Gold $1315.00 down $8.00

Silver 18.96 down 2 cents

In the access market 5:15 pm

Gold: 1314.40

Silver: 18.99

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix Sept 15 (10:15 pm est last night): $ not available/holiday

NY ACCESS PRICE: $n/a (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ not available/holiday

NY ACCESS PRICE: n/a (AT THE EXACT SAME TIME)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Sept 15: 5:30 am est: $1320.10 (NY: same time: $1321.20: 5:30AM)

London Second fix Sept 8: 10 am est: $1310.80* (NY same time: $1311.80 , 10 AM)*after a beautifully orchestrated criminal raid today.

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

For comex gold:The front September contract month we had 72 notices filed for 7200 oz

For silver: the front month of September we have a total of 94 notices filed for 470,000 oz

Yesterday, you could have bet the farm that there is going to be a raid on gold and silver today due to the Chinese festival. They will be on holiday until Monday. With no physical to draw on, it was relatively easy for our crooks to supply 70 tonnes of gold in seconds to cause gold to falter down to 1308.00 before recovering.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 487 contracts down to 193,466. The open interest fell despite the fact that the silver price was up 7 cents in yesterday’s trading .In ounces, the OI is still represented by just LESS THAN 1 BILLION oz i.e. .967 BILLION TO BE EXACT or 138% of annual global silver production (ex Russia &ex China). the crooks are doing a great job fleecing unsuspecting longs

In silver we had 94 notices served upon for 470,000 oz

In gold, the total comex gold fell by 1,179 contracts as the price of gold fell BY $0.50 yesterday . The total gold OI stands at 573,823 contracts. The level of OI now is good for us as it will support a rise in gold price.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

LAST NIGHT WE HAD ONE change out of the GLD/ A HUGE WITHDRAWAL OF 3.27 TONNES FROM THE GLD/

Total gold inventory rest tonight at: 932.22 tonnes of gold

SLV

we had no changes with respect to inventory at the SLV

THE SLV Inventory rests at: 362.434 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver fell by 487 contracts down to 193,466 as the price of silver fell by 7 cents with yesterday’s trading.The gold open interest fell 1179 contracts down to 573,823 as the price of gold fell $0.50 IN YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

end

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed FOR HOLIDAY/ /Hang Sang closed UP 144.95 points or 0.63%. The Nikkei closed DOWN 209.23 POINTS OR 1.63% Australia’s all ordinaires CLOSED UP 0.23% Chinese yuan (ONSHORE) closed HUGELY UP at 6.6583/Oil ROSE to 44.02 dollars per barrel for WTI and 46.21 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.6580 yuan to the dollar vs 6.6583 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS HUGELY AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)Korea:

none

b) REPORT ON JAPAN

The high libor in uSA terms is causing real problems for certain Japanese banks as they are having a tough time finding liquidity. Then this: one major Japanese bank was so desperate that they borrowed 60 billion USA from money market funds last month;

(courtesy zero hedge)

c) REPORT ON CHINA

China floods her economy with over 1 trillion yen in new August credit as most of this “total Social Financing” went into house mortgages which is a huge big industry in China and makes up a considerable chunk of their shadow banking sector. This is a house of cards waiting to falter

( zero hedge)

4 EUROPEAN AFFAIRS

i)BANK OF ENGLAND

No surprises here: the Bank of England keeps its rate unchanged at .25%/ The level of QE remains the same. Many members of the Central Bank expect a cut in its rate to zero in the near future

( zero hedge)

ii)SPAIN

Rajoy blows any chance of a coalition when he appoints a person to a lucrative position at the world bank even though he has received graft in the past.

( Mish Shedlock)

iiib Then last night, this was bound to happen: German right wing extremists came in contact with 20 refugees in the German town of Baitzem located close to the Czech border and 60 km from Dresden:( zero hedge)

iiic) After a humiliating defeat in her own home town last month, Merkel is bracing for more misery with the Berlin area elections this Sunday:

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

none today

7.OIL ISSUES

OIL plunges again as Libya and Nigeria are set to supply which will increase the glut

( Bloomberg)

8.EMERGING MARKETS

none today

9.PHYSICAL STORIES

i)My goodness that was a lot of paper gold dumped at exactly 8:30 this morning.

Ladies and Gentlemen: your crime scene. These crooks have no gold behind them and their act is nothing but criminal!

( Dave Kranzler)

ii)With the Fed beginning to embrace the concept of negative rates in the USA, the only GO to asset will be gold/silver.

( Stefan Gleason/Lawrie onGold)

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)A good look at our impoverished inner cities

( Michael Snyder/Economic Collapse blog)

ii)Ford announces that it plans to shift all small car production to Mexico. If Trump gets in, he will introduce a 35% tax and that will stop their move in a heart-beat

( zero hedge)

iii)The following is a big miss as retail sales growth tumbles to a 6 month lows as it rose just 1.9%/year over year. Month over month saw a drop in sales.

( zero hedge)

iv)Initial claims lower to 260,000 but forward looking expectations in employment for both service and manufacturing sectors do not look good

( zero hedge)

v)Wow!! this is a good one: the NY Empire manufacturing index mysteriously rises even though ALL of its components deteriorate. Figure that one out

( zero hedge)

vi)Another biggy!! Industrial production falls by .4% month over month in August, its biggest drop since March. Its year over year drop 1.1%: the longest non recessionary slump in over 100 years

( zero hedge)

vii This is another biggy: average weekly wages declines in most of the USA counties. Janet and Stanley still believe the USA economy is doing fine?

( zerohedge)

viii)The following indicator is the best one to indicate recession or not: Sales to Business inventories. Last month: business inventories rose .5% but business sales dropped .8% and the 19th consecutive month of declines and inventory builds. The all important ratio rises to 1.39 and in extreme recession levels.

(courtesy zero hedge)

Let us head over to the comex:

The total gold comex open interest fell to an OI level of 573,823 for a loss of 1179 contracts as the price of gold FELL by $0.50 with yesterday’s trading. We are now in the NON active month of SEPTEMBER/

The contract month of Sept saw it’s OI RISE by 55 contracts UP to 209. We had 16 notices filed yesterday so we GAINED 71 contracts or 7100 additional oz will stand for delivery. The next delivery month is October and here the OI FELL by 1046 contracts down to 39,790. This level is extremely high and no doubt many of these will wait it out and take delivery at the end of the month. The next contract month of December showed an decrease of 1,706 contracts down to 427,358 .The estimated volume today at the comex: 171,811 fair Confirmed volume yesterday: 210,555 which is good.

And now for the wild silver comex results. Total silver OI fell by 487 contracts from 193,953 down to 193,466 with the FALL in price of silver to the tune of 7 cents yesterday. We are moving away from the all time record high for silver open interest set on Wednesday August 3: (224,540). We are now into the next active month of September and here the OI fell by 56 contracts down to 830. We had 106 notices filed upon YESTERDAY so we GAINED BACK 50 contracts or 250,000 additional oz will stand for delivery in this active month of September. The next non active delivery movement of October hardly moved rose by 12 contracts up to 282 contracts. The next big delivery month will be December and here it fell, down 274 contracts to 168,287. The volume on the comex today (just comex) came in at 59,956 which is excellent The confirmed volume yesterday (comex and globex) was huge at 84,733 . Silver is not in backwardation. London is in backwardation for several months.

today we had 94 notices filed for silver: 460,000 oz

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz |

NIL |

| Withdrawals from Customer Inventory in oz nil |

nil

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

578.700 oz

Delaware

|

| No of oz served (contracts) today |

72 notices

7,200 oz

|

| No of oz to be served (notices) |

137 contracts

(13,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

2416 contracts

241,600 oz

7.5147 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | 192.90 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 76,117.3 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 72 contract of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped (received) by jPMorgan customer account.

To me, the only thing that makes sense is the fact that “kilobars” are entries or hypothecated gold sent to other jurisdictions so that they will not be short in their derivatives like they are in England. This would be similar to the rehypothecated gold used by Jon Corzine. If this is the case, this would be the greatest fraud perpetrated on USA soil!!.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

392,272.500 OZ

CNT

|

| Deposits to the Customer Inventory |

600,555.650 oz

BRINKS

|

| No of oz served today (contracts) |

94 CONTRACTS

(460,000 OZ)

|

| No of oz to be served (notices) |

736 contracts

(3,680,000 oz)

|

| Total monthly oz silver served (contracts) | 2310 contracts (11,550,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,021,672.1 oz |

SEPT 9/ we had a big changes tonight out of the GLD/ there were two major withdrawals

i) first early morning: 1.19 tonnes

ii) second: 10.68 tonnes of gold

total: 11.87 tonnes

Total gold inventory rest tonight at: 939.94 tonnes of gold

end

NPV for Sprott and Central Fund of Canada

end

And now your overnight trading in gold,THURSDAY MORNING and also physical stories that may interest you:

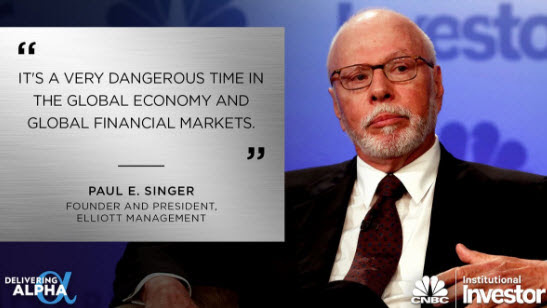

Buy Gold – Bonds Are ‘Biggest Bubble In World’ – Billionaire Singer Warns

Buy gold as bonds are in the “biggest bubble in the world” and it is a “a very dangerous time in the global economy” according to billionaire investor, Paul Singer.

Speaking at the CNBC Delivering Alpha Conference, the respected hedge fund manager, Singer said he favours a diversification into gold right now.

He thinks that gold is “underrepresented in many portfolios as the only money and store of value that has stood the test of time.” He added that at current prices gold is “undervalued.”

For Singer, the founder of the $27 billion Elliott Management, owning gold is “opposite confidence in central banks” who have made the bond market “the biggest bubble in the world.”

Singer urged the room of investors to sell their bonds:

“I think owning medium to long-term G-7 fixed income is a really bad idea. By removing these things that are bad ideas, that’s a helpful thing. Sell your 30-year bonds. ”

The bond market is $60 trillion. Right now, nearly $10 trillion in fixed income is negative yielding. He added that these prices and yields contain a “tremendous, never-before seen asymmetry between potential further reward and risk.”

Singer is among a number of hedge fund managers who have become increasingly vocal against central bank policy. He said that central banks have created a “tremendous increase in hidden risk and “unusual dangers that are unique in the ‘5,000 years-ish’ history of finance.”

Transcript of Singer interview with CNBC here and video here

Gold and Silver Bullion – News and Commentary

Gold holds on to gains as steady as equities wobble (Reuters)

Gold holds mostly steady in Asia as investors await BoJ, Fed next week (Investing.com)

U.S. Stocks Fade as Jitters Persist Amid Oil Rout; Bonds Advance (Bloomberg)

Gold snaps a five-session slide as the dollar retreats (Marketwatch)

Greenspan Worries That ‘Crazies’ Will Undermine the U.S. System (Bloomberg)

No matter which way the bond bull market ends, it’s going to get ugly (Moneyweek)

Bridgewater’s Dalio: There’s a ‘dangerous situation’ in the debt market now (CNBC)

Welcome To Third World – Poor American Kids Become Prostitutes To Buy Food (Dollar Callapse)

Now Hundreds Of Paper Claims For Every Available Ounce Of Physical Gold & Silver (King World News)

Gold Prices (LBMA AM)

Gold Prices (LBMA AM)

15 Sep: USD 1,320.10, GBP 999.82 & EUR 1,174.23 per ounce

14 Sep: USD 1,323.20, GBP 1,001.40 & EUR 1,177.91 per ounce

13 Sep: USD 1,328.50, GBP 1,000.36 & EUR 1,183.69 per ounce

12 Sep: USD 1,327.50, GBP 1,000.80 & EUR 1,182.54 per ounce

09 Sep: USD 1,335.65, GBP 1,004.68 & EUR 1,184.86 per ounce

08 Sep: USD 1,348.00, GBP 1,009.11 & EUR 1,195.81 per ounce

07 Sep: USD 1,348.75, GBP 1,008.60 & EUR 1,199.85 per ounce

Silver Prices (LBMA)

15 Sep: USD 18.96, GBP 14.32 & EUR 16.87 per ounce

14 Sep: USD 19.04, GBP 14.42 & EUR 16.96 per ounce

13 Sep: USD 19.16, GBP 14.44 & EUR 17.06 per ounce

12 Sep: USD 18.72, GBP 14.11 & EUR 16.68 per ounce

09 Sep: USD 19.41, GBP 14.58 & EUR 17.23 per ounce

08 Sep: USD 19.93, GBP 14.90 & EUR 17.65 per ounce

07 Sep: USD 19.92, GBP 14.89 & EUR 17.71 per ounce

Recent Market Updates

– Silver Bullion Market – “Most Bullish Story Ever Told?”

– “Sorry, You Can’t Have Your Gold Bullion”

– Global Stocks, Bonds Fall Sharply – Gold Consolidates After Two Weeks Of Gains

– Gold, Silver, Blockchain and Fintech – Solutions To Negative Rates, Bail-ins, Cash Confiscations and Cashless Society

– Jan Skoyles Appointed Research Executive At GoldCore

– Silver Bullion Surges 3.5% To Over $20/oz

– Ireland “Especially Exposed” To “International Shocks” Warns Central Bank

– Deutsche Bank Tries To Explain Failure To Deliver Physical Gold

– Physical Gold Delivery Failure By German Banks

– Avoid Paper Gold – “Gold Delivery” Refused By Gold Exchange Traded Commodity

– Debt Bubble in Ireland and Globally Sees Wealthy Diversify Into Gold

– “Why Case Against Gold Is Wrong” – James Rickards

– Obama To Leave $20 Trillion Debt Crisis For Clinton Or Trump

end

My goodness that was a lot of paper gold dumped at exactly 8:30 this morning.

Ladies and Gentlemen: your crime scene. These crooks have no gold behind them and their act is nothing but criminal!

(courtesy Dave Kranzler)

YOUR CRIME SCENE

Someone Dumped 70 Tons Of Paper Gold At 8:30 a.m.

September 15, 2016Financial Markets, Gold, Market Manipulation, Precious Metals, U.S. EconomyComex gold, gold cartel, gold manipulation, retail sales

At 8:30 a.m. this morning, 10 minutes after the Comex gold pit opens, over 70 tons of gold was dropped into the entire Comex trading system. If this happened on the NYSE, one of the ECN’s (usually BATS) would have mysteriously “broke” and trading would have been halted – before the damaging effects of the systemic paper overload hit the market.

From 8:30 to 9:30 a.m. EST, a total of 6,289,900 ozs of paper gold, or 196.5 tons was unloaded on the Comex. To put this in perspective, the Comex is reporting 2.37 million ounces of gold in its registered account (the gold that can be delivered). That amount of paper gold that would unloaded was 2.7x the amount of gold available to be delivered. It represents 58% of the entire amount of gold reported to be in Comex vaults.

It’s hard to find any specific news trigger that would have motivated anyone to sell one ounce of gold, let alone nearly 3x the amount of physical gold available to be delivered.

Perhaps the worst economic news reported was retail sales, which dropped .3% in August vs. the expectation of no change. This is the 4th month in a row retail sales have dropped on monthly sequential basis. Retail sales have declined 6 out of 8 months this year.

There’s probably nothing to see in that chart above – just like the allegations of Hillary’s poor health.

http://investmentresearchdynamics.com/someone-dumped-70- tons-of-paper-gold-at-830-a-m/

***

end

With the Fed beginning to embrace the concept of negative rates in the USA, the only GO to asset will be gold/silver.

(courtesy Stefan Gleason/Lawrie onGold)

Unprecedented Global Bond Bubble. Gold and Silver an Escape Hatch.

By Stefan Gleason*

While the article below is aimed at the U.S. investment community, there are parallels throughout the world where negative interest rates are already in effect, or being contemplated.

The world has rarely seen a bond bull market that is not only 36 years old, but also shows few signs of ending. And never before in recorded history have interest rates gotten so low across the board.

How much lower can interest rates go? Conventional wisdom once held that rates could only get as low as 0%. WRONG! In the current crazed central banking climate, yields on cash can move below zero, and they could stay there for longer than anyone can possibly imagine.

Negative rates – where lenders pay interest to borrowers – are a strange-but-true phenomenon in Japan and throughout much of Europe. They aren’t confined just to overnight rates set directly by central banks. They have spread across the yield curve to afflict the long-term bond market as well.

THE FED IS SPEAKING WARMLY ABOUT IMPOSING NEGATIVE RATES IN AMERICA

The U.S. Federal Reserve is now contemplating a negative interest rate policy even as it jawbones about raising rates. At its August Jackson Hole gathering, Fed officials listened to economist Marvin Goodfriend make the case for negative rates (and another draconian measure, as I’ll explain in a moment).

“It is only a matter of time before another cyclical downturn calls for aggressive negative nominal interest rate policy,” he said. The U.S. economy is overdue for a recession, and when the one hits, Goodfriend suggests the Federal funds rate will be dropped to as low as -2%.

Goodfriend is no friend to holders of cash. Not only does he want to penalize savers; he also proposes eliminating coins and paper notes from circulation.

After all, if your bank account “pays” negative interest, holding physical cash under your mattress would give you a higher yield. So central bankers would rather see cash be eliminated to prevent you from pulling it out of the bank.

Fed Vice Chairman Stanley Fischer said in a recent Bloomberg interview that negative interest rates “seem to work.” While he denied that the Fed has any immediate plans to pursue a negative rate policy, he sure sounded favorable to the concept.

THERE IS STILL AN ESCAPE HATCH TO SOUND MONEY

There is an escape hatch for those who fear being trapped in a negative yield regime. Hard assets, including physical precious metals, have no interest rate attached to them.

Putting aside capital appreciation qualities, a gold coin with a 0% yield also offers a superior yield to any currency instrument with a negative rate affixed to it. Gold and silver are normally seen as more attractive forms of cash when cash instruments yield less than the inflation rate (i.e., negative real interest rates). But in a negative yield environment, precious metals also have the advantage of sporting nominally higher yields.

Many economists, who assume that markets are efficient and that investors make rational choices, remain puzzled as to why negative yielding bonds have attracted nearly $16 trillion in inflows globally. The standard models for evaluating bonds assume that a bond must offer at least some nominal yield above cash to make it more attractive than simply holding cash itself.

Logically, there shouldn’t be any demand for negative yielding bonds under any circumstance. Why would investors in a free market wittingly pursue sure-fire losses? And yet, today, there is enormous demand for bonds that promise to pay back holders less than the principal they invest.

It’s important to recognize that negative yields are being imposed on markets by central banks. Many institutional investors such as commercial banks, pension funds, and insurance companies are effectively forced to own government bonds regardless of what they yield.

Then, speculators come in who don’t care about logic or sound fundamentals, but only care about chasing extant trends. Continuation of this trend seems likely when we have central banks willing and able to create unlimited amounts of currency to buy bonds. This trend begets followers, and followers exacerbate the trend – often to the point of “irrational exuberance,” as Alan Greenspan once put it.

DON’T BET AGAINST THE GOVERNMENT BOND MARKET

Bond market speculators can potentially reap capital gains even on bonds that carry negative yields. If future bonds get issued with rates that are even more deeply negative, then the values of all previously issued bonds will keep climbing.

Given that rates in the U.S. are still positive, the bond bubble could get much bigger before it bursts. U.S. Treasuries with yields of 1%-2% may be historically low, but they look fat and juicy to Japanese and European investors who get literally less than nothing on bonds in their home markets. In other words, the government bond market still looks like a raging bull.

Before you go chasing after capital gains in Treasuries, however, consider the risks of owning bonds at today’s ultra-low yields. You could subject yourself to massive real losses over time if inflation rates perk up. Even nominal capital gains in bonds could prove to be illusory in real terms.

Gold and silver are premier assets to hold if you are concerned about negative real interest rates. Precious metals markets offer no guarantee of inflation-beating returns in any given year, of course. But if you’re thinking 30 years out, would you rather put your trust in metals – or in a bond issued by an over-indebted government that promises to pay you a historically low yield?

Although low to negative interest rates could persist for years, odds are the current low-yield craze won’t last a full 30 years. Therefore, at some point down the road, today’s buyers of 30-year bonds will likely wish they had parked some of their savings in physical precious metals instead.

Stefan Gleason is President of Money Metals Exchange, the national precious metals company named 2015 “Dealer of the Year” in the United States by an independent global ratings group. A graduate of the University of Florida, Gleason is a seasoned business leader, investor, political strategist, and grassroots activist. Gleason has frequently appeared on national television networks such as CNN, FoxNews, and CNBC, and his writings have appeared in hundreds of publications such as the Wall Street Journal, TheStreet.com, Seeking Alpha, Detroit News, Washington Times, and National Review.

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.6583( REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS TO 6.6580) / Shanghai bourse CLOSED FOR HOLIDAY / HANG SANG CLOSED UP 144.95 or 0.63%

2 Nikkei closed DOWN 209.23 OR 1.63% /USA: YEN FALLS TO 102.38

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index UP to 95.38/Euro UP to 1.1242

3b Japan 10 year bond yield: FALLS TO -.038% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 101.87/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 44.02 and Brent: 46.21

3f Gold DOWN /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” ON THE TABLE

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES to +.046%

3j Greek 10 year bond yield RISE to : 8.58%

3k Gold at $1321.40/silver $19.02(7:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble UP 11/100 in roubles/dollar) 65.04-

3m oil into the 44 dollar handle for WTI and 46 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 102.38 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9735 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0944 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.046%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.698% early this morning. Thirty year rate at 2.457% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures, European Stocks Rebound, Bonds Fall Ahead Of US Data Deluge

The overnight session started with more weakness out of Asia, where chatter that the BOJ may end up doing nothing despite all the trial balloons (as we hinted yesterday), sent the USDJPY sliding, pushing the Nikkei lower, leading to a 7th consecutive decline in the Topix, the longest such stretch since 2014 even though the BOJ is now actively buying a record amount of ETFs. However, the modest dip in S&P futures and European stocks proved too much for BTFD algos, and risk promptly rebounded.

Heading into the US open, European stocks and U.S. equity-index futures advanced as investors awaited a batch of US economic data, including retail sales, PPI, and various regional Fed indexes for clues on the strength of the world’s biggest economy and the trajectory of interest rates before next week’s Federal Reserve meeting.

As Bloomberg updates, the Stoxx Europe 600 Index added 0.3 percent at 11:02 a.m. in London. Siemens added 2.2 percent after Chief Executive Officer Joe Kaeser said Europe’s biggest engineering company may beat its earnings forecast for the fiscal year ending this month. Lenders rebounded after their worst three-day drop in two months, with those in Italy, Spain and Portugal leading the advance. The U.K.’s FTSE 100 Index gained 0.2 percent before the BOE decision. Hennes & Mauritz AB declined 3.1 percent after the Swedish fashion retailer’s August sales missed estimates because of hot weather. Next Plc dropped 5.1 percent after warning that the current quarter will be its toughest this year and 2017 sales will be hurt by Brexit-induced price increases. Electricite de France SA fell 0.9 percent after the U.K. government approved its plan to build two nuclear reactors for 18 billion pounds in southwest England. Energy producers were among the worst performers in the index, with Royal Dutch Shell Plc and BP Plc weighing the heaviest, as oil traded below $44 a barrel.

Futures on the S&P 500 Index gained 0.3 percent after the underlying benchmark retreated 0.1 percent on Wednesday. The MSCI Asia Pacific Index fell 0.3 percent. Japan’s Topix index lost ground for the seventh day in a row, led by declines in real-estate shares.

About $2 trillion has been wiped off the value of global equities over the past week as anxiety over the oil market coincided with signs major central banks were preparing to recalibrate monetary policy. While the odds of a U.S. interest-rate hike on Sept. 21 are 20 percent, the probability is 52 percent for a move this year. Prospects may be swayed on Thursday as August data on industrial output, producer prices and retail sales are released. In the U.K., BOE policy makers are forecast to leave the key rate at a record-low. Markets in mainland China, South Korea and Turkey are shut Thursday for holidays. “Markets are at the mercy of central banks but there’s a bit of a problem regarding credibility,” said Thomas Thygesen, SEB AB’s head of cross-asset strategy in Copenhagen. “Until we get a true picture of where global monetary policy is headed, markets can’t really pick a direction.”

Crude oil traded at $43.81 a barrel following a two-day slide of almost 6 percent. Libya and Nigeria, two OPEC members whose supplies have been crushed by domestic conflicts, are preparing to add hundreds of thousands of barrels to world markets within weeks.

U.S. data showed crude stockpiles fell 559,000 barrels last week, compared with a 4 million gain forecast in a Bloomberg survey. “The market is getting a little more conservative about when the balance will return and prices are adjusting to that,” said Ric Spooner, chief market analyst at CMC Markets in Sydney. “We have moderating demand combined with the possibility of increased supplies from Libya and Nigeria. There is also the potential for non-OPEC output to start increasing.”

In the bond market, the yield on U.S. Treasuries due in a decade rose one basis point to 1.71 percent, after falling three basis points the previous day. Thirty-year yields increased two basis points to 2.47 percent, leaving the spread between the two securities at 75 basis points, having reached the widest in more than six weeks on Wednesday. Yields rose across the euro area as Spain and France sold bonds. Germany’s benchmark 10-year bond yield increased three basis points to 0.048 percent. Yields on similar-maturity French bonds also rose three basis points, to 0.35 percent, and Spain’s were one basis point higher at 1.09 percent.

Market WrapS&P 500 futures up 0.3% to 2121

- Stoxx 600 up 0.1% to 339

- FTSE 100 up 0.1% to 6683

- DAX up less than 0.1% to 10379

- German 10Yr yield up 2bps to 0.04%

- Italian 10Yr yield up 2bps to 1.32%

- Spanish 10Yr yield down less than 1bp to 1.07%

- S&P GSCI Index up 0.3% to 347.4

- MSCI Asia Pacific down 0.3% to 136

- Nikkei 225 down 1.3% to 16405

- Hang Seng up 0.6% to 23336

- S&P/ASX 200 up 0.2% to 5240

- US 10-yr yield up less than 1bp to 1.7%

- Dollar Index up 0.07% to 95.4

- WTI Crude futures up 0.3% to $43.71

- Brent Futures up 0.6% to $46.13

- Gold spot down 0.1% to $1,321

- Silver spot up less than 0.1% to $18.98

Top Global News:

- Bond Market Flashes Signal Traders Haven’t Seen Since 2012: Yield curve steepens as traders trim bets on higher Fed rates

- Oil Holds Losses Below $44 as Global Oversupply Seen Worsening: Libya, Nigeria may boost shipments within weeks

- Wells Fargo Bogus-Account Scandal Said to Draw U.S. Probe: N.Y., California prosecutors said to look at bank, individuals

- BlackRock Sides With BOJ in Debate Over Tokyo Whale’s ETF Buying: critics say BOJ buying could make stocks hard to trade

- Telia Says U.S., Dutch Propose $1.4b Uzbek Settlement: Could be largest fine ever under U.S. foreign corruption act

- Fiat Chrysler Said to Explore China Venture With BAIC Group: Partnership would be second in China for Fiat Chrysler

- Tesla Investigates Potential Autopilot Link in Fatal China Crash: Beijing court has accepted family’s lawsuit, CCTV reports

- Magna Considering New Car Plants After Getting BMW 5-Series Deal: Production of new 5-Series will start in 2017 in Austria

- Ford, Rolls-Royce Skip Paris as Car-Show Glitz Fades in Web Age: Companies scramble to woo consumers on Instagram, YouTube

- Informa Agrees to Buy Penton Information for $1.6b: Deal expands U.K.-based information provider in U.S.

- United Technologies Board Hands Chairman Title to CEO Hayes: The 55-year-old executive succeeds Edward Kangas

Looking at regional markets,Asian stocks traded mixed following a similar lead from the US where WTI crude futures declined 3% for the second consecutive day, with price action otherwise subdued amid various market closures in the region. This led to early weakness in ASX 200 (+0.2%) and Nikkei 225 (-1.3%) with the latter also pressured by a firmer JPY. Hang Seng (+0.6%) outperformed its regional counterparts ahead of tomorrow’s closure, after better than expected Chinese New Yuan Loans and Aggregate Financing figures, while mainland China, Taiwan and South Korea had already begun their long weekend. 10yr JGBs traded relatively flat despite the risk averse tone in Japan, while today’s enhanced-liquidity auction also failed to support price action with a lower b/c than prior.

Top Asian News

- Mitsubishi Mulls Lawson Majority Stake Amid Commodity Shift: Japan trading house moving away from commodities businesses

- Japan Shares Slide for 7th Day on Negative-Rate Speculation: Banks pace decline on concern over delayed earnings recovery

- China’s H Shares Go From Best to Worst as Stimulus Bets Recede: shares declined this week as volatility increased

- Australia’s Jobless Rate Declines as Fewer People Seek Work: hours worked fall and underemployment rises in labor market

- Iron Ore Hits the Skids as Miners, Banks Wrangle Over Supply: Vale SA says S11D ramp-up will take four years to complete

- Battleground Shifts to 20-Year Japan Bond as Liquidity Ebbs: analysts say trend to continue if 10-year yield stays negative

- Singapore’s Rough Week for Shipping Foreshadows Challenging 2017: Firms face record $1.8b in bond maturities next year

- China Issues Highest Typhoon Alert as Meranti Makes Landfall: Typhoon Meranti kills 1 in Taiwan

In Europe, equities traded modestly lower initially as participants remain tentative ahead of upcoming risk events. In terms of stock specific news, the UK government has finally confirmed that the Hinkley Point nuclear power plant will go ahead after a new agreement has been agreed. Elsewhere, Morrisons (MRW LN) posted strong earnings which led to shares in the Co. rising just over 7%.

From a sector perspective, energy names remain the worst performers amid further weakness in the energy markets WTI is currently down 0.44%. Finally, in fixed income markets things have been particularly sideways with participants awaiting the latest BoE announcement and US data deluge.

Top European News

- U.K. Approves EDF’s GBP18b Nuclear Power Project: Approval delayed by review of subsidy, Chinese involvement

- SNB Keeps Rates on Hold as Brexit Fallout Clouds Global Outlook: Deposit rate stays at -0.75% as forecast by economists

- VW Extends European Market Share Losses After Diesel Scandal: Industrywide auto sales growth resumed after 1.8% July dip

- U.K. Retail Sales Fall Less Than Forecast as Confidence Holds: Dip follows strongest July increase in sales since 2002

- Nokia CEO Stung by Failed Mergers Speeds Alcatel Integration: ‘World does not wait’ for companies to integrate, Suri says

- Glaxo’s Shingles Shot Maintains Efficacy for Four Years in Study: Filing for FDA approval for Shingrix is on track for 2016

- Morelli Returns to Paschi as CEO to Salvage Rescue Plan: Will lead bank as it prepares for vital recapitalization deal

- Next Sees Tough Quarter Ahead and Price Hikes Coming in 2017: Higher garment costs could drag down sales by as much as 1%

- Morrison Beats Estimates as Potts Brings Stability to Grocer: Three-year cost-saving and cash flow targets will be exceeded

In FX, the Bloomberg Dollar Spot Index added less than 0.1%. The New Zealand dollar led

declines with a 0.3 percent drop, after second-quarter gross domestic

product increased less than economists predicted. Japan’s yen was

little changed at 102.44 per dollar. Morgan Stanley said the Bank of

Japan will probably cut the rate on some bank reserves to minus 0.2

percent from minus 0.1 percent at next week’s meeting. Kyodo News

reported Wednesday that such a move will be considered by the BOJ, while

a Nikkei newspaper article said that the central bank was exploring a

deeper foray into negative rates to stoke inflation. The euro fell

0.1 percent to $1.1242 as a report confirmed that inflation stayed well

below the European Central Bank’s goal last month, and as Governing

Council member Klaas Knot said the institution’s quantitative easing

program will be maintained until the end of 2020 as maturing debt is reinvested.

In Commodities, crude oil traded at $43.81 a barrel following a two-day slide of almost 6 percent. Libya

and Nigeria, two OPEC members whose supplies have been crushed by

domestic conflicts, are preparing to add hundreds of thousands of

barrels to world markets within weeks. U.S. data showed crude stockpiles

fell 559,000 barrels last week, compared with a 4 million gain forecast

in a Bloomberg survey. “The market is getting a little more

conservative about when the balance will return and prices are adjusting

to that,” said Ric Spooner, chief market analyst at CMC Markets in

Sydney. “We have moderating demand combined with the possibility of

increased supplies from Libya and Nigeria. There is also the potential

for non-OPEC output to start increasing.” Copper held near its highest level in almost four weeks in London. It jumped 2.6 percent on Wednesday — the most in three months — after a report showed Chinese lending increased in August by more than economists estimated, brightening the outlook for demand in the world’s top user of industrial metals. Copper producer KGHM Polska Miedz S.A. climbed 1.2 percent, boosting Polish shares. KGHM had fallen as much as 9.7 percent last week.

Bulletin Headline Summary From RanSquawk and Bloomberg

- European equities trade modestly lower as participants remain tentative ahead of upcoming risk events

- UK retail sales exceeded expectations with upwards revisions to the previous’. All eyes now on the BoE

- Looking ahead, highlights include UK rate decisions, UK Retail Sales Data, EU CPI, US Manufacturing, Retail Sales, Industrial Production and weekly jobs report

- Treasuries little changed in overnight trading with global equities mixed, Bank of England rate decision at 7am ET with forecast seeing no change.

- The Swiss National Bank maintained its ultra-loose negative interest-rate policy, with its deposit rate unchanged at a record low of -0.75%, and pledged to intervene in currency markets if needed

- Marco Morelli was CFO at Banca Monte dei Paschi di Siena SpA, Italy’s third-largest bank, and helped led it to the edge of collapse. Now, six years after leaving, Morelli is returning as chief executive officer

- Products synonymous with the credit crisis like “collateralized debt obligations” and “synthetic securitization” are returning as investors take on more risk while banks are forced by regulators to reduce it

- The $13.6 trillion Treasury market is sending a signal it hasn’t flashed in more than four years – shorter-dated debt is the place to be as traders gain confidence the Federal Reserve will keep interest rates on hold

- The BOJ has gained an influential ally in its effort to ease concern over central bank intervention in the nation’s $5 trillion stock market. BlackRock said investor fears of getting crowded out by the BOJ’s exchange-traded fund purchases are overblown

- The offshore yuan headed for the biggest weekly advance since July, with suspected intervention by China’s central bank choking supplies of the currency and driving borrowing costs to an eight-month high

- Amid the most enduring global oil glut in decades, two OPEC crude producers whose supplies have been crushed by domestic conflicts are preparing to add hundreds of thousands of barrels to world markets within weeks

DB’s Jim Reid completes the overnight summary

In terms of the rest of markets yesterday, it had looked like equities might recover some of Tuesday’s losses with most major bourses initially rebounding in the early going, but another sharp leg lower for Oil had the usual pretenders in the energy sector leading markets lower into the close. The S&P 500 (-0.06%), Dow (-0.18%), Stoxx 600 (-0.09%) and DAX (-0.08%) all finished just about in the red although the Nasdaq (+0.36%) did push higher with a decent gain for Apple.

With regards to those Oil moves, WTI (-2.94%) closed back below $44/bbl for just the second time in the last five weeks despite what was actually a fairly bullish release of inventory data. The EIA reported that stockpiles actually fell 600k last week after forecasts were for a gain. That said stockpiles of gasoline and distillates did rise, while the news that Libya is planning to resume shipments from a long-closed port likely also had an impact.

That weak close in the US, combined with a slightly firmer Yen (+0.30%) this morning has seen the Nikkei (-1.20%) and Topix (-1.06%) weaken in early trading. The ASX (-0.18%) has also faded although the Hang Seng (+0.34%) is performing better. Markets in China are closed for a public holiday so overall newsflow is reasonably light.

Away from Oil and the bond market moves yesterday there wasn’t a whole lot more to report. Datawise in the US the only release was a slightly lower than expected import price index reading for August (-0.2% mom vs. -0.1% expected). In Europe the latest industrial production print for the Euro area was slightly softer than expected for July at -1.1% mom (vs. -1.0% expected) while France reported no revision to the August CPI print of +0.3% mom. In the UK the latest employment numbers were also released and largely met expectations. The ILO unemployment rate held steady at 4.9% yoy in the three months to July, while the Claimant Count rate was also unchanged at +2.2% yoy. Average weekly earnings did nudge down two-tenths to +2.3% yoy although that was a couple of tenths ahead of consensus.

That continues the run of largely decent and pretty supportive post-Brexit data in the UK. It’s worth noting that today we have the BoE monetary policy meeting, however our Economists don’t expect the Bank to shift policy today – a view also shared by the wider market. Our economists continue to have the November meeting pencilled in for the next easing.

Yesterday The House View team published a one-page infographic on the debate surrounding the current policy mix. They argue that despite the increasing focus on a shift away from monetary policy, we shouldn’t hold our breath for a swift paradigm shift, given other levers (fiscal easing, structural reform, financial regulation) are unlikely to deliver much. See here for the report: http://pull.db-gmresearch.com/p/11552-ADC1/11106326/DB_TheHouseView_2016….

Looking at the day ahead, we kick off this morning with more data out of the UK, this time in the form of the August retail sales data where a -0.7% mom headline reading is expected which would represent some payback from the strong July data. Following that we’ll get the final revisions to August CPI for the Euro area, along with the July trade data. The Bank of England at midday follows this. It’s a packed diary in the US this afternoon, so hold your breath. The highlight of the early releases will likely be the August retail sales data where expectations are for a small decline (-0.1% mom) in headline sales, but ex auto and ex auto and gas sales to increase +0.2% mom and +0.3% mom respectively. As always the control group component (+0.4% mom expected) is always worth keeping an eye on given its input into the GDP accounts. Also due out will be the August PPI data where prices are expected to have risen modestly, while the Philly Fed manufacturing survey, Empire manufacturing survey and initial jobless claims data are also out early doors. Shortly after we’ll then get industrial production (-0.2% mom expected) for last month, along with capacity utilization, manufacturing production and finally business inventories. If that wasn’t enough, there’s also more Central Bank action in the form of the SNB decision this morning (no change expected).

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed FOR HOLIDAY/ /Hang Sang closed UP 144.95 points or 0.63%. The Nikkei closed DOWN 209.23 POINTS OR 1.63% Australia’s all ordinaires CLOSED UP 0.23% Chinese yuan (ONSHORE) closed HUGELY UP at 6.6583/Oil ROSE to 44.02 dollars per barrel for WTI and 46.21 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.6580 yuan to the dollar vs 6.6583 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS HUGELY AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

3a)NORTH KOREA:

none today

b) REPORT ON JAPAN

The high libor in uSA terms is causing real problems for certain Japanese banks as they are having a tough time finding liquidity. Then this: one major Japanese bank was so desperate that they borrowed 60 billion USA from money market funds last month;

(courtesy zero hedge)

CLSA: “One Major Japanese Bank Is Borrowing $60 Billion From Money Market Funds”

One month ago, when tracing the contagion from the recent surge in Libor rates, we tracked it down in an unexpected location: Japan.

As we reported at the time, “some Japanese lenders have been trying to pre-empt the Libor blow out. Sumitomo Mitsui Financial Group cut its global CP and CD funding by $7 billion in the year to June, while a $28 billion jump in deposits outpaced a $19 billion increase in lending globally, according to Deutsche Bank. As a result, its loan-to-deposit ratio shrank from 149.6 percent in March 2015 to 135.5 percent at end-June. Mitsubishi UFJ also saw its ratio fall to 115.1 percent from 117.8 percent in March 2015 on the back of a rise in deposits.”

The problem, however, is that in the short term, Japanese lenders would unlikely be able to raise enough from deposits to replace the lost access to U.S. money markets. Prime money-market funds slashed their holdings of Japanese securities to $115 billion at the end of July, down 25% from $153 billion two months ago, according to ICI. Previously second to only the U.S. by country of issuer, Japan has now fallen to third behind France.

Being increasingly locked out of money markets means that beyond paying up substantially for U.S. dollars, Japanese banks have few options. Leverage requirements mean global banks are reluctant to provide repos, while foreign-exchange swaps would be a more expensive way to access U.S. dollar funding, said Koichi Sugisaki, a rates strategist at Morgan Stanley MUFG Securities cited by Bloomberg. Three-month CP and CDs now cost roughly 80bp-90bp on an annual basis, but three-month FX forwards have also become more expensive at around 1.5 percent per year, he said.

As we observed at the time, one option for Japanese banks is to access US dollar bond funding, by directly selling short-dated, US-denominated bonds, which could provide Japanese banks with some respite from short-term dollar funding pressure. “Japanese banks could consider issuing short-end bonds from the operating bank level in the future to meet short-term liquidity needs as an alternative to CP/CDs,” said Masanori Kato, head of debt capital markets for J.P. Morgan in Tokyo. “Short-term notes would be a possible alternative avenue, and demand would be there for it as Japanese banks are seen as a safer haven due to Brexit concerns.”

However, even that option may not be feasible. According to Chris Wood, who in his latest Greed and Fear report also observes the ongoing blow out in 3M Libor rates and Libor-OIS spreads, he notes something troubling. To wit: “the new rules require institutional prime money market funds, which are not invested primarily in government debt, to report a floating NAV based on the current value of the assets they hold.”

Then there is this: As a consequence of the pending changes, many prime money market funds have been reclassified to government funds over the past year. Consequently, US prime money market funds’ total assets have declined by US$668bn since the end of October 2015 to US$789bn on 7 September, while government MMFs have risen by US$741bn over the same period to US$1.755tn (see Figure 3).

That, in itself, is not news to our readers. What is, however, is the following:

The above raises an issue for non-government borrowers of US dollars such as Japanese mega banks.For example GREED & fear heard this week in Tokyo that one major Japanese bank is borrowing US$60bn from money market funds.

$60 billion in Libor reliance for just one Japanese bank, whose funding costs on just one tranche increased by hundreds of millions? One wonders just how much pain this and other Japanese banks can sustain as their short-term funding costs soar, while their assets generate less and less income (thanks Kuroda), and more importantly, how long before the “counterparty stigma” trade emerges.

Ironically, and as we pointed out first a month ago, the first casualty to the US Libor blow-out is not be in the US at all, but in Japan, a country whose central bank just managed to unleash the most recent episode of global market turmoil. Something tells us that should the Libor move continue, that risks for Japanese banks will not be “contained.”

c) Report on CHINA

China floods her economy with over 1 trillion yen in new August credit as most of this “total Social Financing” went into house mortgages which is a huge big industry in China and makes up a considerable chunk of their shadow banking sector. This is a house of cards waiting to falter

(courtesy zero hedge)

China Floods Economy With Over Rmb 1 Trillion In New August Credit

When one month ago China announced that it had created just Rmb 488 billion in total new credit as per its broadest credit aggregation metric, Total Social Financing, there was concern among the liquidity addicted community that the PBOC had again hit the brakes on the country’s rampant credit expansion. Those concerns were more than allayed, however, overnight, when the PBOC released its latest August credit data, which not only saw a surge in new Yuan bank loans, but a dramatic jump in TSF – the second highest since 203 – with indications that the shadow banking pipeline, in the form of Bankers Acceptances, which had been shut for most of 2016, is slowly reopening.

The main points from the report:

- August money and credit data were all above expectations. Mortgage loans continued to be strong: medium- to long-term new loans to the household sector were Rmb 529bn.

- Total social financing flows accelerated. In addition to the higher RMB loans, bank acceptance bills also contributed to stronger headline growth (Rmb -38 bn in August, vs Rmb -512 bn in July).

- On a broad basis, after adjusting for local government bond issuance, total financing flows were Rmb 2238 bn, much higher than the Rmb 809 bn in July.

Here are the highlights:

- New CNY loans: Rmb 949 bn in August (RMB loans to the real economy: Rmb 797 bn) vs.consensus: Rmb 750 bn.

- Total social financing (TSF, flow, before adding local government bond net issuance): Rmb 1470 bn in August vs. GSe: Rmb 1300 bn, consensus: Rmb 900 bn, July: Rmb 488 bn.

- M2: 11.4% yoy in August (17.7% SA ann mom) vs. GSe: 11.0% yoy, Bloomberg consensus: 10.5% yoy. July: 10.2% yoy (7.6% SA ann mom by GS).

And the details: adjusted TSF stock soared to Rmb 1.47 trillion exceeding by more than half a median estimate of CNY900 Bn. The figure was a whopping Rmb 1 trillion higher than July’s Rmb 488 Bn. The number rose 16.0% yoy in August, higher than 15.7% in July. The implied month-on-month growth was 18.2% SA ann mom, up from 14.0% in July. (There was Rmb 768 bn of local government bond net issuance in August compared with Rmb 322 bn of issuance in July according to WIND data.) Still, according to the PBOC, TSF stock growth (not adjusting for local government bond issuance) was 12.3% yoy in August, below the year-end target of 13%.

As can be seen in the chart below, “shadow banking”, typically represented by Banker Acceptances, declined by just CNY38 billion, the smallest monthly contraction since March. The series has soaked up nearly CNY2 trillion YTD, and the latest data suggests that China may be easing back from its crackdown on the local shadow banks.

The rebound in money and credit supply supported real economic activity growth in August, as observed in recent Factory and retail sales data. Sequential IP growth rebounded from a mere 2% in July to 6-7% trend level in August. The 18.2% mom sequential TSF growth was meaningfully higher than the 14.0% in July and the second highest reading since August 2013 (only June 2015 growth was comparable at 18.3% mom). Strong sequential real economic activity growth in August was also supported by faster government expenditure growth (August fiscal expenditure at 10.5%yoy, vs 0.3% yoy in July), strong industrial export delivery sequential growth (August export delivery 13%, vs 0.7% in July), and possibly technical factors (a larger number of working days and higher than usual temperatures which boosted items such as power consumption).

This rebound in broad money and credit supply came after the report of slowing money and credit growth amid slowing real economic activity growth in July which led to rising concerns about growth momentum. As a result there was likely an intentional stealth loosening which occurred in August. The stronger than expected activity data in August likely eased policy makers’ concerns about growth momentum but they appear to be highly vigilant on this, for good reasons:

- Export growth was exceptionally high in August given the current pace of external demand and is likely to moderate over the remainder of the year.

- Any beneficial effect of high temperatures on output data should disappear going into September as it is only during the hottest (July and August) and coldest months of the year that temperature has a meaningful impact on activity growth. At other times of the year when temperature is mild variations from the norm make little difference to activity growth.

- G20 related shutdowns, which were only lifted on 7th September, may weigh on industrial activity growth in early September. Although the shutdowns started in August, the reinforcement was probably more stringent in September as the main summit approached.

- Although calendar effects should theoretically be adjusted for in seasonal factors, there may be some residual bias and the effect will go the other way in September (from two more days in August 2016 vs 2015, to one fewer in September 2016).

However, without ongoing domestic policy support, growth could fade again. The State Council regular meeting last week appeared to signal that policy stance has turned more supportive (See China: State Council meeting sent out clear signal of another round of policy loosening, Sep 06, 2016). Recent open market operations by the PBOC since August led to some concerns in the market that the central bank is trying to tighten monetary policy. Today’s data and the State Council meeting should ease those concerns as the broad loosening bias of government becomes increasingly clear.

Finally, this is how Wall Street evaluated the number:

BERNSTEIN (Wei Hou)

- Aug. total social financing, or debt held by individuals and private companies, large beat was due to continuously strong issue of mortgages

- Corporate loans remained weak; lack of medium and long-term loan demand poses risk to economy in 2H

- Household medium-term, long-term loans formed 85% of new loans to non-financial private sector in Aug.

- Prefers big-4 SOE banks over mid-sized banks due to relatively stronger balance sheet

DAIWA (Leon Qi)

- New RMB loan growth continues to rely on households; Sees continued growth in mortgages from Sept. as banks lack other growth drivers

- Higher than expected social finance aggregate growth on shadow banking channels, equity financing

DBS (Shujin Chen)

- Long-term corporate loan decline reflects lower infrastructure project demand after prior strong months

- Strong loans are key for banks’ net interest income improvement

- Prefers banks that would recover earlier than peers, such as China Merchants Bank, Bank of Communications

GOLDMAN SACHS (Nan Li)

- Aug. total social financing driven by robust loan growth, corp. bond issuance and smaller decline in bank acceptances

- Incremental stimulus less likely due to earnings recovery even as credit conditions remain loose

- Corporate earnings recovery on better revenue growth and lower funding cost may stabilize banks NPLs

- Prefers large banks with high dividend yields and mid-caps with strong, improving retail focus

4 EUROPEAN AFFAIRS

SPAIN

Rajoy blows any chance of a coalition when he appoints a person to a lucrative position at the world bank even though he has received graft in the past.

(courtesy Mish Shedlock)

Expect Third Election In Spain: Rajoy Blows Any Coalition Chance With Graft Appointee

Submitted by Mike Shedlock via MishTalk.com,

Any hope of Rajoy securing a coalition or even a minority government via abstention flew out the window yesterday.

Rajoy had secured the backing of Ciudadanos on the premise Rajoy would clean up corruption.

But moments after the last coalition vote, which failed, Rajoy’s economy minister attempted to appoint a corrupt and disgraced colleague to a lucrative position at the World Bank.

Accusations have been ongoing ever since, and yesterday things blew up in Spanish parliament in a very heated debate.

Please consider Spanish Economy Minister Under Fire Over Cronyism.

Luis de Guindos, Spain’s economy minister, faced criticism in parliament on Tuesday over a contentious decision — since withdrawn — to appoint a disgraced former colleague to a lucrative position at the World Bank.

The affair has triggered a political backlash both against Mr de Guindos and against Spain’s caretaker government under Mariano Rajoy, the acting prime minister. In a tense and at times ill-tempered session of the parliament’s economic affairs committee on Tuesday evening, opposition leaders repeatedly accused Mr de Guindos of lying to the public — and urged him to withdraw.

The furore erupted this month, when the government announced that it had nominated José Manuel Soria to serve as Spain’s new executive director at the World Bank. The move came just six months after Mr Soria — a close ally of both Mr Rajoy and Mr de Guindos — resigned as industry minister over the Panama Papers tax haven leak. He was named in the documents as the director of a Panama-based shell company, prompting a denial from Mr Soria that turned out to be false only days later.

His appointment to the World Bank job sparked immediate accusations of cronyism, triggering a political row that forced Mr Soria’s resignation from the post just four days after the announcement was made on September 2. Public suspicions over the decision were heightened because the announcement was slipped out on a Friday night, just minutes after Mr Rajoy failed in his second attempt to secure parliamentary approval for a second term in office. The revelation met with particular fury among leaders of the centrist Ciudadanos party, which had supported Mr Rajoy’s candidacy but only after extracting a promise from him to boost political transparency and step up the fight against corruption.

Third Election Coming Up

With that bit of extreme foolishness, Rajoy all but guaranteed a third election. The only possible way out would be for Rajoy to step down. That’s not likely, and it may not even be enough after this fiasco.

Moreover, this incident is going to hurt Rajoy’s chances very badly in the next election. Rajoy’s days are likely numbered.

Expect a new election in December, possibly earlier if all the political parties give up their attempt to form a government. The other parties may as well give up their chance, as no coalition government at all is possible at this stage.

Besides, from the opposition point of view, it’s better to hold elections as soon as possible after this mess Rajoy’s party created.

END

BANK OF ENGLAND

No surprises here: the Bank of England keeps its rate unchanged at .25%/ The level of QE remains the same. Many members of the Central Bank expect a cut in its rate to zero in the near future

(courtesy zero hedge)

Bank of England Keeps Rate, QE Unchanged As Expected, Hints May Cut More

As was expected by the consensus of economists, and facilitated by the recent surge of positive economic data out of the UK, moments ago the BOE did not surprise, when it kept its interest rate at 0.25% after a unanimous 9-0 vote, which also included keeping the BOE’s government bond and corporate bond purchases unchanged at GBP 435 and 10bn, respectively.

However, while the nine-member Monetary Policy Committee admitted that recent near-term data has been far stronger than anticipated since the Brexit vote, and certainly by comparison to the BOE’s apocalyptic vision, it couldn’t draw inferences for its longer-term forecasts. Officials said their view of the “contours of the economic outlook” hadn’t changed.

In its analysis, the MPC said if the outlook in November is “broadly consistent” with the projections published last month, when it announced a new stimulus package, “a majority of members expected to support a further cut in bank rate to its effective lower bound” later this year. The committee sees that lower limit at close to, but just above, zero.

* * *

Summarizing the statement:

- BOE says MPC majority expect another rate cut this year if economy is broadly consistent with their August projections

- Kristin Forbes, Ian McCafferty say current outlook don’t warrant additional gilt purchases; Forbes says argument also applies to corp. bond purchases

- BOE says initial impact of August stimulus is encouraging

- BOE says some near-term indicators better than expected; 2H GDP growth may slow less than forecast in August

- BOE says MPC view of “contours of economic outlook” are unchanged

- BOE says policy makers will assess recent news at November forecast round

- BOE sees inflation reaching 2% target in 1H 2017

The full statement by the BOE:

The Bank of England’s Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target and in a way that helps to sustain growth and employment. At its meeting ending on 14 September 2016, the MPC voted unanimously to maintain Bank Rate at 0.25%. The Committee voted unanimously to continue with the programme of sterling non-financial investment-grade corporate bond purchases totalling up to £10 billion, financed by the issuance of central bank reserves. The Committee also voted unanimously to continue with the programme of £60 billion of UK government bond purchases to take the total stock of these purchases to £435 billion, financed by the issuance of central bank reserves.

The package of measures announced by the Committee at its August meeting led to a greater than anticipated boost to UK asset prices. Short and long-term market interest rates fell notably following the announcement; corporate bond spreads narrowed, and issuance was strong; and equity prices rose. Since then, some of the falls in yields have reversed, driven by somewhat stronger-than-expected UK data and a generalised rise in global yields.

Many banks announced cuts in Standard Variable Rate and Tracker mortgage rates in line with the cut in Bank Rate. Deposit rates fell in August, although on average these falls were slightly smaller than the cut in Bank Rate. Fixed rates on new mortgage lending also fell.

Overall, while the evidence on the initial impact of the policy package is encouraging, the Committee will monitor closely changes in asset prices and in interest rates facing households and firms and their effect on economic activity.

The MPC set out its most recent detailed assessment of the economic outlook in the August Inflation Report. Based on the data available at that time, the Committee judged that the UK economy was likely to see little growth in the second half of 2016. In light of the tendency for survey indicators to overreact to unexpected events, the Committee expected some bounce-back in surveys of business and consumer sentiment following the sharp falls in the immediate aftermath of the vote to leave the European Union. Nevertheless, since the August Inflation Report, a number of indicators of near-term economic activity have been somewhat stronger than expected. The Committee now expect less of a slowing in UK GDP growth in the second half of 2016.

It was more difficult to draw a strong inference from these data about the Committee’s projections for 2017 and beyond. Moreover, there had been no new information since the August Inflation Report relevant for longer-term prospects for the UK economy.

In the August Inflation Report, the Committee judged that some parts of the economy would be more sensitive than others to heightened uncertainty. Business and housing investment were expected to decline in the second half of 2016, while consumption growth was expected to slow more gradually, alongside households’ real disposable incomes. While most business investment intentions surveys weakened further since the August Inflation Report, the near-term outlook for the housing market is less negative than expected and the indicators of consumption have been a little stronger than expected. Overall, these data remain consistent with the Committee’s judgement in the August Inflation Report that business spending would slow more sharply than consumer spending in response to the uncertainty associated with the United Kingdom’s vote to leave the European Union.

Data on global economic activity have generally been in line with the Committee’s August Inflation Report projections, with growth in the United Kingdom’s major trading partners expected to continue at a modest pace over the next three years.

Twelve-month CPI inflation remained at 0.6% in August, lower than projected at the time of the August Inflation Report, and well below the 2% inflation target. As the unusually large drags from energy and food prices attenuate, CPI inflation is expected to rise to around its 2% target in the first half of 2017, consistent with the August Inflation Report, albeit with the projection a little lower over the remainder of 2016 than had been anticipated in August.

The Committee’s view of the contours of the economic outlook following the EU referendum had not changed. News on the near-term momentum of the UK economy had, however, been slightly to the upside relative to the August Inflation Report projections. The Committee will assess that news, along with other forthcoming indicators, during its November forecast round. If, in light of that full updated assessment, the outlook at that time is judged to be broadly consistent with the August Inflation Report projections, a majority of members expect to support a further cut in Bank Rate to its effective lower bound at one of the MPC’s forthcoming meetings during the course of this year. The MPC currently judges this bound to be close to, but a little above, zero.

Against that backdrop, at its meeting ending on 14 September, MPC members judged it appropriate to leave the stance of monetary policy unchanged.

Merkel Meets With German CEOs To Address 99.97% Unemployment Among “Highly Unqualified” Migrants

It’s been a bad couple of months for German Chancellor Angela Merkel, whose approval ratings have fallen sharply over her continued support of open-border immigration policies that have allowed over 1 million refugees to flow into the country since 2015. Increasingly more Germans have blamed Merkel for the surge in refugee terrorist attacks over the past couple of months and have shifted their support to more nationalist-leaning political parties. In fact, just a few weeks ago Merkel suffered a massive, embarrassing defeat in her home state to her nemesis, the anti-immigation AfD party (see “Merkel Stunned By Defeat To Anti-Immigrant Party In Her Home State“). Alas, despite calls from voters for a shift in Germany’s immigration policies, Merkel continues to double down.

One of the original selling points for accepting migrants from the Middle East was the apparent economic “benefits” associated with adding 100,000s of new, young consumers/laborers to the German economy. In fact, the wave of new immigrants was sold as the perfect solution for Germany’s demographic dilemma which is expected to see its working-age population shrink by 6 million people by 2030.

While it sounded like a great plan, it doesn’t really work that well if new migrants fail to find jobs and become economically productive members of society which, according to Reuters, is exactly what is happening. Apparently,German companies have only been able to find jobs for about 100 of the 1 million migrants that have recently found their way into the country.

According to the latest figures from the German Labor Office, about 346,000 people with asylum status were seeking jobs in Germany in August. With 100 migrants actually employed, that’s an unemployment rate of about 99.97%.

While a “good” start, we suspect Merkel planned be slightly further along by now in achieving her original goal of 100,000 new job opportunities for migrants.

As such, yesterday, Merkel hosted a meeting with the CEO’s of Germany’s largest

corporations to see what could be done to find jobs for Germany’s unemployed migrants that were, for the time being, still being supported by the German taxpayers. Apparently, Merkel quickly discovered that it’s difficult to employ people who can’t prove their qualifications, don’t speak German and have an uncertain immigration status.

Many of the companies say a lack of German-language skills, the inability of most refugees to prove any qualifications, and uncertainty about their permission to stay in the country mean there is little they can do in the short term.

A survey by Reuters of the 30 companies in Germany’s DAX stock market index found they could point to just 63 refugee hires in total. Several of the 26 firms who responded said they considered it discriminatory to ask about applicants’ migration history, so they did not know whether they employed refugees or how many.

Of the 63 hires, 50 are employed by Deutsche Post DHL, which said it applied a “pragmatic approach” and deployed the refugees to sort and deliver letters and parcels.

“Given that around 80 percent of asylum seekers are not highly qualified and may not yet have a high level of German proficiency, we have primarily offered jobs that do not require technical skills or a considerable amount of interaction in German,” a spokesman said by email.

Other companies cited that migrants are having difficultly meeting German regulatory requirements to pass a background check.

Others among Germany’s top listed companies, mainly in the financial or airline sectors, say it is practically impossible for them to take on refugees at all. They cite regulatory reasons such as the need for detailed background checks on staff.

But we thought everyone was being heavily vetted? Surely if refugees can pass a “thorough” government screening they should have no problem with a quick corporate background check, right?

end

After a humiliating defeat in her own home town last month, Merkel is bracing for more misery with the Berlin area elections this Sunday:

(courtesy zero hedge)

Merkel Braces For More Misery With Humiliating Berlin Election Rout

Two weeks ago we reported that chancellor Angela Merkel was facing humiliation, political defeat in in an election in her home state. Sure enough, she lost by a wide margin, with the anti-immigrant AfD party soaring in the first shock result of the current political cycle. That, however, was only the beginning because as Reuters writes today, still reeling from the state election rout, Angela Merkel’s conservatives “are bracing for further losses in the Berlin city vote on Sunday.”

Following the CDU’s disastrous performance in the election in Mecklenburg-Vorpommern, Merkel’s home state, which pushed Merkel’s party into an unprecedented third place by the AfD, her conservative CSU allies in Bavaria have blamed Merkel personally and demanded a migrant cap, which she rejects. Polls show the center-left Social Democrats (SPD) may be able to drop Merkel’s Christian Democrats (CDU) as coalition partners in the capital’s assembly.

Meanwhile, with the ruling coalition in shambles as a result of Merkel’s widely unpopular immigration policies, the AfD, which has won seats in nine of Germany’s 16 states, has soared by successfully playing on immigration concerns, validated most recently on Wednesday night by the violence between locals and refugees in the German town of Bautzen.

Meanwhile, even the locals are pushing back against Merkel: Berlin candidate Georg Pazderski has said: “I favor educating these people (immigrants) but not integrating them. We must prepare them for going back.”

Not surprisingly, then, after its humiliation in Mecklenburg-Vorpommern, the CDU continues to slide. An INSA poll this week put the CDU on 18 percent in Berlin, down more than five points from the 2011 vote and only four points ahead of the AfD. The SPD – which is in coalition with Merkel at the federal level – is expected to remain the biggest party in Berlin and aims to form a coalition with the Greens and radical Left. They are led by printer Michael Mueller, who acknowledges he falls short in the “glamour” stakes compared with his party-loving predecessor Klaus Wowereit who dubbed Berlin “poor but sexy”.

Meanwhile Merkel, cheered by modest 2,500 conservative supporters at a recent rally in the leafy western suburb of Lichterfelde on a sunny evening, knows what is at stake, especially as it is only a year unril the next federal election. The chancellor’s “open door” policy decision a year ago to open German borders has crushed her popularity and dominated the campaign, boosting support for the anti-immigrant Alternative for Germany (AfD)party. What is most surprising is that judging by her actions,she still fails to realize this.

And while she has no obvious rival, Reuters writes that the losses have raised questions about whether she will even run for a fourth term in 2017.