Gold $1267.90 UP $7.10

Silver 17.62 UP 3 cents

In the access market 5:15 pm

Gold: 1269.50

Silver: 17.69

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix OCT 18 (10:15 pm est last night): $ 1267.16

NY ACCESS PRICE: $1263.75 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1265.60

NY ACCESS PRICE: 1261.75 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!! 4 dollars

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: OCT 19: 5:30 am est: $1269.75 (NY: same time: $1266.75: 5:30AM)

London Second fix OCT 19: 10 am est: $1269.80 (NY same time: $1269.80 , 10 AM)

Shanghai premium in silver over NY: 87 cents.

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

11 NOTICES FILED FOR 1100 OZ

For silver:

for the Oct contract month: 0 notices for nil oz.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 2317 contracts UP to 189,229. The open interest ROSE as the silver price was UP 16 cents in yesterday’s trading .In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .946 BILLION TO BE EXACT or 135% of annual global silver production (ex Russia &ex China).

In silver for October we had 0 notices served upon for NIL oz

In gold, the total comex gold ROSE by 4,124 contracts with the RISE in price of gold( $6.40 YESTERDAY) . The total gold OI stands at 497,061 contracts.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

TODAY WE HAD NO CHANGES AT THE GLD:

Total gold inventory rests tonight at: 967.21 tonnes of gold

SLV

we had a good sized deposit of .855 million oz at the SLV/

THE SLV Inventory rests at: 363.140 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE by 2,317 contracts UP to 189,229 as the price of silver ROSE by 16 cents with yesterday’s trading.The gold open interest ROSE by 4124 contracts UP to 497,061 as the price of gold ROSE $6.40 IN YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

end

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 0.844 POINTS OR 0.03%/ /Hang Sang closed DOWN 89.42 POINTS OR 0.38%. The Nikkei closed UP 35.30 POINTS OR 0.21% Australia’s all ordinaires CLOSED UP 0.414% /Chinese yuan (ONSHORE) closed UP at 6.7367/Oil ROSE to 50.91 dollars per barrel for WTI and 52.33 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.7417 yuan to the dollar vs 6.7367 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

i)In just one month, China injects another 1/4 trillion dollars of debt (Total Social Financing) to jump start their economy. That is equivalent to 2.5 trillion USA dollars per year or 25% of their entire GDP. However that is not the scary part: you must also include two other very important debt items: Government debt, sovereign and local as well as the huge shadow banking sector: Peer to Peer lending. The total rate of debt expansion is twice the level of GDP

( zero hedge)

ii)Global markets hardly move as China just manages to meet GDP expectations of 6.7% Here are the other important data points for China this morning!

( zero hedge)

4 EUROPEAN AFFAIRS

i)GERMANY/ENGLAND

(Merkel is said to offer no back door concessions to England as the enter discussions on a BREXIT. The problem for Merkel is that Germany will be the net loser as their exports to England will falter badly especially in the light of the lower pound

( zero hedge)

ii)GERMANY

Problems continue with respect to refugees from Africa:

(courtesy zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia is getting ready for war: they are deploying the largest naval force since the cold war. It is heading for Syria.

( zero hedge)

6.GLOBAL ISSUES

7.OIL ISSUES

WTI rises after another huge inventory drawdown. However production increases.

(courtesy zero hedge)

8.EMERGING MARKETS

this once prosperous nation with the world’s largest oil reserves has now gone into its death spiral. Probably within one month or two it will default on its debt and hopefully their misery will end and they can start over but they need to rid themselves of their leader Maduro

( zero hedge)

9.PHYSICAL STORIES

i)Silver eagle demand (as well as gold eagle demand return to extremely high levels in October as the world economy shakes:

( SRSRocco/ Steve St Angelo)

ii)Chris Powell questions why the Wall Street Journal must question central banking!

( Chris Powell/GATA)

iii)The media is trying to portray Trump’s campaign as anti-semitic, which is furthest from the truth..it is Hillary’s campaign with its closer ties to Iran that must be viewed as dangerous.

( zero hedge)

iv)GATA”s main focus has always been on central banks and not bullion banks

( Chris Powell/GATA)

v)As we pointed out to you last week, premiums are now surfacing in India for the first time in 9 months. This is in spite of a 10% tax and excise duties:

( Reuters)

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)What a story!! Massive voter fraud exposed by project Veritas Part ii

( zero hedge)

ii)Michael Snyder explains why Obama is threatening Russia with Word War iii, right before the election.

( Mish Shedlock)

iv)It sure looks like Hillary has committed perjury: Wikileaks:

as for her personal emails….

“I asked that they be deleted”!!!!!!!!!!!!!!!!!!!!!!!!!!!!

(courtesy zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 4124 CONTRACTS to an OI level of 497,061 as the price of gold ROSE $6.40 with YESTERDAY’S trading.

We are in the delivery month is October and here the OI LOST 6 contracts DOWN to 121. We had 5 notices filed yesterday so we lost 1 contract or 100 additional oz will not stand.

The next delivery month is November and here the OI FELL by 32 contract(s) DOWN to 3004 contracts. This level is extremely elevated as generally November is a very poor delivery month.To give you an idea of size, on Oct 18 2015, we had an OI of only 248 contracts.The next contract month and the biggest of the year is December and here this month showed an decrease of 597 contracts up to 367,212.

And now for the wild silver comex results. Total silver OI ROSE BY 2317 contracts from 186,912 UP TO 189,229 as the price of silver ROSE to the tune of 4 cents yesterday. We are moving further from the all time record high for silver open interest set on Wednesday August 3: (224,540). The next non active delivery month is October and here the OI rose by 13 contracts up to 163. We had 0 notices filed yesterday so we gained 13 contracts or 65,000 additional oz will stand for delivery.The November contract month saw its OI LOSE 1 contract DOWN to 329. The next major delivery month is December and here it ROSE BY 524 contracts UP to 149,177.

VOLUMES:

Today the estimated volume was 131,988 contracts which is fair.

Yesterday, the confirmed volume was 165,006 which is also poor.

today we had 1 notice filed for 5,000 oz of silver:

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | NIL |

| Withdrawals from Customer Inventory in oz nil |

138,239.094 oz

HSBC

MALCA

SCOTIA

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

1100.000 oz

BRINKS

???

|

| No of oz served (contracts) today |

11 notices

1100 oz

|

| No of oz to be served (notices) |

110 contracts

11,000

oz

|

| Total monthly oz gold served (contracts) so far this month |

8535 contracts

854,500 oz

26.544 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 313,673.1 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 11 contractS of which 0 notices were stopped (received) by jPMorgan dealer and 11 notice(s) was (were) stopped received) by jPMorgan customer account.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

235,780.35 oz

CNT

Scotia

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

163 contracts

(815,000 oz)

|

| Total monthly oz silver served (contracts) | 356 contracts (1,780,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,191,804.6 oz |

end

NPV for Sprott and Central Fund of Canada

Central fund data not available today.

end

And now your overnight trading in gold,WEDNESDAY MORNING and also physical stories that may interest you:

“Higher Gold Prices” On Global Trade Slowdown – HSBC

HSBC’s respected chief precious metals analyst James Steel has written a note pointing out that the global trade slowdown will likely lead to “higher gold prices” as reported by Bloomberg.

Analysts at HSBC Group Inc. are telling clients that gold may be about to have another shining moment, as the precious metal’s status as a safe haven asset could boost prices, given the prospect of a looming downward shift in globalization.

The firm’s Chief Precious Metals Analyst James Steel says in a note published on Friday that “demand for gold is often stimulated by the same factors that fan protectionist and populist sentiment” and that “abrupt declines in cross border trade, investment and immigration, the dislocation of global economic policies, and a beggar-thy-neighbor approach to trade is almost tailor-made for higher gold prices.”

Previously, Steel advocated owning gold as a “long term insurance policy”.

When asked about whether he has a “message for gold bugs … people who have Krugerrands in their dressing room drawer”, Steel spoke of gold’s portfolio insurance benefits and “the diversification argument is the most powerful … it is an insurance policy”.

See the full article on Bloomberg here

Gold and Silver Bullion – News and Commentary

Gold holds gains on weaker dollar, rising stocks cap gains (Zeebiz)

Confidence Among Homebuilders in U.S. Falls From 11-Month High (Bloomberg)

Gold futures notch best settlement in nearly 2 weeks (MarketWatch)

Rising gasoline, rents push U.S. inflation higher in September (Reuters)

UK inflation sees biggest jump in two years (RTE)

Why gold will rise no matter who becomes the next U.S. president (MarketWatch)

Gold regain ground in 2017 but ‘bumpy road’ ahead (Reuters)

The Importance of The Deutsche Bank Silver Fix Lawsuit Settlement (TFMetalsReport)

Long term case for gold remains intact (ZeroHedge)

Gold Prices (LBMA AM)

19 Oct: USD 1,269.75, GBP 1,031.29 & EUR 1,154.97 per ounce

18 Oct: USD 1,261.65, GBP 1,031.15 & EUR 1,145.33 per ounce

17 Oct: USD 1,252.70, GBP 1,029.59 & EUR 1,139.58 per ounce

14 Oct: USD 1,256.15, GBP 1,028.79 & EUR 1,140.08 per ounce

13 Oct: USD 1,258.00, GBP 1,029.93 & EUR 1,141.76 per ounce

12 Oct: USD 1,255.70, GBP 1,024.53 & EUR 1,139.05 per ounce

11 Oct: USD 1,256.40, GBP 1,021.58 & EUR 1,130.76 per ounce

Silver Prices (LBMA)

19 Oct: USD 17.69, GBP 14.38 & EUR 16.11 per ounce

18 Oct: USD 17.65, GBP 14.37 & EUR 16.03 per ounce

17 Oct: USD 17.40, GBP 14.30 & EUR 15.83 per ounce

14 Oct: USD 17.47, GBP 14.28 & EUR 15.86 per ounce

13 Oct: USD 17.59, GBP 14.40 & EUR 15.95 per ounce

12 Oct: USD 17.44, GBP 14.23 & EUR 15.83 per ounce

11 Oct: USD 17.48, GBP 14.26 & EUR 15.78 per ounce

Recent Market Updates

– Euro “Will Collapse” As Is “House of Cards” Warns Architect of Euro

– Property Bubble In Ireland Developing Again

– “Gold Is A Great Hedge Against Politicians” – Goldman

– Sell Gold Now – Time To Liquidate Gold ETF, Pooled and Digital Gold

– Gold In GBP Up 43% YTD – “Massive Twin Deficits” To Impact UK Assets

– Ron Paul Says “Gold Going Up” Whether Trump Or Clinton Elected

– Gold Trading COT Report “Means Lower – Then Much Higher – Prices Coming”

– Currency Shock Sees Sterling Gold Surges 5% In One Minute “Flash Crash”

– Top Gold Forecaster: “As Quickly As Gold Fell” May “Rally Back” on Global Risks

– Gold Buying ‘Opportunity’ After Surprise 3.4% Drop

– Deutsche Bank “Is Probably Insolvent”

– GBP Gold Rises 1.3% as Sterling Slumps On ‘Hard Brexit’ Concerns, Up 36% YTD

– Why Krugman, Roubini, Rogoff And Buffett Hate Gold

END

Silver eagle demand (as well as gold eagle demand return to extremely high levels in October as the world economy shakes:

(courtesy SRSRocco/ Steve St Angelo)

Silver Eagle Demand Returns With A Vengeance As Political & Economic Turmoil Increases

by SRSrocco on October 18, 2016

U.S. Mint Silver Eagle sales surged in the first half of October due to increased turmoil in the political system and economic markets. Silver Eagle sales were strong in the first five months of the year, but weakened in the summer due to several factors.

One factor was the fall-off in demand by the Authorized Dealers (wholesalers) who had continued to purchase record Silver Eagles in the first part of 2016, even though retail investor demand had softened.. The other factor was a weakening of investor demand as the contagion from the U.K exit of the European Union subsided in the summer.

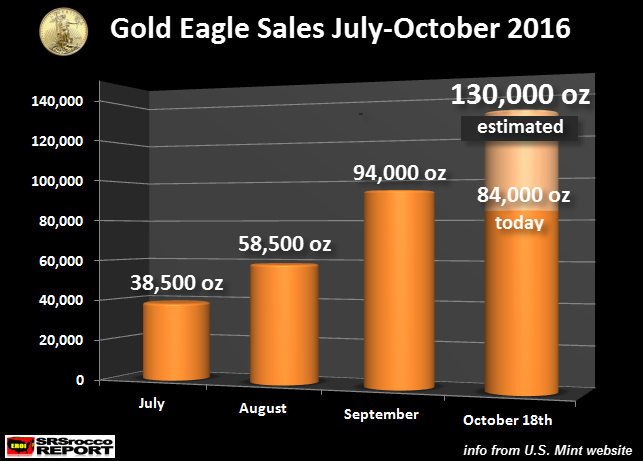

Regardless, U.S. Mint Silver Eagle sales came back with a vengeance in the first half of October, reaching 2,925,000 according to their most recent update today (Oct 18th). If we look at the chart below, we can see how much demand has increased compared the previous three months:

Silver Eagle sales as of October 18th are 75% higher than total sales for September of 1,675,000. Furthermore, they have already surpassed June’s sales of 2,837,000. If Silver Eagle sales continue to remain strong for the remainder of the month, I estimate that at least 4,000,000 will be sold.

In addition, Gold Eagle sales are also much stronger in October. Even though Gold Eagle sales of 84,000 oz have not yet surpassed the total of 94,000 oz in September, we still have nearly two more weeks remaining in October.

Also, if Gold Eagle sales remain strong for the next two weeks, they could reach 130,000 for the month. Not only is this much higher than September’s sales, it would be the highest monthly sales for the year…. even beating January’s record of 124,000 oz.

I believe investors are buying more Gold & Silver Eagles due to the continued disintegration of the financial and economic markets and the “Political Circus” called the U.S. Presidential Race. There has never been a more bizarre U.S. Presidential Campaign than the one we are witnessing today.

And then we had this headline from Zerohedge today, Saudis, China Dump Treasuries; Foreign Central Banks Liquidate A Record $346 Billion In US Paper. I imagine this is only the beginning, as the situation in the United States continues to unravel after the election… regardless of who is elected.

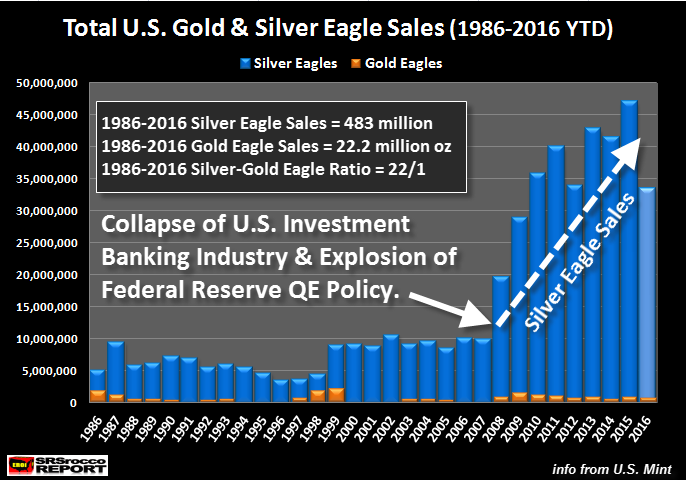

Precious metals investors need to understand just how much Silver Eagle demand increased after the collapse of the U.S. Investment Banking and Housing Market in 2008. As the Fed pumped massive amounts of liquidity via its QE policy (Quantitative Easing = Money Printing) into the U.S. markets, Silver Eagles sales have reached a staggering 325 million since 2008 (2008-2016 ytd):

While total cumulative Silver Eagle sales are 483 million oz (Moz) since the U.S. Mint started the program in 1986, investors purchased a stunning 325 Moz since 2008. Thus, Silver Eagle demand for the past nine years accounts for 67% of total sales since 1986.

Looking at it a different way, investors purchased 325 Moz of Silver Eagles from 2008-2016, versus 158 million oz from 1986-2007.

When the markets finally crack in the future, investors who have purchased physical gold and silver will be holding onto the best quality “Stores of Wealth” providing much better options that those stuck with most Stocks, Bonds and Real Estate.

end

As we pointed out to you last week, premiums are now surfacing in India for the first time in 9 months. This is in spite of a 10% tax and excise duties:

(courtesy Reuters)

Reuters

India gold trades at premium for first time in 9 months – dealersGold prices in India swung to a premium for the first time in nine months on Wednesday as jewellers and dealers in the world’s No.2 consumer of the metal ramped up purchases ahead of major festivals.

Dealers were charging up to $2 an ounce over official domestic prices, the first time premiums have been seen since mid-January, said Bachhraj Bamalwa, director at the All India Gems and Jewellery Trade Federation.

Gold importers have traditionally charged premiums to mitigate risks they take due to currency and price fluctuations.

But the precious metal had been trading at a discount for most of this year due to weaker-than-usual demand and a rise in smuggling. Discounts hit a record high of $100 an ounce in July.

“In the last 10 days, demand has improved due to festivals. The correction in prices is helping to attract buyers,” said Bamalwa.

Gold prices in India have fallen over 8 percent since hitting a peak of 32,455 rupees ($485) per 10 grams in July, the highest level in nearly three years.

Demand for gold usually strengthens in the final quarter as India gears up for the wedding season as well as festivals such as Diwali and Dussehra, when buying the precious metal is considered auspicious.

($1 = 66.6950 Indian rupees)

-END-

Chris Powell questions why the Wall Street Journal must question central banking!

(courtesy Chris Powell/GATA)

Dear Wall Street Journal: You don’t have to be a Nazi to question central banking

Submitted by cpowell on Tue, 2016-10-18 17:39. Section: Daily Dispatches

Tuesday, October 18, 2016

Editor, The Wall Street Journal

1211 Avenue of the Americas

New York, N.Y. 10036

Dear Editor:

Before your Bret Stephens again casually attributes anti-Semitism to complaints about central banking, as he did in his October 18 commentary, “The Plot Against America” —

http://www.wsj.com/articles/the-plot-against-america-1476745874

— he should try attending the monthly meetings of the Federal Open Market Committee and the Bank for International Settlements, where unelected officials gather secretly to determine what money is worth, to allocate huge amounts of it to favored institutions but not to others, and to plot surreptitious intervention in markets, thereby determining the value of all capital, labor, goods, and services in the world.

The Wall Street Journal itself seems to accept this most undemocratic wielding of immense power as the natural order of things.

But just as the old advertising slogan for rye bread noted that “you don’t have to be Jewish to love Levy’s,” you don’t have to be a Nazi to question central banking. Theoretically, at least, you could even be a journalist, if not at The Wall Street Journal.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

USA

CPowell@GATA.org

END

The media is trying to portray Trump’s campaign as anti-semitic, which is furthest from the truth..it is Hillary’s campaign with its closer ties to Iran that must be viewed as dangerous.

(courtesy zero hedge)

New York Sun: The alt-Trump?

Submitted by cpowell on Tue, 2016-10-18 17:55. Section: Daily Dispatches

From The New York Sun

Tuesday, October 18, 2016

The idea that Donald Trump’s campaign is borderline anti-Semitic is being hauled out this week as we hurtle toward Election Day. No one suggests Mr. Trump himself is hostile to Jews. The idea seems to be that because some of the alt-right groups are kvelling over his criticism of the big international banks and the Federal Reserve, Jews should vote for Hillary Clinton. Never mind that the Democrats have emerged as the party of appeasement in respect of, in Iran, the world’s most anti-Semitic regime.

This all burst into the headlines after Mr. Trump’s speech Thursday at Palm Beach. It was praised on a Web site called the Daily Stormer, which reported that in the speech Mr. Trump “affirmed” that the “the mass media isn’t ‘biased’ in the innocent sense; it’s the lying Jewish mouthpiece of international finance and plutocracy, seeking to protect agendas that make trillions of dollars for a small film of scum at the very top, at the expense of middle- and working-class Americans.”

The Daily Stormer article was being emailed around by some of the most distinguished journalists in the country. So imagine our surprise when we called up on the Web the text (and then the video) of Mr. Trump’s tirade only to discover that neither the Jews, nor Israel, nor Zionism were mentioned in the speech at all. Not once. The only thing that came close was when Mr. Trump attacked the Obama administration for sending $1.7 billion — in cash — to the Iranians. …

… For the remainder of the commentary:

END

GATA”s main focus has always been on central banks and not bullion banks

(courtesy Chris Powell/GATA)

Central banks, not bullion banks, long have been GATA’s primary target

Submitted by cpowell on Tue, 2016-10-18 23:34. Section: Daily Dispatches

7:40p ET Tuesday, October 18, 2016

Dear Friend of GATA and Gold:

In commentary today (http://www.gata.org/node/16850) Sharps Pixley CEO Ross Norman rebutted your secretary/treasurer’s skepticism about the need for a price benchmarking mechanism in gold like the venerable daily gold price fixings in London, which are operated by a few large investment banks (http://www.gata.org/node/16845).

Maybe your secretary/treasurer should have been clearer from the outset, but it seems to GATA that valid benchmarks could be derived entirely from price and trade volume data at the end of each day, benchmarks that would result from all trading and not the trading of a few banks talking confidentially to each other and to God-only-knows who else.

So why use a benchmark? Well, thousands of companies will refer in their contracts to “the gold price” and it needs to be defined. Many will not actually trade on a particular fix but the financial transaction they are a party to will be linked to it. Hence they need to know that the price is fair and reflects reality.

Take a mining company or a jewellery company. One will sell and the other might buy through a contract with a counterparty at the average of the PM fix for the month plus, say, $1. But they may not be active on each and every fix. Their contracts will refer to “the gold price,” but you have to ask: Which one?

The spot price is no good as they are merely subjective adverts by individual banks (adverts displaying their buying and selling interest and not a “traded at” price) and thus massively open to manipulation — or a closing price that again can be gamed by market participants. (But this is quite similar to the fixings in base metals.)

People have looked at volume-weighted averages and other procedures but most are fallible or can be corrupted. The gold fix in our opinion is exceptionally difficult to game — and if you were so minded, then there are far easier ways to do so such as simply front-running a trade in the spot market. Who would ever know?

In short, the real market (that’s to say producers and consumers) needs a fair, reliable, and representative price against which to honor its contracts and commitments. I happen to think that the gold market has done a pretty good job in evolving and devising the best foolproof way of deriving an objective price for those who may not actually be trading that particular day but will be affected by the outcome.

Any other prices are simply subjective and therefore invalid or not representative.

2) Deutsche Bank and the other banks. I think they are a red herring. It is tempting to imagine that banks hold a central role in determining price outcomes when in fact they are just a conduit and merely reflect what is going on around them. They are far more clueless than you think. If the Basle III banking regulatory framework goes ahead as anticipated, then most will become history anyway by 2018 as far as commodities trading goes.

It is proposed that holdings in gold will be valued at a mere 15 percent for capital adequacy purposes and the costs of funding or holding positions will skyrocket, which will drive most banks out of the market if regulation and compliance have not already done so by then. They are all already in significant retreat, and for a good many houses bullion is now simply tacked onto the side of foreign-exchange trading and managed by a currency trader who knows little about the market — and cares even less.

In short, the banks are a much-diminished influence and getting less significant, with a few exceptions.

Few people will shed a tear as the commodities traders at the banks retreat, but do ask yourself what you think might replace them, like unregulated entities, and how well they will treat you. Be careful what you wish for.

The news that Deutsche Bank has “settled” by paying a $38 million fine confirms my point. They “settled” without admitting guilt or being found guilty; they just wanted out. This is why the fine is so small.

Now it may still transpire at some point that there have been some minor irregularities around the London gold fix and, again, it’s not for me to defend the people and institutions. I am defending only the London fix as the best solution there is, and if you wanted to cheat, it’s the worst place to do so.

3) Central banks. I think it is a popular myth to blame the investment banks and commodity traders for all evils. They are actually just guys who play within the framework set by the regulators. No malice aforethought. As said, they are losing relevance.

However, there is an invisible hand at play and it sets the rules of the game and often attempts to pre-determine its outcome — that is the official sector. Once benign custodians of the reserve assets of countries, official sectors here are the architects of the economy and masters of its narrative. I fear that we are moving toward a centrally planned and managed economy of the sort once mocked in the former Soviet Union.

If GATA’s gripe was with these institutions rather than the conduit through which they trade, I think your efforts would resonate with many more market observers and participants.

END

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.7367( REVALUATION NORTHBOUND SLIGHTLY /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS TO 6.7417 / Shanghai bourse CLOSED UP 0.844 POINTS OR 0.03% / HANG SANG CLOSED DOWN 89.42 POINTS OR 0.38%

2 Nikkei closed UP 35.30 OR 0.21% /USA: YEN FALLS TO 103.35

3. Europe stocks opened ALL IN THE RED ( /USA dollar index DOWN to 97.83/Euro UP to 1.0978

3b Japan 10 year bond yield: LOWERS TO -.057%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 103.96/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.91 and Brent:52.33

3f Gold UP /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS QUITE A BIT to +024%

3j Greek 10 year bond yield RISES to : 8.44%

3k Gold at $1270.40/silver $17.77(7:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble UP 27/100 in roubles/dollar) 62.85-

3m oil into the 50 dollar handle for WTI and 52 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 103.35 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9891 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0858 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.024%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.749% early this morning. Thirty year rate at 2.509% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures, Global Stocks Mixed After Lackluster Chinese Economic Data; Oil Rises Over $51

US futures were little changed, with European shares lower, and Asian stocks higher as caution returned after last night’s Chinese economic data did little to clear up how the world’s second largest economy is performing, and provided few positives for investors ahead of the third and final U.S. presidential debate; imminent announcements from both the ECB and the Fed also will keep traders on their toes today.

All eyes, however, will be on the third U.S. presidential debate on Wednesday night in Las Vegas, which comes as opinion polls show a substantial lead for Hillary Clinton over Donald Trump.

The U.S. dollar fell from a seven-month peak on Wednesday, combining with signs of an easing supply glut to help lift oil prices back towards a one-year high. The weaker dollar boosts oil, which gained over 1 percent on Wednesday, pushing WTI over $51. The bounce in commodity prices has helped bolster inflation expectations in the euro zone, nudging the bloc’s bond yields further away from the record lows struck after Brexit.

The overnight mood was set by a relatively uneventful set of Chinese economic reports, which saw a GDP and Retail sales meet expectations, while Industrial Production missed modestly.

- Chinese GDP SA (Sep) Q/Q 1.80% vs. Exp. 1.80% (Prey. 1.80%); Chinese GDP (Q3) Y/Y 6.70% vs. Exp. 6.70% (Prey. 6.70%).

- Chinese Industrial Production (Sep) Y/Y 6.10% vs. Exp. 6.40% (Prey. 6.30%); Chinese Industrial Production YTD (Sep) Y/Y 6.00% vs. Exp. 6.10% (Prey. 6.00%).

- Chinese Retail Sales (Sep) Y/Y 10.70% vs. Exp. 10.70% (Prey. 10.60%): 8-month high. Chinese Retail Sales YTD (Sep) Y/Y 10.40% vs. Exp. 10.30% (Prey. 10.30%).

The MSCI All Country World Index of shares was umchanged after rallying in the last session by the most in almost a month. Hong Kong stocks swung to a loss, while Chinese equities and the Australian dollar erased gains after an unexpected slowdown in China’s industrial output cast a cloud over gross domestic product figures that matched estimates. The Dollar remained near a one-week low following U.S. inflation data that damped expectations for interest-rate hikes. Crude oil rose after data showed American supplies fell, while aluminum dropped.

“China won’t do anything new in terms of policy because the economy isn’t sliding,” said Ben Kwong, a Hong Kong-based director at KGI Asia Ltd. “Under these conditions, the market doesn’t really have a direction. It needs to wait for news on U.S. rates.”

European stocks retreated as investors assessed Chinese data for indications of the health of the global economy, while awaiting updates from the European Central Bank and Federal Reserve. The Stoxx Europe 600 Index was down 0.2 percent as of 8:16 a.m. London time, after surging 1.5 percent on Tuesday. ASML Holding NV jumped by the most in eight months after Europe’s largest semiconductor-equipment maker forecast profitability above analysts’ estimates for the final three months of the year.

The MSCI Asia Pacific Index added 0.3 percent, having been up 0.4 percent prior to the China data. The Hang Seng Index declined 0.5 percent and the Shanghai Composite Index was little changed. China’s gross domestic product expanded 6.7 percent in the last quarter from a year earlier, the third straight period at that pace. Industrial output rose 6.1 percent, less than the median forecast for a 6.4 percent gain.

S&P 500 futures slipped were unchanged after the underlying gauge added 0.6 percent on Tuesday. While only 57 of the benchmark’s members have reported results so far, about 80 percent announced earnings that exceeded analysts’ estimates, according to data compiled by Bloomberg.

The yield on US 10Y Treasuries was little changed at 1.74%. It fell three basis points on Tuesday as core inflation, which excludes energy and food costs, came in weaker than economists estimated. The probability of the Fed hiking interest rates this year slipped by three percentage points in the last session to 63 percent, futures prices indicate. Australia’s 10-year bonds gained for the first time in four days, pushing their yield four basis points lower to 2.30 percent. The rate on similar-maturity U.K. notes increased by two basis points to 1.10 percent.

Market Snapshot

- S&P 500 futures down less than 0.1% to 2131

- Stoxx 600 down 0.2% to 342

- FTSE 100 down 0.1% to 6992

- DAX down 0.2% to 10611

- German 10Yr yield down 1bp to 0.02%

- Italian 10Yr yield down 2bps to 1.37%

- Spanish 10Yr yield down less than 1bp to 1.09%

- S&P GSCI Index up 0.6% to 377.9

- MSCI Asia Pacific up 0.4% to 140

- Nikkei 225 up 0.2% to 16999

- Hang Seng down 0.4% to 23305

- Shanghai Composite up less than 0.1% to 3085

- S&P/ASX 200 up 0.5% to 5435

- US 10-yr yield up less than 1bp to 1.74%

- Dollar Index down 0.2% to 97.7

- WTI Crude futures up 1.4% to $51.01

- Brent Futures up 1.4% to $52.42

- Gold spot up 0.7% to $1,271

- Silver spot up 0.6% to $17.72

Top Global Headlines

- Donald Trump and Hillary Clinton face off in final presidential debate at University of Nevada in Las Vegas

- China Life Invests in $2b of Starwood Capital Hotels: Insurer, other companies buy stake in portfolio of 280 hotels

- Saudi Arabia Says Many Nations Will Join OPEC Output Cuts: Producers will start with output freeze, maybe a small cut

- Airlines Would Provide Refunds for Late Bags Under U.S. Plan: U.S. announces additional consumer protections for passengers

- For Wells Fargo, Angry Questions About Profiling Latinos: Employees step forward after scandal over bogus accounts

- Imperva Sale Process Said to Be on Hold as It Seeks Better Price: Potential suitors wait to see if the company’s growth can improve enough to justify a higher price

- Staples Turns to Licensing to Push Brand Beyond Office Supplies: First product is online service for managing records

- Clinton Has 9-Point Lead as Comeback Obstacles Loom for Trump: Bloomberg Politics survey taken after leaked video

- Salesforce M&A Draft Document Included Adobe, ServiceNow: WSJ

Looking at regional markets, we start in Asia, where stocks traded mostly higher following the positive lead from the US although gains were capped as participants digested a slew of tier-1 Chinese data including GDP, Industrial Production and Retail Sales. ASX 200 (+0.4%) and Nikkei 225 (+0.2%) traded modestly higher as oil names benefitted from advances in WTI after an unexpected drawdown in API crude inventories, while consumer discretionary outperformed in Australia on M&A news flow regarding an AUD 11bIn merger between Tabcorp and Tatts Group. Chinese markets were mixed with Shanghai Comp. flat, while Hang Seng (-0.4%) lagged after mixed data in which GDP printed in line with estimates and Retail Sales posted an 8-month high, however Industrial Production fell short of estimates and several HK firms issued profit warnings. 10-yr JGBs were flat despite mild gains seen in Nikkei 225, as the BoJ were also in the market to the tune of JPY 1.12tIn in 1yr-25yr-F government debt.

For those who missed China’s economic data, here is a quick summary:

- Chinese GDP SA (Sep) Q/Q 1.80% vs. Exp. 1.80% (Prey. 1.80%); Chinese GDP (Q3) Y/Y 6.70% vs. Exp. 6.70% (Prey. 6.70%).

- Chinese Industrial Production (Sep) Y/Y 6.10% vs. Exp. 6.40% (Prey. 6.30%); Chinese Industrial Production YTD (Sep) Y/Y 6.00% vs. Exp. 6.10% (Prey. 6.00%).

- Chinese Retail Sales (Sep) Y/Y 10.70% vs. Exp. 10.70% (Prey. 10.60%): 8-month high. Chinese Retail Sales YTD (Sep) Y/Y 10.40% vs. Exp. 10.30% (Prey. 10.30%).

- China National Bureau of Statistics said the economy is better than expected, although still faces uncertainty. The stats bureau also stated that employment is better than expected and that China is to ensure it will achieve its annual growth target.

Top Asia News

- Hedge Fund Startups Plummet in Asia Amid Low Returns, High Fees

- Standard Chartered Moving Past India Woes With Essar Payment

- Mitsubishi Motors Shares Surge on Report Ghosn to Be Chairman

- Minsheng Bank Said to Explore Setting Up Bad-Loan Asset Manager

- Super Typhoon Threatens Philippines, May Also Hit Hong Kong

- ‘Quick Learner’ Jokowi Building Momentum After Slow Start

In Europe, equities (EuroStoxx -0.2%) are trading softer this morning after data from China failed to inspire gains. Chinese GDP came inline with expectations but the weak industrial production number seems to have dampened sentiment across markets. In terms of a sectors, Industrials are underperforming after FTSE listed Travis Perkins opened lower by 5.6% after announcing jobs cuts and store closures citing uncertain trading conditions. Bunds opened relatively flat, although we have seen some outperformance in the long end of the yield curve ahead of upcoming supply, which was eventually absorbed with a solid b/c of 1.7. Furthermore, participants may also be sitting on the sidelines ahead of the ECB rate decision where we could see an extension of its bond buying program which was due to finish in March 2017.

Top European News

- U.K. Labor Market Slows as Squeeze on Household Incomes Begins: Real incomes rise at the slowest rate since early 2015. Employment growth slows to 106,000 in quarter through August

- ASML Forecasts Higher Profit Margins, Says EUV Sales Advance: Chip-equipment maker sees gross margins up to 48% of sales. Customers order three of its latest extreme ultraviolet gear

- Monte Paschi Jumps as Board Presses Ahead With Business Plan: Lender’s board set to approve new business plan on Oct. 24. Bank continues with recapitalization, disposals of bad loans

- Apple Supplier Laird Plunges on ‘Brutal’ Price Competition: Expected pick-up in smartphone-related orders later than usual. Parts maker highlights increased margin pressure due to prices

- Reckitt, Travis Perkins Drops After Earnings Drag Down FTSE 100: British equities fell for the second time this week amid disappointing earnings results

In FX, the Bloomberg Dollar Spot Index was little changed after losing 0.5 percent over the last two days. The measure advanced over the last two weeks as speculation the Fed was getting closer to a rate hike prompted hedge funds and money managers to boost bullish bets on the greenback. The pound weakened 0.2 percent versus the dollar. The U.K.’s departure from the European Union could lead to a 4.5 percent drop in gross domestic product by 2030, the Guardian newspaper reported, citing an average of estimates that was included in a paper circulated at a Brexit cabinet committee meeting. Australia’s dollar was steady, after earlier strengthening as much as 0.3 percent. New Zealand’s currency was up 0.1 percent, having recorded a gain of 0.6 percent in the run-up to the Chinese data. Both countries count China as their biggest export market. “If the Aussie and Kiwi are looking for fresh fuel, they didn’t find it in the China data,” said Sean Callow, a senior strategist at Westpac Banking Corp. in Sydney.

In commodities, West Texas Intermediate crude climbed 1.3 percent, rising over $51.00 a barrel in New York. U.S. oil stockpiles dropped by 3.8 million barrels last week, API reported yesterday, on expectations of an inventory build. Oil has risen about 14 percent since OPEC reached a deal to manage supply last month. Aluminum declined 0.7 percent, after earlier rallying as much as 0.8 percent. China, which accounts for more than half of world output, reported Wednesday that its production surged to a 15-month high in September as new and idled plants were fired up. “The smelters are coming back in a rush now, so that’s a concern,” said Paul Adkins, managing director of aluminum consultancy AZ China Ltd. “For the rest of this year, two million tons of annual capacity is guaranteed to come in and guaranteed not to exit.” That’s “going to put a lot of pressure on prices when we get to November or December onwards,” he said. Rubber futures in Japan fell 3.4 percent, the most in a month. Global production is increasing and China’s economic data also weighed on sentiment, according to Gu Jiong, an analyst at Yutaka Shoji, a commodity broker in Tokyo.

Looking at the day ahead, the focus will be on the housing market with the release of the September housing starts and building permits data. Both are expected to have rebounded last month. The Fed will release its latest Beige Book this evening. Away from the data the Fed’s Williams is scheduled to speak, followed by Kaplan. Earnings wise Morgan Stanley (prior to the open), eBay and American Express (both after the close) are among the 25 S&P 500 companies reporting today. Of course the other big focus is the third and final US Presidential debate at 2am BST tomorrow morning (or 9pm ET tonight).

* * *

DB’s Jim Reid concludes the overnight wrap

We’re straight to China this morning where the latest GDP data is in. There have been few surprises however with Q3 GDP printing bang in line with the market at 6.7% yoy for the quarter. Remarkably that follows identical 6.7% readings for both Q1 and Q2 this year too and puts the economy on track to meet the government’s full year target of at least 6.5% growth. Released alongside the GDP data were the September activity indicators. Both retail sales (+10.7% yoy from +10.6%) and fixed asset investment (+8.2% yoy from +8.1%) rose one-tenth from the prior month and matched the consensus estimates, however the one negative from this morning’s data was industrial production (+6.1% yoy vs. +6.4% expected) which declined two-tenths unexpectedly last month.

Markets have been fairly muted in response to the data. In China the CSI 300 and Shanghai Comp are +0.05% and +0.16% respectively which isn’t too different to where the bourses were prior to the release suggesting that there’s little change in policy expectation from the PBoC. Elsewhere the Nikkei is +0.14%, Hang Seng -0.12%, ASX +0.39% and Kospi +0.33%. The Aussie Dollar is flat and has pared earlier gains while US equity index futures are modestly higher.

So it’s been a pretty busy last 24 hours for important data. Yesterday we got the double dose of inflation numbers from both the UK and US which were interesting. In the UK we learned that headline CPI rose +0.2% mom in September and a bit more than expected (+0.1% expected), helping the YoY rate to rise to +1.0% from +0.6% which is the highest since November 2014. Sterling weakened -1.26% in September but is down another -5.00% in October so it’s still early days to assess the full impact of the FX pass through which might appear more in the data next year. The core reading also increased two-tenths and a bit more than expected to +1.5% yoy (vs. +1.4% expected). Sterling outperformed following the data sending the Pound up +0.94% to $1.2298 for its best day since September 6th while 10y Gilt yields rallied 4.3bps to close at 1.078%, outperforming the wider market. The Pound was mostly boosted by softening Brexit concerns following comments from James Eadie, a UK government lawyer. He suggested that the Brexit process was ‘very likely’ to be subject to ratification process in parliament following a court hearing yesterday. According to the BBC, the vote would take place after negotiations have taken place and Article 50 already triggered. By then it will probably be too late for Parliament to have much influence but perhaps markets felt that it would ensure that the government negotiated a less hardline Brexit given the scrutiny of MPs.

Meanwhile, inflation in the US was a little bit more underwhelming. Headline CPI rose +0.3% mom in September as expected however the core (+0.1% mom vs. +0.2% expected) missed with the YoY core rate dipping one-tenth to +2.2% as a result. The YoY headline rate did rise to +1.5% from +1.1%. Our US economists made some interesting observations yesterday and noted that the categories that have been underpinning the core CPI have been nondiscretionary sectors such as housing rents and medical care. This is partly the result of a near double-digit surge in prescription drug prices over the last few months. In their view, surging medical care inflation is not necessarily indicative of robust underlying consumer demand. Demographics, particularly the aging of the baby boomers, are exerting upward pressure on demand for healthcare. For example, over the two years ending in Q2, healthcare services and pharmaceuticals spending have accounted for 33% of the improvement in inflation-adjusted personal consumption expenditures. This is usually only the case during a recession, when nondiscretionary spending is curtailed. Two sectors within the core CPI that are more discretionary, apparel and recreation costs, are not showing nearly as much inflationary pressure. In point of fact, the year-over-year changes of these series, which in September were -0.1% and +0.8%, respectively, are running well below that of the overall core CPI (+2.2%).

The end result in markets was for Treasury yields to track lower. The benchmark 10y yield fell 2.8bps to close at 1.739% having touched 1.786% intraday, while 30y yields ended close to 2bps lower. The Greenback pared early declines to finish more or less unchanged while it was a broadly stronger day for risk assets with corporate earnings also well in focus. In Europe the Stoxx 600 initially closed up +1.50% with financials driving the gains, before the S&P 500 finished the day +0.62% making it nine sessions in a row now that the index has alternated gains and losses day to day. The healthcare sector was at the forefront of gains following a decent earnings report from UnitedHealth while the Banks were under the spotlight again following Goldman Sachs’ Q3 results. As has been the theme so far in the sector, Goldman reported beats at both the revenue and earnings lines with revenues from FICC jumping +49% yoy and much more than expected by the market. While the consensus EPS estimate of $3.88 was more or less the lowest in the last twelve months for the quarter, the reported number of $4.88 was still well ahead of the highest ($4.57) consensus forecast in that time, unlike what we saw with Citi and JP Morgan.

Elsewhere, credit markets were also slightly stronger yesterday with CDX IG and the iTraxx Main both finishing 1bp tighter. Energy credits also got a boost after WTI bounced back +0.70% to close just above $50/bbl. It’s up another +1% this morning after the American Petroleum Institute reported that inventories dropped by 3.8m barrels last week.

Speaking of issuance, it was hard to ignore Professor Otmar Issing’s comments from earlier this week. According to the Telegraph, the first chief economist of the ECB warned that the ‘decline in the quality of eligible collateral is a grave problem’ and that ‘the ECB is now buying corporate bonds that are close to junk and the haircuts can barely deal with a one notch credit downgrade’. He went on to say that the ‘reputational risk of such actions by a central bank would have been unthinkable in the past’. He also warned that the ECB is on a ‘slippery slope’, has ‘crossed the Rubicon’ and ‘realistically it will be a case of muddling through, struggling from one crisis to the next’. He summed this up by saying that ‘one day, the house of cards of will collapse’ when asked about the future of the ECB and the euro. That’s one to ponder over your morning coffee.

Staying with existential European matters, with Italy’s constitutional referendum looming it was interesting to see the latest poll yesterday conducted by IPR Marketing for RAI’s Porta a Porta. The poll showed that 48.5% of Italian voters would vote ‘Yes’ in the referendum versus 51.5% for a rejection. That put the ‘Yes’ voters up 2.5pts versus the previous month according to the survey although the takeaway for us is just how to close voting is. While the number of undecided voters declined (17% versus 25% previously) the proportion is still relatively high so it’ll be worth keeping an eye on future polls in the run up.

Before we look at today’s calendar, in their report this morning, our European equity strategists argue that the most important question for markets right now is whether we are at the cusp of a paradigm shift from disinflation to reflation. There is some evidence to support this notion: higher commodity prices, the recent strengthening in global growth momentum, some upside surprises to inflation and the hope for a hand-over from monetary to fiscal stimulus. However, our strategists argue that the current state of low growth, low inflation and low bond yields is nonetheless likely to persist for a while longer, given that the oil price seems to have overshot fundamentals. They also see downside risks for US and Chinese growth, which is set to weigh on inflation. Lastly, they highlight that fiscal stimulus has a track record of only being employed in reaction to macro stress. As a consequence, our strategists remain cautious on European equities as well as the cyclical and financial sectors that would benefit in a reflationary environment.

Looking at the day ahead, this morning we’re kicking off in the UK again where we’ll get the August and September employment data which includes the ILO unemployment rate (expected to hold steady at 4.9%), average weekly earnings and claimant count prints. The focus across the pond this afternoon is on the housing market with the release of the September housing starts and building permits data. Both are expected to have rebounded last month. The Fed will release its latest Beige Book this evening. Away from the data the Fed’s Williams is scheduled to speak this afternoon (1.45pm BST) followed by Kaplan (6.30pm BST) this evening. BoE Chief Economist, Andy Haldane, speaks this evening in London while Chancellor Hammond is due to speak before the Treasury Committee in the afternoon. Earnings wise Morgan Stanley (prior to the open), eBay and American Express (both after the close) are among the 25 S&P 500 companies reporting today. Of course the other big focus is the third and final US Presidential debate at 2am BST tomorrow morning (or 9pm ET tonight).

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 0.844 POINTS OR 0.03%/ /Hang Sang closed DOWN 89.42 POINTS OR 0.38%. The Nikkei closed UP 35.30 POINTS OR 0.21% Australia’s all ordinaires CLOSED UP 0.414% /Chinese yuan (ONSHORE) closed UP at 6.7367/Oil ROSE to 50.91 dollars per barrel for WTI and 52.33 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.7417 yuan to the dollar vs 6.7367 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

3a)THAILAND/SOUTH KOREA/SOUTHEAST ASIA:

b) REPORT ON JAPAN

none today

c) Report on CHINA

In just one month, China injects another 1/4 trillion dollars of debt (Total Social Financing) to jump start their economy. That is equivalent to 2.5 trillion USA dollars per year or 25% of their entire GDP. However that is not the scary part: you must also include two other very important debt items: Government debt, sovereign and local as well as the huge shadow banking sector: Peer to Peer lending. The total rate of debt expansion is twice the level of GDP

(courtesy zero hedge)

China Injects Economy With A Quarter Trillion In Debt In One Month, But The Full Story Is Much Scarier

Overnight the PBOC reported its debt statistics for the month of September and it will probably not come as a surprise that for yet another month, China flooded its economy with the latest massive new loan injection, while the country’s broadest aggregate measure of new credit, Total Social Financing, again surpassed estimates with the number exceeding a quarter trillion dollars in total new debt, in order to fuel, what Bloomberg dubbed, “the economy’s continued stabilization”, even though the economy is inherently unstable due to the massive stock of debt already present inside China’s financial system.

To summarize, this is what China’s credit creation looked like in September:

- Aggregate financing was 1.72 trillion yuan, or $255 billion, higher than the median estimate of 1.39 trillion Yuan

- New yuan loans stood at 1.22 trillion yuan, higher than the median estimate of 1 trillion Yuan

- Of this, new home mortgage loans rose 205.5b yuan from year ago, Shanghai Securities News reported

- New home mortgage loans in first three quarters at 3.63t yuan, making up 35.7% of total new loans

Visually, the ongoing surge in TSF is shown below:

The table below shows TSF broken down by component. The notable changes, aside from the surge in plain vanilla Yuan loans, was the latest decline in FX loans, which some suggest is how a modest amount of capital is used to exit the country, as well as the CNY 220 billion slump in Bankers acceptances, which together with entrusted loans, comprise the core funding conduits of China’s shadow banking system.

Also notable is that the broad M2 money supply rose 11.5% from a year earlier, fractionally below the 11.6% estimate but higher than the 11.4% in August, a pace that remains nearly double that of the country’s GDP, which suggests that it takes roughly 2 Yuan in new debt to generate 1 Renminbi in GDP. Meanwhile M1 has stopped growing.

Putting this ongoing debt binge – which as on previous occasions has succeeded in stabilizing the economy, however left it with even less breathing space for the next time the economy needs a debt-funded push – in context, policy makers are switching focus to reining in soaring home price gains that cheap borrowing costs have spurred. As Bloomberg notes, China urgently needs a plan to address a build up of corporate debt that’s manageable but with a window to address it “closing quickly,” according to an International Monetary Fund working paper. As the September data reveals, the only solution Beijing has to the debt problem, is to provide even more of it.

Below are some of the dazed and confused economist takeaways from last night’s data:

- “The government is in a dilemma: if they tighten the real estate sector too much, the economy could turn down sharply; but if they don’t control it, they’ll allow the bubble to expand,” said Shen Jianguang, chief Asia economist at Mizuho Securities Asia Ltd. in Hong Kong. He expects a sharp slowdown in credit expansion in October.

- “It’s more of the same: more yuan lending, more debt, no real increase in M2 growth and a much larger rise in M1 growth,” said Michael Every, head of financial markets research at Rabobank in Hong Kong. “It screams ’Liquidity trap!”

- “The property frenzy will certainly limit the PBOC’s appetite for further easing,” said Raymond Yeung, chief greater China economist at Australia & New Zealand Banking Group Ltd. in Hong Kong. “While it is too early to call for tightening, deleveraging is certainly an ongoing theme” in the fourth quarter.

- “While credit growth remains rapid relative to a couple of years ago, it has been slowing in recent months,” Julian Evans-Pritchard, economist at Capital Economics in Singapore, wrote in an e-mail. “Broader worries about credit risks means further monetary easing is unlikely. It will take time for this more cautious policy stance to impact economic growth.”

- “Beijing talks about controlling credit but allows the banks to increase loans,” said Andrew Collier, an independent analyst in Hong Kong and former president of Bank of China International USA. “The official message is not the same as the reality. Pressure from the banks for profits, from corporates for loans, and from local governments for revenue from the property sector is driving the Chinese economic bus more than the policy makers in Beijing.”

* * *

Incidentally, the real picture is even worse than shown above.

A quick background on Total Social Financing (TSF), courtesy of Barclays:

In early 2011, the PBoC launched a new data series, total social financing (TSF), as a comprehensive indicator to monitor the economy’s total fundraising. Its development was in response to the rapidly growing shadow banking and direct financing amid increasing financial disintermediation and regulatory arbitrage. As a result of these changes in China’s financial landscape, it was thought that traditional indicators such as bank loans or deposits no longer captured the full picture of financing/investment and money supply/demand.

Over time, TSF developed into a macro control tool, together with broad money (M2). “To maintain a reasonable growth in the money credit and TSF” is now a phrase written in the annual government work report since 2011. In March 2016, the government for the first time set an explicit target for TSF growth of 13%, slightly higher than actual growth of 12.4% in 2015, in addition to its 13% M2 growth target (up from a target of 12% in 2015).

Defined by the PBoC to measure the domestic financial sector’s (non-government) support to the real economy, the TSF statistics include bank loans, corporate bonds, three traditional shadow banking activities, as well as equity financing since its release in 2011(Appendix). The shadow credit includes loans by trust companies, inter-corporate entrusted loans, and undiscounted bankers’ acceptance bills. The TSF by design excluded: 1) government bonds, but has included the local government financing vehicle (LGFV) loans and bonds; and 2) external debt, such as foreign direct investment and other foreign borrowings.

However, as we showed previously even TSF is not sufficient to capture all the nuances of China’s debt. Two core credit items in which the TSF are missing are Government bonds, both central government and local government, and “Non-traditional shadow credit channelled by banks and NBFIs.” To be sure, there is much more to Chinese credit creation, much of it in the “shadow banking sector” as the following graphic shows:

… but if one adds just those two inclusions, the result is a far greater annual increase in the broadest credit aggregate which includes TSF, Government Bonds, LG bonds, and Bank claims on NBFIs (shadow banking), one gets the light blue line shown below.

What happens if one uses these adjusted credit aggregates instead of the widely accepted TSF? Here are some thoughts from Barclays:

From a stock perspective, broad credit is 20-30% higher than what is counted in the official TSF data. Relative to GDP, our five measures put China’s credit-to-GDP ratio currently in a range from 260% to 275% of GDP as of September 2016.

From a growth rate perspective, the speed of credit expansion is alarming. Our methods put the current pace of credit growth in China in a range between 19% and 20%, well above the reported official TSF growth of 12.4% and new loan growth of 13.0% in September.

Using a bottom-up approach, we made ballpark estimations of the size of “shadow credit” based on the above discussions, which reached around CNY63trn as of September 2016. This is calculated by adding the ultimate forms of credit, ie, trust loans (September: CNY5.9trn), entrusted loans (CNY12.5trn), bankers’ acceptances (CNY3.8trn), corporate bonds (CNY17.3trn), and other non-standard credit assets5 (CNY23.5trn).

Frankly, these are mindblowing numbers and yet, Barclays does not think China’s debt bubble is about to burst despite admitting that this pace of debt growth is unsustainable.

As the bank admits, “China’s debt crisis does not appear to be imminent. China’s debt is largely domestically owned. Hence, unless there is bank run or capital flight by local residents, the typical EM-style financial crisis, like the Asia Financial Crisis, is less likely. The heavy state involvement, with the majority of loans coming from state-controlled banks to state-owned enterprises, the strengthening state control and sizable state assets suggest that the Chinese government still has the capacity to manage the pace of NPL recognition and debt restructuring in the banking system.”

But it’s not all good news: “On the other hand, the current pace of credit expansion, more than twice the rate of nominal GDP growth, is clearly unsustainable (Figure 13).” It then concludes as follows:

“The interconnectedness between the corporate sector and the banks points to systemic risks in the economy, especially as the economy is forecast to slow further.Such perceived “implicit guarantees” by the state have resulted in excessive risk-taking across asset classes (equity, bond and property), across economic agents (corporate, local governments and households), and across financial intermediaries. With rising central government’s contingent liability, the sovereign risks are increasing. Moody’s downgraded its outlook on Chinese government debt to negative from stable in March 2016, questioning China’s surging debt burden and the government’s ability to enact reforms.”

So far the only “reform” the government has enacted has been to mask debt with even more debt, roughly 300% of GDP. However, as banks, rating agencies, the IMF and even the G-20 admit, the days of kicking the can for China are coming to an end. What waits on the other side of that particular journey is not pleasant: either massive social revolt by China’s middle class, as the government renormalizes its economy in the process hiring tens of million of (soon to be angry) workers, or it unleashes the biggest banking crisis the world has every seen: at $35 trillion in total financial assets, China’s banking system is more than double the size of the US. We wish Beijing (and Janet Yellen) the best of luck with their hopes that it will somehow be contained..

end

Global markets hardly move as China just manages to meet GDP expectations of 6.7% Here are the other important data points for China this morning!

(courtesy zero hedge)

- Industrial Production YoY MISS: 6.1% vs +6.3% Exp from +6.3% prior (6.0% to 6.5% range)

- Retail Sales YoY MEET: +10.7% vs +10.7% Exp from +10.6% prior (10.5% to 11.0% range)

- Fixed Assets Investments YTD YoY MEET: +8.2% vs +8.2% Exp from +8.1% prior (8.0% to 8.6% range)

- GDP YoY MEET: +6.7% vs +6.7% Exp from +6.7% prior (6.4% to 6.9% range)

Global Markets Shrug As China ‘Manages’ To Meet GDP Expectations

A couple of trillion dollars of freshly created debt and a collapsing currency (which did nothing for the trade balance which was described as “not very solid” by authorities) along with a dead stock market, a bond market at record low yields (unconvinced at any recovery) and a housing bubble and China’s National Statistics Bureau ‘nails it’ with ‘meets’ across the board (albeit Industrial production disappointed).

Yuan is accelerating weaker to 6 year lows… (but it didn’t help trade)

And yet another resurgence in total social financing (aggregate credit) In China…

And the data was a snoozefest:

- Industrial Production YoY MISS: 6.1% vs +6.3% Exp from +6.3% prior (6.0% to 6.5% range)

- Retail Sales YoY MEET: +10.7% vs +10.7% Exp from +10.6% prior (10.5% to 11.0% range)

- Fixed Assets Investments YTD YoY MEET: +8.2% vs +8.2% Exp from +8.1% prior (8.0% to 8.6% range)

- GDP YoY MEET: +6.7% vs +6.7% Exp from +6.7% prior (6.4% to 6.9% range)

Bloomberg notes that the industrial output gain is weaker than forecast while retail sales are bang in line – confirming the narrative that China’s economy is rebalancing steadily toward consumption from manufacturing.

It seems the surge in credit is not helping…

NBS says in statement that China’s economy still faces uncertainties. Sheng says economic situation generally stable in Jan.-Sept.

China’s economy remained stable in the third quarter, all but ensuring the government’s full-year growth target will be hit and paving the way for a policy switch toward reining in financial risks.

Bloomberg’s Chief Asia Economics Correspondent Enda Curran notes:

These numbers put to bed any talk of a Chinese hard landing in 2016. Anything can happen in the final quarter, of course, but it’s hard to see the narrative shifting too much as we head into a year of political change.

The bigger issue now is whether the authorities have the confidence to take on the really thorny issues around paring back debt and leverage. That very much remains to be seen.

Top three challenges in the coming months: containing the property surge, paring back debt and, let’s not forget, keeping a lid on capital outflows.

If the Fed ever does get round to hiking and the dollar resumes its rally, that will put downward pressure on the yuan and test the resolve of SAFE to defend it.

* * *

The reaction to the data – for now – is a rebound weaker in the Yuan (marginal) and a tick or two in USDJPY and US equity futures. Stephen Innes, a Singapore-based senior trader at foreign exchange company OANDA, said:

“There was a collective sigh of relief with the key GDP print coming in on the government target.

As the dust settles with the retail sales print looking rather bouncy, the China economy as a whole appears to be in better shape than some of the pessimistic analysts’ reads heading into the data. Global risk should remain supported.”

4 EUROPEAN AFFAIRS

Merkel is said to offer no back door concessions to England as the enter discussions on a BREXIT. The problem for Merkel is that Germany will be the net loser as their exports to England will falter badly especially in the light of the lower pound

(courtesy zero hedge)

Sterling Stumbles On Report Merkel Said To Shut Brexit “Back Door” Channels

Moments ago, sterling reverted to its familiar downward sliding trajectory and took a steep move lower following a Bloomberg report that German Chancellor Angela Merkel’s government is “battening down the hatches for coming Brexit talks, instructing officials to avoid any back-door contacts that could hand the U.K. an advantage”, citing people familiar with the discussions.

According to the report, Merkel’s chancellery is receiving U.K. diplomats but refusing to grant U.K. any favors in advance of the official negotiations. It adds that some government ministries are instructed to shun official contacts with U.K. counterparts that could reveal negotiating positions.

German message in private is same as in public: can’t start discussions before U.K. triggers Article 50 exit clause.

Bloomberg adds that Merkel’s core message to U.K. “has been consistent” – full participation in EU single market means accepting EU’s four freedoms: German govt spokesman Steffen Seibert last week.

GBPUSD slumped as much as 1.227 after trading above 1.23 on ongoing speculation about UK negotiations involving “hard brexit.”

END

GERMANY

Problems continue with respect to refugees from Africa:

(courtesy zero hedge)

German City Mayor Warns Government Of “Massive Crime Problems…Blacks Are In Charge Of The Town”

As German chancellor Angela Merkel begins to wake up to what her ‘open borders’ policy has unleashed on the citizenry, none other than the mayor of the popular Bavarian resort of Garmisch-Partenkirchen has penned a letterto the regional government begging them to tackle the “massive problems” posed by crime rates among refugees, while police say “blacks are in charge of the town.”

Mayor Sigrid Meier Hofer fears for “public safety and order” in the popular tourist destination and her letter, which was leaked to the Garmisch-Partenkirchen / Murnauer Tagblatt, leaves no room for speculation over the cause. It is clear and unambiguous, because it makes the volatile situation ruthlessly clear. Some call it an urgent letter, for others it is a cry for help… (as RT reports)

“There has been an increasingly deteriorating situation over the past weeks around the refugee registration center Abrams,” Meierhofer wrote.

The mayor then argued that the very future of her city could be in disarray because of the 250 migrants now living in the Abrams center. 150 of its residents are Africans, and unaccompanied young men make up 80 percent of them, while in previous years the facility mostly accommodated Syrian families.

Garmisch-Partenkirchen, a picturesque resort town in Bavaria, lies close to Germany’s highest mountain – the Zugspitze. Due to its mild winter climate, the town is also a popular holiday spot for skiing, snowboarding, and hiking, having some of the best skiing areas in the country.

Meierhofer made it plain that she is increasingly worried about “public order and security,” while most of the Garmisch residents believe migrants are responsible for most sexual assaults and petty crime in the area.

Bans on migrants entering certain places like the town’s spa park have been imposed in the past few weeks, but “massive problems” are still there, she went on, saying “this is not to be ignored or tolerated.”

In the meantime, police say migrants brawl in the streets and vandalize public property, echoing the mayor’s words.

Thomas Holzer, deputy police chief, told Merkur that migrants are almost “in charge” of the town,adding that officers have responded to more incidents in the past six weeks in and around the Abrams center than in the past 12 months altogether.

“There are brawls, fights and property damage. The blacks occupy the best Wi-Fi spots and choose who sleeps in what room. The situation is a problem for us and causes some concern. In September, we recorded a quarter of our annual operations,” he said.

Repeat offenders have reportedly been moved from the center to other facilities in the area, but the measure did not prove efficient.

Germany sustained a massive influx of refugees last year, with approximately 900,000 people coming in. Up to 300,000 refugees are expected to arrive this year, according to Frank-Jurgen Weise, head of the country’s migration agency BAMF.

Meanwhile, German Chancellor Angela Merkel has called for a “nationwide push” to deport refugees whose asylum applications were refused, signaling a slight change in her much-criticized “open door policy.” The refugee crisis caused numerous problems both for Merkel and her conservative bloc, losing supporters to the anti-immigrant Alternative for Germany. However, some observers insist that the scale of the crisis is exaggerated by the German media. Martin Dolzer, a Left Party MP, told RT last week that one million arrivals is not a large figure for a wealthy country like Germany, which has a population of about 80 million.

“As the [West] pursues the strategy of destabilizing Libya, Mali and Somalia as well as other African and Middle Eastern countries, refugees will come,” he stressed.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia is getting ready for war: they are deploying the largest naval force since the cold war. It is heading for Syria.

(courtesy zero hedge)

Russia Is Deploying The Largest Naval Force Since The Cold War For Syria: NATO Diplomat

Just moments ago we reported that in the latest escalation involving Syria, the Russian aircraft carrier Kuznetsov was now sailing past Norway on its way to Syria, where it is expected to arrive in just under 2 weeks. As part of the carrier naval group, Russia also deployed an escort of seven other Russian ships, which we dubbed the “most powerful Russian naval task force to sail in northern Europe since 2014” according to Russia’s Nezavisimaya Gazeta daily reports.

It turns out it was more than this and as Reuters reported second ago, citing a NATO diplomat, Russia is in fact deploying the largest naval force since end of Cold War to reinforce its Syria campaign.

- SENIOR NATO DIPLOMAT SAYS RUSSIA IS DEPLOYING ALL OF NORTHERN FLEET AND PART OF BALTIC FLEET TO REINFORCE SYRIA CAMPAIGN

- DEPLOYMENT IS RUSSIA’S LARGEST NAVAL DEPLOYMENT SINCE END OF COLD WAR – NATO DIPLOMAT

- DEPLOYMENT WILL INCREASE NUMBER OF RUSSIAN FIGHTER BOMBERS IN SYRIA, MOSCOW MAY LAUNCH FINAL AIR ASSAULT ON ALEPPO IN TWO WEEKS – NATO DIPLOMAT

While there is little we can add to this that we did not just say in the previous post, we want to remind readers what the east Meditteranean looked like in the summer of 2013, when the first escalation between Russia and the US converted the sea off the Syrian coastline into a parking lot for warships.

In two weeks, it is about to get much busier.

* * *

For those who missed it, here are the highlights from our previous post on the composition of the Russian flotilla:

According to a report by the Norwegian military which released pictures taken by surveillance aircraft, we know that the Kuznetsov accompanied by a fleet of Russian warships, is currently on its way to Syria and is sailing in international waters off the coast of Norway near Trondheim. Photos of the vessels, which include the aircraft carrier Admiral Kuznetsov and the Pyotr Velikiy battle cruiser, were taken near Andoya island, in northern Norway on Monday.

As reported by Reuters , a spokesman for the Norwegian military intelligence service said the country’s armed forces frequently releases such footage, while newspaper VG quoted General Morten Haga Lunde, head of the service, as saying the eight ships involved “will probably play a role in the deciding battle for Aleppo”. According to Russia’s TASS state news agency, the aircraft carrier would carry 15 Su-33 and MIG-29K jet fighters and over 10 Ka-52K, Ka-27 and ??-31 helicopters.

The naval group which includes the carrier and its escort of seven other Russian ships, is the most powerful Russian naval task force to sail in northern Europe since 2014, Russia’s Nezavisimaya Gazeta daily reports. The carrier can carry more than 50 aircraft and its weapons systems include Granit anti-ship cruise missiles.

Next in the flotilla, in terms of firepower, is the Russian nuclear-powered battle cruiser Peter the Great.

The Kirov-class cruiser Peter the Great escorts the carrier

As BBC adds, a Norwegian Lockheed P-3 Orion reconnaissance plane, monitoring the force, photographed the ships. MiG-29 Fulcrum jets and combat helicopters were visible on the carrier’s deck.