Gold $1321.70 up $2.30

Silver 19.12 up 8 cents

In the access market 5:15 pm

Gold: 1320.75

Silver: 19.08

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix Sept 29 (10:15 pm est last night): $ 1329.99

NY ACCESS PRICE: $1324.25 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1326.88

NY ACCESS PRICE: 1322.00 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Sept 29: 5:30 am est: $1320.85 (NY: same time: $1321.75: 5:30AM)

London Second fix Sept 16: 10 am est: $1318.10 (NY same time: $1319.60 , 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:The front September contract month we had 6 notices filed for 600 oz

For silver: the front month of September we have a total of 468 notices filed for 2,340,000 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 1010 contracts DOWN to 200,476. The open interest ROSE DESPITE THE FACT THAT the silver price was DOWN 5 cents in yesterday’s trading .In ounces, the OI is still represented by just MORE THAN 1 BILLION oz i.e. 1.0002 BILLION TO BE EXACT or 144% of annual global silver production (ex Russia &ex China).

In silver we had 468 notices served upon for 2,340,000 oz

In gold, the total comex gold FELL by 8755 contracts as the price of gold fell BY $6.50 YESTERDAY . The total gold OI stands at 574,406 contracts.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

LAST NIGHT WE HAD NO CHANGES OUT OF THE GLD//

Total gold inventory rests tonight at: 949.14 tonnes of gold

SLV

we had no changes at the SLV

THE SLV Inventory rests at: 362.909 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL by 1010 contracts down to 200,476 as the price of silver FELL by 5 cents with yesterday’s trading.The gold open interest FELL by 8,755 contracts DOWN to 575,406 as the price of gold fell $6.50 IN YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

end

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed UP 10.63 POINTS OR .30%/ /Hang Sang closed UP 119.82 POINTS OR 0.51%. The Nikkei closed UP 228.31 POINTS OR 1.39% Australia’s all ordinaires CLOSED UP 1.09% /Chinese yuan (ONSHORE) closed UP at 6.6672/Oil FELL to 46.91 dollars per barrel for WTI and 48.27 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.6771 yuan to the dollar vs 6.6672 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)Korea:

none

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

i)China’s beige book reveals real problems in the Chinese economy. We have highlighted to you last week that loan demand is down badly (corporate loans) while house loan demand is up (and thus the huge housing bubble)

( zero hedge)

ii)As we pointed out to you yesterday, China has a massive housing bubble which will burst at any time. There is not enough growth to sustain those higher prices

( zero hedge)

4 EUROPEAN AFFAIRS

i)Germany

Germany’s second largest bank Commerzbank this morning scraps its dividend and fires 20% of its workforce. And this is Germany, the powerhouse of Europe. The growth in the economy is just not existent.

( zero hedge)

ibMajor problems with Deutsche bank tonight as hedge funds that deal with DB as counterparties are withdrawing their funds as they fear the worst. Also there is a huge shortage of dollars similar to what happened with Lehman.European bank have just increased their demand for dollars by 6000%. Short dated CDS (credit default swaps on DB is skyrocketing.

Ladies and Gentlemen: I believe we are having a Lehman moment!

(courtesy zero hedge)

ic) On the same subject as above: he is correct on everything he asserts!

ii)England

These bozos are planning ZIRP/NIRP in perpetuity!

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia vs USA

a)

What is wrong with these doorknobs: John Kerry gives Russia an ultimatum to stop bombing Aleppo or else…

nothing will happen

(courtesy zero hedge)

b)

This caused gold to rise about 4.00 dollars. Gold never jumps on anything so this was rather strange:

( zero hedge)

ii)Saudi Arabia vs USA

Obama is not a happy camper with the veto overide.

( zero hedge)

iii)Saudi Arabia

6.GLOBAL ISSUES

none today

7.OIL ISSUES

i)The bickering begins as Iraq disagrees with the OPEC method of oil production estimates:This deal has no chance of happening!

( zero hedge)

ib)Then Iraq claims it cannot accept this deal with the wrong Iraqi oil production. Unless changed the deal is off:

( zero hedge)

ii)Goldman Sachs must be long in oil: They state that the OPEC deal will add 10 dollars to the price of oil:

( Goldman Sachs/zero hedge)

8.EMERGING MARKETS

none today

9.PHYSICAL STORIES

i)A good paper today from Steve St Angelo on the demand for our 4 precious metals:

( Steve St Angelo/SRSRocco Report)

ii)Gold miner Petropavlovsk (Peter Hambro’s operation) finally turns a profit, its first in 4 years:

( London’s Telegraph)

iii)Shangdong gold is the top bidder from Glencore’s gold property is Kazakhstan

(courtesy Bloomberg/GATA)

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)Your humour story of the day:

Jobless claims at 40 yr lows:

( zero hedge)

ii)Final Q2 GDP comes in at only 1.4% but slightly higher than the expected 1.3%.This is an extremely slow growth.

( zero hedge)

iii)First it was Samsung phone exploded and now Apple 7 iphone just did the same. Apple’s stock and Nasdaq fell on the news. Can you imagine how those central bank’s feel that purchased Apple stock

( zero hedge)

iv) We now have a trifecta: First new home sales faltered, then existing home sales fell and now pending home sales slump to 7 month lows:

(courtesy NAR/zero hedge)

Let us head over to the comex:

The total gold comex open interest FELL BY AN HUGE 8,755 CONTRACTS to an OI level of 574,406 as price of gold FELL by $6.50 with YESTERDAY’S trading.We are continuing with the ritual that as soon as we approach the first day notice of an active month, the entire open interest complex obliterates. We are now in the NON active month of SEPTEMBER/

The contract month of Sept saw it’s OI fell by 108 contracts down to 36. We had 12 notices filed yesterday so we LOST 96 gold contracts or an additional 9600 gold ounces will NOT stand for delivery.THIS MAKES NO SENSE AT ALL!! WHY WOULD THEY STAND FOR THE ENTIRE MONTH, PUT UP ALL THE MONEY AND ROLL?. THESE GUYS WERE BOUGHT WITH WITH CASH PLUS A FIAT BONUS. The next delivery month is October and here the OI lost 4,614 contracts DOWN to 9,704. This level is still extremely elevated. To give you an idea as to its size, I will give you the burn rates for the 3 dates Sept 29 and Sept 30 last yr:

.

Sept 29.2015: 4351 contracts rolled vs SEPT 2016: 4614. (9704 still remaining)

Sept 30.2015: 1252 contracts rolled leaving 3092 OI standing or 309,200 oz (9.66 tonnes) standing for delivery. which was pretty good last yr.

We are a good 6,000 contracts ahead of last year. The next contract month of December showed an decrease of 7,478 contracts down to 450,651. The estimated volume today at the comex: 151,136 which is WEAK. Confirmed volume yesterday: 218,381 which is good.

And now for the wild silver comex results. Total silver OI FELL BY 1010 contracts from 201,209 down to 20,476 as the price of silver fell to the tune of 5 cents yesterday. We are moving FURTHER FROM the all time record high for silver open interest set on Wednesday August 3: (224,540). We are now into the next active month of September and here the OI fell by 25 contracts down to 468. We had 30 notices filed upon yesterday so we GAINED 5 contracts or 25,000 additional oz will stand for delivery in this active month of September. The next non active delivery movement of October lost 1 CONTRACT TO 474 contracts. The next big delivery month is December and here it FELL by 2370 contracts DOWN to 171,352. The volume on the comex today (just comex) came in at 48,766 which is very good. The confirmed volume yesterday (comex and globex) was huge at 71,608 . Silver is not in backwardation. London is in backwardation for several months.

today we had 468 notices filed for silver: 2,340,000 oz

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz |

NIL |

| Withdrawals from Customer Inventory in oz nil |

40,293.327 oz

Brinks

HSBC

|

| Deposits to the Dealer Inventory in oz | 2999.94 oz

Brinks |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

6 notices

600 oz

|

| No of oz to be served (notices) |

30 contracts

(3000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

2676 contracts

267,600 oz

8.323 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | 192.90 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 539,307.9 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 6 contract of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped (received) by jPMorgan customer account.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

249,832.45 oz

Brinks

CNT, Scotia

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

468 CONTRACTS

(2,340,000 OZ)

|

| No of oz to be served (notices) |

5 contracts

(25,000 oz)

|

| Total monthly oz silver served (contracts) | 3215 contracts (16,075,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 8,674,337.6 oz |

end

NPV for Sprott and Central Fund of Canada

end

And now your overnight trading in gold,THURSDAY MORNING and also physical stories that may interest you:

ECB Refused “To Answer Questions” – Deutsche Bank “Systemic Threat” Is “Not ECB Fault”

The potential collapse of Deutsche Bank and the systemic risk it poses to banks and the European financial and monetary system moved into the German political sphere yesterday. The German government denied it was preparing a rescue of the embattled bank and the Bundestag attempted to ask questions of ECB President Mario Draghi about the causes of the “systemic risks” posed by the bank.

Ralph Orlowski | Reuters

Ralph Orlowski | Reuters

ECB President Mario Draghi refused to answer questions in German parliament

The ECB president brazenly “refused to answer questions” regarding Deutsche Bank during a closed-door meeting in the German parliament. Afterwords in conversation with journalists, he denied that the negative interest rates being imposed by the ECB are partly responsible for Deutsche Bank and the German financial system’s troubles.

However, many analysts rightly assert that zero interest rate policies (ZIRP) and now negative interest rate policies (NIRP) are a factor and partly contributing to the challenges facing banks in much of the western world. Not to mention causing bubbles in many property markets and indeed in stock and bond markets.

Source FT

Source FT

“If a bank represents a systemic threat it cannot be because of low interest rates. It has to be for other reasons,” Mr Draghi asserted to reporters somewhat dogmatically and simplistically. He was contradicted by the head of Germany’s BdB banking association, Michael Kemmer, who told Deutschlandfunk radio that the ECB’s low interest rate policy was partly responsible for the current problems that Deutsche Bank and Commerzbank are facing.

This morning, Commerzbank, the second-biggest bank in Germany after Deutsche, suspended its dividend and revealed it is slashing more than 9,000 job losses as it too desperately tries to shore up its business in the face of ultra-low interest rates and increasing loan losses.

Anxiety over eurozone banks has risen since the market turmoil following the June UK vote to leave the EU. Until recently, however, concerns have focused on the bloc’s periphery, particularly banks in Italy.

Now the banking crisis is moving to the core. This poses the real risk of financial contagion in the European monetary system and the global banking system.

See “Euro Might Start To Unravel” If Collapse Of Deutsche Bank

Gold and Silver Bullion – News and Commentary

Gold extends losses as dollar, stocks rise (Reuters)

Gold prices mostly steady in Asia as rates, politics and OPEC mix (Investing)

WTO cuts 2016 world trade growth forecast to 1.7 percent, cites wake-up call (Reuters)

City-by-city look as house price gains slow (MarketWatch)

IMF sounds alarm bells over trade slowdown and low inflation (Telegraph)

What the return of politics means for your money (MoneyWeek)

Dollar Going the Way of the Denarius (InternationalMan)

Transition of Price Discovery in the Global Gold and Silver Market (SafeHaven)

Will Deutsche Bank’s Collapse Be Worse Than Lehman Brothers? (GoldEagle)

Deutsche Bank To Blow Up and Create Euro “Chaos”? (DollarCollapse)

Gold Prices (LBMA AM)

29 Sep: USD 1,320.85, GBP 1,016.92 & EUR 1,177.14 per ounce

28 Sep: USD 1,324.80, GBP 1,020.10 & EUR 1,181.06 per ounce

27 Sep: USD 1,335.85, GBP 1,031.01 & EUR 1,187.84 per ounce

26 Sep: USD 1,336.30, GBP 1,033.23 & EUR 1,188.91 per ounce

23 Sep: USD 1,335.90, GBP 1,027.17 & EUR 1,192.16 per ounce

22 Sep: USD 1,332.45, GBP 1,019.59 & EUR 1,186.68 per ounce

21 Sep: USD 1,319.60, GBP 1,015.96 & EUR 1,183.81 per ounce

Silver Prices (LBMA)

29 Sep: USD 19.01, GBP 14.61 & EUR 16.95 per ounce

28 Sep: USD 19.12, GBP 14.69 & EUR 17.05 per ounce

27 Sep: USD 19.42, GBP 14.99 & EUR 17.26 per ounce

26 Sep: USD 19.44, GBP 15.04 & EUR 17.29 per ounce

23 Sep: USD 19.82, GBP 15.28 & EUR 17.66 per ounce

22 Sep: USD 19.88, GBP 15.22 & EUR 17.69 per ounce

21 Sep: USD 19.43, GBP 14.95 & EUR 17.43 per ounce

Recent Market Updates

– Do You Really Own Your Gold?

– “Gold Will Likely Soar To A Record Within Five Years”

– Savings Guarantee? U.N. Warns Next Financial Crisis Imminent

– Gold Up 1.5%, Silver Surges 3% – Yellen Stays Ultra Loose At 0.25%

– Trump and Clinton Are “Positive For Gold” – $1,900/oz by End of Year

– Gold Bugs Rejoice – Central Banks Think You’re On To Something

– ‘Hard’ Brexit Looms For Ireland

– EU Bail In Rules Ignored By Italy – Mother Of All Systemic Threats and World War?

– Buy Gold – Bonds Are ‘Biggest Bubble In World’ – Billionaire Singer Warns

– Silver Bullion Market – “Most Bullish Story Ever Told?”

– “Sorry, You Can’t Have Your Gold Bullion”

– Global Stocks, Bonds Fall Sharply – Gold Consolidates After Two Weeks Of Gains

– Gold, Silver, Blockchain and Fintech – Solutions To Negative Rates, Bail-ins, Cash Confiscations and Cashless Society

THE TOP FOUR PRECIOUS METALS: Which Will Be The Best Investments During The Next Financial Crash

When the next financial crash occurs, investors need to understand which of the top four precious metals are the best to invest in. Unfortunately, there has been a great deal of faulty analysis that has mislead many investors about the fundamentals of gold, platinum, palladium and silver.

I will provide information in this article on the top four precious metals that has not been covered correctly by the majority of analysts. While some may have touched on individual aspects, very few have put together an in-depth analysis on these metals to properly educate investors.

However, before I get into the details of these top four precious metals, I would like to share some very important information.

When I wrote my article (few weeks ago) titled, THE COMING BREAKDOWN OF U.S. & GLOBAL MARKETS EXPLAINED: What Most Analysts Missed, it generated the most interest and commentary of any of my previous articles. It seemed to have hit a nerve in my followers and new readers.

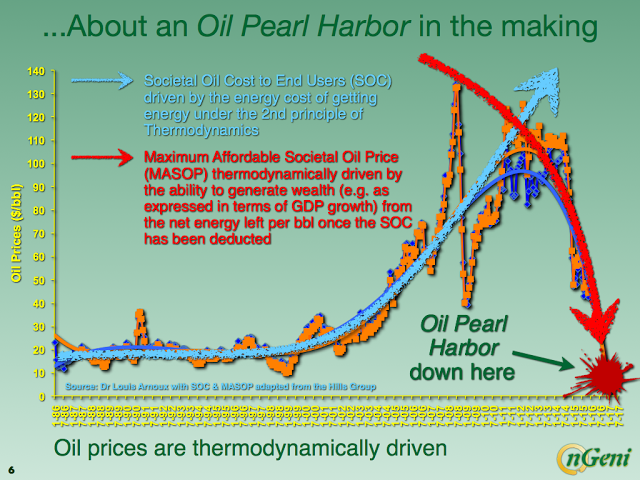

In that article, I posted some of the charts by Louis Arnoux and the Hills Group. These charts explained the coming “Thermodynamic Collapse” of the oil price and global oil industry… in a relatively short period of time. Since then, I have had several long conversations with Louis on the science and math of their work.

Let me tell you all, any doubts I have had about the accuracy and legitimacy of their work… IS COMPLETELY GONE.

Folks… we are in a real mess. And the damned thing of it all, the world has no clue. While I have been pessimistic about the ramifications of peak oil and the Falling EROI – Energy Returned On Investment for many years, now I understand there is a TIME CLOCK. And, we don’t have much time.

I have mentioned in a few interviews and articles that I was planning to have these gentlemen on for an interview to explain their work on the “Thermodynamic Oil Collapse.” I’d planned to have them on already, but it took more time to understand the science behind their work. Basically, it took more time for me to wrap my mind around the ramifications of this work.

Furthermore, it is extremely important to present this information in a way in which individuals can “GET IT’ or “CONNECT THE DOTS.” Because, once an individual understands this information, it’s like taking the ULTIMATE RED PILL. Once you comprehend it, you can’t go back. Thus, it will force you to look at the world in a completely different way.

I will be wrapping up the discussion between Louis and the Hills Group, and we will have them on in the next few weeks to discuss their work. Moreover, I have decided that we will likely do several interviews to get the point across as well as discuss the dire ramifications.

Lastly, my article THE DEATH OF THE BAKKEN OIL FIELD HAS BEGUN: Means Big Trouble For The U.S., went viral on many sites a week ago. It received nearly 100,000 views on Zerohedge. However, a really bizarre event took place on the peakoil.com website. When it was posted on the peakoil.com site, it received the most comments ever (from what the members stated). Normally, there are only about 35 diehard members that leave comments. Most articles only received between 10-30 comments.

However, my DEATH OF THE BAKKEN article received nearly 300 comments on the peakoil.com site, and the majority of them came from 100+ new members that day. What was really bizarre, was that the comments from these new members were all negative and may have been generated by what is called, a TROLL BOT ATTACK . This is what some of the members of the site were discussing.

The peakoil.com site has been discussing peak oil for years, so the information in my article wasn’t anything new. Although, the way it was presented or the title must have hit a nerve to generate such a large barrage of negative comments. So, it seems as if the global oil industry is in a much bigger trouble than I realized.

Please stay tuned for our upcoming interview on the Thermodynamic Collapse of Oil. It will be the most important information for individuals and investors to understand.

The Important Fundamentals Of the Top Four Precious Metals

Mine Production:

As I mentioned in the beginning of the article, there is a lot of incorrect analysis on the top four precious metals that has confused investors to no end. I will try to clear this up.

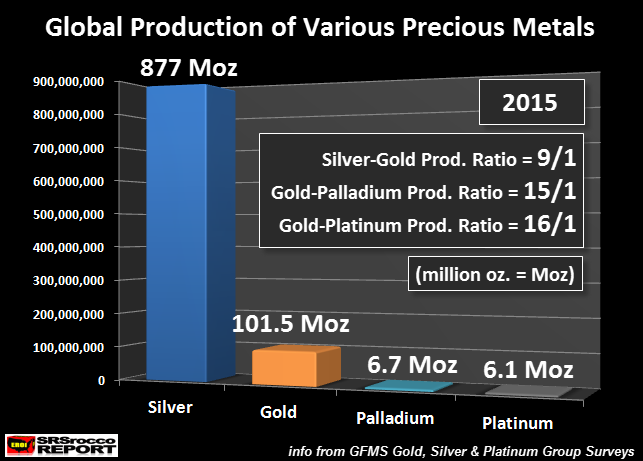

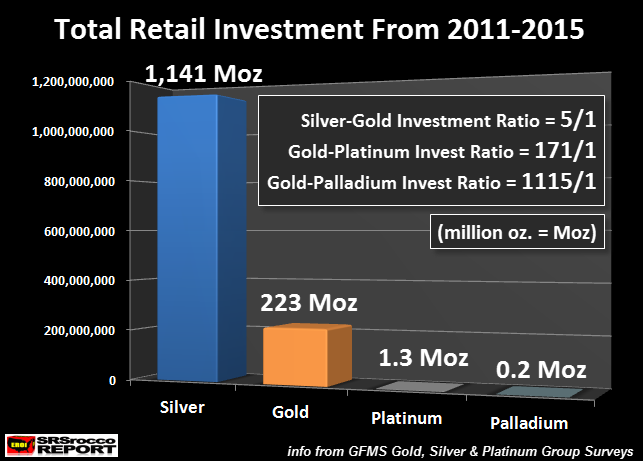

Let’s look at the annual mine production of silver, gold, palladium and platinum. According to the Gold, Silver & Platinum Group Surveys provided by GFMS (Thomson Reuters), the world produced 877 million oz (Moz) of silver, 101 Moz of gold, 6.7 Moz of palladium and 6.1 Moz of platinum in 2015:

As we can see, there are 9 times more silver produced than gold, 15 times more gold than palladium and 16 times more gold than platinum. Many analysts have erroneously stated that due to the rarity of platinum or palladium, its value should be much higher than gold. Furthermore, other analysts believe the value of silver should be much higher than its current 69/1 price ratio to gold, due to there being only nine times more silver produced than gold.

The silver to gold production ratio may have been more a representation of the market value of these two precious metals hundreds of years ago or in ancient times, due to the way it was extracted from the earth (by human and animal labor). However, this has changed since the late 1800’s, as the energy sources of coal and oil replaced human and animal labor.

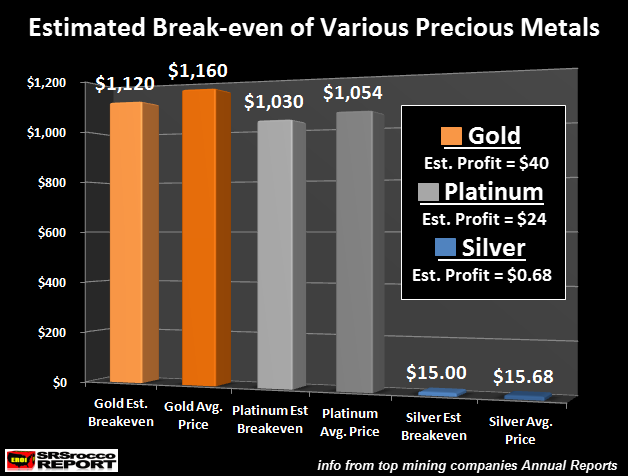

Gold, Platinum & Silver Estimated Production Cost:

The current values of the top four precious metals are based on their cost of production, not their production ratio. The chart below shows the estimated cost of production of gold, platinum and silver. I omitted palladium in my cost analysis below, because the largest producers of the metal are a by-product of nickel and platinum production. Regardless, I would imagine the few primary palladium producers probably produce palladium at the similar cost margins as gold, platinum and silver shown below:

My estimated breakeven for gold was based on using the mining companies of Barrick and Newmont. For platinum, it was Anglo American Platinum and Impala Platinum, and for silver,it was Pan American Silver and Tahoe Resources. These where the two largest primary metal producing companies for each metal.

NOTE: This was not my normal in-depth approach using many different formulas, but rather more of a simple cost approach using the mining companies net or adjusted income divided by total primary metal production. While the calculations could be more accurate, the figures above represent a pretty good estimated breakeven for these precious metals.

If we look at the chart above, we can see that the estimated break even for gold (Barrick & Newmont) in 2015 was $1,120 an ounce. The average price of gold in 2015 was $1,160. Thus, these top two gold mining companies made a $40 per ounce profit.

For platinum, the estimated breakeven was $1,130 in 2015, while the average price was $1,054. So, these top two platinum miners made a profit of $24 per oz. I believe this estimated platinum breakeven is a good estimate for the platinum industry as these two top companies produced 2.9 Moz of the total 6.1 Moz of platinum in 2015.

Now for silver. The top two primary silver mining companies estimated breakeven for 2015 was $15.00, while the average spot price was $15.68. Which means, these two primary silver miners made a profit of $0.68 an ounce. Actually, Tahoe Resources reported a very large profit, while Pan American Silver stated a loss in 2015. However, if we average these two companies, we come up with a $0.68 profit.

Basically, the profit margins of these three metals, based on my estimated breakeven, were 2.2% for platinum, 3.4% for gold and 4.5% for silver. These are very thin margins. These production cost profiles of these metals are what I believe the traders and or algorithms use to value gold, platinum and silver. I would imagine the same would be true for palladium, even though I did not construct a breakeven analysis.

So, the value of these metals are not based on their production ratio, but rather their cost of production. Which means, any precious metal analyst who says, “gold is the key monetary store of value metal”, doesn’t understand that it is currently being valued as a MERE COMMODITY, just like platinum, palladium and silver.

However, my analysis suggests the current gold and silver “commodity priced mechanism” will change to a high quality store of value when the worst financial crash in history takes place in the near future.

The Top 4 Precious Metals Investment:

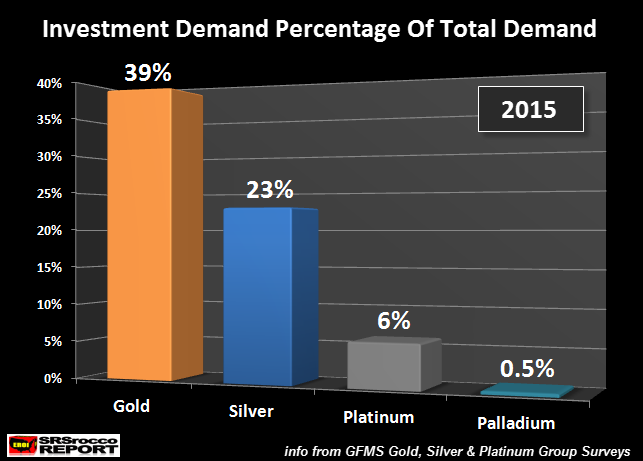

While most precious metals websites focus on promoting gold and silver investment, several are touting the benefit of owning platinum and palladium. Unfortunately, the majority of the reasons stated to own platinum or palladium may turn out to be incorrect or untrue in the future. That being said, let’s take a look at the percentage of physical retail investment versus total demand for each metal in 2015:

Gold was the clear winner as 39% of total demand was in physical retail and Central Bank investment. Gold was the only metal in which I included net Central Bank purchases. I excluded all investments (flows in or out) of ETF’s in each metal. Basically, the figures above represent physical retail investment (including Central Bank for gold).

Silver came in second as 23% of total demand was in bar and coin investment. As we can see, platinum investment was 6% of total demand, while palladium investment was only 0.5% (half percent) of total demand. All figures came from GFMS Gold, Silver & Platinum Metals Group Surveys.

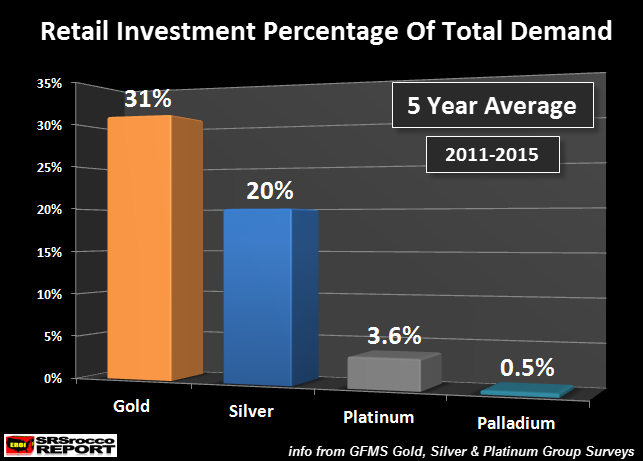

I decided to take a longer view of physical investment of these metals, so the chart below shows the average over a five-year period (2011-2015):

We can clearly see, gold and silver retail physical investment represent the highest percentages of total demand in the group. For whatever reason, investors innately understand the 2,000+ year history of gold and silver as money or a high quality store of value.

Even though gold enjoys a much higher investment percentage (31%) of total demand in the five-year period, silver is the clear winner when it comes to total amount of metal (in ounces) invested by the public:

Investors purchased a total of 1,141 Moz (1.14 billion oz) of silver 2011-2015, while gold investment was 223 Moz, platinum was 1.3 Moz and palladium at a distant fourth at 0.2 Moz.

These figures reveal a very significant “mindset” or “psychology” of investor preference. Of course, the total Dollar amount of gold investment of the 223 Moz is much higher than the 1,114 Moz of silver, but the volume of metal purchased, proves that investors have a real affinity for silver.

Why Gold & Silver, Not Platinum & Palladium Will Be The Key Precious Metals To Own During The Next Financial Crash

Looking at these figures, I would suggest that gold and silver will be the go to assets during the next financial crisis, not platinum and palladium. While platinum and palladium could provide the investor with some relative store of value properties in the future, the upcoming Thermodynamic Oil Collapse will destroy the market’s ability to produce or consume platinum and palladium at anywhere near the current volumes.

Unfortunately, most of the public has no clue about investing in platinum or palladium or realizing these metals as a store of value. Most of the investment into these (true) industrial metals are a hedge or bet on future supply shortages or price spikes. Rather, gold and silver are known more to the public as money and true stores of value.

While silver is PIGEON-HOLED by the Mainstream media and by many of the precious metals analysts to be more of an industrial metal, it is still an excellent store of value as gold. The only difference is its cost of production. However, the cost of production will become less of a driver for the value of gold and silver in the future as the $250 trillion in Global Bonds, Stocks, Real Estate and Insurance Funds evaporate in the future.

Again, this will be due to the coming Energy Pearl Harbor, shown in one of Louis Arnoux’s charts below:

Unfortunately, very few people understand the energy cliff that is heading our way. Instead, they cling to a notion that while a financial crash will be difficult, once the dust settles, we will begin growing and expanding our economy based on real money. Folks, growth as we know it, will be over for good.

This is why it is important to understand the ramifications of this energy cliff. Investors who understand the implications of this energy cliff will consider moving out of most stocks, bonds and real estate and into physical gold and silver.

end

Gold miner Petropavlovsk (Peter Hambro’s operation) finally turns a profit, its first in 4 years:

(courtesy London’s Telegraph)

Gold miner Petropavlovsk turns first profit since 2012

Submitted by cpowell on Wed, 2016-09-28 12:25. Section: Daily Dispatches

By Jon Yeomans

The Telegraph, London

Wednesday, September 28, 2016

Russia-based gold miner Petropavlovsk has posted its first profit since 2012, as it looks to move on from a torrid few years.

Petropavlovsk reported a pre-tax profit of $4.8 million in the six months to June, against a loss of $26 million for the same period a year ago. Revenue slipped 14.5 percent to $254 million as gold production fell after poor weather in the Amur region of Russia where it mines.

The company nearly went bust in 2015 but now expects to close a refinancing deal with its creditors next month that will extend its debt repayment schedule to 2022. Petropavlovsk borrowed heavily this decade to fund expansion, only to be hit by a downturn in gold prices. In the first half of the year it slashed $12.4 million from its debt pile, bringing it down to $598 million.

Chairman Peter Hambro, a City veteran, said: “It’s been a long struggle, but even a small profit is better than what we had in the past.” …

… For the remainder of the report:

http://www.telegraph.co.uk/business/2016/09/28/gold-miner-petropavlovsk-

END

Shangdong gold is the top bidder from Glencore’s gold property is Kazakhstan

(courtesy Bloomberg/GATA)

Shandong Gold said to be top bidder for $2 billion Glencore mine

Submitted by cpowell on Wed, 2016-09-28 04:06. Section: Daily Dispatches

By Dinesh Nair and Vinicy Chan

Bloomberg News

Tuesday, September 27, 2016

China’s Shandong Gold Mining Co. has emerged as the lead bidder for Glencore’s gold mine in Kazakhstan, which may fetch about $2 billion in a sale, according to people familiar with the matter.

Shandong Gold, one of China’s largest gold producers, outbid other parties, including Silk Road Fund, which had teamed up with state-owned China National Gold Group Corp., the people said, asking not to be identified as the information is private. Glencore is still weighing all options for the asset, including selling future production from the mine for a fixed amount, and may decide to retain it, the people said. …

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2016-09-27/shandong-gold-said-to-…

END

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.6672( REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS TO 6.6771 / Shanghai bourse CLOSED UP 10.63 POINTS OR 0.30% / HANG SANG CLOSED UP 119.82 POINTS OR 0.51%

2 Nikkei closed UP 228.31 OR 1.39% /USA: YEN RISES TO 101.49

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index UP to 95.50/Euro DOWN to 1.1229

3b Japan 10 year bond yield: RISES TO -.080%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 101.49/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 46.91 and Brent: 48.27

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES A BIT to -.119%

3j Greek 10 year bond yield FALLS to : 8.25%

3k Gold at $1317.40/silver $19.02(8:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble DOWN 08/100 in roubles/dollar) 63.16-

3m oil into the 46 dollar handle for WTI and 48 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 101.49 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9689 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0877 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLS to -.119%

/German 10+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.582% early this morning. Thirty year rate at 2.310% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Crude Declines As OPEC Deal Doubts Emerge; Futures Roll Over

After oil soared over 5% yesterday, its biggest jump since April which pushed the commodity to a three week high on the unexpected announcement that OPEC had agreed on cutting as much as 700kbpd in production (without providing any actual detail who would cut), overnight skepticism and doubts have emerged about the viability and compliance with the deal, coupled with a boost in production by non-OPEC producers, and as a result WTI has dipped back under $47, down 0.5%, suggesting that the OPEC surge may be short-lived and modestly pressuring US equity futures.

“Skepticism on the implementation is probably weighing on prices today – but we also need to see how the U.S. market reacts,” says Giovanni Staunovo, commodity analyst at UBS. Adding to the sentiment was Templeton Emerging Markets Group executive chairman Mark Mobius who said that “OPEC agreement to cut production is not set in stone and, as we have seen in the past, the words often don’t match the deeds.”

The modest rolloff in oil prices has also put a “cap” on US equity futures overnight, which were trading roughly unchanged during the overnight session, but not before yesterday’s euphoria pushed stocks in Asia and Europe higher. India’s assets fell after it attacked terrorist targets in Pakistan.

Energy companies led gains on the MSCI All-Country World Index, which is on course for its best quarter since 2013. Sovereign bonds fell amid speculation higher energy prices will revive inflation. After posting its biggest gain in five months, crude slipped under $47 a barrel. India’s rupee fell the most in three months after the biggest military escalation since 1999.

For those who missed yesterday’s main event, Bloomberg conveniently summarizes that OPEC said its members agreed a preliminary deal to trim production to a range of 32.5 million to 33 million barrels per day following informal talks in Algiers, although it won’t decide on targets for each country until a November meeting in Vienna.

A global oil glut has weighed on crude prices for more than two years as a result of the Saudi historic November 2014 decision to break away from the OPEC cartel in order to put shale companies out of business (a decision which appears to have been undone as of yesterday, handing the victory to US shale), damping inflation, hurting corporate earnings, and leading to negative bond yields in two of the world’s four biggest economies.

“It really caught people on the hop — we weren’t expecting a cut in output at all,” said Derek Mitchell, a fund manager at Royal London Asset Management in London. His fund owns shares of Royal Dutch Shell Plc and BP Plc and has assets under management of 93.8 billion pounds ($122 billion). “It sends a message that there’s now a floor under the oil price. A tighter oil market will support earnings. There’s rightly a great deal of skepticism as to whether this cut will last, but for the time being, it’s a very nice thing to wake up to.”

Some of the winners from OPEC’s plan include:

- Energy markets, from natural gas to coal and carbon were buoyed by the announcement.

- The Norwegian krone, the currency of Western Europe’s largest oil producer, touched its strongest level against the euro since August 2015, before giving up gains.

- Equity markets in Russia, Dubai, Qatar and Malaysia.

- Industrial metals lead and tin climbed to the highest in more than a year, as higher oil prices raise the cost of production.

- A global gauge of energy stocks rose. Tullow Oil Plc led gains among European oil-related companies.

Some of the losers from OPEC’s plan include:

- Bonds fell, while measures of the market’s inflation outlook in the U.S. and U.K. climbed.

- Travel-and-leisure stocks fell in Europe, with airlines including Deutsche Lufthansa AG leading the drop on prospects of higher fuel costs.

- Japan’s yen slumped amid speculation that increased oil costs will help the central bank achieve its policy goals.

The global reaction to the OPEC announcement was broadly bullish for risk assets which soared in kneejerk response, and the MSCI global index gained 0.4% as in early trade, extending this quarter’s advance to 5.4%. A gauge of energy shares jumped 1.5 percent after surging 2.8 percent in the last session. The Stoxx Europe 600 Index rose 0.7 percent, with oil companies leading the charge. Africa-focused explorer Tullow Oil jumped 7.1 percent, while Total SA and Shell added 4.5 percent or more.

Lenders took their rebound into a second day, with Deutsche Bank AG up 0.9 percent. Commerzbank AG bucked the trend, falling 0.6 percent after announcing plans to reduce 9,600 jobs and suspend dividends as Chief Executive Officer Martin Zielke seeks to shore up the German lender’s profitability. Travel-and-leisure stocks were among the casualties of the OPEC deal, as higher fuel costs make traveling more expensive and erode profits at companies including Lufthansa, which fell 2.7 percent, and Ryanair Plc, down 2.9 percent. Thomas Cook Group Plc dropped 3.6 percent.

S&P futures were fractionally lower, after U.S. shares advanced Wednesday on the back of rising oil prices. Investors will look to data Thursday, including wholesale inventories, gross domestic product, initial jobless claims and pending home sales, for indications of the health of the world’s biggest economy.

Federal Reserve Chair Janet Yellen is scheduled to speak Thursday, as are regional Fed chiefs for Atlanta, Minneapolis and Philadelphia. These will follow yesterday’s Fed speeches by dissenter Esther George (Voter, Hawk) who said the diversity of views is healthy for the FOMC and added the Fed needs to move forward on rate hikes slowly and surely. Fed’s Mester (Voter, Hawk) said the Fed could ruin its credibility by not acting on data and may fall behind curve if there is a delay in a hike. Mester also commented that sometimes being prudent means increasing rates and that fundamentals of the economy remain sound.

Bond market measures for the inflation outlook climbed from the U.S. to the U.K. following OPEC’s decision. The 10-year break-even rate in the U.K. was set for its highest close since July last year. A similar measure in the U.S. approached its highest level since June. The yield on 10-year U.S. Treasuries was steady at 1.58% and that for German bunds increased by three basis points to minus 0.12 percent. “The rise in Treasury yields after the OPEC news was contained because the decision to really cut production won’t be finalized until November,” Shinichiro Kadota, an FX strategist at Barclays told BLoomberg. “The Fed’s rate-increase path isn’t gaining momentum, making it unlikely for yields to extend their climb.”

Market Snapshot

- S&P 500 futures down less than 0.1% to 2162

- Stoxx 600 up 0.7% to 345

- FTSE 100 up 1.1% to 6922

- DAX up 0.9% to 10533

- German 10Yr yield up 3bps to -0.12%

- Italian 10Yr yield up 2bps to 1.2%

- Spanish 10Yr yield up 3bps to 0.92%

- S&P GSCI Index down less than 0.1% to 360.1

- MSCI Asia Pacific up 0.4% to 141

- Nikkei 225 up 1.4% to 16694

- Hang Seng up 0.5% to 23739

- Shanghai Composite up 0.4% to 2998

- S&P/ASX 200 up 1.1% to 5471

- US 10-yr yield up 1bp to 1.58%

- Dollar Index up 0.1% to 95.53

- WTI Crude futures down 0.6% to $46.78

- Brent Futures down 0.9% to $48.23

- Gold spot up less than 0.1% to $1,322

- Silver spot down 0.3% to $19.14

Top Global News

- Saudis Shock Oil World With Higher Prices Over Free Markets: OPEC to cap production at 32.5-33mbbl/d; revisit quotas at Nov. meeting.; Shale Drilling Revival Seen Ahead as Oil Price Recovers

- India Strikes Pakistan Terror Camps as Modi Hits Back for Attack: Heavy casualties inflicted on militants assembled to infiltrate India, according to India’s director general of military operations Ranbir Singh said.

- 9/11 Victim Families Can Sue Saudis; Obama Veto Overturned: Other countries may respond by allowing lawsuits vs U.S. for actions by American soldiers, diplomats or corporate executives.

- California Suspends Wells Fargo From Bond, Investing Work: U.S.’s largest issuer of municipal bonds WFC from underwriting state debt, handling its banking transactions.

- Elliott’s Paul Singer Buys More of GE’s 3-D Printer Target: Singer plans to acquire additional voting rights in SLM Solutions Group in the next 12 months.

- Sears, Claire’s at High Risk of Retail Failures: Fitch: Cos. named in report that found retailers wind up liquidated almost 3x more often than other companies in bankruptcy.

- Fed Politics in Spotlight as Yellen Cornered by Lawmaker: Republican congressman cornered Fed chair on whether key policy maker would have conflict of interest in discussing presidential post.

- Och-Ziff Unit Said to Plan to Plead Guilty Over Bribes: Agreed to enter deferred-prosecution agreement, also subsidiary plead guilty in probe into bribes funneled to African officials.

- Compromise Said to Be Discussed Ahead of FCC Set-Top Box Vote: FCC chairman offered concessions to win support for proposal to make it easier for consumers to buy set-top boxes from cos. other than their cable TV provider.

- YouTube Hires Ex-Def Jam Boss to Smooth Music Industry Ties: Hired Lyor Cohen as its global head of music.

- Yahoo! Hacked by Criminals, Not State Sponsor: Security Firm: Accounts were hacked in 2014 by cybercriminals, InfoArmor says.

Looking at regional markets, we begin in Asia where stock markets traded higher across the board as the energy sector coat-tailed on the 5% surge in crude, following the agreement by OPEC to cut output for the first time since 2008. This boosted oil names in both the ASX 200 (+1.1%) and Nikkei 225 (+1.4%), with the latter outperforming on JPY weakness after USD/JPY surged above 101.00. Shanghai Composite (+0.4%) and Hang Seng (+0.5%) conformed to the positive risk sentiment, although gains were capped amid rising repo rates, which followed a weaker liquidity injection by the PBoC ahead of next week’s Golden Week holiday. 10yr JGBs recovered initial losses amid a lack of demand due to the positive risk sentiment seen across Asia. Furthermore, today’s 2yr auction was tepid in which the b/c fell to its lowest since June 2015, while the latest securities transactions data showed foreign investors offloaded the largest amount of Japan bonds last week since 2014.

Top Asian News

- Deutsche Bank Said to Face Hurdle Moving China Sale Proceeds: German lender raising up to $3.9b from Huaxia sale

- China’s Big Ball of Money Isn’t Going Anywhere Near Stock Market: Investors flock to property, spurring bubble warnings

- Fulham’s Billionaire Rises From Dishwasher to Takata Bidder: Flex-N-Gate is said to be one of five bidders for Takata

- Turnbull Steps Up Attack on Renewables After Australian Blackout: Says Australian states’ renewable targets risk energy security

- Korean Court Rejects Arrest-Warrant Request for Lotte Chief: Prosecutors sought arrest on embezzlement allegations

European equity cash markets have seen buying support following the upside witnessed in the futures overnight, following OPEC agreeing on a production limit. The energy sector is the predicable outperformer in equity markets, up 5% on the session as WTI Crude futures now trade around USD 47.00/bbl with the next key resistance level being August’s 49.00/bbl high. Oil prices have weighed on airline names; Easyjet (-1.6%) and Lufthansa struggle in the Dax, (-2.4%). German Banks continue to be in focus with Commerzbank releasing downbeat news; source reports stating that the Co. is to lay off 20% of their workforce (10,000 employees) and furthermore, the bank is to suspend their dividend payments, expecting a write-down of EUR 700mln, although do still expect a small profit this year.

Top European News

- Deutsche Bank Said to Face Hurdle Moving China Sale Proceeds: Govt creating potential headache for seeking to sell $3.9b stake in a Chinese lender, also seeking permission to move proceeds offshore.

- German Unemployment Unexpectedly Rises in Sign Economy Slowing: Number of people out of work increased by seasonally adjusted 1,000 to 2.68m.

- Commerzbank Plans to Cut Jobs, Suspend Div. in CEO Overhaul: Bank will take costs of about ~EU1.1b to restructure businesses.

- Man Group CEO Sees Event-Driven Hedge Fund Pressure: “When individual funds get too big, or when they get stale, or when they get lazy to be honest the money will flow away from them,” Man Group CEO Luke Ellis said.

- Renault Defends Electric-Car Headstart With Longer-Range Zoe: Car will be able to travel as far as 400km on a single charge, compared with 240km now.

- Spanish Socialists Crack Under Pressure to Let Rajoy Rule: Dispute over whether to let acting PM Mariano Rajoy return to office tore apart Spain’s Socialist leadership.

In FX, the Bloomberg Dollar Spot Index rose 0.2 percent from its lowest close in more than two weeks. The yen slid 0.7 percent, among the biggest losers of major currencies, as investors favored higher-yielding assets outside of Japan. the ringgit strengthened 0.4 percent, leading gains among the currencies of oil-exporting nations. The Norwegian krone slipped 0.3 percent following a 1 percent jump in the last session. South Africa’s rand lost 0.9 percent and Turkey’s lira declined 0.7 percent. Mexico’s peso retreated from near a two-week high before a monetary policy review on Thursday, with most economists predicting interest rates will be raised. Taiwan also has a central bank meeting and its currency strengthened 0.2 percent from Monday’s close as trading resumed following a hurricane. Just over half of the economists in a Bloomberg survey forecast the island’s borrowing costs will be left unchanged, while the remainder were looking for a cut.

In commodities, crude oil fell 0.5 percent to $46.83 a barrel, retreating from a three-week high.The lower end of OPEC’s new production target equates to a nearly 750,000 barrels-a-day drop from what the group said it pumped in August. Saudi Arabia and Iran had signaled before the meeting that an agreement was unlikely in Algiers, while all but two of 23 analysts surveyed by Bloomberg predicted there would be no deal. Goldman Sachs Group Inc. said OPEC’s agreement to cut output could add as much as $10 a barrel to oil prices, though it remains skeptical along with other banks on how the accord will be implemented. Year-ahead European coal jumped to 20-month high amid increasing import demand from China. The equivalent Dutch gas contract surged to the highest for eight weeks and carbon permits rose to a three-month high. French and German power contracts both advanced to the highest since August 2015 amid reduced availability of French nuclear plants. Tin gained 0.5 percent to trade just shy of $20,000 a metric ton, a level last seen in early 2015. The metal used for solder in electronics has jumped 17 percent this quarter, the best performance on the London Metal Exchange. Lead rose 0.8 percent, heading for the highest since May last year. The LME index of six industrial metals is heading for a third successive quarterly gain for the first time since 2011 helped by an improving economy in China, the biggest consumer.

Bulletin Headline Summary from RanSquwk and Bloomberg

- European equities trade higher as European participants digest the fallout of yesterday’s OPEC announcement

- Naturally, energy names trade higher across the board with softness in airliners with not much else to report from the session thusfar

- Looking ahead, highlights include German unemployment, CPI, US GDP, weekly jobless data, as well as a host of speakers from Fed, ECB, BoE and BoJ

- Long-end Treasuries fall while global equities rally; oil prices drop after yday’s OPEC announcement sparked a rally in WTI.

- Goldman Sachs Group Inc. said OPEC’s deal to cut output could add as much as $10 a barrel to oil prices, though it remains skeptical along with other banks on how the accord will be implemented

- Oil analysts, many of whom were surprised by OPEC’s decision on Wednesday to set out the framework of a deal to limit oil production, remain split about the impact of the producer group’s plan

- BOJ’s Kuroda said in overnight speech that options for further easing include targeting lower rates in yield curve control, boosting asset purchases and increasing the pace of monetary base expansion

- Federal Reserve Bank of Philadelphia President Patrick Harker says U.S. “economy has reached a point where monetary policy has done what it can”

- Commerzbank AG plans to reduce 9,600 jobs, or about a fifth of the workforce, and suspend dividends as Chief Executive Officer Martin Zielke seeks to shore up profitability at the German lender

- German unemployment unexpectedly rose in September for the first time in a year, in a sign of concern among businesses over an economic slowdown and the consequences of Britain’s decision to leave the European Union

- Euro-area economic confidence unexpectedly improved in September in a sign the region’s recovery is maintaining its momentum

- Institutions face returns that will be lower than historical gains and in some cases less than what they need to meet their liabilities, according to Oaktree Capital Groups Howard Marks

- India said it attacked terrorist camps just across the border in Pakistan, the biggest military escalation since a standoff in 1999, as Prime Minister Narendra Modi retaliated for a deadly strike against Indian soldiers earlier this month

DB’s Jim Reid concludes the overnight wrap

It’s probably fair to say that over the last few weeks and months, markets had become somewhat accustomed to the flurry of jawboning, back-and-forth headlines and general bickering between the major Oil producing nations over whether or not to curb output. It therefore felt like the general consensus was leaning towards a ‘more of the same’ type outcome from the sideline OPEC meeting so when the headlines broke last night reporting that the cartel had agreed to the framework of a deal that will cut production, that was enough to send Oil related assets surging.

Indeed WTI rallied as much as 7% off the intraday lows before finishing the day with a +5.33% gain, the most since April 8th. Brent also rallied +5.92% and closed at the highest level ($48.69/bbl) since August 30th. WTI is up a further +0.20% this morning. The rest of the energy complex got a boost too with Gasoline (+6.03%) and Heating Oil (+5.75%) in particular up sharply. Oil sensitive currencies gained with the Russian Ruble (+1.35%), Norwegian Krone (+1.00%) and Canadian Dollar (+0.89%) coming out top. Unsurprisingly it was energy stocks which dragged US equities up from early session lows. The S&P 500 was down as much -0.38% but swung to a +0.53% gain by the closing bell with the energy sector alone up over +4%. Oil heavyweights Exxon Mobil (+4.40%), Chevron (+3.20%), Schlumberger (+3.56%) and ConocoPhillips (+6.97%) all leading the sector higher. In credit markets CDX IG ended 2bps tighter.

The move by OPEC to a preliminary agreement to cut production to 32.5m barrels per day is the first reduction since 2008 and according to our commodity strategists would lower 2017 production by 1.1m barrels per day based on their assumptions. The early indications suggest that the agreement may follow the outline of an Algerian proposal for a 1.6% reduction from the Jan-Aug averages for all member countries apart from Libya, Iran and Nigeria. Under this proposal, Iran would be permitted to raise production only up to 3.7m barrels per day which is a small increment from its reported August production of 3.64m barrels. The devil is in the detail though and as our colleagues highlight the precise country level production quotas will not be decided until the November 30th OPEC ordinary meeting. As a result countries may not act to reduce output until December. A more complete assessment of the overall impact will likely depend on the eventual shape of the final agreement which we might have to wait until the end of November to get, along with the potential participation of any non-OPEC producing countries.

So there are still the details to iron out and perhaps the greater question is whether or not the market will trust OPEC to follow through with action and actually cut. Waiting until November also brings a kicking the can type element to all this and one would imagine that implementing the individual country quotas could be where the disputes start but to be fair the preliminary agreement is certainly more than most would have expected.

This morning in Asia bourses are off to a decent start and it won’t come as a surprise to hear that the energy sector is leading the way. The Nikkei (+1.42%), Hang Seng (+0.34%), Shanghai Comp (+0.68%), Kospi (+0.81%) and ASX (+0.93%) are all up with energy sectors generally up between 3% and 6%. Emerging market currencies are on the whole stronger this morning while the Yen has weakened -0.60%. Credit indices are also 1-2bps tighter while US equity index futures are also pointing towards to positive start. The only data released this morning came in Japan where retail sales disappointed last month (-1.1% mom vs. -0.6% expected).

Staying in Asia, yesterday our Chief China Economist Zhiwei Zhang published a report titled ‘China’s Property Bubble’. Zhiwei believes that a property bubble is rising in some Chinese cities. After conducting a bottom up analysis of 252 land auctions in ten cities, Zhiwei found that property prices have already risen 23% yoy in these cities, but soaring land auction premiums revealed a very high expectation of further property price inflation. He notes that if property prices stay at the current level, developers in 105 cases may lose money, accounting for 53% of total land sales value. If property prices fall by 30%, these numbers would go up to 181 cases and 81% of total land sales value. Zhiwei and his team also believe that the risk of a bubble is spreading to more cities in China and notes that if the property cycle trends down from here with prices falling 10% nationwide, some 28% buyers in land auctions since July 2015 may lose money. The loss could be around RMB243 billion. To avoid a collapse of the property bubble Zhiwei is expecting the PBoC to cut interest rates in Q2 next year and loosen liquidity conditions. He has also trimmed his 2018 GDP forecast to 6%, but kept his 2017 forecast at 6.5% based on policy easing.

Moving on. Prior to the OPEC headlines last night the latest durable and capital goods orders numbers in the US made for a bit of mixed reading. The preliminary August data was broadly better than expected. Headline durable goods orders were unchanged last month versus expectations for a -1.5% mom decline while the ex-transportation declined a little bit less than expected (-0.4% mom vs. -0.5% expected). Core capex orders (+0.6% mom vs. -0.1% expected) also surprised to the upside. What was disappointing though were the downward revisions to the July data. Headline orders were revised down to +3.6% from +4.4%, ex transportation to +1.1% from +1.3% and core capex orders to +0.8% from +1.5%. As a result the Atlanta Fed trimmed its Q3 GDP forecast to 2.8% from 2.9%.

There was also a reasonable amount of Fedspeak to take stock of yesterday but none of which really moved the dial. The latest to speak was the Kansas City Fed’s George (a renowned hawk) who said that ‘we need to slowly but surely make progress in adjusting that interest rate so we don’t get far behind’. The Cleveland Fed’s Mester – another dissenter – said that ‘at this point, I think there’s a very compelling case to take the next step on a very gradual path’, warning also that any delay increases the risk to having to undertake a considerably steeper policy path later on. The rest of the comments came from the centrist and more dovish camp. The Chicago Fed’s Evans said that the ‘economy is actually doing quite well’ but that ‘if inflation were closer or at our objective then it probably would be closer to the time to be raising rates’. Meanwhile the Minneapolis Fed’s Kashkari said that ‘the economy still has room to run before it overheats’.

Elsewhere, Fed Chair Yellen was also speaking yesterday in a testimony before the House Financial Services Committee. Much of the testimony was focused on Yellen defending the regulatory role of the Fed and addressing accusations of potential conflicts of interest although the Fed Chair also highlighted that monthly job gains are well above a sustainable long run path, although she isn’t yet seeing upward pressure on inflation.

Her colleague at the ECB, Mario Draghi, was also busy defending recent action by the ECB from German lawmakers, saying on balance that savers, employees and pensioners across the Euro area are better off today and tomorrow because of the actions of the ECB. It was a better day for European stocks yesterday with the Stoxx 600 closing up +0.70% and the DAX +0.74%, the latter gaining for the first time since last Thursday.

Looking at the day ahead, this morning in Europe the early data release comes from Germany where the September unemployment rate print is due. Shortly following that we turn our attention to the UK where money and credit aggregates data is due, along with the August mortgage approvals data. We’ll then get various confidence indicators for the Euro area before its back to Germany with the preliminary September CPI report. Across the pond this afternoon the main focus will be on the third reading of Q2 GDP. The market is expecting the reading to be revised up to +1.3% qoq from +1.1% while our US economists have pegged an increase to +1.4%. Also due out is the advance goods trade balance reading for August, wholesale inventories for last month, the latest initial jobless claims print and finally pending home sales data. Away from the data there’s no shortage of Fedspeak scheduled. Harker is due to speak at 10am BST followed by Lockhart at 1.20pm BST, Powell at 3pm BST and Kashkari at 7pm BST. If that wasn’t enough, Fed Chair Yellen is also scheduled to address a minority banking conference tonight at 9pm BST. Away from the Fed we’ll also hear from the ECB’s Praet this morning and Constancio this afternoon, along with the BoE’s Forbes around lunchtime.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed UP 10.63 POINTS OR .30%/ /Hang Sang closed UP 119.82 POINTS OR 0.51%. The Nikkei closed UP 228.31 POINTS OR 1.39% Australia’s all ordinaires CLOSED UP 1.09% /Chinese yuan (ONSHORE) closed UP at 6.6672/Oil FELL to 46.91 dollars per barrel for WTI and 48.27 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.6771 yuan to the dollar vs 6.6672 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

3a)NORTH KOREA:

none today

b) REPORT ON JAPAN

none today

end

c) Report on CHINA

China’s beige book reveals real problems in the Chinese economy. We have highlighted to you last week that loan demand is down badly (corporate loans) while house loan demand is up (and thus the huge housing bubble)

(courtesy zero hedge)

“It’s A Lot More Negative Than People Think” – China Beige Book Issues Stark Warning About The Economy

While China’s excess debt problems have been extensively documented, the overall economy appears to also be slowing substantially as a result of the decline in the most recent credit impulse, noted as recently as one week ago when we reported that “Chinese Loan Demand Dropped To All Time Low.” Overnight, the latest warning about China’s economy came from the authors of the China Beige Book, a quarterly survey that tracks the world’s second-largest economy, who said that recent stability in the Chinese economy masks deep-seated problems that threaten to rattle global markets in advance of a leadership change next year, and added that ignoring these risks is shortsighted.

As reported by the WSJ, data from the group’s Q3 survey of 3,100 Chinese firms and 160 bankers point to some potential problems. New growth engines intended to shift the economy away from investment toward consumption-led growth are increasingly wobbly as corporate cash flow is squeezed and Beijing doubles down on traditional engines to stabilize output, the China Beige Book says.

“I’d find it earth-shatteringly surprising if we don’t have a significant problem between now and China’s leadership change” in the fall of 2017 when the 19th Party Congress convenes, said Leland Miller, China Beige Book’s president. “This is not a stable economy. It’s one that twists and turns and happens to end up at the same spot. There are real problems below the surface.”

More troubling, the report notes, growth in China’s service industry, a cornerstone of its planned transition to a new and more sustainable economic model, weakened during the third quarter as financial services, private healthcare, telecommunications, media and other subsectors flagged. In retail, the apparel, luxury goods and food sectors slowed, it said, as online retailers continued to cannibalize brick-and-mortar sales.

Despite Beijing’s pledge to reduce excess Industrial capacity and pare debt, China remains heavily dependent on government spending to power traditional debt-fueled growth engines, the group said. Much of the economic momentum during the third quarter came from infrastructure, manufacturing, commodities and real estate and many of these sectors are in danger of losing momentum, it said.

As the WSJ further notes, while property sales remained strong in major cities, cash flow in the sector tightened and borrowing increased, a sign that investors should “think about getting off this train sooner rather than later,” the China Beige Book said.“ Deteriorating corporate finances and a rebalancing reversal seem a high price to pay for a quarter’s worth of stability,” the group added.

When China reports Q3 GDP next month, it is expected to goalseek a number around 6.7%, the level it posted in both the first and second quarters. Gauges such as industrial production and fixed-asset investment have been surprisingly robust over the past month. However, the trigger for another potential market jolt in the next few quarters could be the release of particularly weak Chinese service or retail data coinciding with a Federal Reserve interest rate rise or another global event, Miller said. “Right now, the markets are lulled to sleep,” he said. “People become used to the stable China narrative until they start looking more closely into the data.”

For now, however, most are unwilling to look more closely into the data.

Economists say they expect the Chinese economy to remain relative stable through the once-in-five-year leadership change, which is expected to be in October or November of 2017, as long as Beijing continues stimulating the economy enough to avoid a drop in growth. “I don’t think there’s going to be a crisis next year,” said Julian Evans-Pritchard, an economist with Capital Economics Pte. “But they often take their foot off the pedal too much, then tend to panic again and put it back on, creating a lag.”

The Bank for International Settlements warned last week that mounting leverage raises the risk of a financial crisis in China. The nation’s total debt, led by rising corporate obligations, is on target to reach 253% of gross domestic product by the end of 2016, a doubling over the past eight years, according to credit ratings agency Fitch Ratings Inc.

It wasn’t all bad news however: courtesy of the recent wave to preserve zombie enterprises and near-insolvent corporations, the Chinese job market remains strong. The manufacturing outlook improved with new domestic and international factory orders picking up and deflationary pressure on industry ebbing. “It was not a disaster of a quarter,” Mr. Miller said.

“But it’s a lot more negative than people think.”

end

As we pointed out to you yesterday, China has a massive housing bubble which will burst at any time. There is not enough growth to sustain those higher prices

(courtesy zero hedge)

China’s Richest Man Says Mainland Real Estate Is The “Biggest Bubble In History”

The richest man in China, Wang Jianlin, made his ~$30 billion fortune by developed huge malls and office complexes across China but he now says Chinese real estate is the “biggest bubble in history.”

Certainly, one has to look no further than our post from yesterday entitled “Viral Surveillance Video Reveals A Shocking Scene From China’s Housing Bubble” to get a sense of just how “bubblicious” the China property market has become. Below is footage from a surveillance camera that caught the moment a new real estate development in east Hangzhou opened for sale on September 24th.

The big problem, according to Jianlin, is that prices keep rising in major Chinese cities like Shanghai but are collapsing in thousands of smaller cities where huge numbers of properties lie vacant. Per an interview with CNN, Jianlin notes that rising household debt is a major issue fueling the bubble but Chinese officials have been reluctant to restrict leverage due to the fear of the economic consequences.

“I don’t see a good solution to this problem,” he said. “The government has come up with all sorts of measures — limiting purchase or credit — but none have worked.”

It’s a serious worry in China, where the economy is slowing at the same time as high debt levels continue to increase rapidly. There are massive sums at stake in the real estate market: direct loans to the sector stood at roughly 24 trillion yuan ($3.6 trillion) at the end of June, according to Capital Economics.

“The problem is the economy hasn’t bottomed out,” Wang said. “If we remove leverage too fast, the economy may suffer further. So we’ll have to wait until the economy is back on the track of rebounding — that’s when we gradually reduce leverage and debts.”

Jianlin has been warning of a bubble in Chinese real estate for a while which has prompted his recentbuying spree of international assets. So far in 2016, Jianlin has been gobbling up U.S. based media companies including the Hollywood studio Legendary Entertainment, the movie theater business Carmike Cinemas and he is currently in talks to buy Dick Clark Productions.

Meanwhile UBS China Economist, Tao Wang, says the China real estate bubble isn’t a concern because it hasn’t yet pushed household debt to alarming levels…

Not yet a bubble that’s about to significantly damage the economy. The recent property market frenzy has not yet spread to a great many cities, pushed household debt up to alarming levels, or led to strong construction growth.

…Even though her charts seem to paint a slightly different picture.

Property prices seem to be surging across the board…

…while buyers are relying on a record amount of leverage to fund purchases…

…pushing household consumer debt closer to 250% of disposable income…

…all while there is seemingly 4-5 years worth of incremental residential supply under construction.

But we’ll take Wang’s word for it…probably nothing to see here.

end

4 EUROPEAN AFFAIRS

Germany

Germany’s second largest bank Commerzbank this morning scraps its dividend and fires 20% of its workforce. And this is Germany, the powerhouse of Europe. The growth in the economy is just not existent.

(courtesy zero hedge)

Pain Spreads To Germany’s Second Biggest Bank: Commerzbank Scraps Dividend, Fires 20% Of Workforce

With Deutsche Bank mercifully missing from overnight headlines for the first day in almost two weeks, it is time to bring attention to Germany’s second largest bank which, as we first reported earlier in the week citing a Handelsblatt leak, confirmed it is also going through a historic rough patch. This morning, Commerzbank said it plans a wide-ranging business restructuring that includes scrapping the bank’s dividend for the rest of the year, terminating nearly 10,000 jobs – roughly 20% of its workforce – and merging two large units.

“The focus on the core business, with some business activities being discontinued, and the digitalization and automation of workflows will lead to staff reductions amounting to around 9,600 full-time positions,” Germany’s second-largest lender said.

The plan, according to the WSJ, is a strong sign new Chief Executive Martin Zielke is determined to shrink the partially state-owned bank amid a protracted period of ultra-low or negative interest rates and weak client demand.

While the overhaul and liquidity “shoring” was previously reported in recent weeks, it came as a surprise because the bank portrayed the picture of an institute that is done emerging from an extensive overhaul when former Chief Executive Martin Blessing in November last year said he would leave the bank. However, now the bank is merging its investment bank with the unit that caters to small and midsize enterprises. The renewed efforts to streamline Germany’s second-largest bank mark the first moves Mr. Zielke, who took the helm at Commerzbank in May.

There is a silver lining: the 20% headcount reduction will be offset by the hiring of 2,300 new workers as the bank efforts to make workflows more digital.

The bottom line: the restructuring will cost about €1.1 billion ($1.2 billion) and it will book a €700 million loss in the third quarter. It added that it would therefore scrap dividend payments for “the time being.” It paid €0.20 a share in May for 2015, the first dividend since its €18 billion government bailout in 2008, and originally planned to pay a dividend for this year.

end

Germany Deutsche bank

Major problems with Deutsche bank tonight as hedge funds that deal with DB as counterparties are withdrawing their funds as they fear the worst. Also there is a huge shortage of dollars similar to what happened with Lehman.European bank have just increased their demand for dollars by 6000%. Short dated CDS (credit default swaps on DB is skyrocketing. Ladies and Gentlemen: I believe we are having a Lehman moment as we are experiencing an old fashioned run on Deutsche bank

(courtesy zero hedge)

The Run Begins: Deutsche Bank Hedge Fund Clients Withdraw Excess Cash

Deutsche Bank concerns just went to ’11’ as Bloomberg reports a number of funds that clear derivatives trades with Deutsche Bank AG have withdrawn some excess cash and positions held at the lender, a sign of counterparties’ mounting concerns about doing business with Europe’s largest investment bank.

While the vast majority of Deutsche Bank’s more than 200 derivatives-clearing clients have made no changes, some funds that use the bank’s prime brokerage service have moved part of their listed derivatives holdings to other firms this week, according to an internal bank document seen by Bloomberg News.

Millennium Partners, Capula Investment Management and Rokos Capital Management are among about 10 hedge funds that have cut their exposure, said a person familiar with the situation who declined to be identified talking about confidential client matters.

The hedge funds use Deutsche Bank to clear their listed derivatives transactions because they are not members of clearinghouses. Millennium, Capula and Rokos declined to comment when contacted by phone or e-mail.

Which explains why short-dated CDS is soaring.

“Our trading clients are amongst the world’s most sophisticated investors,” Michael Golden, a spokesman for Deutsche Bank, said in an e-mailed statement.

“We are confident that the vast majority of them have a full understanding of our stable financial position, the current macroeconomic environment, the litigation process in the U.S. and the progress we are making with our strategy.”

Clients review their exposure to counterparties to avoid situations like the 2008 collapse of Lehman Brothers Holdings Inc. and MF Global’s 2011 bankruptcy when hedge funds had billions of dollars of assets frozen until the resolution of lengthy legal proceedings.

As expected, Deutsche Bank stock in NY is sliding.

If the most sophisticated professionals in the world are withdrawing cash, why are German depositors leaving their life savings at risk… ahead of a long weekend in Germany (Monday is a bank holiday).

* * *

And for those believing that there is no contagion and this is all ring-fenced…

And US banks are sliding…

As a reminder, if the liquidity run forces DB to start unwinding or being forced to novate derivatives, it could get ugly.

Those who have cash parked at Deutsche Bank, and at last check there was about €566 billion, they may want to consider moving it for the time being to a safer bank.

* * *

Earlier this morning, we reported that Europe is experiencing a sudden and acute dollar shortage, which we attributed to Deutsche Bank. It now appears this was accurate. Since Deutsche’s recent highs, the short-end of the EUR-USD basis swap curve has collapsed:

Simplifying – this chart measures the degree of USD shortage

(willingness to spend money just to get USD now) across time – the lower

the level, the more desperate for USDs.

And no, it’s not a quarter-end issue:

Still not sure… Then explain why European banks just increased

their demand for USDs from The ECB’s 7-day lending facility by over

2000%…

As @Landonthomasjr notes, since 2009: DB shareholders put up 13.5 billion euros in equity. DB has paid 19.3 billion euro in bonuses. Perhaps they should have saved some of that cash eh?

Simply put – trust in the European Banking system is faltering, counterparty risk hedging is accelerating:

And liquidity concerns are exploding, ahead of Germany’s bank holiday on Monday.

Deutsche Bank Is Now Smaller Than Twitter

ust some context for what has happened…

Of course EV would be a more accurate comp, but still, things are not good.

Still Bob Pisani says it’s nothing to worry about, probably.

The Financial System Is On The Cusp Of Collapse

DB stock is now in a full panic sell-off as I write this. It just hit another new all-time NYSE low on by the heaviest volume ever in the stock since its 2001 NYSE listing. It’s currently down almost 10%. No doubt the Central Banks will try to bounce it.