April 12/Raid foiled again/Gold and silver advance/European investors totally dissatisfied with the deal to rescue our insolvent Italian banks/The Italian Stock exchange halted all Italian bank stocks from trading in mid afternoon/Valeant given a notice of default by one company who did not go along with the deal/Fun and games tomorrow/

Today, the bankers got a good look at the real OI for today in both gold and silver(remember that OI is always reported one day late and this gives the house a huge advantage) and they decided en masse that it was necessary to orchestrate a raid. The problem of course was the fact that many investors were waiting in the wings and they gobbled up many of the huge offerings from our bankers. Over on the other side of the pond in London, physical gold and silver are disappearing off the planet and thus it is much harder for the bankers to do their usual and customary (and criminal) raids. The OI for both gold and silver no doubt will be much higher tomorrow and the bankers will need to burn the midnight oil deciding whether to raid or not.

Let us have a look at the data for today

.

At the gold comex today, we had a GOOD delivery day, registering 123 notices for 12300 ounces for gold,and for silver we had 0 notices for nil oz for the non active April delivery month.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 214.39 tonnes for a loss of 85 tonnes over that period.

In silver, the open interest rose by a whopping 4,750 contracts UP to 180,058 as the silver price was UP 59 cents with respect to yesterday’s bullish trading. In ounces, the OI is still represented by .900 billion oz or 128% of annual global silver production (ex Russia ex China). We are now at multi year highs in OI with respect to silver

In silver we had 0 notices served upon for NIL oz.

In gold, the total comex gold OI ROSE BY A GIGANTIC 14,345 contracts UP to 498,189 contracts as the price of gold was UP $14.10 with YESTERDAY’S trading.(at comex closing).

We had another big change in the GLD, a withdrawal of 2.67 tonnes / thus the inventory rests tonight at 815.14 tonnes. The fact that gold has a huge three days, I rather suspect that the bankers need to get their hands on physical quickly and the thus raided the GLD cookie jar. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,we had no changes and thus the Inventory rests at 336.151 million oz.

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver RISE by 4750 contracts UP to 180,058 as the price of silver was UP 59 cents with YESTERDAY’S trading.Today, the bankers TRIED TO ATTACK AND AGAIN THEY FAILED. The total OI for gold rose by 14,345 contracts to 498,189 contracts as gold was UP $14.10 in price from yesterday’s level. THE HIGH OI FOR GOLD WAS THE REASON FOR THE ATTEMPTED RAID TODAY.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

b) COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late MONDAY night/ TUESDAY morning: Shanghai closed down 10.31 POINTS OR 0.34% (even with last hr rescue) / Hang Sang closed UP 63.63 OR 0.31%. The Nikkei closed UP 177.66 POINTS OR 1.13% . Australia’s all ordinaires CLOSED UP 0.89%. Chinese yuan (ONSHORE) closed UP at 6.4606. Oil ROSE to 40.66 dollars per barrel for WTI and 43.12 for Brent. Stocks in Europe ALL IN THE GREEN . Offshore yuan trades 6.4702 yuan to the dollar vs 6.4606 for onshore yuan. LAST WEEK:Japanese INDUSTRIAL PRODUCTION plunges the most in almost 5 years as negative interest rates ARE KILLING BUSINESS./JAPANESE TANKEN CONFIDENCE INDEX PLUMMETS/JAPAN HAS NEVER RECOVERED FROM THOSE BAD DATA RELEASES/TODAY THE USA/YEN CROSS REMAINS AT THE 108 CROSS SETTING OFF GLOBAL TENSIONS WHICH IN TURN IS CAUSING THE SPECIAL MEETING AT THE FED.

REPORT ON JAPAN SOUTH KOREA AND CHINA

a) REPORT ON JAPAN

ii)Our famous Mr Yen, Eisuke Sakakibara now says that Japan’s currency may strengthen to 100 yen to the dollar. He states that intervention will be fruitless. Although Japanese officials state that the 100 yen to the dollar is no problem for the Japanese economy it will surely wreck havoc on the rest of the world especially with the trillions of yen carry traders getting annihilated.

( zero hedge)

iii)An extremely important paper where the former chief IMF economist Olivier Blanchard admits how the end game will be played out. He discusses that Japan already has 34% of all Japanese issuance of bonds and by next year they will approach 50%. He then states that there will be a scarcity of sellers which will force Japan to taper buying of bonds. This will then force yields higher and with that deflation will turn on a dime into hyperinflation

a must read…

( zero hedge)

b) REPORT ON CHINA

iv)China will still due to stealth devaluation despite the blasting from USA’s Lew.

Even though the yuan/yuan has been stable, take a look at how the yuan is behaving against its currency basket: falling!!

The Japanese yen is out of ammo to cause its currency to falter. The USA has made a decision to lower its currency (thus hurting the yen by causing it to rise as well as causing the Euro to rise) so as not to allow the devaluation of the yuan against it.

( zero hedge)

v) a terrific article on the plight of China:

( David Stockman/ContraCorner)

EUROPEAN AFFAIRS

i) Italy announced its long awaited rescue for its troubled banking sector. They have 360 billion euros of non performing loans. So they now set up a fund called Atlas or Atlante to buy up the troubled loans. The problem: the fund is only 5 billion euros.

( zero hedge)

ii)Confusion is the order of the day, as Schauble met Draghi early this morning. The meeting was meant to smooth over things that the ECB said and where it was heading. Schauble was not impressed!

( zero hedge)

iii)Late in the European session, we now witness Italian banks are halted and they are also LIMIT DOWN. The tiny rescue pkg is just not enough. The USA markets then proceeded to turn south:

( zero hedge)

GLOBAL ISSUES

WHAT A JOKE: the IMF has now cut its global growth forecast for 2016 to 3.2% from 3.4%.

These guys have no clue and their forecasting skills are worth zero

( zero hedge)

OIL ISSUES

i)Early this morning, Bloomberg oil strategist Julian Lee warns us not to be bullish on the DOHA freeze talks scheduled for April 17.2016:

( zero hedge)

ii)This phony headline sends the Dow and Nasdaq skyrocketing. It was total garbage:

( zero hedge)

Crude, Stocks Soar On Russia-Saudi “Production Freeze” Headline

iii)Well that did not last long! Oil falters after a surprisingly large inventory build:

( zero hedge)

PHYSICAL MARKETS

i)Silver continues to be the star performer as we have highlighted to you, the commercials seem to be “getting out of Dodge”

( zero hedge)

ii)Silver continues to be the star performer as we have highlighted to you, the commercials seem to be “getting out of Dodge”

( zero hedge)

iii)Huge Chinese demand for March equal to 183.2 tonnes or 43.6 tonnes per week.They are still importing massive amounts of gold and they are not stopping

( Lawrie Williams/Sharp’s Pixley)

iv)John Embry discusses the fact that the prices of gold and silver are rising due to the scarcity of the physical metals. Also gold/silver equity companies are also recognizing the physical shortage and thus their shares are nicely bid.

John Embry takes note of the IMF warnings of the health of insurance companies. These guys are having a real tough time in the NIRP world

a great interview…

( John Embry/Kingworldnews)

v)Chris Powell is interviewed on Bloomberg TV and India TV( GATA/Chris Powell)

vi)Very unusual!! A former Yellen adviser goes against the Fed and proposes sweeping reforms of the Fed system: i.e. making the Fed transparent and a public vehicle, not a private one

( zero hedge)

USA STORIES WHICH WILL INFLUENCE THE PRICE OF GOLD/SILVER

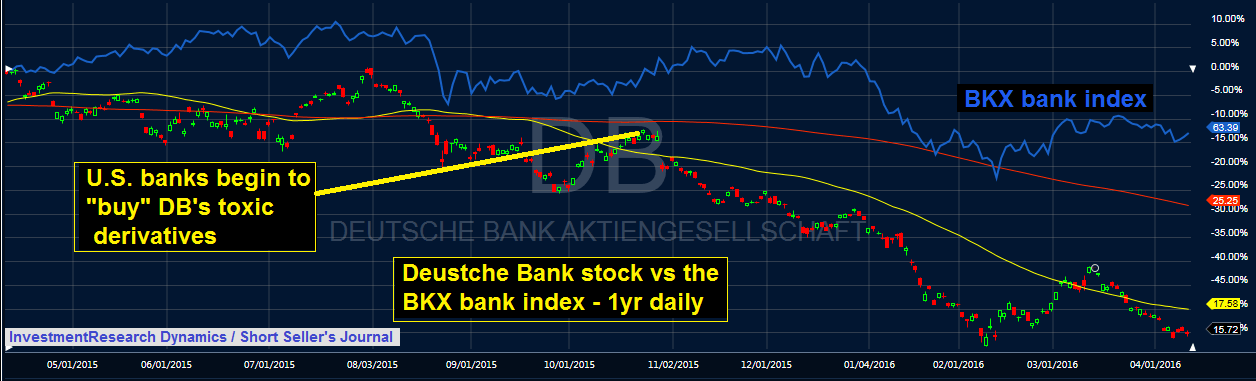

i)We now know that the Fed has 3 meetings this week, the first was held on Monday, the second one, today and one tomorrow. Dave Kranzler and I are of the same opinion that these meetings were how to save Deutsche Bank with all of their huge amounts of derivatives underwritten. We differ on the fact that once DB blows up there is nobody on earth that can save them: they have now well over 75 trillion dollars worth of derivative underwritten. (They had 75 trillion in 2014)

( Dave Kranzler/IRD)

ii)It now seems that New York is joining London England where luxury real estate is plummeting in price.( zero hedge)

iii)Oh boy!! this ought to be fun. Centerbridge has notified Valeant after hours that it intends to call a default event as our darling company broke covenants with its reporting requirements. Valeant had sought a delay and was willing to give a bonus interest for the privilege. Centerbridge said no and this called it a default event.

Let us see what happens tomorrow:

( zero hedge)

iv)Jeff Gundlach, of Doubleline is one smart cookie. He is a bond guru. He is stating that he remains bullish on gold and that there will be only one Fed hike and it was done in December. In other words one and done!

( Jeff Gunlach/zero hedge)

v)We have Bank of America’s credit card data and it suggest a huge April retail sales plunge!!

( bank of America/zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE to an OI level of 498,189 for a gain of 14,345 contracts as the price of gold was UP $14.10 in price with respect to yesterday’s bullish trading. We are now entering the active delivery month of April. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month or for that matter an inactive month, and 2) a continual drop in the amount of gold standing in an active month. We certainly witnessed both parts today . In the front month of April we lost 101 contracts from 3575 contracts down to 3474. We had 30 notices filed so we lost 71 contracts or an additional 7100 gold ounces that will not stand for delivery. The next non active contract month of May saw its OI rise by 63 contracts up to 2855. The next big active gold contract is June and here the OI ROSE by 11,107 contracts UP to 375,245. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was POOR at 156,787 . The confirmed volume YESTERDAY (which includes the volume during regular business hours + access market sales the previous day was poor at 180,194 contracts. The comex is not in backwardation.

Today we had 123 notices filed for 12,300 oz in gold.

And now for the wild silver comex results. Silver OI ROSE by a considerable 4750 contracts from 175,308 UP to 180,058 AS the price of silver was up 59 cents with yesterday’s rise in price. We are now in the next contract month of April and here the OI ROSE by 2 contracts falling to 64. We had 0 notices filed on yesterday so we gained 2 silver CONTRACTS or an additional 10,000 ounces of silver will stand for delivery in this non active month of April. The next active contract month is May and here the OI rose by 1334 contracts up to 98,575. This level is exceedingly high. We do have 2 and 1/2 weeks before first day notice on Friday, April 29.The volume on the comex today (just comex) came in at 80,145, which is huge. The confirmed volume yesterday (comex + globex) was humongous at 90,432. Silver is not in backwardation. In London it is in backwardation for several months.

The bankers must be getting very anxious as they attempted a raid again today with the obvious objective to loosen many gold and silver leaves from the silver tree as possible. They failed miserably!! The record high OI in silver in concert with a very low silver price has not resolved itself after 5 yrs of trading.

Total monthly oz gold served (contracts) so far this month

1286 contracts (128,600 oz)

Total accumulative withdrawals of gold from the Dealers inventory this month

nil

Total accumulative withdrawal of gold from the Customer inventory this month

78,877.4 oz

Today we had 1 dealer deposit

i) Into Brinks: 65,452.74 oz

and that entry I can understand.

Total dealer deposits; 65,452.74 oz

Today we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

Today we had 1 customer deposit:

Into Scotia: Exactly 16,000.000 oz ???

how could we have such an entry and this is not divisible by 32.15 so it is not kilobars

they can making a farce of the comex

Total customer deposits: 16,000.0000 oz

Today we had 2 customer withdrawal:

i) Out of MANFRA: 160.75 oz

ii) Out of Scotia: 1768.25 oz (55 kilobars)

total customer withdrawals: 1929.000 oz 60 kilobars

Today we had 0 adjustments:

.

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 123 contracts of which 34 notices was stopped (received) by JPMorgan dealer and 33 notices were stopped (received) by JPMorgan customer account.

To calculate the initial total number of gold ounces standing for the Mar contract month, we take the total number of notices filed so far for the month (1286) x 100 oz or 128,600 oz , to which we add the difference between the open interest for the front month of April (3474 CONTRACTS) minus the number of notices served upon today (123) x 100 oz x 100 oz per contract equals the number of ounces standing.

Thus the initial standings for gold for the April. contract month:

No of notices served so far (1286) x 100 oz or ounces + {OI for the front month (3474) minus the number of notices served upon today (123) x 100 oz which equals 463,700 oz standing in this non active delivery month of April (14.423 tonnes).

Since the comex allows GLD shares to be used for settling, it may take quite a while for the physical gold to enter the comex vaults. So far I have seen little evidence of any settling of contracts but I will continue to monitor it for you.

We thus have 14.423 tonnes of gold standing for April and 12.871 tonnes of registered gold for sale, waiting to serve upon those standing. The bankers are still doing their best in cash settling as there is not enough registered gold to satisfy those that are standing.

We now have partial evidence of gold settling for last months deliveries We now have 14.423 tonnes (April) +2.2311 tonnes (March) + 7.99 (total Feb)- .940 (probable delivery on March 1) tonnes -.0434 tonnes (March 11,12,17,18) + March 31: 1.2470 and then April 1,2: – .0006 tonnes = 22.413 tonnes still standing against 12.871 tonnes available. .

Total dealer inventor 413,811.03 oz or 12.871 tonnes

Total gold inventory (dealer and customer) =6,892,738.779 or 214.39 tonnes

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 214.39 tonnes for a loss of 85 tonnes over that period.

JPMorgan has only 21.15 tonnes of gold total (both dealer and customer)

end

And now for silver

APRIL INITIAL standings

/April 12/2016:

Silver

Ounces

Withdrawals from Dealers Inventory

nil

Withdrawals from Customer Inventory

1,127,825.283 OZ. CNT, Delaware

SCOTIA,JPM

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

456,809.400 OZ

Brinks,Delaware

No of oz served today (contracts)

0 contracts

nil oz

No of oz to be served (notices)

66 contracts)(330,000 oz)

Total monthly oz silver served (contracts)

123 contracts (615,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

nil oz

Total accumulative withdrawal of silver from the Customer inventory this month

3,374,818.6 oz

today we had 0 deposits into the dealer account

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 2 customer deposits:

i) Into BRINKS: 455,789.300 oz

ii)Into Delaware: 1020.100 oz

total customer deposits: 456,809.400 oz

We had 4 customer withdrawal

i) Out of CNT: 10,057.900 oz

ii) Out of Delaware: 981.600 oz

iii) Out of Scotia: 660,996.483

iv) Out of JPM: 455,789.300 oz

:

total customer withdrawals: 1,127,825.283 oz

we had 0 adjustments

The total number of notices filed today for the April contract month is represented by 2 contracts for 10,000 oz. To calculate the number of silver ounces that will stand for delivery in April., we take the total number of notices filed for the month so far at (123) x 5,000 oz = 615,000 oz to which we add the difference between the open interest for the front month of April (66) and the number of notices served upon today (0) x 5000 oz equals the number of ounces standing

Thus the initial standings for silver for the April. contract month: 123 (notices served so far)x 5000 oz +(x66{ OI for front month of April ) -number of notices served upon today (0)x 5000 oz equals 945,000 oz of silver standing for the March contract month.

we gained 2 silver contracts or an additional 10,000 ounces will stand in this non active delivery month.

Total dealer silver: 32.452 million

Total number of dealer and customer silver: 154.596 million oz

The open interest on silver is now at multi year highs. Expect a raid tomorrow.

end

And now the Gold inventory at the GLD

April 12/another huge withdrawal of 2.67 tonnes of gold from the GLD and again despite the rise in gold. The boys must be desperate to get their hands on some physical.

Inventory rests at 815.14 tonnes.

April 11. We had a huge withdrawal of 1.79 tonnes of gold despite the rise in gold. No doubt whatever physical gold the GLD had just went over to China/inventory rests tonight at 817.81 tonnes

APRIL 8/no changes in tonnage of gold/rests tonight at 819.60 tonnes

APRIL 7/ a huge deposit of 4.17 tonnes of “paper” gold was added to our GLD/Inventory rests tonight at 819.60 tonnes

APRIL 6/a withdrawal of .29 tonnes of gold and probably this was to pay for fees for the custodian and insurance/inventory rests at 815.43 tones

April 5/ a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 815.72 tonnes

APRIL 4/a withdrawal of 1.19 tonnes from the GLD/Inventory rests at 818.09 tonnes of gold

April 1/no changes in gold inventory at the GLD/Inventory rests at 819.28 tonnes

MARCH 31/a small withdrawal of 1.19 tonnes/inventory rests tonight at 819.28 tonnes

MARCH 30/no changes in inventory/inventory rests tonight at 820,47 tonnes

March 29/a withdrawal of 3.27 tonnes of gold from the GLD/Inventory rests at 820.47 tonnes. (No doubt we will see a rise in gold inventory with tomorrow’s reading)

March 28/no change in inventory at the GLD/Inventory rests at 823.74 tonnes

March 24.2016: a deposit of 2.08 tonnes of gold into its inventory/and this after a big drubbing these past two days??/Inventory rests at 823.74 tones

March 23/no changes at the GLD today despite the gold drubbing. Inventory rests at 821.66 tonnes

March 22./no changes in inventory at the GLD/Inventory rests at 821.66 tonnes

April 12.no change in silver inventory/rests tonight at 336.151 million oz

April 11.2016; a huge addition of 1.427 million oz of “paper” silver entered the SLV/Inventory rests at 336.151 million oz

APRIL 8/no changes in silver inventory/rests tonight at 334.724 million oz

APRIL 7/no change in silver inventory/rests tonight at 334.724 million oz

April 6/no change in silver inventory/Inventory rests at 334.724 million oz

April 5/ a deposit of 2.146 million oz of silver into the SLV/Inventory rests at 334.724 million oz/

APRIL 4/no change in silver inventory tonight/inventory rests at 332.578 million oz

Apri 1: we had a huge deposit of 2.189 million oz of silver into the SLV (with silver badly down?)/.Inventory rests tonight at 332.578 million oz

MARCH 31/ no change in silver inventory at the SLV tonight/inventory rests at 330.389 million oz

MARCH 30/no change in inventory/inventory rests at 330.389 million oz

March 29.2016: a huge deposit of 1.475 million oz of silver into the SLV/Inventory rests at 330.389 million oz

March 28/no change in silver inventory at the SLV/Inventory rests at 328.914 million oz

March 24.2016/no change in inventory/rests tonight at 328.914 million oz/

March 23/we lost 1.428 million oz as a withdrawal today/SLV inventory rests at 328.914 million oz

.

April 12.2016: Inventory 336.151 million oz

.end

1. Central Fund of Canada: traded at Negative 4.9 percent to NAV usa funds and Negative 5.3% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.4%

Percentage of fund in silver:36.6%

cash .0%( April 12.2016).

2. Sprott silver fund (PSLV): Premium to NAV falls to -.82%%!!!! NAV (April12.2016)

3. Sprott gold fund (PHYS): premium to NAV rises to +16% to NAV ( April12.2016)

Note: Sprott silver trust back into negative territory at -.82%% due to purchase of 75 million dollars worth of silver/Sprott physical gold trust is back into positive territory at +.16%/Central fund of Canada’s is still in jail.

It looks like Eric Sprott got on the nerves of our bankers as they lowered the premium in silver to -.82%. Remember that Eric is to get 75 million dollars worth of silver. Please note that for the first time in quite a while, Eric’s gold fund went positive in premium.

end

And now your overnight trading in gold, FRIDAY MORNING and also physical stories that may interest you:

Trading in gold and silver overnight in Asia and Europe

By Mark O’Byrne

Silver Bullion Surges 8% In 6 Days To Over $16 Per Ounce

Silver bullion prices surged 3.65% yesterday and have surged 8% in just six trading days. Silver rose 56 cents from $15.34 to $15.90 per ounce yesterday, made further gains in Asian and early European trading and broke above the psychological resistance of $16 per ounce.

Since last Monday (April 4), silver has surged from $14.93 to $16.12 per ounce for an 8% gain as ongoing robust physical demand finally seems to be impacting on prices which remain depressed. Silver is now testing technical resistance at $16.15/oz and a close above that level could see silver quickly move to test the next level of resistance at $18 per ounce seen in May 2015.

The surge in recent days was impressive as it came against a backdrop of negative economic data, concerns about corporate earnings, the U.S. and global economy and weakness in stock markets globally.

The supply demand dynamics in the silver market remain conducive to higher prices in the coming months. Industrial and particularly investment demand for silver is strong.

Industrial demand for silver is expected to rise 3% in 2016 according to Capital Economics. Investment demand for silver bullion coins and bars has risen by 400% from under 50 million ounces in 2006 to 200 million ounces in 2015. Investment demand remains robust as seen in the silver holdings of the iShares Silver Trust, the biggest exchange-traded product in the metal. SLV holdings have increased by nearly 9% year to date. This is also seen in demand for silver bullion legal tender coins such as

Separately, one of the leading silver investment vehicles – the Sprott Physical Silver Trust, a trust created to invest and hold substantially all of its assets in physical silver bullion and managed by Sprott Asset Management LP, announced today that it has priced its follow-on offering of 12,300,000 transferable, redeemable units of the Trust (“Units”) at a price of US$6.09 per Unit (the “Offering”). As part of the Offering, the Trust has granted the underwriters an over-allotment option to purchase up to 1,845,000 additional Units. The gross proceeds from the Offering will be US$74,907,000 and this will likely result in a substantial amount of silver coming out of an already quite tight market.

Investment demand is likely to remain robust and may even increase due to ineffectual QE policies, still ultra loose monetary policies, negative interest rates leading to increased allocations to non yielding bit non negative yielding silver.

Silver remains undervalued from a historical perspective and from the all important inflation adjusted perspective. This means that reaching the record nominal high over $49/oz (seen in 1980 and 2011) is likely again.

Longer term the inflation adjusted 1980 high of $150/oz remains realistic – especially given the increasing use of silver in various industrial application and silver’s increasing investment demand – with silver continuing to be seen as the cheaper, better value, alternative to gold.

Gold Prices (LBMA)

12 April: USD 1,259.20, EUR 1,102.15.84 and GBP 880.18 per ounce

11 April: USD 1,247.25, EUR 1,095.84 and GBP 878.96 per ounce

8 April: USD 1,235.00, EUR 1,085.18 and GBP 877.33 per ounce

7 April: USD 1,237.50, EUR 1,086.07 and GBP 879.70 per ounce

6 April: USD 1,225.75, EUR 1,079.76 and GBP 868.38 per ounce

Silver Prices (LBMA)

12 April: USD 15.96, EUR 13.98 and GBP 11.15 per ounce 11 April: USD 15.56, EUR 13.66 and GBP 10.93 per ounce 8 April: USD 15.16, EUR 13.34 and GBP 10.78 per ounce

7 April: USD 15.22, EUR 13.38 and GBP 10.81 per ounce

6 April: USD 15.07, EUR 13.28 and GBP 10.71 per ounce

Gold News and Commentary

Gold at 3-wk high as dollar struggles amid US rate outlook (Reuters)

Gold posts highest settlement in over 3 weeks (Marketwatch)

Gold Prices Unlikely To Slow Down, $1,350/oz In 2017: Credit Suisse (Value Walk)

Global Stocks Rise Amid China Data as Crude Climbs, Dollar Slips (Bloomberg)

London Luxury-Home Pipeline Would Cover Hyde Park Twice (Bloomberg)

Bloomberg interview GATA secretary about gold market rigging (Bloomberg)

A third of homes in some London boroughs have cut their asking prices (City AM)

Making Most of Your Personal Freedom & Financial Opportunity – Casey (Gold Seek)

BofA Warns “Europe Looks Frightening” – Trades Like 2001, 2008 (Zero Hedge)

Gold Should Glisten As Confidence in Central Banks Sags (Real Money)

Silver continues to be the star performer as we have highlighted to you, the commercials seem to be “getting out of Dodge”

(courtesy zero hedge)

Silver Surges To 8-Month Highs As Hedgers Unwind

Silver is now up almost 10% from its spike lows last week (up over 5% since Friday), has broken above $16, snapped 2016’s highs at $16.17 and is back at its highest since October 2015. Amid the big tumble in commercial hedgers positions, we also note the Gold/Silver ratio has plunged to 2-month lows – just as we suggested.

Silver breaks 2016 highs…

To October levels…

As hedgers unwind…

A month ago we said, So bottom line, if you’re a speculator in precious metals, now may be a good time to consider trading in some gold for silver.

And since then,Silver is up 4.6% and gold unch…

Leaving the Gold/Silver ratio at 2-month lows…

end

Huge Chinese demand for March equal to 183.2 tonnes or 43.6 tonnes per week.

They are still importing massive amounts of gold and they are not stopping

For those avid watchers of the Shanghai Gold Exchange (SGE) withdrawal figures, those for the month of March came in at a respectable 183.2 tonnes – well above the rather abject February level (107.6 tonnes) which was kept down by the SGE’s closure over the Chinese Lunar New Year holiday, but well below that for January which saw a bit of a buying surge ahead of that holiday. With Q1 gold withdrawal figures always affected by the timing of the New Year holiday period, which fell on February 6th this year, it is always difficult to draw any sensible conclusions as to what these early year figures mean in terms of likely total Chinese demand for the full year.

Looking at the total Q1 figure, this came in at 515.9 tonnes – 17.5% down on that for the Q1 figure for the first quarter of last year when the full year total was a massive 2,596.4 tonnes, but it is a respectable figure nonetheless suggesting a full year total of over 2,000 tonnes for the fourth year in a row.

A big unknown here of course is how much the considerably lower growth in the Chinese economy, coupled with higher gold prices should they continue, or indeed rise further, will do for Chinese gold demand. The Chinese are believed to be bargain hunters in terms of the gold price, climbing in when they perceive it to be weak – as witness the huge surge in demand in April 2013 when the gold price was knocked back very sharply indeed in the West, leading to what was then a big new record year for Chinese gold demand – since surpassed in 2015.

The performance of the Chinese stock markets will also be relevant – but whether the big fall from its peak last year (down over 40%) will encourage safe haven gold investment, or restrict demand because of loss of capital, is something of an unknown. However fear of a possible gradual devaluation of the yuan against the US dollar as the country defends its export earnings, could well see a boost to gold demand. We shall see.

-END-

John Embry discusses the fact that the prices of gold and silver are rising due to the scarcity of the physical metals. Also gold/silver equity companies are also recognizing the physical shortage and thus their shares are nicely bid.

John Embry takes note of the IMF warnings of the health of insurance companies. These guys are having a real tough time in the NIRP world

a great interview…

(courtesy John Embry/Kingworldnews)

Strength of HUI gold share index impresses Embry

Submitted by cpowell on Tue, 2016-04-12 08:58. Section: Daily Dispatches

4:55p SGT Tuesday, April 12, 2016

Dear Friend of GATA and Gold:

Sprott Asset Management’s John Embry, interviewed by King World News, says gold price suppression is showing strains, the strength of the gold mining index HUI is impressive, and the Sprott silver fund is about to take a huge chunk of metal off the market. An excerpt from the interview is posted at KWN here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

Chris Powell is interviewed on Bloomberg TV and India TV

(courtesy GATA/Chris Powell)

Bloomberg TV and Times of India TV interview GATA secretary about gold market rigging

Submitted by cpowell on Tue, 2016-04-12 07:57. Section: Daily Dispatches

3:55p SGT Tuesday, April 12, 2016

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed for a few minutes this morning in Singapore by Angie Lau in Hong Kong for Bloomberg Television’s “First Up” program, discussing the ever-increasing evidence of surreptitious central bank intervention in the gold market and the need for mainstream financial news organizations to ask central banks some specific questions about it. The interview can be seen at Bloomberg here:

Bloomberg Radio interviewed your secretary/treasurer for about about five minutes in Hong Kong last week.

Also today, your secretary/treasurer was interviewed from Singapore by The Times of India’s “Economic Times Now” television network in a live broadcast in India. Again the subject was surreptitious intervention against gold by central banks. Video of the program is not available but a transcript of your secretary/treasurer’s remarks, headlined “If Central Banks Get Out of Market, Gold Will Pick Up a Lot of Steam: Chris Powell, GATA,” is posted at the Times’ Internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

Very unusual!! A former Yellen adviser goes against the Fed and proposes sweeping reforms of the Fed system: i.e. making the Fed transparent and a public vehicle, not a private one

(courtesy zero hedge)

Former Yellen adviser proposes sweeping reform of Fed system

Submitted by cpowell on Tue, 2016-04-12 09:13. Section: Daily Dispatches

By Craig Torres

Bloomberg News

Monday, April 11, 2016

A former aide to Federal Reserve Chair Janet Yellen has broken ranks with his former employer and issued a blueprint for a sweeping reform of the U.S. central bank, including regular government audits and shorter term limits for policy makers.

Dartmouth College professor Andrew Levin targeted four areas of change for the Federal Reserve system: make the Fed a fully public institution; ensure that the process of picking regional Fed presidents is transparent; set seven-year term limits for regional presidents and board governors; and make the entire Fed subject to external review.

The proposals were taken up by the union-backed activist group Fed Up, which promoted them Monday in a conference call with journalists, and come during an election year where the central bank has been a campaign topic.

“There is one key principle in this document, which is the Fed needs to become a public institution,” Levin said. “Pragmatic, reasonable Fed reform should be able to be passed by the Congress, by both parties. That is my hope.” …

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.4606 / Shanghai bourse CLOSED DOWN 10.30 OR 0.34% / HANG SANG CLOSED UP 63.63 OR 0.31%

2 Nikkei closed up 177.66 or UP 1.13% (STILL REACTING TO POOR INDUSTRIAL PRODUCTION/POOR RETAIL SALES/TERRIBLE TANKEN CONFIDENCE INDEX/USA: YEN RISES SLIGHTLY TO 1.0828)

3. Europe stocks opened ALL IN THE GREEN /USA dollar index DOWN to 93.86/Euro UP to 1.1417

3b Japan 10 year bond yield: FALLS TO -.093% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.66

3c Nikkei now WELL BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 40.66 and Brent: 43.12

3f Gold UP /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES to 0.122% German bunds in negative yields from 9 years out

Greece sees its 2 year rate RISE to 11.09%/:

3j Greek 10 year bond yield RISE to : 9.24% (YIELD CURVE NOW INVERTED)

3k Gold at $1257.80/silver $16.00 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble UP 33/100 in roubles/dollar) 66.36

3m oil into the 39 dollar handle for WTI and 41 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN COLLAPSES TO 108.33 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9529 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0888 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN STARTS ITS CAMPAIGN AS TO WHETHER EXIT THE EU.

3r the 9 Year German bund now in negative territory with the 10 year RISES to + .122%

/German 9 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.76% early this morning. Thirty year rate at 2.59% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Rebound On Weaker Yen; Oil Hits 2016 Highs

In recent days, we have observed a distinct trading pattern: a ramp early in the US morning, usually triggered by some aggressive momentum ignition, such as today’s unexplained pump then dump in the EURUSD…

… with stocks rising after the European open, rising throughout the US open, then peaking around the time the US closed at which point it is all downhill for the illiquid market.

So far today, the pattern has held, and after trading flat for most of the overnight session, with Europe initially in the red perhaps on disappointment about the Italy bank bailout fund,a bout of early Europe-open associated buying pushed US futures up, following the first rebound in the USDJPY after 7 days of declines which also helped the Nikkei close 1.1% higher (even though as BBG notes, investors in the options markets don’t seem to share enthusiasm that the USDJPY will rebound as the premium for USD/JPY puts over calls is 164 bps versus 161 bps yesterday; has climbed about 94 bps in favor of puts in just this month).

Oil, likewise, has continued to climb and earlier hit new 2016 highs when WTI rose just 9 cents shy of $41 on the same recurring catalyst: the Doha OPEC meeting (where even Russia admitted yesterday nothing will happen), and hopes shale production will contract even as many companies reactivate DUCs and quite the opposite may in fact happen.

Brent crude was up 50 cents at $43.33 a barrel at 0842 GMT and earlier in the session reached a 2016 high of $43.53. U.S. crude gained 39 cents to $40.75 a barrel. “The weak dollar is one important reason,” said Eugene Weinberg of Commerzbank. “Also, the fact that we are above $40 and at multi-month highs is also contributing to the price increase as it is prompting some speculative buying.”

As Reuters adds, also supporting prices was rising vehicle sales in China – a further sign of strong gasoline demand in the No. 2 consumer – and a plan by thousands of oil and gas workers in Kuwait to go on strike from Sunday. “If it is not clear if the strike will last long and will have any meaningful impact on exports or domestic production (including refineries), it does illustrate further the amount of pain that (Gulf) oil producers are also facing at current price levels,” said Olivier Jakob, analyst at Petromatrix.

For now, however, as Bloomberg puts it, “crude oil’s advance above $40 a barrel boosted economic optimism” and the MSCI All-Country World Index advanced for a third-straight day and Russia’s ruble joined the Australian dollar and Norway’s krone among the best-performing currencies. Metals prices jumped, helping push the Bloomberg Commodity Index to the highest this month.

The key catalyst preserving stability for the time being are emerging markets which are “strong, mainly on the back of the weak U.S. dollar and strong oil,” Maarten-Jan Bakkum, a senior strategist at NN Investment Partners, told Bloomberg. “Flows have clearly improved, Chinese risks are lower for the short term, but we do not see a convincing improvement in growth momentum yet.”

Here is a snapshot of where markets stand right now:

S&P 500 futures up 0.3% to 2040.6

Stoxx 600 up 0.1% to 333.1

Euro Stoxx 50 up 0.1%

FTSE 100 up -0.2%

DAX up 0.4%

Euro up 0.21% to $1.1432

Italian 10Yr yield up 1bps to 1.35%

Spanish 10Yr yield up 1bps to 1.52%

US 10Yr yield up 3bps to 1.76%

Dollar Index down 0.17% to 93.79

German 10Yr yield up 4bps to 0.15%

MSCI Asia Pacific up 1% to 127.9

Nikkei 225 up 1.1% to 15928.8

Hang Seng up 0.3% to 20504.4

Kospi up 0.6% to 1981.3

Shanghai Composite down 0.3% to 3023.6

Gold spot up 0.2% to $1260.4/oz

Brent Futures up 1.4% to $43.4/bbl

WTI Futures up 0.6% to $40.62/bbl

Top Global News

‘Brexit’ Akin to Unilateral Disarmament, David Miliband to Say: Miliband will be speaking in London today

Nomura Said Planning to Exit European Equities, Cut 1,000 Jobs

Italy Forms $5.7b Fund to Shake Off Doubts in Banks: Atlante fund managed by Quaestio Capital investment firm

Spain Heading for Fresh Elections as Podemos Targets Socialists: lawmakers must choose leader by May 2 or new vote triggered

Roche Sees Superior Efficacy of Ocrelizumab in Relapsing MS: comments in emailed statement

Vivendi to Acquire Equity Interest in Fnac of About 15%: move is part of strategic partnership for cultural activities

Shell CEO Van Beurden Sees Iran as Investment Opportunity: Van Beurden speaks to reporters in Perth, Australia

AB InBev Offers Remedies to EU in Review of SABMiller Deal: EU sets new deadline of May 24 to rule on beer deal after getting commitments offer

Looking at regional markets, we start in Asia where equities shrugged off Wall St.’s weak lead with the region’s bourses mostly positive on short-covering. Nikkei 225 (+1.2%) recovered from opening losses to trade higher by over 1% as participants found a reprieve from a pause in JPY strength and took the opportunity to bargain hunt following yesterday’s declines. ASX 200 (+0.6%) traded higher led by financials and materials with the latter underpinned by strength across commodities in which iron ore rose nearly 5%. Elsewhere, Chinese markets saw mixed trade after the PBoC upped its liquidity injections and China released a negative list for investment which included steel and coal as off-limit sectors. 10yr JGBs traded marginally higher despite heightened risk appetite in Japan with today’s 10yr inflation-linked auction printing a higher than prior b/c, while yields in the super-long-end were also under mild pressure with the 30yr yield falling to a fresh record low.

Top Asia News

CIC, Ormat, Malakoff Said to Weigh Bids for Chevron Asian Assets: Bids due end-May for $3b of Asian geothermal fields

Chinese Debtors Have Never Faced Such Hard Times Paying Interest: Oper. profit double interest costs, down from ratio of six

Strengthening Yen Leaves Kuroda Facing More Radical Options: Credit Agricole joins those forecasting action in April

Indian Bankers Said to Be Wary of Solar as SunEdison Totters: Financial risks seen from rock-bottom Indian solar power rates

An air of caution swirls in European equities ahead of the forthcoming slew of US earnings as the Eurostoxx oscillated between gains and losses, with luxury names lower this morning amid soft earnings from large cap LVMH. However, EU bourses pared the entirety of their earlier declines amid the upside in the commodities complex supporting miners with Anglo American also driving higher on the back of higher diamond sales from their De Beers unit. Elsewhere, pull back in European stocks saw Bunds trip below yesterday’s low situated at 163.74, with the long end weighed given the long-duration supply, including a Buxl auction and the 20 and 50 dual tranche from France.

European Top News

Asos 1H Retail Gross Margin Beats, On Track to Achieve Outlook: 1H retail gross margin up 40bps, est. up 7bps

Lonmin CFO to Step Down, Sucessor Search at an Advanced Stage: Simon Scott to stand down as CFO and director

Mercedes Sales Climb Twice as Fast as BMW in 1Q: Daimler is closing in on goal of overtaking German rival

EPH Utility Plans Infrastructure Unit IPO in Prague, London: Czech utility expects to complete unit offering this quarter

Al-Thani Private Bank KBL to Buy Dutch Firm From BNP Paribas: KBL plans Insinger de Beaufort & Theodoor Gilissen combination

BayWa in Talks With U.K., European Investors to Sell Solar Farms: BayWa still to short-list candidates

In FX, stronger than forecast UK inflation has given GBP a fresh bid, with Cable having extended through a series of resistance levels, but topping out at 1.4320 as yet (last week’s high). EUR/GBP was knocked back under .8000, and with EUR/USD holding 1.1465-70 resistance in another test higher (traded 1.1464), the pullback has added some fresh momentum in the cross rate. The USD as a whole has lost yet more ground on the day, with the commodity rates all benefitting. NZD has traded to within a few ticks of .6900 again, while AUD/USD has tipped .7670. USD/CAD has fallen to just shy of 1.2850, matching the recent lows, but a clean break below here required to suggest a deeper move towards 1.2500-1.2600. The USD index now not too far off stronger support levels in the mid 92.00’s, with the more cautious approach by the Fed still keeping the greenback offered. USD/JPY is digging in a little though, but 107.60-108.40-45 still containing trade here for now — stocks keenly watched. Swedish inflation also stronger than expected, and giving the SEK a fresh bid — long term highs vs the USD matched just under 8.0300.

In commodities, energy prices enter the US session in positive territory with WTI holding above the USD 40/bbl handle. In terms of energy specific newsflow, this has been somewhat light this morning but according to a spokesman of KNPC, Kuwait has stopped exporting oil from all ports due to bad weather. Elsewhere gold rose in European trade remain around 3-week highs amid the softness in the USD-index, while iron ore extended on its advances alongside strength in steel prices, which posted 10-month highs.

Bulletin Headline Summary from RanSquawk and Bloomberg

European equities pare their opening losses while luxury names fall on the back of soft LVMH sales.

UK CPI drives GBP higher, with GBP/USD breaking above the 1.4300 level with gains further exacerbated by the weaker greenback.

Looking ahead, highlights include US Import Price Index, API Crude Oil Inventories and Fed’s Harker.

Treasuries lower in overnight trading as global equity markets, WTI crude oil and metals rally; week’s auctions begin with $24b 3Y notes, WI 0.86%; sold at 1.039% in March, was second straight 3Y auction to tail after all but one of previous 19 stopped through.

Alcoa Inc. cut forecasts for its largest manufacturing unit as the biggest U.S. aluminum producer prepares to split itself in two amid slumping profit, 1Q net income fell 92 percent to $16 million

Italian officials and bank executives agreed to create a multibillion-euro fund to help troubled lenders raise capital and offload bad loans, as the nation tries to assuage investor jitters. The new vehicle will be named Atlante (Harvey: will not work)

Nomura plans to shut down its European equity operations and cut 1,000 jobs as it reduces costs after years of failing to become profitable overseas, a person with knowledge of the matter said

At its annual investor conference in San Francisco in May 2014, with oil trading at $102 a barrel, Wells Fargo boasted that in just two years it had almost doubled its energy exposure and seized the title of Wall Street’s top oil and gas banker. The timing couldn’t have been worse

U.K. inflation accelerated to a 15-month high in March as an early Easter boosted air fares and clothing prices increased. Consumer prices rose 0.5% from a year earlier, the fastest pace since December 2014

Just as monetary easing is pushing Chinese bond yields to record lows, firms generated just enough operating profit to cover the interest expenses on their debt twice, down from almost six times in 2010

The Bank of Japan is reducing the share of funds financial institutions keep at the BOJ that will be subject to the new negative interest rate policy

Brazilian lawmakers pushed President Dilma Rousseff a step closer to impeachment after a committee in the lower house voted for her ouster in the first formal test of sentiment in Congress

Sovereign 10Y bond yields mostly higher; European, Asian equity markets higher; U.S. equity-index futures rise. WTI crude oil, gold and copper rally

DB’s Jim Reid wraps up the overnight summary

yesterday saw the starting whistle blown for Q1 with Alcoa unofficially getting things started after the closing bell. The numbers were fairly mixed. While earnings came in above consensus, a miss on revenues and a downgrade to full year aluminium demand saw shares down 3% or so in extended trading. Prior to this it had felt like markets were in a bit of a wait and see mode with little else to particularly drive sentiment. That said, momentum certainly faded as the US session in particular wore on with the S&P 500 eventually finishing last night with a -0.27% loss. This came after performance for most European bourses had been relatively positive (Stoxx 600 +0.30%, DAX +0.63%) and after further gains for Oil, with WTI rising +1.61% and closing back above $40/bbl again.

This morning in Asia and outside of a slight reversal for markets in China, the tone is relatively positive with Japan in particularly leading the way. The Nikkei is currently +1.23% and gaining as the session wears on, with the move coinciding for a softer day for the Yen (-0.26%) which is coming off the back of seven consecutive days of gains. The Hang Seng (+0.20%), Kospi (+0.44%) and ASX (+0.68%) are all following suit, while credit markets are generally posting modest gains. It’s China which is the relative underperformer however with the Shanghai Comp -0.65%. Despite Alcoa shares dropping last night, US equity index futures are currently flashing green on our screens.

The modest weakening for the Yen this morning has seen it hover just north of 108 meanwhile. Yesterday, DB’s George Saravelos published a note highlighting that Japan’s biggest problem with the recent Yen rally is that it is justified by fundamentals, with the bulk of metrics suggesting that USDJPY is still expensive or just approaching fair value. George highlighted that taking the average of three of DB’s FX valuation models, he and his team come up with a USD/JPY equilibrium rate of 97, more than 10% below current levels. There are two implications of this. Firstly, it is unlikely that Japanese FX intervention is going to be very successful in pushing USD/JPY significantly higher – there is no misalignment to correct in the first place. The very public commitments the G20 have made against competitive devaluations make large-scale, sustained intervention even less likely. Second, unless the BoJ can convince the market that it is able to bring inflation expectations back up (and real yields down) it is unclear what can be done to reverse the yen rally. On the one hand, the market is likely to challenge the reflationary impact of further rate cuts into negative territory. On the other hand, an expansion of JGB purchases seems more straightforward, but it is not clear how many more marginal JGB holders are left to squeeze out into other (foreign) assets.

Back to yesterday. One notable snippet of news was out of Italy with the announcement from PM Renzi that following drawn out talks, Italian officials and financial institutions have agreed on the terms for a €5bn bailout fund aimed at shoring up the weaker banks through raising capital and unloading bad loans. According to the FT the deal apparently defied expectations that it could have been softened at the last moment, while the terms of the deal show that in return for providing private funds, the Italian government has agreed to align Italy’s laws around bankruptcy (previously seen as being behind the times) with the rest of Europe. Unsurprisingly it was Italian equities which were the relative outperformer yesterday in anticipation of the news with the FTSE MIB gaining +1.25%, driven by big moves higher for the Banks with the likes of Banco Popolare and also Banca Monte dei Paschi gaining +10.30% and +9.78% respectively.

Staying in Europe, sovereign bond yield curves were generally a bit steeper by the close yesterday with 10y Bunds in particular back above 10bps in yield after moving nearly 2bps higher to 0.109%. With the shorter end of the curve dipping lower however, it was interesting to note that the average yield for all outstanding German Bunds fell to 0% yesterday for the first time in history. The Bundesbank once-a-day quoted rate (also known as the Umlaufrendite) had been testing that level for some time but notably failed to quite reach the historic level in April last year (when it got as low as 5bps) during the big rally across rates markets.

With regards to some of the macro, while there was a complete lack of economic data for investors to dig their teeth into, we did hear from the Dallas Fed President Kaplan who played down the possibility of a hike this month (which won’t come as a surprise) but highlighted that ‘it is worth in this environment being patient and basically being willing to be cautious and let events unfold’ before suggesting that he is open minded to the possibility of possible tightening at the June meeting. Kaplan also made mention to what is likely to be a soft Q1 GDP report for the US, indicating that this is ‘probably inconsistent with the job numbers’. Kaplan did however suggest that his forecasts have growth bouncing back in the next couple quarters.

END

ASIAN AFFAIRS

i)Late MONDAY night/ TUESDAY morning: Shanghai closed down 10.31 POINTS OR 0.34% (even with last hr rescue) / Hang Sang closed UP 63.63 OR 0.31%. The Nikkei closed UP 177.66 POINTS OR 1.13% . Australia’s all ordinaires CLOSED UP 0.89%. Chinese yuan (ONSHORE) closed UP at 6.4606. Oil ROSE to 40.66 dollars per barrel for WTI and 43.12 for Brent. Stocks in Europe ALL IN THE GREEN . Offshore yuan trades 6.4702 yuan to the dollar vs 6.4606 for onshore yuan. LAST WEEK:Japanese INDUSTRIAL PRODUCTION plunges the most in almost 5 years as negative interest rates ARE KILLING BUSINESS./JAPANESE TANKEN CONFIDENCE INDEX PLUMMETS/JAPAN HAS NEVER RECOVERED FROM THOSE BAD DATA RELEASES/TODAY THE USA/YEN CROSS REMAINS AT THE 108 CROSS SETTING OFF GLOBAL TENSIONS WHICH IN TURN IS CAUSING THE SPECIAL MEETING AT THE FED.

FIRST REPORT ON JAPAN SOUTH KOREA AND CHINA

a) JAPAN ISSUES

Our famous Mr Yen, Eisuke Sakakibara now says that Japan’s currency may strengthen to 100 yen to the dollar. He states that intervention will be fruitless. Although Japanese officials state that the 100 yen to the dollar is no problem for the Japanese economy it will surely wreck havoc on the rest of the world especially with the trillions of yen carry traders getting annihilated.

(courtesy zero hedge)

“Mr. Yen” Warns USDJPY May Hit 100 By Year-End

Having correctly predicting the yen’s advance beyond 115 and then 110 per dollar, former Japanese Finance Minister Eisuke Sakakibara now says Japan’s currency may strengthen to 100 by year-end.

As Bloomberg reports, having been in charge of currency intervention in Japan, Sakakibura was dubbed Mr. Yen for his ability to influence the exchange rate in the 1990s,seems to suggest – uinlike Suga overnight – that intervention is unlikely (or unlikley to be successful).

The yen has renewed its highs despite increased rhetoric from Japanese officials in the past week aimed at restraining its advance. Bank of Japan Governor Haruhiko Kuroda said Monday financial markets continue to be volatile, and he is watching the effect on the economy.

Chief Cabinet Secretary Yoshihide Suga reiterated the government is watching foreign-exchange movements “with vigilance,” and will take appropriate action if necessary. A weaker currency has been a linchpin of Prime Minister Shinzo Abe’s program to stoke a recovery and exit deflation.

A yen at 105 per dollar is “no problem” for Japan’s economy, the 75-year-old Sakakibara, who is currently a professor at Aoyama Gakuin University, said in a Bloomberg Television interview.

Any currency intervention can only be done with agreement from the U.S. and other counter parties, he said.

While noting that 105 would be “no problem” for Japan’s economy, we suspect theimplied drop in the S&P 500 to 1550 would be a problem for the world’s “economy”.

END

An extremely important paper where the former chief IMF economist Olivier Blanchard admits how the end game will be played out. He discusses that Japan already has 34% of all Japanese issuance of bonds and by next year they will approach 50%. He then states that there will be a scarcity of sellers which will force Japan to taper buying of bonds. This will then force yields higher and with that deflation will turn on a dime into hyperinflation

a must read…

(courtesy zero hedge)

Former IMF Chief Economist Admits Japan’s “Endgame” Scenario Is Now In Play

Back in October 2014, just after the BOJ drastically expanded its QE operation, we warned that the biggest risk facing the BOJ (and the ECB, and the Fed, and all other central banks actively soaking up securities from the open market) was a lack of monetizable supply. We cited Takuji Okubo, chief economist at Japan Macro Advisors in Tokyo, who said that at the scale of its current debt monetization, the BOJ could end up owning half of the JGB market by as early as in 2018. He added that “The BOJ is basically declaring that Japan will need to fix its long-term problems by 2018, or risk becoming a failed nation.”

Which is why 17 months ago we predicted that, contrary to expectations of even more QE from Kuroda, we said “the BOJ will not boost QE, and if anything will have no choice but to start tapering it down – just like the Fed did when its interventions created the current illiquidity in the US govt market – especially since liquidity in the Japanese government market is now non-existent and getting worse by the day.”

As part of our conclusion, we said we do not “expect the media to grasp the profound implications of this analysis not only for the BOJ but for all other central banks: we expect this to be summer of 2016’s business.”

Since then, the forecast has panned out largely as expected: both the ECB and BOJ, finding themselves collateral constrained, were forced to expand into other, even more unconventional methods of easing, whether it be NIRP in the case of the BOJ, or the outright purchases of corporate bonds as the ECB did a month ago.

* * *

Then, in September of 2015, the IMF realized the severity of what our forecast meant for Japan, and released a working paper with the non-pretentious title “Portfolio Rebalancing in Japan; Constraints and Implications for Quantitative Easing“, which however had momentous implications because it was a replica of what we had said a year earlier.

In the paper, the IMF said that the Bank of Japan may need to reduce the pace of its bond purchases in a few years due to a shortage of sellers. The paper predicted a world in which, just as we cautioned, “the BoJ may need to taper its JGB purchases in 2017 or 2018, given collateral needs of banks, asset-liability management constraints of insurers, and announced asset allocation targets of major pension funds… there is likely to be a “minimum” level of demand for JGBs from banks, pension funds, and insurance companies due to collateral needs, asset allocation targets, and asset-liability management (ALM) requirements. As such, the sustainability of the BoJ’s current pace of JGB purchases may become an issue.”

The paper’s shocking punchline was how Japan would survive this inevitable phase shift, or as we rhetorically asked, what happens when the regime shifts from the current buying phase to its inverse: The IMF response: “As this limit approaches and once the BoJ starts to exit, the market could move from a situation of shortage to one with excess supply. The term premium could jump depending on whether the BoJ shrinks its balance sheet and on the fiscal deficit over the medium term.

When considering that by 2018 the BOJ market will have become the world’s most illiquid (as the BOJ will hold 60% or more of all issues), the IMF’s final warning is that “such a change in market conditions could trigger the potential for abrupt jumps in yields.”

Or as we put last September, “at that moment the BOJ will finally lose control.”

We even timed it: “But before we get to the QE endgame, we first need to get the interim point: the one where first the markets and then the media realizes that the BOJ – the one central banks whose bank monetization is keeping the world’s asset levels afloat now that the ECB has admitted it is having “problems” finding sellers – will have no choice but to taper, with all the associated downstream effects on domestic and global asset prices.

It’s all downhill from there, and not just for Japan but all other “safe collateral” monetizing central banks, which explains the real reason the Fed is in a rush to hike: so it can at least engage in some more QE when every other central bank fails.

But there’s no rush: remember to give the market and the media the usual 6-9 month head start to grasp the significance of all of the above.

Sure enough, it took the market about 6 months to finally grasp that the BOJ is out of ammo: the result has been a dramatic surge in the Yen coupled with a plunge in the Nikkei, meanwhile Kuroda is left scratching his head what he can do in a world in which the G-20 have specifically prohibited him from easing and making the dollar stronger as that will lead to a return of China’s weak currency-driven, capital outflow crisis.

As for our other forecast from October 2014 in which we said “expect the media to grasp the profound implications of this analysis not only for the BOJ but for all other central banks: we expect this to be summer of 2016’s business” this too was quite prescient. Because while summer is just around the corner, earlier today the mainstream media, in this case the Telegraph’s Ambrose Evans-Pritchard, finally caught up with a piece titled: “Olivier Blanchard eyes ugly ‘end game’ for Japan on debt spiral.” In it he cites none other than the IMF’s former chief economist, Olivier Blanchard who left the IMF just at the time the IMF’s study from last September was made public.

The content of Pritchard’s piece should be familiar to anyone who has followed our musings on this topic for the past two years.

In it, he says that “Japan is heading for a full-blown solvency crisis as the country runs out of local investors and may ultimately be forced to inflate away its debt in a desperate end-game, one of the world’s most influential economists has warned.”

From the article:

Olivier Blanchard, former chief economist at the International Monetary Fund,said zero interest rates have disguised the underlying danger posed by Japan’s public debt, likely to reach 250pc of GDP this year and spiralling upwards on an unsustainable trajectory.

Prof Blanchard said the Japanese treasury will have to tap foreign funds to plug the gap and this will prove far more costly, threatening to bring the long-feared funding crisis to a head.

“If and when US hedge funds become the marginal Japanese debt, they are going to ask for a substantial spread,” he told the Telegraph, speaking at the Ambrosetti forum of world policy-makers on Lake Como.

Analysts say this would transform the country’s debt dynamics and kill the illusion of solvency, possibly in a sudden, non-linear fashion.

That moment in which the illusion dies, is precisely the phase shift which we descibed in September as the moment “market conditions could trigger the potential for abrupt jumps in yields.”

Said otherwise, from plummeting deflation Japan would be faced with soaring yields and hyperinflation as the last recourse buyer, the BOJ, is swept aside.

Prof Blanchard, now at the Peterson Institute in Washington, said the Bank of Japan will come under mounting political pressure to fund the budget directly, at which point the country risks lurching from deflation to an inflationary denouement.

“One day the BoJ may well get a call from the finance ministry saying please think about us – it is a life or death question – and keep rates at zero for a bit longer,” he said.

Pritchard here catches up to what we said in October of 2014, namely that the “BoJ is soaking up the entire budget deficit under Govenror Haruhiko Kuroda as he pursues quantitative easing a l’outrance.” Incidentally, this is the same Pritchard who several years ago was lauding Japan’s QE.

He next points out something we have also warned about for year: “the central bank owned 34.5pc of the Japanese government bond market as of February, and this is expected to reach 50pc by 2017.”

This is us circa last September.

What comes next is the scary part, the part we have been focusing on for years:

Prof Blanchard did not elaborate on the implications of Japan’s woes for the global financial system, but they would surely be dramatic and there are growing fears that this could happen within five years. Japan is still the world’s third largest economy by far. It is also the global laboratory for an ageing crisis that the rest of us will face to varying degrees.

Once markets begin to suspect that Tokyo is deliberately engineering an escape from its $10 trillion public debt trap by means of an inflationary ‘stealth default’, matters could spin out of control quickly.

It might lead to an abrupt reappraisal of sovereign debt risk in other parts of the world, especially in Europe with its own Japanese pathologies of low-growth and bad demographics. Roughly $7 trillion of debt is trading at negative yields worldwide, an accident waiting to happen for the bond market.

After Japan comes Europe:

Prof Blanchard said the risk for the eurozone is the election of populist “rogue governments” that let rip with spending in defiance of Brussels. “Investors would have serious thoughts about buying their sovereign bonds,” he said. The European Central Bank would be legally prohibited from activating its back-stop mechanism (OMT) to prevent yields soaring since these governments would not be in compliance with EU rules. “Some of them have very high debt and presumably would have to default,” he said.

Perhaps, or the ECB will simply unleash the first helicopter money if it can get over the loud German chorus of disagreement. Although once Europe launches Helicopter money, it will be promptly followed by the US as the global monetary devaluation round enters the final sprint. It is no coincidence that earlier today none other than Ben Bernanke admitted that “Helicopter Money May Be The Best Available Alternative.”

What shape the final stand of failed monetary policy takes, is irrelevant. What is relevant, is that for the first time, not only is the Japanese doomsday scenario finally in the mainstream press, but it is acknowledged by none other than one of the Keynesian luminaries AEP is so impressed by:

Prof Blanchard is one of the world’s top theoretical economists over the last quarter century and might have won the Nobel Prize by now if he had not been cajoled into IMF service by his fellow Frenchman, Dominique Straus-Kahn.

He transformed the IMF into a brain-trust of progressive ‘Keynesian’ thinking, much to the fury of Berlin. A leaked document from the German finance ministry said the institution should be renamed the ‘Inflation Maximizing Fund’.

Evans-Pritchard’s conclusion:

“Professor Blanchard has had the last laugh on that joke. Seven years after the Lehman crisis the eurozone is in outright deflation and yields on 10-year German Bunds are trading at an historic low 0.11pc. Touché.”

Actually let’s check back in another 7 years, because now that even one of the world’s “top theoretical economists” acknowledges that the endgame for trillions in debt ends in a hyperinflationary supernova, and not a deflationary black hole, all those years of sliding interest rates around the globe are about to be flipped on their head. At that point it will be the Germans who are laughing last.

Sadly, there will be nothing else to laugh about as the Keynesian “progressive thinkers” will have finally reached the inevitable and disastrous “end-game” of their failed religion.

END

b) CHINA ISSUES

China will still due to stealth devaluation despite the blasting from USA’s Lew.

Even though the yuan/yuan has been stable, take a look at how the yuan is behaving against its currency basket: falling!!

The Japanese yen is out of ammo to cause its currency to falter. The USA has made a decision to lower its currency (thus hurting the yen by causing it to rise as well as causing the Euro to rise) so as not to allow the devaluation of the yuan against it.

(courtesy zero hedge)

China’s Stealth Devaluation Continues Despite Lew Blasting “Unacceptable” FX Practices

“Intervention in foreign exchange markets in order to gain a competitive advantage is unacceptable,” proclaims US Treasury Secretary Jack Lew in a strongly worded statement today with regard America’s position in the global economy. That we note this comment is only relevant as, despite the apparent “stability” of the Chinese Yuan against the USD, relative to the 13-currency-basket with which China primarily trades, the Yuan has collapsed to 17-month lows – with JPY and EUR appearing to bear the brunt of the pain.

The US Dollar has traded within a relatively “stable” band against the offshore Yuanfor much of the last six weeks…

But when compared to the collapse of the Yuan “basket” – as PBOC devalued against the rest of the major trading partners – the ‘stealth’ devaluation is obvious…

Is it any wonder that JPY is surging – despite all of Kuroda’s best jawboning efforts?

As other countries gain greater voice in the international system, they also must accept greater responsibilities. A major one is to engage in responsible foreign exchange practices. Currency fluctuations are a normal and even desirable attribute of the global economy. When the values of currencies are allowed to move according to market forces, the global economy can better adapt to changes in relative economic performance among countries. What is unacceptable, however, is intervention in foreign exchange markets in order to gain a competitive advantage in trade or impede adjustments in the balance of payments.

Competitive devaluation represents a beggar-thy-neighbor fight for a shrinking global pie, not a pathway to stronger global growth.

Strong multilateral institutions such as the IMF and the G-20 are important vehicles for reinforcing norms against predatory currency practices and for mobilizing multilateral pressure against countries that engage in them. At the G-20 meeting in Shanghai this February, members not only committed to using all tools of policy—monetary, fiscal, and structural—to boost economic growth in a time of weak demand. They also committed to refrain from competitive devaluation and, for the first time, to consult on foreign exchange markets to avoid surprises that could threaten global financial stability.

So the question is – Is it ok to “devalue” your currency against other non-reserve-status currencies? As long as the veil of “stability” is maintained against The USD?

END

What a terrific article on the plight of China:

(courtesy David Stockman/ContraCorner)

The New Middle Kingdom Of Concrete And The Red Depression Ahead

No wonder the Red Ponzi consumed more cement during three years (2011-2013) than did the US during the entire twentieth century. Enabled by an endless $30 trillion flow of credit from its state controlled banking apparatus and its shadow banking affiliates, China went berserk building factories, warehouses, ports, office towers, malls, apartments, roads, airports, train stations, high speed railways, stadiums, monumental public buildings and much more.

If you want an analogy, 6.6 gigatons of cement is 14.5 trillion pounds. The Hoover dam used about 1.8 billion pounds of cement. So in 3 years China consumed enough cement to build the Hoover dam 8,000 times over—-160 of them for every state in the union!

Having spent the last ten days in China, I can well and truly say that the Middle Kingdom is back. But its leitmotif is the very opposite to the splendor of the Forbidden City.The Middle Kingdom has been reborn in towers of preformed concrete. They rise in their tens of thousands in every direction on the horizon. They are connected with ribbons of highways which are scalloped and molded to wind through the endless forest of concrete verticals. Some of them are occupied. Alot, not.

The “before” and “after” contrast of Shanghai’s famous Pudong waterfront is illustrative of the illusion.

The first picture below is from about 1990 at a time before Mr. Deng discovered the printing press in the basement of the People’s Bank of China and proclaimed that it is glorious to be rich; and that if you were 18 and still in full possession of your digital dexterity and visual acuity it was even more glorious to work 12 hours per day 6 days per week in an export factory for 35 cents per hour.

I don’t know if the first picture is accurate as to its exact vintage. But by all accounts the glitzy skyscrapers of today’s Pudong waterfront did ascend during the last 25 years from a rundown, dimly lit area of muddy streets on the east side of Huangpu River. The pictured area was apparently shunned by all except the most destitute of Mao’s proletariat.

But the second picture I can vouch for. It’s from my window at the Peninsula Hotel on the Bund which lies directly accross on the west side of the Huangpu River and was taken as I typed this post.

Today’s Pudong district does look spectacular—–presumably a 21st century rendition of the glory of the Qing, the Ming, the Soong, the Tang and the Han.

But to conclude that would be to be deceived.The apparent prosperity is not that of a sustainable economic miracle; its the front street of the greatest Potemkin Village in world history.

The heart of the matter is that output measured by Keynesian GDP accounting—-especially China’s blatantly massaged variety— isn’t sustainable wealth if it is not rooted in real savings, efficient capital allocation and future productivity growth. Nor does construction and investment which does not earn back its cost of capital over time contribute to the accumulation of real wealth.

Needless to say, China’s construction and “investment” binge manifestly does not meet these criteria in the slightest. It was funded with credit manufactured by state controlled banks and their shadow affiliates, not real savings. It was driven by state initiated growth plans and GDP targets. These were cascaded from the top down to the province, county and local government levels—–an economic process which is the opposite of entrepreneurial at-risk assessments of future market based demand and profits.

China’s own GDP statistics are the smoking gun. During the last 15 years fixed asset investment—–in private business, state companies, households and the “public sector” combined—–has averaged 50% of GDP. That’s per se crazy.

Even in the heyday of its 1960s and 1970s boom, Japan’s fixed asset investment never reached more than 30% of GDP. Moreover, even that was not sustained year in and year out (they had three recessions), and Japan had at least a semblance of market pricing and capital allocation—unlike China’s virtual command and control economy.

The reason that Wall Street analysts and fellow-traveling Keynesian economists miss the latter point entirely is because China’s state-driven economy works through credit allocation rather than by tonnage toting commissars. The gosplan is implemented by the banking system and, increasingly, through China’s mushrooming and metastasizing shadow banking sector. The latter amounts to trillions of credit potted in entities which have sprung up to evade the belated growth controls that the regulators have imposed on the formal banking system.

For example, Beijing tried to cool down the residential real estate boom by requiring 30% down payments on first mortgages and by virtually eliminating mortgage finance on second homes and investment properties. So between 2013 and the present more than 2,500 on-line peer-to-peer lending outfits (P2P) materialized—-mostly funded or sponsored by the banking system—– and these entities have advanced more than $2 trillion of new credit.

The overwhelming share went into meeting “downpayments” and other real estate speculations. On the one hand, that reignited the real estate bubble——especially in the Tier I cities were prices have risen by 20% to 60% during the last year. At the same time, this P2P eruption in the shadow banking system has encouraged the construction of even more excess housing stock in an economy that already has upwards of 70 million empty units.

In short, China has become a credit-driven economic madhouse. The 50% of GDP attributable to fixed asset investment actually constitutes the most spectacular spree of malinvestment and waste in recorded history. It is the footprint of a future depression, not evidence of sustainable growth and prosperity.

Consider a boundary case analogy. With enough fiat credit during the last three years, the US could have built 160 Hoover dams on dry land in each state. That would have elicited one hellacious boom in the jobs market, gravel pits, cement truck assembly plants, pipe and tube mills, architectural and engineering offices etc. The profits and wages from that dam building boom, in turn, would have generated a secondary cascade of even more phony “growth”.