Gold at (1:30 am est) $1187.90 DOWN $2.90

silver at $16.66: UP 8 cents

Access market prices:

Gold: 1188.50

Silver: 16.62

Tomorrow is the last day for option’s expiry. We should see gold and silver rise once this criminal activity is over with for this month. Also the low OI for the complex will no doubt help in our precious metals rise in price. I only wish, if investors want to buy gold and silver, that they only buy physical and not paper obligations.

Tomorrow is also first day notice for both the gold and silver and both are active months.

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

TUESDAY gold fix Shanghai

Shanghai morning fix Nov 29 (10:15 pm est last night): $ 1219.88

NY ACCESS PRICE: $1191.25 (AT THE EXACT SAME TIME)/premium $28.63

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1216.15

NY ACCESS PRICE: 1190.85 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $25.30

China rejects NY pricing of gold as a fraud

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Nov 29: 5:30 am est: $1187.30 (NY: same time: $1187.50 5:30AM)

London Second fix Nov 29: 10 am est: $1186.55 (NY same time: $1186.50 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR NOVEMBER CONTRACT MONTH: 19 NOTICE(S) FOR 1900 OZ TONNES

For silver:

NOTICES FOR NOVEMBER CONTRACT MONTH FOR SILVER: 0 NOTICE(s) OR nil OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 3008 contracts DOWN to 163,166 with YESTERDAY’S trading. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .816 BILLION TO BE EXACT or 116% of annual global silver production (ex Russia & ex China).

In November, in silver, 0 notice(s) filings: FOR nil OZ

In gold, the total comex gold FELL by 4,763 contracts WITH THE RISE IN THE PRICE OF GOLD ($12.40 with YESTERDAY’S trading ).The total gold OI stands at 410,824 contracts. The bankers have done a good job of eviscerating gold (and silver) longs.

In gold: we had 19 notice(s) filed for 1900 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD,

Inventory rests tonight: 885.04 tonnes

.

SLV

we HAD NO CHANGES at the SLV/

THE SLV Inventory rests at: 346.150 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver FELL by 3,008 contracts DOWN to 163,166 as price of silver ROSE by $.12 with YESTERDAY’S trading. The gold open interest FELL by 4,763 contracts DOWN to 410,824 as the price of gold ROSE BY $12.40 WITH YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) FRBNY foreign gold movement

(Harvey)

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 5.94 POINTS OR 0.18%/ /Hang Sang closed DOWN 93.50 OR 0.41%. The Nikkei closed DOWN 49.85 OR .27%/Australia’s all ordinaires CLOSED DOWN 0.22% /Chinese yuan (ONSHORE) closed UP at 6.8988/Oil FELL to 45.88 dollars per barrel for WTI and 46.90 for Brent. Stocks in Europe: ALL IN THE GREEN EXCEPT LONDON Offshore yuan trades 6.9232 yuan to the dollar vs 6.8988 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

The following will be something that I will be watching out for: the rising Chinese bond yields (lower prices on bonds). The fact that the USA is raising rates has caused China to tighten as well. If they let interest rates remain pat then the yuan would contract even more. So China matches the USA in rising yields to prevent their yuan from collapsing

( zero hedge)

4 EUROPEAN AFFAIRS

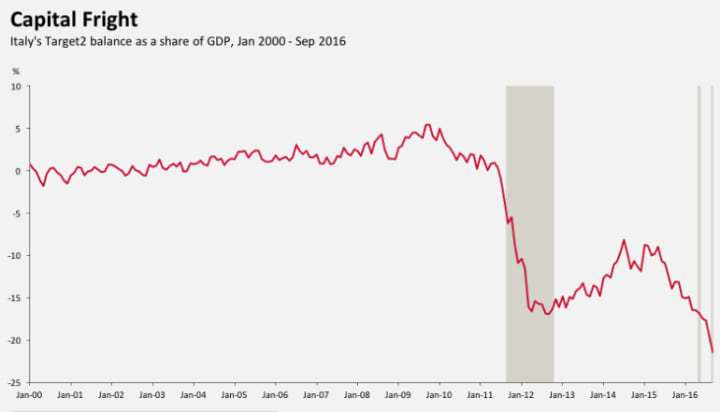

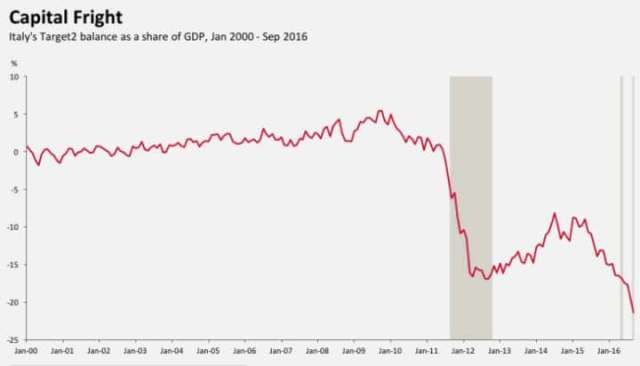

i)This Sunday, Dec 4 is the referendum date for Italy and the polls indicate strongly that the rejection of the establishment. Renzi may quit as promised but we are just not sure. He does not want to be gatekeeper of a technocrat government similar to what happened when Berlusconi left and Monti was appointed.

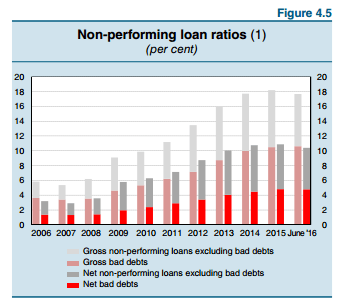

The ECB is ready to purchase as many Italian bonds as possible trying to keep the yields from skyrocketing. As I have pointed out on many occasions to you, the Italian banking system has 18% non performing loans totaling 360 billion euros. The bank system in Italy is insolvent.

( zero hedge)

ii)Another huge paper: Ambrose discusses the huge 360 billion euros of bad debt on the balance sheet of the banks. The problem here is the new rules which will not allow a bailout by the sovereign Italy. There must be a bail in and most of the bonds are owned by Italian citizens.

a must read..

(courtesy Ambrose Evans Pritchard/UKTelegraph)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)It appears that Assad’s army will on the verge of taking Aleppo and that will be a slap in the face of the USA

(courtesy zero hedge)

ii) In another slap in the face to the USA, Egypt shuns Washington and now supports the Russian backed coalition in Syria

Gorka/Stragic-Culture.org.)

iii) After months stating that Turkey was o Syrian soil to the fight ISIS, Erdogan has now changed his tune and states that he is in Syria to oust Assad!

an act of war???

(courtesy zero hedge)

6.GLOBAL ISSUES

This latest Jim Willie paper is pretty good as it outlines the 11 or more problems facing the globe:

( Jim Willie/GoldenJackass)

7. OIL ISSUES

i)Oil tumbles as it looks like there will not be a cut in production from the OPEC/Non Opec group

( zero hedge)

ii)Who would have thought that this was coming? WTI plunges near 44 dollars after Iran states no production cuts:

( zero hedge)

iii)Iran turns the tables and states that it is the Saudis that should cut production by over 1 million barrels by themselves.

iv) Late tonight, this is where we stand with respect to the possible oil deal: it seems that Iran and Iraq are the stumbling blocks.( zero hedge)

8. EMERGING MARKETS

The following describes what hyperinflation is like in Venezuela: shopkeepers weight vast piles of notes instead of counting them!

( London’s the Guardian)

9. PHYSICAL MARKETS

i)This is a very worthwhile organization as they are doing their utmost exposing the fraud in the gold/silver market. I urge you do donate if you can

( Chris Powell//GATA)

ii)The real reason that India banned the large notes: to suppress India’s gold demand and I agree 100% with the author’s assessment

( Stewart Dougherty/Dave Kranzler/IRD)

10.USA STORIES

i)Dr Price, an Orthopedic surgeon and a strong critic of Obamacare is to head the Health team along with sidekick Verma. This no doubt will seal the fate of Obamacare

( zero hedge)

ib)We would be extremely happy if Trump selects John Allison, a former CEO of BB and T and formerly of the prestigious CATO institute. He wants to abolish the Fed and return to the gold standard (along with Judy Shelton)

this is the man we want..

( zero hedge)

ii)With our highly backed figures, the second revision to GDP showed a gain to 3.2% beating expectations of a 3% reading

( zero hedge)

iii)Who would have thought that this was going to happen: a Trump victory seems consumer confidence soaring?:

( Conference Board Consumer Confidence/zero hedge)

iv)UBS states that traders have got the signals wrong with respect to the USA/Yen cross due to the Trump victory. Markets are reacting to the infrastructure spending proposed by Trump as a reason for the USA/Yen to climb to 120/1. However they do not seem to pay attention to the isolationist policy of Trump which should cause the Yen to rise to 98/1: Not only that but Japan proposing new tariff rules which will knock out major competitors. Protectionism from all angles will cause the yen to rise in value.

( zero hedge)

Let us head over to the comex:

The total gold comex open interest FELL by 4,763 CONTRACTS to an OI level of 410,824 DESPITE THE FACT THAT GOLD ROSE $12.40 with YESTERDAY’S trading. In the front month of November we had 26 notices standing for a LOSS of 3 contracts. We had 2 notices served upon YESTERDAY so we LOST 1 GOLD CONTRACTS OR AN ADDITIONAL 100 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF NOVEMBER. The next contract month and the biggest of the year is December and here this month showed a HUGE DECREASE of 46,783 contracts DOWN to 30,773.( much higher than usual), The December contract month is still highly elevated compared to a year ago. On FRIDAY Nov 27/2015 comex reading day, we had a total of 24,018 contracts standing ( a loss of 36,141 contracts from Nov 25/2015. To give you more detail as to how the front month of December/2015 contracted, the final Nov 30 contract had an OI of 7,849 contracts standing or 24.41 tonnes standing as we lost 16,169 contracts.) The OI for the entire complex was around 393,000 or similar to the low readings this year. It certainly emphasizes the huge demand for physical gold.We have exactly 1 more trading day left. THIS SHOULD EXPLAIN TO YOU WHY THE BANKERS ARE CONSTANTLY WHACKING OF GOLD (AND SILVER): THE HIGH OI FOR DECEMBER AND THE HIGH PROBABILITY THAT MANY WILL TAKE DELIVERY. It looks to me like we will have 14,000 contracts or higher standing: 43.65 tonnes of gold

And now for the wild silver comex results. Total silver OI FELL by 3008 contracts from 166,174 DOWN TO 163,166 as the price of silver ROSE BY $0.12 with YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540). The front month of November had an OI of 0 and thus a LOSS of 1 contract(s). We had 1 notice(s) filed yesterday so we neither lost nor gained any contracts (oz) that will stand for delivery in this non active month of November. The next major delivery month is December and here it FELL BY 15,293 contracts DOWN to 11,855. The December contract month is WORSE compared to a year ago. On Nov 27/2015 reporting day, we had a level of 16,868 contracts having lost 10,053 contracts on the day. On the final day of November/2015, we had 5,975 contracts stand for 29.875 million oz. We lost 4078 contracts on the last day prior to first day notice. It looks like we will end up with around 5,000 contracts standing or 25 million oz.

In silver had 0 notice(s) filed for NIL oz

Eventually at the end of December 2015: 6.4512 tonnes of gold stood for delivery

Eventually at the end of December 2015: 18.84 million oz of silver stood for delivery.

Note how much paper settlements occurred in December last yr and I surely doubt if we will get any paper settlements this year.!!

VOLUMES: for the gold comex

Today the estimated volume was 233,259 contracts which is good.

Friday’s confirmed volume was 343,641 contracts which is excellent

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil |

113,245.190 oz

Brinks

HSBC

Scotia

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

68,263.496 oz

Scotia

brinks

(incl 1 kilobar)

|

| No of oz served (contracts) today |

19 notice(s)

1900 oz

|

| No of oz to be served (notices) |

27 contracts

2700

oz

|

| Total monthly oz gold served (contracts) so far this month |

2692 contracts

269,200 oz

8.3732 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 746,957.7 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 19 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

24,026.65 oz

HSBC

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

38,711.830 oz

brinks

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

0 contracts

(nil oz)

|

| Total monthly oz silver served (contracts) | 469 contracts (2,345,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,790,555.7 oz |

end

end

NPV for Sprott and Central Fund of Canada

END

FEDERAL RESERVE BANK OF NEW YORK; FOREIGN GOLD MOVEMENTS

Last month I reported to you that 5 tonnes of gold moved out of the FRBNY which was much smaller than before as Germany was not getting its required amount of gold.

Now this month:

FRBNY gold holdings Sept: 7841

FRBNY gold holdings Oct: 7841

all figures are million dollars worth of gold at the official rate of 42.22 dollars per oz

amount leaving: 0

Amount repatriated: zero

Germany must be royally angry!

(HARVEY)

end

Major gold/silver stories for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE

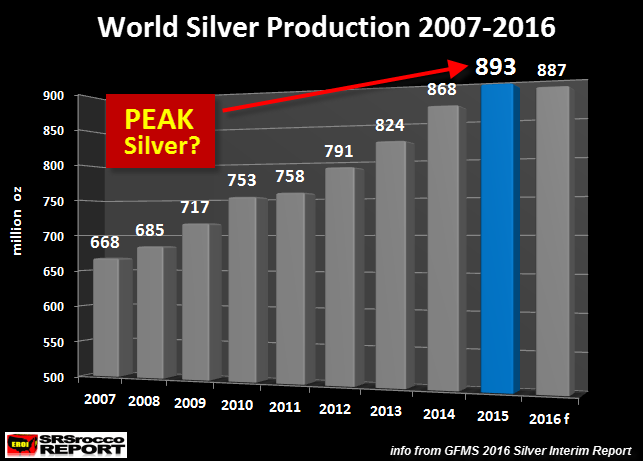

Peak Silver – Supply Deficits Mean Higher Prices

- Peak Silver – Supply deficits continue meaning higher prices

- May have experienced a peak in world silver production

- Global silver market suffered another large net supply deficit in 2016

- Peak silver likely as global silver production will decline to 887 million oz (Moz), down from 893 Moz in 2015

“While forecasted global silver production for 2016 is down only slightly versus last year, GFMS also stated this in their report:

We estimate that mine supply peaked in 2015 and will trend lower in the foreseeable future.

Declining total supply is expected to be a key driver of annual deficits in the silver market going forward.

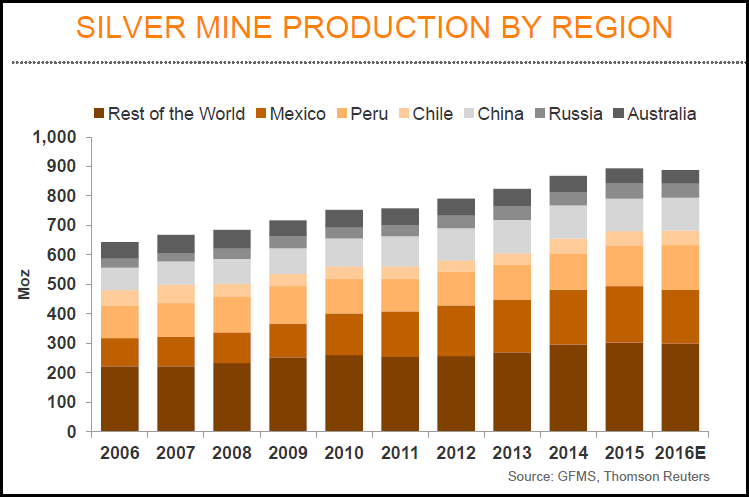

I will get to the annual silver deficits in a minute, but let’s look at their world silver mine supply by region:

“What is interesting here, is that GFMS forecasts the number one silver producer, Mexico, to be down in 2016 by more than 6 Moz. Last year, I forecasted that global silver production would likely be lower in 2015. I was going by data by the “World Metals Statistics.” However, Mexico’s INEGI (government agency) considerably revised their figures higher for 2015. While I have seen revisions take place, the revisions by Mexico’s INEGI for 2015 were quite substantial.

Regardless, GFMS does a pretty good job with the silver mine supply data. The important take-away here is that the trend of global silver production will likely be lower going forward.”

Read the full report on SRS Rocco here

GIVE THE GIFT OF SILVER THIS CHRISTMAS

Silver bullion coins – like Silver Maples, Philharmonics, Britannias, Nuggets (Kangaroos) and Eagles – are great gifts for loved ones at Christmas time.

Silver Maples 2016 (1 oz)

Silver Maples 2016 (1 oz)

Besides being a wonderful Christmas present for loved ones, they are a great way to pass on wealth to the next generation. They are a great way to teach younger generations the value of savings and the value of insurance against currency debasement and financial collapse.

We have very competitive prices – some of the most competitive internationally. We are now delivering legal tender silver coins, VAT free, in the UK and throughout the EU. Give the most precious of gifts this Christmas.

Gold and Silver Bullion – News and Commentary

Gold little changed as dollar holds losses (Reuters.com)

Gold Posts Biggest Advance in Four Weeks as Dollar Declines (Bloomberg.com)

Oil up ahead of OPEC meeting; dollar, stocks dip (Reuters.com)

London zinc charges to 9-yr high, lead hits 5-yr high (Reuters.com)

Islamic finance body approves standard for gold-based products (Reuters.com)

Bonds set to snap three-decade winning streak as Fed, Trump plot next moves (CNBC.com)

How Donald Trump’s economic plans will lead the Fed to reverse course on policy: Schiff (CNBC.com)

Interventions in gold and currency markets by central banks (GoldSeek.com)

Here’s what happened when ancient Romans tried to drain the swamp (SovereignMan.com)

The Hyperinflationary Endgame: Venezuela Currency Crashes 15% In One Day (ZeroHedge.com)

Gold Prices (LBMA AM)

29 Nov: USD 1,187.30, GBP 952.45 & EUR 1,119.98 per ounce

28 Nov: USD 1,189.10, GBP 956.51 & EUR 1,117.99 per ounce

25 Nov: USD 1,187.50, GBP 953.30 & EUR 1,121.83 per ounce

24 Nov: USD 1,187.25, GBP 953.60 & EUR 1,125.04 per ounce

23 Nov: USD 1,213.25, GBP 980.00 & EUR 1,143.00 per ounce

22 Nov: USD 1,217.55, GBP 978.91 & EUR 1,144.98 per ounce

21 Nov: USD 1,214.95, GBP 984.72 & EUR 1,143.39 per ounce

Silver Prices (LBMA)

29 Nov: USD 16.54, GBP 13.26 & EUR 15.61 per ounce

28 Nov: USD 16.68, GBP 13.45 & EUR 15.73 per ounce

25 Nov: USD 16.47, GBP 13.21 & EUR 15.55 per ounce

24 Nov: USD 16.31, GBP 13.09 & EUR 15.43 per ounce

23 Nov: USD 16.56, GBP 13.36 & EUR 15.59 per ounce

22 Nov: USD 16.76, GBP 13.46 & EUR 15.77 per ounce

21 Nov: USD 16.68, GBP 13.47 & EUR 15.69 per ounce

Recent Market Updates

– Bail In Risk – €4 Trillion Banking System In Italy Poses Contagion Risk as Referendum Looms

– Gold Down 13.5% In 13 Days – Trump Bearish For Gold?

– War On Cash Just Got Real – India and Citibank In Australia

– Russia Gold Buying In October Is Biggest Monthly Allocation Since 1998

– Stocks, Bonds, Pension Funds “Will Be Wiped Out…” – Rickards

– Physical Gold Is A “Long-Term Position” as “Hedge Against Governments”

– Gold Sell Off On Fed Noise – “Interesting Times” To “Support Gold”

– Islamic Gold – Vital New Dynamic In Physical Gold Market

– Peak Gold Globally – “Bullish For Gold”

– Gold Price Should Go Higher On Global Risks and Trump – Capital Economics

– President Trump – Why Market Loves Him and Experts Wrong

– ‘Helicopter Money President’ Trump To Create Inflation and Gold Will Rise

– Central Bank Gold Demand continues in Q3

END

This is a very worthwhile organization as they are doing their utmost exposing the fraud in the gold/silver market. I urge you do donate if you can

(courtesy Chris Powell//GATA)

Has GATA’s work made any difference? Will it ever?

Submitted by cpowell on Mon, 2016-11-28 21:04. Section: Daily Dispatches

4:05p ET Monday, November 28, 2016

Dear Friend of GATA and Gold:

If you have made a donation by credit card in response to our appeal Sunday for financial support —

http://www.gata.org/node/16947

— and have not received a personal note of thanks from your secretary/treasurer by e-mail, it’s because I did not have or could not locate an e-mail address for you. Please do e-mail me to cite any donation made by credit card so that I can acknowledge it most gratefully. Our credit card donation mechanism does not make any provision for contact information and, for security reasons, provides us with little more information about donors than their name.

If you make a donation by mailing a check, please include your e-mail address there too. This will save GATA the expense of regular postage in thanking you.

Meanwhile, a devoted friend in Canada who long has been advocating for GATA conveys this criticism he got from an acquaintance:

“GATA has been banging the drum for a long time now but what has it accomplished in a practical sense? GATA reveals information that is ignored. GATA appears before commodity market regulators who are indifferent to the evidence presented. GATA has been unable to sway the mining industry itself. This war has proven fruitless. Maybe it’s time to accept that and move on. If GATA got and spent a million dollars in donations, there would be no appreciable effect. No one who profits from the game as it is now played is going to roll over and change based on any facts or exposure, and no entity with the authority to act is going to intervene. It’s a captured market.”

This criticism is not entirely unfair. Yes, GATA has not yet wiped the tyranny of central banking from the face of the earth. But we have exposed to a wide audience — an audience including at least two major governments — the part of that tyranny that rigs the gold and currency markets, and have explained how this ultimately rigs all markets for totalitarian and imperialistic purposes. We have evidence that people are acting on this knowledge and that our work has forced the market riggers to expend even more resources and become even more obvious. If, as we believe, what they are doing is evil, it will break eventually and the ascent of man will continue. For as James Russell Lowell wrote in defiance when the Slave Power seemed to have a lock on America:

Truth forever on the scaffold, Wrong forever on the throne —

Yet that scaffold sways the future, and, behind the dim unknown,

Standeth God within the shadow, keeping watch above His own.

In any case we know one thing: Doing nothing makes nothing happen.

Yes, for those who believe in free markets, limited and accountable government, and individual liberty, these seem like our Valley Forge days, and of course many good causes are always failing from exhaustion. But what could be a grander cause than this one, a cause contending for the definitions of money and justice as they apply to all the capital, labor, goods, and services in the world?

GATA is indeed an amateur operation, doing work that should be done by others, like the World Gold Council, which, as it turns out, exists only to ensure that there never is a world gold council. But until professionals who are willing to take on the work turn up, we mean to keep at it, with the hope and faith that Arthur Hugh Clough put in rhyme:

Say not the struggle nought availeth,

The labor and the wounds are vain,

The enemy faints not, nor faileth,

And as things have been they remain.

If hopes were dupes, fears may be liars;

It may be, in yon smoke concealed,

Your comrades chase e’en now the fliers,

And, but for you, possess the field.

For while the tired waves, vainly breaking

Seem here no painful inch to gain,

Far back through creeks and inlets making,

Comes silent, flooding in, the main.

And not by eastern windows only,

When daylight comes, comes in the light.

In front the sun climbs slow, how slowly,

But westward, look, the land is bright.

We still need your help:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The real reason that India banned the large notes: to suppress India’s gold demand and I agree 100% with the author’s assessment

(courtesy Stewart Dougherty/Dave Kranzler/IRD)

The Deep State’s Attempt To Suppress India’s Gold Demand

November 29, 2016Financial Markets, Gold, Market Manipulation, Precious MetalsDeep State, Modi, war on cash

The primary objective of the Indian currency demonetization was to sharply reduce gold demand in the world’s most important retail market, India, one that is controlled by the Deep State oligarchy via a captured agent, its Prime Minister [Modi]. The manner in which the demonetization was carried out indicates some kind of desperation…Stewart Daugherty

Indian Demonetization Denotes Severe Stress in the Global Gold Market

By Stewart Dougherty

It is becoming clear that the Indian currency demonetization is actually a planned attack on Indian gold demand, launched to disrupt gold prices and discredit gold as an asset class. The attack was required to alleviate severe stress in the global gold market that is becoming increasingly difficult for the Deep State controllers to contain.

For two decades, physical gold has been migrating from the west to the east in increasing quantities. Numerous reports cross-confirm that the world’s leading refineries are operating at capacity to convert western gold into the kilo products demanded by Asian buyers. Refiners also confirm that the sourcing of western gold has become problematic, as supplies dry up in the face of voracious world, and particularly eastern demand.

Western central bankers and their Deep State handlers have made it clear that they intend to transition to a cashless society. However, they are not yet ready to make this transition. Therefore, their current focus is to start the process by eliminating high-denomination currency, such as Euro 500 and USD 50 and 100 notes. At the same time, they are working to digitize the payment infrastructure, a prerequisite to the elimination of cash.

Their problem is the steady awakening of the people to the disturbing implications of a cashless society, and to the assault on human liberty it represents. The Deep State oligarchs must implement their agenda before the people mobilize to prevent it from being imposed upon them.

The Deep State oligarchs understand that the western governments they commandeer are bankrupt. To continue operations, they must tap into the people’s private wealth for funding. In fact, the IMF has produced a position paper recommending a “one off capital levy of 10%” (a 10% wealth tax), to deal with western governments’ intractable fiscal problems. The authors of this paper state that the “levy” must be imposed at night and by total surprise, to prevent citizens from being able to take any steps to avoid it.

This type of ambush is exactly what just happened in India, with its shock demonetization.

The IMF’s proposal does nothing to change governments’ current trajectory of greater deficits and debt; the money raised would simply be used to service existing debt. This means the first capital levy will just be one of many going forward. Governments’ only solution is to expropriate the private wealth of the people, which is exactly what the IMF has admitted.

If people have cash and other private monetary assets outside of the banking system when the “capital levy” is imposed, governments will lose out. This is one of their primary motivations to eliminate cash: in order to maximize proceeds from the capital levy, they need the greatest possible amount of money within the banking system, in non-withdrawable, digitized form, when the levy is executed.

It is not in the interests of governments if people figure out that they are far better off being their own bankers, by privatizing their monetary assets, than handing them over to commercial bankers, who have become wards and enforcement agents of the state. Therefore, a full scale campaign is underway to demonize cash and to make precious metals appear dangerous by routinely pulverizing their prices.

In the meantime, supplies of physical metals in the west constantly diminished and are now strained. This means that the bullion banks’ LBMA and Comex paper price suppression activities must steadily escalate for them to maintain control of a market that is spinning out of their control. Unlike eastern investors, western investors tend to buy into rising prices, as they chase momentum. Rising prices can lead to a buying stampede. If a buying stampede were to break out in today’s supply-stressed precious metals market, prices would surge, which would be antithetical to the Deep State oligarchs’ agenda.

Given that Deep State operatives can do nothing to increase western gold supply, their only options are to somehow discover supply elsewhere, and/or to crush gold demand.

The “somehow” is India, a nation whose people possess an estimated 20,000 tons of gold, and who buy hundreds more tons of it each year. Prime Minister Modi, the Deep State establishment’s captured and controlled facilitator, has been instructed to obtain supply and control demand of gold in India, and he has been working overtime to achieve both objectives ever since his election.

First, Modi launched a Paper Gold scheme, whereby the Indian people were urged to tender their personal gold holdings to the state, in exchange for “notes” and “bonds” paying less-than-inflation interest rates on the value of the gold they provided. The notes are irredeemable for gold for at least five years, by which time the gold will be long gone from India and used in the bullion banks’ market rigging and other for-profit operations. Modi’s Paper Gold scheme failed, because the Indian people did not trust it, and correctly so.

Next, Modi imposed a 10% import duty on gold (India produces next to no gold, so virtually all of it is imported). This resulted in a multi-week strike by jewelers, which did reduce demand, one of the two aims of the Deep State oligarchs’ plan.

But shortly, this scheme failed, too, because gold smuggling surged, enabling the Indian people to obtain the gold they desire at prices roughly 5% over global spot, reasonable in the circumstances.

In a companion effort to crimp demand, Modi enacted a special reporting regulation. Enacted in 2015, it requires anyone purchasing jewelry or precious metals having a value of 200,000 rupees or more (the equivalent of roughly US$ 2,900) to present an Indian PAN Card. PAN stands for Permanent Account Number, a ten digit alpha-numeric number issued by India’s Tax Department to individuals and businesses. The PAN enables tax personnel to track all of a card holder’s financial transactions over their entire lifetime.

Only 17% of India’s population have obtained a PAN number to date, meaning that 83% of the population are unable to purchase $2,900 or more worth of jewelry or bullion in a single transaction; without a PAN Card, it is illegal to do so. This regulation has reduced jewelry and bullion purchases by upscale Indians who do have PAN but do not want their personal transactions permanently recorded. Alternatively, it has led them to make smaller purchases that do not require presentation of a PAN Card.

While the PAN regulation curbed demand in the $3,000+, high end of the market, it did nothing to address the vibrant, lower end, cash market. Smaller purchases of jewelry and bullion have traditionally been paid in cash, using 500 and 1,000 rupee currency notes. This was the Deep State’s Achilles’ heel in India, and they decided to deal with it.

Accordingly, on November 8, 2016, in a shock move, Modi “extinguished” all Indian 500 and 1000 rupee notes. Holders of the old notes have been required to exchange them for new ones, but the process has been extremely difficult and time consuming. Further, there are sharp restrictions on the amount of new currency citizens can obtain. Withdrawals are capped at 40,000 rupees per week, roughly $575.00. After paying for living expenses (90% of Indian purchases are made with cash), very little is left over for discretionary purchases such as gold jewelry. Given that the demonetization was specifically timed to occur in the middle of the robust festival and wedding season, the reduction in demand has been pronounced. Jewelers in Mumbai, the nation’s largest retail market by far, report sales being off by up to 90%.

We believe that the primary objective of the Indian currency demonetization was to sharply reduce gold demand in the world’s most important retail market, India, one that is controlled by the Deep State oligarchy via a captured agent, its Prime Minister. The manner in which the demonetization was carried out indicates some kind of desperation, because it defied all economic prudence, logic, humanitarian regard and common sense. India is the only country where this kind of attack on demand could have been carried out, and this is why it occurred there. It indicates to us that the bullion banking cabal is coming up against the wall, and that there is severe supply – demand stress in the global gold market that is rapidly becoming non-containable. Desperate times are producing desperate measures by the manipulators.

It is critical to note that the Governor of the Reserve Bank of India up until mid-2016, Raghuram Rajan, declined a second three year term. Rajan was a former Chief Economist at the International Monetary Fund, the “capital levy” people. He is also a member of the Group of Thirty, along with Larry Summers, the head cheerleader for the elimination of one hundred dollar bills in the United States, and cash in general. Much more important, Rajan has now become Vice Chairman of the Bank for International Settlements, the so-called “central bank of central banks,” and long regarded as the chief architect and enabler of global gold manipulation and price oppression. He has been characterized in the press as being “a vocal votary for increased coordination among central banks.” Clearly, an important Deep State global agenda is now in play.

Brexit and the Trump victory have demonstrated that the people can only be pushed so far, but the Deep State oligarchs are far too addicted to easy money and god-like power to hear the message. They are pushing forward as if nothing whatsoever has changed in the world. The retention by the people of financial liberty is far more important to them than Brexit or Trump, and we believe they will defend their rights to it, particularly as they awaken to the full implications of the tyranny that will be unleashed by its elimination.

As demand rebuilds from the shock demand reduction that has occurred in India, we believe the market for precious metals will become stronger than ever. First, India has discredited governments’ prized monopoly product: fiat currency. Second, India’s demonetization-related gold demand shock has no effect whatsoever on demand from Russia, China and the rest of Asia, which is stronger than ever. Third, the fiscal and monetary realities of governments throughout the west continue to worsen, strengthening the already compelling case for precious metals. Fourth, and as we have pointed out in previous articles, supply cannot withstand even a fractional redeployment of liquid personal assets into metals, without prices being forced significantly higher than where they are today. And fifth, the bullion banks and Deep State schemers are running out of curve balls to throw at the people. In fact, the stunt they just pulled in India might be their last, at least of anywhere near this magnitude. While we put nothing past them, including desperate dumping of remaining western central bank metals holdings (which might not even exist at this late stage) and prohibitions that the people will realize they must ignore if they are to have any chance of remaining financially free, it seems clear to us that they are fast running out of options.

Stewart Dougherty

November 28, 2016

P.S. One additional inference we draw from events in India is that it almost certainly proves the United States gold reserve is gone. What has happened in India indicates that a critical supply – demand imbalance exists in gold, which required an unprecedented, draconian and reckless “solution.” Actually, it has solved nothing; it has only bought the oligarchs some time, and probably not much of it. If western, and particularly U.S. gold reserves had been available, they almost certainly would have been deployed before a massive, destructive currency demonetization in the world’s second largest nation, by population, would have been ordered.

Stewart Dougherty is the creator of Inferential Analytics (IA), a forecasting method that applies to events proprietary, time-tested principles of human instinct, desire and action. In his view, forecasting methods not fundamentally based upon principles of human action are unlikely to be reliable over time. He is a graduate of Tufts University (BA) and Harvard Business School (MBA), is a 35+ year veteran of the business trenches and has developed IA over a period of 15+ years.

http://investmentresearchdynamics.com/the-deep-states- attempt-to-suppress-indias-gold-demand/

***

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.8988(SMALL REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS TO 6.9232 / Shanghai bourse CLOSED UP 5.94 POINTS OR 0.18% / HANG SANG CLOSED DOWN 93.50 OR 0.41%

2. Nikkei closed DOWN 49.85 POINTS OR .27% /USA: YEN RISES TO 112.98

3. Europe stocks opened ALL IN THE GREEN EXCEPT LONDON ( /USA dollar index RISES TO 101.42/Euro DOWN to 1.0582

3b Japan 10 year bond yield: FALLS +.020%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.01/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 45.88 and Brent:46.90.

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES TO +.206%

3j Greek 10 year bond yield FALLS to : 6.94%

3k Gold at $1183.50/silver $16.50(7:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 41/100 in roubles/dollar) 65.27-

3m oil into the 45 dollar handle for WTI and 46 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.98 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0165 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0755 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.205%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.329% early this morning. Thirty year rate at 2.986% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Pressured As Oil Slides On OPEC Deal Concerns; US Futures, Dollar Rise

European stocks were little changed and oil fell as investors assessed declining prospects for an OPEC deal and risks from Italy’s referendum. Asian stocks declined, while S&P futures pointed to a fractionally higher open, erasing 3 points from yesterday’s drop.

Trader attention today – and tomorrow – will be focused on oil which retreated back under $47 as OPEC members failed to bridge differences on production cuts, while a rally in metals ran out of steam. The rand plunged after President Jacob Zuma survived a leadership threat.

“We have a very important OPEC meeting and there’s a flow of expectations in front of this meeting, therefore the oil price is shaky as well as oil-related companies,” Herbert Perus, head of equities at Raiffeisen Capital Management in Vienna, told Bloomberg. The market is giving just 30% odds to an agreement to end the oil supply glut, according to Goldman Sachs; pessimism about the make-or-break talks is helping to damp a commodities rally.

Commodity and energy producers were the biggest decliners in the Stoxx Europe 600 Index. Crude slid as Iraq and Iran raised objections over the distribution of output reductions and Russia said it’s not planning to attend crucial talks with the Organization of Petroleum Exporting Countries on Wednesday (more in a subsequent update on oil prices). “What we are seeing now is a tug of war among OPEC members to get their share of the pie,” Son Jae Hyun, a global market analyst at Mirae Asset Daewoo Co., said by phone from Seoul. “If a deal isn’t made this time, none of them will benefit.”

Copper slumped for the first time in seven days and the Bloomberg Dollar Spot Index ended a two-day loss. The rand was the biggest decliner among major currencies.

European shares posted modest gains in early trading on Tuesday, after taking a battering from banks the previous day, but weak oil prices before a meeting of OPEC producers limited gains. 8 out of 19 Stoxx 600 sectors fall with basic resources, oil and gas underperforming while financial services outperforming; about half of Stoxx 600 members decline.

Italian banking stocks staged a recovery but miners came under renewed selling pressure after a sharp decline in commodities prices. Oil prices fell more than 1.5% on jitters over whether OPEC would be able to hammer out a meaningful output cut during a meeting on Wednesday to rein in a global supply overhang and prop up prices.

The miner-heavy FTSE 100 index was down 0.38% but the FTSE Mid 250 was up 0.15% 0940 GMT (5:40 a.m. ET). “The fact that the FTSE 100 is going one way and the FTSE 250 is going the other way suggests that there is a sector specific event going on, as the FTSE 100 is more commodities heavy,” said Investec economist Philip Shaw cited by Reuters.

There was a slew of European economic data reported this morning, most of which either met or exceeded expectations:

- (FR) 3Q P GDP 0.2% QoQ; est. 0.2%, prior 0.2%

- (FR) 3Q P GDP 1.1% YoY; est. 1.1%, prior 1.1%

- (FR) Oct. Consumer Spending 0.9% MoM; est. 0.25%, prior -0.2%

- (FR) Oct. Consumer Spending 1.5 YoY; est. 1.0%, prior 0.7%

- (EC) Nov. Economic Confidence 106.5; est. 106.8, prior 106.3

- (EC) Nov. Industrial Confidence -1.1; est. -0.5, prior -0.6

- (EC) Nov. Services Confidence 12.1; est. 12.5, prior 12

- (EC) Nov. Consumer Confidence -6.1; est. -6.1, prior -6.1

- (EC) Nov. Business Climate Indicator 0.42; est. 0.6, prior 0.6

The MSCI index of Asia-Pacific shares outside fell 0.27% after two days of gains. Tokyo stocks slipped

0.3% hit by a stronger yen. Asian stocks fell after a three-day rally as investors adopted a cautious tone ahead of key events from OPEC talks to the U.S. jobs report and Italy’s referendum. 8 out of 10 sectors fall with industrials, energy underperforming and telcos, financials outperforming. Chinese stocks rose by 0.2% with the Shanghai Composite reaching 3,283: “The government is tightening property so maybe some of that excess liquidity is flowing into the A-share market again,” said Ben Kwong, a Hong Kong-based director at KGI Asia Ltd.

The moved higher on the yen to reach112.62 after month-end flow profit-taking pulled it down as far as111.58. It remains over 7% higher for the month. Dealers reported Japanese buying for the new month with orders today settling on Dec. 1. Against a basket of currencies, the dollar held at 101.280 .DXY and not far from last week’s14-year peak. The greenback was still on track for its strongest two-month gain since early 2015, underpinned by expectations the FederalReserve is almost certain to hike interest rates next month.

European government bond markets were also trending in this direction, with safe-haven

Germen government bond yields up 1-2 basis points and lower-rated

Italian, Spanish and Portuguese bond yields lower. Italian 10-year bonds posted a modest advance, with the yield falling five basis points to 2.02%, but the gain comes just days after the bond yields hit their highest level since September 2015. The rebound came after Prime Minister Matteo Renzi’s office denied news reports that he is considering stepping down even if he wins the Dec. 4 referendum on constitutional reform.

Italian bond yields have been rising before Sunday’s referendum on constitutional change, on which Prime Minister Matteo Renzi has staked his future.

“Citi’s base case is for a No vote to prevail with political uncertainties likely to remain elevated over the near-term,” wrote analysts at Citi. “It’s worth watching whether PM Renzi resigns in the event of a No vote as promised, before rushing into euro shorts.” The event has brought Italy’s ailing banking sector sharp relief, and earlier this week Italian banking stocks hit their lowest point since end-September on continued worries over a cash call at troubled Monte dei Paschi.

In the US, 10Y Treasury yields rose two basis points to 2.34% after falling five basis points on Monday.

Later today, investors will get further insight on the U.S. economy with gross domestic product data, followed by Friday’s payrolls report on Dec. 2.

Bulletin Headline Summary from RanSquawk

- European equities trade modestly higher amid some mild reprieve in banking names while the FSTE 100 lags amid a firmer GBP

- A modest resumption in the USD buying seen today, despite reports that fund managers will — on balance — be selling the greenback into month end

- Looking ahead, highlights include German CPI, Eurozone sentiment figures, US GDP, API Inventories, Fed’s Dudley and Powell

Market Snapshot

- S&P 500 futures up 0.2% to 2204

- Stoxx 600 unchanged at 340

- FTSE 100 down 0.6% to 6759

- DAX up 0.1% to 10593

- German 10Yr yield down less than 1bp to 0.2%

- Italian 10Yr yield down 5bps to 2.02%

- Spanish 10Yr yield down less than 1bp to 1.56%

- S&P GSCI Index down 1.2% to 365.8

- MSCI Asia Pacific down 0.3% to 136

- Nikkei 225 down 0.3% to 18307

- Hang Seng down 0.4% to 22737

- Shanghai Composite up 0.2% to 3283

- S&P/ASX 200 down 0.1% to 5457

- US 10-yr yield up 2bps to 2.33%

- Dollar Index unchanged at 101.33

- WTI Crude futures down 1.8% to $46.23

- Brent Futures down 1.7% to $47.43

- Gold spot down 0.5% to $1,188

- Silver spot down 0.4% to $16.54

Top Headlines

- OPEC Said to Remain Split as Russia Says It Won’t Attend Meeting: Delegates said to fail to bridge divisions after 10-hour talks

- Samsung Plan to Boost Share Value Falls Short of Elliott Goals: Stock buybacks, increased dividends will make up cash return

- Chicken Producers Asked for Affidavits Confirming Price Data: U.S. chicken producers including Tyson Foods and Sanderson Farms are being asked by the Georgia Department of Agriculture to meet new requirements for a price index

- Korea’s Scandal-Hit President Says She’s Willing to Resign: Park says will follow what parliament decides on her future

- Strategists Shun Aging U.S. Bull Market for New One in Japan: Morgan Stanley upgrades Japan stocks, downgrades U.S. equities

- Facebook Fake News Doesn’t Need Policing, Publisher Says: Axel Springer CEO says Facebook shouldn’t regulate content

- Apple’s iPhone India Sales Surged Immediately After Note Ban: ET

* * *

Looking at regional markets, Asia stocks traded mixed following a negative lead from Wall St, where financials were pressured alongside weakness in their European peers and the S&P 500 testing 2200 to the downside. Nikkei 225 (-0.3%) was lower amid recent JPY strength weighing on the index after USD/JPY briefly fell below 112.00, while losses in ASX 200 (-0.1 %) were stemmed by health care and financials. Chinese markets were mixed amid continued reports China is to tighten capital controls and restrict outbound flows with profit taking in the Hang Seng (-0.2%) after yesterday’s Shenzhen stock connect-inspired gains, while the Shanghai Comp (+0.2%) initially took a breather before extending on 11-month highs. Elsewhere, the Kospi (+0.2%) rose 0.4% in reaction to news that South Korean President Park apologized for causing concern with her short-comings and stated that she will leave it to parliament to decide all affairs including reducing her term. 10yr JGBs traded flat despite a cautious tone for riskier assets, with the curve steepening as the short-end outperformed following a 2yr bond auction in which the lowest bid surpassed estimates and tail in price remained non-existent.

PBoC injected CNY 90bIn in 7-day reverse repos, CNY 70bIn in 14-day reverse repos and CNY 30bIn in 28-day reverse repos. PBoC set mid-point at 6.8889 (Prey. 6.9042).

Top Asian News

- UBS Wealth Sees Trump Bubble Burst Driving Yen to 98 per Dollar: Protectionist policies to precede fiscal stimulus, Ibayashi says

- Macquarie to Merge Trading Businesses Into Unit Led by Downe: Brings together securities and commodities & markets groups

- Thailand’s Parliament to Invite Vajiralongkorn to Become King: Vajiralongkorn would succeed the late King Bhumibol Adulyadej

In Europe, equities spent the morning in modest positive territory(Euro Stoxx 50: +0.6%), with the exception of the FTSE 100 (-0.3%), which has been weighed on by a stronger GBP as well as energy and material names. Elsewhere, sentiment has also been bolstered on the continent by upside in Banca Monte dei Paschi shares (+5.6%), paring some of the significant downside seen yesterday in the wake of their debt to equity swap green light. Elsewhere, Actelion (-5%) are among the worst performers this morning after reports in the FT that the Co. is considering a complicated deal to combine with part of Johnson & Johnson, without seeing a full takeover as was previously touted. Fixed income markets have been relatively quiet with participants amid the looming month-end and Italian referendum, as such volumes are somewhat on the light side. Today has also seen a noticeable narrowing of the IT/GE spread, in terms of reports from Italy Italian PM Renzi’s office denied premarket reports suggesting that the Italian leader would resign, even in the event of Sunday’s referendum seeing a ‘yes’ vote.

Top European News

- Actelion Slumps on Report J&J Talks Will Leave It Independent: Financial Times reported that a complex transaction being discussed with Johnson & Johnson would allow the Swiss company to remain independent.

- Sweden’s Economy Slows as Investments Stall in Third Quarter: Growth slowed in the third quarter as an expansion in the Nordic region’s largest economy continues to abate from last year’s output peak.

- Tesco’s Ex-CEO Clarke Avoids Prosecution Over Accounting Scandal: Clarke informed by Serious Fraud Office he won’t be charged

- VW, BMW, Ford to Set Up Charging Network to Spur E-Car Demand: Automakers plan first stations on European highways in 2017

In currencies, Bloomberg’s dollar gauge, which tracks the greenback against 10 major peers, increased 0.1%. The yen weakened 0.6 percent to 112.57 per dollar, set for its biggest monthly drop since 2009, amid speculation that Trump will pursue inflationary spending and tax policies prompting a faster pace of monetary-policy tightening by the Federal Reserve. The rand depreciated 1.5 percent after Zuma staved off a bid by officials in the ruling party to oust him. The Norwegian krone dropped 0.3 percent. The South Korean won edged 0.1 percent higher as President Park Geun-hye said she’s willing to resign amid an influence-peddling scandal.

In commodities, WTI crude slipped 1.9 percent to $46.20 a barrel as of 10:45 a.m. in London, after rising 2.2 percent on Monday, as jitters returned that OPEC will fail to reach a successful deal when it meets tomorrow. Copper futures dropped 1.6 percent on the London Metal Exchange, nickel lost 2.2 percent while zinc declined 1.1 percent. Gold for immediate delivery fell 0.5 percent following last session’s 0.9 percent jump.

Among today’s key events, we’ll get the second reading of Q3 GDP where the market is expecting growth to be revised up modestly to +3.0% qoq from +2.9% in the first estimate. In addition to the data the BEA will also release new information concerning corporate profits which is usually worth taking a look at. Also due out across the pond will be the November consumer confidence survey and also the S&P/Case-Shiller house price index. There is also some Fedspeak with Dudley due to speak at 1.15pm GMT (albeit on the Puerto Rico economy) while Powell speaks at 5.40pm GMT.

US Event Calendar

- 8:30am: GDP Q3 Est. 3% (prior 2.9%)

- 8:55am: Redbook weekly sales

- 9am: S&P CoreLogic CS 20-City y/y NSA, Sept., est. 5.20% (prior 5.13%)

- 9:15am: Fed’s Dudley speaks in Puerto Rico

- 10am: Consumer Confidence Index, Nov., est. 101.5 (prior 98.6)

- 4:30pm: API weekly oil inventories

* * *

DB’s Jim Reid concludes the overnight wrap

Sunday’s referendum in Italy is coming into full view now and even though a rejection is probably the most likely scenario, what happens after that is still open to much debate. Indeed DB’s Marco Stringa published an updated report yesterday looking at the risks after and beyond Italy’s referendum. He notes that given the recent underperformance in Italian assets, the impact of a rejection may already have partially been reflected in valuations. But when looking at implied moves from options, the equity market seems to be mostly pricing in limited probability of extreme scenarios. An apparent lack of concern over contagion risks is even more apparent in broader European indices. The report goes through Marco’s various downside and upside scenarios for which his central case still remains a muddle-through government with limited scope and duration. In this case he expects an early election from June 2017.

The last 24 hours suggests, certainly in Europe, that markets have started to turn their focus fully towards Sunday. Italy’s FTSE MIB (-1.81%) was the standout underperformer yesterday with Italy’s banking sector under pressure following a number of negative newswire reports. The Stoxx 600 edged down -0.77% although the Stoxx 600 Banks index tumbled -1.90% for its biggest one-day loss since November 2nd with Italian lenders unsurprisingly at the heart of that.

Markets in the US also slipped yesterday. Having touched record highs on Friday the S&P 500 (-0.53%), Dow (-0.28%), Nasdaq (-0.56%) and Russell 2000 (-1.29%) all simultaneously declined with banks also at the forefront of the weakness. In fact that drop for the Russell 2000 was, amazingly, the first since November 3rd (15 sessions) with the run of gains since the longest for that index since 1996. Elsewhere, Treasuries seem to have hit their yield ceiling for now. 10y yields were over 4bps lower yesterday at 2.315% and are now 10bps or so down from the intraday highs in yield last week. Sovereign bond markets were also a bit stronger in Europe yesterday. 10y Bund yields dropped 3.5bps to 0.201% while BTP’s underperformed at the margin, although still edged a couple of basis points lower to 2.064%.

The other obvious mover and shaker right now ahead of tomorrow’s meeting is Oil. Yesterday WTI rebounded +2.21% to a shade above $47/bbl again, although it has dropped below that level again this morning in Asia. The constant barrage of will-they-won’t-they headlines has the makings of the next great soap opera. The suggestion yesterday was that Iran and Iraq have continued to express objections to Saudi Arabia demands for their share of output cuts and for now that appears to be the main sticking point. We’ll wait to see what the latest round of headlines bring us today.

To the latest in Asia now where it’s been another relatively mixed start to trading. The Nikkei (-0.26%) in particular is trading lower despite some signs of improvement in the data this morning. Overall household spending, while still soft, did improve to -0.4% yoy in October from -2.1% in the month prior. Retail sales were also reported as rising +2.5% mom last month (vs. +1.1% expected) – the quickest since May 2014 – while over in the labour market the jobless rate was unchanged at 3.0%. Elsewhere this morning the Hang Seng (-0.02%), ASX (+0.06%) and Kospi (-0.03%) are little changed, while the Shanghai Comp (+0.30%) has edged higher. Rates markets are similarly mixed, although moves are relatively modest, while US equity index futures are fairly flat.

Moving on. Yesterday the OECD released their twice-yearly economic outlook including updated growth forecasts. Summing up, growth was revised up for the UK to 2.0% for 2016 (from 1.8% at the September projections) and 1.2% in 2017 (from 1.0%). Growth in 2018 is expected to be 1.0% but unsurprisingly the OECD used the caveat that the unpredictability of the exit process from the EU is the major downside risk. For the US, growth has been revised up to 1.5% for this year (from 1.4%) while 2017 growth was revised up two-tenths to 2.3%. Growth is expected to be 3.0% in 2018 with the organisation painting a fairly positive picture about of the impact of President-elect Trump’s proposed infrastructure spending plans on US growth. According to the OECD, world growth is expected to be 2.9% this year (unchanged) and 3.3% in 2017 (up from 3.2%).

Meanwhile, the data flow in Europe was a little bit soft at first glance. The ECB’s money and credit aggregates revealed a slowing in M3 money supply growth to +4.4% yoy in October from +5.1% the month prior. Market expectations had been for little change. However, after adjusting for sales and securitisation household lending rose +1.8% yoy and was unchanged versus September, while the three-month average for total credit was little changed at +1.7% yoy. Private sector credit rose with the three-month average up to +0.9% yoy from +0.6%. Meanwhile, the sole release in the US was the Dallas Fed’s manufacturing survey for this month which showed headline business conditions as rising nearly 12pts to +10.2 which is actually the highest reading since July 2014.

Also released yesterday was the latest ECB CSPP holdings data. As of November 25th, total holdings amounted to €46.231bn. That implies net purchases settled last week of €1.909bn or an average daily run rate of €382m. In fact, the daily average more or less matches the daily average since the program started (€385m) so we’re still yet to see any obvious signs of a slowdown into yearend just yet.

Staying with the ECB and wrapping up, President Draghi also spoke yesterday in a testimony to European Parliament, although his comments weren’t particularly groundbreaking. Draghi spoke about the ECB’s perspective on economic and monetary developments post Brexit and talked about the ‘encouraging resilience’ that the Euro area has so far displayed. Unsurprisingly Draghi said that longer term potential spillover effects will ‘vary across countries depending on their trade links with the UK’. Following the various press reports suggesting a possible delay in the decision concerning an extension of the ECB’s stimulus program, Draghi said that the Governing Council will assess the various options that will allow the Council to ‘preserve the very substantial degree of monetary accommodation necessary to secure the sustained convergence of inflation towards level below but close to 2%’.

Looking at the day ahead, this morning in Europe we’re kicking off in France where we’ll get the second Q3 GDP reading. Following that we turn over to the UK where money and credit aggregates data is due to be released, including last month’s mortgage approvals data. Confidence indicators for the Euro area then follow before we get the flash November CPI report for Germany. Over in the US this afternoon we’ll get the second reading of Q3 GDP where the market is expecting growth to be revised up modestly to +3.0% qoq from +2.9% in the first estimate. In addition to the data the BEA will also release new information concerning corporate profits which is usually worth taking a look at. Also due out across the pond will be the November consumer confidence survey and also the S&P/Case-Shiller house price index. There is also some Fedspeak with Dudley due to speak at 1.15pm GMT (albeit on the Puerto Rico economy) while Powell speaks at 5.40pm GMT.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 5.94 POINTS OR 0.18%/ /Hang Sang closed DOWN 93.50 OR 0.41%. The Nikkei closed DOWN 49.85 OR .27%/Australia’s all ordinaires CLOSED DOWN 0.22% /Chinese yuan (ONSHORE) closed UP at 6.8988/Oil FELL to 45.88 dollars per barrel for WTI and 46.90 for Brent. Stocks in Europe: ALL IN THE GREEN EXCEPT LONDON Offshore yuan trades 6.9232 yuan to the dollar vs 6.8988 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

3a)THAILAND/SOUTH KOREA/:

b) REPORT ON JAPAN

c) Report on CHINA

The following will be something that I will be watching out for: the rising Chinese bond yields (lower prices on bonds). The fact that the USA is raising rates has caused China to tighten as well. If they let interest rates remain pat then the yuan would contract even more. So China matches the USA in rising yields to prevent their yuan from collapsing

(courtesy zero hedge)

Chinese Bond Yields Jump Most In 10 Months On “Liquidity Fears”

It is probably a coincidence that one day after we commented on what is emerging as “the market’s next headache”, namely China’s (not so) stealth tightening, which in the last few weeks has led to a creep higher across the curve, the yield on China’s sovereign 10Y bond jumped 6.5bps to 2.94% on what Bloomberg dubbed were “liquidity fears.” This was the biggest one day spike for the benchmark bond since Jan. 25, according to ChinaBond data.

As a result of the selloff, the most actively traded 10-year govt bond futures were down 0.72%, while five-year futures dropped 0.74%.

The tightening was broad-based, with 1-year rate swaps rising 13bps to 19-month high at 3.17%; additionally the overnight repo rate also rose to 2.31%, the highest level this month.

Quoted by Bloomberg, Wu Sijie, bond trader at China Merchants Bank said “tightening interbank liquidity and the expectation of even higher short-term borrowing costs are driving up swap costs and affecting sentiment on the cash bond market.”

Meanwhile, signalling no change at all in its posture, overnight the PBOC drained funds in open-market operations for the fourth consecutive day, bringing the total withdrawal to 130 billion yuan.

Why is all of the above relevant? Because while so far the global capital markets have been immune to the substantial tightening in financial conditions resulting from the sharp rise in the US Dollar and US interest rates, a similar tightening in China – which is now clearly taking place – will be far more difficult for global risk assets to ignore.

As we reported yesterday, “since Oct 21, yield of 10Y Chinese Government Bond (CGB) has risen by 20bps, from 2.65% to 2.85%, partly in response to the strong global rates and USD move since the US election.” Bank of America expects Chinese yields to rise further to 3.40% by the end of 2017. Furthermore, with credit spreads near all-time lows, the bank warns that there is a risk that the move can widen sharply in the near future.

Judging by the biggest jump in yields in over a year taking place the very next day, this appears to be playing out as expected.

As Cui wrote, the local equity market reacted progressively less favorably to rising rates the last four times as investors turned ever less optimistic about growth outlook. The bank believes that “the rising rates this time may put pressure on equities in general as it would occur in an environment of lackluster growth.” In other words, while the US stock market may be ignoring the signal sent by rapidly rising yields, China may not have that luxury.

The biggest concern: if rising rates are caused by no-growth factors, such as inflation and the government’s desire to control debt growth (which seemed to be the case with Episodes 3 and 4), the market reacted sharply lower. This time, the pressure appears to be mainly driven by a less accommodating monetary policy as a result of housing bubble risk, debt control need and exchange rate pressure, despite a fairly lackluster economic growth outlook. In this case, Cui concludes, “the rising rate should not be a net positive to the equity market, in our view.”

Finally, what is most troubling for China, is that should financial conditions continue to grind tighter, the PBOC may have little recourse in response: as the Yuan has tumbled on the back of the stronger dollar, the central bank has been forced to tighten conditions to avoid an even steeper descent. This has eliminated the possibility of engaging in further aggressive easing as the alternative would be an even sharper drop in the Yuan, leading to even greater capital flight – something Beijing has been grappling with since early 2015.

Ultimately, the sharp move higher in Chinese yields may mean that just as “international conditions” prevented the Fed from hiking any time after the December 2015 rate hike, so this time too it may be global tightening conditions, and the stronger dollar that cause the next round of capital markets pain in a repeat of the market’s reaction to the last time the Fed hiked to telegraph the economy was “strong enough” that it could sustain a tightening cycle. It wasn’t.

So while traders have gotten used to tracking the daily fixing of the Yuan, keep a close eye on Chinese yields too. At this point it may be they that crack first.

4 EUROPEAN AFFAIRS

This Sunday, Dec 4 is the referendum date for Italy and the polls indicate strongly that the rejection of the establishment. Renzi may quit as promised but we are just not sure. He does not want to be gatekeeper of a technocrat government similar to what happened when Berlusconi left and Monti was appointed.

The ECB is ready to purchase as many Italian bonds as possible trying to keep the yields from skyrocketing. As I have pointed out on many occasions to you, the Italian banking system has 18% non performing loans totaling 360 billion euros. The bank system in Italy is insolvent.

(courtesy zero hedge)

Brexit Redux: ECB Ready To Buy More Italian Bonds If Referendum “Rocks Markets”

In a report confirming that the ECB is preparing for a rerun of a post-Brexit scenario, Reuters writes that the ECB is ready to temporarily step up purchases of Italian government bonds if the result of next Sunday’s crucial referendum, which according to WSJ will likely determine the future of not only Monte Paschi but other insolvent Italian banks, “rocks markets” and sharply drives up borrowing costs for the euro zone’s largest debtor.

As observed here over the past week, Italian government bonds and bank shares have sold off steeply ahead of the Dec. 4 referendum on constitutional reforms as the market has grown to appreciate the risk of political turmoil. Opinion polls suggest the ‘No’ camp is heading for substantial victory, which could force out Prime Minister Matteo Renzi in the latest upheaval against the ruling establishment sweeping the developed world. Heavily indebted Italy’s borrowing costs are closely watched as a potential flashpoint for market instability in the wider euro zone.

Just like in the hours after the Brexit announcement, when the ECB and other regional central banks vowed to step in and stabilize markets, the ECB will likely use its €80 billion monthly bond-buying program – which already hold nearly €1.2 trillion in European bonds – to counter any immediate, further spike in bond yields after the vote, smoothing market moves and supporting bonds, according to four euro zone central bank sources who asked not to be named.

The sources added the scheme was flexible enough to allow for a temporary increase in Italian purchases and that such a move would not necessarily need to be rubber-stamped by the ECB’s Governing Council, which is due to meet on Dec. 8 to decide on whether to keep buying bonds after March.

But they stressed this would be limited to days or weeks, to counter any immediate market volatility, because the asset-purchase program was designed to shore up inflation and economic growth in the entire euro zone and was not intended to fight crises in individual countries.

This means that, if Italy or its banks needed longer-term financial support, Rome would need to formally ask for help.

“The Governing Council understands that there is some space to help Italy, which will be used, if needed. The asset purchase program has built-in flexibility,” said one of the sources. “The key is that the ECB has to be convinced the volatility can be overcome by using this flexibility.”

Last week ECB Vice President Vitor Constancio opened the door to a central bank intervention last week but also stressed that still-low Italian bond yields did not point to investor fears that the country may crash out of the euro zone. Indeed, concerns about deposit flight and the health of Italian banks, rather than Italy’s own borrowing costs, have become Rome’s biggest worry in the aftermath of a ‘No’ vote.

Italy’s 10-year bond yields stand at 2% the highest level in more than a year but nowhere near the 7% level that prompted emergency ECB purchases in 2010-11 and eventually led to the resignation of Prime Minister Silvio Berlusconi, when Draghi refused to intervene in capital markets in a show of force with the then-Italian PM to demonstrate who is the real boss.

Reuters also adds that Euro zone central bank sources say there is little the ECB can do about the banks’ need for capital unless Italy itself asks for a rescue program for its banking sector. This would also unlock further, country-specific ECB purchases of Italian debt, known as Outright Monetary Transactions (OMT). These, unlike the current asset-purchase program, are not tied to the “capital key”, or how much capital each country has paid into the central bank.

“There is a risk that a bout of volatility would have a broader impact on the bank sector,” one of the sources said. “At that point, it’s not for the ECB to act. That’s typically where OMT needs to come in with all the requirements, including a (rescue) program.”

Logistic aside, BTP futures briefly spiked higher, gaining ~30 ticks in 2 minutes, to session high of 135.46, after Reuters cites unidentified sources to report ECB ready to temporarily step up Italy bond purchases if referendum causes yield spike.

end

Another huge paper: Ambrose discusses the huge 360 billion euros of bad debt on the balance sheet of the banks. The problem here is the new rules which will not allow a bailout by the sovereign Italy. There must be a bail in and most of the bonds are owned by Italian citizens.

a must read..

(courtesy Ambrose Evans Pritchard/UKTelegraph)

Subject:Fears Italy may need €40bn bail-out for its crumbling banks

Markets are bracing for a string of failures in the Italian banking system and a possible EU bail-out, fearing defeat for Matteo Renzi’s reformist government in a crucial referendum this weekend.Shares of Banca Monte dei Paschi di Siena (MPS) crashed 11pc on fears that a €5bn plan to recapitalise the broken lender could unravel if a ‘No’ vote leads to months of political turmoil, potentially bringing the anti-euro Five Star Movement closer to national office for the first time.Italy’s biggest bank Unicredit fell 4.3pc and is approaching lows last seen in the financial panic in July. It has lost almost two-thirds of its value over the last year.Sources in Rome say the Italian government may have to turn to the European Stability Mechanism (ESM) for a bank rescue, a humiliating and painful course that must be approved by the German Bundestag and other EMU parliaments. It would amount to a partial ‘Troika’ administration under terms dictated by the EU.“We think the banks will have to raise €40bn in fresh capital. This is going to need an ESM bail-out,” said one senior Italian banker.“The problems in the banks are becoming an excuse to put Italy under an EU programme. It won’t happen under Renzi because he won’t be there any longer after a ‘No’ vote. What we expect is a technocrat government that pushes this through,” he said.Pier Carlo Padoan, the finance minister, has been widely touted as the next premier, though his appointment at this delicate juncture would invite a populist backlash.

Italian bad debts are 18pc of bank balance sheets, but only the red ones are really, really bad. Tensions are rising. A sell-off in Italian sovereign bonds is driving a nasty ‘feedback loop’ for the financial system since the country’s banks own €400bn of this debt. They are now nursing big paper losses that must be partially ‘marked to market’ on a quarterly basis, eroding their core capital ratios even further.Yields on Italian 10-year bonds have doubled since the late summer, pushing the risk spread over benchmark German Bunds to a two-year high of 191 basis points.The worry is that weaker lenders such as MPS, Veneto Banca, or Popolare di Vicenza, could be forced into closure since they have lost access to the capital markets and cannot raise fresh money.This would wipe out bondholders under the EU’s draconian resolution regime.Premier Renzi has been lashing out at Brussels, bedecking his office with the Italian Tricolore flag and adopting an openly eurosceptic tone. “I couldn’t care less what the European Commission says. The time for Diktats is over,” he said.Mr Renzi is angry that new rules have forced Italy to ‘bail in’ small savers, often shunted into forms of bonds without being aware of the risk. Worse yet, EU rules make it almost impossible for the Italian state to rescue the banking system and restore confidence.The EU banking union has never got off the ground because Germany is still blocking any form of risk sharing, let alone agreeing to debt mutualisation to clear the legacy problems from the eurozone crisis. Italy is caught in the worst of all worlds.

The risk spread on Italian 10-year bonds over German Bunds is soaringLuigi Zingales from the University of Chicago says Italy needs a state plan to recapitalize the banks along the lines of the US Treasury’s ‘TARP’ programme eight years ago, but this is prohibited by EU state aid rules.Ignazio Visco, the Bank of Italy’s governor, said distressed lenders will be forced to conduct a “fire sale” of their non-performing loans (NPLs). “Some may have a tough time,” he said.Mr Visco said the rules were poorly drafted and cut across the ability of national regulators to deal with systemic risk, noting acidly that North European countries bailed out their own banks during crisis but then imposed the new regime just when Italy needed to do the same. “The timing has been unfortunate,” he told the journal Central Banking.The governor insists that Italian banks were victims of a credit crunch caused the eurozone’s double-dip recession by the “external shock” of the sovereign debt crisis. Little of this was their fault.The Bank of Italy says NPLs have come down slightly to €356bn, or 17.7pc of balance sheets. The closely-watched ‘Texas Ratio’ of NPLs to equity capital and loan loss reserves is 101pc, above the triple-digit danger line.