Good evening Ladies and Gentlemen:

Gold: $1,233.60 up $0.50 (comex closing time)

Silver 16.25 down 6 cents

In the access market 5:15 pm

Gold $1233.00

silver: 16.24

I hope you all watched a very important video where Rob Kirby and Greg Hunter discuss the purchase of the Chinese of the SWIFT system. Now the Chinese can combine their CIP with the new SWIFT system and bypass the USA altogether. Rob Kirby describes this as a knife into the heart of the USA. (CIP transfers money/Swift provides the information packet. Up until now you had to settle in dollars as there was no way around the SWIFT system.)

Let us have a look at the data for today

.

At the gold comex today, we had a fair delivery day, registering 35 notices for 3500 ounces for gold,and for silver we had 18 notices for 90,000 oz for the non active April delivery month.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 218.990 tonnes for a loss of 84 tonnes over that period.

In silver, the open interest rose by another 1447 contracts UP to 194,076 as the silver price was UP 14 cents with respect to FRIDAY’s bullish trading. In ounces, the OI is still represented by .970 billion oz or 138% of annual global silver production (ex Russia ex China). We are now at multi year highs in OI with respect to silver

In silver we had 18 notices served upon for 90,000 oz.

In gold, the total comex gold OI fell BY A rather small 2675 contracts DOWN to 494,212 contracts DESPITE THE FACT THAT the price of gold was UP $8.10 with FRIDAY’S TRADING(at comex closing).

We had another huge change in gold inventory at the GLD,this time a deposit of 6.38 tonnes thus the inventory rests tonight at 812.46 tonnes. (Yesterday we also had 3.26 tonnes removed) The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. Our 670 tonnes of rock bottom inventory in GLD gold has been broken. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold, after they deplete the GLD will be the FRBNY and the comex. In silver,we had another withdrawal of .951 million oz of silver despite silver’s rise. No doubt that this silver was used in the fruitless attempt at knocking down the silver price. Thus the Inventory rests at 333.297 million oz.

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver RISE by 1447 contracts UP to 194,076 as the price of silver was UP 14 cents with FRIDAY’S trading. The gold open interest fell by small 2675 contracts.Somebody big is standing FOR SILVER and surrounding the comex with paper longs ready to ponce once called upon to take out physical silver.

(report Harvey)

2 a) Gold trading overnight, Goldcore

(Mark OByrne)

3. ASIAN AFFAIRS

i)Late SUNDAY night/ MONDAY morning: Shanghai closed DOWN 44.46 POINTS OR 1.44% / Hang Sang closed DOWN 154.97 OR 0.73%. The Nikkei closed DOWN 572.08 POINTS OR 3.40% . Australia’s all ordinaires CLOSED DOWN 0.40%. Chinese yuan (ONSHORE) closed DOWN at 6.4777. Oil FELL to 38.92 dollars per barrel for WTI and 41.65for Brent. Stocks in Europe ALL IN THE RED . Offshore yuan trades 6.4888 yuan to the dollar vs 6.4777 for onshore yuan.

REPORT ON JAPAN SOUTH KOREA AND CHINA

a) REPORT ON JAPAN

ii)Just in time inventory is now killing the Japanese economy as everything grinds to a halt due to critical supply chains hurt by the earthquake:

( zero hedge)

b) REPORT ON CHINA

iii)China’s GDP just does not add up!

( zero hedge)

4.EUROPEAN AFFAIRS

i) We now have 3 countries were we are witnessing negative mortgage rates:

( zero hedge)

ii)Buba’s Thiel warns against the abolishment of cash: and criminalizing cash hoarind is out of line with one’s freedom:

5.Global issues

With the news of no deal in the oil patch: the Cdn loonies plunges by a considerable .01418 or 1.11%

( zero hedge)

end

6.EMERGING MARKETS

The impeachment process begins in Brazil:

( zero hedge)

OIL MARKETS

i)Late Friday night: Saudi Prince announces that there will be no deal with Iran

( zero hedge)

ii)Saturday morning: Iran pulls out of the DOHA meeting altogether

iii)Sunday afternoon: is there a deal or isn’t there?

iv)Sunday afternoon: is there a deal or isn’t there?

v) No deal Sunday night: Oil futures crash by the most in 7 months/stocks also tumble!

vi)Unbelievable oil soars 8% off its lows and erases the entire post DOHA drop

7.PHYSICAL MARKETS

i)NY POST picks up on the DB confession: where are the rest of the news organizations?

( post/GATA

ii)The following is self explanatory: what the Deutsche bank’s confession means for gold and silver investors.

From my perspective, I want the emails between them and also BAFIN”s

( Chris Powell/GATA)

iii)Jim Rickards is stating that gold is haunting our monetary system as it is the only true form of money

( zero hedge)

iv)Two big billion dollar lawsuits are filed in Ontario following Deutsche bank’s admission of gold and silver rigging;

( zero hedge)

v)The gold and silver scam is really made up of two parts:

a) the fraudulent fix where the crooks lower the price on the morning and afternoon fix

b) the lending and selling of non existent gold into the market.

the latter is far worse and I am sure we will get emails on both:

( John Rubino/DollarCollapse.com)

vi)China has been buying gold by the bucketful to support RMB internationalization:

( Koos Jansen)

vii)Kyle Bass states that negative interest rates in the real world do not make sense

8.USA STORIES WHICH WILL INFLUENCE THE PRICE OF GOLD/SILVER:

i)Morgan Stanley relies almost entirely on marginal trading revenue and its important wealth management unit. They disappointed the street with trading revenue down 40% and profits down more than 50%

( zero hedge)

ii)Over the weekend we saw the Saudi threat to dump all of its treasuries if it is deemed that they had a role in the Sept 11 attack: There are 28 pages redacted. The bill wants those 28 pages in the clear;

( zero hedge)

iii)Two weeks ago we brought you the story that United Health will back out of providing policies next year in Arkansas and in Georgia. Today you can two more states to the list: Michigan and Oklahoma

Let us head over to the comex:

The total gold comex open interest FELL SLIGHTLY to an OI level of 494,212 for a loss of 2675 contracts DESPITE THE FACT THAT the price of gold UP $8.10 with respect tO FRIDAY’S TRADING. We are now entering the active delivery month of April. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month or for that matter an inactive month, and 2) a continual drop in the amount of gold standing in an active month. We certainly witnessed both parts today . In the front month of April we lost 109 contracts from 2307 contracts down to 2198. We had 91 notices filed ON FRIDAY so we LOST 18 CONTRACTS or an additional 1800 gold ounces will NOT stand for delivery. The next non active contract month of May saw its OI RISE by 170 contracts UP to 2934. The next big active gold contract is June and here the OI FELL by 5,020 contracts DOWN to 366,827. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was POOR at 173,030 . The confirmed volume YESTERDAY (which includes the volume during regular business hours + access market sales the previous day was POOR at 127,597 contracts. The comex is not in backwardation.

Today we had 35 notices filed for 3500 oz in gold.

April contract month:

INITIAL standings for APRIL

April 18/2016

April 18/2016

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil | 64.30 oz (Manfra)

2 kilobars |

| Deposits to the Dealer Inventory in oz | nil

|

| Deposits to the Customer Inventory, in oz | nil

|

| No of oz served (contracts) today | 35 contracts 3500 oz) |

| No of oz to be served (notices) | 2163 contracts 216,300 oz/ |

| Total monthly oz gold served (contracts) so far this month | 2317 contracts (231,700 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 103,123.5 oz |

Today we had 0 dealer deposit

Total dealer deposits; NIL oz

Today we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

Today we had 0 customer deposit

Total customer deposits: nil oz

Today we had 1 customer withdrawal:

i) Out of Manfra: 64.30 oz

Today we had 1 adjustment: JPM

We had 201.489 oz adjusted out of the dealer and this landed in the customer account of JPMorgan

APRIL INITIAL standings

/April 18/2016:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 653,507.47 oz

CNT, JPM, Scotia . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil

|

| No of oz served today (contracts) | 18 contracts

90,000 oz |

| No of oz to be served (notices) | 6 contracts)(30,000 oz) |

| Total monthly oz silver served (contracts) | 189 contracts (945,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,100,499.2 oz |

today we had 0 deposits into the dealer account

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil

we had 0 customer deposits:

Total customer deposits: 0 oz.

We had 3 customer withdrawals

i) Out of CNT: 25,332.39 oz

ii) Out of JPMorgan: 599,999.700 oz

iii) Out of Scotia: 28,175.360 oz

:

total customer withdrawals: 653.507.47 oz

we had 0 adjustments

APRIL 8/no changes in tonnage of gold/rests tonight at 819.60 tonnes

APRIL 7/ a huge deposit of 4.17 tonnes of “paper” gold was added to our GLD/Inventory rests tonight at 819.60 tonnes

APRIL 6/a withdrawal of .29 tonnes of gold and probably this was to pay for fees for the custodian and insurance/inventory rests at 815.43 tones

April 5/ a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 815.72 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

April 18.2016: inventory rests at 812.46 tonnes

end

And now your overnight trading in gold, MONDAY MORNING and also physical stories that may interest you:

By Mark O’Byrne

By Mark O’Byrne

Marc Faber: “Messiah” Central Banks Helicopter Money Printing “Will Not End Well”

Marc Faber has warned that a new financial crisis is coming and will be worse than the 2008 one and told Bloomberg TV that the “messiah” central banks “helicopter money ” policies “will not end well.”

Marc Faber

Faber warns that ultimately “you cannot grow an economy by just throwing money at people” and that “QE for the people” will be like “throwing gasoline on a fire.”

Faber is entertaining, has a good chuckle at the central banks and IMF’s monetary policies and laughs at the idiocy of the IMF’s recent counterfactual statement when Lagarde said the world economy would be worse off without negative interest rates:

… they will always say, if we hadn’t done this and hadn’t done that, it would be much worse. They have no proof for this assertion. In my view, it would have been better to let the crisis, already the first one in 2000, run its course and prevent the colossal credit bubble that was built up that then led to an even bigger crisis, and now they’re doing the same mistake.

According to Faber, credit as a percent of the global economy is up “very strongly” since 2007.

“[M]ost of the credit is now for transfer payments, and that is very negative for long term structural economic growth because it allows, actually, the government to become bigger and bigger and to have more regulations,” Faber said. “And I can tell you, I’m in the financial sector and I talk to people in the financial sector. Half the time is nowadays consumed with filling out forms by regulators.”

The financial crises in 2000 and 2008 would have been better if central banks hadn’t intervened, Faber said. He warns against the upcoming “helicopter money” policies:

“… the magicians at central banks, they always come out with a new trick and these negative interest rates that we have today, this is for the first time in recorded human history from the times of Babylon up to today that we have negative interest rates, and it’s not going to end well. That, I can tell you. But the sequence of how it will not end well, I’m not so sure. But they still have a lot of ammunition. What they can do is helicopter money. In other words, they can send you and Mr. Bloomberg and me and everybody, say a check for $10,000, and that is like throwing gasoline into a fire…. will it help the economy? That is the question. It won’t help in the long run. You cannot grow an economy by just throwing money at people.”

“… the less policies, the better it would be. We all learned at school that the free market and the capitalistic system is the best allocator of resources, and now what we have is the worst allocation of resources because it’s the government that tells you how these resources are allocated and they continuously expand their interventions, and I can tell you, I started to work in 1970. In the 70’s and early 1980’s, central banks actually never came up in discussions. They have now become like the messiah, and everybody watches what the central banks do and in the end, in my view, they will have, from a long term perspective, no impact whatsoever. Now can they move markets short term? Yes, but maybe not in the direction they want to.”

Faber recently told GoldCore in a webinar how he will “never sell his gold”, he buys “more every month” and believes owning gold in vaults in Singapore “is safest.”

Faber’s interview with Bloomberg (recorded 18/03/16) can be watched here

Faber’s interview with GoldCore and storing gold in Singapore can be watched here

Gold Prices (LBMA)

18 April: USD 1,240.30, EUR 1,101.04 and GBP 874.96 per ounce

15 April: USD 1,229.75, EUR 1,092.16 and GBP 867.46 per ounce

14 April: USD 1,240.30, EUR 1,101.04 and GBP 874.96 per ounce

13 April: USD 1,245.75, EUR 1,100.37 and GBP 875.33 per ounce

12 April: USD 1,259.20, EUR 1,102.15 and GBP 880.18 per ounce

Silver Prices (LBMA)

18 April: USD 16.20, EUR 14.33 and GBP 11.41 per ounce

15 April: USD 16.17, EUR 14.33 and GBP 11.40 per ounce

14 April: USD 16.13, EUR 14.32 and GBP 11.39 per ounce

13 April: USD 15.98, EUR 14.14 and GBP 11.21 per ounce

12 April: USD 15.96, EUR 13.98 and GBP 11.15 per ounce

Gold News and Commentary

Gold Advances on Haven Demand as Oil, Shares Retreat After Doha (Bloomberg)

Safe-haven bids buoy gold as oil slides on failure to freeze output (Reuters)

Asian shares drop, crude tumbles after Doha deal fails (Reuters)

Doha oil-freeze pact fails as Saudis insist that Iran participate (Marketwatch)

Funds Are Betting the Gold Rally Isn’t Over Yet (Bloomberg)

Silver overtakes gold as best precious metal – Up 17% YTD (Mineweb via Bloomberg)

Silver Hasn’t Flashed This “Buy” Signal in Almost a Decade (Casey Research)

“Monetary Bankruptcy, Groupthink & Hubris of Central Banks (Price of Everything)

Wishes Aside, Gold Is Going To Fly (Zero Hedge)

Gold “Is Not Overpriced Enough” – Dizard (FT)

Read More Here

Knowledge Is Power. Read Our Most Popular Guides in Recent Months

END

NY POST picks up on the DB confession: where are the rest of the news organizations?

(courtesy post/GATA

NY Post picks up on Deutsche’s confession but where are other news organizations?

Submitted by cpowell on Sun, 2016-04-17 20:25. Section: Daily Dispatches

4:28p ET Sunday, April 17, 2016

Dear Friend of GATA and Gold:

While the New York Post yesterday took note of Deutsche Bank’s confession to gold and silver market manipulation and its pledge to incriminate other banks — see the report appended — as far as your secretary/treasurer can determine, only Reuters and Bloomberg News, among mainstream financial news organizations, have yet reported the story, not counting the predictably snarky and beside-the-point commentary Friday in the Financial Times by its columnist John Dizard:

http://www.gata.org/node/16385

GATA has alerted most major Western financial news organizations to the Deutsche Bank story, though they were almost certainly fully aware of it already.

While Deutsche Bank’s confession makes gold and silver market rigging impossible to deny, financial news organizations remain willing to suppress the story as they have been doing for years, lest they aggravate their advertisers and governments. So while the struggle is slowly breaking our way, it very much continues, with financial news organizations and gold and silver mining companies bearing much responsibility for the injustice they won’t acknowledge.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Investors Get the Gold off of Banks’ Precious Metals Manipulation

By Michael Gray

New York Post

Saturday, April 16, 2016

http://nypost.com/2016/04/16/investors-make-golf-off-banks-manipulation-…

For many years, precious metal commodity investors have screamed over certain price movements.

Then came the convictions and penalties for the banks involved in the Libor rigging scandal, which gave the gold and silver traders some ammo for their own challenge.

In 2014 these precious metal future traders sued a group of banks including Deutsche Bank, HSBC, Scotiabank, and UBS, alleging in a number of civil suits that they unlawfully manipulated the price of gold and silver and their derivatives.

Investors accused the banks of abusing their power as three of the world’s largest silver and gold bullion banks by dictating the price of the precious metals through a secret, once-a-day meeting known as the Silver Fix and Gold Fix.

No one involved thought the case had much of a chance — despite getting class-action status last year.

Yet last week Deutsche Bank agreed to settle US litigation over the allegations that it illegally conspired with others to fix precious metal prices at the expense of investors, according to a court filing.

Although terms were not disclosed, Deutsche will include a monetary payment to the plaintiffs, a letter filed in Manhattan federal court by lawyers for the investors said.

Deutsche has signed a binding settlement term sheet and is negotiating a formal settlement agreement to be submitted for approval by Manhattan federal Judge Valerie Caproni, who oversees the litigation.

A Deutsche spokeswoman declined to comment. Lawyers for the investors did not respond to requests for comment.

According to the lawsuit, the defendants distorted prices on the roughly $30 billion of silver and silver financial instruments traded annually, violating US antitrust law. Deutsche is also cooperating with the investor group to release further information regarding correspondences with other banks on the fix.

Spokesmen for HSBC and Scotiabank declined to comment, saying they could not discuss pending litigation. A spokeswoman for UBS did not respond to requests for comment.

end

The following is self explanatory: what the Deutsche bank’s confession means for gold and silver investors.

From my perspective, I want the emails between them and also BAFIN”s

(courtesy Chris Powell/GATA)

What does Deutsche Bank’s confession mean for gold and silver investors?

Submitted by cpowell on Mon, 2016-04-18 01:55. Section: Daily Dispatches

For the time being, probably just a lot more litigation.

* * *

10:14p ET Sunday, April 17, 2016

Dear Friend of GATA and Gold:

What do Deutsche Bank’s confession to gold and silver market rigging and its pledge to incriminate other bullion banks mean?

Almost certainly they mean more litigation on top of the federal class-action lawsuit in New York that prompted the confession and pledge. Beyond that it’s anyone’s guess.

Of course gold traders, investors, and gold and silver mining companies and their investors are wondering what’s in it for them. That’s hard to say.

Ordinarily in a successful class-action lawsuit the court devises remediation that is available to everyone affected by the misconduct at issue in the suit — available not just to the plaintiffs named in the suit but to everyone similarly situated, everyone damaged by the misconduct. Once the court settles on such remediation, its availability is publicized to potential members of the class and they are invited to register with the court so they may be paid. So no one has to become a plaintiff in the suit to receive damages.

.But the focus of the Deutsche Bank class action seems to be narrow; it involves those who traded gold and silver on exchanges like the New York Commodities Exchange. It does not seem to cover trading and valuations that took place outside such exchanges, though of course other gold and silver transactions and the trading of the shares of gold and silver mining companies well may have been heavily influenced by the trading covered in the lawsuit.

For example, shareholders who were wiped out by the bankruptcy of Allied Nevada Gold Corp. a year ago have to be wondering whether the gold and silver market manipulation to which Deutsche Bank has admitted and in which the bank’s associates also may have been involved harmed their investment and entitles them to damages. Indeed, shareholders of anygold or silver mining company must wonder whether Deutsche Bank and the other banks should be liable to them for damages as well.

Those concerns seem to go beyond the scope of the current class-action lawsuit. But once the court in that lawsuit puts substantial evidence on the record or makes a formal finding, all sorts of gold and silver investors and mining companies may do well to engage their own legal counsel to explore their options.

(If only gold and silver mining companies cared about the rigging of the markets for their products, or even understood the true nature of their products as money. If any mining company has even noted the development with Deutsche Bank, there is as yet no evidence of it.)

Deutsche Bank may not be culpable enough to be obliged to make whole every gold and silver investor and mining company in the world, but if enough other big banks are incriminated, they may create a target rich enough to invite many other lawsuits, individual and class-action.

Of course the bigger issue for GATA is whether the class-action suit against Deutsche Bank and the other banks alleged to have manipulated the gold and silver markets will expose the intervention of central banks, directly or through intermediaries. That is, for example, were Deutsche Bank and the other accused banks ever trading on behalf of central banks and front-running those central bank trades?

For reprehensible and illegal as it is, market rigging by big traders is not so unusual and tyrannical as surreptitious trading by central banks. For the world’s sake, the latter sort of market rigging needs far more exposure.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Jim Rickards is stating that gold is haunting our monetary system as it is the only true form of money

(courtesy zero hedge)

Jim Rickards: Gold is the spectre haunting our monetary system

Submitted by cpowell on Sun, 2016-04-17 23:10. Section: Daily Dispatches

7:10p ET Sunday, April 17, 2016

Dear Friend of GATA and Gold:

The ubiquitous Jim Rickards has broken into the Telegraph and London with an essay explaining why gold just won’t go away and why various nations have an interest in continuing to recognize it as the best sort of money even as others are determined to stamp it out. Rickards’ essay is headlined “Gold Is the Spectre Haunting Our Monetary System” and it’s posted at the Telegraph here:

http://www.telegraph.co.uk/business/2016/04/17/gold-is-the-spectre-haunt…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Two big billion dollar lawsuits are filed in Ontario following Deutsche bank’s admission of gold and silver rigging;

(courtesy zero hedge)

Billion Dollar Lawsuits Filed Following Deutsche Bank’s Admission Of Gold, Silver Rigging

Overnight, two class action lawsuits seeking $1 billion in damages on behalf of Canadian gold and silver investors were launched in the Ontario Superior Court of Justice.

The first class action alleges that the defendants, including The Bank of Nova Scotia, conspired to manipulate prices in the silver market under the guise of the benchmark fixing process, known as the London Silver Fixing, for a fifteen-year period.

More from the suit:

It is further alleged that the defendants manipulated the bid-ask spreads of silver market instruments throughout the trading day in order to enhance their profits at the expense of the class. This alleged conduct affected not only those investors who bought and sold physical silver, but those who bought and sold silver-related financial instruments.

Law enforcement and regulatory authorities in the United States, Switzerland, and the United Kingdom have active investigations into the defendants’ conduct in the precious metals market.

The case is on behalf of all persons in Canada who, between January 1, 1999 and August 14, 2014, transacted in a silver market instrument either directly or indirectly, including investors who participated in an investment or equity fund, mutual fund, hedge fund, pension fund or any other investment vehicle that transacted in a silver market instrument.

A copy of the Notice of Action can be found at sotosllp.com. Potential class members can register on the website to obtain more information as the case progresses.

The plaintiffs and the proposed national class are being represented by a national team of lawyers from Sotos LLP (www.sotosllp.com), Koskie Minsky LLP (www.kmlaw.ca) and Camp Fiorante Matthews Mogerman (www.cfmlawyers.ca) with offices in Ontario and British Columbia.

An identical class action lawsuit was also launched for gold manipulation.

This is just the tip of the iceberg: with DB’s official “admission”, countless other plaintiffs will step up, and everyone who may have “lost” money trading gold over the noted 15 year period will surely demand to be made whole.

More importantly, we are curious to see what if anything the discovery process will unveil. This is what we said on Thursday:

Since this is just one of many lawsuits filed over the past two years in Manhattan federal court in which investors accused banks of conspiring to rig rates or prices in financial and commodities markets, we expect that now that DB has “turned” that much more curious information about precious metals rigging will emerge, and will confirm what the “bugs” had said all along: that the precious metals market has been rigged all along.

Now that Canada has broken the seal, we expect similar lawsuits to follow in the U.S.

* * *

As a reminder, this is what the gold and silver settlement terms sheets looked like.

end

China has been buying gold by the bucketful to support RMB internationalization:

(courtesy Koos Jansen)

China Embraces Gold In Advance Of Post-Dollar Era

Submitted by Koos Jansen via AllChinaReview.com,

To challenge the US dollar hegemony and increase its power in the global realm of finance, China has a potent gold strategy. Whilst the State Council is preparing itself for the inevitable decay of the current international monetary system, it has firmly embraced gold in its economy. With a staggering pace the government has developed the Chinese domestic gold market, stimulated private gold accumulation and increased its official gold reserves in order to ensure financial stability and support the internationalisation of the renminbi.

“The outbreak of the crisis and its spillover to the entire world reflect the inherent vulnerabilities and systemic risks in the existing international monetary system…. The desirable goal of reforming the international monetary system, therefore, is to create an international reserve currency that is disconnected from individual nations and is able to remain stable in the long run…”

Quote from Governor of the PBOC Zhou Xiaochuan 2009.

In the present zeitgeist we find ourselves on the verge of a shift in the global monetary order. The shocks through the financial complex in 2008 that reaffirmed the innate fragility of the US dollar as the world reserve currency have sparked China to become a vocal proponent of de-Americanization, although its end goal is communicated less clearly. Being the second largest economy of the world but relatively in arrears regarding physical gold reserves, China has a strong motive to surreptitiously work on its gold program until completion. For, if it would be candid in its gold ambitions, the price would significantly run higher, potentially disturbing financial markets and narrowing its window of opportunity to prepare for the next phase.

State Council Rapidly Developed Domestic Gold Market And Stimulated Private Hoarding

China has been infatuated with gold for thousands of years. In the mainland, gold mining and use can be traced back to at least 4,000 years ago, and the metal has always represented economic strength and was regarded as the emperors’ symbol of power. Although the Communist Party of China captured the monopoly in gold trade and heavily restricted private gold possession since 1949, in lockstep with the gradual liberalisation and the ascend of the Chinese economy the state started to develop the domestic gold market in the late seventies, which accelerated in 2002.

A new page was turned when the Gold Armed Police started operating in 1979, not coincidentally a few years after the US detached its dollar, the world reserve currency, from gold. This army division was initially assigned to gold mining exploration and has done so quite fruitfully. Since 1979, Chinese domestic mining output has grown 2,137 % from an annual 20 tonnes to an estimated 467 tonnes in 2015. In 1982, the first steps were taken in reviving China’s gold retail channels. For the first time since 1949 people were allowed to buy jewelry and the China Gold Coin Incorporation started issuing Panda coins. The Peoples Bank Of China (PBOC) continued to be the primary gold dealer that fixed the price and controlled all supply flows.

The real reform of the Chinese gold market was implemented on 30 October 2002 by the launch of the Shanghai Gold Exchange, erected to serve the full liberalisation of the domestic gold market. From that date the fixing of the gold price in China was transmitted from the PBOC to the free market. In 2004, the State Council approved gold as an investment for individuals and the PBOC slowly repelled control over supply flows. The Chinese gold market fiercely rose from its ashes. By 2007 the market was functioning as intended when nearly all gold supply and demand was flowing through the SGE system6. A year later, in 2008, the Shanghai Futures Exchange launched a gold futures contract supplementing existing derivatives at the SGE.

The Shanghai Gold Exchange (SGE), which is a subsidiary of the PBOC, is the very core of the Chinese physical gold market. Its infrastructure provides a single liquid exchange overseen by the state, granting all participants a trusty venue that can be efficiently developed and monitored. The mechanics of the Chinese market incentivise nearly all supply and demand to connect within the SGE system. As a consequence, by the amount of gold withdrawn from the vaults of the SGE – data that was published up until December 2015 in the Chinese Market Data Weekly Reports – we could gauge Chinese wholesale gold demand.

After the crisis in 2008, it became apparent in the higher echelons of the Chinese government that the development of the gold market and private accumulation had to accelerate to protect the Chinese economy from looming turmoil. Through state owned banks and media wires the citizenry were stimulated to diversify savings into physical gold. Currently, at Chinese banks, numerous gold saving programs can be entered into, or individuals can open an SGE account and purchase gold directly in the wholesale market.

“Individual investment demand is an important component of China’s gold reserve system, …. Practice shows that gold possession by citizens is an effective supplement to official reserves and is essential for our national financial security.”

Quote by the President of the China Gold Association 2012.

When the gold price came down sharply in April 2013, Chinese gold demand literally exploded as in a once in a lifetime event. In between 22 and 26 April, 117 tonnes of physical gold were withdrawn from the vaults of the SGE.

China has been a gigantic gold buyer ever since. Withdrawals from the vaults of the SGE in 2015 accounted for 2,596 tonnes (90 % of global annual mine output), up from a mere 16 tonnes in 2002. SGE withdrawal data correlates with elevated gold import by China.

Whilst clearly enjoying their bargain purchases, China has established a trend of increasingly obfuscating the true size of its gold demand. Not long ago several reports were released in the mainland that disclosed total gold demand to be the equivalent to SGE withdrawals. Since 2012 these reports have been hidden from public eyes and in January 2016 the SGE ceased publishing withdrawal data10. Although annual SGE withdrawals have exceeded 2,100 tonnes since 2013, what is generally publicised as gold demand is roughly half of this, merely the demand at jewelry shops and banks that excludes direct purchases from individual and institutional clients at the SGE. As a result, the global consensus is that Chinese gold demand is approximately 1,000 tonnes a year though in reality it’s twice this volume.

PBOC Accumulating Gold To Support Renminbi Internationalisation

To free itself from US dollar supremacy and force the sequent monetary system, China’s goal is to internationalise the renminbi. For achieving its target, gold is identified as the key. It is the absolute monetary asset to support the renminbi, the dollars’ Achilles heel and a hedge during monetary stress. Next to the swift progression in the Chinese private gold market we can observe the PBOC is covertly buying gold and has launched the Shanghai International Gold Exchange to prepare renminbi internationalisation.

“For China the strategic mission of gold lies in the support of renminbi internationalization, and so let China become a world economic power…. Gold is both a very honest asset and forms the very material basis for modern fiat currencies…. Gold is the world’s only monetary asset that has no counter party risk, and is the only cross-nation, cross-language … and cross-culture globally recognized monetary asset.

That is why in order for gold to fulfill its destined mission, we must raise our gold holdings a great deal, and do so with a solid plan. Step one should take us to the 4,000 tonnes mark, more than Germany and become number two in the world, next, we should increase step by step towards 8,500 tonnes, more than the US.”

Quote by the President of the China Gold Association 2014.

Not surprisingly, China’s strategy is everything but linear. Let us analyse the State Council’s most recent actions with respect to gold and the internationalisation of the renminbi. In addition to gold accumulation, the State Council has aimed to kick start renminbi internationalisation by having it included into the International Monetary Fund’s (IMF) basket of currencies, the Special Drawing Rights (SDR), in 2015. For acceptance, the IMF required openness of China’s international reserves, of which the PBOC hadn’t updated its gold reserves since 2009. Here we found the PBOC stretched between opposing forces; it obviously preferred to hoard gold in concealment not to disturb financial markets, while at the same time it was requested to open its books. In July 2015 the PBOC decided to revise its official gold reserves by 604 tonnes to 1,658 tonnes, which was probably not the whole truth but served both means, as markets barely reacted to the increment – the gold price has not increased since then – and the IMF has granted annexation of the renminbi into the SDR.

How much gold does the PBOC truly hold? Before we make an estimate we must first address the question, how and where does the PBOC buy gold? Some analysts assume the PBOC buys gold in the domestic market at the SGE. According to my research this is not true. My sources in the bullion industry tell me first hand that the PBOC buys gold in the international OTC market using Chinese banks as proxies. And this intelligence fits into the wider analysis, as there are many reasons why the PBOC would not buy gold through the SGE.

A rough estimate suggests the PBOC holds nearly 4,000 tonnes in gold reserves, more than twice the amount they officially disclose. In a quest for any clues we must visit the heart of the gold wholesale market. Data by the London Bullion Market Association points out there have been approximately 1,700 tonnes of monetary gold exported from London between 2011 and 2015. China’s central bank is the foremost suspect for these purchases, given its size and motives, and the tonnage exported from London is consistent with other sources that state the PBOC has bought roughly 500 tonnes a years since 2009. All clues together point to the PBOC holding roughly 4,000 tonnes currently. Although this remains speculation.

More of China’s gold strategy was revealed by the recent launch of the Shanghai International Gold Exchange (SGEI) that offers gold trading in renminbi for clients worldwide, in an attempt by China to strengthen the internationalisation of the renminbi. In itself the SGEI clearly underlines China’s gold ambitions16, but the punch line was added with the launch of the Silk Road Gold Fund in 201517. Led by the SGE(I), the $16 billion fund will boost the gold industry along the Silk Road and in turn “will facilitate gold purchases for the central banks of member states to increase their holdings of the precious metal”, according to the Chinese state press agency Xinhua18. Not only is China trying to persuade all mining and consumption of gold along the Silk Road economic project to be settled through the SGEI in renminbi, additionally the Chinese promote gold as an essential component of central banks’ international reserves going forward.

We must conclude that the State Council views gold as part of the coming international monetary system. Why else does it quickly develop the domestic gold market to be embedded in financial markets, surreptitiously accumulate vast gold reserves and establish a framework to boost gold business on the Eurasian continent around the SGEI? In my view, China contributes significant value to its gold strategy in the shadow of the apparent failure of the current fiat monetary system. And if true, China’s central bank having nearly 4,000 tonnes of gold is well on its way to introduce the next phase.

The gold and silver scam is really made up of two parts:

a) the fraudulent fix where the crooks lower the price on the morning and afternoon fix

b) the lending and selling of non existent gold into the market.

the latter is far worse and I am sure we will get emails on both:

(courtesy John Rubino/DollarCollapse.com)

Is Deutsche Bank’s Gold Manipulation The Main Scam Or Just A Side-Show?

Submitted by John Rubino via DollarCollapse.com,

For years now, the easiest way to finesse a debate over whether precious metals markets are manipulated has been to say, “well, if they’re not manipulated they’re the only market that isn’t.”

That was unsatisfying, though, because as the big banks got caught scamming their customers on interest rates, mortgage bonds, forex and commodities trades, those markets (presumably) began to operate more-or-less honestly. Gold and silver, meanwhile, kept right on acting strangely, for instance plunging in the middle of the night on no news but massive futures volume, to the detriment of honest investors and traders who naively bet their capital on fundamentals. The (already huge) amount of money thus stolen from gold bugs kept rising.

So it is with relief that fans of honest markets have greeted the news that at least one kind of precious metals manipulation has been exposed:

Deutsche Bank Settles Silver, Gold Price-Manipulation Suits

(Bloomgerg) – Deutsche Bank AG has reached settlements in lawsuits over allegations it manipulated gold and silver prices, lawyers for traders of the commodities said in court filings.

Attorneys for futures contract traders in two private lawsuits said in letters filed Wednesday and Thursday in Manhattan federal court that the bank has executed term sheets and is negotiating final details for the accords.

The German financial firm also agreed to help the plaintiffs pursue similar claims against other banks as part of the settlements, according to the letters. Vincent Briganti and Robert Eisler, attorneys for traders in the silver-fixing lawsuit, said Deutsche Bank will turn over instant messages and other communications to help further their case. Financial terms of the settlements weren’t disclosed.

“In addition to valuable monetary consideration to be paid into a settlement fund, the term sheet also provides for other valuable consideration such as provisions requiring Deutsche Bank’s cooperation in pursuing claims against the remaining defendants,” attorneys Daniel Brockett and Merrill Davidoff said in their letter Thursday in the gold-fixing lawsuit.

Silver and gold futures traders sued groups of banks in 2014 alleging they rigged prices for the precious metals and their derivatives. Silver traders brought claims against Deutsche Bank, HSBC Holdings Plc, Bank of Nova Scotia and UBS AG. Gold traders additionally sued Barclays Plc and Societe Generale SA.

The traders alleged the banks abused their positions of controlling daily silver and gold fixes to reap illegitimate profits from trading and hurting other investors in those markets who use the benchmark in billions of dollars of transactions, according to versions of the complaints filed in 2015. Of those banks, only Deutsche Bank has reached a settlement.

Amanda Williams, a spokeswoman for Deutsche Bank, declined to comment on either accord. Rick Roth, a spokesman for Scotiabank, the operating name for the Bank of Nova Scotia, and HSBC spokesman Robert Sherman also declined to comment. Representatives from UBS, Barclays and Societe Generale didn’t immediately respond to requests for comment.

The silver case is In re: London Silver Fixing Ltd. Antitrust Litigation, 1:14-md-02573. The gold case is In re: Commodity Exchange, Inc. Gold Futures and Options Trading Litigation, 14-md-2548, U.S. District Court, Southern District of New York (Manhattan).

Deutsche Bank’s plea is of course just the beginning of the story. It will apparently name its co-conspirators, while providing details on how the scam was run. This will be interesting and amusing (those instant messages promise to be classic), especially at a time when those same banks are also in the news for falling earnings, rising layoffs and exploding loan loss reserves.

But is this gaming of the London precious metals fix the same thing as – or even tangentially related to –the main manipulation of the gold price, which is the practice of central banks “lending” their gold to big commercial banks, which then sell that gold on the open market to depress the price? These seem to be two different frauds, and if only the first comes to light while the second continues unimpeded, there’s no reason to expect precious metals to start trading rationally — which is to say in line with fundamentals like soaring global debt, ever-increasing money creation and general geopolitical and economic instability. At least not until Western central banks run out of gold.

Kyle Bass On The Resurgence Of Gold And Why “In Reality, Negative Rates Make No Sense”

Hayman Capital founder Kyle Bass sat down recently for a conversation with Maria Bartiromo and Gary Kaminsky on Wall Street Week. He covered a variety of topics such as NIRP, income inequality, and the U.S. presidential race. As our regular readers know, Kyle correctly predicted the housing crisis, and is now calling for the yuan to be dramatically devalued.

On the growing use of negative interest rates as a central bank policy tool, he pointed out that while the central planners have their PhD’s and elaborate excel models, the reality is that not all people behave rationally, and thus in the real world those types of policies won’t necessarily work as intended. He also touched on the fact that a concern that should be on the front of everyone’s mind is the fact that if NIRP goes full Shinzo Abe and banks start charging customers for keeping cash at their banks, that there will be a run on cash.

“I think this is where the academics are kind of clashing with the practitioners. I think on paper negative rates make a lot of sense if you’re running academic models, but in reality they make no sense. Having seven or eight trillion dollars of debt trading at negative rates, having thirty year JGB’s trading at fifty basis points is absolutely ludicrous. This experiment that’s going on we all know will end poorly at some point in time, I just don’t know when that time is.”

“I think that one of the fears that they have is a run on cash. If they told you and I that they’re going to tax your deposits by a hundred basis points, well it’s better to put it in a safe or under your mattress. And that’s why you see a resurgence in gold. The more they move to negative rates, the more gold is gonna take off because there’s no carrying cost.“

Regarding what’s going on in Asia, he reiterates his call that there’s a giant credit bubble (as we discussed here, here, and here) that’s reached its breaking point and it’s going to burst over the next two or three years. He says that he believes the implosion of the china credit bubble will have a 40-50% chance of causing a recession in the U.S. within the next year.

“From the perspective of what’s going on in Asia, Asia has a giant credit bubble that they’ve been building for the last ten years or longer that has reached its atrophy level, and it’s going to happen over the next two or three years. Whether that causes the U.S. to have a brief, minor recession, I think it’s kind of forty, fifty percent chance in the next year personally.”

He goes on to hammer the central banks’ monetary policy decisions, saying that they can’t generate true organic growth and that we’ve been doing the same thing for the past eight years and we’re still in the situation we’re in. Something Zero Hedge has been pointing out consistently over the past seven years.

“I don’t buy this idea that monetary policy can generate true organic growth. It can help us out of a crisis, and it’s proven to do so, but listen we’ve had eight years of full out excessive monetary and fiscal policies and here we are today. So when Lagarde goes to the G-20 and says we all need to work together, we’ve been working together. Everybody has been on easy monetary policy, we’ve pulled all the demand forward that we can, and now we’re stuck with kind of stagnation and excess capacity and a lot of debt.”

“Economics assumes that everyone is a rational actor, and we all know in this world there aren’t many rational actors. That’s where there’s a divergence between academia and practitioners.”

When the conversation turns to the U.S. presidential race, Bass said that Hillary would be the best choice given everyone that’s running. When Maria mentioned that Hillary would raise taxes, Kyle lambasted the federal reserve easy monetary policy that only made the rich richer.

“So I’ll give you a crazy answer, I think it’s Hillary. I think she’s the most sane actor of them all.”

“Raising taxes, I mean, one thing you have to think about is this divide between the haves and the have-nots. One unintended consequence of Fed easy monetary policy has been this distributive nature where it made the rich richer. How many rich people do you know today that are worse off than they were at the peek of 2006. I don’t know one, minus some of the Lehman people, I don’t know one. What happened is we went to this policy where we went to QE, QE what that did was raise asset prices, well the only people with assets are rich people in general, so they became much more rich.“

Emergency Fed Meetings Spooked Investors Into Purchasing Record Gold Eagles

Sales of the U.S. Mint Gold Eagles surged last week as investors were spooked by the emergency Fed meetings. As several news sources reported last week, this was the first time both the President and Vice President “unexpectedly” met with the Fed Chairman to discuss the state of the American and global economy.

In addition, according to the news release, SuperStation95 – TWO MORE! Closed-Door, Expedited Meetings of Federal Reserve:

After Monday’s expedited, closed-door meeting of the Federal Reserve, Chair Janet Yellen met with Obama and Biden in an extraordinary meeting. Then, the fed called another, “expedited meeting” for Tuesday, April 12 to discuss a “Bank Supervisory Matter” and now, has called yet a THIRD closed-door meeting for Wednesday, 13 April, over “financial markets . . .”

The calling of three, closed-door meetings of the federal reserve Board of Governors and an extraordinary meeting with the President AND Vice-President, signals something is very serious; and the answer seems to rest with today’s meeting about a “Bank Supervisory Matter.”

Which bank?

Which bank has a “supervisory” matter so serious that it had to be taken-up by the federal reserve Board of Governors at an emergency, closed-door meeting?

Many rumors were spread around the blogosphere as to why there were several emergency Fed meetings. One such rumor is the U.S. government being force to enact martial law due to a systemic breakdown of the banking industry. Other rumors floating around are tied to the ramifications of the U.S. Dollar and U.S. Treasury market when China launches its gold-backed Yuan tomorrow, April 19th.

Regardless, the rumors had investors spooked enough to purchase the most Gold Eagles in a week since Jan 11th. Last week, the U.S. Mint sold 33,000 oz of Gold Eagles and 6,000 Gold Buffalos. That’s a lot of Gold Eagles sold in a week compared to 38,500 oz sold in the entire month of March:

The majority of Gold Eagle sales were the 1 oz coin which totaled 29,500, followed by 1,000 oz of the 1/2 oz coin, 1,500 oz of the 1/4 oz coin and 1,000 oz of the 1/10th oz coin. Again, these are shown in total ounces. For example, the U.S. Mint sold a total of 10,000 of the 1/10th oz Gold Eagle coins which equals 1,000 oz.

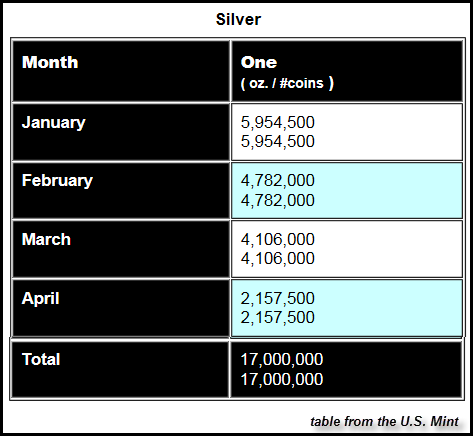

Furthermore, the U.S. Mint continues to sell out of its weekly allocation of Silver Eagles as total sales for the year reached 17 million– 26% higher than sales during the same period last year (CoinNews.net):

It will be interesting to see what takes place after the Chinese Yuan-denominated gold benchmark starts tomorrow. If this wasn’t going to be such a big deal, then why all the emergency Fed meetings?

The U.S. and global financial markets are in serious trouble. Investors who haven’t taken a position in owning physical precious metals may be running out of time to do so.

-END-

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.4777 / Shanghai bourse CLOSED DOWN 44.46 OR 1.44% / HANG SANG CLOSED DOWN 154.97 OR 0.73%

2 Nikkei closed DOWN 572.08 or 3.40%%/USA: YEN FALLS TO 108.34)

3. Europe stocks opened ALL IN THE RED /USA dollar index DOWN to 94.60/Euro UP to 1.1306

3b Japan 10 year bond yield: FALLS TO -.123% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.34

3c Nikkei now WELL BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 40.49 and Brent: 42.84

3f Gold UP /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS to 0.121% German bunds in negative yields from 8 years out

Greece sees its 2 year rate FALL to 11.17%/:

3j Greek 10 year bond yield FALL to : 8.95% (YIELD CURVE NOW DEEPLY INVERTED)

3k Gold at $1237.85/silver $16.21 (7:45 am est)

3l USA vs Russian rouble; (Russian rouble DOWN ONE AND 24/100 in roubles/dollar) 67.73

3m oil into the 38 dollar handle for WTI and 41 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/expect a huge devaluation imminently from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN COLLAPSES TO 108.33 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9652 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0912 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN STARTS ITS CAMPAIGN AS TO WHETHER EXIT THE EU.

3r the 8 Year German bund now in negative territory with the 10 year FALLS to + .121%

/German 8 year rate negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.75% early this morning. Thirty year rate at 2.56% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Wipe Out Most Overnight Losses Following Dramatic Rebound In Crude

Following yesterday’s OPEC “production freeze” meeting in Doha which ended in total failure, where in a seemingly last minute change of heart Saudi Arabia and specifically its deputy crown prince bin Salman revised the terms of the agreement demanding Iran participate in the freeze after all knowing well it won’t, oil crashed and with it so did the strategy of jawboning for the past 2 months had been exposed for what it was: a desperate attempt to keep oil prices stable and “crush shorts” while global demand slowly picked up.

As a result what followed was crude’s biggest drop in months, a plunge of some 7% in the early Sunday trading hours, which also dragged down US equity markets and currencies of commodity-exporting nations. Furthermore, as can be seen in the chart below, with oil the most important commodity for global stock prices, many wondered if central banks would allow this drop to persist: after all by now everyone knows central banks’ only mandate is keeping asset prices propped up.

And whether it was central banks, or chronic BTFDers, just 12 hours after oil opened for trading with a loud crash, the commodity has nearly wiped out all losses, and both brent and WTI were down barely 2%, leading to both European stocks and US equity futures virtually unchanged on the session. Most of the losses were wiped out just after the European open, with WTI Jun’16 futures breaking back above USD 40/bbl to take out USD 40.50/bbl to the upside in the process. Almost as if the market was waiting for the ECB to start buying.

The Stoxx Europe 600 Index was little changed, after earlier sliding 1.4 percent, and U.S. equity-index futures also pared declines.

Whether oil’s dramatic overnight reversal will persist, however, remains to be seen: we expect OPEC nations will desperately try to figure out what the proper “jawboning” headline is to launch algo buying programs, now that “Doha freeze” has been exhausted. One early candidate has emerged:

- RUSSIA TO HOLD TALKS W/ SAUDIS ON OIL OUTPUT FREEZE:RIA

Then again, Iran once again refuses to comply, and with good reason – it is right to demand to be able to produce as much as it did before the US sanctions.

- IRAN ISN’T RESPONSIBLE FOR OIL OVERSUPPLY: ZANGANEH ON RADIO

So for now, all eyes are on oil.

“Oil is the most dominant theme today,” said Thu Lan Nguyen, a currency strategist at Commerzbank AG in Frankfurt. “It is a relatively clear pattern of commodity currencies being under pressure. On the other hand there is general risk aversion on the rise, which is supporting safe-haven currencies like the yen.”

One catalyst that is helping prop up oil prices is Kuwait whose crude production tumbled by 60% to 1.1 million barrels a day and its refineries scaled back operations as the state oil company took emergency measures Sunday to cope with the first day of an open-ended labor strike. Kuwait produced 2.81 million barrels a day last month, making it OPEC’s fourth-largest member.

In the other top story overnight, lawmakers in Brazil’s lower house of Congress reached the threshold of 342 votes needed to advance the motion to impeach Rousseff to the Senate on Sunday.

Morgan Stanley, is among companies reporting earnings on Monday after financial firms led stocks higher last week, with JPMorgan Chase & Co. and Bank of America Corp. climbing after announcing reductions in first-quarter expenses that beat analysts’ estimates. International Business Machines Corp. and Netflix Inc. are also due to release results.

This is where the markets stand now:

- S&P 500 futures down 0.2% to 2071

- Stoxx 600 down 0.2% to 342

- FTSE 100 down 0.2% to 6329

- DAX down 0.3% to 10024

- German 10Yr yield up less than 1bp to 0.13%

- Italian 10Yr yield down less than 1bp to 1.33%

- Spanish 10Yr yield up less than 1bp to 1.5%

- S&P GSCI Index down 1.2% to 332.3

- MSCI Asia Pacific down 1.5% to 130

- Nikkei 225 down 3.4% to 16276

- Hang Seng down 0.7% to 21162

- Shanghai Composite down 1.4% to 3034

- S&P/ASX 200 down 0.4% to 5137

- US 10-yr yield down 2bps to 1.74%

- Dollar Index down 0.1% to 94.6

- WTI Crude futures down 3% to $39.14

- Brent Futures down 2.4% to $42.07

- Gold spot up 0.1% to $1,235

- Silver spot down 0.3% to $16.19

Global Top News

- Oil Plunges After Output Talks Fail Amid Saudi Demands Over Iran: no Doha deal as Saudi insists all OPEC members must join

- Verizon Said to Lead Bids for Yahoo, Wall Street Journal Reports: Time Inc., Alphabet, IAC/InterActiveCorp dropped out

- McGraw Hill Sells J.D. Power Unit to XIO Group for $1.1 Billion: sale expected to close in third quarter

- Rousseff Hangs by a Thread After Losing Impeachment Vote: Rousseff open to dialogue, but not demoralized by vote

- Japanese Stocks Tumble After Oil Talks Deadlock as Yen Advances: insurers, Sony, Toyota drop in wake of deadly earthquake

- Amazon Rivals Netflix With Stand-Alone Video Subscriptions: Amazon Prime will be available on monthly payment plan of $10.99

- Disney’s on a roll as ‘Jungle Book’ Opens at $103.6 Million: debut was third-biggest so far this year, ComScore says

- Autohome Gets Takeover Bid From CEO’s Group, Topping Ping An: takeover proposal follows Ping An offer to buy Telstra’s stake

Looking at regional markets, Asian equities began the week on the back-foot, as oil prices slumped after output freeze talks in Doha failed. Nikkei 225 (-3.4%) underperformed in the aftermath of another earthquake over the weekend which has resulted in losses in insurers and has disrupted several large manufacturers’ operations, while a firmer JPY also added to the tone. ASX 200 (-0.4%) was led lower by energy names following the failure to strike an output freeze deal as Saudi demanded that Iran be included in an agreement, while Iran had shunned the meeting. Shanghai Comp (-1.4%) also conformed to the risk-averse tone despite continued improvement in home prices (Y/Y +4.9% vs. Prey. 3.6%), as the rampant property sector could also encourage inflows from stocks. 10yr JGBs traded marginally higher amid the risk-averse tone and the BoJ in the market for JPY 450b1n 5-10yr JGBs, which 20yr also yields decline to fresh record lows.

Asian top news:

- China Home-Price Gains Spread as Easing Measures Spur Demand: New-home prices climbed in 62 cities in March, 47 in Feb.

- Credit Suisse to Halt Earnings Previews in Japan Following Probe: Firm won’t allow analysts to visit cos. to gather information before they report earnings,

- High-Frequency Trading Chief Lashes Out at Proposed India Probe: Panel advising India’s regulator recommended investigation

- Alipay Owner Said to Start Shanghai IPO Process as Soon as 2016: Alibaba affiliate said to meet need for 3-years of profit

- CIMB’s Nazir Takes Leave Amid Audit of Political Fund Transfers: Bank chairman helped distribute funds to politicians in 2013

- Quake Death Toll Rises in Japan as Economic Impact Spreads: Toyota said oper. profit may drop as supplies disrupted

- Siliconware Says Tsinghua Unigroup Deal on Hold: possibility of investment depends on interaction between China, Taiwan govts

European stocks began the week under pressure, weighed on by energy names in the wake of the failed Doha meeting. Although equities later pared the majority of their opening losses, given that expectations of a significant deal coming to fruition had been somewhat small. Elsewhere, Italian banks are lower across the board this morning as doubts continue to mount over whether the new bank bailout fund has the means to revive the sector with some of the funds with investors themselves cynical about its prospects

The risk averse sentiment across Europe has sparked flight-to-quality flow into fixed income markets with Bunds remaining in close proximity to 164.00. However, German paper pulled back from their highs by mid-morning amid the turnaround in equities, allied with another heavy bout of supply this week, with an estimated EUR 20bIn worth of issuance.

European top news:

- Draghi Seen Putting ECB Stimulus Back on Agenda After Summer: analysts say ECB could add asset purchases or cut rates again

- Osborne Warns of Decades of Economic Pain If U.K. Quits EU: Brexit would knock 6% off U.K. GDP by 2030, Treasury argues

- World’s Biggest Miner Says Brexit Would Harm China View of U.K.: Obama to say Britain should stay in EU in London this week

- CaixaBank Bids EU908m for Rest of Banco BPI: offer is subject to scrapping a voting-rights limit at BPI

- Immofinanz Buying 26% of CA Immo in First Step to Merger: companies revisit last year’s hostile battle on friendly terms

- Banker Unrest Threatens Credit Suisse, Deutsche Bank Turnarounds: CEOs Thiam, Cryan face rising discontent

- Hutchison U.K. Mobile Deal Said to Face EU Veto Within Weeks: EU block may halt wave of recent telecoms consolidation

In FX, today has seen a morning of consolidation in the FX markets, with USD/CAD buying seen as the obvious trade in the wake of the collapsed talks in Doha. Given the signals given ahead of the meeting, the Saudi objection to Iran’s omission to an agreement was the clear writing to the wall, so the dip in Oil has been corrected accordingly leading the CAD off its lows. We gapped up to 1.2950 in the spot rate, and after rejecting a move on 1.3000, we have since moved back under 1.2900 to suggest a gap readjustment. AUD and NZD saw similar moves in line with CAD, but we have seen .7700 and .6900 levels reclaimed, but the recent highs look a stretch as yet. The USD index is threatening lower though, so expect a further extension (higher) in the commodity linked currencies, with the EUR and GBP also better bid as a result. USD/JPY is caught in the crossfire, but after more earthquakes in Japan, the pair has been pressured to sub 108.00 again, though briefly so as yet with a modest recovery in the Euro bourses aiding the upturn to just shy of 108.50.

The story of the overnight session so far has been that of commodities and specifically oil, after OPEC and Non-OPEC producers failed to agree to an output freeze deal as Saudi demanded that Iran be part of an agreement and Iran refused to attend the meeting in Doha. (Telegraph) There were comments from several oil ministers including Qatar’s who stated that OPEC needed more time. Furthermore, Russia’s oil minister said that Iran was not the reason behind the breakdown in talks and that the door is not shut for a production freeze, while Nigeria’s oil minister suggested that OPEC should shift to a majority vote system.

The energy complex saw initial downside today after the failed Doha talks, however much of the losses have been paired during the European morning, with WTI Jun’16 futures breaking back above USD 40/bbl to take out USD 40.50/bbl to the upside in the process. In terms of the metals complex, gold prices saw mild support amid risk-averse sentiment, although subdued price action during European hours, while overnight iron ore prices coat-tailed on steel advances which were underpinned by seasonal demand.

Bulletin Headline Summary from RanSquawl and Bloomberg

- The OPEC/non-OPEC talks in Doha over the weekend failed to lead to an agreement, with the fallout seeing downside in oil, and softness in commodity-linked currencies and energy names.

- Much of the immediate fallout from Doha saw a paring during European hours, with many suggesting that chances of a significant deal coming to fruition had been somewhat small.

- Today’s economic calendar is light in data and will see focus fall on potential comments from Fed’s Rosengren, Dudley and Kashkari.

Treasuries little changed in overnight trading even as oil drops below $40/barrel after producers ended talks in Doha without any agreement on limiting supplies; global equity markets drop, gold rises.

Dilma Rousseff’s presidency is hanging by a thread after Brazil’s lower house of Congress voted in favor of her impeachment, a decision that’s likely to cheer investors

As Europe holds its breath over whether or not the U.K. will stay in the union, companies are holding on to their cash. Coming off of an eight-year record for mergers and acquisitions, the U.K. just had its worst quarter for deals since 2010

Leaving the European Union would deliver a blow to Britain’s economy and leave it 6% smaller by 2030, according to a Treasury analysis produced as the government attempts to dissuade the electorate from voting to quit the bloc

Germany’s Finance Minister Schaeuble tells U.K. counterpart George Osborne that Berlin would be tough negotiator on trade agreement if U.K. leaves EU, Financial Times reports

Next ECB head should be from Germany as Mario Draghi’s policies “don’t help anymore,” Markus Soeder, Bavarian finance minister, says in interview with Bild am Sonntag

Something is going on below the surface of earnings that should give bulls pause; quarterly forecasts for the Standard & Poor’s 500 Index show profits are declining at the steepest rate since the financial crisis relative to revenue

China’s home-price gains accelerated last month as the nation’s economic hubs such as Beijing, Shanghai and Shenzhen continued to lead the way amid surging liquidity that underpinned demand

Sovereign 10Y bond yields mixed; European, Asian equity markets lower; U.S. equity-index futures drop. WTI crude oil and copper drop, gold rises

DB’s Jim Reid concludes the overnight wrap

All eyes on oil this morning as the long awaited producers meeting in Doha ended in disappointment last night. Following extended talks, OPEC members and major producers walked away without any agreement on a production freeze. Prior to this, the WSJ had suggested that a draft accord had been circulated calling for a freeze at January levels until the end of October. Saudi Arabia seems to have taken a harder stance however with the major sticking point the lack of participation from Iran, who failed to even send a representative to the meeting. Following the end of the meeting, the energy minister of Qatar was however cited as saying that OPEC members will continue to consult between themselves as well as non-OPEC members up until June with the bi-annual OPEC meeting set to be held on June 2nd.

The immediate reaction when markets opened this morning was for WTI to plunge over 7% and touch a low of $37.61/bbl (after closing at $40.36/bbl on Friday). Oil has since pared part of those heavy losses and is currently hovering just shy of $38.50/bbl (still nearly -5% on the day). The losses have dragged bourses in Asia lower. The Nikkei (-3.08%) is leading the way, not helped by a near +1% safe haven rally for the Yen. Elsewhere the Shanghai Comp is -1.31%, while the Hang Seng (-1.20%), ASX (-0.22%) and Kospi (-0.48%) are all in the red. Commodity sensitive currencies are up to a percent down this morning, while credit markets are unsurprisingly a couple of basis points wider. US equity index futures are also in the red to the tune of half a percent or so.

Meanwhile, the news of the lack of an agreement at yesterday’s meeting is interestingly also coinciding with the news of a forced production cut from Kuwait following a public sector strike which started on Sunday. The Kuwait Oil Company announced in a statement that the OPEC member is to slash production from the usual 3million barrels a day, to just 1.1million barrels a day. Public sector workers are protesting on the back of plans to make cuts to wages and incentives, with the FT reporting that unions had called for the reforms to be cancelled prior to commencing yesterday’s strike. It’s hard to know if this is helping to support a floor on the drop in the Oil price this morning, and ultimately how long this strike will go on for and therefore the overall importance of it, but it’ll be worth keeping an eye on how things progress.

Elsewhere, the other headline grabber this morning is the latest political update out of Brazil where the key lower house vote has happened overnight. Crucially, Congress have voted in favour of President Rousseff’s impeachment, reaching the required threshold of 342 votes. That clears the way for the motion to be passed over to the Senate where it will go in front of a special committee where a simple majority vote (from 81 members) will be taken. Should that majority be reached, then an official impeachment trial is launched, with Rousseff subsequently temporarily removed from office during the trial and Vice-President Temer stepping in.

Moving on to this week now. Although we’ll fully preview it at the end the highlights are tomorrow’s ECB lending survey, the ECB meeting on Thursday, the global flash PMI numbers on Friday and from earnings season as 104 S&P 500 companies and 46 Eurostoxx firms report this week including the remaining banks and also some of the big bellwether tech names. It’ll also be worth keeping a final eye on the Fedspeak tonight (particularly Dudley given his views have been closely aligned with Yellen) with the blackout period kicking in thereafter ahead of the April 26th and 27th FOMC meeting.

With regards to the ECB, their lending survey may offer clues about how Q1 volatility and especially the poor equity performance of banks has impacted lending if at all. Lending rates fell in February and net new lending was positive and while it might still be too early to tell it’s an important release all the same and due out at 9am BST tomorrow.

With regards to their meeting on Thursday, the main focus will likely be on any additional info they can give on their upcoming corporate bond purchasing scheme. They are sure to be asked for more details so it’ll be interesting if they have any. On this topic Michal Jezek in my team has just published a report “How Might Default Risk Shape the ECB Corporate Bond Purchase”. In the report, we explain why we believe the size of the ECB’s corporate bond purchase programme should not be constrained by concerns about default losses, at least not anywhere near current spread levels. We therefore expect the ECB to move all the way down to BBBs rather than keep the programme smaller and stick to higher-rated bonds. However, diversification is a key default-risk-management tool. We estimate that if the ECB aimed to passively buy a slice of the relevant market portfolio but self-imposed a 2% cap on single-issuer exposures, the effective eligible universe would shrink by 12%. With a 1% cap, it would shrink by 38% to about €350bn. Still, we think that even with such a diversification restriction the ECB should be able to build up a portfolio in line with our baseline expectation of monthly purchases averaging €3-5bn, presumably including the primary market. We also think that as long as the ECB can take a portfolio view on default losses, it would make little sense to automatically sell fallen angel corporate debt.

Moving on. Aside from the Doha events, the only other snippet of news from the weekend came from the IMF’s spring meetings, although in truth not much new material appears to have come out of these. IMF Chief Lagarde summed up the mood from officials as having an overall lower level of anxiety relative to their last meeting, with officials demonstrating ‘a collective endeavour to indentify the solution and the responses to the global economic situation’. Some of the talks also focused on FX policy with members reiterating that they would ‘reaffirm previous exchange-rate commitments, including that we will refrain from competitive devaluations’.

A quick recap of how we closed out last week on Friday. Risk assets finished on a bit of a whimper with much of that being attributed to heavy losses in the energy sector as Oil prices moved steadily lower with expectations declining (now justified) ahead of Doha. Some soft US data didn’t help (more on that shortly) while Citigroup became the latest bank to report earnings in the sector. A beat at both the earnings and top line were recorded with the theme being similar to what we’ve seen insofar with much of that profit beat being cost cut driven. The S&P 500 eventually closed with a modest -0.10% loss although the five-day return was still a healthy +1.62%. US credit indices were a smidgen wider while in Europe it was credit which was the relative underperformer on Friday, the iTraxx Crossover in particular ending 10bps wider while the Stoxx 600 closed -0.35% for its first negative day in over a week.

With regards to that data out of the US on Friday, most notable early on was the steeper than expected fall in industrial production last month (-0.6% mom vs. -0.1% expected), the second consecutive monthly decline of that magnitude with the mining and utility sectors leading much of the softness. Manufacturing production (-0.3% mom vs. +0.1% expected) was also down. That said the first factory reading for April was supportive. The NY Fed’s empire manufacturing survey revealed a near 9pt rise to 9.6 (vs. 2.0 expected) and the highest level for that series since January 2015 with new orders, employment and prices paid all strengthening. Elsewhere, the first release of the April University of Michigan consumer sentiment reading revealed an unexpected 1.3pt fall in the index to 89.7 (vs. 92.0 expected) with the expectations component leading much of that. One year inflation expectations were unchanged at 2.7% however it was noted that 5-10y expectations tumbled two-tenths to 2.5%.

Staying in the US, Chicago Fed President Evans was also out with comments on Friday, saying (unsurprisingly) that there is a ‘high hurdle’ for any tightening in policy from the Fed next week. A lot of Evans’ comments were focused on the inflation picture however which he highlighted as informing the Fed’s decisions in the near term.

With the Fed meeting next week, there’s little in the way of Fedspeak although today we will hear Dudley give opening remarks at a conference this afternoon, followed by Kashkari and Rosengren later this evening. The BoE’s Carney is due to speak in Parliament tomorrow afternoon, while on the US election front we’ll get the NY primary tomorrow.