Gold closed at $1208.50 DOWN $8.00

silver closed at $16.61: DOWN $0.15

Access market prices:

Gold: 1208.40

Silver: 16.58

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix Nov 18 (10:15 pm est last night): $ 1218.64

NY ACCESS PRICE: $1207.50 (AT THE EXACT SAME TIME)/premium $11.14

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1219.26

NY ACCESS PRICE: 1209.75 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $9.51

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Nov 18: 5:30 am est: $1206.10 (NY: same time: $1206.15 5:30AM)

London Second fix Nov 18: 10 am est: $1211.00 (NY same time: $1211.00, 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR NOVEMBER CONTRACT MONTH: 522 NOTICE(S) FOR 52,200 OZ TONNES

For silver:

NOTICES FOR NOVEMBER CONTRACT MONTH FOR SILVER: 0 NOTICE(s) OR nil OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 119 contracts UP to 173,552 with yesterday’s trading. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .867 BILLION TO BE EXACT or 124% of annual global silver production (ex Russia & ex China).

In November, in silver, 0 notice(s) filings: FOR NIL OZ

In gold, the total comex gold ROSE by 1,398 contracts DESPITE THE FALL IN THE PRICE OF GOLD ($6.90 yesterday ).The total gold OI stands at 485,381 contracts.

In gold: we had 522 notice(s) filed for 52,200 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD

Inventory rests tonight: 920.63 tonnes

.

SLV

we NO CHANGES at the SLV

THE SLV Inventory rests at: 356.253million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE by 119 contracts UP to 173,552 as price of silver FELL by $0.15 with YESTERDAY’S trading. The gold open interest ROSE by 1,398 contracts UP to 485,381 as the price of gold FELL BY $6.90 in YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 15.60 POINTS OR 0.49%/ /Hang Sang closed UP 81.33 OR 0.37%. The Nikkei closed UP 104.78 points or 0.37%/Australia’s all ordinaires CLOSED UP 0.34% /Chinese yuan (ONSHORE) closed UP at 6.8840/Oil ROSE to 45.55 dollars per barrel for WTI and 46.67 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.8927 yuan to the dollar vs 6.8840 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS DEEPLY AS MORE USA DOLLARS LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

i)The yen has the biggest plunge against the dollar in over 18 years’

( zero hedge)

ii)I have been highlighting to you the dangers of the devaluation of the yuan against the dollar. A lower yuan cheapens Chinese goods like steel etc making mfg in other sovereign jurisdictions difficult to make money as it would be part to compete. This is what we mean by spreading deflation across the globe. China today stated that it may slow down the devaluation of the yuan hoping that capital outflows subside. That may be wishful thinking

a must read…

( zero hedge)

iii)Trump beginning to look statesmanlike. Abe states that Trump is a leader Japan can trust

( zero hedge)

c) REPORT ON CHINA

( zero hedge)

ii)Home prices are still on the rise in China although sales have slowed dramatically as attempts to prick the bubble seem to be working:

( zero hedge)

4 EUROPEAN AFFAIRS

i)Volkswagen, caught in the emissions scandal is to cut 30,000 jobs worldwide or 5% of their entire force:

( zerohedge)

ii)Judy Bergmann of the Gatestone Institute comments that free speech has ended in Europe

an important read.

(courtesy Judy Bergmann)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

i)INDIA

The Indian economy is basically 90% and thus the elimination of the big notes has caused the their economy to grind to a halt with farmers not being paid. It has shaken the faith in the system and more of its citizens will turn to gold

( zero hedge)

ii) CATERPILLAR

7.OIL ISSUES

i)Oil refuses to listen to “optimistic” comments out of OPEC

( zero hedge)

ii)WTI slides after the biggest rig count rise in over 1 1/4 yrs

( zero hedge)

8.EMERGING MARKETS

none today

9.PHYSICAL STORIES

i)a HUGE PAPER from Egon Von Greyerz as he explains why the USA debt will exponentially and why we should own gold

( Egon Von Greyerz)

ii)Craziness in India; the tax man may be calling on gold jewellers as they bought prior to the elimination of the high rupee notes

( Times of India/GATA)

10.USA STORIES

i)Trump’s first victory: Ford does not move its truck production to Mexico

( zero hedge)

ii)Trump offers the post of Attorney General to Jeff Sessions and National Security advisor to Michael Flynn

( zero hedge)

iii)The background on Jeff Sessions:

( zero hedge)

iv a) Trading early this morning: a huge move to the dollar and a sell with everything else:

7:40 am

( zerohedge)

iv b)And this puts the 10 yr treasury yield rising to 2.35% along with the other maturities. The entire treasury yield curve is now lower than at any time in 2016:

( zero hedge)

iv c) End of day results showing global bonds suffering the biggest crash in over 25 years:

(courtesy zerohedge)

v)The following is extremely important as Albert Edwards previews the next Trump recession: we will have -1% yield on the 10 yr and helicopter money will be upon us

Let us head over to the comex:

The total gold comex open interest ROSE by 1,398 CONTRACTS to an OI level of 485,381 DESPITE THE FACT THAT GOLD FELL $6.90 with YESTERDAY’S trading. In the front month of November we had 1075 notices standing for a GAIN of 1016 contracts. We had 1 notice served on yesterday so we GAINED 1074 contracts or 107,400 ADDITIONAL oz will stand for delivery in November. The next contract month and the biggest of the year is December and here this month showed a decrease of 5,652 contracts down to 220,480. The December contract month is still highly elevated compared to a year ago. On Thursday Nov 19/2015 comex reading day, we had a total of 173,288 contracts standing ( a loss of 15,395 contracts from Nov 18/2015) It certainly emphasizes the huge demand for physical gold. THIS SHOULD EXPLAIN TO YOU WHY THE BANKERS ARE CONSTANTLY WHACKING OF GOLD (AND SILVER): THE HIGH OI FOR DECEMBER AND THE HIGH PROBABILITY THAT MANY WILL TAKE DELIVERY.

And now for the wild silver comex results. Total silver OI ROSE by 119 contracts from 173,433 UP TO 173,552 as the price of silver FELL BY $0.15 with yesterday’s trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540). The front month of November had an OI of 1 and thus a loss of 0 contracts. We had 0 notice(s) filed yesterday so we neither gained nor lost any contracts that will stand for delivery in this non active month of November. The next major delivery month is December and here it FELL BY 9,290 contracts DOWN to 73,349. The December contract month is also highly elevated compared to a year ago. On Nov 18/2015 reporting day, we had a level of 66,615 contracts having lost 3,706 contracts on the day).

In silver had 0 notice(s) filed for NIL oz

Eventually at the end of December 2015: 6.4512 tonnes of gold stood for delivery

Eventually at the end of December 2015: 18.84 million oz of silver stood for delivery.

VOLUMES: for the gold comex

Today the estimated volume was 272,288 contracts which is very good.

Friday’s confirmed volume was 271,869 contracts which is very good

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | NIL |

| Withdrawals from Customer Inventory in oz nil |

42,857.108 OZ

SCOTIA

MALCA

INCL 175 KILOBARS

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

NIL oz

|

| No of oz served (contracts) today |

522 notice(s)

52,200 oz

|

| No of oz to be served (notices) |

553 contracts

55,300

oz

|

| Total monthly oz gold served (contracts) so far this month |

2119 contracts

211,900 oz

6.5909 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 630,529.6 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 522 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

12,004.310 oz

CNT

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

300,042.599 oz

CNT

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(nil OZ)

|

| No of oz to be served (notices) |

0 contracts

(nil oz)

|

| Total monthly oz silver served (contracts) | 465 contracts (2,325,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,520,202.7 oz |

end

At 3:30 pm, we receive the COT report which gives us position levels of our major players

WHAT!!!

Let us first head over to the gold COT:

In one word: the bankers are criminals

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 245,750 | 68,090 | 69,056 | 115,191 | 315,157 | 429,997 | 452,303 |

| Change from Prior Reporting Period | ||||||

| -44,110 | -4,532 | -3,357 | 276 | -45,344 | -47,191 | -53,233 |

| Traders | ||||||

| 154 | 99 | 88 | 52 | 50 | 253 | 196 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 49,240 | 26,934 | 479,237 | ||||

| -1,775 | 4,267 | -48,966 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, November 15, 2016 | |||||

Our large specs:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 85,575 | 22,969 | 10,612 | 51,359 | 129,880 | |

| -3,785 | -1,122 | -6,570 | -2,502 | -6,242 | |

| Traders | |||||

| 91 | 50 | 42 | 37 | 37 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 174,831 | Long | Short | |

| 27,285 | 11,370 | 147,546 | 163,461 | ||

| -577 | 500 | -13,434 | -12,857 | -13,934 | |

| non reportable positions | Positions as of: | 154 | 110 | ||

| Tuesday, November 15, 2016 | |||||

end

NPV for Sprott and Central Fund of Canada

END

Major gold/silver stories for FRIDAY

Early morning gold TRADING

Gold Sell Off On Fed Noise – “Interesting Times” To “Support Gold”

Gold Sell Off On Fed Noise – “Interesting Times” To “Support Gold”

Gold prices in dollar terms came under renewed pressure today testing strong support at the $1,200/oz level. Gold dropped another 1% to near a 6 month low and is set for a second week of falls after the dollar soared again after Federal Reserve Chairwoman Janet Yellen suggested a U.S. interest-rate hike could come “relatively soon.”

Source: New York Federal Reserve for Fed Funds Rate, LBMA.org.uk for Gold (PM fix)

Yellen’s prepared comments to U.S. lawmakers yesterday sent gold in dollar terms to its lowest finish since June 2, at $1,216.90 an ounce. It is worth noting that gold’s weakness this week is very much a case of gold prices in dollar terms. Gold in euros has risen from €1,130/oz to €1,137/oz and is essentially flat in sterling pound terms. Gold has risen in Swiss francs, Japanese yen and Australian dollar terms.

Yellen did little to dispel expectations of an interest-rate hike as early as December. The prospect of higher interest rates is considered by less informed market participants to be negative for gold, ignoring the fact that gold prices tend to rise when interest rates rise as was seen in the 1970s and again from June 2003 to June 2007 when interest rates rose from 1% to 5.25% and gold rose from $346 to $651 per ounce (see table above).

Gold is vulnerable when there are positive real interest rates and we are a long way from that now. Indeed, gold tends to be vulnerable towards the end of an interest rate tightening cycle – not at the beginning.

As ever, it is best to ignore both the “all powerful” Fed noise and indeed the market noise regarding rising interest rates being negative for gold. This is clearly wrong as evidenced in the data. It is also the case that the interest rate-hike expectations of just 25 basis points from record lows were already reflected in the market prior to this week.

It is prudent to ignore the incorrect narrative and consensus of gold in much of the “echo chamber” of market “experts”. The experts and “the market” have got most big calls – such as Brexit and Trump – very wrong in recent times.

As we told Marketwatch“gold will likely need a few days to base prior to moving higher again” given “the speed and scale of the recent sell off”:

“The election of Trump has not radically changed the positive fundamentals in the gold market – quite the opposite.

The risk of a Fed rate increase next month likely contributed to the fall and the dollar’s strength. We believe that should the Fed rise rates even 25 points, it will lead to risk aversion and falls in risk assets. This and the very uncertain state of the world – economically and geo-politically – bodes well for gold in 2017.

We are living in ‘interesting times’ and these interesting times should support gold.”

As long as central banks continue to debase their currencies by trying to inflate their way out of fragile economic growth and recessions through zero and negative interest rate policies and massive digital currency creation, gold should continue to build on the gains seen so far in 2016.

Today, interest rates remain close to zero not just in the U.S but in most major economies. There is no opportunity cost to owning the non yielding gold. Indeed, with negative interest rates in many creditor nations, gold has a higher yield then many major currencies.

Gold’s safe haven asset attributes mean that it remains a vital diversification for investors internationally today.

See 5 Key Charts Show Rising Interest Rates Good For Gold & Positives For Gold – Negative and Rising Interest Rates

Gold and Silver Bullion – News and Commentary

Gold slips on strong dollar, Fed rate hike comments (Reuters.com)

Gold set for second weekly loss on impending US rate hike (CNBC.com)

Dollar charges to 14-year high, bonds in full swing (Reuters.com)

Wall St. pulls back from record; utilities slump (Reuters.com)

Gold imports jump over 2-fold to $3.5 bn in October (MoneyControl.com)

India’s currency changes caused a gold rush last week – Washington Post (WashingtonPost.com)

Strong US dollar, a tumbling yuan – so why aren’t markets collapsing? (MoneyWeek.com)

No, inflation isn’t bad for gold – Business Insider (BusinessInsider.com)

Watching The Yuan and Gold (TFMetalsReport.com)

Operation: Shanghai Gold (UnCommonWisdomDaily.com)

Gold Prices (LBMA AM)

18 Nov: USD 1,206.10, GBP 997.11 & EUR 1,135.54 per ounce

17 Nov: USD 1,232.00, GBP 998.81 & EUR 1,148.10 per ounce

16 Nov: USD 1,225.70, GBP 998.43 & EUR 1,144.68 per ounce

15 Nov: USD 1,228.90, GBP 998.86 & EUR 1,138.70 per ounce

14 Nov: USD 1,222.60, GBP 997.80 & EUR 1,136.53 per ounce

11 Nov: USD 1,255.65, GBP 999.19 & EUR 1,154.45 per ounce

10 Nov: USD 1,280.90, GBP 1,034.07 & EUR 1,175.48 per ounce

09 Nov: USD 1,304.55, GBP 1,050.42 & EUR 1,176.84 per ounce

Silver Prices (LBMA)

18 Nov: USD 16.51, GBP 13.30 & EUR 15.54 per ounce

17 Nov: USD 17.04, GBP 13.65 & EUR 15.87 per ounce

16 Nov: USD 16.95, GBP 13.64 & EUR 15.85 per ounce

15 Nov: USD 17.00, GBP 13.68 & EUR 15.80 per ounce

14 Nov: USD 17.20, GBP 13.73 & EUR 15.95 per ounce

11 Nov: USD 18.59, GBP 14.73 & EUR 17.09 per ounce

10 Nov: USD 18.75, GBP 15.11 & EUR 17.20 per ounce

09 Nov: USD 18.81, GBP 15.12 & EUR 16.96 per ounce

Recent Market Updates

– Islamic Gold – Vital New Dynamic In Physical Gold Market

– Peak Gold Globally – “Bullish For Gold”

– Gold Price Should Go Higher On Global Risks and Trump – Capital Economics

– President Trump – Why Market Loves Him and Experts Wrong

– ‘Helicopter Money President’ Trump To Create Inflation and Gold Will Rise

– Central Bank Gold Demand continues in Q3

– Trump Victory Sends Gold Surging 5%

– An uncertain election outcome looks good for gold

– Ignore past elections, this one’s too uncertain

– Gold may be the only winner in US elections

– The London Gold Market – ripe for take-over by China?

– Diwali, Gold and India – Is Love Affair Over?

– Silver Krugerrands By South African Mint Coming Soon – Massive Clearance Sale on Gold Krugerrands

end

a HUGE PAPER from Egon Von Greyerz as he explains why the USA debt will exponentially and why we should own gold

(courtesy Egon Von Greyerz)

Trump Will Grow US Debt Exponentially

Trump Will Grow US Debt Exponentially

By Egon von Greyerz

There is a total misunderstanding of the role of gold and why it is so critical to own physical gold. Gold should not be bought or sold based on rumours or events. In connection with the US election, gold moved for totally the wrong reasons.

The whole Western world had forecast a Clinton victory. The Western media, which does no analysis but only reports what they are fed, spent no time trying to understand what the mood of the people was. It was exactly the same with Brexit. The elite in London, New York and the big metropolitan areas has totally different objectives to ordinary people.

Change in public mood

The trend change in public reaction, which we are seeing now, is not just a temporary phenomenon. Ordinary people are tired of a small elite of bankers, industrialists and politicians helping themselves to unlimited power and wealth whilst normal people are just getting poorer with lower incomes and more debt. And it is the masses which ultimately are responsible for repaying debt which is increasing exponentially in most countries. They will of course not repay the debt because they can’t. Instead, they will suffer immeasurably when global debt of around $250 trillion implodes leading to a severe depression. The gap between the rich and the poor in the West is wider than ever. In the US, the top 0.1% have 22% of total wealth. US top professionals have had an increase in real pay of 51% since 1973 whilst normal workers have seen a reduction of 4.6%. This is a very dangerous trend and when the economic downturn comes, it is likely to lead to violent protests and social unrest.

The Trump win was totally unexpected in the US as well as in other countries. Most politicians in Europe and around the world have ridiculed Trump and assumed that he would never be elected. They all certainly must eat humble pie now.

Investors must ignore paper gold volatility

Coming back to gold, we saw the most incredible volatility during last week. As the Trump victory became clear, gold went from $1,270 to $1,335 in under 4 hours’ overnight trading. Then massive selling of gold futures pushed the price down to $1,270 where it started before election. On Friday last week it was pushed down further to $1,225 which is $110 from the euphoric election peak. Initially, heavy paper speculative buying of gold took place around the world but very little serious physical buying. Some gold experts predicted that gold would go up by at least $100 if Trump won. Well, it did go up $65 but then declined over $100 from there. A dealer in London ran out of physical stock due to panic retail buying. But when the stock markets turned around from down 4-5% to up, the paper longs in gold were liquidated and speculative funds flowed into stock markets instead. Two years of gold production was traded after the election – all in the paper market.

As usual when gold is dumped in the futures market there is little selling of physical. Thus, the paper price of gold is totally false and in no way reflects what is happening in the physical market. It is likely that commercial gold buyers, who are already long, will add to positions at these suppressed levels. The paper market has 100-300 oz of paper gold for every 1 oz of physical gold. When the commercials add to positions at these artificially low levels, there is likely to be a major short squeeze.

Gold investors should totally ignore these short term moves as well as any news or events that temporarily move gold. Sadly, many investors buy gold when it goes up and sell it when it goes down. This behaviour shows a total ignorance of the role of gold and why it is so important to hold physical gold. Because gold is not an investment and should definitely not be seen as a speculative commodity. But futures traders and the bullion banks have no interest in gold for wealth protection purposes. For them it is just a commodity traded in the paper market with no intention of ever taking delivery.

Obama achieved in 8 years what took the US more than 200 years

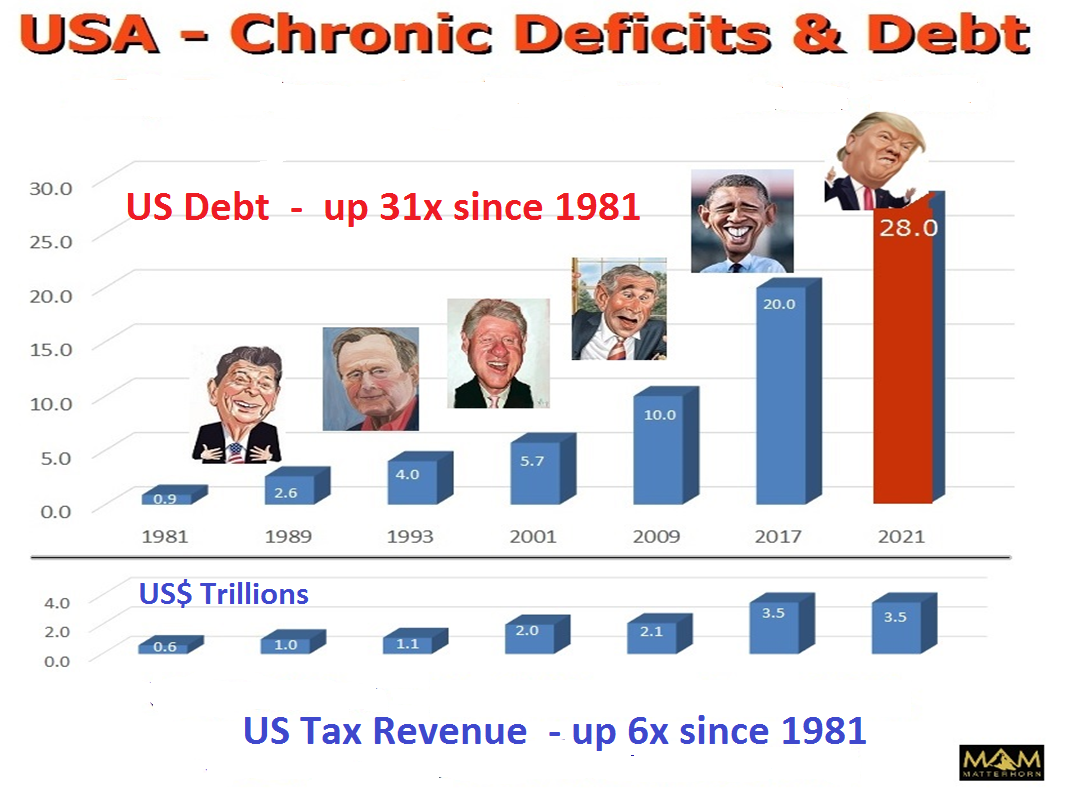

When gold moves strongly based on events, the move is seldom sustained. Those moves are mostly speculative and in the paper market. Sustained moves in gold are due to the debasement of paper money and nothing else. Since the creation of the Fed in 1913, all major currencies have declined 97-99% against gold. The US has not had a real budget surplus since 1960 so the trend is very clear and unlikely to be reversed any time soon. Since 1971 when Nixon abolished the gold backing of the dollar US debt has grown by an average of 9% per year. This means that US federal debt has doubled every eight years. And Obama is no exception. He duly complied with the trend of exponential debt increases and doubled US debt from $10 trillion to $20 trillion. It took the US 232 years to go from zero debt to $10 trillion and Obama managed to double it in just 8 short years. What an achievement!

Neither Clinton nor Trump had any intention of breaking the trend of massive debt expansion. Trump’s proposed tax reductions and major infrastructure investments will add over $5 trillion to the debt. But with this expansive policy, there is absolutely no reason why debt in the next four years will grow by less than the 9% annual average. This would take the US debt to at least $28 trillion by 2021.

But it is likely to get a lot worse. Rising interest rates, higher unemployment, stress in the debt markets and major problems in the global financial system are likely to lead to substantially higher debt as well as massive money printing.

The 35 year interest rate cycle has turned up

Long term US interest rates turned up earlier this year with 10 year Treasury yield up 63% from 1.4% to 2.28%. The 35 year rate cycle has now turned and rates are likely to go back to at least the 16% we saw in 1980 but probably a lot higher as the biggest bond bubble in history bursts. Due to the massive size of this bubble on a global scale, the increase in rates could happen very quickly. This will not just affect debt markets and the ability of governments to pay the interest but also the derivatives market. The $1.5 quadrillion of global derivatives are extremely sensitive to interest rate increases and that market will not survive much higher interest rates.

And if we look around the world, the risks are unprecedented. Japan is totally bankrupt; China has a major debt problem and the European banking system is unlikely to survive in its present form. Also, what started with Brexit is likely to continue in many European countries. Just like in the US, many Europeans are tired of an elite in Brussels ruling over 500 million people with little understanding of the resentment that this unaccountable and unelected elite is causing. The Italian election is next in December and then we have France and Germany in 2017. The breakup of the EU and the end of the Euro is just a matter of time and it could happen a lot faster than anyone expects.

Trump will not reverse chronic trend of deficits and debts

With all these problems around the world, Trump will have major difficulties reversing the trend of debts, deficits and no real growth of the US economy. Global trade is already declining and is likely to deteriorate substantially in the next few years. With both global and US problems of unparalleled proportions, it is not the best time to become president of the biggest and most indebted economy in the world. Clearly, Trump is determined to succeed but running an insolvent economy in a virtually bankrupt world will be a lot harder than building a property empire. But he has made it clear that he is hell-bent on expanding the US economy at all costs. The problem is that he will probably spend more money than anyone can imagine. But sadly, he will be pushing on a string since borrowing and printing money can never repair an economy which is fatally broken.

Reasons for holding gold more compelling than ever

As the world enters a period with risk exponentially greater than in 2006, the reasons for holding physical gold as insurance and wealth protection are more compelling than ever. The continued debasement of the currencies will guarantee a higher gold price. During Obama’s eight years, gold went up by 36% only whilst debt doubled and Trump is likely to grow debt exponentially. In addition, the failure of the paper gold market could happen at any time. When this happens there will be no physical gold available at any price until there is equilibrium in the physical market. At what price that will take place is impossible to forecast but it is certain to be multiples of the current price.

Egon von Greyerz

Founder and Managing Partner

Matterhorn Asset Management AG

matterhorn.gold

goldswitzerland.com

end

Craziness in India; the tax man may be calling on gold jewellers as they bought prior to the elimination of the high rupee notes

(courtesy Times of India/GATA)

India’s income tax men may come calling on gold buyers

Submitted by cpowell on Fri, 2016-11-18 13:11. Section: Daily Dispatches

By Ram Sahgal

The Times of India, Mumbai

Friday, November 18, 2016

MUMBAI — The taxman may knock on your door if you bought gold immediately before or after high denomination currency notes were withdrawn — even if you paid for the precious metal by cheque or credit card.

Excise authorities have issued notices to 600 jewellers to give details of stocks and sales for each day from Nov 7, a day before the announcement, to Nov 10, the India Bullion & Jewellers Association told The Times. This might be one of the reasons to have caused jewellery and bullion demand to fall sharply in the days after the notices were issued last Friday.

… For the remainder of the report:

http://economictimes.indiatimes.com/markets/stocks/news/-income-tax-men-..

end

Newmont opens a new gold mine in Suriname. This mine is seen helping this struggling economy

(Reuters/GATA)

Newmont gold mine opens in Suriname, seen boosting struggling economy

Submitted by cpowell on Fri, 2016-11-18 13:15. Section: Daily Dispatches

By Ank Kuipers

Reuters

Thursday, November 17, 2016

MERIAN MINE, Suriname — Suriname President Desi Bouterse and Newmont Mining Corp Chief Executive Gary Goldberg inaugurated Thursday the open-pit Merian gold mine, which is expected to give a boost to the small, economically struggling South American country.

The mine has gold reserves of about 5.1 million ounces and its annual production is expected to average between 400,000 and 500,000 ounces during the first five full years of operation. Suriname’s state-owned oil company, Staatsolie, has a 25 percent stake in the mine.

“Never before did our country have the courage to participate as an equal partner in such a mining venture,” Bouterse told hundreds of guests and mine employees at the opening ceremony. …

… For the remainder of the report:

http://www.reuters.com/article/us-suriname-mining-newmont-idUSKBN13D08Z

end

We have been highlighting to you the extreme physical gold buying coming from Asia. We also pointed out that gold in London is in backwardation and also premiums are occurring in India and of course in Shanghai which I report to you on a daily basis

a must read…

(courtesy Dave Kranzler/IRD)

Physical Gold Buying Soars In Asia

Gold was pushing $1230/oz overnight, as the methodical take-down of gold and silver in the NYC and London paper markets has triggered an avalanche of demand for physical gold in the eastern hemisphere.

Last night ex-duty import premiums in India were $14 over spot gold. In Shanghai the premium to world gold was $9.76. Delivery volume into the Shanghai Gold Exchange rocketed to an extraordinary 86.55 tonnes (it was 35.9 tonnes on Wednesday). The open interest on the SGE was 807 tonnes. To one observer’s recollection, John Brimelow of John Brimelow’s Gold Jottings, this is the first time the open interest has been over 800 tonnes.

In Viet Nam the premium paid by the public was $90 over world gold. The spread has been wider over the last 15 years, but not much and only during times when there’s been high “backwardation” between the physical delivery bullion markets in the east vs. the fraudulent paper gold markets in London and NYC.

To reinforce this nebulous idea of gold flowing from west to east, and unusually high amount of gold was shipped out of the Comex kilo bar vaults yesterday. 320,434 ozs left the Comex. Over 12,000 kilobars have left JP Morgan’s kilobar vault account in the last two days. This is being attributed as evidence of Asia’s voracious demand right now, as NY and London – when those two conduits actually clear real metal – trade 400oz LBMA grade bars whereas Asia prefers kilobars.

The price of gold is being attacked right now in a manner that is quite reminiscent of the way it was attacked in the summer of 2008, right before the global financial markets collapsed, led by the fall of Lehman.

Something really ugly is coming toward the global economic and financial system. The dollar index soared from 72 to 86 between June 2008 and October 2008, while gold and silver were systematically taken a lot lower. We know how that played.

Similarly, the dollar has gone parabolic in the last week without any visible news or events that would have triggered this move. Too be sure, if Trump implements his borrow and spend program for infrastructure projects, the Fed will have to print a lot of money to monetize the avalanche of Treasury debt issuance, given that the rest of the world is now dumping their Treasuries.

Both of those factors should be dollar-bearish and gold-bullish. In good time that’s how this will play out.

In the latest episode of the Shadow of Truth, we discuss the extraordinary “backwardation” that has developed in the price of gold between the west and the east. We also discuss evidence of the ongoing collapse in the U.S. economy.

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.8840(HUGE DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN WIDENS TO 6.8927 / Shanghai bourse CLOSED DOWN 15.60 POINTS OR 0.49% / HANG SANG CLOSED UP 81.33 OR 0.37%

2. Nikkei closed UP 104.78 points or 0.59% /USA: YEN RISES TO 110.29

3. Europe stocks opened ALL IN THE RED ( /USA dollar index FLAT AT 100.95/Euro UP to 1.0625

3b Japan 10 year bond yield: RISES TO +.04%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.65/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 45.55 and Brent:46.67

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS TO +.275%

3j Greek 10 year bond yield FALLS to : 7.14%

3k Gold at $1211.10/silver $16.60(7:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 12/100 in roubles/dollar) 64.76-

3m oil into the 45 dollar handle for WTI and 46 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a HUGE DEVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.29 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.007 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0710 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.275%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.296% early this morning. Thirty year rate at 3.000% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Euro In Historic Slide As Dollar Surge, Bond Rout Continues

It has been more of the same this morning as the dollar extended its advance on the still undeteremined Trump reflationary policy measures after Yellen signaled an interest-rate hike could be imminent, while bond yields around the globe rose again, metals declined, European stocks advanced and futures were modestly in the red just shy of all time highs.

A quick recap of what Yellen said: she reinforced the message that the Fed was close to raising rates, noting that the case for hiking ‘relatively soon’ would continue to strengthen as long as incoming data held strong. She also signalled the need for the FOMC to avoid delaying rate increases for too long, as “it could end up having to tighten policy relatively abruptly” in the future if the economy began to overheat. Yellen also quelled some fears that the pace of rate hikes would speed up in the future by noting that the FOMC expected that the economy would warrant only “gradual increases” in rates, reasoning that monetary policy was only moderately accommodative at the moment and the risk of “falling behind the curve” in the near future was limited. Yellen also noted her intention to serve out her full four-year term as Fed Chair – thus ending speculation that she might resign following Trump’s criticism of her policies during the former’s presidential campaign. There was some political tension in her remarks though as she defended financial regulations that President elect Trump has sought to partially reverse.

She also cautioned against Congress providing the economy with too much of a budgetary boost and suggested that they should target any stimulus towards the long run productivity of the economy. All in all markets have taken her testimony as signalling a near certain rate hike at the December meeting, with such a scenario now priced in at 96% on Bloomberg (vs. 94% yesterday).

As a result of Yellen’s hawkishness, overnight the dollar DXY index rose as high as 101.43, a new 13 year high, sending the offshore Yuan to record lows above 6.90, and unleashing a Yen selling frenzy, before moderating some of its gains after the European open. The Bloomberg Dollar Spot Index climbed 0.4 percent to trade at its highest level since February. The yen retreated 0.4 percent.

“Right now it is a dollar-dominated story,” Philip Borkin, a senior economist in Auckland at ANZ Bank New Zealand Ltd., said in a client note. “But beyond a Fed rate hike next month, many questions remain over the path of policy going forward – for both fiscal and monetary.”

Japan’s Nikkei 225 Stock Average entered a bull market after it extended its rally from a June low to more than 20 percent after the S&P 500 Index came within four points of a record on Thursday. Equities in Europe rose for a second day. The greenback’s gain weighed on oil, gold and copper, with the industrial metal set for its first weekly slide in four weeks. Global bonds headed for their steepest two-week loss in at least 26 years.

As we reported yesterday, the EUR was about to make a dubious historic record, as it fell for the 10th consecutive day.

It has never done so before, and the last time the European currency declined for 9 straight sessions was just days before the Lehman collapse.

The latest driver of USD strength was Janet Yellen, who In her first public statement since the U.S. election told lawmakers that the Fed is close to hiking rates. The comments torpedoed Treasuries, while American financial stocks pushed their rally since Donald Trump’s presidential victory back above 10 percent Thursday. Speculation that he will boost fiscal stimulus continues to lift industries that are perceived to benefit from economic growth.

“The fact that she didn’t push back against market expectations for a December hike is perhaps the most significant takeaway,” said Jack Spitz, managing director for foreign exchange at National Bank of Canada in Toronto, referring to Fed Chair Yellen. “The dollar is higher as a result.”

In early trading, European equities rose with the Stoxx Europe 600 Index adding 0.3%, heading for a 1.2% weekly advance. Industrial shares contributed the most to the measure’s Friday rally, while mining companies fell with commodities prices. Shippers and carmakers led gains on the Topix index in Tokyo, which rose 0.4 percent. The Nikkei 225 closed at its highest level since January. Telecommunications and consumer stocks drove Australia’s S&P/ASX 200 Index up 0.4 percent, while South Korea’s Kospi index slipped 0.3 percent. Hong Kong’s Hang Seng China Enterprises Index advanced 0.2 percent, while the Shanghai Composite Index dropped 0.5 percent on the mainland.

S&P 500 futures slipped 0.1 percent to at 2,181, following a 0.5% advance in the S&P on Thursday. Bank shares led the index to its highest level since Aug. 15, when the gauge reached an all-time high. “Markets have arrived at a point where they need to weigh the risks of being caught out by the potential stimulatory impacts of the Trump administration’s policies, against the risk of being caught by those policies not being implemented,” Ric Spooner, chief market analyst at CMC Markets, told Bloomberg by email.

Away from the frenzied dollar rally an the equity reflation trade, the biggest concern remained global bonds and at what point will the rising yields put a damped on the risk-on euphoria. As noted earlier, the bond selloff deepened Friday, with yields on U.S., European and Asia-Pacific sovereign debt increasing. The Bloomberg Barclays Global Aggregate Index fell 4 percent from Friday Nov. 4 through Thursday. It’s the biggest two-week rout in the data, which go back to 1990. Yields on Australia’s 10-year notes jumped 15 basis points to 2.72 percent. Yields on similar-maturity Italian debt rose 9 basis points, while those on Treasuries increased two basis points to 2.33 percent, extending the eight basis-point jump last session.

At some point very soon, the financial tightening as a result of surging yields and USD will become self-defeating and lead to a revulsion from risk assets, however for now the markets continue to ignore this flashing red warning.

* * *

Bulletin Headline Summary from RanSquawk:

- The stronger USD has taken its toll on mining, energies and utilities sectors this morning, leading the main indices lower

- A morning of consolidation in the FX markets, but not without a further test higher in the key USD rates where spot JPY has tested 111.00 but held back modestly as yet

- Looking ahead, highlights include Canadian CPI, comments from Fed’s Bullard, Kaplan and George and BoE’s Broadbent

Market Snapshot

- S&P 500 futures down 0.2% to 2181

- Stoxx 600 down 0.3% to 340

- FTSE 100 down 0.6% to 6752

- DAX down 0.3% to 10658

- German 10Yr yield up 3bps to 0.31%

- Italian 10Yr yield up 3bps to 2.12%

- Spanish 10Yr yield up 6bps to 1.65%

- S&P GSCI Index down 0.6% to 355.7

- MSCI Asia Pacific down 0.6% to 134

- Nikkei 225 up 0.6% to 17967

- Hang Seng up 0.4% to 22344

- Shanghai Composite down 0.5% to 3193

- S&P/ASX 200 up 0.4% to 5359

- US 10-yr yield up 2bps to 2.32%

- Dollar Index up 0.28% to 101.17

- WTI Crude futures down 1.1% to $44.91

- Brent Futures down 0.8% to $46.12

- Gold spot down 1% to $1,205

- Silver spot down 1% to $16.51

Top Headline News

- VW to Cut 30,000 Jobs in Landmark $3.9 Billion Savings Pact: Savings deal aimed at boosting the VW brand’s margin to 4%

- Bank Bosses Soften Tone on Brexit as May Extends Olive Branch: Finance executives say London’s status not under threat

- Tesla Shareholders Overwhelmingly Approve SolarCity Deal: SolarCity holders approved deal earlier

- HRG, Owner of Spectrum Brands, Considers a Sale as CEO Exits: Owner of consumer brands, Fidelity insurance seeks advisers

- Copper Miner Says Price Rally May Stall as World Glut Lasts: Antofagasta sees global surplus of up to 400,000 tons in ‘17

- Yum! Brands to Buy Back Up to $2b in Additional Shares

* * *

Looking at regional markets, we start in Asia, where stocks traded mostly higher following the firm lead from Wall St where the post-election rally resumed and financials led as a December rate hike looks all but certain. Nikkei 225 (+0.9%) surged to bull-market territory and 10-month highs after briefly breaking above the 18,000 level with exporters benefitting as USD/JPY printed 5-month highs, while ASX 200 (+0.4%) was also in the green, although gains were capped as USD strength weighed on commodities. In China, Hang Seng (+0.2%) and Shanghai Comp (-0.5%) traded indecisive despite a firm liquidity injection by the PBoC, as participants also digested rampant house prices which could attract funds away from stocks as well as dampen hopes for looser policy. 10yr JGBs were weaker alongside increased demand for riskier assets, with the curve steepening amid underperformance in the super-long end in which Japanese 40yr yields rose to an 8-month high.

Top Asian News

- Nikkei 225 Enters Bull Market After Rising 20% From June Low: Topix index advances for seventh day as yen extends declines

- Malaysia Central Bank Says It’s Intervening in Currency Market: Fears of capital controls are “baseless,” Assistant Governor Adnan Zaylani says

- China Home-Price Growth Slows as Property Curbs Start to Bite: Prices in red-hot cities stabilized after curbs

- Trump Win Gives Kuroda Breathing Room, Ex-BOJ Executive Says: BOJ can remain on hold unless yen strengthens past 100/USD, Hideo Hayakawa says

- Thomas Cook India Sees Holiday Booking Delays on Demonetization: Indian economy to “undergo adjustment” on govt’s demonetization decision, Chairman Madhavan Menon says.

In Europe, the stronger USD has taken its toll on mining, energies and utilities sectors this morning, leading the main indices lower (EUROSTOXX -0.5%), with the mining and energy heavy FSTE 100 down by 0.6%. In company specific news, Volkswagen (+1.7%) are trading higher after the German carmaker announced that it will make job cuts, with labour unions agreeing to 30,000 job cuts by 2021. In Fixed income markets supply is short today, but prices have risen after gapping lower on the open due to the general adverse risk sentiment in markets today. We also saw the UK/Eurozone 10 spread widen to a post Brexit high of 117 bps. Elsewhere in Italy, 10 year bonds are on course for the worst month since 2012 as the run up to referendum intensifies.

Top European News

- LafargeHolcim Cuts 2018 Profit Targets; Raises Dividend: Cement maker also plans to buy back 1 billion francs of stock

- Draghi Says Recovery Still Highly Reliant on ECB Policy Support: ECB sees no consistent strengthening of inflation pressures

- SNB Able to Deliver Further Rate Cut If Needed, Maechler Says: Swiss National Bank Board Member Andrea Maechler speaks at event in Geneva

In currencies, Bloomberg’s dollar gauge climbed for a third session. Odds on the Fed raising the benchmark rate are now at 96 percent, up from 80 percent a week ago and less than 65 percent a month ago, according to futures trading tracked by Bloomberg. The yen weakened 0.4 percent to 110.62 per dollar and is on track for its second weekly retreat of more than 3 percent. The won slipped 0.6 percent. Malaysia’s ringgit retreated 0.5 percent as the nation’s central bank said it’s intervening in the currency market. China’s yuan slid to its weakest level since June 2008.

In commodities, gold tumbled to the lowest in more than five months, dropping as much as 1.1 percent to $1,202.96 an ounce. The precious metal has plunged as investors digested the implications of Trump’s policies, which may boost the economy and lead to higher borrowing costs. Rising bond yields and a stronger dollar are also weighing on gold, which doesn’t pay interest.Oil futures declined 1.6 percent in New York, trimming the first weekly advance since late October, despite a spike in OPEC related headlines. Nickel fell 1.4 percent in London to lead declines by industrial metals. Copper retreated 0.8 percent, heading for a weekly loss after entering a bull market last week.

It’s a quiet end to the week today in terms of data: we have the Conference Board Leading Index for October (+0.1% mom expected; +0.2% previous) and the Kansas Fed manufacturing survey for November due, while Baker Hughes at 1pm will reveal if the US shale industry continues to ramp up production.

DB’s Jim Reid concludes the overnight wrap

If you’re looking for the first flapping of a butterfly’s wings that might eventually cause a tidal wave further down the road perhaps the most interesting development before Monday is the French Les Républicains party and its centre-right allies primaries on Sunday. The general consensus is that the winner will end up being the candidate up against Marine Le Pen in the second round run off for the Presidential elections in the middle of next year. For sometime now Juppe has experienced a far bigger lead against Le Pen than Sarkozy when pollsters have pitted them against each other. Complicating matters is another ex-PM Fillon who has seen his support increase. If no candidate gets 50% the run off will take place next Sunday. So one to watch in these political times.

Yesterday we were all waiting for Yellen’s testimony on the economic outlook delivered before the Joint Economic Committee. She reinforced the message that the Fed was close to raising rates, noting that the case for hiking ‘relatively soon’ would continue to strengthen as long as incoming data held strong. She also signalled the need for the FOMC to avoid delaying rate increases for too long, as “it could end up having to tighten policy relatively abruptly” in the future if the economy began to overheat. Yellen also quelled some fears that the pace of rate hikes would speed up in the future by noting that the FOMC expected that the economy would warrant only “gradual increases” in rates, reasoning that monetary policy was only moderately accommodative at the moment and the risk of “falling behind the curve” in the near future was limited. Yellen also noted her intention to serve out her full four-year term as Fed Chair – thus ending speculation that she might resign following Trump’s criticism of her policies during the former’s presidential campaign. There was some political tension in her remarks though as she defended financial regulations that President elect Trump has sought to partially reverse. She also cautioned against Congress providing the economy with too much of a budgetary boost and suggested that they should target any stimulus towards the long run productivity of the economy. All in all markets have taken her testimony as signalling a near certain rate hike at the December meeting, with such a scenario now priced in at 96% on Bloomberg (vs. 94% yesterday).

Global stock markets responded well to Yellen’s testimony and erased yesterday’s dips as both the STOXX 600 (+0.63%), FTSE (+0.67%) and the S&P500 (+0.47%) all ticked up. The STOXX had a particularly strong day given that every underlying sector ended the day in the green. After a rough showing the previous day, banks (+1.25%) were the top performing sector for the S&P and are now up nearly 10% since the US election results.

At the other end of the risk spectrum we saw US treasuries yields climb across the entire maturity spectrum, with the 2Y and 10Y increasing by +3bps and +7bps respectively, and the 30Y once again heading up just above 3% (+8bps). German 10Y yields ticked down by about -2bps while UK 10Y yields increased by nearly +3bps. Italy, Spain and Portugal 10 year yields rose 5-6bps.

Over in currency markets we saw the US dollar continue its strong rally as it rose against major peers (dollar index +0.6% and highest since February). Oil slipped slightly after being up over 2% earlier in the session with the dollar rally seemingly offsetting optimism from Saudi’s minister for Energy and Industry that OPEC will find a satisfactory agreement to cut output.

Overnight the dollar continues to edge higher with equities in Asia mostly stronger with the exception of China (Shanghai Comp -0.25%). The Nikkei is up +0.78% as we type. 10 year JGBs are 3bps higher at 0.03% as the market digests the consequence of yesterday’s BoJ operations shorter down the curve where they managed to intervene without actually buying any paper. It feels like this story will run and run with the BoJ at some point having to actually spend some money to anchor yields where they want them.

Taking a look now at some of the data out yesterday, we saw Q3 employment numbers out of France where the headline unemployment rate ticked up to 10% and disappointed against expectations of no change (9.9% expected; 9.9% previous). Turning to the UK we saw the October retail sales numbers surprise significantly on the upside by growing at +2.0% mom (vs. +0.4% expected; +0.1% previous) and +7.6% YoY (vs. +5.4% expected; +4.0% previous). These were the highest growth figures seen since July. While this is generally a noisy series, the numbers do still signal resiliency in consumer spending. We also received the final Eurozone October CPI numbers which were unrevised from the flash estimate (+0.5% YoY).

Over in the US, we saw strong data points across inflation, labor market and housing indicators that all seemed to enhance the case for a rate hike in December. Headline CPI numbers ticked up in October and printed in line with expectations at +0.4% mom (+0.3% previous). Labor markets also remained resilient as initial jobless claims (235k actual vs. 257k expected; 254k previous) fell to their lowest levels in over 40years, while continuing claims fell to 1977k (vs. 2030k expected; 2043k previous) and are at their lowest levels since 2000. Homebuilding also picked up as Housing starts reached a nine year high (1323k vs. 1156k expected; 1054k previous) and building permits (1229k vs. 1193 expected; 1225k previous) increased in October to beat expectations. The only weak data point came in the form of the Philadelphia Fed PMI for November which came in at 7.6 (vs. 7.8 expected; 9.7 previous).

It’s a quiet end to the week today in terms of data. In Europe the only data of note is the October PPI report out of Germany (+0.2% mom expected; -0.2% previous) where wholesale inflation is expected to head back into positive territory but remain fairly subdued. In the US we have the Conference Board Leading Index for October (+0.1% mom expected; +0.2% previous) and the Kansas Fed manufacturing survey for November due.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 15.60 POINTS OR 0.49%/ /Hang Sang closed UP 81.33 OR 0.37%. The Nikkei closed UP 104.78 points or 0.37%/Australia’s all ordinaires CLOSED UP 0.34% /Chinese yuan (ONSHORE) closed UP at 6.8840/Oil ROSE to 45.55 dollars per barrel for WTI and 46.67 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.8927 yuan to the dollar vs 6.8840 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS DEEPLY AS MORE USA DOLLARS LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

3a)THAILAND/SOUTH KOREA/:

none today

b) REPORT ON JAPAN

The yen has the biggest plunge against the dollar in over 18 years’

(courtesy zero hedge)

Japanese Yen Set For Biggest Plunge Versus Dollar In 18 Years

With the US dollar soaring to its highest since 2003, unprecedented moves in the Euro, Yen, and Yuan are now daily headine-makers. Overnight saw USDJPY near 111.00 (before rolling over a little this morning), pushing the pair to its best 2 week gain since 1988… and its second best 2-week gain since currencies floated.

As Reuters reports, further underpinning the dollar was a speech by Federal Reserve Chair Janet Yellen, who on Thursday provided a signal that U.S. interest rates would rise next month, in line with most market participants’ expectations.

“What we’re looking at is a broad shift of investment back to the U.S.,” said Richard Cochinos, Citi’s head of G10 currency strategy in London.

“There are expectations for tax cuts next year – which were part of the Trump campaign’s promises – and then there’s also the idea of what type of fiscal boost are you going to have. That’s what’s driving asset prices – it’s people’s expectations for the fiscal impulse next year,” he said.

Cochinos added that political and economic worries in Europe, Britain and Japan were keeping investors away from those currencies, providing the dollar with another boost.

“Dead cat bounce”?

Trump beginning to look statesmanlike. Abe states that Trump is a leader Japan can trust

(courtesy zero hedge)

Abe Says Trump “Is A Leader We Can Trust”, Gives Him A Golf Club As Present

Following Trump’s first official meeting with a foreign leader on Thursday night (one which took place in Trump’s apartment at the Trump Tower), Japanese Prime Minister Shinzo Abe said Trump was a trustworthy leader in comments after his first meeting with the U.S. President-elect, whose statements on trade and security have sparked concern in Japan. Abe told reporters that he had frank discussions in a “warm atmosphere” at Trump Tower, and said he explained his views on a range of issues, but declined to comment on the substance of the talks in a meeting that lasted more than an hour.

“He made time for me, even though he is busy with personnel matters,” Abe said after the meeting. “I am convinced that President-elect Trump is a leader we can trust.” The pair agreed to meet again for broader and deeper talks when their schedules allow, he said.

It was not always so amicable: while campaigning, Trump vowed to drop a Pacific trade deal which shifts the balance of trade power in the Pacific to China, and accused Japan of manipulating its currency. Trump also threatened to pull U.S. troops out of the country unless it pays more for their upkeep, and has suggested Japan might have to develop its own nuclear weapons.

Quoted by Bloomberg, a condescending Robert Dujarric, director of the Institute of Contemporary Asian Studies at Temple University Japan campus in Tokyo said that “it’s good that Abe saw Trump. Trump has little foreign policy knowledge and it’s worth trying to educate him. The approach may fail but it’s worth a try.”

As Bloomberg notes, Japan is America’s second-largest trading partner behind China, with two-way commerce reaching almost $200 billion last year. Japanese businesses provide upward of 800,000 jobs in America. Relations are also prominent in the military realm where Japan, whose own military is restricted by a pacifist constitution drafted by the U.S. after World War II, relies heavily on America’s troops and nuclear weapons for deterrence against growing threats from North Korea and an increasingly powerful China. About 50,000 U.S. military personnel are stationed in Japan.

Trump’s daughter Ivanka, rumored to be groomed as a potential ambassador to Tokyo, was at her father’s residence to greet Abe.

Also present was retired Lieutenant General Michael Flynn, a key military surrogate throughout his campaign, whom Trump offered the job of national security adviser. According to Bloomberg, on a visit to Tokyo last month Flynn said Japan and the U.S. should discuss the cost-sharing arrangement for American troops in Japan. Defense Minister Tomomi Inada said last week that the country makes sufficient contributions to the upkeep of U.S. forces in Japan.

Meanwhile, to cement the goodwill between Japan and the new administration, Abe presented the real estate mogul with a golf club (Japanese media said it was a driver). Trump gave Abe a golf shirt in return. The gift is symbolic: in 1957, then Prime Minister Nobusuke Kishi, Abe’s grandfather and political role model, played a round of golf with President Dwight D. Eisenhower on a course in Maryland outside of the U.S. capital. News reports described the game as a “triumph for diplomacy.”

Nobusuke Kishi and Dwight D. Eisenhower play golf in 1957

The pair are known to be avid golfers. Abe spends his summers playing at courses close to his vacation home near Tokyo. Trump is affiliated with 17 golf properties worldwide, with the golf division of Trump Organization Inc. owning and managing most of the courses. It’s not the first time Abe has used golf diplomacy. On a trip to Vietnam in 2006, during his first spell as prime minister, Abe gave then President George W. Bush a photograph of their grandfathers playing in Maryland. He also gave President Barack Obama a putter made by a Japanese manufacturer

end

c) Report on CHINA

(courtesy zero hedge)

Yuan Smashes Through 6.90… What Next?

While the Renminbi basket (Chinese currency basket relative to biggest world trade partners’ currencies) has been ‘stable’ for almost 5 months, the catchdown in the Yuan’s purchasing power against the US Dollar is accelerating rapidly. Busting through 6.90/$ in early Asian trading, the last time offshore Yuan cratered this quickly, stocks plunged in January. The question is – how much further can the Yuan fall before the Trump bump gets damaged?

Judging by the transition to weakness against the Dollar… 6.90 may be nothing as 7.20 looks likely…

Notice how the PBOC rotates between USD-prone moves and non-USD-prone.

Luckily – this time is different…

For now.

end

I have been highlighting to you the dangers of the devaluation of the yuan against the dollar. A lower yuan cheapens Chinese goods like steel etc making mfg in other sovereign jurisdictions difficult to make money as it would be part to compete. This is what we mean by spreading deflation across the globe. China today stated that it may slow down the devaluation of the yuan hoping that capital outflows subside. That may be wishful thinking

a must read…

(courtesy zero hedge)

China Warns It Is Ready To Slow Yuan Plunge On Capital Outflow Fears

It was just one year ago when the biggest worry for the market – which culminated with a near 10% S&P correction in in early 2016 – was the daily plunge in the Yuan driven by the surging dollar, which in turn prompted China to engage in an unprecedented reserve liquidation (in which it sold both government bonds and equities), leading to a daily selloff in risky assets on days when the Yuan was fixed lower.

Fast forward a year later, when the US Dollar has blown through last year’s highs and is now at levels not seen since 2003, the Yuan is trading at record lows, just shy of 7.00, and yet stocks stubbornly ignore the one catalyst that led to so much headache for the bulls one year ago.

In his daily note, RBC’s cross-asset strategist Charlie McElligott points out that while the market may be oblivious, what is taking place in China is something to be concerned about:

ONE IMPORTANT TACTICAL MACRO POINT WITH REGARDS TO THE NEAR-TERM DIRECTION OF USTs / GLOBAL LONG-END: The yuan ‘slow bleed’ devaluation by the PBoC versus the USD seen since the start of October has without question been tied to at least some of the weakness in the US long-end, as the central bank sells USTs to try and mitigate the depreciation of the yuan against the SDR basket—see here:

One notable distinction from last year is that while bond yields would slide on days when the PBOC intervened to stabilize the currency by selling TSYs, this time around the selling of both assets is taking place concurrently – as shown in the chart above – which may suggest that China’s capital outflow pressure is far greater than what the PBOC would be willing to admit.

It may also explain why the market has been oblivious to the collapse in the Yuan:so far China has kept a very low profile when it comes to its market response to the aggressive devaluation of its currency. But that may be about to change.

As Reuters writes overnight, “Chinese policymakers have been unfazed by the yuan’s recent slide, but are ready to slow its descent for fear of fanning capital flight if the currency falls too quickly through the psychologically important 7-per-dollar level, policy advisers said.”

The inertness of China’s central bank stems from the fact that “Chinese policymakers believe the decline in the yuan since October reflects market trends, especially of late when most currencies have fallen in the face of a resurgent U.S. dollar.”

A policy advisor said that “the central bank is following the trend as the dollar is rising. It’s not necessary for it to resist market forces.”

Not necessary for now.

Ironically, just as Trump has been a blessing in disguise for Europe and Japan, both of whose currencies have plunged against the dollar in the past week on expectations of Trumpflation, so China has also benefited from the weaker currency: “appropriate yuan depreciation will be good for stabilizing market expectations and the economy, as long as there is no sharp, run-away depreciation.”

All of that is about to change however, if the dollar continues its relentless push higher, in the process tripping the 7.00 stops in the Yuan:

Beijing’s biggest concern is that a sharp fall in the yuan will trigger the sort of capital flight that followed August’s surprise devaluation of the currency, which sparked fears the health of the economy was worse than Beijing had let on. China’s currency reserves slumped by more than $400 billion by the end of January as Chinese moved cash overseas.

Outflows from the $3 trillion-plus reserves, by far the world’s largest, have since continued at a much more subdued pace but the yuan’s decline in recent weeks has raised some concerns that capital flight could pick up again if the yuan slides too fast.

Asked about when the Yuan may cross the psychological barrier, a PBOC advisor told Reuters that “I don’t think the breaking of 7 is imminent. We may have to wait until next year.” Actually, at this rate, “breaking” of 7 may happen as soon as next week, to which he adds :”If the pace of depreciation is too fast, if it hit 7 before the end of this year, the central bank will control it.”

And that’s when the liquidation of Chinese USD-denominated reserves begins in earnest, among all those other measures the PBOC implemented a year ago when the market was far less sanguine about the Chinese devaluation:

The policy insiders said the central bank was likely to intervene in currency markets and enforce capital controls to slow the rate of decline in the yuan.

As we expected, the intervention has already started:

traders said large Chinese state banks had offered dollars in the domestic currency market on Thursday in an apparent effort to slow down the depreciation of the yuan. They said there had been no sign of state dollar selling in previous sessions.

Another way of saying “offering dollars” is selling US assets.

And then there are other threats, like how China will respond to the foreign policy programs soon to be adopted by the president-elect who had made trade with China, and the imposition of tariffs, one of the biggest policy points in his presidential campaign.

Concerns about a sharp slowdown in China’s economy have eased to be replaced by worries that Beijing could be heading into a trade war with the United States if Trump follows through on his campaign rhetoric. Trump lambasted China throughout the election, drumming up headlines with pledges to slap 45 percent tariffs on imported Chinese goods and to label the country a currency manipulator.

China was regularly criticized by the United States and some other western governments who argued it used a cheap currency to boost exports. But that criticism has died down in recent years as economic growth slowed and as the government sought to shift away from a reliance on exports and more towards consumption.

“Imposing tariffs on China would do more harm than good for the United States, including its employment, and it has to consider that China could counter with its own measures,” said a commerce ministry researcher.

For now China, like the market, is hoping that Trump won’t rock the boat…

“I don’t think the exchange rate will become an imminent problem. The yuan is depreciating but won’t depreciate too much and many people believe the dollar could fall if Trump takes some radical measures.”

Chinese President Xi Jinping told Trump that cooperation was the only choice for relations between the world’s two largest economies, with Trump saying the two had established a “clear sense of mutual respect”.

Assuming no major ructions from a Trump presidency, some government economists expect the yuan to fall to 7.2 per dollar by the end of 2017, which would imply a drop of 4.2 percent from the current level.

… which, however, may prove to be idealistic. Ultimately, the question will be at what point do China’s residents and savers start pulling out their funds and transferring them offshore – as they did last year – to avoid further loss in purchasing power. 7.00 on the Yuan sounds as good a point to “call it” as any, which means. Which incidentally is dangerously close from the latest print in the USDCNH, now trading just above 6.90.

Another week at the current pace of devaluation, or just a 1-2% increase in the DXY, should do it.

END

Home prices are still on the rise in China although sales have slowed dramatically as attempts to prick the bubble seem to be working:

(courtesy zero hedge)

China Home Price Inflation Hits New Record High, Despite Curbs To Cool Overheating Market

On one hand, China’s recently implemented home-buying curbs to cool the runaway property market worked in October, when following a slump in property sales volume new-home prices gained last month in 62 of the 70 cities tracked by the government, declining from the 63 recorded in September, the National Bureau of Statistics said Friday. Prices dropped in seven cities, compared with six a month earlier.

According to Goldman’s population-weighted calculations, house price inflation decelerated across all tiered cities: In tier-1 cities, October price growth was 0.9% month-over-month after seasonal adjustment, down visibly from the 3.1% month-over-month growth in September. In tier-2 cities, housing price growth was 1.5% month-over-month in October, vs. 2.7% in September. Price growth was also lower in tier-3 and tier-4 cities.

“The property market in China’s first and second-tier cities apparently has cooled in October, while it remained relatively stable in third-tier cities,” Liu Jianwei, a statistician from China’s NBS said in a note accompanying the data.

Housing price growth slowed in October on the back of tightening measures

Source: GS

“Buyers and developers are now taking to the sidelines, creating a standoff in the market,” said Xia Dan, a Shanghai-based analyst at Bank of Communications Co.

As confirmation that its bubble-busting policies are working, China’s statistics bureau said that home prices in first-tier and red-hot second-tier cities “apparently cooled” in the second half of October after those regions announced fine-tuned curbs. Monthly growth slowed in most of China’s first- and second-tier cities. Five cities, from the capital Beijing to southern port city Xiamen, snapped a streak of price gains. New-home prices in Shenzhen, the nation’s hottest property market earlier this year, fell 0.5 percent in October from September, the first decline since October 2014 suggesting restrictions in the hottest markets to curb speculative

buying are starting to bite. Prices in Beijing fell 0.4% in the second half of October, and declined 0.1 percent in Shanghai.

* * *

On the other hand, Beijing’s curbs have a long way to go as October home prices grew at the fastest rate since record-keeping began in 2011, despite a significant slump in property sales volume as local governments stepped up measures to cool skyrocketing prices, and as more discriminating buyers appear to have stepped back from the recent buying frenzy. Despite the fewer transactions, the average property price change in October was up a whopping 12.7% YoY, another record high, following September’s 11.7% surge from the prior year.

Year-over-year basis price growth continued to increase to new all-time highs.

Source: GS

As we noted in the late summer, in an attempt to cool China’s second housing bubble in three years, the housing ministry cracked down on rogue players, started investigating developers and agents for alleged false advertising, urging probes on “illegal” sales and cracking down on investment by online finance and peer-to-peer lenders.

A cooling of the property market may provide some relief to policy makers, who are seeking to avoid a housing bubble without denting economic growth.

It may have its work cut out for it however: in a nation in which capital spending and building empty cities has been synonymous with growth for a decade, even amid the curbs in major cities, property development investment rose 13% from a year earlier in October, the most since at least 2015, Bloomberg calculated. New housing starts, an early indicator of real estate investment, gained 20% from a year earlier, the biggest increase since April.

As Liu Feifan, analyst at Guotai Junan Securities, confirmed, the drop in sales volumes in cities that have imposed restrictions was “a lot milder” than he expected, adding that the 10% drop in transactions was below his prediction of more than 30%, suggesting that the euphoria mentality is still present.

“But momentum is going to slow further, otherwise authorities will step up curbs,” Liu said.

The good news is that just as the housing bubble is bursting, China has not a new commodity market euphoria to look forward to, but a fledging stock market bubble to boot, just like in 2015. Because in China, with its roughly $30 trillion in deposits, bubbles never go away, they just roll over from one asset class to another.

end

4 EUROPEAN AFFAIRS

Volkswagen, caught in the emissions scandal is to cut 30,000 jobs worldwide or 5% of their entire force:

(courtesy zerohedge)

Volkswagen To Cut 30,000 Jobs, 5% Of Workforce

Following a tumultuous year of declining sales as a result of its emissions-cheating scandal, today Volkswagen agreed to cut 30,000 jobs at the core VW, roughly 5% of its global salesforce of 624,000. After months of intense talks, labor and management agreed on a package to balance cost-cutting with investment as the auto industry shifts away from traditional combustion engines and adapts to car-sharing services and self-driving technologies.

The job cuts will come through attrition in the form of early retirement and not replacing workers that leave; the company vowed to refrain from forced layoffs until 2025. The savings comprise 3 billion euros at its German factories and another 700 million euros abroad. Argentina and Brazil will be hit hardest by the staff reduction outside Germany, with Volkswagen’s personnel chief Karlheinz Blessing describing the Brazil cuts as “brutal.”

“This is a big step forward, maybe the biggest in the company’s history,” VW brand chief Herbert Diess said at a press conference in Wolfsburg. “All manufacturers must rebuild themselves because of the imminent changes for the industry. We need to brace for the storm.”

The deal is expected to result in €3.7 billion in expense reductions as the company tries to streamline operations and cut costs. However the compromise leaves the carmaker’s profitability still lagging rivals: the plan is expected to lift the VW brand’s operating margin to 4% by 2020, from 2% this year, but still below rival European carmakers such as Renault and Peugeot Citroen which are targeting an operating margin of 6 percent in 2021.

Volkswagen, Europe’s largest automaker is trying to increase savings at its biggest business in its home base of Germany, where its costs are high. Reuters notes that VOW must also find billions of euros to pay fines and settlements stemming from its diesel emissions cheating scandal as well as fund a strategic shift toward electric and self-drive cars. Volkswagen’s labor leaders said management had agreed to avoid forced redundancies in Germany until 2025 a step which clears the path to cutting 23,000 jobs via buyouts, early retirements and by reducing part-time staff.

Jobs will also be cut in North America, Brazil and Argentina, VW said. Around 114,000 employees work for VW brand in Germany.

Labor leaders agreed to the cuts in exchange for a management pledge to create new 9,000 new jobs in the area of electric cars, mainly at factories in Germany. As all mass layoff announcements, this one too was initially cheered by markets, which sent the company’s shares more than 2% higher to the top of the blue-chip DAX index in early Frankfurt trading, and reducing the drop since the scandal broke in September 2015 to 27 percent. However, later in the day, the gain was all but wiped out.

Hedge fund TCI, which has been critical of Volkswagen management, said it looked like a good deal all round provided it could be made to stick.