Gold $1337.20 up $3.20

Silver 19.73 down 29 cents

In the access market 5:15 pm

Gold: 1337.50

Silver: 19.67

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix Sept 23 (10:15 pm est last night): $ 1337.14

NY ACCESS PRICE: $1335.60 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1337.14

NY ACCESS PRICE: 1333.40 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Sept 23: 5:30 am est: $1335.90 (NY: same time: $1335.30: 5:30AM)

London Second fix Sept 16: 10 am est: $1338.65 (NY same time: $1338.45 , 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:The front September contract month we had 48 notices filed for 4800 oz

For silver: the front month of September we have a total of 50 notices filed for 250,000 oz

Yesterday, we noticed that silver was languishing relative to gold and also the gold/silver equity shares also started to swoon. That was a good sign that they were going to whack today. Friday is a good day for the crooks because the huge physical market in London is already put to bed.

During the night, the boys knocked gold down to $1333 but somehow the demand for gold was just too great as it recovered to the break even point and that is when London closed. The bankers then had a free rein to knock gold down where it finished at 1337.50. However the bankers continued with their temper tantrum and they took it on our poor gold/silver equity shares as these guys were whacked pretty hard.

Do not fret. By Monday morning gold will resume a little northern trajectory. However we still have the comex options expiry, finishing on Tuesday night and the oTC/LBMA options finishing next Friday night, on first day notice for the October contract months.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 4890 contracts UP to 198,391. The open interest FELL as the silver price was UP 33 cents in yesterday’s trading .In ounces, the OI is still represented by just LESS THAN 1 BILLION oz i.e. .991 BILLION TO BE EXACT or 142% of annual global silver production (ex Russia &ex China).

In silver we had 50 notices served upon for 250,000 oz

In gold, the total comex gold fell by 10,066 contracts as the price of gold rose BY $13.50 yesterday . The total gold OI stands at 586,812 contracts. The level of OI is still good for us as it will support a rise in gold price and it will be hard for the boys to raid.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

LAST NIGHT WE HAD A SMALL CHANGE, A DEPOSIT OF .30 TONNES INTO the GLD/

Total gold inventory rest tonight at: 951.22 tonnes of gold

SLV

we had a huge change with respect to inventory at the SLV: a deposit of 1.044 million oz

THE SLV Inventory rests at: 364.523 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver rose by 4455 contracts up to 202,846 as the price of silver ROSE by 33 cents with yesterday’s trading.The gold open interest rose by 10,066 contracts up to 586,812 as the price of gold rose $13.50 IN YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

end

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 8.42 POINTS OR .28%/ /Hang Sang closed DOWN 73.32 POINTS OR .31%. The Nikkei closed DOWN 53.60 POINTS OR .32% Australia’s all ordinaires CLOSED UP 1.06% /Chinese yuan (ONSHORE) closed DOWN at 6.6704/Oil FELL to 46.16 dollars per barrel for WTI and 48.03 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.6704 yuan to the dollar vs 6.6753 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)Korea:

none

b) REPORT ON JAPAN

We have now had 2 days since the Bank of Japan introduced their new policy on QQE. They are trying to target the upper end of the yield curve. The problem with that is that it is much more difficult to control longer term rates. Central bankers can always control the short end of the curve, but the long end has a mind of its own

in other words..the call this new policy disastrous..

( zero hedge)

c) REPORT ON CHINA

none today

4 EUROPEAN AFFAIRS

i)Now there is no question that problems are surfacing inside Deutsche bank when we start to see German politicians getting nervous:

( zero hedge)

ii)A great commentary on the problems facing Italy with respect to the rest of Europe. Italy will propose austerity and hope that the EU grants them concessions to helping them with their huge banking problems

George Frideman/Mauldin Economics.com

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

Low oil is keeping inflation in Canada at zero. However retail sales missed expectations as their economy falters badly.

( zero hedge)

7.OIL ISSUES

i)This morning the rumours started with the Saudis offering to cut oil production if Iran freezes their output (according to Reuters)

( hedge/Reuters)

ii)We all agree that Iran is unlikely to accept a production oil cut!

( zero hedge/Bloomberg)

iii)As promised this proposal did not last long: Iran refuses to cap output;

( zero hedge)

iv) Oil tumbles back to the 44 dollar handle after the Saudis confirm that there will be no decision next week. Also the Fed wants a crackdown on bank commodity holdings, something I brought to your attention last week. However do not your breath as it will take considerable time for this to happen.

( zero hedge)

v)USA rig count rises to a 7th month high and this should increase oil production quite dramatically. Oil extends its losses on the day

( zero hedge)

8.EMERGING MARKETS

none today

9.PHYSICAL STORIES

i)We brought you this story yesterday but it is worth repeating. Russia’s largest bank Sberbank is now a member of the Shanghai Gold Exchange and it will act as an intermediary in purchasing 100 tonnes of gold per year for both sovereign China and citizens

a very big story..

(GATA/Bloomberg)

ii)Alasdair Macleod..with this weekly commentary and message to us:

( Alasdair Macleod/GoldMoney.com)

iii)Belkin and I agree: the Fed’s next move will be easing and not raising rates

( Belkin/Kingworldnews)

iv)A big story: The Fed continues with its push to restrict banks in the commodity business

( Market Watch)

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)Not a very good stat for the USA authorities: New York has now a 60% increase in homelessness. And they call this a recovery?

(courtesy zero hedge)

ii)This is interesting! Both individuals from Platte, Bryan Pagliano and Combetta were given immunity with respect to the Hillary Clinton email scandal and yet both refuse to testify. Their testimony cannot hurt themselves so why did they not testify. The oversight committee will now state that they both are in contempt of Congress:

( zero hedge)

iib)Here is how one twitter user proved the intent that Hillary’s campaign tried to destroy and or tamper with federal records

( zerohedge)

iic)No comment necessary: the judge orders that most of Hillary’s deleted emails will be released after the election due to the huge number of lawsuits filed.

(courtesy zero hedge)

iii a)What is behind the Charlotte riots. Actually 70% of the protesters are outside the state

( zero hedge)

iiib)In reality this is what is going on:

“What was unfolding in Charlotte – and may still be – is not a protest. It’s a violent, unjustified riot by criminals and thugs.”

(zero hedge)

iv)Markit’s PMI for Sept (Manufacturing) missed expectations of 52.0 coming in at 51.4. New orders and inventories declined but payrolls picked up modestly despite lower output.

Let us head over to the comex:

The total gold comex open interest ROSE BY AN HUGE 10,066 CONTRACTS to an OI level of 576,746 as the price of gold ROSE by $13.50 with YESTERDAY’S trading. We are now in the NON active month of SEPTEMBER/

The contract month of Sept saw it’s OI FELL by 46 contract DOWN to 195. We had 66 notices filed yesterday so we gained 20 gold contracts or an additional 2000 gold ounces will stand for delivery. SOMEBODY AGAIN WAS IN GREAT NEED OF PHYSICAL GOLD. The next delivery month is October and here the OI lost 1659 contracts DOWN to 25,590. The next contract month of December showed an increase of 11,225 contracts up to 446,479. The estimated volume today at the comex: 131,769 which is WEAK. Confirmed volume on yesterday: 181,740 which is fair.

And now for the wild silver comex results. Total silver OI ROSE BY A HUGE 4455 contracts from 198,391 UP TO 202,846 with the RISE in price of silver to the tune of 33 cents yesterday. We are moving NOW CLOSER TO the all time record high for silver open interest set on Wednesday August 3: (224,540). We are now into the next active month of September and here the OI fell by 21 contracts down to 562. We had 27 notices filed upon yesterday so we GAINED 6 contracts or 30,000 additional oz will stand for delivery in this active month of September. The next non active delivery movement of October lost 4 CONTRACTS TO 433 contracts. The next big delivery month is December and here it ROSE by 4338 contracts UP to 177,271. The volume on the comex today (just comex) came in at 46,811 which is very good. The confirmed volume yesterday (comex and globex) was huge at 76,478 . Silver is not in backwardation. London is in backwardation for several months.

today we had 50 notices filed for silver: 135,000 oz

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz |

NIL |

| Withdrawals from Customer Inventory in oz nil |

65,907.500 oz

2050 kilobars

Scotia

|

| Deposits to the Dealer Inventory in oz | 5500.01 oz

Brinks ?? |

| Deposits to the Customer Inventory, in oz |

48,293.234 oz

Scotia

|

| No of oz served (contracts) today |

48 notices

4,800 oz

|

| No of oz to be served (notices) |

147 contracts

(14,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

261300 contracts

261,300 oz

8.1275 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | 192.90 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 387,589.6 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 48 contract of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped (received) by jPMorgan customer account.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

856,256.000 oz

CNT, Scotia

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

180,332.500 oz

JPM

|

| No of oz served today (contracts) |

50 CONTRACTS

(250,000 OZ)

|

| No of oz to be served (notices) |

512 contracts

(2,560,000 oz)

|

| Total monthly oz silver served (contracts) | 2676 contracts (13,380,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 7,129,518.6 oz |

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 326,326 | 70,147 | 50,995 | 120,314 | 410,929 | 497,635 | 532,071 |

| Change from Prior Reporting Period | ||||||

| -25,450 | 3,784 | -1,497 | 3,473 | -17,283 | -23,474 | -14,996 |

| Traders | ||||||

| 187 | 98 | 89 | 51 | 64 | 289 | 210 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 61,156 | 26,720 | 558,791 | ||||

| 7,263 | -1,215 | -16,211 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, September 20, 2016 | |||||

And now for our silver COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 113,567 | 30,932 | 8,339 | 45,909 | 142,854 | |

| -225 | -1,292 | 165 | 430 | 700 | |

| Traders | |||||

| 116 | 43 | 35 | 33 | 40 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 193,501 | Long | Short | |

| 25,686 | 11,376 | 167,815 | 182,125 | ||

| -822 | -25 | -452 | 370 | -427 | |

| non reportable positions | Positions as of: | 165 | 105 | ||

| Tuesday, September 20, 2016 | |||||

end

NPV for Sprott and Central Fund of Canada

end

And now your overnight trading in gold,FRIDAY MORNING and also physical stories that may interest you:

Savings Guarantee? U.N. Warns Next Financial Crisis Imminent

Savings Guarantee? U.N. Warns Next Financial Crisis Seems Imminent

“There remains a risk of deflationary spirals in which capital flight, currency devaluations and collapsing asset prices would stymie growth and shrink government revenues. As capital begins to flow out, there is now a real danger of entering a third phase of the financial crisis …”

UN Conference on Trade and Development’s Annual Report (UNCTAD), September 22, 2016

Image from “Extraordinary Popular Delusions and the Madness of Crowds” by Charles Mackay – Wikipedia

Image from “Extraordinary Popular Delusions and the Madness of Crowds” by Charles Mackay – Wikipedia

This hard hitting critique in the UN Conference on Trade and Development’s Annual Report, released this week, is suggesting that the ‘third leg of the world’s intractable depression is yet to come.’

“Alarm bells have been ringing over the explosion of corporate debt levels in emerging economies, which now exceed $25 trillion. Damaging deflationary spirals cannot be ruled out,” said the annual report of the UN Conference on Trade and Development (UNCTAD).

But what does these grand, scary predictions really mean for us? Bankruptcy? Economic collapse? Apocalypse now? End of the world as we know it?

The UN economists certainly think that a la 2007/2008, we are on the verge of the third leg of the global financial crisis – with prospect of epic debt defaults.

We may soon experience the end of the financial world as we know it … but investors and savers feel fine! Many bond and stock markets, including the S&P 500, continue on their merry way to all time record highs.

Few know, or (it seems) care anymore. As we end yet another week with yet another anticlimactic announcement from the “all powerful” Fed, it is understandable that many of us are feeling some cognitive dissonance when it comes to the real impact of central bank announcements, economic forecasts and political changes.

Bail-In Regime Cometh

There was one major ‘solution’ to the crisis that was announced in recent years with so much spin you would be forgiven for thinking it has little to do with you. When in truth you are the one who could be most affected.

In 2012 the release of a joint paper from the US Federal Deposit Scheme and the Bank of England included the words; “deposit schemes may have to contribute to the recapitalisation of a failed bank”. Bail-ins in the UK banking system had become a possibility.

This was made official by a “watershed” moment in 2014 when Mark Carney announced the end of the bail-out era, he was calling time on ‘too big to fail’ for banks.

“Let’s face it, the system we’ve had up until now has been totally unfair…The banks and their shareholders and their creditors got the benefit when things went well. But when they went wrong, the British public and subsequent generations picked up the bill – and that’s going to end.”

The media, politicians and until now, the general public fell for this. The promise of no more bailouts has resulted in feelings of reassurance that the taxpayer won’t be asked to foot the bill when irresponsible bankers mess up.

But this is fundamentally wrong. As we outline in a forthcoming report on bail-ins, the British public and subsequent generations are still going to be ‘picking up the bill’.

For the first time depositors in the form of retail savers and companies with capital, (who also happen to be taxpayers) will also be exposed in the event of governments bailing out banks again.

But what about the much supported Deposit Guarantee Scheme? It’s unlikely to last, or mean much when crunch time comes.

“It is not enough to have just a Deposit Guarantee Scheme [for a major bank rescue] if the losses are vast enough, then the haircuts imposed by the resolution authority can in principle permeate to any level of the creditor stack. In the case of insured deposits, that means Deposit Guarantee Schemes suffering losses …”

Paul Tucker, Deputy Governor Financial Stability of theBank of England, October 2013

In the EU depositors are protected by some form of a deposit guarantee scheme, EUR100,000 or £75,000 for UK depositors, is protected in the event of bank failure. However, as we outline in our forthcoming report this amount or even any kind of insurance, is not guaranteed. Some politicians and think tanks are even recommending that deposit guarantee schemes be removed.

What does this mean in the context of a forthcoming third financial crisis and are your savings”guaranteed”?

Next week Our Guide to Bail-ins will outline how likely UK depositors are to being subject to bail-ins and how they can set about protecting themselves from bail-ins.

Gold and Silver Bullion – News and Commentary

Gold steady, set for biggest weekly gain in two months (Reuters)

Gold shines as dollar slips after Fed decision (Reuters)

Manufacturing behind decline in leading indicators in August (MarketWatch)

Sales of Existing U.S. Homes Unexpectedly Declined in August (Bloomberg)

Russia Targets China for Gold Sales as VTB, Sberbank Expan (Bloomberg)

Gold Sparkles as Central Bank Largesse Burnishes Investor Demand (Bloomberg)

Bank of Japan: we have complete control of the bond market (MoneyWeek)

Pension survival: in the worst case, your pot could fall 60pc in 15 years (Telegraph)

$195 Billion Asset Manager: “The Time Has Come To Leave The Dance Floor” (ZeroHedge)

America Is Not the Greatest Country on Earth. It’s No. 28 (Bloomberg)

Gold Prices (LBMA AM)

23 Sep: USD 1,335.90, GBP 1,027.17 & EUR 1,192.16 per ounce

22 Sep: USD 1,332.45, GBP 1,019.59 & EUR 1,186.68 per ounce

21 Sep: USD 1,319.60, GBP 1,015.96 & EUR 1,183.81 per ounce

20 Sep: USD 1,315.40, GBP 1,011.02 & EUR 1,175.84 per ounce

19 Sep: USD 1,315.05, GBP 1,007.99 & EUR 1,177.36 per ounce

16 Sep: USD 1,314.25, GBP 995.68 & EUR 1,170.08 per ounce

15 Sep: USD 1,320.10, GBP 998.26 & EUR 1,174.23 per ounce

Silver Prices (LBMA)

23 Sep: USD 19.82, GBP 15.28 & EUR 17.66 per ounce

22 Sep: USD 19.88, GBP 15.22 & EUR 17.69 per ounce

21 Sep: USD 19.43, GBP 14.95 & EUR 17.43 per ounce

20 Sep: USD 19.17, GBP 14.78 & EUR 17.15 per ounce

19 Sep: USD 19.12, GBP 14.65 & EUR 17.13 per ounce

16 Sep: USD 18.91, GBP 14.36 & EUR 16.85 per ounce

15 Sep: USD 18.96, GBP 14.32 & EUR 16.87 per ounce

Recent Market Updates

– Gold Up 1.5%, Silver Surges 3% – Yellen Stays Ultra Loose At 0.25%

– Trump and Clinton Are “Positive For Gold” – $1,900/oz by End of Year

– Gold Bugs Rejoice – Central Banks Think You’re On To Something

– ‘Hard’ Brexit Looms For Ireland

– EU Bail In Rules Ignored By Italy – Mother Of All Systemic Threats and World

– War?– Buy Gold – Bonds Are ‘Biggest Bubble In World’ – Billionaire Singer Warns

– Silver Bullion Market – “Most Bullish Story Ever Told?”

– “Sorry, You Can’t Have Your Gold Bullion”

– Global Stocks, Bonds Fall Sharply – Gold Consolidates After Two Weeks Of Gains

– Gold, Silver, Blockchain and Fintech – Solutions To Negative Rates, Bail-ins, Cash Confiscations and Cashless Society

– Jan Skoyles Appointed Research Executive At GoldCore

– Silver Bullion Surges 3.5% To Over $20/oz

– Ireland “Especially Exposed” To “International Shocks” Warns Central Bank

end

We brought you this story yesterday but it is worth repeating. Russia’s largest bank Sberbank is now a member of the Shanghai Gold Exchange and it will act as an intermediary in purchasing 100 tonnes of gold per year for both sovereign China and citizens

a very big story..

(GATA/Bloomberg)

Russian banks aim to sell gold to China as VTB, Sberbank expand

Submitted by cpowell on Thu, 2016-09-22 21:27. Section: Daily Dispatches

By Yuliya Fedorinova

Bloomberg News

Thursday, September 22, 2016

Russia’s gold sales in China are set to expand as VTB Capital boosts sales and Sberbank PJSC prepares to enter the market, chasing demand in the world’s biggest consumer of bullion.

Sberbank CIB plans to register on the Shanghai Gold Exchange and eventually to sell up to 100 tons (3.2 million ounces) a year, according to an e-mail from the investment arm of Russia’s largest bank. VTB Capital, a unit of the second-biggest lender, is targeting sales of as much as 20 metric tons of gold in China in 2017, Sergey Nenashev, the bank’s head of precious metals, said by e-mail. Sales may reach a rate of 100 tons a year near the end of 2018, he said.

Russian banks, which act as intermediaries between the country’s gold producers and the market, aim to tap into Asian growth. Rising incomes and few investment options in China are driving demand for gold jewelry, bars, and coins in China. In July, Shanghai Gold Exchange volumes almost doubled from a year earlier to 1.7 trillion yuan ($255 billion), figures compiled by the bourse show. …

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2016-09-22/russia-boosts-gold-sal…

end

Alasdair Macleod..with this weekly commentary and message to us:

(courtesy Alasdair Macleod/GoldMoney.com)

Alasdair Macleod: The root cause of monetary confusion

Submitted by cpowell on Thu, 2016-09-22 21:37. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney.com, St. Helier, Jersey, Channel Islands

Thursday, September 22, 2016

Arguments about sound and unsound money often degenerate into a them-and-us dispute, with the supporters of unsound money casting sound money proponents as impractical out-of-date libertarian weirdos.

Supporting one side or the other as if they were opposing football teams does not represent constructive debate, which must be approached with an open mind.

This has now become crucial, because conventional and even unconventional monetary policies have demonstrably failed in their objectives, so it is time to look at the problem from another angle. This article does this by drawing on the implications of Gibson’s Paradox, its recent resolution, and its apparent absence in the post-Volcker years. …

… For the remainder of the commentary:

https://wealth.goldmoney.com/research/goldmoney-insights/the-root-cause-…

end

Belkin and I agree: the Fed’s next move will be easing and not raising rates

(courtesy Belkin/Kingworldnews)

Fed’s next move will be easing, not raising, Belkin tells King World News

Submitted by cpowell on Thu, 2016-09-22 21:48. Section: Daily Dispatches

5:46p ET Thursday, September 22, 2016

Dear Friend of GATA and Gold:

Market analyst Michael Belkin bludgeons the Federal Reserve pretty well in comments to King World News this week.

Despite all the Fed’s talk about raising interest rates amid a strengthening economy, Belkin says, “We are teetering on a recession. So I expect that the next Fed move will actually be an easing. They are just waiting for the next election and they are spreading misinformation to make people feel confident about the economy before the election so Obama’s henchwoman gets re-elected.”

An excerpt from the interview is posted at KWN here:

http://kingworldnews.com/top-advisor-to-sovereign-wealth-funds-says-this…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A big story: The Fed continues with its push to restrict banks in the commodity business

(courtesy Market Watch)

Fed proposes to restrict bank involvement with physical commodities

Published: Sept 23, 2016 12:00 p.m. E

WASHINGTON (MarketWatch) — The Federal Reserve on Friday moved forward on a plan to make it more difficult for banks to be involved in physical commodities, citing the legal, reputational and financial risks from disasters such as the BP oil spill. Under the proposal, firms would have to hold more capital, not be able to engage in activities involving power plants and not be allowed to own or store copper. Two banks, Goldman Sachs GS, -1.27% and Morgan Stanley MS, -1.35% have relied on a grandfather clause to engage in physical commodity business that hasn’t been authorized for other Fed-regulated banks, while 12 banks, including Bank of America BAC, -0.32% Citi C, -0.06% and J.P. Morgan Chase JPM, +0.16% are involved in physical commodity trading, energy management and energy tolling activities to some degree.

-END-

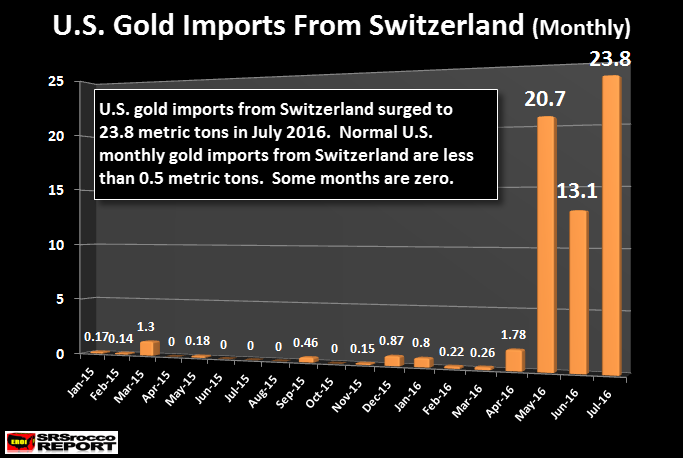

Steve St Angelo discusses the huge increase in USA importation of gold from Switzerland He gives his reasons why this is happening!

(courtesy Steve St Angelo/SRSRocco report)

U.S. Imports Record Amount Of Gold From Switzerland In July

It seems as if the tide has changed as the U.S. imported a record amount of gold from Switzerland in July. Normally, the flow of gold from the United States has been heading toward Switzerland. For example, when the U.S. exported a record 691 metric tons (mt) of gold in 2013, Switzerland received 284 mt, which accounted for 41% of the total. Compare that to the paltry 3 metric tons of gold imported from Switzerland that very same year.

However, something has changed in the market dynamics as the U.S. imported a record 23.8 mt of gold from Switzerland in July:

As I stated in my previous article, WHAT’S GOING ON?? Record Swiss Gold Flow Into The United States: the Swiss exported 20.7 mt of gold in May 2016, up considerably from its monthly average 0.4 mt. Even though gold imports from Switzerland declined the next month to only 13.1 mt in June, they were still much higher than their monthly average going back until Jan. 2015.

But, as we can see… U.S. gold imports from Switzerland jumped 82% in July to 23.8 mt compared to June. There has been speculation in the precious metals community as to why the Swiss are now exporting gold to the United States. While many theories seem plausible, the one that makes the most sense is that investors in Europe who have their gold stored in Switzerland are moving it to the United States to protect it from the implications of negative interest rates.

Furthermore, after the Brexit vote for the U.K. to leave the European Union (In June), it has also put a lot of stress on investors holding assets within the E.U. countries. For whatever reason, gold bullion is now flowing into the United States from Switzerland in record volume for the first time in many years.

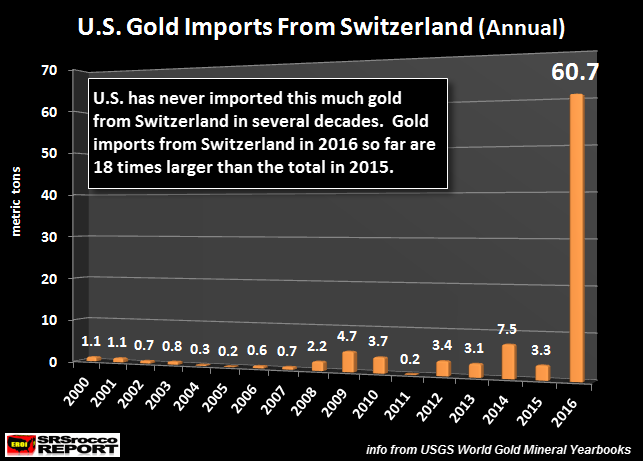

This next chart shows the annual imports of gold from Switzerland going back until 2000:

As we can see, Switzerland’s gold exports to the U.S. are already 60.7 mt in 2016, up more than 18 times the volume in 2015. Again, for whatever reason, Swiss gold is heading into the United States in record volume.

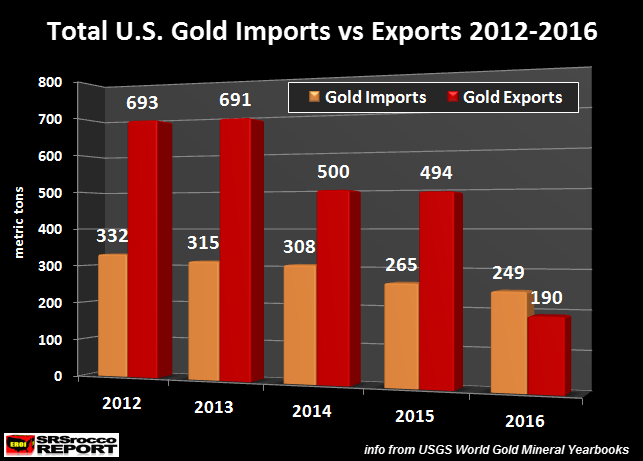

In addition, this is the first year the U.S. has imported more gold than it has exported in several years:

In 2012, the United States exported a record 693 mt of gold, while imports were only 332 mt. Even though the volume of U.S. gold exports declined in 2014 and 2015, they were still much higher than imports (62% & 86% respectively).

However, this has changed in the first seven months of 2016, as the U.S. has imported 249 mt of gold versus exports of only 190 mt. The majority of the increase of U.S. gold imports came from Switzerland. Of the 249 mt of U.S. gold imports Jan-July 2016, Switzerland accounted for 60.7 mt, compared to only 3 mt in 2015.

With the upcoming Chinese Yuan into the IMF SDR (Special Drawing Rights) on Oct 1st, the situation for the U.S. Dollar going forward will come under increased stress as global trade moves more into Chinese Yuan currency. This will negatively impact the U.S. Treasury holdings by foreigners as they move into owning more Chinese Yuan for trade.

The days of the U.S. Dollar Reserve currency status is coming to an end. It is no surprise that Russia and China continue to add a great deal of gold to their official holdings.

Lastly, I will be publishing a very important article on the precious metals next week. It will provide analysis on the top four precious metals (Gold, Platinum, Palladium and Silver) that most investors have not seen before. It will be out either Monday or Tuesday next week.

-END-

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.6704( DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN WIDENS TO 6.6753 / Shanghai bourse CLOSED DOWN 8.42 POINTS OR .28% / HANG SANG CLOSED DOWN 73.32 POINTS OR 0.31%

2 Nikkei closed DOWN 53.60 OR .32% /USA: YEN FALLS TO 100.74

3. Europe stocks opened ALL IN THE RED ( /USA dollar index UP to 95.39/Euro UP to 1.1218

3b Japan 10 year bond yield: LOWERS TO -.043%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 100.74/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 46.16 and Brent: 48.03

3f Gold DOWN /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS to -.093%

3j Greek 10 year bond yield FALLS to : 8.40%

3k Gold at $1337.60/silver $19.81(7:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble UP 20/100 in roubles/dollar) 63.44-

3m oil into the 46 dollar handle for WTI and 48 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 100.74 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9704 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0886 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLS to -.093%

/German 10+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.606% early this morning. Thirty year rate at 2.323% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Central Bank-Driven Stock Rally Fizzles; Crude Rebounds On Saudi Oil Production Cut Report

Until several minutes ago, the rebound in global equities observed this week on the back of continued easy central bank policy, appeared to be running out of steam as oil retreated from a two-week high and a dollar slide ended. Sovereign bonds were headed for their biggest weekly gain since July, buoyed by central bank commitments to keep monetary policies loose.

However, as noted just around 6am, Reuters reported, citing as it usually does various “anonymous sources”, that in a radical departure from its long-held policy of not cutting production, Saudi Arabia was prepared to cut production on the condition that Iran freezes output, as a result of which oil promptly spiked, erasing all the day’s losses, and more importantly, providing a support to US equity futures just as they were rolling over.

(Harvey: this no doubt is a false story)

According to UBS oil analyst Giovanni Staunovo; “The answer from Iran is still pending, so there is no agreement yet,” adding that “considering where Saudi production stands, it’s a smart move to say they’re willing to cut production.”

Until the Reuters rumor, the MSCI All Country World Index had declined for the first time this week, while gold fell for the first time this week. Crude had fallen below $46 a barrel with investors weighing prospects for major producers to agree output constraints at talks next week in Algiers, however it then promptly jumped in the mid-$46 range on the Saudi-Iran report. China’s 10-year bond yield fell to its low for the month, while Germany’s increased following its biggest drop since June.

OPEC troubles aside, it was all central banks in the drivers’ seat as stocks, bonds and commodities climbed this week and the dollar lost ground versus almost all of its major peers after the Fed scaled back plans for interest-rate increases in 2017 and beyond. Investor sentiment also got a lift as the Bank of Japan strengthened its commitment to reviving inflation, while Indonesia and Turkey cut interest rates as New Zealand’s central bank signaled further easing.

“There’s a very bullish case for equities considering that the Fed is now expecting only two rate hikes in 2017,” said James Woods, a strategist at Rivkin Securities in Sydney. “There are uncertainties that could shake up some volatility in the market, including the U.S. elections in November.”

Ironically, the S&P was on the cusp of all time highs as earnings continue rolling over: “Given that macro surprises typically lead earnings revisions by 4 weeks, renewed downside is building. We think 2017 earnings expectations are particularly vulnerable. In Europe, consensus is still expecting 12.9% EPS growth for the Stoxx 600, which would be the highest growth rate since 2010, and materially above our forecast of 5.9%,” Deutsche Bank strategists, including Wolf von Rotberg and Sebastian Raedler, write in note.

In economic news, we got the latest European Flash Mfg and Services PMI data, which was mixed, with German services PMI sliding, offset by far stronger than expected French service service sentiment:

- Eurozone Sept. Flash Composite PMI 52.6; Est. 52.8

- Eurozone Sept. Flash Services PMI 52.1; Est. 52.8

- Eurozone Sept. Flash Manufacturing PMI 52.6; Est. 51.5

- Germany Sept. Flash Composite PMI 52.7; Est 53.6

- Germany Sept. Flash Services PMI 50.6; Est 52.1

- Germany Sept. Flash Manufacturing PMI 54.3; Est 53.1

- French Economy Contracts 0.1% Q/q in 2Q; Prelim Unchanged Q/q

- France Sept. Flash Composite PMI 53.3 Vs 51.9; Est 51.8

- France Sept. Flash Services PMI 54.1; Est 52

- France Sept. Flash Manufacturing PMI 49.5; Est 48.5

After last week’s bond rout, the rates complex continued to stabilize. The Bloomberg Global Developed Sovereign Bond Index rose 1.3% this week through Thursday, when Janus Capital Group’s Bill Gross said a bear market in government debt has been delayed by the actions of monetary authorities. Bonds advanced across most of Asia on Friday, with China’s 10-year yield dropping two basis points to 2.74 percent. In Europe, Germany’s yield rose two basis points to minus 0.08 percent following a 10 basis point slide in the last session. 10Y U.S. Treasuries yielded 1.62 percent, little changed from Thursday and down seven basis points from a week ago. American government debt has handed investors an average return of 4.9 percent so far this year as the Fed refrained from adding to December’s interest-rate increase and former Fed Chairman Alan Greenspan said he expects the rally to be derailed by an expected pickup in inflation.

Everyone’s attention was on Japan however, where the 30-year bonds rose, against the BOJ’s desire for a steeper curve, pushing their yield down by five basis points to 0.47 percent. The move comes two days after the BOJ said it would shift the focus of monetary policy to shaping the yield curve, an adjustment that was seen driving long-term rates higher. “People may fear the BOJ cannot control the yield curve,” said Yoshiyuki Suzuki, the head of fixed income in Tokyo at Fukoku Mutual Life Insurance Co., which has about $66 billion in assets. “I believe the BOJ desires a steeper yield curve, but they can’t guarantee it.”

Market Snapshot

- S&P 500 futures down 0.1% to 2166

- Stoxx 600 down 0.7% to 345

- FTSE 100 down 0.3% to 6894

- DAX down 0.3% to 10644

- German 10Yr yield up less than 1bp to -0.09%

- Italian 10Yr yield up 1bp to 1.2%

- Spanish 10Yr yield up 2bps to 0.94%

- S&P GSCI Index down 1% to 355.4

- MSCI Asia Pacific down 0.2% to 142

- Nikkei 225 down 0.3% to 16754

- Hang Seng down 0.3% to 23686

- Shanghai Composite down 0.3% to 3034

- S&P/ASX 200 up 1.1% to 5431

- U.S. 10-yr yield down less than 1bp to 1.61%

- Dollar Index up 0.05% to 95.49

- WTI Crude futures up 0.2% to $46.53

- Brent Futures up 1.3% to $48.13

- Gold spot down 0.1% to $1,335

- Silver spot down 1% to $19.80

Global Headline News

- Erdogan to Turkey’s Central Bank: Nice Rate Cut, Do More Please: Turkey’s President speaks in interview; Erdogan Doesn’t Care at All If Turkey Gets Downgraded to Junk: Turkish president says credit ratings are based on politics

- Brexit Haunts EU Trade Plans as Nations Push to Save Pacts: EU govts meet in Bratislava today to discuss the bloc’s flagging trade deals

- EU Opposes Key Plank of Basel’s Global Bank Capital-Rule Revamp: 28-nation bloc objects to capital floors in risk measurement

- Bank Regulators Join Investigation Into JPMorgan’s China Hiring: Fed said to seek as much as $62m in possible settlement

- Yahoo Tipped Off to Hack by Report of Data Dump on Dark Web: Attacker was a ‘state-sponsored actor,’ co. says

- Facebook Says It Gave Advertisers Inflated Video Metrics: co. says error has been fixed

- CBOE Said in Talks to Buy Exchange Operator Bats Global: Deal would push CBOE beyond the niche business of options

- RWE Innogy IPO Range Values Green Energy Unit at $22b: Capital increase to raise up to EU2b for Innogy

- Nets Starts Trading as IPO Values Payment Firm at $4.5b: stock started trading in Copenhagen after an offer period to buy shares ended early

- LSE CEO Sees Incentives for Euro Clearing in Single Location: Rolet says clearing complexity makes change difficult, few financial centers can accommodate clearing business

Looking at regional markets, we start in Asia where stocks traded mixed to end a tumultuous central bank-driven week on a quiet note. The region’s bourses opened mostly higher following the firm lead from Wall St. where stocks extended on the FOMC-inspired gains and the NASDAQ finished at a fresh-record closing high, although upside was capped amid a lack of catalyst to spur further price action. Nikkei 225 (-0.3%) underperformed on return from holiday amid a firmer JPY, with USD/JPY having declined nearly 2 points since the last cash close in Tokyo. However, the index then rebounded from its lows as USD/JPY recovered, while some analysts also noted cautiousness as the BoJ reshuffles its ETF buying program in favour of funds that track the TOPIX rather than those that track the Nikkei 225. ASX 200 (+1.0%) took the impetus from Wall St gains, while Shanghai Comp (-0.3%) and Hang Seng (-0.3%) were indecisive despite the PBoC injecting a net CNY 670bn in to the interbank market for the week, as the ample liquidity dampened some hopes for more meaningful policy adjustments. 10yr JGBs saw subdued trade for the session with demand dampened amid an enhanced-liquidity auction for 10yr, 20yr and 30yr JGBs, in which the b/c declined from last month.

Top Asian News

- Watch Next Friday’s BOJ Statement to Gauge Its Yield-Curve Plans: New tools mean officials can buy at any time, in any amount

- Bond Bulls Curb Their Enthusiasm in China’s Leverage Crackdown: Central bank tweaks to money markets boosting funding costs

- Yuan Cost Spike Spreads Onshore as Shibor at Seven-Month High: Borrowing costs climb before week-long mainland holidays

- Whale Ignored as Japan Stock Fund Inflows Fall to 2012 Low: Mutual funds are least loved since before Abe came to power

- Biggest India Central Bank Overhaul to Ease Ties With State: New monetary policy panel marks biggest reform in RBI history

- China’s Xi Puts His Stamp on Communist Party With Promotions: Provincial posts key to rising in upcoming party reshuffle

- China Minsheng Banking Said Planning ~$1.5B Preferred Shrs Issue: Co. plans to sell ~$1.5b of preferred shares in Hong Kong as early as next month

In Europem it has been a quiet morning with the major indices residing in minor negative territory, although when considering the gains seen yesterday, these are relatively small moves. Financials underperform by some margin, with Deutsche Bank down nearly 2% on reports that lawmakers in the country are growing concerned about the company’s troubles. The thin conditions in markets is seen in Fixed income, the Bund higher by a mere 3 ticks Given the light news flow data has taken extra focus, with PMI’s from across the continent showing Eurozone nations in varying degrees of health. Firstly, the French data beat on expectations across the board. PMIs from neighbouring Germany were more mixed however, with a strong reading in manufacturing whilst printing misses on both composite and services. The data in Germany reflected that of the continent as whole and the mixed readings led to a lack of direction being provided to European asset classes.

Top European News

- Deutsche Bank’s Woes Said to Rouse German Concern Over Finances: Social Democrat lawmakers said to discuss bank’s finances

- Lundbeck Falls After Alzheimer’s Drug Fails in Late-Stage Study: co.’s experimental Alzheimer’s drug failed to meet targets in a final-stage patient trial

- Sports Direct’s Founder Ashley Named CEO After His ‘Right Arm’ Quits: Ashley replaces CEO Dave Forsey, who quit yday

- Commerzbank May Cut as Many as 5,000 Jobs, Boersen-Zeitung Says: Lender may merge some corporate units with investment bank

- Maersk Ends Mega-Ship Building Era With New Acquisition Plans: Chairman prefers to buy rivals instead of ordering new ships

- Anglo American Hires Fortescue’s Debt Slashing Finance Chief: co. named Stephen Pearce its new finance director

In FX, the Bloomberg Dollar Spot Index was little changed, headed for a 0.8 percent weekly loss.The yen was down 0.1 percent, trimming its weekly advance to 1.4 percent, after officials signaled they may intervene to counter appreciation and Goldman Sachs Group Inc. reiterated its view that the currency will fall. Japan’s Chief Cabinet Secretary Yoshihide Suga said Friday that moves in the foreign-exchange market have been very sensitive and policy makers are ready to react if the situation continues. A day earlier, the top currency official said speculative moves were undesirable and market activity was being closely monitored. The kiwi dropped 0.5 percent amid growing expectations that New Zealand’s central bank will cut interest rates at its next policy meeting in November.

In commodities, The Bloomberg Commodity Index fell 0.4 percent, its first decline in more than a week. Crude oil slipped as much as 1.2 percent to $45.76 a barrel in New York, before rebounding into the mid $46 range on a Reuters report that Saudi Arabia was prepared to cut production if Iran agrees to a supply freeze. Even if the Reuters report is confirmed to again be bogus, crude is still up more than 6% for the week before major producers meet Sept. 28 in Algiers to discuss ways to stabilize prices. The two nations’ rivalry derailed an oil supply accord earlier this year and Iraq’s OPEC representative said crude prices are unlikely to climb above $50 unless the group cuts production. “If there is an agreement, it’ll probably be a token deal where nations agree to a production cap near the upper limit of capacity,” said Ric Spooner, an analyst at CMC Markets in Sydney. “The market is still in surplus and hasn’t yet arrived at a balance.”

Bulletin Headline Summary From RanSquawk and Bloomberg

- European equities trade modestly lower in what has been a quiet session thus far with energy names lower ahead of next week’s Algiers meeting

- This morning’s slew of Eurozone PMI data did little to instigate price action with the data showing a mixed picture of the region’s health

- Looking ahead, highlights include Highlights Include US Manufacturing PMI, Canadian CPI and Retail sales and Fed’s Harker, Lockhart and Mester all speak

- Treasuries little changed in overnight trading while global stocks drop along with oil and gold and USD rises versus most G-10 peers.

- Deutsche Bank’s finances, weakened by low profitability and mounting legal costs, are raising concern among German politicians after the U.S. sought $14 billion to settle claims related to the sale of mortgage-backed securities

- Junior bonds of Banca Monte dei Paschi di Siena SpA fell to an eight-month low after a media report said the troubled Italian bank may require state support

- One-hundred thousand jobs would be at risk if clearing leaves the U.K., said London Stock Exchange Group Plc Chief Executive Officer Xavier Rolet

- Commerzbank AG is preparing to cut as many as 5,000 jobs under a new strategy by Chief Executive Officer Martin Zielke to boost profitability, Boersen-Zeitung reported, without saying where it obtained the information

- The European Union, home to nearly half of the world’s biggest banks, rejects a central plank of the global capital-rule overhaul under debate in the Basel Committee on Banking Supervision, according to an EU official

- The euro-area economy saw its pace of growth dip to a 20- month low at the end of the third quarter, highlighting the challenge facing policy makers to build momentum

- Turkish President Recep Tayyip Erdogan said that any followers of the Gulen religious movement must be removed from the central bank, one of the only major Turkish institutions that hasn’t publicized widespread purges since a failed coup in July

* * *

DB’s Jim Reid concludes the overnight wrap

The toughest thing over the last 24 hours has been finding an asset that has gone down. Post the FOMC conclusion we’ve seen global equities rally in unison, bond yields fall sharply, credit tighten, EM rejoice and commodities stride confidently on. If you’re really looking for weakness then the following is the (small) list of assets we found that have fallen post-FOMC, not including the obvious decline for the Dollar: Egyptian, Slovakian and Macedonian equities, Corn, Natural Gas, Taiwanese Dollar, Kiwi Dollar and the Chile 2y bond. On another day that might look like a reasonably diversified portfolio!

The ‘everything’ rally seems to have been sparked by a relief that the uncertainty of the Fed is now out the way and markets feel they have a window to exploit carry. Yesterday the S&P 500 closed +0.65% and at one stage traded to within half a percent of its all time highs. It also takes the post FOMC rally to +1.53% for the S&P with real estate names leading the way. European equities were earlier playing catch up with the Stoxx 600 (+1.58%) and DAX (+2.28%) rising steeply. The vast majority of emerging markets have also had a bumper last 35 hours or so. Bourses in Mexico, South Africa, Argentina and Brazil are all up 2-3%. It’s much the same in credit too. CDX IG was another 2.5bps tighter yesterday and is now 5bps tighter in the same time frame, while the iTraxx Main and Crossover indices rallied 3bps and 14bps respectively yesterday. Oil has also been firm with WTI now +1.10% since the FOMC despite dropping this morning in Asia. The VIX has also fallen back to a two-week low following a 20% or so drop.

The bond market has also responded as though it’s been giving the green light for the next few months. The Treasury curve flattened for a second consecutive day. 2y yields were fairly unchanged at 0.772%, but 10y yields were down another 3.3bps to 1.619% and 30y yields finished down closer to 4bps at 2.336%. 10y Treasury yields are now down some 8bps or so in yield post the FOMC but even more impressive have been the moves in European bond markets. 10y Bunds have in fact been one of the biggest outperformers after yields tumbled 9.8bps yesterday to -0.099% – the strongest day since the immediate post-Brexit reaction on June 24th. Other sovereign bond yields in Europe closed 6-10bps lower yesterday.

So as we move slightly away from focusing as much on central banks, we’ll slowly now build to the US elections as the next major observable macro test. Monday’s first debate between the candidates will mark the start of the serious battle ahead. At a micro level earnings season in the US is also just around the corner so that’ll be another important upcoming period.

Switching over to the latest in Asia this morning where Japan is open again following a public holiday yesterday. After initially falling half a percent or so at the open, the Nikkei (-0.12%) has pared most of the early decline, while the Topix is currently -0.26%. The reports of an undersea earthquake 250km from Japan’s coast is perhaps to blame and it’s resulted in the Yen (-0.34%) weakening a bit more this morning. There was good news on the data front though with Japan’s flash manufacturing PMI rising 0.8pts to 50.3 in September. Elsewhere it’s a bit more mixed. The Shanghai Comp (-0.10%) and CSI 300 (-0.28%) are both in the red, while the Hang Seng (+0.07%), Kospi (+0.11%) and ASX (+0.62%) have climbed. Sovereign bond markets have continued to rally. 10y JGB’s are 2bps lower at -0.056% while yields in the rest of Asia are generally 1-8bps lower.

Moving on. The economic data yesterday was largely focused on the US, although it was mainly second tier releases. Perhaps the most significant was the existing home sales reading in August which declined unexpectedly (-0.9% mom vs. +1.1% expected), mirroring the soft pending home sales report. The conference board’s leading index (-0.2% mom vs. 0.0% expected) was also soft for last month, although we did see a one-tenth upward revision to July’s print. On the positive side initial jobless claims were down 8k last week to 252k, while in the manufacturing sector the Kansas City Fed’s manufacturing survey was up a bumper 10pts to +6 (vs. -3 expected) this month, the strongest reading since December 2014. The associated text showed that ‘for the second time in four months we had a positive reading on our composite index’ and that ‘this followed 15 straight months of contraction and suggests regional factory activity may be stabilizing’.

Meanwhile, in Europe confidence indicators in France generally nudged up this month, while in the UK the CBI’s industrial trends survey for September showed no change in total orders at -5, but a 11pt rebound in the volume of output expectations for the next three months to +22 and so taking it back to pre Brexit levels. On that subject, there was a bit of focus over at the BoE yesterday with MPC member Kristin Forbes speaking to Bloomberg News. Forbes said that ‘we may be over-counting the effects’ of uncertainty following the Brexit outcome and that ‘I’ve worried a bit in our forecast that we control for many of the measures that simultaneously control for uncertainty, and then we put in uncertainty effects, so we’re putting them in twice’. Forbes also suggested that there could be some upward revisions to growth forecasts and that ‘at this point I don’t see the case for additional stimulus’. It’s worth noting here that Forbes is considered one of the more hawkish BoE committee members. Sterling was up +0.35% yesterday following those comments.

In one last mention of Brexit, today marks the first full quarter anniversary since the referendum. As a bit of fun, we’ve taken a look at the performance of various assets in that time and included two charts in the PDF today for you to look at. As the charts show, while not quite the biggest underperformer in our sample, the impact on Sterling (-12%) has been clearly evident. It’s actually Corn (-13%) which has been the worst performer although we’d imagine for reasons completely unrelated to Brexit. As a result of the move in the Pound though, looking at Sterling assets there are huge swings between performance in local currency terms and USD hedged terms. Indeed in local currency terms the FTSE 100 and Gilts have done well, returning an impressive +10% and +9% respectively. However this translates into losses of -3% and -5% respectively in US Dollar terms, and so underperforming the likes of the S&P 500 (+4%), EM Equities (+11%), Treasuries (+1%) and US credit (+2% to +4%). The top of the leaderboard, in local terms, is topped by the Hang Seng (+15%), Silver (+15%) and Brazilian Equities (+14%). The same three occupy the top spots in USD terms, albeit in a different order. The bottom of the leaderboard also shows that Oil (-8%) has struggled, while Italian Equities (-7%) and European Banks (-4%) have also weakened. Overall though, in local currency terms 32 out of 42 asset sample have seen positive returns, while 27 assets have seen positive returns in USD terms.

Looking at the day ahead, this morning in Europe we’ll first of all kick off with the final revisions to Q2 GDP in France (no change from the 0.0% qoq reading expected). After that it’s all about the PMI’s with the flash September numbers due out for the Euro area, Germany and France. The market is expecting a very modest deterioration in the composite for the Euro area (52.8 vs. 52.9 previously) led by the manufacturing sector. In the US this afternoon the only data due out is the flash manufacturing PMI which the market consensus expects to stay unchanged at 52.0. Away from the data it’s a reasonably busy day for Fedspeak which should keep the market interested. Harker, Mester and Lockhart are all due to take part in a panel discussion at a conference this evening at 5pm BST, while Kaplan will speak shortly after at 5.30pm BST. The ECB’s Weidmann is also scheduled to speak this afternoon.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 8.42 POINTS OR .28%/ /Hang Sang closed DOWN 73.32 POINTS OR .31%. The Nikkei closed DOWN 53.60 POINTS OR .32% Australia’s all ordinaires CLOSED UP 1.06% /Chinese yuan (ONSHORE) closed DOWN at 6.6704/Oil FELL to 46.16 dollars per barrel for WTI and 48.03 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.6704 yuan to the dollar vs 6.6753 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

3a)NORTH KOREA:

none today

b) REPORT ON JAPAN

We have now had 2 days since the Bank of Japan introduced their new policy on QQE. They are trying to target the upper end of the yield curve. The problem with that is that it is much more difficult to control longer term rates. Central bankers can always control the short end of the curve, but the long end has a mind of its own

in other words..the call this new policy disastrous..

(courtesy zero hedge)

“It May Be Over For The BOJ” – Wall Street Throws Up On Kuroda’s “Disastrous” New Policy

Two days day after the BOJ unveiled its “QQE with Yield Curve Control” (but no fries), the sellside has had time to digest the central bank’s latest proposal and the assessment, unlike that of Dan Loeb, is anything but glowing. In fact, it’s downright “deplorable.”

We start with Goldman, which as we reported two days ago, admitted not only that what the BOJ is launching is tantamount to a “stealth taper”, but more disturbingly, has no idea just how the central bank will effectively control the yield curve:

“it is very unclear at this time exactly how the BOJ intends to “control” the yield curve in the future. Based only on the official statement, we think it is likely it will maintain the yield curve at more or less the current level for the time being. However, the question is how it will control the overall level and shape of the curve when financial and economic conditions change in the future. While the JGB market needs to take time to study the BOJ’s intentions, with interest rate movements lessening, we think the pricing function of interest rates as a mirror reflecting real economic and financial conditions will be increasingly lost.”

Goldman was not the only one confused by what the BOJ unveiled: there was also Deutsche Bank, which tactfully said that it sees a “slight contradiction” in the policy.

In a note titled “It may be over for the BOJ”, DB’s George Saravelos writes that “by targeting nominal rates the BoJ is relinquishing control of real rates. This creates a policy asymmetry that becomes highly pro-cyclical.Consider a negative demand shock that raises demand for JGBs and depresses inflation expectations. The BoJ will end up reducing the amount of JGBs it buys and raising real rates. Consider the opposite: a huge fiscal stimulus from the government that puts upward pressure on yields: the BoJ would effectively monetize the debt raising inflation expectations even further. We worry that a self-fulfilling tightening is more likely than an easing in coming months.”

Saravelos then notes the following:

During World War II, the Federal Reserve established yield targets on US treasuries to help finance the war effort. The yield targets evolved into an indirect financing of the US treasury that persisted throughout the 1950s. By shifting to a yield target, the central bank is indirectly shifting the onus of a “helicopter drop” to the government. This is certainly a positive. But by relinquishing its own power and willingness to act its influence is now being reduced. Until we see more convincing signs of a large and credible fiscal easing from the government the BoJ’s inflation target will lack credibility.

In other words, Kuroda assumes a steady-state equilibrium essentially in perpetuity. However, once the curve starts shifting substantially, either parallel-shifting or steepening (it flattened last night, despite the BOJ’s “best intentions”)the central bank would quickly lose control as its intervention would only exacerbate the underlying move. In practical terms, this means that DB remains “JPY bulls and continue to target a break below 100 in USD/JPY to 94 by the end of the year.”

Chiming in the BOJ hate parade, was CLSA’s traditional skeptic, Chris Wood, who also penned an appropriately titled piece “Kuroda’s Last Stand”, in which he also notes that Kuroda is now trapped, correctly observing that “this attempt to fix the price of ten year money represents a massive hostage to fortune since, in a world where bond markets sell off, the BoJ is committed to potentially unlimited balance sheet expansion to hold the 10-year JGB at 0%.”

However, unlike Deutsche Bank, Wood reaches the exact opposite conclusion on what the Yen will do, saying that “this would be hugely yen bearish. It could also mark the loss of any lingering credibility that Kuroda still has left.”

And just in case CLSA’s dire assessment of the BOJ’s latest lunacy was unclear, he brings it home in the following paragraph:

The above suggests that Kamikaze Kuroda’s disastrous flirtation with negative rates will not be expanded for now though for “face” reasons it has not been formally abandoned. Indeed the BoJ in a face-saving measure stated that one possible option for additional easing is to cut the short-term policy interest rate. Meanwhile the practical problem for Kuroda is that he remains way below his 2% inflation target which is why it is wrong to assume that there will be no more monetary policy fireworks in Japan. Indeed GREED & fear is still of the view that monetisation of infrastructure stimulus, as recommended by Ben Bernanke, is still on the table in Japan; though it is more likely to be announced once the situation in America becomes clearer following November’s US presidential election. It should be noted that Kuroda has already adopted one of Bernanke’s suggestions floated in his blogs in March and April, namely targeting of rates higher up the yield curve. He can therefore easily implement another. For such reasons GREED & fear would be a seller of the yen, rather than a buyer, on a 12-month view.

Finally, adding to the confusion over what happens to the Yen was Crossborder Capital’s note, according to which the BOJ’s curve shift announcement was the central bank’s “Second Big Error” and shows “policy makers have little understanding of how the yield curve operates” adding that the “end result will be higher Japanese bond yields, a steeper yield curve and a stronger JPY.”

If upward pressure on the 10-year note kicks in, and the BOJ makes good on its commitment to intervene, real term premia will in fact rise, since 20-year and 30-year yields will be pushed up as a result. In other words, the yield curve will be kinked: effectively flat up to 10 years but sharply steepening thereafter. The research firm concludes that central banks can’t fix the shape of the yield curve “rather like squeezing a balloon full of air in one place [it] simply pushes out the balloon somewhere else.”

In Crossborder’s scathing attack on Kuroda, the reports also notes that the “BOJ controls policy rate not term premium” adding that “policy rate accounts for around 25% of yield curve variation, while term premia, outside of BOJ control, determine up to 75% of the variation.” Which is why “if it cannot control three-quarters of movements at the long-end of the curve, the BOJ has barely any control over its overall slope.” Repeating what Saravelos said above, the authors say that “trying to hold down 10Y yields, thus injecting more liquidity into markets, will likely push up 20Y and 30Y yields, resulting in a yield curve with negative convexity” and conclude that “BOJ policy will distort term structure, could strengthen JPY and will likely underscore need for even more fiscal support.” In other words, the BOJ’s attempt to control the BOJ’s yield curve will fail, because “like squeezing a balloon full of air in one place, the BOJ simply pushes out the balloon somewhere else.”

* * *

Summarizing the above, when it comes even to sellside analysts, the BOJ has now lost credibility. Worse, when the time comes for the central bank to intervene in the yield curve – as it will have to, and as it has promised to – it will not only fail to do what it has promised, but its intervention will only makes the problem worse, and lead to the next stage of the global VaR-shocked, bond bubble-bursting stage.

c) Report on CHINA

none today

4 EUROPEAN AFFAIRS

Now there is no question that problems are surfacing inside Deutsche bank when we start to see German politicians getting nervous:

(courtesy zero hedge)

German Politicians Are Getting Nervous About Deutsche Bank

Just a few short days after Germany’s premier financial publication Handelsblatt dared to utter the “n”-word, when it said that in the aftermath of last week’s striking $14 billion DOJ settlement proposal, “some have even raised the possibility of a government bailout of Germany’s largest bank, which would be a defining event and a symbolic blow to the image of Europe’s largest economy”, German lawmakers are finally starting to get nervous.

According to Bloomberg, Deutsche Bank’s suddenly troubling finances, impacted by the bank’s low profitability courtesy of the ECB’s NIRP policy as well as mounting legal costs courtesy of years of legal violations, “are raising concern among German politicians.” At a closed session of Social Democratic finance lawmakers on Tuesday, Deutsche Bank’s woes came up alongside a debate over Basel financial rules. Participants discussed the U.S. fine and the financial reserves at Deutsche Bank’s disposal if it had to cover the full amount.

While the participants in the meeting did not reach any conclusions on the likely outcome, the discussion signals that the risks facing Deutsche Bank have the attention of Germany’s political establishment. Which means it’s almost serious enough where the politicians, in the parlance of Jean-Claude Juncker, “have to lie” or in this case redirect attention, ideally abroad: the German Finance Ministry last week called on the U.S. to ensure a “fair outcome” for Deutsche Bank, citing cases against other banks where the government settled for reduced fines.

Actually lying also works: on February 9 German Finance Minister Wolfgang Schaeuble told Bloomberg Television that he has “no concerns about Deutsche Bank.” That has probably changed.

The solvency problems facing Germany’s biggest bank have been widely documented: it is already ranked among the worst-capitalized lenders in European stress tests before U.S. authorities demanded $14 billion as an RMBS settlement, more than twice the €5.5 billion the bank has set aside for litigation and almost 80% of the bank’s market cap. Also, as we pointed out first in 2013, and as Matteo Renzi takes every chance to remind Germany, Deutsche Bank has a gargantuan €42 trillion in gross notional derivatives on its balance sheet. Just this week, the Italian PM told Bundesbank chief Jens Weidmann not to worry so much about Italy’s massive debt load but instead to solve the problems of German banks which had “hundreds and hundreds and hundreds of billions of euros of derivatives” on their books.”

But what may be most troubling is not what German politicians are talking about behind closed door, but what they are not talking about in public. Bloomberg notes that Merkel’s government is now maintaining a public silence on Deutsche Bank’s woes. Then again, what is there to say: if DB is indeed approaching the cliff, any discussion of the bank would only lead to more concerns about the bank’s viability. There was some discussion of DB, however, during a September 16 meeting of Germany’s Financial Stability Committee, a group of German finance officials and regulators, whose members concluded that the fine demanded by the U.S. government would probably be lowered, Handelsblatt newspaper reported. In other words, hope is once again a strategy. Sadly, when it comes to banks with multi-trillion balance sheets, this may not be the best approach.

And just to make sure that German politicians have even more to talk about, earlier today the Brussels-based Single Resolution Board, the resolution authority for 142 banks (including Deutsche Bank) warned that EU bank may need rescue funds equaling twice their ECB capital. As Bloomberg reported today, requiring banks to have at least that same amount as the minimum capital requirement set by the ECB in loss-absorbing liabilities will ensure that they can recapitalize themselves quickly after restructuring, SRB head Elke Koenig said.

The European Banking Authority said in July that the region’s banks may need as much as 470 billion euros ($524 billion) in additional MREL-eligible funding under conditions similar to those cited by Koenig. The EBA sample consisted of 114 banks representing 70 percent of the EU’s banking assets, including lenders not overseen by the SRB.

And the bulk of these funds will have to be procured by Europe’s largest bank: Deutsche Bank.

end

A great commentary on the problems facing Italy with respect to the rest of Europe. Italy will propose austerity and hope that the EU grants them concessions to helping them with their huge banking problems

George Frideman/Mauldin Economics.com

Italy Is The EU’s Weakest Link

Authored by George Frideman via MauldinEconomics.com,

German Chancellor Angela Merkel, French President François Hollande, and Italian Prime Minister Matteo Renzi met Aug. 22 on an Italian aircraft carrier. They said they were meeting to talk aboutEuropean policy after Brexit. The real discussion was about Italy’s economy and the steps needed to revive it.

The EU’s Integrity Is in Question

The location of their meeting is notable. It is a more militaristic location than Europeans normally prefer. The choice is even more interesting in light of the rumors that Germany might resume the military draft.

The US has been increasingly critical of Europe’s contribution to NATO. The EU’s GDP is larger than that of the US, but the EU’s contribution to its own defense does not reflect that fact. Europe’s limited militaries make it dependent on the US.

Holding the meeting on the aircraft carrier was meant to show that Europe has some defense capability. But it also shows how Brexit diminishes the EU’s military power. It was a good place to have a meeting as European unity is in question, with Italy as a weak link.

Italy’s Crisis Is Worsening

Italy’s economy is weak. There is no growth. The banking system is in bad shape. Unemployment is high. There is substantial public unrest, and Renzi’s standing is weakening. Italy has been somewhere between recession and stagnation since 2008. After eight years, the situation shows no signs of improving.

The Italians want to run a substantial budget deficit to stimulate the economy. The EU operates under a “stability pact.” This requires countries to keep deficits within certain limits but allows for exceptions.

France has operated outside the boundaries of the stability pact for years. Spain and Portugal were given exceptions as well. As Merkel put it, “The stability pact has a lot of flexibility, which we have to apply in a smart way.”

I’m not sure what “a smart way” looks like, but the issue does not apply to Italy. Renzi said, “Italy’s deficit has been at the lowest level of the last ten years.” He said that he “would go ahead with structural reforms and deficit reductions for the good of [Italy’s] children.”

In other words, Renzi said that he would further tighten spending. Merkel called his stance “courageous.” Hollande mentioned that the UK’s decision to leave the EU at some point in the future “requires a response by EU leaders.” Merkel agreed that they need to “deliver results.”

She was not clear on what those results would be.

Renzi’s Motives

Increased austerity has not worked in eight years. Accepting that Renzi is not insane, it is hard to understand why he thinks this move will work any time soon.

Merkel conceded that these actions “won’t show results in four weeks, but it sets the parameters for a sustainable and successful Italy.” No one expects it to work in four weeks, but the question is why it should work at all.

This means the Germans and French are going to use Brexit to explain why increased austerity is needed. It is not clear to me how Brexit leads to austerity, but Merkel seemed to be saying that. Also, Merkel made it clear that the European Commission might be willing to accommodate Renzi.

But Renzi’s proposed strategy hardly begs for accommodation. Renzi, who was seen as a maverick in Europe, is now being more austere than required. If Merkel offers congratulations, she has gotten everything she wants.

Part of this might be political gamesmanship. Renzi needs a victory. He could propose deep austerity and then demand concessions from the EU Commission. Once granted, he can be hailed as a tough negotiator.

But he would be bargaining against his own budget. Politics is strange enough that he might pull it off. An alternative is that by conceding this point, he is setting up an EU concession on the banks. That is pure guesswork, as there wasn’t a hint of it in the talks.

Nationalism in Italy Is on the Rise

In either case, the budget will be extremely unpopular and impose several more years of austerity. It will generate an exit movement, with proponents arguing that EU-imposed austerity caused these problems in the first place. The faster they get out of the EU the better.

For all I know, maverick Renzi lives, and he is doing this to trigger this movement. But whether or not he favors leaving the EU, there will be a movement as a result of this budget.

The argument for staying in the EU will be that Italy can’t get better without the EU. The argument for leaving the union will be that Italy will never get better if it stays.

In any case, the malaise that has gripped Italy for years will continue. It is important not to expect solutions in four weeks.

The problem with European unity is that after eight years, no one expects an improvement in four weeks.The question is whether this is the permanent condition of Europe. Perhaps this is the best Italy will do for a long time.

The scene on the aircraft carrier was designed to remind everyone that Europe has military power and to legitimize European unity in the face of Britain’s decision to leave. But it is not clear whether the Italian public will applaud or demand that the carrier be sold.

It isn’t clear that Italy will choose to leave by any means. But it is clear that the Italian economic crisis is not on its way to clearing up.

* * *

Watch George Friedman’s Ground-breaking Documentary Crisis & Chaos: Are We Moving Toward World War III?

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6. GLOBAL ISSUES

Low oil is keeping inflation in Canada at zero. However retail sales missed expectations as their economy falters badly.

(courtesy zero hedge)

Loonie Tumbles After Canadian Inflation, Retail Sales Plunge

A slew of disappointing data out of Canada has sent the Loonie tumbling this morning (despite higher oil prices).

Canadian Retail Sales and Inflation data missed across the board…

Multi-year lows in CPI, Core CPI, and Retail Sales…

And the result is a tumbling Loonie as expectations of further rate cuts loom…

Charts: Bloomberg

7. OIL ISSUES

This morning the rumours started with the Saudis offering to cut oil production if Iran freezes their output (according to Reuters)

(courtesy zero hedge/Reuters)

Saudis Said To Offer Oil Production Cut If Iran Freezes Output, Reuters Reports

With oil rolling over, and modestly pressuring US equity futures, moments ago Reuters did what it does best, and reported, citing three “anonymous” sources, that Saudi Arabia was prepared to engage in a radical shift in its long-held policy of not cutting production, and has offered to lower its own oil production if Iran agrees to cap its output this year, in “a major compromise” ahead of talks in Algeria next week, “three sources familiar with the discussions told Reuters.”

Reuters adds that “the offer, which has yet to be accepted or rejected by Tehran, was made this month, the sources told Reuters on condition of anonymity” and notes that Riyadh is ready to cut output to lower levels seen early this year in exchange for Iran freezing production at the current level, which is 3.6 million barrels per day, the sources said.

“They (the Saudis) are ready for a cut but Iran has to agree to freeze,” one source said.