Gold $1251.10 DOWN $3.90

Silver 17.46 DOWN 1 cent

In the access market 5:15 pm

Gold: 1255.60

Silver: 17.48

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix OCT 12 (10:15 pm est last night): $ 1261.25

NY ACCESS PRICE: $1258.90 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1259.69

NY ACCESS PRICE: 1255.60 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: OCT 12: 5:30 am est: $1256.40 (NY: same time: $1256.40: 5:30AM)

London Second fix OCT 11: 10 am est: $1256.50 (NY same time: $1256.90 , 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

3 NOTICES FILED FOR 300 OZ

For silver:

for the Oct contract month: 0 notices for NIL oz.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 1,532 contracts DOWN to 187,469. The open interest FELL as the silver price was UP 5 cents in yesterday’s trading .In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .938 BILLION TO BE EXACT or 134% of annual global silver production (ex Russia &ex China).

In silver for October we had 0 notices served upon for nil oz

In gold, the total comex gold fell by 5117 contracts with the tiny rise in price of gold( $1.50 yesterday) . The total gold OI stands at 500,328 contracts. The bankers have done a great job fleecing longs

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

LAST NIGHT WE HAD NO CHANGES OUT OF THE GLD//

Total gold inventory rests tonight at: 958.90 tonnes of gold

SLV

we had NO CHANGES at the SLV

THE SLV Inventory rests at: 361.147 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL by 1532 contracts DOWN to 187,469 as the price of silver rose by 5 cents with yesterday’s trading.The gold open interest FELL by 5517 contracts DOWN to 500,328 as the price of gold rose $1.50 IN YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

end

2c) Federal Reserve Bank of New York/earmarked gold removal

(Harvey)

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 6.72 POINTS OR 0.22%/ /Hang Sang closed DOWN 142,47 POINTS OR 0.60%. The Nikkei closed DOWN 184.76 POINTS OR 1.09% Australia’s all ordinaires CLOSED DOWN 0.09% /Chinese yuan (ONSHORE) closed UP at 6.67157/Oil ROSE to 51.06 dollars per barrel for WTI and 52.63 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.6721 yuan to the dollar vs 6.67197 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND:

Thai stocks plummet along with their currency on concerns of the King’s health and the Fed rate hike. Remember it was Thailand that caused the Asian contagion in 1997:

(courtesy zero hedge)

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

NONE TODAY

4 EUROPEAN AFFAIRS

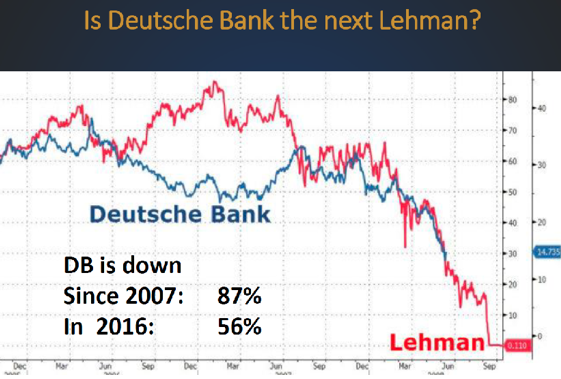

i)GERMANY/DEUTSCHE BANK

Deutsche bank sells another 1.5 billion dollars worth of bonds at a yield of 4.25%: basically at junk. This is done prior to any announcement of a settlement. In January these guys can be bailed in if trouble occurs:

( zero hedge)

ii)ENGLAND

The now have a British bond bloodbath (occurring right after a huge downfall in the currency:

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

ERICSSON/SWEDEN

A good indicator of troubles throughout the globe; huge telecom giant Ericsson plunges 17% after a profit warning:

( zero hedge)

7.OIL ISSUES

i)Crude tumbles after OPEC raises doubts over the timing of cuts:

( zero hedge)

ii)Confusion with OPEC: they do not know who is to cut first. Oil will head southbound especially when China stops buying;

8.EMERGING MARKETS

none today

9.PHYSICAL STORIES

i)To understand gold you must realize that the market is just not normal

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)Another of Janet’s favourites: the JOLTS survey which details job openings and leavings. The job opening s missed the most on record and tumbles to last yrs level.

( zero hedge)

ii)Consumer spending again deteriorates in September.

( zero hedge)

iii)The FOMC minutes were released and in it we find that the hawkish fed is very fearful of losing credibility. They also state that the no hike decision was a close call

( zero hedge)

iv)Let’s close with this important paper from Egon Von Greyerz:

(courtesy Egon Von Greyerz/Matterhorn)

Let us head over to the comex:

The total gold comex open interest FELL BY 5517 CONTRACTS to an OI level of 500,328 as the price of gold ROSE by $1.50 with YESTERDAY’S trading.

We are in the delivery month is October and here the OI LOST 146 contracts DOWN to 152. We had 156 notices filed yesterday so we gained another 10 contracts or 1000 additional oz will stand.

The next delivery month is November and here the OI ROSE by 1 contract up to 3026 contracts. The next contract month and the biggest of the year is December and here this month showed an decrease of 6081 contracts down to 379,949.

And now for the wild silver comex results. Total silver OI FELL BY 1532 contracts from 189,021 down to 187,469 as the price of silver rose to the tune of 5 cents yesterday. We are moving further from the all time record high for silver open interest set on Wednesday August 3: (224,540). The next non active delivery month is October and here the OI rose by 2 contracts up to 114. We had 0 notices filed yesterday so we gained 2 contracts or 10,000 additional oz will stand for delivery.The November contract month saw its OI FELL by 3 contracts DOWN to 341. The next major delivery month is December and here it FELL BY 1863 contracts DOWN to 153,348

VOLUMES.

Today the estimated volume was 117,327 contracts.

Yesterday, the confirmed volume was 155,362

today we had 0 notices filed for silver:

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | NIL |

| Withdrawals from Customer Inventory in oz nil |

44,480.719 Scotia

Manfra

incl

3 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz

|

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

3 notices

300 oz

|

| No of oz to be served (notices) |

149 contracts

14,900

oz

|

| Total monthly oz gold served (contracts) so far this month |

7948 contracts

794,800 oz

24.7216 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 129,678.8 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 156 contract of which 2 notices were stopped (received) by jPMorgan dealer and 44 notice(s) was (were) stopped received) by jPMorgan customer account.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

902,910.520 oz

Brinks

CNT

HSBC

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

581,935.519 oz

|

| No of oz served today (contracts) |

0 CONTRACTS

(20,000 OZ)

|

| No of oz to be served (notices) |

114 contracts

(570,000 oz)

|

| Total monthly oz silver served (contracts) | 353 contracts (1,765,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,986,418.5 oz |

end

NPV for Sprott and Central Fund of Canada

will not provide today.

end

FEDERAL RESERVE BANK OF NEW YORK/GOLD INVENTORY MOVEMENT:

Last month we had a reading of 7883 million dollars worth of gold at the FRBNY at $42.22 dollars per oz. This month we had a reading of 7849 million dollars

Thus we had 34 million dollars worth of gold valued at $42.22 shipped out.

In oz:

34,000,000 divided by $42.22 = 805,305 oz

in tonnage:25.048 tonnes

Since Germany is the only official nation seeking its gold, no doubt that this gold was repatriated towards Frankfurt.

end

And now your overnight trading in gold,WEDNESDAY MORNING and also physical stories that may interest you:

Gold In GBP Up 43% YTD – “Massive Twin Deficits” To Impact UK Assets

Gold in GBP has risen another 3.5% in the last 3 trading days as the British pound continues to be “pounded” on international markets. Gold in GBP terms is now 43% higher year to date and has risen from £716/oz on January 1st to £1024/oz today.

Sterling is now the worst performing major currency in 2016 and gold the best.

Gold in GBP (10 Years)

The pound has completed its worst four day performance since Brexit and the pound remains considerably weaker versus the dollar, euro and gold since the Conservative Party conference, when Theresa May promised to trigger article 50 within six months.

Heavy losses sent sterling down by another 2 per cent yesterday to below $1.21 against the dollar, while against the euro, the pound fell below €1.10.

The pound has bounced back a little today but market participants are increasingly alarmed at the political prospect of a severe rupture between the UK and EU. All the focus has been on the real risks posed by a “Hard Brexit” but another major risk is being greatly underestimated. There is also the significant risk posed by the very poor financial situation that the UK finds itself in – with its massive twin deficits.

HSBC’s respected currency analyst David Bloom warned in a note:

“the question we have asked hundreds of investors throughout the world is do you want to buy a currency that has massive twin deficits with an unknown political direction and for that risk you can get zero rates?”

UK gilts have come under selling pressure in recent days and the yield on the 10 year is now at 1.03%.

The UK current account and budget deficits combined are around 10% of UK GDP. The UK budget shortfall was 33.8 billion pounds ($44 billion) in the first five months of the 2016-17 fiscal year. The UK budget deficit for August alone was £10.5 billion, higher than economists forecast.

Kit Juckes at Societe Generale in London warns that the demise of the UK currency could soon start impacting a broader range of assets:

“Press comment is now shifting to embracing the positive effects of a weak Pound and in due course that’ll be true but any further weakness from here might simply reflect loss of confidence and be bad for UK assets (gilts, equities, house prices, you name it…) in general.

“The market’s very short, but if Sterling weakness starts to feed weakness across assets, we will have all the conditions for a classic overshoot to start.”

Currency analysts expect sterling to fall a lot further which underlines the value of owning gold, both against local currency depreciation and also the loss of value of UK assets denominated in sterling.

HSBC is forecasting GBP—USD at 1.20 by year end and 1.10 by end 2017, taking EUR–GBP to parity. Morgan Stanley is targeting 1.24 in USD and 0.92 for EUR—GBP “relatively soon.”

Sterling dived 10% against US dollar in seconds last Friday night but the trade was later cancelled. Despite the cancelling of the allegedly “rogue trade”, a “flash crash” of 6% was still registered.

With this hugely volatile and uncertain backdrop, allied to the uncertain global geo-political and economic outlook, we are confident that gold in GBP terms will reach new nominal highs over £1,200/oz in the coming months, from £1,024/oz today (see chart above). It remains an important diversification and hedge for UK investors, savers and pension owners.

Understanding gold begins with realizing that its market isn’t normal

4:06p ET Tuesday, October 11, 2016

Dear Friend of GATA and Gold:

When he’s not touting mining stocks in which he has invested, 321Gold’s Bob Moriarty is assuring his readers that everything in the monetary metals markets is perfectly normal and that anyone who expresses contrary suspicion is not merely mistaken but stupid, a charlatan, and a scam artist.

So it is again with Moriarty’s commentary published today at The Gold Report, “The Wolves Get the Golden Fleece as the Sheep Get Shorn One More Time”:

http://www.theaureport.com/pub/na/the-wolves-get-the-golden-fleece-as-th…

“The gold and silver markets,” Moriarty writes, “are filled with wolves that want nothing more than to get your money in exchange for feeding your fantasies. At every market low they are whining about how the bullion banks are manipulating the gold price and keeping it suppressed. At every high they are suggesting a Comex default is about to happen and prices are going to skyrocket. Or the market is about to have a ‘commercial signal failure.’ Of course they just made it up.

“Comex can’t default; there are provisions in every commodity market for cash settlement.”

Yet legal as it may be, “cash settlement” is exactly what many people mean by a default — the failure of a counterparty to deliver what was promised and expected. Moriarty knows very well that this is how his adversaries define default and indeed how the readers of his adversaries understand it.

If there were no provisions for cash settlement, Moriarty adds, “anyone with pockets deep enough could force every commodity market into failure.”

Indeed, and anyone with pockets deep enough can control any commodity futures market. But Moriarty has not the slightest curiosity about the surreptitious intervention by governments and central banks — which have the deepest pockets — in the commodity futures markets, intervention documented by filings with the U.S. Commodity Futures Trading Commission and the Securities and Exchange Commission:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

Moriarty continues: “We hear about how the shorts are into ‘naked short selling’ one more time even though there is no such thing.”

Yet even the lowliest trader working out of his parents’ basement can open a commodity futures trading account and, having posted a certain amount of earnest money, sell a contract for a commodity he does and may never own.

“Some of these fools,” Moriarty writes, “want to convince their readers that the central banks are behind a ‘gold takedown,’ but if you go to Google and put in ‘central banks buying gold’ you can find dozens of articles showing that, contrary to the con men, actually the central banks are buying gold.”

Yes, a few central banks outside North America and Europe lately have reported buying gold. Most central banks lately havenot reported buying gold, even as the Bank for International Settlements, the central bank of the central banks, recently reported reviving its gold swap operations and the director of market operations for the Banque de France, another central bank that has not reported adding to its gold reserves, told the London Bullion Market Association meeting in Rome three years ago that his bank is secretly trading gold for itself and other central banks “nearly on a daily basis”:

http://www.gata.org/node/16704

http://www.gata.org/node/13373

That is, there is a lot more activity by central banks in the gold market than the occasional purchase announcements cited by Moriarty.

Moriarty goes on: “Yet another writer on one of those single-string banjo-playing web sites said he doubted the central banks had half the gold they claim, but through Google we now know that not only have the central banks been buying gold, they have been buying gold stocks with both hands.”

But even the International Monetary Fund has admitted that central banks have done a lot of gold “leasing,” which means that certain gold reserves are, to put it politely, impaired, and that doubts about those reserves are well-founded:

http://www.gata.org/node/12016

As for central banks “buying gold stocks with both hands,” the most we can find on this point is Zero Hedge’s report a month ago that two central banks, Norway’s and Switzerland’s, lately have bought gold stocks:

http://www.zerohedge.com/news/2016-09-08/switzerland-and-norway-begin-ma…

Maybe other central banks have bought gold stocks too, but if such purchases have been reported, GATA has missed them and maybe Google has missed them too. At least GATA is a little less credulous than Moriarty, as we concede that Google is not the final word, that Google doesn’t know everything, in part because central banks don’t tell Google everything.

Back to Moriarty: “One word the experts, the gurus, and all the other fools never use is ‘correction.’ All markets go up and down. It’s the way of the world. A market enters a bull phase but it will correct. A market enters a bear phase but it corrects. If you are reading anyone taking about naked short sales or Comex defaults or gold takedowns and you never hear the word ‘correction,’ either the writer is a fool or you are. And in the greatest bull market in history, you are going to lose all your money because at the very top they are going to be telling you to buy.”

But Moriarty is the one always telling people to buy — to buy the stocks he already has bought.

Fools and charlatans as we may be, GATA is telling people that 1) central banks have been surreptitiously manipulating the gold market for longstanding policy reasons involving the defense of their currencies and bonds, manipulating markets so much lately that it’s barely surreptitious anymore; 2) that this manipulation is destroying market economies and doing great injustice around the world; 3) that justice, if and when it comes, will be a cosmic correction made endurable only by a form of money without counterparty risk, the ultimate money, the money whose market central banking has always sought to control — gold; and 4) there is no understanding the gold market and the world financial system generally without discerning what central banks are doing with the gold market — that the gold market is not the normal market Moriarty likes to imagine.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Bill Holter discusses the walking zombie bank Deutsche bank

(courtesy Bill Holter/Greg Hunter/USAWatchdog)

Deutsche Bank Walking Dead-Bill Holter

By Greg Hunter On October 12, 2016

By Greg Hunter’s USAWatchdog.com

Financial writer Bill Holter says if you want to know how bad the global financial problems are in the world, start with Germany’s Deutsche Bank (DB). The problems keep mounting, and it’s been all downhill since June when the International Monetary Fund (IMF) deemed DB as the most systemically dangerous bank in the world. Holter warns, “Deutsche Bank is dead. It’s a walking dead institution. . . .Just the fact that there is a debate, whether or not there’s a problem, means they’re dead. Once you start talking about a financial institution and whether or not they are solvent or not, it doesn’t matter. The sharks are going to come into the water.”

There is much more wrong than just the one global mega bank in trouble. Holter goes on to point out, “The markets need to be and pretty much have been locked down. We’ve seen virtually zero volatility in the stock market, and even the credit markets have been nonvolatile for the last two or three months. The reason being when volatility picks up, then margin calls happen. When you’ve got an illiquid system, you can’t allow margin calls to occur because margin calls can’t be met.”

Holter, who has decades of financial and broker experience, circles back to DB that he estimates has a $15 billion market cap. This may seem like a lot of money, but Holter contends it is not much with trillions of dollars in derivative exposure. Holter explains, “$15 billion would not even cover a 1% move in their book. A 1% move would be something like $50 billion. So, they (DB) are so undercapitalized that any type of margin call turns them upside down. Deutsche Bank is one of the biggest links in the derivatives chain. If they break, the whole thing goes. . . . This is not a Bill Holter opinion. This is math.”

In the second Presidential debate, Donald Trump said his opponent Hillary Clinton “would be in jail” if he were President. Holter contends, “I have been saying for months now, there is a better than a coin toss chance that we do not have an election. During the debate, Trump basically said he’d have his Attorney General appoint a Special Prosecutor, and you (Clinton) are going to go to jail. The problem is it’s not just Hillary. It goes throughout all of Washington, and it includes both the Democrat and Republican Party. If it looks like Trump is going to win, and he does not get assassinated, they may cancel the election by starting a war.”

Holter closed by saying, “The conservatives are not going to be separated from the liberals. When this thing goes down, it’s going to be all the American people. If this election gets stolen, all American people are going to be targeted. We are all going to be destroyed. . . . Between now and the election is extremely, extremely dangerous.”

Join Greg Hunter as he goes One-on-One with financial expert Bill Holter of JSMineset.com.

(There is much more in the video interview.)

Video Link

http://usawatchdog.com/deutsche-bank-walking-dead-bill- holter/

-END-

A thorough analysis of what is going on in the class action suit against Deutsche bank, Bank of Nova Scotia, HSVC and Societe Generale

(courtesy Market Slant)

Market Slant: What happens next in antitrust suit against London gold fix banks

8:56p ET Tuesday, October 11, 2016

Dear Friend of GATA and Gold:

Market Slant, which last week broke the story about the advancement of the antitrust lawsuit against the banks involved with the daily London gold fix, today examines the discovery procedures ahead as the plaintiffs pry evidence out of the defendants, a process that could take a long time but also produce much incriminating evidence. Market Slant’s report is headlined “Gold Fix: ScotiaBank Ordered to Produce Internal Documents” and it’s posted here:

http://www.marketslant.com/articles/gold-fix-scotiabank-ordered-produce-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Scotia must go first and supply emails

(COURTESY MARKET SLANT/FROM THE ABOVE STORY)

UPDATE:Scotia Bank Gets Tapped for Documents

Today, we learned that Scotia Bank, one of 5 defendant banks in the case, is the first to be ordered to produce internal documents requested by the plaintiffs. These documents go back years covering emails, Instant Message records, internal memorandums, notes from risk meetings and anything the plaintiffs’ attorneys think to ask for that could help their case. Things are about to start getting interesting. Here’s why.

Why Things are Different Now

Judge Caproni’s decision was a landmark event for the plaintiffs. It is the first time that a precious metals manipulation case had made it past the “Opinion and Order” stage with a recommendation the case be litigated.

The decision is key in that the plaintiffs will be able for the first time to obtain evidence through discovery and depositions of the defendants. We cannot emphasize that enough. A barrier has been broken that cannot be put back in place. The production of discovery, depositions of witnesses, and other evidentiary processes have never been on the table before are now accessible.

The Defendants Have Risk

Using a different analogy, cans of worms are being opened now. The defendants have real risks now. Risks like: perjury, internal contradictions, contradictions across different firms, and escalation up the corporate ladder (respondeat superior). The defendants know it. And Daniel Brockett, the point man for the plaintiffs knows it.

“They have to produce all the relevant emails and chat room instant messages, however they communicated with each other”--Daniel Brockett, senior partner and litigator at Quinn Emanuel Urquhart & Sullivan LLP

So, to what ends do these requests for documents serve?

What Do the Plaintiffs Hope to Find?

Broadly speaking, we believe the plaintiffs’ attorneys hope to find 2 types of proof from the documents; proof of intent and proof of Sherman Antitrust law violations. In essence: 1) Did they mean it? and 2) Were they working together?

Proving Intent-The Plaintiffs’ attorneys will look for evidence of intent. Intent is the most difficult part to prove in any manipulation case. Intent involves knowing what the “manipulator” was thinking leading up to the action. Essentially, did the offender intend to do what he did? There are at least 3 ways of proving intent, none of which are easy.

- The defendant admits it- a product of depositions and/or discovery

- A written audit trail that shows intent exists- discovery

- An email in which a defendant describes why he did a trade- a written admission

- An internal inquiry asking for justification in the scope of the firm’s risk- usually involves a superior officer and getting the 2 parties to contradict each other in deposition

- An operational or programming person was made privy to the intent as a function of their duties.- underutilized in our opinion

These are very real risks and if the defendants don’t “get their story straight” (not pejorative), any divergence between word and deed can hurt their credibility and open the door for more aggressive tactics by the plaintiffs.

Proving Antitrust Law Violations-The plaintiffs will seek putative damages under the Sherman Anti-trust act. Specifically under Section 1 governing unlawful restraint of trade. Section 1 delineates and prohibits specific means of anti-competitive conduct. The plaintiffs seek to prove collaboration between 2 or more defendant banks. They will attempt to prove cartel-like behavior between the defendants. The burden of proof here, even with evidence is high.

As stated in Judge Caproni’s decision(emphasis ours):

“Because the Sherman Act does not prohibit [all] unreasonable restraints of trade . . . but only restraints effected by a contract, combination, or conspiracy, . . . [t]he crucial question is whether the challenged anticompetitive conduct stem[s] from independent decision or from anagreement, tacit or express.”

Sherman Anti-Trust Act, Section 1:

“Every contract, combination in the form of trust or otherwise, or conspiracy, in restraint of trade or commerce among the several States, or with foreign nations, is declared to be illegal.”

The purpose of the Sherman Act was to preserve a competitive marketplace and protect consumers from abuses. However its more recent applications involve the prevention of cartel operations or monopolies (Wikipedia). Certainly an email from an employee of Scotia Bank to one of its fellow defendants describing what it has done or intends to do would serve this purpose well. But the burden of proof is high.

Even with the uphill battle ahead for the plaintiffs, Brockett was not blowing hot air when he said,

“The ruling is a major victory for the plaintiffs because it upholds the core anti-trust claim against the five fixing banks, and the statutory commodity manipulation claim against the five fixing banks.”

What’s Next

- Requests for documents will come in for each defendant.

- Plaintiff attorneys will review the documents and drawn up their plan of attack.

- Depositions of defendant personnel will occur as plaintiffs will look for contradicting and/or corroborating statements of the documents reviewed

- New requests are made

Defendant Legal Tactics

The following are legitimate reasons for difficulty complying with a court order. They are however easily abused.

- Delay: “Those documents have been archived. It will take time to get them”

- Inability to Comply: ” ..and some of them have been destroyed as a matter of the statute for keeping records has expired”

- Redirect: “check (former employee) their personal cell phone records”

- No longer works here: “We do not employ that person anymore”

- Trade Secrets: “We cannot give you information that our competitors can use to destroy our business”

- The Peter Gabriel: ” I don’t remember, I don’t recall”

Lesser Evils Get Ranked

The Prisoner’s Dilemma grid will come into play, even if nothing was done wrong. There will be triage as well.

- Contempt over perjury

- Perjury over fraud/ intent

- Fine over jail

- Rogue employee over Ceo scandal

Why This is Far from Over

The law operates on facts, not intuition. That means inductive logic, patterns of abuse, and circumstantial evidence don’t prove intent.In manipulation cases, intent is the hardest leg to prove of the 3 legged stool concept in law. Judge Caproni said as much in her decision.

From Page 1

Whether the detailed statistical analyses contained in the Complaint reveal ground truth about the activities of the Defendant banks who participated in the Gold Fix or are on the “lies, damn lies and statistics” side of the dichotomy remains to be seen.

In context of her whole statement we take that to mean: “In my judgment you have met the burden of proof and have the right to seek the facts you need to corroborate your statistical conclusions. But statistics are not facts, they are probabilities. You will need facts after today.”

DeutscheBank Opted Out

h/t Silverdoctors

Final Word From the Players Themselves

For The Plaintiffs

“So we’ll be able to tell from the communications whether the traders were actually agreeing to manipulate the gold fix price for their own personal gain, which is what we allege.”- Daniel Bockett

They may be able to tell. Doubtful if the communications alone will offer a smoking gun, as cool as that would be. A world of grey exists here.

For The Defendants

“We are unable to comment as the matter is still before the courts,”- Rick Roth for Scotia

We bet you are unable to do a lot of things, like produce documents in a timely manner if at all.

END

Scotia bank is ordered to provide emails immediately in the gold manipulation case:

(courtesy Kitco/Market Slant)

Scotia Bank Pressed For Emails In Gold Manipulation Case

Tuesday October 11, 2016 12:07

(Kitco News) – Move over Hillary Clinton, Scotia Bank is now being pressed for internal emails in a trial looking to shed light on allegations of gold manipulation involving five major banks.

Last week, Kitco News broke the news that a New York judge said there is validity behind manipulation allegations in a class action lawsuit involving five banks accused of manipulating gold prices through the twice-daily London Fix.

Last week, Kitco News broke the news that a New York judge said there is validity behind manipulation allegations in a class action lawsuit involving five banks accused of manipulating gold prices through the twice-daily London Fix.

The London gold fix, the benchmark used by miners, jewelers and central banks to value the metal, may have been manipulated for a decade by the banks setting it, researchers said.

However, the Judge dismissed all claims against global firm UBS, leaving The Bank of Nova Scotia, Barclays, Deutsche Bank, HSBC, and Societe Generale still facing manipulation charges.

On Tuesday, the Financial Post reported that Canada’s Bank of Nova Scotia will now have to turn over internal emails and other correspondence spanning several years, this according to their source, Daniel Brockett, the New York lawyer leading the U.S. lawsuit. Kitco News confirmed the news with a source close to the matter.

“They have to produce all the relevant emails and chat room instant messages, however they communicated with each other,” Brockett said in an interview with the Financial Post. Brockett is a senior litigation partner at Quinn Emanuel Urquhart & Sullivan LLP.

By Daniela Cambone of Kitco News; dcambone@kitco.com

END

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.67175( REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS TO 6.67218 / Shanghai bourse CLOSED DOWN 6.72 POINTS OR 0.22% / HANG SANG CLOSED DOWN 142.47 POINTS OR 0.60%

2 Nikkei closed DOWN 184.76 OR 1.09% /USA: YEN RISES TO 103.72

3. Europe stocks opened ALL IN THE RED ( /USA dollar index UP to 97.76/Euro DOWN to 1.1023

3b Japan 10 year bond yield: FALLS TO -.056%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 103.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.06 and Brent:52.63

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES QUITE A BIT to +061%

3j Greek 10 year bond yield FALLS to : 8.24%

3k Gold at $1252.00/silver $17.41(8:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble DOWN 15/100 in roubles/dollar) 62.54-

3m oil into the 51 dollar handle for WTI and 52 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 103.72 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9898 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0908 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISES to +.061%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.789% early this morning. Thirty year rate at 2.519% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Pressured By Weak Earnings, Rate Hike Concerns; Pound Jumps

The big macro story is the jump in the sterling which soared as much as 200 pips after Theresa May accepted a debate on a motion from the opposition Labour Party today who are arguing for a ‘full and transparent debate on the government’s plan for leaving the EU’ and which will allow for MP’s to be able to ‘properly scrutinize’ the government’s plan prior to the start of formal negotiations. The motion will be debated in Parliament today. However, according to Bloomberg May did table an amendment that added that there shouldn’t be an attempt to block Brexit or undermine the government’s position and while there is no binding result attached the fact that there will at least be some discussion amongst Parliament is slightly easing some of those hard Brexit concerns this morning.

“The vote is a major concession that does reduce the room to maneuver for Theresa May’s government in the negotiation,” said Hans Redeker, Morgan Stanley’s chief global currency strategist in London. “That is currently read as positive for sterling.”

Meanwhile, the next potentially interesting event for the fate of sterling comes tomorrow where the High Court will deem whether or not an Act of Parliament is needed for Article 50 to be triggered. A second hearing is scheduled for October 17th. A loss for the government would then force the issue into the House of Commons and House of Lords which could lead to delays although we’d expect appeals in such an outcome. One to watch however.

Ericsson AB sank 17 percent after the Swedish network maker reported a slump in third-quarter sales and profitability, dragging a gauge of technology shares to the worst performance of the Stoxx Europe 600 Index’s 19 industry groups. BASF SE rose 0.6 percent after the world’s largest chemical maker posted a smaller-than-expected decline in quarterly profit. Fresnillo Plc slipped 2.2 percent as the precious-metals miner said silver production slowed in the third quarter from a year earlier due to personnel issues and availability of equipment.

“The market will need some reassurance that a soft start to earnings season has been nothing more than a few outliers,” said Alan Higgins, chief investment officer at Coutts & Co. in London. His firm oversees the equivalent of $18 billion. “Investors are also building in a higher probability of a Fed hike as each week goes past. These next few months will be very busy.”

The MSCI Asia Pacific Index dropped 0.6 percent. Hong Kong’s Hang Seng Index retreated 0.6 percent in a third day of losses as Bank of China Ltd. and Bank of Communications Co. sank more than 2.8 percent. In Japan, the Topix lost 1 percent.

Aside from Europe, the MSCI Asia Pacific Index retreated to a three-week low. Thailand’s stock market and currency extended this week’s losses after the royal palace said Sunday that King Bhumibol Adulyadej’s condition was unstable.

Emerging markets are once again feeling the heat on concerns a Fed hike may lead to a return in capital outflows from EM, leading to preemptive. The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, was little changed after rising for the past two days and closing at the strongest level since July 25 on Tuesday. Investors will scrutinize minutes from the Fed’s latest decision due Wednesday, with odds of a U.S. rate increase by year-end climbing to 68 percent amid speculation the recent surge in oil prices will fuel inflation, based on futures data compiled by Bloomberg.

Responding to the stronger dollar, China’s central bank weakened the yuan’s reference rate for a sixth day, pushing it to the lowest in 6 years with a USDCNY fixing of 6.7258, down 5.5% Y/Y, the longest run of cuts in nine months, amid speculation policy makers will allow further declines as the dollar rises.

S&P 500 Index futures were little changed, after falling Tuesday to an almost four-week low as an early batch of disappointing corporate results including those from Alcoa Inc. damped optimism over a rebound in earnings.

Oil climbed as OPEC received further commitments from Russia that the world’s largest energy exporter is willing to participate in a coordinated effort to curb production.

In rates, the big movers were Sterling corporate borrowing costs which have risen back to early August levels, reversing a decline sparked by an interest-rate cut and the Bank of England’s announcement of plans to buy company bonds to help ease the economic impact of Brexit. The average yield has climbed to 2.48 percent, based on a Bloomberg Barclays index. Australian government debt extended declines, with 10-year yields rising for a seventh straight day, adding five basis points to 2.30%. Spanish bonds led declines in the euro region’s fixed-income market on speculation that caretaker Prime Minister Mariano Rajoy may face a confidence vote this month. The vote could come on Oct. 28, El Mundo reported on Wednesday, using its own calculations pegged to the King of Spain’s talks with parties. The 10-year yield rose four basis points to 1.06 percent.

10Y US Treasuries have lost 5.8% in the three months through Monday, the most among 144 government bond indexes tracked by Bloomberg and the European Federation of Financial Analysts Societies. The nation will auction $24 billion of three-year notes and $20 billion of 10-year securities on Wednesday.

Market Snapshot

- S&P 500 futures down 0.1% to 2131

- Stoxx 600 up less than 0.1% to 340

- FTSE 100 down 0.4% to 7040

- DAX down 0.1% to 10565

- German 10Yr yield up 1bp to 0.04%

- Italian 10Yr yield up 2bps to 1.4%

- Spanish 10Yr yield up 4bps to 1.06%

- S&P GSCI Index up 0.4% to 377.2

- MSCI Asia Pacific down 0.6% to 139

- MSCI Asia Pacific down 0.6% to 139

- Nikkei 225 down 1.1% to 16840

- Hang Seng down 0.6% to 23407

- Shanghai Composite down 0.2% to 3058

- S&P/ASX 200 down less than 0.1% to 5475

- US 10-yr yield up less than 1bp to 1.77%

- Dollar Index up 0.05% to 97.74

- WTI Crude futures up 0.5% to $51.03

- Brent Futures up 0.7% to $52.79

- Gold spot up 0.3% to $1,256

- Silver spot up 0.4% to $17.53

Top Global Headlines

- Trump’s attacks on GOP leaders ignite civil war inside party: GOP nominee escalates feud with party’s most visible figures; poll shows Trump trailing Clinton by nine points.

- Pound advances as Brexit angst eases with May accepting that Parliament should be allowed to vote on Brexit plan; crude oil Holds Above $50; sterling snaps drop with Parliament to discuss Brexit plan; MSCI’s Asian equity index falls to lowest level in three weeks.

- Sprint seeks to raise $3.5b from spectrum, WSJ says: U.S. carrier to mortgage about 10% of airwaves; CFO said in March up to $5b could be raised on spectrum.

- Deutsche Bank said to increase size of private bond issue; raised $1.5b following a $3b deal; yield on notes 290 bpss more than benchmark.

- Samsung cuts profit outlook by $2.3b after killing Note 7 phone.

- Thailand stocks, currency slump amid concern over king’s health; SET Index falls almost 9% this week in biggest drop in world: Baht weakens after foreigners sell sovereign bonds.

- Fed minutes could show depth of hawkish rebel camp in FOMC: Fed watchers looking to tally hike support among non-voters; critical debate likely to center on labor market, inflation.

- OPEC hails Putin production pledge as internal disputes persist; Russian companies fall into line as Putin backs supply accord: Iraq, Venezuela dispute output estimates underpinning deal.

- ‘Flash-Crash’ Trader Faces End of Road in U.K. Extradition Fight: Navinder Sarao will ask judge to reconsider extradition appeal; Sarao charged in U.S. with making millions spoofing markets.

Looking at regional markets, Asia stocks traded lower across the board and tracked the losses seen in the US where healthcare names underperformed as Hillary Clinton widened her lead in the US Presidential race, while a pullback in oil, further increases December Fed hike expectations and Alcoa missing at the start of earning season also dampened sentiment. This pressured Asian markets from the open with ASX 200 (-0.2%) dragged by commodity names, while Nikkei 225 (-0.9%) was weighed by a firmer JPY. Shanghai Comp. (-0.3%) and Hang Seng (-1.0%) were subdued after the PBoC kept its liquidity injections light, while the property sector continued to lag following recent measures to cool the rampant market. BoJ Governor Kuroda said he will ease further if it is deemed to be beneficial and would lower rates further into negative territory if merits outweigh costs.

Top Asian News

- Australia Sells $5.8 Billion of 30-Year Bonds in Record Deal New 2047 notes priced to yield 3.27%.

- UBS Said to Hire Top Asia Private Bankers From Deutsche Bank: Latest defections amid growing competition for Asian wealth.

- Saka Shuts Credit Hedge Fund as Low Rates Offer Muted Gains: Singapore-based asset manager returns money to investors.

- Samsung Cuts 3Q Op Profit to 5.2t Won From 7.8t Won on Note 7: Co. also revises 3Q sales to 47t won from 49t won.

- Kirin Said to Buy Stake in Brooklyn Brewery in Craft Beer Chase: Japan brewers are seeking ways to grow as consumption falls.

- Analysts’ Perfect Stock Plunges as China Property Risks Grow: China Resources Land is falling fastest on Hang Seng Index

European markets remain subdued this morning (DAX -0.16%) with IT the major laggard across the continent, as Ericsson issued a profit warning with the CEO stating the result is significantly lower than we expected, with a particularly weak end of the quarter. Elsewhere, healthcare (-0.37%) names also traded softer as Presidential candidate Clinton edges ahead in the polls (previously criticised excessive pharma Co. profits). In Fixed income markets, Bunds are largely flat only up 8 ticks with fixed income markets awaiting FOMC minutes.

Top European News

- Ericsson Profit Plunges as Equipment Maker’s Woes Intensify

- Germany, Utilities Said to Agree Nuclear Deal From Feb. 2017

- Brexit Proves Bane for This U.K. Stock Index as Peers Rally

- VTB to Continue Cutting Back London Operations: CEO Kostin

- Ericsson Slumps to Lowest Since 2008 on Earnings Miss: Chart

- Costly Rule Changes to Spark More M&A by Europe’s Asset Managers

- Goldman Sees ‘Sharpening of Knives’ in South Africa’s ANC

In FX, the pound climbed 1.1 percent to $1.2250 in early trading London, rebounding from near a three-decade low. Parliament will debate on Wednesday a motion from the opposition Labour Party calling for a “full and transparent debate on the government’s plan for leaving the EU” and for lawmakers to be able to “properly scrutinize that plan” before May begins formal talks. In response, May tabled an amendment that effectively accepted the motion, adding that there shouldn’t be an attempt to block Brexit or “undermine the negotiating position of the government.” The Bloomberg Dollar Spot Index was little changed after rising for the past two days and closing at the strongest level since July 25 on Tuesday. Investors will scrutinize minutes from the Fed’s latest decision due Wednesday, with odds of a U.S. rate increase by year-end climbing to 68 percent amid speculation the recent surge in oil prices will fuel inflation, based on futures data compiled by Bloomberg. China’s central bank weakened the yuan’s reference rate for a sixth day, the longest run of cuts in nine months, amid speculation policy makers will allow further declines as the dollar rises. The currency was little changed at a six-year low. South Africa’s rand swung between gains and losses after tumbling 3.9 percent on Tuesday, the most in more than three months, after Finance Minister Pravin Gordhan was summoned to appear in court.

In commodities, West Texas Intermediate crude added 0.3 percent to $50.96 a barrel after Saudi Arabia’s oil minister left Istanbul with a pledge that Russia would join efforts to limit oil production. That leaves internal OPEC disagreements over how to share the burden of the cuts as the last obstacle to a global deal. Russia’s two largest oil producers said Tuesday they would comply with any government instructions to curb oil output, following President Vladimir Putin’s backing on Monday for a supply deal with the Organization of Petroleum Exporting Countries. Gold for immediate delivery gained 0.2 percent to $1,255.64 an ounce following a 0.5 percent drop last session, its ninth decline in 12 days. Zinc rallied 0.3 percent after sliding the most in 10 months, while copper added 0.2 percent on the London Metal Exchange.

Looking at the day ahead, the lone data is the JOLTS job openings report. Remember that this data is closely followed by Yellen however given that the data corresponds to August and we have since had the September employment report, the numbers will probably look a bit stale. The focus today will of course be on those September FOMC meeting minutes which are out at 2pm ET. Away from the data the Fed’s Dudley (1pm BST) and George (2.40pm BST) are both scheduled to speak today along with the ECB’s Mersch and Coeure. The other event worth watching today, with obvious implications for Sterling and FX markets, is the UK Parliament debate about the government’s plan for leaving the EU.

* * *

Bulletin Headline Summary from Ransquawk and Bloomberg

- European bourses remain subdued this morning with IT the major laggard across the continent

- Wednesday’s market was expected to be a day of consolidation, but from early Asia, we have again seen GBP taking the headlines

- Looking ahead, highlights include FOMC Meeting Minutes, US JOLTs, WASDE Crop Report, EU Industrial Production and comments from BoE’s Cunliffe, Fed’s George and Dudley

- The pound rallied after Prime Minister Theresa May accepted that Parliament should be allowed to vote on her Brexit plan

- Minutes of the Federal Reserve’s September policy meeting released today could guide expectations of a 2016 rate hike

- An election victory for Hillary Clinton may boost the peso enough for Mexico to stave off a credit-rating downgrade

- A potential downgrade of South Africa’s debt rating to junk isn’t fully priced in by markets, according to Goldman Sachs

- Deutsche Bank boosted the size of its private dollar bond sale by $1.5b less than a week after raising $3b; Germany wants a swift settlement between Deutsche Bank and the U.S. government over an MBS fine

- Kirin will acquire about a 25% stake in a Brooklyn craft beer company to tap the specialty lager trend

- Ericsson blindsided investors with a surprise profit warning, with no turnaround in sight

- In Europe’s primary market, financials lead the way today with three issuers including a tier 3 sale from CNP Assurances

US Event Calendar

- 7am: MBA Mortgage Applications, Oct. 7 (prior 2.9%)

- 8am: Fed’s Dudley speaks in Albany, New York

- 9:40am: Fed’s George speaks in Chicago

- 10am: JOLTS Job Openings, Aug., est. 5.800m (prior 5.871m)

- 2pm: FOMC Minutes, Sept. 20-21

- 4:30pm: API weekly oil inventories

DB’s Jim Reid concludes the overnight wrap

It feels that markets have been experiencing the Great British Sell-Off of late and it was another challenging session for the pound yesterday but we’ve seen a strong bounce back in Asia as PM May agreed late last night to allow Parliament to debate the type of Brexit we’ll see today. More on this below but across the wider global market, the last 24 hours have seen a combination of forces weaken sentiment. Fears over central banks reaching the end of the road in the current regime, slowly increased expectations that the Fed’s hurdle rate for hiking is getting lower, Oil’s recent strong rally, a plunging pound and hard Brexit talk are all factors that have destabilised bond markets over recent weeks and yesterday these factors combined with a weak start to the US earnings season to prompt a sharp turnaround in equities. The S&P 500 (-1.24%) fell by the most in a month to a near 4-week low and dipped below the 100 day moving average.

Given that a lot of the concerns focus on central banks at the moment tonight is a timely look at how close the FOMC came to raising rates last month with the minutes being released. Remember there were three dissenters so it’s likely that these will be one of the more hawkish set of no rate change minutes. While we’ve always thought the Fed would get practically nowhere in terms of rate hikes in this cycle it’s becoming clearer that they are now prepared to hike on much shakier economic foundations than at virtually any point in their history.

Aside from those minutes tonight the other big focus today will almost certainly be on all things Brexit and Sterling related. Before this morning’s bounce back, yesterday the Pound suffered a late-day sell off to close down -1.93% versus the Dollar at $1.2123. That is actually the worst one-day fall for Sterling since July 5th although it did actually touch $1.2090 intraday which compares to the flash crash low on Friday (assuming you use the reported Bloomberg level) of $1.1841. A generally strong day for the US Dollar certainly didn’t help matters however comments from BoE MPC member Michael Saunders didn’t exactly exude confidence. He said that ‘given the scale and persistence of the UK’s current account deficit, I would not be surprised if sterling falls further’ and that while the largest part of the drop ‘is an adjustment to the prospect of an EU exit, we don’t know yet the exact shape of Britain’s post-exit arrangements’.

It’s a very different story this morning however with the Pound bouncing back +1.60% as we type to $1.2316. The renewed optimism appears to reflect the news late last night that PM Theresa May has accepted a debate on a motion from the opposition Labour Party today who are arguing for a ‘full and transparent debate on the government’s plan for leaving the EU’ and which will allow for MP’s to be able to ‘properly scrutinize’ the government’s plan prior to the start of formal negotiations. The motion will be debated in Parliament today. According to Bloomberg May did table an amendment that added that there shouldn’t be an attempt to block Brexit or undermine the government’s position and while there is no binding result attached the fact that there will at least be some discussion amongst Parliament is slightly easing some of those hard Brexit concerns this morning.

Meanwhile, the next potentially interesting event comes tomorrow where the High Court will deem whether or not an Act of Parliament is needed for Article 50 to be triggered. A second hearing is scheduled for October 17th. A loss for the government would then force the issue into the House of Commons and House of Lords which could lead to delays although we’d expect appeals in such an outcome. One to watch however.

Despite weaker Sterling yesterday, Gilts actually had a better day with the 10y yield falling 4.4bps to 0.976%. That follows a run of five consecutive sessions of yields rising steadily higher. Other European sovereign bond yields also edged a bit lower although 10y Treasury yields were up nearly 5bps to 1.765% and the highest since June 3rd. Despite WTI Oil slipping -1.09% we’d put the rise in Treasury yields yesterday down to a bit of catch up from that big Oil rally on Monday.

As we noted earlier, it was a tough start to earnings season yesterday in the US. Alcoa missed at both the earnings and revenue lines and painted a slightly bleaker than expected outlook on the call. Shares tumbled 11% however that wasn’t the only damage from earnings season yesterday. Fastenal also missed versus earnings expectations which saw shares fall more than 5%. The big mover yesterday however was the biotech company Illumina whose shares fell nearly 25% after cutting revenue guidance. That weighed on the wider health care sector (-2.51%) in the S&P 500 while the Nasdaq Biotech index (-3.77%) had its worst day since June 24th.

While US equity index futures are a touch firmer this morning, bourses in Asia have generally followed the lead from the close on Wall Street last night. The Nikkei (-0.58%), Hang Seng (-0.80%), Shanghai Comp (-0.28%), Kospi (-0.12%) and ASX (-0.36%) are all currently in the red, while it’s been a similarly weak start for most credit indices. Sovereign bond markets are more mixed. Also of note were comments from BoJ board member Harada. He said this morning that the ‘bank should take additional easing measures without hesitation’ in the event that a situation arises where the inflation target becomes difficult to achieve.

Moving on. There was a little bit of economic data to highlight yesterday. In the US the NFIB small business optimism reading declined a fairly modest 0.3pts to 94.1 (vs. 95.0 expected) in September. While that reading has declined for two consecutive months, perhaps as a reflection of some jitters ahead of the US election, the current level is in line with the 2016 average. Meanwhile the labour market conditions index weakened -2.2pts in September (vs. +1.5 expected). It’s the second straight month that the index has fallen. Prior to this the lone release in Europe came in Germany where the ZEW survey for this month revealed an increase in both the current situation index (+4.4pts to 59.5; 55.5 expected) and expectations index (+5.7pts to 6.2; 4.0 expected).

Before we look at today’s calendar, there was also some more chatter out of the Fed with Minneapolis Fed President Kashkari speaking. A voter next year, he came across as relatively dovish, saying that ‘my view is let’s let the economy keep creating jobs, bringing workers off the sidelines so long as it’s not creating inflation’. He also added that the Fed continues to undershoot its inflation target and so ‘I don’t see the urgency’.

Looking at the day ahead, this morning shortly after this hits your emails we’ll get the final revisions to CPI in France during September. Following that we then get the August industrial production print for the Euro area which the market is expecting to print at +1.5% mom. This afternoon in the US the lone data is the JOLTS job openings report. Remember that this data is closely followed by Yellen however given that the data corresponds to August and we have since had the September employment report, the numbers will probably look a bit stale. The focus today will of course be on those September FOMC meeting minutes which are out at 7pm BST. Away from the data the Fed’s Dudley (1pm BST) and George (2.40pm BST) are both scheduled to speak today along with the ECB’s Mersch and Coeure. The other event worth watching today, with obvious implications for Sterling and FX markets, is the UK Parliament debate about the government’s plan for leaving the EU.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 6.72 POINTS OR 0.22%/ /Hang Sang closed DOWN 142,47 POINTS OR 0.60%. The Nikkei closed DOWN 184.76 POINTS OR 1.09% Australia’s all ordinaires CLOSED DOWN 0.09% /Chinese yuan (ONSHORE) closed UP at 6.67157/Oil ROSE to 51.06 dollars per barrel for WTI and 52.63 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.6721 yuan to the dollar vs 6.67197 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

3a)THAILAND:

Thai stocks plummet along with their currency on concerns of the King’s health and the Fed rate hike. Remember it was Thailand that caused the Asian contagion in 1997:

(courtesy zero hedge)

Thai Stocks, Currency Plunge On Concerns Over King’s Health, Fed Hike

Ever since the 1997 Asian Financial Crisis, investors have kept a close eye on financial developments in Thailand as canary in the Asian financial conditions coalmine, and overnight there was little to look forward to after Thai stocks crashed the most in over a year, plunging as much as 6.9% before settling 4.1%, lower while the baht currency tumbled 1.1%, its steepest plunge in three years. The Thai stock market was the worst performing in Asia, with the sharp selloff attributed to concerns about the health of the king and “sudden” fears about the prospect of a December rate hike.

Thai stocks approached a correction, after sliding 8.8% in the week, the most among about 100 benchmark share indexes tracked by Bloomberg. Default risk also spiked with Thai CDS rising 8%, and more than 12 per cent since the start of the week. The Thai currency traded at 35.768 per dollar, headed for an eighth day of losses in the longest stretch since July 2015. It sank as much as 1.5 percent to 35.902, the lowest since Jan. 26, and is headed for its steepest weekly drop since 2013. The 10-year sovereign bond yield rose five basis points to 2.35 percent, the highest since January.

“Concern about the U.S. interest-rate increase and dollar strength will continue to damp sentiment and foreign fund flows,” said Koraphat Vorachet, an investment strategist at Capital Nomura Securities Pcl in Bangkok.

In addition to fears about tightening monetary conditions, and an imminent capital outflow should the Fed hike in a rerun of last December, Thailand’s stocks and currency have fallen every day after the royal palace said Sunday that the condition of King Bhumibol Adulyadej, the world’s longest reigning monarch, was unstable, Bloomberg reported. In a statement, the royal household bureau said the king’s blood pressure had dropped as he was being prepared for a procedure to treat kidney failure.

“The 88-year-old monarch’s health is closely watched as he is revered by many for what they say has been his unifying presence during a seven-decade reign. Foreign funds pulled $426 million from Thai sovereign bonds in the first two days of the week, exchange data show.”

The baht’s slide was “mostly related to the king’s health,” said Sean Yokota, head of Asia strategy at Skandinaviska Enskilda Banken AB in Singapore. “It’s about the political stability that the king has provided and his being a reconciliatory buffer between the major parties.”

Quoted by Bloomberg, Kesara Manchusree, the Stock Exchange of Thailand’s president, said on Tuesday that Thailand’s stock market faces a “challenging time” with a jump in volatility amid lingering concern over domestic and overseas factors, The fundamentals of the Thai economy and listed companies’ earnings remain strong, she said.

As a reminder, Thailand has been ruled by a military junta since 2014, and last month voters backed a new constitution to give the military more power, despite opposition from both main political parties.

END

b) REPORT ON JAPAN

none today

end

c) Report on CHINA

none today

4 EUROPEAN AFFAIRS

GERMANY/DEUTSCHE BANK

Deutsche bank sells another 1.5 billion dollars worth of bonds at a yield of 4.25%: basically at junk. This is done prior to any announcement of a settlement. In January these guys can be bailed in if trouble occurs:

(courtesy zero hedge)

Deutsche Bank Sells Another $1.5 Billion In Debt At Junk Bond Terms

We were surprised when, just after the close on Friday, Deutsche Bank announced it would issue $3 billion in five year paper carrying a nosebleeding coupon of 4.25%, and a spread of 300 bps over Treasuries. By issuing debt at such a high yield – indicatively 300 basis points is close to the average for highly-rated junk debt in dollars and more than twice the 143 basis points Deutsche Bank paid for similar notes in August 2015 – DB management confirmed it had liquidity concerns (the issue did nothing to help the bank’s ailing capitalization).

As we said on Friday, “some have wondered why the need to sell new paper at such a wide concession: after all as we reported before, DB has no current liquidity constraints courtesy of substantial ECB generosity, which backstop DB’s existing liquidity reserves of just over €200 billion” leading to the question: “does DB know something investors don’t?.”

While the question remains unanswered, a similar question emerged last night when taking advantage of the still open issuance window, Deutsche Bank raised another US$1.5 billion in bonds, tapping last Friday’s $3 billion 5-year issue. The self-led tap of its 4.25% October 2021s priced at similar terms, at 100.263 and a spread of 290bp over Treasuries for a yield of 4.191%, and a coupon of 4.25%. According to Bloomberg, the German lender targeted mostly the same investors who bought last week’s $3 billion private deal. The deal was priced at a premium of 290 basis points, once again suggesting that at least from the perspective of investors, DB is effectively a junk rated credit.

The two-day issuance was Deutsche Bank’s first since the U.S. Justice Department demanded $14 billion to settle RMBS misselling claims, a leaked report of which in mid-September sent the stock tumbling.

“The private debt sale shows they can still access the market for sizable term funding,” said Ben Sy of JPM in Hong KOng. Even so, “it has to pay a significant premium and that may shake confidence among investors,” he said. Which is good because as we showed yesterday, DB’s funding costs in short-term markets continue to rise even as most other European banks are paying less.

As Bloomberg notes, “the bonds will become more vulnerable to losses from Jan. 1, when a German law takes effect that subordinates existing notes to deposits, derivatives and structured notes. Senior bonds could be bailed in if post-tax losses exceed 20 billion euros or if some lower-ranking bonds don’t provide a cushion because they’re not governed by EU law, Hank Calenti, an analyst at Wells Fargo & Co. in London, wrote in a note to clients.”

“Short term, it’s a good thing for Deutsche that they’re raising money even though they have to pay a higher spread than they want to,” said Jonathan Rochford, a Sydney-based portfolio manager at Narrow Road Capital, which manages A$35 million ($26.5 million). “It gives people confidence that they’re getting funding. But the long-term issues haven’t changed. They’re still undercapitalized.”

Precisely, and in the meantime, the bank’s leverage keeps growing especially if the use of funds from the bond issuance will promptly exit through the front door to pay for either more litigation charges or other non-business purposes, while the underlying business model continues to deteriorate.

END

ENGLAND

The now have a British bond bloodbath (occurring right after a huge downfall in the currency:

(courtesy zero hedge)

British Bond Bloodbath Despite ‘Softening’ Brexit Sterling Bounce

It appears Theresa May’s mild concession to the opposition to debate Brexit has done nothing to stop the selling in bonds as Gilt yields spike to Brexit levels despite a bounce in the pound.

- *DAVIS: NO ONE WILL BE ABLE TO VETO BREXIT REFERENDUM RESULT

Speaking in Parliament on Wednesday, May promised lawmakers would get to debate her negotiating strategy for Brexit. When asked explicitly during her weekly questions session whether there would be a vote, May refused to rule it in or out. “The idea that parliament wasn’t going to be able to discuss, debate, question issues around” Brexit was “frankly completely wrong,” May said, over interruptions. “Parliament’s going to have every opportunity to debate this issue.”

It seems the ‘debate’ has done nothing to stop the carnage…

With 10Y Gilt yields spiking to pre-Brexit “MP is dead” highs…

Even as 5Y5Y inflation breakevens limp back modestly off spike highs.

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

NONE TODAY

6. GLOBAL ISSUES

ERICSSON/SWEDEN

A good indicator of troubles throughout the globe; huge telecom giant Ericsson plunges 17% after a profit warning:

(courtesy zero hedge)

“We Didn’t Know Things Were This Bad” – Ericsson Shares Plunge 17% After Shocking Profit Warning

Our condolences to anyone long Swedish telecom giant Ericsson, who will observe the following chart first thing upon waking up today.

The reason for Ericsson’s 17% crash, is that the Swedish network maker reported a surprising slump in third-quarter sales and profitability, warning investors that its business was deteriorating faster than expected, with no turnaround in sight. Unexpectedly, the company said sales in the third quarter had dropped by 14% while its operating profit was all but wiped out, falling from SKr5.1bn a year ago to SKr300m. The sales drop was the biggest in 13 years, going back all the way to 2013.

Cited by Bloomberg, Mathias Lundberg, an analyst at Swedbank said that “we knew that the business climate was weak, and that would show in the numbers, but we didn’t know that things were this bad,” Lundberg said by phone. “That was a surprise both to us and the market.”

Jan Frykhammar, the acting chief executive, said: “Our result is significantly lower than we expected, with a particularly weak end of the quarter, and deviates from what we previously have communicated regarding market development.”

Hardly encouraging for mobile companies (elsewhere Samsung had a just as ugly morning after the Korean handset maker slashed its quarterly profit forecast by a third), according to the FT, Ericsson blamed a “further deterioration in demand for mobile broadband and said the current trends were likely to continue in the short term.” Since selling its mobile phone business in 2012, the group has focused on selling network equipment to telecoms operators as well as a less-than-successful push into media and services. Not helping matters is that troubled Ericsson has been without a permanent chief executive, having ousted Hans Vestberg in July.

Discontent among its two main shareholders, holding companies Industrivarden, and Investor, the Wallenberg family investment vehicle, has led to pressure to cut costs with a fifth of workers in Sweden axed last week. But rumors are swirling around Stockholm that one or other of the two main owners could sell out as Ericsson’s performance worsens.

Acting CEO Frykhammar hinted at more restructuring to come as the group adapts to fierce competition from rivals such as Finland’s Nokia and China’s Huawei. “We will continue to drive the ongoing cost program and implement further reductions in cost of sales to meet the lower sales volumes.”

As the FT adds, Ericsson’s sales decline was worst in its main networks business, which saw revenues drop 19 per cent. Ericsson blamed markets such as Brazil, Russia and the Middle East for much of the decline as well as lower sales in Europe. Ericsson’s gross margin fell to 28 per cent from 34 per cent a year ago and 32 per cent in the previous quarter.This was the lowest margin since the dot com bust.

Even excluding restructuring charges of SKr1.3bn taken in the quarter, operating profit fell by nearly three-quarters.

Cited by FT, Gareth Jenkins, analyst at UBS, said the warning implied a cut of 15-25 per cent in expected full-year operating profits. “It will be the job of the new CEO to turn Ericsson around,” he added.

“Since we now are in a situation where volumes are dropping, we have to adjust the cost of sales resources both external and internal,” Frykhammar said. “That’s clear given the volume reductions.”

END

OIL ISSUES

Crude tumbles after OPEC raises doubts over the timing of cuts:

(courtesy zero hedge)

Crude Tumbles After OPEC Raises Doubts Over Cut Timing

Just when everyone thought “oil” was “fixed” the meeting ends and OPEC secretary-general drops this little tape-bomb – BARKINDO: NOT DECIDED WHETHER OPEC WOULD CUT BEFORE NON-OPEC…

We haven’t decided yet whether OPEC and non-OPEC would make cuts at the same time, or OPEC would move first, Secretary-General Mohammed Barkindo tells reporters in Istanbul.

And WTI slumps…

Even More OPEC Confusion: Unclear Who Cuts First, If Anyone, As Production Hits New Record High

Following yesterday’s latest IEA report which showed that OPEC production had hit an all time high, this morning OPEC released its own estimate of production by OPEC member nations for September and, not surprisingly, the latest report showed that in the month OPEC was supposed to be set on “cutting” production, the 14-nation group produced a whopping 33.39 million b/d crude in Sept., up 220k b/d from August.

While Saudi Arabia showed the largest decline of 88K to 19.49mmbpd, other members promptly ate up the Saudi market share which as recently as last month hit a record. To wit

- Iraq +105k, 4.46m

- Nigeria +95k, 1.52m

- Libya +93k, 363k (an increase of 34%)

Even more notable is what we touched upon last month after the Algiers deal was announced, namely that Venezuela and Iraq oil output may be underestimated by as much as 565k b/d for Sept., according to secondary sources cited in OPEC’s monthly oil market report.

- Venezuela reported crude output of 2.33m b/d in Sept. to OPEC, 245k more than secondary source estimates

- Iraq reports 4.78m b/d in Sept., 320k above secondary source estimates

- Secondary source estimates also lower for 5 other OPEC members; higher for members Angola, Nigeria, Qatar.

Recall that OPEC “agreed” to cut total output to 32.5m-33m b/d as part of agreement to steady oil markets, however both Iraq, Venezuela have disputed secondary sources. This means that if OPEC agrees with the country’s own source data, the cartel will need to cut as much as 565k more, an output cut which would have to come out of Saudi production.

This is how Bloomberg put it:

The scale of the internal differences OPEC must resolve before securing a deal to cut supply was revealed Wednesday as the group’s latest output estimates showed a half-million-barrel difference of opinion over how much two key members are pumping.

Venezuela and Iraq’s own figures on how much crude they produced in September were 565,000 barrels a day higher than estimates compiled by the Organization of Petroleum Exporting Countries from so-called secondary sources. The two nations are disputing the data, which could determine the production target for each country when caps on members’ output are decided next month.

Venezuela told OPEC it pumped 2.33 million barrels of crude a day in September, 245,000 more than estimated by secondary sources, which include news organizations such as Platts and Argus Media as well as the International Energy Agency. Iraq said it pumped 4.78 million barrels a day, 320,000 more than the secondary-source view. The total discrepancy for both countries equals the daily production of Ecuador.

Of OPEC’s 14 member countries, Iraq and Venezuela are the only two that have publicly criticized the sources’ figures. Yet there are five others whose own estimates are higher than those provided by secondary sources. Three nations — Angola, Nigeria and Qatar — provided estimates that are lower.

But what was most amusing in light of the above, is that according to the OPEC secretary general Mohammed Barkindo tells reporters in Istanbul. “OPEC has still hasn’t decided yet whether OPEC and non-OPEC would make cuts at the same time, or OPEC would move first.”

So the OPEC production cut will take place… but non-OPEC – i.e., Russia and US shale – cuts first?

And just to top the soaring confusion, Putin said that Russia would only join OPEC if the organization agreed on a freeze, something which considering the scramble by all non-Saudi nations to pick up Saudi market share, is very unlikely to happen. Oh, and Russia refuses to cut production.

Finally, as a reminder, this is what will happen in November according to Goldman if there is no deal:

The post-Algiers rally in oil prices has continued, fueled by comments by Russia and Saudi Arabia today (October 10) that point to a greater probability of reaching a deal to cut production. Saudi Arabia likely holds the reigns to such an agreement, with signs of elevated funding stress potentially driving Saudi to commit on November 30. As usual, risks of a disagreement are not negligible with Iraq currently the most vocal opponent, aiming to grow production next year and disputing usual measures of its production as too low.Failure to reach such a deal would push prices sharply lower to $43/bbl in our view as we forecast that the global oil market is in surplus in 4Q16.

Good luck OPEC.

end

Then oil tumbles after the biggest crude inventory build in 6 monthgs

(courtesy zero hedge)

Oil Tumbles After Biggest Crude Inventory Build In 6 Months