Gold at (1::30 am est) $1178.20 down $10.90

silver at $16.46: down 8 cents

Access market prices:

Gold: 1283.50

Silver: 16.55

Let us begin with my work in progress:

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

THURSDAY GOLD FIXES:

Shanghai morning fix Nov 24 (10:15 pm est last night): $ 1215.21

NY ACCESS PRICE: $1186.00 (AT THE EXACT SAME TIME)/premium $29.21

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1212.41

NY ACCESS PRICE: 1186.20 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $26.21

China rejects NY pricing of gold!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Nov 24: 5:30 am est: $1187.25 (NY: same time: $1187.00 5:30AM)

London Second fix Nov 24: 10 am est: $11.85.35 (NY same time: $1187.10, 10 AM)

FRIDAY gold fix Shanghai

Shanghai morning fix Nov 25 (10:15 pm est last night): $ 1202.15

NY ACCESS PRICE: $1177.30 (AT THE EXACT SAME TIME)/premium $24.85

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1200.91

NY ACCESS PRICE: 1187.40 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $13.51

China rejects NY pricing of gold stating that it is a fraud

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Nov 25: 5:30 am est: $1187.50 (NY: same time: $1188.00 5:30AM)

London Second fix Nov 25: 10 am est: $xxxx (NY same time: $1186.30 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR NOVEMBER CONTRACT MONTH: 0 NOTICE(S) FOR NIL OZ TONNES

For silver:

NOTICES FOR NOVEMBER CONTRACT MONTH FOR SILVER: 0 NOTICE(s) OR nil OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today (Preliminary data)

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 2108 contracts DOWN to 167,583 with YESTERDAY’S trading. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .837 BILLION TO BE EXACT or 120% of annual global silver production (ex Russia & ex China).

In November, in silver, 0 notice(s) filings: FOR NIL OZ

In gold, the total comex gold FELL by 37,676 contracts WITH THE HUGE FALL IN THE PRICE OF GOLD ($21.90 with yesterday’s trading ).The total gold OI stands at 423,386 contracts. The gold specs have been blown out of the water again

In gold: we had 0 notice(s) filed for NIL oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD: (to be reported on Sat/Sun)

We had another huge change in tonnes of gold at the GLD, a withdrawal of 19.87 tonnes of gold

Inventory rests tonight: 885.04 tonnes

.

SLV (to be reported Sat/Sun)

we HAD A CHANGE at the SLV/. A WITHDRAWAL OF 949,000 OZ

THE SLV Inventory rests at: 346.150 million oz

Now my work in progress:

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver FELL by 2108 contracts DOWN to 167,583 as price of silver FELL by $0.24 with YESTERDAY’S trading. The gold open interest FELL by 37,676 contracts DOWN to 423,386 as the price of gold FELL BY $21.90 WITH YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 20.20 POINTS OR 0.62%/ /Hang Sang closed UP 114.96 OR 0.57%. The Nikkei closed UP 47.81 OR .26%/Australia’s all ordinaires CLOSED UP 0.39% /Chinese yuan (ONSHORE) closed DOWN at 6.9207/Oil FELL to 47.49 dollars per barrel for WTI and 48.45 for Brent. Stocks in Europe: ALL IN THE RED EXCEPT LONDON Offshore yuan trades 6.9485 yuan to the dollar vs 6.9207 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS DEEPLY AS MORE USA DOLLARS LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)Thursday:

China press lashes out that it is the dollar’s strength that is causing the yuan to weaken. As the yuan weakens, the globe is whacked with deflation as lower Chinese prices force other countries to lower their prices to compete. Emerging markets are now in complete turmoil

( Dan Steinbok/ChinaDaily.com)

4 EUROPEAN AFFAIRS

i)EURO

The huge drop in the value of the Euro due to dollar rising is causing huge significant risks in Europe and they warn of a abrupt market reversal

no kidding..

( zero hedge)

ii)GERMANY

This does not look good: Germany’s NordBank reports that in its shipping loan boopk almost 40% of loans are non performing:

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

TURKEY

Europe temporarily suspends Turkey’s entry into the EU due to deteriorating human rights violations. The Lira tanked to 3.42 before recovering as Erdogan raised Turkey’s overnight rates to 8.5%. The real problem here is what will Erdogan do with the 2 million refugees?

( zero hedge)

6.GLOBAL ISSUES

none today

7. OIL ISSUES

i)Now who would have thought that this could happen: in the last minute the big OPEC players demand production cuts from non OPEC: still think a deal is possible?

( zero hedge)

ii)Oil then falls as the Saudis refuse to attend a non OPEC producers meeting:

8. EMERGING MARKETS

i)INDIA

Devastation runs supreme in India as the Rupee crashes to a record low. Only 40% of old cash has been turned in with a huge 60% left to go. I would say that close to 90% of the Indian economy is cash and the removal of the big bills has already shaved 2% off of GDP. Modi also is trying to rein in citizens appetite for gold

(courtesy zero hedge

ii)And then this: India will impose a 60% tax on all deposits into banks with unaccounted money. They will also try and curb gold holdings per individual.

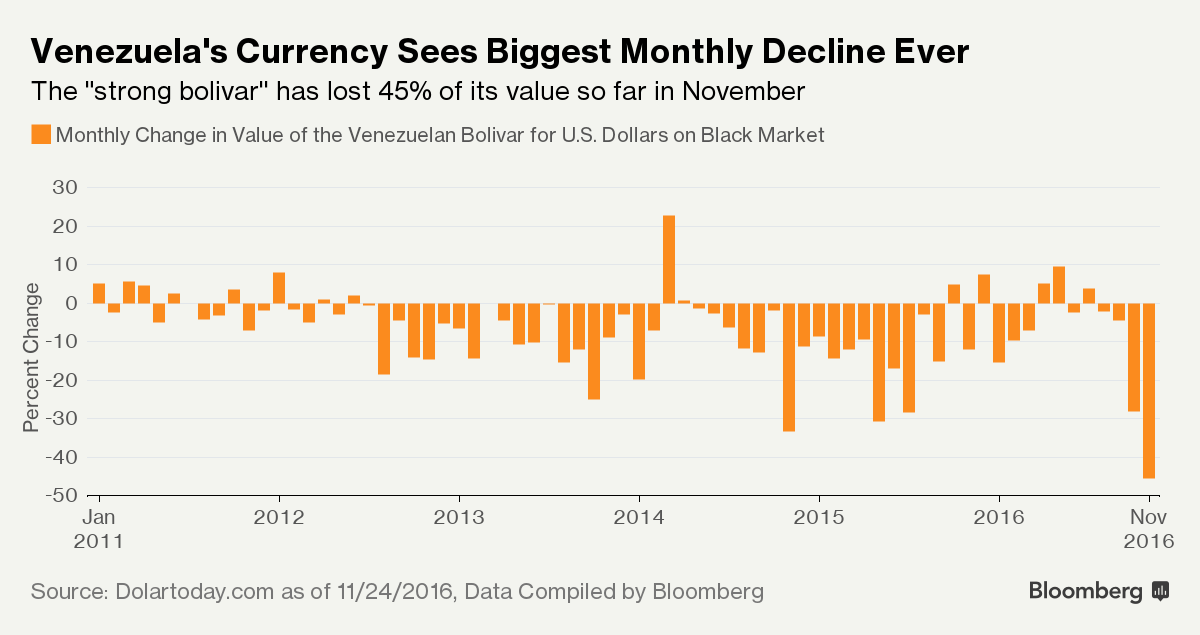

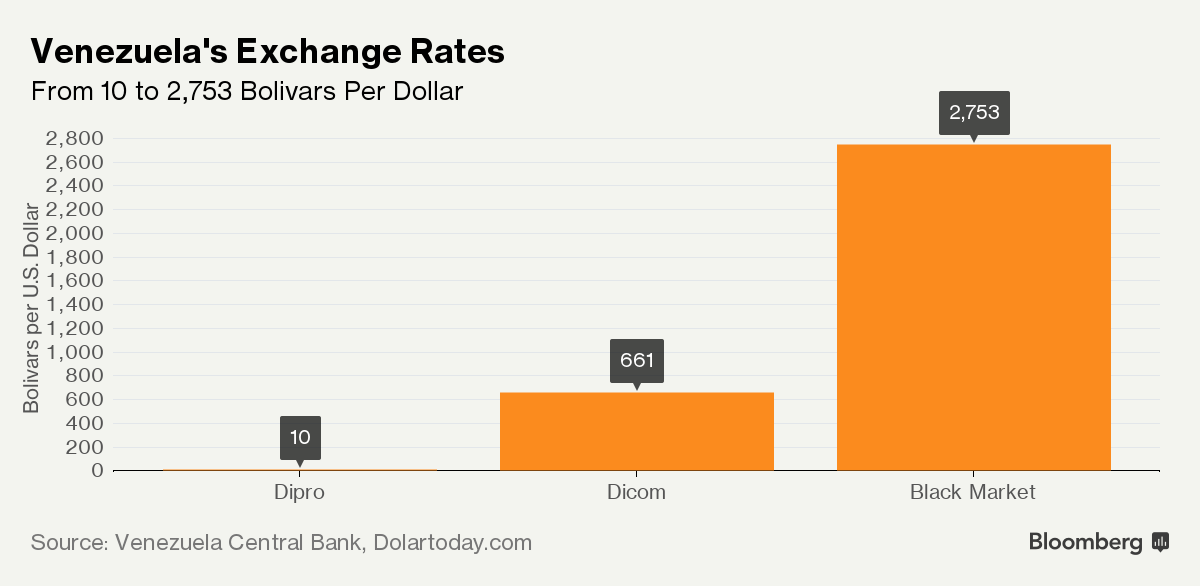

Venezuela now enters hyperinflation officially as it takes over 2700 bolivars per dollar.

(courtesy zero hedge)

iv Brazil

Brazil may get impeachment hearings in a new corruption scandal involving President Temer

(courtesy zero hedge)

9. PHYSICAL MARKETS

i)Now that the hedgies have disappeared from the silver market, it is now time for the commercials to enter the long side

( zero hedge/Dana Lyons/Tumbler)

ii)Chris Powell interviewed showing that paper gold is the elephant in the room

( Goldletter/Hodson/ChrisPowell

iii)John Hathaway discusses the Trump victory and what it will mean for gold:

( John Hathaway/GATA)

iv)A must read: Alasdair Macleod with his thoughts on the banning of high denomination notes in India and what that will do to gold in this region.

( Alasdair Macleod/)

10.USA STORIES

i)Wow!! a huge deficit of 62 billion dollars. Who would have thought that this would happen with a high dollar: poor exports, higher imports!! Wholesaler inventories contract signalling recession:

( zero hedge)

ib)The USA reports a big drop in the service sector. Remember that today the USA reported huge trade deficits and a huge drop in inventories. How could Markit report a high mfg number two days ago?

(courtesy zer0 hedge)

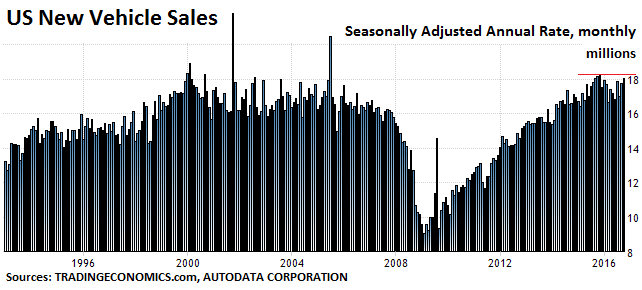

ii)The strong pillar of USA car sales is now reeling.

( Wolf Richter/WolfStreet)

iii)Michael Snyder discusses that one half the population of the world is dirt poor with the elitists trying to keep it that way

( Michael Snyder/EconomicCollapseBlog)

iv)A strong message from Michael Snyder to us all

( Michael Snyder/EconomicCollapseBlog)

v)Is my favourite politician Nigel Farage going to have a position in the Trump administration after he announces that he is moving to the USA

( zero hedge)

end

COMEX

The data this morning is preliminary. The final OI numbers will probably be lower and I will update them for you on Sat/Sunday. The amount standing is correct

Let us head over to the comex:

The total gold comex open interest FELL by 37,676 CONTRACTS to an OI level of 423,386 AS GOLD FELL $21.90 with YESTERDAY’S trading.reading on Friday will see a In the front month of November we had 221 notices standing for a GAIN of 194 contracts. We had 16 notices served YESTERDAY so we GAINED 178 GOLD CONTRACTS OR AN ADDITIONAL 17,800 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF NOVEMBER. The next contract month and the biggest of the year is December and here this month showed a DECREASE of 58,431 contracts DOWN to 106,069. The December contract month is still highly elevated compared to a year ago. On FRIDAY Nov 27/2015 comex reading day, we had a total of 24,018 contracts standing ( a loss of 36,141 contracts from Nov 25/2015. To give you more detail as to how the front month of December contracted, the final Nov 30 contract had an OI of 7,849 contracts standing or 24.41 tonnes standing. On the last day we lost 16,169 contracts. The OI for the entire complex was around 393,000 or similar to the low readings this year. It certainly emphasizes the huge demand for physical gold.We have exactly 3 more trading days left. THIS SHOULD EXPLAIN TO YOU WHY THE BANKERS ARE CONSTANTLY WHACKING OF GOLD (AND SILVER): THE HIGH OI FOR DECEMBER AND THE HIGH PROBABILITY THAT MANY WILL TAKE DELIVERY.

And now for the wild silver comex results. Total silver OI FELL by 2108 contracts from 169,661 DOWN TO 167,583 as the price of silver FELL BY $0.24 with YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540). The front month of November had an OI of 1 and thus a LOSS of 0 contracts. We had 0 notice(s) filed yesterday so we neither lost nor gained any contracts (oz) that will stand for delivery in this non active month of November. The next major delivery month is December and here it FELL BY 1983 contracts DOWN to 40,393. The December contract month is a little elevated compared to a year ago. On Nov 27/2015 reporting day, we had a level of 16,868 contracts having lost 10,053 contracts on the day. On the final day of November, we had 5,975 contracts stand for 29.875 million oz. We lost 4078 contracts on the last day prior to first day notice.

In silver had 0 notice(s) filed for NIL oz

Eventually at the end of December 2015: 6.4512 tonnes of gold stood for delivery

Eventually at the end of December 2015: 18.84 million oz of silver stood for delivery.

Note how much paper settlements occurred in December last yr and I surely doubt if we will get any!!

VOLUMES: for the gold comex

Today the estimated volume was 405,569 contracts which is HUGE.

Friday’s confirmed volume was 514,416 contracts which is huge

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil |

nil

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

32,582.430 oz

includes 1000 kilobars Scotia

also Brinks deposit

|

| No of oz served (contracts) today |

0 notice(s)

NIL oz

|

| No of oz to be served (notices) |

221 contracts

22100

oz

|

| Total monthly oz gold served (contracts) so far this month |

2671 contracts

267,100 oz

8.3079 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 633,712.5 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

507,525.390 oz

Brinks

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(nil OZ)

|

| No of oz to be served (notices) |

1 contracts

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 465 contracts (2,325,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,766,529.7 oz |

end

end

NPV for Sprott and Central Fund of Canada

will provide on Saturday/Sunday

END

Major gold/silver stories for FRIDAY

Early morning gold TRADING

Gold Down 13.5% In 13 Days – Trump Bearish For Gold?

- Gold down 13% in 13 trading days since Trump election

- Factors that have led to lower gold prices

- Trump bearish for gold in coming four years?

- ‘Trumpflation’ cometh

- Sharia gold – vaulted gold accessible to 110 million new investors

- What to do? Diversify and geometric price cost average

Donald Trump was elected President and the gold price surged 5%, over $60, from $1,271/oz to $1,336/oz. As many of us had suggested it would. And then something strange happened, something not expected by the majority of market participants – it started to fall, the dollar strengthened.

We now have a gold price that is down 13% since the US election result – from a high of $1,336/oz to a low of $1,177/oz this morning. This is a drop of 13% in just 13 trading days since the election.

Does this mean that Trump and his Presidency isn’t going to be very bullish for gold prices as so many of us predicted? Does this mean that gold is going to underperform or worse, enter a bear market in the next four years?

We don’t think so. Indeed, we see this as extremely unlikely. We outline below just some of the factors that have lead to the recent declines in the gold price, and outline why we don’t think this is a sign of things to come.

US dollar strengthens as Federal rate hike looms

For many in the gold space the miserable gold price is thanks to the expectations that Janet Yellen and co. will decide to hike rates thanks to some mixed data that suggestes a strengthening US jobs market. These were the noises emanating from the recent Federal Reserve Open Markets Committee meeting press release.

The US Dollar has rallied to its highest level since 2005 this week, largely on the back of these Fed expectations. Higher borrowing costs can hurt gold bullion as strategic buyers look at gold in the context of yields and interest payments. Although this is less the case now given ultra loose zero percent and negative interest rate monetary policies.

ETF support gone … for now

In 2016 gold demand has been supported by stellar ETF demand as, according to the World Gold Council, the high gold price in Q3 had a negative impact on gold demand, elsewhere.

For the SPDR Gold Trust and the iShares Gold Trust combined inflows are worth around $13.6 billion for this year (a record).

Both jewellery and gold bars and coin sales have reached levels this year not seen since 2009. But physical demand has not reflected such levels in Q3. After very significant demand and the price surge in Q1 and Q2, Q3 saw a reduction in demand for jewellery and coins and bars.

Whilst central banks, which have been huge buyers (and therefore supporters) in the physical gold market, have reduced gold reserve diversification to 33% of that in 2015.

“ETPs were the only bright spot during the quarter, with 146t of inflows helping to counterbalance weak demand elsewhere, notably in jewellery (-21%), bars and coins (-36%) and purchases by central banks (-51%).”

But that bright spot has started to dim since the Trump’s victory:

According to ETF.com “in the week since the election, outflows from the SPDR Gold Trust and the iShares Gold Trust totalled $1.7 billion…the aftermath of the elections has clearly dampened enthusiasm for gold among ETF investors.”

Therefore it is unsurprising that a market that has been significantly supported by one investment product is now struggling as the outflows add up.

But the ETF argument raises an interesting point

As the World Gold Council stated in their recent report, much of the activity surrounding gold purchases this year (especially in the area of ETFs) shows strategic buying rather than investment buying.

This was no more clear than on the early hours of the election night on November 9th, as Jim Rickards recently outlined,

“Gold prices surged late on Nov. 8 and into the early morning hours of Nov. 9 as a Trump victory became clear. This was exactly in line with my expectations. Based on sentiment and momentum, gold should have held those gains.

Instead, one of the largest and most visible individual gold investors, Stan Druckenmiller, decided to liquidate his entire gold position in the middle of the night. Druckenmiller told CNBC: “I sold all my gold on the night of the election… All the reasons I have owned it for the last couple of years, it seems to me they may be ending. And by the way, they’re ending globally.”

The move by Druckenmiller saw gold continue to decline in the following days thanks to a change in sentiment. Many sheep like traders adopted a ‘me too’ attitude. Momentum is a powerful thing in markets.

Do the reasons to own gold no longer exist?

In short, no.

In lengthier words, still no. One of the main reasons for the dollar strength and uptick in industrial metals is because Trump is expected to spend, spend, spend his way back to making ‘America Great Again.’ The Donald in the White House means reduced regulation, a fall in corporate taxes and trillions of dollars of fiscal stimulus.

‘Trumpflation’ cometh.

All of this without any thought to the inflationary effects.

Jim Rickards, explains:

“If the Fed accommodates the deficit with “helicopter money,” inflation will surge. If the Fed leans against the big deficits with rate hikes, this will cause a stronger dollar and lead to a global liquidity crisis in emerging markets.

If bank regulation is eased, banks can be relied upon to leverage up with risky derivatives, which will make the next financial crisis more, not less, likely. Druckenmiller’s stated reasons for selling gold are equivalent to saying, ‘I cancelled my fire insurance because now that Trump is president, we won’t have any more fires.’ Don’t count on it.”

Druckenmiller is a great investor but like the majority of investors simply does not understand gold’s role as a hedging instrument and financial insurance – either through choosing not to or through lack of knowledge.

Both Brexit and the Trump victory have wrong footed the financial markets and we are heading into unchartered territory both politically and economically. Unchartered territory means complex decisions are needed to be made by both governments and investors in order to navigate their way through over the coming years.

Uncertainty will lead to bargain hunting

A lot of uncertainty remains in both the geopolitical and economic arenas.

Conventional wisdom told us that gold would benefit from a Trump win, and in truth we haven’t seen the results of Trump win. This will play out over the next four years, and this is where we expect the precious metal to benefit.

Aside from Trump’s disastrous spending policies and strategic gold buyers dumping the metal for equities, there are some highlights to consider in the next few months.

With each Republican nomination contest we see at least one candidate mention the role of gold in the monetary system. In this recent one, we had a couple and one of them was Donald Trump.

It’s highly unlikely Trump is going to be forcing Janet Yellen to announce a return to the gold standard, but we may well see more discussion about gold’s monetary role.

In addition to Trump taking a shine to gold, the gold market is soon to see a significant increase in investors when vaulted gold coins and bars become accessible to over 110 million Muslim investors in Turkey, Pakistan, Malaysia, Indonesia, Bahrain, Qatar, Saudi Arabia and the United Arab Emirates

As we outlined last week, the Sharia Gold Standard or Islamic Gold Standard is set to be announced, this will allow Muslims around the world to invest in physical gold.

The reasons to own gold have not disappeared in the dawn-of Trump. As Rickards says:

“The reasons to own gold are insurance against extreme risk, as a hedge against inflation, and as a sound form of money in a world where central banks are losing control. All of those reasons still apply”

There are also the not inconsiderable risks posed by the Italian referendum on Sunday week, December 4th, and the French general election on April 23, 2017. Both of which have the potential to plunge the Eurozone into a new crisis – a potentially existential one.

Medium and Long Term (2017-2025) ‘MSGM’ Fundamentals

The long term case for having an allocation to precious metals is due to the still positive fundamentals:

- Macroeconomic risk is high as there is a serious risk of recessions in major industrial nations with negative data emanating from the debt laden Eurozone, Japan and China. Even the recoveries in the UK and the U.S. are tentative at best. Issues with banks, a la Lehman or Deutsche, or a major terrorist incident or another war could badly impact fragile consumer and investor sentiment.

- Systemic risk remains high as little of the problems in the banking system have been addressed. There remains the risk of another ‘Lehman Brothers’ moment or a new ‘Grexit’ moment and seizing up of the global financial system. The massive risk from the unregulated “shadow banking system” continues to be significantly underappreciated. There are many potential Lehman Brothers out there both in the Eurozone with Deutsche Bank looking very vulnerable.

- Geopolitical risk remains elevated – and Trump’s election seems likely to exacerbate these risks. This is seen in the continuing significant tensions in Lebanon, Syria etc and between Iran and Israel. There is the real risk of conflict and the consequent effect on oil prices and the global economy. While tensions with Russia may subside with the Trump election, tensions with Iran and other Muslim nations look set to worsen.Indeed Trump’s trade and economic policies have the potential to create significant tensions even with major trading partners in the EU and with China.

- Monetary risk is high as the policy response of the Federal Reserve, the ECB, the Bank of England, the BOJ and the majority of central banks to the risks mentioned above continues to be ultra-loose monetary policies, zero interest rate policies (ZIRP), negative interest rate policies (NIRP), the printing and electronic creation of a tsunami of currency and the debasement of paper and electronic currencies.Should the macroeconomic, systemic and geopolitical risks increase even further in the coming months, then the central banks’ response will likely again be more cheap money policies. This will lead to further currency debasement and there is a risk of currency wars deepening.

Given these real risks, investors should use this latest correction to diversify into physical gold.

There is a strong case for having higher allocations to physical gold today, of as much as 25% of a portfolio, given the risks above. We advise owning physical gold as gold ETFs have significant levels of legal indemnifications and various forms of force majeures that exposes investors to unnecessary risks with little recourse.

Hence the importance of physical, allocated and segregated gold“outside the banking system.”

Those seeking to allocate funds to precious metals should geometrically price cost average into position by front loading their initial allocation and allocating as much of 50% of their allocation to gold on the first transaction.

This latest bout of weakness will allow value buyers to accumulate physical on the dip.

Gold and Silver Bullion – News and Commentary

Gold hits 9-1/2-month low on firm dollar; set for third weekly loss (Reuters.com)

Gold futures fall further below $1,200 mark (MarketWatch.com)

Gold edges lower on dollar and U.S. rate prospects (Reuters.com)

Potential gold-import ban by India could be biggest bombshell since Nixon (MarketWatch.com)

Mastercard, Visa Set to Reap Spoils of India’s War on Cash (Bloomberg.com)

$6 billion ‘puke’ sends gold plunging below $1200. Source Zero Hedge

Trump’s Victory: What Does it Mean for Gold? (TocqueVille.com)

ECB Warns There Is “Significant Risk Of Abrupt Market Reversal” (ZeroHedge.com)

$6 Billion Puke Sends Gold Plunging Below $1200 As Dollar Index, Bond Yields Spike (ZeroHedge.com)

Chart of the week: “shrinkflation” hits the chocolate market (MoneyWeek.com)

Gold: valuable reserve amid unprecedented policy environment (Gold.org)

Gold Prices (LBMA AM)

25 Nov: USD 1,187.50, GBP 995.33 & EUR 1,121.83 per ounce

24 Nov: USD 1,187.25, GBP 995.36 & EUR 1,125.04 per ounce

23 Nov: USD 1,213.25, GBP 998.00 & EUR 1,143.00 per ounce

22 Nov: USD 1,217.55, GBP 997.89 & EUR 1,144.98 per ounce

21 Nov: USD 1,214.95, GBP 984.72 & EUR 1,143.39 per ounce

18 Nov: USD 1,206.10, GBP 971.15 & EUR 1,135.54 per ounce

17 Nov: USD 1,232.00, GBP 988.19 & EUR 1,148.10 per ounce

Silver Prices (LBMA)

25 Nov: USD 16.47, GBP 13.21 & EUR 15.55 per ounce

24 Nov: USD 16.31, GBP 13.09 & EUR 15.43 per ounce

23 Nov: USD 16.56, GBP 13.36 & EUR 15.59 per ounce

22 Nov: USD 16.76, GBP 13.46 & EUR 15.77 per ounce

21 Nov: USD 16.68, GBP 13.47 & EUR 15.69 per ounce

18 Nov: USD 16.51, GBP 13.30 & EUR 15.54 per ounce

17 Nov: USD 17.04, GBP 13.65 & EUR 15.87 per ounce

Recent Market Updates

– War On Cash Just Got Real – India and Citibank In Australia

– Russia Gold Buying In October Is Biggest Monthly Allocation Since 1998

– Stocks, Bonds, Pension Funds “Will Be Wiped Out…” – Rickards

– Physical Gold Is A “Long-Term Position” as “Hedge Against Governments”

– Gold Sell Off On Fed Noise – “Interesting Times” To “Support Gold”

– Islamic Gold – Vital New Dynamic In Physical Gold Market

– Peak Gold Globally – “Bullish For Gold”

– Gold Price Should Go Higher On Global Risks and Trump – Capital Economics

– President Trump – Why Market Loves Him and Experts Wrong

– ‘Helicopter Money President’ Trump To Create Inflation and Gold Will Rise

– Central Bank Gold Demand continues in Q3

– Trump Victory Sends Gold Surging 5%

– An uncertain election outcome looks good for gold

END

Now that the hedgies have disappeared from the silver market, it is now time for the commercials to enter the long side

(courtesy zero hedge/Dana Lyons/Tumbler)

Silver Enters Bear Market As Hedgies Flee

After tagging $19 the night of Trump’s victory, Silver prices have tumbled 15% (the biggest drop since Summer 2013’s taper tantrum). However, as large speculators dumped their longs en masse, this week also marked another milestone as Silver drops 24% from its post-Brexit peak (above $21) and entered a bear market once again.

As the dollar surges, Bloomberg reports that gold and silver holdings in exchange-traded funds are set for the biggest monthly drop in more than three years.

“Everyone is looking for a December rate hike, and that’s what’s been priced into gold and silver at the moment,” Tom Kendall, head of precious metals strategy at ICBC Standard Bank Plc, said by phone from London.

“The dollar remains a key driver.”

And, just as we have seen in gold futures, hedge fund speculative longs in silver are also decling rapidly…

And this selling pressure has slammed Silver to six-month lows (down 24% from Brexit highs in June)…

But, as Dana Lyons’ Tumblr explains, Silver prices are testing a confluence of potential support levels.

We often get questions about our technical analysis on specific assets or securities, especially as it pertains to potential support or resistance levels on the chart. We don’t post many of those types of charts anymore but we present one today in the chart of the popular iShares Silver Trust, ticker, SLV. The impetus was partially because of the amount of attention on PM’s, but primarily due to a potential inflection point on the chart.

Everyone asks “when is XYZ going to bottom”? There is no way to ever know for sure. The best thing you can do is identify the most likely points of support in order to put the best odds of success on your side. And the best setups are always when multiple key potential support levels line up in the same vicinity. Such a setup may be present now in the chart of SLV, in our view.

So what are the potential support levels?:

- The 61.8% Fibonacci Retracement of the November-August Rally ~15.62

- The 500-Day Simple Moving Average ~15.64

- The June 7 closing price (15.60) from which SLV gapped up, launching it on its final run to 19.71

As the chart shows, SLV is testing this level today. In fact, the low of the day was exactly 15.60.

So will this 15.60 level hold? Obviously nobody knows for sure. At least there are multiple key levels of potential support there, however. That puts decent odds of success with the silver bulls – as well as giving them a level with which to play off of. If SLV remains above there, it can bounce. If it closes below there without an immediate reversal, perhaps there is more downside to come for silver prices.

How far will SLV bounce if it holds? Obviously, we can’t know that either. There appears to be considerable potential resistance near 16.80 and just above 18.00, if the SLV does bounce. So, that would be about 7-15% of upside – without even breaking the post-summer intermediate-term downtrend. It would take a lot more strength to convince us that the post-2015 uptrend is resuming. So, even holding this level doesn’t mean it’s up, up and away again for silver.

For now, precious metals fans will have to be satisfied with, “Hi Ho Silver, A-Bounce!”

* * *

More from Dana Lyons, JLFMI and My401kPro.

end

Chris Powell interviewed showing that paper gold is the elephant in the room

(courtesy Goldletter/Hodson/ChrisPowell

Paper gold is the elephant in the room

Submitted by cpowell on Wed, 2016-11-23 15:54. Section: Daily Dispatches

Gold Newsletter’s Fergus Hodgson interviews GATA Secretary/Treasurer Chris Powell.

* * *

By Fergus Hodgson

Gold Newsletter, Metairie, Louisiana

Wednesday, November 23, 2016

Many people seek gold as a safeguard against inflation of fiat currencies, but they often forget how fiat currencies came to be in the first place.

This blind spot has permitted the very same deceit to play out in our time — but without detection in the major financial press.

The blind spot is fractional reserves. It is the holding of precious metals — the hard money — below the number of claims of customers. It was the precursor to modern fiat currencies, which now only have shadow “reserves” of more cash. Similarly, conventional banks now hold cash as “reserves” for checkbook and digital money.

Who is the dummy in this situation? As Chris Powell of the Gold Anti-Trust Action Committee says, “If you don’t know who … you’re the dummy.”

Powell, an editor and journalist by trade, began GATA in 1999 and spoke at this year’s New Orleans Investment Conference. He is also a longtime Gold Newsletter subscriber, and we sat down with him to get a better sense for the prevalence of fractional reserves. He laid waste to the corruption of central banks and to cowardly members of his profession when it comes to reporting on manipulation of the gold market.

“Most gold buyers, for investment purposes, never take possession of the metal,” he explains. “That allows central banks and investment banks … to operate a fractional-reserve gold banking system. They sell certificates against gold that doesn’t exist, very confident that they’ll never be called on it.”

The scope of this is difficult to determine, and Powell cited one estimate with a ratio as high as 92-to-1 of paper gold to real gold. While that may not be the case, “even the gold merchants at the bullion banks would acknowledge that there’s a lot more certificate gold circulating than there is real metal backing it.” A “very conservative” estimate is that less than half the nominal gold has real backing.

There are other ways to inflate supply, often on a short-term basis, including gold leasing, but a more important question is how the everyday investor can avoid being the owner of a dud title. Those in the know will often say “if you can’t hold it, you don’t own it.” This, however, raises concerns over transportation and liquidity, and that’s why people often prefer to hold gold in secure vaults.

Powell likewise believes that one need not rely solely on physical possession. He recommends institutions “outside the banking system,” such as Gold Money, Anthem Vault, or Bullion Vault, since they maintain their own vaults, and the gold is transferable. His warning is against commercial or investment banks, where you are “very vulnerable.”

What compounds the problem is that it is a no-go topic in major outlets such as The Wall Street Journal and the Financial Times. This absence of reporting has gone on for so long now that a widespread awakening would be a “deadly danger to the whole investment system. … If this issue were ever examined critically, you’d realize that the values that we are living with in the economy every day are totally false.”

This overlooking of fractional reserves also hints at collusion between major outlets and their key advertisers and partners. Governments, Powell claims, are striving to keep this a secret, as are “big financial houses.” Reporters need to show some spine and report the evidence presented to them. Many are aware of the problem yet remain silent.

“They know there would be hell to pay. In the Wall Street Journal on every other page in the A section every day there will be an ad from JPMorganChase, Goldman Sachs, Citigroup, or any of those investment banks that may be involved in the gold market. … The financial press is largely controlled by the financial industry.”

The big losers are regular investors, but you need not be one of them. As microeconomics tells us, though, prices send signals and allocate resources. That is why on a broader level market manipulation creates perverse incentives and rewards unproductive behavior.

“The destruction of the market economy is going on all around” and Powell believes “all of civilization is the loser. … We’re also losing our democracy. A very small elite is benefiting from this — that is central banks and those who live off the patronage of central banks.”

To listen to Gold Newsletter’s podcast with Powell, please visit:

http://goldnewsletter.com/podcast/chris-powell-paper-gold-is-the-elephan…

end

John Hathaway discusses the Trump victory and what it will mean for gold:

(courtesy John Hathaway/GATA)

John Hathaway: What does Trump’s victory mean for gold?

Submitted by cpowell on Thu, 2016-11-24 17:08. Section: Daily Dispatches

12:10p ET Thursday, November 24, 2016

Dear Friend of GATA and Gold:

In his latest market letter, Tocqueville Gold Fund manager John Hathaway notes that the smashing of gold after the U.S. presidential election involved the dumping of futures contracts nominally equivalent to two years of production.

“We have observed on repeated occasions,” Hathaway writes, “that purely speculative paper transactions distort the price of real-world physical goods. In our view, price-disruptive distortions of this sort (including commodities other than gold) are enabled and encouraged by the willingness of the Chicago Mercantile Exchange to promote high-frequency trading to build profitability.”

That seems to be as close as any respectable participant in the financial markets can get to the issue of manipulation of the gold market.

Hathaway notes that the systemic risks to the world’s economy have not vanished with the election and argues that “exposure” to gold “may make more sense than ever.” His letter is headlined “Trump’s Victory: What Does it Mean for Gold?” and it’s posted at the Tocqueville internet site here:

http://tocqueville.com/insights/trumps-victory-what-does-it-mean-gold

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A must read: Alasdair Macleod with his thoughts on the banning of high denomination notes in India and what that will do to gold in this region.

(courtesy Alasdair Macleod/)

Alasdair Macleod: The economic consequences of Mr. Modi

Submitted by cpowell on Thu, 2016-11-24 18:50. Section: Daily Dispatches

1:53p ET Thursday, November 24, 2016

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod writes today that India’s repudiation of most of its outstanding paper currency will deepen distrust of that currency as well as of government generally and increase confidence in gold. Macleod’s commentary is headlined “The Economic Consequences of Mr. Modi” and it’s posted at GoldMoney here:

https://wealth.goldmoney.com/research/goldmoney-insights/the-economic-co…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.9207(BIG DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN WIDENS TO 6.9485 / Shanghai bourse CLOSED UP 20.20 POINTS OR 0.62% / HANG SANG CLOSED UP 114.96 OR 0.57%

2. Nikkei closed UP 47.81 POINTS OR .26% /USA: YEN FALLS TO 113.01

3. Europe stocks opened ALL IN THE RED EXCEPT LONDON ( /USA dollar index FALLS TO 101.45/Euro UP to 1.0589

3b Japan 10 year bond yield: RISES +.042%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.01/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 47.49 and Brent:48.45

3f Gold UP /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS TO +.234%

3j Greek 10 year bond yield RISES to : 6.94%

3k Gold at $1187.70/silver $16.47(7:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 10/100 in roubles/dollar) 64.60-

3m oil into the 47 dollar handle for WTI and 48 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a HUGE DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.01 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0137 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0734 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.234%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.382% early this morning. Thirty year rate at 3.03% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Relentless Dollar Surge Continues: Asian Currencies Plunge To 7 Year Lows, Hitting Emerging Markets

The regional FX plunge will likely deter regional central banks from easing monetary policies as the prospects of higher U.S. rates spurred capital outflows according to Toru Nishihama, an emerging-market economist at Dai-ichi Life Research Institute who added that depreciating currencies are making it very hard for central banks to ease on concerns about inflationary pressure and acceleration of fund outflows.

The dollar also pushed its way past more of last year’s peaks against the euro to hit $1.0550 in early European action, with only the March 2015 high of $1.0457 standing in the way of a drive toward parity, likewise the yen skidded to an eight-month low and China’s yuan to an 8-1/2 year low, while the highly sensitive Turkish lira and Indian rupee hit new historic troughs, although the USD has since given up some of the gains.

“There doesn’t seem to be anything stopping U.S. yields going higher in the near-term so I think people are going to stay on the dollar trend,” said Michael Metcalfe, head of global macro strategy at State Street Global Markets.

While so far US equity markets have ignored the jump in the DXY to a near 14 year highs, dollar gains reverberated through emerging markets. India’s rupee and Vietnam’s dong slid to records, while the Philippine peso dropped to its weakest level in eight years. In Turkey, the lira rebounded from an all-time low after the central bank unexpectedly raised interest rates, although even that move has now been faded. Copper’s surge pulled a gauge of commodities higher for a fourth day, the longest rally in a month. Rosneft PJSC approved a $17 billion bond program, the biggest ever by a Russian company as the nation’s largest oil producer refinances debt. Copper was set to close at its highest level in more than a year.

As Bloomberg writes this morning, central banks worldwide are being pushed to take action in the face of the stronger dollar.

In Turkey, policy makers opted to support the nation’s beleaguered currency, while the European Central Bank warned that the risk of an abrupt global market correction on the back of rising political uncertainty has intensified, posing a threat to banks, stability and economic growth. The market odds of a December rate hike in the U.S. are 100 percent and traders are adding to bets that Fed Chair Janet Yellen will lead further action in 2017. U.S. equity benchmarks extended records last session before the Thanksgiving holiday.

“The dollar has been really strong in anticipation of Yellen’s move next month and that strength in the U.S. dollar is ultimately going to mean that emerging-market assets would be seen as disadvantaged,” said Nicholas Teo, a strategist at KGI Fraser Securities in Singapore.

In Currencies, the greenback advanced 0.4 percent to 113 yen at 6:25 a.m. New York time, having reached an almost eight-month high. It slipped 0.2 percent to $1.0577 per euro, after surging 0.7 percent the previous day. Turkey’s lira strengthened 0.3 percent and stocks rallied after the central bank unexpectedly raised interest rates for the first time since January 2014. Policy makers increased the overnight lending rate by 25 basis points to 8.50 percent and the repurchase rate by 50 basis points to 8 percent. Economists had predicted no change in either rate. The rupee tumbled as global funds dumped Indian assets. The central bank will take appropriate action to deal with the currency’s decline, a government official said earlier Thursday, asking not to be identified, citing rules. State-run lenders sold dollars, probably on behalf of the central bank, three Mumbai-based traders said, asking not to be named. A gauge of implied price swings in the euro versus dollar over the next two weeks jumped to its highest level since the aftermath of the U.K.’s Brexit vote, as traders await the ECB’s Dec. 8 policy meeting. The euro has slid 4.2 percent against the dollar since the U.S. election amid speculation that the ECB will extend its stimulus, maintaining a policy divergence with the Fed. The MSCI Emerging Markets Currency Index dropped for a second day, heading for the lowest level since June 27, days after the U.K. voted to leave the European Union

In commodities, the Bloomberg Commodity Index was up 0.3 percent, extending gains to a fourth day, the longest run since Oct. 19. Copper for deliver in three months rose 1.9 percent to $5,848.50 a metric ton on the London Metal Exchange in London, heading for the highest close since June 2015, while zinc and lead also posted gains. The LMEX Index of six base metals on Wednesday closed at the highest level in 18 months. West Texas Intermediate crude was little changed at $48.04 a barrel after retreating 0.2 percent last session. Iraq’s prime minister said the country will cut production as part of a broader OPEC supply deal, while Russia is seen agreeing to a freeze rather than a reduction. Gold for immediate delivery dropped as much as 0.7 percent to $1,180.38 an ounce, the lowest level since February, on expectations of higher rates and a stronger dollar.

end

Friday

Furious Dollar Rally Fizzles On “Black Friday”; US Stocks Set To Open At New All-Time Highs

Having soared to fresh 13 year highs in a quiet overnight session on thin liquidity due to the US Thanksgiving holiday, which sent the USDJPY just shy of 114 and the Yuan to 6.96, the dollar pared back its weekly advance with modest profit taking after traders wondered if the rally has gotten “too stretched.” European shares were fractionally higher, with Asian stocks and US equity futures rising and both the Dow Jones and the S&P set for new all time highs. Oil followed the USD lower, down fractionally ahead of next week’s OPEC meeting where negotiations now focus on whether non-OPEC led by Russia nations will cut or freeze.

With the US offline yesterday, American markets are set for another early close on Black Friday: U.S. equity markets close at 1pm, bond markets close at 2pm.

The Bloomberg Dollar Spot Index fell from the highest level in more than a decade, while emerging-market currencies clawed back gains after India’s rupee and Turkey’s lira fell to record lows on Thursday. U.S. equity-index futures signaled stocks will edge higher as trading resumes following the Thanksgiving holiday. European shares were little changed, oil pared a weekly gain and Treasuries fell.

The recurring story every day since Trump’s election is that as a result of the upcoming debt-funded fiscal stimulus, inflation is poised to jump which in turn has fueled a surge in bets on Federal Reserve rate hikes, propelling the greenback higher against all but two of it peers this month. Traders see an increase in borrowing costs in December as a certainty, while the odds of additional moves by June have risen to more than 60 percent, according to futures data tracked by Bloomberg.

As shown virtually every day on these pages, the “Trumpflation” bet on global reflation has sent the USD soaring, while slamming EM currencies, fading the prospect of future rate cuts by these economies, while industrial metals like copper continue to soar.

Expectations of rises in U.S. inflation and interest rates have driven the greenback to a gain of more than 6 percent in October and November combined, its strongest performance over a similar period since its rally in early 2015. Most investors expect those gains to continue, but a combination of the Thanksgiving break in the United States, market participants’ need to process corporate flows at the end of the month and a raft of risks in the first half of December all speak for cashing in some of those gains now.

“The dollar bull run had perhaps become a little stretched,” said Lee Hardman, a currency strategist at Bank of Tokyo-Mitsubishi UFJ Ltd. in London. “We’ve had a very strong run since the election and it’s just a bit of a pull back.”

It is Black Friday in the US, and the National Retail Federation projects that about 137.4 million consumers will make purchases in stores or online over the four-day weekend that starts on Thanksgiving, marking the kickoff to the holiday shopping season. U.S. retail spending is expected to rise 3.6% to $655.8 billion in November and December, the Washington-based NRF estimates. Retailers are poised to take full advantage of the Thanksgiving holiday period, now known by some as Black Week, which accounts for about 15 percent of holiday spending, according to the trade group. However, the amount Americans have spent has declined in the last three years, slipping 26 percent from 2013 to an average of $299.60 per person last year, according to the trade group, so there are risks.

This holiday season is expected be better for retailers with unemployment, gasoline prices and inflation low, while wages, home values and the stock market continue to rise. Companies such as Kohl’s Corp., Gap Inc. and Barnes & Noble Inc. have said the U.S. presidential election was a major cause of consumers’ recent reluctance to open their wallets. With the outcome settled, they’re expecting the dollars to finally flow. “We’ve had some, we believe, pent-up demand — just based on the economics of our consumer,” J.C. Penney Co. Chief Executive Officer Marvin Ellison said in an interview this month. “We’re anticipating we’ll see pent-up demand released, and it being post-election will only help that.”

As the following chart of retail stock performance shows, the market is as optimistic as the retailers coming into Black Friday.

The MSCI world equity index, which tracks shares in 46 countries, was up 0.2% in early European trading and headed to close the week around 1 percent higher. In Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan added 0.7 percent. European equities were steady in morning business, with a rally in defensive sectors such as healthcare and utilities offsetting weaker banking and commodities stocks. The pan-European STOXX 600 index was unchanged, on track for a third straight week of gains.

European shares have gained 4.5 percent since Donald Trump’s surprise victory in this month’s U.S. presidential election. “It looks as if the market is taking a breather after a good run. The market view is that Trump is going to spend more and will shield the U.S. more so that we get higher inflation and higher domestic growth,” Ronny Claeys, senior strategist at KBC Asset Management, said. “The market has reacted positively on Trump, but this could change as his policies are vague at this stage. Investors will react more on his policy details” Claeys added cited by Reuters. Emerging-market shares are poised for the first weekly increase in more than a month, led by commodity and energy producers.

In rates, U.S. yields gapped higher at the open, rising as high as 2.411%, “but have been unable to hold those gains and that has encouraged some profit-taking,” said Jeremy Stretch, head of currency strategy at CIBC in London, and the 10Y was last trading at 2.37%. “There is a degree of consolidation (but) there is still a consistent bias that means the dollar will remain pretty much supported into the Fed meeting next month. The message seems to be to take some profit and we will be looking to go again.”

In the European bond market, short-dated German government bond yields set a new record low and were on track for their biggest two-week fall in more than three years, highlighting demand for top-rated assets. Demand for German debt for use as collateral for short-term lending in repo markets has helped drive two-year bond yields lower this week. Jitters ahead of an Italian referendum on Dec. 4 has also bolstered demand for German bonds, regarded as among the safest assets in the world. Rates on 10-year German bunds fell two basis points on Friday to 0.24%. Yields on 40-year Japan government bonds slid five basis points to 0.715 percent, reversing an earlier climb after an auction of the debt saw 499.7 billion yen ($4.4 billion) of securities sold at a highest yield of 0.725 percent. “The 40 year bonds were well received in the auction, triggering a bout of bond buying,” said Masahiko Sato, an analyst at Nomura Holdings Inc. in Tokyo.

* * *

Bulletin Headline Summary from RanSquawk

- Price action in Europe thus far has been muted amid ongoing holiday-thinned conditions and a lack of notable newsflow

- A day of profit taking and position adjustment, while month end (real money) flow is also starting to kick in with the USD rally taking another pause

- Looking ahead, highlights include UK GDP and US Services PMI. Note there are also early US closures today for yesterday’s Thanksgiving Holiday

Market snapshot

- S&P 500 futures up 0.2% to 2205

- Stoxx 600 up less than 0.1% to 342

- FTSE 100 down less than 0.1% to 6828

- DAX up less than 0.1% to 10690

- German 10Yr yield down 2bps to 0.24%

- Italian 10Yr yield down less than 1bp to 2.12%

- Spanish 10Yr yield down 2bps to 1.57%

- S&P GSCI Index down 0.3% to 370.2

- MSCI Asia Pacific up 0.6% to 136

- Nikkei 225 up 0.3% to 18381

- Hang Seng up 0.5% to 22723

- Shanghai Composite up 0.6% to 3262

- S&P/ASX 200 up 0.4% to 5508

- US 10-yr yield up 2bps to 2.37%

- Dollar Index down 0.26% to 101.44

- WTI Crude futures down 0.7% to $47.63

- Brent Futures down 1% to $48.53

- Gold spot up 0.3% to $1,188

- Silver spot up 0.9% to $16.44

Global Headline News

- J&J Said to Make Takeover Approach for Drugmaker Actelion: Actelion shares soar by most in more than 2 years; deliberations said to be at early stage after initial offer

- Amazon Said in Talks to Buy Dubai’s Souq.com in $1b Deal: no final decisions have been made, talks could still falter; MidEast e-commerce site initially planned to sell a stake

- Black Friday Merchants See Americans Exhaling After Election: with uncertainty gone, stores see consumers poised to spend; Thanksgiving weekend accounts for 15% of holiday sales

- Holiday Price War Intensifies as Wal-Mart, Target Pursue Amazon: brick-and-mortar chains offering bigger discounts than in 2015

- U.S. Boosts Refiners’ 2017 Biofuel Quotas to Record Levels: EPA mandates above levels the agency proposed in May

- Chevron to Pick Winner of Indonesian Geothermal Bid in Dec./Jan.: co. reviewing bids from 5 companies, including Marubeni, Pertamina

- Trump Expected to Pick Ross for Commerce Job, Person Says: President-elect Trump is expected to nominate as secretary of commerce investor Wilbur Ross

- OPEC’s Last Push for Oil Deal Shifts Focus to Iran, Russia: Algerian minister to meet his counterpart in Tehran Saturday

- GoDaddy Said in Exclusive Talks to Buy Host Europe: Reuters

- KKR Said to Partner With Arrow Pharma for INova Bid: AFR

- Samsung Bioepis Nasdaq IPO May Be Delayed: Maeil Business

- U.S. equity markets close at 1pm, bond markets close at 2pm

In Asia, stock markets traded mostly positive, although gains were reserved after a small lead from Wall St. where US participants were absent due to Thanksgiving holiday. Nikkei 225 (+0.3%) traded choppy throughout the session with the index driven by JPY fluctuations, while ASX 200 (+0.4%) was also higher despite upside being limited by weakness in gold. Hang Seng (+0.5%) conformed to the positive tone while Shanghai Comp (+0.6%) initially lagged amid quiet news flow and after the PBoC reduced its weekly net liquidity injection by around 90% from the prior week. 10yr JGBs were initially pressured amid gains in riskier assets and as yields rose alongside their US counterparts. However, JGBs then recovered from their lows in the wake of a firmer 40yr auction leading to outperformance in the super-long end and curve flattening. PBoC injected CNY 120bIn in 7-day reverse repos, CNY 70bIn in 14-day reverse repos, CNY 25b1n in 28-day reverse repos for a weekly net injection of CNY 40bIn vs. last week’s CNY 425b1n net injection.

Japan reported its latest consumer price data, which met or beat most expectations:

- Japanese National CPI (Oct) Y/Y 0.1% vs. Exp. 0.0% (Prey. -0.5%)

- Japanese National CPI Ex. Food (Oct) Y/Y -0.4% vs. Exp. -0.4% (Prey. -0.5%)

- Japanese Tokyo CPI (Nov) Y/Y 0.5% vs. Exp. 0.2% (Prey. 0.1%)

- Japanese Tokyo CPI Ex-Food (Nov) Y/Y -0.4% vs. Exp. -0.4% (Prey. -0.4%).

Top Asian News

- Macquarie, ANZ to Pay $11 Million Over Malaysia Rates Probe: Australian banks admit attempted cartel conduct in 2011

- In Asia Currency-Reserve Checkup, Two Countries Come Out on Top: IMF gauge shows Thailand, Philippines offer resilience

- China Bad-Loan Disposal No Easy Task With Slowdown, Survey Shows: Only 4% of bad-loan managers find it easy to dispose of NPLs

- JAL Plans First Post-Bankruptcy Bond to Fund Airbus Purchases: Airline plans to sell about 20 billion yen of notes next month

- Angry Soldiers Another Headache for Modi Amid Rupee Note Crisis: Suspected suicide of voluntary reservist highlights concerns

In Europe, as expected, given yesterday’s US thanksgiving holiday, newsflow and price action has been light today. European equities trade flat, with Actellion higher by almost 10% amid talk of a potential merger, with Shire touted as a bidder. To the downside, Banca Monte Paschi traders got their usual morning break as Co. shares were halted limit down once again, this time as a consequence of the EUR 5bIn capital raising. Fixed income and commodity markets have been equally dull, with Bunds marginally higher today amid light volumes and little to drive price action. The energy complex has seen modest softness as all eyes focus on next week’s OPEC meeting, with participants becoming somewhat saturated with comments from the different nations in the build up.

Top European News

- U.K. Economy Shows No Sign of Brexit Effect as Spending Rises: consumers and businesses increased their spending in 3Q as the U.K. economy registered resilient performance after Brexit vote

- Brexit May Take Decade So Give the Pound a Rest, Investors Say: Pound already reflects changing economy, Standard Life says; Kames Capital now “slightly more optimistic” on currency

- Nordea Chairman Says Talks With ABN Amro Are Unlikely to Resume: Nordea isn’t tempted to buy ABN shares, Wahlroos says

- Greece’s Biggest Bank Sees Trump Boost to Country’s Economy: Piraeus Bank chair Handjinicolaou speaks in interview, declines to give timeframe for pending CEO pick

- Lufthansa Condemns ‘Emotional’ Pilots as Strike to Span Weekend: union has extended action, claiming company aims to destroy it

In currencies, the Bloomberg Dollar Spot Index fell 0.3 percent at London morning trading, leaving it up 0.3 percent this week. Japan’s currency gained 0.4 percent to 112.80 per dollar. It’s down 1.8 percent in the week, the worst performance among major currencies. The rupee strengthened 0.4 percent after sinking to a record low Thursday, while the Turkish lira gained 0.3 percent. China’s yuan, which fell to an eight-year low against the dollar this week, was little changed. The yuan rose this week to an August high versus a basket of peers, signaling that its declines against the greenback have been more moderate than those of other currencies. South Africa’s rand headed for its first weekly gain in three weeks before a credit-rating review by Moody’s Investors Service.

In commodities, West Texas Intermediate crude oil slipped 0.8 percent to $47.58 a barrel. OPEC’s focus has shifted to negotiations with Iran and non-member Russia for production curbs after Iraq’s prime minister signaled it will agree to cut output. Gold for immediate delivery rose 0.7 percent to $1,190.24 an ounce, the first advance in four days. Copper slipped less than 0.1 percent in London and has surged 8.2 percent this week. The industrial metal has soared 21 percent this month.

Looking at today’s events, the main focus this morning was on the UK where we got the second estimate of Q3 GDP which came in at 0.5%, as expected. Also in the UK today was the CBI’s Distributive Trades Survey for November which soared from 21 to 26, smashing expectations of a 12 print, while French consumer confidence data is the early print this morning. Markets in the US should be quiet again today but there is some data due out including the remaining flash November PMI’s (services and composite), wholesale inventories and the advance goods trade balance for October. It’ll also be worth keeping an eye on any retail sales data for Black Friday sales in the US. A reminder that this Sunday the second and final round of the French centre-right primary is due to be held. The run-off is between Francois Fillon and Alain Juppe, the former coming out on top in the first round, with the winner going on to be the chosen Republican candidate. We should know the winner around 9pm GMT on Sunday evening.

US Event Calendar

- 8:30am: Advance Goods Trade Balance, Oct., est. -$59b (prior -$56.5b)

- 8:30am: Wholesale Inventories m/m, Oct P, est. 0.2% (prior 0.1%); Retail Inventories m/m, Oct. (prior 0.3%)

- 9:45am: Markit US Services PMI, Nov. P, est. 54.8 (prior 54.8)

* * *

DB’s Jim Reid concludes the overnight wrap

Good luck to all those braving the sales today. It’s staggering to see the number of ‘How to Survive Black Friday’ articles out there now and how many more stories there are with tips and strategies to get the best bargains on the day. Apparently it now takes weeks of precise planning and preparation. It sounds like you’ll need a decent plate of leftover turkey this morning to build up the energy first.

If the last 24 hours is anything to go by then it’s likely to be another fairly quiet day ahead with the US scheduled for an early close. While there wasn’t much to shout about in markets yesterday the most interesting story concerned a Bloomberg report about the ECB possibly putting off decisions about the future of its bond-buying program until next year. The crux of the story concerned the parameters of the program and how the technical issues relating to bond scarcity may have eased with the recent rise in yields. The story also suggested that ‘some’ policy makers would consider a delay on the QE extension decision but we’d also caveat that with the mention of ‘most’ policymakers still seeing a need to send a dovish message at next month’s meeting given the inflation outlook. Indeed we’d highlight that the recent message from ECB officials has been just that including President Draghi’s recent comments. A reminder too that the 2019 staff forecasts will be available for the first time at the meeting next month. That said, it is worth noting that expectations were fairly high for a QE announcement in December 2014 and we had to wait for January 2015 for the decision to eventually be made so you can’t entirely rule out the possibility a delay.

With that Bloomberg report coming as markets in Europe closed we didn’t get to see too much of a reaction. 10y Bund yields finished little changed at 0.251% with yields, if anything, a couple of basis points higher following the story. The periphery was a bit more mixed (Portugal and Spain 1bp lower and Italy 1bp higher) but again moves were fairly modest. This morning we’ve seen 10y Treasury yields rise nearly 5bps however. There was also some focus on FX markets yesterday with a number of EM currencies making new recent lows including currencies in India, Malaysia, Vietnam and Philippines. The Turkish Lira (-1.44%) was also under pressure despite Turkey’s central bank raising rates for the first time in nearly three years. Following that though the European Parliament then voted overwhelmingly in favour of suspending EU membership talks with Turkey.

Elsewhere, equity markets in Europe yesterday were generally a touch firmer despite volumes some 50% or so below the usual daily average The Stoxx 600 closed up +0.31% as healthcare and tech stocks led the move higher, while credit indices were marginally tighter. A bit of stability in the Oil complex seemingly helped too with WTI continuing to hover around the $48/bbl level ahead of the OPEC meeting next week.

Back to the ECB, Vice-President Constancio also added to the recent chorus of dovish communication from the Bank yesterday. He said that ‘we want our policies, including unconventional policies, in place until we are convinced there is a sustained path toward our objective of inflation’. The ECB’s twice-yearly Financial Stability Review was also released yesterday with the report warning about the risk of a possible abrupt global correction on the back of political uncertainty and elevated geopolitical tensions which is posing risks to stability, banks, confidence and economic growth.

This morning in Asia, with the exception of China it’s been a broadly positive session for equity markets. The Nikkei (+0.77%), Hang Seng (+0.38%), Kospi (+0.10%) and ASX (+0.62%) are all up although in China the Shanghai Comp (-0.43%) has dipped lower. US equity index futures are also a smidgen higher while sovereign bond markets are generally weaker. 10y JGB yields in particular are a couple of basis points higher at 0.053% and the highest yield since mid-February. The Yen (-0.25%) however is under pressure and approaching ¥114 following the latest leg higher for the Dollar. The latest CPI data was also out in Japan overnight. The good news is that headline CPI return to positive territory at +0.1% yoy versus -0.5% in September, however the core remains rooted in deflation at -0.4% yoy (from -0.5%). The core-core did also improve to +0.2% yoy from 0.0%. Our economists noted that the increase in overall CPI was mainly due to a sharp increase in the price of fresh vegetables due to unfavourable weather.

The only other snippet to mention from yesterday was the economic data. The most significant came from Germany where there was no final revisions made to the Q3 GDP print of +0.2% qoq, leaving the YoY rate at +1.7%. The components of the report showed that growth mainly came from domestic demand, especially private and government consumption. Meanwhile Germany’s November IFO survey revealed a business climate reading of 110.4 which was unchanged from the month prior. A slight increase in the current assessment component was offset by a modest decline in expectations. In France business confidence was also unchanged in November at 102.

Looking at today’s calendar the main focus this morning in the European session will likely be on the UK where we’ll get the second estimate of Q3 GDP and where the Office for National Statistics is expected to confirm that GDP grew at +0.5% qoq during the quarter. We’ll also receive the wider components of the GDP report which will be interesting to see. Also due out in the UK today is the CBI’s Distributive Trades Survey for November while French consumer confidence data is the early print this morning. Markets in the US should be quiet again today but there is some data due out including the remaining flash November PMI’s (services and composite), wholesale inventories and the advance goods trade balance for October. It’ll also be worth keeping an eye on any retail sales data for Black Friday sales in the US.

A quick reminder before we sign off that this Sunday, the second and final round of the French centre-right primary is due to be held. As a reminder the run-off is between Francois Fillon and Alain Juppe, the former coming out on top in the first round, with the winner going on to be the chosen Republican candidate. We should know the winner around 9pm GMT on Sunday evening.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 20.20 POINTS OR 0.62%/ /Hang Sang closed UP 114.96 OR 0.57%. The Nikkei closed UP 47.81 OR .26%/Australia’s all ordinaires CLOSED UP 0.39% /Chinese yuan (ONSHORE) closed DOWN at 6.9207/Oil FELL to 47.49 dollars per barrel for WTI and 48.45 for Brent. Stocks in Europe: ALL IN THE RED EXCEPT LONDON Offshore yuan trades 6.9485 yuan to the dollar vs 6.9207 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS DEEPLY AS MORE USA DOLLARS LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

3a)THAILAND/SOUTH KOREA/:

b) REPORT ON JAPAN

c) Report on CHINA

Thursday:

China press lashes out that it is the dollar’s strength that is causing the yuan to weaken. As the yuan weakens, the globe is whacked with deflation as lower Chinese prices force other countries to lower their prices to compete. Emerging markets are now in complete turmoil

(courtesy Dan Steinbok/ChinaDaily.com)

China Press Lashes Out – It’s The Dollar, Not The Yuan That Threatens Global Stability

Originally posted at ChinaDaily.com,

Recently, the Chinese currency fell to its lowest level since late 2008. The renminbi has been trading around 6.92 to the US dollar.The plunge is typically explained with the anticipated US Federal Reserve rate increase in December and president-elect Donald Trump’s threat to label China a currency manipulator and slap tariffs on Chinese exports.

In reality, there is much more to the story.

In the long term, China’s growth will translate to currency power in foreign-exchange markets. In October, the renminbi officially joined the International Monetary Fund’s currency reserve basket, known as Special Drawing Rights. In the coming decade, the renminbi will expand rapidly through the IMF reserve basket, the allocations of central banks, and those of public, private, sovereign and individual investors.

After summer, the renminbi’s fundamentals improved thanks to positive spillover effects from overcapacity reduction, fiscal stimulus and a boost to export competitiveness, due to weaker exchange rate.

In the fourth quarter, the Chinese currency will also feel the adverse impact of a mild correction of property prices.

The renminbi’s short-term volatility is also compounded by the tumultuous global environment and the US dollar. Along with other emerging market currencies, the renminbi must cope with the US dollar, which recently hit a 14-year high, driven by rising US bond yields, expectations of a Trump fiscal stimulus and the impending Fed rate hike. In the process, other Asian currencies?the Japanese yen, Indian rupees, Korean won, Indonesian rupiah and the Malaysian ringgit?suffered a sell-off.

In the long term, the spillovers from the US and Chinese financial markets are likely to have a different impact on financial markets in the Asia-Pacific region. Studies conducted by central banks suggest that in normal times China’s influence in the equity has risen close to the US’ level, although the relative impact of the US has been stronger during crisis periods.

The influence of China is based on a regional pull, while that of the US reflects a global push. The current crisis favors the dollar, but over time stability will support the renminbi.

Unfortunately, the renminbi, along with other emerging market currencies, must also cope with the dollar’s growing risk in the world economy. Before the 2008-09 global financial crisis struck, there was a close correlation between leverage and the volatility index (VIX). When the VIX was low, the appetite for borrowing went up, and vice-versa. That correlation no longer prevails, due to years of ultra-low rates and rounds of quantitative easing by advanced economies’ central banks.

Recently, the Bank for International Settlements reported that the US dollar has replaced the volatility index as the new fear index.

As the VIX’s predictive power has diminished, the dollar has become the indicator of risk appetite and leverage. This dynamic has distressing implications, because it has pushed international borrowers and investors toward the dollar.

And yet, as the dollar’s appreciation is exposing borrowers and lenders to valuation changes, the US’ fundamentals are eroding, as president-elect Trump himself has acknowledged. The US’ sovereign debt has soared to $19.9 trillion. And in the past year, foreign central banks sold almost $375 billion in US Treasuries.

In these conditions, the Fed rate hikes could boost the US dollar as a kind of global Fed funds rate, which would result in dollar tightening and deflationary constraints?which, in turn, could impair emerging economies that today fuel global growth prospects.

It is not the renminbi but the US dollar that today poses the greatest risk to the global economy and serves as its fear gauge.

* * *

Authored by Dan Steinbock, the founder of Difference Group and has served as research director at the India, China and America Institute (USA) and visiting fellow at the Shanghai Institutes for International Studies (China) and the EU Center (Singapore).

4 EUROPEAN AFFAIRS

The huge drop in the value of the Euro due to dollar rising is causing huge significant risks in Europe and they warn of a abrupt market reversal

no kidding..

(courtesy zero hedge)

ECB Warns There Is “Significant Risk Of Abrupt Market Reversal”

One week after the BIS issued an unexpectedly stern, if completely ignored warning, that the surge in the USD is leading to an abrupt tightening in financial conditions around the globe, making the repayment of trillions in USD-denominated cross-border debt increasingly more difficult and suggesting that the Dollar index itself is the new “fear indicator”, overnight another central bank, the European Central Bank warned that the risk of “abrupt” global asset market corrections “have intensified” on the back of rising political uncertainty, posing a threat to banks, stability and economic growth.

“More volatility in the near future is likely and the potential for an abrupt reversal remains significant amid heightened political uncertainty around the globe and underlying emerging market vulnerabilities,” the ECB warned in its twice-yearly Financial Stability Review published on Thursday.

“Elevated geopolitical tensions and heightened political uncertainty amid busy electoral calendars in major advanced economies have the potential to reignite global risk aversion and to trigger a major confidence shock.”

In its report, the ECB warned about the recent period of dramatic, unexpected political results that started with the Brexit vote and culminated with Donald Trump’s victory, which have increased volatility and herald profound economic-policy changes whose implications for the euro area are still hard to gauge. “Financial stability implications for the euro area stemming from changes in U.S. economic policies are highly uncertain at this point in time.”

The Central bank noted out that while the currency bloc’s economy and financial system have remained resilient so far, more political instability in coming months may put pressure on weak banks and countries with high sovereign debt.

The ECB also focused on domestic banks and admitted that “vulnerabilities remain significant for euro-area banks,” confirming the ongoing Deutsche Bank lament that “profitability prospects overall remain low across the euro area in a subdued economic growth environment.” The good news is that – largely unexpectedly – the Trump victory has spurred a pick-up in bank stocks as investors saw the risk of ever tighter regulation recede. If sustained, this would “provide some support for euro area banks’ profitability prospects,” according to the ECB. The ECB also said that steeper yield curves “may provide some support for euro-area banks’ profitability prospects.”

The good news is that “despite relatively volatile global financial markets, bank and sovereign systemic stress indicators for the euro area have remained fairly stable at low levels.”