compares the purchases of gold eagles vs silver eagles over a 30 yr period and also compares sales of gold/silver eagles vs inventory held at SLV/GLD

( Steve St Angelo/SRSRocco report)

USA STORIES WHICH WILL INFLUENCE THE PRICE OF GOLD/SILVER

i)Rail traffic volumes tumble greatly as coal is being stockpiled at an alarming and record rate. The USA economy is faltering!

( zero hedge)

ii)Boeing will terminate 4500 jobs this year. So much for the uSA recovery. Any the USA is creating jobs??

Let us head over to the comex:

The total gold comex open interest fell to 480,441 for a loss of 2195 contracts despite the fact that the price of gold was up $15.70 in price with respect to yesterday’s trading as we are now entering the active delivery month of April. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month or for that matter an inactive month, and 2) a continual drop in the amount of gold standing in an active month. Today, the OI fell but not nearly as much due to the dovish Yellen speech of yesterday. The front March contract month is now off the board. After March, the active delivery month of April saw it’s OI fall by 57,994 contracts down to 29,571 which is extremely high for one day to go. The next non active contract month of May saw its OI rise by 349 contracts up to 2585. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was good at 250,358. However we had considerable rollovers.. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day was excellent at 401,093 contracts. The comex is not in backwardation. First day notice is tomorrow, March 31. The options for the comex was over on Tuesday. However we still have LBMA options and OTC options which expire March 31.2016.

Today we had 20 notices filed for 2000 oz in gold.

March contract month:

FINAL standings for MARCH

March 30/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 128.60 oz

Brinks,Manfra |

| Deposits to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 9596.45 oz

Brinks,Delaware

|

| No of oz served (contracts) today | 20 contracts (2,000 oz) |

| No of oz to be served (notices) | nil oz/

off the board |

| Total monthly oz gold served (contracts) so far this month | 743 contracts (74,300 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 192,421.9 oz |

Today we had 0 dealer deposits

Total dealer deposits; nil oz

Today we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

Today we had 2 customer deposits: AND ANOTHER DOOZY

i) Into brinks: 9500.00000 oz (not divisible by 32.15 and therefore no kilobars!! how is this possible???????)

ii) Into Delaware; 96.45 oz

total customer deposits: 9596.45 oz oz

Today we had 2 customer withdrawals:

i) Out of Brinks: 32.15 oz (1 kilobar)

ii) Out of Manfra: 96.45 oz

total customer withdrawals; 128.60 oz

Today we had 0 adjustment:

MARCH FINAL standings

/March 30/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 16,011.16 OZ. BRINKS,CNT, |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 47,112.75 oz

brinks |

| No of oz served today (contracts) | 9 contracts

45,000 oz |

| No of oz to be served (notices) | off the board) |

| Total monthly oz silver served (contracts) | 1355 contracts (6,775,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 11,215,705.4 oz |

today we had 0 deposits into the dealer account

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 1 customer deposits

i) Into Brinks: 47,112.75 oz

total customer deposits: 47,112.75 oz

We had 2 customer withdrawals:

i) Out of Brinks:

8032.810 oz

ii) Out of CNT: 7978.35 oz

:

total customer withdrawals: 16,011.16 oz

we had 0 adjustments

And now the Gold inventory at the GLD

MARCH 30/no changes in inventory/inventory rests tonight at 820,47 tonnes

March 29/a withdrawal of 3.27 tonnes of gold from the GLD/Inventory rests at 820.47 tonnes. (No doubt we will see a rise in gold inventory with tomorrow’s reading)

March 28/no change in inventory at the GLD/Inventory rests at 823.74 tonnes

March 24.2016: a deposit of 2.08 tonnes of gold into its inventory/and this after a big drubbing these past two days??/Inventory rests at 823.74 tones

March 23/no changes at the GLD today despite the gold drubbing. Inventory rests at 821.66 tonnes

March 22./no changes in inventory at the GLD/Inventory rests at 821.66 tonnes

MARCH 21/another big deposit of 2.68 tonnes/inventory rests tonight at 821.66 tonnes

(and this was done with gold down $10.00 today!!)

March 18.I GIVE UP!! WITH GOLD DOWN TODAY, THE CROOKS OVER AT GLD ADDED ANOTHER IDENTICAL 11.89 TONNES OF PAPER GOLD INTO THEIR INVENTORY.

INVENTORY RESTS THIS WEEKEND AT 818.98 TONNES. IF I WAS A SHAREHOLDER OF THIS ENTITY I WOULD BE VERY WORRIED.

March 17/we had a whopper of a deposit tonight: 11.89 tonnes/with London in backwardation this is nothing but a paper addition/inventory rests tonight at 807.09 tonnes

March 16.2016:/we had a deposit of 2.09 + 2.97(last in the evening) tonnes of gold into the GLD/Inventory rests at 795.20 tonnes

March 15/ no changes in gold inventory at the GLD/Inventory rests at 790.14 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

March 30.2016: inventory rests at 820.47 tonnes

end

And now your overnight trading in gold, WEDNESDAY MORNING and also physical stories that may interest you:

By Mark O’Byrne

World’s Largest Asset Manager Likes “Inflation Linked Bonds and Gold As Diversifiers”

BlackRock Inc. have joined Pacific Investment Management Co. (PIMCO) in recommending inflation linked bonds and gold, warning costs are poised to pick up and there is a growing risk of inflation.

“We like inflation-linked bonds and gold as diversifiers” said New York-based BlackRock which is the world’s largest asset manager, managing $4.6 trillion, reported Bloomberg.

![]()

“Stabilizing oil prices and a tighter labor market could contribute to rising actual, and expected, U.S. inflation,” Richard Turnill, BlackRock’s global chief investment strategist, wrote Monday on the company’s website.

“If you look at inflation expectations as they are reflected in the bond market we think they are too low,” Joachim Fels, global economic adviser for Pimco said in an interview on Bloomberg Television. “We still think markets are pricing in too low a profile for inflation. We don’t think inflation will move significantly above central bank’s targets, but we think that there’s a good chance that over the next 12 months or so, particularly in the U.S., that we will get back to 2 percent.”

“We like Treasury Inflation Protected Securities,” Pimco’s Worah said in a video on the company’s website this month. “The market is pricing 1 percent inflation in the U.S. for next year. We think it’s likely to be closer to 2 percent.”

“We may well at present be seeing the first stirrings of an increase in the inflation rate — something that we would like to happen,” Stanley Fischer, vice chairman of the Fed Board of Governors, said this month.

PIMCO already recommend owning gold as part of diversified portfolios. In 2013 they introduced a ‘Multi Real Asset Strategy’ specifically created to tackle “inflation risk”.

“The strategy tactically invests in multiple inflation-sensitive asset classes, allocating across a broad opportunity set of real assets, including global inflation-linked bonds, commodities, real estate, currencies and gold … Gold has characteristics of both a commodity that is easily stored for a long period of time and a currency whose supply is limited.”

Gold Prices (LBMA)

30 Mar: USD 1,238.20, EUR 1,094.12 and GBP 860.23 per ounce

29 Mar: USD 1,216.45, EUR 1,087.71 and GBP 853.04 per ounce

24 Mar: USD 1,216.45, EUR 1,088.75 and GBP 861.89 per ounce

23 Mar: USD 1,232.20, EUR 1,101.76 and GBP 870.03 per ounce

22 Mar: USD 1,251.80, EUR 1,117.35 and GBP 876.96 per ounce

Silver Prices (LBMA)

30 Mar: USD , EUR and GBP per ounce (Released at 1200 GMT)

29 Mar: USD 15.06, EUR 13.44 and GBP 10.56 per ounce

24 Mar: USD 15.28, EUR 13.70 and GBP 10.82 per ounce

23 Mar: USD 15.58, EUR 13.92 and GBP 10.99 per ounce

22 Mar: USD 15.89, EUR 14.16 and GBP 11.12 per ounce

Gold News and Commentary

Gold Bulls Cheer Yellen Caution With More `Easy Money’ Predicted (Bloomberg)

Dovish Yellen, softer dollar support gold near $1,240 (Reuters)

Spot gold jumps after Fed signals cautiousness (Reuters)

Russia becomes world’s top gold buyer (Russia Today)

Russia Adds $6 Billion to Its Gold Reserves in a Week (Sputnik News)

Rickards: Why Gold Is Going To $10,000 (Hedgeye)

HSBC: Gold is a highly regarded asset – Audio (Bloomberg)

Ed Butowsky: Calculating The True Cost of Living (Peak Prosperity via Youtube)

Buying gold in 2016 is like buying stocks in 1941 (Marketwatch)

Pensions Timebomb – Europe’s Predicament (WSJ)

Read More Here

‘7 Real Risks To Your Gold Ownership’ – Must Read Gold Guide Here

Please share our website with friends, family and colleagues who you think may benefit from it.

Thank you

END

My goodness these guys are good. They can buy 846 tonnes of silver (27.1 million oz) in March so far without causing the price to rise.

(courtesy zero hedge)

Silver Bulls Are Buying-The-Dip As ETFs Gain Most Since 2013

The recent weakness in Silver has done nothing to dissuade precious metal ‘hoarders’ from buying-the-dip.Silver ETF holdings rose 846 metric tons in March (so far) – the biggest jump since August 2013 – to the highest since April 2015.

And all of this buying has occurred as prices dropped to one-month lows, as it seems – like China and Russia – taking advantage of lower precious metal prices amid the collapse of central bank credibility around the world.

Continued fund buying shows longer-term investors haven’t been put off by recent price declines, said Ole Hansen, head of commodity strategy at Copenhagen-based Saxo Bank A/S.

However, we do note that commercial hedgers are the most-hedged in 10 years…

Charts: Bloomberg

end

A must read…James Turk describes the gold options manipulation from Europe and the manipulation is even worse than in the uSA

(courtesy James turk/Kingworldnews)

Gold options manipulation is even worse in Europe, Turk tells KWN

Submitted by cpowell on Wed, 2016-03-30 07:19. Section: Daily Dispatches

2:19p ICT Wednesday, March 30, 2016

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk, interviewed by King World News, discusses the manipulation of gold prices around futures option expiration dates, manipulation that is even more obvious in Europe than in the United States. Turk’s interview is excerpted at KWN here:

http://kingworldnews.com/james-turk-says-todays-gold-rally-is-definitely…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Quite a good article. Rickards states that as the world continues to advance the theory and use negative interest rates, the more gold will be used. Why? gold does not pay out an interest rate. Rickards states that the Swiss refiners are working 24/7 at great speed to produce kilobars

(courtesy James Rickards/GATA)

As interest rates turn negative, gold becomes the high-yield asset, Rickards says

Submitted by cpowell on Wed, 2016-03-30 09:01. Section: Daily Dispatches

3:58p ICT Wednesday, March 30, 2016

Dear Friend of GATA and Gold:

Wall Street for Main Street’s Jason Burack gets some interesting observations out of financial writer and geopolitical strategist James G. Rickards in an interview posted this week. Among other things, Rickards remarks:

— As interest rates increasingly become negative, gold becomes the high-yield asset even as it may pay no interest at all.

— Governments can’t reliably dump U.S. government debt instruments to protect themselves against dollar devaluation, since the president can freeze any threatening financial transaction, none more easily than government bond transactions. But governments can hedge their dollar exposure by buying gold, and many indeed are doing so.

— A major Swiss gold refinery can’t keep up with orders, especially from China.

— China’s government wants a lower gold price at the moment because the government is still pursuing acquiring at least another 3,000 tonnes, so the Shanghai Gold Exchange is not likely to be permitted to boost the gold price for a while.

— The gold price “has been manipulated for over a hundred years” by governments, but investors should buy the monetary metal anyway because “all the manipulations ultimately fail.” But do the manipulations necessarily fail within the lifespans of all gold investors? Burack didn’t ask and Rickards didn’t say.

The interview is 38 minutes long and can be heard at YouTube here:

https://www.youtube.com/watch?v=Kdd_-w0-_Xc&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Very unusual that Chris Powell was granted an interview to talk about gold manipulation on a Toronto radio station

(Chris Powell/GATA/CFMJ ratio station)

50,000-watt Toronto radio station airs interview with GATA secretary

Submitted by cpowell on Wed, 2016-03-30 09:31. Section: Daily Dispatches

4:28p ICT Wednesday, March 30, 2016

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed March 19 on “The Real Money Show” broadcast on Toronto radio station CFMJ-AM640, discussing the extensive documentation of gold market manipulation by governments and central banks. CFMJ is a 50,000-watt station, the strongest signal allowed in North American radio, and it was unusual for GATA to be offered that much of a broadcast audience, the mainstream news media in Canada being just as determined as the mainstream news media in the United States to avoid the issue of market rigging by government.

The interview was conducted by Darren Long of Guildhall Wealth Management, is 45 minutes long, and begins at the 7:50 mark at the show’s Internet site here:

http://therealmoneyshow.com/guildhall-wealth-management-inc-interviews-c…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Strange!!: we now hear that Germany wants 1/2 of its gold back by 2020. For the past 3 months they got zero from the FRBNY.

We wish Germany all the luck in the world:

(courtesy Lawrie on Gold/Lawrie Williams/Sharp’s Pixley)

German Gold Reserve Repatriation, Gold ETF Accumulation, Bulls and Bears

The latest Strengths, Weaknesses, Opportunities and Threats (SWOT) analysis for last week from Frank Holmes – CEO and Chief Investment Officer for U.S. GlobalInvestors

Strengths

- The best performing precious metal for the week was platinum, however still down -2.35 percent. Price action was driven by increased auto demand in the European Union, reports Market Realist, which rose 14 percent in February. Platinum and palladium is used in the production of catalytic converters.

- Germany announced this week that it wants half of its gold reserves back by the year 2020, reports Bloomberg. Bundesbank, the country’s central bank (which has gold in London and New York), has repatriated 1,400 metric tons, or 41.5 percent, of Germany’s gold reserves to Frankfurt.

- Even though gold prices haven’t done much this month, investors are still pouring cash into gold exchange-traded funds, reports Bloomberg. Gold ETF assets continue to increase, with holdings currently near a two-year high.

Weaknesses

- The worst performing precious metal for the week was silver, down -3.96 percent. The precious metal plunged on Wednesday, and remains low today, mainly driven by a stronger U.S. dollar.

- The U.S. dollar gained this week against all major peers, causing gold traders and analysts to turn bearish for the third time in four weeks, according to Bloomberg. The dollar was boosted on prospects for higher U.S. interest rates, in turn cutting the precious metal’s appeal as an alternative investment. This week gold headed for its biggest weekly slump since November.

- As seen in the chart below, Bloomberg reports that the gold momentum gauge is flashing a bearish sign as the metal’s rally has started to fizzle. Head of metals research for Societe Generale, Robin Bhar, told Kitco News that the recent gold price rally looks unsustainable. Bhar cited financial turmoil and expectations that the U.S. and global economies will fall into recession have been the factors behind the move, reports Kitco, although these appear to be extreme scenarios.

Opportunities

Opportunities

- A prominent forecaster from JPMorgan Chase believes investors are better off betting on gold, explaining that the market’s rally is in trouble. An article on CNBC clarifies Marco Kolanovic’s view that the popular trade of being long momentum stocks against a short position on S&P 500 is being unwound. Kolanovic is widely followed by the hedge fund industry and concludes the rally in the broader market has been driven by short covering of bets that the market would fall, thus if stocks reverse, gold should be a beneficiary of the shift.

- Reuters reports that the 19-day strike by Indian jewelers finally came to an end on Saturday, after government assured they will not be “harassed” by the excise department in collecting a new tax. The jewelers went on strike at the beginning of March following the reintroduction of a 1 percent excise duty on gold jewelry after four years.

- Klondex Mines reported fourth quarter and year-end results after market close on Thursday. The results were positive with costs coming in better than expectations and free cash flow higher than forecast. Klondex forecasts a 16 percent increase in production for 2016, while most companies are flat-to-negative on growth. Cash balances increased 30 percent for the year. We expect further positive developments as we see 2016 progress.

Threats

- A wholly-owned subsidiary of Kinross Gold Corp., Compania Minera Maricunga (CMM), was notified by Chile’s environmental regulatory authority of a resolution starting a legal process, according to a news release on March 21. The resolution will seek to require CMM to close the Maricunga mine’s water pumping wells located in the Pantanillo area of Region III due to drought. Kinross responded stating it is committed to responsible environmental management.

- James Bullard, president of the Federal Reserve Bank of St. Louis, told policy makers this week that they should consider raising interest rates at their next meeting, reports Bloomberg, which would help boost the greenback. Gold has fallen to its lowest in a month as the dollar advance saps up demand in addition to some policy makers saying that recent economic data justifies tighter monetary policy.

- Gold miners are letting the hedge grow, writes Peter Ker. The price of gold has neared record highs in Australian dollar terms, with the largest gold miner on the ASX deciding to embrace hedging. On Thursday, Newcrest Mining confirmed that a portion of the gold produced at the Telfer mine in Western Australia has been hedged until 2018. This could signify that miners don’t believe the high gold prices can last.

end

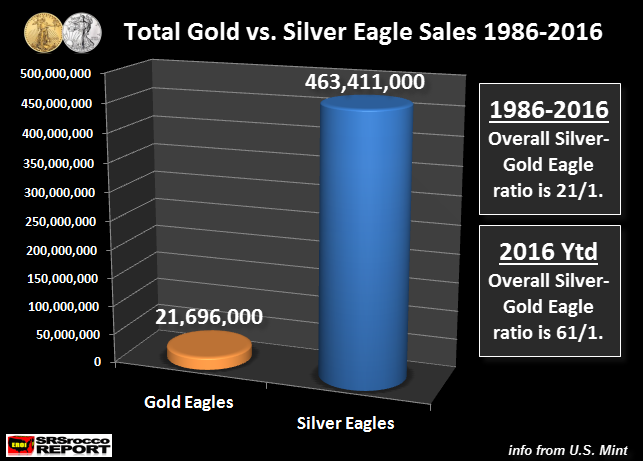

Steve St Angelo compares the purchases of gold eagles vs silver eagles over a 30 yr period and also compares sales of gold/silver eagles vs inventory held at SLV/GLD

Have fun with this:

(courtesy Steve St Angelo/SRSRocco report)

SILVER vs. GOLD: 2 Must See Charts

by SRSrocco on March 29, 2016

What is the better investment? Silver or Gold? Well, if we look at the following two charts below, we can spot some interesting trends. The U.S. Mint has been producing Gold and Silver Eagles for over thirty years now. Since 1986, the U.S. Mint has sold 21.7 million Gold Eagles versus 463.4 million Silver Eagles. The overall Silver-Gold Eagle Ratio from 1986- 2016 is 21.1:

However, if we look at the Gold Eagle sales of 252,500 oz versus Silver Eagles at 14,842,500 for 2016, the ratio is 61/1. Investors are currently buying Silver Eagles this year at three times the historic overall ratio. Furthermore, if we break down Gold versus Silver Eagle sales in the following two periods, we can see an interesting trend:

From 1986-2006, the U.S. Mint sold a total of 13.8 million Gold Eagles compared to 148.3 million Silver Eagles. This 21 year period that took place before the collapse of the U.S. Investment Banking and Housing Markets, shows that investors favored buying Gold Eagles more than Silver Eagles as the Silver-Gold ratio was only 11/1.

However, this changed after 2007, when investors bought a massive 315 million Silver Eagles versus 7.9 million Gold Eagles. During the 2007-2016 period, the Silver-Gold Eagle ratio jumped nearly four times to 40.1. In addition, total Gold Eagle sales were less in the second period, but Silver Eagle sales were more than double (148.3 million vs. 315 million).

Here is another interesting statistic. Let’s compare Gold and Silver Eagle sales versus the total inventories at the GLD and SLV ETF’s:

Gold & Silver Eagles vs. GLD & SLV ETF’s (million – Moz):

Total Gold Eagles = 21.7 Moz

Total GLD inventories = 26.5 Moz

Total Silver Eagles = 463. 4 Moz

Total SLV inventories = 330 Moz

What is interesting is that there are more Silver Eagles held in private hands (463.4 Moz) than the total inventories on the SLV ETF (330 Moz). On the other hand, there is more gold (supposedly) held at the GLD ETF (26.5 Moz) compared to the Gold Eagles held by the public (21.7 Moz).

Now, we have no idea if the GLD and SLV ETF’s have all the metal they say they do, but I would much rather own physical Gold and Silver Eagles than paper gold shares.

I believe silver will outperform gold significantly in percentage terms in the future. We can see that investors (large and small) must also agree as they are buying a lot more Silver Eagles than Gold Eagles since 2007.

NOTE: I will be releasing a new BULLET REPORT on the Gold Market this week. It provides charts and data on how the recent flows are setting up the Gold Market for a big move in the future.

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan up to 6.4774 / Shanghai bourse IN THE GREEN, UP 80.81 OR 2.77%/: / HANG SANG CLOSED up 437.09 or 2.15%

2 Nikkei closed down 224.57 or down 1.31% (POOR INDUSTRIAL PRODUCTION/POOR RETAIL SALES)

3. Europe stocks opened ALL in the green /USA dollar index down to 94.87/Euro up to 1.1326

3b Japan 10 year bond yield: FALLS TO -.087% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.27

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 38.90 and Brent: 39.62

3f Gold DOWN /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS to 0.127% German bunds in negative yields from 8 years out

Greece sees its 2 year rate FALL to 9.76%/:

3j Greek 10 year bond yield RISE to : 8.81% (YIELD CURVE NOW INVERTED)

3k Gold at $1236.50/silver $15.37 (7:15 am est)

3l USA vs Russian rouble; (Russian rouble UP 61/100 in roubles/dollar) 67.63

3m oil into the 38 dollar handle for WTI and 39 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9629 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0910 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN STARTS ITS CAMPAIGN AS TO WHETHER EXIT THE EU.

3r the 8 Year German bund now in negative territory with the 10 year FALLS to + .127%

/German 8 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.82% early this morning. Thirty year rate at 2.62% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

“Bad News Is Great Again” – Global Stocks Soar After Yellen Admits Global Economy Is Much Weaker

At the end of the day, it was all about the dollar.

Starting March 18, the Bloomberg Dollar Spot had risen as much as 1.9% as Fed officials including Lacker, Williams and Bullard noted upside risks on rate-hike projection and suggested a rate hike may be imminent as soon as April. And then Yellen unleashed the latest round of dovishness, when she made it very clear that the Fed is no longer just the U.S. central bank, but that of the world (but mostly China) and as such its prerogative is to not only keep stocks high, but to also assure there is no currency crisis in Beijing (where a month ago she met other G-20 central bankers to decide precisely this).

The result of Yellen’s much discussed speech, was an immediate plunge in the Dollar spot index of 1.2% to 8 month lows, its worst month in 5 years, a drop which has continued this morning, and is on par to equal the dollar’s tumble from the first week of March when Bill Dudley likewise came out very dovish, and when the index dropped 1.7% within a week.

What is notable about these two crying doves is that both have roundly ignored the simmering “mutiny” by the Fed’s hawks (remember Hilsenrath’s humorous “The Decline of Dissent at the Fed” last week) advice of central banker incubator Goldman Sachs, that it is in the US interest to push the dollar higher (it had a report just last week titled “Inflation Finally Begins to Firm”). It will be very interesting to see how this particular conflict is resolved.

For now, however, the die has been cast, and the result is a surge in risk assets around the globe: stocks jumped in Asia (except in Japan where the Yen strength pushed the Nikkei lower by 1.3%, however the Shanghai’s 2.3% jump just over 3000 should more than make up for that) and Europe, with US equity futures 0.6% higher at this moment. Commodities climbed as the dollar extended its worst month in more than five years.

The reason for this stock surge, as we noted last night, is absurdly delightful: Yellen signaled “weakening world growth” and “less confidence in the renormalization process.” In other words, the “bad news is good news” mantra is back front and center. As such, calls for a slow approach to tightening policy ignited gains for shares from Shanghai to Frankfurt after U.S. equities erased their losses for the year. Diminishing prospects for a first-half Fed rate increase sent the Bloomberg Dollar Spot Index toward the lowest since June and drove emerging-market currencies toward their best month since 1998. Credit markets rallied and U.S. oil gained for the first time in five days.

“We have seen European markets broadly head higher on Yellen’s dovish

note last night,” said Michael Hewson, the London-based market analyst

at CMC Markets Plc. “It’s the only factor driving them up today.”

Indeed, the worse the global economy gets from this point on, the better for risk assets, even if it means that the S&P’s GAAP P/E is north of 23x as of this morning.

As Bloomberg adds, futures show traders now see no chance of Yellen changing policy next month, a roughly 20% chance of a June hike as of this moment, and only a 54% likelihood of an increase by November after she dialed back some of the commentary made by other officials the past two weeks. The Fed chair emphasized during her appearance at the Economic Club of New York that the central bank remains wary of raising rates amid threats to American growth from a slowing global economy.

The MSCI All-Country World Index added 0.8 percent as of 10:29 a.m. London time for a fourth-straight advance. The Shanghai Composite Index gained 2.8 percent and Germany’s DAX Index added 1.6 percent. The Bloomberg Dollar Spot Index fell 0.2 percent.

Global Market Snapshot

- S&P 500 futures up 0.5% to 2057

- Stoxx 600 up 1.2% to 341

- FTSE 100 up 1.5% to 6199

- DAX up 1.5% to 10034

- German 10Yr yield down less than 1bp to 0.14%

- Italian 10Yr yield down 1bp to 1.23%

- Spanish 10Yr yield down less than 1bp to 1.44%

- MSCI Asia Pacific up 0.9% to 129

- Nikkei 225 down 1.3% to 16879

- Hang Seng up 2.1% to 20803

- Shanghai Composite up 2.8% to 3001

- S&P/ASX 200 up 0.1% to 5010

- US 10-yr yield up less than 1bp to 1.81%

- Dollar Index down 0.26% to 94.91

- WTI Crude futures up 1.7% to $38.94

- Brent Futures up 1.4% to $39.69

- Gold spot down 0.2% to $1,239

- Silver spot up 0.2% to $15.39

Top Global News

- Boeing to Trim 4,000 Jobs Amid Makeover of Commercial Jet Unit: part of a broader effort to reduce costs amid fierce competition from Airbus Group SE

- Amazon Assembly, Installation Services Bolster Big-Product Sales: retailer has put together an army of workers who can handle everything from mounting flat TVs on walls to assembling treadmills

- Exxon Climate Science Probe Expands as New York Gains Allies: Massachusetts joins New York in investigating Exxon Mobil

- Yellen Spurs Global Stock Rally as Dollar Tumbles for Second Day: Stocks jumped around the world after Yellen reasserted the central bank’s gradual approach to raising interest rates

- Earnings Optimism Drawing Short Seller Wrath in U.S. Equities: Short interest in ETF tracking industry highest in 20 months

Looking at regional markets, we start in Asia, where in the aftermath of yesterday’s dovish deluge stocks traded mostly positive as the region cheered Fed Chair Yellen’s dovish remarks, which had already underpinned the S&P 500 to its highest close YTD. However Nikkei 225 (-1.3%) underperformed, weighed by a stronger JPY and poor Industrial Production figures which declined the most since 2011, while Shanghai Comp (+2.8%) outperforms amid upbeat earnings results and prospects China’s pension fund could start investment in the nation’s stock markets this year. 10yr JGBs tracked T-notes higher following the aforementioned dovish Yellen and amid weakness in Japanese stocks, while the BoJ were also in the market for JPY 1.2trl of government debt.

Top Asian News

- China Said to Accelerate Financial Regulatory Overhaul Plans: Proposals for new system of oversight could come in summer

- China’s Large Banks Wary on Li Keqiang’s Plan for Bad Loans: Higher risk weights for equity stakes would weaken banks

- Fortunes Reverse for Hedge Funds That Won in Past Selloffs: Hao’s China hedge fund lost 6.1% after last year’s 149% gain

- Takata Said to Put Worst-Case Recall Costs at $24 Billion: Supplier said to peg total recall at 287.5m inflators

- Antibiotic Apocalypse Fear Stoked by India’s Drugged Chickens: Feeding chickens antibiotics may speed diseases costing $100t

In Europe, risk on sentiment dominated the price action this morning as dovish comments by Fed’s Yellen on Tuesday prompted market participants to reassess their expectations of further rate hikes by the Fed. Consequently, USD index remained under pressure for the much of the first half of the EU session. Looking elsewhere, despite the upside in stocks and supply related positioning, Bunds traded little changed, though prices moved off the best levels after it was reported that inflation in German states edged back into positive territory. Also of note, peripheral bond yield spreads continued to tighten, supported by large quarter-end negative supply in April.

Top European News

- Metro Plans to Split in Two in Move to Boost Company’s Value: Shares jump as much as 10% in Frankfurt on demerger plan. Split should take place by middle of next year, company says

- Swedbank Chairman Fails to Win Re-Election After CEO Scandal: development follows the dismissal earlier this year of Chief Executive Officer Michael Wolf

- Tata Steel Will Study Sale of Its U.K. Unit as Market Worsens: Producer says its holding talks with British government. Slump in global prices has forced it to consider selling its U.K. business

- Europe’s Bond Shortage Means Draghi Is About to Shock the Market: ECB’s monthly debt purchases rise by 20 billion euros in April. Ten-year bunds headed for biggest quarterly gain since 2011

In FX, the early European session continued to the North American sell off in the wake of Fed Chair Yellen’s speech in NY yesterday, where the level of dovish rhetoric took the market by surprise. All the majors saw significant moves against the greenback, and these have all been extended, after a relatively quiet Asian session which was largely consolidative. EUR/USD has now pushed up to 1.1333 while USD/JPY printed a 112.00 low to push the USD index down towards key mid-March support.

The commodity currencies have also made some gains, but giving back some of this more recently, with USD/CAD meeting strong demand at 1.3000. NZD/USD took out key resistance around .6900 to suggest some much stronger gains ahead, though AUD/USD through the recent .7680 highs has only generated modest momentum since, with .7700 still intact.

Bloomberg’s dollar index, which tracks the greenback against 10 major peers, has lost 3.7 percent in March, set for a second straight monthly drop and the biggest decline since September 2010. The U.S. currency slipped 0.3 percent to $1.1321 per euro and weakened 0.4 percent to 112.27 yen as it dropped against all of its major counterparts.

The Fed would act “cautiously” as it looks to raise rates against a backdrop of deteriorating global growth, Yellen said. Policy makers including St. Louis Fed President James Bullard and San Francisco Fed boss John Williams said last week that higher borrowing costs were possible as soon as next month.

“Yellen indicated that core Fed members take into account the global context more than regional officials,” said Etsuko Yamashita, chief economist at Sumitomo Mitsui Banking Corp. in New York. “A June rate hike would be difficult as global financial turmoil earlier this year affects the real economy with a time lag.”

In commodities, WTI and Brent have both traded positively with WTI currently trading higher by USD 0.72/bbl just above the USD 39.00/ bbl level. Gold has also seen moves higher during European trade but has now started consolidating after reaching highs of 1244.27/oz. Meanwhile in base metals copper and iron ore price action was subdued with the red metal remaining at its lowest level since early March. Nickel for three-month delivery advanced 0.8 percent to $8,520 a metric

ton on the London Metal Exchange. Gold declined 0.3 percent to $1,238.22

an ounce in the spot market following a 1.7 percent jump last session.

West Texas Intermediate crude snapped a four-day, 7.7% tumble to rise 1.7 percent Wednesday, to $38.94 a barrel. Brent crude gained 1.2 percent to $39.59. The weaker dollar makes crude and other commodities cheaper in other currencies.

Bulletin Headline Summary from RanSquawk and Bloomberg

- European equities remain elevated on the back of dovish commentary from Fed Chair Yellen who stresses need to hike rates slowly.

- USD index remained under pressure consequently supporting flows into higher yielding currencies such as AUD and NZD.

- Going forward will see the latest US ADP report, weekly DoE inventories data, comments Fed’s Evans and also the US Treasury will sell USD 28b1n in 7y notes.

- Treasuries little changed in overnight trading, global equity markets rally on post-Yellen euphoria; this week’s auctions conclude with $28b 7Y notes, WI yield 1.59%, compares with 1.568% awarded in Feb., lowest 7Y auction stop since 1.496% in May 2013.

- U.S. Treasuries are poised for their best quarter in almost four years as bond traders cut the probability of a rate boost at the April meeting to zero after Yellen’s warning Tuesday about global economic risks; The dollar headed for its worst month in more than five years, the yen strengthened

- Boeing plans to cut about 4,000 jobs from its commercial airplanes division by mid-year as part of a broader effort to reduce costs amid fierce competition from Airbus Group SE. The U.S. planemaker doesn’t plan any involuntary layoffs, for now

- ECB Governor Draghi prepares to increase and broaden his bond-buying program, leaving investors to face even higher demand for government bonds with supply unable to keep up and some of Europe’s biggest banks are predicting yields are headed for even more record lows

- The European Central Bank isn’t discussing directly financing government stimulus, or “helicopter money,” Executive Board member Benoit Coeure said

- Euro-area economic confidence fell to the lowest level in more than a year just as the European Central Bank deployed fresh stimulus to spur growth and quash the threat of deflation

- Japan’s industrial production dropped 6.2% in February, the most since the March 2011 earthquake as falling exports sapped demand and a steel-mill explosion halted domestic car production at Toyota Motor Corp

- $6.45b IG credit priced yesterday, WTD $11.1b, MTD $155.905b, YTD $450.155b; $1.07b HY priced yesterday, WTD 4 deals $2.57b, MTD 26 deals for $16.435b, YTD 51 deals for $31.29b

- Sovereign 10Y bond yields mixed; European and Asian equity markets higher; U.S. equity-index futures rise. WTI crude oil rallies, gold and copper fall

DB’s Jim Ried concludes the overnight wrap

Well after ten days or so of some surprisingly hawkish chatter from a handful of the regional Fed Presidents, it was back to the cautious FOMC script of two weeks ago for Fed Chair Yellen following her comments yesterday at the Economic Club of New York. In stark contrast to much of the rhetoric in the interim period since the last FOMC meeting to twenty-four hours ago from her colleagues, a dovish Yellen provided a firm and effective reminder that the Fed is clearly not going to be rushed into prematurely tightening further, while at the same time surely putting to bed any possibility that the Fed could move next month, as some of the previous Fedspeak comments had alluded to.

In terms of what Yellen said exactly, the main focus was on her comment that ‘given the risks to the outlook, I consider it appropriate for the committee to proceed cautiously in adjusting policy’. This was quickly followed up by the Fed Chair also making mention to the fact that ‘this caution is especially warranted because, with the federal funds rate so low, the FOMC’s ability to use conventional monetary policy to respond to economic disturbances is asymmetric’. Yellen also highlighted that the outlook for US inflation had become ‘somewhat more uncertain’ and that recent readings on the US economy are ‘somewhat mixed’. The Fed Chair even went as far as to say that the committee has ‘considerable scope’ to ease policy if necessary and that ‘while these tools may entail some risks and costs that do not apply to the federal funds rate, we used them effectively to strengthen the recovery from the Great Recession, and we would do so again if needed’. Both China and volatility in Oil prices were also made mention to several times as risks to the US outlook.

In the lead up another rough day for Oil markets, which we’ll touch on shortly, had seen US equity markets trend lower initially, but risk markets latched onto the dovish tone with sentiment swinging as Yellen spoke, culminating with the S&P 500 eventually finishing with a +0.88% gain and in turn reaching a fresh high for the year. Credit indices also took comfort in the comments with CDX IG (1bp tighter on the day) nearly 2.5bps tighter from the earlier intraday wides. Unsurprisingly the US Dollar was hit hard with the Dollar index (-0.82%) eventually concluding a second consecutive down day. Gold finished +1.62%, while elsewhere Treasury yields were already marching lower with the moves for Oil before the Fed Chair’s comments added an extra kick, the benchmark 10y eventually finishing the day over 8bps lower at 1.804%. The probability of a hike in June fell to a fresh post-FOMC low of 28% (around 10% lower than Monday’s close), although it’s worth reminding that we still have three employment reports to come before that meeting starting with the March report this Friday.

Refreshing our screens this morning, with the exception of Japan bourses in Asia are following much of the post-Yellen gains made in the US yesterday evening. The Shanghai Comp (+1.24%), Hang Seng (+1.38%), Kospi (+0.36%) and ASX (+0.26%) are all up while iTraxx credit indices in Asia and Australia are both tighter. US equity market futures are posting modest gains. The sell-off for the US Dollar has seen the Yen benefit the most and that’s weighing on Japanese equity markets with the Nikkei currently down -0.33%. A softer than expected industrial production report out of Japan (-6.2% mom vs. -5.9% expected) is also not helping sentiment there. Meanwhile there’s better news to come out of the latest Westpac consumer sentiment reading for March in China, with the index up nearly 7pts to 118.1 and the highest level since September.

Back to yesterday and specifically those moves for Oil. WTI closed down -2.82% yesterday and a shade above $38/bbl for its fifth consecutive daily decline. In fact prices are now $4 lower than the intraday highs of less than two weeks ago with much of this being attributed to the rising skepticism building for hopes of any material outcome from the upcoming April 17th meeting between major producers in Doha. The latest dent yesterday came out of Kuwait with the acting oil minister announcing that production is to restart in the Kharfi oil field, a 300k barrel-a-day joint operation by state owned Kuwait and Saudi Arabian oil producers which had been closed since October 2014. Oil had been rallying on hopes that the upcoming Doha meeting may bring about a production freeze but questions are being asked about the seriousness of such an outcome in light of news such as this.

With regards to the economic data yesterday, the main takeaway of note was a decent rise in the March consumer confidence index to 96.2 (vs. 94.0 expected) from an upwardly revised 94.0 last month. While the details showed the present situation index declining for the second consecutive month, the expectations index did retrace nearly its entire February decline. The only other data of note in the US was the S&P/Case-Shiller house price index which showed that house prices increased +0.8% mom during January (vs. +0.7% expected) in the 20 major cities. Prior to this in Europe we saw the ECB report its money and credit aggregates for February. The M3 money supply growth rate was unchanged at 5.0% yoy as expected, however there was a reported increase in loans to both households and non-financial corporates.

Staying in Europe, European equity markets reopened from the long weekend with broad-based gains yesterday, the Stoxx 600 (+0.50%) in particular snapping the four days of consecutive losses which had made up last week. Meanwhile sovereign bond yields in Europe continue to close in on their February lows. 10y Bund yields were over 4bps lower yesterday and at 0.136% are only just above the 0.107% we reached at the end of last month. It was noted that Spanish 5y yields struck a new record low yesterday at 0.318%.

Before we take a look at today’s calendar, there was actually some other Fedspeak away from Yellen yesterday although this was clearly overshadowed by the comments from the Fed Chair. San Francisco Fed President Williams said that the future pace of rate hikes will be gradual and thoughtful while offering a slightly more positive outlook for global growth relative to that of Yellen. Meanwhile Dallas Fed President Kaplan said that although he considers all eight Fed meetings to be ‘live’, the Fed President stressed the need for the Central Bank to move in a ‘cautious, deliberate and patient’ manner.

Looking at the day ahead now then, the early data out of Europe this morning will see the release of the March confidence indicators for the Euro area (where little change is expected in the economic confidence index) before we get the first read of the March CPI reading for Germany (expected at +0.6% mom). This afternoon in the US the focus will be on the ADP employment change reading for March as a prelude for the Friday employment report, with market expectations currently sitting at 195k. Away from this it’s fairly quiet although we are due to hear from Chicago Fed President Evans (at 6.00pm BST) where he is expected to speak in NY on the economy and monetary policy, with Q&A scheduled for after.

end

i)Late TUESDAY night/ WEDNESDAY morning: Shanghai closed UP BY 80.81 POINTS OR 2.77% , / Hang Sang closed UP 437.09 POINTS OR 2.15% / The Nikkei closed DOWN 224.57 POINTS OR 1.31% . Australia’s all ordinaires was CLOSED UP 0.11%. Chinese yuan (ONSHORE) closed UP at 6.4774. Oil ROSE to 38.99 dollars per barrel for WTI and 39.66 for Brent. Stocks in Europe ALL IN THE GREEN . Offshore yuan trades 6.4808 yuan to the dollar vs 6.4774 for onshore yuan. Japanese INDUSTRIAL PRODUCTION plunges the most in almost 5 years as negative interest rates ARE KILLING BUSINESS. (see below)

FIRST: report on Japan

Japanese Industrial Production Crashes Most Since 2011 Tsunami

While we are sure this will not deter Japanese officialdom from declaring that QQE and NIRP is working and that the deflation-mindset is being beaten, the fact is that when February’s 6.2% collapse in Japanese industrial production is compared to the devastatingly poor plunge after March 2011’s quake, tsusnami, and nuclear ‘event’, something has gone disastrously wrong in Japan.

Across every sub-sector, it was a total disaster…

Find the silver-lining in that – we dare you!

SECOND: report on China

China responds favourably to Yellen’s message that the Fed will be very dovish and not raise their interest rate. Thus the POBC set their yuan much higher at 6.4774 on shore. The off shore yield also fell to 6.4808

EUROPEAN AFFAIRS

IBM Laying Off 1000 Workers In Germany

In recent weeks, the stock of IBM has staged a dramatic rebound surging from a February 11 low of $118 to $150 today, on what we previously assumed had to be another long-overdue bout of stock buybacks. However, for that to make sense, the company – already at risk of being downgraded if it did not take further cost-cutting measures to offset the additional debt interest expense – would need to engage in another round of mass layoffs.

This is precisely what happened moments ago when Germany press reported that Big Blue is cutting some 1000 jobs in Germany.

More details, Google translated from Morgenpost.

The IT group IBM apparently is planning massive job cuts in Germany. According to the trade union Verdi, the Group has informed on Wednesday about the planned reduction of nearly 1,000 jobs by March 2017th This was announced by Verdi in a newsletter. Primarily affects service segments. The group had invited the workers’ representatives to negotiations for a social plan and balance of interests. In Hannover, a region should be shut down with about 200 employees, said a Verdi representatives. The Hanover stay but generally preserved.

“IBM has informed the participation and invited to negotiations,” confirmed an IBM spokesman. A hiring freeze, it will not give: IBM will continue to hire employees with key skills. For years, the IT group struggling with a decline in sales. IBM is in a time-tag, to be replaced by new one when the old segments such as the sale of servers or infrastructure.

Nationwide 16,500 employees

Trade unionists feared already last year the job losses in the IT group in Germany. At that time there was talk of 2,500 jobs over the next two years. With the new announcement is not yet clear that it will not come to a further job cuts, said the Verdi representatives. Nationwide, the US group most recently employed about 16,500 employees. 2009 there were still 21,100 employees. (Dpa)

So with one of the key staples of the new abnormal back, namely “bad news = good news”, we are happy to see that the other one, replacing employees for buybacks, never left.

*Credit Suisse rout continues. 5y default probability – measured by CDS – jumps to 12.7%.

*06:32 Macro Update: Oil

GLOBAL ISSUES

Amazing, 1/3 of all sales in Vancouver, Canada came from wealthy Chinese who are desperate to take their yuan and buy assets like homes and gold. It did not help Alberta as their housing market is dead as can be:

(courtesy zero hedge)

“It’s Worse Than 2008”: Toronto’s “Condo King” Weighs In On The Death Of Alberta’s Housing Market

Last week, National Bank’s Peter Routledge did some “back of the envelope” calculations and determined that Chinese buyers might well have accounted for one-third of all real estate purchased in Vancouver during 2015. Here’s how he came to that rather startling conclusion:

“The NAR estimates that buyers from China invested US$28.6 billion in U.S.-domiciled residential real estate properties over the 12 months ending March 31, 2015. The results of a multiple choice survey the Financial Times solicited from 77 high net worth and affluent individuals from China (admittedly not a statistically significant sample size) [show that] of those who had purchased residential real estate outside China, 33.5% had done so in the United States, 11.7% in Vancouver, and 8.3% in Toronto. From this survey data, one could hypothesize that for every three high net worth investors from China who purchase a U.S. residence, one purchases a residence in Vancouver. One can then apply these ratios to the NAR’s estimate of US$28.6 billion in U.S. residential real estate investment made by buyers from China. From this, we hypothesize that, in 2015, homebuyers from China invested ~US$9.9 billion / Cdn$12.7 billion in Vancouver residential real estate; this amounts to 33% of total purchase volume.

If that’s even close to accurate, it would confirm what we and others have been saying for quite a while: namely that capital flight from China is driving the explosion of housing prices in red hot markets like London, Hong Kong, and yes, Vancouver.

Persistent CAD weakness made Canadian homes look particularly attractive to Chinese buyers who had traded in their RMB for USD. The same dynamic – combined with the allure of a burgeoning tech industry – also drove outsized gains in Toronto, Waterloo, and other markets across the country.

But Alberta wasn’t so lucky. Situated at the heart of Canada’s dying oil patch, the province was the only territory where real GDP contracted in 2015. While manufacturing sales across Canada rose 2.3% in January, Y/Y sales plunged 13.2% in Alberta, the sixth decline in seven months and a sure sign that the oil slump has spilled over into the rest of the economy. Provincial manufacturing sales dropped 16% last year.

The dire outlook for the provincial economy has weighed on the housing market in places like Calgary. Have a look, for instance, at the following chart which we’re fond of presenting.

As you can see, one of those three markets is not like the others.

Underscoring just how bad things truly are in Alberta, Toronto’s “condo king” Brad Lamb is putting the brakes on two condo projects planned for Alberta. “The 36-storey Jasper House and 45- storey North will be delayed at least a year,” The Calgary Herald reports. Here’s more:

“The situation in Alberta is worse than 2008,” said Brad Lamb, known as Toronto’s condo king and for his humorous billboard ads depicting his face on a sheep’s body. “This is a unique event that is annihilating anywhere in the world that produces oil.” Executives at Fortress Real Developments Inc., which partnered with Lamb on the projects, declined to comment.

Lamb is pulling back as condo sales in Calgary and Edmonton posted the steepest decline in 2015 since the financial crisis. Sales of condos fell 38 percent in Calgary, Alberta’s biggest city, and declined 56 percent in Edmonton, according to Altus Group Ltd.

Prices for Calgary apartments have been among the hardest hit in the housing market, sliding 8.7 percent to $279,697 in January, while the average Edmonton condo declined 10 percent to $227,052 over the same period, according to the real estate boards for those cities.

Yes, “it’s worse than 2008,” and any locale where the economy depends at least partly on crude has been “annihilated.”

Lamb insists that the two postponed projects will eventually be completed. Construction on Jasper House, for instance, will begin in 2017. In the meantime, if you should happen to own a Toronto condo and want to take advantage of the soaring prices made possible by the billions upon billions fleeing China…

…don’t hesitate to give Brad a call…

EMERGING MARKETS

It now seems that the USA Fed is now the Fed for the world and Mother Lioness Yellen is intent on keeping her lion cubs, (Bullard et al) in line. As a result emerging currencies are on a tear…

(courtesy zero hedge)

Emerging Market Currencies Have Best Month In 18 Years As Yellen Buoys Sentiment

Herding cats is a notoriously difficult task, but Janet Yellen served notice on Tuesday that no matter what emanates from other members of the US monetary politburo, there’s only onehouse view and that’s her’s. “As she spoke, I couldn’t help picturing a mother lion swatting her misbehaving cubs back into line,” Bloomberg’s Richard Breslow wrote this morning.

While there’s something disturbing about picturing the “diminutive” Fed chair as a “mother lion,” the analogy seems apt.

“[There was] a lot of ‘let’s not forget the far more hawkish statements other Fed officials made last week,’ [but] this was not a bolt out of the blue,” Breslow continues, noting that Yellen’s speech at the New York Economic Club “was the third dovish announcement in a matter of weeks: by the boss.”

Indeed. The biggest “boss” of them all has spoken, and this is one “mother lion” who was intent on playing the dove in March. And that’s great news for EM FX, which just had its best run in 18 years. “Developing currencies rallied in March by the most since 1998, with commodity exporters Russia and Brazil enjoying the biggest gains,” Bloomberg writes. “As an index of stocks covering developing countries headed for the best month since October 2011, Fed Chair Janet Yellen gave the rally a boost overnight by giving the strongest indication yet that she will go slow with rate increases.” Bloomberg’s dollar index is down 3.7% this month – its second consecutive monthly decline and the biggest drop in more than four and a half years.

Here’s what we wrote earlier this morning:

“Starting March 18, the Bloomberg Dollar Spot had risen as much as 1.9% as Fed officials including Lacker, Williams and Bullard noted upside risks on rate-hike projection and suggested a rate hike may be imminent as soon as April. And then Yellen unleashed the latest round of dovishness, when she made it very clear that the Fed is no longer just the U.S. central bank, but that of the world (and mostly China) and as such its prerogative is to not only keep stocks high, but to also assure there is no currency crisis in Beijing (where a month ago she met other G-20 central bankers to decide precisely this). The result of Yellen’s much discussed speech, was an immediate plunge in the Dollar spot index of 1.2% to 8 month lows, its worst month in 5 years, a drop which has continued this morning, and is on par to equal the dollar’s tumble from the first week of March when Bill Dudley likewise came out very dovish, and when the index dropped 1.7% within a week.”

“Emerging-market currencies rallied during March mainly due to a dovish Fed statement, which undermined the USD,” said Khoon Goh, a Singapore-based FX strategist at Australia & New Zealand Banking Group. There was a time when EM was stuck in a kind of lose-lose scenario vis-a-vis the FOMC. Liftoff was bad because it presaged USD strength and thus accelerated capital outflows, but the longer the Fed waited to start hiking the more nervous the EM world became. For now anyway, the emerging world seems to have found a happy medium wherein the Fed has gotten the first hike out of the way, but is now set to prove that when the Committee says “gradual,” they really mean it.

But it’s not clear that Yellen is entirely pleased with the predicament she’s put herself in by effectively transforming the Eccles Building into the headquarters of what is now the Federal Reserve Bank of the World. “At February’s G-20 meeting, Yellen most assuredly heard some pretty undiplomatic language behind closed doors on her broader responsibilities [and] it wasn’t like the joy of a bank executive to learn she is now global rather than just U.S. head,” Breslow goes on to write, before asking if we “remember the photo-op picture at the end of the meeting when everyone but [Yellen] was smiling.”

Yes Richard, in fact we do remember that and much like a similar snapshot taken last year, we found it quite amusing:

As for the rally in EM currencies, we would note that there’s a very real possibility it will be short-lived. After all, part of the strength stems from higher commodity prices and that, in turn, is linked to the market’s (likely mistaken) assumption that next month’s meeting in Doha is actually going to yield some kind of concrete set of measures designed to change the exceptionally bearish fundamental backdrop that’s kept a lid on crude since the Saudis executed the petrodollar in November of 2014. Hopes for a (farcical) output freeze have combined with the weak dollar to give crude a boost, even as the rally now looks set to dissipate quickly.

Additionally, not everyone is buying the dovish overtones. Goldman, for instance, is hell bent on insisting that economic realities in the US will make it all but impossible for the Fed to hold off much longer on the nascent tightening cycle. Tune in on Friday to see if the BLS will give the Fed’s “mother lion” another excuse to stay dovish, or whether they’ll goalseek an upside surprise to perpetuate the illusion that the US labor market is still “robust.”

Then again, it doesn’t really matter. Even if the US economy added 500,000 jobs in March all it would take is one 8% selloff on the SHCOMP for “data dependent” Janet to get cold feet – or cold “paws,” as it were.

OIL MARKETS

Oil pops in price as USA production tumbles to 16 month lows:

(courtesy zero hedge)

Crude Pops As US Production Tumbles To 16-Month Lows

Following last night’s API-reported near-expectations build in crude, DOE reports a smaller-than-expected 2.3mm build (against expectations of a 3.1mm build) and draws in Cushing, Gasoline, and Distillates. Oil prices surged on this. Production is more in focus now as it has fallen 9 of the last 10 weeks to its lowest since Nov 2014. Crude prices dropped pre-data, then spiked,. but are struggling to maintain gains.

Of course, crude is soaring on the heels of Yellen’s dove-tardiness.

API Details:

- Crude +2.64mm (+3.1mm exp.)

- Cushing -319k (confirming Genscape)

- Gasoline -1.94m

- Distillates -95k

DOE Details:

- Crude +2.3m (+3.1m exp.)

- Cushing -272k (-500k exp.)

- Gasoline -2.5m

- Distillates -1.075m

This is the 7th weekly build in inventories in a row…

The oil rally “is to do with external factors — a weaker dollar and increased risk appetite following Fed Chair Yellen’s statements,” says Commerzbank commodity strategist Carsten Fritsch.

“The API number was not far away from market expectations, so not much repositioning necessary,” says Fritsch; the market is watching U.S. crude production…

Production had dropped 9 of the last 10 weeks…

The reaction in crude…

Charts: Bloomberg

As Net-Long Positions Near Records, Is The Oil Rally Overdone?

Submitted by Nick Cunningham via OilPrice.com,

Since February, major investors have predicted that oil prices were poised for a huge rally. Hedge funds and money managers piled into bets on rising oil prices, going long on the crude rally.

Short sellers were squeezed, and the stampede become too much for many, resulting in a large liquidation of shorts. The short selling drove the rally, increasing oil prices by about 50 percent since early February.

That has fueled optimism that the worst of the oil bust is over. And there is good reason to think that a rally is justified. U.S. oil production is off by about 600,000 barrels per day since the April 2015 peak. Disruptions in Nigeria and Iraq have caught the markets by surprise, knocking off another several hundred thousand barrels per day. Gasoline demand is at record highs in the United States, and OPEC is a few weeks away from meeting to discuss its production freeze deal, which may not cut into oversupply, but has nevertheless given the markets some hope.

But there are warning signs on the horizon. The fundamentals are still very weak. Inventories are atrecord highs in the U.S. and still rising, and global oil production continues to exceed demand. As I wrote last week, the rally could be overdone.

Barclays backed that hypothesis up in a recent report, warning that several commodities could be poised for declines as the recent two-month price rally exceeds what the fundamentals suggest is merited. In other words, the reason that oil faces downside pricing risk is that there is a disconnect right now between the fundamentals and market sentiment.

On the one hand, you have incredibly bullish speculators. John Kemp at Reuters writes hedge funds and money managers have cobbled together a near-record high in net-long positions as of March 22, as shorts were closed out and investors bet that oil prices were on their way up. Net-long positions have surged to the equivalent of almost 579 million barrels, double the volume of net-long positions recorded at the end of 2015.

The last peak in net-long positions was 572 million barrels, about a month or so before oil prices began declining. For context, the record before that was the 626 million barrels in long positions posted in June 2014 when ISIS emerged and took over swathes of Iraqi territory.

Barclays analyst Kevin Norrish says that commodities prices have surged in 2016, but the recent rush into bullish bets may have gone as far as they can realistically go. “However, in the absence of any concerted fundamental improvements, those returns are unlikely to be repeated in the second quarter, making commodities vulnerable to a wave of investor liquidation,”Norrish wrote in the bank’s latest report, referring to commodities in general, though that includes crude oil. Hedge funds may have overshot on the upside, meaning the risk of oil prices going in the other direction are now more pronounced.

“Key commodities markets such as oil and copper already face overhangs of excess production capacity and inventories, but also now face another obstacle in the recovery process, that of positioning, which is now approaching bullish extremes,” Norrish said.

Just as the rally was supercharged by short sellers abandoning their positions, the oil markets are at risk of snapping back in the other direction in the next few weeks as net-long positions are undone. If speculators start to get the sense that the market is changing directions, they will start to unwind their net-long positions. But, of course, these things tend to move quickly. Once the herd starts to see the market heading down, a stampede for the exits could ensue.

While it may seem like arcane market idiosyncrasies, the potential for speculators to shift their money back to the short side would have huge influence over the oil price. In fact, as Kemp of Reuters details in an interesting chart, oil prices and hedge fund positions are closely correlated.

In short, oil prices will only rally when the fundamentals show much more of a balance, which appears to still be a few months away.

Perhaps the rush has just begun?

Crude Crashes Into Red Post-Yellen

Well, that escalated quickly…

Gold is clinging to unch, bonds are down, and now crude has crashed back into the red post-Yellen…

Only stocks remain positive – which makes perfect sense given Yellen’s implied downgrade of every positive economic indicator (and the 22.5x GAAP P/E).

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings/WEDNESDAY morning 7:00 am

Euro/USA 1.1326 up .0028 ( STILL REACTING TO USA FAILED POLICY)

USA/JAPAN YEN 112.27 DOWN 0.400 (Abe’s new negative interest rate (NIRP)a total bust/SIGNALS U TURN WITH INCREASED NEGATIVITY IN NIRP)

GBP/USA 1.4403 UP .0020 (STILL THREAT OF BREXIT)

USA/CAN 1.3028 DOWN.0036

Early THIS WEDNESDAY morning in Europe, the Euro ROSE by 28 basis points, trading now WELL above the important 1.08 level RISING to 1.1102; Europe is still reacting to deflation, announcements of massive stimulation (QE), a proxy middle east war, and the ramifications of a default at the Austrian Hypo bank, an imminent default of Greece, Glencore, Nysmark and the Ukraine, along with rising peripheral bond yield further stimulation as the EU is moving more into NIRP, and NOW THE USA’S NON tightening by FAILING TO RAISE THEIR INTEREST RATE / Last night the Chinese yuan was UP in value (onshore) The USA/CNY DOWN in rate at closing last night: 6.4774 / (yuan UP / RESPONDS IN KIND TO THE USA’S YELLEN’S MESSAGE NOT TO RAISE RATES / SO CHINA WILL NOT DEVALUE ITS CURRENCY

In Japan Abe went BESERK with NEW ARROWS FOR HIS Abenomics WITH THIS TIME INITIATING NIRP . The yen now trades in a SOUTHBOUND trajectory RAMP as IT settled DOWN in Japan by 40 basis points and trading now well BELOW that all important 120 level to 112.27 yen to the dollar. NIRP POLICY IS A COMPLETE FAILURE AND ALL OF OUR YEN CARRY TRADERS HAVE BEEN BLOWN UP/SIGNALS TO THE MARKET THAT THEY MAY DO A U TURN ON NIRP AND INCREASE NEGATIVITY

The pound was UP this morning by 20 basis points as it now trades JUST ABOVE the 1.44 level at 1.4403.

The Canadian dollar is now trading UP 36 in basis points to 1.3028 to the dollar.

Last night, Chinese bourses AND JAPAN were MIXED/Japan NIKKEI CLOSED DOWN 224.57 OR 1.31%HANG SANG UP 437.09 OR 2.15% SHANGHAI UP 80.81 OR 2.77% / AUSTRALIA IS HIGHER BY .11% / ALL EUROPEAN BOURSES ARE STRONGLY IN THE GREEN, as they start their morning/.

We are seeing that the 3 major global carry trades are being unwound. The BIGGY is the first one;

1. the total dollar global short is 9 trillion USA and as such we are now witnessing a sea of red blood on the streets as derivatives blow up with the massive rise in the rise in the dollar against all paper currencies and especially with the fall of the yuan carry trade. The emerging market which house close to 50% of the 9 trillion dollar short is feeling the massive pain as their debt is quite unmanageable.

2, the Nikkei average vs gold carry trade (blowing up and the yen carry trade HAS BLOWN up/and now NIRP)

3. Short Swiss franc/long assets blew up ( Eastern European housing/Nikkei etc.

These massive carry trades are terribly offside as they are being unwound. It is causing global deflation ( we are at debt saturation already) as the world reacts to lack of demand and a scarcity of debt collateral. Bourses around the globe are reacting in kind to these events as well as the potential for a GREXIT>

The NIKKEI: this WEDNESDAY morning: closed DOWN 224.57 OR 1.31%

Trading from Europe and Asia:

1. Europe stocks ALL IN THE GREEN AS THEY START THEIR DAY

2/ CHINESE BOURSES GREEN/ : Hang Sang CLOSED IN THE GREEN. ,Shanghai IN THE RED/ Australia BOURSE IN THE GREEN: /Nikkei (Japan)CLOSED/IN THE RED/India’s Sensex in the GREEN /

Gold very early morning trading: $1234.60

silver:$15.36

Early WEDNESDAY morning USA 10 year bond yield: 1.82% !!! UP 1 in basis points from MONDAY night in basis points and it is trading WELL BELOW resistance at 2.27-2.32%. The 30 yr bond yield FALLS to 2.62 UP 1 in basis points from TUESDAY night.

USA dollar index early WEDNESDAY morning: 94.87 DOWN 31 cents from TUESDAY’s close.(Now below resistance at a DXY of 100.)

This ends early morning numbers WEDNESDAY MORNING

end

And now your closing WEDNESDAY NUMBERS

Portuguese 10 year bond yield: 2.94% UP 2 in basis points from TUESDAY

JAPANESE BOND YIELD: -.088% DOWN A BIT in basis points from TUESDAY

SPANISH 10 YR BOND YIELD:1.43% DOWN 1 IN basis points from TUESDAY

ITALIAN 10 YR BOND YIELD: 1.21 DOWN 3 basis points from TUESDAY

the Italian 10 yr bond yield is trading 22 points lower than Spain.

GERMAN 10 YR BOND YIELD: .156% (UP 2 BASIS POINT ON THE DAY)

end

IMPORTANT CURRENCY CLOSES FOR WEDNESDAY

Closing currency crosses for WEDNESDAY night/USA dollar index/USA 10 yr bond: 2:30 pm

Euro/USA 1.1329 UP .0041 (Euro UP 41 basis points/still represents to DRAGHI A COMPLETE POLICY FAILURE/reacting to dovish YELLEN

USA/Japan: 112.47 DOWN 0.202 (Yen UP 20 basis points) and a major disappointment to our yen carry traders and Kuroda’s NIRP. They stated that NIRP would continue.

Great Britain/USA 1.4376 DOWN .0008 Pound DOWN 8 basis points/(LESS Brexit concern.)

USA/Canada: 1.2972 down .0.0091 (Canadian dollar UP 91 basis points DESPITE THE FACT THAT oil wasHARDLY MOVED (WTI = $38.39)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

This afternoon, the Euro was UP by 41 basis point to trade at 1.1328 as the markets REACT TO YELLEN’S DOVISHNESS

The Yen ROSE to 112.47 for a GAIN of 20 basis pints as NIRP is a big failure for the Japanese central bank/also all our yen carry traders are being fried.

The pound was DOWN 2 basis points, trading at 1.4376 (LESS BREXIT CONCERNS)

The Canadian dollar ROSE by 91 basis points to 1.2972 , despite the fact that the price of oil was CONSTANT today (as WTI finished at $38.38 per barrel)

the 10 yr Japanese bond yield closed at -.088% DOWN A BIT IN basis points in yield

Your closing 10 yr USA bond yield: UP 1 basis point from TUESDAY at 1.82% //trading well below the resistance level of 2.27-2.32%) policy error

USA 30 yr bond yield: 2.65 UP 4 in basis points on the day and will be worrisome as China/Emerging countries continues to liquidate USA treasuries (policy error)

\

Your closing USA dollar index, 94.89 DOWN 30 cents on the day at 2:30 pm

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for WEDNESDAY

London: CLOSED UP 97.27 POINTS OR 1.59%

German Dax :CLOSED UP 158.67 OR 1.60%

Paris Cac CLOSED UP 77.73 OR 1.78%

Spain IBEX CLOSED UP 61.90 OR .70%

Italian MIB: CLOSED UP 203.46 OR 1.12%

The Dow was up 83.55 points or 0.47%

Nasdaq up 22.67 points or 0.47%

WTI Oil price; 38.36 at 2:30 pm;

Brent Oil: 39.27